Embed Size (px)

Citation preview

m a r c h 2 0 1 2 | v 2 2 . n 2

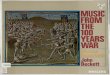

30 Years with John Damgard

Annual Volume Survey | OTC Clearing in Asia | SEF Aggregation

SwapClear is the only clearing service to have successfully handled an OTC interest rate swap default. When the worst happens, you need the best on your side.

“Experience” is an overused buzzword. Until there’s a default.

swapclear.com

We’re ready. Are you?

DATE: 2.15.12 PROJECT: LCH.Clearnet SwapClear Ad: FIA, March Issue

TRIM: 8.375 in. x 10.75 in. BLEED: 8.625 in. x 11 in. PRINTS: 4-CP

SwapClear is the only clearing service to have successfully handled an OTC interest rate swap default. When the worst happens, you need the best on your side.

“Experience” is an overused buzzword. Until there’s a default.

swapclear.com

We’re ready. Are you?

DATE: 2.15.12 PROJECT: LCH.Clearnet SwapClear Ad: FIA, March Issue

TRIM: 8.375 in. x 10.75 in. BLEED: 8.625 in. x 11 in. PRINTS: 4-CP

features

06 President’s Message By John Damgard

08 News Briefs

47 Washington Watch By Joanne Morrison

depar tments

54 Tech Talk By James Woods

58 @Markets

61 Prominent People

30 Years with John DamgardAt the end of March John Damgard will step down after 30 years as the FIA’s president. In this interview, he discusses many of the critical developments that took place during his tenure as the head of FIA, including the shift to electronic trading, the Shad-Johnson Accord, and the industry’s response to the 9-11 attacks. | By Joanne Morrison

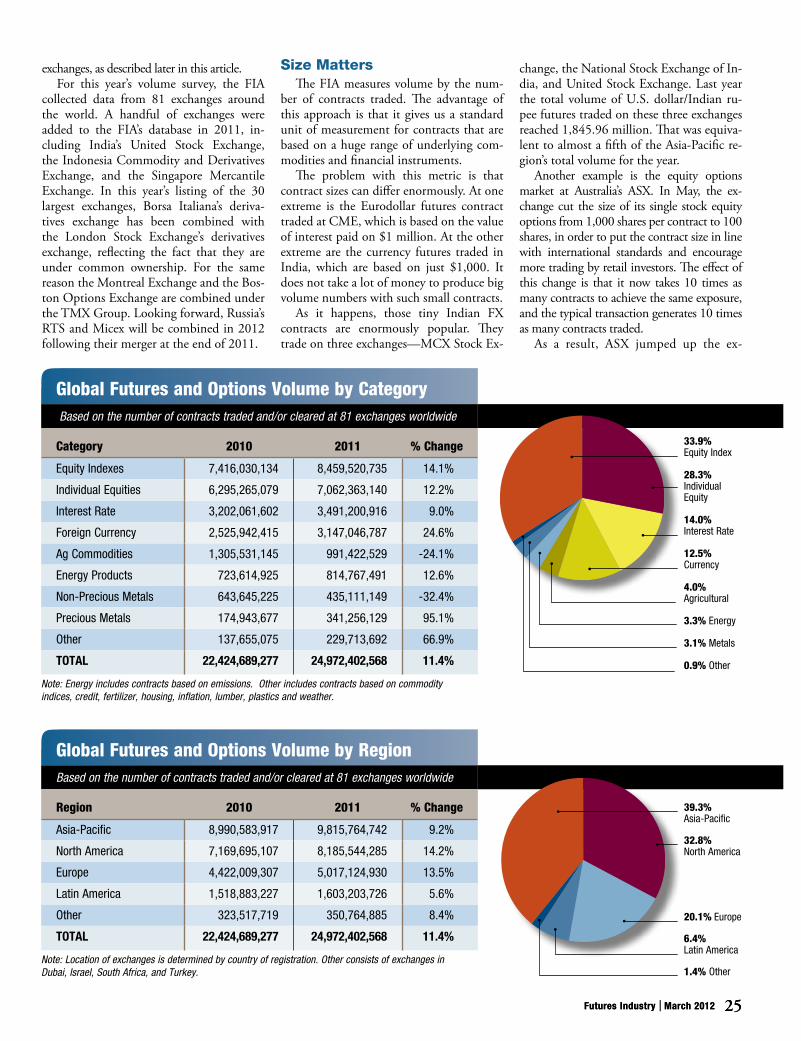

annual Volume survey: 24 Volume climbs 11.4% to 25 BillionThe global listed derivatives markets enjoyed a solid but not spectacular increase in trading activity in 2011. | By Will Acworth

34 Otc clearing in asia: under constructionAsia-Pacific regulators are putting in place requirements for mandatory clearing of over-the-counter derivatives while new OTC clearing services are being developed in every major financial center in the region. Three jurisdictions are relatively far along in the process—Japan, Singapore and Hong Kong. | By Will Acworth

clearing Interest rate swaps: 38 cme Group’s risk management frameworkTwo clearing experts at CME Group describe key elements of CME’s clearing solution for interest rate swaps, including the margin methodology and the “waterfall” of financial protections in case of a default. | By Sasha Rozenberg and Udesh Jha

swaps Liquidity aggregation43 The coming fragmentation of the swaps markets presents an opportunity for dealers and technology companies to provide tools for aggregating liquidity across multiple swap execution facilities. | By Kevin McPartland

16

m a r c h 2 0 1 2 | v 2 2 . n 2

Futures Industry | March 2012 03

Futures Industry five times a year by the Futures Industry As soc iation, ISSN #10656855, 2001 Pennsylvania Avenue N.W., Suite 600, Wash ington, D.C. 20006-1823; (202) 466-5460. Sub scriptions are $24 Domestic and $32 Inter na-tional, and are included as part of the member dues. Periodicals postage paid at the Washington, DC and additional mailing offices. Postmaster: Send address changes to Futures Industry, 2001 Pennsylvania Avenue N.W., Suite 600, Wash ington, D.C. 20006-1823. Copyright 2012 by the Futures Industry Association.

Materials contained herein may not be reproduced for general distribution, advertising or promotional purposes without the expressed consent of the FIA. The statements of fact and opinion in signed articles are the sole responsibility of the authors, and do not necessarily reflect the positions of the officers, mem-bers or staff of FIA, nor the employers of the authors.

Futures IndustryEditor-in-Chief Editor Mary Ann Burns Will Acworth

Deputy Editor Assistant Editor Joanne Morrison Tracy Wahler

Futures Industry edItorIal advIsory BoardRussell Abramson, J.P. Morgan Arthur Bell, Arthur Bell Certified Public Accountants Galen Burghardt, Newedge USA Christopher Culp, Lexecon Kevin Foley, Katten Muchin Rosenman LLP Diane Garnick Michael Gorham, Illinois Institute of Technology Anthony Leitner, A J Leitner and Associates, LLC Terrence Martell, Baruch College John Munro, ION Trading Gerry Perez, Interactive Brokers Group Leslie Sutphen, Newedge USA Barbara Wierzynski, Futures Industry Association

The Futures Industry Association is the international trade organization for the futures industry. Its mem-bership includes more than 28 of the largest futures commission merchants. FIA estimates that its mem-bers are responsible for more than 90% of all public customer business executed on U.S. contract mar-kets. FIA membership also includes more than 30 international futures and options exchanges and clearinghouses in North and South America, Europe, Africa, Asia and Australia, plus banks, law and ac-counting firms, money managers, end users, and service providers with an interest in the derivatives industry.

@Markets is a registered trademark of the Futures Industry Association.

MeMBershIp InFo & advertIsIng ratesToni Vitale ChanFutures Industry Association 2001 Pennsylvania Avenue N.W., Suite 600 Washington, D.C. 20006-1823 Phone: (312) 636-2919 Fax: (202) 772-3075 E-mail: [email protected] Web: www.futuresindustry.org

04 Futures Industry | www.futuresindustry.com

Board of directors officers n Michael C. DawleyManaging Director, Co-Head of Futures and Derivatives Clearing Services Goldman, Sachs & Co. Chairman

n Peter G. JohnsonManaging Director, Global Head of Futures, OTC Clearing and FX Prime Brokerage Bank of America Merrill Lynch Vice Chairman

n Najib LamhaouarGlobal Head of OTC Clearing and ETD HSBC Securities (USA) Inc. Secretary

board members Patrice BlancPresident Jefferies Futures Brokerage and Chief Executive Officer Jefferies Bache LLC

n Philippe BuhannicChairman and Chief Executive Officer TradingScreen Inc.

Gonzalo Chocano

n Gerald F. CorcoranChairman and Chief Executive Officer R.J. O’Brien & Associates LLC

Robert T. Cox

n George E. CrappleCo-Chairman and Co-Chief Executive Officer Millburn Ridgefield Corporation

n John M. DamgardPresident Futures Industry Association

Laurie FerberExecutive Vice President and General Counsel MF Global Holdings Ltd.

Fredrik GentzelManaging Director, Global Head of Listed Derivatives Deutsche Bank AG

n Arthur W. HahnPartner Katten Muchin Rosenman LLP

n Christopher K. HehmeyerManaging Member HTG Capital Partners LLC

nM. Clark Hutchison, IIIGlobal Co-Head of Listed Derivatives Morgan Stanley

nJeffrey D. JenningsManaging Director, Global Head Listed Derivatives Credit Suisse Securities (USA) LLC

Sanjay KannambadiChief Executive Officer and Global Head BNY Mellon Clearing LLC

n Jerome KempGlobal Head of Exchange Traded Derivatives Sales and Clearing Citigroup Global Markets Limited

n Andy MilnesHead of Supply and Trading, Global Oil Americas BP Corporation North America, Inc.

n David S. MitchellPartner Fried, Frank, Harris, Shriver & Jacobson LLP

Reinhardt OlsenManaging Director and North America Head of ETD UBS Securities LLC

n Todd E. PetzelChief Investment Officer Offit Capital Advisors LLC

n Emily PortneyManaging Director, Global Head of Futures and Options JP Morgan Securities LLC

n Kenneth M. RaislerPartner Sullivan & Cromwell LLP

n Edward J. RosenPartner Cleary Gottlieb Steen & Hamilton LLP

n Michael Schaefer

n Stephen SchulerCo-Managing Member GETCO, LLC

n William SextonChief Executive Officer Newedge USA LLC

n Donald R. Wilson, Jr.Chief Executive Officer DRW Trading Group

Jeremy WrightGlobal Head of Futures and Options RBS Futures (London)

n Alice Patricia White

n Michael YarianManaging Diretor, Head of Futures and OTC Derivative Trading Barclays Capital Inc.

special advisorsRichard BerliandManagement Consultant

Gary DeWaal Senior Managing Director and Global General Counsel Newedge USA LLC

n Executive Committee Member n Associate Member Director n Public Director

FIa Chapters and divisions presidents/Chairmen fia asiaPaul S. DaviesGoldman Sachs Futures Pte Ltd.

fia chicagoBill MetzgerHM Consulting

f ia european principal traders associationRemco LentermanIMC Trading B.V.

futures servicesVincent MatteraDennis Murray Consulting

information technologyMatthew ReesR.J. O’Brien & Associates

japan chapterMitch FulscherChairman

Shozo OhtaTokyo Financial Exchange President

law & complianceMaria ChiodiCredit Suisse Securities (USA) LLC

fia principal traders groupDonald R. Wilson, Jr.DRW Trading Group

the Futures Industry association, Inc.John Damgard President

Walt Lukken Incoming President and CEO

Barbara Wierzynski Executive Vice President and General Counsel

Mary Ann Burns Executive Vice President, Industry Relations

Guy Sheetz Senior Vice President, Chief Financial Officer and Chief Operating Officer

Tracy Wahler Vice President of Communications

Angelique Wilkins Vice President, Conferences and Meetings

Maria Banks Accounting Assistant

Adoncia Boykins Director Member Services

Steven Bradbury Senior Accountant

Michael Cho Senior Accountant

Gary Herman Controller

Mary Kincheloe Communications Assistant

Linda Leerdam Receptionist

Roselia Marmolejos Administrative Assistant

Steve Proctor Technology Coordinator

Damon Roberts Meetings Coordinator

Marsha Saunders Manager, Meetings and Events

Mindy Serin eCommunications Coordinator

Toby Taylor Executive Assistant and Office Manager

Beth Thompson Law & Compliance Division Coordinator

ThE

This is my last President’s Message, and on this occasion I’d like to take a moment to talk about leadership. The FIA serves many purposes, but none are more important than its

role in bringing the industry together at a time of crisis and building a consensus on how to protect and preserve the integrity of our markets. As we deal with the aftermath of MF Global and its reper-cussions for the protection of customer funds, we would do well to look back at how we handled past crises and consider what lessons may still apply.

I am thinking in particular about how this industry responded to the collapse of Barings Bank in February 1995. For many of you, the collapse of Barings may seem like an episode out of the distant past, but for those of us who were around at the time, we well remember what a shock it was to see one of the most venerable names in banking brought down almost overnight because of a single rogue trader on the futures desk in Singapore. That incident dealt a severe blow to public confidence in our industry and in par-ticular in the safety of cross-border trading.

Less than a month later, at our annual industry conference in Boca Raton, we formed a task force to address the problems exposed by Barings. That task force consisted of 60 people from a broad range of exchanges, intermediaries and customers. Those were the days before email, so to get this done we had to hold any number of long arduous phone calls as well as two in-person meet-ings—one in Washington and another in London.

After a lot of hard work and sometimes difficult discussions, we reached a consensus on a broad range of recommendations on best practices for futures trading and clearing. That laid the foundation for the report that we issued in June and shared with regulators and exchanges and clearinghouses around the world. That report went a long way towards establishing new standards for our industry, and restoring the confidence of our customers and our regulators in this industry’s ability to tackle difficult issues in a pro-active way.

PrESIDENT’S

now, in the aftermath of MF Global, we are faced with a chal-lenge perhaps even greater than Barings, and I am proud to say that the FIA is once again taking a leadership role. In January we formed a task force under the leadership of FIA Chairman Mike Dawley to undertake a serious self-appraisal of policies and procedures for protecting customer funds and to consider ways to improve industry practices. As I have said before, the shortfall in the customer funds at MF Global was a huge black eye for our industry. Even though we still don’t know exactly what happened, there is no question that customer confidence in the protections for their funds has been seri-ously damaged, and it is now the industry’s responsibility to come together to respond.

At the end of February, the task force put forward an initial set of practical recommendations focused on policies and practices at futures commission merchants. Some of those can be imple-mented immediately. Others will require rule changes by either the federal regulators or the industry’s self-regulators to establish better visibility into the handling of customer funds and higher standards for internal controls. We also issued a “frequently asked questions” paper to provide customers with more transparency on the current protections in place for customer funds. And these are just the first steps. We are continuing to talk with a broad range of market participants and regulators, just as we did with Barings, and we expect to have more suggestions and recommendations in the near future that will help reassure customers that their money will be held safely and securely.

During my 30 years as FIA chairman, we have always been the industry’s champion through thick and thin. That is never more important than when we are dealing with difficult issues. I wish I could take credit for all of these achievements, but the truth is that it was all of you, the members of the FIA, who made it possible. The strength of the FIA has always been and will always be the

willingness of our members to step up and volunteer their time, energy and expertise to these industry-wide projects. Together we have overcome a whole host of challenges, and I am confident that with your unstint-ing support we will continue to do so in the years ahead.

John DamgardPresident

Leadership in Times of Crisis

06 Futures Industry | www.futuresindustry.com

Europe is changing. Stay ahead of the curve.

Today’s markets twist and turn – nowhere more so than in Europeanfixed income. As the region changes,you need to stay on top of interest raterisk while spotting new opportunities as they arise.

On Eurex Exchange, you can stayahead of the European yield curve withthe world's most heavily traded EUR-denominated fixed income derivatives.

With open interest of more than 2.5 million contracts in futures and more than 2.6 million contracts in options, it’s a market that’s both diverse and reassuringly liquid.

Euro-Schatz, Euro-Bobl, Euro-Bund andEuro-Buxl® Futures – futures contractson triple A-rated German governmentbonds that often serve as standardreference for interest rates in Europe.

And if you’re hedging non-triple A-ratedEuropean government bonds, we offerShort-, Mid- and Long-Term Euro-BTPFutures contracts based on notional debtsecurities issued by the Republic of Italy.

Besides these longer term products, on Eurex Exchange you can accessmoney market rates through EURIBORderivatives, while maximizing off-order book opportunities through

our EurexOTC services – available for fixed income and money marketderivatives.

And each of these trades is handledthrough Eurex Clearing – one of theworld’s leading CCP clearing housesand an innovator in risk management.

Products to capitalize on the moment.The safety and assurance you shouldexpect.

Discover more on Eurex Exchange.

www.eurexchange.com

The information published in this publication is for general information purposes only. It is not intended to constitute investment advice nor is it intended for solicitation purposes.Eurex is not responsible for any errors or omissions contained in this publication. Before trading, persons should consider the risks involved and the legal requirements of the relevant jurisdiction.

Eurex Reappraisal _FI Mag_Mar12_Futures Industry Magazine 01.02.12 10:41 Seite 1

8 Futures Industry | www.futuresindustry.com

EU Blocks Deutsche Börse and NYSE Euronext MergerThe European Commission on Feb. 1 announced its official opposition to the pro-posed merger between Deutsche Börse and nYSE Euronext, stating that the combined entity would have a “quasi-monopoly” in European financial derivatives.

“These markets are at the heart of the fi-nancial system and it is crucial for the whole European economy that they remain com-petitive. We tried to find a solution, but the remedies offered fell far short of resolving the concerns,” said Joaquín Almunia, vice president in charge of competition policy.

The two exchanges expressed disap-pointment with the decision but said they have agreed to terminate their merger plans. “It is now time to move on and return our sole focus to executing our compelling exist-ing strategy—a strategy we have continued to implement without missing a beat over the last year,” said Jan-Michiel Hessels, nYSE Euronext chairman.

Since then nYSE Euronext has re-launched a plan to develop in-house clearing services for its European deriva-tives markets, an effort that was put on hold when the merger deal was announced. Dur-ing a February conference call with investors and analysts, nYSE Euronext officials said this project will convert nYSE Liffe Clearing into a full-service clearinghouse and end the exchange’s reliance on LCH.Clearnet for clearing services. The officials also said they plan to develop the ability to clear over-the-counter products.

“We look forward to engaging with us-ers to develop a full-service U.K.-based clearinghouse, which will offer operating and capital efficiencies, provide innovative solutions across listed and OTC markets and provide an unrivaled level of customer service,” Duncan niederauer, the ex-change’s chief executive officer, said on the call. “With legislation beginning to crystallize on the new mandates which will be imposed for central clearing of derivatives, now is the right time in our opinion to be working with users to develop competitive clearing solu-tions that will meet their needs.”

European Policy Makers Finalize EMIR The European Union announced on Feb. 9 that after a long period of negotiations, the European Parliament and the EU Council have agreed on the final text of the Euro-pean Market Infrastructure Regulation. This regulation includes a number of provisions that will directly impact members of the FIA and their affiliates, including mandatory clearing and trade reporting requirements for over-the-counter derivatives as well as organizational and prudential requirements for clearinghouses.

“I congratulate the European Parlia-ment and the Council on reaching today an important agreement on a regulation for more stability, transparency and efficiency in derivatives markets,” Michel Barnier, EU Commissioner for Internal Market and Ser-vices, said in a statement. “The EU has now also fulfilled its G20 commitments in this field, and on time.”

Barnier noted that the regulation ensures that information on all European deriva-tive transactions will be reported to trade repositories, thereby giving policy makers and market supervisors “a clear overview of what is going on in the markets.” He also commented that the regulation requires standard derivative contracts to be cleared through central counterparties and estab-lishes “stringent” organizational, business conduct and prudential requirements for these CCPs.

The next step will be a plenary vote in the European Parliament and then adoption by the Council, both of which are expected to take place in March. Once that occurs, the European Securities and Markets Authority will be required to draft technical standards for the application of EMIR.

In related news, ESMA announced the first step in putting EMIR into effect. On Feb. 16 ESMA issued a discussion paper on the “technical standards” for the implementation of the new regulation. The discussion paper covers such topics as the organizational and prudential requirements for clearinghouses and the scope of the clearing requirements for OTC derivatives. Comments are due by

March 19. Based on the responses that it receives, ESMA will prepare draft technical standards for another round of consultation during the summer.

ESMA also announced two other initia-tives related to the implementation of EMIR. It is working with the European Banking Authority and the European Insurance and Occupational Pensions Authority on a joint discussion paper for technical standards for OTC derivatives that are not subject to clearing requirements. In addition, the EBA is expected to issue in the coming weeks a discussion paper on technical standards for clearinghouse capital requirements.

Singapore Proposes OTC Derivatives Rules The Monetary Authority of Singapore is-sued a consultation paper on Jan. 13 on the regulatory oversight of the over-the-counter derivatives market in Singapore. The proposed regulatory regime will cover both financial and commodity derivatives and includes provisions requiring the use of clearinghouses and trade repositories as well as rules for market operators, clear-ing facilities, trade repositories and market intermediaries. The consultation does not propose mandatory trading on electronic platforms or exchanges. MAS said it is talk-ing with the industry on the potential costs and benefits of such a requirement and will consult on this at a later date.

To determine which OTC derivatives should be subject to the clearing mandate, the MAS proposal said it would look at such factors as potential systemic risk, degree of standardization, depth and liquidity of the market, availability of pricing data, the clear-inghouse’s risk management capabilities, and the international regulatory approach to that type of contract. Interest rate swaps denominated in Singapore and U.S. dollars and non-deliverable forwards in Asian cur-rencies “appear to fulfill these criteria,” the MAS said.

Under the proposal, market participants would not be required to use a Singapore-located clearinghouse; the MAS said this would “limit choices for market participants,

newsbriefs

CLIENT NAME: element79JOB#: 15526DESC: Harris

OPERATOR: tjcROUND: 2DATE: 01/31/12

FILE NAME: I15526A.indd QC Check __________

__________

__________

80 70 70 10010.2 7.4 7.4 100 100 100100 100 60 100 100 70 70 30 30 100 100 60 100 100 100 10070 70 30 30 100 100 60 70 70 4070 70 30 30 100 40 100 40 40 100 10 40 40 20 70 70 3.1 2.2 2.270 40 40 75 66 6650 40 4025 19 19B 0 0 0 0

100 70 30 100 10 25 50 75 90 100100 60 100 70 30 100 60 40 70 4070 30 100 40 40 100 40 100 40 70 40 70 40 40 340 70 40 70 40 40100 60A

3%ISO 12647-7 Digital Control Strip 2009

Title: Space/Color:Bleed Size:Trim Size:Live Size:Media:

Creative Director: Art Director: Copywriter: Print Producer: Project Manager: Acct. Mgr.: Keyliner:

Billing #: HARBB P17579

Element79 200 E. Randolph 33rd Floor Chicago, IL 60601 • www.element79.com

HARBB17579FIHarris Bank/Commercial Banking

A. SpindleZ. Orozco

J. NiccumD. TroppB. BattleL. Ruedger_1/31/12_2

"EXECUTION."FP 4/CB8.75" w x 11.25" h8.5" w x 11" h8.25” w x 10.75” hFutures Industry

Material Close: 2/6/12 Insertion Date: March 2012

Execution.Consistency.Expertise. Successful futures organizations look to partners BMO Harris Bank and BMO Capital Markets for execution that defines best in class. Through our long-standing, consistent presence in the industry, we deliver an uncompromising level of service. The combination of our expertise, accessibility, stability, and responsiveness has made us the leader in delivering tailored products and services to the futures industry.

www.bmoharris.com www.bmocm.com

BMO Harris® is a trade name used by BMO Harris Bank N.A. and its affiliates. Loan and deposit products and services are provided by BMO Harris Bank N.A. Member FDIC. BMO Capital Markets is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A. and Bank of Montreal Ireland p.l.c., and the institutional broker dealer businesses of BMO Capital Markets Corp., BMO Nesbitt Burns Trading Corp. S.A., BMO Nesbitt Burns Securities Limited and BMO Capital Markets GKST Inc. in the U.S., BMO Nesbitt Burns Inc. in Canada, Europe and Asia, BMO Nesbitt Burns Ltée/Ltd. in Canada, BMO Capital Markets Limited in Europe, Asia and Australia and BMO Advisors Private Limited in India. ® Registered trademark of Bank of Montreal in the United States, Canada and elsewhere.

10 Futures Industry | www.futuresindustry.com

newsbriefslead to fragmentation of liquidity, reduce netting benefits and increase costs for [financial institutions] currently clearing with foreign CCPs.” The MAS instead proposed a mutual recognition framework under which foreign CCPs could apply for authorization to offer clearing services in Singapore.

Iosco Reviews Swap Trading PlatformsThe International Organization of Securi-ties Commissions issued a report on Jan. 25 describing the different types of trading platforms currently available for the execu-tion of OTC derivatives transactions in Iosco member jurisdictions. The report noted that there are two broad categories: those with multiple liquidity providers (multi-dealer platforms) and those with a single liquid-ity provider (single-dealer platforms). The report described the differences in the trade execution models, the participant cover-age, the degree of automation, the scope of asset class or product coverage, and the geographic coverage. Iosco said the report was drafted to help regulators and policy-makers as they develop derivatives trading policy proposals.

Dodd-Frank Amendments Advance in House The House Agriculture Committee on Jan. 25 approved by a voice vote six bills that would modify derivatives-related provi-sions of the Dodd-Frank Act. The bills have already cleared the House Financial Services Committee but will not become law unless and until approved by the Senate and Presi-dent Obama.

“Without these important changes, regulations could deter businesses from hedging against risk. That increases costs for consumers and reduces stability in the market place, which is contrary to the intent of the original Dodd-Frank legislation,” said House Agriculture Committee Chairman Frank Lucas (R-Okla).

One bill (H.R. 1840) requires the Com-modity Futures Trading Commission to assess the costs and benefits of proposed actions. Another bill (H.R. 2682) clari-fies that end-users are exempt from the

FIa

ACTIONS

FIA Participates in Coalition Urging China to Modernize Financial SectorFIA President John Damgard joined with the heads of 11 other financial services trade associations in writing a letter to Chinese vice President Xi Jing-ping in advance of his visit to the U.S. The letter emphasized that the fastest way for China to modernize its financial system is to open the financial sector to greater participation by foreign financial services firms. “Continued reform and modernization of China’s financial sector is essential if China is to achieve its economic goals of maintaining high rates of growth and job creation, build-ing a more services-based, consumer-driven economy, reducing poverty, and ensuring a more equitable distribution of opportunity and prosperity,” the coali-tion said in its letter.

ISDA, SIFMA and FIA Comment on “Available to Trade” RulemakingThe International Swaps and Derivatives Association, the Securities Industry and Financial Markets Association and the Futures Industry Association filed a joint letter on Feb. 13 to the Commodity Futures Trading Commission com-menting on the agency’s proposed rulemaking concerning the process by which over-the-counter swaps will be made “available to trade,” a term established by certain provisions of the Dodd-Frank Act. The three associations noted that the designation of a swap as “available to trade” will have broad ramifications for the market because such a swap will no longer be permitted to trade on a bilateral basis. The three associations offered a number of recommendations to avoid inappropriate designations. These included a recommendation that the determination should be made by the CFTC, not a swap execution facility or an exchange. The groups also recommended that the CFTC perform an in-depth study of the market to determine the amount of liquidity in a particular type of swap before designating it as “available to trade.” Furthermore, the trading requirement should not take effect until at least six months after the swap has been made “available to trade.”

Groups Warn of Extraterritorial Impact of Swap Dealer Registration RequirementsSix leading financial industry trade associations have expressed concern about the impact of U.S. swap dealer registration requirements on firms engaged in the global swap markets. In a Feb. 2 letter to the Commodity Futures Trading Commission, the six groups, which included the FIA, warned that the new rules could force dealers into “costly, disruptive, and time-consuming” restructuring of their operations.

“Legal entity restructuring is a costly, disruptive and time-consuming pro-cess, involving extensive re-documentation of client agreements, re-allocation of scarce capital, re-assignment or re-location of personnel as well as po-tentially extensive systems development and compliance infrastructure,” the groups warned.

In addition to the FIA, the signatories included the Securities Industry and Fi-nancial Markets Association, The Clearing House, The Financial Services Round-table, ABA Securities Association, and Institute of International Bankers.

PARTNERSas of 27 February

SPONSORSas of 27 February

Visit www.idw.org.uk for a complete exhibitor listing. Limited sponsorships and exhibit space are still available.

Contact Toni Vitale Chan +1.312.636.2919; [email protected] Bernadette Connolly +44 [0]20 7090 1334; [email protected]

IDX GALA IN AID OF FUTURES FOR KIDSWednesday 27 June – The Artillery Garden at the HAC, London EC1

FIA and FOA are pleased to announce that the IDX Gala Dinner will, once again, be held in aid of Futures for Kids (FFK). FFK was established in March 2008 to provide a fundraising vehicle through which this industry can raise money to support charities working to improve the lives of children around the world. For further information, to reserve tables / places or to discuss supporting the Dinner as a sponsor, please contact Bernadette Connolly by email ([email protected]) or tel +44 (0)20.7090.1334.

FIA/FOA Internati onal Derivati ves Expo26-27 June 2012

The Brewery, Chiswell Street, London EC1www.idw.org.uk

12 Futures Industry | www.futuresindustry.com

newsbriefs

MF

glo

ba

l UPDATE

CFTC FCM Study: No Material Breach of Customer Funds ProtectionThe Commodity Futures Trading Commission on Jan. 25 re-leased the findings of a review of futures commission merchants begun shortly after the MF Global collapse. The agency said it did not find any material breaches of customer funds protection requirements during the spot check. The review, which covered 70 FCMs, found that firms maintained excess funds in both segregated accounts and secured accounts. The FCMs held a total of roughly $166 billion in segregated accounts, which was about $13 billion in excess of the $153 billion owed to custom-ers. The FCMs also held about $48 billion in Part 30 secured accounts, which was about $7 billion in excess of the secured amount obligation. The CFTC reviewed customer segregated accounts at 14 of the largest FCMs. The CME and nFA re-viewed 56 other FCMs carrying customer funds.

FIA Establishes Task Force to Respond to MF GlobalThe Futures Industry Association announced on Jan. 24 that it has established a special committee to address issues related to the bankruptcy of MF Global. The Futures Market Finan-cial Integrity Task Force will develop and recommend specific measures that can be implemented in the near term through both industry best practices and regulatory change. In addition to these measures, the FIA intends to work with end-users and other market participants to examine the adequacy of current customer funds protection models in response to concerns raised by the MF Global bankruptcy.

“The FIA looks forward to partnering with end-users, regula-tors, legislators and clearinghouses to restore customer confi-dence in the futures markets,” said Michael Dawley, chairman of the FIA and managing director, Goldman Sachs & Co. “Although we still do not know for certain what caused the significant shortfall in customer segregated funds required to be held at MF Global, any loss of customer assets is entirely unacceptable and the reasons for the deficiency need to be identified.”

The task force will be headed by a steering committee con-sisting of a diverse group of futures commission merchants with institutional, commercial and retail customer bases as well as representatives of other industry segments.

SROs to Jointly Review Customer Segregation Protections In response to the MF Global collapse, national Futures As-sociation, CME Group, IntercontinentalExchange, Kansas City Board of Trade and the Minneapolis Grain Exchange have joined together to consider how to strengthen current safeguards for customer segregated funds. The coordinated effort by all of the

futures industry’s self-regulatory organizations will examine what changes can be made to rules or to the ways in which firms demonstrate compliance with those rules to prevent customer losses due to the insolvency of a futures commission merchant.

“Self-regulation has served the futures industry and its cus-tomers very well for a very long time,” said Daniel Roth, presi-dent of nFA. “However, the MF Global bankruptcy has dealt a severe blow to the public’s confidence in the financial integrity of our futures markets and it is incumbent upon the industry’s SROs—in collaboration with the Commodity Futures Trading Commission—to take the necessary steps to enhance cus-tomer protection, particularly in the area of segregated funds.”

CME Establishes $100 Million Fund to Protect Family Farmers and RanchersCME Group announced on Feb. 2 that it will establish a $100 million fund designed to provide further protection of customer segregated funds for U.S. family farmers and ranchers who hedge their business in CME’s futures markets. “In light of the recent MF Global failure, in which a clearing firm violated CFTC regulations and misused customer monies that should have been kept segregated, CME Group is adding this extra security measure to protect the country’s food producers who are using CME Group futures markets to hedge their crops and livestock that feed the world,” CME said. Under the Family Farmer and Rancher Protection Fund, expected to be in effect by March 1, 2012, farmers and ranchers using CME Group products will be eligible for up to $25,000 per account in the case of losses resulting from the future insolvency of a clearing member or other market participant. Farming and ranching cooperatives also will be eligible for up to $100,000 per cooperative. If losses in a future failure total more than $100 million, participants will be eligible for a pro-rata share of the fund, up to $100 million. This new fund is expected to be backed by an insurance policy and will not be available retroactively.

FSOC to Undertake MF Global ReviewTreasury Secretary Tim Geithner on Feb. 2 announced that the Financial Stability Oversight Council will investigate what changes are needed to better protect customer funds in the wake of the MF Global collapse, working with the Commodity Futures Trad-ing Commission and the Securities and Exchange Commission. “The failure of customer account segregation rules to protect the customers of MF Global illustrates that we have some work to do ahead,” Geithner said in a speech on the state of financial reform. “Recently, the CFTC finalized rules to improve protections for certain customer funds. The Council, working with the SEC and the CFTC, will undertake a broad review of what other changes are necessary to strengthen these protections further.”

Futures Industry | March 2012 13

margin requirements, while another (H.R. 3527) clarifies that energy and agriculture end-users are not misclassified as swap dealers. Inter-affiliate swap transactions would be exempt from Dodd-Frank provi-sions under another bill (H.R. 2779) passed by the committee. Small banks and farm credit institutions would not be classified as swap dealers under another bill passed (H.R. 3336).

The committee also voted on a bill (H.R. 2586) to modify provisions related to swap execution facilities. This bill prohibits regula-tors from requiring a minimum number of participants to receive or respond to deriva-tives transactions quote requests. It also prohibits regulators from limiting the means of interstate commerce that market participants can use to execute swaps and prohibits the agencies from requiring a SEF to delay quotes for any specific period of time.

CFTC Re-Regulates SEC-Registered Investment CompaniesThe Commodity Futures Trading Commis-sion on Feb. 9 issued a final rule regarding registration and compliance obligations for commodity pool operators and commodity trading advisors under section 4.5 of the Commodity Exchange Act. The rule passed 4-1, with CFTC Commissioner Jill Sommers in opposition.

The final rule substantially narrows exemptions from the CFTC’s CPO rules for fund managers that are registered with the Securities and Exchange Commission and reinstates a number of reporting and other regulatory requirements. In effect, the final rule will require these fund managers submit to dual regulation by the CFTC and the SEC or else reduce their trading of derivatives. The rule also will require CPOs and CTAs to provide more information to the CFTC about their financial condition and trading activi-ties, including information on assets under management, user of leverage, counterparty credit risk exposure, and trading and invest-ment positions for each pool.

“This rule reinstates the regulatory requirements in place prior to 2003 for registered investment companies that trade

over a de minimis amount in commodities or market themselves as commodity funds,” CFTC Chairman Gary Gensler explained. “This rule enhances transparency in a num-ber of ways and increases customer protec-tions through amendments to the compli-ance obligations for CPOs and CTAs.”

Sommers warned that the rule could be overturned in court. “It is unlikely, in my view, that the cost-benefit analysis supporting the rules will survive judicial scrutiny if chal-lenged,” she said.

The Investment Company Institute, a trade association that represents mutual funds and other fund managers, expressed strong opposition to the final rule. “We have serious concerns about amended CFTC Rule 4.5 and the unnecessary operational and compliance burdens it appears to impose on many mutual fund advisers,” ICI said in a statement. “While we continue to review the new rule in detail, it appears that it fails to address numerous concerns raised by ICI and others, and will impose needless costs on funds and fund shareholders.”

The CFTC also released a proposed rule aimed at reducing the compliance burdens associated with dual regulation by both the CFTC and SEC. The proposed rule, which was approved unanimously, asks for public comment on amending the reporting re-quirements applicable to certain investment companies registered under the Investment Company Act of 1940, whose advisors would be required to register with the CFTC as CPOs. The CFTC said this proposal seeks to harmonize CFTC and SEC require-ments to minimize the compliance burden on these registrants.

Obama Administration Proposes CFTC Budget Hike and 60/40 RepealPresident Obama’s proposed budget for fiscal 2013, which was released on Feb. 13, includes large increases to the budgets for the Commodity Futures Trading Commis-sion. If approved by Congress, the CFTC’s budget would rise to $308 million from the $205 million approved by Congress for fis-cal 2012, an increase of almost 50%. The increased budget would allow the agency

to add 296 employees, bringing its total staff to 1,015 people. The budget increase also would allow the agency to ramp up its investment in data and technology to $105 million from the current level of $60 million.

The Obama administration said the CFTC will need the additional funds to implement the swaps market regulation mandated by the Dodd-Frank Act. For example, the CFTC expects that the number of exchanges and trading platforms under its purview will triple between 2011 and 2013. The CFTC also plans to double the capacity of its market surveillance infrastructure.

The administration also proposed a partial repeal of the 60/40 tax treatment for futures and options. According to the Treasury Department, dealers in futures and options would be required to treat income from day-to-day transactions in futures and options as ordinary income rather than capital gains. This would apply to dealers in equity options as well as options on futures. Treasury estimated that this would raise $1.2 billion in revenues for the government over the next five years.

In contrast to the administration’s budget proposals for fiscal 2012, the new bud-get proposal does not include a user fee. Instead, the administration said it “strongly supports” legislation to fund the CFTC through user fees on transactions in futures, options and swaps. In December four House Democrats introduced a bill, H.R. 3665, that would authorize the CFTC to collect user fees up to the amount appro-priated by Congress. no action has been taken on that bill yet, however.

EU Lawmakers Seek Stricter Controls on HFT Members of the European Parliament’s economic and monetary affairs committee called for stricter controls on high-frequency trading to be included in the European Com-mission’s review of the Markets in Financial Instruments Directive. At a Feb. 13 hear-ing, Markus Ferber, a German member of the committee who is acting as rapporteur for the MiFID legislation, said the proposal “does not go far enough” in addressing problems caused by high-frequency trading.

14 Futures Industry | www.futuresindustry.com

newsbriefspurpose of the report is to describe the trad-ing and clearing of swaps in each area and identify areas of regulation that could be har-monized. In the third section of the report, the two agencies described several aspects of clearing where there are significant “divergences.” These include: requirements for mandatory clearing; segregation and portability; clearinghouse ownership and governance; and clearinghouse location.

NYSE Liffe to Introduce Position Limits for Commodity FuturesnYSE Liffe plans to introduce an “enhanced position management regime” for its com-modity futures and options contracts traded in London, the exchange said in a Feb. 15 notice to members. The exchange said the new regime, which will include hard limits in the front month as well as accountability levels in all months, is tentatively set to take effect in november for coffee, December for sugar and cocoa, and January 2013 for feed wheat. The exchange explained that it decided to introduce these changes after consulting with market participants and hearing requests for a more “formalized and prescribed” position management regime. The exchange also noted that European regulators have proposed formalized posi-tion management regimes in the MiFID 2 legislation. Feedback on the proposed changes is due by March 9.

U.S. Senator Calls for Limits on Mutual Fund Investments in CommoditiesAt a Jan. 26 hearing of the Senate Home-land Security’s permanent subcommittee on investigations, Senator Carl Levin (D-Mich.) urged the Internal Revenue Service to cease allowing mutual funds to avoid limits on their commodity investments. Levin, who chairs the subcommittee, claimed the policy has “opened the floodgates” to excessive speculation that has driven up prices for gasoline and heating oil.

Levin was referring to IRS rulings that have allowed mutual funds to raise their commodity holdings above 10% of income without triggering corporate income tax

Pascal Canfin, a French member of the committee, said long-term investors com-plain that they are at a disadvantage to the faster HFT traders and suggested that the proposal should include a “latency period” for orders and a limit on the number of can-celled orders. Other lawmakers noted the U.S. experience with the flash crash in May 2010 and complained that high-frequency traders pull out of the market when the liquidity they provide is most needed.

Several lawmakers expressed doubt, however, about the Commission’s proposal to address this problem by requiring all trad-ers using algorithms to continuously provide quotes to the markets during the trading day. Ferber said the committee is “rethinking” this approach. In addition, several lawmakers suggested that they will look at academic re-search before supporting greater restrictions on HFT. Kay Swinburne, a U.K. member, cautioned that more data is needed before deciding whether HFT is good or bad, and noted that the U.K. government’s Foresight project is analyzing a number of expert reports and studies on this issue.

CFTC Creates Advisory Panel on Automated and High-Frequency TradingThe Commodity Futures Trading Commis-sion on Feb. 9 voted to create a new advi-sory subcommittee on automated and high-frequency trading. The CFTC also published a notice requesting nominations for industry representatives to serve on the panel. The subcommittee will report to the full Tech-nology Advisory Committee. Developing a common definition of high-frequency trading will be a focus of this new panel. The subcommittee will be chaired by Andrei Kirilenko, the CFTC’s chief economist.

CFTC and SEC Release Joint Report on International Swap RegulationAs required by the Dodd-Frank Act, the Commodity Futures Trading Commission and the Securities and Exchange Com-mission issued a joint report on Jan. 31 on how swaps are regulated in the U.S., Asia and Europe. The regulators said that the

requirements. According to Levin, this has been accomplished by making the invest-ments through commodity-linked notes or through offshore shell corporations. At least $50 billion has been invested in commodi-ties by mutual funds, he said.

U.K. FSA Issues Guidance on Counterparty Credit Risk at ClearinghousesThe Financial Services Authority on Jan. 31 issued guidance on how clearinghouses should manage counterparty credit risk. The guidance was developed in response to changes in the clearing market, notably an uptick in the applications for new clearing services as well as increased regulatory attention to systemic risk issues. The guid-ance focuses on certain aspects of coun-terparty credit risk management, namely risk models and associated governance, processes and procedures, and does not address other aspects such as participant eligibility criteria. In particular, the guid-ance covers the following eight areas: risk management governance and counterparty credit risk control framework, initial margin models, variation margin calculation, default fund, stress testing, wrong way risk and concentration risk, collateral, and validation and back-testing.

ICE Clear Credit Launches Portfolio Margining for Clearing ParticipantsIntercontinentalExchange announced in January that ICE Clear Credit, its clearing-house for credit default swaps, is now offer-ing portfolio margining benefits for clearing members’ proprietary positions. ICE said it has petitioned the Commodity Futures Trading Commission and the Securities and Exchange Commission for permission to provide the same margining benefits to customers. “Customer portfolio margining is a key prerequisite to making CDS clearing attractive to clients,” Tom Benison, manag-ing director at J.P. Morgan, said in a state-ment. “Clients currently can avail themselves of offsetting trades in the bilateral world, so it’s important that they have the same ability within the clearing framework.”

Join Profit & Loss at our series of global Forex Network Conferences and events; Enjoy interactive panel discussions andnetworking opportunities with leading international and local industry leaders; Visit our world class FX technology trade shows.

Forex Network Asia 2012 in association with ACI Singapore Singapore, February 16Forex Network Colombia 2012 Bogota, March 27Forex Network Mexico 2012 Mexico City, March 29Forex Network London 2012 (with P&L Digital FX Awards Dinner) London, April 18 Forex Network New York 2012 (with P&L Readersʼ Choice Digital Markets Awards Dinner) New York, May 31Forex Network Chicago 2012 Chicago, September 27-28Forex Network Chile 2012 Santiago, OctoberForex Network Brazil 2012 Sao Paolo, OctoberForex Network Canada 2012 in association with FMAC Toronto, November 15

To book your place at any of our events* please contact Jessica Randal: +44 (20) 7377 6383 or email [email protected] For information on sponsoring or exhibitingplease contact Michelle Hemstedt or Cindy Loveday: +44 (20) 7377 6383: email [email protected] or call our New York office on +1 646 290 5255. *Delegate fees apply.

PROFIT & LOSS FOREX NETWORK CONFERENCES 2012

PROFIT & LOSS EVENTS2012

SINGAPORE BOGOTA MEXICO CITY

LONDON NEW YORK CHICAGO

SANTIAGO SAO PAOLO TORONTO

ALLEVENTS 12_HSAD_NEW JAN:Layout 1 1/9/12 10:52 AM Page 1

John Damgard has served as president of the FIA since 1982. At the end of March he will step down from this position, but he leaves a strong legacy at both the FIA and the futures industry. Under his leadership the association has grown to more than 270 members from nearly 30 countries. As the industry’s leading representative in Washington, the FIA has become a respected source of information about the trading and clearing of derivatives and a champion for free markets everywhere. In his role as the public face of the industry, Damgard has testified countless times before Congressional committees and has worked with every presidential administration since Ronald Reagan. He has been widely recognized in the media as a premier spokesman on all issues related to the futures, options and over-the-counter cleared derivatives markets. In this interview, he discusses many of the critical developments that took place during his tenure as the head of FIA. Among those are the shift to electronic trading and the enactment of the Commodity Futures Modernization Act, both of which helped foster innovation and growth in the derivatives market, the collective actions taken by the industry after serious events such as the collapse of Barings Bank, the September 11 attack and most recently the impact of MF Global.

16 Futures Industry | www.futuresindustry.com

John Damgard

30 Years with

By Joanne Morrison

FI: Over the course of your 30 years at the FIA, the futures markets have changed dramatically. Can you talk about how things looked when you started, the number of exchanges, how the markets were used, and how that compares to what we have today?

DAMGARD: Well, it was all open outcry when I started, and the business was still predominately agricultural and metals. The first big change came when people outside of the agricultural community recognized that these instruments could be used for other products besides bushels of corn and pork bel-lies. Once the Chicago exchanges showed that you could use the futures markets for things like foreign exchange and interest rates, it really set off a revolution in the financial markets that has continued right up to the present day.

Plus there was innovation in commodities as well. It may be hard to imagine now, but the New York Mer-cantile Exchange did not have any energy contracts un-til the late 1970s, and there weren’t any futures on crude oil until 1983. So when I stepped into this job in 1982, we were right in the midst of tremendous innovation.

The other really big change over the past 30 years was the advent of electronic trading. Once open outcry gave way to screen-based trading, it com-pletely changed the nature of the business. Elec-tronic trading took away the so-called trader’s edge, which had existed on the floor of the exchanges for a long time. Electronic trading leveled the playing field, which in the long run has been very good for everyone in the business.

Of course, in those days the exchanges were owned by the people on the floor, and open outcry forever was their cry. What overcame that resistance was the competition from exchanges in Europe, which had gone electronic well before the exchanges in Chicago and New York. Plus the fact that a handful of people in the industry saw which way the wind was blowing. You have to give credit to people like Leo Melamed who recognized that change was inevitable. He went down on the floor of the Merc and persuaded them to support Globex, which was one of the early electronic trading systems.

FI: Do you think the competition from Liffe and Eurex was a catalyst to help drive the U.S. to electronic trading?

DAMGARD: Without a doubt. When those two exchanges came to the U.S. and offered electronic trading for the benchmark interest rate futures, it really forced the U.S. exchanges to be competitive.

FI: One of the turning points in the history of elec-tronic trading was in the late 1990s when Liffe lost the bund contract to Eurex. At that time, Liffe was an open outcry exchange and many people in the industry were not sure it would survive. What was it that helped revive Liffe?

DAMGARD: The person I would single out as key to Liffe’s recovery is Brian Williamson, who was a member of the original group that established Liffe in 1982. Williamson returned to Liffe for a second stint as chairman from 1998 to 2003 and led the exchange through a profound restructuring. That was when the exchange abandoned open outcry in favor electronic trading and converted itself into a profit-oriented organi-zation owned by shareholders. And of course it survived and thrived to the point where now it’s one of the crown jewels of NYSE Euronext.

FI: Over the course of your tenure, there’s been a lot of consolidation among the FCMs. What impact do you think this has had on the industry?

DAMGARD: Well you’re right, the FCM business has consolidated tremendously. A lot of the old names with great standing in the industry for many years are no longer around. But that’s not all bad. The FCM busi-ness is extremely competitive, and the people who have invested in technology and improved their efficiency have been able to buy out the firms that for whatever reason did not want to stay in the business. If this con-tinues, however, I would be concerned that customers will have fewer choices. I think it is pretty important to have multiple choices as we move toward man-datory clearing for over-the-coun-ter-derivatives.

John came to Washington during the Nixon Administration to work as an aide to Vice

President Agnew.

John shows former Chicago Mayor Harold

Washington around the Futures & Options

Expo ’86 exhibit hall.

FI: There’s been a tremendous change in the role and function of exchanges. They have gone from mem-bership organizations dominated by floor traders to shareholder-owned for-profit enterprises. How do you think that has impacted the industry?

DAMGARD: One of the results is that a lot of the tension has gone out of the relationship between exchanges and clearing firms. It has become more of a partnership. You can see that in the way that the ex-changes are recognizing that they need the backing of the clearing firms to support things like new clearing services, or a new set of products.

FI: Over the last 30 years, there have been some land-mark changes in regulation. Can you talk about that?

DAMGARD: I have to start out with the Dodd-Frank Act. This legislation and subsequent reforms will affect the futures markets far more than expected. We have been busy at the FIA with dozens of working groups comprised of our members who have com-

mented on the proposed rules and have made wide ranging recommendations

on these rules

John and FIA general counsel Barbara Wierzynski at one of many FIA board meetings.

that will greatly impact our industry.Looking back, I would say creation of the CFTC

in 1974 was critical. In those days, virtually all futures contracts were based on agricultural commodities. There was very little interest on the part of the Securi-ties and Exchange Commission in regulating that mar-ket, so a separate futures markets agency was created with exclusive jurisdiction over futures.

That came into question with the advent of futures contracts based on equity products, which led to argu-ments about the legality of those products and whether they should be regulated by the CFTC as futures products or by the SEC as equity products. The real watershed event came in 1981, when Phil Johnson and John Shad, the chairmen of the CFTC and the SEC, negotiated what became known as the Shad-Johnson Accord. The SEC was given jurisdiction over options on securities, and the CFTC was given jurisdiction over futures and options on futures. That might look confusing, but it resolved the uncertainty and allowed the industry to move forward. Certainly it would have made it more difficult for the futures exchanges to create so many innovative products if they had been operating under the SEC’s oversight.

Passage of the Commodity Futures Modernization Act in 2000 was another very important regulatory milestone. With this law, our markets were able to grow and innovate while operating under a principles-based approach to regulation. By regulating through core principles rather than prescriptive rules, the CFTC was able to achieve its statutory goals while still giving the industry the flexibility it needed to adjust to changes in the markets and create new products.

The CFMA also provided legal certainty for the swaps market. The more volume that came into the swaps markets, the more the dealers were looking for ways in which to lay off their risk in the futures markets. I think it has been a very complimentary relationship not a competitive one.

FI: How do you think the industry’s voice has been heard in Congress on Dodd-Frank issues?

DAMGARD: It is always hard to have an effective voice in Congress when legislation is being drafted in response to a market crisis. That was the case when Congress began drafting Dodd-Frank. On top of that, there was one party controlling the White House and both the House and Senate.

FI: Just over 10 years ago you faced a very different kind of challenge—the September 11 attacks. The collapse of the World Trade Center buildings struck right at the heart of the futures industry in New York. What role did the FIA take in helping your members and the markets regroup?

DAMGARD: By the time I arrived at work the sec-ond airplane had hit the second tower. It was then that we realized that this was not some little airplane that hit the World Trade Center by accident.

FIA board members meet with President George H.W. Bush in 1990.

DAMGARD: The real question is, what’s prudent and what’s punishment? I think, since 2008, it’s been very good politics to demonize Wall Street and demonize people who are speculating in the market. The truth is that an awful lot of businesses out there depend on these markets for managing risk. I think we’re pretty vulnerable to new exchanges outside the United States operating under less costly regimes attracting the business. We know that markets move.

FI: You’ve been very vocal over the years about the im-pact of imposing position limits. Could you discuss this?

DAMGARD: Position limits have worked pretty well in the ags. The FIA has always been supportive of position reporting. We think it is important for regu-lators to have this information for proper surveillance of the markets, but we do not support the hard limits that have been set by the CFTC.

FI: A transaction tax proposal is again circulating in Congress. More than anyone else, you know this is not a new idea. It’s been proposed in the past by both Republicans and Democrats. Do you think we’ll ever see something like that?

DAMGARD: Other countries have tried it. Brazil tried it. Sweden

Our offices are only a few blocks from the White House, and as I was standing in my office with my staff, we caught a glimpse of the airplane that crashed into the Pentagon.

Our immediate concern was the personal safety of our staff and members. Quite a few of our member firms had offices in the towers. We also reached out almost immediately to the exchanges. The New York Board of Trade’s floor was completely destroyed and the New York Mercantile Exchange was severely damaged. Also the CFTC’s New York office was in one of the tow-ers. So we were very concerned about everyone’s safety.

The first hours we were constantly in contact with those firms and exchanges trying to locate people. Thankfully nearly all of them were able to evacuate the buildings. The folks at Carr and Cantor unfortunately were not able to get out in time, and to this day I can’t think about that day without remembering those who lost their lives in 9-11.

One of the remarkable things about that trag-edy was the way the whole industry came together. Normally the firms are fierce competitors but after 9-11 that was set aside. The firms that were relatively unaffected voluntarily offered to share office space and equipment and access to the exchanges with the firms that were really hit hard by the destruction.

As we have with other market emergencies over the years, the FIA provided a central communications point for the industry. The day after the attacks, we began hosting conference calls for member firms, exchanges and clearing firms. We held more than 25 calls in the six or seven days following the attacks. We also maintained con-tact with other critical industry trade groups to keep each other aware of decisions being made in various markets.

On a personal note, on Oct. 16, about five weeks after the attack, I accompanied Senator Bob Dole on a visit to Ground Zero, where we were joined by Mayor Rudy Giuliani. I was overcome by the devastation. The smoke, the debris, the dust, the sheer scale of the destruction—it was absolutely overwhelming.

FI: What did you learn about our industry after the September 11 attacks?

DAMGARD: I think it’s remarkable that the markets were up and running just days later, that we were more resilient than the stock market, than any number of other industries. There was this pride at the exchange level and among our members. Cooperation among market participants was outstanding. For example, the futures exchanges were willing to synchronize their hours with those of the cash markets during the re-opening process. We also were reminded of the impor-tance of being prepared for disasters. Since 2001 the FIA has worked regularly with exchanges and member firms on disaster recovery and preparedness issues.

FI: There seems to be a tone in Washington that regula-tors can keep pace with innovations in the market. Has that thought ever been as prominent as it is now?

John entertains the audience at

the 2006 FIA Asia Derivatives Conference

in Mumbai, India.

John addresses delegates of the

International Futures Industry Conference in

Boca Raton, FL.

20 Futures Industry | www.futuresindustry.com

tried it. And the first chance they had to rescind it,

they did. They saw how detrimental it

is to the market. I remember saying in testimony one time:

“Tax us on the money we make, but don’t tax us on how we make our

money.” I have concerns about money going to the Treasury with no cap and

no relationship to the cost of the regulation that the fee is suppose to address. I also

have concerns that fees and taxes will be used in an attempt to influence how people trade

and to affect market behavior generally.

FI: Over the years, jurisdiction of the CFTC has always been in the agriculture committees. How has that worked?

DAMGARD: My own view is that the institutional knowledge of these markets resides in the House and Senate Agriculture Committees. And nothing has persuaded me that that should necessarily change.

Ever since I’ve started, I’ve been able to go up to the Hill and visit with members of the Ag Committee such as Senator Lugar and say here’s what really makes sense and here’s what doesn’t make much sense. Very often the members themselves came from a farming background and they understood what it meant to hedge. So they always had a very good understanding of what it takes to draft legislation that strikes the right balance between promoting innovation and protecting the integrity of these markets.

FI: Last fall MF Global, one of the largest FCMs in the business, declared bankruptcy. How would you characterize the impact of that collapse and in particu-lar the shortfall in customer funds on the industry?

DAMGARD: This is the worst black eye that the in-dustry has ever received. The safety of customer money has been one of the sacrosanct principles of this indus-try. The idea that this has been violated is something that is going to take awhile to address and restore.

As tempting as it is to jump right in and say “we’ve got to do this and we’ve got to do that,” let’s not amputate the wrong leg. Let’s figure out what’s wrong with the patient before we decide what we’re going to do. There’s been a cry for moving the regulation function out of the exchanges. But it’s important to re-member that from an exchange standpoint, they want to make sure that the people that they trust to become clearing members of their clearinghouse are, in fact, well capitalized and are working within the rules.

But we’ve been through crises before. We had Vol-ume Investors. We had Sumitomo. We had the Hunt Brothers squeezing the silver market. We had Barings Bank. I think the industry has done a pretty good job over the years of looking at each of those incidents and addressing the causes and fixing the problems.

We’re going to do that again. I don’t know that we can honestly say that there will never be another prob-lem. But I do know that this industry will figure out what went wrong with MF Global and how to prevent that kind of thing from happening again.

FI: Did you expect to run a trade association for more than three decades?

DAMGARD: I’m told that I beat out Jack Valenti in terms of longevity. We’ve probably faced more crises and more uncertainty, as an industry, than perhaps any other trade association in town.

This wasn’t something that I expected to happen. When you study hard at school, you don’t necessarily say, “Boy, I can hardly wait to grow up and run a trade association.” It’s always a little accidental.

In my case, it was having worked in the White House for President Nixon and Vice President Agnew. Both of them went down in flames. I felt like I needed another experience to point to, and I went to the Department of Agriculture under Earl Butz—where I inherited a bunch of programs—one of which was the Commodity Exchange Authority, which of course was the predecessor to the CFTC.

I am very, very grateful to fate that I was selected for this job by John Conheeny in 1982. I’ve had 30 some years to watch the industry grow. All of the work we’ve done here at the FIA over the years could not have happened without the strength and talent of our members. It’s been a great ride. ..............Joanne Morrison is the deputy editor of Futures Industry.

FIA New York Expo May 17, 2012

NY Marriott Marquis1535 Broadway

New York, NY

The Futures Industry Association will hold its fi rst NY Expo on Thursday, May 17 at the New York Marriott Marquis.

One Day. Twelve Sessions. 24 Exhibits. Multiple networking opportunities.

Panel Topics Will Include:

New York Expo Exhibitors (as of February 27)

ADVA Optical Networking • CME Group • GlobalRisk Corporation • NYSE EuronextOrc • TMX | Montréal Exchange • WhenTech LLC • Omgeo LLC • Solarfl are Comminications

www.futuresindustry.org/nyexpo

WorkshopsReporting Requirements/SDRs • Getting Ready For OTC Clearing/Registration • LSOC/Margin & Collateral Risk Audits • Position Limits

Products Interest Rate Swaps • Energy

ClearingClearinghouse Leaders • Customer Protection Post MF Global • Clearing Certainty • Gross Margining Give-Up Best Practices

ExecutionTop Tech Trends • SEF Landscape • Risk Controls for SEFs and CCPs • Risk Management Recom-mendations • IT Challenges of Dodd-Frank

Partners Sponsors

Contact [email protected] for sponsorship and exhibiting opportunities.

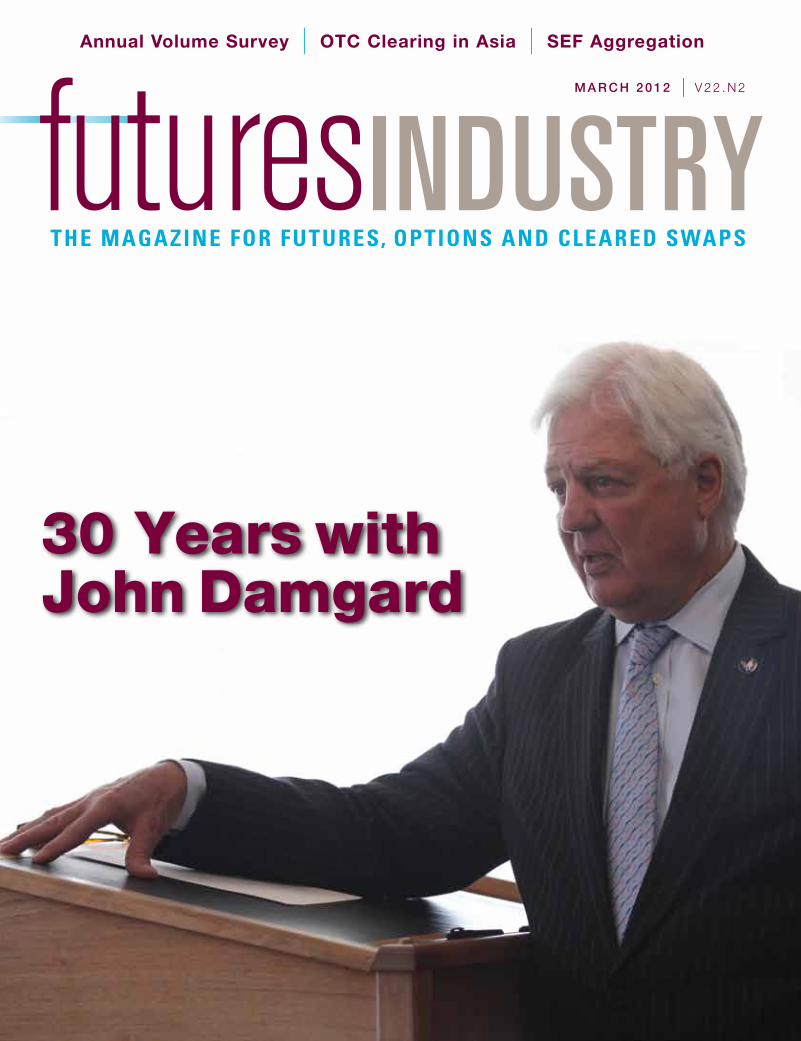

Wednesday May 9, 2012

2:00 – 4:00 p.m.Session 1. Soup to Nuts

4:30 – 6:00 p.m.Session 2. Protection of Customer Funds

6:00 – 7:00 p.m.Opening Reception

Thursday May 10, 2012

CONCURRENT SESSIONS (choice of three panels)

8:30 – 10:00 a.m.Session 3. Looking West and East: The International Implications of Clearing Swaps and Trading Futures Post MF Global

Session 4. An Exchanges and SEF Update

Session 5. “Who, What and Where?” – Product and Entity Defi nitions

10:30 a.m. – noonSession 6. Meet the CFTC Directors – Where We Are Going in 2012Noon – 1:45 p.m.Keynote Lunch

CONCURRENT SESSIONS (choice of three panels)

2:00 – 3:30 p.m.Session 7. Litigation and Enforcement Update

Session 8. The Role of the Compliance Offi cer and Internal Controls in the New World

Session 9. “Sanity Clauses” – Basics in Documentation

CONCURRENT SESSIONS (choice of three panels)

4:00 – 5:30 p.m.Session 10. The Federal Reserve Board – The Industry’s New Regulator

Session 11. Professional Responsibility

Session 12. The Basics of Give Ups and Back Offi ce Operations

7:00 – 9:00 p.m.Reception and Dinner

Friday May 11, 2012

CONCURRENT SESSIONS (choice of three panels)

8:30 – 10:00 a.m.Session 13. “Aggregation, Implementation & Frustration”— Position Limits and Other Developments in Commodities

Session 14. The Clearing of OTC Swaps

Session 15. Basics of Execution Issues(Anti-disruptive Trading and Order Handling)

CONCURRENT SESSIONS (choice of three panels)

10:30 – noonSession 16. The Nuts and Bolts of Reporting and Recordkeeping

Session 17. Asset Management Developments

Session 18. “What Clients and Regulators Want” – Internal and External Business Conduct Standards

Noon – 2:00 p.m.Farewell Networking Box Lunch

Program is subject to change without notice.

www.futuresindustry.org/lc

SPONSORS

SPONSORSHIP OPPORTUNITIESA limited number of sponsorship opportunities are still available.

Contact Toni Vitale Chan at [email protected] or 312.636.2919.

Preliminary Program

FIA Law and Compliance Division Presents:

Conference on the Regulation of Futures, Derivatives and OTC Products

May 9-11, 2012Marriott Waterfront • Baltimore, Maryland

MARRIOTT WATERFRONT • 410.385.3000Located in Baltimore’s Harbor East neighborhood, the Baltimore Marriott Waterfront sits on the water’s edge. You’ll enjoy spectacular views from this Inner Harbor hotel, as well as easy access to the city’s fi nest shopping and restaurants. The hotel is a short drive to and from BWI airport and the Baltimore’s Penn Station.

Rooms have been reserved at special rates and are valid May 8-12. Rates range from $231-281/night and are quoted exclusive of applicable state and local taxes, occupancy, applicable service, and/or other hotel specifi c fees. The room block cut-off date is April 19, 2012. However, rooms are limited and available on a fi rst-come, fi rst-serve basis—they may sell out early! Any rooms available after the deadline will be on a space and rate available basis only. Please confi rm all cancellation policies and forfeiture of deposits directly with the hotel when booking your reservation. Please contact the hotel directly for reservations:

By phone: dial 1.800.266.9432 and mention “2012 Futures Industry Association - Annual Law & Compliance Division Conference” to apply for the group rate.

By internet: visit www.futuresindustry.org/lc and click on “Hotel and Area Information”

REGISTRATIONMembers of the FIA L&C Division 2012**For those who have already renewed their 2012 L&C Membership Through April 19 - $650 l After April 19 - $750Members of the FIA

Through April 19 - $700 l After April 19 - $800Price includes one-year membership in the FIA Law & Compliance Division

Non-Members of the FIA Through April 19 - $850 l After April 19 - $950CANCELLATIONS: Notice of cancellation must be received in writing before April 4 and will be subject to a $100.00 administrative fee. No refunds will be made after April 4. Substitutions may be made at any time without penalty. E-mail [email protected] with changes.

REGISTER AT WWW.FUTURESINDUSTRY.ORG/LC

www.futuresindustry.org/lcwww.futuresindustry.org/lc

Wednesday May 9, 2012

2:00 – 4:00 p.m.Session 1. Soup to Nuts

4:30 – 6:00 p.m.Session 2. Protection of Customer Funds

6:00 – 7:00 p.m.Opening Reception

Thursday May 10, 2012

CONCURRENT SESSIONS (choice of three panels)

8:30 – 10:00 a.m.Session 3. Looking West and East: The International Implications of Clearing Swaps and Trading Futures Post MF Global

Session 4. An Exchanges and SEF Update

Session 5. “Who, What and Where?” – Product and Entity Defi nitions

10:30 a.m. – noonSession 6. Meet the CFTC Directors – Where We Are Going in 2012Noon – 1:45 p.m.Keynote Lunch

CONCURRENT SESSIONS (choice of three panels)

2:00 – 3:30 p.m.Session 7. Litigation and Enforcement Update

Session 8. The Role of the Compliance Offi cer and Internal Controls in the New World

Session 9. “Sanity Clauses” – Basics in Documentation

CONCURRENT SESSIONS (choice of three panels)

4:00 – 5:30 p.m.Session 10. The Federal Reserve Board – The Industry’s New Regulator

Session 11. Professional Responsibility

Session 12. The Basics of Give Ups and Back Offi ce Operations

7:00 – 9:00 p.m.Reception and Dinner

Friday May 11, 2012

CONCURRENT SESSIONS (choice of three panels)

8:30 – 10:00 a.m.Session 13. “Aggregation, Implementation & Frustration”— Position Limits and Other Developments in Commodities

Session 14. The Clearing of OTC Swaps

Session 15. Basics of Execution Issues(Anti-disruptive Trading and Order Handling)

CONCURRENT SESSIONS (choice of three panels)

10:30 – noonSession 16. The Nuts and Bolts of Reporting and Recordkeeping

Session 17. Asset Management Developments

Session 18. “What Clients and Regulators Want” – Internal and External Business Conduct Standards

Noon – 2:00 p.m.Farewell Networking Box Lunch

Program is subject to change without notice.

www.futuresindustry.org/lc

SPONSORS

SPONSORSHIP OPPORTUNITIESA limited number of sponsorship opportunities are still available.

Contact Toni Vitale Chan at [email protected] or 312.636.2919.

Preliminary Program

FIA Law and Compliance Division Presents:

Conference on the Regulation of Futures, Derivatives and OTC Products

May 9-11, 2012Marriott Waterfront • Baltimore, Maryland

MARRIOTT WATERFRONT • 410.385.3000Located in Baltimore’s Harbor East neighborhood, the Baltimore Marriott Waterfront sits on the water’s edge. You’ll enjoy spectacular views from this Inner Harbor hotel, as well as easy access to the city’s fi nest shopping and restaurants. The hotel is a short drive to and from BWI airport and the Baltimore’s Penn Station.

Rooms have been reserved at special rates and are valid May 8-12. Rates range from $231-281/night and are quoted exclusive of applicable state and local taxes, occupancy, applicable service, and/or other hotel specifi c fees. The room block cut-off date is April 19, 2012. However, rooms are limited and available on a fi rst-come, fi rst-serve basis—they may sell out early! Any rooms available after the deadline will be on a space and rate available basis only. Please confi rm all cancellation policies and forfeiture of deposits directly with the hotel when booking your reservation. Please contact the hotel directly for reservations:

By phone: dial 1.800.266.9432 and mention “2012 Futures Industry Association - Annual Law & Compliance Division Conference” to apply for the group rate.

By internet: visit www.futuresindustry.org/lc and click on “Hotel and Area Information”

REGISTRATIONMembers of the FIA L&C Division 2012**For those who have already renewed their 2012 L&C Membership Through April 19 - $650 l After April 19 - $750Members of the FIA

Through April 19 - $700 l After April 19 - $800Price includes one-year membership in the FIA Law & Compliance Division

Non-Members of the FIA Through April 19 - $850 l After April 19 - $950CANCELLATIONS: Notice of cancellation must be received in writing before April 4 and will be subject to a $100.00 administrative fee. No refunds will be made after April 4. Substitutions may be made at any time without penalty. E-mail [email protected] with changes.

REGISTER AT WWW.FUTURESINDUSTRY.ORG/LC

www.futuresindustry.org/lcwww.futuresindustry.org/lc

24 Futures Industry | www.futuresindustry.com

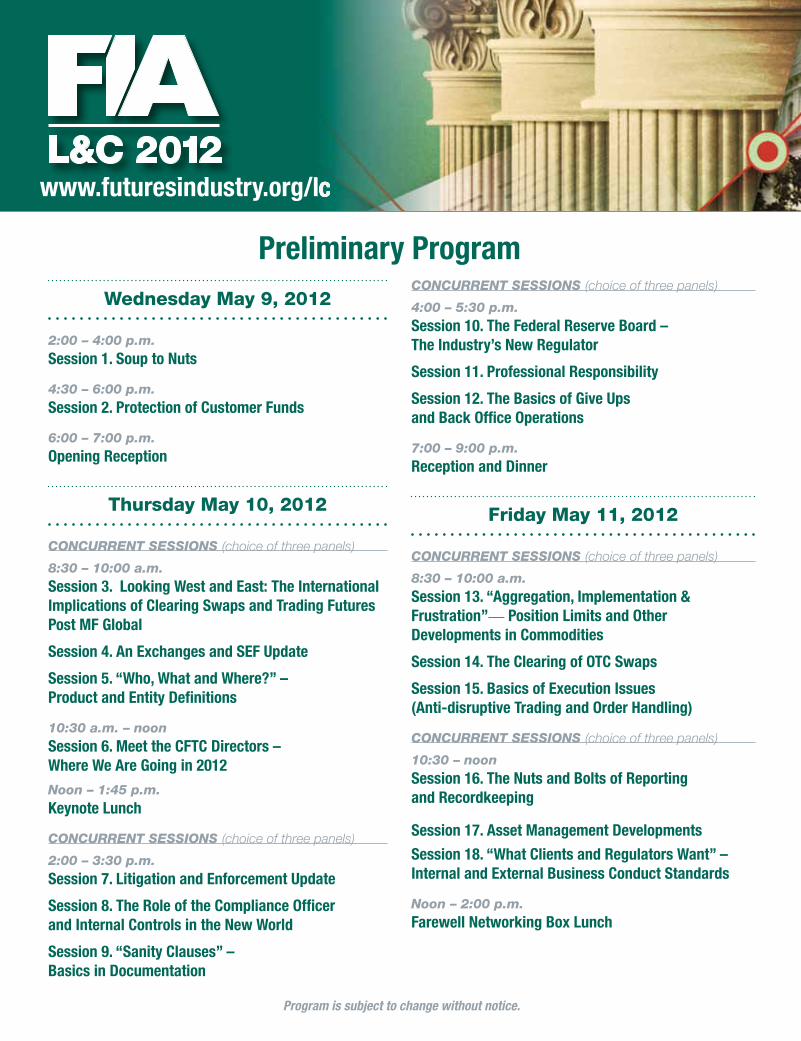

2011 was not a year when the trading of futures and options around the world was characterized by

one big theme, such as the rise of emerging markets or a boom in commodities trading. Instead it was

a year of many smaller trends. Some of those trends were a continuation of what we saw emerge in

previous years, such as the recovery of the fixed income markets from the credit crisis of 2008. Others

came as a surprise, such as the substantial decline in some of China’s largest commodity markets.

Annual Volume Survey Volume Climbs 11.4% to 25 Billion Contracts WorldwideBy Will Acworth

24 Futures Industry | www.futuresindustry.com

Global Futures and Options VolumeBased on the number of contracts traded and/or cleared at 81 exchanges worldwide

2010 2011 % Change

Futures 12,049,275,638 12,945,211,880 7.4%