Embed Size (px)

Citation preview

Asia Pan-Asia Strategy

28 March 2011

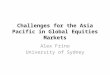

Asia Equities Daily Focus Today's research headlines Asian Edition

Deutsche Bank AG/Hong Kong

All prices are those current at the end of the previous trading session unless otherwise indicated. Prices are sourced from local exchanges via Reuters, Bloomberg and other vendors. Data is sourced from Deutsche Bank and subject companies. Deutsche Bank does and seeks to do business with companies covered in its research reports. Thus, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 007/05/2010

Periodical

Asian Index Closings EQUITIES Close 1D Chg %Chg

SHSZ300 3294.48 1.33 5.31 HSCEI 12975.54 1.12 2.23 HSI 23158.67 1.06 0.54 TWSE 8610.39 0.40 -4.04 KOSPI 2054.04 0.85 0.15 FSSTI 3070.84 0.91 -3.74 KLCI 1515.55 0.11 -0.22 SENSEX 18815.64 2.53 -8.26 NIFTY 5654.25 2.39 -7.83 SET 1037.73 0.32 0.48 JCI 3607.11 -0.13 -2.60 PCOMP 3875.81 0.89 -7.74 ASX200 4742.60 0.92 -0.06 FOREX (vs US$) Close 1D Chg YTD %Chg Rmb 6.56 0.08 0.76 HK$ 7.79 0.00 -0.27 NT$ 29.46 0.42 -0.54 Won 1114.20 0.62 1.06 S$ 1.26 -0.10 1.70 M$ 3.03 0.05 1.22 Rupee 44.68 0.18 0.07 Baht 30.26 0.00 -0.66 Rupiah 8717.00 0.01 3.20 Peso 43.33 0.04 1.09 A$ 1.03 0.38 0.18

Source: Bloomberg Finance LP

Latest Commodity Prices COMMODITIES Close 1D %Chg YTD %Chg West Texas 105.12 0.07 15.04 Brent 115.67 0.08 22.66 CRB 359.57 0.30 8.04 Copper 440.85 -0.13 -0.70 Gold (Spot) 1427.83 -0.20 0.50 Alum. (LME) 2630.00 -0.04 6.48 Baltic Dry 1583.00 1.15 -10.72

Source: Bloomberg Finance LP

DB CORPORATE ACCESS DB Access Indonesia Small Cap Corporate Day - SG 4/5 - 6 DB Access Asia Conference 2011 - Singapore 5/23 - 26 DB Access Taiwan Conference 2011 - Taipei 11/7 - 8 DB Access Korea Conference 2011 - Seoul 11/10 - 11 DB Access Indonesia Conference 2011 - Jakarta 11/29 - 12/1

Research Team

Carissa Szeto Equity Focus (+852) 2203 6171 [email protected] Ching-Li Teo, CFA Equity Focus (+852) 2203 6206 [email protected]

Co

mp

any

Glo

bal

Mar

kets

Res

earc

h

Nodita_ 1. 2.

TOP STORIES F.I.T.T. China Chemicals Tour Increasing the focus on the domestic

consumer Tim Jones Page 5

Shipping vs Shipbuilding Shipbuilding newsflow continues to be strong

Joe Liew Page 6

POSCO (005490.KS),KRW502,000.00 Buy Price Target KRW620,000.00

Set to ride the tailwinds of volume and price Chanwook

Park Page 7

RECOMMENDATION CHANGES

Li & Fung (0494.HK),HKD39.05 Hold Price Target HKD41.10

Fairly valued; downgrading to Hold Anne LingPage 8

ESTIMATE & TARGET PRICE CHANGES

CRE (0291.HK),HKD29.80 Buy Price Target HKD35.50

Bigger and more profitable; maintaining Buy

Rebecca JiangPage 9

ENN Energy (2688.HK),HKD26.15 Buy Price Target HKD28.30

FY10 results in-line with DBe but 5%below consensus

Eric ChengPage 10

Giordano (0709.HK),HKD4.58 Buy Price Target HKD5.77

2011 outlook; maintaining Buy Anne LingPage 11

PICC (2328.HK),HKD9.23 Sell Price Target HKD7.90

Premium solvency at 18.3%;maintaining Sell

Bob LeungPage 12

Cosco Corporation (COSC.SI),SGD2.01 Buy Price Target SGD2.45

LOI with Sevan worth over US$1bn Kevin ChongPage 13

PT Bukit Asam (PTBA.JK),IDR20,950.00 Buy Price Target IDR33,300.00

Adjusting for 2010 results Cherie KhoengPage 14

STRATEGY/ECONOMICS

Asia Economics Daily Malaysia CPI and Singapore IP Kaushik DasPage 15

Asia Credit Weekly Mixed results on property Gene CheonPage 19

Asia Local Markets Week Policy versus supply Sameer GoelPage 20

US Daily Economic Notes Payrolls, production & income dominate data docket

Joseph A. LaVorgna Page 21

US Economics Weekly Staying strong on above trend growth Joseph LaVorgna Page 22

28 March 2011 Strategy Asia Equities Daily Focus

Page 2 Deutsche Bank AG/Hong Kong

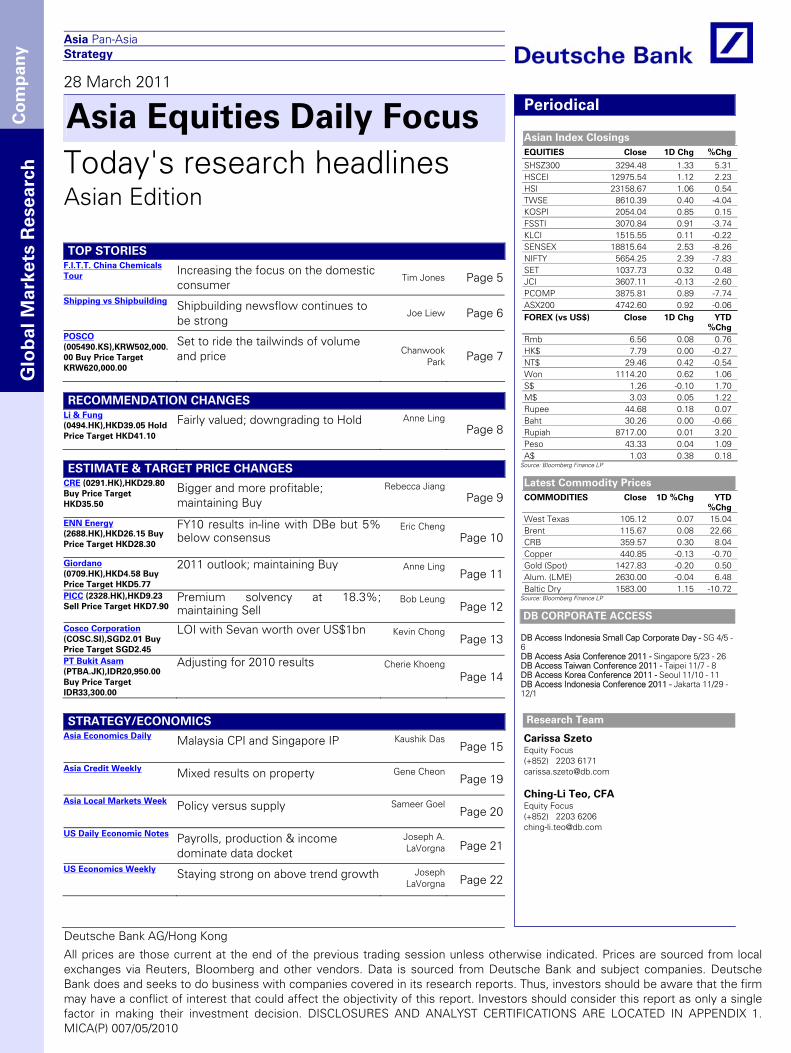

Global Commodities Daily China Macro Outlook Improves Soozhana Choi

Page 25

India Economics Weekly Impact of monetary tightening on growth, weekly WPI update

Taimur BaigPage 27

ADDITIONAL RESEARCH DB MIC

China TMT Daily CM capex; also, 0763.HK, BIDU Alan Hellawell III Page 28 Indonesian Politics

Guest-Speaker: Mr. Wimar Witoelar, Consultant with InterMatrix Communications/Adjunct Professor at Deakin University, Australia

China Comm Services (0552.HK),HKD5.43 Hold Price Target HKD5.20

2H preview Eva LeungPage 29 24 Mar @5pm HK/SG / 4pm Jakarta / 9pm UK

DB CONFERENCE/CORPORATE DAY DB Access Indonesia Small Cap Corporate Day - SG 4/5 - 6

China Construction Bank (0939.HK),HKD7.32 Buy Price Target HKD8.60

2010 NPAT understated on conservative provisioning

Tracy YuPage 30

China Minsheng Bank (1988.HK),HKD7.06 Hold Price Target HKD6.53

More risks, Higher returns Tracy YuPage 31

China Shenhua Energy (1088.HK),HKD34.80 Buy Price Target HKD40.00

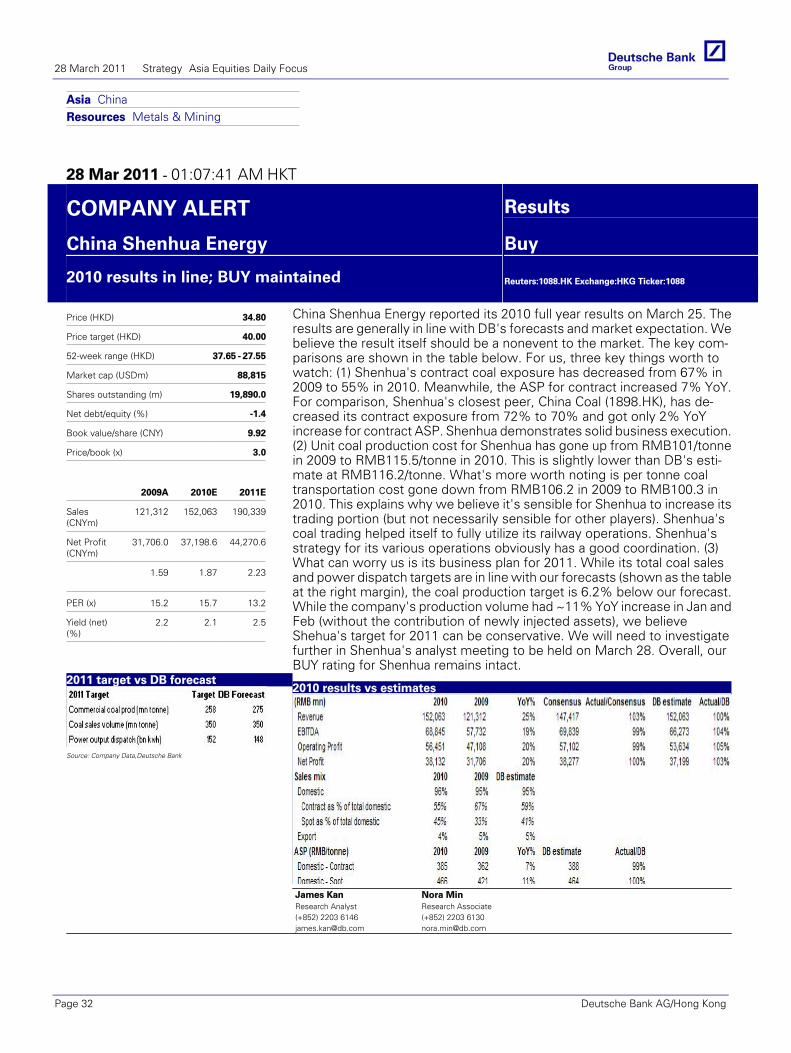

2010 results in line; BUY maintained James KanPage 32

DB Access Asia Conference 2011 - Singapore 5/23 - 26 DB Access Taiwan Conference 2011 - Taipei 11/7 - 8 DB Access Korea Conference 2011 - Seoul 11/10 - 11 DB Access Indonesia Conference 2011 - Jakarta 11/29 - 12/1

NDRs Renhe Commercial Holdings (1387 HK) - SG 3/28 China Unicom

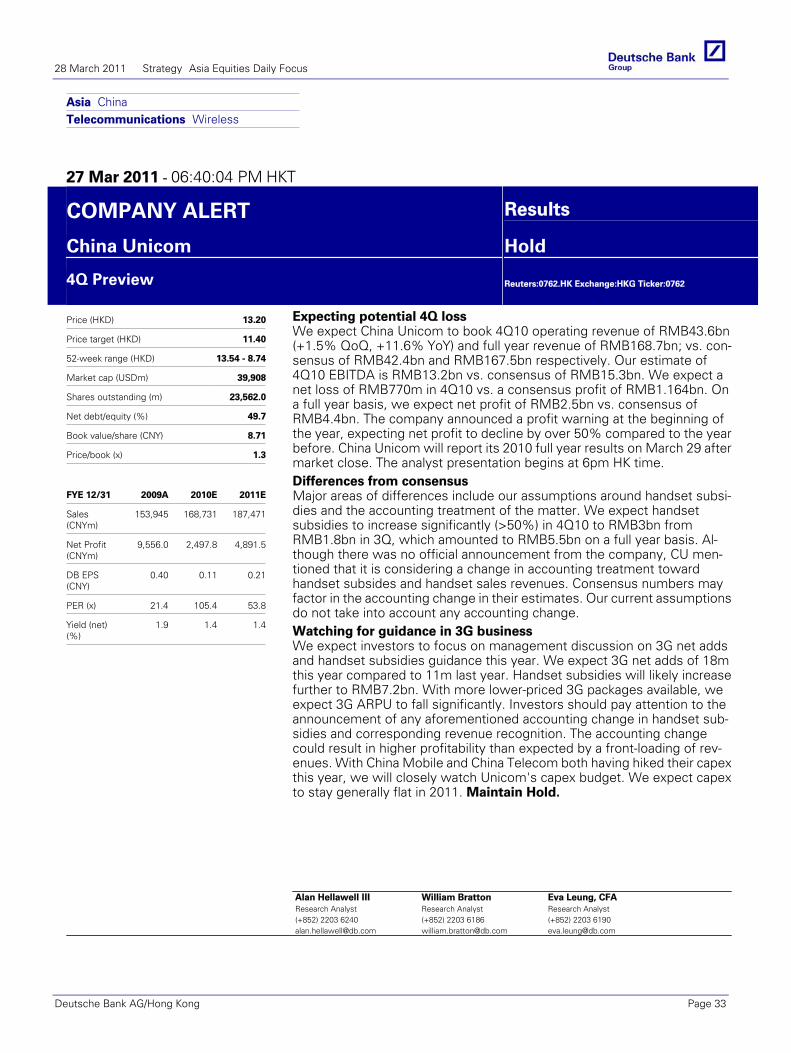

(0762.HK),HKD13.20 Hold Price Target HKD11.40

4Q Preview Alan Hellawell III Page 33 China SCE Property Holdings (1966 HK) - HK 3/28, SG

3/30 China High Speed Transmission Equipment (658 HK) - HK 3/28 - 29 Greentown China Holdings (3900 HK) - HK 3/30 Shenzhen Expressway Co (548 HK) - HK 3/31 Industrial and Commercial Bank of China (1398 HK) - HK 3/30

Shenzhen Expressway-H (0548.HK),HKD4.75 Buy Price Target HKD6.12

2010 results ahead of expectation Phyllis WangPage 34

West China Cement (2233.HK),HKD3.44 Buy Price Target HKD3.76

Xinjiang - new growth phase ahead James KanPage 35

Jack Hu - SG 3/30 - 31 China Shipping Container Liner (2866 HK) - HK 3/31 - 4/1 Nan Ya Printed Circuit Board Corp (8046 TT) - HK 3/30 - 31, Shenzhen 4/1 Hengan International Group (1044 HK) - HK 3/31 C C Land Holdings (1224 HK) - HK 3/31

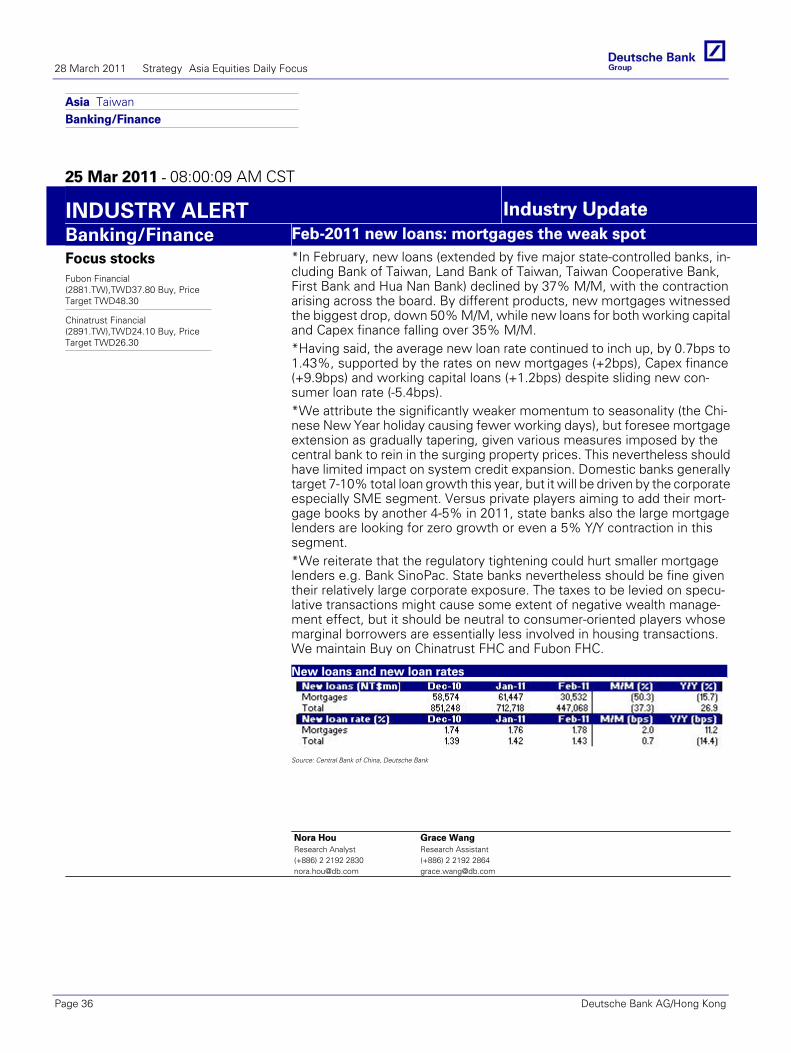

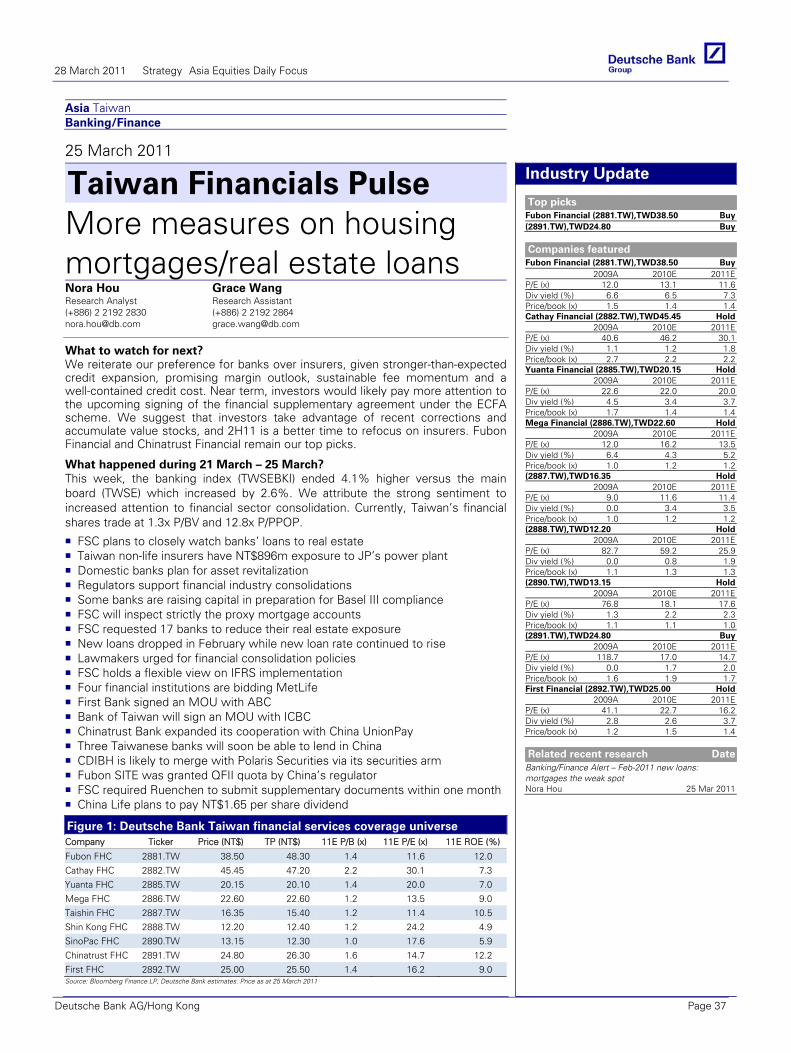

Banking/Finance Feb-2011 new loans: mortgages the weak spot

Nora HouPage 36

Taiwan Financials Pulse More measures on housing mortgages/real estate loans

Nora HouPage 37 NEW: Central China Real Estate (832 HK) - HK 3/31

PT Nippon Indosari Corpindo (ROTI IJ) - HK 4/4 Evergrande Real Estate Group (3333 HK) - SG 4/5, SZX 4/6, PEK 4/8 PT Gajah Tunggal Tbk (GJTL IJ) - HK 4/7 - 8

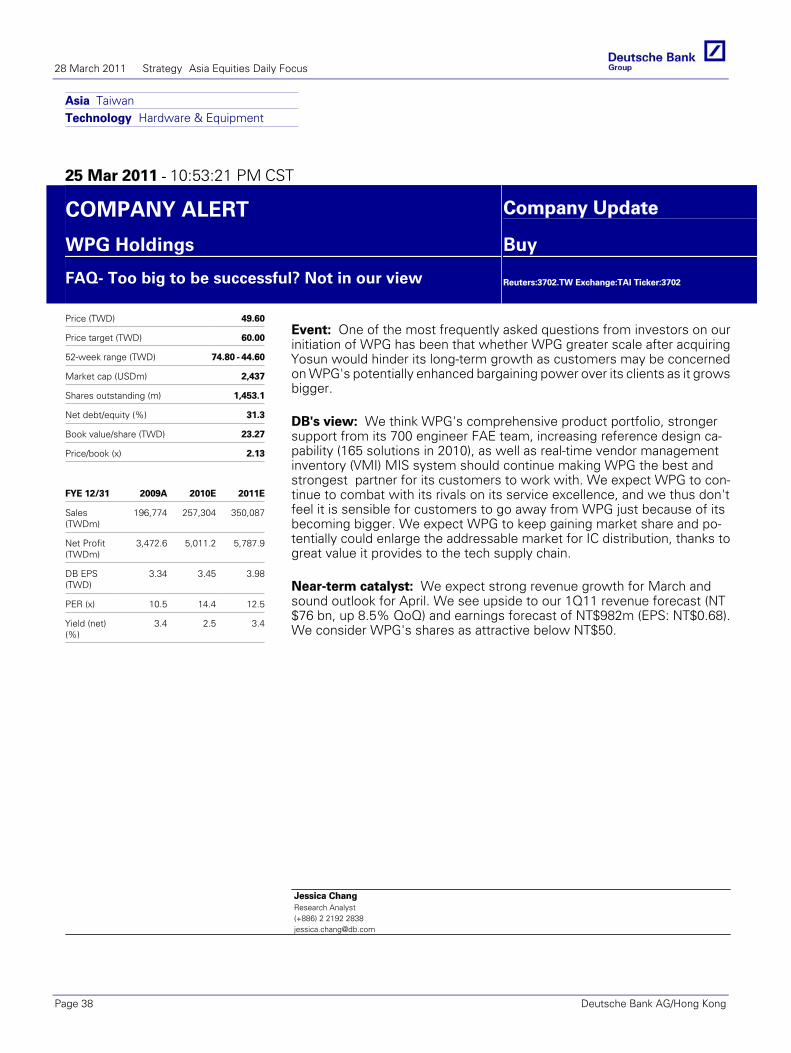

WPG Holdings (3702.TW),TWD49.60 Buy Price Target TWD60.00

FAQ- Too big to be successful? Not in our view

Jessica ChangPage 38 H TC Corporation (2498 TT) - SG 6/21 - 22, HK 6/23 - 24

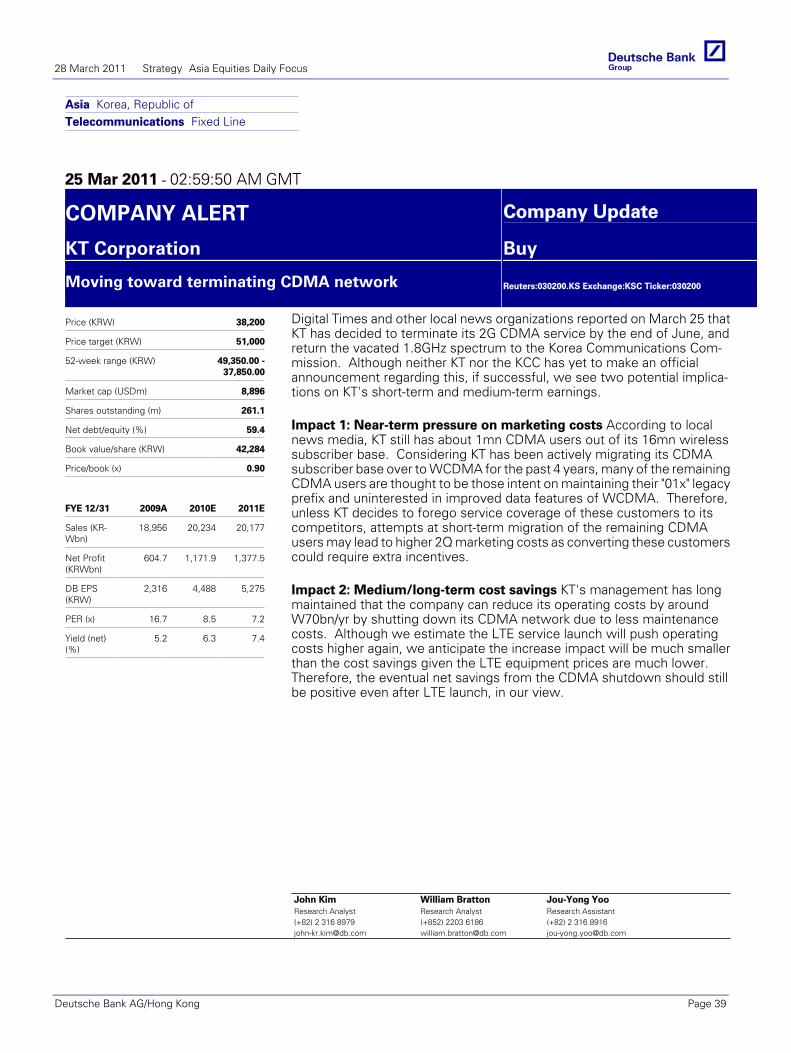

DB ANALYST/SALES ROADSHOWS KT Corporation (030200.KS),KRW38,250.00 Buy Price Target KRW51,000.00

Moving toward terminating CDMA network

John Kim

Page 39 Sanghi Han: Korea Construction and LS Corp./Utilities - HK 3/28 - 29, SG 3/30 - 31 Wei-Shi Wu: Singapore/Malaysia Telecoms - Wiring up the Nation: the Telecoms Transformation - HK 3/30 - 31Gamuda

(GAMU.KL),MYR3.85 Buy Price Target MYR4.45

On track for robust growth; Vietnam property launched

Aun-Ling ChiaPage 40

Srinivas Rao: Telecom & Automotive - SG 3/28 - 29, HK 3/30 & 4/1 NEW: Jack Hu: Post 4Q Take-aways - SG 3/30 - 31, HK 4/6 - 7 Phyllis Wang: China Expressway & Rail - HK 4/1 Christopher Wane: CROCI Global - HK 3/31 & 4/1, SEL 4/4, SG 4/5 - 6, PEK 4/7 John Kim: Korea Telecom - HK 4/1

Mapletree Logistics Trust (MAPL.SI),SGD0.88 Buy Price Target SGD1.06

Acquires Hiroshima Centre for S$114m

Elaine KhooPage 41

Sembcorp Industries Ltd (SCIL.SI),SGD5.04 Buy Price Target SGD7.00

Solid value Kevin ChongPage 42

Marico Limited (MRCO.BO),INR130.55 Buy Price Target INR150.00

Sweekar divested Gaurav BhatiaPage 43

Pharmaceuticals/Biotechnology

NEW: Andrew Hill: Singapore & Malaysia Banks - SG 4/4 Worawat Saisuphatphol: Thai Banking - SG 4/4 - 5, HK 4/6 - 7 Tony Tsang: China & HK Property - PEK 4/7, HK 4/11 - 12, SG 4/14 - 15 Jihyun Song: Korea Consumer - HK 4/11 - 12, SG 4/13 - 14

DB INTERNATIONAL PRODUCT ROADSHOWS

Teva‘s JV with P&G for branded OTC is the way to grow

Abhay Shanbhag Page 44

Software & Services Accenture 2QFY11 : Read through for Indian vendors

Aniruddha Bhosale Page 45

Brett Feldman: US Telecommunications - SEL 3/28, PEK 3/29, HK 3/30, SG 4/1 Rizwan Ali: Telecom - SG 3/29, HK 3/30 Continental AG (CON GR) - HK 4/8 Lloyds Banking Group (LLOY LN) - PEK 4/11, HK 4/12, SG 4/13 Rod Lache: US Auto Industry - PEK 4/11, HK 4/14, SG 4/15 Torsten Slok, Chief International Economist: Global Economics - SEL 4/12, PEK 4/13, SG 4/14

China Shipping Container Liner (2866 HK): Metals & Mining - SG 4/12, HK 4/13, PEK 4/14 Diageo (DGE LN) - HK 5/9, SG 5/10, PEK 5/11

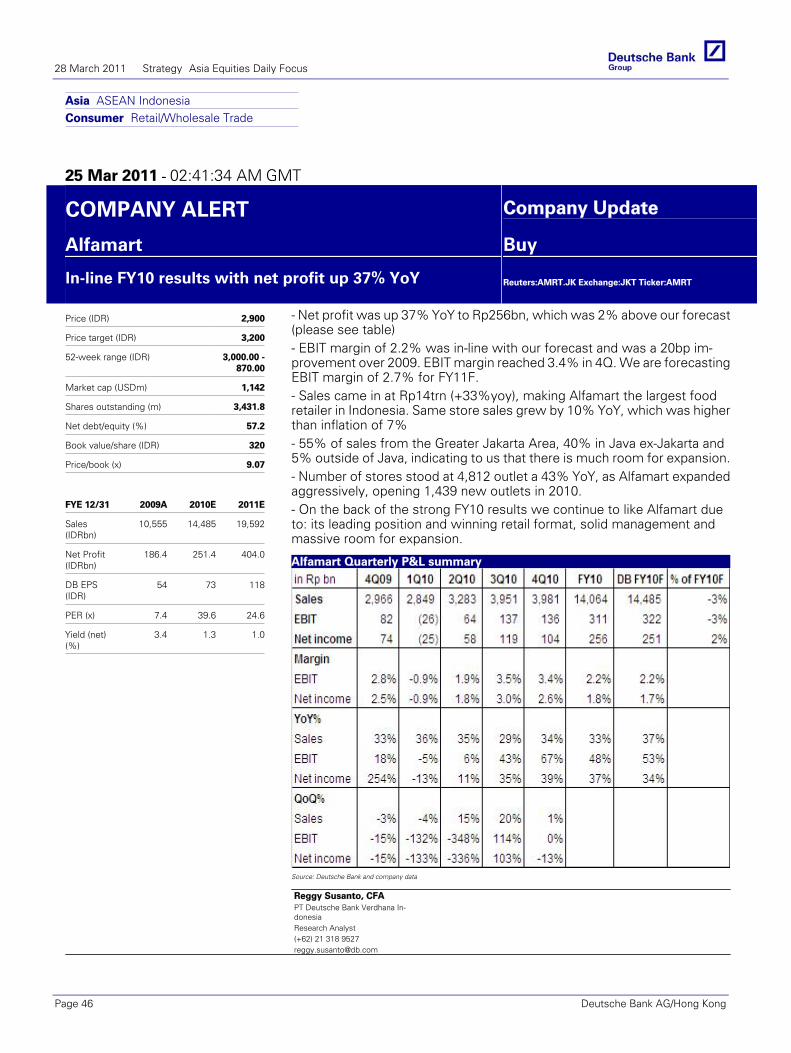

Alfamart (AMRT.JK),IDR2,900.00 Buy Price Target IDR3,200.00

In-line FY10 results with net profit up 37% YoY

Reggy SusantoPage 46

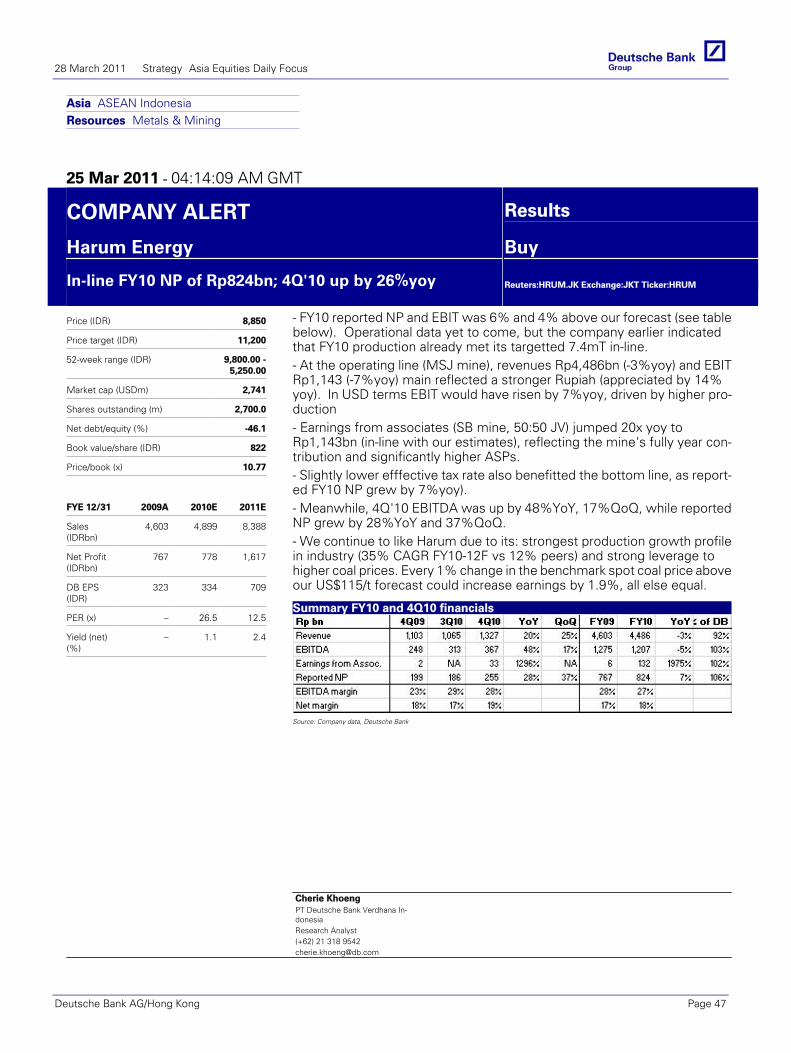

Harum Energy (HRUM.JK),IDR8,650.00 Buy Price Target IDR11,200.00

In-line FY10 NP of Rp824bn; 4Q'10 up by 26%yoy

Cherie KhoengPage 47

Indonesia strategy Key points from DB MIC on politics Heriyanto Irawan Page 48

GLOBAL RESEARCH

Japan auto assemblers Forecast and TP changes: Estimating the earnings impact

Kurt SangerPage 49

Japan Equities Weekly Japan’s recovery capabilities Naoki Kamiyama Page 50

Japan Economics Weekly Restoration demand and "Japan crash thesis" revisited

Mikihiro Matsuoka Page 51

The notes and reports contained in this Daily are all excerpts of previously published documents. Please refer to the published notes on our web site for details on risks, valuations and earnings changes

28 March 2011 Strategy Asia Equities Daily Focus

Page 4 Deutsche Bank AG/Hong Kong

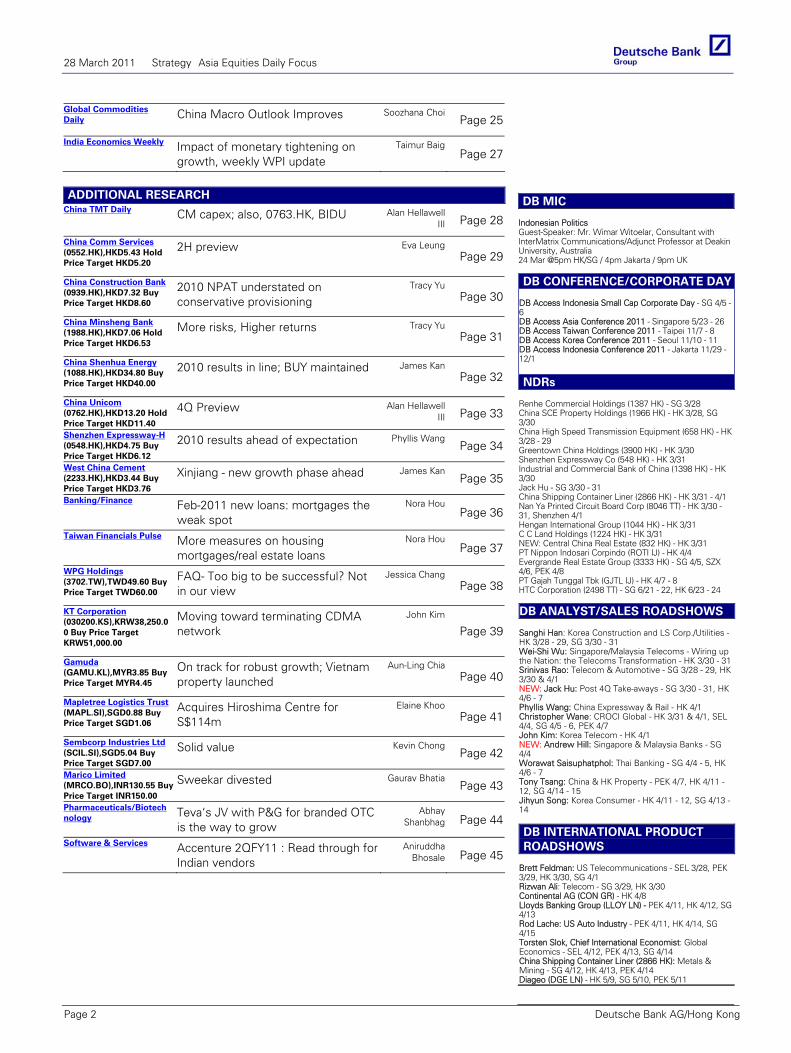

DAILY REVISIONS: TARGET PRICE CHANGES

Company Ticker Date New Previous Chg (%)

Cosco Corporation [Buy] COSC.SI 25-Mar ▲ 2.45 2.30 6.5

ENN Energy [Buy] 2688.HK 27-Mar ▲ 28.30 28.20 0.4

Giordano [Buy] 0709.HK 25-Mar ▲ 5.77 5.35 7.9

PICC [Sell] 2328.HK 25-Mar ▼ 7.90 8.10 -2.5

POSCO [Buy] 005490.KS 25-Mar ▲ 620,000.00 600,000.00 3.3

PT Bukit Asam [Buy] PTBA.JK 25-Mar ▼ 33,300.00 35,600.00 -6.5

EPS REVISIONS

Company Ticker Date FY New Previous Chg (%)

Cosco Corporation [Buy] COSC.SI 25-Mar Dec 11 ▲ 0.12 0.12 3.5

Dec 12 ▲ 0.15 0.14 6.4

Dec 13 ▲ 0.14 0.14 6.5

ENN Energy [Buy] 2688.HK 27-Mar Dec 09 ▲ 0.86 0.86 0.3

Dec 10 ▼ 1.00 1.02 -2.7

Dec 11 ▼ 1.18 1.19 -1.0

Dec 12 ▼ 1.37 1.39 -1.5

Giordano [Buy] 0709.HK 25-Mar Dec 10 ▲ 0.37 0.31 19.2

Dec 11 ▲ 0.37 0.33 13.3

Dec 12 ▲ 0.40 0.35 14.3

Dec 13 0.44

Kasikornbank [Buy] KBAN.BK 25-Mar Dec 13 0.00 nm

PICC [Sell] 2328.HK 25-Mar Dec 10 ▲ 0.47 0.40 17.6

Dec 11 ▲ 0.51 0.48 7.8

Dec 12 ▲ 0.57 0.56 1.3

POSCO [Buy] 005490.KS 25-Mar Dec 10 ▼ 50,153.54 51,994.29 -3.5

Dec 11 ▲ 50,947.52 47,179.08 8.0

Dec 12 ▲ 53,050.68 49,116.46 8.0

Dec 13 57,691.33

PT Bukit Asam [Buy] PTBA.JK 25-Mar Dec 10 ▲ 882.79 854.68 3.3

Dec 11 ▼ 1,561.65 1,575.80 -0.9

Dec 12 ▼ 2,457.18 2,528.06 -2.8

Dec 13 2,629.73

Siam Commercial Bank [Buy] SCB.BK 25-Mar Dec 13 0.00 nm

TMB Bank [Sell] TMB.BK 25-Mar Dec 13 0.00 nm Source: Deutsche Bank

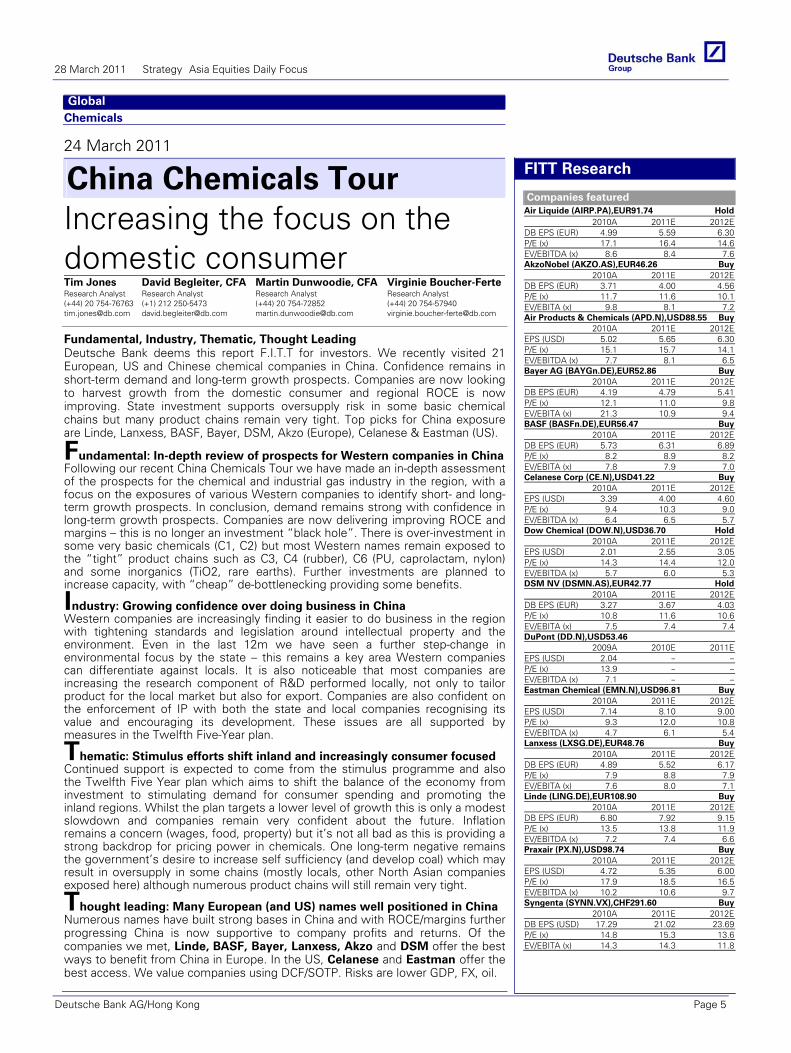

Global Chemicals

24 March 2011

China Chemicals Tour Increasing the focus on the domestic consumerTim Jones Research Analyst (+44) 20 754-76763 [email protected]

David Begleiter, CFA Research Analyst (+1) 212 250-5473 [email protected]

Martin Dunwoodie, CFA Research Analyst (+44) 20 754-72852 [email protected]

Virginie Boucher-FerteResearch Analyst (+44) 20 754-57940 [email protected]

Fundamental, Industry, Thematic, Thought Leading Deutsche Bank deems this report F.I.T.T for investors. We recently visited 21 European, US and Chinese chemical companies in China. Confidence remains in short-term demand and long-term growth prospects. Companies are now looking to harvest growth from the domestic consumer and regional ROCE is now improving. State investment supports oversupply risk in some basic chemical chains but many product chains remain very tight. Top picks for China exposure are Linde, Lanxess, BASF, Bayer, DSM, Akzo (Europe), Celanese & Eastman (US).

FITT Research

Companies featured Air Liquide (AIRP.PA),EUR91.74 Hold

2010A 2011E 2012EDB EPS (EUR) 4.99 5.59 6.30P/E (x) 17.1 16.4 14.6EV/EBITDA (x) 8.6 8.4 7.6AkzoNobel (AKZO.AS),EUR46.26 Buy

2010A 2011E 2012EDB EPS (EUR) 3.71 4.00 4.56P/E (x) 11.7 11.6 10.1EV/EBITA (x) 9.8 8.1 7.2Air Products & Chemicals (APD.N),USD88.55 Buy

2010A 2011E 2012EEPS (USD) 5.02 5.65 6.30P/E (x) 15.1 15.7 14.1EV/EBITDA (x) 7.7 8.1 6.5Bayer AG (BAYGn.DE),EUR52.86 Buy

2010A 2011E 2012EDB EPS (EUR) 4.19 4.79 5.41P/E (x) 12.1 11.0 9.8EV/EBITA (x) 21.3 10.9 9.4BASF (BASFn.DE),EUR56.47 Buy

2010A 2011E 2012EDB EPS (EUR) 5.73 6.31 6.89P/E (x) 8.2 8.9 8.2EV/EBITA (x) 7.8 7.9 7.0Celanese Corp (CE.N),USD41.22 Buy

2010A 2011E 2012EEPS (USD) 3.39 4.00 4.60P/E (x) 9.4 10.3 9.0EV/EBITDA (x) 6.4 6.5 5.7Dow Chemical (DOW.N),USD36.70 Hold

2010A 2011E 2012EEPS (USD) 2.01 2.55 3.05P/E (x) 14.3 14.4 12.0EV/EBITDA (x) 5.7 6.0 5.3DSM NV (DSMN.AS),EUR42.77 Hold

2010A 2011E 2012EDB EPS (EUR) 3.27 3.67 4.03P/E (x) 10.8 11.6 10.6EV/EBITA (x) 7.5 7.4 7.4DuPont (DD.N),USD53.46

2009A 2010E 2011EEPS (USD) 2.04 – –P/E (x) 13.9 – –EV/EBITDA (x) 7.1 – –Eastman Chemical (EMN.N),USD96.81 Buy

2010A 2011E 2012EEPS (USD) 7.14 8.10 9.00P/E (x) 9.3 12.0 10.8EV/EBITDA (x) 4.7 6.1 5.4Lanxess (LXSG.DE),EUR48.76 Buy

2010A 2011E 2012EDB EPS (EUR) 4.89 5.52 6.17P/E (x) 7.9 8.8 7.9EV/EBITA (x) 7.6 8.0 7.1Linde (LING.DE),EUR108.90 Buy

2010A 2011E 2012EDB EPS (EUR) 6.80 7.92 9.15P/E (x) 13.5 13.8 11.9EV/EBITDA (x) 7.2 7.4 6.6Praxair (PX.N),USD98.74 Buy

2010A 2011E 2012EEPS (USD) 4.72 5.35 6.00P/E (x) 17.9 18.5 16.5EV/EBITDA (x) 10.2 10.6 9.7Syngenta (SYNN.VX),CHF291.60 Buy

2010A 2011E 2012EDB EPS (USD) 17.29 21.02 23.69P/E (x) 14.8 15.3 13.6EV/EBITA (x) 14.3 14.3 11.8

Fundamental: In-depth review of prospects for Western companies in China Following our recent China Chemicals Tour we have made an in-depth assessment of the prospects for the chemical and industrial gas industry in the region, with a focus on the exposures of various Western companies to identify short- and long-term growth prospects. In conclusion, demand remains strong with confidence in long-term growth prospects. Companies are now delivering improving ROCE and margins – this is no longer an investment “black hole”. There is over-investment in some very basic chemicals (C1, C2) but most Western names remain exposed to the “tight” product chains such as C3, C4 (rubber), C6 (PU, caprolactam, nylon) and some inorganics (TiO2, rare earths). Further investments are planned to increase capacity, with “cheap” de-bottlenecking providing some benefits.

Industry: Growing confidence over doing business in China Western companies are increasingly finding it easier to do business in the region with tightening standards and legislation around intellectual property and the environment. Even in the last 12m we have seen a further step-change in environmental focus by the state – this remains a key area Western companies can differentiate against locals. It is also noticeable that most companies are increasing the research component of R&D performed locally, not only to tailor product for the local market but also for export. Companies are also confident on the enforcement of IP with both the state and local companies recognising its value and encouraging its development. These issues are all supported by measures in the Twelfth Five-Year plan.

Thematic: Stimulus efforts shift inland and increasingly consumer focused Continued support is expected to come from the stimulus programme and also the Twelfth Five Year plan which aims to shift the balance of the economy from investment to stimulating demand for consumer spending and promoting the inland regions. Whilst the plan targets a lower level of growth this is only a modest slowdown and companies remain very confident about the future. Inflation remains a concern (wages, food, property) but it’s not all bad as this is providing a strong backdrop for pricing power in chemicals. One long-term negative remains the government’s desire to increase self sufficiency (and develop coal) which may result in oversupply in some chains (mostly locals, other North Asian companies exposed here) although numerous product chains will still remain very tight.

Thought leading: Many European (and US) names well positioned in China Numerous names have built strong bases in China and with ROCE/margins further progressing China is now supportive to company profits and returns. Of the companies we met, Linde, BASF, Bayer, Lanxess, Akzo and DSM offer the best ways to benefit from China in Europe. In the US, Celanese and Eastman offer the best access. We value companies using DCF/SOTP. Risks are lower GDP, FX, oil.

28 March 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 5

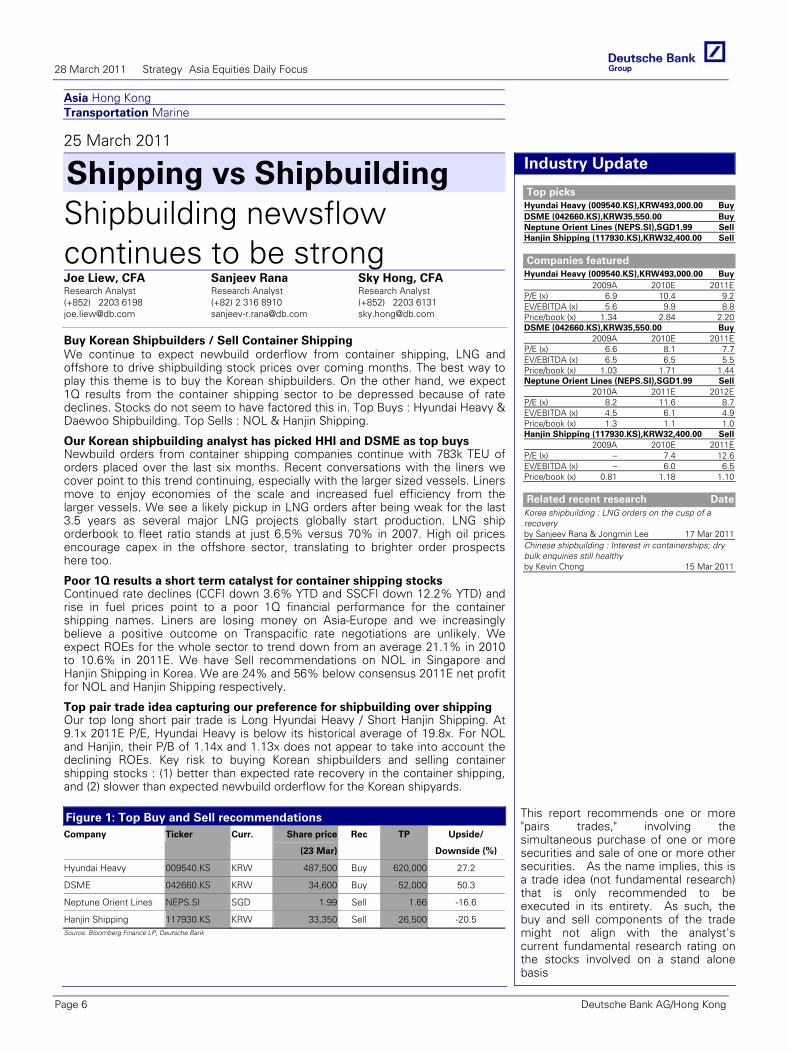

Asia Hong Kong Transportation Marine

25 March 2011

Shipping vs Shipbuilding Shipbuilding newsflow continues to be strongJoe Liew, CFA Research Analyst (+852) 2203 6198 [email protected]

Sanjeev Rana Research Analyst (+82) 2 316 8910 [email protected]

Sky Hong, CFA Research Analyst (+852) 2203 6131 [email protected]

Buy Korean Shipbuilders / Sell Container Shipping We continue to expect newbuild orderflow from container shipping, LNG and offshore to drive shipbuilding stock prices over coming months. The best way to play this theme is to buy the Korean shipbuilders. On the other hand, we expect 1Q results from the container shipping sector to be depressed because of rate declines. Stocks do not seem to have factored this in. Top Buys : Hyundai Heavy & Daewoo Shipbuilding. Top Sells : NOL & Hanjin Shipping.

Industry Update

Top picks Hyundai Heavy (009540.KS),KRW493,000.00 Buy DSME (042660.KS),KRW35,550.00 Buy Neptune Orient Lines (NEPS.SI),SGD1.99 Sell Hanjin Shipping (117930.KS),KRW32,400.00 Sell

Companies featured

Hyundai Heavy (009540.KS),KRW493,000.00 Buy 2009A 2010E 2011E

P/E (x) 6.9 10.4 9.2EV/EBITDA (x) 5.6 9.9 8.8Price/book (x) 1.34 2.84 2.20DSME (042660.KS),KRW35,550.00 Buy

2009A 2010E 2011EP/E (x) 6.6 8.1 7.7EV/EBITDA (x) 6.5 6.5 5.5Price/book (x) 1.03 1.71 1.44Neptune Orient Lines (NEPS.SI),SGD1.99 Sell

2010A 2011E 2012EP/E (x) 8.2 11.6 8.7EV/EBITDA (x) 4.5 6.1 4.9Price/book (x) 1.3 1.1 1.0Hanjin Shipping (117930.KS),KRW32,400.00 Sell

2009A 2010E 2011EP/E (x) – 7.4 12.6EV/EBITDA (x) – 6.0 6.5Price/book (x) 0.81 1.18 1.10

Related recent research Date

Korea shipbuilding : LNG orders on the cusp of a recovery by Sanjeev Rana & Jongmin Lee 17 Mar 2011Chinese shipbuilding : Interest in containerships; dry bulk enquiries still healthy by Kevin Chong 15 Mar 2011

This report recommends one or more "pairs trades," involving the simultaneous purchase of one or more securities and sale of one or more other securities. As the name implies, this is a trade idea (not fundamental research) that is only recommended to be executed in its entirety. As such, the buy and sell components of the trade might not align with the analyst's current fundamental research rating on the stocks involved on a stand alone basis

Our Korean shipbuilding analyst has picked HHI and DSME as top buys Newbuild orders from container shipping companies continue with 783k TEU of orders placed over the last six months. Recent conversations with the liners we cover point to this trend continuing, especially with the larger sized vessels. Liners move to enjoy economies of the scale and increased fuel efficiency from the larger vessels. We see a likely pickup in LNG orders after being weak for the last 3.5 years as several major LNG projects globally start production. LNG ship orderbook to fleet ratio stands at just 6.5% versus 70% in 2007. High oil prices encourage capex in the offshore sector, translating to brighter order prospects here too.

Poor 1Q results a short term catalyst for container shipping stocks Continued rate declines (CCFI down 3.6% YTD and SSCFI down 12.2% YTD) and rise in fuel prices point to a poor 1Q financial performance for the container shipping names. Liners are losing money on Asia-Europe and we increasingly believe a positive outcome on Transpacific rate negotiations are unlikely. We expect ROEs for the whole sector to trend down from an average 21.1% in 2010 to 10.6% in 2011E. We have Sell recommendations on NOL in Singapore and Hanjin Shipping in Korea. We are 24% and 56% below consensus 2011E net profit for NOL and Hanjin Shipping respectively.

Top pair trade idea capturing our preference for shipbuilding over shipping Our top long short pair trade is Long Hyundai Heavy / Short Hanjin Shipping. At 9.1x 2011E P/E, Hyundai Heavy is below its historical average of 19.8x. For NOL and Hanjin, their P/B of 1.14x and 1.13x does not appear to take into account the declining ROEs. Key risk to buying Korean shipbuilders and selling container shipping stocks : (1) better than expected rate recovery in the container shipping, and (2) slower than expected newbuild orderflow for the Korean shipyards. Figure 1: Top Buy and Sell recommendations Company Ticker Curr. Share price

(23 Mar)

Rec TP Upside/

Downside (%)

Hyundai Heavy 009540.KS KRW 487,500 Buy 620,000 27.2

DSME 042660.KS KRW 34,600 Buy 52,000 50.3

Neptune Orient Lines NEPS.SI SGD 1.99 Sell 1.66 -16.6

Hanjin Shipping 117930.KS KRW 33,350 Sell 26,500 -20.5 Source: Bloomberg Finance LP, Deutsche Bank

28 March 2011 Strategy Asia Equities Daily Focus

Page 6 Deutsche Bank AG/Hong Kong

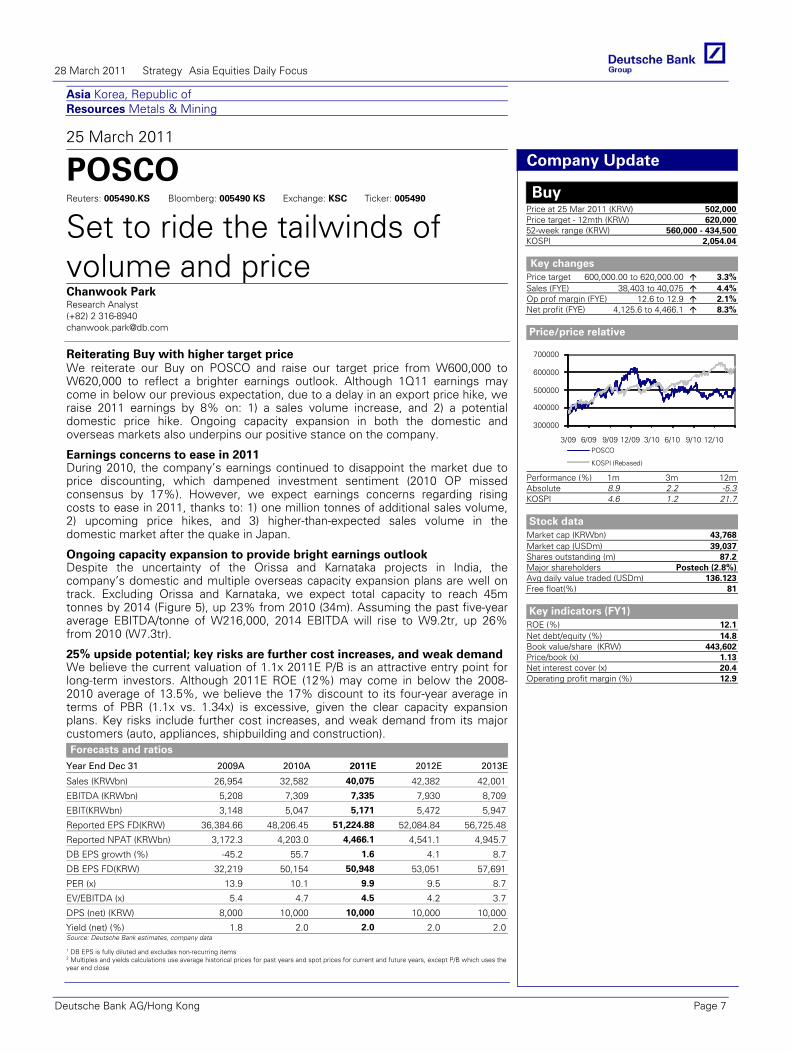

Asia Korea, Republic of Resources Metals & Mining

25 March 2011

POSCO Reuters: 005490.KS Bloomberg: 005490 KS Exchange: KSC Ticker: 005490

Set to ride the tailwinds of volume and price Chanwook Park Research Analyst (+82) 2 316-8940 [email protected]

Reiterating Buy with higher target price We reiterate our Buy on POSCO and raise our target price from W600,000 to W620,000 to reflect a brighter earnings outlook. Although 1Q11 earnings may come in below our previous expectation, due to a delay in an export price hike, we raise 2011 earnings by 8% on: 1) a sales volume increase, and 2) a potential domestic price hike. Ongoing capacity expansion in both the domestic and overseas markets also underpins our positive stance on the company.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Sales (KRWbn) 26,954 32,582 40,075 42,382 42,001

EBITDA (KRWbn) 5,208 7,309 7,335 7,930 8,709

EBIT(KRWbn) 3,148 5,047 5,171 5,472 5,947

Reported EPS FD(KRW) 36,384.66 48,206.45 51,224.88 52,084.84 56,725.48

Reported NPAT (KRWbn) 3,172.3 4,203.0 4,466.1 4,541.1 4,945.7

DB EPS growth (%) -45.2 55.7 1.6 4.1 8.7

DB EPS FD(KRW) 32,219 50,154 50,948 53,051 57,691

PER (x) 13.9 10.1 9.9 9.5 8.7

EV/EBITDA (x) 5.4 4.7 4.5 4.2 3.7

DPS (net) (KRW) 8,000 10,000 10,000 10,000 10,000

Yield (net) (%) 1.8 2.0 2.0 2.0 2.0Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Company Update

Buy Price at 25 Mar 2011 (KRW) 502,000Price target - 12mth (KRW) 620,00052-week range (KRW) 560,000 - 434,500KOSPI 2,054.04

Key changes

Price target 600,000.00 to 620,000.00 3.3%Sales (FYE) 38,403 to 40,075 4.4%Op prof margin (FYE) 12.6 to 12.9 2.1%Net profit (FYE) 4,125.6 to 4,466.1 8.3%

Price/price relative

300000

400000

500000

600000

700000

3/09 6/09 9/09 12/09 3/10 6/10 9/10 12/10POSCO

KOSPI (Rebased)

Performance (%) 1m 3m 12mAbsolute 8.9 2.2 -5.3KOSPI 4.6 1.2 21.7

Stock data

Market cap (KRWbn) 43,768Market cap (USDm) 39,037Shares outstanding (m) 87.2Major shareholders Postech (2.8%)Avg daily value traded (USDm) 136.123Free float(%) 81

Key indicators (FY1)

ROE (%) 12.1Net debt/equity (%) 14.8Book value/share (KRW) 443,602Price/book (x) 1.13Net interest cover (x) 20.4Operating profit margin (%) 12.9

Earnings concerns to ease in 2011 During 2010, the company’s earnings continued to disappoint the market due to price discounting, which dampened investment sentiment (2010 OP missed consensus by 17%). However, we expect earnings concerns regarding rising costs to ease in 2011, thanks to: 1) one million tonnes of additional sales volume, 2) upcoming price hikes, and 3) higher-than-expected sales volume in the domestic market after the quake in Japan.

Ongoing capacity expansion to provide bright earnings outlook Despite the uncertainty of the Orissa and Karnataka projects in India, the company’s domestic and multiple overseas capacity expansion plans are well on track. Excluding Orissa and Karnataka, we expect total capacity to reach 45m tonnes by 2014 (Figure 5), up 23% from 2010 (34m). Assuming the past five-year average EBITDA/tonne of W216,000, 2014 EBITDA will rise to W9.2tr, up 26% from 2010 (W7.3tr).

25% upside potential; key risks are further cost increases, and weak demand We believe the current valuation of 1.1x 2011E P/B is an attractive entry point for long-term investors. Although 2011E ROE (12%) may come in below the 2008-2010 average of 13.5%, we believe the 17% discount to its four-year average in terms of PBR (1.1x vs. 1.34x) is excessive, given the clear capacity expansion plans. Key risks include further cost increases, and weak demand from its major customers (auto, appliances, shipbuilding and construction).

28 March 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 7

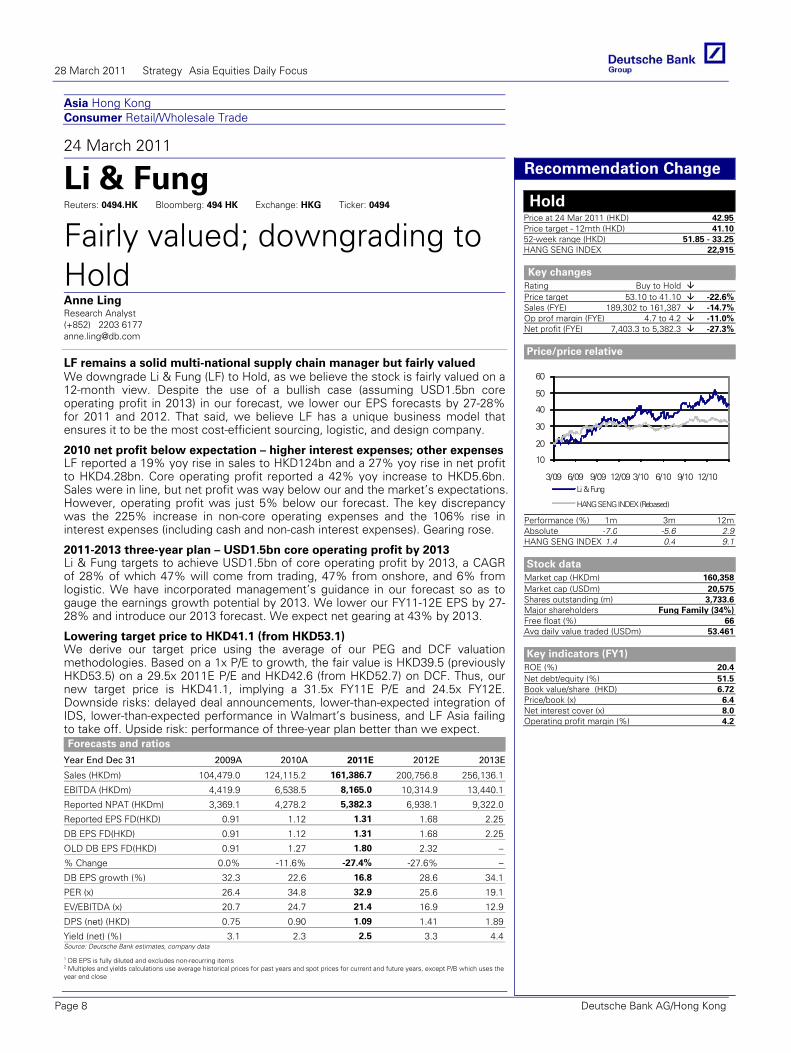

Asia Hong Kong Consumer Retail/Wholesale Trade

24 March 2011

Li & Fung Reuters: 0494.HK Bloomberg: 494 HK Exchange: HKG Ticker: 0494

Fairly valued; downgrading to Hold Anne Ling Research Analyst (+852) 2203 6177 [email protected]

LF remains a solid multi-national supply chain manager but fairly valued We downgrade Li & Fung (LF) to Hold, as we believe the stock is fairly valued on a 12-month view. Despite the use of a bullish case (assuming USD1.5bn core operating profit in 2013) in our forecast, we lower our EPS forecasts by 27-28% for 2011 and 2012. That said, we believe LF has a unique business model that ensures it to be the most cost-efficient sourcing, logistic, and design company.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Sales (HKDm) 104,479.0 124,115.2 161,386.7 200,756.8 256,136.1

EBITDA (HKDm) 4,419.9 6,538.5 8,165.0 10,314.9 13,440.1

Reported NPAT (HKDm) 3,369.1 4,278.2 5,382.3 6,938.1 9,322.0

Reported EPS FD(HKD) 0.91 1.12 1.31 1.68 2.25

DB EPS FD(HKD) 0.91 1.12 1.31 1.68 2.25

OLD DB EPS FD(HKD) 0.91 1.27 1.80 2.32 –

% Change 0.0% -11.6% -27.4% -27.6% –

DB EPS growth (%) 32.3 22.6 16.8 28.6 34.1

PER (x) 26.4 34.8 32.9 25.6 19.1

EV/EBITDA (x) 20.7 24.7 21.4 16.9 12.9

DPS (net) (HKD) 0.75 0.90 1.09 1.41 1.89

Yield (net) (%) 3.1 2.3 2.5 3.3 4.4Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Recommendation Change

Hold Price at 24 Mar 2011 (HKD) 42.95Price target - 12mth (HKD) 41.1052-week range (HKD) 51.85 - 33.25HANG SENG INDEX 22,915

Key changes

Rating Buy to Hold Price target 53.10 to 41.10 -22.6%Sales (FYE) 189,302 to 161,387 -14.7%Op prof margin (FYE) 4.7 to 4.2 -11.0%Net profit (FYE) 7,403.3 to 5,382.3 -27.3%

Price/price relative

10

20

30

40

50

60

3/09 6/09 9/09 12/09 3/10 6/10 9/10 12/10Li & Fung

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute -7.0 -5.6 2.9HANG SENG INDEX 1.4 0.4 9.1

Stock data

Market cap (HKDm) 160,358Market cap (USDm) 20,575Shares outstanding (m) 3,733.6Major shareholders Fung Family (34%)Free float (%) 66Avg daily value traded (USDm) 53.461

Key indicators (FY1)

ROE (%) 20.4Net debt/equity (%) 51.5Book value/share (HKD) 6.72Price/book (x) 6.4Net interest cover (x) 8.0Operating profit margin (%) 4.2

2010 net profit below expectation – higher interest expenses; other expenses LF reported a 19% yoy rise in sales to HKD124bn and a 27% yoy rise in net profit to HKD4.28bn. Core operating profit reported a 42% yoy increase to HKD5.6bn. Sales were in line, but net profit was way below our and the market’s expectations. However, operating profit was just 5% below our forecast. The key discrepancy was the 225% increase in non-core operating expenses and the 106% rise in interest expenses (including cash and non-cash interest expenses). Gearing rose.

2011-2013 three-year plan – USD1.5bn core operating profit by 2013 Li & Fung targets to achieve USD1.5bn of core operating profit by 2013, a CAGR of 28% of which 47% will come from trading, 47% from onshore, and 6% from logistic. We have incorporated management’s guidance in our forecast so as to gauge the earnings growth potential by 2013. We lower our FY11-12E EPS by 27-28% and introduce our 2013 forecast. We expect net gearing at 43% by 2013.

Lowering target price to HKD41.1 (from HKD53.1) We derive our target price using the average of our PEG and DCF valuation methodologies. Based on a 1x P/E to growth, the fair value is HKD39.5 (previously HKD53.5) on a 29.5x 2011E P/E and HKD42.6 (from HKD52.7) on DCF. Thus, our new target price is HKD41.1, implying a 31.5x FY11E P/E and 24.5x FY12E. Downside risks: delayed deal announcements, lower-than-expected integration of IDS, lower-than-expected performance in Walmart’s business, and LF Asia failing to take off. Upside risk: performance of three-year plan better than we expect.

28 March 2011 Strategy Asia Equities Daily Focus

Page 8 Deutsche Bank AG/Hong Kong

Asia China Consumer Retail/Wholesale Trade

25 March 2011

CRE Reuters: 0291.HK Bloomberg: 291 HK Exchange: HSI Ticker: 0291

Bigger and more profitable; maintaining Buy Rebecca Jiang, CFA Research Analyst (+852) 2203 6152 [email protected]

Anne Ling Research Analyst (+852) 2203 6177 [email protected]

Mabel Wong, CFA Research Analyst (+852) 2203 6178 [email protected]

Maintaining Buy with SOTP target price of HK$35.5 We believe CRE can balance sales expansion with profitability improvement and management’s near-term priority on gaining market share can translate into better future earnings. We believe the operating environment remains favorable for the supermarket business and raw material cost inflation is unlikely to hurt beer margins in FY11. We fine-tune our forecasts and target price and maintain Buy.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Sales (HKDm) 64,131.0 86,728.0 108,176.9 129,025.6 150,575.0

EBITDA (HKDm) 5,084.0 5,934.0 8,766.1 10,699.8 12,630.8

Reported NPAT (HKDm) 2,913.0 5,674.0 2,621.8 3,442.4 4,230.0

Reported EPS FD(HKD) 1.21 2.36 1.09 1.43 1.77

DB EPS FD(HKD) 0.58 0.80 1.09 1.43 1.77

OLD DB EPS FD(HKD) 0.58 0.81 1.11 1.43 –

% Change 0.0% -2.0% -1.7% 0.4% –

DB EPS growth (%) 36.8 38.4 36.8 31.4 23.7

PER (x) 31.6 37.5 26.9 20.5 16.6

EV/EBITDA (x) 9.3 11.7 7.5 6.0 5.0

DPS (net) (HKD) 0.49 0.52 0.44 0.58 0.71

Yield (net) (%) 2.7 1.7 1.5 2.0 2.4Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Forecast Change

Buy Price at 24 Mar 2011 (HKD) 29.35Price target - 12mth (HKD) 35.5052-week range (HKD) 35.15 - 24.70HANG SENG INDEX 22,915

Key changes

Price target 35.52 to 35.50 -0.1%Sales (FYE) 103,195 to 108,177 4.8%Op prof margin (FYE) 5.0 to 4.9 -2.2%Net profit (FYE) 2,667.7 to 2,621.8 -1.7%

Price/price relative

812162024283236

3/09 6/09 9/09 12/09 3/10 6/10 9/10 12/10CRE

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute 7.1 -7.3 6.9HANG SENG INDEX 1.4 0.4 9.1

Stock data

Market cap (HKDm) 70,353Market cap (USDm) 9,027Shares outstanding (m) 2,397.0Major shareholders China Resources Hldg (51.46%)Free float (%) 48Avg daily value traded (USDm) 13.506

Key indicators (FY1)

ROE (%) 8.3Net debt/equity (%) -9.8Book value/share (HKD) 13.56Price/book (x) 2.2Net interest cover (x) –Operating profit margin (%) 4.9

FY10 results broadly in line; 4Q10 weakness on temporary SSSg moderation CRE reported FY10 net profit of RMB5.7bn and core underlying net profit of RMB1.89bn (3% lower than our RMB1.95bn estimate). CRE saw a slowdown in 4Q10 SSSg to 6-7% (from c.10% in 3Q10) and recorded a RMB40m loss from Home World, which are the key reasons for the 4Q10 earnings miss. However, we believe the SSSg moderation is temporary and in line with the trends seen by most food retailers due to a higher base in 4Q09. The company has already seen a SSSg rebound in 1Q11, which we believe will last for 1H11 amid higher CPI.

Encouraging margin trend We believe CRE is on track with margin improvement in its retail business, with China supermarket NPM improving to 0.9-1% in FY10 from 0.5% in FY09 despite accelerated network expansion and losses from new markets. We expect such trends to continue, supported by better margins in its home base. Management is also comfortable with maintaining the GPM for its beer business in FY11 and we continue to expect CRE to make value-accretive beer acquisitions.

SOTP-based target price of HK$35.5; maintaining Buy We derive our target price from a sum-of-the-parts valuation. We value the four key businesses as follows: 1) retail – 29x 12-month forward PE, or 1x PEG, 2) beer – 13x 12-month forward EV/EBITDA, 3) beverage – 9x 12-month forward FY11E EV/EBITDA, and 3) food – 18x 12-month forward PE. Key risks are start-up losses in new markets and rising raw material/operating costs.

28 March 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 9

Asia ChinaUtilities Utilities

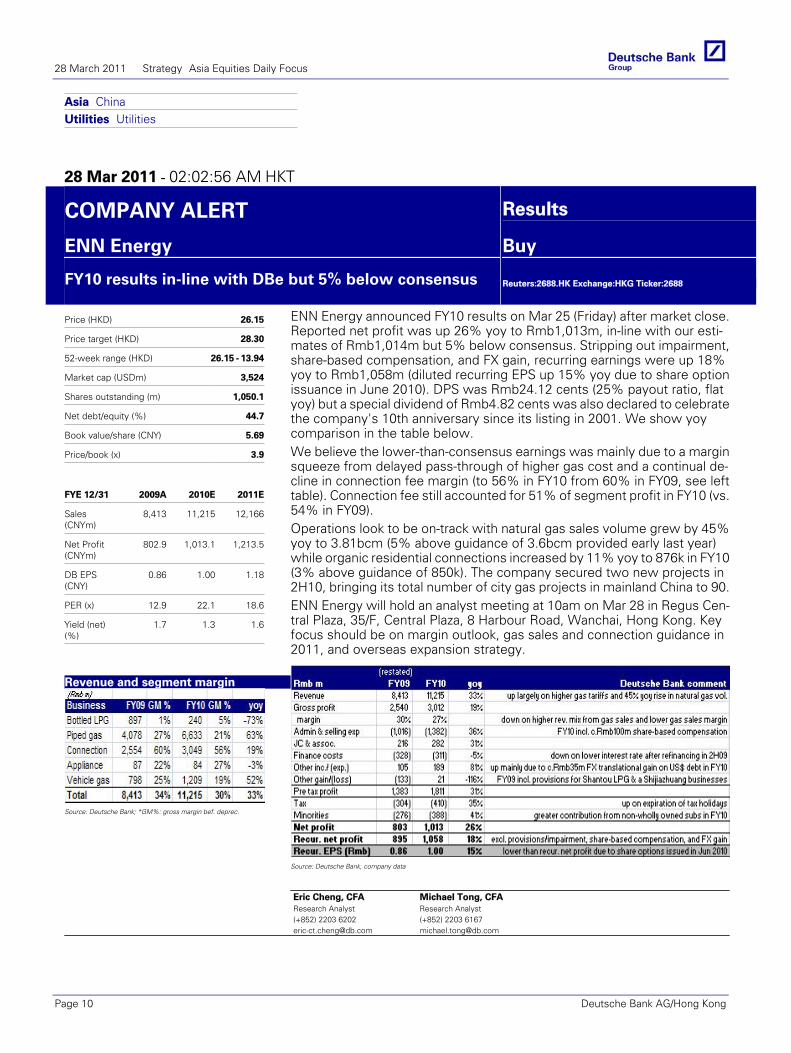

28 Mar 2011 - 02:02:56 AM HKT

COMPANY ALERT Results

ENN Energy Buy

FY10 results in-line with DBe but 5% below consensus

Reuters:2688.HK Exchange:HKG Ticker:2688

Price (HKD) 26.15

Price target (HKD) 28.30

52-week range (HKD) 26.15 - 13.94

Market cap (USDm) 3,524

Shares outstanding (m) 1,050.1

Net debt/equity (%) 44.7

Book value/share (CNY) 5.69

Price/book (x) 3.9

FYE 12/31 2009A 2010E 2011E

Sales(CNYm)

8,413 11,215 12,166

Net Profit(CNYm)

802.9 1,013.1 1,213.5

DB EPS(CNY)

0.86 1.00 1.18

PER (x) 12.9 22.1 18.6

Yield (net)(%)

1.7 1.3 1.6

Revenue and segment margin

Source: Deutsche Bank; *GM%: gross margin bef. deprec.

ENN Energy announced FY10 results on Mar 25 (Friday) after market close.Reported net profit was up 26% yoy to Rmb1,013m, in-line with our esti-mates of Rmb1,014m but 5% below consensus. Stripping out impairment,share-based compensation, and FX gain, recurring earnings were up 18%yoy to Rmb1,058m (diluted recurring EPS up 15% yoy due to share optionissuance in June 2010). DPS was Rmb24.12 cents (25% payout ratio, flatyoy) but a special dividend of Rmb4.82 cents was also declared to celebratethe company's 10th anniversary since its listing in 2001. We show yoycomparison in the table below.We believe the lower-than-consensus earnings was mainly due to a marginsqueeze from delayed pass-through of higher gas cost and a continual de-cline in connection fee margin (to 56% in FY10 from 60% in FY09, see lefttable). Connection fee still accounted for 51% of segment profit in FY10 (vs.54% in FY09).Operations look to be on-track with natural gas sales volume grew by 45%yoy to 3.81bcm (5% above guidance of 3.6bcm provided early last year)while organic residential connections increased by 11% yoy to 876k in FY10(3% above guidance of 850k). The company secured two new projects in2H10, bringing its total number of city gas projects in mainland China to 90.ENN Energy will hold an analyst meeting at 10am on Mar 28 in Regus Cen-tral Plaza, 35/F, Central Plaza, 8 Harbour Road, Wanchai, Hong Kong. Keyfocus should be on margin outlook, gas sales and connection guidance in2011, and overseas expansion strategy.

Source: Deutsche Bank, company data

Eric Cheng, CFAResearch Analyst(+852) 2203 [email protected]

Michael Tong, CFAResearch Analyst(+852) 2203 [email protected]

28 March 2011 Strategy Asia Equities Daily Focus

Page 10 Deutsche Bank AG/Hong Kong

Asia Hong Kong Consumer Retail/Wholesale Trade

24 March 2011

Giordano Reuters: 0709.HK Bloomberg: 709 HK Exchange: HKG Ticker: 0709

2011 outlook; maintaining Buy

Anne Ling Research Analyst (+852) 2203 6177 [email protected]

Raising FY11-13 PE by 12-13%; introducing 2013 forecast We reiterate Buy on Giordano because we believe 1) the improvement in its operating performance and operating efficiencies achieved in 2011 are likely to continue; 2) successful product launches charge a higher ASP and GPM; and 3) there has been a resumption in store growth in China since 2H09. The Hong Kong operating environment is a concern to us. However, the stock is trading at an inexpensive PE multiple. We are raising our target price to HK$5.77 at 14.8x rolling Jul11-Jun12 forward PE.

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E 2013E

Sales (HKDm) 4,233.0 4,731.0 5,089.7 5,502.6 5,947.2

EBITDA (HKDm) 422.0 784.0 815.7 886.2 963.8

Reported NPAT (HKDm) 288.0 537.0 563.7 616.9 677.0

Reported EPS FD(HKD) 0.19 0.36 0.37 0.40 0.44

DB EPS FD(HKD) 0.19 0.37 0.37 0.40 0.44

OLD DB EPS FD(HKD) 0.19 0.31 0.33 0.35 –

% Change 0.0% 19.2% 13.3% 14.3% –

DB EPS growth (%) 6.7 91.0 1.1 8.3 9.7

PER (x) 10.1 10.0 12.3 11.3 10.3

EV/EBITDA (x) 5.1 5.7 6.9 6.2 5.0

DPS (net) (HKD) 0.16 0.27 0.28 0.31 0.00

Yield (net) (%) 8.3 7.4 6.2 6.8 0.0Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Forecast Change

Buy Price at 25 Mar 2011 (HKD) 4.58Price target - 12mth (HKD) 5.7752-week range (HKD) 4.97 - 2.81HANG SENG INDEX 22,915

Key changes

Price target 5.35 to 5.77 7.9%Sales (FYE) 4,856 to 5,090 4.8%Op prof margin (FYE) 13.1 to 13.8 5.3%Net profit (FYE) 503.0 to 563.7 12.1%

Price/price relative

1.0

2.0

3.0

4.0

5.0

6.0

3/09 6/09 9/09 12/09 3/10 6/10 9/10 12/10Giordano

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute 9.3 5.5 84.7HANG SENG INDEX -0.4 0.4 10.3

Stock data

Market cap (HKDm) 6,828Market cap (USDm) 876Shares outstanding (m) 1,490.8Major shareholders Management (1%)Free float (%) 98Avg daily value traded (USDm) 1.410

Key indicators (FY1)

ROE (%) 25.9Net debt/equity (%) -51.9Book value/share (HKD) 1.53Price/book (x) 3.0Net interest cover (x) –Operating profit margin (%) 13.8

2010 results beat expectation due to gross margin expansion Giordano reported a sales increase of 11.8% yoy to HKD4.7bn and net profit rose 86.5% yoy to HKD537m. Sales growth was in line with our expectations, while net profit was much better than our forecast of 15% growth. Same-store sales in 2H10 were up 6.4% vs. 4.5% in 1H10. During the period, the company added 183 stores for the group markets, of which 171 are in China.

More stores in China, the growth market; we are more cautious on HK It targets to open 300 outlets in China in 2011. The majority of the new stores will be via franchisees, and based in tier 2-3 cities. Overall, management expects GPM to improve, more than offsetting an operating cost increase. However, we are more conservative in our model, and expect EBIT to decline to 13.8% in 2011 from 14.5% in 2010, mainly due to concern over the Hong Kong operations, with consumers’ disposable income affected by high CPI and rental cost increases.

Valuation – raising target price from HK$5.34 to HK$5.77; risks As the company has gone through a recovery year and will likely see more stable growth, we use the five-year average P/E to set our target price. This translates to a target price of HK$5.77, based on 14.8x rolling Jul11-Jun12 P/E (from HK$5.35 on a 16x FY11E P/E). Risks: 1) the recoveries in Singapore and Taiwan prove to be unsustainable and 2) the China market does not recover. (More details on page 3.)

28 March 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 11

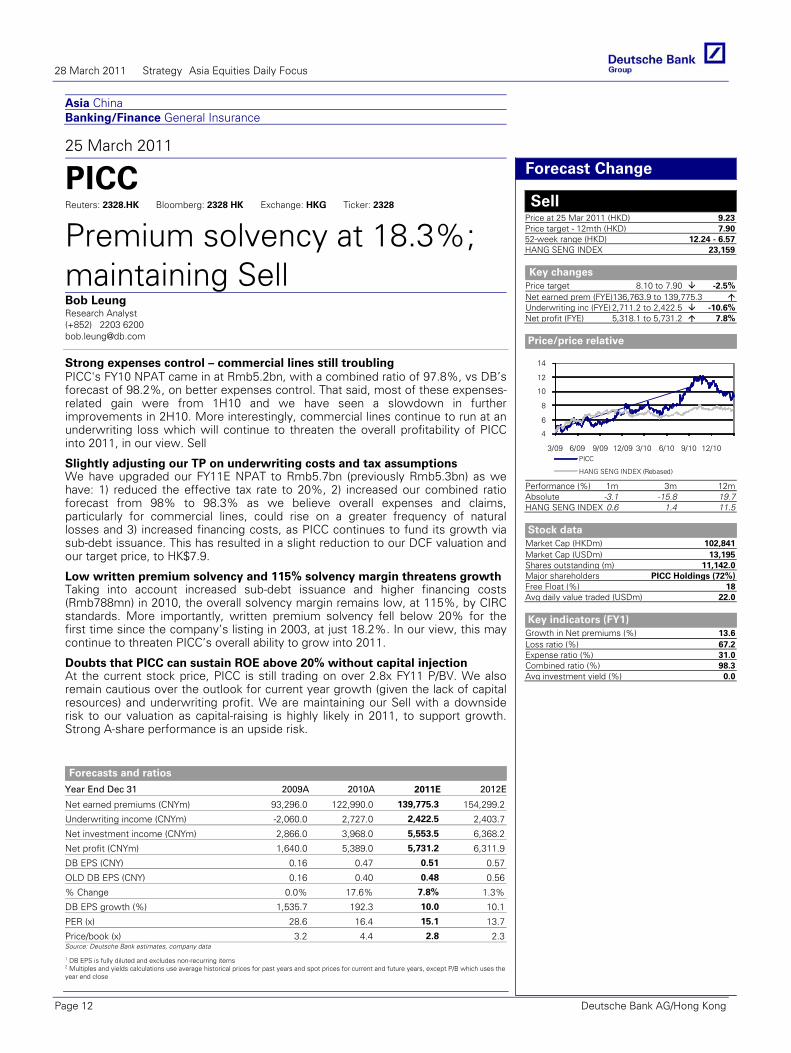

Asia China Banking/Finance General Insurance

25 March 2011

PICC Reuters: 2328.HK Bloomberg: 2328 HK Exchange: HKG Ticker: 2328

Premium solvency at 18.3%; maintaining Sell Bob Leung Research Analyst (+852) 2203 6200 [email protected]

Strong expenses control – commercial lines still troubling PICC's FY10 NPAT came in at Rmb5.2bn, with a combined ratio of 97.8%, vs DB’s forecast of 98.2%, on better expenses control. That said, most of these expenses-related gain were from 1H10 and we have seen a slowdown in further improvements in 2H10. More interestingly, commercial lines continue to run at an underwriting loss which will continue to threaten the overall profitability of PICC into 2011, in our view. Sell

Forecasts and ratios

Year End Dec 31 2009A 2010A 2011E 2012E

Net earned premiums (CNYm) 93,296.0 122,990.0 139,775.3 154,299.2

Underwriting income (CNYm) -2,060.0 2,727.0 2,422.5 2,403.7

Net investment income (CNYm) 2,866.0 3,968.0 5,553.5 6,368.2

Net profit (CNYm) 1,640.0 5,389.0 5,731.2 6,311.9

DB EPS (CNY) 0.16 0.47 0.51 0.57

OLD DB EPS (CNY) 0.16 0.40 0.48 0.56

% Change 0.0% 17.6% 7.8% 1.3%

DB EPS growth (%) 1,535.7 192.3 10.0 10.1

PER (x) 28.6 16.4 15.1 13.7

Price/book (x) 3.2 4.4 2.8 2.3Source: Deutsche Bank estimates, company data

1 DB EPS is fully diluted and excludes non-recurring items 2 Multiples and yields calculations use average historical prices for past years and spot prices for current and future years, except P/B which uses the year end close

Forecast Change

Sell Price at 25 Mar 2011 (HKD) 9.23Price target - 12mth (HKD) 7.9052-week range (HKD) 12.24 - 6.57HANG SENG INDEX 23,159

Key changes

Price target 8.10 to 7.90 -2.5%Net earned prem (FYE)136,763.9 to 139,775.3Underwriting inc (FYE) 2,711.2 to 2,422.5 -10.6%Net profit (FYE) 5,318.1 to 5,731.2 7.8%

Price/price relative

4

6

8

10

12

14

3/09 6/09 9/09 12/09 3/10 6/10 9/10 12/10PICC

HANG SENG INDEX (Rebased)

Performance (%) 1m 3m 12mAbsolute -3.1 -15.8 19.7HANG SENG INDEX 0.6 1.4 11.5

Stock data

Market Cap (HKDm) 102,841Market Cap (USDm) 13,195Shares outstanding (m) 11,142.0Major shareholders PICC Holdings (72%)Free Float (%) 18Avg daily value traded (USDm) 22.0

Key indicators (FY1)

Growth in Net premiums (%) 13.6Loss ratio (%) 67.2Expense ratio (%) 31.0Combined ratio (%) 98.3Avg investment yield (%) 0.0

Slightly adjusting our TP on underwriting costs and tax assumptions We have upgraded our FY11E NPAT to Rmb5.7bn (previously Rmb5.3bn) as we have: 1) reduced the effective tax rate to 20%, 2) increased our combined ratio forecast from 98% to 98.3% as we believe overall expenses and claims, particularly for commercial lines, could rise on a greater frequency of natural losses and 3) increased financing costs, as PICC continues to fund its growth via sub-debt issuance. This has resulted in a slight reduction to our DCF valuation and our target price, to HK$7.9.

Low written premium solvency and 115% solvency margin threatens growth Taking into account increased sub-debt issuance and higher financing costs (Rmb788mn) in 2010, the overall solvency margin remains low, at 115%, by CIRC standards. More importantly, written premium solvency fell below 20% for the first time since the company’s listing in 2003, at just 18.2%. In our view, this may continue to threaten PICC’s overall ability to grow into 2011.

Doubts that PICC can sustain ROE above 20% without capital injection At the current stock price, PICC is still trading on over 2.8x FY11 P/BV. We also remain cautious over the outlook for current year growth (given the lack of capital resources) and underwriting profit. We are maintaining our Sell with a downside risk to our valuation as capital-raising is highly likely in 2011, to support growth. Strong A-share performance is an upside risk.

28 March 2011 Strategy Asia Equities Daily Focus

Page 12 Deutsche Bank AG/Hong Kong

Asia ASEAN SingaporeTransportation

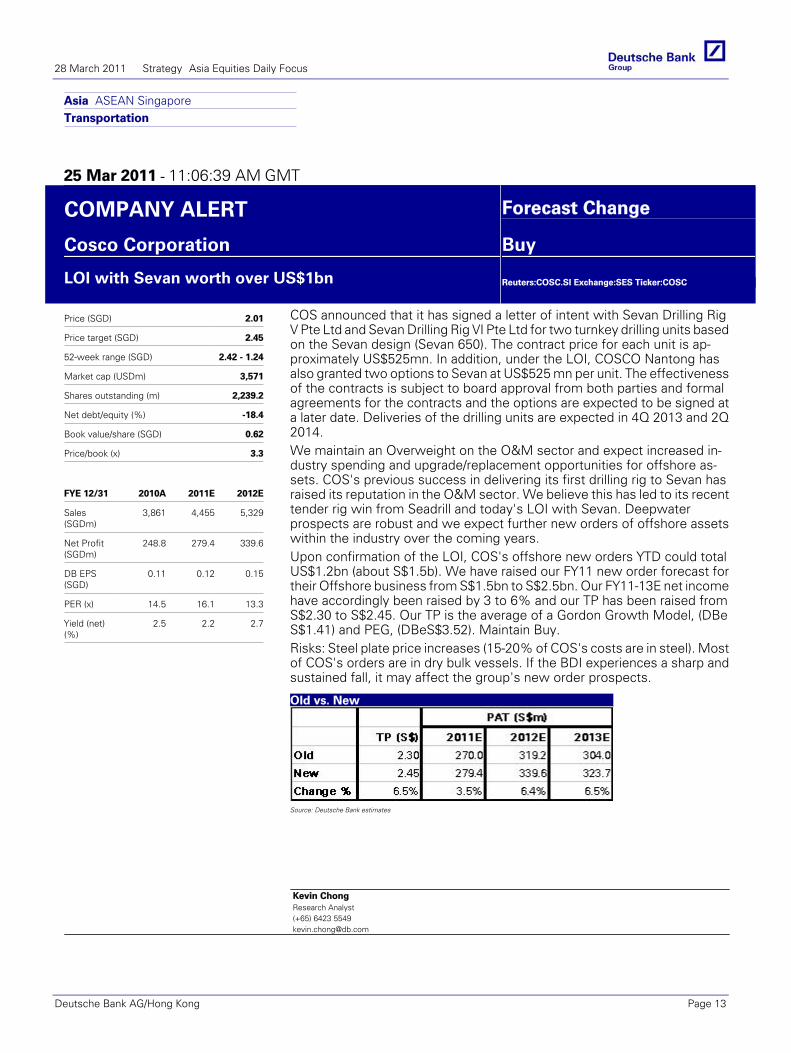

25 Mar 2011 - 11:06:39 AM GMT

COMPANY ALERT Forecast Change

Cosco Corporation Buy

LOI with Sevan worth over US$1bn

Reuters:COSC.SI Exchange:SES Ticker:COSC

Price (SGD) 2.01

Price target (SGD) 2.45

52-week range (SGD) 2.42 - 1.24

Market cap (USDm) 3,571

Shares outstanding (m) 2,239.2

Net debt/equity (%) -18.4

Book value/share (SGD) 0.62

Price/book (x) 3.3

FYE 12/31 2010A 2011E 2012E

Sales(SGDm)

3,861 4,455 5,329

Net Profit(SGDm)

248.8 279.4 339.6

DB EPS(SGD)

0.11 0.12 0.15

PER (x) 14.5 16.1 13.3

Yield (net)(%)

2.5 2.2 2.7

COS announced that it has signed a letter of intent with Sevan Drilling RigV Pte Ltd and Sevan Drilling Rig VI Pte Ltd for two turnkey drilling units basedon the Sevan design (Sevan 650). The contract price for each unit is ap-proximately US$525mn. In addition, under the LOI, COSCO Nantong hasalso granted two options to Sevan at US$525 mn per unit. The effectivenessof the contracts is subject to board approval from both parties and formalagreements for the contracts and the options are expected to be signed ata later date. Deliveries of the drilling units are expected in 4Q 2013 and 2Q2014.We maintain an Overweight on the O&M sector and expect increased in-dustry spending and upgrade/replacement opportunities for offshore as-sets. COS's previous success in delivering its first drilling rig to Sevan hasraised its reputation in the O&M sector. We believe this has led to its recenttender rig win from Seadrill and today's LOI with Sevan. Deepwaterprospects are robust and we expect further new orders of offshore assetswithin the industry over the coming years.Upon confirmation of the LOI, COS's offshore new orders YTD could totalUS$1.2bn (about S$1.5b). We have raised our FY11 new order forecast fortheir Offshore business from S$1.5bn to S$2.5bn. Our FY11-13E net incomehave accordingly been raised by 3 to 6% and our TP has been raised fromS$2.30 to S$2.45. Our TP is the average of a Gordon Growth Model, (DBeS$1.41) and PEG, (DBeS$3.52). Maintain Buy.Risks: Steel plate price increases (15-20% of COS's costs are in steel). Mostof COS's orders are in dry bulk vessels. If the BDI experiences a sharp andsustained fall, it may affect the group's new order prospects.

Old vs. New

Source: Deutsche Bank estimates

Kevin ChongResearch Analyst(+65) 6423 [email protected]

28 March 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 13

Asia ASEAN IndonesiaResources Metals & Mining

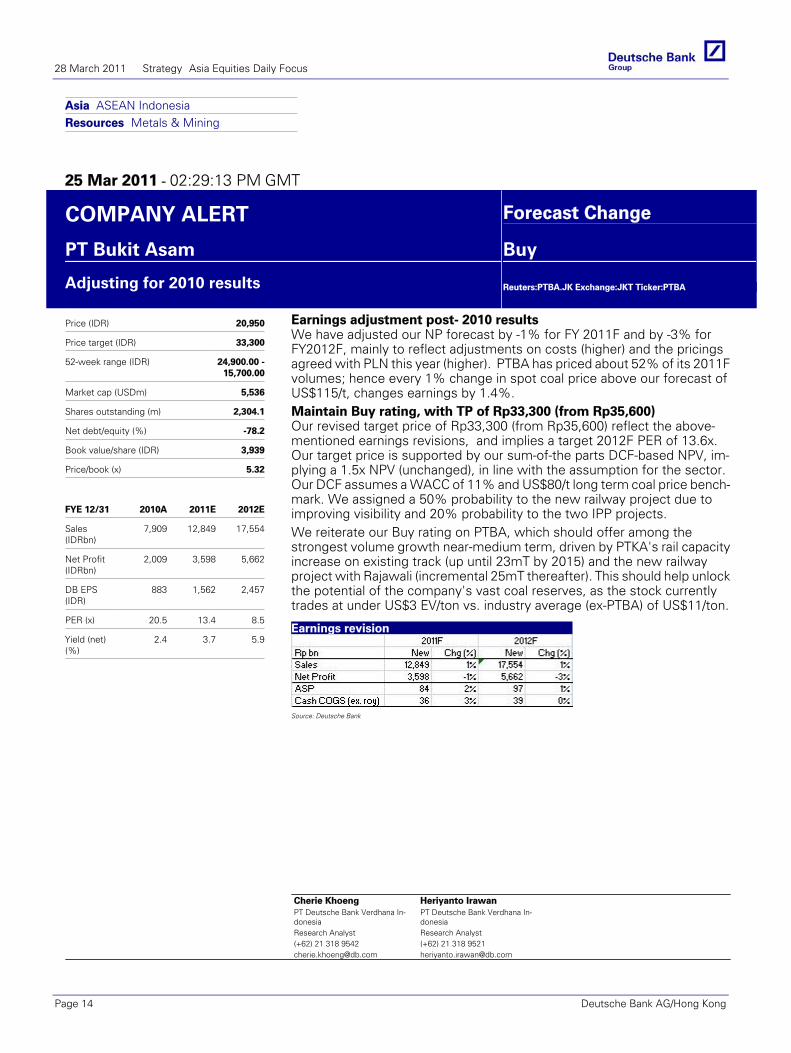

25 Mar 2011 - 02:29:13 PM GMT

COMPANY ALERT Forecast Change

PT Bukit Asam Buy

Adjusting for 2010 results

Reuters:PTBA.JK Exchange:JKT Ticker:PTBA

Price (IDR) 20,950

Price target (IDR) 33,300

52-week range (IDR) 24,900.00 -15,700.00

Market cap (USDm) 5,536

Shares outstanding (m) 2,304.1

Net debt/equity (%) -78.2

Book value/share (IDR) 3,939

Price/book (x) 5.32

FYE 12/31 2010A 2011E 2012E

Sales(IDRbn)

7,909 12,849 17,554

Net Profit(IDRbn)

2,009 3,598 5,662

DB EPS(IDR)

883 1,562 2,457

PER (x) 20.5 13.4 8.5

Yield (net)(%)

2.4 3.7 5.9

Earnings adjustment post- 2010 resultsWe have adjusted our NP forecast by -1% for FY 2011F and by -3% forFY2012F, mainly to reflect adjustments on costs (higher) and the pricingsagreed with PLN this year (higher). PTBA has priced about 52% of its 2011Fvolumes; hence every 1% change in spot coal price above our forecast ofUS$115/t, changes earnings by 1.4%.Maintain Buy rating, with TP of Rp33,300 (from Rp35,600)Our revised target price of Rp33,300 (from Rp35,600) reflect the above-mentioned earnings revisions, and implies a target 2012F PER of 13.6x.Our target price is supported by our sum-of-the parts DCF-based NPV, im-plying a 1.5x NPV (unchanged), in line with the assumption for the sector.Our DCF assumes a WACC of 11% and US$80/t long term coal price bench-mark. We assigned a 50% probability to the new railway project due toimproving visibility and 20% probability to the two IPP projects.We reiterate our Buy rating on PTBA, which should offer among thestrongest volume growth near-medium term, driven by PTKA's rail capacityincrease on existing track (up until 23mT by 2015) and the new railwayproject with Rajawali (incremental 25mT thereafter). This should help unlockthe potential of the company's vast coal reserves, as the stock currentlytrades at under US$3 EV/ton vs. industry average (ex-PTBA) of US$11/ton.

Earnings revision

Source: Deutsche Bank

Cherie KhoengPT Deutsche Bank Verdhana In-donesiaResearch Analyst(+62) 21 318 [email protected]

Heriyanto IrawanPT Deutsche Bank Verdhana In-donesiaResearch Analyst(+62) 21 318 [email protected]

28 March 2011 Strategy Asia Equities Daily Focus

Page 14 Deutsche Bank AG/Hong Kong

Asia

25 March 2011

Asia Economics Daily

Malaysia CPI and Singapore IP

Michael Spencer, Ph.D Chief Economist, Asia (+852) 2203 8303 [email protected]

Jun Ma, Ph.D Chief Economist, Greater China (+852) 2203 8308 [email protected]

Taimur Baig, Ph.D Chief Economist, India (+65) 6423 8681 [email protected]

Juliana Lee Senior Economist (+852) 2203 8312 [email protected]

Kaushik Das Economist (+91) 22 6658 4909 [email protected]

Eco

no

mic

s

HIGHLIGHTS

Malaysia - CPI inflation touches 2.9% in February Singapore – Production activities remain weak in February, below expectations Philippines - Trade deficit widens in January Taiwan -- M2 rises by 6.1%yoy in February

UPCOMING RELEASES

Taiwan- Leading Indicator (Feb) DB forecast 0.2%(0.6% in Jan) Thailand- Manufacturing Production (Feb) DB forecast 1.8%(3.7% in Jan) Vietnam- GDP (Q1’11) DB forecast 6.3%(7.7% in Q4’10) Vietnam- Exports (ytd) (Mar) DB forecast 43.9%(40.3% in Feb) Vietnam- Industrial Production (ytd) (Mar) DB forecast 15.0%(14.6% in Feb) Vietnam- Retail Sales (ytd) (Mar) DB forecast 24.0%(23.5% in Feb) Sri Lanka – GDP (Q4) DB forecast 7.7%(8.0% in Q3)

Sri Lanka’s economy is likely to post a 7.7%yoy real GDP growth in 4Q’10, slightly lower than the 8.0% outturn in 3Q. This should lead to a 2010 full year growth of 7.8%, reversing sharply from the 3.5% growth recorded in 2009. While farm sector is expected to grow by 5.0%yoy in 4Q, non-farm sector growth is likely to moderate to 8.0%, from 8.3% in the previous quarter.

NEWS IN BRIEF

MALAYSIA CPI inflation (Feb). CPI inflation accelerated to 2.9%yoy in February, sharply up from 2.4% in January, beating our (2.5%) as well as consensus (2.7%) expectations. This upward surprise came from food index, inflation of which rose at a faster pace of 4.7% in February, as compared to 3.6% and 2.8% respectively in the last two months. Meanwhile, housing and transport inflation prices rose by 1.5% and 4.5% respectively in February, marginally higher than 1.4% and 4.3% reported in January. We expect inflation to become more volatile in the coming months as food and fuel subsidies are gradually removed.

(Continued on the next page…)

28 March 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 15

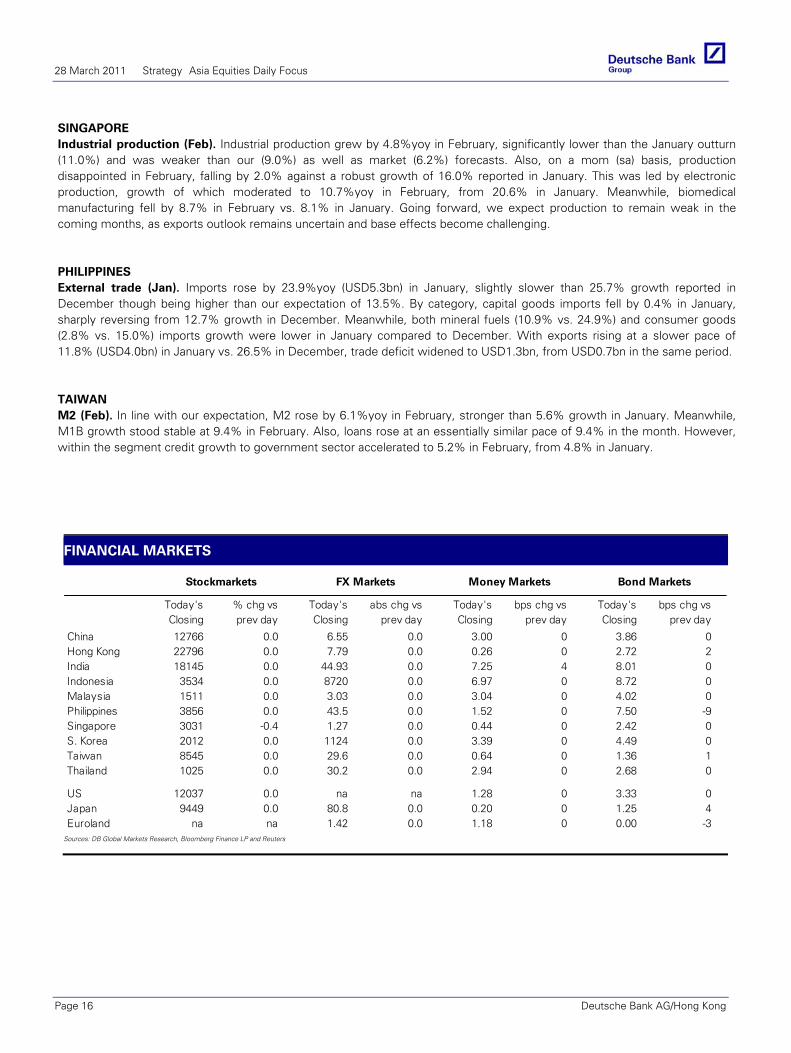

SINGAPORE Industrial production (Feb). Industrial production grew by 4.8%yoy in February, significantly lower than the January outturn (11.0%) and was weaker than our (9.0%) as well as market (6.2%) forecasts. Also, on a mom (sa) basis, production disappointed in February, falling by 2.0% against a robust growth of 16.0% reported in January. This was led by electronic production, growth of which moderated to 10.7%yoy in February, from 20.6% in January. Meanwhile, biomedical manufacturing fell by 8.7% in February vs. 8.1% in January. Going forward, we expect production to remain weak in the coming months, as exports outlook remains uncertain and base effects become challenging.

PHILIPPINES External trade (Jan). Imports rose by 23.9%yoy (USD5.3bn) in January, slightly slower than 25.7% growth reported in December though being higher than our expectation of 13.5%. By category, capital goods imports fell by 0.4% in January, sharply reversing from 12.7% growth in December. Meanwhile, both mineral fuels (10.9% vs. 24.9%) and consumer goods (2.8% vs. 15.0%) imports growth were lower in January compared to December. With exports rising at a slower pace of 11.8% (USD4.0bn) in January vs. 26.5% in December, trade deficit widened to USD1.3bn, from USD0.7bn in the same period.

TAIWAN M2 (Feb). In line with our expectation, M2 rose by 6.1%yoy in February, stronger than 5.6% growth in January. Meanwhile, M1B growth stood stable at 9.4% in February. Also, loans rose at an essentially similar pace of 9.4% in the month. However, within the segment credit growth to government sector accelerated to 5.2% in February, from 4.8% in January.

FINANCIAL MARKETS

Today's % chg vs Today's abs chg vs Today's bps chg vs Today's bps chg vsClosing prev day Closing prev day Closing prev day Closing prev day

China 12766 0.0 6.55 0.0 3.00 0 3.86 0Hong Kong 22796 0.0 7.79 0.0 0.26 0 2.72 2India 18145 0.0 44.93 0.0 7.25 4 8.01 0Indonesia 3534 0.0 8720 0.0 6.97 0 8.72 0Malaysia 1511 0.0 3.03 0.0 3.04 0 4.02 0Philippines 3856 0.0 43.5 0.0 1.52 0 7.50 -9Singapore 3031 -0.4 1.27 0.0 0.44 0 2.42 0S. Korea 2012 0.0 1124 0.0 3.39 0 4.49 0Taiwan 8545 0.0 29.6 0.0 0.64 0 1.36 1Thailand 1025 0.0 30.2 0.0 2.94 0 2.68 0

US 12037 0.0 na na 1.28 0 3.33 0Japan 9449 0.0 80.8 0.0 0.20 0 1.25 4Euroland na na 1.42 0.0 1.18 0 0.00 -3

Stockmarkets FX Markets Money Markets Bond Markets

Sources: DB Global Markets Research, Bloomberg Finance LP and Reuters

28 March 2011 Strategy Asia Equities Daily Focus

Page 16 Deutsche Bank AG/Hong Kong

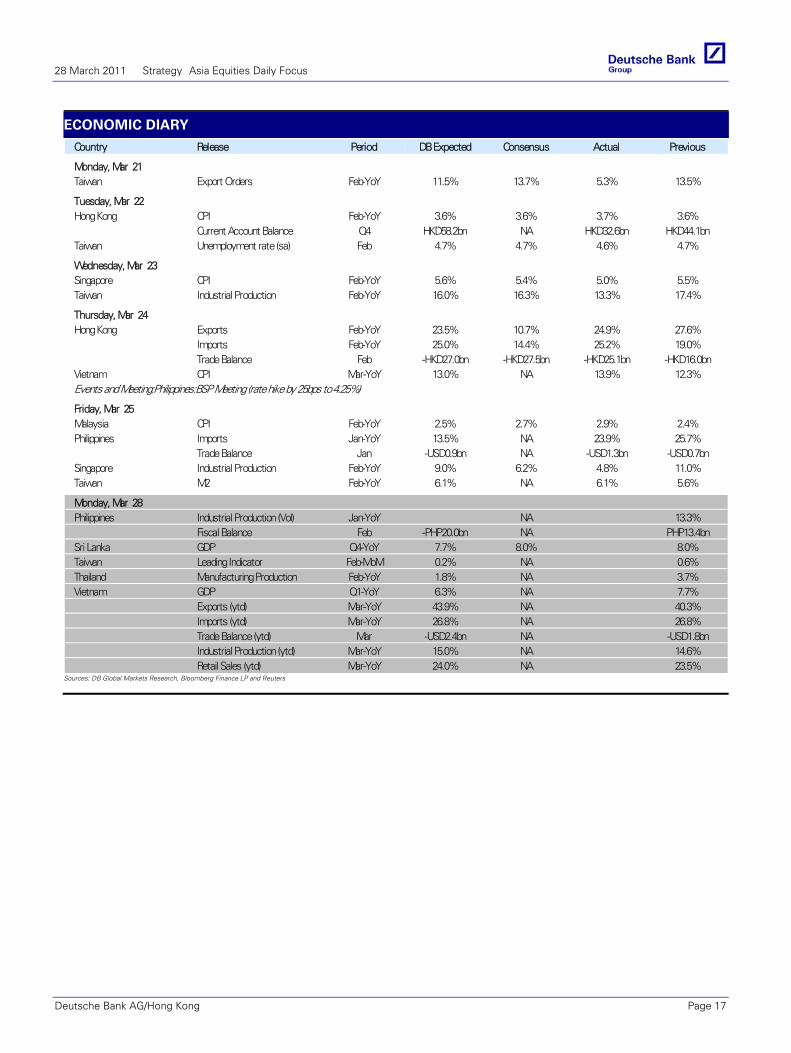

ECONOMIC DIARY

Country Release Period DB Expected Consensus Actual Previous

Monday, Mar 21Taiwan Export Orders Feb-YoY 11.5% 13.7% 5.3% 13.5%

Tuesday, Mar 22Hong Kong CPI Feb-YoY 3.6% 3.6% 3.7% 3.6%

Current Account Balance Q4 HKD58.2bn NA HKD32.6bn HKD44.1bnTaiwan Unemployment rate (sa) Feb 4.7% 4.7% 4.6% 4.7%

Wednesday, Mar 23Singapore CPI Feb-YoY 5.6% 5.4% 5.0% 5.5%Taiwan Industrial Production Feb-YoY 16.0% 16.3% 13.3% 17.4%

Thursday, Mar 24Hong Kong Exports Feb-YoY 23.5% 10.7% 24.9% 27.6%

Imports Feb-YoY 25.0% 14.4% 25.2% 19.0%Trade Balance Feb -HKD27.0bn -HKD27.5bn -HKD25.1bn -HKD16.0bn

Vietnam CPI Mar-YoY 13.0% NA 13.9% 12.3%Events and Meeting:Philippines:BSP Meeting (rate hike by 25bps to 4.25%)

Friday, Mar 25Malaysia CPI Feb-YoY 2.5% 2.7% 2.9% 2.4%Philippines Imports Jan-YoY 13.5% NA 23.9% 25.7%

Trade Balance Jan -USD0.9bn NA -USD1.3bn -USD0.7bnSingapore Industrial Production Feb-YoY 9.0% 6.2% 4.8% 11.0%Taiwan M2 Feb-YoY 6.1% NA 6.1% 5.6%

Monday, Mar 28Philippines Industrial Production (Vol) Jan-YoY NA 13.3%

Fiscal Balance Feb -PHP20.0bn NA PHP13.4bnSri Lanka GDP Q4-YoY 7.7% 8.0% 8.0%Taiwan Leading Indicator Feb-MoM 0.2% NA 0.6%Thailand Manufacturing Production Feb-YoY 1.8% NA 3.7%Vietnam GDP Q1-YoY 6.3% NA 7.7%

Exports (ytd) Mar-YoY 43.9% NA 40.3%Imports (ytd) Mar-YoY 26.8% NA 26.8%Trade Balance (ytd) Mar -USD2.4bn NA -USD1.8bnIndustrial Production (ytd) Mar-YoY 15.0% NA 14.6%Retail Sales (ytd) Mar-YoY 24.0% NA 23.5%

Sources: DB Global Markets Research, Bloomberg Finance LP and Reuters

28 March 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 17

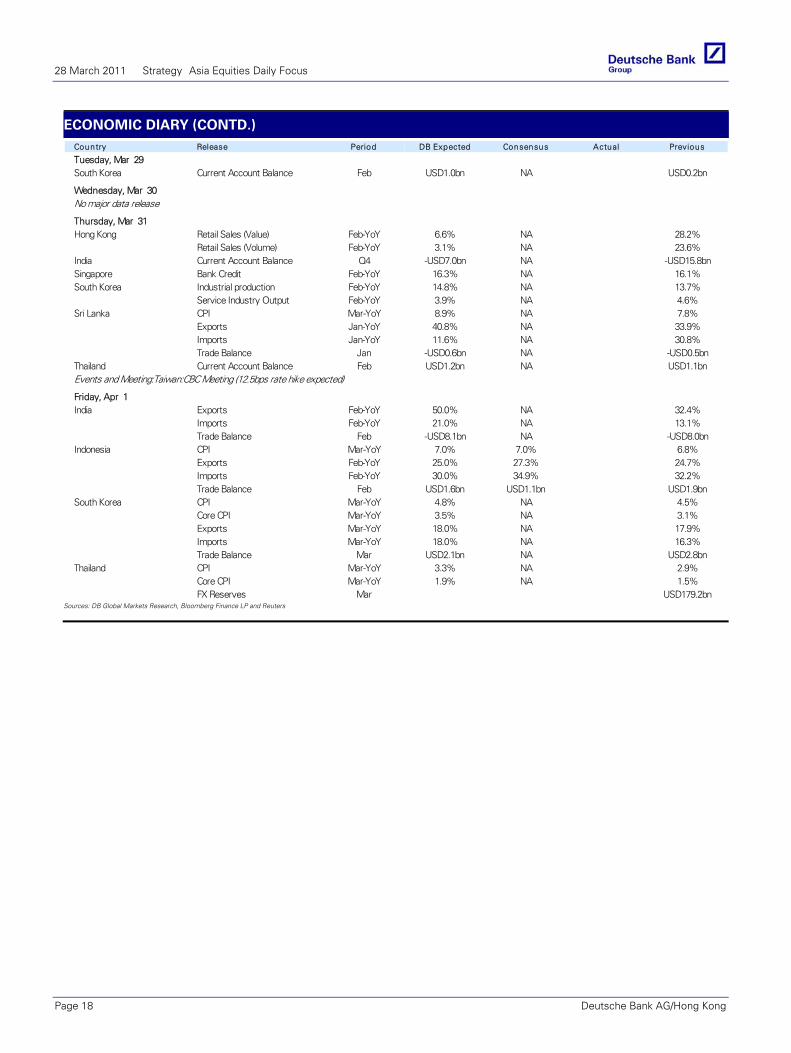

ECONOMIC DIARY (CONTD.) Country Release Period DB Expected Consensus Actual Previous

Tuesday, Mar 29South Korea Current Account Balance Feb USD1.0bn NA USD0.2bn

Wednesday, Mar 30No major data release

Thursday, Mar 31Hong Kong Retail Sales (Value) Feb-YoY 6.6% NA 28.2%

Retail Sales (Volume) Feb-YoY 3.1% NA 23.6%India Current Account Balance Q4 -USD7.0bn NA -USD15.8bnSingapore Bank Credit Feb-YoY 16.3% NA 16.1%South Korea Industrial production Feb-YoY 14.8% NA 13.7%

Service Industry Output Feb-YoY 3.9% NA 4.6%Sri Lanka CPI Mar-YoY 8.9% NA 7.8%

Exports Jan-YoY 40.8% NA 33.9%Imports Jan-YoY 11.6% NA 30.8%Trade Balance Jan -USD0.6bn NA -USD0.5bn

Thailand Current Account Balance Feb USD1.2bn NA USD1.1bnEvents and Meeting:Taiwan:CBC Meeting (12.5bps rate hike expected)

Friday, Apr 1India Exports Feb-YoY 50.0% NA 32.4%

Imports Feb-YoY 21.0% NA 13.1%Trade Balance Feb -USD8.1bn NA -USD8.0bn

Indonesia CPI Mar-YoY 7.0% 7.0% 6.8%Exports Feb-YoY 25.0% 27.3% 24.7%Imports Feb-YoY 30.0% 34.9% 32.2%Trade Balance Feb USD1.6bn USD1.1bn USD1.9bn

South Korea CPI Mar-YoY 4.8% NA 4.5%Core CPI Mar-YoY 3.5% NA 3.1%Exports Mar-YoY 18.0% NA 17.9%Imports Mar-YoY 18.0% NA 16.3%Trade Balance Mar USD2.1bn NA USD2.8bn

Thailand CPI Mar-YoY 3.3% NA 2.9%Core CPI Mar-YoY 1.9% NA 1.5%FX Reserves Mar USD179.2bn

Sources: DB Global Markets Research, Bloomberg Finance LP and Reuters

28 March 2011 Strategy Asia Equities Daily Focus

Page 18 Deutsche Bank AG/Hong Kong

Asia Corporate Credit

25 March 2011

Asia Credit Weekly

Mixed results on property

Market Update

Table of Contents Credit opinion & top movers ........................... Page 2-3Key research & news ....................................... Page 04New issue monitor ........................................... Page 08Earnings calendar ............................................. Page 10Research catalogue .......................................... Page 11

Research Team

Gene Cheon Research Analyst (+65) 64236967 [email protected]

Jacphanie Cheung Research Analyst (+852) 2203 5930 [email protected]

Devinda Paranathanthri Research Analyst (+65) 64235718 [email protected]

Mathura Yogarajah Research Analyst (+65) 6 423-5721 [email protected]

Marie-Anne Garcia Research Analyst (+65) 6 423 5726 [email protected]

Weekly top-movers (IG)

11

9

4

3

3

-23

-23

-27

-28

-60

SINTEL 7.38 '31

PCCW 6.00 '13

ICICI 6.63 '12

TEMASE 4.30 '19

BBLTB 3.25 '15

KDB 4.00 '16

KDB 8.00 '14

INDKOR 7.13 '14

DBSSP 0.91 '21

HUWHY 6.00 'perp

Change in ASW (bp)

Weekly top-movers (HY)

1.3

1.0

0.8

0.5

0.5

-1.0

-1.0

-1.0

-1.0

-2.8

CHOGRP 7.00 '17

EVERRE 9.25 '16

HYUELE 7.88 '17

AGILE 10.00 '16

HIDILI 8.63 '15

CENCHI 12.25 '15

WANHAI 5.50 '15

SHIMAO 8.00 '16

SHIMAO 9.65 '17

KWGPRO 12.50 '17

Change in mid-price

Source : Deutsche Bank

Co

rpo

rate

Cre

dit

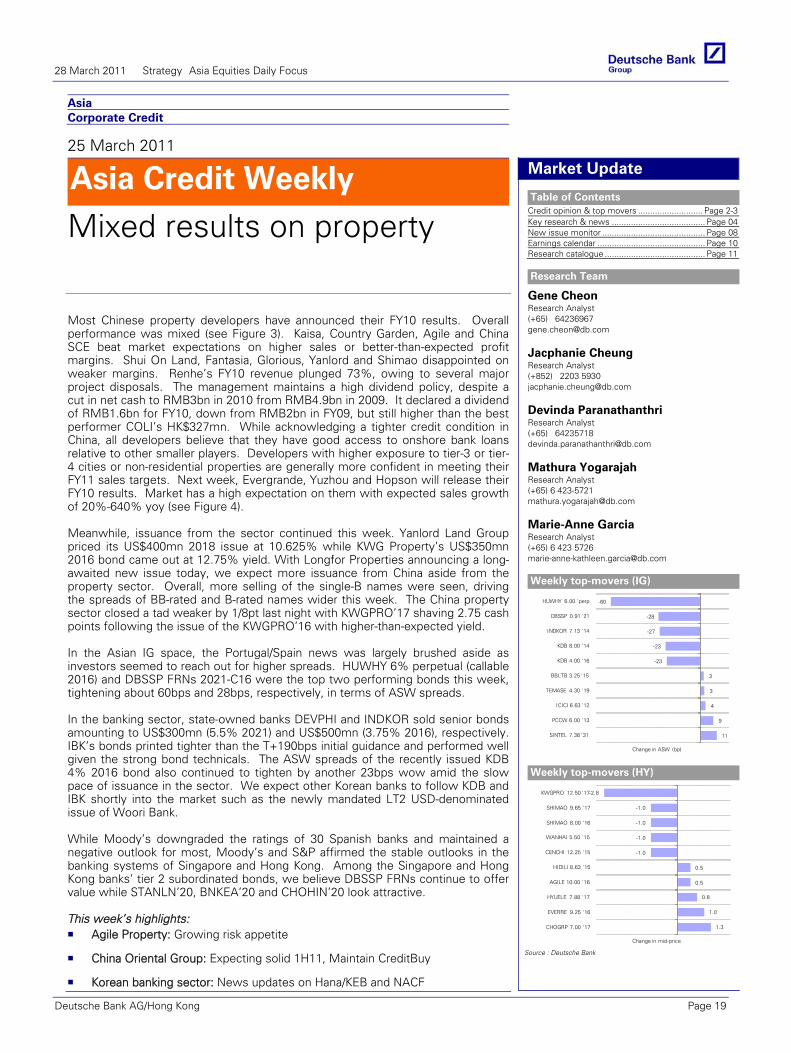

Most Chinese property developers have announced their FY10 results. Overall performance was mixed (see Figure 3). Kaisa, Country Garden, Agile and China SCE beat market expectations on higher sales or better-than-expected profit margins. Shui On Land, Fantasia, Glorious, Yanlord and Shimao disappointed on weaker margins. Renhe’s FY10 revenue plunged 73%, owing to several major project disposals. The management maintains a high dividend policy, despite a cut in net cash to RMB3bn in 2010 from RMB4.9bn in 2009. It declared a dividend of RMB1.6bn for FY10, down from RMB2bn in FY09, but still higher than the best performer COLI’s HK$327mn. While acknowledging a tighter credit condition in China, all developers believe that they have good access to onshore bank loans relative to other smaller players. Developers with higher exposure to tier-3 or tier-4 cities or non-residential properties are generally more confident in meeting their FY11 sales targets. Next week, Evergrande, Yuzhou and Hopson will release their FY10 results. Market has a high expectation on them with expected sales growth of 20%-640% yoy (see Figure 4). Meanwhile, issuance from the sector continued this week. Yanlord Land Group priced its US$400mn 2018 issue at 10.625% while KWG Property’s US$350mn 2016 bond came out at 12.75% yield. With Longfor Properties announcing a long-awaited new issue today, we expect more issuance from China aside from the property sector. Overall, more selling of the single-B names were seen, driving the spreads of BB-rated and B-rated names wider this week. The China property sector closed a tad weaker by 1/8pt last night with KWGPRO’17 shaving 2.75 cash points following the issue of the KWGPRO’16 with higher-than-expected yield. In the Asian IG space, the Portugal/Spain news was largely brushed aside as investors seemed to reach out for higher spreads. HUWHY 6% perpetual (callable 2016) and DBSSP FRNs 2021-C16 were the top two performing bonds this week, tightening about 60bps and 28bps, respectively, in terms of ASW spreads. In the banking sector, state-owned banks DEVPHI and INDKOR sold senior bonds amounting to US$300mn (5.5% 2021) and US$500mn (3.75% 2016), respectively. IBK’s bonds printed tighter than the T+190bps initial guidance and performed well given the strong bond technicals. The ASW spreads of the recently issued KDB 4% 2016 bond also continued to tighten by another 23bps wow amid the slow pace of issuance in the sector. We expect other Korean banks to follow KDB and IBK shortly into the market such as the newly mandated LT2 USD-denominated issue of Woori Bank. While Moody’s downgraded the ratings of 30 Spanish banks and maintained a negative outlook for most, Moody’s and S&P affirmed the stable outlooks in the banking systems of Singapore and Hong Kong. Among the Singapore and Hong Kong banks’ tier 2 subordinated bonds, we believe DBSSP FRNs continue to offer value while STANLN’20, BNKEA’20 and CHOHIN’20 look attractive. This week’s highlights:

Agile Property: Growing risk appetite

China Oriental Group: Expecting solid 1H11, Maintain CreditBuy

Korean banking sector: News updates on Hana/KEB and NACF

28 March 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 19

Asia

25 March 2011

Asia Local Markets Weekly Policy versus supply

Strategy Update

Table of Contents Summary Market Views ................................... Page 02Economics........................................................ Page 03Fixed Income Strategy ..................................... Page 04Foreign Exchange Strategy .............................. Page 10Economic Diary ................................................ Page 11Bond Supply Monitor ....................................... Page 12Monetary Policy Monitor.................................. Page 13Local Markets Analytics ................................... Page 14Asian Economic Indicators ............................... Page 19

Research Team

Sameer Goel Strategist (+65 ) 64236973 [email protected]

Mirza Baig Strategist (+65) 64235930 [email protected]

Linan Liu Strategist (+852) 2203 8709 [email protected]

Arjun Shetty Strategist (+65) 6423 5925 [email protected]

Michael Spencer, Ph.D Chief Economist (++852) 22038303 [email protected]

Dennis Tan Strategist (+65) 6 423-5347 [email protected]

Str

ateg

y

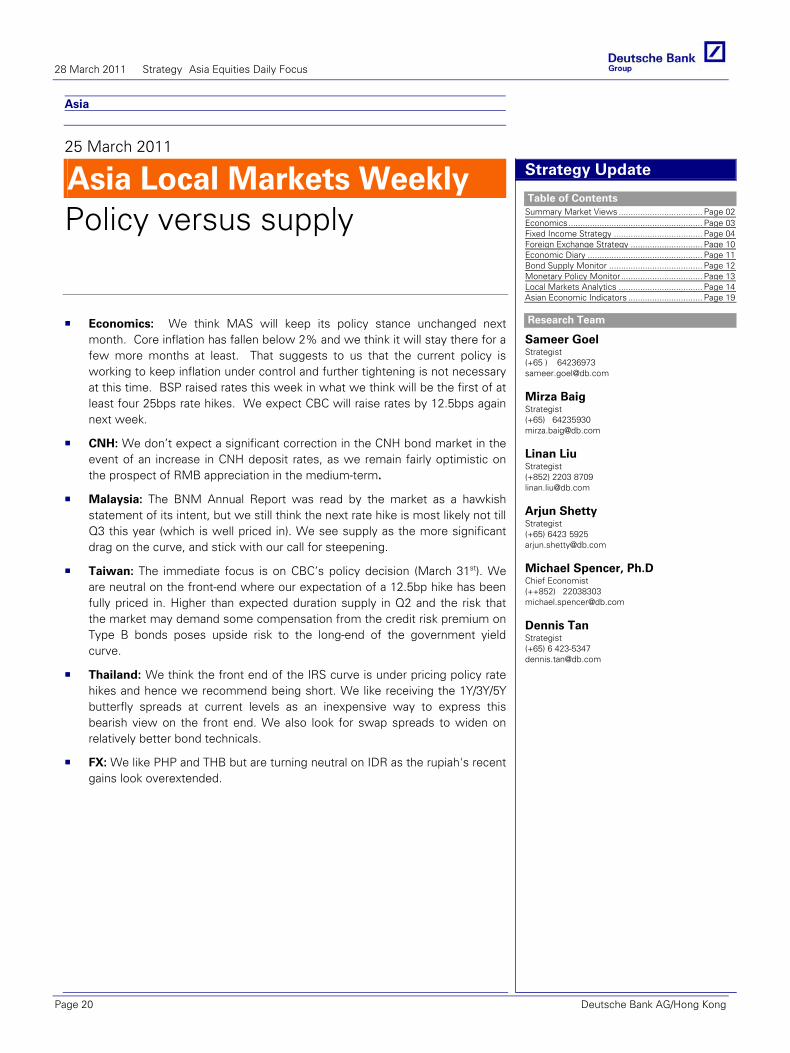

Economics: We think MAS will keep its policy stance unchanged next month. Core inflation has fallen below 2% and we think it will stay there for a few more months at least. That suggests to us that the current policy is working to keep inflation under control and further tightening is not necessary at this time. BSP raised rates this week in what we think will be the first of at least four 25bps rate hikes. We expect CBC will raise rates by 12.5bps again next week.

CNH: We don’t expect a significant correction in the CNH bond market in the event of an increase in CNH deposit rates, as we remain fairly optimistic on the prospect of RMB appreciation in the medium-term.

Malaysia: The BNM Annual Report was read by the market as a hawkish statement of its intent, but we still think the next rate hike is most likely not till Q3 this year (which is well priced in). We see supply as the more significant drag on the curve, and stick with our call for steepening.

Taiwan: The immediate focus is on CBC’s policy decision (March 31st). We are neutral on the front-end where our expectation of a 12.5bp hike has been fully priced in. Higher than expected duration supply in Q2 and the risk that the market may demand some compensation from the credit risk premium on Type B bonds poses upside risk to the long-end of the government yield curve.

Thailand: We think the front end of the IRS curve is under pricing policy rate hikes and hence we recommend being short. We like receiving the 1Y/3Y/5Y butterfly spreads at current levels as an inexpensive way to express this bearish view on the front end. We also look for swap spreads to widen on relatively better bond technicals.

FX: We like PHP and THB but are turning neutral on IDR as the rupiah's recent gains look overextended.

28 March 2011 Strategy Asia Equities Daily Focus

Page 20 Deutsche Bank AG/Hong Kong

North America United States

25 March 2011

US Daily Economic Notes

Payrolls, production & income dominate data docket 4

Eco

n

Economic ResearchResearch TeamJoseph A. LaVorgna Chief US Economist 212 250-7329 [email protected]

Carl J. Riccadonna Senior US Economist 212-250-0186 [email protected]

Brett Ryan Economist 212-250-6294 [email protected]

Policy Speeches

12:40 pm Atlanta Fed President Lockhart (non-voter) speaks on U.S. economy in Atlanta, GA 3:40 pm Chicago Fed President Evans (voter) speaks to reporters in Columbia, SC 4:00 pm Chicago Fed President Evans (voter) speaks on U.S. economy in Columbia, SC 6:00 pm Boston Fed President Rosengren (non-voter) speaks on recession and recovery in Boston, MA

Year End TargetsReal GDP growth: +4.1% Q4/Q4 Core PCE deflator: +2.1% Q4/Q4 Unemployment rate: 7.8% Fed Funds: 0.50%

Fed Policy

We expect fed funds to be range-bound between 0-25 bps through Q3 2011. The Fed is projected to hike rates to 0.50% in Q4 2011.

Tsy Auction

Size Prev. 1:00 pm 2-y note (auc.) $35B $35B

Post Employment Conference Call

Friday March 4, 9:00am ET

Domestic Participant Dial In: (877) 660- 0990/ International: (706) 643-3803 Conference ID: 29101415 Replay # (Begins after 11:30am ET): (800) 642-1687 or (706) 645-9291 Int’l

150

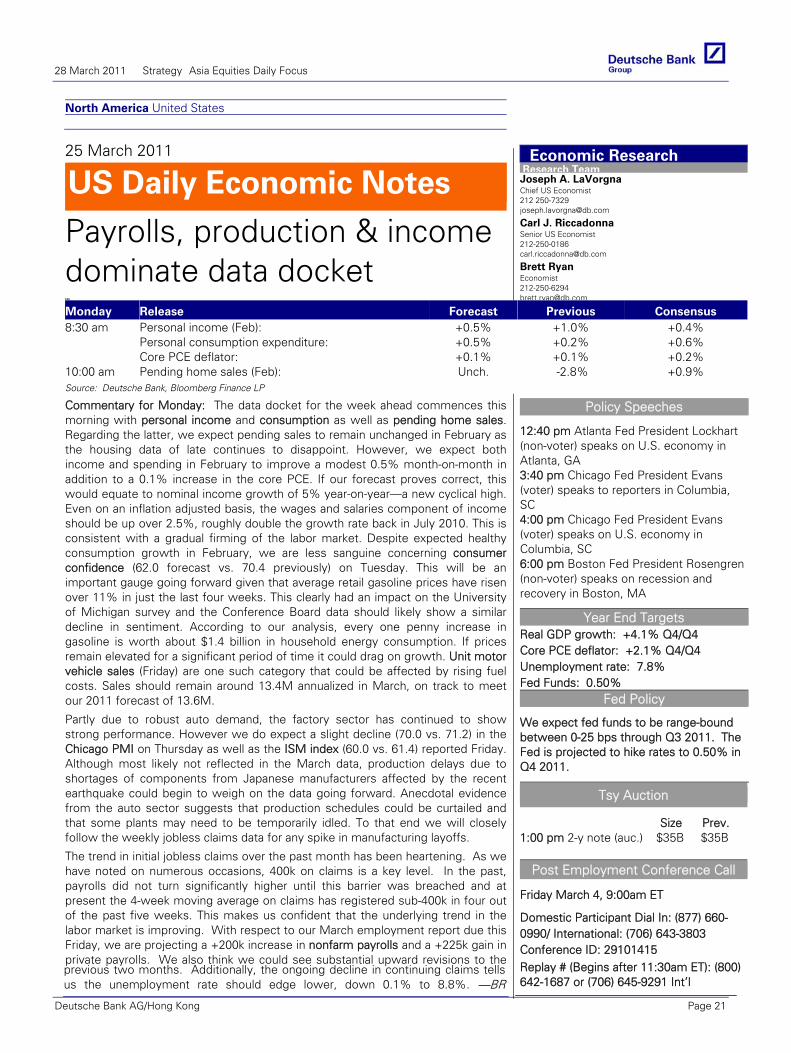

Monday Release Forecast Previous Consensus 8:30 am Personal income (Feb): +0.5% +1.0% +0.4% Personal consumption expenditure: +0.5% +0.2% +0.6% Core PCE deflator: +0.1% +0.1% +0.2% 10:00 am Pending home sales (Feb): Unch. -2.8% +0.9% Source: Deutsche Bank, Bloomberg Finance LP

Commentary for Monday: The data docket for the week ahead commences this morning with personal income and consumption as well as pending home sales. Regarding the latter, we expect pending sales to remain unchanged in February as the housing data of late continues to disappoint. However, we expect both income and spending in February to improve a modest 0.5% month-on-month in addition to a 0.1% increase in the core PCE. If our forecast proves correct, this would equate to nominal income growth of 5% year-on-year—a new cyclical high. Even on an inflation adjusted basis, the wages and salaries component of income should be up over 2.5%, roughly double the growth rate back in July 2010. This is consistent with a gradual firming of the labor market. Despite expected healthy consumption growth in February, we are less sanguine concerning consumer confidence (62.0 forecast vs. 70.4 previously) on Tuesday. This will be an important gauge going forward given that average retail gasoline prices have risen over 11% in just the last four weeks. This clearly had an impact on the University of Michigan survey and the Conference Board data should likely show a similar decline in sentiment. According to our analysis, every one penny increase in gasoline is worth about $1.4 billion in household energy consumption. If prices remain elevated for a significant period of time it could drag on growth. Unit motor vehicle sales (Friday) are one such category that could be affected by rising fuel costs. Sales should remain around 13.4M annualized in March, on track to meet our 2011 forecast of 13.6M.

Partly due to robust auto demand, the factory sector has continued to show strong performance. However we do expect a slight decline (70.0 vs. 71.2) in the Chicago PMI on Thursday as well as the ISM index (60.0 vs. 61.4) reported Friday. Although most likely not reflected in the March data, production delays due to shortages of components from Japanese manufacturers affected by the recent earthquake could begin to weigh on the data going forward. Anecdotal evidence from the auto sector suggests that production schedules could be curtailed and that some plants may need to be temporarily idled. To that end we will closely follow the weekly jobless claims data for any spike in manufacturing layoffs.

The trend in initial jobless claims over the past month has been heartening. As we have noted on numerous occasions, 400k on claims is a key level. In the past, payrolls did not turn significantly higher until this barrier was breached and at present the 4-week moving average on claims has registered sub-400k in four out of the past five weeks. This makes us confident that the underlying trend in the labor market is improving. With respect to our March employment report due this Friday, we are projecting a +200k increase in nonfarm payrolls and a +225k gain in private payrolls. We also think we could see substantial upward revisions to the

previous two months. Additionally, the ongoing decline in continuing claims tells us the unemployment rate should edge lower, down 0.1% to 8.8%. —BR

28 March 2011 Strategy Asia Equities Daily Focus

Deutsche Bank AG/Hong Kong Page 21

North America United States

25 March 2011

US Economics Weekly Staying strong on above trend growth

Economics

Table of Contents Overview.............................................................Page 2Above trend growth expected... .........................Page 4Calendar ..............................................................Page 8Contacts ..............................................................Page 9

Research Team

Joseph LaVorgna Economist (+1) 212 250-7329 [email protected]

Carl Riccadonna Economist (+1) 212 250-0186 [email protected]

Brett Ryan Research Analyst (+1) 212 250-6294 [email protected]

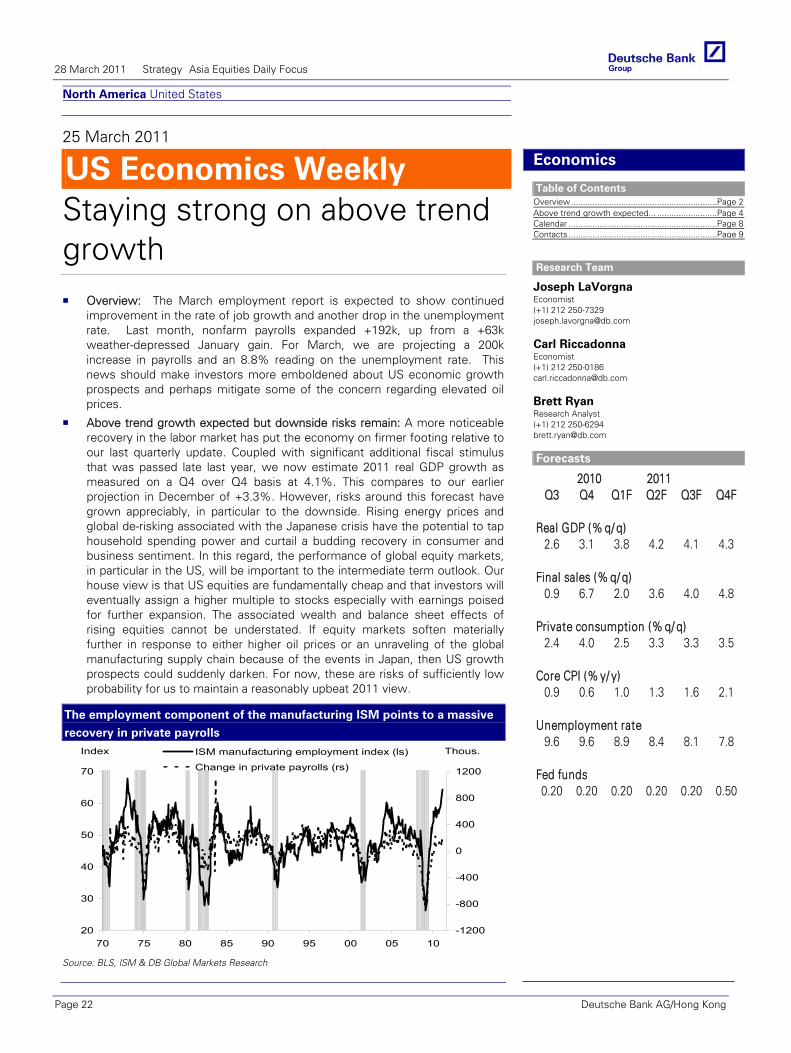

Forecasts

2010 2011Q3 Q4 Q1F Q2F Q3F Q4F

Real GDP (% q/ q)2.6 3.1 3.8 4.2 4.1 4.3

Final sales (% q/ q)0.9 6.7 2.0 3.6 4.0 4.8

Private consumption (% q/ q)2.4 4.0 2.5 3.3 3.3 3.5

Core CPI (% y/ y)0.9 0.6 1.0 1.3 1.6 2.1

Unemployment rate9.6 9.6 8.9 8.4 8.1 7.8

Fed funds0.20 0.20 0.20 0.20 0.20 0.50

Eco

no

mic

s

Overview: The March employment report is expected to show continued improvement in the rate of job growth and another drop in the unemployment rate. Last month, nonfarm payrolls expanded +192k, up from a +63k weather-depressed January gain. For March, we are projecting a 200k increase in payrolls and an 8.8% reading on the unemployment rate. This news should make investors more emboldened about US economic growth prospects and perhaps mitigate some of the concern regarding elevated oil prices.

Above trend growth expected but downside risks remain: A more noticeable recovery in the labor market has put the economy on firmer footing relative to our last quarterly update. Coupled with significant additional fiscal stimulus that was passed late last year, we now estimate 2011 real GDP growth as measured on a Q4 over Q4 basis at 4.1%. This compares to our earlier projection in December of +3.3%. However, risks around this forecast have grown appreciably, in particular to the downside. Rising energy prices and global de-risking associated with the Japanese crisis have the potential to tap household spending power and curtail a budding recovery in consumer and business sentiment. In this regard, the performance of global equity markets, in particular in the US, will be important to the intermediate term outlook. Our house view is that US equities are fundamentally cheap and that investors will eventually assign a higher multiple to stocks especially with earnings poised for further expansion. The associated wealth and balance sheet effects of rising equities cannot be understated. If equity markets soften materially further in response to either higher oil prices or an unraveling of the global manufacturing supply chain because of the events in Japan, then US growth prospects could suddenly darken. For now, these are risks of sufficiently low probability for us to maintain a reasonably upbeat 2011 view.

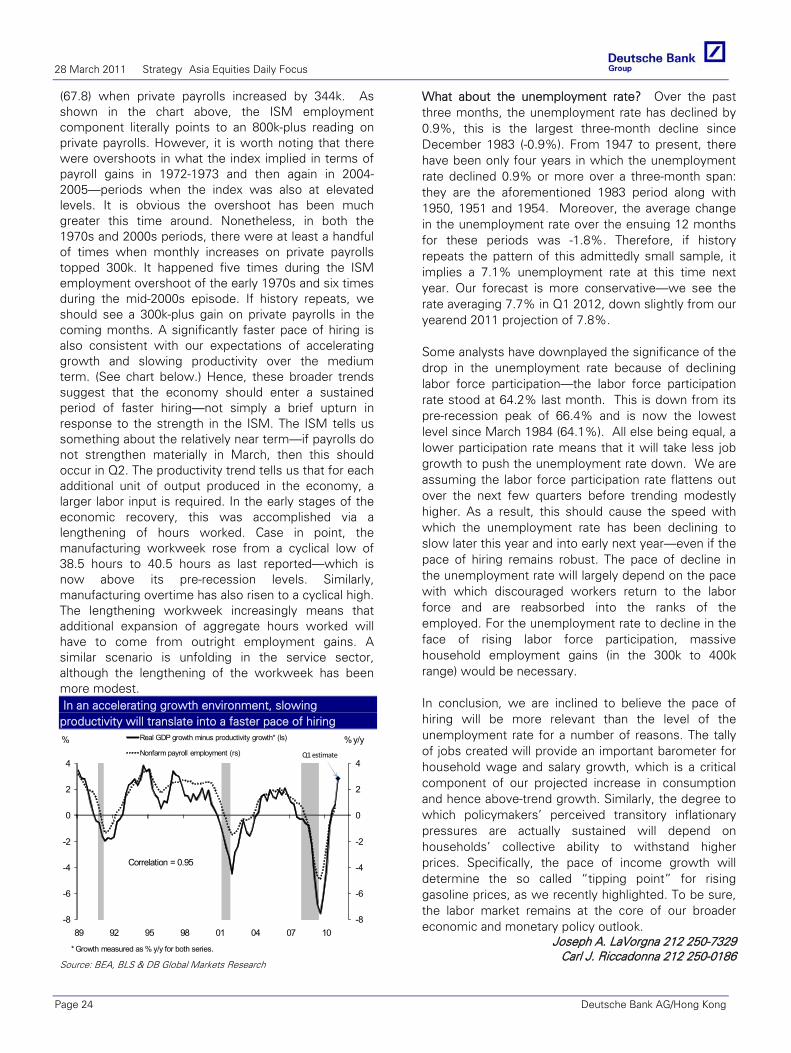

The employment component of the manufacturing ISM points to a massive

recovery in private payrolls

20

30

40

50

60

70

70 75 80 85 90 95 00 05 10

Index

-1200

-800

-400

0

400

800

1200

Thous.ISM manufacturing employment index (ls)

Change in private payrolls (rs)

Source: BLS, ISM & DB Global Markets Research

28 March 2011 Strategy Asia Equities Daily Focus

Page 22 Deutsche Bank AG/Hong Kong

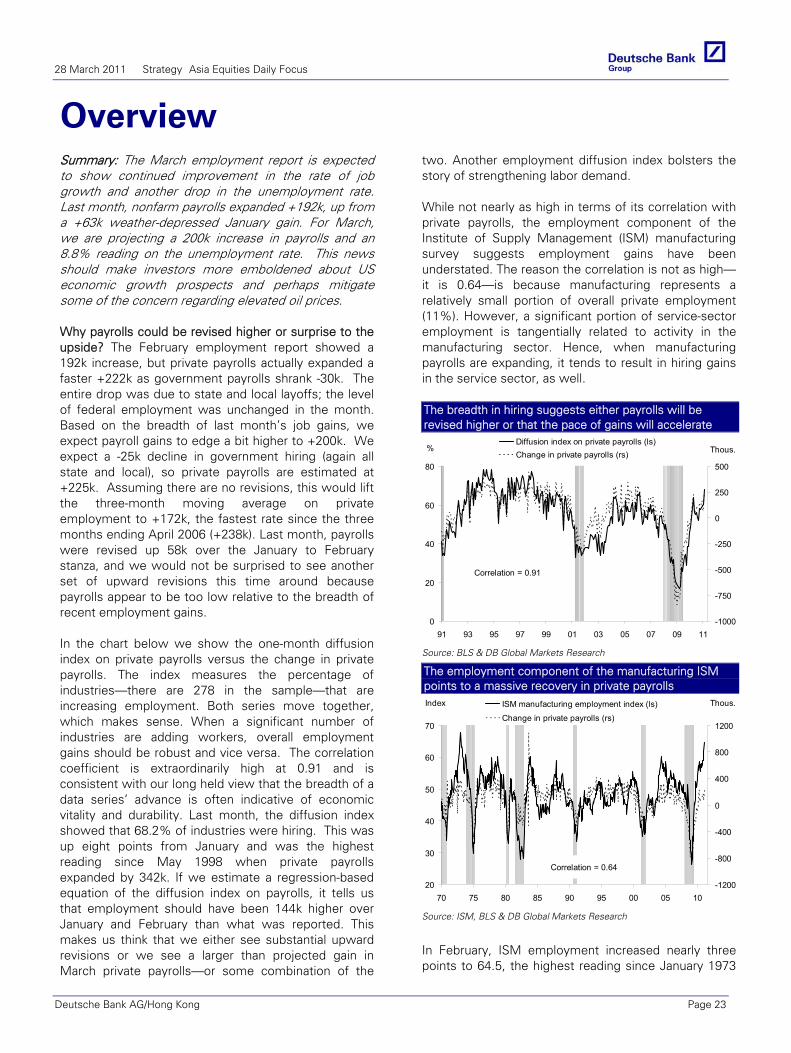

OverviewSummary: The March employment report is expected to show continued improvement in the rate of job growth and another drop in the unemployment rate. Last month, nonfarm payrolls expanded +192k, up from a +63k weather-depressed January gain. For March, we are projecting a 200k increase in payrolls and an 8.8% reading on the unemployment rate. This news should make investors more emboldened about US economic growth prospects and perhaps mitigate some of the concern regarding elevated oil prices. Why payrolls could be revised higher or surprise to the upside? The February employment report showed a 192k increase, but private payrolls actually expanded a faster +222k as government payrolls shrank -30k. The entire drop was due to state and local layoffs; the level of federal employment was unchanged in the month. Based on the breadth of last month’s job gains, we expect payroll gains to edge a bit higher to +200k. We expect a -25k decline in government hiring (again all state and local), so private payrolls are estimated at +225k. Assuming there are no revisions, this would lift the three-month moving average on private employment to +172k, the fastest rate since the three months ending April 2006 (+238k). Last month, payrolls were revised up 58k over the January to February stanza, and we would not be surprised to see another set of upward revisions this time around because payrolls appear to be too low relative to the breadth of recent employment gains. In the chart below we show the one-month diffusion index on private payrolls versus the change in private payrolls. The index measures the percentage of industries—there are 278 in the sample—that are increasing employment. Both series move together, which makes sense. When a significant number of industries are adding workers, overall employment gains should be robust and vice versa. The correlation coefficient is extraordinarily high at 0.91 and is consistent with our long held view that the breadth of a data series’ advance is often indicative of economic vitality and durability. Last month, the diffusion index showed that 68.2% of industries were hiring. This was up eight points from January and was the highest reading since May 1998 when private payrolls expanded by 342k. If we estimate a regression-based equation of the diffusion index on payrolls, it tells us that employment should have been 144k higher over January and February than what was reported. This makes us think that we either see substantial upward revisions or we see a larger than projected gain in March private payrolls—or some combination of the

two. Another employment diffusion index bolsters the story of strengthening labor demand. While not nearly as high in terms of its correlation with private payrolls, the employment component of the Institute of Supply Management (ISM) manufacturing survey suggests employment gains have been understated. The reason the correlation is not as high—it is 0.64—is because manufacturing represents a relatively small portion of overall private employment (11%). However, a significant portion of service-sector employment is tangentially related to activity in the manufacturing sector. Hence, when manufacturing payrolls are expanding, it tends to result in hiring gains in the service sector, as well. The breadth in hiring suggests either payrolls will be revised higher or that the pace of gains will accelerate

0

20

40

60

80

91 93 95 97 99 01 03 05 07 09 11

%

-1000

-750

-500

-250

0

250

500

Thous.Diffusion index on private payrolls (ls)Change in private payrolls (rs)

Correlation = 0.91

Source: BLS & DB Global Markets Research

The employment component of the manufacturing ISM points to a massive recovery in private payrolls

20

30

40

50

60

70