Embed Size (px)

Citation preview

1

29 November 2016

Torotrak plc

(‘Torotrak’, the ‘Company’ or the ‘Group’)

Half Year Results for the six months ended 30 September 2016 (unaudited)

Torotrak (LSE: TRK), a leading developer and supplier of emissions reduction and fuel efficiency technology

for internal combustion engine, hybrid and all electric powered vehicles, today publishes its half year

results for the six months ended 30 September 2016.

Strategy

The Group’s focus and strategic objective is the commercialisation and monetisation of its technology for

the benefit of shareholders. Given the progress made in these areas over the last 12 months, the near term

focus is on licensing V-Charge for passenger cars and Flybrid KERS for off-highway markets.

V-Charge – delivering lower fuel consumption and lower emissions engines

Technology has exceeded expectations in on-engine performance and responsiveness.

Ford Focus demonstrator test drives with 12 OEMs and 6 Tier 1s successfully completed, generating

strong interest in V-Charge.

On track to complete second demonstrator vehicle, Ford S-MAX (with V-Charge enabled 1.0L 3 cylinder

engine replacing a 1.5L 4 cylinder engine).

Significant interest being shown by multiple global OEMs and Tier 1s in V-Charge technology.

Flybrid KERS – launch in off-highway machines

Secured APC funded wheel loader programme in collaboration with Caterpillar Inc.

On track to license KERS into the global off-highway market.

High level of interest shown by multiple OEMs in hydraulically-connected energy recovery systems

(‘ERS’) for excavators, wheel loaders and other off-highway machines.

Financial

26 per cent improvement in equity free cash outflow compared to previous period.

Cash balance of £7.9 million in line with management’s expectations for the half year.

Key Financial Results:

£000’s

Six months ended 30 September 2016 (unaudited)

Six months ended 30 September 2015 (unaudited)

Revenue 935 1,169

Operating loss (3,696) (9,771)

Equity free cash outflow1 (3,390) (4,595)

Cash and cash equivalents 7,915 14,422

1Net decrease in cash and cash equivalents excluding proceeds from the issue of share capital and the repayment of borrowings.

2

Nick Barter, Chairman, commented: “I am pleased with the real progress we are making towards delivering

on our strategic objectives in terms of commercial progress, cash management and organisational

performance.”

Adam Robson, Chief Executive, commented: “I believe we are on track to deliver the demonstrable

monetisation of our technologies that we committed to in 2015. We are seeing real progress in the off-

highway sector for KERS and the hydraulically-connected ERS product and V-Charge is exceeding our

expectations in terms of in-vehicle performance, OEM interest and Tier 1 engagement.”

For more information, please visit www.torotrak.com or contact:

Torotrak plc

Adam Robson, Chief Executive / Rex Vevers, Finance Director

Tel: +44 1772 900931

Cantor Fitzgerald Europe (Financial Adviser & Broker)

Marc Milmo / Will Goode

Tel: +44 20 7894 7000

Tavistock (Financial PR)

Simon Hudson / Lulu Bridges / James Collins

Tel: +44 20 7920 3150

About Torotrak

Torotrak is a leading developer and supplier of kinetic energy recovery systems, engine boosting and

variable drive transmissions for internal combustion engine, hybrid and electric powered vehicles. Our

portfolio of technology solutions substantially improves fuel economy and reduces CO2 and other emissions

in vehicles through capturing and recycling energy that would otherwise be lost, harnessing the power of

supercharging to improve engine performance, emissions and responsiveness.

3

CEO’s Review

Introduction

As I set out in our 2016 Annual Report, the key focus of the Group is on licensing our V-Charge and Flybrid

KERS technologies. During the last six months we have continued to engage extensively with commercial

partners and potential licensees and we have developed meaningful commercial interest and market pull

for both technology solutions. We have made good progress towards our goal of licensing KERS in the off-

highway market and securing a global licence for V-Charge in passenger cars as well as growing our

engineering services order book. In parallel, and in support of our licensing discussions, we have made

progress with the in-house development of our low cost flywheel assembly manufacturing capability and

new low cost manufacturing processes for the discs and rollers at the heart of V-Charge.

I am pleased with the progress we have made over the last six months which has created a strong platform

for our licensing discussions. I report below in detail on the specific activities and the key technical and

other achievements as well as on our progress in improving our cash performance.

Market backdrop and key trends

Passenger cars:

The automotive industry is focused on developing technologies that can help meet the upcoming

regulatory fleet average emissions targets from 2020 onwards, as measured using the new World

Harmonised Light Vehicles Test Procedure (‘WLTP’) and the new real-world driving emissions test (‘RDE’).

The combination of lower emissions targets and more representative ‘real-world’ test procedures, together

with an increasing regulatory focus at national and city levels on air quality and hence reducing emissions

of NOx and particulates, represents a significant challenge for the automotive industry.

The impact of these changes has been an accelerating trend towards increased electrification of vehicle

powertrains which is leading to some significant changes in the focus of technology development by OEMs

and Tier 1s. There is a growing consensus that in the long term electric vehicles (of some form) will

eventually come to dominate the industry but that in the medium term hybrid vehicles will form the largest

group. A report by the International Energy Agency in 2016 indicates that by 2050 nearly 60 per cent. of

the global light duty vehicle stock will be non-electric vehicles. Consequently, there remains a strong

requirement for OEMs to continue to make significant improvements in the efficiency of internal

combustion engines. Indeed, a recent report published by BHP Billiton Limited forecasts that by 2030 the

average light duty vehicle will become one third more efficient, through advances such as improved ICE

thermal efficiency, engine downsizing / rightsizing, more transmission speeds and vehicle light-weighting; a

number of which can be achieved with the Group’s technologies.

OEMs require technologies that can meet the new real-world emissions regulations at the lowest possible

cost, whilst preserving vehicle performance and driveability and importantly remaining affordable for the

end customer. The Group’s V-Charge technology offers OEMs the potential to re-size engines across the

broadest possible range of vehicle platforms - pure ICE and hybrid - reducing fuel consumption and

emissions at a highly attractive cost per gram of CO2 saved. Similarly, our KERS technology can offer OEMs

a lower cost way to hybridise their vehicles when compared to other options, such as further vehicle

electrification. Our traction drive and KERS technologies can also help improve performance, including

acceleration and gradeability of full battery electric vehicles and fuel cell vehicles. In response to the trend

4

towards further vehicle electrification, Torotrak is working with OEMs and Tier 1s to explore opportunities

to use the Group’s technologies cost-effectively across their BEV and PHEV platforms.

Commercial vehicles:

The bus and smaller commercial vehicle sector is influenced by many of the same trends as the passenger

car sector, in particular with respect to urban pollution. But in the off-highway commercial vehicle sector

the principal drivers remains reduced operator costs and payback times. With the continued low oil price

and difficult global market conditions in the mining and resources sector, the uptake of new technologies

remains challenging, but Torotrak’s technologies remain highly relevant because of their cost

competitiveness, controllability and robustness. The Group continues to focus its efforts on reducing the

cost of its technology products and improving fuel efficiency to be able to offer end customers a rapid

payback on the investment in new products. Both KERS and V-Charge offer the potential to downsize

engines without compromising performance-critical factors such as low end torque and rapid transient

response.

V-Charge

The Group has made very good progress during the last six months. We have delivered and exceeded the

technical milestones in the independent study conducted by the University of Bath and we are now

developing OEM / Tier 1 market pull and creating the platform to license the technology into the global

passenger car market.

Technology validation:

During the period the Group announced the successful results of the on-engine V-Charge testing

programme conducted by the University of Bath in collaboration with a global Tier 1 supplier of engine

boosting systems and with the participation of the Ford Motor Company (the ‘Bath Study’). The results of

the independent testing programme confirm that the key performance targets were successfully achieved

or exceeded and that V-Charge outperforms other advanced boosting solutions. The following key targets

were achieved using V-Charge in conjunction with a re-matched turbocharger on a 1.0L 3 cylinder Ford

EcoBoost engine:

Torque of >145Nm at 1,000rpm,

Torque of 240Nm from 1,400rpm upwards,

Torque increase of >40% compared to the base engine with a single turbocharger,

31 Bar BMEP,

Time to 90% of target torque (216Nm) ~1.0s at 1,400 rpm.

Importantly, the on-engine test results confirm that a V-Charge enabled 3 cylinder 1.0L EcoBoost engine

matches the torque output of a 4 cylinder 1.5L EcoBoost engine. The Group has successfully demonstrated

the increased performance of the V-Charge enabled 1.0L engine in a Ford Focus demonstrator vehicle and

is on track to demonstrate the increased performance and driveability of a Ford S-MAX using the V-Charge

enabled 3 cylinder 1.0L EcoBoost in place of the turbocharged 1.5L EcoBoost engine that is normally fitted

to the S-MAX.

Re-sizing engines:

Engine rightsizing and engine downsizing are important strategies to help OEMs meet the upcoming

regulatory emissions targets whilst simultaneously delivering lower emissions of NOx and particulates at an

affordable cost. Both require improvements in engine air boosting, in particular by supercharging. V-

5

Charge is a variable speed mechanical supercharger using the Group’s unique traction drive technology. By

supplying variable air on-demand, V-Charge delivers sustained high power and high torque at any engine

speed with rapid response, avoiding the ‘lag’ of other boosting solutions. Other boosting technologies

including turbochargers and other mechanical superchargers are unable to deliver exactly the required

amount of air on-demand, thereby limiting the opportunity to reduce emissions through smaller engines

(downsizing) or larger engines operating at optimum efficiency (rightsizing). Further, electric superchargers

(“eboosters”), unlike V-Charge, are unable to sustain continuous boost, due to the lack of sufficient

electrical storage on-board, which is a fundamental constraint on their applicability and adoption.

Engine downsizing using existing boosting solutions often results in worse fuel economy in real-world

driving and higher emissions at full load. Current boosting solutions are unable to deliver sustained high

torque at low engine speeds. In an attempt to remedy this problem a smaller turbocharger may be used to

provide quicker response and enhanced low speed torque, however this increases exhaust back pressure

reducing the combustion efficiency of the engine, as well as increasing NOx output due to increased

combustion temperatures. As a consequence of high specific powers and enriched fuelling, downsized

turbocharged gasoline engines require expensive gas particulate filters, whilst downsized turbocharged

diesel engines require expensive de-NOx after treatment systems to mitigate the emissions from smaller

engines operating at high loads. In contrast, V-Charge delivers instant and sustained torque at lower engine

speeds allowing the turbocharger to be sized so that the engine operates more efficiently at higher engine

speeds, reducing the need for expensive after treatment systems. V-Charge offers OEMs the opportunity

to continue to use engine downsizing to reduce emissions and remain fuel efficient in real-world driving.

OEMs are increasing the use of alternative combustion cycles such as Miller to increase engine efficiency.

However, these alternative combustion cycles cannot generate the same engine power, requiring the

engine to be ‘rightsized’, resulting in increased emissions due to greater friction, compared to smaller

engines. V-Charge addresses this problem enabling more extensive use of the Miller combustion cycle even

at high torque and low engine speed, further reducing the emissions penalty of rightsized larger engines.

By delivering sustained high torque and enabling high power, V-Charge offers OEMs the opportunity to fully

exploit the combination of engine downsizing and, where appropriate, engine rightsizing to maximise the

improvements in fuel economy and lower emissions.

Diesel engines:

With an increased focus on improving air quality, there is a growing requirement to eliminate the problems

of soot, NOx and particulates on all engines. This is a particular problem with diesel engines which require

expensive after treatment systems to reduce the noxious emissions.

V-Charge can help reduce NOx and particulates emissions produced by diesel engines, particularly during

transient events, thereby reducing the need for expensive after treatment systems. This is an important

benefit, enabling OEMs to continue to maintain diesel engine powered vehicles as a significant part of their

fleet, thereby avoiding the additional CO2 emissions penalty that would result from moving to more

gasoline engine powered vehicles.

Global market opportunity:

The Group has recently completed an in-depth market study identifying the potential sales opportunities

for V-Charge. Using detailed engine data supplied by IHS Markit Ltd, and following discussions with a range

of OEMs and Tier 1 suppliers, we believe that V-Charge is applicable to a substantial proportion of both

6

single-stage and twin-stage boosted engines, offering fuel economy and emissions benefits which other

boosting technologies such as variable geometry turbochargers and eboosters cannot deliver. The results

of the study, which have been shared with our potential OEM / Tier 1 partners, show that there is a market

opportunity in 2020 of around 25m engines per annum that could be addressed with V-Charge, rising to

around 45m engines per annum in 2025.

Demonstrator vehicle test drives:

The Group has recently completed an extended pan-European tour visiting the main global automotive

OEMS and Tier 1s (including those headquartered outside Europe). The visits included test drives of the V-

Charge enabled Ford Focus demonstrator car, sharing of the results of the Group’s market study and a

detailed presentation of V-Charge, including the technical results from the independent Bath Study. The

meetings and the test drives have generated a significant level of interest in V-Charge and the feedback to

date has been extremely positive, with all participants commenting on the impressive torque response at

low engine speeds delivered by V-Charge in the demonstrator vehicle. We are currently involved in follow-

on meetings with a number of interested parties who have expressed an interest in understanding the full

capability of V-Charge and conducting further technical and commercial evaluation.

In parallel with following up on the interest generated from the pan-European Focus car test drive

programme, as noted above, the engineering team is completing the installation of the V-Charge enabled

1.0L 3 cylinder Ford EcoBoost engine in the S-MAX, replacing the incumbent 1.5L 4 cylinder engine. This

larger vehicle will be used to demonstrate the performance, driveability and improved fuel economy and

emissions of the downsized engine when installed in a vehicle usually equipped with a 1.5L engine as the

smallest displacement engine. The programme is on track to be completed next month.

The focus in the coming months is to build on the significant interest shown in V-Charge and to convert this

interest into market pull from OEM and Tier 1 parties.

KERS

Off-highway:

In April 2016, the Group was awarded a fully-funded programme to design, develop and demonstrate a

high-power KERS for integration in the main drivetrain of a large mining truck. The programme is being

conducted in collaboration with one of the largest global manufacturers of off-highway construction and

mining equipment and within the Energy Technologies Institute’s (‘ETI’) Heavy Duty Vehicle Efficiency

programme. The programme is progressing well. The detailed design work is largely complete with

procurement of long lead time components underway. In parallel, we are in discussions with the ETI about

opportunities to demonstrate the KERS design in an on-highway commercial vehicle application such as an

articulated truck. The programme is on track and we are confident that all the technical requirements of

this demanding application will be delivered by the KERS design, demonstrating the scalability and high

power density of the low cost KERS technology.

The Group recently announced it had been awarded an Advanced Propulsion Centre (‘APC’) funded project

in collaboration with Turner Powertrain Systems (a wholly-owned subsidiary of Caterpillar Inc.). The

purpose of the project is to design and develop a low cost production-intent energy storage and recovery

system using the Group’s core flywheel technology for installation in a range of Caterpillar off-highway

machines. The initial target application is wheel loaders where the KERS technology will be integrated with

Caterpillar’s leading edge hydrostatic continuously variable transmission, delivering significant reductions in

7

fuel consumption and CO2 emissions and enabling engine downsizing. Work on the 42 month project is due

to commence shortly.

The engineering team has recently completed the cost-down design iteration of the hydraulically-

connected flywheel-based energy recovery system (‘ERS’) developed in collaboration with JCB, and funded

by the APC. The improved design has been released to the Group’s supply chain partners who are

conducting a detailed costing exercise, validating the target production-intent system cost. The next stage

in the programme is investment by the Group and its supply chain partners in production tooling to enable

production-intent ERS units and sub-systems to commence full validation testing from mid-2017, in

preparation for market launch in mid-2018. The Group has recently completed a detailed market study

which confirms the significant market opportunity for ERS, offering operator paybacks of less than two

years in a range of off-highway machines including excavators, wheel loaders and materials handling

equipment. In parallel, discussions have been held with the main global Tier 1s and OEMs about trialling the

production-intent ERS product on a range of machines starting in the second half of calendar year 2017.

These discussions are ongoing, with a number of OEMs interested in the ERS product.

We are continuing discussions to licence our KERS technology into the global off-highway sector.

On-highway:

We continue to explore opportunities for the Bus KERS product in on-highway bus and truck applications

outside the UK. Discussions with potential customers and partners are at an early stage and we will update

shareholders with any significant progress in these applications.

Passenger cars:

The passenger car market remains an important target for the Group’s KERS technology. The key driver for

adoption onto vehicle platforms from 2020 onwards is a competitive cost per gram of CO2 saved compared

to alternative hybridisation options, such as electric solutions. The Group is conducting initial feasibility

studies with several OEMs looking at KERS on both hybrid and full battery electric vehicles, where the KERS

technology offers superior cost per gram of CO2 saved.

We are discussing the Group’s participation in an EU-funded consortium including vehicle OEMs and Tier 1s

about the use of our KERS technology in conjunction with an electric motor offering an alternative electro-

mechanical hybridisation solution for hybrid electric vehicles. The project would leverage the Group’s low

cost KERS technology and would be evaluated in a demonstrator vehicle against other hybrid solutions.

IVT/CVT

Our main focus in the last six months has been to build on the progress made earlier in the year in the

development and validation of new low cost mass manufacturing methods for discs and rollers for use in V-

Charge and other applications. The work, being conducted in collaboration with the Advanced Forming

Research Centre and the Manufacturing Technology Centre, underpins the Group’s confidence in achieving

the target, and highly competitive, bill of materials cost for V-Charge.

We have received a number of enquiries from automotive Tier 1s and OEMs about the potential

opportunity to use the Group’s core variator technology in the drivetrain for battery electric vehicles

(‘BEV’). Whilst these enquiries are at an early stage, it appears that drivetrains using our core CVT

technology have the potential to offer BEVs a cost effective improvement in performance, including

8

acceleration and gradeability, whilst maintaining the feel of ‘liquid power’. A number of auxiliary power

applications using the core CVT technology are also in the early stages of evaluation.

The Group continues to support its strategic partner Univance in looking at opportunities for the Group’s

CVT technology in off-highway applications. Univance offers licensees of Torotrak’s variator technology the

opportunity to source low cost discs, rollers and complete variators from an established volume Tier 2

supplier of transmissions and transmission components for lower volume passenger cars and off-highway

applications.

Flywheel assembly manufacturing

During the last six months, the Group has been working to validate the design for lower cost flywheels in

conjunction with the Group’s strategic supply chain partners. Flywheels manufactured using a low cost

forging process have successfully completed the full life durability testing programme, exceeding the target

life requirements for the off-highway market. The next step in the development programme is to validate

further cost-down opportunities using lower cost materials and further improvements to the current

design. This work is important to delivering the step-change reduction in the cost of the hydraulically-

connected ERS product and meeting the challenging cost targets in passenger car applications.

We have completed the set-up of the Group’s low-volume flywheel assembly manufacturing cell facility in

Leyland. This facility includes some initial automation with processes managed to automotive quality

controlled standards. This is a significant step forward in building the in-house capability to assemble

complete flywheels in volumes of up to 10,000 units p.a.

Financial

Revenue in the period was £0.9 million (2015: £1.2 million) reflecting the focus on business development

activities related to licensing V-Charge and KERS and customer funded development programmes

commencing part way through the period. The reduction in gross profit of £0.2 million in the period is due

to lower engineering services revenues and a lack of licensing revenues in the period (2015: £0.1m licence

revenue). Revenue is targeted to increase in the second half of the year.

The operating loss before intangible asset amortisation (know-how) and exceptional items for the period

was £3.3 million, in line with the same period last year. The reduction in gross profit of £0.2 million and

higher non-cash expenses, being depreciation and share-based payments, of £0.2 million were offset by an

11 per cent. reduction in net cash operating expenses of £0.4 million. The loss for the period was £3.5

million, a reduction of £5.9 million over the previous period due to the exceptional costs in the previous

period of £6.0 million relating to the restructure of the Flybrid acquisition agreement, write down of the

Group’s investment in, and loan to, Rotrex A/S and other restructuring costs.

During the period the equity free cash outflow (EFCF1) was £3.4 million (2015: £4.6 million); an

improvement of 26 per cent. This has largely been achieved through the successful reduction in net cash

operating costs as previously reported, a £0.4 million receipt of research and development tax credits and

is despite a £0.1 million increase in capital expenditure, mainly as a result of the investment in the flywheel

assembly facility. 1Net decrease in cash and cash equivalents, excluding proceeds from the issue of share capital and the repayment of borrowings.

9

The closing cash balance of £7.9 million (2015: £14.4 million) is in line with management’s expectations.

Our focus during the period has been on business development to secure licence revenues and to deliver

increased engineering services revenue in the second half of the current financial year and beyond.

Accordingly we expect our cash usage to further improve during the second half of this financial year.

Outlook

The first six months of the year have seen an increase in the level of engagement from potential parties

interested in the Group’s technologies. With a focus on our strategic objective of commercialising and

monetising our technologies, the Group’s immediate priorities for the next 6 months are:

Completing demonstrations of the Ford S-MAX,

Licensing V-Charge into the global passenger car market,

Licensing KERS into the global off-highway market,

Developing commercial interest in the Group’s hydraulically-connected ERS product underpinning

the commercial uptake in excavators and/or wheel loaders from 2018 onwards,

Commencing the production of low cost flywheel assemblies for use in the ERS validation

programme.

I look forward to reporting progress on our delivery against these key priorities.

Adam Robson

Chief Executive Officer

29 November 2016

10

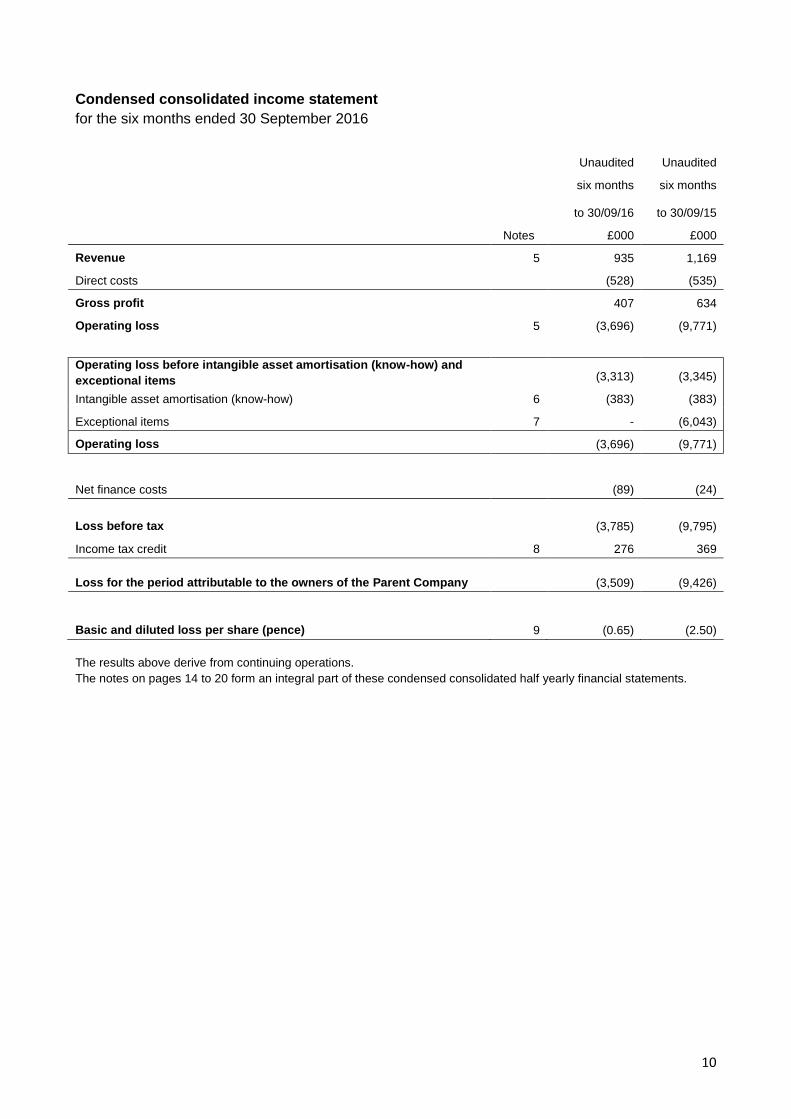

Condensed consolidated income statement

for the six months ended 30 September 2016

Unaudited Unaudited

six months six months

to 30/09/16 to 30/09/15

Notes £000 £000

Revenue 5 935 1,169

Direct costs (528) (535)

Gross profit 407 634

Operating loss 5 (3,696) (9,771)

Operating loss before intangible asset amortisation (know-how) and

exceptional items (3,313) (3,345)

Intangible asset amortisation (know-how) 6 (383) (383)

Exceptional items 7 - (6,043)

Operating loss (3,696) (9,771)

Net finance costs (89) (24)

Loss before tax (3,785) (9,795)

Income tax credit 8 276 369

Loss for the period attributable to the owners of the Parent Company (3,509) (9,426)

Basic and diluted loss per share (pence) 9 (0.65) (2.50)

The results above derive from continuing operations.

The notes on pages 14 to 20 form an integral part of these condensed consolidated half yearly financial statements.

11

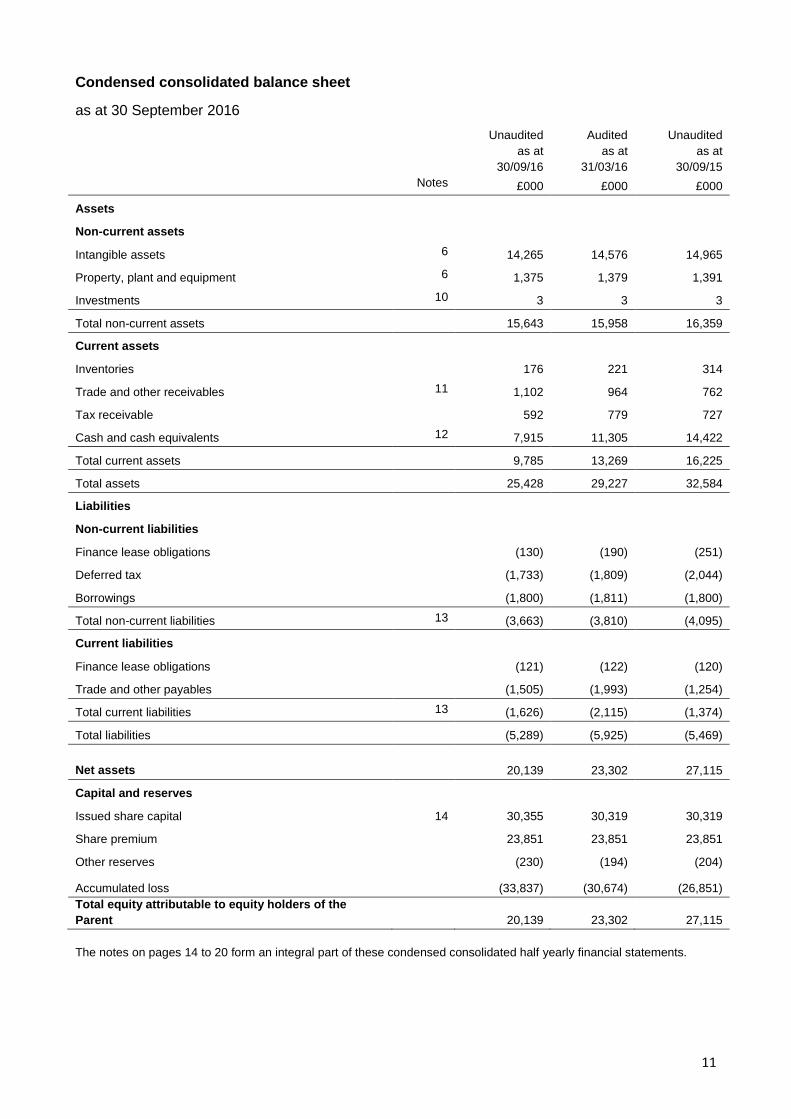

Condensed consolidated balance sheet

as at 30 September 2016

Unaudited Audited Unaudited

as at

30/09/16

as at

31/03/16

as at

30/09/15

Notes £000 £000 £000

Assets

Non-current assets

Intangible assets 6 14,265 14,576 14,965

Property, plant and equipment 6 1,375 1,379 1,391

Investments 10 3 3 3

Total non-current assets 15,643 15,958 16,359

Current assets

Inventories 176 221 314

Trade and other receivables 11 1,102 964 762

Tax receivable 592 779 727

Cash and cash equivalents 12 7,915 11,305 14,422

Total current assets 9,785 13,269 16,225

Total assets 25,428 29,227 32,584

Liabilities

Non-current liabilities

Finance lease obligations (130) (190) (251)

Deferred tax (1,733) (1,809) (2,044)

Borrowings (1,800) (1,811) (1,800)

Total non-current liabilities 13 (3,663) (3,810) (4,095)

Current liabilities

Finance lease obligations (121) (122) (120)

Trade and other payables (1,505) (1,993) (1,254)

Total current liabilities 13 (1,626) (2,115) (1,374)

Total liabilities (5,289) (5,925) (5,469)

Net assets

20,139 23,302 27,115

Capital and reserves

Issued share capital 14 30,355 30,319 30,319

Share premium 23,851 23,851 23,851

Other reserves (230) (194) (204)

Accumulated loss (33,837) (30,674) (26,851)

Total equity attributable to equity holders of the

Parent 20,139 23,302 27,115

The notes on pages 14 to 20 form an integral part of these condensed consolidated half yearly financial statements.

12

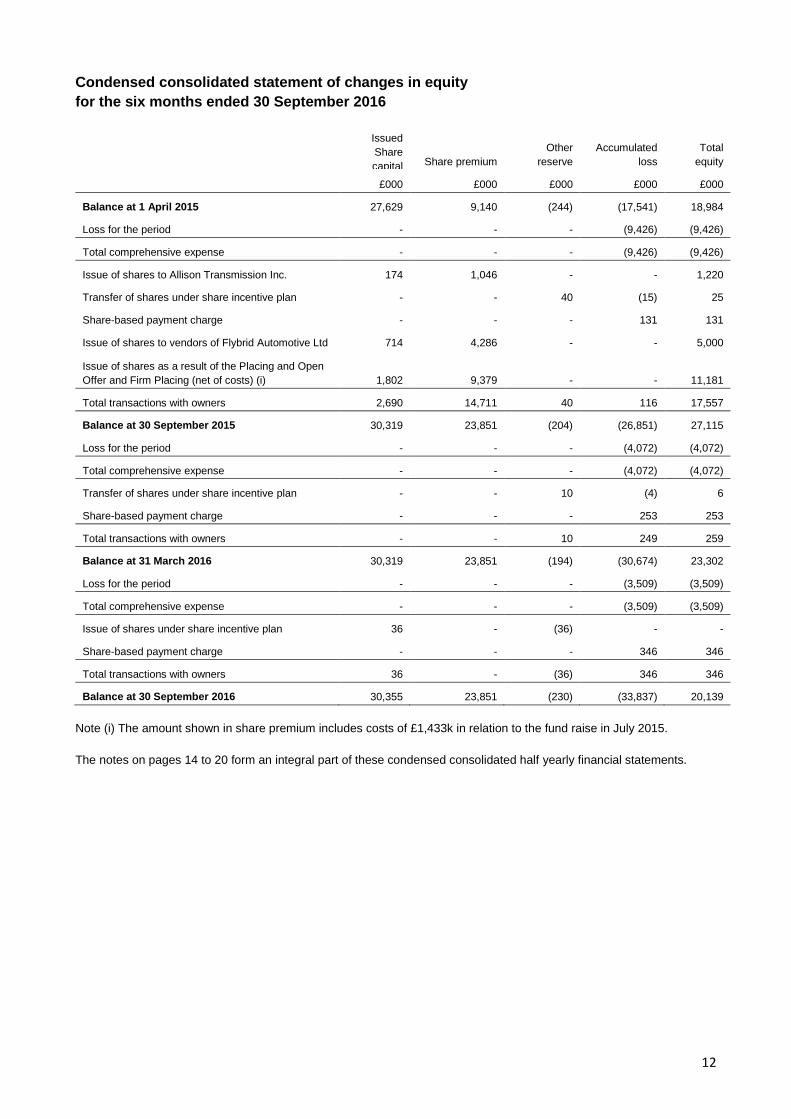

Condensed consolidated statement of changes in equity

for the six months ended 30 September 2016

Issued

Share

capital Share premium

Other

reserve

Accumulated

loss

Total

equity

£000 £000 £000 £000 £000

Balance at 1 April 2015 27,629 9,140 (244) (17,541) 18,984

Loss for the period - - - (9,426) (9,426)

Total comprehensive expense - - - (9,426) (9,426)

Issue of shares to Allison Transmission Inc. 174 1,046 - - 1,220

Transfer of shares under share incentive plan - - 40 (15) 25

Share-based payment charge - - - 131 131

Issue of shares to vendors of Flybrid Automotive Ltd 714 4,286 - - 5,000

Issue of shares as a result of the Placing and Open

Offer and Firm Placing (net of costs) (i) 1,802 9,379 - - 11,181

Total transactions with owners 2,690 14,711 40 116 17,557

Balance at 30 September 2015 30,319 23,851 (204) (26,851) 27,115

Loss for the period - - - (4,072) (4,072)

Total comprehensive expense - - - (4,072) (4,072)

Transfer of shares under share incentive plan - - 10 (4) 6

Share-based payment charge - - - 253 253

Total transactions with owners - - 10 249 259

Balance at 31 March 2016 30,319 23,851 (194) (30,674) 23,302

Loss for the period - - - (3,509) (3,509)

Total comprehensive expense - - - (3,509) (3,509)

Issue of shares under share incentive plan 36 - (36) - -

Share-based payment charge - - - 346 346

Total transactions with owners 36 - (36) 346 346

Balance at 30 September 2016 30,355 23,851 (230) (33,837) 20,139

Note (i) The amount shown in share premium includes costs of £1,433k in relation to the fund raise in July 2015.

The notes on pages 14 to 20 form an integral part of these condensed consolidated half yearly financial statements.

13

Condensed consolidated statement of cash flows

for the six months ended 30 September 2016

Unaudited Unaudited

six months six months

to 30/09/16 to 30/09/15

Notes

£000 £000

Cash flows from operating activities

Loss for the period (3,509) (9,426)

Adjustments for:

Non-cash exceptional cost in relation to the restructure of the Flybrid

acquisition agreement - 5,000

Impairment of investment in Rotrex A/S - 270

Creation of provision against Rotrex A/S loan - 147

Depreciation 6 214 300

Amortisation 6 482 473

Net finance costs 89 24

Loss on disposal of plant and equipment - 9

Taxation 8 (276) (369)

Charge for equity-settled employee share schemes and bonuses 346 131

Decrease in inventories 45 69

(Increase)/decrease in trade and other receivables (140) 406

Decrease in trade and other payables (464) (1,258)

Cash used in operations (3,213) (4,224)

Tax received 386 -

Net cash used in operating activities (2,827) (4,224)

Cash flows from investing activities

Acquisition of property, plant and equipment (286) (67)

Acquisition of intangible assets (patents) (128) (228)

Net cash used in investing activities (414) (295)

Cash flows from financing activities

Proceeds from the issue of share capital (net of costs) - 12,401

Net finance costs (88) (18)

Repayment of borrowings - (1,000)

Net hire purchase finance (61) (58)

Net cash (used in)/generated from financing activities (149) 11,325

Net (decrease)/increase in cash and cash equivalents (3,390) 6,806

Cash and cash equivalents at start of period 11,305 7,616

Cash and cash equivalents at end of period 12 7,915 14,422

The notes on pages 14 to 20 form an integral part of these condensed consolidated half yearly financial statements.

14

Notes to the half year financial information

1. General information

Torotrak plc (the Company) is a public limited company incorporated and domiciled in the UK. The address of its

registered office is 1 Aston Way, Leyland, Lancashire PR26 7UX. The Company is listed on the London Stock

Exchange under the trading symbol TRK. These condensed consolidated interim financial statements were

approved for issue on 28 November 2016.

The Group’s activities focus on the design, development and commercialisation of a range of technologies that

enable vehicle manufacturers to meet new regulations as well as improving fuel-efficiency, reducing emissions and

enhancing performance.

The interim financial statements for the period ended 30 September 2016 do not constitute statutory accounts

within the meaning of section 434 of the Companies Act 2006.

The financial information set out in this interim statement relating to the year ended 31 March 2016 does not

constitute statutory accounts for that period. Full statutory accounts of the Group in respect of that financial year

were approved by the Board of Directors on 26 July 2016 and have been delivered to the Registrar of Companies.

The report of the Auditors on these accounts was unqualified, did not contain an emphasis of matter paragraph and

did not contain a statement under section 498 of the Companies Act 2006.

1.1 Going concern basis

The Group’s business activities, together with the factors likely to affect its future development, performance and

position are set out in the Chief Executive Officer’s Review (‘CEO’s Review’). The financial position of the Group

and liquidity position are described within the CEO’s Review.

After making all necessary enquiries, the Directors have a reasonable expectation that the Group has adequate

resources to continue in operational existence for a period of at least twelve months from the date that these

interim Financial Statements were approved, given the cash resources available to the Group and the future cash

flow forecast. Accordingly, the Directors believe that it is appropriate for the Financial Statements to continue to be

prepared on the going concern basis.

2. Basis of preparation

These condensed consolidated interim financial statements for the six months ended 30 September 2016, have

neither been reviewed or audited, have been prepared in accordance with the Disclosure and Transparency Rules

(DTR) of the Financial Conduct Authority and in accordance with IAS 34, ‘Interim financial reporting’ as adopted by

the European Union (EU). The condensed consolidated interim financial statements should be read in conjunction

with the annual financial statements for the year ended 31 March 2016 which have been prepared in accordance

with International Financial Reporting Standards (IFRSs) as adopted by the EU.

3. Accounting policies

The accounting policies adopted in preparation of the condensed consolidated interim financial statements as at,

and for the six months to, 30 September 2016 are consistent with the policies applied by the Group in its

consolidated financial statements as at, and for the year to, 31 March 2016, except as described below:

- Taxes on income in the interim periods are accrued using the effective tax rate that would be

applicable to expected total annual profit or loss.

There are no new standards or amendments to standards that are mandatory for the first time in the financial year

beginning 1 April 2016 that have an impact on the Group financial statements.

4. Critical accounting estimates and assumptions

In applying the accounting policies, appropriate estimates have been made in many areas. The key areas of

estimation uncertainty, where assumptions and estimates are significant in terms of impact upon the financial

15

statements, are the same as those that are described in the annual financial statements for the year ended 31

March 2016.

5. Operating segments

Operating segmental analysis for the six months ended 30 September 2016

Engineering

services

Income from

licence

agreements

Development

activities

(i)

Total

£000 £000 £000 £000

Revenue (by technology)

IVT 50 - - 50

Flybrid ERS 854 - - 854

V-Charge and other 31 - - 31

Total revenue 935 - - 935

Direct costs (528) - - (528)

Gross profit 407 - - 407

Other operating costs - - (2,416) (2,416)

Total segmental profit/(loss) 407 - (2,416) (2,009)

Other operating costs not allocated to

segments (1,687)

Operating loss (3,696)

Operating segmental analysis for the six months ended 30 September 2015

Engineering

services

Income from

licence

agreements

Development

activities

(i)

Total

£000 £000 £000 £000

Revenue (by technology)

IVT 66 100 - 166

Flybrid ERS 999 - - 999

V-Charge and other 4 - - 4

Total revenue 1,069 100 - 1,169

Direct costs (533) (2) - (535)

Gross profit 536 98 - 634

Other operating costs - - (2,735) (2,735)

Total segmental profit/(loss) 536 98 (2,735) (2,101)

Other operating costs not allocated to

segments (7,670)

Operating loss (9,771)

Note (i) Development activities include research and the creation of intellectual property.

16

Significant customers

The following revenues are attributable to significant customers:

Unaudited Unaudited

six months six months

to 30/09/16 to 30/09/15

£000 £000

Allison Transmission Inc. - 100

Undisclosed customer - 633

Undisclosed customer - 150

Undisclosed customer 762 130

6. Property, plant and equipment and intangible assets

Property plant

and equipment

Intangible assets

(patents)

Intangible

assets

(goodwill and

know-how) Total

£000 £000 £000 £000

Net book value at 1 April 2015 1,698 2,314 12,907 16,919

Additions 7 217 - 224

Disposals (14) - - (14)

Amortisation/depreciation (300) (90) (383) (773)

Net book value at 30 September 2015 1,391 2,441 12,524 16,356

Additions 250 158 - 408

Disposals - (30) - (30)

Amortisation/depreciation (262) (93) (384) (739)

Impairment provision - (40) - (40)

Net book value at 31 March 2016 1,379 2,436 12,140 15,955

Additions 210 171 - 381

Amortisation/depreciation (214) (99) (383) (696)

Net book value at 30 September 2016 1,375 2,508 11,757 15,640

7. Exceptional items

Unaudited Unaudited

as at 30/09/16 as at 30/09/15

£000 £000

Restructuring costs – severance related - 539

Share issue in relation to the restructure of the Flybrid acquisition

agreement - 5,000

Impairment of investment in Rotrex A/S - 270

Provision against the loan to Rotrex A/S - 147

Restructuring costs - one-off legal and other costs - 87

Total - 6,043

The severance related restructuring costs relate to redundancy, severance and associated expenses in relation to

a reduction in employees.

In the financial year ended 31 March 2016 the Group received Shareholder approval to restructure the acquisition

agreement with the vendors of Flybrid Automotive Limited and as such a one-off settlement was agreed with the

vendors by way of issuing new ordinary shares in the Group to the value of £5m. The vendors of Flybrid

Automotive Limited, Jon Hilton (Non-Executive Director) and Doug Cross (Chief Technology Officer), received

17

shares to the value of £3.5m and £1.5m respectively as part of the settlement. The £5m was treated as an

exceptional item.

The investment in Rotrex A/S and the loan due from Rotrex A/S were written down in the financial year ended 31

March 2016 due to the uncertainty of the value of the net assets of Rotrex A/S and also the recoverability of the

loan.

The one-off legal and other costs relate to the restructuring of the Flybrid acquisition agreement.

8. Taxation

The Finance Act 2000 introduced the research and development tax credit, which allows companies with qualifying

expenditure to surrender their tax losses for cash. The credit for research and development tax credits for the

period is based on the estimated effective tax rate of 33.35% (2015: 33.35%).

Changes to the UK corporation tax rates were announced on 8 July 2015. These changes were substantively

enacted as part of the Finance Bill 2015 on 26 October 2015 and include reductions to the main rate to 19% from 1

April 2017 and to 18% from 1 April 2020. On 16 March 2016 further changes to the UK corporation tax rate were

announced including a further reduction in the UK corporation tax rate to 17% from 2020, which supersedes the

change enacted on 26 October 2015, and which was substantively enacted as part of the Finance Bill 2016 on 15

September 2016.

The deferred tax liability relates solely to the intangible assets recognised on the acquisition of Flybrid Automotive

Limited. The deferred tax liability will be amortised through the Income Statement to match the amortisation of the

underlying intangible asset, being over 15 years.

Unaudited Unaudited

as at 30/09/16 as at 30/09/15

£000 £000

R&D tax credit 199 292

Deferred tax 77 77

Total 276 369

9. Loss per share

The basic and diluted loss per share are based on a loss after tax of £3,509,000 (2015: £9,426,000). The weighted

average number of shares was 543.4 million shares (2015: 376.8 million) and the diluted weighted average number

of shares was 621.3 million (2015: 390.7 million).

For the six months ended 30 September 2016 and 2015 potential share options are antidilutive, as their inclusion in

the diluted loss per share calculation would reduce the loss per share, and hence have been excluded.

Unaudited Unaudited

six months six months

to 30/09/16 to 30/09/15

The basic loss per share from continuing operations attributable to the

equity holders of the Company (pence) (0.65) (2.50)

The diluted loss per share from continuing operations attributable to the

equity holders of the Company (pence) (0.65) (2.50)

In accordance with IAS33 ‘Earnings per Share’ the number of shares used in the calculation excludes the weighted

average number of shares held by the Employee Benefits Trust of 4,925,535 (2015: 2,369,723).

18

10. Investments

Unaudited Audited Unaudited

as at 30/09/16 as at 31/03/16 as at 30/09/15

£000 £000 £000

Net investment in Rotrak joint venture 3 3 3

The Group also holds an investment in Rotrex A/S. This investment is no longer supported by the net assets of

Rotrex A/S and as such an impairment provision was created in the financial year ended 31 March 2016 in

accordance with the Group’s accounting policy. This investment has a net book value of £nil (2015: £nil).

11. Trade and other receivables

Unaudited Audited Unaudited

as at 30/09/16 as at 31/03/16 as at 30/09/15

£000 £000 £000

Current assets

Net trade receivables 357 66 153

Other receivables and accrued income 379 367 313

Prepayments 366 531 296

Total trade and other receivables 1,102 964 762

At 30 September 2016 the Group had a loan outstanding of £147k with Rotrex A/S. In the financial year ended 31

March 2016 a provision was created against the value of this loan due to the uncertainty of recoverability. This

loan has a net book value of £nil (2015: £nil).

The net trade receivables includes a provision for impairment of £51k in relation to a potentially unrecoverable debt

in accordance with the Group’s accounting policy.

12. Cash and cash equivalents

Unaudited Audited Unaudited

as at 30/09/16 as at 31/03/16 as at 30/09/15

£000 £000 £000

Cash 17 17 20

Sterling short term cash deposits 7,039 10,481 14,033

Foreign currency and cash deposits 859 807 369

Total cash and cash equivalents 7,915 11,305 14,422

19

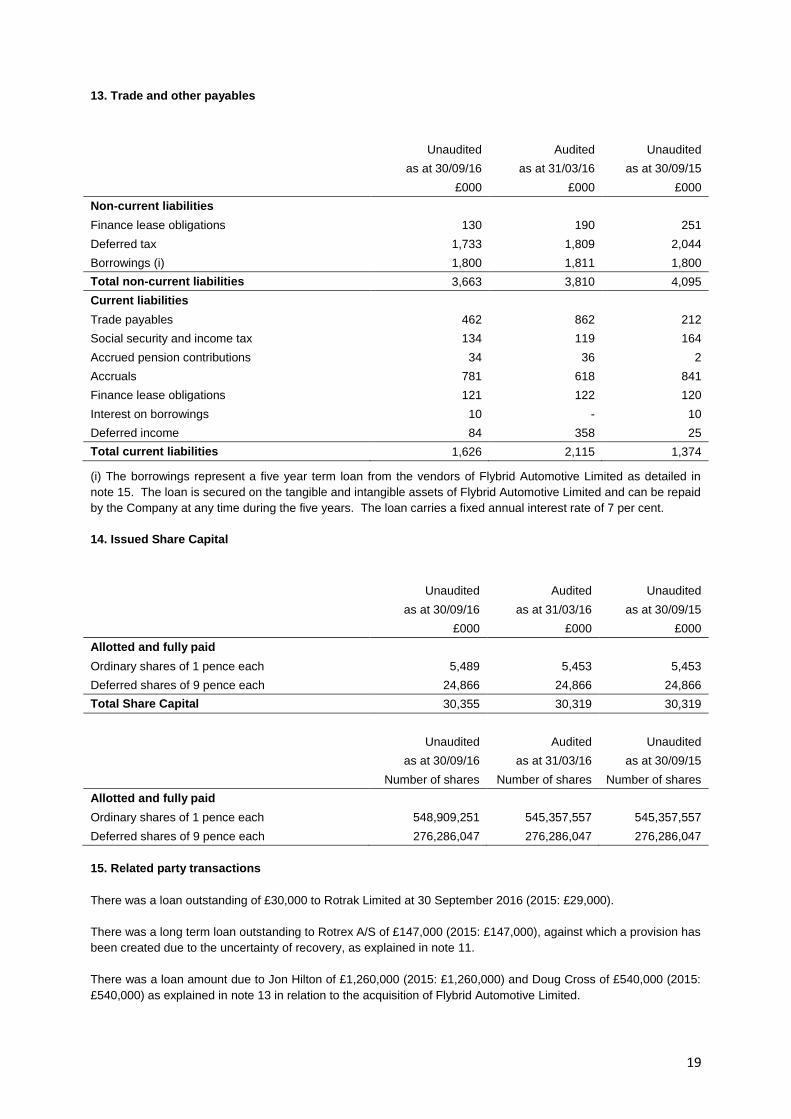

13. Trade and other payables

Unaudited Audited Unaudited

as at 30/09/16 as at 31/03/16 as at 30/09/15

£000 £000 £000

Non-current liabilities

Finance lease obligations 130 190 251

Deferred tax 1,733 1,809 2,044

Borrowings (i) 1,800 1,811 1,800

Total non-current liabilities 3,663 3,810 4,095

Current liabilities

Trade payables 462 862 212

Social security and income tax 134 119 164

Accrued pension contributions 34 36 2

Accruals 781 618 841

Finance lease obligations 121 122 120

Interest on borrowings 10 - 10

Deferred income 84 358 25

Total current liabilities 1,626 2,115 1,374

(i) The borrowings represent a five year term loan from the vendors of Flybrid Automotive Limited as detailed in

note 15. The loan is secured on the tangible and intangible assets of Flybrid Automotive Limited and can be repaid

by the Company at any time during the five years. The loan carries a fixed annual interest rate of 7 per cent.

14. Issued Share Capital

Unaudited Audited Unaudited

as at 30/09/16 as at 31/03/16 as at 30/09/15

£000 £000 £000

Allotted and fully paid

Ordinary shares of 1 pence each 5,489 5,453 5,453

Deferred shares of 9 pence each 24,866 24,866 24,866

Total Share Capital 30,355 30,319 30,319

Unaudited Audited Unaudited

as at 30/09/16 as at 31/03/16 as at 30/09/15

Number of shares Number of shares Number of shares

Allotted and fully paid

Ordinary shares of 1 pence each 548,909,251 545,357,557 545,357,557

Deferred shares of 9 pence each 276,286,047 276,286,047 276,286,047

15. Related party transactions

There was a loan outstanding of £30,000 to Rotrak Limited at 30 September 2016 (2015: £29,000).

There was a long term loan outstanding to Rotrex A/S of £147,000 (2015: £147,000), against which a provision has

been created due to the uncertainty of recovery, as explained in note 11.

There was a loan amount due to Jon Hilton of £1,260,000 (2015: £1,260,000) and Doug Cross of £540,000 (2015:

£540,000) as explained in note 13 in relation to the acquisition of Flybrid Automotive Limited.

20

In the period to 30 September 2016 there was an amount of £44,466 paid to Jon Hilton and an amount of £19,057

paid to Doug Cross in respect of loan interest. £7,250 was due to Jon Hilton and £3,107 due to Doug Cross in

respect of loan interest at 30 September 2016; these amounts were paid on 1 October 2016.

Jon Hilton is a Director of Celeratis Limited. In the period to 30 September 2016 there was an amount of £40,165

paid to Celeratis Limited for consultancy services. There was an amount due to Celeratis Limited of £2,478 at 30

September 2016.

16. Commitments

Capital expenditure contracted for at the balance sheet date but not yet incurred was £nil (2015: £6,000).

17. Financial Risk Management

The Group’s activities expose it to a variety of financial risks including currency risk, credit risk, liquidity risk and

interest rate risk.

The condensed consolidated interim financial statements do not include all financial risk management information

and disclosures required in the annual financial statements; they should be read in conjunction with the Group’s

annual financial statements as at 31 March 2016. There have been no changes in any risk management policies

or financial risks since the year end.

18. Seasonality

The Group’s results and activities are not affected by seasonality.

21

Statement of Directors’ responsibilities

The Directors confirm that, to the best of their knowledge, these condensed consolidated interim financial

statements have been prepared in accordance with IAS 34 ‘interim financial reporting’ as adopted by the European

Union and that the interim management report includes a fair review of the information required by DTR 4.2.7 and

DTR 4.2.8, namely:

an indication of the important events that have occurred during the first six months and their impact on the condensed consolidated interim financial statements, and a description of the principal risks and uncertainties for the remaining six months of the financial year; and

material related-party transactions in the first six months and any material changes in the related-party transactions described in the last annual report.

The Directors of Torotrak plc are listed in the Torotrak plc Annual Report for the year ended 31 March 2016. A list

of current Directors is maintained on the Torotrak plc website: www.torotrak.com.

By order of the Board on 28 November 2016

Adam Robson

Chief Executive

-ends-