Embed Size (px)

Citation preview

28 February 2017

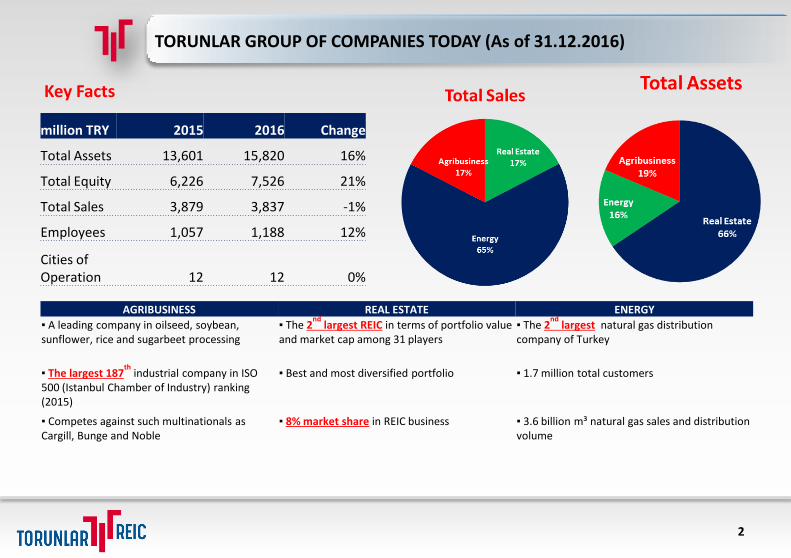

TORUNLAR GROUP OF COMPANIES TODAY (As of 31.12.2016)

AGRIBUSINESS REAL ESTATE ENERGY

▪ A leading company in oilseed, soybean, sunflower, rice and sugarbeet processing

▪ The 2nd

largest REIC in terms of portfolio value and market cap among 31 players

▪ The 2nd

largest natural gas distribution company of Turkey

▪ The largest 187th

industrial company in ISO 500 (Istanbul Chamber of Industry) ranking(2015)

▪ Best and most diversified portfolio ▪ 1.7 million total customers

▪ Competes against such multinationals as Cargill, Bunge and Noble

▪ 8% market share in REIC business ▪ 3.6 billion m³ natural gas sales and distributionvolume

Key Facts

2

million TRY 2015 2016 Change

Total Assets 13,601 15,820 16%

Total Equity 6,226 7,526 21%

Total Sales 3,879 3,837 -1%

Employees 1,057 1,188 12%

Cities of Operation 12 12 0%

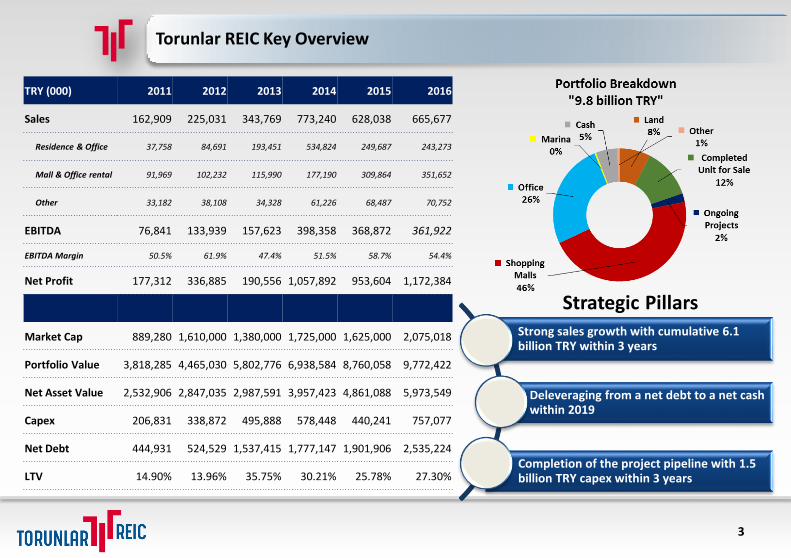

Strong sales growth with cumulative 6.1billion TRY within 3 years

Deleveraging from a net debt to a net cash within 2019

Completion of the project pipeline with 1.5billion TRY capex within 3 years

Torunlar REIC Key Overview

3

Strategic Pillars

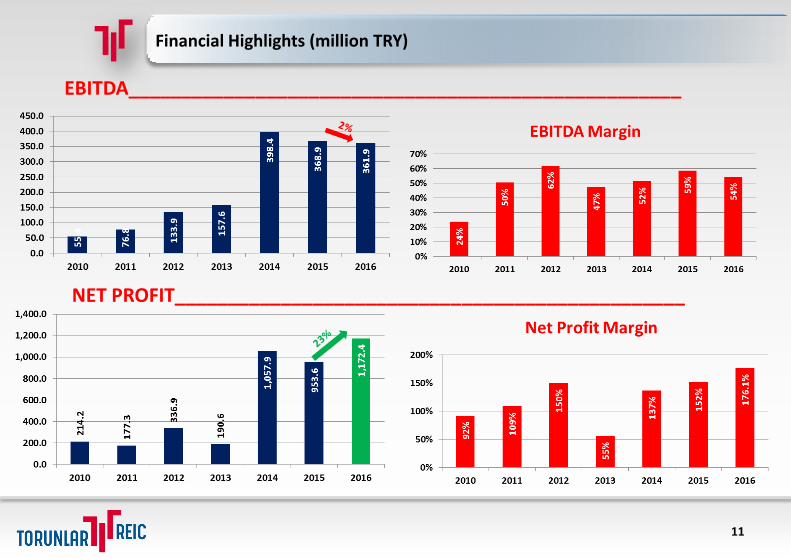

TRY (000) 2011 2012 2013 2014 2015 2016

Sales 162,909 225,031 343,769 773,240 628,038 665,677

Residence & Office 37,758 84,691 193,451 534,824 249,687 243,273

Mall & Office rental 91,969 102,232 115,990 177,190 309,864 351,652

Other 33,182 38,108 34,328 61,226 68,487 70,752

EBITDA 76,841 133,939 157,623 398,358 368,872 361,922

EBITDA Margin 50.5% 61.9% 47.4% 51.5% 58.7% 54.4%

Net Profit 177,312 336,885 190,556 1,057,892 953,604 1,172,384

Market Cap 889,280 1,610,000 1,380,000 1,725,000 1,625,000 2,075,018

Portfolio Value 3,818,285 4,465,030 5,802,776 6,938,584 8,760,058 9,772,422

Net Asset Value 2,532,906 2,847,035 2,987,591 3,957,423 4,861,088 5,973,549

Capex 206,831 338,872 495,888 578,448 440,241 757,077

Net Debt 444,931 524,529 1,537,415 1,777,147 1,901,906 2,535,224

LTV 14.90% 13.96% 35.75% 30.21% 25.78% 27.30%

3

ISTANBUL• Torium Shopping Mall 5. Levent Project• NishIstanbul Mixed-Use Project Mall of İstanbul 2. Phase• Mall of İstanbul Kemankes Land• Torun Tower Kayabasi Land• Torun Center Pasabahce Land

SAMSUN

• Bulvar Samsun Shopping Mall

ANKARA

• ANKAmall Shopping Mall

• Crowne Plaza Hotel

BURSA• Zafer Plaza Shopping Mall• Korupark Shopping Mall• Korupark Residences Phases I-II • Korupark Residences Phase III

MUGLA

• Netsel Marina

ANTALYA

• Deepo Outlet Mall

• Mall of Antalya Project

Project Locations – Turkey –

4

Project Locations – Istanbul –

5

Portfolio size 9.8 billion TRY.

Solid operational performance with 666 million TRY sales revenue, and 362 million TRY EBITDA.

Residential and office deliveries reached 243 million TRY mainly coming from Torun Center.

Rental income at 352 million TRY up by 13.5% y-o-y and like-for-like basis.

Prudent metrics: loan to value at 27.3% and cost of debt in FX is at 4.73%.

Focus on:

obtaining the construction licence of Paşabahçe project,

opening of Mall of Antalya in April 2017,

completing MOI 2nd Phase Hotel and Convention Center project,

delivering some of the residential units at 5th Levent in Q4 2017

destocking of remaining residences and leasing of selected offices and retail area at Torun Center.

Leverage will be ended within the year of 2019.

Consider opportunistic operational asset acquisitions going forward.

2016 Highlights and Forward Strategy

6

Build to Rent Assets

7

(TRY)Operation

DateLand Cost Construction Cost Total Cost *

Appraisal Value

2014 2015 2016

Malls - in operation 503,276,753 753,982,823 1,257,259,576 3,220,992,115 3,753,614,326 3,983,745,000

Zafer 1999 18,448,375 18,448,375 240,172,000 312,857,000 329,020,000

Korupark 3Q 2007 6,719,681 77,315,718 84,035,399 882,235,000 1,007,213,000 1,201,798,000

Deepo Outlet 4Q 2004 7,700,000 10,149,518 17,849,518 254,981,115 292,988,326 286,823,000

Torium 4Q 2010 54,857,072 221,069,212 275,926,284 467,442,000 522,572,000 525,190,000

MOI 2Q 2014 434,000,000 427,000,000 861,000,000 1,376,162,000 1,617,984,000 1,640,914,000

Malls - upcoming 12,335,000 134,171,700 146,506,700 48,956,678 100,577,680 226,547,000

Mall of Antalya 2Q 2017 12,335,000 134,171,700 146,506,700 48,956,678 100,577,680 226,547,000

Offices - in operation 779,800,000 315,037,703 1,094,837,703 1,792,351,000 2,781,258,000 2,520,604,000

Torun Tower 2Q 2014 268,800,000 135,578,740 404,378,740 928,091,000 1,178,280,000 1,492,410,000

Torun Center 1H 2017 511,000,000 179,458,963 690,458,963 864,260,000 1,602,978,000 1,028,194,000

Hotels - upcoming 177,500,000 162,133,200 339,633,200 430,123,000 452,460,000 607,330,000

Hotel Paşabahçe*** 1H 2019 177,500,000 162,133,200 339,633,200 430,123,000 452,460,000 607,330,000

TOTAL 1,472,911,753 1,365,325,426 2,838,237,179 5,492,422,793 5,486,534,984 7,338,226,000

(TRY) GLA (sqm)2015 2016 2017 F

Rental Revenues NOI Yield Rental Revenues NOI Yield Rental Revenues NOI Yield

Malls - in operation 355,577 252,183,687 226,896,464 6.04% 288,216,000 251,128,000 6.30% 331,502,629 285,957,262 7.18%

Zafer 23,449 27,533,565 19,895,754 6.36% 30,000,000 21,876,000 6.65% 34,800,000 22,027,136 6.69%

Korupark 71,267 69,915,588 71,680,893 7.12% 80,994,000 80,072,000 6.66% 88,460,726 85,860,500 7.14%

Deepo Outlet 18,132 19,857,677 20,321,836 6.94% 20,177,000 17,451,000 6.08% 19,755,353 17,845,912 6.22%

Torium 87,872 34,318,971 29,426,559 5.63% 34,431,000 24,632,000 4.69% 39,766,779 28,427,957 5.41%

MOI 154,857 100,557,885 85,571,422 5.29% 122,614,000 107,097,000 6.53% 148,719,771 131,795,757 8.03%

Malls - upcoming 42,000

Mall of Antalya 42,000

Offices - in operation 134,960 52,138,000 50,983,000 4.33% 61,723,000 60,391,000 4.05% 76,780,000 75,123,065 5.03%

Torun Tower 66,286 52,138,000 50,983,000 4.33% 61,723,000 60,391,000 4.05% 76,780,000 75,123,065 5.03%

Torun Center** 68,674

Hotels - upcoming 25,000

Hotel Paşabahçe*** 25,000

TOTAL 557,537 304,321,687 277,879,464 5.63% 349,939,000 311,519,000 6.31% 408,282,629 361,080,327 6.59%

* Total cost denotes historical cost of project

** Torun Center consists of offices and retail area

*** Paşabahçe appraisal value consists both the hotel and villas

Build to Sell Assets

8

(TRY) UnitSellable

Area (sqm)

2017 F 2018 F 2019 F 2020 F 2021 FPROJECT TOTAL

Unit sqm Revenue Unit sqm Revenue Unit sqm Revenue Unit sqm Revenue Unit sqm Revenue

Completed Projects 429 70,571 79 13,074 178,483,044 80 13,097 312,336,712 51 8,367 205,633,000 46 7,552 197,511,184 173 28,481 868,288,746 1,762,252,686

Korupark Residences Ph. III

35 5,858 35 5,858 20,375,400 20,375,400

Torun Center Residences 394 64,713 44 7,216 158,107,644 80 13,097 312,336,712 51 8,367 205,633,000 46 7,552 197,511,184 173 28,481 868,288,746 1,741,877,286

South Tower 164 27,130 14 2,326 43,681,644 26 4,295 86,480,000 27 4,455 96,178,500 27 4,455 101,623,500 70 11,598 274,151,385 602,115,029

East Tower 230 37,583 30 4,890 114,426,000 54 8,802 225,856,712 24 3,912 109,454,500 19 3,097 95,887,684 103 16,883 594,137,361 1,139,762,257

Ongoing Projects 752 119,035 330 51,080 390,393,403 312 48,566 439,053,924 110 19,389 186,141,495 0 0 0 0 0 0 1,015,588,822

5. Levent 1. & 2. Phases 752 119,035 330 51,080 390,393,403 312 48,566 439,053,924 110 19,389 186,141,495 1,015,588,822

Upcoming Projects 938 125,000 13 9,000 486,000,000 313 42,000 775,650,000 312 40,000 711,750,000 300 34,000 340,000,000 0 0 0 2,313,400,000

5. Levent 3. Phase 900 100,000 300 33,000 264,000,000 300 33,000 297,000,000 300 34,000 340,000,000 901,000,000

Paşabahçe 38 25,000 13 9,000 486,000,000 13 9,000 511,650,000 12 7,000 414,750,000 1,412,400,000

TOTAL 2,119 314,606 422 73,154 1,054,876,447 705 103,663 1,527,040,636 473 67,756 1,103,524,495 346 41,552 537,511,184 173 28,481 868,288,746 5,091,241,508

PORTFOLIO VALUE____________________________________________

CAPEX______________________________________________________

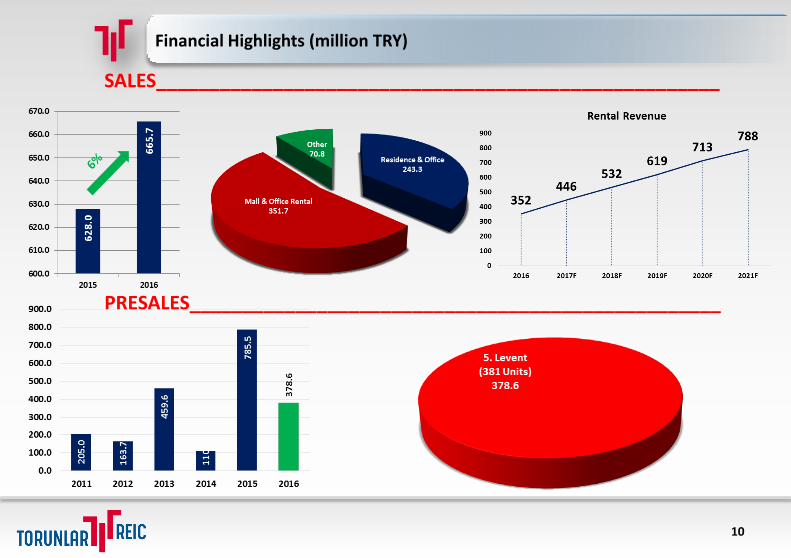

Financial Highlights (million TRY)

9

SALES_____________________________________________________

PRESALES__________________________________________________

Financial Highlights (million TRY)

10

NET PROFIT________________________________________________

EBITDA____________________________________________________

Financial Highlights (million TRY)

11

12

KPI Summary

2015 2016 Change

Total net debt (000 TRY) 1,901,906 2,535,224 33.30%

Average loan term (years) 5 5

Average overall interest rate* 4.26% 4.73% 0.47 pp

Leverage (financial loans as % of total assets) 31.7% 29.4% -2.30 pp

Net debt to Equity ratio 39.1% 42.4% 3.32 pp

Net debt/Assets (%) 21.5% 24.4% 2.97 pp

Equity to assets ratio 54.9% 57.6% 2.71 pp

Loan to Property value ratio (LTV) 25.8% 27.3% 1.53 pp

Interest coverage ratio (times) 5.5 5.2 -4.91%

Net debt/EBITDA (times) 5.16 7.00 35.86%

Net Debt/Mcap 117.0% 122.2% 5.14 pp

Headcount 175 234 33.71%

* Excl. TRY Loans

Net Balance Sheet Position (000) 31.12.2015 31.12.2016 Change

USD -674,621 -616,767 -9%

EUR -196,084 -185,951 -5%

TRY Equivalent -2,584,604 -2,860,387 11%

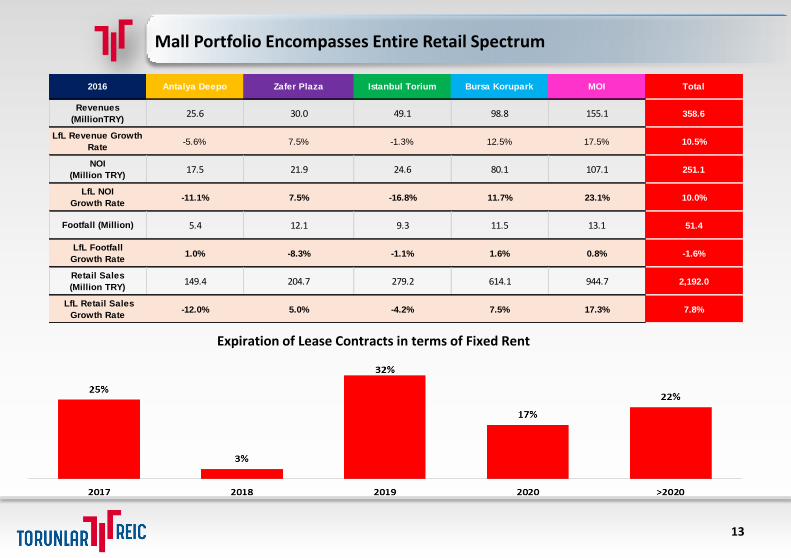

Mall Portfolio Encompasses Entire Retail Spectrum

13

Expiration of Lease Contracts in terms of Fixed Rent

25.6 30.0 49.1 98.8 155.1 358.6

-5.6% 7.5% -1.3% 12.5% 17.5% 10.5%

17.5 21.9 24.6 80.1 107.1 251.1

-11.1% 7.5% -16.8% 11.7% 23.1% 10.0%

5.4 12.1 9.3 11.5 13.1 51.4

1.0% -8.3% -1.1% 1.6% 0.8% -1.6%

149.4 204.7 279.2 614.1 944.7 2,192.0

-12.0% 5.0% -4.2% 7.5% 17.3% 7.8%

Footfall (Million)

2016 Antalya Deepo Zafer Plaza Istanbul Torium Total

Revenues

(MillionTRY)

LfL Revenue Growth

Rate

NOI

(Million TRY)

LfL NOI

Growth Rate

Bursa Korupark MOI

LfL Footfall

Growth Rate

Retail Sales

(Million TRY)

LfL Retail Sales

Growth Rate

• Rank: 2• GLA: 8,205

(2.3%)• 1.9% of Monthly

Fixed Rent

• Rank: 3• GLA: 2,651 (0.7%)• 1.9% of Monthly

Fixed Rent

• Rank: 4• GLA: 10,026 (2.8%)• 1.8% of Monthly

Fixed Rent

• Rank: 7• GLA: 11,633 (3.3%)• 1.6% of Monthly

Fixed Rent

• Rank: 1• GLA: 19,418 (5.5%)• 3.6% of Monthly

Fixed Rent

• Rank: 10• GLA: 5,535 (1.6%)• 1.0% of Monthly

Fixed Rent

• Rank: 9• GLA: 4,497 (1.3%)• 1.1% of Monthly

Fixed Rent

• Rank: 8• GLA: 2,835 (0.8%)• 1.3% of Monthly

Fixed Rent

• Rank: 5• GLA: 13,818

(3.9%)• 1.6% of Monthly

Fixed Rent

• Rank: 6• GLA: 12,655

(3.6%)• 1.6% of Monthly

Fixed Rent

Top 10 tenants account for 25.64% of total GLA and 17.45% of total fixed rent revenues

The Home of the Flagships

14

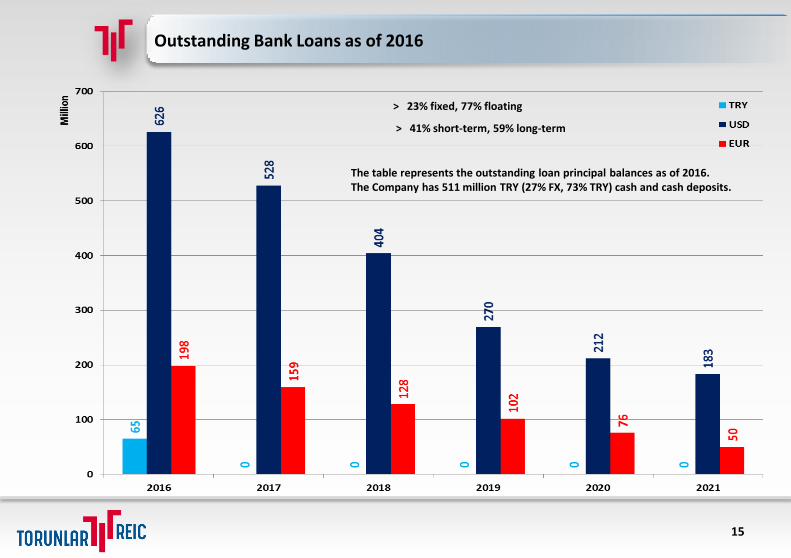

Outstanding Bank Loans as of 2016

15

The table represents the outstanding loan principal balances as of 2016. The Company has 511 million TRY (27% FX, 73% TRY) cash and cash deposits.

> 41% short-term, 59% long-term

> 23% fixed, 77% floating

Project Pipeline – CAPEX (million TRY)

16

CAPEX BudgetActual Spent

to Date2017 2018 2019 2020

MOI 2nd Phase Hotel, Office and Convention Center Project

232.5 81.8 71.1 66.7 12.9

Torun Center 681.7 616.8 37.0 27.9

5. Levent 1,550.4 604.8 538.0 225.1 126.3 56.2

Pasabahce Bosphorus Project 317.5 3.8 105.2 143.9 64.6

Mall of Antalya Project 134.2 85.4 48.8

TOTAL 2,916.3 1,392.7 800.0 463.6 203.8 56.2

Total GLA in Years (m2)

17

Year New GLA (m2) Asset

2017 110,674-Torun Center - Office and retail area-Mall of Antalya

2018 65,000 -Mall of Istanbul 2.Phase Hotel, Office and Convention Center

2019 34,000-Paşabahçe Hotel-Kemankeş Hotel

45

1,9

12

45

1,9

12

56

2,5

86

62

7,5

86

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

2016 2017 2018 2019

110,674

65,000562,586

627,586 34,000

661,586

NAV Evolution (Billion TRY)

18

2020 NAV Breakdown

FUTURE OUTLOOK- 2017 Forecast Income Statement (TRY)

19

(000) TRY 2016 2017F Change

Sales 665,677 1,159,479 74.2%

Residence & Office 243,273 624,978 156.9%

Mall & Office rental 351,652 445,524 26.7%

Other 70,752 88,976 25.8%

Cost of sales (273,417) (475,958) 74.1%

Residence & Office (164,332) (334,814) 103.7%

Mall & Office rental (14,495) (15,000) 3.5%

Other (94,590) (126,145) 33.4%

Gross profit 392,260 683,520 74.3%Gross Margin 58.9% 59.0% 0.02 pp

Gross Margin (Residence & Office) 32.4% 46.4% 13.98 pp

Gross Margin (Mall & Office rental) 74.2% 73.6% -0.58 pp

Opex (48,468) (60,000) 23.8%

General & Admin expenses (39,037) (42,000) 7.6%

Marketing & Selling expenses (9,431) (18,000) 90.9%

Other income (expenses) (1,705) 0 NM

Net gain (loss) fair value adjustments on investment property 1,310,797 700,000 -46.6%

Operating profit 1,652,884 1,323,520 -19.9%

Operating profit excluding fair value adjustment 342,087 623,520 82.3%

Share of profit of associates (recurring) 19,075 22,000 15.3%

EBIT 361,162 645,520 78.7%EBIT margin (%) 54.3% 55.7% 1.42 pp

Depreciation 760 0 NM

EBITDA 361,922 645,520 78.4%EBITDA margin (%) 54.4% 55.7% 1.30 pp

Share of profits (non-recurring) 6,770 10,000 47.7%

Net financial interest income (expense) (69,058) (89,996) 30.3%

Other net financial income (expense) (1,675) 0 NM

Forex gain (loss) (432,895) (160,000) -63.0%

Profit before tax 1,175,101 1,105,524 -5.9%

Corporate tax (2,717) 0 NM

Net profit 1,172,384 1,105,524 -5.7%Net profit margin (%) 176.1% 95.3% -80.77 pp

20

Long Term Sales & EBITDA Forecast (000 TRY)

21

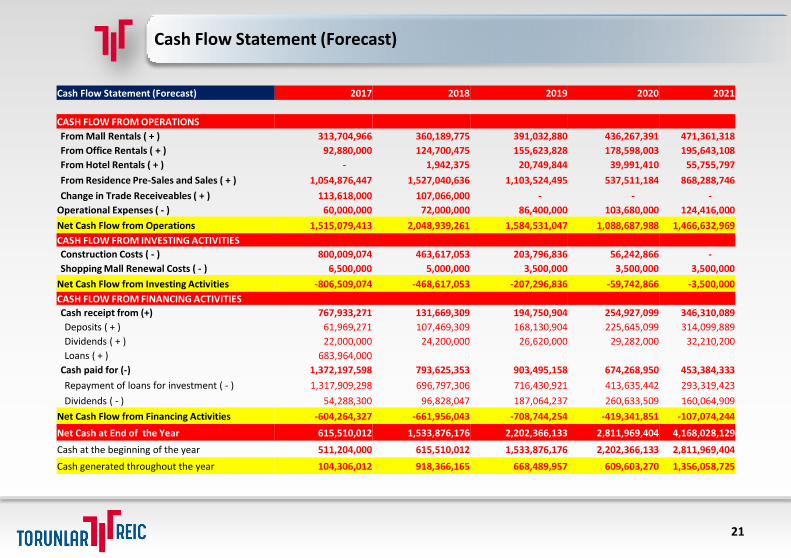

Cash Flow Statement (Forecast)

Cash Flow Statement (Forecast) 2017 2018 2019 2020 2021

CASH FLOW FROM OPERATIONS

From Mall Rentals ( + ) 313,704,966 360,189,775 391,032,880 436,267,391 471,361,318

From Office Rentals ( + ) 92,880,000 124,700,475 155,623,828 178,598,003 195,643,108

From Hotel Rentals ( + ) - 1,942,375 20,749,844 39,991,410 55,755,797

From Residence Pre-Sales and Sales ( + ) 1,054,876,447 1,527,040,636 1,103,524,495 537,511,184 868,288,746

Change in Trade Receiveables ( + ) 113,618,000 107,066,000 - - -

Operational Expenses ( - ) 60,000,000 72,000,000 86,400,000 103,680,000 124,416,000

Net Cash Flow from Operations 1,515,079,413 2,048,939,261 1,584,531,047 1,088,687,988 1,466,632,969

CASH FLOW FROM INVESTING ACTIVITIES

Construction Costs ( - ) 800,009,074 463,617,053 203,796,836 56,242,866 -

Shopping Mall Renewal Costs ( - ) 6,500,000 5,000,000 3,500,000 3,500,000 3,500,000

Net Cash Flow from Investing Activities -806,509,074 -468,617,053 -207,296,836 -59,742,866 -3,500,000

CASH FLOW FROM FINANCING ACTIVITIES

Cash receipt from (+) 767,933,271 131,669,309 194,750,904 254,927,099 346,310,089

Deposits ( + ) 61,969,271 107,469,309 168,130,904 225,645,099 314,099,889

Dividends ( + ) 22,000,000 24,200,000 26,620,000 29,282,000 32,210,200

Loans ( + ) 683,964,000 0 0 0 0

Cash paid for (-) 1,372,197,598 793,625,353 903,495,158 674,268,950 453,384,333

Repayment of loans for investment ( - ) 1,317,909,298 696,797,306 716,430,921 413,635,442 293,319,423

Dividends ( - ) 54,288,300 96,828,047 187,064,237 260,633,509 160,064,909

Net Cash Flow from Financing Activities -604,264,327 -661,956,043 -708,744,254 -419,341,851 -107,074,244

Net Cash at End of the Year 615,510,012 1,533,876,176 2,202,366,133 2,811,969,404 4,168,028,129

Cash at the beginning of the year 511,204,000 615,510,012 1,533,876,176 2,202,366,133 2,811,969,404

Cash generated throughout the year 104,306,012 918,366,165 668,489,957 609,603,270 1,356,058,725

TURKEY REAL ESTATE MARKET REVIEW –Long-Term Demand Forecasts

22

Housing Needs in Turkey, 2014-2020

In millions, except household size 2013 2014e 2015e 2016e 2017e 2018e 2019e 2020e

Population 76.5 77.3 78.2 79.0 79.8 80.6 81.3 82.1

Household size 3.8 3.8 3.8 3.8 3.8 3.8 3.8 3.8

Households 20.1 20.3 20.6 20.8 21.0 21.2 21.4 21.6

New houses needed 0.44 0.44 0.43 0.42 0.41 0.41 0.43

2nd homes and urban transformation 0.37 0.37 0.38 0.37 0.37 0.37 0.37

Foreigners property acquisition 0.01 0.02 0.05 0.05 0.06 0.06 0.06 0.07

Total needed (2015-2020) 5.12

Source: World Bank, TUIK, IMF, HSBC estimates

TURKEY REAL ESTATE MARKET REVIEW –Turkey Residential Sales (in units) (2016)

23

TURKEY REAL ESTATE MARKET REVIEW –Turkey Residential Permits (in units) (2016)

24

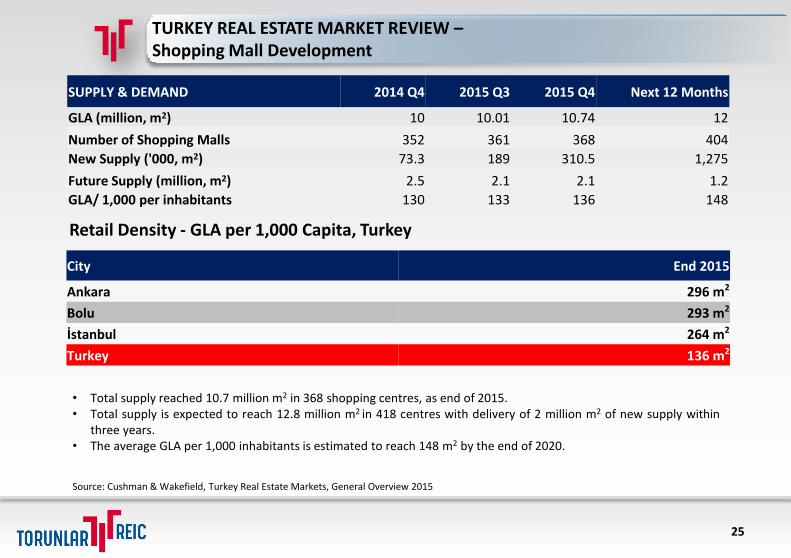

TURKEY REAL ESTATE MARKET REVIEW –Shopping Mall Development

25

Retail Density - GLA per 1,000 Capita, Turkey

Source: Cushman & Wakefield, Turkey Real Estate Markets, General Overview 2015

City End 2015

Ankara 296 m2

Bolu 293 m2

İstanbul 264 m2

Turkey 136 m2

• Total supply reached 10.7 million m2 in 368 shopping centres, as end of 2015.• Total supply is expected to reach 12.8 million m2 in 418 centres with delivery of 2 million m2 of new supply within

three years.• The average GLA per 1,000 inhabitants is estimated to reach 148 m2 by the end of 2020.

SUPPLY & DEMAND 2014 Q4 2015 Q3 2015 Q4 Next 12 Months

GLA (million, m2) 10 10.01 10.74 12

Number of Shopping Malls 352 361 368 404

New Supply ('000, m2) 73.3 189 310.5 1,275

Future Supply (million, m2) 2.5 2.1 2.1 1.2

GLA/ 1,000 per inhabitants 130 133 136 148

TURKEY REAL ESTATE MARKET REVIEW –Turkey’s Mall League

26

Source: Akademetre Research and Eva Real Estate

Mall Opening Date GLA Location Developer

1 Forum Istanbul 2009 178,834 Istanbul Multi Turkmall

2 Mall of Istanbul 2014 154,713 Istanbul Torunlar REIC

3 Marmara Forum 2011 137,500 Istanbul Multi Turkmall

4 Cevahir 2005 110,000 Istanbul Kuwait Investment Authority

5 Vialand 2013 110,000 Istanbul Gursoy & Via Grup

6 ANKAmall 1999 107,804 Ankara Migros / Yeni Gimat REIC

7 Marmara Park 2012 100,000 Istanbul Ece Turkey

8 IstinyePark 2007 88,490 Istanbul Dogus, Orjin

9 Torium 2010 88,455 Istanbul Torunlar REIC

10 Akasya Acibadem 2014 86,500 Istanbul Saf REIC / Akis REIC

11 Anatolium 2010 84,165 Bursa Corio

12 Antares 2007 84,000 Ankara Dolunay

13 Panora 2007 82,591 Ankara Polat Holding

14 Forum Ankara 2008 80,000 Ankara Multi Development TR

15 Kent Park 2008 79,478 Ankara Mega Turk Construction

16 M1 Merkez Adana 2000 76,500 Adana Metro

17 Maltepe Park 2013 75,000 Istanbul CarrefourSA / Ece Turkey

18 Cepa 2007 73,242 Ankara CarrefourSA

19 Korupark 2007 71,267 Bursa Torunlar REIC

20 Forum Mersin 2007 71,125 Mersin Multi Turkmall

21 Anatolium Ankara 2011 70,000 Istanbul Corio

22 M1 Meydan Umraniye 2007 70,000 Istanbul Metro

23 Optimum Outlet 2011 69,000 Adana Ronesans REIC

24 Zorlu Center 2013 66,600 Istanbul Zorlu Real Estate Group

TURKEY REAL ESTATE MARKET REVIEW –Office Market Overview

27

• Total take-up (new leases) was 71,700 m2 in Q4 2015. On annual terms, however, occupational activity volumeswere more or less on par with the results measured in 2014, with over 330,000 m2 of office space contracted.

• Atasehir and Maslak remained the most sought submarkets where the highest new supply volume entered in 2015.• A total of 165,000 m2 of new office space entered the market in Q4 2015, totalling 522,000 m2 for 2015.• Total grade A office supply reached 4.72 million m2, representing a 11% growth (y-o-y).• Total vacancy reached 780,000 m2 with the delivery of new supply and overall vacancy rate slightly increased

compared to Q4 2014 to 16.5%.• While the highest increase in vacancy rates were recorded in Kozyatagi, Kagithane and Maslak, vacancy rates

declined in Kartal-Pendik and Atasehir submarkets.• Total grade A office supply is expected to exceed 5.5 million m2 by the end of 2016, while a total of 1.67 million m2

of new office space is still under construction which is expected to be completed within two years.

Source: Cushman & Wakefield, Turkey Real Estate Markets, General Overview 2015

SUPPLY & DEMAND 2014 Q4 2015 Q3 2015 Q4 Next 12 Months

Total Supply (million, m2) 4.24 4.56 4.72

Total Vacancy (m2) 682,781 767,612 780,717

Vacancy Rate (%) 16 16.8 16.5

Take-up Volume (m2) 122,048 72,120 71,678

Prime Rents (US$/m2/month) 45 45 45

Prime Yields (%) 6.8 6.8 6.8

Future Supply (million, m2) 1.97 1.86 1.67

FINANCIAL STATEMENT - Income Statement

28

(000) TRY Q4 2016 Q4 2015 Change Q3 2016 Q2 2016 Q1 2016

Sales 151,104 299,537 -50% 214,185 170,761 129,627

Residence & Office 45,287 196,778 -77% 108,657 63,878 25,451

Mall & Office rental 88,937 85,061 5% 87,198 88,971 86,546

Other 16,880 17,698 -5% 18,330 17,912 17,630

Cost of sales (59,031) (143,289) -59% (98,400) (73,561) (42,425)

Residence & Office (30,621) (120,241) -75% (70,289) (44,753) (18,669)

Mall & Office rental (3,599) (3,373) 7% (4,106) (3,453) (3,337)

Other (24,811) (19,675) 26% (24,005) (25,355) (20,419)

Gross profit 92,073 156,248 -41% 115,785 97,200 87,202

Gross Margin 60.9% 52.2% 877% 54.1% 56.9% 67.3%

Gross Margin (Residence & Office) 32.4% 38.9% -651% 35.3% 29.9% 26.6%

Gross Margin (Mall & Office rental) 73.2% 77.6% -442% 73.4% 73.0% 77.2%

Opex (17,638) (8,523) 107% (10,680) (13,420) (6,730)

General & Admin exp (15,032) (6,878) 119% (8,306) (10,280) (5,419)

Marketing & Selling exp (2,606) (1,645) 58% (2,374) (3,140) (1,311)

Other income (expenses) (8,012) 829 NM 1,286 2,782 2,239

Net gain (loss) fair value adjustments on investment property 1,191,653 1,001,470 19% 0 119,144 0

Operating profit 1,258,076 1,150,024 9% 106,391 205,706 82,711

Operating profit excluding fair value adjustment 66,423 148,554 -55% 106,391 86,562 82,711

Share of profit of associates (recurring) 0 0 NM 0 13,350 5,725

EBIT 66,423 148,554 -55% 106,391 99,912 88,436

EBIT margin (%) 44.0% 49.6% -564% 49.7% 58.5% 68.2%

Depreciation 157 249 -37% 215 96 292

EBITDA 66,580 148,803 -55% 106,606 100,008 88,728

EBITDA margin (%) 44.1% 49.7% -562% 49.8% 58.6% 68.4%

Share of profits (non-recurring) 5,209 32,799 -84% 6,708 (6,621) 1,474

Net financial interest income (expense) (58,649) (7,865) 646% (8,482) (3,175) 1,248

Other net financial income (expense) (843) 4,693 NM 213 (1,898) 853

Forex gain (loss) (346,731) 150,710 NM (97,384) (32,081) 43,301

Profit before tax 857,062 1,330,361 -36% 7,446 175,281 135,312

Corporate tax (340) (639) -47% (733) (704) (940)

Net profit 856,722 1,329,722 -36% 6,713 174,577 134,372

Net profit margin (%) 567.0% 443.9% 12305% 3.1% 102.2% 103.7%

FINANCIAL STATEMENT - Income Statement

29

(000) TRY 2015 2016 Change

Sales 628,038 665,677 6.0%

Residence & Office 249,687 243,273 -2.6%

Mall & Office rental 309,864 351,652 13.5%

Other 68,487 70,752 3.3%

Cost of sales (250,444) (273,417) 9.2%

Residence & Office (152,924) (164,332) 7.5%

Mall & Office rental (12,306) (14,495) 17.8%

Other (85,214) (94,590) 11.0%

Gross profit 377,594 392,260 3.9%Gross Margin 60.1% 58.9% -1.20 pp

Gross Margin (Residence & Office) 38.8% 32.4% -6.30 pp

Gross Margin (Mall & Office rental) 74.2% 74.2% -0.05 pp

Opex (35,083) (48,468) 38.2%

General & Admin expenses (27,028) (39,037) 44.4%

Marketing & Selling expenses (8,055) (9,431) 17.1%

Other income (expenses) 10,971 (1,705) NM

Net gain (loss) fair value adjustments on investment property 1,001,470 1,310,797 30.9%

Operating profit 1,354,952 1,652,884 22.0%

Operating profit excluding fair value adjustment 353,482 342,087 -3.2%

Share of profit of associates (recurring) 14,392 19,075 32.5%

EBIT 367,874 361,162 -1.8%EBIT margin (%) 58.6% 54.3% -4.32 pp

Depreciation 998 760 -23.8%

EBITDA 368,872 361,922 -1.9%EBITDA margin (%) 58.7% 54.4% -4.37 pp

Share of profits (non-recurring) 35,747 6,770 -81.1%

Net financial interest income (expense) (66,931) (69,058) 3.2%

Other net financial income (expense) (11,175) (1,675) -85.0%

Forex gain (loss) (370,273) (432,895) 16.9%

Profit before tax 956,712 1,175,101 22.8%

Corporate tax (3,108) (2,717) -12.6%

Net profit 953,604 1,172,384 22.9%Net profit margin (%) 151.8% 176.1% 24.28 pp

FINANCIAL STATEMENT - Balance Sheet

30

(000 TRY) 2015 2016 Change

Cash and Cash Equivalents 903,447 511,204 -43.4%

Financial Assets 0 0 NM

Trade & Other Receivables 198,341 206,477 4.1%

Inventory 1,131,546 1,066,462 -5.8%

Prepaid Expenses 100,980 96,466 -4.5%

Other Financial Assets 11,915 1,198 -89.9%

Other Current Assets 2,853 19,475 582.6%

CURRENT ASSETS 2,349,082 1,901,282 -19.1%

Trade Receivables 103,734 70,926 -31.6%

Investment in Associates 321,388 328,158 2.1%

Investment Property 5,751,336 7,753,884 34.8%

Tangible Fixed Property 2,680 2,962 10.5%

Intangible Fixed Assets 553 568 2.7%

Inventory 174,059 137,135 -21.2%

Prepaid Expenses 92,468 91,734 -0.8%

Other Financial Assets 0 0 NM

Other Non-current Assets 67,209 91,031 35.4%

NON-CURRENT ASSETS 6,513,427 8,476,398 30.1%

TOTAL ASSETS 8,862,509 10,377,680 17.1%

ST Financial Liabilities 751,182 144,0966 -75.7%

ST Portion of LT Financial Liabilities 149,170 1,104,235 614.3%

ST Other Financial Liabilities 4,195 4,450 6.1%

Trade Payables 170,227 141,262 -17.0%

Other Payables 15,606 33,420 114.1%

Tax Payables 0 360 NM

Deferred Income 259,735 935,496 260.2%

Others 28,014 23,466 -16.2%

CURRENT LIABILITIES 1,378,129 2,386,785 73.2%

Financial Liabilities 1,905,001 1,798,097 -5.6%

Trade Payables 0 0 NM

Provision For Employment Termination Benefits 749 799 6.7%

Deferred Income 717,542 218,450 -69.6%

NON-CURRENT LIABILITIES 2,623,292 2,017,346 -23.1%

Share Capital 500,000 500,004 0.0%

Share Premium 25,770 25,770 0.0%

Legal Reserves 37,852 53,732 42.0%

Treasury Shares -1,195 -1,195 0.0%

Retained Earnings 3,345,057 4,222,854 26.2%

Net Profit 953,604 1,172,384 22.9%

TOTAL EQUITY 4,861,088 5,973,549 22.9%

TOTAL LIABILITIES AND EQUITY 8,862,509 10,377,680 17.1%

LISTED REIC’s - Torunlar REIC Performance (As of 31.12.2016)

IPO Date (October 2010) = 100

31

Pelin Orsel

Investor Relations / Financial Analyst

Ismail KAZANC

CFO

TORUNLAR REIC (Real Estate Investment Company)Ruzgarlibahce Mah. Ozalp Cikmazi No:4 34805 BeykozIstanbul TURKEYPhone: +90 (216) 425 20 07Fax: +90 (216) 425 59 57

Contacts

This presentation does contain forward-looking statements that reflect the Companymanagement’s current views with respect to certain future events based on the base-caseassumptions. Although it is believed that the expectations reflected in these statements arereasonable, they may be affected by a variety of variables and changes in underlyingassumptions that could cause actual results to differ materially.

Neither Torunlar REIC nor any of its directors, managers or employees nor any other person shallhave any liability whatsoever for any loss arising from the use of this presentation.

Disclaimer