Embed Size (px)

Citation preview

Waikato Regional Retail Study/ pg 92 of 185

Speer & Starr Consulting March 2009

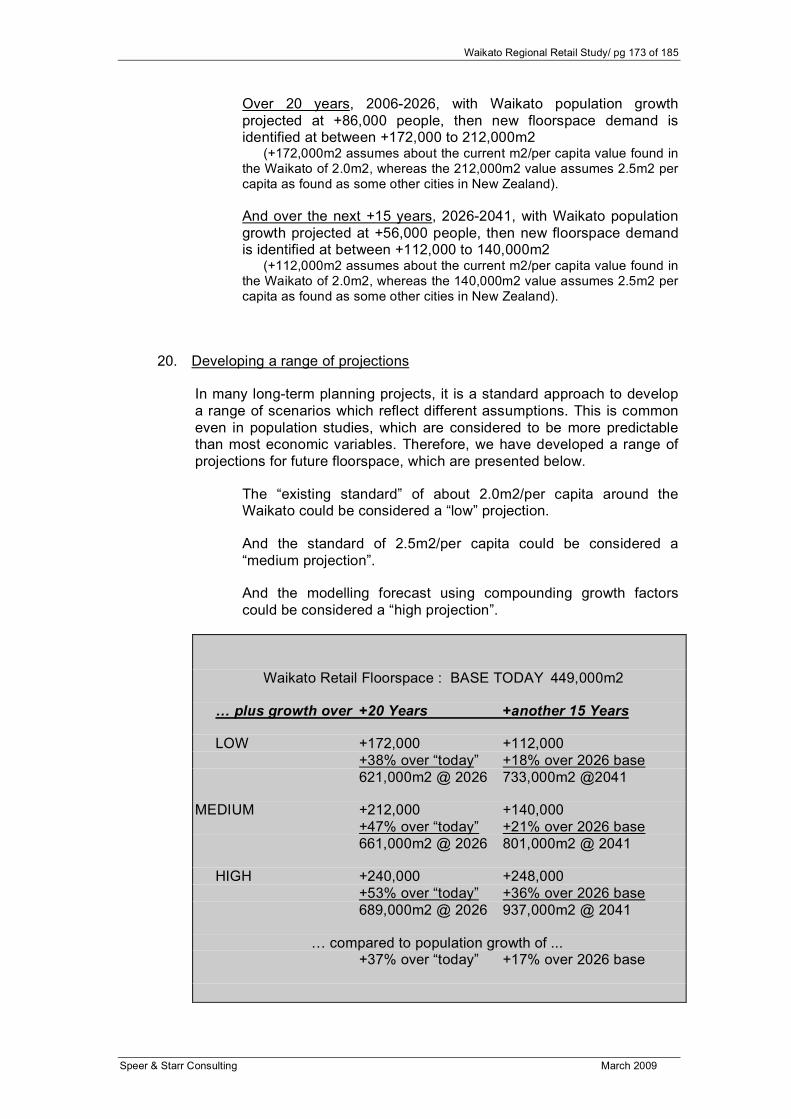

3. Future Growth Demand Issues There are four key issues that will drive future retail growth demand, and these are investigated as follows:

1. Population Growth 2. “Dairying is the Waikato” – a key local economic factor 3. Hamilton is the Employment Hub for the Region 4. “Real” Income and Retail Sales Growth Factor

1. Population Growth The Waikato Region is a major growth sector within New Zealand. Across the study area, growth over the past ten years has been: 1996 / 2001 2001 / 2006 • Hamilton City + 6,471 / +5.9% +13,000 /+11.1% • Waikato District + 717 / +1.8% + 4,100 /+10.3% • Waipa District + 1,464 / + 3.9% + 3,530 /+ 9.1% • Morrinsville Area + 261 / + 3.1% + 435 /+ 4.7% + 8,913 +21,065 /+10.0% VS • Auckland Region + 90,000 / +8.4% +145,000 / +12.4% • National Growth +118,900 / +3.3% +296,150 / + 7.8% Obviously, growth in Hamilton City is the dominant driver to growth in the Region, where growth rates are more akin to the strong Auckland experience. Population growth is significant to retail growth. More people require more food and clothing and other personal goods and services; more households require more appliances and hardware and furniture, etc. Following is a discussion about potential growth in the Study Region, including identification of where the strongest growth sectors are. We have adopted future population projections as prepared by University of Waikato – Population Studies Department, October 2008, for all sectors of the Region. (a) Hamilton City growth In short, it would be fair to describe the future population growth expectations for Hamilton City as strong, in keeping with strong growth that has actually occurred over the past several years. For example, during the 2001 – 2006 period, Hamilton growth levels were quite strong compared to other areas around New Zealand. At over 11% growth over this 5-year period – over 2% per annum, this is a significant growth rate for Hamilton City. Importantly, a steady level of strong growth is expected to continue. This has significant implications for providing new retail activities that can meet this growth demand.

Waikato Regional Retail Study/ pg 93 of 185

Speer & Starr Consulting March 2009

Relative to other major urban centres around the country, the Hamilton growth experience is more comparable to the experience of a major growth area like Auckland, as illustrated in the following table.

Recent Population Growth Experience

Population Growth @ 2006 2001 – 2006 Manukau City 330,000 +46,600 / +16.4% Auckland City 420,000 +40,000 / +10.5% Christchurch City 360,000 +26,700 / + 8.3% North Shore City 207,000 +22,300 / +12.1% Wellington City 183,500 +16,300 / + 9.7% Waitakere City 184,000 +15,000 / + 8.9% HAMILTON CITY 134,400 +13,000 / +11.1% Tauranga District 105,000 +12,900 / +14.0% Rodney District 90,000 +12,300 / +14.0% Nelson/Tasman 93,000 + 4,500 / + 5.1% Dunedin 122,000 + 4,200 / + 3.5% Hastings 72,000 + 3,600 / + 5.3% Kapiti District 46,000 + 3,500 / + 8.2% Palmerston North 76,000 + 2,700 / + 3.7% New Plymouth 69,000 + 2,500 / + 3.7% Napier 57,000 + 2,000 / + 3.6% Lower Hutt City 97,000 + 1,700 / + 1.8% NATIONALLY 4,116,000 +296,150 / + 7.8% A key question is : how much growth can be expected in the future? According to work undertaken by University of Waikato – Population Studies Department (October 2008), and adopting the “medium projection plus EDA [economic development initiatives]”, a 20-year growth expectation for the City is as follows : Population Household Average Growth Growth Persons/dwelling • Base at 2006 134,400 47,550 2.83 • 2006 – 2011 : +12,200 +3,620 3.37 • 2011 – 2016 : +13,000 +4,540 2.86 • 2016 – 2021 : +13,800 +5,290 2.61 • 2021 – 2026 : +12,500 +5,490 2.27 Total Growth : +51,500 +18,940 av.2.72 . . . over 20 yrs . . . Gross Average: +2,575 p.a. + 947 p.a. Total at 2026 : 185,900 66,490

Waikato Regional Retail Study/ pg 94 of 185

Speer & Starr Consulting March 2009

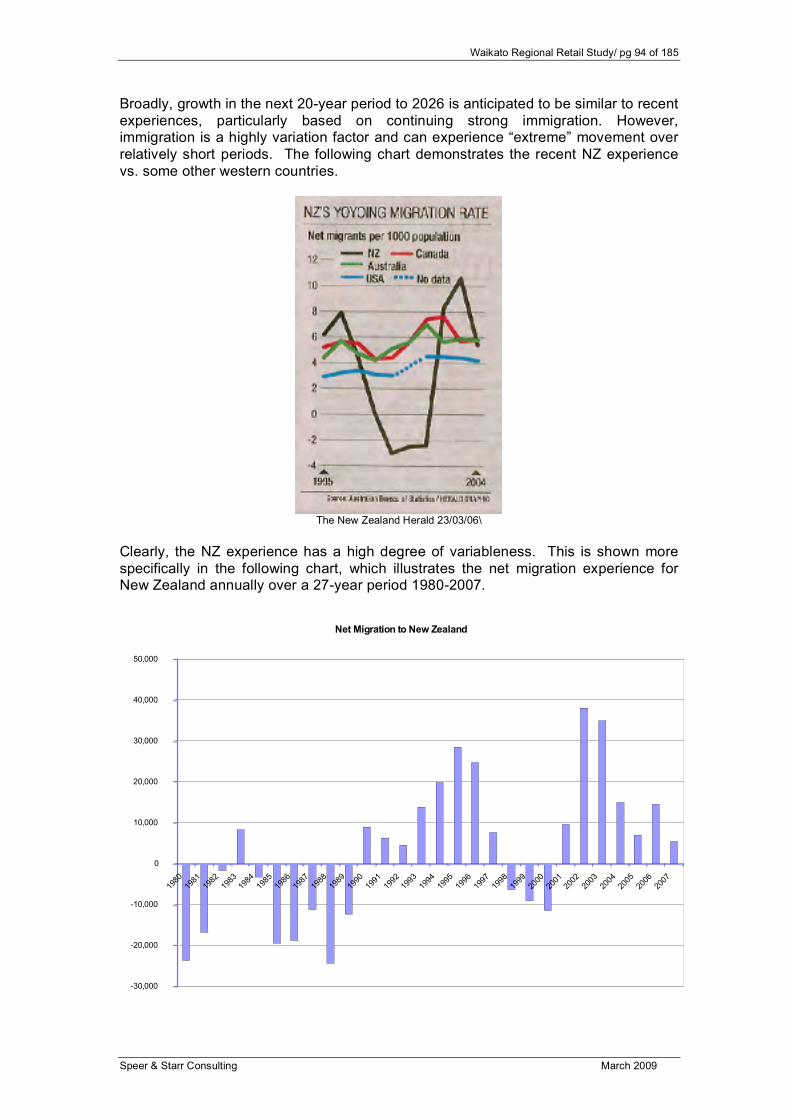

Broadly, growth in the next 20-year period to 2026 is anticipated to be similar to recent experiences, particularly based on continuing strong immigration. However, immigration is a highly variation factor and can experience “extreme” movement over relatively short periods. The following chart demonstrates the recent NZ experience vs. some other western countries.

The New Zealand Herald 23/03/06\

Clearly, the NZ experience has a high degree of variableness. This is shown more specifically in the following chart, which illustrates the net migration experience for New Zealand annually over a 27-year period 1980-2007.

Net Migration to New Zealand

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

40,000

50,000

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Waikato Regional Retail Study/ pg 95 of 185

Speer & Starr Consulting March 2009

The NZ migration experience has “bounced” from positive growth to negative growth several times over this timeframe, with the current experience as at March 2008 nearing “zero” once again. Arrivals in absolute numbers are currently high, nearby double the level of the 1980’s, but departures are also very high, leading to little net gain. The Trans-Tasman movement of labour to/from Australia is the main driver of such variation. Currently, the Australian economy is performing well in international terms; employment is tight, thus wage rates are high. The same scenario broadly applies to NZ currently, but the Australian wage rate is much higher than NZ wages. Hence, the labour attraction to Australia is strong and the current outflow of “Kiwis” reflect this. Accordingly, Hamilton growth in the near future might not achieve the actual levels of growth forecast. But given the wide variableness to immigration, over a 20-year period the total suggested city growth levels are reasonable guidelines to assist other planning work, such as retail demand. A follow-on question to how much growth is expected is : where is growth likely to occur ? For example, during the 5-year period 1996-2001: - growth of +6,500 was experienced across the city, of which . . . - over 60% of city growth occurred in the northeast at Rototuna (+4,000) - and another 30% occurred in the general Western Suburbs (+2,000) . . . while between 2001-2006 . . . - growth of +13,000 was experienced across the city, of which . . . - about 45% of city growth occurred in the northeast at Rototuna (+6,000) - with the rest of growth primarily focused in: • 15% in the general Western Suburbs (+2,000) • 15% in the southeast suburbs around University/Hillcrest (+2000) • 10% in the central city suburbs (+1,300) • 15% scattered elsewhere around the city Obviously, the northeast / Rototuna area has been a very significant growth sector, accounting for at least half of all city growth. Over the last 10-year period, total city growth of almost +20,000 occurred (a gross average of 2,000/p.a.), of which 10,500 occurred in the northeast of Rototuna. Into the future, the next 20-year period has projected growth similar to or slightly greater than the growth experience over the past 5 years – around +2,500 p.a. And, where this will occur is defined by the City’s growth strategy: • New Growth cells at the City fringe: • continuation of growth in the northeast, at Rototuna, = +15,100 • opening a new growth cell in the northwest, at Rotokauri, stage 1 = + 4,350 • opening a new growth cell in the southwest, at Peacocke,stage1 = + 5,700 25,150 • Growth through infill development elsewhere around the City 26,350 Total = +51,500

Waikato Regional Retail Study/ pg 96 of 185

Speer & Starr Consulting March 2009

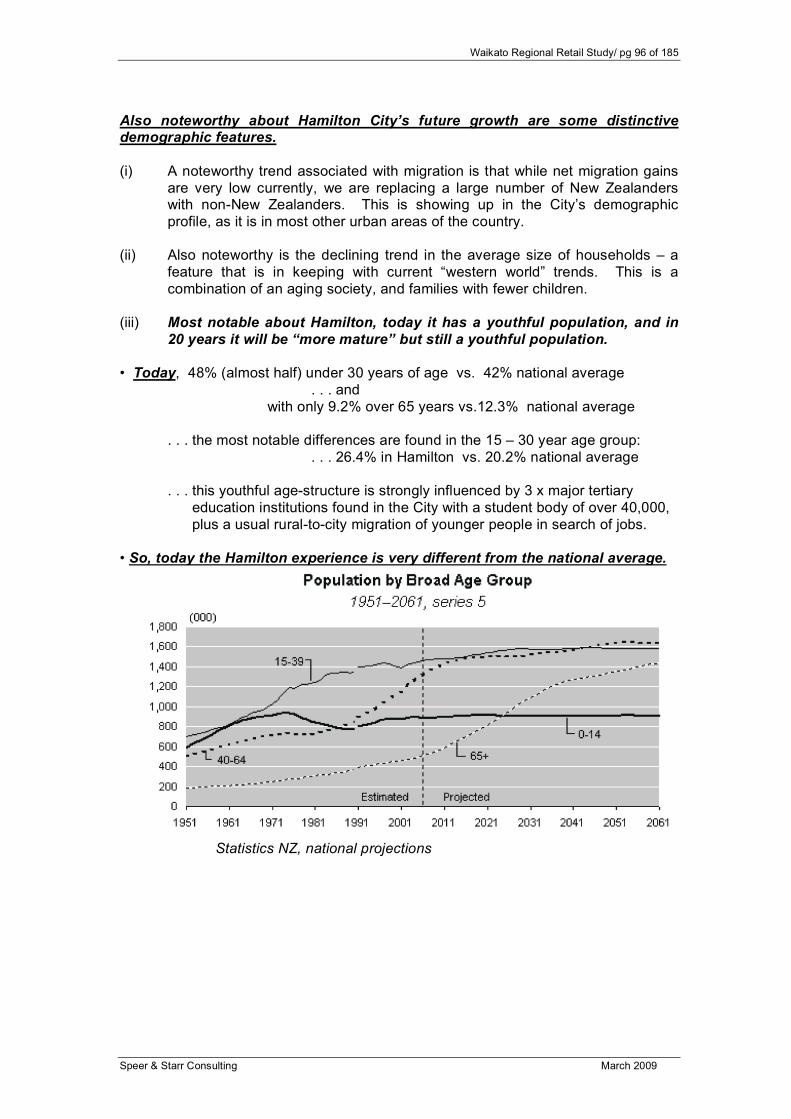

Also noteworthy about Hamilton City’s future growth are some distinctive demographic features. (i) A noteworthy trend associated with migration is that while net migration gains are very low currently, we are replacing a large number of New Zealanders with non-New Zealanders. This is showing up in the City’s demographic profile, as it is in most other urban areas of the country. (ii) Also noteworthy is the declining trend in the average size of households – a feature that is in keeping with current “western world” trends. This is a combination of an aging society, and families with fewer children. (iii) Most notable about Hamilton, today it has a youthful population, and in 20 years it will be “more mature” but still a youthful population. • Today, 48% (almost half) under 30 years of age vs. 42% national average . . . and with only 9.2% over 65 years vs.12.3% national average . . . the most notable differences are found in the 15 – 30 year age group: . . . 26.4% in Hamilton vs. 20.2% national average . . . this youthful age-structure is strongly influenced by 3 x major tertiary education institutions found in the City with a student body of over 40,000, plus a usual rural-to-city migration of younger people in search of jobs. • So, today the Hamilton experience is very different from the national average.

Statistics NZ, national projections

Waikato Regional Retail Study/ pg 97 of 185

Speer & Starr Consulting March 2009

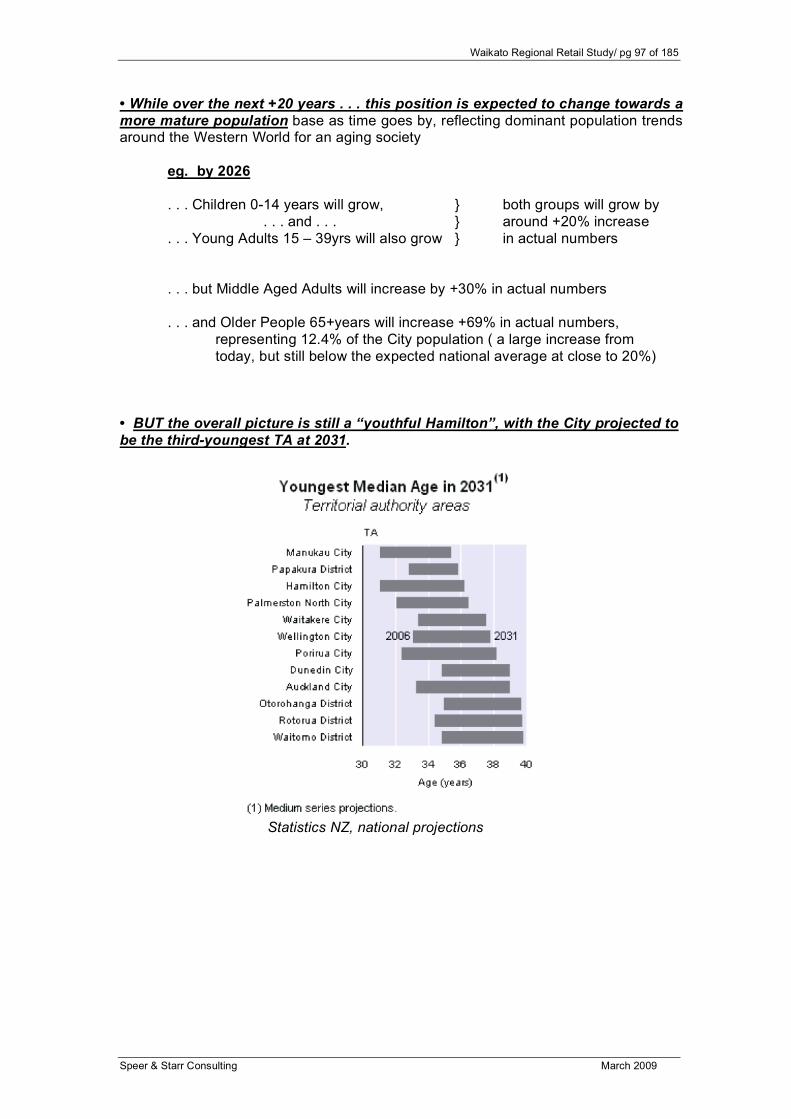

• While over the next +20 years . . . this position is expected to change towards a more mature population base as time goes by, reflecting dominant population trends around the Western World for an aging society eg. by 2026 . . . Children 0-14 years will grow, } both groups will grow by . . . and . . . } around +20% increase . . . Young Adults 15 – 39yrs will also grow } in actual numbers . . . but Middle Aged Adults will increase by +30% in actual numbers . . . and Older People 65+years will increase +69% in actual numbers, representing 12.4% of the City population ( a large increase from today, but still below the expected national average at close to 20%) • BUT the overall picture is still a “youthful Hamilton”, with the City projected to be the third-youngest TA at 2031.

Statistics NZ, national projections

Waikato Regional Retail Study/ pg 98 of 185

Speer & Starr Consulting March 2009

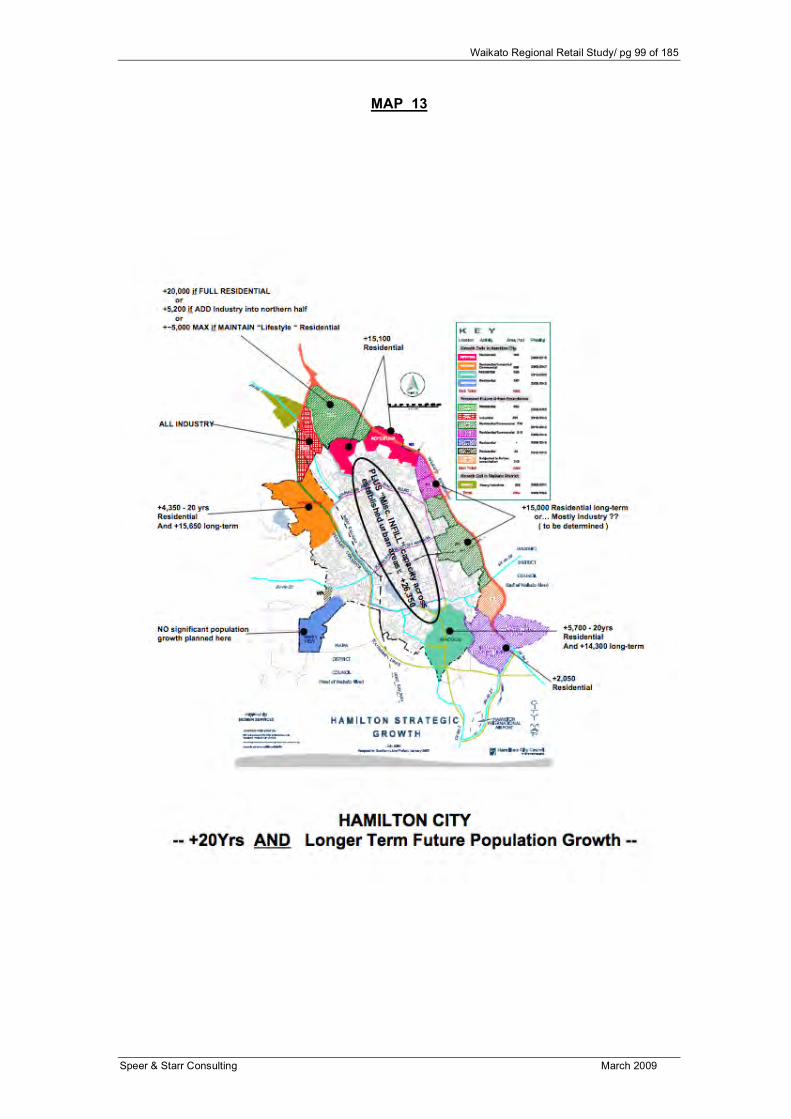

Overall, future growth for Hamilton city has these key elements: • Growth is projected to continue broadly at levels similar to or slightly greater than the growth experience over the past 5 years, around +2,500 p.a., but with obvious yearly fluctuations; • Over the next 20-years, growth is projected at +51,500 people : +38% increase over current levels; • A youthful population age structure will still prevail in 20 years; • Where this new growth will occur is broadly a 50/50 split between : -- growth occurring in the new growth cells of Rototouna, Rotokauri and Peacockes; -- targeted infill development within the urban area … Overall, providing a reasonably balanced distribution in growth across many sectors of the City as compared to recent growth which has strongly emphasised the northern fringe to the City. Refer MAP 13, following, for identification of key growth sectors around the City.

Waikato Regional Retail Study/ pg 99 of 185

Speer & Starr Consulting March 2009

MAP 13

Waikato Regional Retail Study/ pg 100 of 185

Speer & Starr Consulting March 2009

Also noteworthy about Hamilton City’s future growth are some distinctive demographic features. (i) A noteworthy trend associated with migration is that while net migration gains are very low currently, we are replacing a large number of New Zealanders with non-New Zealanders. This is showing up in the City’s demographic profile, as it is in most other urban areas of the country. (ii) Also noteworthy is the declining trend in the average size of households – a feature that is in keeping with current “western world” trends. This is a combination of an aging society, and families with fewer children. (iii) Most notable about Hamilton, today it has a youthful population, and in 20 years it will be “more mature” but still a youthful population. • Today, 48% (almost half) under 30 years of age vs. 42% national average . . . and with only 9.2% over 65 years vs.12.3% national average . . . the most notable differences are found in the 15 – 30 year age group: . . . 26.4% in Hamilton vs. 20.2% national average . . . this youthful age-structure is strongly influenced by 3 x major tertiary education institutions found in the City with a student body of over 40,000 . . . plus a usual rural-to-city migration of younger people searching for job opportunities. • BUT . . . this position is expected to change towards a more mature population base as time goes by, more closely reflecting dominant population trends around the Western World for an aging society eg. by 2026 . . . Children 0-14 years will grow, } both groups will grow by . . . and . . . } around +20% increase . . . Young Adults 15 – 39yrs will also grow } in actual numbers . . . but Middle Aged Adults will increase by +30% in actual numbers . . . and Older People 65+years will increase +69% in actual numbers, representing 12.4% of the City population ( a large increase from today, but still below the expected national average at close to 20%)

Waikato Regional Retail Study/ pg 101 of 185

Speer & Starr Consulting March 2009

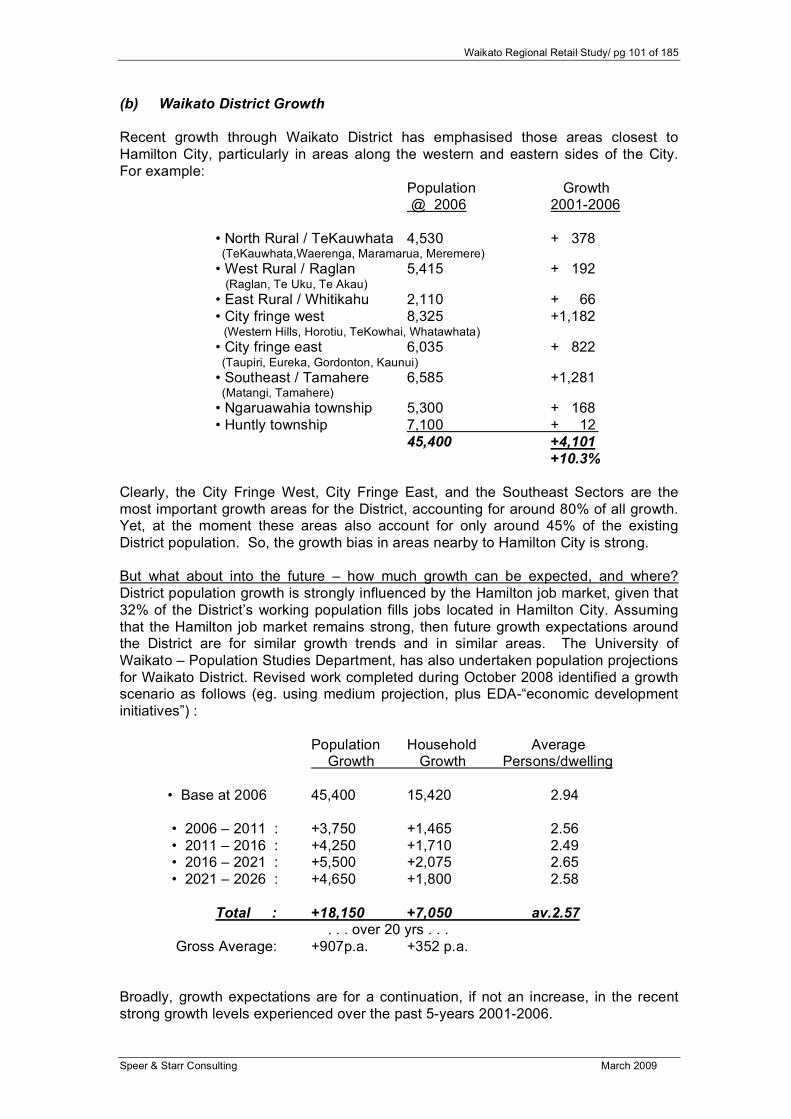

(b) Waikato District Growth Recent growth through Waikato District has emphasised those areas closest to Hamilton City, particularly in areas along the western and eastern sides of the City. For example: Population Growth @ 2006 2001-2006 • North Rural / TeKauwhata 4,530 + 378 (TeKauwhata,Waerenga, Maramarua, Meremere) • West Rural / Raglan 5,415 + 192 (Raglan, Te Uku, Te Akau) • East Rural / Whitikahu 2,110 + 66 • City fringe west 8,325 +1,182 (Western Hills, Horotiu, TeKowhai, Whatawhata) • City fringe east 6,035 + 822 (Taupiri, Eureka, Gordonton, Kaunui) • Southeast / Tamahere 6,585 +1,281 (Matangi, Tamahere) • Ngaruawahia township 5,300 + 168 • Huntly township 7,100 + 12 45,400 +4,101 +10.3% Clearly, the City Fringe West, City Fringe East, and the Southeast Sectors are the most important growth areas for the District, accounting for around 80% of all growth. Yet, at the moment these areas also account for only around 45% of the existing District population. So, the growth bias in areas nearby to Hamilton City is strong. But what about into the future – how much growth can be expected, and where? District population growth is strongly influenced by the Hamilton job market, given that 32% of the District’s working population fills jobs located in Hamilton City. Assuming that the Hamilton job market remains strong, then future growth expectations around the District are for similar growth trends and in similar areas. The University of Waikato – Population Studies Department, has also undertaken population projections for Waikato District. Revised work completed during October 2008 identified a growth scenario as follows (eg. using medium projection, plus EDA-“economic development initiatives”) : Population Household Average Growth Growth Persons/dwelling • Base at 2006 45,400 15,420 2.94 • 2006 – 2011 : +3,750 +1,465 2.56 • 2011 – 2016 : +4,250 +1,710 2.49 • 2016 – 2021 : +5,500 +2,075 2.65 • 2021 – 2026 : +4,650 +1,800 2.58 Total : +18,150 +7,050 av.2.57 . . . over 20 yrs . . . Gross Average: +907p.a. +352 p.a. Broadly, growth expectations are for a continuation, if not an increase, in the recent strong growth levels experienced over the past 5-years 2001-2006.

Waikato Regional Retail Study/ pg 102 of 185

Speer & Starr Consulting March 2009

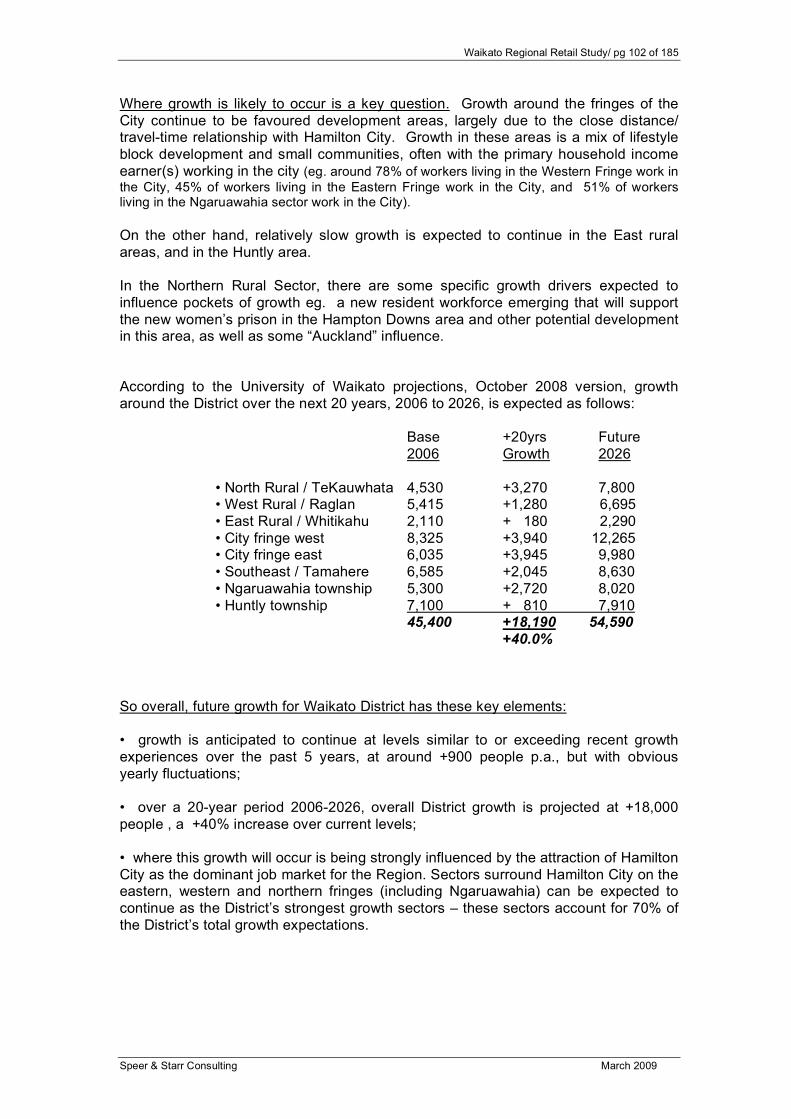

Where growth is likely to occur is a key question. Growth around the fringes of the City continue to be favoured development areas, largely due to the close distance/ travel-time relationship with Hamilton City. Growth in these areas is a mix of lifestyle block development and small communities, often with the primary household income earner(s) working in the city (eg. around 78% of workers living in the Western Fringe work in the City, 45% of workers living in the Eastern Fringe work in the City, and 51% of workers living in the Ngaruawahia sector work in the City). On the other hand, relatively slow growth is expected to continue in the East rural areas, and in the Huntly area. In the Northern Rural Sector, there are some specific growth drivers expected to influence pockets of growth eg. a new resident workforce emerging that will support the new women’s prison in the Hampton Downs area and other potential development in this area, as well as some “Auckland” influence. According to the University of Waikato projections, October 2008 version, growth around the District over the next 20 years, 2006 to 2026, is expected as follows: Base +20yrs Future 2006 Growth 2026 • North Rural / TeKauwhata 4,530 +3,270 7,800 • West Rural / Raglan 5,415 +1,280 6,695 • East Rural / Whitikahu 2,110 + 180 2,290 • City fringe west 8,325 +3,940 12,265 • City fringe east 6,035 +3,945 9,980 • Southeast / Tamahere 6,585 +2,045 8,630 • Ngaruawahia township 5,300 +2,720 8,020 • Huntly township 7,100 + 810 7,910 45,400 +18,190 54,590 +40.0% So overall, future growth for Waikato District has these key elements: • growth is anticipated to continue at levels similar to or exceeding recent growth experiences over the past 5 years, at around +900 people p.a., but with obvious yearly fluctuations; • over a 20-year period 2006-2026, overall District growth is projected at +18,000 people , a +40% increase over current levels; • where this growth will occur is being strongly influenced by the attraction of Hamilton City as the dominant job market for the Region. Sectors surround Hamilton City on the eastern, western and northern fringes (including Ngaruawahia) can be expected to continue as the District’s strongest growth sectors – these sectors account for 70% of the District’s total growth expectations.

Waikato Regional Retail Study/ pg 103 of 185

Speer & Starr Consulting March 2009

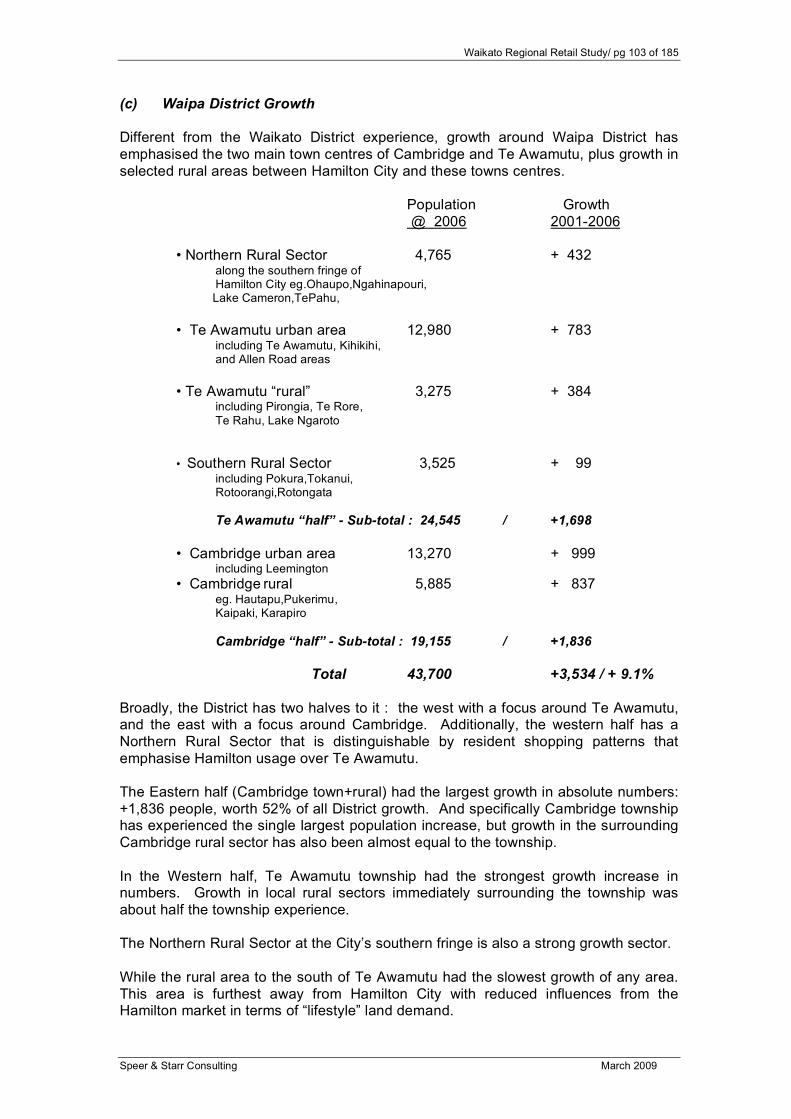

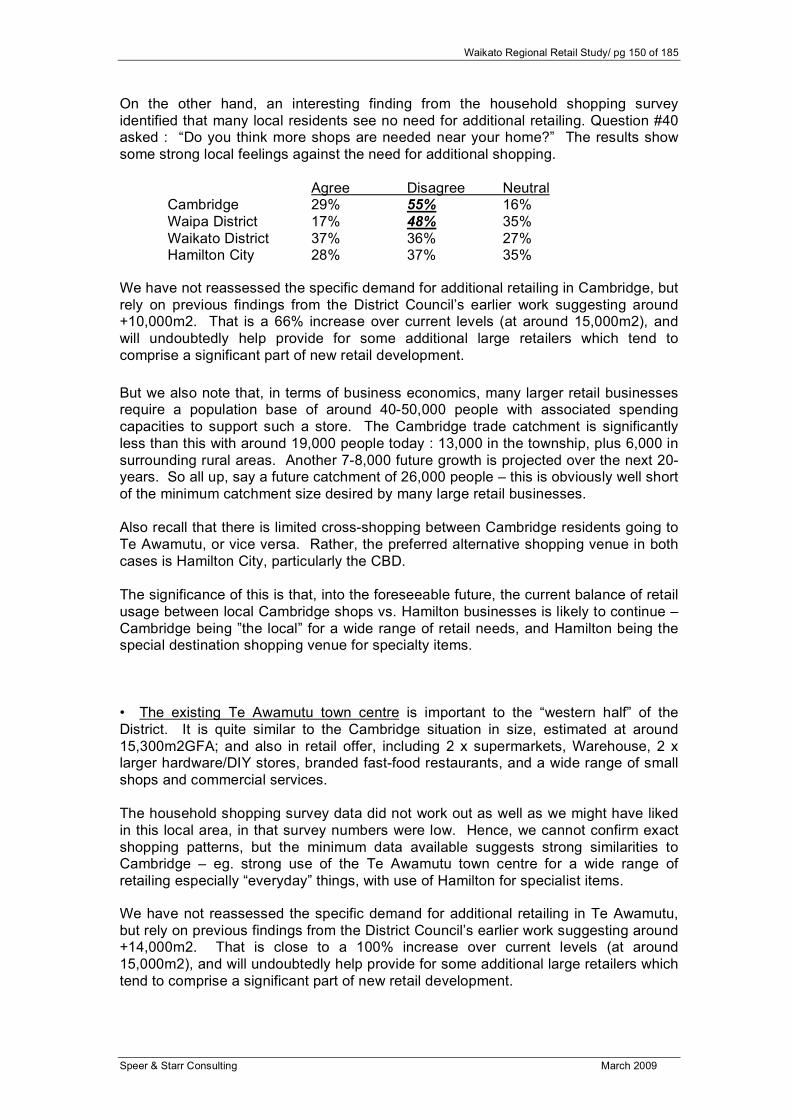

(c) Waipa District Growth Different from the Waikato District experience, growth around Waipa District has emphasised the two main town centres of Cambridge and Te Awamutu, plus growth in selected rural areas between Hamilton City and these towns centres. Population Growth @ 2006 2001-2006 • Northern Rural Sector 4,765 + 432 along the southern fringe of Hamilton City eg.Ohaupo,Ngahinapouri, Lake Cameron,TePahu, • Te Awamutu urban area 12,980 + 783 including Te Awamutu, Kihikihi, and Allen Road areas • Te Awamutu “rural” 3,275 + 384 including Pirongia, Te Rore, Te Rahu, Lake Ngaroto • Southern Rural Sector 3,525 + 99 including Pokura,Tokanui, Rotoorangi,Rotongata Te Awamutu “half” - Sub-total : 24,545 / +1,698 • Cambridge urban area 13,270 + 999 including Leemington • Cambridge rural 5,885 + 837 eg. Hautapu,Pukerimu, Kaipaki, Karapiro Cambridge “half” - Sub-total : 19,155 / +1,836 Total 43,700 +3,534 / + 9.1% Broadly, the District has two halves to it : the west with a focus around Te Awamutu, and the east with a focus around Cambridge. Additionally, the western half has a Northern Rural Sector that is distinguishable by resident shopping patterns that emphasise Hamilton usage over Te Awamutu. The Eastern half (Cambridge town+rural) had the largest growth in absolute numbers: +1,836 people, worth 52% of all District growth. And specifically Cambridge township has experienced the single largest population increase, but growth in the surrounding Cambridge rural sector has also been almost equal to the township. In the Western half, Te Awamutu township had the strongest growth increase in numbers. Growth in local rural sectors immediately surrounding the township was about half the township experience. The Northern Rural Sector at the City’s southern fringe is also a strong growth sector. While the rural area to the south of Te Awamutu had the slowest growth of any area. This area is furthest away from Hamilton City with reduced influences from the Hamilton market in terms of “lifestyle” land demand.

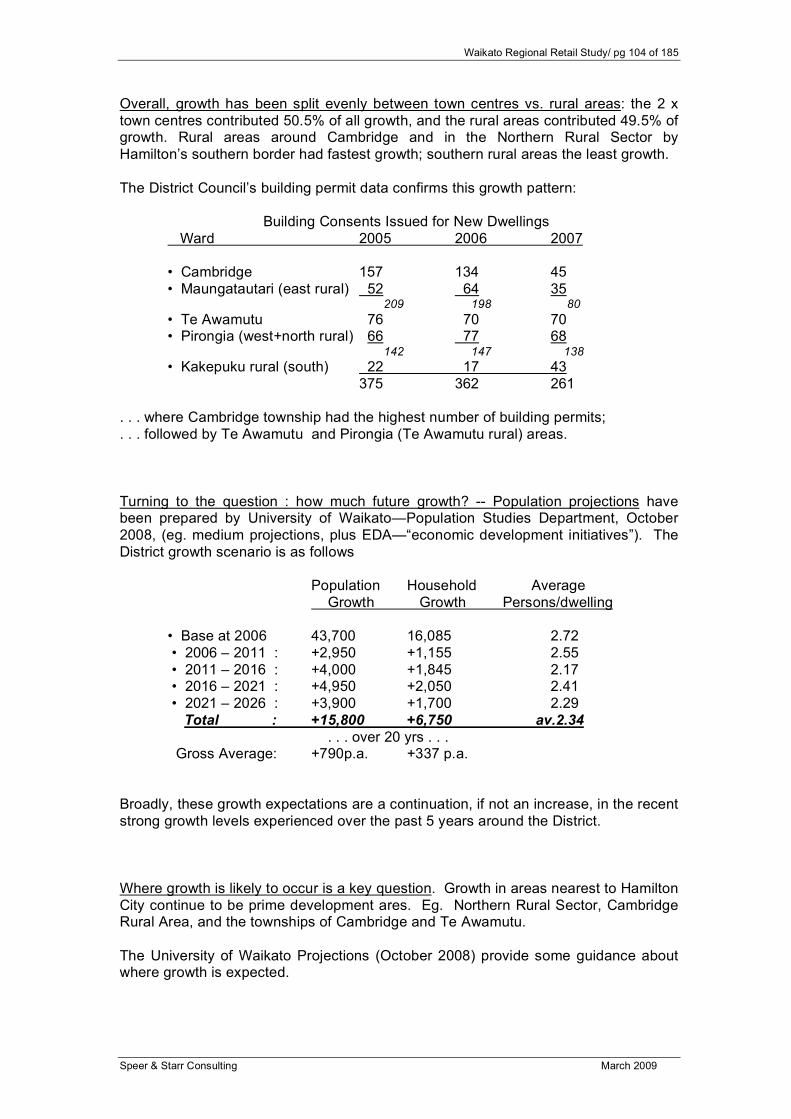

Waikato Regional Retail Study/ pg 104 of 185

Speer & Starr Consulting March 2009

Overall, growth has been split evenly between town centres vs. rural areas: the 2 x town centres contributed 50.5% of all growth, and the rural areas contributed 49.5% of growth. Rural areas around Cambridge and in the Northern Rural Sector by Hamilton’s southern border had fastest growth; southern rural areas the least growth. The District Council’s building permit data confirms this growth pattern: Building Consents Issued for New Dwellings Ward 2005 2006 2007 • Cambridge 157 134 45 • Maungatautari (east rural) 52 64 35 209 198 80 • Te Awamutu 76 70 70 • Pirongia (west+north rural) 66 77 68 142 147 138 • Kakepuku rural (south) 22 17 43 375 362 261 . . . where Cambridge township had the highest number of building permits; . . . followed by Te Awamutu and Pirongia (Te Awamutu rural) areas. Turning to the question : how much future growth? -- Population projections have been prepared by University of Waikato—Population Studies Department, October 2008, (eg. medium projections, plus EDA—“economic development initiatives”). The District growth scenario is as follows Population Household Average Growth Growth Persons/dwelling • Base at 2006 43,700 16,085 2.72 • 2006 – 2011 : +2,950 +1,155 2.55 • 2011 – 2016 : +4,000 +1,845 2.17 • 2016 – 2021 : +4,950 +2,050 2.41 • 2021 – 2026 : +3,900 +1,700 2.29 Total : +15,800 +6,750 av.2.34 . . . over 20 yrs . . . Gross Average: +790p.a. +337 p.a. Broadly, these growth expectations are a continuation, if not an increase, in the recent strong growth levels experienced over the past 5 years around the District. Where growth is likely to occur is a key question. Growth in areas nearest to Hamilton City continue to be prime development ares. Eg. Northern Rural Sector, Cambridge Rural Area, and the townships of Cambridge and Te Awamutu. The University of Waikato Projections (October 2008) provide some guidance about where growth is expected.

Waikato Regional Retail Study/ pg 105 of 185

Speer & Starr Consulting March 2009

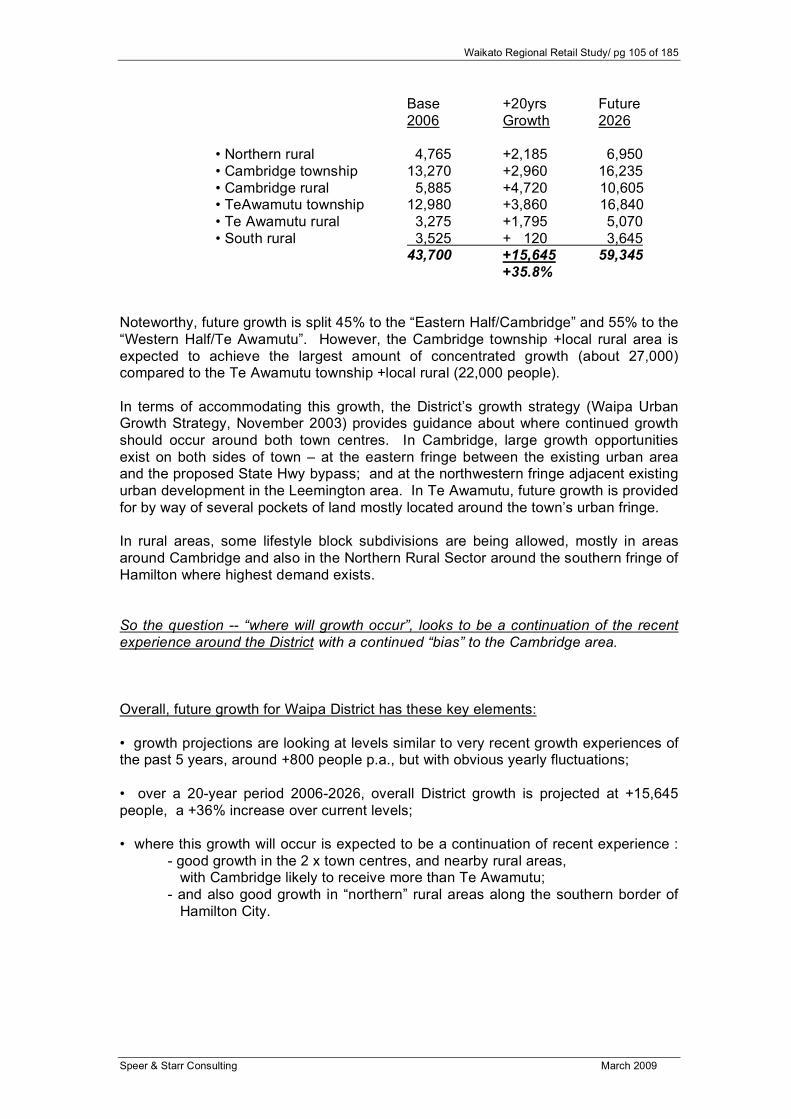

Base +20yrs Future 2006 Growth 2026 • Northern rural 4,765 +2,185 6,950 • Cambridge township 13,270 +2,960 16,235 • Cambridge rural 5,885 +4,720 10,605 • TeAwamutu township 12,980 +3,860 16,840 • Te Awamutu rural 3,275 +1,795 5,070 • South rural 3,525 + 120 3,645 43,700 +15,645 59,345 +35.8% Noteworthy, future growth is split 45% to the “Eastern Half/Cambridge” and 55% to the “Western Half/Te Awamutu”. However, the Cambridge township +local rural area is expected to achieve the largest amount of concentrated growth (about 27,000) compared to the Te Awamutu township +local rural (22,000 people). In terms of accommodating this growth, the District’s growth strategy (Waipa Urban Growth Strategy, November 2003) provides guidance about where continued growth should occur around both town centres. In Cambridge, large growth opportunities exist on both sides of town – at the eastern fringe between the existing urban area and the proposed State Hwy bypass; and at the northwestern fringe adjacent existing urban development in the Leemington area. In Te Awamutu, future growth is provided for by way of several pockets of land mostly located around the town’s urban fringe. In rural areas, some lifestyle block subdivisions are being allowed, mostly in areas around Cambridge and also in the Northern Rural Sector around the southern fringe of Hamilton where highest demand exists. So the question -- “where will growth occur”, looks to be a continuation of the recent experience around the District with a continued “bias” to the Cambridge area. Overall, future growth for Waipa District has these key elements: • growth projections are looking at levels similar to very recent growth experiences of the past 5 years, around +800 people p.a., but with obvious yearly fluctuations; • over a 20-year period 2006-2026, overall District growth is projected at +15,645 people, a +36% increase over current levels; • where this growth will occur is expected to be a continuation of recent experience : - good growth in the 2 x town centres, and nearby rural areas, with Cambridge likely to receive more than Te Awamutu; - and also good growth in “northern” rural areas along the southern border of Hamilton City.

Waikato Regional Retail Study/ pg 106 of 185

Speer & Starr Consulting March 2009

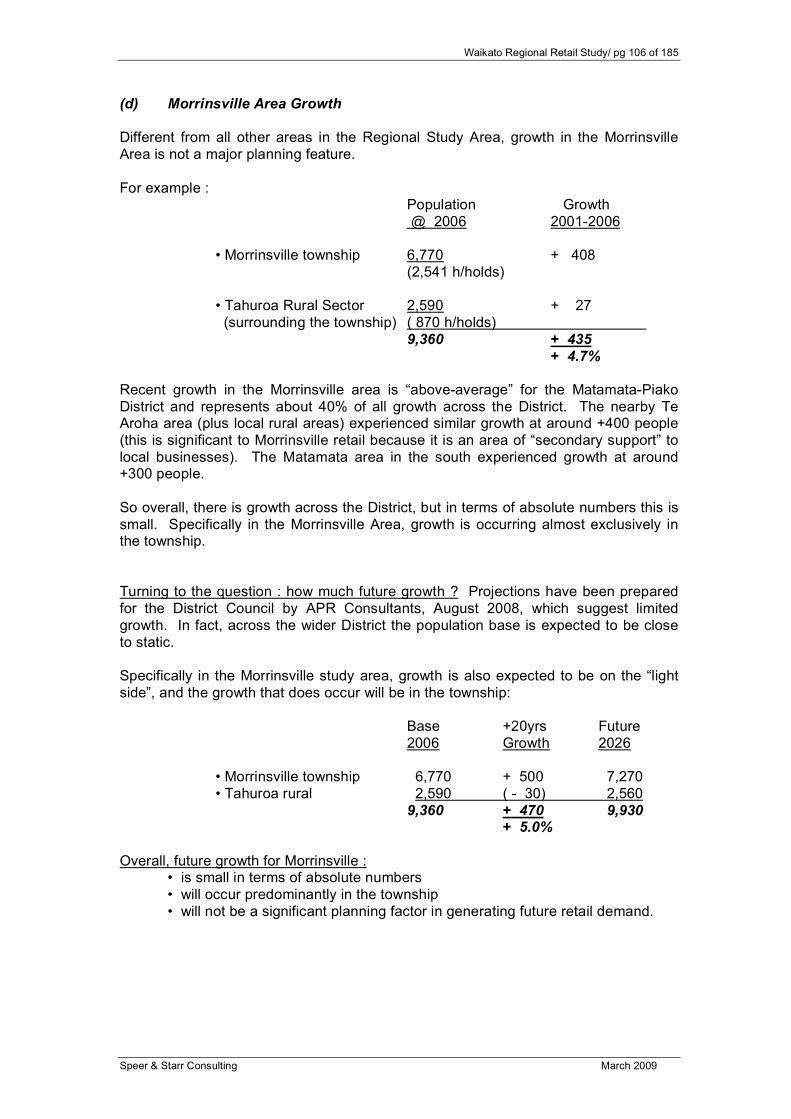

(d) Morrinsville Area Growth Different from all other areas in the Regional Study Area, growth in the Morrinsville Area is not a major planning feature. For example : Population Growth @ 2006 2001-2006 • Morrinsville township 6,770 + 408 (2,541 h/holds) • Tahuroa Rural Sector 2,590 + 27 (surrounding the township) ( 870 h/holds) 9,360 + 435 + 4.7% Recent growth in the Morrinsville area is “above-average” for the Matamata-Piako District and represents about 40% of all growth across the District. The nearby Te Aroha area (plus local rural areas) experienced similar growth at around +400 people (this is significant to Morrinsville retail because it is an area of “secondary support” to local businesses). The Matamata area in the south experienced growth at around +300 people. So overall, there is growth across the District, but in terms of absolute numbers this is small. Specifically in the Morrinsville Area, growth is occurring almost exclusively in the township. Turning to the question : how much future growth ? Projections have been prepared for the District Council by APR Consultants, August 2008, which suggest limited growth. In fact, across the wider District the population base is expected to be close to static. Specifically in the Morrinsville study area, growth is also expected to be on the “light side”, and the growth that does occur will be in the township: Base +20yrs Future 2006 Growth 2026 • Morrinsville township 6,770 + 500 7,270 • Tahuroa rural 2,590 ( - 30) 2,560 9,360 + 470 9,930 + 5.0% Overall, future growth for Morrinsville : • is small in terms of absolute numbers • will occur predominantly in the township • will not be a significant planning factor in generating future retail demand.

Waikato Regional Retail Study/ pg 107 of 185

Speer & Starr Consulting March 2009

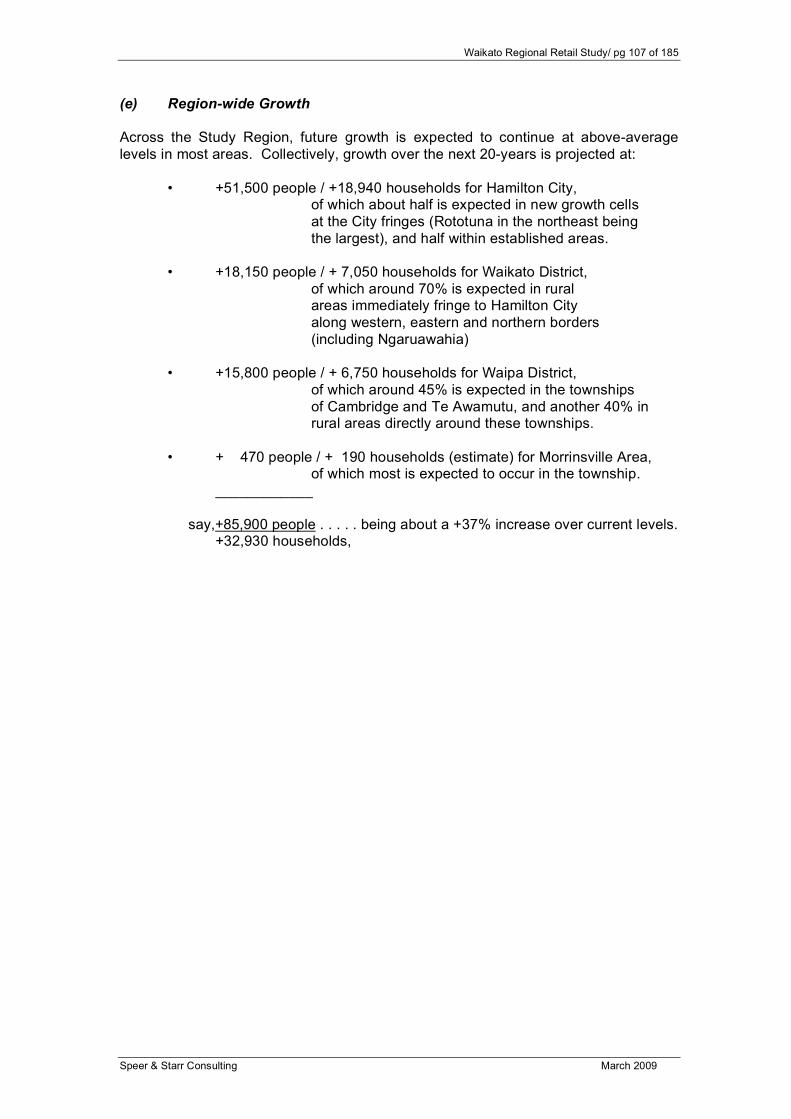

(e) Region-wide Growth Across the Study Region, future growth is expected to continue at above-average levels in most areas. Collectively, growth over the next 20-years is projected at: • +51,500 people / +18,940 households for Hamilton City, of which about half is expected in new growth cells at the City fringes (Rototuna in the northeast being the largest), and half within established areas. • +18,150 people / + 7,050 households for Waikato District, of which around 70% is expected in rural areas immediately fringe to Hamilton City along western, eastern and northern borders (including Ngaruawahia) • +15,800 people / + 6,750 households for Waipa District, of which around 45% is expected in the townships of Cambridge and Te Awamutu, and another 40% in rural areas directly around these townships. • + 470 people / + 190 households (estimate) for Morrinsville Area, of which most is expected to occur in the township. ____________ say,+85,900 people . . . . . being about a +37% increase over current levels. +32,930 households,

Waikato Regional Retail Study/ pg 108 of 185

Speer & Starr Consulting March 2009

2. “Dairying is the Waikato” – a key local economic issue

The Waikato Region has long been an area known for dairy farming. “Dairying is the Waikato” correctly conveys the importance of this industry to the area. In spite of recent changes within the dairy industry and major shifts in production to new areas such as Southland, the Waikato is still the largest dairying region in NZ, worth some 28% of the country’s total milk production.

Even in today’s high-tech world, food supplies are a vital industry and dairy products continue to be staple food items. Current commodity prices for milk-solids are high, reflecting market scarcity/shortages due to a range of issues including some limits on production elsewhere in the world due to droughts and poor production techniques, and on the other hand expansion of the milk consumer market especially through China and India and other Asian countries.

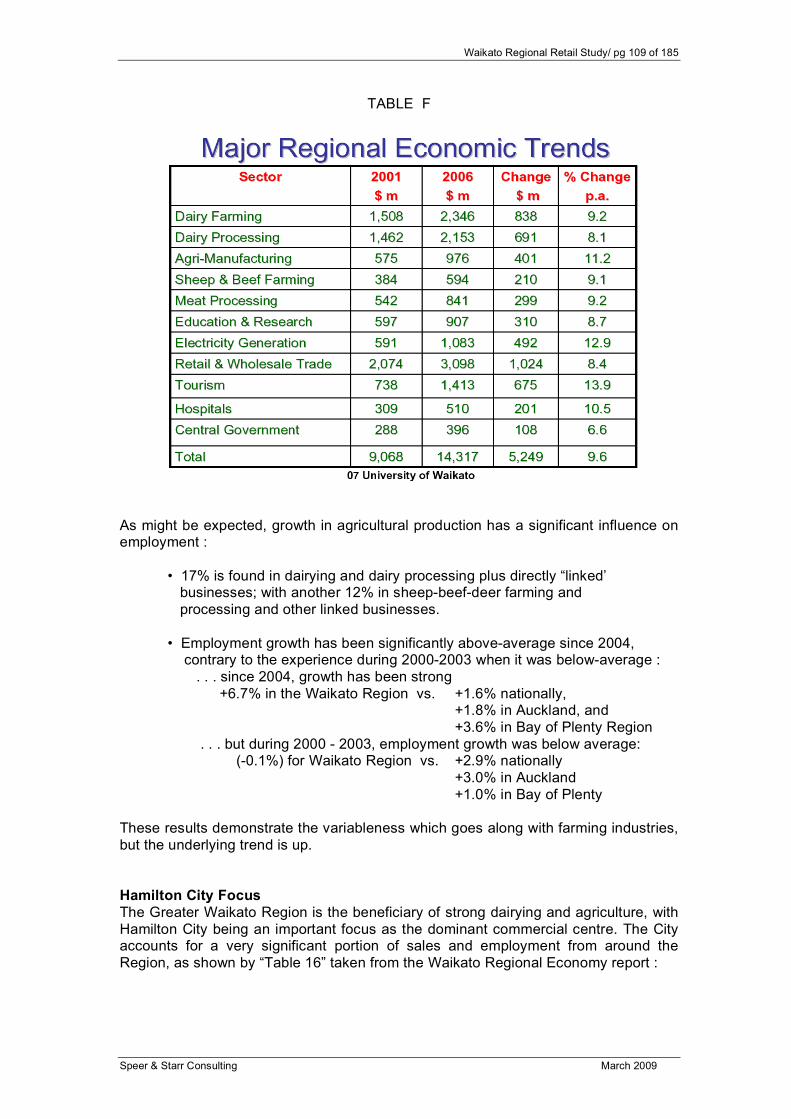

Consequently, the economic future to the Waikato looks set to continue as an important “dairy farm” especially to Asian markets. In fact, more than dairying alone, the Waikato is an important “food bowl” to the world providing over $6 Billion/per annum in milk, meat, vegetables and fruit (with Dairying contributing 1/3rd of this). A recent report entitled “The Waikato Regional Economy”, prepared by the Department of Economics, University of Waikato (April 2007), identified some key issues about the dairy and agricultural industries to the Waikato economy : • The most profitable business sectors in the Waikato includes dairy farming; • The largest exporters in the Waikato includes dairy processing, worth over $2Billion per annum; over 90% of production is exported • After accounting for all linkages from initiating activity, the greatest percentage of employment and value added activity in the Region stems from Dairy Farming and Processing, followed by Education and Scientific Research, and then Sheep Beef Deer Farming & Processing; • The most important activity in the Region is still Dairy Farming & Dairy Processing which, after accounting for all backward and forward linkages, accounts for 17% of the Region’s employment and 24% of its GDP; • Dairying combined with other farming activities, and also with agricultural manufacturing, accounts for about 40% of the Regional economy be it employment or sales; • Between 2001 – 2006, dairy farming and dairy processing sales revenue has increased at around +9% p.a.; . . . so has sales in sheep & beef farming and meat processing; . . . with Agricultural Manufacturing even higher at +11% p.a. • In fact, the entire Waikato Regional Economy has increased at 9.6% p.a., underpinned by an improved dairy industry and strong population inflows (+11,500 new regional residents between 2001-2006, being additional to natural growth of the established population); The following TableF illustrates the growth achieved in key sectors of the regional economy.

Waikato Regional Retail Study/ pg 109 of 185

Speer & Starr Consulting March 2009

TABLE F

As might be expected, growth in agricultural production has a significant influence on employment : • 17% is found in dairying and dairy processing plus directly “linked’ businesses; with another 12% in sheep-beef-deer farming and processing and other linked businesses. • Employment growth has been significantly above-average since 2004, contrary to the experience during 2000-2003 when it was below-average : . . . since 2004, growth has been strong +6.7% in the Waikato Region vs. +1.6% nationally, +1.8% in Auckland, and +3.6% in Bay of Plenty Region . . . but during 2000 - 2003, employment growth was below average: (-0.1%) for Waikato Region vs. +2.9% nationally +3.0% in Auckland +1.0% in Bay of Plenty These results demonstrate the variableness which goes along with farming industries, but the underlying trend is up. Hamilton City Focus The Greater Waikato Region is the beneficiary of strong dairying and agriculture, with Hamilton City being an important focus as the dominant commercial centre. The City accounts for a very significant portion of sales and employment from around the Region, as shown by “Table 16” taken from the Waikato Regional Economy report :

Waikato Regional Retail Study/ pg 110 of 185

Speer & Starr Consulting March 2009

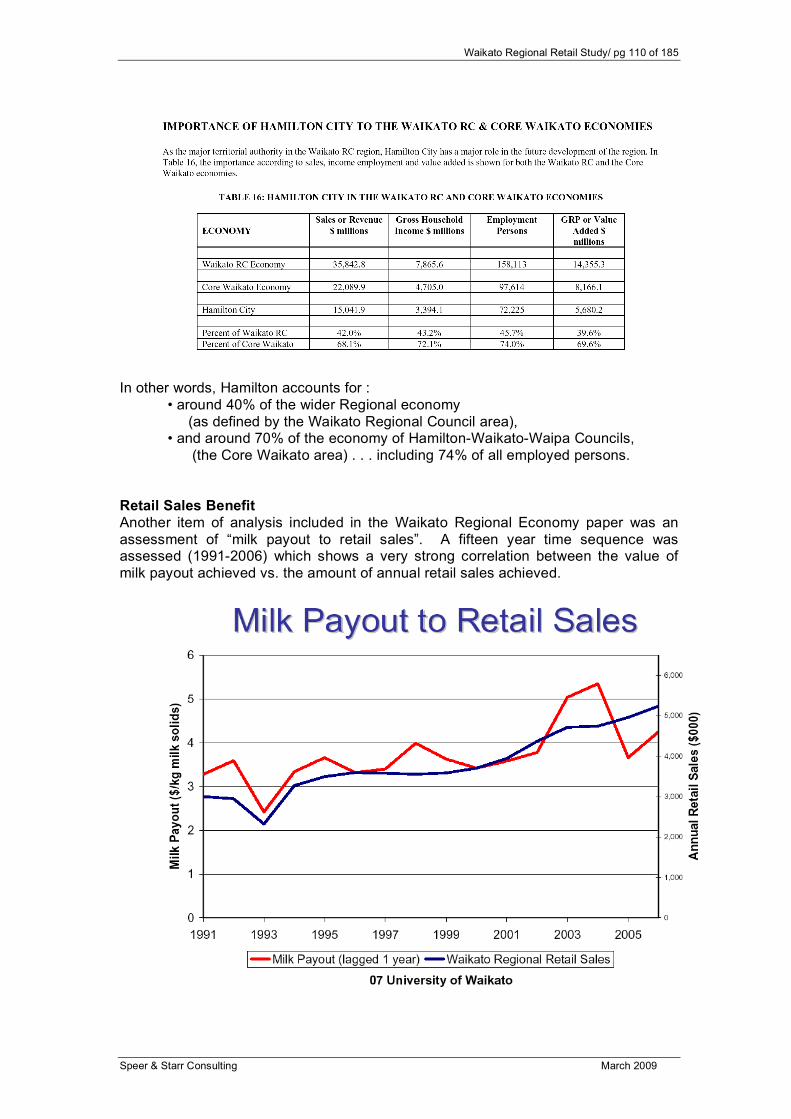

In other words, Hamilton accounts for : • around 40% of the wider Regional economy (as defined by the Waikato Regional Council area), • and around 70% of the economy of Hamilton-Waikato-Waipa Councils, (the Core Waikato area) . . . including 74% of all employed persons. Retail Sales Benefit Another item of analysis included in the Waikato Regional Economy paper was an assessment of “milk payout to retail sales”. A fifteen year time sequence was assessed (1991-2006) which shows a very strong correlation between the value of milk payout achieved vs. the amount of annual retail sales achieved.

Waikato Regional Retail Study/ pg 111 of 185

Speer & Starr Consulting March 2009

With dairying worth 24% of the Regional Economy, and other farming and agri-manufacturing businesses worth a further 16%, there is little wonder at the tight correlation between Milk Payout and Retail Sales. Obviously around the Waikato, as dairying goes so goes retail. Or, as the economic report concludes, “Dairying [plus other farming activities] drives Waikato growth – and everything else”. This is an important fundamental to keep an eye on regarding future retail growth.

Waikato Regional Retail Study/ pg 112 of 185

Speer & Starr Consulting March 2009

3. Hamilton City is the Employment Hub for the Region

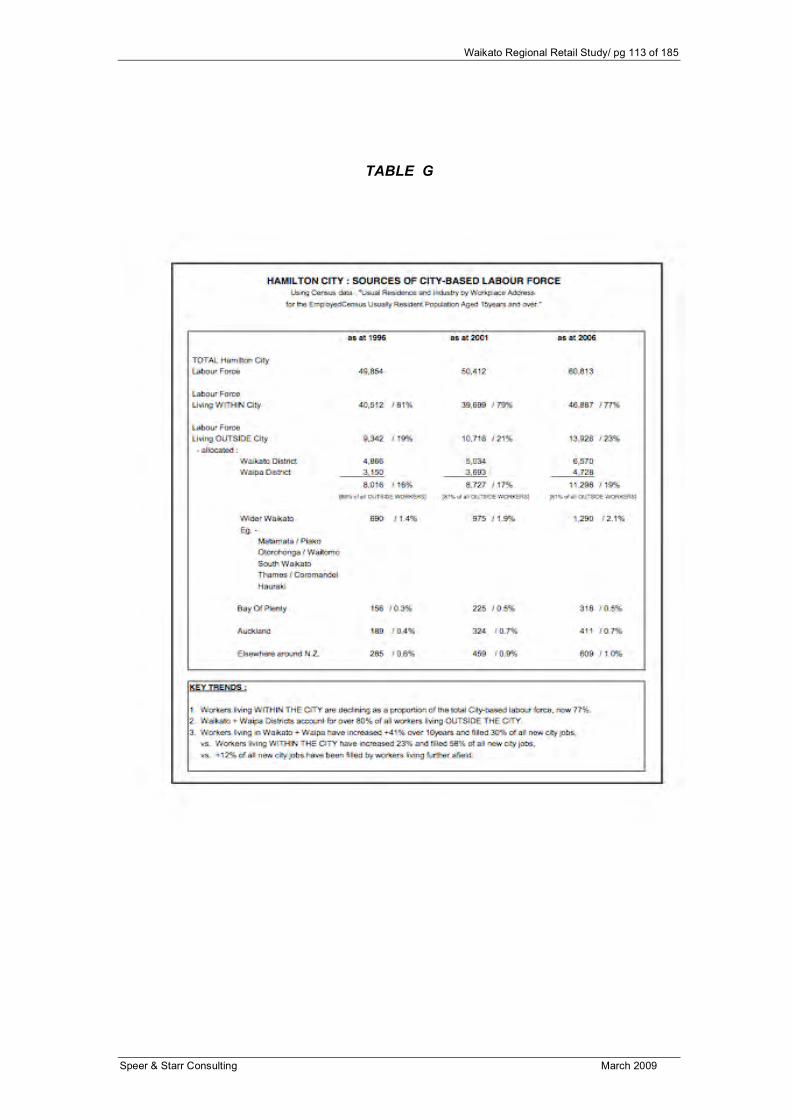

A notable feature about the Study Region is the high level of influence which Hamilton City-based employment holds over the total employment structure. Data is available from Statistics NZ identifying the number of people in the labour force, and also “travel to work” data is available from the Census indicating the origin and destination of work trips (that is, where workers come from to undertake employment in area “x”). The size of the labour force “usually resident” in each territorial authority area can be found in Statistics NZ : 2006 regional summary tables. Specifically for the Waikato Study Area, the overall resident labour force is identified as follows: Total Unemployed Active Labour Force Labour Force • Hamilton City : 67,353 4,581 62,772 = 52% • Waikato District : 21,978 1,158 20,820 = 17% • Waipa District : 22,656 753 21,820 = 18% • Matamata-Piako : 15,720 588 15,132 = 13% (including Morrinsville) 127,707 7,080 120,627 =100% Travel to Work data from the Census identifies where people travel from and where they travel to for work. The following Table G identifies the results of this data over three time periods -- 1996, 2001, 2006 – and is focused on Hamilton City as the destination for work trips. Noteworthy trends over this ten-year period include: • employment/jobs filled by residents living within the City is declining in favour of more workers commuting into the city from elsewhere (as a proportion of the total labour force) ; • at 2006, some 77% of all city-based employment was filled by City residents vs. 79% in 2001, and 81% in 1996; • at 2006, of the 23% of workers coming from outside the City:

- 11% came from Waikato District - 8% came from Waipa District - 2% came from the wider Waikato “region”, including Morrinsville - 2% came from misc. elsewhere.

• Waikato and Waipa District resident workers account for 81% of all workers “living outside the city”. Further, these two areas are growing in importance as a source of employees to fill city-based jobs, now filling 19% of all city jobs at 2006, up from 17% in 2001 and 16% in 1996. • Hence, it is not surprising to find that the number of workers coming into Hamilton City from Waikato and Waipa Districts has increase by +41% over the past 10 years -- +3,300 new workers, filling 30% of all new jobs created in Hamilton.

Waikato Regional Retail Study/ pg 113 of 185

Speer & Starr Consulting March 2009

TABLE G

Waikato Regional Retail Study/ pg 114 of 185

Speer & Starr Consulting March 2009

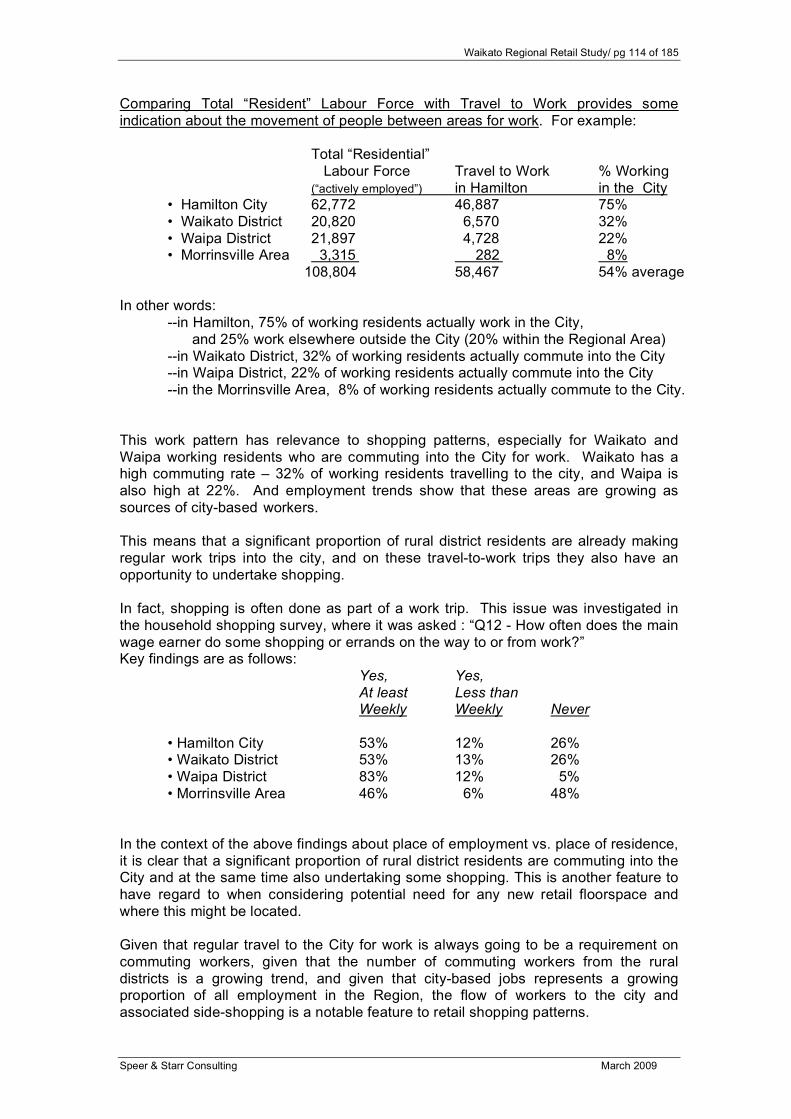

Comparing Total “Resident” Labour Force with Travel to Work provides some indication about the movement of people between areas for work. For example: Total “Residential” Labour Force Travel to Work % Working (“actively employed”) in Hamilton in the City • Hamilton City 62,772 46,887 75% • Waikato District 20,820 6,570 32% • Waipa District 21,897 4,728 22% • Morrinsville Area 3,315 282 8% 108,804 58,467 54% average In other words: --in Hamilton, 75% of working residents actually work in the City, and 25% work elsewhere outside the City (20% within the Regional Area) --in Waikato District, 32% of working residents actually commute into the City --in Waipa District, 22% of working residents actually commute into the City --in the Morrinsville Area, 8% of working residents actually commute to the City. This work pattern has relevance to shopping patterns, especially for Waikato and Waipa working residents who are commuting into the City for work. Waikato has a high commuting rate – 32% of working residents travelling to the city, and Waipa is also high at 22%. And employment trends show that these areas are growing as sources of city-based workers. This means that a significant proportion of rural district residents are already making regular work trips into the city, and on these travel-to-work trips they also have an opportunity to undertake shopping. In fact, shopping is often done as part of a work trip. This issue was investigated in the household shopping survey, where it was asked : “Q12 - How often does the main wage earner do some shopping or errands on the way to or from work?” Key findings are as follows: Yes, Yes, At least Less than Weekly Weekly Never • Hamilton City 53% 12% 26% • Waikato District 53% 13% 26% • Waipa District 83% 12% 5% • Morrinsville Area 46% 6% 48% In the context of the above findings about place of employment vs. place of residence, it is clear that a significant proportion of rural district residents are commuting into the City and at the same time also undertaking some shopping. This is another feature to have regard to when considering potential need for any new retail floorspace and where this might be located. Given that regular travel to the City for work is always going to be a requirement on commuting workers, given that the number of commuting workers from the rural districts is a growing trend, and given that city-based jobs represents a growing proportion of all employment in the Region, the flow of workers to the city and associated side-shopping is a notable feature to retail shopping patterns.

Waikato Regional Retail Study/ pg 115 of 185

Speer & Starr Consulting March 2009

4. “Real” Income and Retail Sales Growth Factor The importance of retailing to the average Waikato Household

If we examine the average household expenditure pattern, we see that about 70% of household income is spent at retail. The only significant non-retail expenditures are housing, health, and communication. Because the great majority of personal income is spent at retail, it is imperative that retail planning be conducted in a way that makes this expenditure convenient and personally satisfying. Significant under- or over-provision of retailing facilities will have a direct negative impact on overall quality of life.

Economic growth outlook

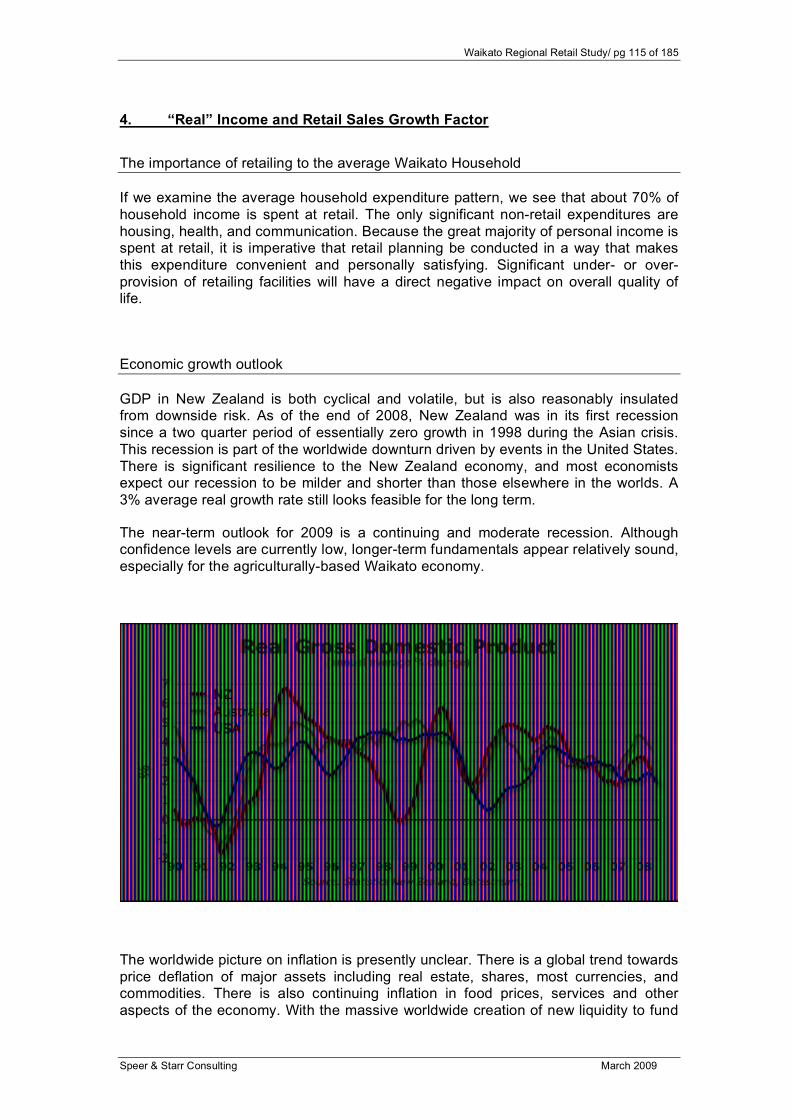

GDP in New Zealand is both cyclical and volatile, but is also reasonably insulated from downside risk. As of the end of 2008, New Zealand was in its first recession since a two quarter period of essentially zero growth in 1998 during the Asian crisis. This recession is part of the worldwide downturn driven by events in the United States. There is significant resilience to the New Zealand economy, and most economists expect our recession to be milder and shorter than those elsewhere in the worlds. A 3% average real growth rate still looks feasible for the long term.

The near-term outlook for 2009 is a continuing and moderate recession. Although confidence levels are currently low, longer-term fundamentals appear relatively sound, especially for the agriculturally-based Waikato economy.

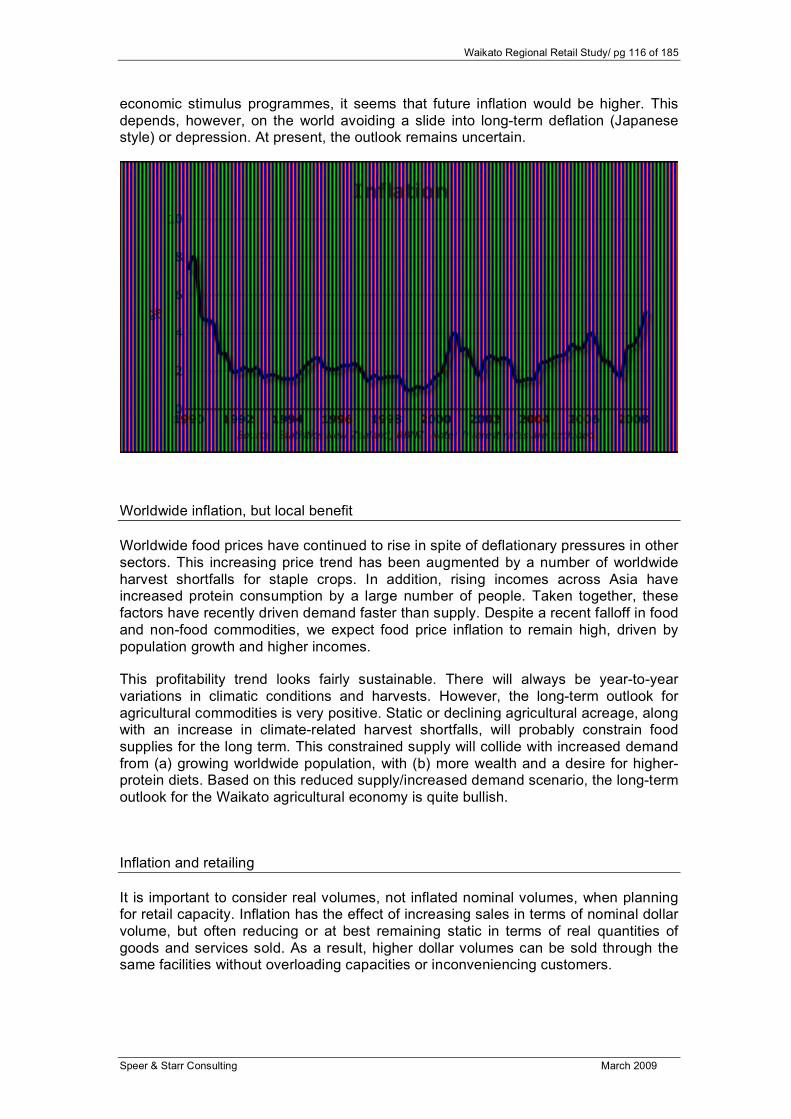

The worldwide picture on inflation is presently unclear. There is a global trend towards price deflation of major assets including real estate, shares, most currencies, and commodities. There is also continuing inflation in food prices, services and other aspects of the economy. With the massive worldwide creation of new liquidity to fund

Waikato Regional Retail Study/ pg 116 of 185

Speer & Starr Consulting March 2009

economic stimulus programmes, it seems that future inflation would be higher. This depends, however, on the world avoiding a slide into long-term deflation (Japanese style) or depression. At present, the outlook remains uncertain.

Worldwide inflation, but local benefit

Worldwide food prices have continued to rise in spite of deflationary pressures in other sectors. This increasing price trend has been augmented by a number of worldwide harvest shortfalls for staple crops. In addition, rising incomes across Asia have increased protein consumption by a large number of people. Taken together, these factors have recently driven demand faster than supply. Despite a recent falloff in food and non-food commodities, we expect food price inflation to remain high, driven by population growth and higher incomes.

This profitability trend looks fairly sustainable. There will always be year-to-year variations in climatic conditions and harvests. However, the long-term outlook for agricultural commodities is very positive. Static or declining agricultural acreage, along with an increase in climate-related harvest shortfalls, will probably constrain food supplies for the long term. This constrained supply will collide with increased demand from (a) growing worldwide population, with (b) more wealth and a desire for higher-protein diets. Based on this reduced supply/increased demand scenario, the long-term outlook for the Waikato agricultural economy is quite bullish.

Inflation and retailing

It is important to consider real volumes, not inflated nominal volumes, when planning for retail capacity. Inflation has the effect of increasing sales in terms of nominal dollar volume, but often reducing or at best remaining static in terms of real quantities of goods and services sold. As a result, higher dollar volumes can be sold through the same facilities without overloading capacities or inconveniencing customers.

Waikato Regional Retail Study/ pg 117 of 185

Speer & Starr Consulting March 2009

Past experience also shows that wages and income lag behind inflation. This means that during inflationary periods, households will increase consumption at a slower rate, or even decrease real consumption for periods of time.

Projecting real retail growth rate

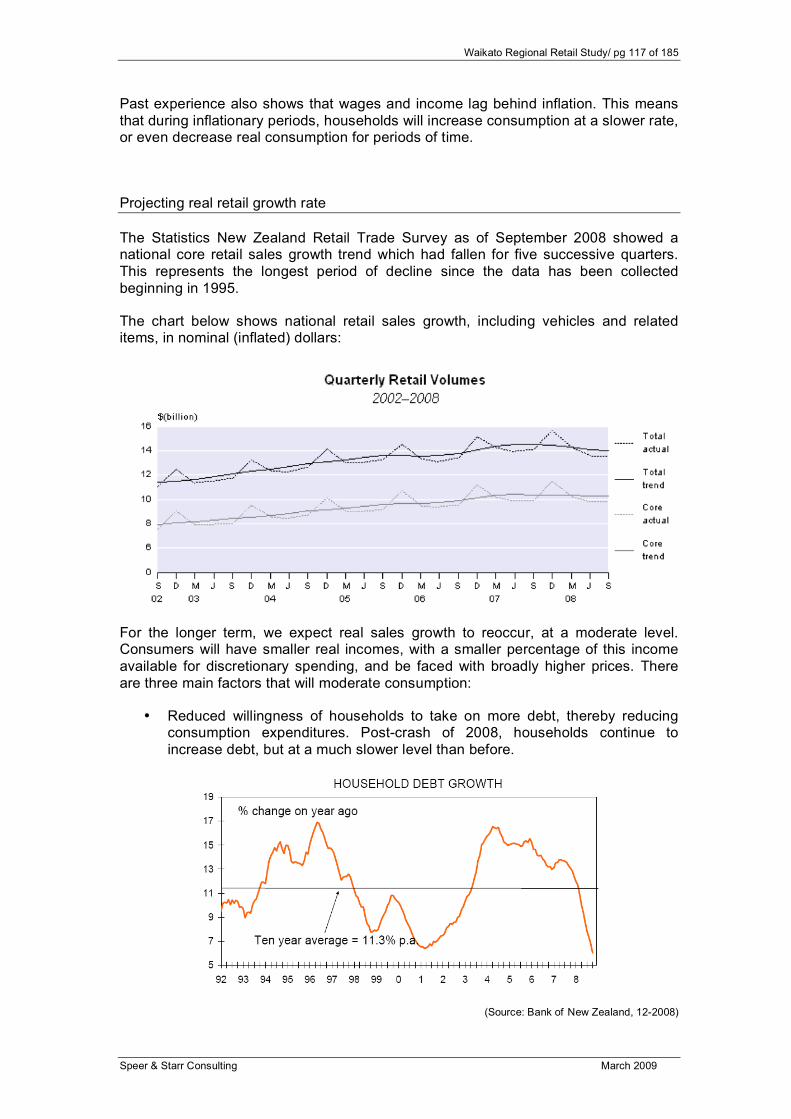

The Statistics New Zealand Retail Trade Survey as of September 2008 showed a national core retail sales growth trend which had fallen for five successive quarters. This represents the longest period of decline since the data has been collected beginning in 1995.

The chart below shows national retail sales growth, including vehicles and related items, in nominal (inflated) dollars:

For the longer term, we expect real sales growth to reoccur, at a moderate level. Consumers will have smaller real incomes, with a smaller percentage of this income available for discretionary spending, and be faced with broadly higher prices. There are three main factors that will moderate consumption:

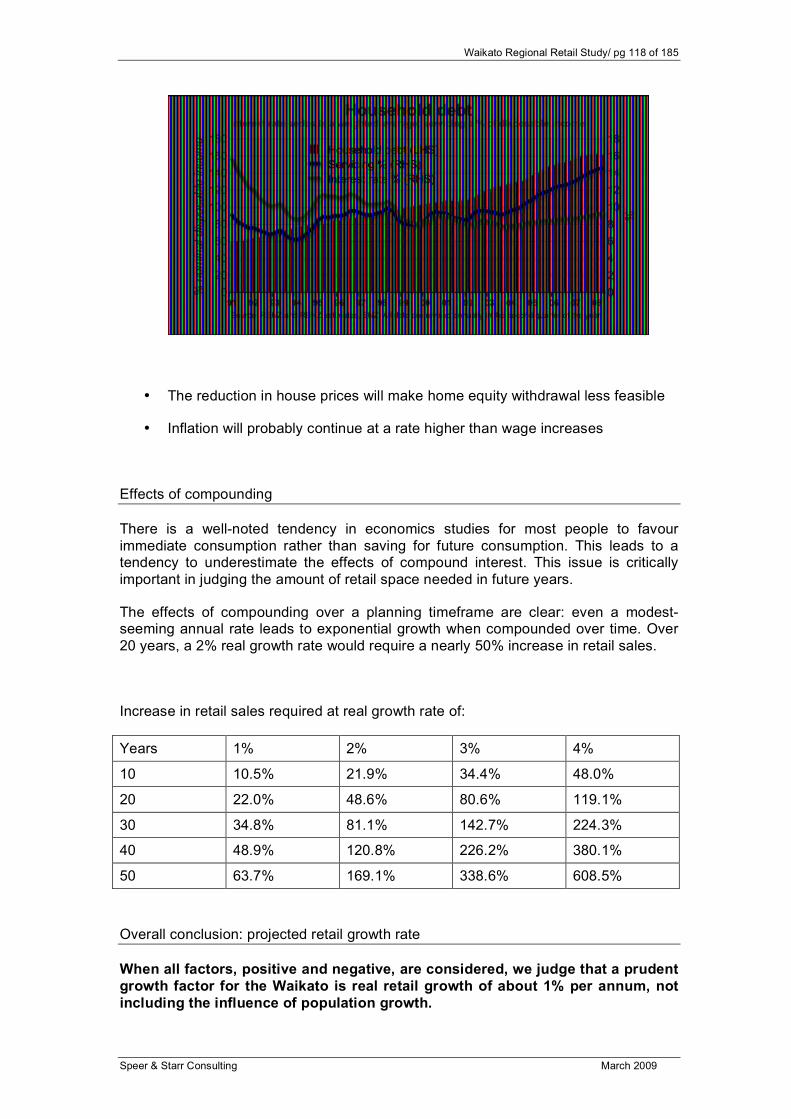

• Reduced willingness of households to take on more debt, thereby reducing consumption expenditures. Post-crash of 2008, households continue to increase debt, but at a much slower level than before.

(Source: Bank of New Zealand, 12-2008)

Waikato Regional Retail Study/ pg 118 of 185

Speer & Starr Consulting March 2009

• The reduction in house prices will make home equity withdrawal less feasible

• Inflation will probably continue at a rate higher than wage increases

Effects of compounding

There is a well-noted tendency in economics studies for most people to favour immediate consumption rather than saving for future consumption. This leads to a tendency to underestimate the effects of compound interest. This issue is critically important in judging the amount of retail space needed in future years.

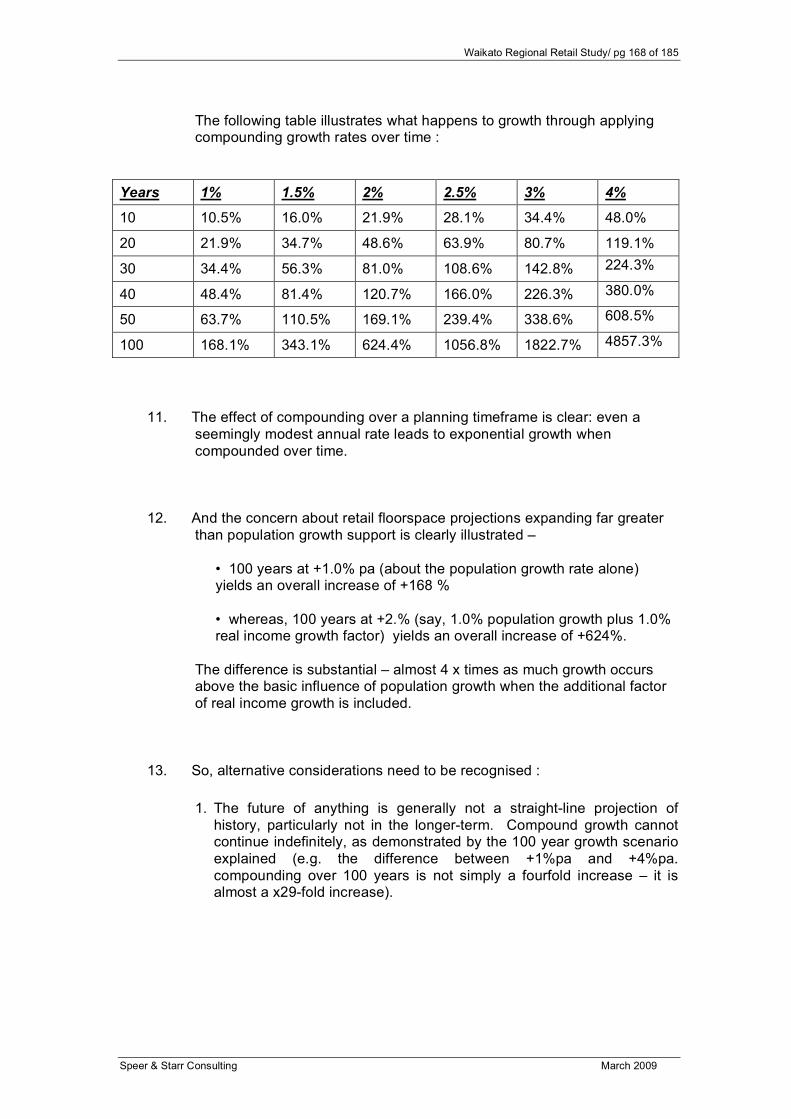

The effects of compounding over a planning timeframe are clear: even a modest-seeming annual rate leads to exponential growth when compounded over time. Over 20 years, a 2% real growth rate would require a nearly 50% increase in retail sales.

Increase in retail sales required at real growth rate of:

Years 1% 2% 3% 4%

10 10.5% 21.9% 34.4% 48.0%

20 22.0% 48.6% 80.6% 119.1%

30 34.8% 81.1% 142.7% 224.3%

40 48.9% 120.8% 226.2% 380.1%

50 63.7% 169.1% 338.6% 608.5%

Overall conclusion: projected retail growth rate

When all factors, positive and negative, are considered, we judge that a prudent growth factor for the Waikato is real retail growth of about 1% per annum, not including the influence of population growth.

Waikato Regional Retail Study/ pg 119 of 185

Speer & Starr Consulting March 2009

4. Demand for Additional Retail Floorspace In this section, we employ a model for future demand. We identify the methodology and assumptions used, and the outcomes for potential demand for new retail floorspace over the next 20-year planning period, 2006 -2026. Background: Modelling Retail Space and Land needs

How retailers respond to demand changes

Real changes in retail spending are measured in “constant dollars” by deducting inflation as measured by the Consumer Price Index (CPI). If retail spending increases in real terms, this means that more physical goods are sold, and more services produced and sold.

The retail environment will need to react to an increase in demand with a mix of three types of responses. Any or all of these responses may occur:

• Sell more goods and services through existing retail facilities, resulting in higher sales per square metre

and/or

• Expand existing retail facilities

and/or

• Build additional new retail facilities

The amount of new retail land required (if any) will be directly affected by a) the level of increased demand and b) the responses current and new retailers make to changing sales patterns.

Optimising retail space

There is an optimal level of sales for a given retail facility, which also holds true for shopping precincts and the overall retail network.

If retail sales per store are too low, ramifications include:

• Reduced employment per store

o Resulting in lower-intensity usage with less economic output

o Impairing customer service levels

• Lack of reinvestment, leading to deteriorating facilities

• Reduction of stock levels and variety

These issues may, in turn, lead to:

• Fewer customers

Waikato Regional Retail Study/ pg 120 of 185

Speer & Starr Consulting March 2009

• A “downward spiral” as the retailer/area become unappealing

• Financial failures of retailers

• Store vacancies

If retail sales per store are too high, retailer profitability generally increases, but customer satisfaction reduces. This can reduce the long-term sales growth rate. Ramifications of selling too much per store (“overtrading”) include:

• Traffic congestion

• Difficulty in parking

• Crowded stores

• Above-average out-of-stock levels for products

• Reduced customer service

This will lead to a lower growth rate than would otherwise be achieved, and will often stimulate new competing stores to open. If the new stores are too large relative to the overall aggregate demand, the retailing system then has an oversupply of space. This can lead to reduced sales per store, with the problems noted above.

Overall, the retail market is constantly adjusting to too much, or too little, floor space due to a wide range of stimuli. The challenge for any planning agency is to have a retail strategy that can make available the ”right amount of retail space” with neither serious shortages nor gross oversupplies at any given time.

Strategic Concerns

Broader strategic concerns are worth mentioning in this regard.

Overspending: The Reserve Bank was concerned (as of 2007-2008) that New Zealanders were spending more than their current incomes, and this led to one of the tightest monetary policies in the world. Despite major reductions in interest rates in 2008, New Zealand rates are still above those in many other countries. The Reserve Bank would prefer that retail space be minimised to reduce this effect.

Employment: In terms of income and local employment, it should be noted that jobs in retailing require relatively low skills, and are quite low paid compared to manufacturing or other occupations. An over-provision of retail land may have an opportunity cost if more desirable employment options are bypassed.

Foregone amenities: Retailing is generally placed in prime, easily-accessible locations. Devoting these areas to retailing means they cannot be used for other purposes which may have higher amenity value.

Waikato Regional Retail Study/ pg 121 of 185

Speer & Starr Consulting March 2009

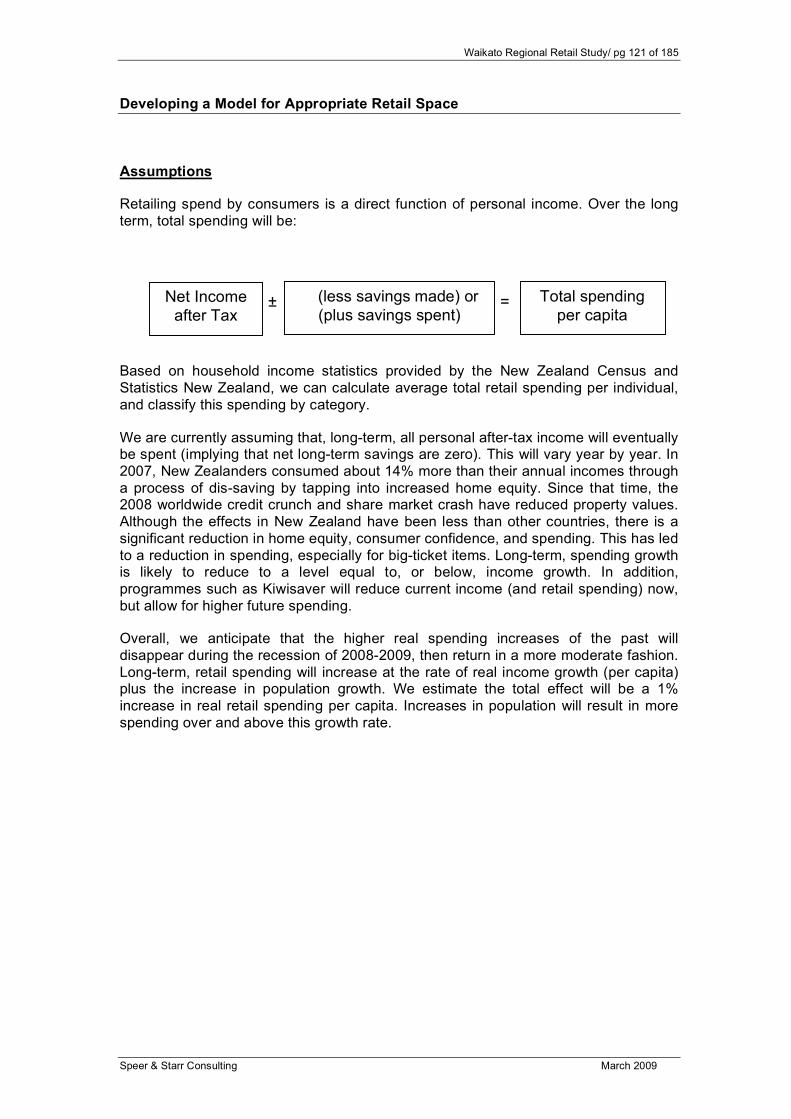

Developing a Model for Appropriate Retail Space

Assumptions

Retailing spend by consumers is a direct function of personal income. Over the long term, total spending will be:

Based on household income statistics provided by the New Zealand Census and Statistics New Zealand, we can calculate average total retail spending per individual, and classify this spending by category.

We are currently assuming that, long-term, all personal after-tax income will eventually be spent (implying that net long-term savings are zero). This will vary year by year. In 2007, New Zealanders consumed about 14% more than their annual incomes through a process of dis-saving by tapping into increased home equity. Since that time, the 2008 worldwide credit crunch and share market crash have reduced property values. Although the effects in New Zealand have been less than other countries, there is a significant reduction in home equity, consumer confidence, and spending. This has led to a reduction in spending, especially for big-ticket items. Long-term, spending growth is likely to reduce to a level equal to, or below, income growth. In addition, programmes such as Kiwisaver will reduce current income (and retail spending) now, but allow for higher future spending.

Overall, we anticipate that the higher real spending increases of the past will disappear during the recession of 2008-2009, then return in a more moderate fashion. Long-term, retail spending will increase at the rate of real income growth (per capita) plus the increase in population growth. We estimate the total effect will be a 1% increase in real retail spending per capita. Increases in population will result in more spending over and above this growth rate.

= ± Net Income after Tax

(less savings made) or (plus savings spent)

Total spending per capita

Waikato Regional Retail Study/ pg 122 of 185

Speer & Starr Consulting March 2009

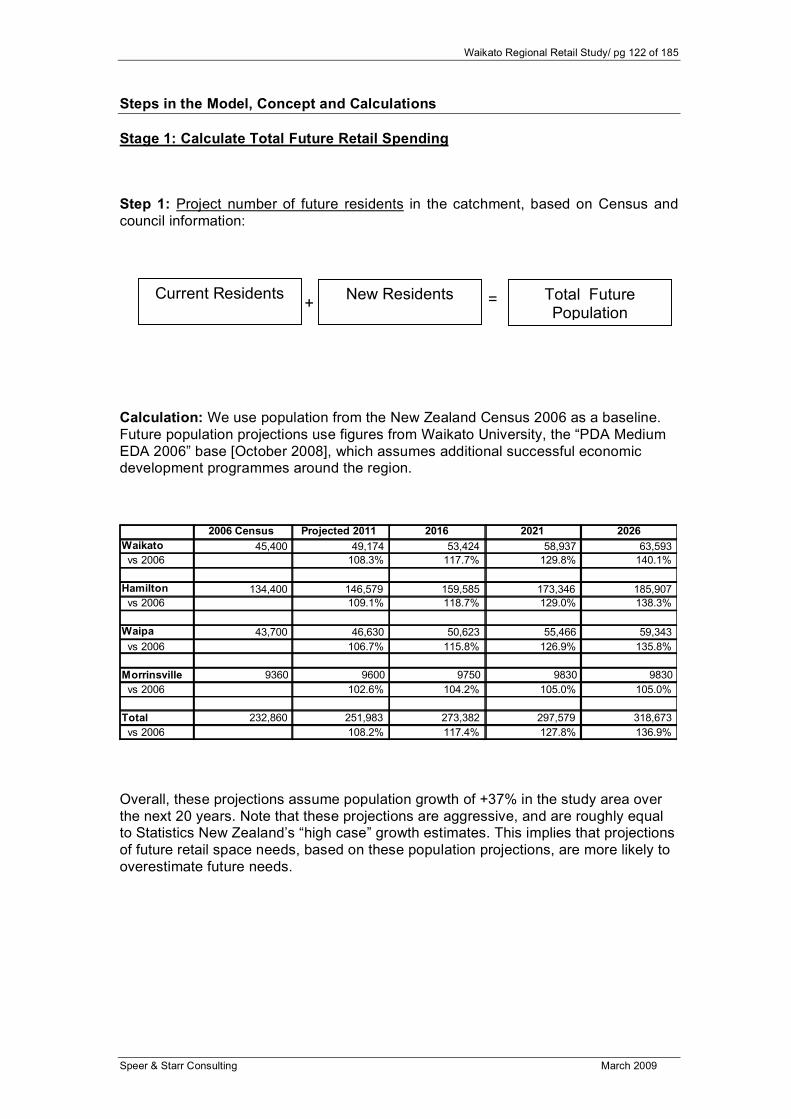

Steps in the Model, Concept and Calculations

Stage 1: Calculate Total Future Retail Spending

Step 1: Project number of future residents in the catchment, based on Census and council information:

Calculation: We use population from the New Zealand Census 2006 as a baseline. Future population projections use figures from Waikato University, the “PDA Medium EDA 2006” base [October 2008], which assumes additional successful economic development programmes around the region.

2006 Census Projected 2011 2016 2021 2026

Waikato 45,400 49,174 53,424 58,937 63,593

vs 2006 108.3% 117.7% 129.8% 140.1%

Hamilton 134,400 146,579 159,585 173,346 185,907

vs 2006 109.1% 118.7% 129.0% 138.3%

Waipa 43,700 46,630 50,623 55,466 59,343

vs 2006 106.7% 115.8% 126.9% 135.8%

Morrinsville 9360 9600 9750 9830 9830

vs 2006 102.6% 104.2% 105.0% 105.0%

Total 232,860 251,983 273,382 297,579 318,673

vs 2006 108.2% 117.4% 127.8% 136.9%

Overall, these projections assume population growth of +37% in the study area over the next 20 years. Note that these projections are aggressive, and are roughly equal to Statistics New Zealand’s “high case” growth estimates. This implies that projections of future retail space needs, based on these population projections, are more likely to overestimate future needs.

Current Residents New Residents = + Total Future Population

Waikato Regional Retail Study/ pg 123 of 185

Speer & Starr Consulting March 2009

Step 2: Calculate current retail sales per capita as a national average:

Calculation: We use the Statistics New Zealand Retail Trade Survey, March 2008, and 2008 population [from Waikato University, “PDA Medium EDA 2006” base, October 2008] to calculate:

Total Retail Sales 2008 $ (millions)Excluding vehicles, fuel,

repairs, accommodation 44,706.00$

Divided by Population 2008 4,262,900

=

Retail sales per capita 10,487.23$ (national average)

- Total retail sales 2008

Less vehicles & accommodation

÷ Population

= Current retail spend per capita

Waikato Regional Retail Study/ pg 124 of 185

Speer & Starr Consulting March 2009

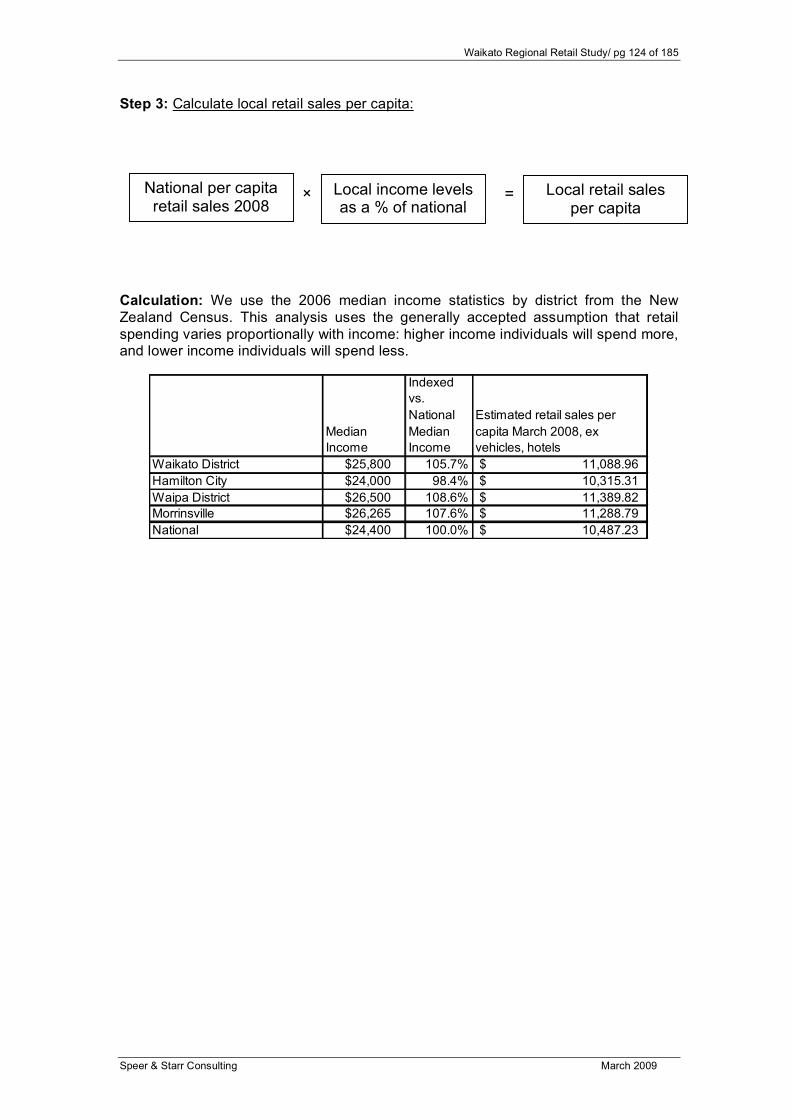

Step 3: Calculate local retail sales per capita:

Calculation: We use the 2006 median income statistics by district from the New Zealand Census. This analysis uses the generally accepted assumption that retail spending varies proportionally with income: higher income individuals will spend more, and lower income individuals will spend less.

Median

Income

Indexed

vs.

National

Median

Income

Estimated retail sales per

capita March 2008, ex

vehicles, hotels

Waikato District $25,800 105.7% 11,088.96$

Hamilton City $24,000 98.4% 10,315.31$

Waipa District $26,500 108.6% 11,389.82$

Morrinsville $26,265 107.6% 11,288.79$

National $24,400 100.0% 10,487.23$

× National per capita retail sales 2008

Local income levels as a % of national

= Local retail sales per capita

Waikato Regional Retail Study/ pg 125 of 185

Speer & Starr Consulting March 2009

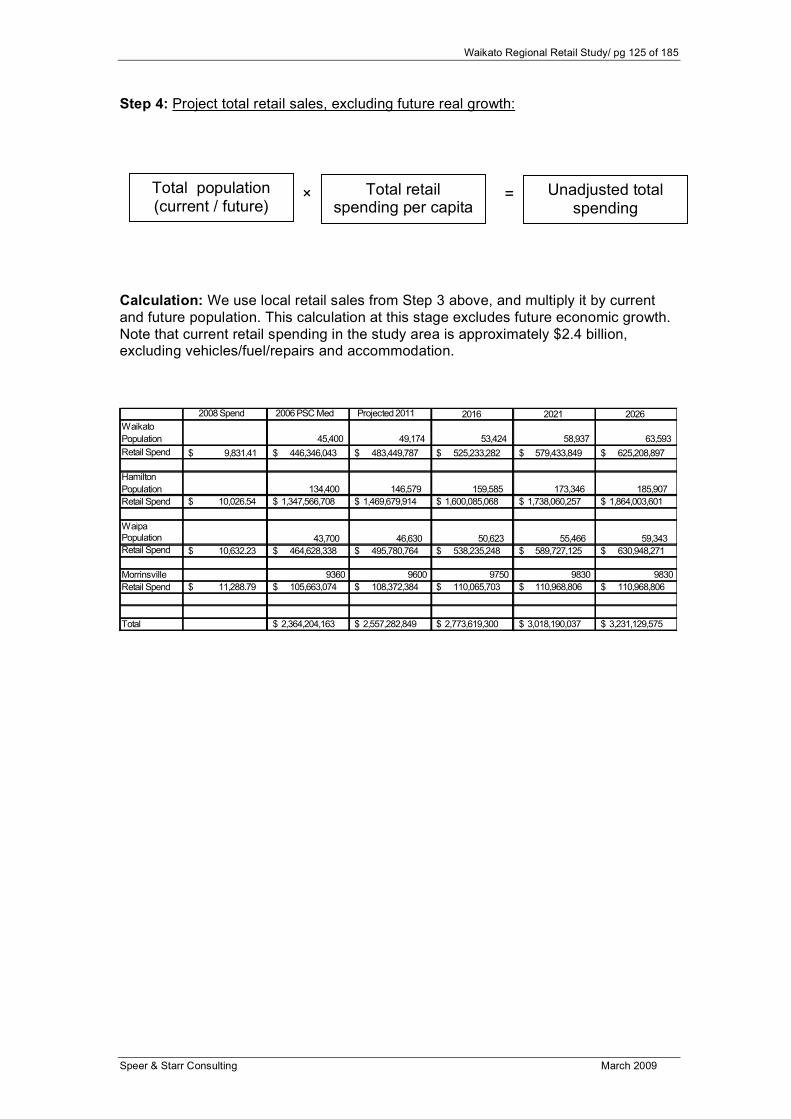

Step 4: Project total retail sales, excluding future real growth:

Calculation: We use local retail sales from Step 3 above, and multiply it by current and future population. This calculation at this stage excludes future economic growth. Note that current retail spending in the study area is approximately $2.4 billion, excluding vehicles/fuel/repairs and accommodation.

2008 Spend 2006 PSC Med Projected 2011 2016 2021 2026

Waikato

Population 45,400 49,174 53,424 58,937 63,593

Retail Spend 9,831.41$ 446,346,043$ 483,449,787$ 525,233,282$ 579,433,849$ 625,208,897$

Hamilton

Population 134,400 146,579 159,585 173,346 185,907

Retail Spend 10,026.54$ 1,347,566,708$ 1,469,679,914$ 1,600,085,068$ 1,738,060,257$ 1,864,003,601$

Waipa Population 43,700 46,630 50,623 55,466 59,343 Retail Spend 10,632.23$ 464,628,338$ 495,780,764$ 538,235,248$ 589,727,125$ 630,948,271$

Morrinsville 9360 9600 9750 9830 9830

Retail Spend 11,288.79$ 105,663,074$ 108,372,384$ 110,065,703$ 110,968,806$ 110,968,806$

Total 2,364,204,163$ 2,557,282,849$ 2,773,619,300$ 3,018,190,037$ 3,231,129,575$

× Total population (current / future)

Total retail spending per capita

= Unadjusted total spending

Waikato Regional Retail Study/ pg 126 of 185

Speer & Starr Consulting March 2009

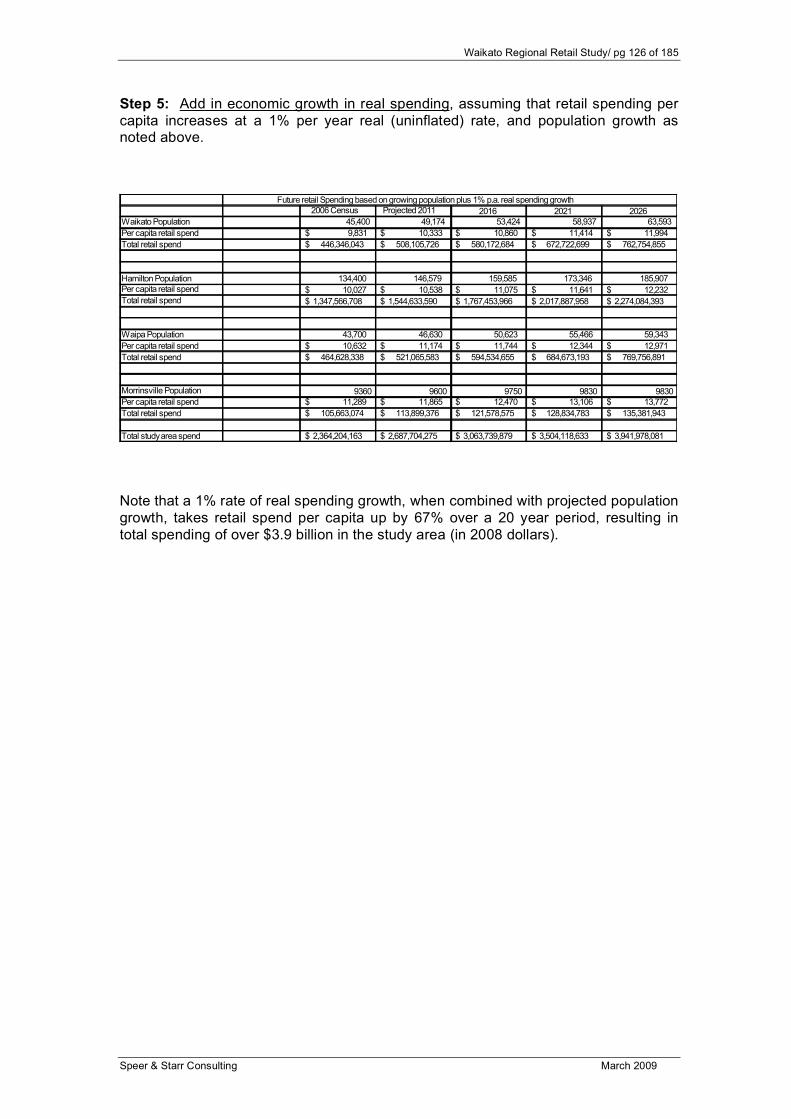

Step 5: Add in economic growth in real spending, assuming that retail spending per capita increases at a 1% per year real (uninflated) rate, and population growth as noted above.

2006 Census Projected 2011 2016 2021 2026Waikato Population 45,400 49,174 53,424 58,937 63,593

Per capita retail spend 9,831$ 10,333$ 10,860$ 11,414$ 11,994$

Total retail spend 446,346,043$ 508,105,726$ 580,172,684$ 672,722,699$ 762,754,855$

Hamilton Population 134,400 146,579 159,585 173,346 185,907 Per capita retail spend 10,027$ 10,538$ 11,075$ 11,641$ 12,232$ Total retail spend 1,347,566,708$ 1,544,633,590$ 1,767,453,966$ 2,017,887,958$ 2,274,084,393$

Waipa Population 43,700 46,630 50,623 55,466 59,343

Per capita retail spend 10,632$ 11,174$ 11,744$ 12,344$ 12,971$

Total retail spend 464,628,338$ 521,065,583$ 594,534,655$ 684,673,193$ 769,756,891$

Morrinsville Population 9360 9600 9750 9830 9830Per capita retail spend 11,289$ 11,865$ 12,470$ 13,106$ 13,772$

Total retail spend 105,663,074$ 113,899,376$ 121,578,575$ 128,834,783$ 135,381,943$

Total study area spend 2,364,204,163$ 2,687,704,275$ 3,063,739,879$ 3,504,118,633$ 3,941,978,081$

Future retail Spending based on growing population plus 1% p.a. real spending growth

Note that a 1% rate of real spending growth, when combined with projected population growth, takes retail spend per capita up by 67% over a 20 year period, resulting in total spending of over $3.9 billion in the study area (in 2008 dollars).

Waikato Regional Retail Study/ pg 127 of 185

Speer & Starr Consulting March 2009

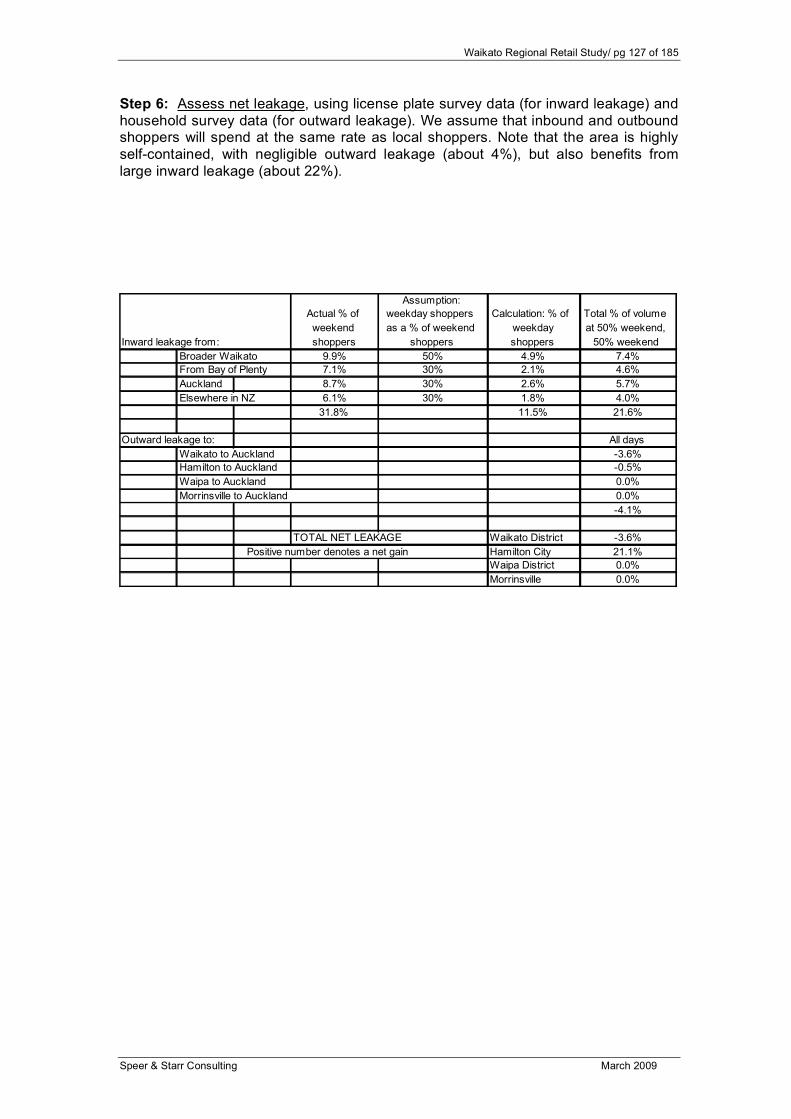

Step 6: Assess net leakage, using license plate survey data (for inward leakage) and household survey data (for outward leakage). We assume that inbound and outbound shoppers will spend at the same rate as local shoppers. Note that the area is highly self-contained, with negligible outward leakage (about 4%), but also benefits from large inward leakage (about 22%).

Actual % of

weekend

shoppers

Assumption:

weekday shoppers

as a % of weekend

shoppers

Calculation: % of

weekday

shoppers

Total % of volume

at 50% weekend,

50% weekend

Broader Waikato 9.9% 50% 4.9% 7.4%

From Bay of Plenty 7.1% 30% 2.1% 4.6%

Auckland 8.7% 30% 2.6% 5.7%

Elsewhere in NZ 6.1% 30% 1.8% 4.0%

31.8% 11.5% 21.6%

Outward leakage to: All days

Waikato to Auckland -3.6%

Hamilton to Auckland -0.5%

Waipa to Auckland 0.0%

Morrinsville to Auckland 0.0%

-4.1%

TOTAL NET LEAKAGE Waikato District -3.6%

Positive number denotes a net gain Hamilton City 21.1%

Waipa District 0.0%

Morrinsville 0.0%

Inward leakage from:

Waikato Regional Retail Study/ pg 128 of 185

Speer & Starr Consulting March 2009

Step 7: Calculate total current and future spending, by adding in effects of positive leakage to the unadjusted spending totals from Step 5:

Leakage 2006 Census Projected 2011 2016 2021 2026Waikato Population 43,400 49,174 53,424 58,937 63,593

Per capita retail spend 9,831$ 10,333$ 10,860$ 11,414$ 11,994$

Total retail spend 426,683,222$ 508,105,726$ 580,172,684$ 672,722,699$ 762,754,855$

With outward leakage -3.6% 411,322,626$ 489,813,920$ 559,286,467$ 648,504,682$ 735,295,680$

Hamilton Population 131,700 146,579 159,585 173,346 185,907 Per capita retail spend 10,027$ 10,538$ 11,075$ 11,641$ 12,232$ Total retail spend 1,320,495,055$ 1,544,633,590$ 1,767,453,966$ 2,017,887,958$ 2,274,084,393$ Net inward leakage 21.1% 1,599,119,512$ 1,870,551,277$ 2,140,386,752$ 2,443,662,318$ 2,753,916,200$

Waipa Population 42,500 46,630 50,623 55,466 59,343

Per capita retail spend 10,632$ 11,174$ 11,744$ 12,344$ 12,971$

Total retail spend 451,869,665$ 521,065,583$ 594,534,655$ 684,673,193$ 769,756,891$

No leakage 0.0% 451,869,665$ 521,065,583$ 594,534,655$ 684,673,193$ 769,756,891$

Morrinsville Population 9360 9600 9750 9830 9830Per capita retail spend 11,289$ 11,865$ 12,470$ 13,106$ 13,772$

Total retail spend 105,663,074$ 113,899,376$ 121,578,575$ 128,834,783$ 135,381,943$

No leakage 105,663,074$ 113,899,376$ 121,578,575$ 128,834,783$ 135,381,943$

Total study area spend 2,567,974,877$ 2,995,330,156$ 3,415,786,449$ 3,905,674,975$ 4,394,350,714$

Future retail spending, with growing population, 1% p.a. real spending growth, and leakage

These 7 steps result in a sound estimate of the total retail spending that can be expected in the study area in the future.

Waikato Regional Retail Study/ pg 129 of 185

Speer & Starr Consulting March 2009

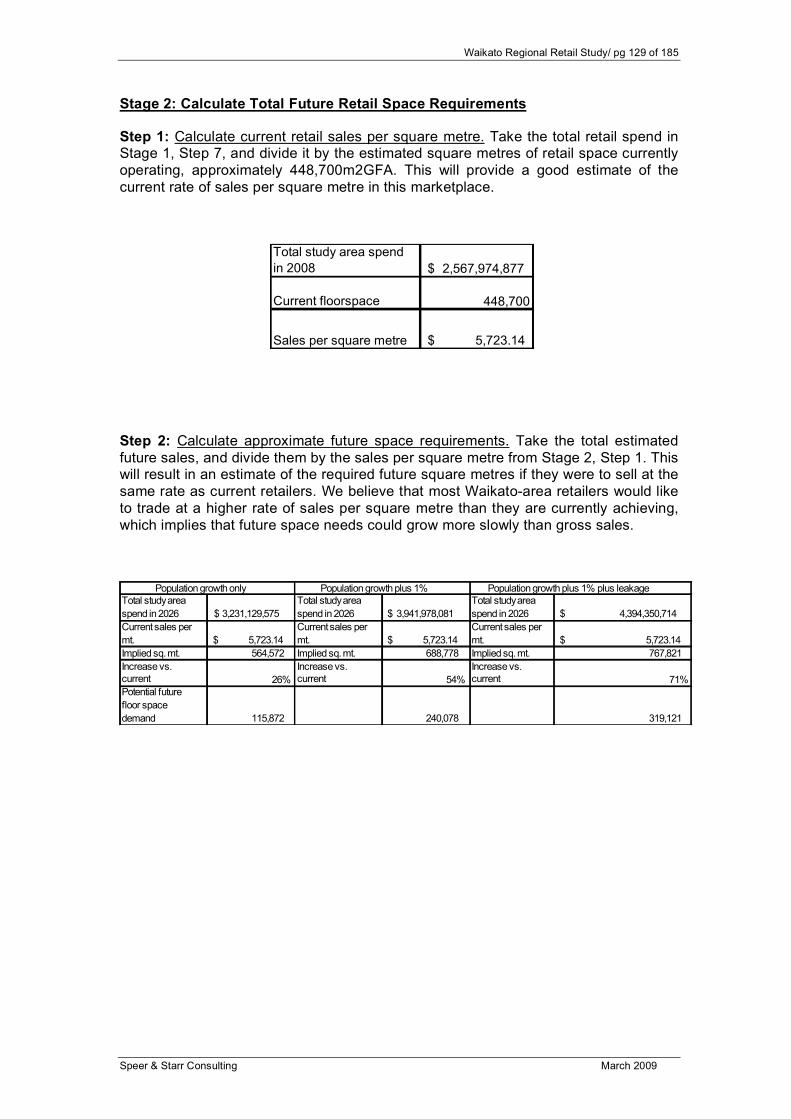

Stage 2: Calculate Total Future Retail Space Requirements

Step 1: Calculate current retail sales per square metre. Take the total retail spend in Stage 1, Step 7, and divide it by the estimated square metres of retail space currently operating, approximately 448,700m2GFA. This will provide a good estimate of the current rate of sales per square metre in this marketplace.

Total study area spend

in 2008 2,567,974,877$

Current floorspace 448,700

Sales per square metre 5,723.14$

Step 2: Calculate approximate future space requirements. Take the total estimated future sales, and divide them by the sales per square metre from Stage 2, Step 1. This will result in an estimate of the required future square metres if they were to sell at the same rate as current retailers. We believe that most Waikato-area retailers would like to trade at a higher rate of sales per square metre than they are currently achieving, which implies that future space needs could grow more slowly than gross sales.

Total study area

spend in 2026 3,231,129,575$

Total study area

spend in 2026 3,941,978,081$

Total study area

spend in 2026 4,394,350,714$

Current sales per

mt. 5,723.14$

Current sales per

mt. 5,723.14$

Current sales per

mt. 5,723.14$

Implied sq. mt. 564,572 Implied sq. mt. 688,778 Implied sq. mt. 767,821

Increase vs. current 26%

Increase vs. current 54%

Increase vs. current 71%

Potential future

floor space

demand 115,872 240,078 319,121

Population growth only Population growth plus 1% Population growth plus 1% plus leakage

Waikato Regional Retail Study/ pg 130 of 185

Speer & Starr Consulting March 2009

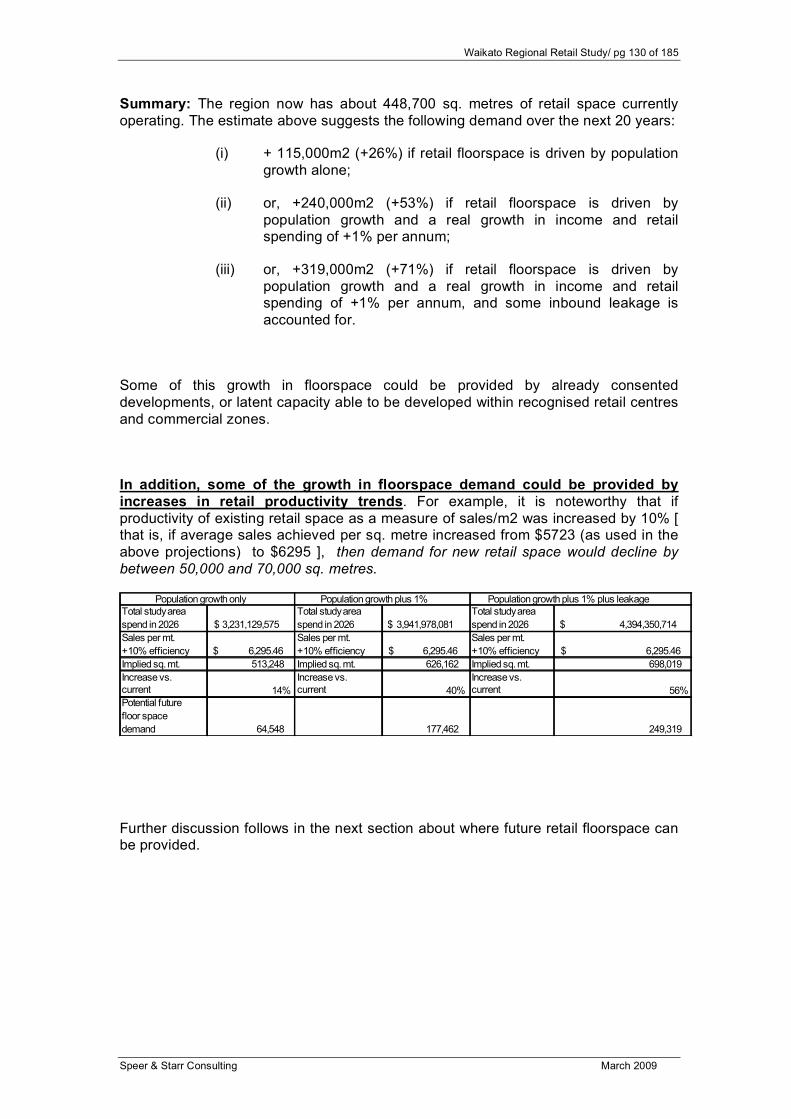

Summary: The region now has about 448,700 sq. metres of retail space currently operating. The estimate above suggests the following demand over the next 20 years:

(i) + 115,000m2 (+26%) if retail floorspace is driven by population growth alone;

(ii) or, +240,000m2 (+53%) if retail floorspace is driven by population growth and a real growth in income and retail spending of +1% per annum;

(iii) or, +319,000m2 (+71%) if retail floorspace is driven by population growth and a real growth in income and retail spending of +1% per annum, and some inbound leakage is accounted for.

Some of this growth in floorspace could be provided by already consented developments, or latent capacity able to be developed within recognised retail centres and commercial zones.

In addition, some of the growth in floorspace demand could be provided by increases in retail productivity trends. For example, it is noteworthy that if productivity of existing retail space as a measure of sales/m2 was increased by 10% [ that is, if average sales achieved per sq. metre increased from $5723 (as used in the above projections) to $6295 ], then demand for new retail space would decline by between 50,000 and 70,000 sq. metres.

Total study area

spend in 2026 3,231,129,575$

Total study area

spend in 2026 3,941,978,081$

Total study area

spend in 2026 4,394,350,714$

Sales per mt.

+10% efficiency 6,295.46$

Sales per mt.

+10% efficiency 6,295.46$

Sales per mt.

+10% efficiency 6,295.46$

Implied sq. mt. 513,248 Implied sq. mt. 626,162 Implied sq. mt. 698,019

Increase vs. current 14%

Increase vs. current 40%

Increase vs. current 56%

Potential future

floor space

demand 64,548 177,462 249,319

Population growth only Population growth plus 1% Population growth plus 1% plus leakage

Further discussion follows in the next section about where future retail floorspace can be provided.

Waikato Regional Retail Study/ pg 131 of 185

Speer & Starr Consulting March 2009

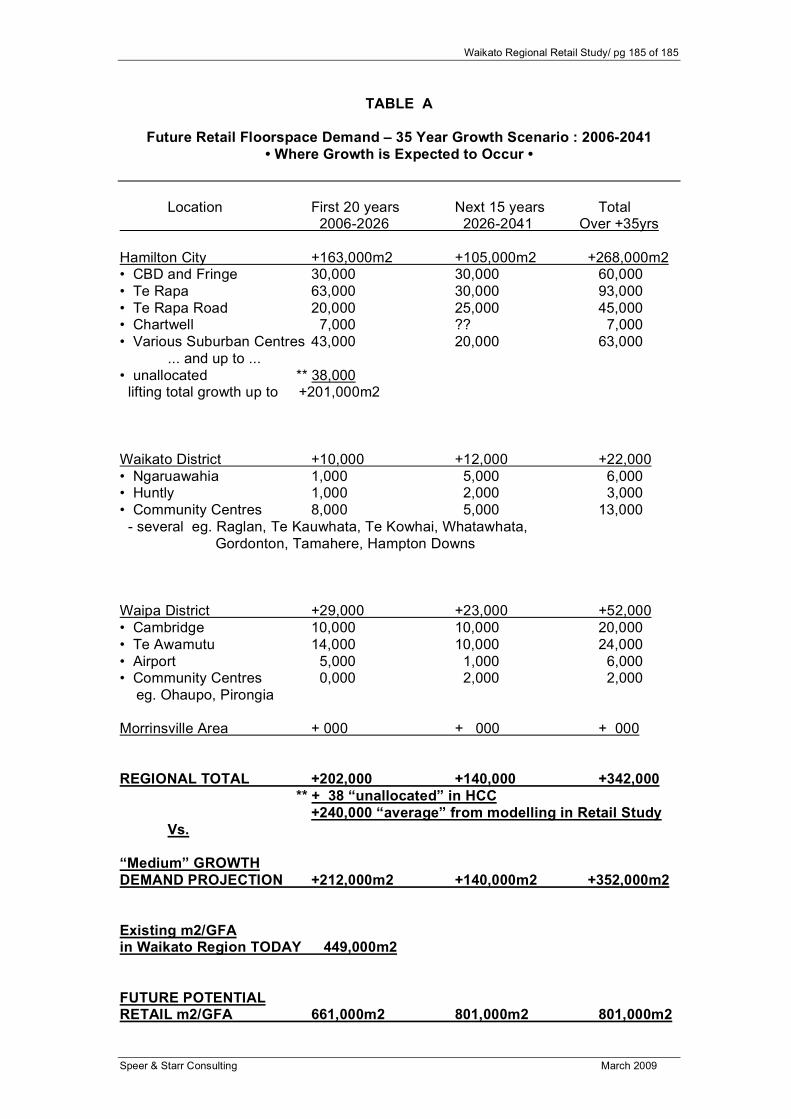

5. “Where” to Provide for Additional Floorspace Report Sector 4 considered the “demand” issue to help identify a likely range of new retail floorspace potentially required over the next 20 years. The results identified : • Current Base = 448,700m2 ... plus future growth for 20yrs to 2026... • Option (i) = +115,000m2 based on population growth only; • Option (ii) = +240,000m2 based on population growth and +1% p.a income/spending growth • Option (iii) = +319,000m2 based on population growth and +1% p.a income/spending growth and inbound leakage influences. A subsequent question is : where should this additional floorspace be provided? Hamilton City As the main regional commercial centre, Hamilton City is an obvious starting point for this assessment, but we also look at local features in Waikato and Waipa and Morrinsville areas. The research undertaken during this project has confirmed the importance of Hamilton to the wider Region, recalling key findings like:

• around 26% of customers to the three major city retail centres come from Waikato-Waipa-Morrinsville; plus, there is a significant “tourist/passing traffic” component worth another 24%;

• over 50% of Waikato District residents make use of Hamilton businesses on a regular basis for a wide range of retail activities;

• Waipa residents making strong use of local town centres for many retail goods but relying on Hamilton businesses for specialist goods;

• Morrinsville residents have a shopping pattern similar to Waipa residents, making strong use of local town centres for many retail goods but relying on Hamilton businesses for specialist goods;

As a starting point, we have investigated what opportunities exist for new development within existing commercial centres. To do this we have undertaken interviews with major retail property owners in Hamilton, and also discussions with council officers to identify known potential future retail developments. Business Interviews (i) Major Retail Property Owners We were able to obtain interviews with representatives from the 5 x major retail property owners around the City: Tainui Group Holdings, Jonmar Property/AMP Group, Westfield NZ Limited, Kiwi Income Property Trust, and Dominion Funds Limited. We discussed with the management at these businesses their views on future retail development around Hamilton and for their specific land holdings.

Waikato Regional Retail Study/ pg 132 of 185

Speer & Starr Consulting March 2009

• Tainui Group Holdings Limited (meeting with Nathan York, general manager property) Tainui Group is a major landowner around Hamilton City. Its property interests

range across retail, hotels, offices, education, residential, and rural activities. In a retail context, the Group’s primary asset is The Base, a major retail centre

located in Te Rapa at the northern edge of the city. The Base is a large multi-staged development. To date, around 36,000m2GFA has been developed with emphasise on large-format retailing but also including a freestanding Dressmart Centre. Future development capacity for another 25,000m2 has received planning consent, broadly falling into two parts : more large-format retailing up to around 7,000m2, and a new integrated mall at around 18,000m2.

Into the future, the Group expects to see the Base will go through an evolution where is becomes more of a “town centre” with a broadened range of activities including offices, leisure/recreation, and motel/hotel accommodation. A major railway station/ transportation hub is being provided for.

A second retail project involving Tainui Group is as the owner of the WINTEC

tertiary education site, located central to the CBD. Particularly relevant to this site is potential re-development of land directly along Ward Street frontage for retail purposes. This land is directly across the street from the Hamilton Central Mall, and across the street (across Anglesea Street) from Downtown Plaza and Centre Place and the core retail focus to the CBD.

Re-development of Ward Street into more of a “main street” character is one of

the matters which the City Council has been working on recently as part of its City Heart Revitalisation project. The main focus for upgrading Ward Street has been in the precinct between Angelsea St and Victoria St (generally between Centre Place and Downtown Plaza, with Ward Street running through the middle of these two centres). None-the-less, Tainui have collaborated with Council and other property owners (including Dominion Funds, owner of Hamilton Central Plaza across the street from WINTEC and fronting Ward Street) about integrating Ward St. “west”” precinct around WINTEC with Ward St. “east”.

Main-streeting Ward Street has wider application to the City’s vision to more

closely integrate the CBD with re-development work around the city centre including work proceeding at Claudelands Events Centre and the need for associated upgrading between these two activity centres.

A third matter mentioned by Tainui is an interest to broaden the City’s east-west

focus and minimise its north-south extention. In particular, Tainui is the owner of land in the Ruakura area (eastern fringe of the city), and would like to see a significant part of this land used to emphasise new industry and business as a means to help break-down the “live in the east, work in the west” scenario that currently applies. Specific to retail, it has been suggested that part of this area could include some form of “suburban retail centre” – something considerably less than The Base or Chartwell, and more akin to a Thomas Road or Dinsdale scale centre with a distinctly local business trading focus.

• Jonmer Property/AMP Group (discussions with David Haines from Haines Planning,

as representative for Jonmar Property; also with Darren Pocock, AMP development executive)

Waikato Regional Retail Study/ pg 133 of 185

Speer & Starr Consulting March 2009

Jonmer/AMP are now joint owners of the “Supa Centa” site in Te Rapa. Jonmer has undertaken several “supa centa” projects around the country, its largest being the Manukau Supa Centa at Manukau City Centre. AMP Group has been a major retail developer and long-term investor over many years, with its current “signature project” being Botany Town Centre in Auckland. Their Hamilton property is about 1km north of The Base, and is currently comprised of Placemakers and Harvey Norman operations but otherwise is vacant land with capacity for considerable new development up to around +35,000m2GFA. The site has a Commercial Services Zone, enabling retail development for large-format retail and/or an integrated mall if greater than 5,000m2,

Waikato Regional Retail Study/ pg 134 of 185

Speer & Starr Consulting March 2009

These companies confirmed their long-term interest in developing the site for retail. In the short-term, the nearby Base has achieved stronger development momentum, but ultimately development will proceed on the Supa Centa site – it is seen as only a matter of timing. AMP in particular has a long-term business vision and practices land banking to provide for future development opportunities; their Hamilton site is seen in this light.

• Westfield NZ Limited (meeting with Clive Mackenzie, general manager development;

and Allan Lockie, development executive) Westfield is the largest shopping centre owner in New Zealand, and in Hamilton is

the owner of the Chartwell Mall located in the northeast sector of the city. During 2006/2007, Chartwell was expanded by +8,000m2 including expansion of a Foodtown supermarket, new shops, and a new cinema complex around 3,500m2. This lifted the total centre size to around 22,000m2GLA.

Planning consent for further expansion has been recently issued in March 2008,

enabling the addition of a further +7,000m2 through expansion of the centre in a southerly direction by converting existing open carpark land into shops plus a carpark building. When complete, total centre size will be around 29,000m2 – a significant shopping centre within a NZ context – cf. Westfield 277 Newmarket, 22,000m2; Westfield Glenfield, 31,000m2; Westfield Manukau City, 32,000m2;

Our discussions with management highlighted their interest in expanding

Chartwell even further, as and when it was economic to do so. They also put forward their opinion on future retail development for Hamilton City, which is an interest to see a “centres based” strategy adopted including integrating retail centres with public transport. They also expressed concern to avoid any changes to existing retail controls in industrial zones which might reduce permitted retailing below the existing 1000m2GFA minimum size, because a collection of multiple smaller shops could create alternative focal points outside of acknowledged “centres” for traditional specialty shop retailing in areas like fashion and homewares, with consequential dispersion of shopping and dilution of economic strength away from established centres. This is an approach which the company has generally adopted in many planning exercises around the country.

• Kiwi Income Property Trust (meeting with Mark Luker, general manager development;

and Ivan Bartley, development manager) Kiwi is a large national property company with development interests spanning

many activities including shopping malls. Their “signature retail project” currently is Sylvia Park in Auckland, but locally Kiwi operates the two largest shopping centres in the CBD precinct – Centre Place, and across the street is Downtown Plaza.

Philosophically, management confirmed its commitment to a “centres based’

development strategy for the city which emphasises the use and enhancement of existing assets. They reiterated some fundamental economic differences between central city / shopping mall retailing and more fringe retail locations, where basic rent/operating costs can differ by 200-300%. It was acknowledged that not all retail tenants can afford to pay higher rentals, but cautioned that if a major retail focus with a significantly lower cost structure, is developed outside acknowledged centres, then it becomes very difficult to maintain/attract tenants in central locations and difficult to justify any additional investment in central city properties.

Waikato Regional Retail Study/ pg 135 of 185

Speer & Starr Consulting March 2009

At this time, Kiwi management has expressed its strong interest in re-developing

and expanding its central city properties. Adjacent properties to the two main shopping centres have been acquired to help round-out development potential. A comprehensive redesign of all properties is underway with an intent to achieve stronger integration on all fronts -- linking Centre Place with Downtown Plaza, with Garden Place and other CBD retail beyond, with Ward Street frontage (on the south side including “main streeting” building fronts and walkways), and with Barton Street precinct (on the north side).

Essentially, the Kiwi land holding can be considered a core location to the City’s

CBD, with important linkages in all directions. At this time, up to around +20,000m2 of expansion is under consideration – this is 100% increase over the current retail base of 15,500m2 in Centre Place and 5,000m2 in Downtown Plaza.

If redevelopment of the magnitude suggested did occur here, it would represent a

very significant commitment to the future strength of the CBD business base, and is a matter that requires regard in any future retail strategy.

• Dominion Funds (meeting with Andrew Bishop, national retail manager) Dominion is the owner of Hamilton Central Mall, located at the western fringe to

the CBD precinct; it is more or less across the street (across Angelsea Street) from Centre Place and Downtown Plaza, across Ward Street from WINTEC and its concept for street front redevelopment, and adjacent a new freestanding Warehouse building.

Today, Central Mall consists of a large K-Mart department store, and about 20

other small shops. Dominion acknowledges that currently the centre is in an undesirable state, and a comprehensive re-development is being planned. Dominion has collaborated with the City regarding the “main-streeting” of Ward Street frontage, and Dominion’s redesign of its centre includes expansion onto properties fronting Ward Street (which currently have non-retail uses like vehicle servicing).

The challenge for the Central Mall is how to best integrate with the CBD retail cor,

which requires crossing Angelsea Street, plus some improved integration with the adjacent Warehouse site.

At the broader city level, management’s opinion about a city-wide retail strategy is

that it is imperative for the CBD to have a “distinction” from other retail centres, and that such a distinction can be primarily achieved through emphasising specialty shopping like fashion, homewares and design, and “lifestyle” activities like eating and entertainment. This distinction will help to maintain customer flows into city businesses and a general vibrancy in the CBD. On the other hand, concern is held over any freeing up of retail development outside of acknowledged centres, which will result in diluted customer flows into the CBD and reduced justification for any investment in central city development/re-development.

Waikato Regional Retail Study/ pg 136 of 185

Speer & Starr Consulting March 2009

(ii) Council Officer Discussions We were able to confer with council officers regarding the status of any major new retail projects either approved or in various planning stages. There are several to have regard to. • Approved planning consent has been granted for expansion at The Base, up to

+25,000m2. This has been explained above, under Tainui Group. • Approved planning consent has been granted for expansion at Chartwell Mall, up to

+7,000m2. This has been explained above, under Westfield. • Te Rapa “Homezone” - Approximately midway between the CBD and The Base,

along Te Rapa Road near Vardon Road intersection, is a new retail centre that has planning consent to proceed. It is described as a “homezone” centre – primarily a focus for home improvement type businesses. The site is adjacent the existing Bunnings Hardware site which is a very large DIY outlet around 10,000m2 GFA. The site is large, some 4.5 ha, and development is progressing in stages : a new car sales dealership has just opened along part of the Te Rapa Road frontage; a series of small shops up to 1250m2 GFA is intended to be developed along the remainder of the road frontage; and behind the roadfront businesses is the bulk of the site which is predominantly for large-format retailing up to around 12,250m2GFA. Overall, around +13,500m2GFA in new retail space can be added.

• Rotokauri Suburban Centre - Rotokauri is a major growth cell in the northwest of