Embed Size (px)

Citation preview

1

INTU PROPERTIES PLC (Registration number UK3685527) ISIN Code: GB0006834344

JSE Code: ITU 28 FEBRUARY 2014

INTU PROPERTIES PLC AUDITED RESULTS FOR THE YEAR ENDED 31 DECEMBER 2013 David Fischel, Chief Executive of Intu Properties plc, commented “Intu advanced significantly in 2013 with a rebranding, strategic acquisitions, debt refinancing, equity issuance and key planning consents for our £1.2 billion development programme. The benefits to customers, retailers and staff from our rebranding as intu have surpassed our expectations. Successful multi-channel retailers continue to regard flagship stores in the larger super-regional and major city centres as core to their overall business. With the economy appearing to improve and total profit for the year including revaluations increased from £159 million to £364 million, we are prepared to withstand some minor reduction in like-for-like net rental income in the short term as we continue to invest in our centres to drive their total returns through our robust asset management approach, tenant mix repositioning and development projects.” Enquiries: Intu Properties plc David Fischel Chief Executive +44 (0)20 7960 1207 Matthew Roberts Finance Director +44 (0)20 7960 1353 Kate Bowyer Business Relations Director +44 (0)20 7960 1250 Public relations UK: Michael Sandler/Wendy Baker, Hudson Sandler +44 (0)20 7796 4133 SA: Frédéric Cornet/Nick Williams, Instinctif Partners +27 (0)11 447 3030 A presentation to analysts and investors will take place at UBS, 1 Finsbury Avenue, London EC2 at 09.30GMT on 28 February 2014. The presentation will also be available to international analysts and investors through a live audio call and webcast. The presentation will be available on the Group’s website intugroup.co.uk. A copy of this announcement is available for download from our website intugroup.co.uk. Contents: Page 2013 Highlights 3 Chairman’s Statement 4 Chief Executive’s Review 6 Financial Review 16 Key Risks and Uncertainties 22 Top Properties 24 Statement of Directors’ Responsibilities 26 Financial Information 27 Investment and Development Property 49 Financial Covenants 50 Underlying Profit Statement 52 Glossary 53 Dividends 56

Press ReleasePress ReleasePress ReleasePress Release

2

NOTES TO EDITORS Intu Properties plc (formerly Capital Shopping Centres Group PLC) is the UK’s leading developer, owner and manager of prime regional shopping centres. Intu owns and operates some of the best shopping centres, in some of the strongest locations right across the UK including ten of the UK’s top 25 and one of the top centres in Spain. With 18 million sq. ft. of retail, catering and leisure space, valued at £7.6 billion at the end of 2013, our centres attract around 350 million customer visits a year and two thirds of the UK population live within a 45 minute drive time of one of our centres. At the forefront of UK shopping centre evolution since the 1970s our focus is on creating compelling destinations for consumers, with added theatre. In 2013 we launched our nationwide consumer facing shopping centre brand – intu – transforming our customer experience and digital proposition including a transactional website, with a view to providing the UK’s leading shopping centre experience both on and offline. Intu has a UK development pipeline of £1.2 billion over the next ten years on active management projects at most of our centres and major extensions. Funding for this programme will include recycling of existing assets including possible disposals and introduction of partners. Intu also has interests outside the UK comprising an effective interest of 9 per cent in Equity One, a US retail REIT, a 32 per cent interest in Prozone, an Indian shopping centre developer, a joint venture in Spain for predevelopment activity on three major sites under option in Malaga, Valencia and Vigo and a joint partnership interest in a regional shopping centre in Oviedo, Northern Spain. Over 80,000 people are employed at our centres across the UK and we are fully committed to supporting our local communities and the wider environment through meaningful and hands-on initiatives.

This press release contains “forward-looking statements” regarding the belief or current expectations of Intu Properties plc, its Directors and other members of its senior management about Intu Properties plc’s businesses, financial performance and results of operations. These forward-looking statements are not guarantees of future performance. Rather, they are based on current views and assumptions and involve known and unknown risks, uncertainties and other factors, many of which are outside the control of Intu Properties plc and are difficult to predict, that may cause actual results, performance or developments to differ materially from any future results, performance or developments expressed or implied by the forward-looking statements. These forward-looking statements speak only as at the date of this press release. Except as required by applicable law, Intu Properties plc makes no representation or warranty in relation to them and expressly disclaims any obligation to update or revise any forward-looking statements contained herein to reflect any change in Intu Properties plc’s expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based. Any information contained in this press release on the price at which shares or other securities in Intu Properties plc have been bought or sold in the past, or on the yield on such shares or other securities, should not be relied upon as a guide to future performance.

3

2013 HIGHLIGHTS Robust asset management approach, focused on medium-term total property return

• high occupancy at 95 per cent • signed 201 long-term leases for £42 million new annual rent at an average 4 per cent above previous passing rent • encouraging tenant investment in stores - £70 million in 2013

Financial performance affected by repositioning

• underlying earnings per share 15.0 pence (2012 – 16.1 pence) reflecting £10 million impact of tenants who entered administration in late 2012 and early 2013

• property valuations increased 1.8 per cent, comparing favourably with IPD index which increased 0.8 per cent • total property return 7.3 per cent (2012 – 6.0 per cent) • net asset value per share (diluted, adjusted) reduced by 12 pence including reduction of 15 pence from early

termination of interest rate swaps and 7 pence dilution from equity placing Growth from acquisitions in UK and Spain with substantial organic development pipeline

• development pipeline now amounts to £1.2 billion programme over 10 years • representing some 2.6 million sq. ft. of new retail, restaurants and leisure of which 1.8 million sq. ft. (£0.7 billion) has

planning approval • funding will include recycling of existing assets including possible disposals and introduction of partners

Transformed debt structure

• £1.8 billion refinanced through bond issues and new bank facilities • achieved 40 basis points reduction in average cost of debt to 4.8 per cent and 2 year increase in weighted average

maturity to 8 years • cash, short-term investments and committed facilities of £325 million at 31 December 2013; £110 million further debt

raised 2014 to date Launched nationwide consumer-facing brand and digital proposition

• customer experience improved, with strong take-up of free Wi-Fi following installation of high capacity fibre-optic networks at nine centres; Intu owns platform and resulting data

• previously out-sourced facilities management and customer-facing teams brought in-house; all employees trained in World Class Service

• single brand for company and shopping centres bringing operating efficiencies and nationwide business opportunities

Financial highlights 1

Twelve months ended 31 December

2013 2012

Net rental income (£m) 370 363

Underlying earnings (£m) 140 138

Property revaluation surplus (£m) 126 41

Profit for the year (£m) 364 159

Underlying EPS (pence) 15.0 16.1

Dividend per share (pence) 15.0 15.0

As at 31 December

2013 2012

Market value of investment properties (£m) 7,624 7,073

Net external debt (£m) 3,698 3,504

NAV per share (diluted, adjusted) (pence) 380 392

Debt to assets ratio (per cent) 48.5 49.5

1 Please refer to glossary for definition of terms

4

CHAIRMAN’S STATEMENT

Introduction A year ago, following our announcement of the new brand and digital initiatives, I commented that we were at the beginning of a new phase in the Group’s life, with our market leadership position in the sector providing many opportunities for growth, both organically and by acquisition. Since then we have oriented the business around the principle that improved customer experience driven by motivated customer service attracting leading retailers is a powerful virtuous circle creating value for our shareholders, employees, communities and partners. Overview of 2013 activity I am delighted that the cultural change throughout the Group has exceeded all expectations – as have other changes associated with our brand. These include new signage, information desks and uniforms, World Class Service training, transfers of employment to Intu Retail Services, free Wi-Fi, the launch of an online business, the formation of intu Experiences for promotional activities and national marketing campaigns. We have only just begun to realise the full potential of our national consumer brand. But that was far from all we achieved in 2013. We acquired a great centre, Midsummer Place, Milton Keynes, filling a gap in our national coverage. We strengthened our financial position by raising equity and as capital markets improved we successfully refinanced, ahead of time and on a long-term basis, tranches of borrowings coming due between 2015 and 2017. We appreciate the commitment of our shareholders and lenders. Our asset management and development teams have been exceptionally busy, signing up new tenants, dealing with lease expiries, lodging planning applications and getting capital projects underway. We have plans for every centre. For example, we are on site transforming the malls at intu Eldon Square, remodelling the intu Lakeside food court, refurbishing intu Victoria Centre and reinvigorating what we now call Platinum Mall at intu Metrocentre. Major projects not yet on site, such as the extension of intu Watford into the adjoining Charter Place, are rapidly moving forward. Internationally, the highlight was the acquisition of a leading Spanish centre, Parque Principado, Oviedo, with a top quality partner, Canada Pension Plan Investment Board. 2013 financial performance As discussed in the Chief Executive’s Review, the Group’s financial performance for the year reflects some income reduction from tenant failures but robust valuations contributed to a healthy total property return. Looking forward Thinking ahead, how we combine retail, catering and leisure, how we adapt to the digital and smart phone era, how we take our brand forward, how we keep our centres fresh and appealing to customers, the next steps we take to grow our footprint in the UK regional shopping centre industry – these are the themes which will define our success in the years to come. In that context we will remain focused on achieving strong returns over the medium term from each of our assets individually, including through our significant plans for development, and through their combined power as the only UK national branded network of prime centres. Turning to external factors, it is encouraging to see some signs of recovery, with retailers continuing to address the impact of changing shopping habits on their own business models. In providing customers with fresh experiences in some of the best destinations, we offer retailers compelling opportunities to thrive, driving the total returns from our assets over the long term. Directors and staff I would like to record my thanks to the Board and all our staff for their commitment and dedication to intu’s values and vision in this year of fast-paced change. Further, I would like to welcome the 1,300 employees of Intu Retail Services who joined the Group in July and October 2013. Including expansion in other areas, we now have a team of over 2,000 people delivering our nationwide brand aspirations and values. Our third annual employee survey showed the overwhelming majority of our expanded workforce is enthusiastically supporting the evolution of the Group. On behalf of the Group I would like to thank Rob Rowley, who stepped down from the Board on 18 October 2013 after nine years, and Andrew Huntley and Adèle Anderson, who have taken on the roles of Senior Independent Director and Chairman of the Audit Committee respectively. Corporate responsibility Intu’s award-winning CR programmes reinforce our long-term commitment to sustainable and community-minded business practice in the development and promotion of our shopping centres and I take great personal interest and satisfaction from my involvement in many of our projects.

5

In 2013 we achieved an impressive seven per cent reduction in carbon emissions, a total of 18 per cent over two years and were awarded Gold in the annual Business in the Community CR Index. Our employees engaged with 12 regional and national community partners to deliver practical help to disadvantaged young people in the communities served by Intu centres and, overall, our projects directly reached almost 2,500 people in 2013. All our projects are subject to thorough evaluation and, as members of the London Benchmarking Group, we carry out an annual appraisal of all our community involvement efforts to ensure a close fit with the core goals of our business. Dividends The Directors are recommending a final dividend of 10.0 pence per share bringing the amount paid and payable in respect of 2013 to 15.0 pence, unchanged from 2012. A scrip dividend alternative will be offered. Details of the apportionment between the PID and non-PID elements per share will be confirmed in due course as the cash dividend is likely to be partly PID and partly non-PID and the scrip alternative wholly non-PID. Responsible corporate behaviour and high quality service are key underlying values which inform our approach to every aspect of our affairs. We take very seriously our responsibility as a good corporate citizen. Our staff work hard to provide real benefit to our customers, partners and the wider communities in which we are based. We know people like to deal with companies they can trust so, as well as intangible benefits, this approach reinforces our ability to provide real returns to our shareholders in the long term. Patrick Burgess Chairman 28 February 2014

6

CHIEF EXECUTIVE’S REVIEW INTRODUCTION Overview of 2013 activity Intu has moved forward markedly in the year with a high level of activity and dynamism. The cultural change we instigated as part of our rebranding has surpassed our expectations, we have reached significant milestones within our project pipeline and we have much improved our financial position with new debt and equity. We end the year better positioned to create long-term value through the opportunities afforded by the changing retail landscape. Significantly, we have:

• secured 30 planning consents, including for major extensions at intu Watford and intu Lakeside. Altogether 1.8 million sq. ft. (£0.7 billion) of the 2.6 million sq. ft. pipeline is now consented, over half of which is catering and leisure

• reached agreement with Nottingham City Council setting the way forward for intu Victoria Centre and intu Broadmarsh • made strategic acquisitions in the UK, including filling a gap in our national coverage at Milton Keynes • made a strategic acquisition with a strong partner in Spain, a market with considerable opportunity • refinanced most of the debt falling due in the next three years, reducing the cost of debt and achieving a duration

appropriate for our long-term income stream

• trained our operational and head office staff in World Class Service, initiating a process of cultural change to embed our values in every aspect of operations

• launched free Wi-Fi at more than half of our centres with the remainder imminent, and derived operational and infrastructural efficiencies from the fibre-optic platform

• rolled out our new brand, demonstrating physical change and new experiences to each visitor and the scale of our operations to retailers

A number of the positive actions which we have taken in the year have had the impact of reducing some of the 2013 headline financial measures. Total property return was a healthy 7.3 per cent supported by robust valuations particularly for our super-regional centres. Net asset value per share reduced by three per cent largely as a result of costs associated with reorganising our debt structure and the equity raising for the acquisition of Midsummer Place in which many of our major shareholders participated. Total financial return was one per cent. Good operational progress in the form of lettings was disappointingly masked in terms of earnings by the cost of tenants who entered administration in late 2012 and in early 2013. We continue to take a robust line to ensure that we achieve the right rental level for our prime product and we are prepared to withstand some short-term reduction in earnings as we continue to improve our centres. While we would prefer to see unbroken positive trends, we remain confident of our strategy for the medium- and long-term performance of our assets and that the underlying business remains on course. Outlook and priorities for 2014 We are encouraged that the UK economy has continued to recover during 2013. While household purchasing power remains stretched, there are signs of returning consumer confidence and increasing appetite for lending. Well configured space in the best shopping centres such as Intu’s will become increasingly important as retail businesses adapt to the challenge of changing shopping habits. Looking forward to 2014, the relative stability of the second half of 2013 has enabled us to prepare for upcoming developments by holding space vacant or on flexible terms to enable a timely start to a number of our projects. Altogether 2.4 per cent of ERV is now held for development, of which around a third is let on short-term leases for flexibility. Additionally the benefit of 2013’s new lettings will be more than offset by the short-term impact of lease expiry concentrations and the residual impact of 2013 tenant failures. We expect the combination of these factors to create a further year of reducing like-for-like net rental income. However, we are confident that our development projects, tenant mix repositioning and effective asset management approach will significantly enhance the long-term total return of the business.

7

We will continue to focus in 2014 on four main goals which, we believe, will result in strong total returns over the medium term: • optimising the performance of our existing assets, through active asset management • driving forward our £1.2 billion investment programme and, where appropriate opportunities arise, considering strategic

acquisitions • continuing to improve our financial flexibility through debt and capital recycling from existing assets including disposals

and possible introduction of partners • reinforcing our brand and digital presence including property management innovation to drive demand for our assets

and create broader commercial value

8

MARKET REVIEW

Investment market The value of UK shopping centre investment transactions in 2013 was well above the previous few years with strong demand pushing yields down. Investor appetite has spread well beyond London with good volumes in several regions. As well as international investors continuing to target the most prime assets, the improvement in macro indicators (see below) has stimulated increased interest in strong secondary assets. Demand from cash-funded investors has been supplemented by a significant improvement during 2013 in the range and depth of debt funding sources to the sector. These have extended to financing assets outside the most prime and should continue to underpin values. Shopping centre development across the UK remains at a fraction of the level of the mid 2000’s, providing limited new supply. Completions in 2013 and the pipeline for 2014 and beyond are focused on extensions and reconfigurations of existing centres.

Occupier market The UK economy showed signs of improvement in 2013, with four quarters of GDP growth and a sharp rebound in consumer confidence towards the end of the year. This has yet to be reflected in any significant increase in UK average household disposable income with the Asda benchmark index showing a rise of 1.8 per cent over the year. Whilst inflation has declined and employment has risen, year-on-year wage growth has fallen to below one per cent. Despite the continued constraints on household finances, consumer spending has been increasing with higher like-for-like non-food retail sales reported by the BRC throughout 2013, aggregating to around two per cent for the year. Retailer administrations continued at an elevated level in the early part of 2013 according to the Centre for Retail Research but reduced in the middle of the year to end slightly lower overall than the high levels of 2012. This trend was reflected in Intu’s portfolio with no significant tenant failures in the second half of 2013 after four per cent of the rent roll entered administration in the first half. The chart below shows a marginal pick up in vacancy across retail property categories in 2013, with notably lower levels in larger centres such as Intu’s.

9

Changing UK retail Our research shows that, with an increasing number of ways to buy products, customers come to shopping centres for much more than just purchasing. As the boundaries between shopping, entertainment and dining become blurred, our visitors want a place to socialise, to be entertained and to discover something new. The top shopping centres, such as Intu’s, are better able to offer this range and so it is no surprise that they are attracting an increasing share of national retail footfall and achieving a lower level of vacancy than small centres. With 12 per cent of retail sales conducted online in the last quarter of 2013 according to estimates, digital technology is an inseparable part of everyday life. Shopping now is browsing, trying, researching, asking opinions through social media, sharing ideas and transacting on and offline, using digital tools to make life easier. In that context, many successful retailers have developed effective on and offline capabilities and are continuing to review their store networks to best suit multi-channel strategies. Physical retailing space in the key destination centres is a core part of many business models, with continued space reductions in less core locations. For example Next, which has successfully converted its Directory business to a strong online offer, has made flagship investments at four Intu centres in 2013 and now occupies 650,000 sq. ft. across the portfolio, a third more than in 2008. Focusing on customer experience, with technology as an enabler With our rebranding in 2013, we have oriented every aspect of our asset management, operational delivery and property development around the customer experience in our centres. Examples of initiatives implemented during the year and in particular the increasing importance of providing catering and leisure options are discussed in Asset management below. Our digital strategy is to help customers to get more from our shopping centres, when they are physically there and when they are not. Digital connectivity is not a separate process, but an integral part of the physical experience, increasing convenience and widening our reach. Our digital initiatives are focused on using technology for example to help with practicalities and with sharing ideas. We chose to invest in a high quality fibre-optic backbone and Wi-Fi network infrastructure, owned rather than out-sourced, seeing it as the heart of our digital strategy. This means we manage the entire customer journey and the data which results from it. With an encouraging 60 per cent of our Wi-Fi registrants “opting in” to receive marketing information, the potential to make targeted offers is significant, with scope for development of a powerful single customer view across multiple interactions with Intu. Our ownership of the platform enables us to sell services to our commercial partners including both use of the infrastructure and marketing opportunities. We are also benefiting from operating synergies and cost savings as elements of building management, lighting and security systems migrate onto the platform. Other initiatives include a transactional website launched during 2013 offering high quality, editorial content which enables us to engage with customers both away from our shopping centres and within them. Its magazine-style content inspires customers and encourages sharing through social media. This offers our retailers around the clock interaction with our customers and vice versa, with the added convenience of click and collect of multiple retailer purchases at one point in our centres. We have also trialled a customer lounge and intend to roll out a concierge-style concept to other centres during 2014.

10

DELIVERING ON OUR STRATEGY 2013 performance: Valuation The aggregate like-for-like market value of our investment property increased by 1.8 per cent in the year, twice that of the IPD monthly index (up 0.8 per cent), with consistent progress in each of the two halves. This contributed to a robust total property return of 7.3 per cent (see Operating metrics below).

The weighted average nominal equivalent yield at 31 December 2013 was 5.79 per cent, a reduction of 15 basis points in the year, reflecting market conditions and our ongoing asset management initiatives maintaining the prime and resilient nature of our assets. Based on the gross portfolio value, the net initial yield “topped up” for the expiry of rent free periods was 4.97 per cent. The like-for-like change in ERV also continued to out-perform the benchmark with a further marginal increase in the second half of 2013.

Full Second First year half half 2013 2013 2013 Group revaluation surplus – like-for-like +1.8% +0.8% +1.0% IPD* capital growth +0.8% +2.0% -1.1% Group weighted average nominal equivalent yield 5.79% 5.79% 5.85% Like-for-like change in Group nominal equivalent yield -15bp -6bp -9bp IPD* equivalent yield shift -17bp -18bp +1bp Group “topped up” initial yield (EPRA) 4.97% 4.97% 5.10% Group change in like-for-like ERV +0.3% +0.1% +0.2% IPD* change in rental value index -1.3% -0.5% -0.8%

* IPD monthly index, retail

In general the larger super-regional and major city centres continue to out-perform with stronger valuation surpluses, with slight reductions in some centres where improvement expenditure has not yet been fully reflected in prospective ERVs. Notable changes in individual valuations include:

• intu Trafford Centre (+£94 million (H2 £47 million), +5.3 per cent) has benefited from an increase in headline rent and the satisfactory conclusion of 2013 lease expiries and rent reviews as well as market yield improvement for super-regional centres

• intu Lakeside (+£26 million (H2 £5 million), +2.4 per cent) has benefited from an earnings-enhancing food court redevelopment as well as market improvement in yield for super-regional centres

• intu Eldon Square (-£7 million (H2 -£3 million), -2.9 per cent) has been affected by refurbishment expenditure, the potential effect of which has not yet been reflected in the valuation ERV

• St David’s, Cardiff (+£16 million (H2 £7 million), +6.4 per cent) has benefited from continued growth of income in the 2009 extension as well as market yield improvement for top centres in major cities

• intu Bromley (-£7 million (H2 -£2 million), -4.1 per cent) has not yet benefited from the valuation impact of committed refurbishment expenditure

• Manchester Arndale (+£15 million (H2 £7 million), +3.7 per cent) continues to benefit from national evidence of stronger yields for top centres in major cities

• intu Potteries (-£6 million (H2 -£2 million), -3.6 per cent) has been affected by some pockets of ERV reduction as we conclude relettings following the 2013 lease expiries

• Cribbs Causeway (+£7 million (H2 £6 million), +2.8 per cent) has benefited from the satisfactory conclusion of 2013 lease expiries, increasing security of income and improving tenant mix, as well as market yield improvement for super-regional centres

11

Operating metrics

2013 2012 Occupancy 95% 96% – of which, occupied by tenants trading in administration 1% 3% Leasing activity – number, new rent 201, £42m 169, £44m

– new rent relative to previous passing rent 4% above 7% above Like-for-like change in net rental income -1.9% -2.7%

Total property return 7.3% 6.0% Footfall -2% -1% Retailer sales (like-for-like centres) +0%* +1% Rent to estimated sales (exc. anchors and major space users) 13.5% 13.9%

* excluding impact of trading interruptions during major tenant relocations at intu Braehead and Cribbs Causeway

• Occupancy remains firm at the 95 per cent level at which we have operated for most of the year and compares favourably to PMA’s vacancy measure for “big shopping centres” of ten per cent. In our view the rent foregone and direct cost of an extra one per cent vacancy in the year is a worthwhile investment in the ongoing quality, tenant mix and, ultimately, value of our prime assets

• We agreed 201 new long-term leases in the year, amounting to £42 million new annual rent, at an average of four per cent above previous passing rent (like-for-like units) and, excluding strategic deals reported in the third quarter, in line with valuers’ assumptions. Significant signings in the year include:

o new lettings addressing lease expiry concentrations at intu Trafford Centre, Cribbs Causeway and intu Potteries, also some important repositioning ahead of intu Braehead’s 2014 expiry concentration (see below)

o 12 retailers including Urban Outfitters, Adidas, Sealife, and The White Company took a unit in an Intu centre for the first time, with a substantial number of others opening further stores in additional centres

o 139 new shops opened or refitted in our centres in 2013, around five per cent of our 2,600 units. Tenants have invested around £70 million in these stores, a significant demonstration of their commitment to our centres. As well as major flagship store investments across the portfolio, Next chose intu Watford to launch their new concept Lipsy shopfit in December

• Like-for-like net rental income was 1.9 per cent lower in 2013 than 2012, with a narrower 0.9 per cent decrease in the second half. Tenants failing in late 2012 and early 2013 accounted for around £10 million of rent foregone and direct costs. Income interruption around concentrations of lease expiries also temporarily affected earnings from two centres

• At the property level, the total return from Intu’s portfolio has been robust at 7.3 per cent (2012 – 6.0 per cent) compared to the IPD quarterly index, retail, of 8.1 per cent (2012 – 1.5 per cent). The combination of capital value preservation and broadly stable income demonstrates the strength of Intu’s assets over the medium term

• The number of visitors to our centres has reduced marginally year-on-year in 2013, the two per cent decline representing a significant out-performance of Experian’s measure of UK national retail footfall which declined four per cent

• Estimated retailer sales in our centres were broadly flat in the year excluding the impact of trading interruptions during major tenant relocations at intu Braehead and Cribbs Causeway. The ratio of rents to estimated sales for standard units marginally reduced in the year to 13.5 per cent, continuing the trend of the previous few years

• The lease expiry cycle, while bringing the risk of some short-term earnings impact, is a good opportunity to effect significant repositioning. In the last two years 21 per cent of rent has been subject to expiry of which all but four per cent has been dealt with. In 2013, for example, six new retailers were introduced to intu Potteries and more than one in five stores were refitted. This gave a significant boost to the overall feel of the centre although the rental tone has settled at the lower level which was anticipated in the December 2012 valuation

At intu Braehead we created major new stores for Next and JD Sports, providing new anchors for areas of the centre and establishing improvement and change ahead of a concentration of expiries in 2014. The chart below illustrates that the pattern of lease expiries across the portfolio is broadly even, with a weighted average unexpired term of 7.5 years (31 December 2012 – 7.8 years)

12

Asset management We aim to create the best places to eat, drink, shop and socialise. We manage our centres to offer a mix of attractions to encourage our visitors to come from further, for longer, more often. This reinforces their position as must have locations for retailers. Experience As well as offering an evolving mix of the retail brands our customers want to see, with best flagship shopfits, and the catering and leisure options to encourage them to stay into the evening, we are focused on improving their overall experience in our centre including events, quality of service and environment:

• we have changed the look and feel of all our directly-managed centres with the roll out of the new brand’s refreshing style in the form of physical signage and new uniforms. More comprehensive refurbishments are also underway or imminent at a number of centres (see Looking to the future below)

• with the in-sourcing of facilities management and World Class Service training, we have aligned our teams with our nationwide brand aspirations and values, allowing us to take more control of the customer experience. Customer rating measured by our first Institute of Customer Services survey exceeded the retail sector benchmark

• our fibre-optic infrastructure now provides high quality Wi-Fi in nine centres with the final four to follow in early 2014 (see Market review above)

• as the only nationwide branded network of prime UK shopping centres, we can now entertain customers with quality events which offer a unique proposition to commercial partners. During the year we hosted significant footfall-driving events including a weekend-long nationwide performing arts expo, student nights attracting over 100,000 and generating over £2 million incremental sales, over 125,000 watching our Hello magazine-branded fashion shows, around 40,000 minutes of Cosmo-sponsored style advice plus the nationwide tour of a flagship arts programme, Elephant Parade

• with the single name for the Company and our centres, media coverage of events and news has roughly doubled

Catering and leisure Across the country, we have well over 400 catering and leisure outlets, which contribute 11 per cent of our rent roll. Our super-regional centres, which have always been day out destinations, have a notably higher proportion than most of those in city centres. Our research shows that those who eat or drink at one of our centres stay much longer and spend significantly more than just their extra dining expense. In 2013, around a third of visitors chose to dine and the amount on average they spent on catering rose by nine per cent. Our strategy for providing catering is not just about the volume of outlets – to encourage dwell and dine, we are focused on increasing the diversity of the offer. We offer a wider than ever range of operators with specific spend and dwell niches, regional as well as national and international operators. We have analysed gaps in each of our centres and are working on providing new clusters and zones to fill them. Our pipeline of investments (see below) will almost double the amount of dining and recreation space from 1.9 million sq. ft. to 3.4 million sq. ft., with the vast majority having obtained planning consent. At intu Lakeside, for example, our catering strategy is to close the current gap between the traditional fast food offer of the food court and the casual dining Boardwalk with its roughly three times longer dwell time and spend. We are introducing a range of new operators such as Wasabi, Rhythm Kitchen, Gino D’Acampo and Five Guys in a contemporary environment. Also the fourth champagne bar for our portfolio opened successfully at intu Lakeside just before Christmas.

UK acquisitions We believe that our scale and focus is key to our successful development and operation of UK prime regional shopping centres. Such assets are rarely traded, so where opportunities arise to acquire interests, particularly where our operator skills can be applied through our specialist asset and property management teams, we remain keen to consider the value creation opportunities.

13

We announced last month that we were in discussions with Westfield regarding the potential acquisition of its Derby shopping centre and its equity interest in Merry Hill, Dudley. Those discussions continue to progress satisfactorily. If the acquisition were to proceed, it is likely that it would be funded through a combination of new debt and equity raised through a rights issue. However, there can be no certainty that any transaction will be undertaken. In March 2013 we filled a gap in our national coverage, acquiring Midsummer Place, the aspirational fashion quarter of the UK’s number 16 retail destination by catchment spend, central Milton Keynes. Adjacent to centre:MK with the two centres treated as a single destination by shoppers, Midsummer Place’s major tenants include Debenhams, H&M, Apple, Superdry, Zara and Topshop. Since acquisition new retailers and catering operators including Hugo Boss, Timberland and Ed’s Diner have opened and Topshop/Topman has invested in a new flagship shopfit. In April 2013 we acquired Charter Place, Watford, adjacent to intu Watford, and have subsequently received planning consent for its replacement with a leisure- and catering-focused extension to the main centre (see Looking to the future below).

International In October 2013 we acquired with Canada Pension Plan Investment Board (“CPPIB”) Parque Principado Shopping Centre, Oviedo, a 75,000m

2 (approximately 800,000 sq. ft.) prime regional retail destination in Asturias, Northern Spain. One of Spain’s

top-ranked retail destinations with nine million visitors in 2013, the well-located and 98 per cent occupied centre is anchored by Primark, Zara, H&M, Cortefiel, C&A, Mango and Eroski hypermarket, with catering and leisure representing around 20 per cent of space. The net initial yield for the property at the implied purchase price of €162 million was 7.2 per cent. The acquisition, on attractive and earnings accretive terms, firmly establishes Intu’s presence on the ground in a country where we see considerable growth opportunities in the regional shopping centre industry and the potential to generate superior total returns over the long term. The market is quite fragmented in terms of ownership and considerable scope exists for improvement, along the lines of regionally pre-eminent destinations in the UK and elsewhere, in the shopping centre provision for many major catchments in Spain. Spain is one of the few major European countries without a committed pipeline of prime shopping centre developments and limited investor competition currently provides a contra-cyclical opportunity to acquire large, high quality centres at historically low pricing. Intu also has a site under option near Malaga in Andalucia, for 80,000m

2 of retail space with additional leisure and, as previously

announced, has entered into arrangements with Eurofund, a local partner with a track record of successful retail development, for pre-development activity on this site and at two major sites under option, in Valencia and Vigo. We are aiming to attract additional third party capital to assist with funding Intu’s Spanish activities without diverting significant financial resources from Intu’s organic development pipeline in the UK. In this context, we are actively investigating the creation of a special purpose investment vehicle for our Spanish activities, such as a Spanish REIT, following a number of recent regulatory improvements to this product. The Group also has the following other investments outside the UK:

• 11.4 million redeemable joint venture units in Equity One, a US retail REIT, providing an effective interest of nine per cent. These were received in January 2011 as a result of the restructuring of our previous direct investment in Californian property and are valued at £154 million based on the 31 December 2013 share price of $22.44. Dividends in the year amounted to $0.88 per unit. Equity One owns, develops and manages US neighbourhood shopping centres anchored by supermarket chains and has continued to be active in upgrading its property portfolio with an ongoing disposal programme of non-core assets. Operational metrics continued to improve in 2013 with leasing spreads on renewals and new leases showing good uplifts relative to previous rental levels

• 32 per cent of listed Indian shopping centre developer, Prozone, and ten per cent of its former parent company, the

Indian listed retailer Provogue, valued at a combined £37 million at 31 December 2013. Prozone has continued to progress the construction of its mixed-use projects at Coimbatore, Nagpur and Indore. Discussions are progressing with anchor tenants at the proposed Coimbatore shopping centre and an agreement has been signed with the multiplex cinema operator. The operational mall at Aurangabad has showed encouraging increases in tenant sales and footfall in 2013

14

LOOKING TO THE FUTURE

We have made significant progress in the year with our pipeline of organic development opportunities: • Two thirds of our 2.6 million sq. ft. of additional space has now received planning consent, including major extension

projects in Watford, Nottingham and at intu Lakeside • We have agreed with local authority partners in Watford and Nottingham a firm basis for major development

We have improved our financial flexibility to progress these projects by restructuring much of the debt which was to mature in the next few years. Since the end of 2013 we have increased the level of borrowing secured on intu Trafford Centre.

Further, we plan to recycle capital from existing assets to reinvest into these organic growth opportunities. This may include asset disposals and/or introducing partners into existing assets. For example intu Uxbridge is currently being marketed.

In the case of major extensions and creation of significant new or reconfigured space, we aim to achieve pre-letting of around two thirds of projects by space and the majority of the rent before proceeding with construction.

A particular area of focus is investment in improving the range, quality and setting of the dining and leisure options across our centres. These will reinforce the long-term attractiveness of the assets and, with operators keen to expand into our high footfall destinations, are intended to contribute to a superior financial return for shareholders.

Our plans include 1.5 million sq. ft. of extra catering and leisure space, an 80 per cent increase on the current level. 900,000 sq. ft. has already received planning consent and we have applied for a further 360,000 sq. ft.

Examples include the new food court at intu Lakeside, a new dining quarter at intu Eldon Square, a major new destination in the heart of Watford, a street food concept at Midsummer Place and a nine screen cinema at intu Potteries.

The table below sets out a summary of the project pipeline. In the case of expansionary projects which create additional space for which direct incremental rent can be identified, we would expect most projects to generate a stabilised initial yield on cost in the range of six to ten per cent and at least seven per cent for major projects. Where no significant additional space is created, we assess project return in the context of an internal rate of return based on the overall impact of the expenditure on centre performance through enhancing the ambience, the tenant mix and the rental tone.

Expected

Indicative Intu

Size1 construction investment

‘000 sq. ft. timing2 £m

Committed intu Lakeside food court refurbishment

3 – 2013-14 7

intu Victoria Centre refurbishment4 – 2014-15 40

intu Potteries leisure extension 58 2014-15 19 Other committed

5 41 2014-15 20

86 Active management pipeline

intu Trafford Centre – Barton Square courtyard

enclosure and second floor retail 112 2014-15 40

intu Bromley Queen’s Gardens restaurants 14 2014-15 4

intu Eldon Square “Sidgate” redevelopment and restaurants – 2014-15 12

intu Metrocentre “Qube II” restaurants – 2014-15 11

intu Lakeside hotel6 8 2014-15 7

Other active management5 89 2014-18 141

215

Major projects

intu Watford – Charter Place 380 2014-17 100

intu Broadmarsh redevelopment 51 2015-16 78

intu Lakeside leisure extension 225 2015-17 80

intu Lakeside Northern extension 438 2016-18 180

intu Braehead extension7 475 2016-18 200

Cribbs Causeway extension8 200 2018-20 30

intu Victoria Centre extension 505 2018-20 240

2,274 908

2,596 1,209

1 Represents net additional floor space of retail, catering and leisure

2 Timing subject to change due to a number of internal and external factors

3 Total project cost £9 million of which £2 million has already been spent

4 Total project cost £42 million of which £2 million has already been spent

5 Smaller committed and pipeline projects do not necessarily involve the creation of additional floor space

6 Size refers to catering element only

7 Size excludes arena and hotel

8 Intu share 33 per cent of total project cost of £90 million

15

Principal projects include: • intu Watford: our plans for a 380,000 sq. ft. extension to create a new shopping, dining and entertainment hub for

Watford received planning consent in January 2014. The anchor cinema is under offer and we are encouraged by the level of enquires for the large format retail and restaurant units. Subject to satisfactory pre-letting, we anticipate that enabling works could be under way by Winter 2014/15 with a target for completion in 2017

• Nottingham: we recently signed a major agreement with Nottingham City Council setting out a way forward for the complementary development of intu Broadmarsh and intu Victoria Centre. Our development of a restaurant quarter and significant refurbishment of intu Victoria Centre is underway. This project has already reignited interest from retailers currently not represented in the city. We will this year initiate public consultation on our leisure- and convenience-led refurbishment and redevelopment of intu Broadmarsh. Subject to legal and commercial preconditions, work could commence in 2015. Further, proposals for a possible extension of intu Victoria Centre have now received planning approval

• intu Lakeside: in addition to the food court refurbishment referred to above, we now have planning consent for two major projects which together would add over 600,000 sq. ft. of new retail, catering, leisure and hotel attractions, significantly increasing intu Lakeside’s draw and reach and providing more reasons to stay longer. Given the current high demand from restaurant and entertainment operators for the leisure scheme, we hope to secure sufficient pre-lets to start construction of a first phase in 2015

• intu Trafford Centre: having received planning consent to increase overall space and broaden the range of uses at Barton Square, we are in advanced negotiations with a major fashion retailer currently not represented at intu Trafford Centre for a flagship store on a new second floor. The enabling development, which we expect to start this year to complete in 2015, will include an impressive glass roof to enclose the central courtyard

• intu Metrocentre: as well as proceeding with our repositioning of Platinum Mall to create a more aspirational ambience, we have received planning consent for a 45,000 sq. ft. extension to the "Qube" dining area adjacent to the 12 screen Imax Odeon cinema. This will add a further 11 catering outlets and will introduce several new operators to the region. We anticipate securing sufficient pre-letting to start construction this year, to open in 2015

• intu Potteries: with a nine screen Cineworld cinema as a powerful anchor, we now have all five restaurant units exchanged or under offer and anticipate starting construction on the leisure extension shortly, for completion in 2015

• intu Eldon Square: our major refurbishment includes refreshing 65,000 sq. ft. of malls, replacing 13,000 sq. ft. of roof lights and constructing a new feature entrance from Northumberland Street and is due to complete later this year. We are carrying out the majority of the work overnight to minimise disruption to our shoppers and retailers, with up to 120 operatives on site each evening. Our proposed new restaurant cluster in the "Sidgate" mall area has received strong interest from operators new to the region as well as those already trading locally and, subject to pre-letting, we anticipate starting construction later this year

• intu Braehead: we are awaiting the outcome of the public enquiry by the Scottish Government into the Local Development Plan for Renfrew which should, amongst other things, confirm Braehead’s role as a town centre

Priorities for 2014 We will continue to focus in 2014 on four main goals which, we believe, will result in strong total returns over the medium term:

• optimising the performance of our existing assets, through active asset management – with customer experience as the focus for our business plan for each centre, we combine development, tenant mix and operational actions to address the needs and potential of each centre

• driving forward our £1.2 billion investment programme – as discussed above, with a majority of planning consents now secured, we will determine the timing of expenditure as we secure pre-lettings with the appropriate mix of retailers and operators to create new attractions for each of the destinations. In addition, where opportunities arise to acquire interests in appropriate assets, we will continue to consider strategic acquisitions

• continuing to improve our financial flexibility – we will proceed with debt issues and capital recycling from existing assets including disposals and possible introduction of partners in order to provide the funding at the appropriate time to undertake our investment programme. In February 2014 we issued further notes under the intu Trafford Centre CMBS transaction established in 2000

• reinforcing our brand and digital presence – following a successful roll out in 2013 we will develop our brand with its unique integration of digital and physical capabilities to drive demand for our assets and create broader commercial value. As well as completing our Wi-Fi installation programme at the final four centres, we are preparing trials of a number of property management and service innovations, analytical tools and upgraded online experience

David Fischel Chief Executive 28 February 2014

16

FINANCIAL REVIEW In 2013 the Group’s financial management has focused on creating the financing flexibility to advance the business. The Group has refinanced £1.8 billion of debt in the year, significantly de-risking the 2015-2017 debt maturities and demonstrating the Group’s prime assets can be financed at around 50 per cent loan to value at competitive interest margins. In addition to the £1.8 billion of debt financing, the Group issued 86 million new ordinary shares at 325 pence per share raising net proceeds, after costs, of £273 million to fund the acquisition of Midsummer Place. Key points of note

• A combination of market conditions and repositioning affected the financial results for the year (see Results for the year ended 31 December 2013 below):

o Underlying earnings of £140 million, up 2 per cent on 2012, giving earnings per share of 15.0 pence, down 7 per cent on 2012 due to higher level of shares in issue

o NAV per share at 380 pence; total financial return for the year 1 per cent • Improved financial flexibility (see Financial position at 31 December 2013 below):

o Debt to assets ratio at 48.5 per cent, below the Group’s target maximum level of 50 per cent. Actual ratio would reduce to around 44 per cent were the convertible bonds to convert to equity

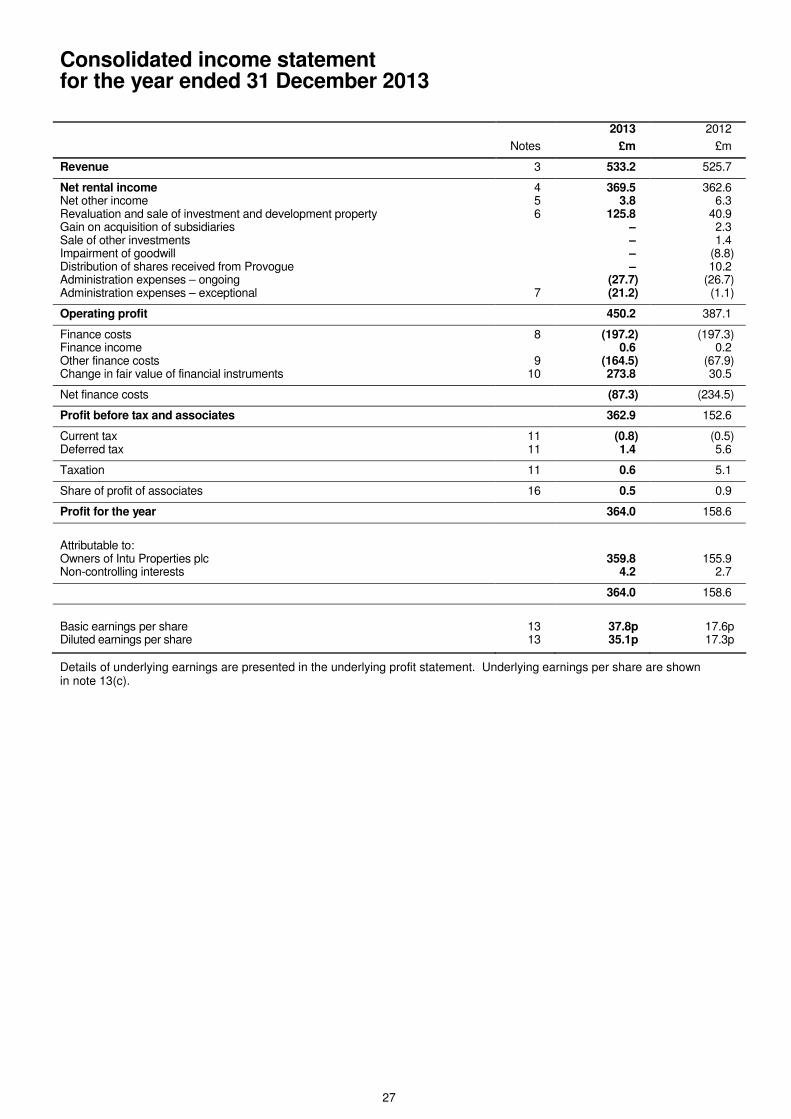

o Interest cover ratio at 1.71x, above the Group’s targeted minimum level 1.60x RESULTS FOR THE YEAR ENDED 31 DECEMBER 2013 Income statement The Group recorded a profit for the year of £364 million, an improvement on the £159 million reported for the year ended 31 December 2012. At an underlying level, excluding valuation and exceptional items, earnings were £2 million higher at £140 million (2012 – £138 million). The major factors in the £205 million increase in profit to £364 million are valuation related items, including:

• an increase in the revaluation gain on property valuations to £126 million (2012 – £41 million) • an increase in the credit arising from the change in fair value of the Group’s financial instruments. 2013 benefited from a

£274 million credit, whereas 2012 included £31 million These positive factors were partially offset by:

• higher exceptional finance costs of £158 million (2012 – £61 million), largely interest rate swap terminations in connection with the debt refinancing in the year (see below in Interest rate swaps section of this report)

Underlying earnings, which excludes valuation and exceptional items, were £2 million ahead in 2013 at £140 million as shown in the chart below and as set out in the Underlying Profit Statement. Taking into account additional shares issued as part of the Midsummer Place acquisition, underlying earnings per share reduced by 7 per cent to 15.0 pence.

17

The principal components of the change in underlying earnings are as follows: • while increasing overall due to the impact of the acquisitions of Midsummer Place and Parque Principado, like-for-like

net rental income reduced by 1.9 per cent largely due to the impact of tenant administrations in the first half of the year. This has been partially offset by the favourable impact of new lettings and rent reviews at intu Trafford Centre, Manchester Arndale and intu Lakeside

• as detailed in the table below the Group’s net rental income margin has remained in line with the 87 per cent achieved in 2012 with property operating expense reducing despite the acquisitions in the year, offsetting higher void costs. Property operating expenses in the year ended 31 December 2013 includes £10 million (2012 - £10 million) in respect of car park operating costs and the Group’s contribution to shopping centre marketing of £8 million (2012 - £8 million)

Year ended Year ended

31 December 31 December

2013 2012

£m £m

Gross rental income 448 442 Head rent payable (24) (25) 424 417 Net service charge expense and void rates (16) (13) Bad debt and lease incentive write-offs (9) (10) Property operating expense (29) (31) Net rental income 370 363

Net rental income margin 87% 87%

• underlying net finance costs, which exclude exceptional items, reduced by £1 million due to the favourable impact of

lower interest rates following the debt refinancings that were completed in the year offsetting the slightly higher debt levels

• costs related to intu Digital totalling £3 million which were in line with our plans in its first year • the impact of ongoing administration expenses increasing to £28 million (2012 – £27 million), largely due to costs of

new employees recruited throughout the year continuing the process of broadening the Group’s skill base Balance sheet The Group’s net assets attributable to shareholders have increased by £0.5 billion to £3.5 billion at the end of 2013 due to equity raised in the year to fund the acquisition of Midsummer Place and the retained profit for the year after payment of dividends. As detailed in the table below, net assets (diluted, adjusted) have increased by £289 million from December 2012 to £3,804 million as at the end of December 2013.

31 December 31 December

2013 2012

£m £m

Investment, development and trading properties 7,551.8 7,011.8

Investments 190.7 189.7

Net external debt (3,698.4) (3,504.2)

Other assets and liabilities (423.0) (691.1)

Net assets 3,621.1 3,006.2

Non-controlling interest (102.3) (29.2)

Attributable to shareholders 3,518.8 2,977.0

Fair value of derivatives (net of tax) 198.1 481.8

Other adjustments 83.7 56.6

Effect of dilution 3.8 –

Net assets (diluted, adjusted) 3,804.4 3,515.4

The largest factor in the increase in investment and development properties of £540 million is the acquisition of Midsummer Place and Parque Principado, valued at £251 million and £145 million respectively at acquisition. The 1.8 per cent valuation gain added £126 million to the value of the Group’s properties. The investments of £191 million as at 31 December 2013 comprise the Group’s interests in the US and India. The investment in the US comprises 11.4 million shares in a joint venture with Equity One, a listed US REIT. Based on the Equity One share price of $22.44 at 31 December 2013 the Group’s investment has been valued at £154 million.

18

The remaining investments represent the Group’s interests in India, largely comprising a 32 per cent interest in Prozone, a shopping centre developer, listed on the Indian stock market. As Prozone is classified as an associate company of the Group, the holding is valued as the Group’s percentage share of the associate’s underlying net assets. The carrying value of the investment is based on the Group’s accounting policies and therefore includes property valuations undertaken in accordance with “Red Book” guidelines. At 31 December 2013 Prozone’s listed shares were trading at a 75 per cent, £27 million, discount to the Group’s carrying value. We believe utilising independent valuations is the most appropriate valuation methodology at this time and will continue to monitor the situation. The reduction in other assets and liabilities in the year is due to the reduction in the provision for fair value of derivative financial instruments largely due to payments made in the year. The increase in non-controlling interest represents CPPIB’s 49 per cent interest in Parque Principado. Adjusted net assets per share As illustrated in the chart below, diluted, adjusted net assets per share were 380 pence at 31 December 2013, a reduction of 12 pence in the year. The most significant factor in the reduction is the termination of interest rates swaps as part of the debt refinancings in the year. This was partially offset by the property valuation gain that contributed 13 pence per share to the Group’s adjusted net assets per share. Total dividends of 15 pence per share were covered by the 15 pence per share of underlying earnings generated for the year.

Cash flow The cash flow summary below shows a net decrease in cash and cash equivalents of £26.6 million in the year.

2013 2012

£m £m

Underlying operating cash generated 338.0 344.3

Net finance charges paid (180.7) (191.5)

Exceptional finance and other costs (179.2) (62.1)

Net movement in working capital 0.8 (4.0)

Taxation/REIT entry charge (0.7) (11.0)

Cash flow from operations (21.8) 75.7

Capital expenditure on property assets (44.6) (81.2)

Sale proceeds of property/investments 15.6 49.9

Other investing activities – (17.2)

Acquisition of businesses (391.0) (4.2)

Cash acquired with businesses 8.9 1.6

Dividends (90.9) (117.2)

Cash flow before financing and equity raises (523.8) (92.6)

Net debt raised 159.7 192.7

Equity capital raised 273.0 0.1

CPPIB funding of Parque Principado 71.1 –

Other (6.6) (2.3)

Net (decrease)/increase in cash and cash equivalents (26.6) 97.9

19

Acquisition of businesses includes £249 million in respect of Midsummer Place and £142 million on Parque Principado. £71 million was received from CPPIB, the Group’s partner in the acquisition, giving a net outflow of £71 million for the Group’s economic share of the asset. Capital expenditure on property assets includes £8 million in respect of the purchase of two properties adjacent to the Group’s interest in Charter Place, Watford. Expenditure on existing assets included intu Eldon Square (£5 million), intu Lakeside (£5 million) and intu Metrocentre (£4 million). Net debt raised is discussed in the Debt structure section below.

The table below illustrates that recurring cash flow covers the 2013 interim dividend of 5.0 pence per share that was paid in the year and the proposed final dividend of 10.0 pence per share that will be paid subject to approval at the Annual General Meeting. The actual cash dividend outlay will be less than the 15 pence per share dividend declared due to the impact of scrip dividends. The cash saving to the Group in 2013 from the scrip take up on the 2012 Final and 2013 Interim dividends amounted to £56.2 million.

2013

Pence per

share

Underlying operating cash generated 36.1

Net finance charges excluding exceptional items (19.3)

Convertible bond coupon (0.6)

Net movement in working capital 0.1

Recurring cash flow 16.3

Dividends paid and proposed for 2013 15.0

Capital commitments The Group has an aggregate cash commitment to capital projects of £86 million at 31 December 2013. In addition to the committed expenditure, the Group has an identified uncommitted pipeline of active management projects and major extensions that may become committed over the next five years (see Looking to the future above). It is anticipated that a total of approximately £70 million will be spent on capital projects in 2014. Tax strategy and charge for the year Being a Real Estate Investment Trust (REIT) significantly reduces the taxation costs of the Group, but brings with it the requirement to operate within the rules of the REIT regime. The Group’s approach to taxation is approved by the Board and is subject to regular review. The Group maintains an open, up-front and no-surprises policy in dealing with HMRC. The Group seeks pre-clearance from HMRC in complex areas and actively engages in discussions on potential or proposed changes in the taxation system that might affect property tax and REIT legislation. Since becoming a REIT in 2007 the Group has paid REIT entry charge payments of £199 million. The Group continues to pay tax on overseas earnings, any UK non-property income under the REIT rules, business rates, and transaction taxes such as stamp duty land tax and (until 17 July 2012, when it was abolished) the REIT entry charge. In the year ended 31 December 2013 the total of such payments to tax authorities was £26.5 million, of which £25.0 million was in the UK, £0.6 million in the US and £0.9 million in Spain. In addition, the Group also collects VAT, employment taxes and withholding tax on dividends for HMRC. Business rates, principally paid by tenants, in respect of the Group’s properties amounted to around £261 million in 2013. The tax credit in the year of £0.6 million comprises current tax expenses on the Group’s US and Spanish investments of £0.6 million and £0.2 million respectively, offset by a deferred tax credit of £1.4 million largely on the revaluation of interest rate swaps and investments.

20

FINANCIAL POSITION AT 31 DECEMBER 2013 At 31 December 2013, the Group had net external debt of £3,698 million, an increase of £194 million compared to 31 December 2012. In addition to cash balances of £166 million the Group had undrawn facilities of £90 million and £69 million of CMBS notes issued by intu Metrocentre which were received as cash in February 2014. This gave total headroom at the end of 2013 of £325 million. Debt structure A significant proportion of the Group’s debt has been refinanced in the year. The majority of the debt still remains largely arranged on an asset-specific basis, with limited or non-recourse from the borrowing entities to other Group companies. As a result of the refinancings the Group has diversified its sources of funding. The range of debt instruments now includes CMBS and other bonds plus syndicated bank debt with corporate-level debt remaining limited to the revolving credit facility and convertible bond.

Following the refinancing activity in the year the above chart illustrates that there is a minimal refinancing requirement in the next two years. During the year there was a significant amount of financing activity, including: In February the Group established a new debt funding platform (“Secured Group Structure”) by contributing £2.3 billion of assets into a flexible, ring-fenced security pool and raising £1.15 billion of bond and bank debt secured on it. The inaugural bond issue was highly successful with strong demand resulting in two tranches of ‘A’ rated bonds totalling £800 million being issued with the balance of £350 million provided by a five year bank loan. The bond tranches of £450 million and £350 million mature in 2023 and 2028 respectively. The debt was raised at a blended cost of 4.4 per cent, in line with previous funding cost of debt secured on the four assets, whilst extending the weighted maturity on these assets from 2 years to 10 years. The structure has a tiered operating covenant regime giving the Group a significant degree of flexibility when the covenant measures are below certain levels. In higher tiers the level of flexibility is reduced. Further details are given in the Financial covenants section of this report. In July the Group arranged a £125 million facility secured on Midsummer Place. The facility is for a term of three years and three months with the possibility of being extended up to a further two years subject to both parties agreeing. In November the Group issued a £485 million bond secured on intu Metrocentre the proceeds being used to repay the existing facility secured on the centre. The bond was a single issue 10 year tranche at a rate of 4.125 per cent and represented a 55 per cent loan to value ratio. The cost of borrowing of the new bond represented a saving of 160 basis points compared to the previous facility. In connection with the repayment of the previous bonds £31 million of cash payments were required to terminate interest rate swaps and are included in the £158 million exceptional finance cost in the year.

31 December 31 December

2013 2012

Debt to assets 48.5% 49.5%

Interest cover 1.71x 1.69x

Weighted average debt maturity 8.0 years 6.1 years

Weighted average cost of gross debt 4.8% 5.2%

Proportion of gross debt with interest rate protection 92% 95%

The table above summarises the Group’s main debt measures, with the average maturity increasing and the average cost decreasing as a result of the refinancings in the year. The proportion of debt with interest rate protection has reduced due to drawings of £285 million of the unhedged revolving credit facility at 31 December 2013. This facility was not drawn at the end of 2012.

21

Interest rate swaps Just over 40 per cent of the Group’s debt is floating rate. The Group uses interest rate swaps to fix short- and medium-term interest obligations, reducing cash flow volatility caused by changes in interest rates. Combining the impact of this hedging and the fixed rate debt the Group’s debt is effectively 92 per cent fixed. The table below sets out the nominal amount and average rate of hedging, excluding lenders’ margins, in place under current and forward starting swap contracts.

Average

Nominal amount rate

In effect on or after: £m %

1 year 1,791 3.39

2 years 1,862 3.45

5 years 804 4.99

10 years 678 4.82

15 years 668 4.83

20 years 443 4.59

The nominal value of interest rate swap contracts has reduced by £1.1 billion to £2.1 billion at 31 December 2013 due to terminations associated with refinancings completed in the year. The majority of new debt raised in the year is fixed rate therefore terminated swaps have not been replaced. The fair value net liability of these interest rate swaps at 31 December 2013 is £206 million, a reduction of £287 million from the £493 million at 31 December 2012. This movement in the liability can be largely attributed to cash payments in respect of the reduction in the nominal value described above. Cash payments in the year in respect of interest rate swaps totalled £215 million of which £153 million has been classified as an exceptional finance cost as it relates to the termination of swaps (£128 million) or payments in respect of unallocated swaps (£25 million). The balance of the payments have been included as underlying finance costs as they relate to ongoing interest rate swaps used to hedge debt. The majority of the additional reduction in the fair value liability of £72 million is due to a movement in the interest rate yield curve reducing the required fair value provision for the ongoing interest rate swaps. As previously detailed, the Group has a number of interest rate swaps which are unallocated as, due to a change in lenders’ practice, they cannot be used for hedging the Group’s borrowings. Using the 31 December 2013 forward interest rate yields, these swaps have a market value liability of £143 million (2012 - £199 million). Based on these rates and values, it is estimated the Group will be required to make cash payments on these swaps of £25 million in 2014 in line with the level of payments made in 2013. Covenants Full details of the loan financial covenants are included in the Financial covenants section of this report. The Group is in compliance with all of its corporate and asset-specific loan covenants. As detailed in that analysis, the headroom over the minimum covenant levels has generally increased in the year. Matthew Roberts Finance Director 28 February 2014

22

KEY RISKS AND UNCERTAINTIES Intu’s Board has overall responsibility for managing risk across the Group and establishing the Group’s appetite to risk based on the balance of potential returns and negative impacts. Intu recognises that it faces a number of risks in achieving its strategic objectives. Effective identification and management of these risks is a major factor in Intu’s ability to deliver these objectives. Our risk management framework targets the early identification of key risks and the formation of plans to remove or mitigate them. We apply the methodology of identify, analyse, action and implement, together with our overall culture of risk management to ensure that everyday management decisions are taken in the context of sound risk management principles as well as achieving our strategic objectives. This involves all areas of the business in identifying and reviewing risk and creating appropriate action plans in line with the Group’s risk appetite. Identify and analyse: Operational reviews focus on the impact of changing risks on each function’s key objectives and, along with review of current controls, are subject to executive challenge. The executive team also conducts a strategic review of changes in the overall environment which may hinder the business. Action plans are subject to a detailed review and challenge process, including by the Audit Committee and Board. Implementation is regularly monitored and informs the next phase of identification and analysis. The risk management process continues to evolve to provide Intu with appropriate methodology as the operating environment changes. The key risks and uncertainties facing the Group are as set out in the table below:

Change in Risk and impact Mitigation level of risk 2013 commentary Property market Macro environment weakness could undermine rental income levels and property values, reducing return on investment and covenant headroom

• Focus on prime assets • Covenant headroom monitored and

stress tested • Regular monitoring of tenant

strength and diversity

- • Overall increase in valuation of assets, out-

performing IPD benchmark

• Reinforcing our prime centres with emerging brands and broader offer of leisure and catering, including reconfiguration of space to meet retailer demand

• Digital investment to improve relevance as shopping habits change

• Improvement in covenant headroom on individual properties during the year

Financing Reduced availability of funds could limit liquidity leading to restriction of investing and operating activities and/or increase in funding cost

• Regular reporting to Board of current and projected funding position

• Effective treasury management aimed at balancing long debt maturity profile and diversification of sources of finance

• Consideration of financing plans including potential for recycling of capital before commitment to transactions and developments

���� • Major refinancings significantly reduced risk of upcoming maturities – £1.8 billion of new facilities in the year:

• innovative new security platform • extension of maturity profile • diversification of sources • reduced cost of debt

23

KEY RISKS AND UNCERTAINTIES (continued)

Operations Accidents, system failure or external factors could threaten the safe and secure environment provided for shoppers and retailers, leading to financial and/or reputational loss

• Strong business process and procedures supported by regular training and exercises

• Annual audits of operational standards carried out by internal and external consultants

• Culture of visitor safety • Rigorous ICT security framework;

crisis management simulations include cyber security threats

• Retailer liaison and briefings • Appropriate levels of insurance

- • Significant operational change implemented, with smooth transition to in-sourced facilities management managed through a large scale mobilisation project. Risk of change mitigated by detail of contract, choice of culturally aligned and experienced partner and major training programme

• New structure better uses Intu’s scale and efficiently delivers better control, consistency and application of best practice, e.g. new Group-wide structure for quality, safety, health and environment management. Preparation is underway to achieve ISO accreditation in 2014/15

• Undertaking review of cyber risks in context of new digital services

• Review of insurance partners, with new appointment better aligned to business structure

• Robust crisis management and communication protocols tested and improved with major exercises

• Reduced exposure to future energy costs and taxes through award-winning energy reduction initiatives – 18 per cent reduction in carbon emissions since 2011

Strategy and execution Misjudged or poorly executed strategy fails to create shareholder value

• Annual strategic review by Board informed by external research and advice

• Board and management team experienced in shopping centre and broader retail industry

• Engagement with national and international retailers

• Specialist advice and extensive research supporting major initiatives

• Careful assessment of potential partners to complement Intu’s skills and resources

���� • Rigorous control and review procedures in place to ensure successful implementation of significant strategic initiatives executed in the year including:

• Regular reporting to and review by Board of progress on rebranding, in-sourcing of facilities management, investment in digital infrastructure and services and non-UK expansion

• Specialist advice on evolving digital strategy

• Development of KPIs for monitoring of key deliverables

Development and acquisition Misjudged or poorly executed project results in increased cost or income foregone, hence fails to create shareholder value

• Capital Projects Committee reviews detailed appraisals before and monitors progress during significant projects

• Research and third party due diligence undertaken for transactions

- • Property and market due diligence and detailed business plans developed before acquisition in Spain

• Significant detailed planning, appraisal and analytical exercises underway in advance of committing to major extension projects

• Continued focus on pre-letting space before committing capital to projects

24

25

26

Statement of Directors’ Responsibilities The Group’s Annual Report for the year ended 31 December 2013 contains the following statement of Directors’ responsibilities. Certain parts of the Annual Report are not included within this announcement. The Directors are responsible for preparing the Annual Report, the Directors’ remuneration report and the financial statements in accordance with applicable law and regulations. Company law requires the Directors to prepare financial statements for each financial year. Under that law the Directors have prepared the Group and Company financial statements in accordance with International Financial Reporting Standards (IFRSs) as adopted by the European Union. Under company law the Directors must not approve the financial statements unless they are satisfied that they give a true and fair view of the state of affairs of the Group and the Company and of the profit or loss of the Group and Company for that period. In preparing these financial statements, the Directors are required to: (a) select suitable accounting policies and then apply them consistently (b) make judgements and accounting estimates that are reasonable and prudent (c) state whether applicable IFRSs as adopted by the European Union have been followed, subject to any material

departures disclosed and explained in the financial statements (d) prepare the financial statements on the going concern basis, unless it is inappropriate to presume that the Company will