Embed Size (px)

Citation preview

1 1

320.326: Monetary Economics and the

European Union

Lecture 6

Instructor: Prof Robert Hill

Lessons from the Global Financial Crisis

1

2

The sources used to prepare this lecture include the following:

Malkiel B. G. (2010), Bubbles in Asset Prices, CEPS Working Paper No.

200.

Malkiel B. G. (2011), The Efficient Market Hypothesis and the Financial

Crisis, Mimeo.

Mishkin F. S. (2010), Monetary Policy Strategy: Lessons from the Crisis

downloadable at:

http://www0.gsb.columbia.edu/faculty/fmishkin/papers/10ecb.pdf

Case K. E. and J. M. Quigley (2008), “How Housing Booms Unwind:

Income Effects, Wealth Effects, and Feedbacks through Financial

Markets,” European Journal of Housing Policy 8(2), 161–180.

Cecchetti S. G. (2008), Monetary Policy and the Financial Crisis of

2007-2008

3

1. Asset Market Bubbles

A bubble is a situation where the price of an asset rises to a level

that can only be justified by expectations of future capital gains,

and not by the underlying stream of returns the asset is able to

provide.

A bubble does not necessarily imply a departure from the

efficient markets hypothesis (EMH) – usually defined as a

situation where it is not possible to obtain profits by

instantaneously trading assets of equal risk.

If you think everyone else expects the price to keep rising, then

maybe you should too. If everyone expects the price to rise it

probably will. This is a self-fulfilling prophecy.

4

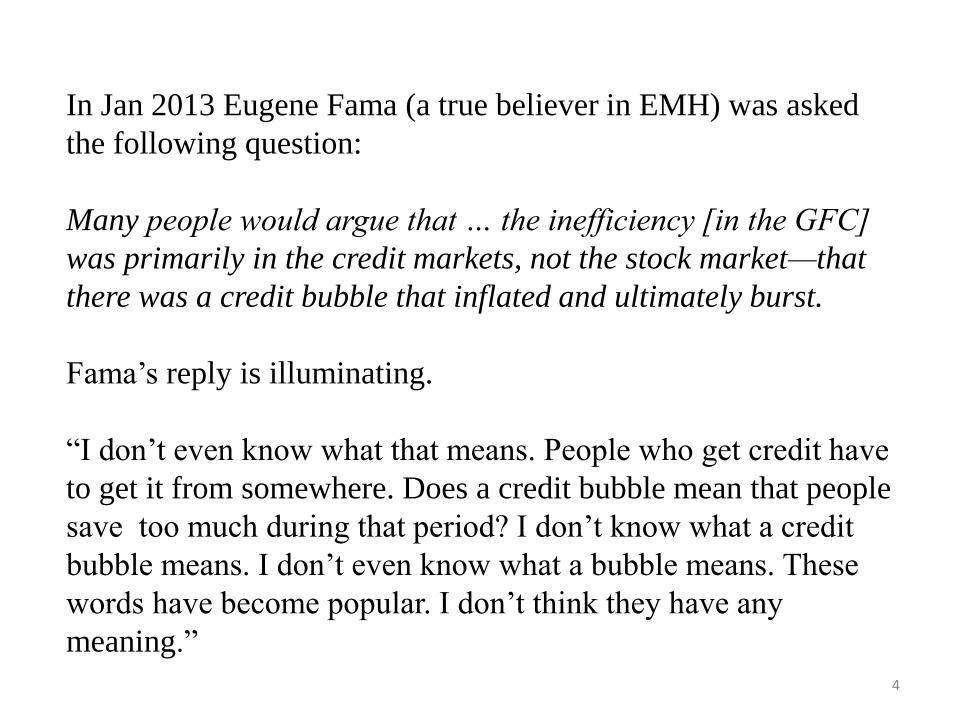

In Jan 2013 Eugene Fama (a true believer in EMH) was asked

the following question:

Many people would argue that … the inefficiency [in the GFC]

was primarily in the credit markets, not the stock market—that

there was a credit bubble that inflated and ultimately burst.

Fama’s reply is illuminating.

“I don’t even know what that means. People who get credit have

to get it from somewhere. Does a credit bubble mean that people

save too much during that period? I don’t know what a credit

bubble means. I don’t even know what a bubble means. These

words have become popular. I don’t think they have any

meaning.”

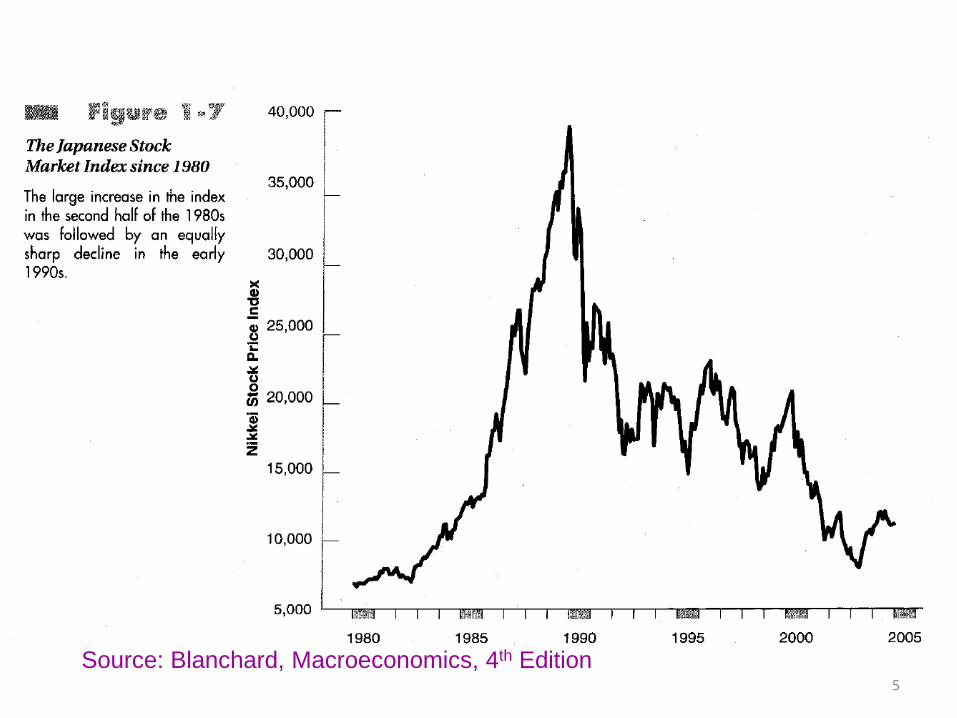

Source: Blanchard, Macroeconomics, 4th Edition 5

The rise and fall of NASDAQ stocks

Source: Burda and Wyplosz, Macroeconomics: A European Text, 5th Edition 6

7

I find this statement remarkable.

Admittedly measuring the fundamental value of an asset is

highly problematic. In a boom, expectations of the

fundamantal value are likely to rise with asset prices. Hence

during a boom it may be difficult to tell whether the price is

above its equilibrium level.

Robert Shiller on the other hand has described EMH as “the

most remarkable error in the history of economic thought.”

Fama and Shiller shared the 2013 Nobel prize in economics for

their work on asset pricing.

8

Another Nobel prize winner (Paul Krugman) said the

following:

“the belief in efficient financial markets blinded many if not

most economists to the emergence of the biggest financial

bubble in history. And efficient-market theory also played a role

in inflating that bubble in the first place.”

Malkiel (another believer in EMH) denies that the housing

bubble in the US was a violation of EMH.

According to him the EMH implies that there are no

unexploited riskless arbitrage opportunities in the market.

9

Malkiel then acknowledges that:

“Markets can make mistakes, sometimes egregious ones,

and those mistakes can have extremely unfortunate

macroeconomic consequences. But there were no ex ante

arbitrage opportunities.”

If you think there is a bubble, you can bet against it by

shorting the market. But the problem is you do not know

when the bubble will burst.

Markets can remain irrational much longer than you can

remain solvent betting against the market.

10

In other words, betting against a bubble is risky (even if you

are certain it is a bubble).

But arbitrage opportunities are hardly ever completely

riskless. Even George Soro’s arbitrage on the British pound in

1992 was not 100 percent riskless.

Soros saw that the British pound was overvalued in the

European Exchange Rate Mechanism (ERM).

Soros borrowed in pounds and converted them into DM. After

the pound was forced out of the ERM and the subsequent

depreciation, he converted DM back into pounds, paid off the

loan and had more than $1 billion left over.

11

Malkiel’s definition of EMH makes it very hard to ever

observe a clear violation of EMH. In this sense it ceases to be

a testable hypothesis.

Also, irrespective of what Malkiel thinks, many market

participants believed in EMH and also believed that EMH

implies that markets do not make mistakes.

2. Hyman Minsky‘s Instability Hypothesis

Minsky (1982) described a scenario that fits well with what

happened in the GFC. He argued that stability sows the seeds

of instability in a capitalist system.

12

Periods of economic expansion and relative stability lead

market participants to reduce the premiums they demand to

hold risky assets and to tolerate greater amounts of debt than

they had previously accepted.

The increased willingness of borrowers to borrow and

lenders to lend leads to a growth in the availability and flow

of credit, which in turn drives up asset prices to levels that

may be inconsistent with their fundamental values.

The process ends with what has been called a “Minsky

Moment.”

Sadly, Minsky died in 1996 and so did not live to see the

vindication of his ideas.

3. The Subprime Crisis of 2007

Housing mortgages in the US were collected together into large

pools, sliced up into standardized strips and sold to investors.

This process is referred to as securitization.

Pooled and sliced mortgages of this type are also known as

mortgage backed securities (MBS).

Problems:

(i) The mortgage initiator sold the mortgage on to a financial

intermediary, who then packaged them into MBS and sold them

to investors.

This created a principle-agent problem.

13

14

The purchaser of an MBS is the principle.

The mortgage initiator is the agent.

In the event of default it is the principle not the agent who bares

the cost. The agent therefore does not care about default risk.

The extreme case was NINJA mortgages (NINJA=no income, no

job or assets).

Buyers of MBS did not realize until too late the extent of the

principle-agent problem.

(ii) Default risk was highly correlated across subprime mortgages,

and foreclosed houses sell for far less than expected once the

housing bubble burst.

(iii) MBS were often packaged together with other debt products

like credit card debt and student loans to form collateralized debt

obligations (CDOs).

The securities were so complicated that nonone was then sure how

much overpriced they were once the crisis started.

The rating agencies – Moody´s, Standard and Poor´s, and Fitch –

gave the CDOs and MBS good credit ratings until 2007.

15

16

Not knowing the value of their own balance sheets, banks did

not know how much they could lend, or how solvent their

counterparties were. Increased volatility in the markets also

increased the perceived level for risk, causing banks to further

cut back lending.

The result was a severe credit crunch that threatened to drive

not only insolvent firms, but also even slightly illiquid but

solvent firms into bankruptcy.

After the collapse of Lehman brothers in 2008 even the

payment system wobbled.

The whole financial system came close to collapse in late 2008.

17

4. MBS and the US Housing Bubble

There was until 2007 high demand for MBS securities.

Investors (including banks) saw MBS and CDOs as a new low

risk asset class that would allow them to further diversify their

portfolios.

The high demand for MBS (stimulated partly by the inflow of

funds from China and oil rich countries) encouraged an increase

in supply of MBS, thus eroding lending standards.

The stable macroeconomic environment also encouraged

market participants to underestimate the level of systemic risk.

18

This effectively provided house buyers with a huge amount of

additional funding to buy houses, which helped trigger a

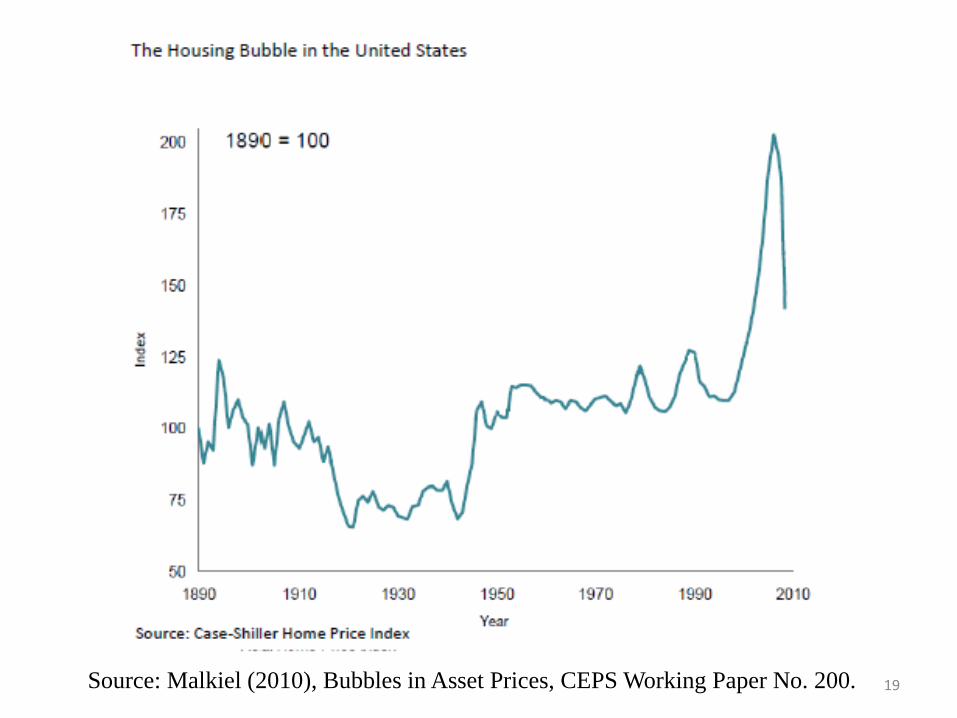

housing boom. The Figure on the next slide shows real house

prices in the US from 1890 to 2010.

5. The Psychology of Bubbles

Kahneman and Tversky in a series of papers argue that people

often follow simple heuristic rules when making decisions.

In asset markets (especially the housing market) they observe

the recent trend and may then expect this trend to continue.

This mentality of extrapolating recent trends leads naturally to

booms and busts.

19 Source: Malkiel (2010), Bubbles in Asset Prices, CEPS Working Paper No. 200.

20

Shiller (2000) makes a similar argument. He emphasizes the

role of feedback loops in the way people form their

expectations.

Rising asset prices generate enthusiasm, which leads to

increased demand for the asset and further price rises, etc.

Both perspectives share the theme that investors are more

influenced by recent price trends than considerations of where

the current price stands relative to the asset‘s underlying

fundamental value.

Bottom line: Asset markets are prone to booms and busts.

This is something central banks should pay attention to.

21

6. The Impact of a Bust in the Housing Market on the

Economy

(i) Wealth effects

According to Syz (2008), about one third of total wealth is tied

up in residential housing.

Consumption depends on both wealth and income. When house

prices rise, households feel wealthier and increase consumption,

either by withdrawing equity from their house or by saving less.

Conversely, households cut consumption when house prices fall.

22

Case, Quigley and Shiller (2005) find that changes in house

prices have a larger impact than changes in stock market prices

on household consumption. They find that a 1 percent rise in

housing wealth increases consumption by 0.11-0.17 percent.

(ii) Income effects

When home sales and housing starts rise this increases the

income of mortgage brokers, building inspectors, appraisers,

mortgage lenders, home appliance firms, and real estate agents.

The housing construction industry depends on the number of

housing starts (i.e., new builds). In 2006 new investment in

residential structures accounted for 5.5 percent of US GDP.

Housing starts in the US more than halved from 2006 to 2008.

23

(iii) Financial market effects

During a boom more money is deposited in banks. Banks are

keen to lend out this money. Hence their lending standards

become more lax. Also, during a boom, banks and other market

participants tend to stop paying enough attention to risk.

This leads to overinvestment in the whole economy (not just in

the housing sector).

During a bust (and recession) the reverse happens. Less money

is deposited in banks. Hence banks are less keen to lend and

start applying stricter lending rules. Also, having just lost

money they are acutely aware of risk. Hence the fall in

investment is even bigger than it otherwise would be.

This pattern of lax lending during booms and tight lending in

busts tends to accentuate the boom bust cycle.

24

(iv) Fiscal effects

Recapitalizing banks in a crisis increases the level of

Government debt. In Ireland and Spain this process beginning

in 2009 caused huge increases in Government debt.

In 2007 Ireland’s debt to GDP ratio was 29 percent. By 2011 it

had risen to 110 percent.

The large increase in government debt in Ireland and Spain

increased the perceived risk of default, and hence the risk

premium went up (i.e., governments started having to pay

more interest on new bond issues).

25

In most countries the buyer of a house pays a percentage tax on

the purchase price of the house.

These taxes are an important source of tax revenue for

governments during booms. When boom turns to bust, tax

revenue hence falls.

More generally, housing busts tend to cause recessions. In a

recession, less people are employed and paying taxes, while

more are unemployed receiving unemployment benefits. This

also hurts the government budget.

26

7. Possible Responses of Central Banks to Housing Booms

(i) Distinguishing between types of bubbles

Mishkin argues that it is important to distinguish between credit

driven bubbles and other bubbles, and that credit driven bubbles

are much more dangerous. A bursting credit driven bubble can

endanger the financial system.

Housing bubbles are almost inevitably credit driven and hence

warrant serious attention.

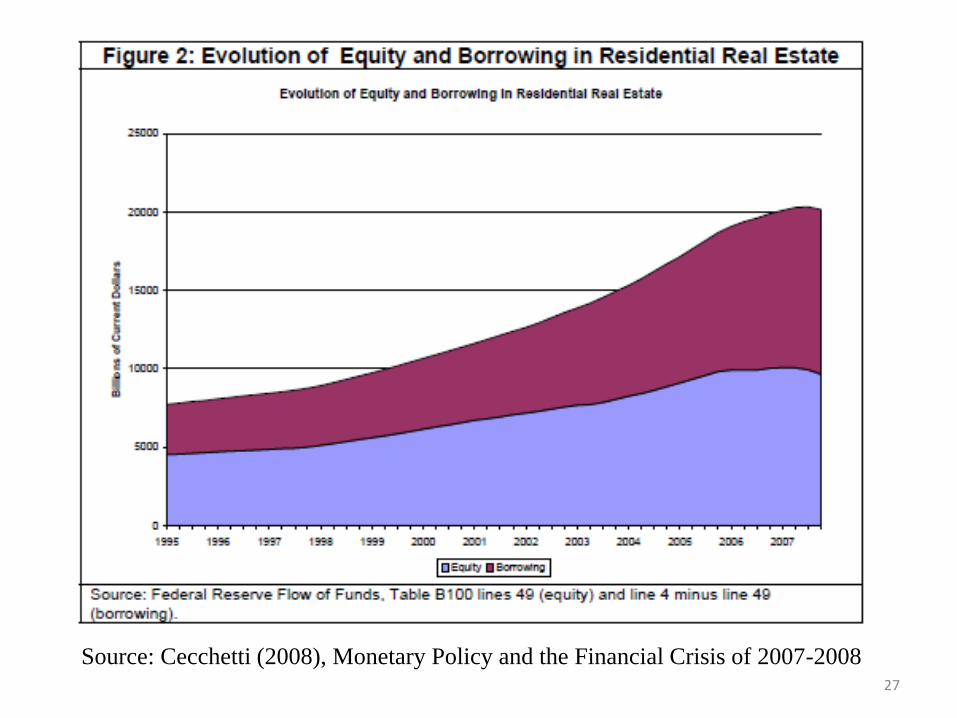

The next slides shows a decomposition of housing wealth into

equity and borrowing (i.e., credit). The share of total housing

wealth that is mortgaged in the US rose steadily during the

housing boom.

27

Source: Cecchetti (2008), Monetary Policy and the Financial Crisis of 2007-2008

28

(ii) Distinguishing between booms and bubbles

Some ways to check for bubbles in the housing market are to

look at the following statistics.

(a) The rate of credit growth in the economy

(b) The ratio of house prices to income

(c) The ratio of house prices to rents

Central banks should monitor closely these statistics.

29

(iii) Using interest rates to lean on bubbles

One way for a central bank to lean on a housing boom is to

raise interest rates.

Many monetary economists and central bankers do not like

doing this. They argue that interest rates should be used to

control inflation and that if we use them to manage asset

prices as well, then we have a two goal-one instrument

problem.

Also, it takes away the clarity of inflation targeting making it

harder for a central bank to manage expectations in the

market.

30

(iv) Prudential Regulation

Those monetary economists and central bankers who have since

the GFC become more willing to lean against bubbles tend to

prefer using prudential regulation of the banking sector.

Prudential regulation of banks includes the following:

- Caps on loan-to-value ratios for mortgages

- Caps on debt-to-income ratios for mortgages

- Caps on leverage relative to assets

- Liquidity requirements

These types of regulations are focused on individual firms.

31

Macroprudential regulation

It is possible that the problem lies more with the whole system.

Interactions between firms could be generating externalities that

act to destabilize the system.

Example: the rise in asset values in a boom encourages banks to

increase lending in the face of an unchanging benchmark for

loan-to-value ratios In a bust, bank lending can drop

precipitously, causing a credit crunch.

Macroprudential regulation focuses on trying to reduce the level

of risk in the whole system by for example allowing the

maximum loan-to-value ratio to vary over the business cycle.

32

Mishkin notes that prudential and macroprudential regulation

may not be enough to manage the financial sector.

This is because the regulated firms (mostly banks) will lobby

the regulator to relax regulatory rules (particularly when the

economy is booming and regulation is most needed).

Mishkin therefore reluctantly accepts that central banks may

need to use interest rates as well to restrain financial markets

during booms.

33

8. Beyond Inflation Targeting?

There is a feeling amongst some market participants that

inflation targeting encouraged central banks to ignore asset

prices in the build up to the GFC, and since the crisis they have

not done enough to encourage growth.

For this reason, some alternatives to inflation targeting have

recently been discussed that it has been argued may work

better in recession hit economies (e.g., in the aftermath of a

burst bubble).

We consider some of these here.

34

(i) Unemployment targeting

Bernanke announced on 12 Dec 2012 that the US Federal

Reserve is adopting an unemployment target of 6.5 percent.

“That is the level the Federal Reserve now says it wants the US

unemployment rate to fall to, before it will consider raising

interest rates.

There are caveats to this promise, and it is not independent of

what happens to inflation. In its statement yesterday, the Fed

said that its forecast for inflation would also need to be below

2.5% for them to think about raising rates.” (Source: Stephanie Flanders, BBC website, 13 Dec 2012)

Bernanke’s successor as Fed chair (Janet Yellen) abandoned this

unemployment target in mid March 2014.

35

(ii) Nominal GDP targeting

In a speech on 11 December 2012, Mark Carney – then the

Governor of the Bank of Canada and now the Governor of the

Bank of England – said that

“it might make more sense in today's circumstances to target not

the growth of prices (inflation) but the growth in the cash value

of economic output: nominal GDP.”

A nominal GDP target (say of 4.5 percent) merges concerns

over inflation and growth into a single target.

A nominal GDP target is like a flexible inflation target that

varies over the business cycle (i.e., the target is lower in a boom

and higher in a recession).

36

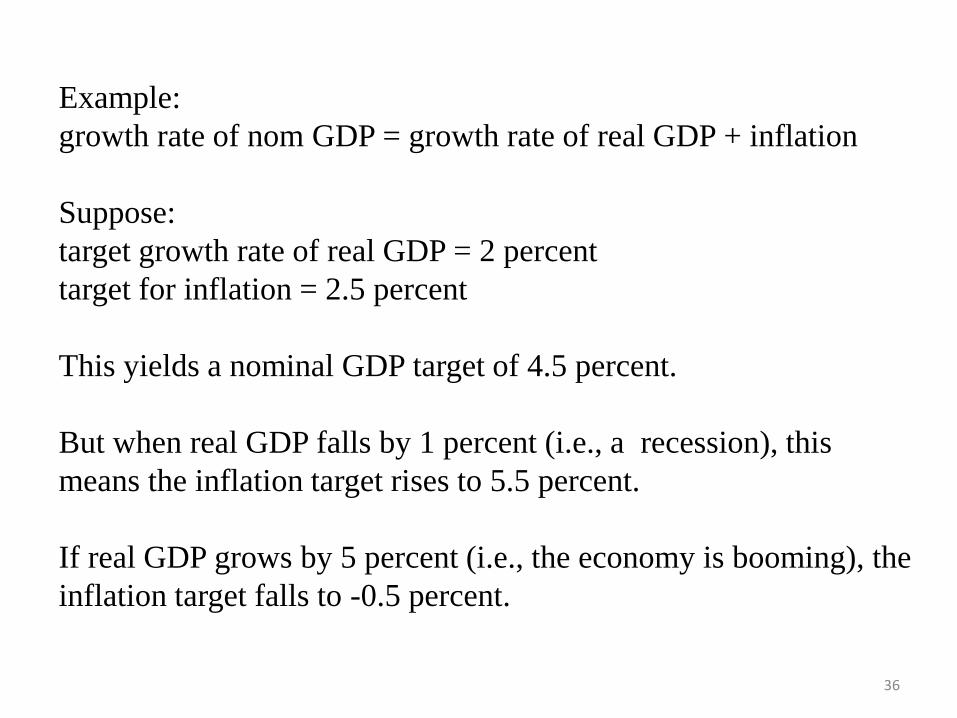

Example:

growth rate of nom GDP = growth rate of real GDP + inflation

Suppose:

target growth rate of real GDP = 2 percent

target for inflation = 2.5 percent

This yields a nominal GDP target of 4.5 percent.

But when real GDP falls by 1 percent (i.e., a recession), this

means the inflation target rises to 5.5 percent.

If real GDP grows by 5 percent (i.e., the economy is booming), the

inflation target falls to -0.5 percent.

37

Two problems with nominal GDP targeting are:

(a) It is not clear what the right nominal GDP target is. For

example it should be a lot higher for a fast growing

country like China than for the USA.

If set at too low a level (say 5 percent in China) then this

will push the Chinese central bank to try and create strong

deflation, which will hurt the Chinese economy.

If set at too high a level, it can lead to higher than desired

inflation.

(b) Central banks do not really have any experience with

nominal GDP targeting.

38

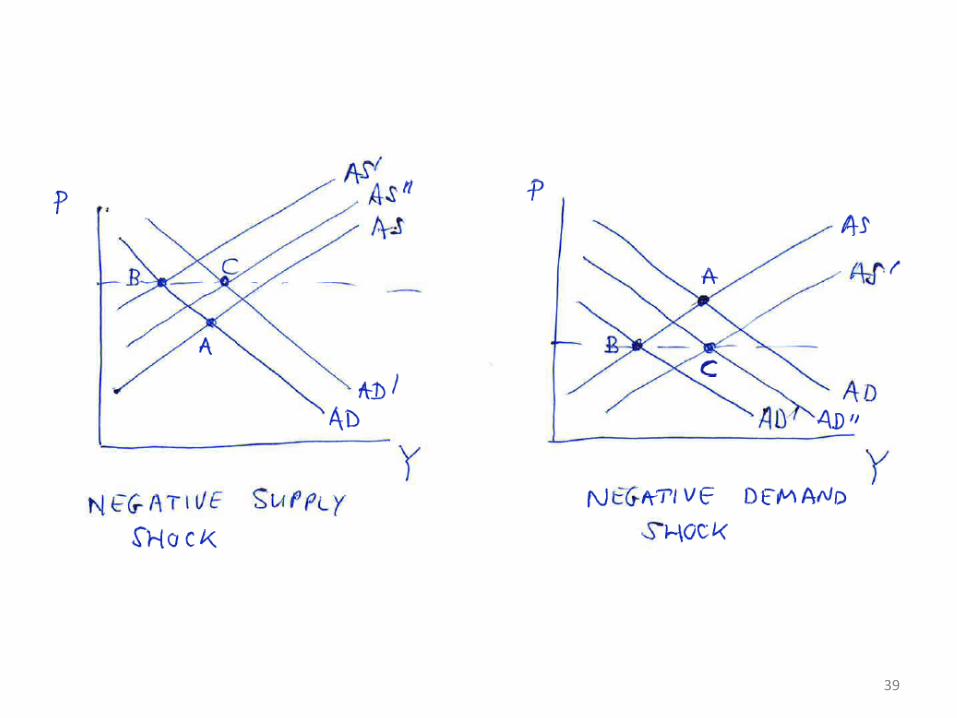

(iii) Price level targeting

Consider a rise in the price of oil. This shifts the AS curve to the

left. An inflation targeting central bank will respond with an

expansionary monetary policy (see Figure on next slide) while a

price level targeting central bank will not.

The shock moves the economy from A to B. A price level targeter

will wait for the economy to return to point A. An inflation

targeter does not care that the price level is now higher, and only

wants to stabilize the price level at its new higher level. The

inflation targeter therefore aims for point C.

39

40

Conversely, in response to a negative demand shock, a price level

targeting central bank will respond with a more expansionary

monetary policy than an inflation targeting central bank (again see

Figure).

The shock takes the economy from A to B. An inflation targeter

will again aim for point C (to stabilize the price level at its new

lower level). A price level targeter will aim to return the economy

to point A.

The second case is more relevant in a financial crisis, where there

is a big fall in aggregate demand. A price level target implies that

the central bank will be willing to tolerate higher inflation during

the period of recovery from the crisis so as to get the price level

back to its target level.

41

9. Monetary Policy After the GFC

The GFC has hopefully persuaded most economists that central

banks should not ignore asset prices. Cecchetti (2005) lists the

options for managing asset market booms as follows:

(i) Take them into account only insofar as they influence

forecasts of future inflation.

(ii) Act only after the bubble bursts, reacting to the fallout of the

bubble.

(iii) Lean against the bubble, raising interest rates in an attempt

to keep it from enlarging.

(iv) Include housing prices directly in the price index that the

central bank targets.

(v) Look for regulatory solutions both to keep the bubble from

developing and to reduce the impact of a crash should one occur.

42

We conclude by assessing each of these in turn.

(i) Take them into account only insofar as they influence

forecasts of future inflation

Bean (2003) argues that in an inflation targeting framework,

when the entire future path of expected inflation and growth is

considered there is no independent role for asset prices.

In practice though inflation targeting is typically based on 1-3

year ahead forecasts. Hence asset prices get insufficient weight.

Forecasting over longer horizons is anyway probably not a

serious option since the realibilty of the forecasts declines

rapidly.

43

(ii) Act only after the bubble bursts, reacting to the fallout of

the bubble

This position is completely discredited since the GFC.

It rested on three incorrect assumptions.

(a) The central bank cannot tell that there is a bubble until it

bursts.

Focusing on housing, very high price-rent ratios and price-

income ratios, and rapid growth in credit are clear indicators

of a bubble.

44

(b) If the central bank can tell there is a bubble so can market

participants. As soon as the market thinks there is a bubble, it

will immediately stop.

Not necessarily. Markets can remain irrational longer than

you can remain solvent betting against it.

No-one knows when a bubble will burst.

Most fund managers want to run with the herd. If you lose

money at the same time as everyone else loses money, then

you probably keep your job.

If you lose money by betting against a bubble while everyone

else continues riding the bubble, you may well lose your job.

45

(c) The central bank can clean up the mess after a bubble

bursts.

Until the GFC, the damage that a credit dsriven burst bubble

(e.g., a housing bubble) can cause was hugely unestimated.

The bubble almost brought down the whole financial system.

A central bank cannot afford to wait until a credit driven

bubble bursts by itself.

46

(iii) Lean against the bubble, raising interest rates in an

attempt to keep it from enlarging.

The post GFC consensus is moving in this direction,

although probably in combination with (v). The Australian

and Swedish central banks have successfully leant against the

housing market.

There is great reluctance among central bankers to actually

include an asset price index explicitly in the Taylor rule.

The Taylor rule is derived from a loss function, and it is not

clear how asset prices could be included in the loss function.

47

Most supporters of leaning using interest rates say that it

should be done in an informal way.

The central bank simply says that it is raising interest rates this

month because of concerns over the housing market.

Critics object that this makes monetary policy less transparent.

It should be noted though that nominal GDP targeting

provides a natural way of leaning against the wind. This is

because, while inflation may be stable during a housing boom,

the economy itself is likely to boom along with the housing

market. The rise in real GDP will trigger a rise in interest rates

(even if inflation is stable).

48

(iv) Include housing prices directly in the price index that the

central bank targets

There is strong opposition to targeting a broader measure of

inflation that includes asset prices, since this approach lacks

firm theoretical foundations.

However, the CPI could be made more responsive to changes in

house prices by changing the way the cost of housing services

of owner-occupied housing (OOH) are included in the CPI.

The problem with the current approach (rental equivalence) is

that during a housing boom rents often remain stable. Hence the

CPI is not really affected by a housing boom.

49

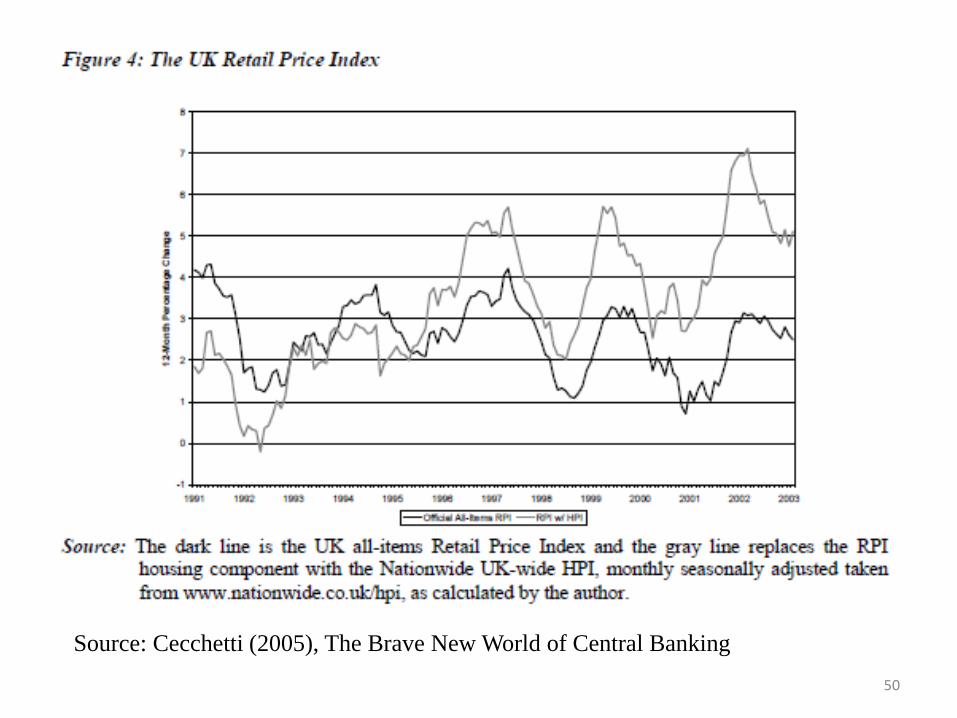

If OOH was treated differently, then leaning against a housing

bubble could happen naturally in an inflation target.

See the example the graph on the next slide which shows a

CPI for the UK where the cost of housing services of OOH

has been made more responsive to movements in house prices.

50

Source: Cecchetti (2005), The Brave New World of Central Banking

51

(v) Look for regulatory solutions both to keep the bubble

from developing and to reduce the impact of a crash should

one occur

More use should be made of macroprudential regulation,

such as maximum loan-to-value ratios that are lowered

during booms and raised in recessions.

Such regulatory rules should probably be used in

combination with either (iii) or (iv).