Embed Size (px)

Citation preview

19

90

| 2

01

5

Evolution of an industry over 25 years How the industry went mainstream P6

Separating fiction from reality Challenging hedge fund myths P20

Virtual roundtable of industry leaders Five years yonder... P38

25 Years in Hedge FundsA special publication to mark AIMA's 25th anniversary

Contents

Contributors

4.

IntroductionA global mantra

The international nature of investing, trading and regulation means it has never been more necessary for the hedge fund industry to have a global representative.

By Jack Inglis

6. Then and Now

Evolution of an industry over 25 years

Alternative investments have gone from the periphery ever more towards the

mainstream of the financial world in the past 25 years — and AIMA has played an

increasingly significant role along the way By Neil Wilson

12.

Timeline

14. How the landscape

has changed for hedge funds

The legal and regulatory environment for hedge funds has changed beyond recognition over the course of the

last 25 years By Iain Cullen

Neil Wilson, Wilson WillisNeil was for many years at HedgeFund Intelligence, starting in January 2001 as editor of EuroHedge, and then later becoming managing editor and editorial director for all of the HedgeFund Intelligence publications, which also include AsiaHedge, InvestHedge and Absolute Return, with responsibility for all of their associated online news, special reports and events. He has more than 25 years’ experience in financial journalism and publishing, specialising mainly in derivatives and alternative investments.

Prior to 2001, he was European editor of MAR/Hedge, editor of Futures & Options Week and assistant editor of The Banker. Over the years, he has contributed to various other publications including The Financial Times, The Economist and Risk magazine. He has a BA with honours in Philosophy, Politics and Economics from the University of Oxford.

Iain Cullen, Simmons & Simmons LLP Iain Cullen is a partner in the Financial Services Group at Simmons & Simmons LLP. He joined Simmons & Simmons in 1977, qualified as a solicitor in 1980 (working for the first 18 months in the firm’s Brussels office) and became a partner in 1986. Since 1993 Iain’s practice has concentrated on structuring hedge funds and advising hedge fund managers.

Iain has served as General Counsel of the Alternative Investment Management Association since its foundation in 1990, was Co-Chairman from 1991 − 1995 of the Commodities, Futures and Options Committee of the Section on Business Law of the International Bar Association and is the co-editor of Hedge Funds: Law and Regulation published by Sweet & Maxwell (2001).

Niki Natarajan, In Ink After writing and editing InvestHedge, a publication from HedgeFund Intelligence, for more than 12 years, Niki founded In Ink (London), a company specialising in creative content and communication consultancy. Niki has more than 20 years' experience as a financial journalist, specialising in investment management, with particular expertise of the global funds of hedge funds industry.

Prior to working at HedgeFund Intelligence, Niki launched the hedge fund and securities finance coverage at Financial News. Niki was also the launch editor of Global Fund News; editor of Foreign Exchange Letter; and reporter on Global Money Management, all formerly publications of Institutional Investor's newsletter division. A qualified NLP coach and trained yoga teacher, Niki graduated in Geography from Durham University.

This report was prepared in collaboration with Wilson Willis Management Ltd. Wilson Willis was founded in January 2014 to provide specialised services including analysis, commentary, bespoke research and conferences for the asset management world, with a primary focus on hedge funds.

The views and opinions expressed do not necessarily reflect those of AIMA or the AIMA Membership. AIMA does not accept responsibility for any statements herein. Reproduction of part or all of the contents of this publication is strictly prohibited, unless prior permission is given by AIMA. © The Alternative Investment Management Association Ltd (AIMA) 2015. All rights reserved.

2

20. Separating fiction

from realityDespite plenty of evidence to the contrary,

many myths have grown up about hedge funds during the last quarter-century that

still persist in the popular imagination By Neil Wilson

24.

Learning the lessons of the pastAs the hedge fund industry has evolved since 1990 it has had to learn a series of

important lessons By Niki Natarajan

30.

Accessing hedge funds

How 'solutions' are the new FoHFs

The roles of consultants and funds of hedge funds (FoHFs) have increasingly converged

over the years, with significant ramifications for both fund managers

and investors By Niki Natarajan

34. The next five yearsThere is a wealth of research from recent surveys and studies looking to the future

— and how hedge funds are likely to continue to grow, but are also grappling with various complex challenges ahead

By Neil Wilson

38. Virtual roundtable

Five years yonder...After 25 years of rapid growth and change

in hedge funds since the foundation of AIMA, a group of leading players from

around the world give their views on the outlook ahead for markets, investors and

the industry Compiled by Neil Wilson

3,000

2,800

2,000

2,200

2,400

2,600

1,800

1,600

1,400

1,200

1,000

AuM

Fund

s

800

600

400

200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20140

10,800

7,920

8,640

9,360

10,080

7,200

6,480

5,760

5,040

4,320

3,600

2,880

2,160

1,440

720

0

Assets $bn Number of funds

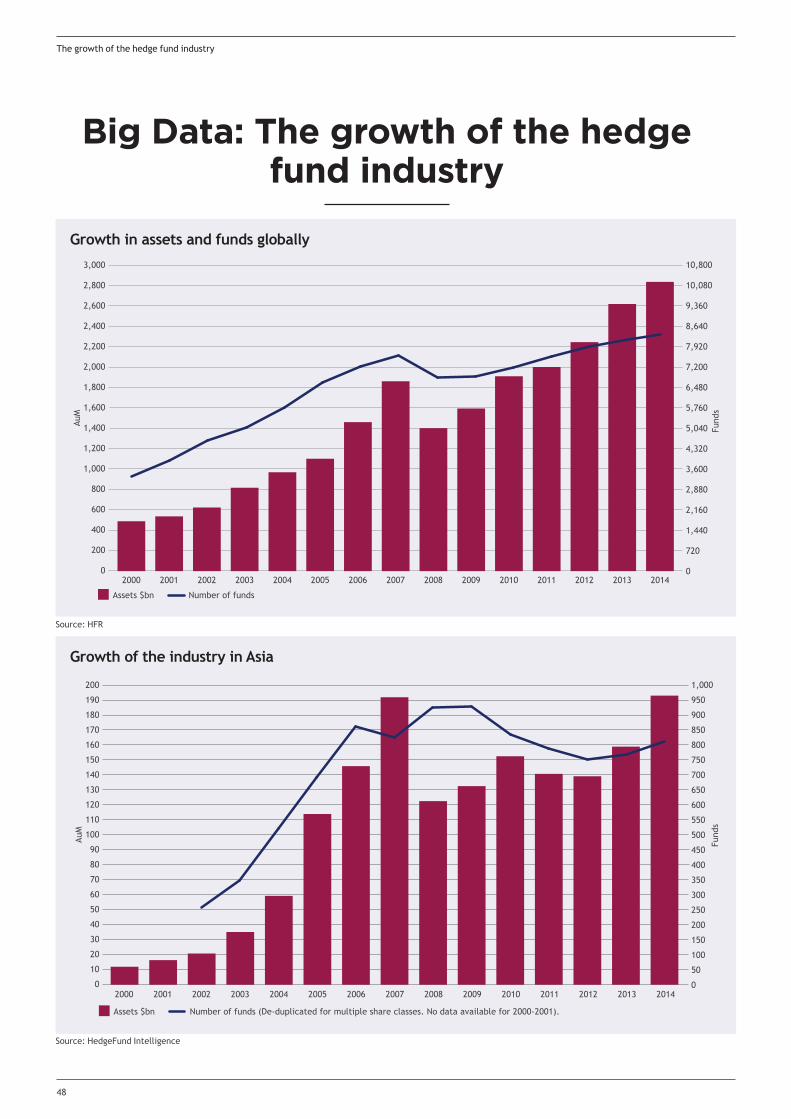

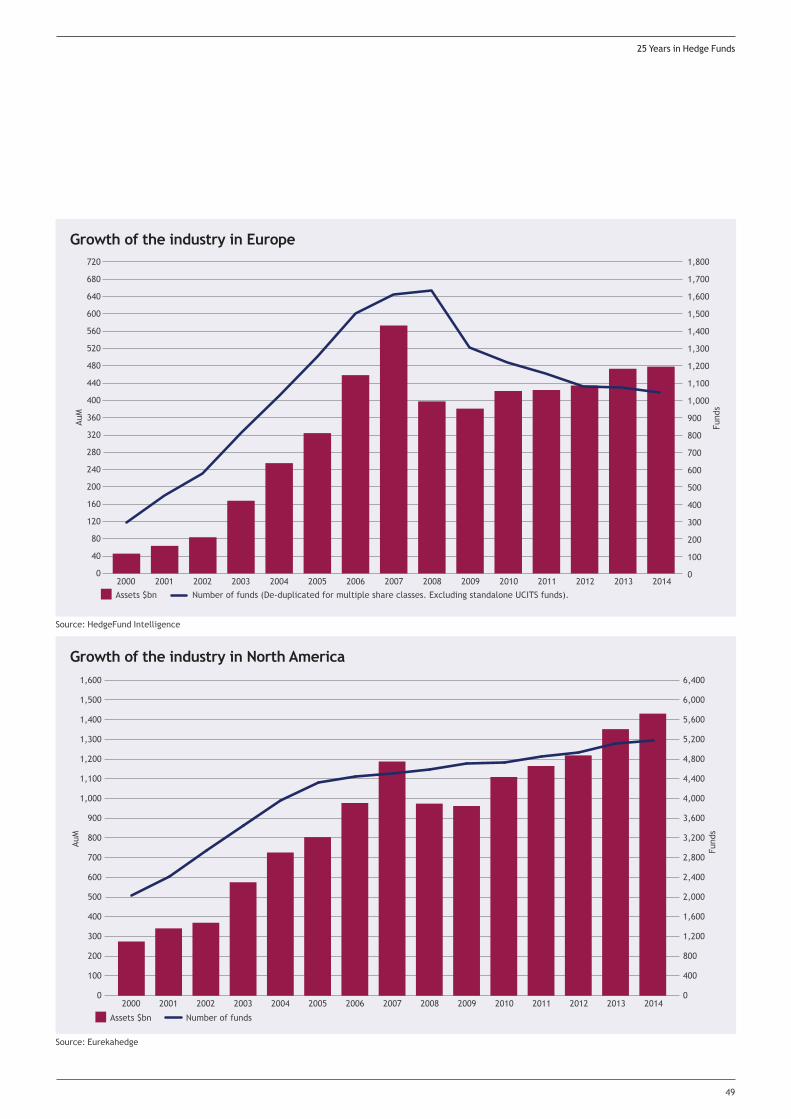

48. Big Data

The growth of the global hedge fund industry

25 Years in Hedge Funds

3

Evolution of an industry over 25 years

I am proud to introduce this special publication to mark the 25th anniversary of AIMA. Founded in Europe in 1990 by fewer than 20 managers and service providers who recognised the need for mutual representation, AIMA has grown into a truly global

organisation, with offices in every region of the world and members in well over 50 countries.

Most financial industry bodies are country and jurisdiction-specific, but ‘global’ has been AIMA’s mantra. The international nature of investing, trading and regulation means it has never been more necessary for the hedge fund industry to have a global representative.

From small European beginnings, an impressive international network encompassing Asia-Pacific, EMEA and the Americas has been constructed. The US has the dominant market share in the industry and represents over 50% of the aggregate AUM of our global membership; our Americas presence is further augmented by the existence of our National Groups in Canada and Cayman as well as our activities in Brazil. In Asia-Pacific, we have National Groups operating in Hong Kong, Singapore, Japan and Australia, combined under a single regionally-focused operation.

The growth of the association in terms of membership and staff reflects the expansion of the industry. In 1990, what was then still very much a boutique sector, managing less than $40 billion in assets, was served by a part-time secretary and volunteers; in 1994 we were still operating out of shared office space in Paris.

As recently as 2005, by which time we had around 900 corporate member firms, and our head office had relocated to London, we still had only eight staff members. Today, we have a total of 38 staff; 25 in the London head office and a further 13 in our representative offices around the world. The industry manages around $3 trillion in assets, much of it on behalf of institutional investors such as pension funds.

Well over 1,500 corporate member firms and almost 10,000 individuals take advantage of AIMA membership.

It is of course our members who are the backbone of the association. They comprise both the largest and smallest firms around the world, all contributing to important output such as responses to regulatory consultations, updates to DDQs and new industry guides. We have more than 70 committees and working groups globally, comprising more than 600 individuals from over 350 firms. It is that support that allows us to continue to deliver all the services our members ask us for; and to undertake, with the help of the members who volunteer their time, all our work on behalf of the industry around the world.

We are hugely grateful to our various sponsor organisations. Our Sponsoring Partner members continue to provide unstinting and important support − Bloomberg, Clifford Chance, Dechert, Deloitte, EY, K&L Gates, KPMG, Macfarlanes, Man, Maples and Calder, Permal, PwC, Simmons & Simmons, Societe Generale, State Street, UBS, Wells Fargo and Willis.

Special thanks are also due to the sponsors of the 25th Anniversary Annual Conference and Dinner, whose advertisements you will see in this publication − Simmons & Simmons, EY and State Street. Iain Cullen of Simmons & Simmons, our General Counsel since inception, provides a wonderfully rich recent history both of the industry and the association within this publication.

How the hedge fund industry has evolved in 25 years is obviously a theme of this publication. The sector has changed substantially in a generation. Challenges and occasional crises as well as tremendous opportunities have punctuated a period marked more broadly by institutionalisation, globalisation and increased regulation. The next 25 years will doubtless see even more change. Ever present will be AIMA, the global hedge fund industry’s representative. •

A global mantra

The international nature of investing, trading and regulation means it has never been more necessary for the hedge fund

industry to have a global representative

Introduction by Jack Inglis, CEO, AIMA

4

AIMA — 25 years in Hedge FundsAIMA expanded into Hong Kong in 1999

Traders in the City of London stop for lunch in this 1991 photograph

Back in 1990, the year of AIMA’s founding, it would be safe to say that both managed futures and hedge funds — indeed, alternative investments in

general — were regarded as somewhat peripheral to the financial markets, very much on the outer fringes of the mainstream financial world.

A lot has changed in the past 25 years. Both hedge funds and managed futures have grown enormously over the intervening years. And AIMA has played an increasingly central role in championing the cause of the industry, developing sound practices and providing a forum for industry practitioners.

Of course, hedge funds and alternative investments were not completely new in 1990. Alfred Jones invented what was generally regarded as the first modern hedge fund — a fund with the ability to use leverage and to go short as well as long — way back in 1949. And the first notable boom in hedge funds had occurred in the US back in the early 1970s.

That first wave of funds was largely snuffed out by the rampant inflation and fierce bear market in equities that followed the oil price

Alternative investments have gone from the periphery ever more towards the mainstream of the financial world in the past 25 years

By Neil Wilson

Evolution of an industry over 25 years

Thenand

now

7

25 Years in Hedge Funds

shocks of that decade. But by 1990, there were still a few hardy survivors of the early period left — including legendary ‘global macro’ players like George Soros, who had survived by making the right macro calls over the years across multiple asset classes; and Julian Robertson’s Tiger group, which had done so too though with a greater focus on equities in particular.

It was no accident, however, that the first group of players who decided to form a trade association were focused on the managed futures space. By the early 1990s, many of the biggest players in alternatives globally were either macro managers like Paul Tudor Jones and Louis Bacon, who had strong roots in commodity futures, or pure commodity trading advisors (CTAs) — operating primarily in the futures markets, often with systematic trend-following strategies.

When EMFA, the forerunner to AIMA, first appeared, it was not clear yet that Europe — and London in particular — would become such a major centre of the nascent industry. But even at that time, there were London-based firms like ED&F Man group that were already thinking a lot bigger. In the early 1990s, seeing a need to source new capacity, Man had the foresight to acquire the UK-based managed futures firm AHL and also spawned a range of further top rank CTAs including Winton Capital and Aspect Capital.

Today, the US remains by far the biggest region for hedge funds by assets under management — with New York by a long way the top single centre, alongside significant clusters in other regions around the country in Connecticut, Massachusetts, Illinois, Texas, California and elsewhere.

London has for many years been the second biggest centre globally. And in the managed futures space, in particular, many of the world’s operators are now based in Europe — and all around the Continent too, including the likes of Transtrend in Rotterdam, Lynx in Stockholm and Capital Fund Management in Paris.

Sterling crisis Arguably, the first time that hedge funds reached the public consciousness, at least in Europe, was in 1992 — when the Bank of England was forced to give up its policy of trying to keep sterling within the European exchange rate mechanism (ERM), the forerunner of the euro. That was not until after the Bank of England had suffered major losses in a failed attempt to keep sterling inside the ERM — and various hedge fund managers, led by Soros, famously made massive profits by betting successfully against it.

While there was much hot air expended by critics at the time — venting about these ‘buccaneering’, ‘upstart’ hedge funds being allowed to humble the stately Bank of England — the resulting exit of sterling from the ERM proved a boon for the UK economy.

Evolution of an industry over 25 years

AIMA was early to establish a presence on the ground in Asia — at a time when feelings were still running high about hedge funds' perceived role in the Asian financial crisis.

During the 1990s, while many CTAs continued to thrive and generally make good returns (not without some volatility), they were gradually over-shadowed by managers investing instead in a long-running bull market in equities. TT International had launched what was widely regarded as the first hedge fund managed in Europe in the late 1980s. And notable early long/short equity managers who emerged in Europe during the early 1990s included Crispin Odey, who launched his first hedge fund in 1992, and John Armitage, who went live with Egerton Capital in 1994.

The pace of development, however, was quite slow in Europe in those early days. In the US, by contrast, the industry was already growing rapidly — and not just in equity-related strategies, but into other areas such as convertible arbitrage, distressed debt and fixed income relative value. It was in the latter strategy area that hedge funds next made big headlines — after the Asia and Russia crises of 1997 and 1998 was followed by the sudden and shocking implosion of Long Term Capital Management.

The huge scale of the leverage deployed by LTCM caused what looked like a potential systemic problem — raising serious questions for the first time that hedge funds were perhaps becoming so big that they could constitute a danger to the whole market. For the first time in 1998, hearings were held in Washington to investigate this notion — with Congress even summoning George Soros to answer for the industry.

At the time, industry representatives were able to argue successfully that LTCM was very much a one-off case — and that hedge funds in general were just too small and too

8

modestly leveraged to pose a genuine systemic risk. But, over the years since, regulators and legislators have continued to be pressed by sceptical or hostile public opinion — re-ignited whenever there has been any significant hedge fund-related ‘blow-up’ or scandal. So 1998 turned out to be just the first in a series of debates about potentially damaging new regulations that have continued all the way through to the present day.

Global reachIt was very timely, therefore, that in 1997 the managed futures-focused and still largely European EMFA evolved to become the broader, and globally-aspiring, AIMA — seeking to represent the increasing community of hedge funds as well as CTAs. The importance of this development was again probably not widely appreciated at the time — given what was still a nascent industry driven by fiercely competitive and independent-minded individuals.

As a breed, hedge fund managers and CTAs have of course always been entrepreneurial, and fiercely competitive among themselves — and hence by nature very hard to rally together behind the same banner.

Yet the new AIMA was not slow to take up the task with enthusiasm. As early as 1997, AIMA was issuing its first due diligence questionnaire. In 2000, AIMA’s first Regulatory Forum was held. And by September 2002, AIMA’s first Guide to Sound Practices had been published. The association was also beginning to expand globally — first into Hong Kong in 1999, and then into Australia and Japan in 2001. Canada, Cayman, Singapore and other locations would gradually follow.

AIMA was early to establish a presence on the ground in Asia — starting at a time when feelings were still running high about hedge funds in many parts of the region following their perceived role in ‘shorting’ various markets during the Asia crisis. In the late 1990s, there were very few funds managed from within the region itself and they were mostly focused on Japan. Over the years since, while assets have waxed and waned in what have often been volatile markets, the ex-Japan markets have grown dramatically — with Hong Kong and Singapore emerging as the leading centres for managers to be based in the region.

Meanwhile, by the late 1990s the industry in Europe was also taking off in a very significant way, with a whole new generation of managers being inspired to leave the institutions where they worked, set up on their own and deploy the most sophisticated asset management techniques to deliver the best risk-adjusted returns.

The LTCM affair — given not least the pedigree of a management team including Nobel laureates — had certainly been a shock when it happened. But in retrospect it looks more like a mere blip — with funds launching at the time finding it more difficult than they had expected to raise capital, but most of them going ahead anyway.

Those launching their first funds during that period — including AQR, Marshall Wace, Viking Global and Lansdowne Partners, and firms like BlueCrest that were leading a new wave of fixed income and macro focused players — have gone on to become some of the biggest names in the global hedge fund industry of today.

This was despite the fact that markets at the time continued to be volatile and

challenging. By 1999, the ‘dotcom bubble’ was in full swing — making it hard for hedge funds, including the growing community of long/short equity managers, to stand out from traditional long-only funds that were riding a raging bull market.

But hedge funds began to look increasingly compelling after the dotcom bubble burst — during the subsequently sharp bear market of 2001 − 2003. While equity markets were plunging 30% and more, hedge funds on average were generally retaining their value — and many individual managers, even in equity strategies, were continuing to produce gains.

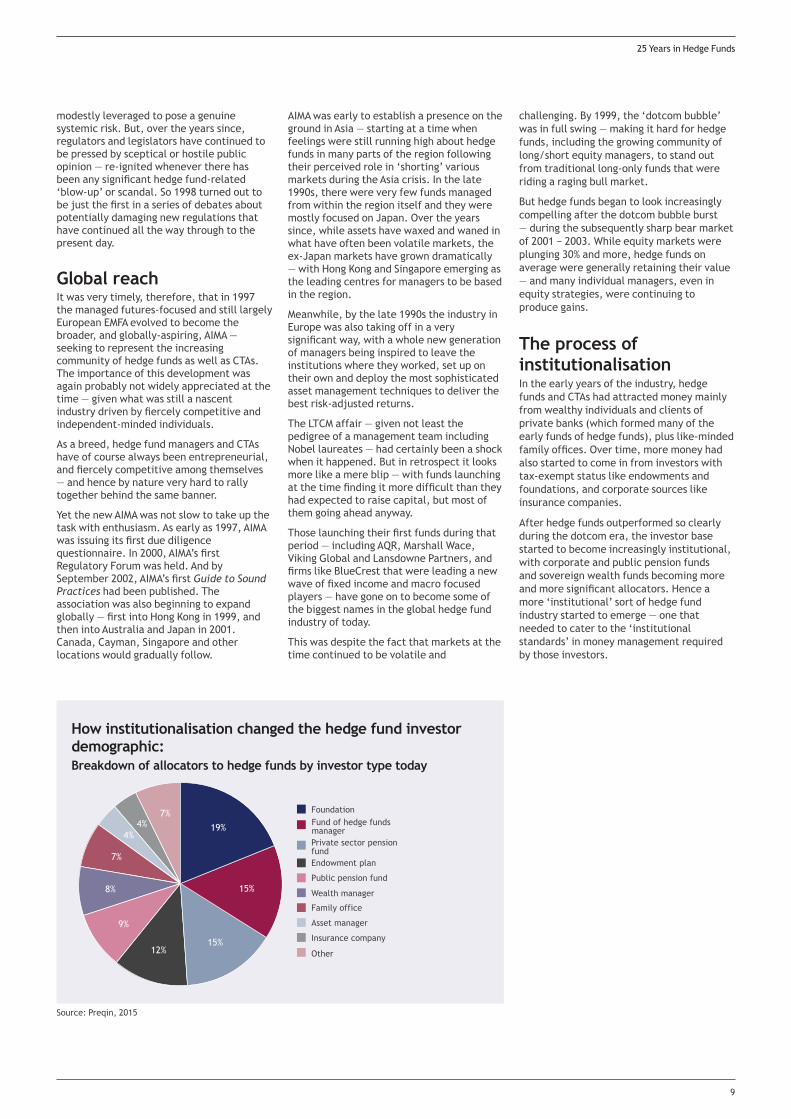

The process of institutionalisation In the early years of the industry, hedge funds and CTAs had attracted money mainly from wealthy individuals and clients of private banks (which formed many of the early funds of hedge funds), plus like-minded family offices. Over time, more money had also started to come in from investors with tax-exempt status like endowments and foundations, and corporate sources like insurance companies.

After hedge funds outperformed so clearly during the dotcom era, the investor base started to become increasingly institutional, with corporate and public pension funds and sovereign wealth funds becoming more and more significant allocators. Hence a more ‘institutional’ sort of hedge fund industry started to emerge — one that needed to cater to the ‘institutional standards’ in money management required by those investors.

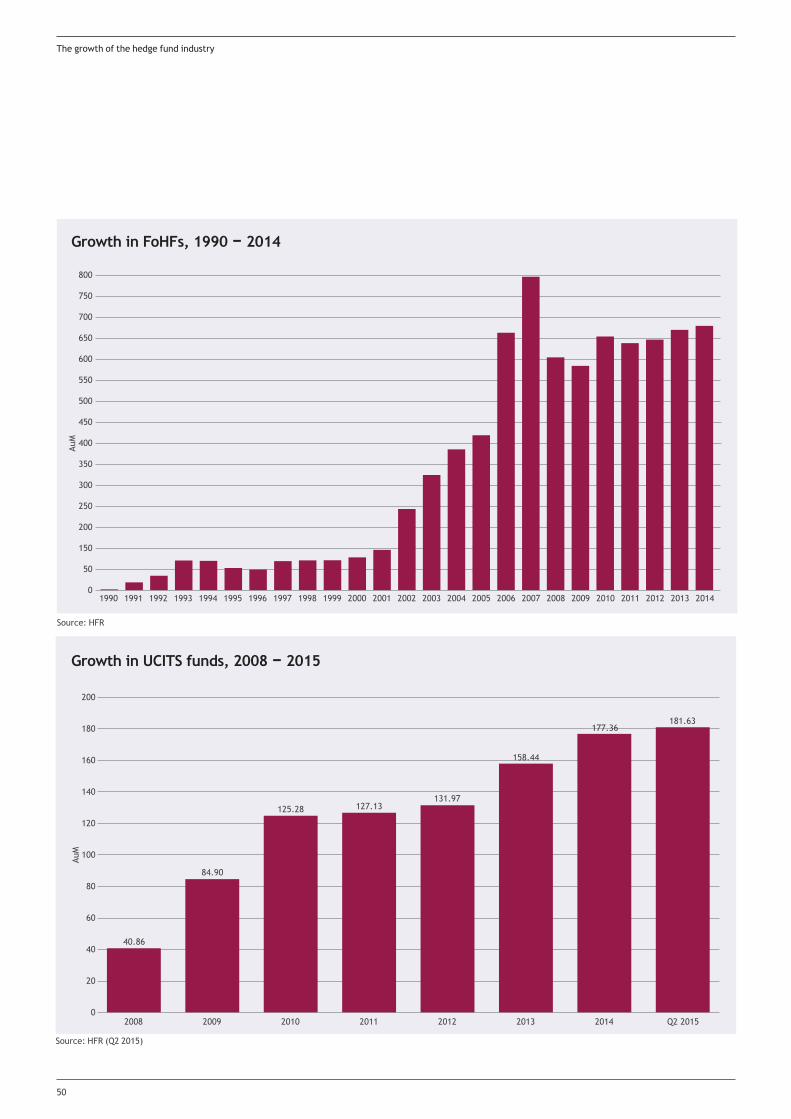

How institutionalisation changed the hedge fund investor demographic: Breakdown of allocators to hedge funds by investor type today

Source: Preqin, 2015

15%

15%

9%

8%

7%

4%4%

7%

12%

19%

FoundationFund of hedge funds managerPrivate sector pension fundEndowment plan

Wealth manager

Family office

Asset manager

Insurance company

Other

Public pension fund

25 Years in Hedge Funds

9

This process of institutionalisation was to continue over a number of years and did not really reach its zenith until after the financial crisis of 2008 — with the assets managed for institutional allocators like pension funds eventually coming to exceed the amount hedge funds managed for their traditional private bank, high net worth and family office type of clientele.

Over the five years just before the crisis, from 2003 − 2007, there was largely a slow and steady rising market in equities, plus a major boom in credit markets — where an increasing number of hedge funds also began to focus. These were conditions in which numbers of players and assets could grow robustly — as indeed they did. In that period, HFI was routinely recording well over 1,000 new hedge fund launches a year.

The combined assets of AIMA’s global membership had reached the $1 trillion mark as early as 2005. And the long-running Hedge Fund Research database put aggregate global assets at a peak of almost $1.9 trillion by 2007, though some other data providers put the number even higher. HedgeFund Intelligence reported assets breaching the $2 trillion level that year — and (albeit very briefly) even exceeding $2.5 trillion just before the financial crisis hit.

As the industry became more institutional during this period, there was an accompanying trend towards more consolidation too — with an increasing number of managers monetising the value of their firms through selling stakes, such as to Petershill, a private equity vehicle managed by Goldman Sachs, or by creating listed vehicles all the way through to full-scale IPOs.

The impact of the financial crisisWith assets growing so robustly, there were however mutterings among investors that overall performance — which had been strong historically — had become increasingly tepid or lacklustre, which was indeed being reflected in the indexes of composite performance as that period wore on. But few investors seemed to be prepared for the sort of aggregate performance that came through after the ‘credit crunch’ of 2007 gave way to the collapse of Lehman Brothers and the full-blown financial crisis of 2008.

Many of the newer investors, in particular, had been sold on the notion that hedge funds were ‘absolute return’ products. And so, somewhat naively perhaps, they were simply not prepared for the eventuality that hedge fund performance in aggregate could be significantly negative — even if there was a complete meltdown of the whole financial system.

In the febrile, panicky conditions of late 2008, the situation was made significantly worse by a virtual tidal wave of redemption requests hitting the industry. This led some

hedge funds to suspend redemptions or ‘gate’ investors — in order to avoid realising massive losses in a collapsing market. At the same time, many other managers were criticised for realising major losses — precisely because they were obliging investors by liquidating assets in a market with no buyers. For many hedge fund managers, it was an invidious position to be in.

In the circumstances, it should have been no surprise that the databases were showing average losses of 15 − 20% for hedge funds in 2008 — although that was of course nothing like as bad as equity market returns at the time. Alongside the simultaneous flood of redemptions, asset levels overall suddenly dropped by 30%.

The Madoff affairThere were further aggravating factors. At the depth of the crisis in December 2008, the wave of redemptions finally caught out Bernie Madoff — who was revealed after many years to have been running a fraudulent ‘Ponzi scheme’. The smattering of fraud cases involving (supposed) hedge funds which had occurred intermittently over the years before were mostly small and obscure cases with minimal impact. But Madoff was truly shocking in its scale — and for the fact that, although Madoff was not strictly a hedge fund manager himself, he had been acting as a sub-adviser running feeder funds or accounts for many investors in the industry.

The Madoff affair took a heavy toll on the fund of hedge funds (FoHF) sector, despite the fact that most FoHF groups had no exposure to him. Research published by InvestHedge showed that only 22 of the top 150 FoHF groups were known to have exposures to Madoff, and the vast majority of the money Madoff had raised had not come via FoHFs but from direct investors, sometimes via feeder funds or managed accounts and even some in onshore structures — on all of which he was reporting bogus returns.

Nevertheless, following the crisis and the Madoff affair, the proportion of assets allocated to the industry via the FoHF sector began to drop — from over 50% before 2008 to around 20% — 25% today.

The recoveryAssets started to recover quite quickly after the crisis — within a year or so after the equity market bottom in March 2009. That was after it became apparent that aggregate hedge fund performance had not in fact been all that bad during the crisis — not when you considered that global equity markets had plummeted 30 − 40%, more than twice as much as hedge funds on average had fallen.

Moreover, while the dispersion in returns across the industry had been enormous

during the crisis, many individual funds had indeed continued to deliver positive returns in 2008 — on some measures up to around 20% — 25% of those trading at the time.

Those who made profits during the period included some huge gains from managers who had called the credit crunch correctly; from some big macro funds; and across the board from CTAs — who once again reaffirmed their non-correlation with average gains of 15 — 20% in 2008, with many of them up considerably more.

As the dust settled on the crisis, and investors began to take these sorts of facts on board, asset levels began to recover — as they have continued to do steadily year after year since 2010. Both the HFR and HFI databases now show global assets surpassing previous peaks and reaching record highs around the $3 trillion level, including a rising proportion in onshore structures like UCITS and 40 Act funds.

Evolution of an industry over 25 years

10

Increased regulationYet the image of the industry — as indeed of the whole financial sector — took a battering during the crisis. With governments (and their taxpayers) in the major economies being asked to borrow hundreds of billions to bail out the banks, it provoked widespread hostility to the financial sector as a whole. If anything, the fact that some hedge funds had correctly diagnosed the mounting problems in the financial sector only seemed to attract greater opprobrium.

Other key facts — such as the reality that hedge funds had not caused the crisis, or that many of them were badly impacted by it — and had never received a penny of bail-out money — were very difficult to get across to the press, the public and the politicians. In such a hostile atmosphere, it was inevitable that pressure would mount on politicians for ‘something to be done’ to address what had caused the crisis — and prevent it from happening again.

Thus, it was critically important that AIMA was there — with a long record of

encouraging good standards in the industry — to fight the industry’s corner, and to prevent the results from being too negative, and perhaps even destroying the industry. Extremely effective campaigns were waged on a variety of fronts particularly in Europe and the US.

The world changed in 2008/9, and with it, AIMA changed too. Following the crisis, the Association built new structures and brought in new people to address the challenges posed by the crisis and the regulatory reforms that followed. Amid a spirit of constructive and proactive engagement, AIMA and the industry achieved significant amendments to proposals that could have threatened the industry’s very existence.

Instead, we have an industry that has been growing again at a good pace of around 10% a year or more since 2009 — though one that looks very different from before. While assets under management have been growing, the numbers of players trading has not — with higher barriers to entry reflected in a falling number of new funds coming through, especially in Europe, and the big

getting bigger, with an increasing concentration of assets among the biggest firms of the Billion Dollar Club. According to HFI figures, these top 400+ firms globally now account for close to $2.5 trillion of the industry’s assets — well over 85% of the total.

Challenges, and risks, remain. The industry today is more global, more institutionalised, and more diverse in terms of investment strategies than it has ever been, even allowing for the consolidation that inevitably has occurred. It remains a source of innovation and entrepreneurialism. It is playing an ever increasing role in the ‘real economy’. Its investors continue to earn significant sums and allocate ever greater shares of that portfolio.

The past 25 years have been instructive, they have been incredibly difficult at times, but ultimately it has been a rewarding period. For the new generation of hedge fund managers, the next 25 years could be yet more exciting.•

25 Years in Hedge Funds

11

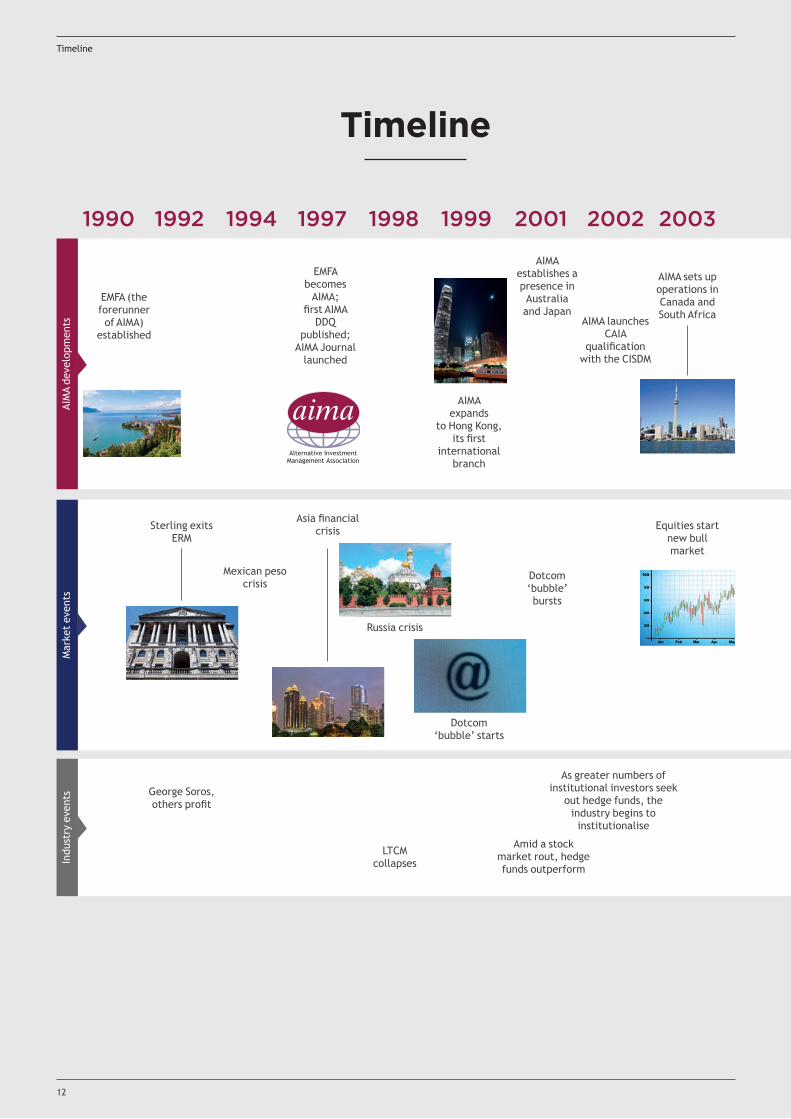

Timeline

1990 20031992 1994 1997 1998 1999 2001 2002

EMFA (the forerunner of AIMA)

established

AIMA sets up operations in Canada and South Africa

EMFA becomes

AIMA; first AIMA

DDQ published;

AIMA Journal launched

AIMA expands

to Hong Kong, its first

international branch

AIMA establishes a presence in Australia and Japan

AIMA launches CAIA

qualification with the CISDM

Sterling exits ERM

Equities start new bull market

Asia financial crisis

Russia crisis

Dotcom ‘bubble’ starts

Dotcom ‘bubble’ bursts

LTCM collapses

Amid a stock market rout, hedge funds outperform

As greater numbers of institutional investors seek

out hedge funds, the industry begins to institutionalise

Mexican peso crisis

George Soros, others profit

AIM

A de

velo

pmen

tsM

arke

t ev

ents

Indu

stry

eve

nts

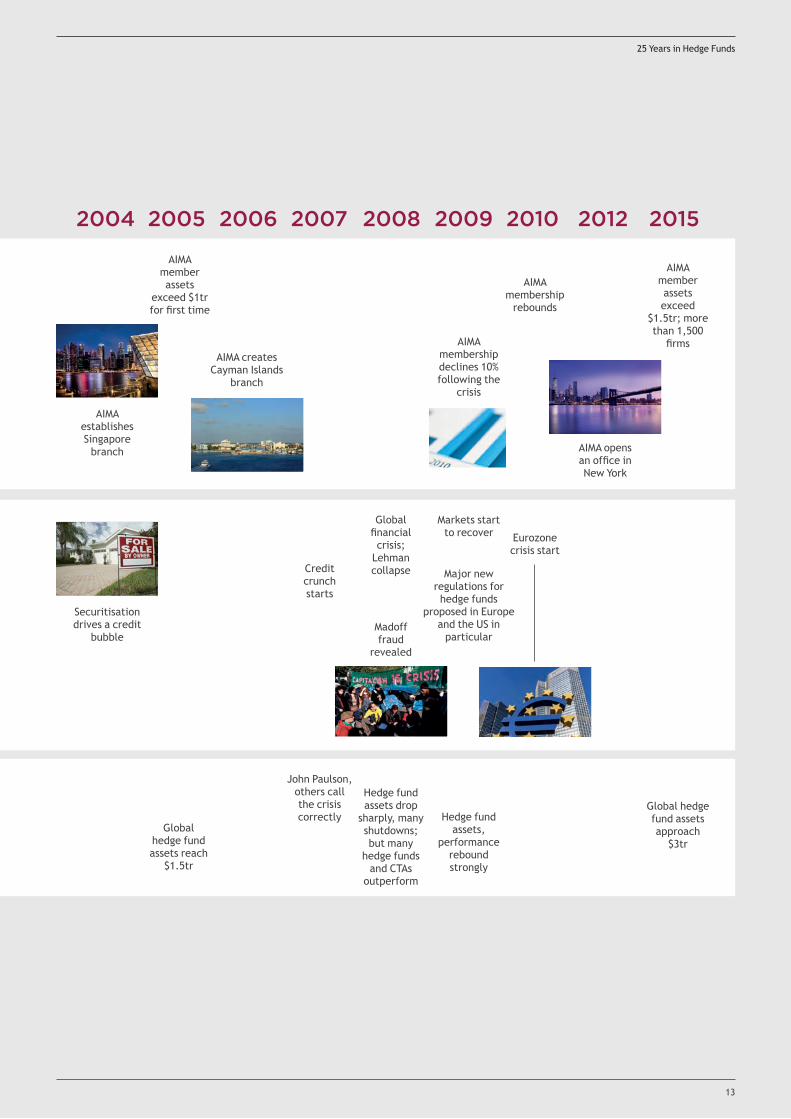

Timeline

12

2004 2005 2006 2007 2008 2009 2010 2012 2015

AIMA establishes Singapore

branch

Securitisation drives a credit

bubble

AIMA creates Cayman Islands

branch

AIMA membership

rebounds

AIMA opens an office in New York

Global hedge fund assets reach

$1.5tr

AIMA member assets

exceed $1tr for first time

Credit crunch starts

Global financial crisis;

Lehman collapse

Markets start to recover Eurozone

crisis start

Major new regulations for hedge funds

proposed in Europe and the US in

particularMadoff fraud

revealed

John Paulson, others call the crisis correctly

Hedge fund assets drop

sharply, many shutdowns; but many

hedge funds and CTAs

outperform

Hedge fund assets,

performance rebound strongly

Global hedge fund assets approach

$3tr

AIMA member assets exceed

$1.5tr; more than 1,500

firmsAIMA membership declines 10% following the

crisis

25 Years in Hedge Funds

13

How the landscape has changed for hedge funds

How the landscape has changed for hedge fundsThe legal and regulatory environment for hedge funds has changed beyond recognition over the course of the last 25 years

By Iain Cullen

14

Little did those of us who sat around the table in a hotel in Montreux Switzerland (some say it was in Lausanne, others Geneva!) in the summer of 1990

imagine that what started out as a fledgling idea of a few individuals involved in various capacities in the managed futures and futures broking business, would grow into an organisation of the size, influence and reach of AIMA.

Reflecting its founders’ affiliations, the association was initially called the European Managed Futures Association (EMFA). Some seven years later, in 1997, in recognition of the evolution of the alternative investment management industry to encompass a much broader range of strategies, EMFA changed its name to the Alternative Investment Management Association (having for a mercifully short intervening period been known as the European derivatives and investMent Funds Association).

From a boutique association for a boutique industry at launch, AIMA has now become a global association for a global industry. When formed, it had between 11 and 17 members (recollections also vary on this!). By 2003 (when the SEC held its first Hedge Fund Roundtable in Washington D.C. which I attended on behalf of AIMA) it had 500 corporate members from 29 countries. When AIMA celebrated its 15th anniversary in 2005, it had 870 corporate members from 46 countries, and now it has in excess of 1500 corporate members based in over 50 countries.

From the legal perspective, the most important development came about due to the growth in the size of AIMA’s membership

Hedge fund manager registration and reporting became mandatory in the US under the Dodd-Frank Act, which was enacted by Congress in the wake of the financial crisis.

15

25 years in Hedge Funds

when, in 2002, AIMA was converted from an association with unlimited liability to a company with limited liability.

Whilst there have been substantial developments in the regulation of hedge fund managers in the 25 years since AIMA’s foundation, the way hedge funds are structured has not changed to the same extent. In the early days, it was common for separate standalone funds to be established for different types of investors, with such funds investing in parallel. This gave rise to the need to rebalance the portfolios of such parallel funds whenever investors subscribed or redeemed therefrom, leading to unnecessary operational complexity. As a result, it became common for such funds to be established as feeder funds into an offshore master fund, such that there was a single portfolio of investments to be managed and thus no requirement for rebalancing.

Similarly, in the early days, where it was desired to offer investors the ability to subscribe for shares denominated in different currencies to reflect investors’ preference for a particular currency exposure, separate offshore funds were established with shares denominated in the desired currencies. This resulted, however, in the existence of additional parallel funds and it was not long before separate classes of shares in a single fund but denominated in different currencies began to be launched.

Around the same time, managers who had been rebating to their partners and employees the management and performance fees charged on shares held by them in their funds, on the basis that it made

no economic sense for them to be paying fees to manage their own money, began to realise that such rebates constituted taxable income in the recipients’ hands. As a result, many funds started to create so-called management shares for partners, employees and, sometimes, family and friends which were identical in all respects to shares issued to investors save that no fees were payable thereon.

In terms of domicile, most offshore corporate funds have always been established in the Cayman Islands, although for largely historic reasons certain managers have established their funds in the BVI. So far as limited partnership funds are concerned, the majority have tended to be established in Delaware although for various reasons in more recent times a sizeable minority have been and continue to be established in the Cayman Islands.

Whilst the dominance of the Cayman Islands has continued, both Ireland and Luxembourg have also attracted a number of hedge funds, usually where the manager wished to target European institutional investors. Such investors are generally considered to prefer, and to some extent are restricted to, investing in funds established in jurisdictions where they are more highly regulated.

Lastly, it is perhaps worth mentioning that there was a time when many new funds sought a listing of their shares on the Irish Stock Exchange which it was thought would assist in marketing the fund to institutional investors. It was also thought a listing might give investors in an offshore fund established in a more lightly regulated jurisdiction, such as the Cayman Islands, a level of comfort

How the landscape has changed for hedge funds

The LTCM debacle in 1998 was the catalyst which led to the world's leading regulatory authorities first seeking to understand what the hedge fund industry was about.

16

Knowing your business

“A dominant presence in the hedge funds market… …They are a top firm and provide excellent service.” Chambers & Partners 2015

Simmons & Simmons has a highly specialised international financial services team. We advise on the full range of domestic and cross-border legal and regulatory issues for market participants on both the sell-side and buy-side.

Together with our award-winning hedge funds practice, the financial services team provides a service specifically tailored to the asset management industry, including a dedicated online resource for start-up hedge funds – Simmons & Simmons LaunchPlus.

To discuss how we can help your business, contact Iain Cullen or your usual contact at Simmons & Simmons.

Iain CullenPartner

T +44 20 7825 4422E [email protected]

simmons-simmons.comelexica.com@SimmonsLLP

As a founding member of AIMA, Simmons & Simmons would like to congratulate AIMA on its 25th anniversary

Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated practices. Simmons & Simmons LLP is a limited liability partnership registered in England & Wales with number OC352713 and with its registered office at CityPoint, One Ropemaker Street, London EC2Y 9SS. It is regulated by the Solicitors Regulation Authority.

that some body (albeit not a regulatory one as such) would have an ongoing oversight role in relation to the fund’s activities under the stock exchange’s continuing obligation rules. In more recent years, however, the number of such listings has substantially decreased.

Although the structure of hedge funds may not have changed much, there have been many changes in the way hedge funds are operated, driven frequently by the demands of an increasingly sophisticated investor base rather than by regulation. These include the appointment of administrators, unaffiliated with the manager, to provide an independent valuation of a fund’s assets, though in this regard the EU Alternative Investment Fund Managers Directive has to some extent turned the clock back as it places the responsibility for valuation on the manager. Another change has been an increased focus on corporate governance which has led increasingly to the appointment to the boards of funds of a majority of independent directors who are unaffiliated with the manager or the fund’s service providers.

LTCM debacle AIMA’s industry views were not always sought or welcomed in the early days by regulators, politicians or the press. It was the LTCM debacle in 1998 that was the catalyst which led to the world’s leading regulatory authorities first seeking to understand what the hedge fund industry was all about. That the willingness to listen to AIMA’s views and those of its membership changed, at least so far as the regulators are concerned, is demonstrated by the willing participation of regulators from the US and Europe at AIMA’s first International Regulatory Forum in 2000. Despite serious concerns about the potential of hedge funds to cause systemic risk, the main consequence of LTCM was that prime brokers began to demand greater portfolio transparency from their clients.

In the years leading up to 2005 when politicians (who can forget the senior German politician’s description of hedge funds as a “swarm of locusts”?), journalists, central bankers, academics and company managements first began to comment on the need for increased regulation of hedge funds, AIMA actively pursued, in line with its objectives, an agenda which involved: educating its members on the benefits of sound practices; publishing its first DDQ in 1997; the first edition of its Guide to Sound Practices for Hedge Fund Managers in September 2002; and in 2005 the first editions of its Offshore Alternative Fund Directors’ Guide and of its Guide to Sound Practices for Hedge Fund Valuation.

The first occasion when regulation was actually mooted was in January 2004 when the European Parliament submitted to the European Commission a proposal for a directive introducing the concept of a sophisticated alternative investment vehicle (the so-called “Purvis Report”). Subsequently

this was quietly dropped; indeed, very few people now recall its existence.

Later the same year, the French Autorité des marchés financiers (AMF) worked with AIMA and the French fund managers’ association on the development of the AMF’s new regulations for French domestic hedge funds, in particular with respect to their relationships with prime brokers. Approximately one year later, in June 2005, the UK Financial Services Authority (FSA), as it then was, issued two discussion papers, the first seeking to assess the risks posed by hedge funds and to identify the risk mitigation steps it would consider taking; and the second seeking views of the investment community in relation to the possibility of permitting wider retail access to hedge funds. Neither of these papers led, however, to any concrete proposals for regulation.

A range of international bodies, including IOSCO, the G8, the Bank for International Settlements, the Bank of England and the Financial Stability Forum (now the Financial Stability Board) amongst others, published pronouncements and reports commenting on the risks posed by hedge funds to financial stability and on ways potentially to mitigate those risks from 2005 onwards, both before and after the 2008 financial crisis. Somewhat surprisingly, whilst the 2008 financial crisis led to developments in fund documentation relating to gates, suspension provisions and side pockets, it did not lead to any immediate changes in regulation, perhaps because there was no evidence that the activities of hedge funds posed any systemic risk.

AIFMD introduced In an effort to head off regulation of the industry, the Hedge Fund Standards Board (HFSB) was established in 2009 by 14 leading hedge fund managers to develop practice standards to be adopted by its members, compliance with which the FSA stated would be taken into account when making supervisory judgements. This was a laudable aim but with hindsight it came too late as, by then, bureaucrats within the European Commission had already begun dreaming up what, in 2009, became the first concrete proposal to regulate the hedge fund industry, namely the proposal for an Alternative Investment Fund Managers Directive (AIFMD).

As General Counsel of AIMA I was privileged to see, and to be allowed to comment on,

early drafts of several provisions of the draft directive and subsequently to lead the AIMA working group commenting on later drafts of the directive published by the European Council, Commission and Parliament, until AIMA’s highly competent Asset Management Regulation team took over the running.

As is now all only too well known, AIFMD, which finally came into force in July 2014, has had a significant impact, and will continue to do so, on the management and marketing in the EU of alternative investment funds such as hedge funds. Most recently this has been reflected in the European Securities and Markets Authority’s advice and opinion on the possible extension of the marketing passport under AIFMD to non-EU alternative investment fund managers and/or alternative investment funds. Looking ahead, AIFMD provides that by 22 July 2017 the European Commission must commence a review of the application of the directive and, if appropriate, make proposals for amendments to it. In other words, AIFMD 2 may be upon us in the not too distant future.

This tour d’horizon would not be complete without an attempt to identify what else the future might hold for hedge funds and their managers. It seems likely that the slowdown that we have seen in the last few years in the formation of new hedge fund managers will not be reversed, at least in Europe, and that new managers will instead continue to join existing platforms. This is because not only are the costs of compliance and of the necessary operational infrastructure unlikely to reduce but also the difficulty of raising assets is unlikely to decline if the institutionalisation of the hedge fund investor base continues. It also seems likely that hedge fund managers which pursue an activist investment strategy will begin to set their sights on European companies despite the perceived difference between the legal regimes in Europe and the US where they have mostly concentrated their efforts to date.

It is also noteworthy that the Financial Stability Board recently announced that it was temporarily shelving plans to designate particular entities, such as hedge funds, as systemically important financial institutions and would instead concentrate on looking at whether certain activities that asset managers undertake are particularly risky. Hot on the heels of that announcement, however, came a statement by Mark Carney, the Governor of the Bank of England, that the Bank was now looking at whether risky activity had migrated from banks to hedge funds such that the Bank might need more power to regulate such funds!

In conclusion, it seems fair to say that, like it or not, the regulatory environment for hedge funds will continue to develop, even if the legal environment does not. •

Who can forget the senior German politician's description of hedge funds as a "swarm of locusts"?

How the landscape has changed for hedge funds

18

19© 2

014

Erns

t & Y

oung

LLP

. All

Righ

ts R

eser

ved.

ED

Non

e.

A global footprint requires a global vision. Follow the leader.

Wherever you are in the world, it’s vital to know your market. We have a broad and deep understanding of the assurance, tax, transaction and advisory needs of asset managers globally. So no matter where you are, we can help guide you.

To find out more, visit ey.com/wealthassetmgmt

Myths about hedge funds

r e a l i t yf i c t i o nDespite plenty of evidence to the contrary, many myths have

grown up about hedge funds during the last quarter-century that still persist in the popular imagination

By Neil Wilson

Separating fiction from reality

Perhaps it is in the nature of the beast. But it is undoubtedly true that a mythology has grown up around hedge funds in the public mind — one that

bears little relation to the actual industry which tens of thousands of people work in every day.

It is in the nature of the beast, arguably, because hedge funds were historically shy of publicity and maintained a very low profile — and hence were slow to challenge the assumption that they were ‘secretive’. Hedge funds were often founded and led by entrepreneurs who felt they had developed some deeper insight into the market which gave them an ‘edge’ — a competitive advantage they were naturally reluctant to disclose.

The fact that certain hedge funds delivered exceptional performance — which made the managers very rich — only served to burnish their mystique, one that many in the industry did little to dispel. So hedge funds started to be seen both as ‘secretive’ and as ‘rich’ — even though the latter is only really true of a few in the very top echelons of the industry. Numerous surveys by recruitment consultants have shown that remuneration for the majority is akin to that of a doctor or lawyer.

There have of course been further factors that made hedge funds an object of suspicion to the wider public — such as that they could go short as well as long, which looked to some sceptics like they were trying to damage certain companies; that they were often domiciled offshore — which looked to others like they had something to hide; and that you only ever heard about them in the news on the odd occasion when there was a ‘blow-up’ or a fraud.

You almost never heard about the many hedge funds going about their jobs quietly and delivering steady, superior risk-adjusted returns. In the public mind, by contrast, hedge funds had developed a somewhat raffish image — one that some managers perhaps embraced with a certain relish, but that the great majority just did not recognise and wanted to challenge.

Over the years, many in the industry have sought to tackle these myths — either individually or collectively through organisations like AIMA — and to produce research that challenges the negative perceptions and shines a light on the many positive ways the industry operates. But it has often proven to be a frustrating task — with continuing preconceptions frequently repeated and reinforced by commentators making it difficult to get key points across to the public and politicians.

Hence the battle to improve the industry’s image has been ongoing for several years now, and with increasing intensity since the financial crisis. With many politicians still seeming to target the industry, it is far from being won yet.

As there are many myths about hedge funds, it is difficult if not impossible to put together a comprehensive or exhaustive list. But there are perhaps three main types, which are to do with:

●● Risk — centring on the accusation that hedge funds are more ‘risky’ than traditional investments, and hence ‘dangerous’ for investors and/or for the markets in general;

●● Ethics — centring on the accusation that hedge funds are ‘bad actors’ in the markets and/or in society generally; and

●● Performance — centring on the accusation that hedge fund performance either isn’t all that good or downright bad; and/or not worth the fees investors pay.

In reality, of course, none of these accusations really stack up — as the various research papers produced by AIMA and others have clearly shown. So, in the ongoing quest to help dispel them, let’s take each area in turn:

20

Common risk-related mythsMyth: Hedge funds are very risky compared to traditional investments

Reality: Hedge funds on average are not more risky either than the markets or than traditional long-only investment funds. Over time, indices show that hedge fund returns on average are higher — and, importantly, with considerably less volatility — even if one takes into account ‘survivorship bias’ (allowing for the disappearance over time of poorer-performing funds from the databases, a factor that affects all types of investment indices, not only hedge fund indices). See more on myths about hedge fund performance below.

Myth: Leverage is too high and/or investments are too illiquid

Reality: Hedge fund leverage varies enormously — depending on market conditions at any particular time and on the type of strategy. In long/short equity, one of the biggest strategy areas, it is usually modest — often varying from one to two-and-a-half times (100% — 250%) of assets under management. In fixed income strategies, it can often be a lot more — say 10-12 times — but that is usually in instruments that themselves have very low volatility (like Treasury securities) and often with a market neutral exposure (equally long and short but of different maturities for instance) rather than leveraged and directional.

The leverage among some other financial businesses such as banks, for instance, is by contrast typically a lot higher — with the size of bank balance sheets being typically 10-20 times bigger than their capital base (and often without taking into account off balance sheet instruments like derivatives).

Not many hedge fund strategies focus on illiquid instruments — which are more usually suited to longer-term investment vehicles

like private equity. Those hedge funds that do invest in such areas, such as specialists in distressed debt, tend to require longer liquidity terms for their investors too — to avoid a potential liquidity mismatch — and usually run with little or no leverage.

Myth: A lot of hedge funds ‘blow up’

Reality: A hedge fund 'blow-up' is where investors lose a substantial portion of their investment. These occur very rarely. Past blow-ups have occurred sometimes due to funds running with too much leverage, as was the case with LTCM in 1998, and/or too much concentrated exposure to positions that became illiquid, such as occurred with Peloton in 2007. But lessons have been learned from such experiences in the past, and risk management across the industry has improved as a result. While many funds may have been shut down over the years after suffering modest losses, blow-ups have become increasingly rare — and of course no hedge fund has ever been bailed out by taxpayers.

The ‘failure’ rate of hedge funds has never been inconsiderable — with up to 10% of funds trading shutting down each year, according to research from HedgeFund Intelligence prior to 2008. But most of those shutting down each year were smaller funds, where the managers were giving up because they could not raise enough assets to make them economic — not because their performance was particularly bad. The shutdown rate did spike a little during and just after the extreme conditions of the financial crisis in 2008, but has since dropped again to well below 10% a year.

Myth: Hedge funds cause systemic risk

Reality: Very few funds operate with large enough assets under management and with sufficient leverage to make their potential failure an issue of systemic concern to regulators. Since the financial crisis, studies by regulators have consistently confirmed

this. The problem of “too big to fail” does not affect hedge funds. Unlike banks, hedge funds are considered “safe to fail” by academics and many policymakers.

Common ethics-related mythsMyth: Hedge funds are self-serving and don't contribute to society

Reality: Hedge funds manage money for the public — not to bet against it. The majority of assets under management in the industry are managed on behalf of average citizens — often via their pension funds — as well as for sovereign wealth funds, endowments, foundations, family offices and other sorts of private investors. Surveys have shown for several years that well over 50% of assets in hedge funds are managed for institutional investors.

Myth: They are secretive/opaque

Reality: Many hedge funds may indeed be protective of the intellectual property which is at the basis of their returns. But most are not so secretive as may have been the case in the early days of the industry. Today, hedge funds are far from unregulated — and are indeed required to be registered and to report positions regularly in major jurisdictions (i.e. on a quarterly basis to the SEC on securities held in the United States). The vast majority of hedge funds also now routinely report their monthly returns to one or more of the industry databases.

Myth: They are run by and for only the rich

Myth: They avoid tax

Reality: Hedge funds around the world employ a significant number of people in the financial sector — over 300,000, according to AIMA research. And they are often in high-skilled jobs — which can generate significant tax revenues in jurisdictions like the US, UK, Canada, Australia, Japan, Singapore and

Dollar value of the hedge fund industry's historic returns to investors

Note The estimates contained in the above table and this report are based upon the Hedge Fund Research Database, which tracks the hedge fund industry (including funds of hedge funds). The majority of fund information in the Database is distributed to Hedge Fund Research subscribers, with permission of the fund managers. Funds that decline to be included in the distributed hedge fund database are tracked internally by Hedge Fund Research. Asset size and performance for a subset of internally-tracked funds are determined by internal company estimates and a variety of other sources. In order to arrive at the total assets and asset flows by strategy, Hedge Fund Research uses total assets from all funds contained in the Hedge Fund Research Database as well as all funds tracked internally. Funds of funds are not included in the overall Industry estimates to avoid double-counting. Funds in the Hedge Fund Research Database submit assets under management consistent with conventional reporting methods which specify investor capital under management, net performance fees.

Year Net asset flows ($bn)

Performance-based AUM change ($bn)

2005 $46.9 $85.9

2006 $126.5 $232.7

2007 $194.5 $209.4

2008 ($154.5) ($306.9)

2009 ($131.2) $324.2

2010 $55.5 $261.8

2011 $70.6 $20.1

2012 $34.4 $209.9

2013 $63.7 $312.2

2014 $76.4 $140.3

Total change since 2005 $382.9 $1,489.5

Source: Hedge Fund Research

25 Years in Hedge Funds

21

Hong Kong, where many management firms are located. AIMA estimates that the total tax take for governments worldwide runs into the tens of billions each year; in the UK alone AIMA estimates annual tax revenues from hedge fund firms and professionals amount to some £4 billion ($6 billion).

As with other successful sectors that generate considerable wealth, such as technology, hedge funds have also become massive contributors to charitable causes — both individually, through foundations that they have created, and collectively through industry-wide charities.

Myth: Hedge funds have no economic value or are bad for markets and other investors

Myth: Short selling has a negative impact/‘irresponsible’ shorting causes problems in markets

Reality: Short selling is a perfectly legitimate activity. It is facilitated via the securities lending market — where owners of securities make them available to borrow (for a fee). This helps narrow bid/offer spreads and improves liquidity, making the market more efficient, less volatile and hence more attractive to all sorts of participants.

For hedge funds, the ability to go short is the main means by which they are able to hedge — to reduce the risk and volatility of their overall portfolio and to hold long positions with greater confidence — as well as to make specific bets that the prices of certain individual securities they believe are over-valued are likely to fall.

Short selling activity is unlikely to exacerbate a crisis or panic situation in the market — because, when prices are falling fast, borrowing stock becomes typically much more expensive if not very difficult or

impossible to execute. Hedge funds are only likely to profit in such a situation if they had put the short positions on long before prices started to fall.

With the ability to go short as well as long, hedge funds are in fact well placed to help the markets puncture speculative ‘bubbles’ that can and do occur, as they will tend to short securities that they believe are getting over-valued.

Similarly, when prices are declining, hedge funds with open short positons are often the only natural buyers in the market at that time — when ‘long-only’ investors are more likely to be selling — and so can effectively create a buffer against a falling market turning into a complete collapse. In practice, to realise profits on short positions, hedge funds need to be ‘buying back’ — at lower prices than they had previously sold.

Myth: Hedge funds were responsible for the financial crisis/crash

Reality: Hedge funds were not responsible for the financial crisis. The crisis was created by irresponsible lending in the banking sector, encouraged by the easy ability of banks (in the pre-crisis period) to create and then securitise ‘toxic’ loans in areas like US sub-prime mortgages. Some hedge funds were indeed among the first to identify that these loans were toxic and to go short of them, realising enormous gains. But the vast majority of hedge funds, which do not focus on the credit sector, were negatively impacted — just like most other types of businesses — when the entire banking system threatened to implode.

Certain hedge funds may have shorted certain bank stocks during the financial crisis. But hedge funds being short was not

the reason why those banks failed or had to be bailed out — that was simply due to the scale of the losses the banks had incurred.

Myth: Activist funds are just in it for themselves

Reality: Certain types of hedge funds have been singled out for causing a negative impact on markets or society — including ‘activist’ funds which encourage companies to enhance shareholder value. But plenty of research (including a 2015 report by AIMA) shows that their impact has generally been positive — on individual companies and the wider economy.

Myth: Hedge funds are not long-term investors

Reality: While some hedge fund strategies involve a large amount of short-term trading, others — including many activists and distressed debt investors — involve a much more long-term approach.

Common performance-related mythsMyth: Returns are not all they are cracked up to be/are poor or really bad

Myth: Returns are very good — but only for the rich

Myth: Assets are falling because performance isn’t good

Reality: As highlighted above, overall hedge fund performance over time has been considerably better than the returns in equity markets — and with considerably less volatility — even allowing for ‘survivorship bias’ (the disappearance over time of poorer performing funds from the databases, a factor that is also present in equity indices).

Hedge funds are not 'riskier' than traditional asset classes: Comparison of annualised volatility of hedge funds, S&P 500 and global bonds

0.0%

6.0%

4.0%

2.0%

8.0%

10.0%

16.0%

14.0%

12.0%

Annu

alis

ed v

olat

ility

3.9%

9.1%

HFRIFWC

S&P 500

BarclaysGA ex-USD

3 Year (Jan 2012− Dec 2014)

5.5%

5 Year (Jan 2010− Dec 2014)

HFRIFWC

S&P 500

BarclaysGA ex-USD

5.2%

13.0%

7.2%

10 Year (Jan 2005− Dec 2014)

HFRIFWC

S&P 500

BarclaysGA ex-USD

6.3%

14.7%

8.1%

20 Year (Jan 1995− Dec 2014)

HFRIFWC

S&P 500

BarclaysGA ex-USD

7.0%

8.2%

15.1%

Source: HFR, Barclays, AIMA research

Myths about hedge funds

22

This outperformance has been most pronounced during periods when equity markets have fallen sharply — such as during the ‘dotcom’ bust of 2000-2003 and during the financial crisis of 2008, when even though hedge funds on average may have produced negative returns they were still well ahead of the losses in equity markets.

Certain commentators have argued that net returns from hedge funds over time — after allowing for fees — have been negligible, which may have appeared to be the case for some investors immediately after the sharp drop of 2008. But such contentions have not stood up to more rigorous scrutiny.

Over shorter time frames, hedge fund performance has indeed sometimes lagged equities — most often during periods when there have been sharp rallies or strong bull market trends. Over other shortish timeframes, sometimes running to multi-year periods in gently rising markets, hedge fund return correlations have sometimes risen too — but the correlation has usually dropped whenever volatility spiked again.

There have been various sources of confusion in the debate about hedge fund returns. For one thing, the composition of the various hedge fund indices vary considerably, which can result

in them showing rather different returns over the same time series. This partly reflects the fact that hedge fund returns, even with the same strategy area, vary considerably — with considerable dispersion among the individual funds. Many of the indices focus on a simple median of the funds included — not allowing for any skew in the distribution of returns, which can often be to the high side of the median (i.e. with a significant minority outperforming by a wide margin).

Another common problem is a widespread misperception that hedge funds are an asset class — like equities or bonds — and this misleading notion has still only been partially dispelled over time. Hedge funds are not an asset class. Rather, they adopt a range of strategies with varying approaches — including the use of long and short positions and leverage — across a range of different asset classes. Hence it does not really make a great deal of sense to compare hedge fund returns in general against equity indices. It makes more sense to compare equity hedge fund returns against equities, fixed income hedge funds against bonds and so on.

For strategies which trade across a range of asset classes — such as global macro or managed futures — it probably makes more sense to compare those only against the risk-free interest rate in the relevant currency. Judged by that more appropriate yardstick, the outperformance of those funds has been considerable over many years.

It is not surprising, therefore, that hedge fund assets have risen strongly over the years — apart from the sharp drop of 2008, since when they have been rising again at a rate if more than 10% a year. Investors would not be putting so much more money in if the performance was indeed disappointing. •

0%

-200%

1000%

800%

600%

400%

200%

1173%

906%

403%

349%

1200%

1400%

HFRI Fund Weighted Composite IndexMSCI World (Local Currency TR)

S&P 500 (TR)Barclays Global Agg (TR USD UNH)

Jan-

90Ja

n-91

Jan-

92Ja

n-93

Jan-

94Ja

n-95

Jan-

96Ja

n-97

Jan-

98Ja

n-00

Jan-

01Ja

n-02

Jan-

03Ja

n-04

Jan-

05Ja

n-06

Jan-

07Ja

n-08

Jan-

09Ja

n-10

Jan-

11Ja

n-12

Jan-

13Ja

n-14

Jan-

15Hedge funds beat the traditional asset classes: Hedge funds versus main asset class cumulative returns (1990 − 2015)

For more detailed evidence, take a look at the following reports on the AIMA website:

• Financing the Economy — The Role of Alternative Asset Managers in the Non-Bank Lending Environment — AIMA, May 2015

• Tax Paid by the UK Hedge Fund Industry at Record Levels — AIMA research, February 2015

• Unlocking Value — The Role of Activist Alternative Investment Managers — AIMA, February 2015

• The Way Ahead — Helping trustees navigate the hedge fund sector — AIMA/CAIA, January 2015

• Capital Markets and Economic Growth — Long-Term Trends and Policy Challenges — AIMA, May 2014

• Apples and Apples — How to Better Understand Hedge Fund Performance — AIMA, April 2014

• Contributing to Communities — AIMA Review of Hedge Fund Charitable Activities — May 2013

• The Value of the Hedge Fund Industry to Investors, Markets and Broader Economy — AIMA, April 2012

• The Value of the Hedge Fund Industry to Investors, Markets and Broader Economy — AIMA, April 2012

• No hedge fund today should be deemed systemically important — AIMA statement, July 2011

• Global Hedge Fund Industry employs 300,000 — AIMA research, December 2010

25 Years in Hedge Funds

23

Learning the lessons from

the pastAs the hedge fund industry has evolved since 1990 it has had to

learn a series of important lessons

By Niki Natarajan

Confucius said, "Study the past, if you would divine the future". If he was right, then what should we study to prepare for the future? Are there lessons the long-only world can teach the hedge fund industry as it enters a new ‘retail’ era with liquid

alternatives? What feedback can the hedge fund industry use from ‘failures’ such as Long Term Capital Management, Bear Stearns, Bernard Madoff and Amaranth Advisors, among others, as it moves forward?

Regulators are working overtime trying to interpret their solutions to many of the ‘lessons’ that the various credit crunches, liquidity

mismatches and counterparty risks, to name but a few, have taught us, to make banking and investing more ‘safe’ for investors.

But might their zeal to avoid the past be creating problems in the future? Is the availability heuristic—a behavioural bias that relies on using only the most readily available information to make decisions about the future—driving decisions without considering that there might be data further back in the archives?

What are the top 10 lessons from the last 25 years, and has the industry learned them?

Learning the lessons from the past

24

25

Temple of Confucius

Learning the lessons from the past

Lesson 1 Liquidity —

available in theory, but is it there in practice?

Selling is often harder than buying. In the past, liquidity mismatching in portfolios was too often overlooked — that was, until the aftermath of it drying up. Today, the mantra is liquidity, liquidity, liquidity, and yet precious returns can of course be lost if that liquidity is not really required.

As underlying strategies are applied to more liquid onshore structures, often via the use of derivatives, an important question to ask is: ‘In the event of needing it, will it be available?’

Roger Lowenstein, author of When Genius Failed, and of an essay in The New York Times September 2008 entitled: Long Term Capital: It’s a Short-Term Memory, has pointed out that it may not be. “The belief that one can get safely out of a ‘liquid’ market is one of the great fallacies of investing,” he wrote.

Few thought that after the crisis involving Long Term Capital Management (LTCM) in 1998, liquidity could dry up again so fast. And yet it has done time and again, resulting for instance in the near-collapse of Bear Stearns in 2008. The investment bank, which was eventually bought by JP Morgan, got caught out in a supposedly liquid market in sub-prime mortgage investments and the notice of bankruptcy of its two funds investing in these strategies may have been a catalyst for the financial crisis. Ensuring the strategy’s liquidity requirements and liquidity of the wrapper are carefully matched is what is essential, in particular as the industry heads into a new era of ‘liquid alternatives’.

Lesson 2 Derivatives — friend or foe?

One operative word linking LTCM and Bear Stearns is derivatives. Derivatives enable users to find new ways to re-package old structures, such as debt and mortgages, to provide ‘solutions’ to challenges that clients present.

When looking closely at how a sudden loss of liquidity hit both LTCM and Bear Stearns, it is important to highlight that the issue was less the assets they traded, but their reliance on off-balance sheet derivatives as a way to trade them.

Today there are two industry shifts that are likely to see the increased use of derivatives. The first is the UCITS revolution that allows hedge fund strategies to fit into a liquid wrapper — where, in many cases, derivatives are being used to achieve this. And the second is the regulators’ recent and ongoing moves to deleverage the system.

New regulations such as Basel III are forcing banks to be more parsimonious with their exposures both on and off balance sheet — and hence be more selective as to which hedge funds they finance. Hedge funds that cannot get financing through the traditional channels may have to look at new synthetic financing via derivatives to structure their trades.

The lesson of previous crises is that derivatives of course cannot really remove risk, but rather allow for the transformation of where risk resides. Investors need to pay attention to where the risk really is.

Lesson 3 Leverage — Hedge funds may have to get by with less

Leverage was one of the factors allowing hedge funds to post outsized returns in the past. Regulation and low interest rates have now conspired to reduce leverage and credit to support such trading strategies of the past.

Bubbles occur when credit is easy to obtain — so regulators globally are now on a mission to make sure that banks and hedge funds are more constrained in terms of their borrowing. In the short term, the new regulations they have been pushing through are likely to stymie returns from some hedge fund strategies. But in the long term it is more than likely that savvy hedge funds will find alternative sources of funding, such as through so-called shadow banking or synthetic financing.

Again investors need to ask: Will the next set of financing innovations potentially bring with them a new set of unintended consequences?

26

Lesson 4 Transparency — now you have it, but do you understand it?

Thanks to a number of factors including the institutionalisation of the industry and even the Madoff affair, the hedge fund industry has recognised the importance of transparency. For many investors today, third party managed account platforms are no longer a luxury item but an essential business tool.

Few now buy hedge funds without knowing that they get plenty of transparency on what is in the portfolio, but answering questions like: ‘what information do you want?’; ‘how often do you need it?’; ‘what format would you like it in?’; and ’how do you intend to use it?’ is a different story.

One of the greatest liabilities an investor has today is having the transparency but not doing anything with it — or not really knowing what to do with it.

Lesson 5 Diversification — how correlated are you still?

In the early 1990s, more investors moved from balanced to specialist investing, and in doing so they ‘diversified’ into Japan, emerging markets, US and other ‘exotic’ markets — mainly or all through equities. So when the global stock markets crashed in 1997 in the aftermath of the Asian crisis, many discovered they were not so diversified after all.

A similar thing happened during the financial crisis. Many investors that thought they were diversified because of their hedge fund holdings only to discover too late that those holdings had become highly correlated during panic selling of all stocks in the stressed market.

Whether it is avoiding an over-concentration in stocks from banks and financial institutions, as many investors had going into the financial crisis, or not being simply in one hedge fund into which all the ‘alternatives’ allocation was investing in, genuine diversification across asset classes and across providers continues to be one of the most important investment lessons to remember.

The crisis highlighted that diversification alone cannot save a portfolio. Low correlation between assets held is key to capital preservation.

Lesson 6 Key allocator risk — don’t forget consultant risk

Hedge funds have always known about the importance of diversifying their client base. Indeed there are more than one or two managers who will remember their single largest investor pulling their allocation, resulting in their fund’s closure.

Few, however, will have made this connection with consultants. This is a lesson that any hedge fund manager that has been removed from a consultant's buy list can attest to.

When a consultant takes a hedge fund off its buy list, rapid inflows can turn to rapid outflows almost overnight. As the hedge fund industry becomes reliant on the consulting community for institutional inflows, increasingly consultant risk is a lesson in waiting.

25 Years in Hedge Funds

27

Lesson 7 Ongoing due diligence — never skimp on it

From an investor point of view, due diligence is like the right fuel for a car, essential to get right all the time. Without it, or with the wrong kind, the car won’t run.

In the hedge fund space, where alpha is mercurial and profitable traders thrive on loopholes, a park-and-play attitude to investing can land investors in hot water. A number of funds of funds and one consultant found this out the hard way in the case of Amaranth Advisors: Rocaton Investment Advisors, an investment consultant, ended up paying $2.75 million to San Diego County Employees’ Retirement Association for recommending Amaranth.

Diversification across hedge funds helped those FoHFs with exposure on a performance basis, but not necessarily on a reputational basis. As more and more allocators buy hedge funds directly, and in many cases put lots of eggs in one basket, ongoing due diligence is going to be key to avoid investment-related mishaps.

Lesson 8 Risk management — is it more than just risk reporting?

“The market can stay irrational longer than you can stay solvent” — as said John Maynard Keynes. Risk management is about knowing when to cut positions (or add to them), it is not about avoiding risk.