Embed Size (px)

Citation preview

SOFTWARE SECTOR REVIEW

BostonTwo International Place

24 Floor

Boston, MA 02110

617-482-7501

Jeff [email protected]

San Francisco575 Market Street

31 Floor

San Francisco, CA 94105

415-288-4260

Mike [email protected]

London63 Brook St

London, W1K 4HS

United Kingdom

Phone: +44 (0) 20 7518 8900

Thierry [email protected]

2Q 2014

TECHNOLOGY • MEDIA • TELECOM GROUP:

Technology • Media • Telecom

To subscribe please email:

Investment banking services are provided by Harris Williams LLC, a registered broker-dealer and member of FINRA and SIPC, and Harris Williams & Co.Ltd, which is authorized and regulated by the Financial Conduct Authority. Harris Williams & Co. is a trade name under which Harris Williams LLC andHarris Williams & Co. Ltd conduct business.

TABLE OF CONTENTS

2

3

4

5

6

8

14

16

DEAL SPOTLIGHT

HW&CO. TMT GROUP OVERVIEW

WHAT WE’VE BEEN READING

NOTEWORTHY SOFTWARE TRANSACTIONS

SOFTWARE M&A ACTIVITY

SOFTWARE SECTOR OVERVIEWS

SOFTWARE IPO OVERVIEW

MIDDLE MARKET DEBT OVERVIEW

Technology • Media • Telecom

RECENT HW&CO. TMT TRANSACTIONS

SOFTWARE

• Application Software

• Infrastructure Software

• Data and Informatics

• Healthcare IT

• M2M Technologies

• Telecom and Data Center

Solutions

KEY FOCUS THEMES

• Big Data / Analytics

• Cloud

• Mobilization

INTERNET & DIGITAL MEDIA

• eCommerce

• Information and Media

• Consumer Internet

• eLearning

• Internet and Social Gaming

• Online Advertising and

Marketing

• Network Optimization

• SaaS and Subscription Models

• Vertical-Specific Solutions

HW&CO. TMT GROUP FOCUS AREAS

• EIGHT OFFICES

• APPROXIMATELY 225

EMPLOYEES

• 10 INDUSTRY GROUPS

Boston

San Francisco

London

Richmond

Minneapolis

Philadelphia

Cleveland

Frankfurt

HW&CO. GLOBAL PRESENCE

Technology • Media • Telecom

RECENT HW&CO. TMT TRANSACTIONS

HARRIS WILLIAMS & CO. OVERVIEW

2

has been acquired by

a division of

has been acquired by

a portfolio company of

and

has been acquired by

a portfolio company of

and

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

has received a significant investment

from

a portfolio company of

has been acquired by

a portfolio company of

has merged with

a portfolio company of

a portfolio company of

pending acquisition by

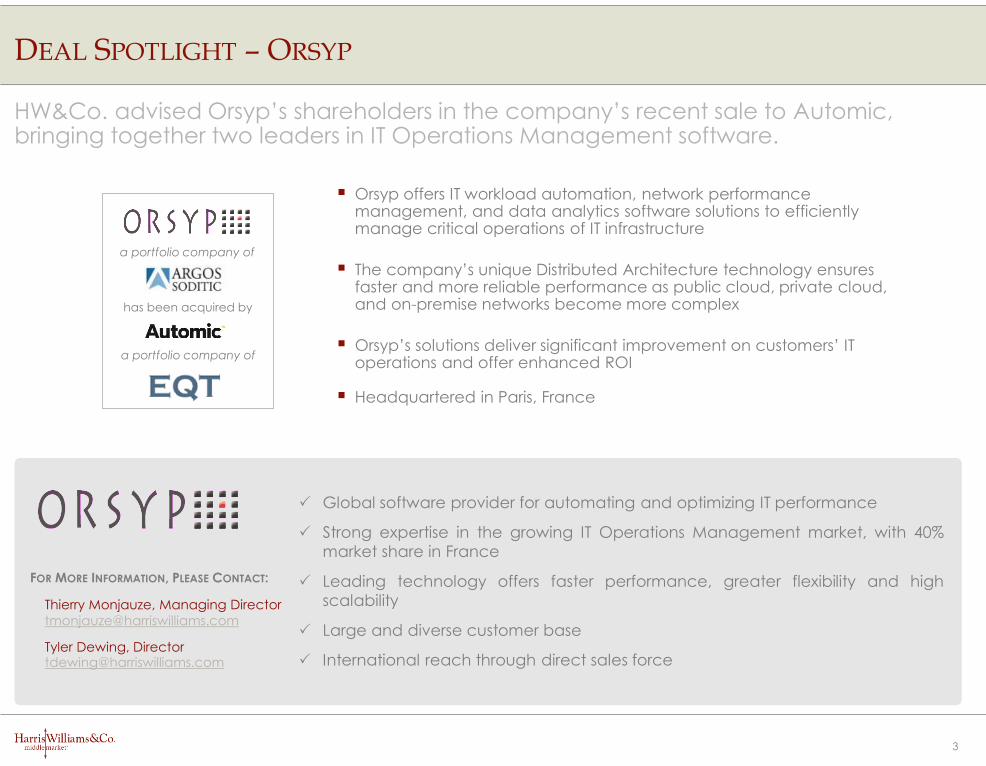

DEAL SPOTLIGHT – ORSYP

HW&Co. advised Orsyp’s shareholders in the company’s recent sale to Automic, bringing together two leaders in IT Operations Management software.

3

Global software provider for automating and optimizing IT performance

Strong expertise in the growing IT Operations Management market, with 40%

market share in France

Leading technology offers faster performance, greater flexibility and high

scalability

Large and diverse customer base

International reach through direct sales force

FOR MORE INFORMATION, PLEASE CONTACT:

Thierry Monjauze, Managing Director

Tyler Dewing, [email protected]

has been acquired by

a portfolio company of

a portfolio company of

Orsyp offers IT workload automation, network performance management, and data analytics software solutions to efficiently manage critical operations of IT infrastructure

The company’s unique Distributed Architecture technology ensures faster and more reliable performance as public cloud, private cloud, and on-premise networks become more complex

Orsyp’s solutions deliver significant improvement on customers’ IT operations and offer enhanced ROI

Headquartered in Paris, France

Internet of Things Market to Hit $7.1T by 2010: IDCZDNet, 6/5/14

According to IDC, the global Internet of Things (“IoT”) market was estimated to be $1.9 trillion in 2013and is projected to grow at an 18% CAGR through 2020 to $7.1 trillion.

The interest in IoT devices is stemming from both the consumer end market as well as increasedadoption by the business community, which is interested in the implication of the technology.

Read the full article here.

Government Support to Drive Rapid Growth in US Healthcare IT IndustryDigital Journal, 6/12/14

The U.S. Healthcare IT market is expected to grow at a 10% CAGR during 2014 to 2018, which is largelydue to declining costs of HCIT systems’ implementation, stricter government regulations, and largeincentives.

Industry trends including the emergence of cloud computing in HCIT, growing strategic collaborationsand rapid technological upgrading in the industry are also driving growth in the industry.

Read the full article here.

Analytics and Enterprise Applications to Drive Software Market Growth Until 2018VSR, 6/10/14

According to IDC, the global software market is projected to grow 5.9% YoY in 2014 and will continueto grow at a 6% CAGR until 2018.

Structured data management software, collaborative applications and data access, analysis anddelivery solutions are expected to experience the strongest growth over the five-year forecast periodwith a CAGR near 9% from 2013-2018.

Read the full articlehere.

Global Technology M&A Update: 1Q14Ernst & Young, 4/4/14

Technology M&A continued its torrid pace in the first quarter of 2014, with a 15% YoY spike in dealvolume to 758 deals and 83% YoY spike in deal value to $67B.

Private equity acquisitions represented $13B of value encompassing 70 deals, an increase for the fifthstraight quarter.

Read the full article here.

Utility Spending on Smart Grid as a Service Will Total $57.6 Billion from 2014 through 2023Navigant, 5/19/14

Smart Grid as a Service (“SGaaS”) technology is expected to drive significant growth for smallerutilities, which traditionally lack access to adequate financial and human resources.

The SGaaS market is projected to grow from $1.7 billion in 2014 to $11.2 billion in 2023, representing a23% CAGR.

Read the full report here.

Meeker’s 2014 Internet Trends Report Reveals Significant Mobile GrowthDex Media, 7/16/14

According to technology analyst Mary Meeker’s annual internet trends report for 2014, mobile datatraffic is experiencing over 81% accelerating growth, with video being the strongest driver.

Mobile usage now accounts for 25% of all web traffic, up from only 14% a year ago.

Global internet advertising grew 16% in the past year, with mobile advertising growing nearly 47%.

Read the full article here.

WHAT WE’VE BEEN READING

4

NOTEWORTHY SOFTWARE TRANSACTIONS – 2Q 2014

5

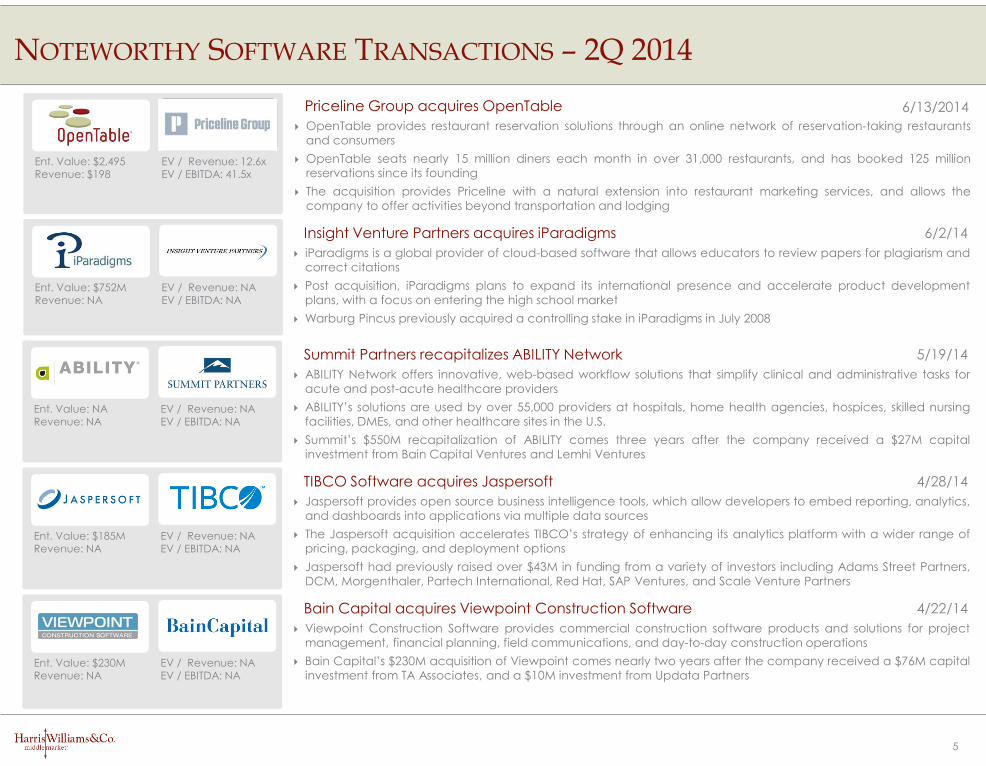

4/28/14

Ent. Value: $185MRevenue: NA

EV / Revenue: NAEV / EBITDA: NA

Jaspersoft provides open source business intelligence tools, which allow developers to embed reporting, analytics,

and dashboards into applications via multiple data sources

The Jaspersoft acquisition accelerates TIBCO’s strategy of enhancing its analytics platform with a wider range of

pricing, packaging, and deployment options

Jaspersoft had previously raised over $43M in funding from a variety of investors including Adams Street Partners,

DCM, Morgenthaler, Partech International, Red Hat, SAP Ventures, and Scale Venture Partners

TIBCO Software acquires Jaspersoft

iParadigms is a global provider of cloud-based software that allows educators to review papers for plagiarism and

correct citations

Post acquisition, iParadigms plans to expand its international presence and accelerate product development

plans, with a focus on entering the high school market

Warburg Pincus previously acquired a controlling stake in iParadigms in July 2008

Insight Venture Partners acquires iParadigms 6/2/14

Ent. Value: $752MRevenue: NA

EV / Revenue: NAEV / EBITDA: NA

5/19/14

Ent. Value: NARevenue: NA

EV / Revenue: NAEV / EBITDA: NA

ABILITY Network offers innovative, web-based workflow solutions that simplify clinical and administrative tasks for

acute and post-acute healthcare providers

ABILITY’s solutions are used by over 55,000 providers at hospitals, home health agencies, hospices, skilled nursing

facilities, DMEs, and other healthcare sites in the U.S.

Summit’s $550M recapitalization of ABILITY comes three years after the company received a $27M capital

investment from Bain Capital Ventures and Lemhi Ventures

Summit Partners recapitalizes ABILITY Network

4/22/14

Ent. Value: $230MRevenue: NA

EV / Revenue: NAEV / EBITDA: NA

Viewpoint Construction Software provides commercial construction software products and solutions for project

management, financial planning, field communications, and day-to-day construction operations

Bain Capital’s $230M acquisition of Viewpoint comes nearly two years after the company received a $76M capital

investment from TA Associates, and a $10M investment from Updata Partners

Bain Capital acquires Viewpoint Construction Software

6/13/2014

Ent. Value: $2,495Revenue: $198

EV / Revenue: 12.6xEV / EBITDA: 41.5x

OpenTable provides restaurant reservation solutions through an online network of reservation-taking restaurants

and consumers

OpenTable seats nearly 15 million diners each month in over 31,000 restaurants, and has booked 125 million

reservations since its founding

The acquisition provides Priceline with a natural extension into restaurant marketing services, and allows the

company to offer activities beyond transportation and lodging

Priceline Group acquires OpenTable

6

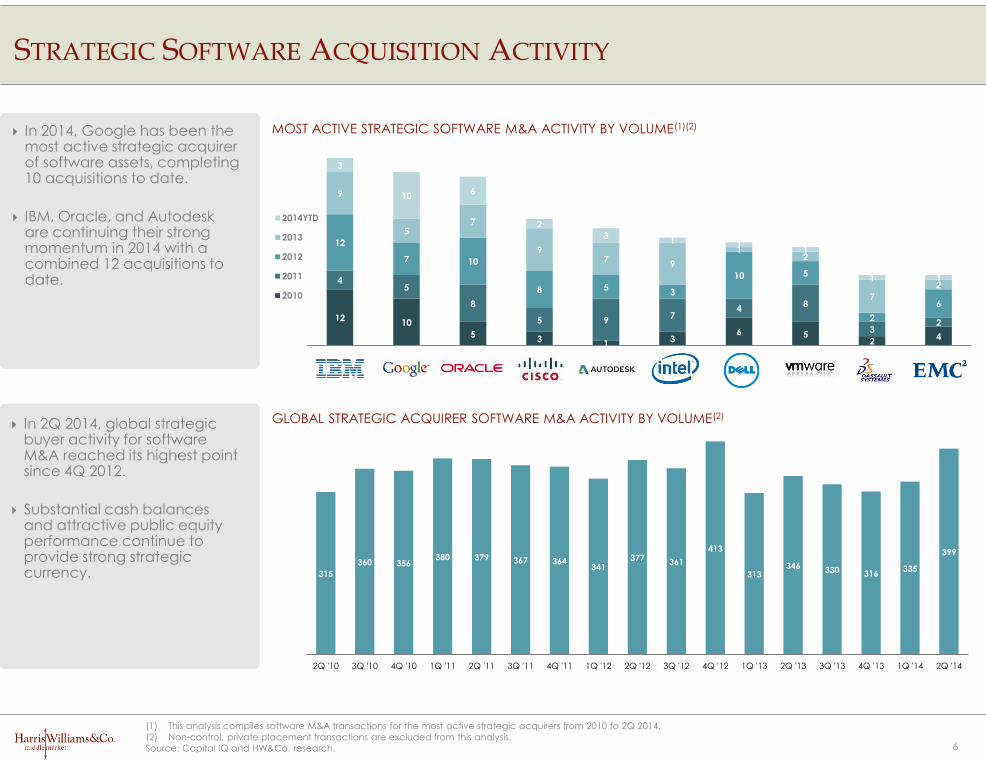

In 2014, Google has been the most active strategic acquirer of software assets, completing 10 acquisitions to date.

IBM, Oracle, and Autodesk are continuing their strong momentum in 2014 with a combined 12 acquisitions to date.

In 2Q 2014, global strategic buyer activity for software M&A reached its highest point since 4Q 2012.

Substantial cash balances and attractive public equity performance continue to provide strong strategic currency.

STRATEGIC SOFTWARE ACQUISITION ACTIVITY

(1) This analysis compiles software M&A transactions for the most active strategic acquirers from 2010 to 2Q 2014.

(2) Non-control, private placement transactions are excluded from this analysis.

Source: Capital IQ and HW&Co. research.

MOST ACTIVE STRATEGIC SOFTWARE M&A ACTIVITY BY VOLUME(1)(2)

GLOBAL STRATEGIC ACQUIRER SOFTWARE M&A ACTIVITY BY VOLUME(2)

1210

53

13

6 52

4

45

8

5 97

48

32

12

7 10

8 53

10 5

2

6

9

57

97

9

12

7

2

3

106

2

31

11

1 1

2014YTD

2013

2012

2011

2010

315

360 356380 379 367 364

341377

361

413

313346 330 316

335

399

2Q '10 3Q '10 4Q '10 1Q '11 2Q '11 3Q '11 4Q '11 1Q '12 2Q '12 3Q '12 4Q '12 1Q '13 2Q '13 3Q '13 4Q '13 1Q '14 2Q '14

NEW PLATFORM PRIVATE EQUITY SOFTWARE ACQUISITION VOLUME(1)(2)

13

13 32

2

1 3 2

1

2 3

9 6

3

1

22

3 2

2 1

6

3

4

5

15 2 1

2 1

3

2

1

3 31

1 2

1

2014YTD

2013

2012

2011

2010

7

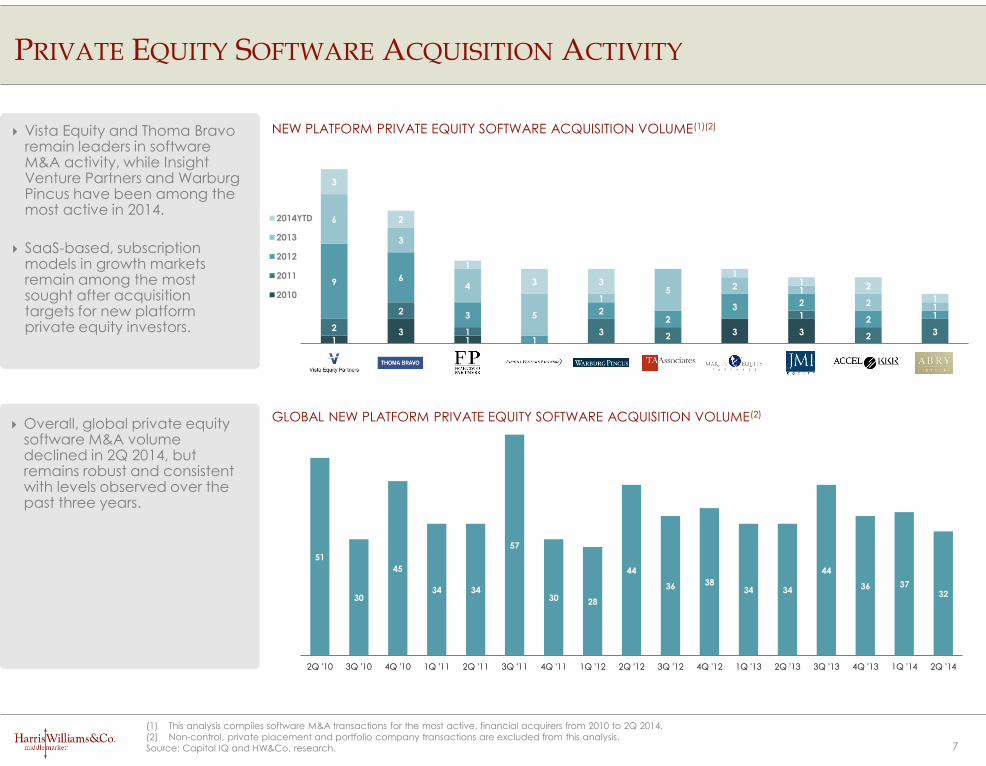

Vista Equity and Thoma Bravo remain leaders in software M&A activity, while Insight Venture Partners and Warburg Pincus have been among the most active in 2014.

SaaS-based, subscription models in growth markets remain among the most sought after acquisition targets for new platform private equity investors.

Overall, global private equity software M&A volume declined in 2Q 2014, but remains robust and consistent with levels observed over the past three years.

PRIVATE EQUITY SOFTWARE ACQUISITION ACTIVITY

GLOBAL NEW PLATFORM PRIVATE EQUITY SOFTWARE ACQUISITION VOLUME(2)

(1) This analysis compiles software M&A transactions for the most active, financial acquirers from 2010 to 2Q 2014.

(2) Non-control, private placement and portfolio company transactions are excluded from this analysis.

Source: Capital IQ and HW&Co. research.

51

30

45

34 34

57

30 28

44

36 3834 34

44

36 3732

2Q '10 3Q '10 4Q '10 1Q '11 2Q '11 3Q '11 4Q '11 1Q '12 2Q '12 3Q '12 4Q '12 1Q '13 2Q '13 3Q '13 4Q '13 1Q '14 2Q '14

Date

Closed Acquirer Target Description

Enterprise

Value ($mm)

Revenue

Multiple

Application Software

Pending Oracle Corporation MICROS Systems, Inc. Hotel and retail enterprise software solutions. $4,433 3.3x

06/17/14 WEX Inc. Evolution1, Inc. Electronic payment, on-premise, and cloud computing healthcare solutions. $533 NA

06/16/14 Intuit Inc. Check, Inc. Mobile finance applications. $360 NA

06/16/14 Cadence Design Systems Inc. Jasper Design Automation, Inc. Semiconductor design and verification software. $170 NA

06/03/14 Deltek, Inc Axium XTS Corporation Project-focused software for architectural and engineering firms. NA NA

05/21/14 The Carlyle Group LP Talent Partners, Inc. Talent payment software. $114 2.2x

05/02/14 SAP AG Fieldglass, Inc. Human capital management solutions. $1,000 NA

04/28/14 Dassault Systemes SA Accelrys Inc. Scientific business intelligence software and solutions. $683 4.1x

04/22/14 Bain Capital Private Equity Viewpoint, Inc. Construction management software. $230 NA

04/10/14 Hellman & Friedman LLC Renaissance Learning Inc. Computer-based assessment technology and school improvement programs. $1,100 NA

04/07/14 Wolters Kluwer Third Coast Holdings Inc Enterprise legal management software. $290 5.1x

03/12/14 The Carlyle Group LP ECi Software Solutions, Inc. ERP software for SMBs. $420 3.8x

02/05/14 Amadeus Americas, Inc. NMTI Holdings, Inc. NMTI Holdings, Inc. provides software for the hospitality industry. $500 NA

Median $460 3.8x

APPLICATION SOFTWARE M&A VOLUMEGLOBAL

8

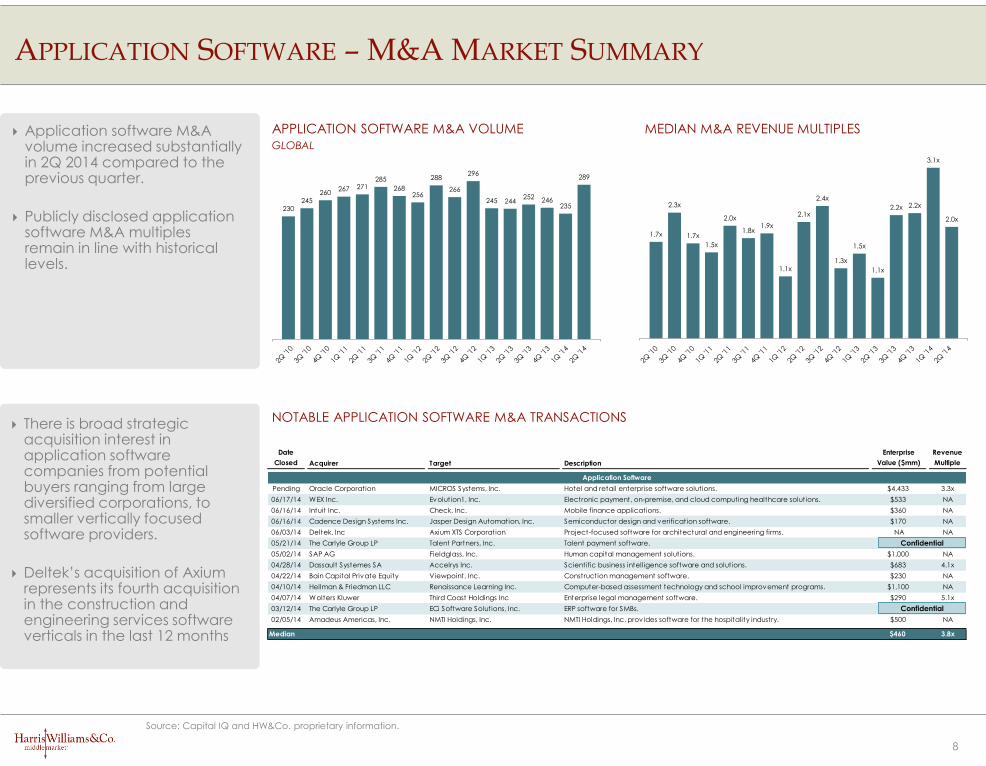

Application software M&A volume increased substantially in 2Q 2014 compared to the previous quarter.

Publicly disclosed application software M&A multiples remain in line with historical levels.

There is broad strategic acquisition interest in application software companies from potential buyers ranging from large diversified corporations, to smaller vertically focused software providers.

Deltek’s acquisition of Axiumrepresents its fourth acquisition in the construction and engineering services software verticals in the last 12 months

APPLICATION SOFTWARE – M&A MARKET SUMMARY

Source: Capital IQ and HW&Co. proprietary information.

Confidential

NOTABLE APPLICATION SOFTWARE M&A TRANSACTIONS

MEDIAN M&A REVENUE MULTIPLES

2Q '1

0

3Q '1

0

4Q '1

0

1Q '1

1

2Q '1

1

3Q '1

1

4Q '1

1

1Q '1

2

2Q '1

2

3Q '1

2

4Q '1

2

1Q '1

3

2Q '1

3

3Q '1

3

4Q '1

3

1Q '1

4

2Q '1

4

2Q '1

0

3Q '1

0

4Q '1

0

1Q '1

1

2Q '1

1

3Q '1

1

4Q '1

1

1Q '1

2

2Q '1

2

3Q '1

2

4Q '1

2

1Q '1

3

2Q '1

3

3Q '1

3

4Q '1

3

1Q '1

4

2Q '1

4

Confidential

230245

260267 271

285

268256

288

266

296

245 244252 246

235

289

1.7x

2.3x

1.7x

1.5x

2.0x

1.8x1.9x

1.1x

2.1x

2.4x

1.3x

1.5x

1.1x

2.2x 2.2x

3.1x

2.0x

9

SaaS acquisition volume increased in 2Q 2014 over the prior quarter and remains in line with with 2012 and 2013 averages.

Growing SaaS companies continue to trade at highly attractive multiples.

Private equity is driving a substantial portion of SaaS M&A activity.

OpenTable’s valuation represents a recent “high water mark” for strategic SaaS transactions.

SAAS – M&A MARKET SUMMARY

Source: Capital IQ and HW&Co. proprietary information.

NOTABLE SAAS M&A TRANSACTIONS

SAAS M&A VOLUMEGLOBAL

MEDIAN M&A REVENUE MULTIPLES

2Q '1

0

3Q '1

0

4Q '1

0

1Q '1

1

2Q '1

1

3Q '1

1

4Q '1

1

1Q '1

2

2Q '1

2

3Q '1

2

4Q '1

2

1Q '1

3

2Q '1

3

3Q '1

3

4Q '1

3

1Q '1

4

2Q '1

4

2Q '1

0

3Q '1

0

4Q '1

0

1Q '1

1

2Q '1

1

3Q '1

1

4Q '1

1

1Q '1

2

2Q '1

2

3Q '1

2

4Q '1

2

1Q '1

3

2Q '1

3

3Q '1

3

4Q '1

3

1Q '1

4

2Q '1

4

Date

Closed Acquirer Target Description

Enterprise

Value ($mm)

Revenue

Multiple

SaaS

Pending Insight Venture Partners iParadigms, LLC Cloud-based educational technologies. $752 NA

Pending Warburg Pincus LLC PayScale, Inc. Cloud based compensation software. NA NA

Pending The Priceline Group Inc. OpenTable, Inc. Restaurant reservation solutions. $2,496 12.6x

06/04/14 E2open, Inc. Serus Corporation Intelligent operations management solutions. $26 NA

06/02/14 Marin Software Incorporated NowSpots, Inc. Digital advertisement platform. $23 NA

05/30/14 GTCR, LLC Vocus Inc. Marketing and public relations software. $442 2.4x

05/19/14 Summit Partners LLP ABILITY Network Inc. Web-based workflow solutions for healthcare applications. NA NA

05/12/14 Thoma Bravo, LLC TravelCLICK, Inc. Cloud-based revenue-generating solutions for hoteliers. $930 NA

04/23/14 Intralinks, Inc. docTrackr, Inc. Data security solutions. $10 NA

03/11/14 Thoma Bravo, LLC Global Healthcare Exchange, LLC Cloud-based healthcare technology for supply chain management. NA NA

02/28/14 Corporate Executive Board Co. KnowledgeAdvisors, Inc. Learning and talent measurement software. $52 NA

02/06/14 Oracle Corporation Responsys, Inc. Marketing solutions across various interactive channels. $1,597 8.2x

12/19/13 The Hearst Corporation Homecare Homebase, LLC SaaS solutions for the homecare and hospice industry. $625 8.9x

12/19/13 Omnitracs, Inc. Roadnet Technologies, Inc. Fleet and workforce management and GPS tracking solutions. NA NA

11/15/13 Vista Equity Partners The Active Network, Inc. Cloud computing applications for activ ity and participant management. $961 2.1x

11/04/13 Vitera Healthcare Greenway Medical Software solutions and managed business serv ices to healthcare providers. $632 4.7x

Median $629 6.5x

Confidential

27

39

50

34

3133

36

41

37

41

52

38

47

37

40

33

40

5.0x

2.5x

0.8x

2.1x

2.6x2.4x

2.6x 2.7x

5.5x

1.2x

2.3x

5.0x

2.7x2.9x

8.2x

3.6x

2.9x

10

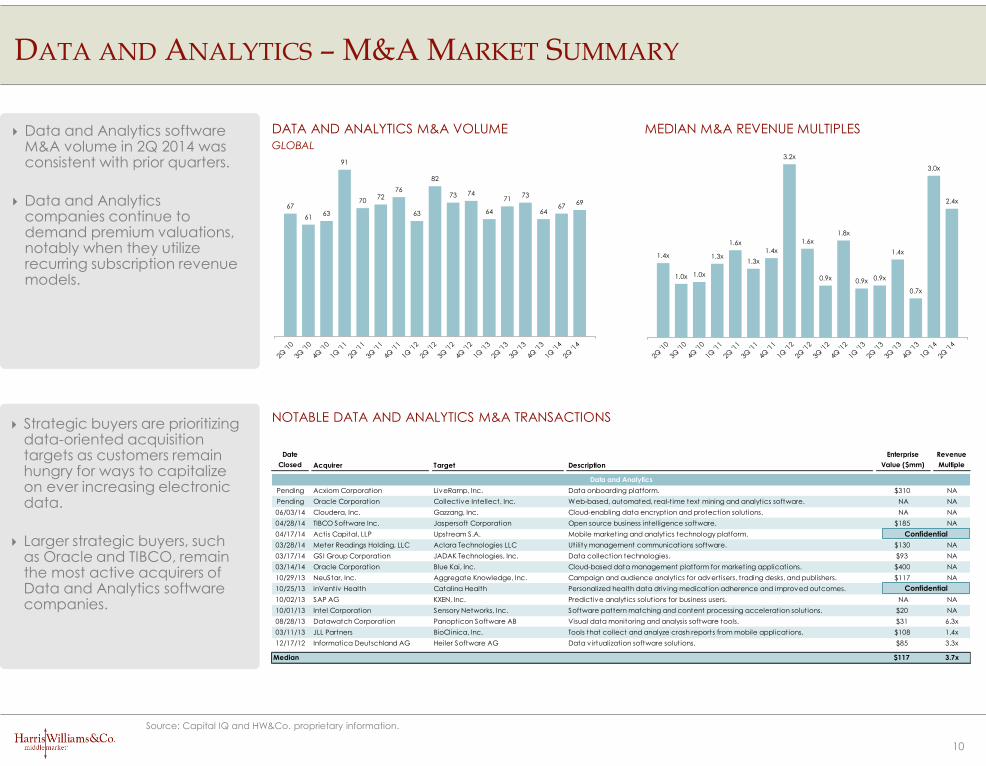

Data and Analytics software M&A volume in 2Q 2014 was consistent with prior quarters.

Data and Analytics companies continue to demand premium valuations, notably when they utilize recurring subscription revenue models.

Strategic buyers are prioritizing data-oriented acquisition targets as customers remain hungry for ways to capitalize on ever increasing electronic data.

Larger strategic buyers, such as Oracle and TIBCO, remain the most active acquirers of Data and Analytics software companies.

DATA AND ANALYTICS – M&A MARKET SUMMARY

Source: Capital IQ and HW&Co. proprietary information.

NOTABLE DATA AND ANALYTICS M&A TRANSACTIONS

DATA AND ANALYTICS M&A VOLUMEGLOBAL

MEDIAN M&A REVENUE MULTIPLES

2Q '1

0

3Q '1

0

4Q '1

0

1Q '1

1

2Q '1

1

3Q '1

1

4Q '1

1

1Q '1

2

2Q '1

2

3Q '1

2

4Q '1

2

1Q '1

3

2Q '1

3

3Q '1

3

4Q '1

3

1Q '1

4

2Q '1

4

2Q '1

0

3Q '1

0

4Q '1

0

1Q '1

1

2Q '1

1

3Q '1

1

4Q '1

1

1Q '1

2

2Q '1

2

3Q '1

2

4Q '1

2

1Q '1

3

2Q '1

3

3Q '1

3

4Q '1

3

1Q '1

4

2Q '1

4

Date

Closed Acquirer Target Description

Enterprise

Value ($mm)

Revenue

Multiple

Data and Analytics

Pending Acxiom Corporation LiveRamp, Inc. Data onboarding platform. $310 NA

Pending Oracle Corporation Collective Intellect, Inc. Web-based, automated, real-time text mining and analytics software. NA NA

06/03/14 Cloudera, Inc. Gazzang, Inc. Cloud-enabling data encryption and protection solutions. NA NA

04/28/14 TIBCO Software Inc. Jaspersoft Corporation Open source business intelligence software. $185 NA

04/17/14 Actis Capital, LLP Upstream S.A. Mobile marketing and analytics technology platform. $161 4.2x

03/28/14 Meter Readings Holding, LLC Aclara Technologies LLC Utility management communications software. $130 NA

03/17/14 GSI Group Corporation JADAK Technologies, Inc. Data collection technologies. $93 NA

03/14/14 Oracle Corporation Blue Kai, Inc. Cloud-based data management platform for marketing applications. $400 NA

10/29/13 NeuStar, Inc. Aggregate Knowledge, Inc. Campaign and audience analytics for advertisers, trading desks, and publishers. $117 NA

10/25/13 inVentiv Health Catalina Health Personalized health data driv ing medication adherence and improved outcomes. NA NA

10/02/13 SAP AG KXEN, Inc. Predictive analytics solutions for business users. NA NA

10/01/13 Intel Corporation Sensory Networks, Inc. Software pattern matching and content processing acceleration solutions. $20 NA

08/28/13 Datawatch Corporation Panopticon Software AB Visual data monitoring and analysis software tools. $31 6.3x

03/11/13 JLL Partners BioClinica, Inc. Tools that collect and analyze crash reports from mobile applications. $108 1.4x

12/17/12 Informatica Deutschland AG Heiler Software AG Data v irtualization software solutions. $85 3.3x

Median $117 3.7x

Confidential

Confidential

67

6163

91

7072

76

63

82

73 74

64

7173

6467

69

1.4x

1.0x 1.0x

1.3x

1.6x

1.3x

1.4x

3.2x

1.6x

0.9x

1.8x

0.9x 0.9x

1.4x

0.7x

3.0x

2.4x

4.3x

3.4x

1.3x

0.7x

2.3x

3.1x

4.8x 4.8x

1.8x

2.3x

2.8x

0.5x

1.8x

1.3x

4.0x

3.0x

2.5x

Date

Closed Acquirer Target Description

Enterprise

Value ($mm)

Revenue

Multiple

Infrastructure Software

Pending Sphere 3D Corporation Overland Storage Inc. Unified data management and data protection solutions. $84 1.6x

05/28/14 Automic Software GmbH ORSYP S.A.S. IT operations management solutions. $95 1.8x

05/20/14 Proofpoint, Inc. NetCitadel, Inc. Security orchestration platform for development of security infrastructure. $24 NA

04/16/14 HGGC, LLC Serena Software, Inc. Software products for mainframe change management. $436 2.4x

03/25/14 Synopsys Inc. Coverity, Inc. Source code analysis tools. $350 NA

03/21/14 Sphere 3D Corporation V3 Systems, Inc. Desktop cloud management solutions. $16 NA

03/04/14 Zayo Colocation, Inc. CoreXchange, Inc. Data center and networking solutions. $18 NA

02/18/14 Akamai Technologies, Inc. Prolexic Technologies, Inc. Distributed denial of serv ice (DDoS) detection solutions. $403 NA

01/07/14 Juniper Networks, Inc. WANDL, Inc. Network planning and management software. $29 NA

01/06/14 JDS Uniphase Corporation Network Instruments, LLC Network troubleshooting and analysis solutions. $200 5.0x

12/30/13 FireEye, Inc. Mandiant Corporation Internet security and response software and managed serv ices. $826 3.8x

12/06/13 Splunk, Inc. Cloudmeter, Inc. Application monitoring solutions in the cloud and datacenters. $21 NA

11/15/13 Computer Sciences Corp. Serv iceMesh, Inc. Cloud application management platform. $310 NA

10/07/13 Cisco Systems, Inc. Sourcefire, Inc. Intelligent cybersecurity technologies. $2,194 8.9x

09/17/13 F5 Networks, Inc. Versafe Ltd. Security applications for identity theft and online fraud prevention applications. $88 NA

09/10/13 Bain, Golden Gate, Insight BMC Software, Inc. Software that provides system and serv ice management solutions. $6,867 3.1x

Median $148 3.1x

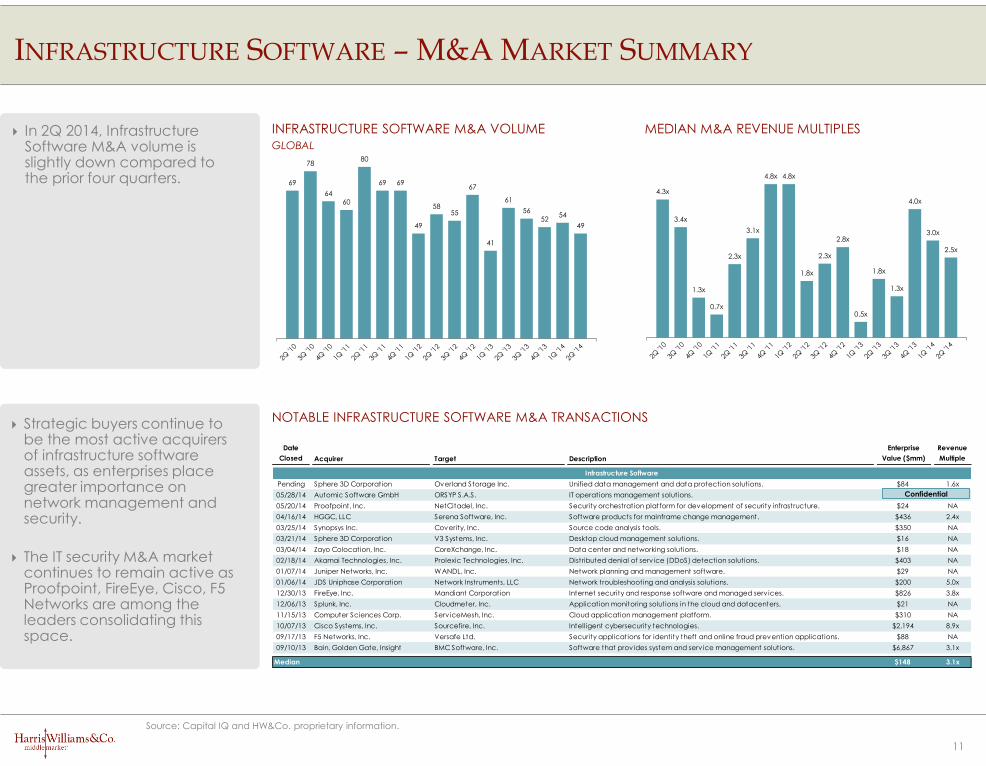

11

In 2Q 2014, Infrastructure Software M&A volume is slightly down compared to the prior four quarters.

Strategic buyers continue to be the most active acquirers of infrastructure software assets, as enterprises place greater importance on network management and security.

The IT security M&A market continues to remain active as Proofpoint, FireEye, Cisco, F5 Networks are among the leaders consolidating this space.

INFRASTRUCTURE SOFTWARE – M&A MARKET SUMMARY

Source: Capital IQ and HW&Co. proprietary information.

INFRASTRUCTURE SOFTWARE M&A VOLUMEGLOBAL

NOTABLE INFRASTRUCTURE SOFTWARE M&A TRANSACTIONS

MEDIAN M&A REVENUE MULTIPLES

2Q '1

0

3Q '1

0

4Q '1

0

1Q '1

1

2Q '1

1

3Q '1

1

4Q '1

1

1Q '1

2

2Q '1

2

3Q '1

2

4Q '1

2

1Q '1

3

2Q '1

3

3Q '1

3

4Q '1

3

1Q '1

4

2Q '1

4

2Q '1

0

3Q '1

0

4Q '1

0

1Q '1

1

2Q '1

1

3Q '1

1

4Q '1

1

1Q '1

2

2Q '1

2

3Q '1

2

4Q '1

2

1Q '1

3

2Q '1

3

3Q '1

3

4Q '1

3

1Q '1

4

2Q '1

4

Confidential

69

78

64

60

80

69 69

49

5855

67

41

61

56

5254

49

12

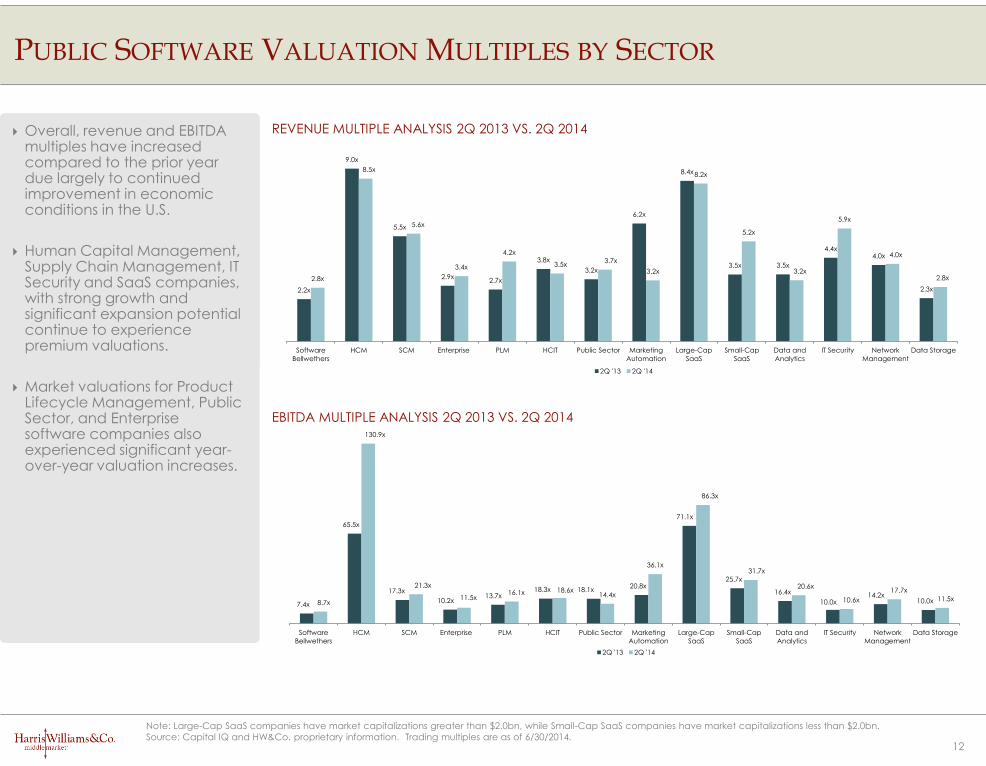

Overall, revenue and EBITDA multiples have increased compared to the prior year due largely to continued improvement in economic conditions in the U.S.

Human Capital Management, Supply Chain Management, IT Security and SaaS companies, with strong growth and significant expansion potential continue to experience premium valuations.

Market valuations for Product Lifecycle Management, Public Sector, and Enterprise software companies also experienced significant year-over-year valuation increases.

PUBLIC SOFTWARE VALUATION MULTIPLES BY SECTOR

2.2x

9.0x

5.5x

2.9x2.7x

3.8x

3.2x

6.2x

8.4x

3.5x 3.5x

4.4x4.0x

2.3x

2.8x

8.5x

5.6x

3.4x

4.2x

3.5x3.7x

3.2x

8.2x

5.2x

3.2x

5.9x

4.0x

2.8x

Software

Bellwethers

HCM SCM Enterprise PLM HCIT Public Sector Marketing

Automation

Large-Cap

SaaS

Small-Cap

SaaS

Data and

Analytics

IT Security Network

Management

Data Storage

2Q '13 2Q '14

7.4x

65.5x

17.3x

10.2x13.7x

18.3x 18.1x20.8x

71.1x

25.7x

16.4x

10.0x14.2x

10.0x8.7x

130.9x

21.3x

11.5x16.1x 18.6x

14.4x

36.1x

86.3x

31.7x

20.6x

10.6x

17.7x

11.5x

Software

Bellwethers

HCM SCM Enterprise PLM HCIT Public Sector Marketing

Automation

Large-Cap

SaaS

Small-Cap

SaaS

Data and

Analytics

IT Security Network

Management

Data Storage

2Q '13 2Q '14

Note: Large-Cap SaaS companies have market capitalizations greater than $2.0bn, while Small-Cap SaaS companies have market capitalizations less than $2.0bn.

Source: Capital IQ and HW&Co. proprietary information. Trading multiples are as of 6/30/2014.

EBITDA MULTIPLE ANALYSIS 2Q 2013 VS. 2Q 2014

REVENUE MULTIPLE ANALYSIS 2Q 2013 VS. 2Q 2014

KEY METRICS BY SECTOR – PUBLIC SOFTWARE COMPANIES

13

`

EV / LTM Revenue MultipleNTM Revenue

Growth

90%

84%

21%

28%

32%

-7%

NTM EBITDA Growth

LTM EBITDA Margin

-67%

-46%

-3%

Correlation with EV/R Multiple

Correlation with EV/R Multiple

Correlation with EV/R Multiple

26%

14%

3%

20%

23%

2%

68% -7% -53%21% 0% 3%

-3%

96% 20% -77%9% 6% 21%

88% 43% 60%15% 13% 28%

59% -36% 81%7% 9% 22%

21% 8% 22%12% 31% 20%

85% 94% -3%15% 16% 18%

6%

25%

70% 68% -28%4% 7% 30%

17% 17% -27%

97% 23% -71%13% 6% 12%

-11% 29% -69%25% 27% 5%

91% 0% -55%

Note: Large-Cap SaaS companies have market capitalizations greater than $2.0bn, while Small-Cap SaaS companies have market capitalizations less than $2.0bn.

Source: Capital IQ and HW&Co. proprietary information, data shown as of 6/30/2014.

2.8x

2.8x

3.2x

3.2x

3.4x

3.5x

3.7x

4.0x

4.2x

5.3x

5.6x

5.9x

8.2x

8.5x

Software Bellwethers

Data Storage

Marketing Automation

Data and Analytics

Enterprise

HCIT

Public Sector

Network Mgmt

PLM

Small-Cap SaaS

SCM

IT Security

Large-Cap SaaS

HCM

78% 47% -20%4% 16% 20%

14

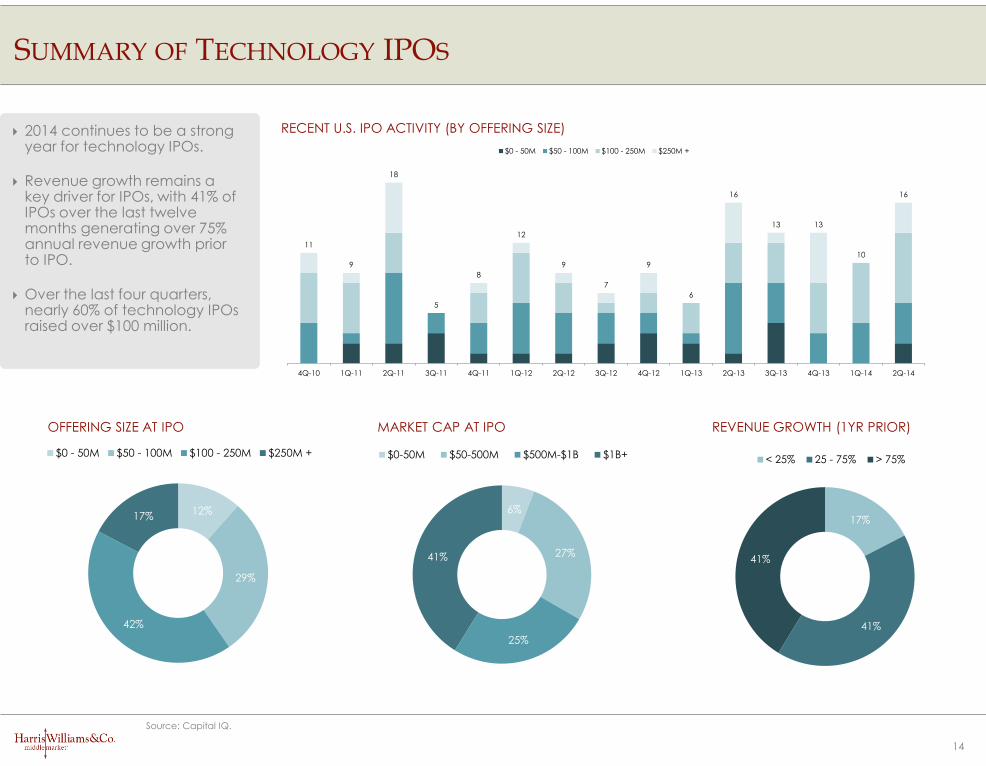

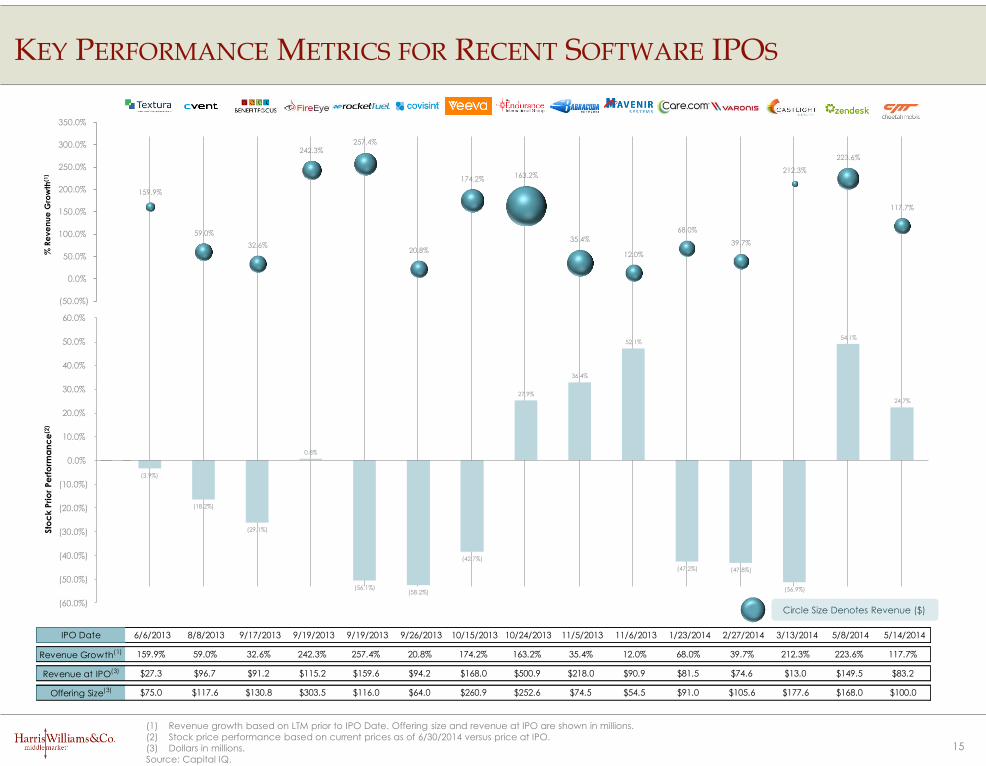

2014 continues to be a strong year for technology IPOs.

Revenue growth remains a key driver for IPOs, with 41% of IPOs over the last twelve months generating over 75% annual revenue growth prior to IPO.

Over the last four quarters, nearly 60% of technology IPOs raised over $100 million.

SUMMARY OF TECHNOLOGY IPOS

RECENT U.S. IPO ACTIVITY (BY OFFERING SIZE)

OFFERING SIZE AT IPO MARKET CAP AT IPO REVENUE GROWTH (1YR PRIOR)

Source: Capital IQ.

11

9

18

5

8

12

9

7

9

6

16

13 13

10

16

4Q-10 1Q-11 2Q-11 3Q-11 4Q-11 1Q-12 2Q-12 3Q-12 4Q-12 1Q-13 2Q-13 3Q-13 4Q-13 1Q-14 2Q-14

$0 - 50M $50 - 100M $100 - 250M $250M +

12%

29%

42%

17%

$0 - 50M $50 - 100M $100 - 250M $250M +

17%

41%

41%

< 25% 25 - 75% > 75%

6%

27%

25%

41%

$0-50M $50-500M $500M-$1B $1B+

(1) Revenue growth based on LTM prior to IPO Date. Offering size and revenue at IPO are shown in millions.

(2) Stock price performance based on current prices as of 6/30/2014 versus price at IPO.

(3) Dollars in millions.

Source: Capital IQ.

Circle Size Denotes Revenue ($)

% R

eve

nu

e G

row

th(1

)

KEY PERFORMANCE METRICS FOR RECENT SOFTWARE IPOS

15

IPO Date 6/6/2013 8/8/2013 9/17/2013 9/19/2013 9/19/2013 9/26/2013 10/15/2013 10/24/2013 11/5/2013 11/6/2013 1/23/2014 2/27/2014 3/13/2014 5/8/2014 5/14/2014

Revenue Growth(1) 159.9% 59.0% 32.6% 242.3% 257.4% 20.8% 174.2% 163.2% 35.4% 12.0% 68.0% 39.7% 212.3% 223.6% 117.7%

Revenue at IPO(3) $27.3 $96.7 $91.2 $115.2 $159.6 $94.2 $168.0 $500.9 $218.0 $90.9 $81.5 $74.6 $13.0 $149.5 $83.2

Offering Size(3) $75.0 $117.6 $130.8 $303.5 $116.0 $64.0 $260.9 $252.6 $74.5 $54.5 $91.0 $105.6 $177.6 $168.0 $100.0

(3.9%)

(18.2%)

(29.1%)

0.8%

(56.1%)(58.2%)

(42.7%)

27.9%

36.4%

52.1%

(47.2%) (47.8%)

(56.9%)

54.1%

24.7%

159.9%

59.0%

32.6%

242.3% 257.4%

20.8%

174.2% 163.2%

35.4%

12.0%

68.0%

39.7%

212.3%

223.6%

117.7%

(50.0%)

0.0%

50.0%

100.0%

150.0%

200.0%

250.0%

300.0%

350.0%

33.9%

20.1%

4.5%

93.5%

(16.0%)

(44.7%)

(27.6%)

21.5%

75.3%

94.8%

11.9%

(29.4%)

(9.4%)(12.8%)

(26.3%)

Sto

ck

Prio

r Pe

rfo

rma

nc

e(2

)

(3.9%)

(18.2%)

(29.1%)

0.8%

(56.1%)(58.2%)

(42.7%)

27.9%

36.4%

52.1%

(47.2%) (47.8%)

(56.9%)

54.1%

24.7%

(60.0%)

(50.0%)

(40.0%)

(30.0%)

(20.0%)

(10.0%)

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

4.9x4.8x

4.1x4.0x

3.4x

3.8x 3.8x

4.3x

4.7x 4.7x

5.6x

4.5x

3.3x

4.2x 4.3x

4.5x

4.8x4.9x

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1Q14

FLD/EBITDA SLD/EBITDA Other Sr Debt/EBITDA Sub Debt/EBITDA

16

Overall, the middle market debt market continues to strengthen, with lenders actively seeking high quality software credits.

Middle market LBO loan multiples have steadily increased since their low in 2009 and are on approaching peak 2007 levels.

MIDDLE MARKET DEBT / LBO MARKET OVERVIEW

LBO LOAN VOLUME BY INDUSTRY(2) SPONSORED LOAN VOLUME BY PURPOSE(2)

MIDDLE MARKET LOAN VOLUME(1)

(1) PNC Capital Markets.

(2) S&P LCD stats.

MIDDLE MARKET LBO LOAN MULTIPLES(1)

0.7%

0.5%

1.3%

1.6%

2.0%

2.9%

9.5%

15.6%

25.4%

40.7%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0%

Other

Corporate Purpose

Recap / Stock Purchase

Merger

Recap / General Recap

Recap / IPO

Acquisition

Recap / Dividend

LBO

Refinancing

2013 Volume: $322.3 Billion

20.8%

4.4%

5.9%

6.1%

6.2%

6.9%

12.8%

17.2%

19.8%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Other

Oil & Gas

Chemicals

Manufacturing & Machinery

Building Materials

Retail

Servicse & Leasing

Food & Beverage

Computer & Electronics

2013 Volume: $81.7 Billion

$43B

$66B

$54B

$72B

$141B

$120B

$53B

$62B

$115B

$88B

$126B

$137B

$189B

$164B

$125B$127B

$162B

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Institutional Pro Rata

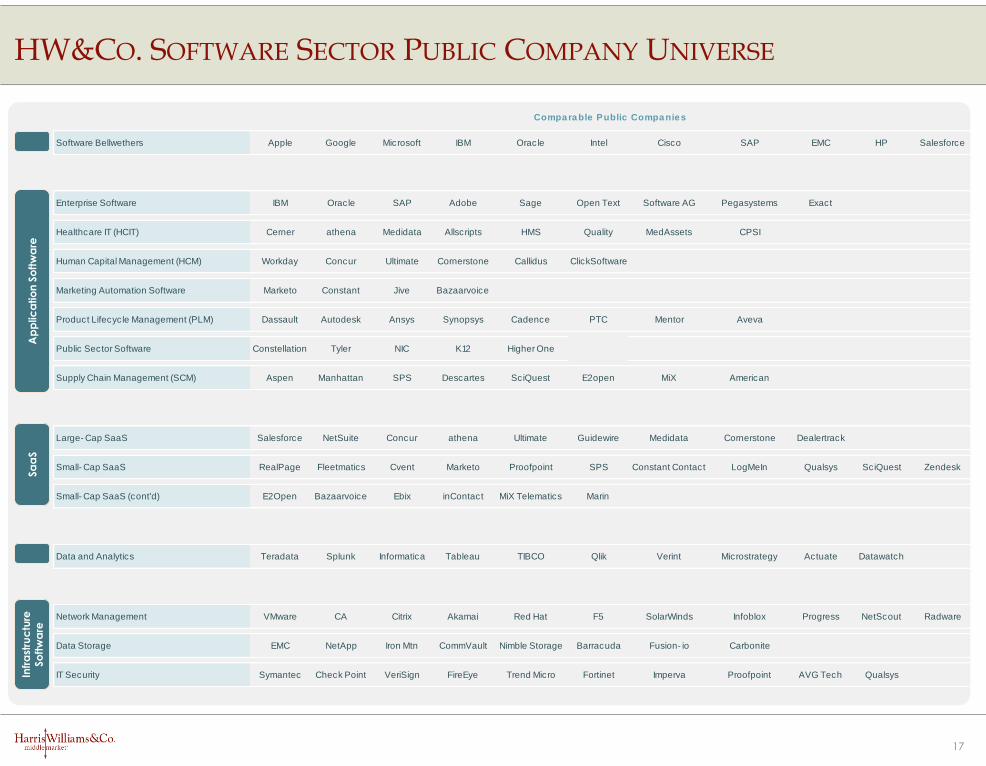

Software Bellwethers Apple Google Microsoft IBM Oracle Intel Cisco SAP EMC HP Salesforce

Enterprise Software IBM Oracle SAP Adobe Sage Open Text Software AG Pegasystems Exact

Healthcare IT (HCIT) Cerner athena Medidata Allscripts HMS Quality MedAssets CPSI

Human Capital Management (HCM) Workday Concur Ultimate Cornerstone Callidus ClickSoftware

Marketing Automation Software Marketo Constant Jive Bazaarvoice

Product Lifecycle Management (PLM) Dassault Autodesk Ansys Synopsys Cadence PTC Mentor Aveva

Public Sector Software Constellation Tyler NIC K12 Higher One

Supply Chain Management (SCM) Aspen Manhattan SPS Descartes SciQuest E2open MiX American

Large- Cap SaaS Salesforce NetSuite Concur athena Ultimate Guidewire Medidata Cornerstone Dealertrack

Small- Cap SaaS RealPage Fleetmatics Cvent Marketo Proofpoint SPS Constant Contact LogMeIn Qualsys SciQuest Zendesk

Small- Cap SaaS (cont'd) E2Open Bazaarvoice Ebix inContact MiX Telematics Marin

Data and Analytics Teradata Splunk Informatica Tableau TIBCO Qlik Verint Microstrategy Actuate Datawatch

Network Management VMware CA Citrix Akamai Red Hat F5 SolarWinds Infoblox Progress NetScout Radware

Data Storage EMC NetApp Iron Mtn CommVault Nimble Storage Barracuda Fusion- io Carbonite

IT Security Symantec Check Point VeriSign FireEye Trend Micro Fortinet Imperva Proofpoint AVG Tech Qualsys

Compa ra ble Public Compa nie s

Sa

aS

Ap

plic

atio

n S

oft

wa

reIn

fra

stru

ctu

re

So

ftw

are

HW&CO. SOFTWARE SECTOR PUBLIC COMPANY UNIVERSE

17

Harris Williams & Co. (www.harriswilliams.com) is a preeminent middle market investment bank focused on the advisory needs of clientsworldwide. The firm has deep industry knowledge, global transaction expertise, and an unwavering commitment to excellence. HarrisWilliams & Co. provides sell-side and acquisition advisory, restructuring advisory, board advisory, private placements, and capital marketsadvisory services.

Investment banking services are provided by Harris Williams LLC, a registered broker-dealer and member of FINRA and SIPC, and HarrisWilliams & Co. Ltd, which is authorized and regulated by the Financial Conduct Authority. Harris Williams & Co. is a trade name under whichHarris Williams LLC and Harris Williams & Co. Ltd conduct business.

THIS REPORT MAY CONTAIN REFERENCES TO REGISTERED TRADEMARKS, SERVICE MARKS AND COPYRIGHTS OWNED BY THIRD-PARTYINFORMATION PROVIDERS. NONE OF THE THIRD-PARTY INFORMATION PROVIDERS IS ENDORSING THE OFFERING OF, AND SHALL NOT IN ANYWAY BE DEEMED AN ISSUER OR UNDERWRITER OF, THE SECURITIES, FINANCIAL INSTRUMENTS OR OTHER INVESTMENTS DISCUSSED IN THIS REPORT,AND SHALL NOT HAVE ANY LIABILITY OR RESPONSIBILITY FOR ANY STATEMENTS MADE IN THE REPORT OR FOR ANY FINANCIAL STATEMENTS,FINANCIAL PROJECTIONS OR OTHER FINANCIAL INFORMATION CONTAINED OR ATTACHED AS AN EXHIBIT TO THE REPORT. FOR MOREINFORMATION ABOUT THE MATERIALS PROVIDED BY SUCH THIRD PARTIES, PLEASE CONTACT US AT +1-804-648-0072.

The information and views contained in this report were prepared by Harris Williams & Co. (“Harris Williams”). It is not a research report, assuch term is defined by applicable law and regulations, and is provided for informational purposes only. It is not to be construed as an offerto buy or sell or a solicitation of an offer to buy or sell any financial instruments or to participate in any particular trading strategy. Theinformation contained herein is believed by Harris Williams to be reliable, but Harris Williams makes no representation as to the accuracy orcompleteness of such information. Harris Williams and/or its affiliates may be market makers or specialists in, act as advisers or lenders to,have positions in and effect transactions in securities of companies mentioned herein and also may provide, may have provided, or mayseek to provide investment banking services for those companies. In addition, Harris Williams and/or its affiliates or their respective officers,directors and employees may hold long or short positions in the securities, options thereon or other related financial products of companiesdiscussed herein. Opinions, estimates and projections in this report constitute Harris Williams’ judgment and are subject to change withoutnotice. The financial instruments discussed in this report may not be suitable for all investors, and investors must make their own investmentdecisions using their own independent advisors as they believe necessary and based upon their specific financial situations and investmentobjectives. Also, past performance is not necessarily indicative of future results. No part of this material may be copied or duplicated in anyform or by any means, or redistributed, without Harris Williams’ prior written consent.

Copyright © 2014 Harris Williams & Co., all rights reserved.

HW&CO. CONTACT INFORMATION AND DISCLAIMER

18