Embed Size (px)

Citation preview

30th April 2014

“This third annual event will demonstrate, by way of case examples, how developments in Analytics are leading to increased competitive advantage”

Behavioural, Social, Unstructured Data

Digital “Fingerprint”

On-line behaviour

• Zoral AI/ML software research and development

• 150 staff, established 2004

• Advanced predictive analytics

• Unstructured/behavioural/social data

• Finance sector

• Risk

• Clients - Consumer/SME, Insurance/Credit Products

• STP, e-commerce

• High level of automation

• High volume

• Pioneer

• North America, Europe, Australasia, Africa

Context – what we do

• Lending/insuring online

• Unknown customers (Consumer/SME)

• Challenging markets

• Small to large

• Existing platforms

• Sales/marketing

• Underwriting

• Collections

• Compliance

Context – what our clients do

• Which leads?

• Which channels?

• Customer/Product routing/conversion

• Acceptance/Default

• Fraud

• Collections

• “Their” behaviour/Client behaviour

• Renewals

• Affordability

• Marketing

Context – what our clients need to know

STP

Automated

The problem

“Conventional” credit bureau and application data is highly useful, essential, but not enough to meet the “needs”

The questions

If we add behavioural, social, unstructured dataInto the mix…

• Does it help?• How much?• What are the issues?

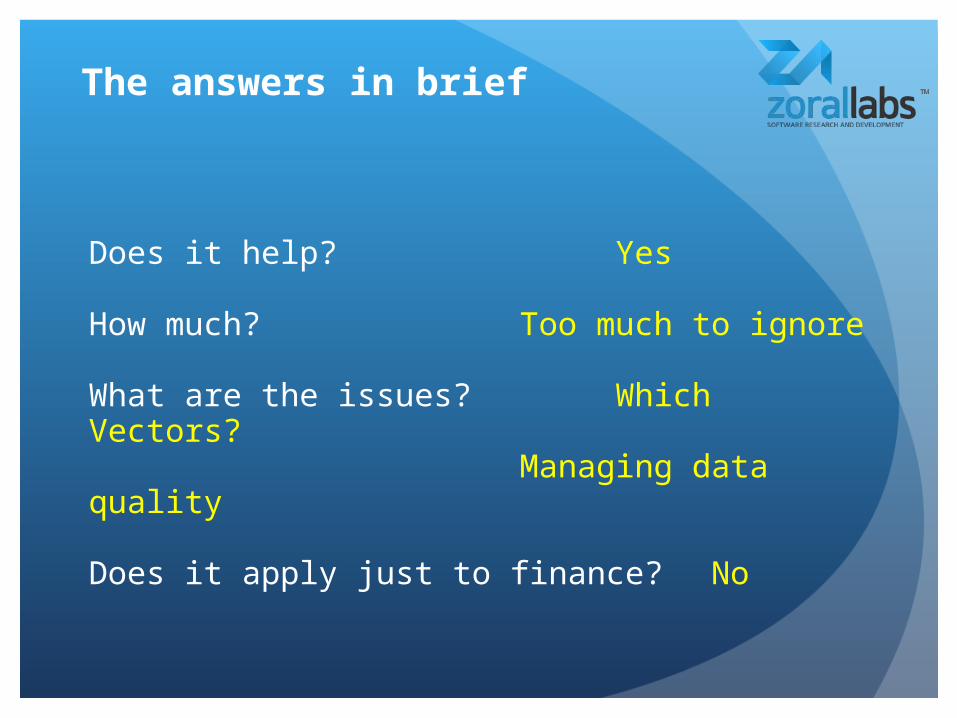

The answers in brief

Does it help? Yes

How much? Too much to ignore

What are the issues? Which Vectors?

Managing data quality

Does it apply just to finance? No

What do we mean by behavioural and social data?

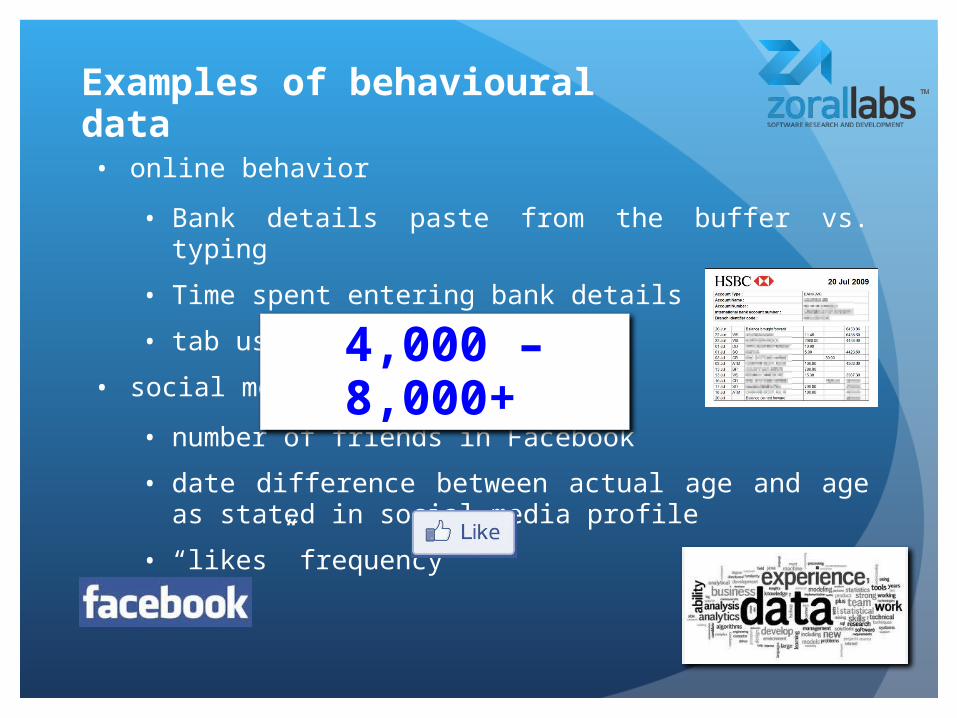

• online behavior

• Bank details paste from the buffer vs. typing

• Time spent entering bank details

• tab usage vs. mouse usage

• social media

• number of friends in Facebook

• date difference between actual age and age as stated in social media profile

• “likes” frequency

Examples of behavioural data

4,000 – 8,000+

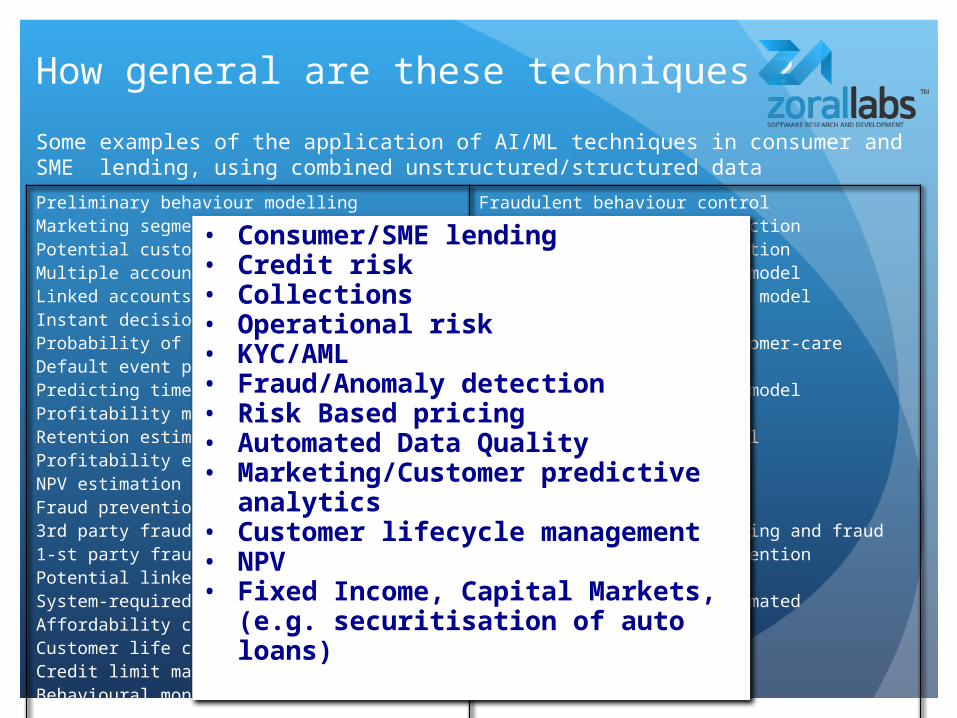

How general are these techniques ?

Preliminary behaviour modellingMarketing segmentationPotential customer-value modelMultiple accounts discovery modelLinked accounts discovery modelInstant decision customer-based modelsProbability of defaultDefault event predictionPredicting time of defaultProfitability modelRetention estimationProfitability estimationNPV estimationFraud prevention3rd party fraud detection1-st party fraud detectionPotential linked fraud estimationSystem-required verificationAffordability control modelCustomer life cycle management systemCredit limit managementBehavioural monitoringFraudulence monitoringCollateral Valuation

Fraudulent behaviour controlCollectability event predictionCollectability time predictionContactability estimation modelMethods for contactability modelCollection schedule modelRetention control and customer-care modelsIndividual retention plan modelIndividual pricing modelAffordability control modelSystem health monitoringData quality controlData quality monitoringOperational errors monitoring and fraudAnomaly detection and preventionModel quality monitoringModel quality control/automated retrainingMarketing modelsCost optimisation moduleBudgeting moduleProvisioning module Using Neural Nets, SVM, Bayes, decision trees, Markov Chains, random forest, genetic algorithms, survival analysis, anomaly detection, etc.

Some examples of the application of AI/ML techniques in consumer and SME lending, using combined unstructured/structured data

• Consumer/SME lending• Credit risk• Collections• Operational risk• KYC/AML• Fraud/Anomaly detection• Risk Based pricing• Automated Data Quality• Marketing/Customer predictive

analytics• Customer lifecycle management• NPV• Fixed Income, Capital Markets, (e.g.

securitisation of auto loans)

An example of how this is used

Client context/issues

• Large consumer/SME on-line finance

• Conventional LMS, underwriting platform, scoring

• Advanced identity verification

• Manual/scaling issues

• Fraud/Default

• 1st party, 3rd party

• Low volume of known negative samples

• Mobile

• Wide country/sector variation

• Rapidly changing environment, frequent model update

Consumer and SME lending example

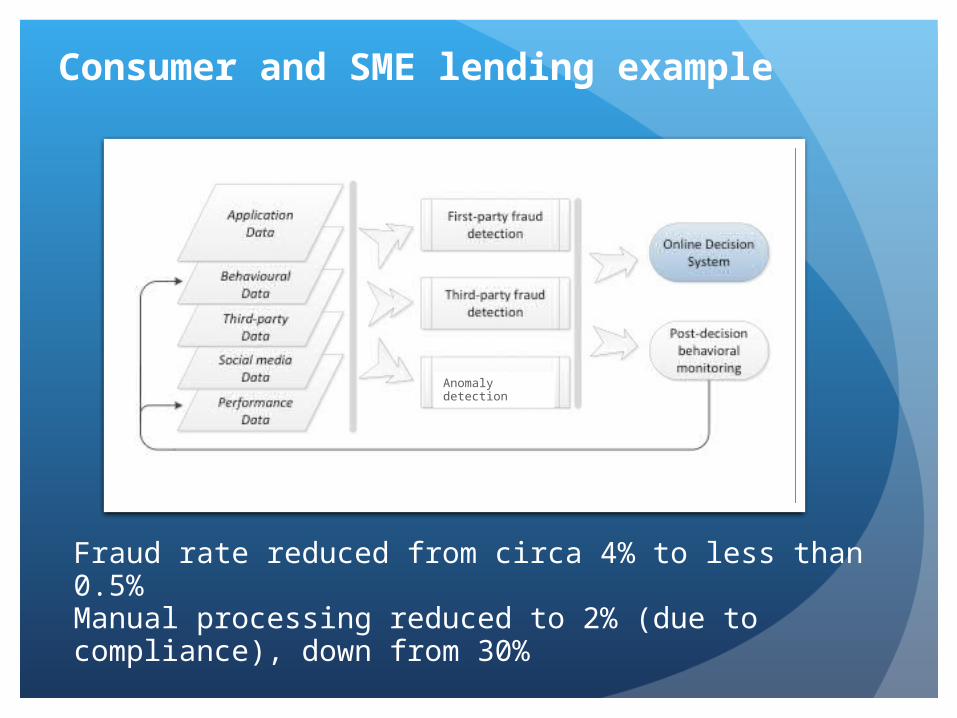

Fraud rate reduced from circa 4% to less than 0.5%Manual processing reduced to 2% (due to compliance), down from 30%

Anomaly detection

Consumer and SME lending example

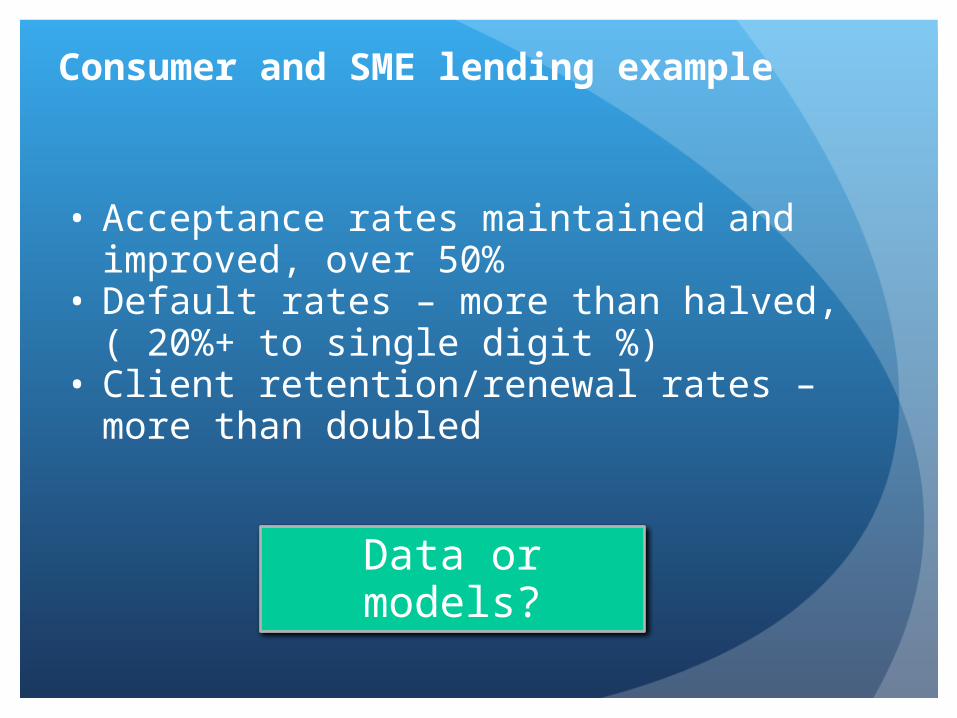

• Acceptance rates maintained and improved, over 50%

• Default rates – more than halved, ( 20%+ to single digit %)

• Client retention/renewal rates – more than doubled

Consumer and SME lending example

Data or models?

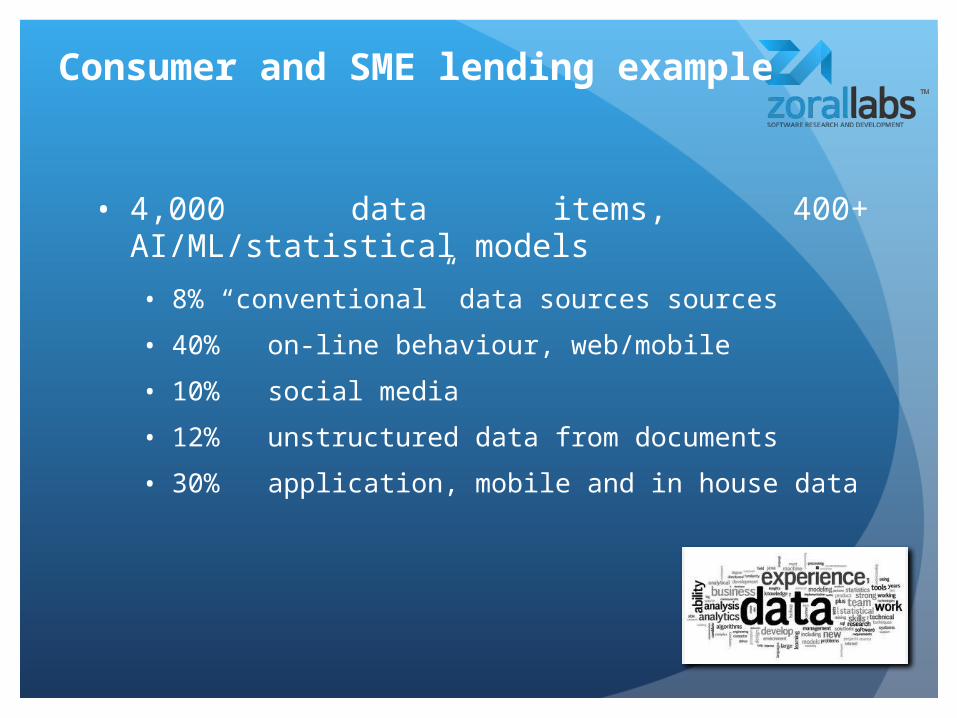

• 4,000 data items, 400+ AI/ML/statistical models

• 8% “conventional” data sources sources

• 40% on-line behaviour, web/mobile

• 10% social media

• 12% unstructured data from documents

• 30% application, mobile and in house data

Consumer and SME lending example

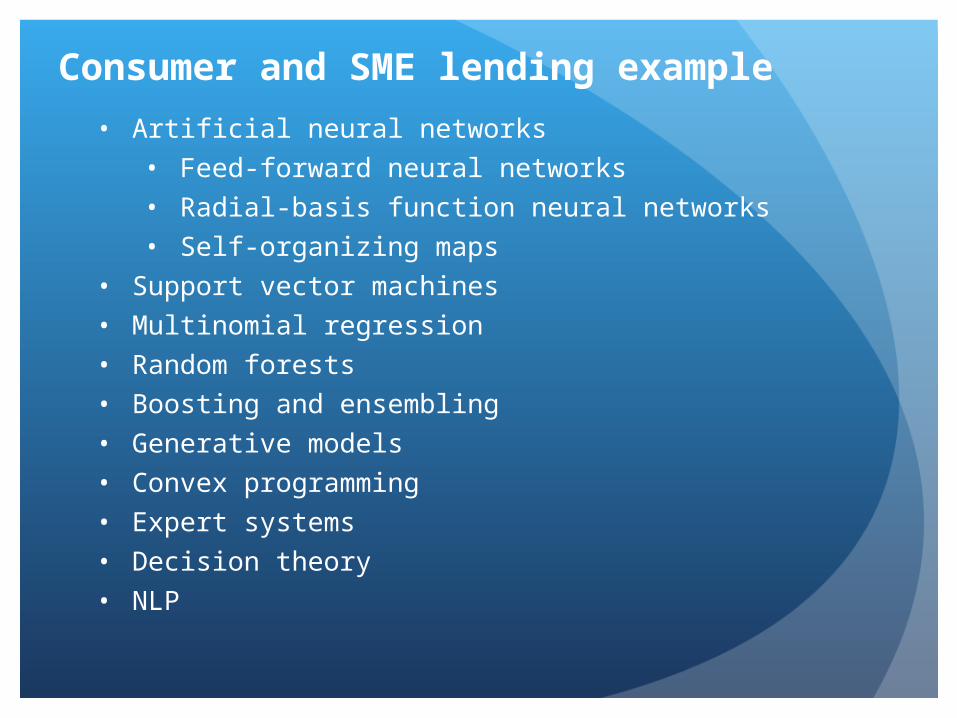

• Artificial neural networks• Feed-forward neural networks• Radial-basis function neural networks• Self-organizing maps

• Support vector machines• Multinomial regression• Random forests• Boosting and ensembling• Generative models• Convex programming• Expert systems• Decision theory• NLP

Consumer and SME lending example

• Data, data and data

• Which vectors are predictive and when?

• Quality, unstructured, “alternative” sources

• How do you measure the quality?

• Quality variability, automated control

• Data dimensionality

• Combined

• Structuring unstructured data

• Sourcing - fragmented, “young”, emerging

What are the issues?

More examples

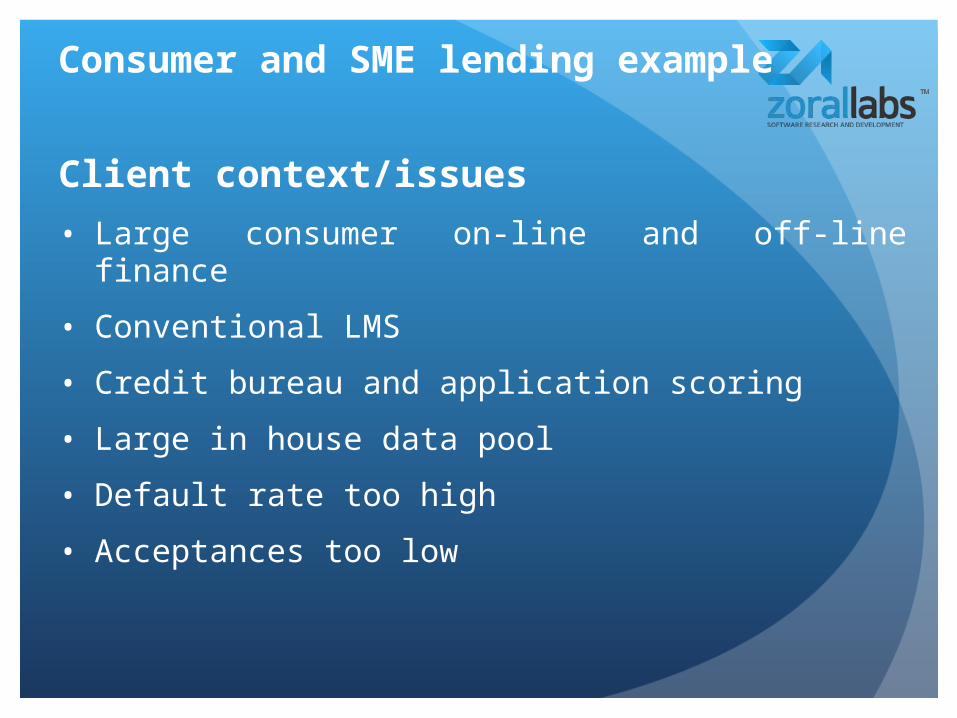

Client context/issues

• Large consumer on-line and off-line finance

• Conventional LMS

• Credit bureau and application scoring

• Large in house data pool

• Default rate too high

• Acceptances too low

Consumer and SME lending example

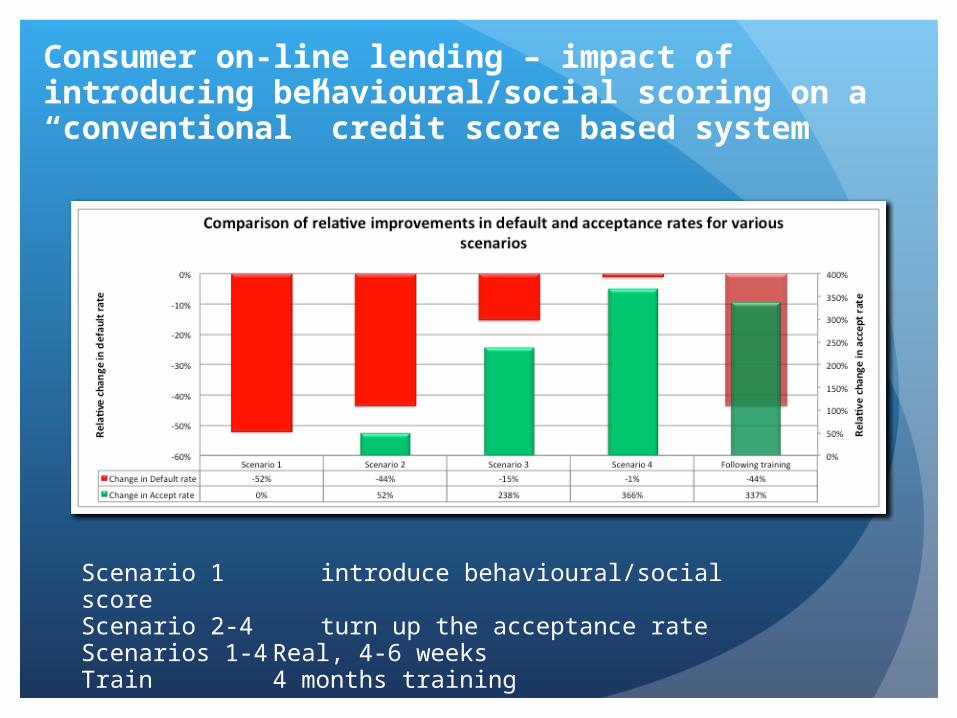

Consumer on-line lending – impact of introducing behavioural/social scoring on a “conventional” credit score based system

Scenario 1 introduce behavioural/social scoreScenario 2-4 turn up the acceptance rateScenarios 1-4 Real, 4-6 weeksTrain 4 months training

1-100 100-200 200-300 300-400 400-500 500-600 600-700 700-800 800-900 900-10000.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

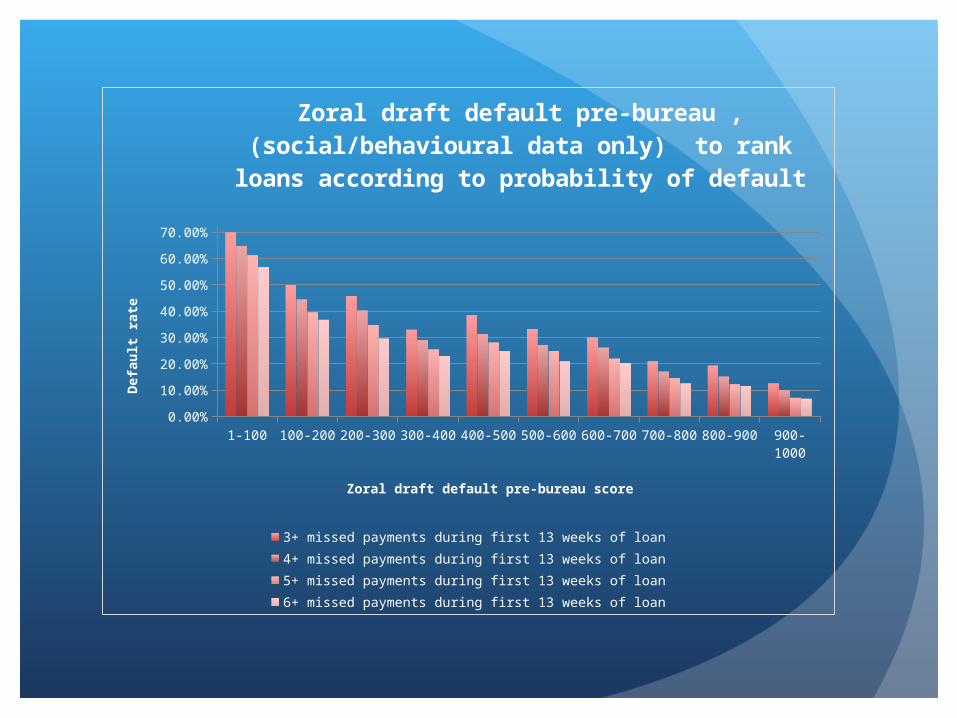

Zoral draft default pre-bureau , (social/behavioural data only) to rank loans according to probability of default

3+ missed payments during first 13 weeks of loan 4+ missed payments during first 13 weeks of loan5+ missed payments during first 13 weeks of loan 6+ missed payments during first 13 weeks of loan

Zoral draft default pre-bureau score

Defa

ult r

ate

8.11.10

1-100 100-200 200-300 300-400 400-500 500-600 600-700 700-800 800-900 900-10000.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

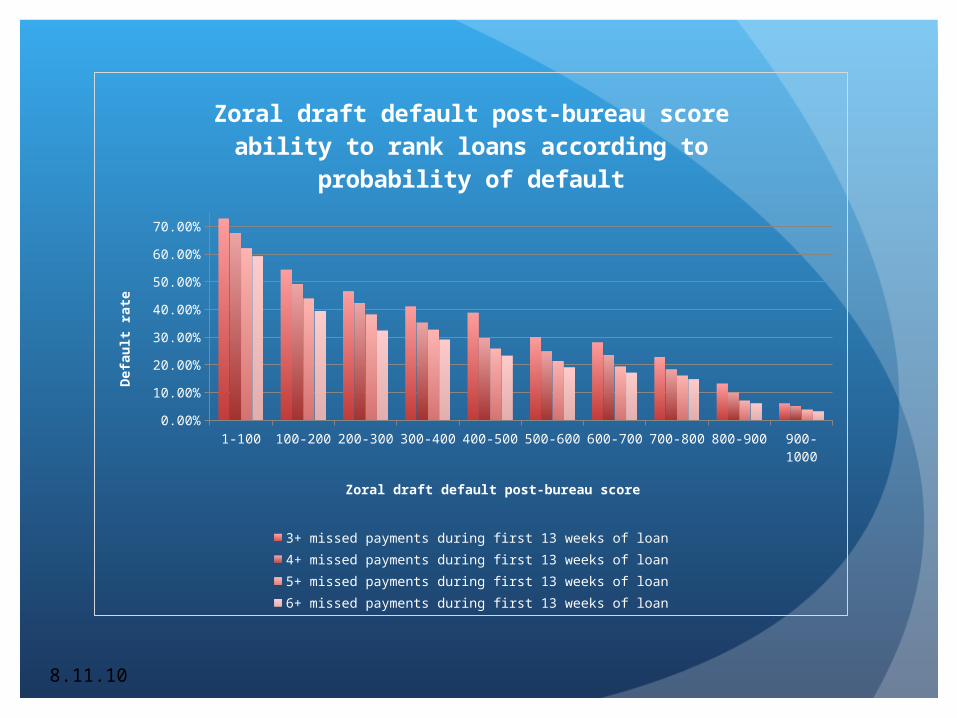

Zoral draft default post-bureau score ability to rank loans according to probability of default

3+ missed payments during first 13 weeks of loan 4+ missed payments during first 13 weeks of loan5+ missed payments during first 13 weeks of loan 6+ missed payments during first 13 weeks of loan

Zoral draft default post-bureau score

Defa

ult r

ate

This is OK for consumers, but what about companies?

• Companies generate predictive data

• Typical sources

• Where else?

What about companies?

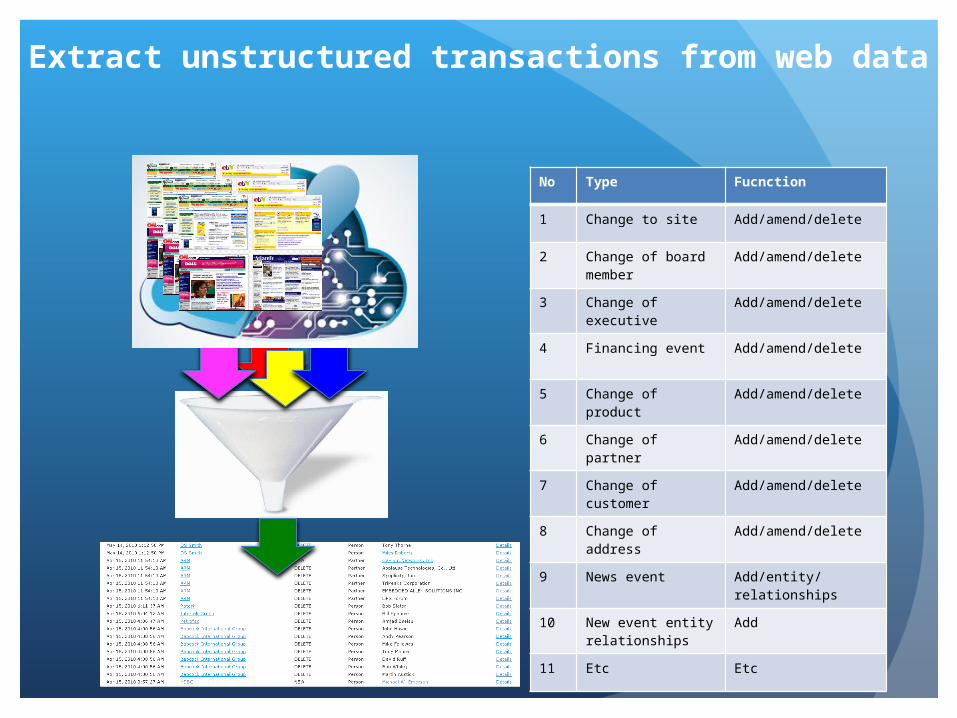

No Type Fucnction

1 Change to site Add/amend/delete

2 Change of board member

Add/amend/delete

3 Change of executive

Add/amend/delete

4 Financing event Add/amend/delete

5 Change of product Add/amend/delete

6 Change of partner Add/amend/delete

7 Change of customer

Add/amend/delete

8 Change of address Add/amend/delete

9 News event Add/entity/relationships

10 New event entity relationships

Add

11 Etc Etc

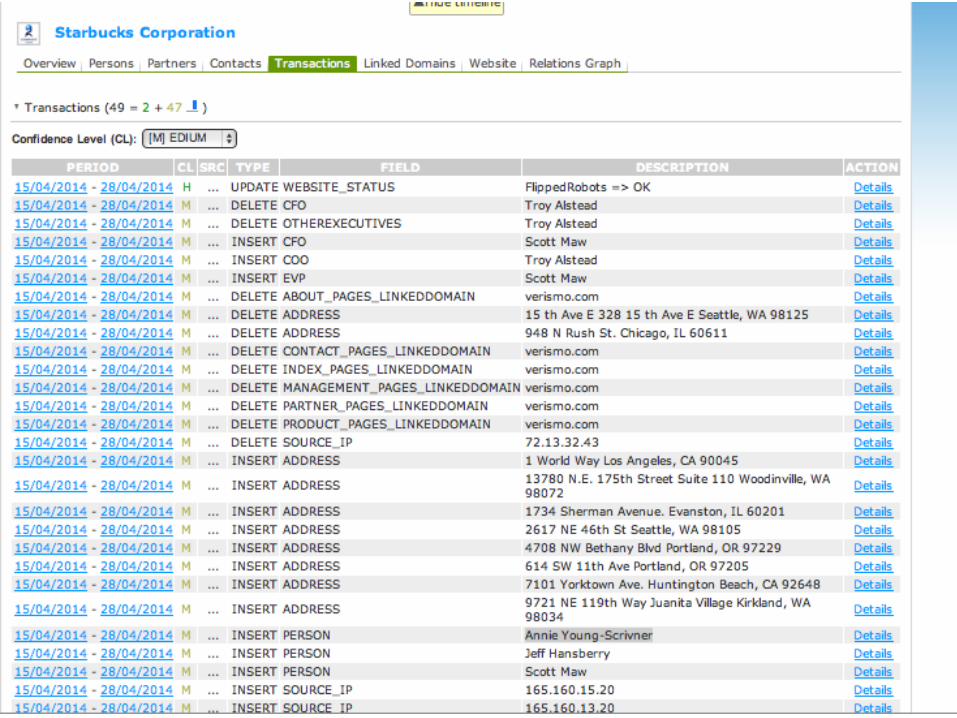

Extract unstructured transactions from web data

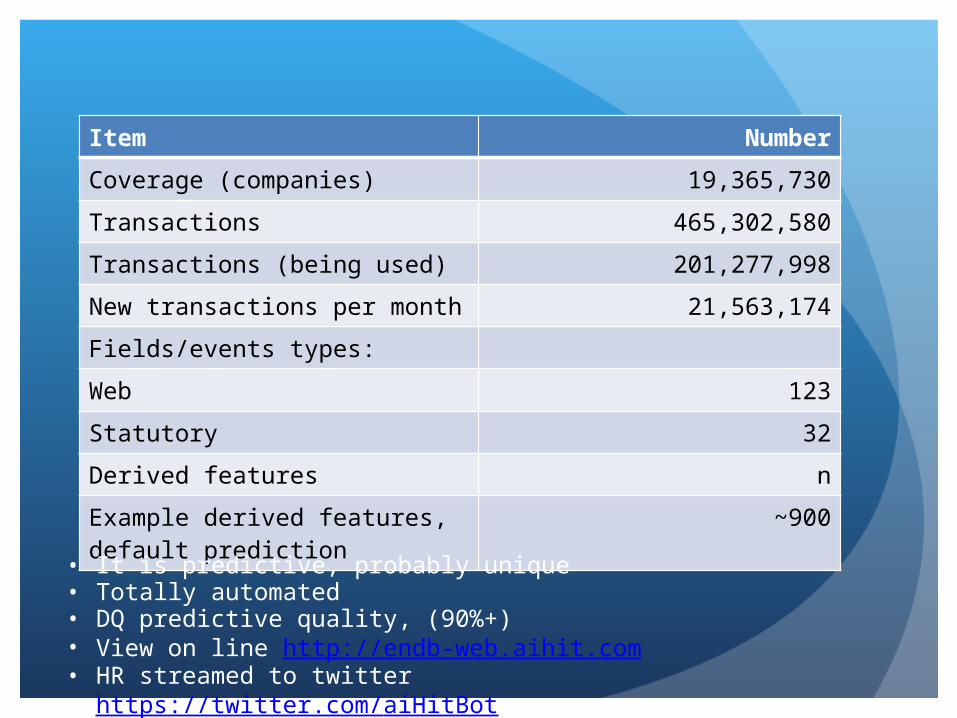

Item Number

Coverage (companies) 19,365,730

Transactions 465,302,580

Transactions (being used) 201,277,998

New transactions per month 21,563,174

Fields/events types:

Web 123

Statutory 32

Derived features n

Example derived features, default prediction

~900

• It is predictive, probably unique• Totally automated• DQ predictive quality, (90%+)• View on line http://endb-web.aihit.com• HR streamed to twitter https://twitter.com/aiHitBot

8.11.10

Mgmt Reshuffle

Changes to Partners

Board/Mgmt Reshuffle

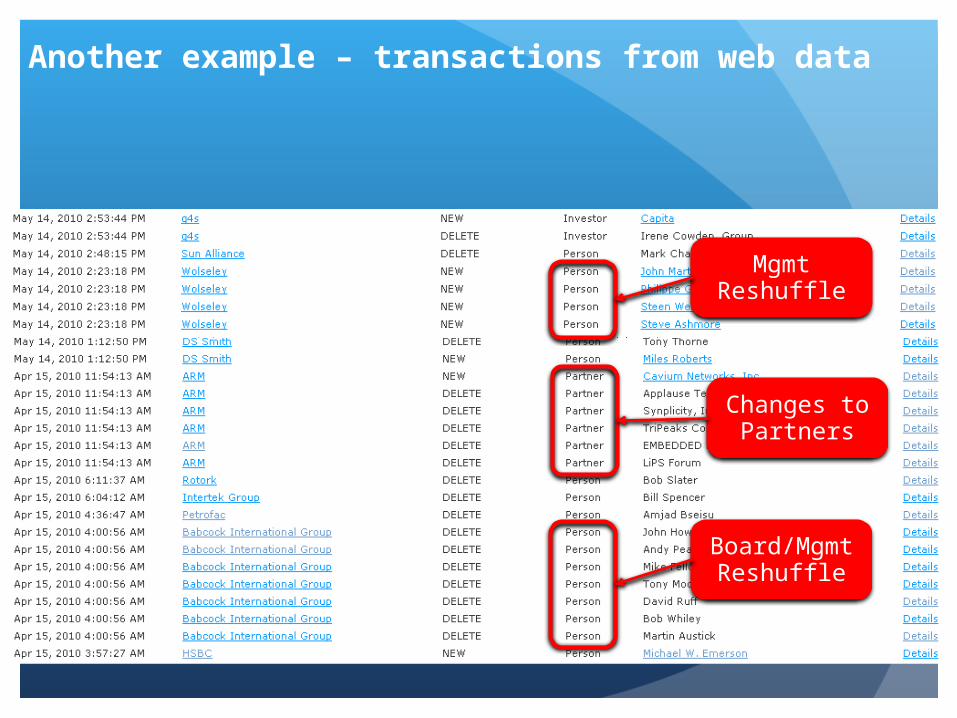

Another example – transactions from web data

they’re not in Google, they’re not in the news…

Board only,Mgmt Reshuffle not

mentioned

• Is it true? - Yes

• What are the issues? – complex but surmountable

• What are the improvement metrics? – various, but in a number of cases, significant and justifiable

• How “general” are these approaches? – reasonably wide, becoming more generalised

• Applicability? (e.g. marketing, applications, customer interaction, collections, fraud etc.) – applicable to most facets of financial product sales

“By capturing, understanding and using behavioural data for predictive modeling we can:

• lower the cost and improve trading metrics, and

• gain additional insight into our clients’ behaviour and predictability

1. Are you using behavioural data to model, predict, optimise each step of the marketing/sales/customer lifecycle?

2. How much?

3. Could you use more?

4. What is the quality? How is measured?

5. How much better could your results be if 1-4 are optimised?

6. How much more could you automate operations using the techniques discussed today?

7. How does your organisation compare to market norms and best practice in this area?

8. What would it add to the “bottom line” if behavioural data modeling were applied to each, applicable area of your business?

9. Where to start?

Now what?

Good news