Embed Size (px)

Citation preview

© Take Charge Today – August 2013 – Choosing to Save – Page 1 Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Ins tute at The University of Arizona

2.4.1.F1

Choose to Save Advanced Level

Saving money is an essen al part your financial plan. When you save you accumulate funds by inten onally

spending less than you earn. Savings is the por on of income not spent on consump on (the purchase of goods

and services).

An important reason to have savings is for emergency expenses. Without savings, paying cash for an unexpected

expense may be difficult. Emergency savings (cash set aside to cover the cost of unexpected events) creates a

sense of financial security. The lack of an emergency fund not only creates financial stress, but also drives the

consumer into debt.

Savings contributes to your net worth (wealth) and is recorded as a financial asset on your Statement of Financial

Posi on. Be sure this financial asset (your emergency fund) is in an “easily‐accessible” account (usually a savings

account) that can be accessed in a day or two without penalty. Financial assets easily converted into cash are called

liquid. Liquidity is defined as how quickly and easily you can access your assets and convert them into cash.

How much money to save

Most experts recommend having between 3‐6 months of expenses put aside in emergency savings. Let’s say your

goal is to save six months of expenses. If you normally have $2,000 in expenses each month then you should try

to build up a total of $12,000 in emergency savings. Be careful

not to confuse the funds you’ve saved for emergencies with

funds you’d like to spend on vaca ons with friends and family or

on big expenses like a new flat screen TV or newer furniture.

Emergency funds are just that; funds set aside only to be used in

an emergency!

How to save money

Saving is an important part of se ng and reaching financial goals. Your

goal may be to build your emergency savings fund or to buy a car, new

furniture or the down payment on your first home. You begin by se ng

your financial goal and working backwards to determine a realis c amount

you can save during a specific me period. Saving money for future

consump on always requires not purchasing something today. You must

ensure the trade‐offs are realis c and the opportunity cost of what you are

giving up won’t nega vely impact your well‐being.

What savings goal do you have in

place?

What are examples of emergency expenses a household may encounter?

© Take Charge Today – August 2013 – Choosing to Save – Page 2 Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Ins tute at The University of Arizona

2.4.1.F1

How to save money con nued…

Your spending plan helps you determine how much you can save based on your income and expenses. A frequent

assessment of what you spend your money on is a good habit to develop.

Here are a few money‐saving sugges ons:

Examine current spending – Examine expenses in your Income and Expense Statement and your Spending

Plan to determine changes that can be made to decrease your spending. Start with small expenses (your daily

coffee shop drink, new clothes) and then review your larger expenditures (cable and cell phone plans and

some mes grocery bills) to see if there are opportuni es to decrease your spending.

The following are ps to decrease spending:

1. Communica on ‐ Could you cancel your cable/satellite television or

reduce the cost of your current package? Could you reduce the cost of

your cell phone package? Could you drop your home Internet and use

public Internet at places such as a library?

2. Food ‐ Could you eat at restaurants less? Could you purchase items in

bulk instead of at a vending machine or gas sta on?

3. Transporta on ‐ Could you use public transporta on instead of owning

a vehicle?

4. Housing ‐ Would you consider moving to a smaller or less expensive

home or apartment in order to reduce your mortgage/rent payment and/or u li es?

A er reviewing your monthly expenditures, if you s ll can’t reach your saving goal you might consider:

1. Increasing your income by lobbying for a raise, switching to a job that pays more or taking on a part me

job if even only for a short period of me to increase your savings.

2. DIY – You’ve seen the “do it yourselfers” on TV, so why not try a couple of personal tasks on your own.

Not only can this save you money (if you do it right the first me!) it but it can also give you a sense of

accomplishment! However, the cost to you of doing something on your own is your investment of me

(and materials) in place of the money you otherwise would spend. Make sure you are willing to give up

the me and have the proper skills needed to complete do it yourself tasks.

The following examples are Do It Yourself (DIY) ac vi es:

Food ‐ Pack your lunch and prepare food/beverages from scratch instead of purchasing ready‐to‐eat

items such as coffee and frozen meals.

Transporta on – Develop skills that allow you to take care of very basic vehicle maintenance and

repairs.

Housing ‐ Maintain the inside and outside of your home; visit your local home improvement center to

learn about home DIY projects.

It may be difficult to decrease

or remove contractual

expenses from your spending

plan. With a contractual

expense, you have signed a

contract that requires you to

pay that expense for a specific

amount of me. Make sure to

consider the consequences of

a contract before signing.

What are three ways you could start saving today?

© Take Charge Today – August 2013 – Choosing to Save – Page 3 Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Ins tute at The University of Arizona

2.4.1.F1

Having solid savings habits helps you reach your financial goals. A successful saving

strategy for many is to “pay yourself first.” Paying yourself first means saving for

the future by pu ng money aside before paying your regular monthly bills or

using your income for discre onary purchases.

Make paying yourself first automa c. Ways to accomplish this include:

Automa c transfers ‐ Most depository ins tu ons allow you to set up

automa c transfers among accounts within their depository ins tu on or to

accounts at other ins tu ons. Once the ini al setup is complete, the money is

automa cally moved from one account to another on dates designated by

you.

Payroll Deduc on ‐ Many employers offer payroll deduc on to employees.

With this type of payroll deduc on, you designate a certain percentage or

specific amount of your paycheck to be deposited into an account of your

choice.

Many resources are out there to help you reach saving goals. Websites like h ps://secure.piggymojo.com and

h p://www.s ckk.com, help you develop goals and s ck to them with peer support. Internet‐based spending

plan programs such as h ps://www.mint.com, and programs offered by depository ins tu ons offer goal

tracking through online/mobile banking.

Increasing the value of money

Saved money can increase in value while providing for your future. Time value of money is the idea that money

available at the present me (today) is worth more than the same amount if received in the future. That’s

because if you have it today, it can grow over me. Understanding this core principle of personal finance will help

mo vate you to save early and o en. The factors that affect the size of your savings balance in the future are

me, the interest rate, and the amount you save each period.

Interest rate

Interest is the price paid for using someone else’s money. The interest rate is the percentage rate used to

calculate interest. Interest is earned (if you are the lender) or paid (if you are the borrower). When you save

money in an interest earning account you earn interest. Savings tools are products offered by depository

ins tu ons that, in most cases, allow your deposits to earn interest.

If you don’t withdraw the interest earned from an account, the interest has an opportunity to earn addi onal

interest. Earning interest on interest is known as compound interest.

Graph 1 is an illustra on of how higher interest rates and compound interest

increase the value of savings.

$1,000 Saved for 5 Years with Compounding Interest

To maximize your return:

Save at the highest

interest rate possible!

Save for as long as

possible!

Save as much as

possible, as o en as

possible!

© Take Charge Today – August 2013 – Choosing to Save – Page 4 Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Ins tute at The University of Arizona

2.4.1.F1

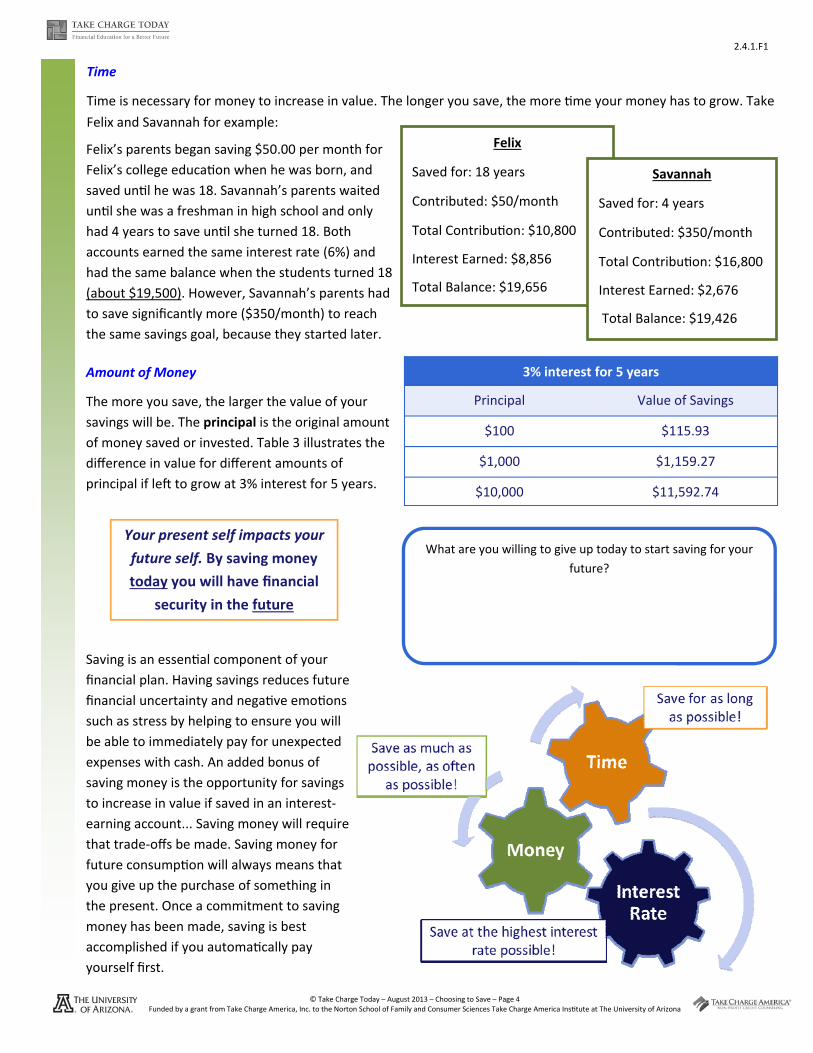

Your present self impacts your

future self. By saving money

today you will have financial

security in the future

Time

Time is necessary for money to increase in value. The longer you save, the more me your money has to grow. Take

Felix and Savannah for example:

Felix

Saved for: 18 years

Contributed: $50/month

Total Contribu on: $10,800

Interest Earned: $8,856

Total Balance: $19,656

Savannah

Saved for: 4 years

Contributed: $350/month

Total Contribu on: $16,800

Interest Earned: $2,676

Total Balance: $19,426

Felix’s parents began saving $50.00 per month for

Felix’s college educa on when he was born, and

saved un l he was 18. Savannah’s parents waited

un l she was a freshman in high school and only

had 4 years to save un l she turned 18. Both

accounts earned the same interest rate (6%) and

had the same balance when the students turned 18

(about $19,500). However, Savannah’s parents had

to save significantly more ($350/month) to reach

the same savings goal, because they started later.

Amount of Money

The more you save, the larger the value of your

savings will be. The principal is the original amount

of money saved or invested. Table 3 illustrates the

difference in value for different amounts of

principal if le to grow at 3% interest for 5 years.

3% interest for 5 years

Principal Value of Savings

$100 $115.93

$1,000 $1,159.27

$10,000 $11,592.74

Saving is an essen al component of your

financial plan. Having savings reduces future

financial uncertainty and nega ve emo ons

such as stress by helping to ensure you will

be able to immediately pay for unexpected

expenses with cash. An added bonus of

saving money is the opportunity for savings

to increase in value if saved in an interest‐

earning account... Saving money will require

that trade‐offs be made. Saving money for

future consump on will always means that

you give up the purchase of something in

the present. Once a commitment to saving

money has been made, saving is best

accomplished if you automa cally pay

yourself first.

What are you willing to give up today to start saving for your

future?

Page | 13 2.4.1.L1

© Take Charge Today – August 2013 – Choose to Save Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Why save?

Choose to Save Note Taking Guide

Total Points Earned

Name

Total Points Possible

Date

Percentage

Class

Saving ‐

Results in...

Savings ‐

What type of asset is saving?

Define liquidity How much should be saved?

Identify three ways money can be saved.

By saving money

___________________

You will have financial

security in the

___________________

Page | 14 2.4.1.L1

© Take Charge Today – August 2013 – Choose to Save Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Describe pay yourself first.

How can you make the process automatic?

Why is setting a financial goal an important part of

the saving process?

Why should trade‐offs be considered when saving?

Why is time value of money important to saving?

Describe interest.

How does compounding interest work?

How does each factor affect the time value of

money?

Interest Rate

Money

Time

Page | 11 2.4.1.A1

© Take Charge Today – August 2013 – Choose to Save Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

My Wish List

My Saving Quest

Total Points Earned

Name

20 Total Points Possible

Date

Percentage

Class

Part 1: My Wish List (7 points)

What are three things on your personal wish list? Include anything of monetary value. Approximately how much does each item cost? Place a star next to the item you would like to start saving for today.

$

$

$

Page | 12 2.4.1.A1

© Take Charge Today – August 2013 – Choose to Save Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Part 2: My Current Spending (7 points)

Identify three changes you are willing to make today to your current income or spending to start saving for the future.

What is the trade‐off for each change? Place a star next to items with a realistic opportunity cost.

Part 3: Implementing My Saving Quest (6 points)

•Trade‐off: •Trade‐off: •Trade‐off:

How much can you realistically save each week for your item?

What is one strategy you will use to make the saving process automatic?

What is your financial goal?

Describe how your goal can be reached using the time value of money.

Page | 6 1.14.3.A1

© Family Economics & Financial Education – May 2012 – Time Value of Money Math Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

By educators… for educators

Time Value of Money Math Practice

Total Points Earned

Name

19 Total Points Possible

Date

Percentage

Class

Directions: Solve each of the following mathematical problems. Round each calculation to the nearest thousandth. (.5 point per blank)

Step 1: Principal X Interest Rate (in decimal form) X Time Periods = Interest Earned

Step 2: Principal + Interest Earned = Amount Investment is Worth

1. Sara deposited $600.00 into a savings account one year ago. She has been earning 1.2% in annual simple interest. Complete the following calculations to determine how much Sara’s money is now worth.

Step One __________principal x _________ interest rate x _________time period = __________ interest earned

Step Two __________ principal + __________interest earned = __________ amount investment is worth

How much is Sara’s investment worth after one year? ___________________

P (1 + r) n = A

Principal (1 + Interest Rate) Time Periods

= Amount Investment is Worth 2. Tim’s grandparents have given him $1,500.00 to invest while he is in college to begin his retirement fund. He will earn 2.3% interest, compounded annually. What will his investment be worth at the end of four years?

What is the equation? ________ Principal x (1 + ________ interest rate) ________ (time period) = Amount investment is worth

Step One 1 + ________ interest rate = ________

Step Two ________ (answer Step One) ________ time period = ________

Step Three ________ (answer Step Two) x ________ principal = ________ Amount investment is worth

What will Tim’s investment be worth at the end of four years? ________

Simple Interest

Compound Interest – Single Sum Investment

Page | 15 2.4.1.A2

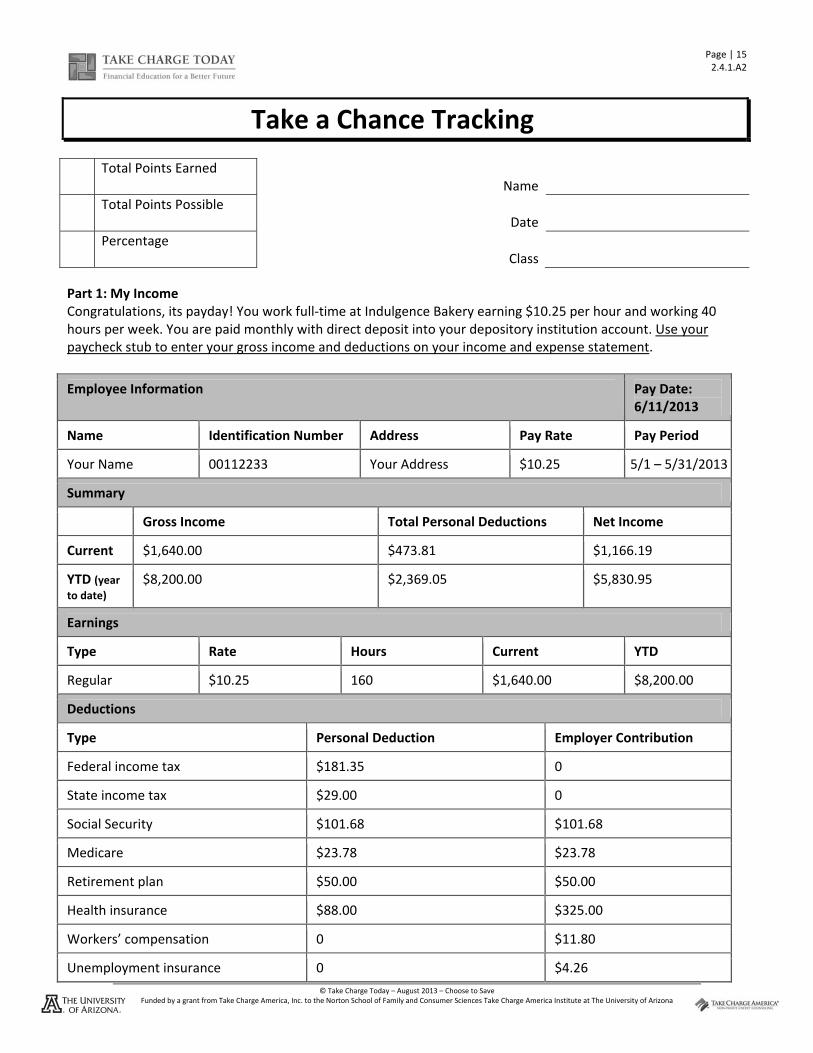

© Take Charge Today – August 2013 – Choose to Save Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Take a Chance Tracking

Total Points Earned

Name

Total Points Possible

Date

Percentage

Class

Part 1: My Income Congratulations, its payday! You work full‐time at Indulgence Bakery earning $10.25 per hour and working 40 hours per week. You are paid monthly with direct deposit into your depository institution account. Use your paycheck stub to enter your gross income and deductions on your income and expense statement.

Employee Information Pay Date: 6/11/2013

Name Identification Number Address Pay Rate Pay Period

Your Name 00112233 Your Address $10.25 5/1 – 5/31/2013

Summary

Gross Income Total Personal Deductions Net Income

Current $1,640.00 $473.81 $1,166.19

YTD (year to date)

$8,200.00 $2,369.05 $5,830.95

Earnings

Type Rate Hours Current YTD

Regular $10.25 160 $1,640.00 $8,200.00

Deductions

Type Personal Deduction Employer Contribution

Federal income tax $181.35 0

State income tax $29.00 0

Social Security $101.68 $101.68

Medicare $23.78 $23.78

Retirement plan $50.00 $50.00

Health insurance $88.00 $325.00

Workers’ compensation 0 $11.80

Unemployment insurance 0 $4.26

Page | 16 2.4.1.A2

© Take Charge Today – August 2013 – Choose to Save Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

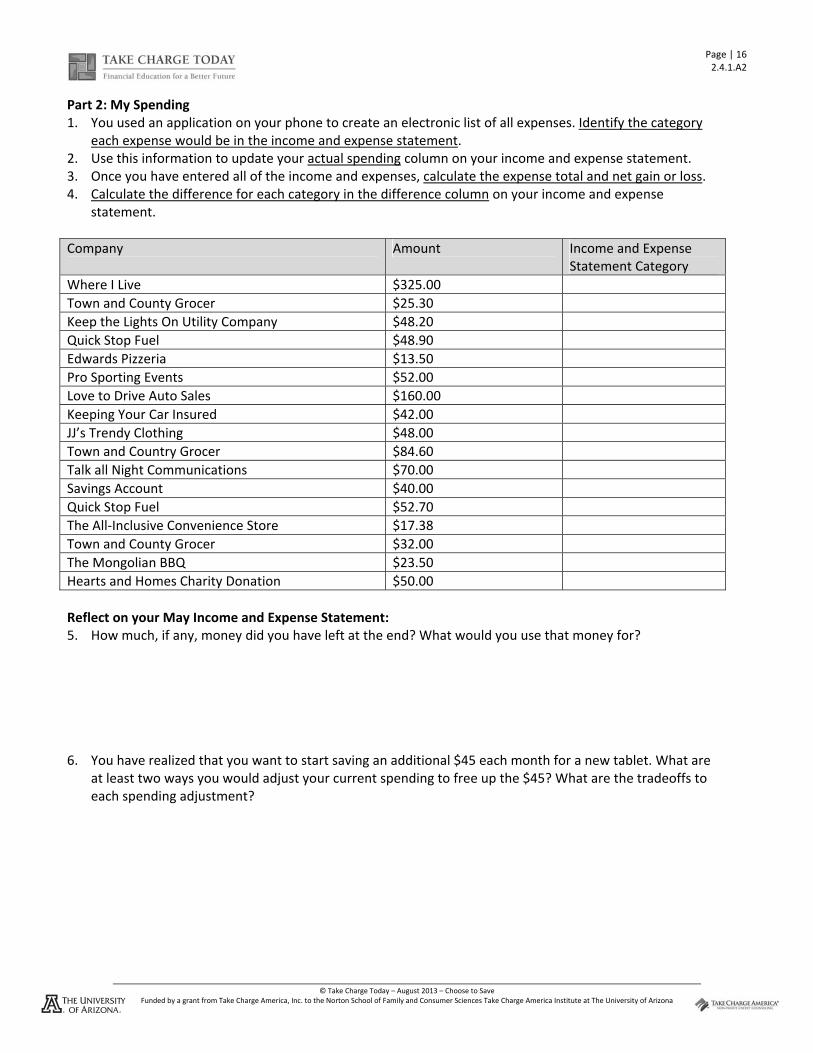

Part 2: My Spending 1. You used an application on your phone to create an electronic list of all expenses. Identify the category

each expense would be in the income and expense statement. 2. Use this information to update your actual spending column on your income and expense statement. 3. Once you have entered all of the income and expenses, calculate the expense total and net gain or loss. 4. Calculate the difference for each category in the difference column on your income and expense

statement.

Company Amount Income and Expense Statement Category

Where I Live $325.00

Town and County Grocer $25.30

Keep the Lights On Utility Company $48.20

Quick Stop Fuel $48.90

Edwards Pizzeria $13.50

Pro Sporting Events $52.00

Love to Drive Auto Sales $160.00

Keeping Your Car Insured $42.00

JJ’s Trendy Clothing $48.00

Town and Country Grocer $84.60

Talk all Night Communications $70.00

Savings Account $40.00

Quick Stop Fuel $52.70

The All‐Inclusive Convenience Store $17.38

Town and County Grocer $32.00

The Mongolian BBQ $23.50

Hearts and Homes Charity Donation $50.00

Reflect on your May Income and Expense Statement: 5. How much, if any, money did you have left at the end? What would you use that money for?

6. You have realized that you want to start saving an additional $45 each month for a new tablet. What are at least two ways you would adjust your current spending to free up the $45? What are the tradeoffs to each spending adjustment?

Page | 17 2.4.1.A2

© Take Charge Today – August 2013 – Choose to Save Funded by a grant from Take Charge America, Inc. to the Norton School of Family and Consumer Sciences Take Charge America Institute at The University of Arizona

Income and Expense Statement for: You!

Time Period: May 1‐31st

Spending Plan Actual Amount

Spent Difference

Income

Earned Income

Wages or salary before deductions $1640.00

Commissions/tips/bonuses

Unearned Income

Money from savings and investments to help pay expenses during this time period

Scholarships from non‐government sources

Total Income $1640.00

Expenses

Deductions Often Taken from Paychecks

Federal and State Income tax $210.35

Social Security $101.68

Medicare $23.78

Saving and Investing (Pay Yourself First)

Contribution to emergency savings $40.00

Contribution to savings for a financial goal $0.00

Retirement $50.00

Insurance Premiums

Health insurance $88.00

Automobile insurance $42.00

Life insurance $0.00

Housing Costs

Housing payment (rent or mortgage) $325.00

Utilities (gas, electricity, water, garbage) $50.00

Transportation Costs

Car payment $160.00

Fuel (gasoline/diesel) $110.00

Automobile repairs and maintenance $30.00

Food Costs

Food at the grocery store $135.00

Meals at restaurants $54.19

Other: $0.00

Communication and Computers

Cell phone $70.00

Medical Costs Not Covered by Insurance

Medical care and medications $0.00

Clothing and Personal Care

Clothing $50.00

Personal care (shampoo, haircuts, cosmetics, laundry, etc.) $25.00

Educational Expenses

Tuition for private school or higher education $0.00

Entertainment

Movies, books, toys, and other entertainment $75.00

Credit Costs

Credit card payment $0.00

Giving

Donations $0.00

Total Expenses $1640.00

Net Gain or Net Loss (Income less Expenses) $0