Embed Size (px)

Citation preview

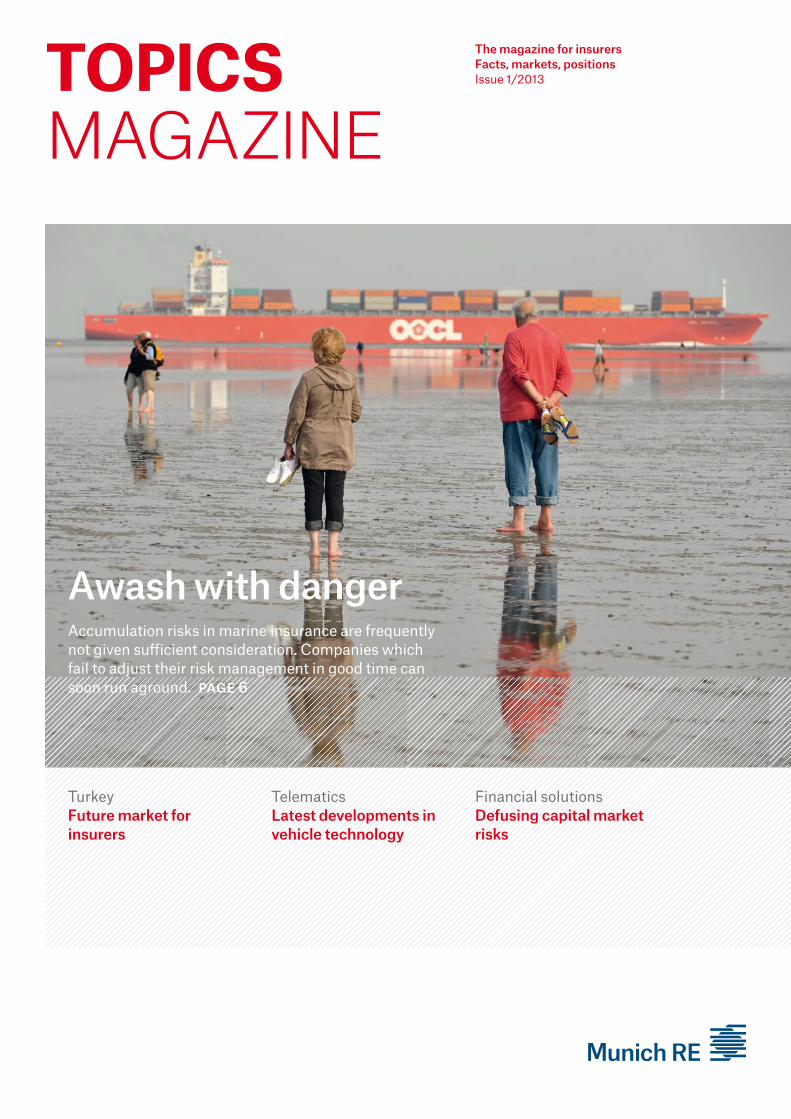

Awash with danger

TelematicsLatest developments in vehicle technology

Financial solutionsDefusing capital market risks

TOPICSMAGAZINE

The magazine for insurersFacts, markets, positionsIssue 1/2013

TOPIC

S M

AG

AZIN

E 1/2013A

ccumulation risks in m

arine insurance · Market study Turkey · Telem

atics · Financial solutionsM

unich Re

Accumulation risks in marine insurance are frequently not given su� icient consideration. Companies which fail to adjust their risk management in good time can soon run aground. PAGE 6

TurkeyFuture market for insurers

1Munich Re Topics Magazine 1/2013

Editorial

Dear Reader,

Optimists see every problem as something that demands to be solved. They have a similarly constructive approach to challenges, which gives them a huge advantage over pessimists. The optimist sees risk as an opportunity. Finding the right balance between risk and opportunity is also ultimately what our work is about. Genuine success comes only to those that can identify and properly assess both sides.

The devastating natural catastrophes of recent years have heightened risk managers’ awareness of the fact that accumulation losses can reach astronomical levels in the worst case. And yet there are still areas where this problem is not given sufficient consideration. Our cover story highlights the special features of marine risks and shows how insurers operating in this sphere can identify accumulations that could threaten their survival, and adjust their exposure accordingly.

Turkey’s economic performance and assured foreign policy have impressed many observers in recent years. Now Ankara is looking ahead to the Republic of Turkey’s centenary in 2023, by which time it hopes to be one of the world’s ten leading economies. This rapid development also opens up many opportunities for the insurance industry. Read our market analysis to find out more.

What will the future bring? Exciting innovations for one thing. For ex ample, driverless cars that can take you anywhere you want to go. “The allseeing black box” is an article that will give you a taste of what the world of telematics will bring us in the future.

I hope you find this issue of Topics interesting and informative, and remain every bit as optimistic in 2013.

Munich, December 2012

Dr. Torsten JeworrekMember of the Munich Re Board of Management and Chairman of the Reinsurance Committee

NOT IF, BUT HOW

2 Munich Re Topics Magazine 1/2013

6Containing accumulation risks

Controlling accumulations does not always receive the attention it merits in marine insurance, as mobile risks are so difficult to assess. But even the specific features of marine risks can be addressed by means of adequate risk management. We highlight trends, developments and solutions.

3Munich Re Topics Magazine 1/2013

Life insurers have been severely affected by the financial crisis. Munich Re offers life insurers tailored solutions and advice on corporate financing.

3016

MarinEAvoiding accumulation risks 6 Risk managers should be addressing the topic of accumulation control in marine insurance.

turkEyAnatolian tiger poised to pounce 16A competitive economy and consolidated budget are pointing the way forward for Turkey. A market study.

Price competition affects all players 20Muzaffer Aktaş, Managing Director of reinsurance brokers Willis Re in Turkey, talks about the current state of the Turkish insurance market and outlines its future prospects.

Effective support for Turkish farmers 27Tarsim – How the governmentsupported agricultural insurance pool works. risk ManagEMEnt solutionsNew ways to manage undiversifiable risks 30Solutions that help life insurers on key corporate finance issues.

logisticsAttention! Perishable goods 36Technological progress presents new challenges in the transport and storage of perishable goods. How insurers can adapt their products to meet these new challenges.

tElEMaticsThe all-seeing black box 40 Vehicles that can reach their destination without drivers, talk to traffic lights and communicate with one another.

Editorial 1News 4Literature 39Column 46Imprint 47

Contents

Turkey’s ambitious goal: It wants to be among the top ten global economies by 2023. An overview of the economic situation and insurance market in Turkey.

Know

ledge in dialogue 2013M

unich Re

Knowledge in dialogueClient seminar programme 2013

4 Munich Re Topics Magazine 1/2013

nEws

Nikolaus von Bomhard has been named 2012 “Insurance Leader of the Year” by St. John’s University’s School of Risk Management in New York. The school has presented this annual award to industry leaders for outstanding achievement since 1995. Widespread admiration for his style of leadership in the service of all Munich Re stakeholders was one of the reasons cited for the award. His personal approach to leadership and his stance on economic and political issues in these testing times was another. The School of Risk Management was founded in 1901 as the Insurance Society of New York. It was merged with St. John’s University in 2001. The official awards ceremony will take place on 16 January 2013 in New York.

awardNikolaus von Bomhard is the 2012 insurance manager of the year

Munich Re has an attractive programme of seminars and workshops in 2013 tailored to the needs of our international clients. We have around 50 seminars and workshops on primary insurance and reinsurance topics in life and nonlife areas as well as a selection on enterprise risk management at insurance companies. The seminars are held in Munich and at other locations in our international organisation. With the “Knowledge in dialogue 2013” seminar programme, we offer our clients an ideal forum for knowledge transfer and for constructive dialogue and networking. If you are interested in receiving a copy of the “Knowledge in Dialogue” programme, just contact your Client Manager.

>> More information at connect.munichre.com

cliEnt sEMinarsUp-to-date knowledge

The inaugural RISK Award was presented at the International Disaster and Risk Conference (IDRC) in Davos on 26 August by the Munich Re Foundation, UNISDR and GRF Davos. The €100,000 prize (the highest riskprevention award in the world) went to a stunningly simple earlywarning system developed specifically for Beira in Mozambique, but which could easily be replicated throughout the world. Hollow tubes with a float inside are installed at strategic points in rivers, streams and drainage channels. If the water level rises, an electric switch is tripped by means of the snorkel principle. Local people can then take themselves and their belongings to safety.

>> More information at www.munichre-foundation.org/de/ home/Projects/DisasterPrevention

risk awardA simple but ingenious early-warning system

Since August 2012, Munich Re has been supporting a twoyear project to protect buildings, infrastructure and human lives in Aizawl, India. Our partner in this project is the nonprofit organisation GeoHazards International, which aims to reduce loss of life and suffering from geological perils in the world’s poorest regions. For example, the project supports a programme in India to make schools more earthquakeresistant. More information can be found at www.geohaz.org.

In its new information platform Touch Engineering, Munich Re presents solutions competence for the insurance of technical risks. You can find out about interesting Munich Re engineering projects, get to know our experts and read about our range of services. www.munichre.com/engineering

The Munich Re Foundation’s 2013 Dialogue Forums will focus on the topic “The (im)mobile society – Ready for the future?” The series of forums will run from January to May 2013. Participants at these five events will include leading figures from politics and the economy, who will be joined by experts on the environment, climate, transport, energy, ergo nomics and the social sciences to discuss this topical issue. You can find out more at www.munichre-foundation.org.

It may surprise many people to know that the increase in weatherrelated loss occurrences is highest in North America not Asia. Our new client publication “Severe weather in North America” offers a detailed analysis of the different weatherrelated risks and exposure in North America. You can obtain “Severe weather in North America: Perils – Risks – Insurance“ via our client portal connect.munichre.com.

News in brief

5Munich Re Topics Magazine 1/2013

nEws

Topics: The havoc wreaked by Hurricane Sandy on the power stability of the northeastern US surprised many people worldwide. Your office is based in Connecticut, one of the hardest hit states, where some 600,000 people lost power for days on end. Can you describe the experience?

William H. Bartley: Imagine a twentyfoot wall of water coming down the street, a surge powerful enough to take out entire neighbourhood blocks – houses, stores, cars, all gone. That’s what we saw happen down the coast from New York to Virginia. The damage was devastating in many areas. Hundreds of thousands of people lost power for days, and in many cases, for weeks.

As an electrical engineer and expert on power systems, how would you explain the technical reasons behind the widespread blackouts?

We have two ways of distributing power: above ground and below ground. Within densely populated urban areas, substations, breakers, transformers and cable systems are often located underground in tunnels or subway systems. When the water came surging into the New York and New Jersey area, these systems were all flooded. The utilities had to shut them down to prevent extensive damage and avert safety hazards. Utility crews had to wait until the water had receded before they were able to go down there and reenergise the systems.

Hurricane Sandy brings New York to a standstill

And what about areas that rely on aboveground distribution?

Many people throughout the US – in cities and rural areas alike – receive power distributed by way of aboveground cables and poles. And in the areas affected by Sandy, thousands of these were damaged by strong winds and falling trees.

Is one system more impervious to damage than the other?

Unfortunately both systems are ul tim ately vulnerable to nature. Flood waters can cause as much damage to underground systems as high winds to aboveground power lines and poles. Cost is also a consideration. Building the infrastructure required to install distribution and transmission lines underground is extremely expensive.

Does the energy mix itself play a role in the stability of a city’s power distribution?

Not in terms of system damage caused by natural or manmade disasters. Like coalfired generation plants, renewable energy sources – such as large wind or solar farms – have to be hooked up to the power transmission grid. If power lines are down or a substation fails, the energy source itself doesn’t matter. It’s simply a distribution problem.

So what can be done to prevent these types of mass outage in the future?

We can’t always prevent a power outage, but through better emergency planning, we can reduce the impact.

natural hazards

Being prepared means having a plan, procedures, regular training and readiness drills. When something like Sandy comes along and knocks out the power for hundreds of thousands of people in multiple states, a tremendous amount of coordination among utility companies and engineers is required – from the initial assessment and diagnostic phases to safe restoration.

What sort of advice do you offer clients in terms of safeguards against blackouts?

While the risks associated with power outages can’t be fully mitigated, we do advise our clients to develop their own preemergency plans for computer backup, water and emergency power. We also advise our clients to use more energyefficient equipment that not only reduces the burden on the power grid, but also benefits the environment in the long run.

William H. Bartley, P.E., is Assistant Vice President and Principal Electrical Engineer at Munich Re’s subsidiary, The Hartford Steam Boiler Inspection and Insurance Company.

William H. Bartley, P.E., sheds some light on power supply and stability in the USA.

7Munich Re Topics Magazine 1/2013 7

Marine

Christian Forwick and Gerhard Vogl

As a rule, when the insurance sector turns its atten-tion to accumulation losses, property insurance takes centre stage. Major natural catastrophes in recent years have heightened risk managers’ awareness of the fact that extremely high losses can accumulate here in the worst case. In the special line of marine insurance, on the other hand, the problem of accumu-lation continues to receive far too little attention. Quite a risk, considering that this sector is taking up an increasing proportion of insurers’ portfolios. The reasons are various: Transport capacities by sea, land and air are increasing throughout the world and both port logistics and speed of trans-shipment are keep-ing pace with this development. This results in higher value concentrations and consequently higher insured values. Offshore energy is also gaining in importance. The Gulf of Mexico alone has around 4,000 oil platforms. Even a moderately severe hurri-cane could lead to enormous losses there.

Real treasures can be found here in Singapore’s port and container terminals. Constantly increasing value concentra-tions lead to ever higher insured values.

Avoiding accumulation risks Global transport capacities, value concentrations and insured values are all rising to unprecedented levels. Companies which fail to adjust their risk management in good time can soon run aground under Solvency ii.

However, there are already enough sophisticated, state-of-the-art modelling tools for offshore energy risks to ensure that accumulation risks are adequately assessed. With these tools, leading providers of off-shore energy capacity can successfully control their accumulated liability commitments.

Risk of multi-line loss accumulations

Considered in isolation, marine exposure should not pose any great problem for the majority of property-casualty insurers. Despite this, companies operating predom inantly in property insurance should not neglect supposedly less highly exposed lines of busi-ness such as marine insurance, for the problem of accumulation can intensify existing negative trends in the property sector or jeopardise tightly calculated profitability margins. The extreme case of a multi-line accumulated loss can even escalate into a threat to a company’s continued existence. For instance, if a major port were to be destroyed by an earthquake or tsunami. Losses under property and marine covers

8 Munich Re Topics Magazine 1/2013

Marine

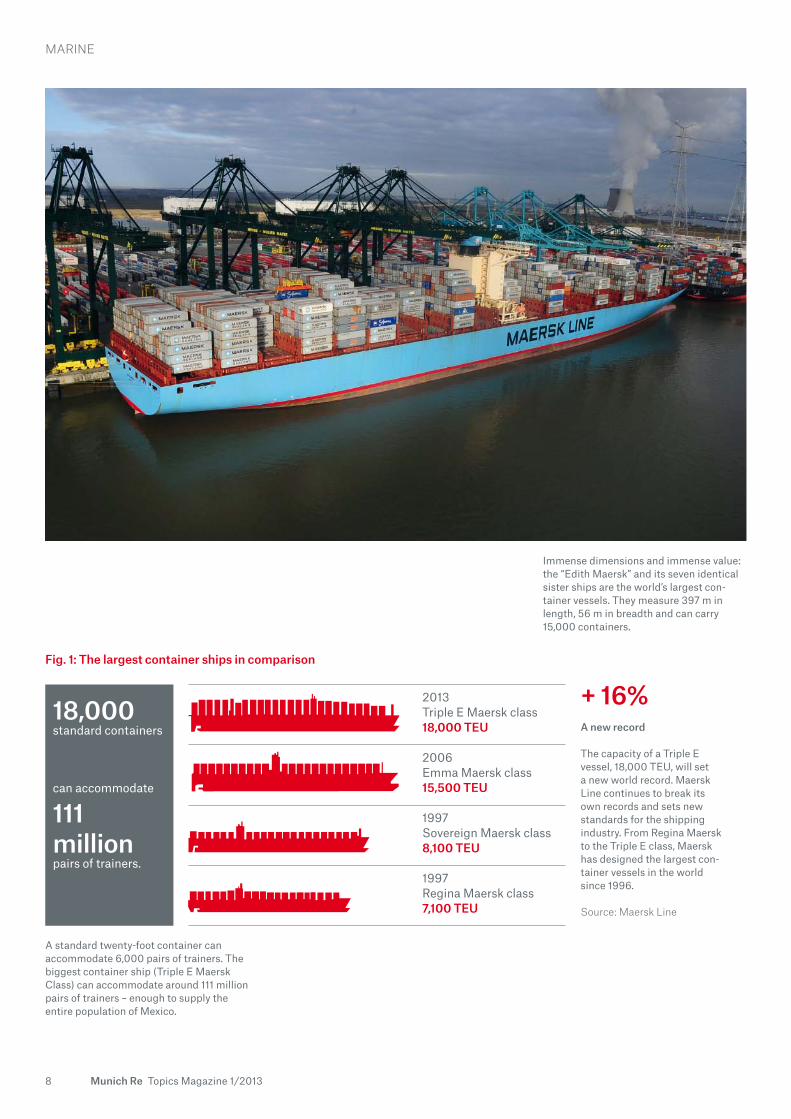

Fig. 1: The largest container ships in comparison

+ 16%A new record

The capacity of a Triple E vessel, 18,000 TEU, will set a new world record. Maersk Line continues to break its own records and sets new standards for the shipping industry. From Regina Maersk to the Triple E class, Maersk has designed the largest con-tainer vessels in the world since 1996.

Source: Maersk Line

2013Triple E Maersk class18,000 TEU

2006Emma Maersk class15,500 TEU

1997Sovereign Maersk class8,100 TEU

1997Regina Maersk class7,100 TEU

18,000standard containers

can accommodate

111 millionpairs of trainers.

A standard twenty-foot container can accommodate 6,000 pairs of trainers. The biggest container ship (Triple E Maersk Class) can accommodate around 111 million pairs of trainers – enough to supply the entire population of Mexico.

Immense dimensions and immense value: the “Edith Maersk” and its seven identical sister ships are the world’s largest con-tainer vessels. They measure 397 m in length, 56 m in breadth and can carry 15,000 containers.

9Munich Re Topics Magazine 1/2013

Marine

could very quickly accumulate in such a case, for example if the port has large warehouses and oper-ates as a trans-shipment centre. Obvious and usually considerable property losses suffered by the stored goods are not infrequently accompanied by conse-quential losses due to disrupted production chains directly leading to business interruption/contingent business interruption losses. The major earthquakes in Japan (11 March 2011/magnitude: 9.0) and Chile (27 February 2010/magnitude: 8.8), the floods in Aus-tralia in late 2010/early 2011 and the floods in Thai-land in late 2011 are examples of recent losses with a high exposure for marine insurers.

Unlike the stationary risks encountered in property insurance, marine risks are normally mobile. Never-theless, goods can easily remain in one place for a longer period of time (up to 60 days according to the Institute Cargo Clauses (ICC) and sometimes consid-erably longer); major fluctuations in insured values and accumulations at the storage locations are conse-quently characteristic features of cargo business. It is often claimed that potential loss accumulations can-not be determined in advance because it is impos-sible to say exactly when any given number of risks will aggregate in a certain place. The loss accumula-tion scenarios, risk models and vulnerability curves which have proved their value in property insurance are therefore unlikely to yield satisfactory results when determining the probable maximum loss in marine business.

Special features of mobile risks

However, this stance does not stand up to closer scru-tiny, for parallels do indeed exist: a significant number of marine risks are likewise stationary and subject to assessment criteria very similar to those used in prop-erty business. They include the majority of offshore oil and gas platforms, shipyards, marinas, exhibition goods (fine art) and warehouses with revolving stocks. They all have a fixed location, but fall within the domain of marine insurance.

The accumulated insured values or insurance limits can therefore be determined fairly accurately. Another feature common to many mobile risks is that they come together for a certain period of time in such trans-shipment and trading “hubs” as distribution warehouses, ports, exhibitions and museums.

This basically means that no line of marine insurance business can be excluded when considering accumu-lations. On the contrary, the possible magnitude of loss following a major event must be individually established for each line of business and correlations between the individual lines taken into account, as they are usually linked by a close causal relationship. The following trends and developments must be noted:

Not colourful Lego bricks scattered about a child’s playroom but innumerable con-tainers that were whirled about and scat-tered like toy bricks by the tsunami on 12 March 2011 in Sendai, northern Japan.

11Munich Re Topics Magazine 1/2013

Marine

0

5

10

15

20

0,0

0,2

0,4

0,6

0,8

1,0

20,000

18,000

16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

Fig. 2: Development of world trade

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

The increasing globalisation of the economy since the beginning of the 21st century has led to substantial growth in world trade.

Source: WTO

– Increasing trade flowsForeign trade volumes are being driven steadily upwards by globalisation and the associated inter-connection of otherwise distant economic regions. Growth has become enormously dynamic as markets have opened up and taken their place in the global division of labour, allowing such booming economies as the BRIC countries (Brazil, Russia, India and China) to grow at above-average rates. Increasingly short product life cycles, especially for electronic devices (smartphones, tablets, laptops) are another driving force leading to ever higher trade volumes. They are also boosted by the general cost-motivated increase in the speed of sales (“time is money”), as reflected in the continuing trend towards just-in-time logistics systems. Insurers must expect higher exposures as a result of these trends and developments. Stockyards, warehouses, trading centres and ports are exposed to the perils typical of coastal regions – particularly floods, earthquakes, tsunamis and windstorm – with corresponding accumulation risks for insurers’ global marine portfolios.

– Growing transport capacitiesModern container vessels can carry roughly 15,000 standard twenty-foot containers instead of the 700 carried in 1967. As a result, the insured value of the cargo is frequently in the range of €1bn or more. In order to cut transport costs further, ships measuring 400 m in length and accommodating up to 18,000 TEU are soon to be launched (see Fig. 1: Development of

ship sizes). An accumulation of individual major risks, such as a collision between two “mega-ships” (tankers, container vessels), is a possible scenario, considering the steadily rising tonnages and increas-ing density of shipping traffic. The probability of such an event increases as crew sizes are cut, standards of training decline, language barriers increase and cost-cutting measures take their toll on safety standards. Furthermore, the marine lines are also strongly linked: a collision may not only result in the total loss of cargo and vessel, the shipowner’s liability insurance may also have to pay the cost of remedying the environ-mental damage.

– Higher exposure in shipbuildingThe trend towards bigger tonnages and better tech-nological standards is driving up the hull value of shipbuilding projects. Standardisation and more effi-cient production processes are also leading to shorter construction times, with the result that shipyards can work on several projects simultaneously. In the event of a builders’ risk loss, substantial additional exposure must be expected in the form of delayed delivery and the resultant consequences for business interruption insurance.

– Accumulation potential of port facilitiesPort facilities (including piers, wharves, docks, dis-patch terminals, loading and loading logistics, ware-houses) are essentially stationary risks of a predom-inantly property nature and consequently have similar accumulation scenarios. Considered in isolation, port facilities do not constitute any undue risk for the insurer. When viewed in combination with other marine risks, especially the goods stored in the port, however, the situation looks very different.

Luxury yachts moored tightly side by side in Monaco’s harbour. The resultant accu-mulation potential is considerable, particu-larly as pleasure craft spend most of the time anchored in their home marina.

US$ bn

12 Munich Re Topics Magazine 1/2013

Marine

For all classes of insurance, the problem essentially lies in property-type risks. Since port facilities are often located near large cities or even form part of an industrial city, they should always be included in the overall assessment of accumulation risks. This was clearly demonstrated by the earthquake off the Jap-anese coast in March 2011. The subsequent tsunami caused major damage along a stretch of coast several hundred kilometres long. The insured losses were immense and affected not only property, but also the sectors marine hull, marine cargo and even aviation.

– Value concentration in marinasThe large number of geographically concentrated individual risks makes pleasure craft business a potential source of major losses in conjunction with such natural hazards as windstorms, tsunamis or floods. This is due to the fact that pleasure craft nor-mally remain within a closely confined radius and are kept most of the time at anchor in their home marina. As a result, the potential accumulation is high, par-ticu larly as the yachts are being increasingly luxuri-ously equipped, driving up the sums insured. The risk of fire is also higher in winter months, as the vessels are often kept tightly packed in large halls during the winter season.

– Higher risks with offshore energyAs the comparatively accessible onshore oil fields are gradually being exhausted, oil companies are making ever greater efforts to tap the deposits under the sea-bed. According to the International Energy Agency (IEA), more than half the new reserves discovered since the turn of the millennium are located in deep water. This has led to a steep rise in insured values and value concentrations per platform, a higher risk of pollution (Deepwater Horizon 2010) and above all higher accumulation risks due to the higher exposure to natural hazards (wind, huge waves, earthquakes and seaquakes). Much the same can be said of off-shore wind farms which are, at present, additionally exposed to a disproportionately high prototype risk.

– Solvency II calls for accumulation control The trends outlined above show how important it is to look beyond the immediate horizons and to establish the level of exposure over all the various fields of busi-ness. Insurers can only take account of worst-case scenarios in their underwriting policy and adequately include accumulation risks in their premium and li -ability calculations if they are aware of the possible accumulation potentials. Solvency II makes accumu-lation control more important than ever, as the new regulations not only demand that risks be made fully transparent, but also require a capital base commen-surate with the risk. If (internal) risk models are used, uncertainties in the exposure figures are penalised actuarially by safety loadings. This inevitably leads to higher prices and a diminishing competitiveness in the market. Furthermore, competition for capital within a company is a disadvantage, as more profit must be earned on the increased risk capital. Non-EU countries, for instance in Asia and South America, are also closely monitoring the introduction of Solvency II and considering whether or not to introduce a similar supervisory system.

Risk management in three stages

For marine insurance, a balanced and sustainable risk management system within the meaning of Solv-ency II should comprise three stages in practice:

1. Micro-assessment of the accumulation riskSince the various subclasses cargo, hull and liability (P&I) normally correlate in the event of a loss, this increases the risk of accumulation for the insurer. Even on the level of individual policies, however, con-siderable exposures can accumulate and exceed the limits in force. Particular attention must be paid to portfolios with a geographical concentration of off-shore energy risks. Each marine class written must therefore be individually assessed with regard to the potential loss accumulation.

2. Macro-assessment of the accumulation riskEven comparatively small marine portfolios should be considered as a whole, for the risks can rapidly accu-mulate with those of other segments, as the above example of port facilities in industrial centres has shown. In an extreme case, losses under marine covers can prove to be the proverbial final straw.

3. Solvency assessment and determination of the need for reinsurancePrimary insurers are responsible for risk-adequate underwriting, maximum risk transparency and for adequately safeguarding their risk capital.

13Munich Re Topics Magazine 1/2013

Marine

Topics: What are your responsibili-ties as deputy harbour master?

Andreas Brummermann: The har-bour master and his crew (port authority) are legally respons ible for ensuring the safety, flow and environ-mental compliance of shipping traffic. As the police authority responsible for shipping, we also exercise certain regulatory powers. The port authority is responsible for port regulations, acts as the licensing body for harbour shipping and as the authority super-vising the harbour pilots.

Natural catastrophes, weather risks and major accidents can cripple trad-ing hubs like sea ports, airports and logistics centres. Tell us about your emergency scenarios and safety pre-cautions.

Hamburg made significant improve-ments following the 1962 floods. A central disaster management service (ZKD) was set up to ensure optimum handling in the event of loss or dam-age. Depending on the magnitude of the loss, the ZKD can be enlarged fol-lowing a major or accumulated loss and centrally manages the individual regional disaster management ser-vices (RKD). The port authority’s naut ical centre acts as the reporting point for the port of Hamburg. Losses of every kind are reported there and evaluated before appropriate action is taken. Within disaster manage-ment, we distinguish between defen-sive disaster management (acci-dents, damage, etc.) and preventive disaster management (storm surge).

How do you manage to ensure a smooth flow of traffic for freighters and container vessels of all sizes?

Traffic within the port of Hamburg is managed through the port authority’s nautical centre. This is the focal point for all operations needed to ensure the smooth and safe flow of shipping traffic. The nautical centre works closely with the national estuary centres, the port and river pilots on the river Elbe, the tugs, line handlers, quay operators and shipbrokers. We are particularly concerned with ensuring that every ocean-going ves-sel is given a safe berth here and that the large tide-bound vessels enter and leave the port within the time-frame available to them.

How do you deal with hazardous goods?

Hazardous goods are to be found on virtually every container ship and are loaded in accordance with stowage requirements. Even before a vessel arrives in Hamburg, the harbour police receive a detailed list of all hazardous goods on board. Liquid bulk goods, such as petrol and oils with a low flash point, must be trans-shipped in tanker terminals, where special safety regulations apply.

Which technical aids do you have?

Our most important technical aid is the network of shipping data on the river Elbe. All the estuary centres associated with the river Elbe are interconnected in this system and every inward or outward movement of a ship between the German Bight and its berth in Hamburg is regis-tered there. Inside the harbour, 13 radar stations provide a clear view of each harbour basin. Each vessel can be contacted by VHF radio on spe-cially allotted channels. In foggy con-ditions, harbour pilots provide separ-ate fog advice via allocated radar channels. The telephone system also has a priority function to ensure it is constantly available without disrup-tion.

Are there any times, places or types of vessel that pose a particular danger?

All vessels are treated in accordance with their hazard potential. In the case of tankers, a “ban” can be issued if necessary in poor visibility. General rules of conduct must be observed by all vessels in fog. Above all, tide-bound vessels must enter and leave the port within certain time-frames, otherwise they could end up with too little water under their keel. As far as places are concerned, special priority rules must be observed in the port of Hamburg in order to prevent poten-tially dangerous situations arising.

andreas Brummermann is deputy harbour master at the port of Hamburg. around 10,500 ocean-going vessels from every corner of the globe docked here in 2012 alone. Topics spoke to andreas Brummermann about his work and the risk potentials involved at the port of Hamburg.

Gateway to the world

14 Munich Re Topics Magazine 1/2013

Marine

Made-to-measure reinsurance solutions can help to assure solvency if the calculated capital requirement following a catastrophe exceeds the insurer’s finan-cial capacity.

In future, under Solvency II, the following once-in-200-years loss scenarios – with further subdivision into geographical zones for natural catastrophes – must be taken into account in the standard formula as possible accumulations for marine business:

− Tanker collisions − Loss of an offshore platform or offshore complex

In addition to the purely quantitative assessments required, it must also be demonstrated that all com-pany risks and particularly all major-loss potentials have been correctly estimated and duly included in the strategic business and risk management. This also imposes higher demands on the quality of data, adequate process management and the wording of the underwriting and reinsurance policy. Wide-rang-ing documentation duties are to ensure that supervi-sory authorities can follow the logic of insurers’ appraisals. If the authorities conclude that the quanti-tative calculations do not adequately reflect the risk or that the data material does not meet with the quali-tative requirements, surcharges may be imposed on the required risk capital.

New risk models under development

In short, Solvency II requires a distinctly heightened awareness among primary insurers if they are to underwrite marine risks on a profitable basis in the long term. This requires precise knowledge of all the risks written (underwriting limits, scope of cover, exposure, geographical location, vulnerability to loss), maximum transparency of the portfolio and compli-ance with certain data standards (geographical data, liability data, policy data). However, it also includes collecting risk data as the non-leading primary insurer, for example in relation to warehouses separ-ate in terms of fire risk, or in order to determine the development of container stock (empty/loaded/aver-age values) in a given harbour. Information on how to prepare a suitable risk data model (KISS) can be obtained from the German Insurance Association (GDV). One positive side effect of this heightened risk awareness is that it can create an incentive to develop new risk models or adapt established risk models from property insurance to meet the needs of marine insurance.

OUr eXPerTS

Christian Forwick is a marine underwriter at Munich Re responsible for MGA and French [email protected]

Gerhard Vogl is a marine under-writer at Munich Re responsible for various markets in central and eastern Europe. [email protected]

Solvency II requires a distinctly heightened awareness among primary insurers if they are to underwrite marine risks on a profitable basis in the long term.

15Munich Re Topics Magazine 1/2013

What is it that makes reinsurance so exciting?

You can find out the answers to this question in TOPICS ONLINE. Our magazine for insurers takes you behind the scenes at Munich Re and shows what drives us. We will introduce you to interesting people, address current topics in the worlds of insurance and finance, and present the latest trends, solutions and services.

Have your say: use the comment function to start interesting discus-sions with us. Your opinions are reflected in interactive surveys.

www.munichre.com/en/topicsonline

not if, but how

17Munich Re Topics Magazine 1/2013

Jürgen Brucker and Joachim Mathe

Turkey is a rising star among the emerging markets, its dynamic rate of development earning it the nick-name “Anatolian tiger”. This rapid expansion is driven by the private sector, most notably by industry. The country has extensive integration with the European Union through a customs union. As a result, the EU is not only by far the most important trading partner, but also supplies most of the foreign capital that is directly invested in Turkey. Its geographic location at the point where east meets west is another advan-tage. For many companies, this not only makes it an excellent production location, but also an ideal base from which to do business in Asia, the Middle East and North Africa.

Growth fuelled by direct foreign investment

Turkey’s economic miracle dates back to a home-grown economic crisis that shook the country’s bank-ing system in 2001. At the time, ballooning sovereign debt and runaway inflation forced the government to radically alter its approach. And with great success:

Boomtown: Istanbul’s population is expected to grow by a further five million in the next ten years.

Anatolian tiger poised to pounceTurkey has seen an impressive upswing in recent years, thanks to a competitive economy and successful consolidation of the national budget. With an eye to its centenary celebra-tions in 2023, the country has set itself some ambitious goals: it plans to become a top-ten economy.

in the years that followed, the transformation of the country’s financial system, a flexible exchange rate and economic reforms increasingly attracted foreign capital and stimulated growth. From 2002 to 2011, the nominal gross domestic product (GDP) grew more than three-fold to US$ 773bn, with the result that the country now ranks sixth among the economies of Europe and 16th in the world. Its national budget was also successfully restructured: according to forecasts, the 2012 deficit should be no more than 1.5% and total debt around 37% of GDP.

The upswing went hand-in-hand with major struc-tural changes in the economy. The agricultural sector still makes the greatest contribution to the economy, not only representing over 10% of GDP, but also pro-viding jobs for more than one-third of the country’s working population, with roughly half the country’s land being used for farming. In recent years, however, industry has been gaining. Together with the mega-city Istanbul and the capital Ankara, Izmir and such provincial towns as Kayseri, Konya and Adana have

Turkey

Turkey

18 Munich Re Topics Magazine 1/2013

20,000

15,000

10,000

5,000

0

2006 2007 2008 2009 2010 2011

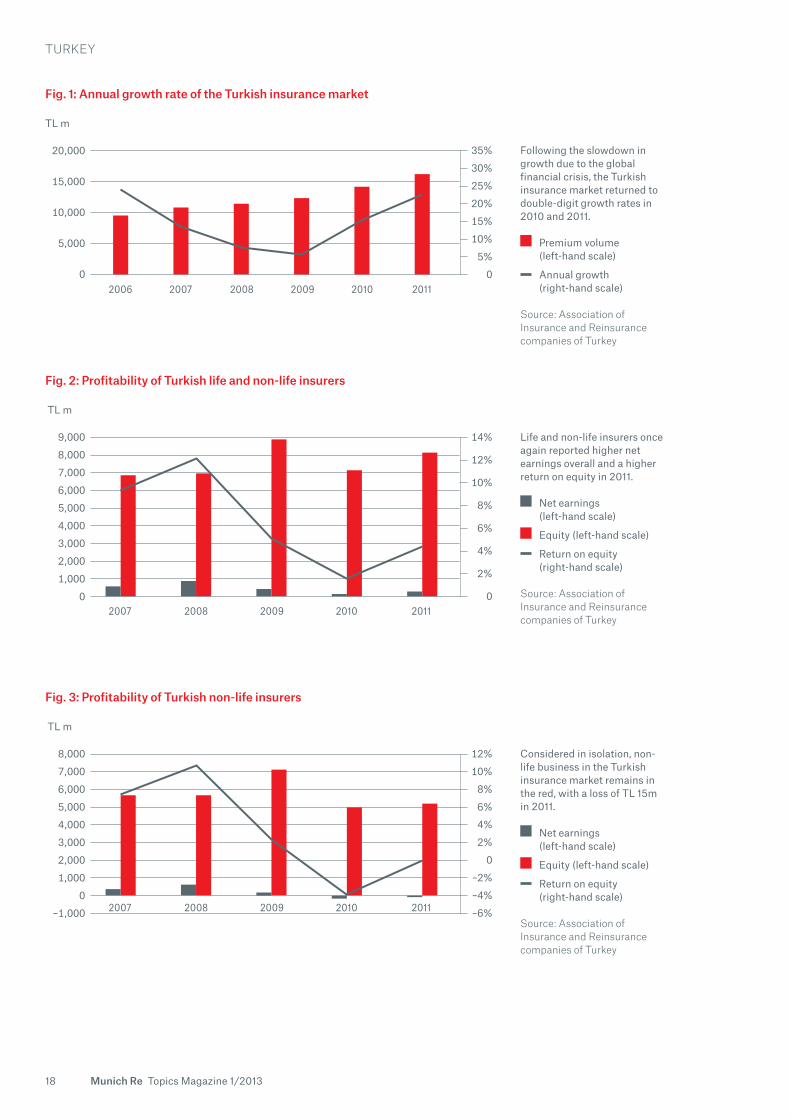

Fig. 1: Annual growth rate of the Turkish insurance market

TL m

35%

30%

25%

20%

15%

10%

5%

0

9,000

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

02007 2008 2009 2010 2011

Fig. 2: Profitability of Turkish life and non-life insurers

TL m

14%

12%

10%

8%

6%

4%

2%

0

Life and non-life insurers once again reported higher net earnings overall and a higher return on equity in 2011.

Net earnings (left-hand scale)

Equity (left-hand scale)

Return on equity (right-hand scale)

Source: Association of Insurance and reinsurance companies of Turkey

Following the slowdown in growth due to the global financial crisis, the Turkish insurance market returned to double-digit growth rates in 2010 and 2011.

Premium volume (left-hand scale)

Annual growth (right-hand scale)

Source: Association of Insurance and reinsurance companies of Turkey

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

–1,000 2007 2008 2009 2010 2011

Fig. 3: Profitability of Turkish non-life insurers

TL m

12%

10%

8%

6%

4%

2%

0

–2%

–4%

–6%

Considered in isolation, non-life business in the Turkish insurance market remains in the red, with a loss of TL 15m in 2011.

Net earnings (left-hand scale)

Equity (left-hand scale)

Return on equity (right-hand scale)

Source: Association of Insurance and reinsurance companies of Turkey

Turkey

19Munich Re Topics Magazine 1/2013

now become industrial centres. In addition to textiles, the country’s main products include motor cars and commercial vehicles as well as consumer goods, such as electrical and household appliances. The services sector including tourism, traffic and transport has also developed rapidly, and the energy market has acquired a new significance as the nation’s economy has grown.

As the economy booms, Turkish consumers are also becoming a more attractive prospect. The Turkish population is one of the youngest in Europe, with 58% of the country’s 74 million people aged under 30. The economy’s positive development is also reflected in rising incomes and growing purchasing power.

Ambitious goals for Turkey’s centenary

The goals pursued by Prime Minister Recep Tayyip Erdoğan are ambitious: by the time the Republic of Turkey celebrates the 100th anniversary of its founda-tion (29 October 1923), it aims to have become one of the world’s ten leading economies and Istanbul is to be home to five million more than its currently esti-mated population of 15 to 17 million. To create living space for this new population, two new urban centres are to be built on the fringes of this densely built-up metropolis, one on the European side and one on the Asian side. Development of the infrastructure is also being stepped up by the government. New ports, a third international airport, a third bridge across and two tunnels under the Bosporus, as well as a high-speed train to Ankara are planned to handle the expected volume of traffic.

However, it is doubtful whether all these projects can be realised within the planned time-frame, for the country still faces several other challenges. After the current account deficit reached the record level of roughly 10% of GDP in 2011, the economy now faces more and more imbalances in foreign trade. The Cen-tral Bank is pursuing a weak-currency policy in an attempt to curb its deficit, making imports more

expensive and fuelling inflation. In addition, the finan-cial sector has become increasingly dependent on short-term foreign funds, making the country suscep-tible to external shocks. But even if Turkey is spared such shocks, GDP is only expected to grow at more moderate rates of between 4% and 5% until 2014.

Rapidly growing insurance market

Despite these uncertainties and the existing struc-tural weaknesses, Turkey’s economic importance is set to increase, as is that of its insurance sector. This sector has already grown rapidly in recent years, from a premium volume of barely 10 billion Turkish lira (TL) in 2006 to TL 17.1bn in 2011 (see Fig. 1). This rise was not solely attributable to economic growth, but also to the market’s generally low insurance penetration. In the past year alone, the market expanded by 21.5%, leaving a phenomenal real growth rate of 8.5% after adjustment for inflation.

Personal accident, life, motor third-party liability (MTPL), fire and health are the biggest segments. Profitability, on the other hand, is unsatisfactory in most lines of business. Although the underwriting result improved slightly in 2011, the market climate in property and casualty insurance remained troubled, with numerous insurers reporting a loss. The difficult market situation is also reflected in the return on equity, which has largely declined since 2008. Non-life companies even reported a negative ratio in 2011 (see Fig. 3).

As the economy booms, Turkish consumers are also becoming a more attractive prospect. The Turkish population is one of the youngest in Europe, with 58% of people aged under 30.

20 Munich Re Topics Magazine 1/2013

Turkey

Topics: What are the driving forces behind Turkey’s economic growth?

Muzaffer Aktaş: Turkey owes its dynamic growth, in part, to increas-ing industrialisation and the rapid development of tourism over the past 25 years. At the same time, visionary economic pol icies and the tough new banking regulations introduced between 2000 and 2002 have also contributed to its growth.

How would you describe the current situation on the Turkish insurance market?

Despite sizeable growth in the last ten years, the market remains rela-tively small. Notwithstanding the current ruinous price war, it offers enormous potential. Large, cap ital-rich international insurance com-panies fighting for market shares are one reason for the fierce struggle over prices. As a result, many of the rates quoted are no longer technic-ally justifiable, but this downward trend cannot continue indefinitely. Ultim ately, even the big players will feel the pinch and be compelled to change tack.

Insurance companies backed by for-eign capital have controlled around 60% of the Turkish market for the last four years. Has this brought any improvements?

International insurers are extremely welcome. They are all leading com-panies with a wealth of experience. I am therefore optimistic that, with their aid, we will be able to make the general public more aware of the benefits of insurance. This will be of enormous benefit to us all.

Muzaffer Aktaş, Managing Director of reinsurance brokers Willis re in Turkey and responsible for the Middle east and Africa, explains the Turkish insurance market’s present situation and outlines its future prospects.

Price competition affects all players

Istanbul threatened by earthquake risks

The pools Tarsim (for agricultural covers, see page 27) and TCIP (for earthquakes) are two special features specific to the Turkish market. While Tarsim was established to reflect Turkey’s significance as an agri-cultural producer, the earthquake pool TCIP was set up following the Izmit quake in 1999 with support from the World Bank, among others. The degree of seismic activity indicates just how important the pool is: more than 1,000 quakes with a magnitude of 5 or higher were registered in Turkey in the period from 1900 to 2011, including ten in the Istanbul region alone (see map of natural hazards on page 25).

The city straddling the Bosporus is particularly at risk, as it is located north of the North Anatolian Fault, partly on the Anatolian Plate and partly on the Eur-asian Plate. Due to the chronological east-west sequence of quakes in northern Turkey to date, it is only a question of time before an earthquake strikes this city and the millions of people living there. Opin-ions diverge as to its magnitude. Some experts con-sider the probability of a violent quake within the next 30 years to be in excess of 60% – with potentially devastating consequences for this densely populated and highly industrialised region. Others expect the tectonic stresses to be reduced in a series of minor earthquakes.

21Munich Re Topics Magazine 1/2013

Turkey

Earthquakes are by far the most important catastrophe risk in Turkey. To what extent is the public aware of the need for suitable covers?

Earthquakes are a terrifying natural hazard. Every major event is vividly remembered for a long time, which makes it easier to sell corresponding products. Market penetration will therefore increase. As people become more aware of the risks, they will also be more willing to pay higher insurance premiums. Mean-while, insurers will spend more on reinsurance cover and reinsurers will increasingly benefit from this devel-opment.

How do you expect the Turkish insurance market to change in the next few years?

On the one hand, I expect further consolidation in the near future, albeit on a smaller scale than at pre-sent. However, I also hope that the international companies operating in Turkey will try to explore the untapped personal lines and intro-duce niche business. If the Turkish economy continues to grow at its present rate, people will soon be able to feel that wealth in their own pock-ets. They will become more aware of the need for insurance cover and be prepared to spend more money on it. That will contribute decisively to the further growth of insurance in Turkey.

Which are the main areas or lines of growth in your opinion?

Growth will be found primarily in construction, small industries and tourism.

What do you think of the efforts to introduce a regime similar to Solv ency II in Turkey?

The Turkish Treasury regards Solv -ency II as an essential tool for achiev-ing financial strength and protecting both insureds and insurance com-panies. Turkey is way ahead of many other non-EU countries in this respect.

The crisis in the eurozone, volatile capital markets and persistently low interest rates are also having an impact on the insurance industry. What challenges do you foresee for the industry in the near future?

Insurance business is based on two pillars – technical income and invest-ment income. Both must be equally strong and generate sufficient profits. The advantage of this two-pillar principle is that difficulties in one area can be mitigated by efforts in the other to reduce financial fluctuations. Since investment income is very low in the present economic situ ation, higher priority must be given to the technical side.

As the latest quakes in Christchurch, New Zealand, have shown, however, even smaller earthquakes can cause considerable damage and losses. Statistically speaking, the next major event is already long overdue: in the last 1,500 years, Istanbul suffered a major earthquake every 100 years on average, the last in 1894.

Obligatory earthquake insurance TCIP

Since it was set up, TCIP has covered losses totalling more than TL 145m. Premium income between 2000 and 2011 totalled around TL 2,290m, and TL 400m in 2012 (as at November 2012). Cover is provided on a first-loss basis with a maximum exposure of around TL 150,000 and a deductible equal to 2% of the sum

insured. The average sum insured is TL 67,000, the average premium TL 100 per year. It is calculated on the basis of five different rating zones and three different construction classes. For houses and apart-ments worth more than TL 150,000, add itional pro-tection can be purchased from the insurers operating in the market. In June 2012, the total sum insured by the TCIP equalled TL 261bn; buildings in Istanbul accounted for 28% of this total, and buildings erected after the 1999 quake made up 60% of the total.

22 Munich Re Topics Magazin 1/2013

Solvency II will ensure that the same solvency standards apply in all EU countries in future. Yet the regula-tions governing the capital base and risk management are also attracting widespread interest outside the EU, too. In Turkey, insurance companies and regulatory authorities are not only keeping a close eye on develop-ments, but even introduced the first changes in 2008. Probably from 2016 on, the supervisory authority will extensively include risks and the necessary capital base in its solvency assessment – and that will have a lasting impact on Turkish insurers’ strategy, organisation and culture, as well as on their business models. The Turkish regulations are not expected to diverge significantly from the European model, although excep-tions are likely in certain areas.

In order to find out just how ready the Turkish insurers are to meet these future requirements, the country took part in the European Union’s fifth Quantitative Impact Study (QIS5) in 2010. Altogether 46 insurers and one reinsurer participated. It was found that the target value for the Solvency Capital Requirement (SCR) was TL 1.2bn higher than the solvency cap ital required under the previous standards, and that this latter was, in turn, equal to 2.4 times the Minimum Capital Requirement (MCR).

To ease the process of adjusting to the SCR, Munich Re has identified ten levers to relieve the solvency capital and strengthen risk-adjusted earnings power.

1) Focus on non-life underwriting

Since non-life underwriting presum-ably ties up the most risk capital – both gross and net – before diversifi-cation, adjustments are likely to bring considerable relief here. Market and insolvency risks follow a long way behind. Where the latter are concerned, important factors include the agents’ traditionally strong pos-ition in Turkey, the fact that premium payments are retained for longer than the European average, and the reinsurers’ rating.

2) Differentiated earthquake tariff

In the long term, the earthquake tariff will make way for insurers’ own models or those of professional mod-ellers. Until then, more differentiation must be achieved in the earthquake tariff as regards zoning, construction standards, etc. in order to achieve a profitable premium level. The Own

Risk and Solvency Assessment (ORSA) forming part of the 2nd pillar of Solvency II must be fully imple-mented and smaller insurers must (also) have both the procedures and data needed to develop their own tariffs.

3) Nat cat offers little potential for optimisation

In the nat cat segment, Turkish insurers traditionally purchase rein-surance covers with a return period of more than 200 years (99.5% VaR). Although, due to earthquakes, the gross exposure to natural perils is by far the largest risk factor, the net risk capital required is significantly lower. The only remaining (very small) potential for optimisation lies in the amount retained.

Looking to Europe

The aim of Solvency II is to ensure a risk-adequate cap-ital base for the insurance sector in the European Union. Although Turkey is not a member of the EU, the new solvency rules will fundamentally change the insurance industry there, too.

Solvency II

Istanbul’s most famous skyscrapers are in the Levent financial district.

23Munich Re Topics Magazin 1/2013

Solvency II

4) Motor business under scrutiny

On a net basis, motor third-party li ability (MTPL) and motor own dam-age (MOD) will probably prove to be the biggest drivers of risk capital in most cases. This is hardly surprising considering that the primary insur-ers’ share of almost 50% for motor insurances is considerably larger in Turkey than in other European mar-kets. At the same time, the market-wide combined ratio is an average 105% (MOD) and 125% (MTPL). For many years, Turkish insurers were able to compensate this weakness with high investment income, but this is no longer possible as it has declined considerably.

5) Growing importance of reinsur-ance

The advantages of reinsurance (relief for the capital structure, more robust profitability) are of even greater con-sequence under Solvency II. The insurance companies were therefore called on to identify reinsurance pro-grammes in 2013 and 2014 that bring an optimisation of capital. Con-sidering the dominant position of MTPL and MOD in the premium and reserve risk, reinsurance is an effect-ive means of relieving risk capital.

6) Reserve quality is key

Retrospective reinsurance solutions (especially loss portfolio transfer) impact the reserve risk and act as a direct relief on capital. However, the quality of the reserve is decisive. In the past three years, the gradual introduction of a modified IBNR cal-culation (incurred but not reported) has had a positive effect here.

7) Relief through proportional rein-surance

Proportional reinsurance solutions will become more important, particu-larly for MTPL and MOD, as the com-bined ratio is driven skywards by high frequency and not by major losses. Quota share solutions are no more tightly structured than trad-itional covers and therefore allow full transfer of the risk. It is advisable to change over to proportional covers at an early stage, as the full effect is only felt after two or three years, due to the subsequent impact on reserves. The reinsurers’ rating, above all, has a decisive effect on capital relief.

8) Focus on profitability

A minimum of technical profitability is needed in order to implement pro-portional reinsurance solutions. Risk-adequate prices must be calculated and enforced; external factors, such as the development of interest rates and catastrophe losses, must not jeopardise the business model. All insurers must therefore scrutinise their complete range of products and services closely.

9) Opportunity costs decide the price

In the fiercely competitive Turkish market, price and reinsurance com-missions are the most important negotiating components, along with the service. However, such factors as the rating or effective capital relief will increasingly determine the (added) value of reinsurance solu-tions. The price of these solutions will also be determined by alternative financing models with equity or debt, as well as the associated opportunity costs.

10) Optimise loss and administra-tion expenses at an early stage

Measures to cut costs should be taken even before Solvency II. Among other things, these could include the introduction of repair networks for cost-efficient claims settlement in motor business or the systematic use of IT to improve the management of fraud cases.

Conclusion

Turkish insurance companies should not wait until a new Solvency regime is adopted, but should instead take strategic steps as soon as possible to optimise their capital structure and possibly realign their business model.

The implementation of Solvency II involves considerable effort on the part of the insurers. Munich Re offers specific and efficient assistance in all areas (non-life, life, health) when pre-paring for the new regime. In collab-oration with the various Business Units, our Solvency Consulting team uses practical examples to ensure transparency and pass on the know-how needed to find a systematic strategy and plan suitable measures. In this context, Munich Re can draw on extensive experience in the devel-opment and use of internal stochas-tic risk models and link them with value-based portfolio management. In addition, we are actively involved in key national, European and inter-national supervisory and technical boards, and ensure both the transfer of knowledge and the development of recommendations for action in operative business.

23Munich Re Topics Magazine 1/2013

24 Munich Re Topics Magazine 1/2013

Turkey

The pool’s obligatory nature results from the fact that TCIP cover must be proved whenever ownership is transferred. The same also applies when concluding a contract with a utility company (gas, water, electri city). However, anyone lacking such cover is unlikely to face sanctions in practice. This may well be due to the fact that the TCIP law was only formally ratified in May 2012, although it was passed in September 2000 with the pool starting its operations immediately. Now that it has been ratified, it is hoped that the num-ber of insureds will rise appreciably in the near future, from approx. 4.2 million today (including 1.2 million in Istanbul) to 6 million in 2014, particularly since insurance penetration can be improved significantly from its present level of 30%.

The TCIP’s governing board of seven members is made up of representatives from various ministries, Istanbul University and the private sector. Operative business and claims settlement were assigned to the insurance company Eureko. Sales are handled by 28 authorised insurers and their agents in return for a commission. Munich Re has been a reliable partner for the TCIP and the pool’s leading reinsurer for several years. When Turkish earthquake risks were placed on the capital market for the first time in 2009, Munich Re assisted the TCIP, collaborating closely

with the teams for traditional reinsurance and for capital market solutions. Munich Re’s European wind-storm risks and the TCIP’s earthquake risks were combined in a joint cat bond issued by Ianus Capital Ltd. The issuance of a further cat bond exclusively for the TCIP’s earthquake risks is currently in the planning phase.

No more than a few seconds’ advance warning

Since experts can do no more than provide estimates of the possible time and magnitude of the next earth-quake, measures to limit the damage and minimise losses are of paramount importance. And Turkey is a very advanced country in this respect. Earthquake research and contingency planning are given high pri-ority, aided, above all, by Istanbul University’s Kandilli Observatory and Ankara Technical University.

Despite all these efforts, however, an early-warning system for Istanbul is still only just being set up. The main problem lies in the short time of just a few seconds’ advance warning. For this reason, loss-mini-misation efforts are focusing on automatic systems.

Morning rush hour at Eminönü Square: This part of Istanbul is on the European side.

Turkey

Iran

Russia

Libya

In the grip of nature’s power

Natural catastrophesEarthquakeWinter stormFlood/Flash flood

The map shows locations where earth-quakes (orange), floods (green) and winter storms (blue) have occurred. Turkey has frequently been hit by devastating natural catastrophes, partly because the whole country is exposed to earthquakes (Zone 0 rather strong to Zone 4 destructive, or even worse). Earthquakes have claimed count-less victims. For example, on 17 August 1999 in Izmit when an earthquake with a magnitude of 7.6 resulted in 18,000 deaths. Or on 26 December 1939 when an earth-quake of 7.8 magnitude in Erzincan killed 30,000 people.

Source: Munich re

Earthquake zones (Mercalli scale)MM V (rather strong)MM VI (strong)MM VII (very strong)MM VIII (destructive)MM IX (violent)

Istanbul

Bursa

Izmir

Antalya

Konya

Ankara

Kayseri

Adana Gaziantep

Diyarbakir

Turkey

25Munich Re Topics Magazine 1/2013

Erzincan

Izmit

Turkey

26 Munich Re Topics Magazine 1/2013

our exPerTS

Jürgen Brucker is a Client Manager in the Southern Europe department responsible for the markets Turkey and Turkic States. [email protected]

Joachim Mathe is Executive Client Manager responsible for Southern [email protected]

As soon as sensors register strong tremors, safety measures are automatically initiated by a communi-cations network which is separate from the mobile telephone network. Lifts are stopped at the next floor, power lines de-energised, gas mains shut off and traffic signals show a red light. Nevertheless, experts believe that Istanbul is still not adequately prepared for a major catastrophe.

The Turkish government has recently launched a pro-gramme to make six million buildings – i.e. one-third of the existing buildings – more earthquake-proof or to replace them completely. The programme spans a period of 20 years. Construction costs for Istanbul alone are estimated at around US$ 100bn.

Contingency plan for insurers

Special construction codes have been in force since 1940 and have been revised nine times, usually fol-lowing an earthquake. However, the regulations were not always complied with. As a result, it is not uncom-mon to find buildings on sandy ground, and the typ-ical multi-storey apartment blocks are widespread, despite their proven instability. According to a study by the World Bank, the codes have been strictly applied since 1999.

A major earthquake in Istanbul would sorely test every insurer’s claims management. Not only would tens or even hundreds of thousands of claims have to be settled quickly and efficiently – a daunting task even in normal conditions – but the insurers them-selves would also have to cope with the consequences of the catastrophe: damaged infrastructure, disrupted communications systems, personnel shortages.

Proactive contingency planning can help to avoid inconsistencies in settlement, as well as delays and inappropriate claims payments. Provided that it has been structured correctly, it can play an important part in preventing a possible loss of confidence and a nega tive impact on the development of business.

Munich Re has prepared a contingency planning guide to assist its clients. Our experience in trad itional claims management combined with findings from past disasters provides an ideal basis for drawing up individual plans in line with regional specifics and the local infrastructure. The guide was presented at the 4th International Istanbul Insurance Conference in October 2012.

Turkey

27Munich Re Topics Magazine 1/2013

Effective support for Turkish farmers

Brigitte Engelhard

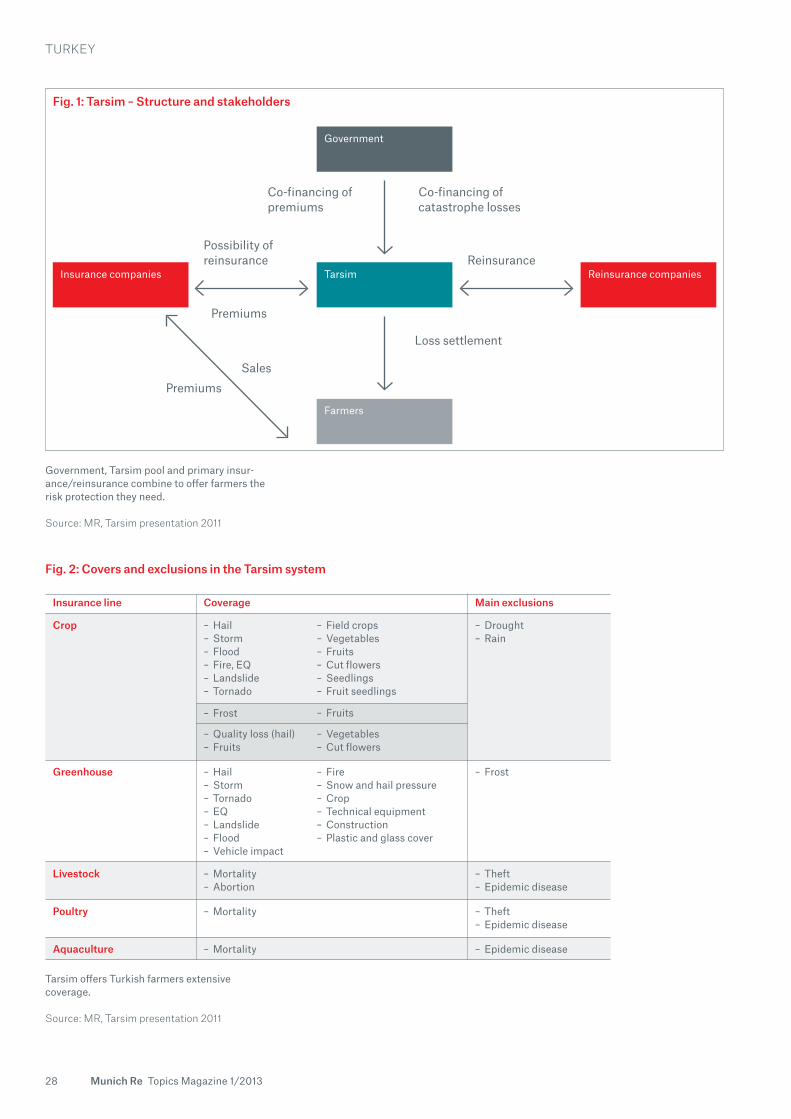

The Turkish Agricultural Insurance Act passed in 2005 laid the foundations for the establishment of a government-supported insurance pool for farmers. The aim of this public-private partnership is to help farmers manage the risks they face. The creation of a central unit – the Tarsim agricultural insurance pool – has resulted in a transparent structure which operates efficiently and effectively, promoting the interests of all concerned.

Founded by Turkish insurance companies, the pool is run by a board of management whose members include the main stakeholders, such as the Ministry of Food, Agriculture and Livestock, Undersecretary of the Treasury, the Union of the Agricultural Chambers and the Insurance Association of Turkey. This board of management determines the system’s strategic orientation and basic principles of operation. The essential pillars and achievements of this public- private partnership (PPP) include:

− Public co-financing of premiums − Public co-financing of catastrophe losses − Cooperation between companies and the establish-ment of uniform terms and conditions − Uniform settlement of claims

The management company of the pool implements the pool’s strategy, carrying out all insurance oper-ations. Sales, on the other hand, are handled by the Turkish insurers’ agents in return for a commission (see Fig. 1).

Tarsim provides coverage for arable crops, fruit and vegetables, livestock (cattle, sheep, goats, poultry), greenhouses and aquaculture. The insured perils and exclusions are shown in Fig. 2.

Modern technology is used in day-to-day operations, for instance to transmit data from agents or loss adjusters to the central office in Istanbul or to simplify the verification of losses. Tarsim is linked to the Min-istry’s registration system from which it can retrieve important data needed for writing policies. A pilot project using geo-information systems (GIS) has also been operating for several years.

Since Tarsim was set up, the level of insurance take-up has risen from less than 1% to 8% today, with a corresponding rise in premium volumes (see Fig. 3). A premium volume of TL 500m (around €215m) is expected for 2012. The loss ratio of the original

Turkish farmers are well-protected by the gov-ernment-supported agricultural insurance pool. Tarsim provides coverage for arable crops, fruit, vegetables and many other agricultural products.

Turkey

28 Munich Re Topics Magazine 1/2013

Reinsurance companiesReinsurance

Government

Insurance companies

Farmers

Tarsim

Co-financing of premiums

Co-financing of catastrophe losses

Loss settlement

Possibility of reinsurance

Premiums

SalesPremiums

Insurance line Coverage Main exclusions

Crop – Hail– Storm– Flood– Fire, EQ– Landslide– Tornado

– Field crops– Vegetables– Fruits– Cut flowers– Seedlings– Fruit seedlings

– Drought– Rain

Greenhouse – Hail– Storm– Tornado– EQ– Landslide– Flood– Vehicle impact

– Fire– Snow and hail pressure– Crop– Technical equipment– Construction– Plastic and glass cover

– Frost

Livestock

Poultry

Aquaculture

– Mortality– Abortion

– Mortality

– Mortality

– Theft– Epidemic disease

– Theft– Epidemic disease

– Epidemic disease

– Frost

– Quality loss (hail)– Fruits

– Fruits

– Vegetables– Cut flowers

Fig. 2: Covers and exclusions in the Tarsim system

Tarsim offers Turkish farmers extensive coverage.

Source: Mr, Tarsim presentation 2011

Government, Tarsim pool and primary insur-ance/reinsurance combine to offer farmers the risk protection they need.

Source: Mr, Tarsim presentation 2011

Fig. 1: Tarsim – Structure and stakeholders

Turkey

29Munich Re Topics Magazine 1/2013

Financial Year

business (excluding costs for loss adjusters) fluctu-ated between 44% and 85% between 2007 and 2011. The average loss ratio over this period was 69%.

Tarsim’s reinsurance is based on a proportional treaty covering all segments. Munich Re has been actively supporting the Turkish agricultural insurance market since the 1960s and strategically promoted its devel-opment right through to the establishment of a PPP solution. From the outset, Munich Re acted as the leading reinsurer and main risk carrier for Tarsim. In this way, Munich Re not only contributed decisively to the pool’s development and growth, but also helped to shape its underwriting structures. Local companies can participate in the proportional reinsurance and acquire shares.

In addition to the quota share reinsurance, the risk retained by Tarsim is protected by the government. The local companies’ shares are likewise protected, albeit with a higher attachment point. The profes-sional reinsurers’ liability for frost and flood losses is limited. In this way, the government relieves private insurers and reinsurers in years in which natural catastrophes have struck. This, in turn, helps to main-tain low premium rates for the farmers.

In terms of its basic conditions (statutory basis, cen-tralised structure, subsidised premiums and public participation in catastrophe losses), the Turkish PPP extensively drew on the international experience in this field – experience which can be found in Munich Re’s “SystemAgro” (www.munichre.com/systemagro). This stands for a system of sustainable multi-peril crop insurance that has been in operation for more than 200 million hectares of land throughout the world for over 35 years. It is primarily designed to assist farmers. Before Tarsim was founded, for ex -ample, Turkish farmers were only able to buy straight hail insurance and a traditional livestock insurance, but now they can purchase more comprehensive cover which also remains affordable due to the sub-sidised premiums. Public participation in the catas-trophe losses additionally makes it pos sible for the insurance and reinsurance industry to provide risk capital on a long-term basis.

The drought which hit the USA in 2012 is a prime example of how public participation in catastrophe losses works. Although 75% of the maize and soybean fields were severely damaged, the PPP was able to survive by sharing the risk, thus maintaining the farmers’ “safety net”. Such catastrophe scenarios must also be expected in Turkey, particularly as climate change progresses. Certain challenges still have to be mastered by the relatively young Tarsim system in order to be prepared for the future. Among other things, its products must be continuously adapted, insurance penetration – a sign of its acceptance by and support among farmers – increased, cost-effi-ciency optimised and risk sharing harmonised among the stakeholders. These changes will allow Tarsim to develop in a sustainable manner and give Turkish farmers the risk protection they need.

our exPerT

Brigitte Engelhard is an underwriter at Munich Re responsible for agri cultural business in [email protected]

500,000

450,000

400,000

350,000

300,000

250,000

200,000

150,000

100,000

50,000

02007 2008 2009 2010 2011

Premium in TL

Aquaculture Poultry Livestock Greenhouse Crop (other perils) Crop (frost)

Fig. 3: Tarsim – Development of premiums and composition of the portfolio

Insurance penetration and conse-quently premium volume have increased substantially since the Tarsim pool was set up.

Source: Mr

Risk ManageMent solutions

30 Munich Re Topics Magazine 1/2013

life insurers have been badly hit by the financial and debt crisis. this is due primarily to capital market risks actually materialising to a significant level, so that the values of the assets and liabilities of many market players have drifted apart. Munich Re has created its Financial solutions unit to develop solutions tailored to the needs of the sector and advise life insurers on corporate finance issues.

New ways to manage undiversifiable risks

Risk managers constantly monitor movements in share prices and interest rates.

Risk ManageMent solutions

31Munich Re Topics Magazine 1/2013

Increasing expectations of asset-liability management

One of the fundamental problems in achieving a balance between assets and liabilities is the duration mismatch, which results from the differing maturities of life insurance policies and the investments cover-ing them on the assets side. The effect of movements in interest rates on assets and liabilities (“interest-rate sensitivity”) has developed to companies’ disadvan-tage since the beginning of the financial and debt crisis and a gap has emerged between the two sides of the balance sheet.

Services and reinsurance solutions devised by our Financial Solutions Team are typically aimed at reducing the negative effects of past and future inter-est-rate movements and, if possible, even eliminating them. A reinsurance contract offers considerable advantages over hedging transactions such as the purchase of interest-rate derivatives, for example the fact that the valuation of insurance and reinsurance contracts for balance-sheet purposes is based on the same principles. Moreover, supervisory requirements – such as reserve increases due to interest-rate move-ments – can be transferred to the reinsurer via the reinsurance treaty. The reinsurer provides the required technology and assumes the administrative work and the operational risk arising out of the use of

Stefan Jaschke and Gunther Kraut

How can companies cope with the new requirements in risk management and corporate finance? As in the past, insurers are working with their reinsurers to find appropriate answers and solutions – especially in the area of underwriting risks – but that is not the case for the capital market and financial risks that are of paramount importance for life insurers in particular. Financial market risks cannot be diversified like underwriting risks, which vary greatly in type and geographical impact. Products and determining fac-tors are the same throughout the world; economies and trading centres are so interwoven that the risks are increasingly cor related globally when crises unfold. Insurers are looking to reinsurers to offer new answers and solutions – particularly in view of the enormous risks accumulating in life insurers’ balance sheets worldwide.

Munich Re has set up a Financial Solutions Team in its global life reinsurance to devise worldwide solu-tions for risks that are difficult to diversify and to advise life insurers on corporate finance issues – the latter with a particular focus on profitability and solv-ency requirements. This puts Munich Re in a position to support its clients as a partner in dealing with all of the risks on their balance sheet.

Transfer Diversification Limitation

Transferable risks Measurable and diversifiable risks

Other risks

Market-consistent valuation

Capital costs Limits and reimbursement

Hedgeable

Insurable

UninsurablePolicyholders

Insurer

Banks/Investors

Pricing and structuring for three risk categories

Clear communication of which risks are to be transferred to whom is vital for product design, ALM and structuring.

Risk ManageMent solutions

32 Munich Re Topics Magazine 1/2013

derivatives, which facilitates acceptance by auditors and supervisory author ities of this form of risk cover.

Comparably effective ALM solutions to these and other risks realised by companies themselves will always be extremely laborious. The stricter require-ments for quantifying liabilities following the intro-duction of MCEV (market-consistent embedded value) and Solvency II alone will involve a great deal of work. To meet these requirements, a high degree of actuarial expertise and knowledge of the financial markets is needed as well as the appropriate technol-ogy – all the more so since the higher level of market consistency demanded by regulators for the valuation of liabilities and the qualitative requirements also mean that ALM processes have to be carried out, monitored and adapted much more frequently.

ALM processes specific to life insurance are needed

The standards in the banking sector are only applicable to a limited extent to the ALM processes required in insurance. Though there are similarities between the regulatory rules applicable to banks and insurance companies, a special procedure is needed to deal with the non-hedgeable market risks typically incurred by life insurers with very long-term contracts. Further-more, the platform solutions used in banking, where the software has often been designed under pressure to standardise and industrialise, do not generally enable life insurers to rapidly and flexibly adapt their product assortment in response to new market requirements.

Topics: No competitor has a unit comparable with Munich Re’s Finan-cial Solutions and setting it up was a major strategic step for the Group. What was the objective?

Stephan Reulein: The first aim was to position ourselves in the market and with our clients. As a leading reinsurer, we always aspire to being the best at managing all risk factors that could adversely affect our clients’ balance sheets.

What part has the financial and debt crisis played?

Since the crisis erupted in 2008, financial market risks have to a great extent materialised. Take equities and interest-rate risks as an example. In the crisis, they moved in a direction that produced remarkable effects and posed challenges especially to life insurers with their predominantly long-term liabilities – guaranteed interest rates for example. Financial Solutions develops solutions to these risks, which – as we have observed in the last few years – are difficult to diversify, complementing the trad-itional reinsurance approach.

We also provide advice on key cor-por ate finance issues, especially our clients’ profitability and solvency. All this makes us the reinsurance partner of choice across the whole risk spectrum.

What makes this business model different?

Instead of concentrating on the trad-itional underwriting risks, we focus on risks that cannot be managed using classic methods of diversifica-tion and present them in a tradeable form. At our client’s request, we then sell them to appropriate invest ors in the financial markets.

“the insurance industry is facing challenges in risk manage-ment and corporate finance that cannot be overcome using traditional reinsurance alone”, says stephan Reulein, Head of Financial solutions at Munich Re.

“new strategies are needed to handle our clients’ most important risks.”

Risk ManageMent solutions

33Munich Re Topics Magazine 1/2013