Embed Size (px)

Citation preview

23rd Annual Investment Conference & Luncheon

Tom Vautin, CFA, CFP®, EA

Senior Financial Planner

Greg Stevens, CFP® Senior Financial Counselor

Cabot Money Management, Inc.

216 Essex Street Salem, Massachusetts 01970

800-888-6468 eCabot.com

Managing Your Wealth in an Unstable Environment

What Has Happened Over the Past 4 Years?

Credit crisis (caused in large part by loose lending standards and excess leverage)

Major banking institutions fail or need government bailout (Lehman, Bear Stearns, AIG…)

Companies lay off employees to adapt to the “new normal”

Unemployment tops 10% at its peak

S&P 500 falls from 1576 on 10/11/2007 to 676 on 9/19/2012 (Drop of 58%!!)

S&P recovers back to 1461 (as of 9/19/2011)

Volatility in the global markets remains on the forefront of all investor’s minds.

*Please refer to the Appendix at the end of this presentation for disclosures.

Tax Law Uncertainty

Income tax changes – Individuals and businesses do not know what the rules

will be next year Payroll tax changes

– Will the temporary lower tax rates be extended in 2013? Estate tax changes

– Similar to income tax changes, but primarily affect individuals only

*Please refer to the Appendix at the end of this presentation for disclosures.

Market Uncertainty

Market volatility – Stocks have not been as volatile recently as they were in 2011 – News headlines in 2012

Eurozone “crisis” Presidential and congressional elections Tax law uncertainty and “fiscal cliff” Debt ceiling Unemployment Low interest rate environment

– Stock markets generally do not like uncertainty

*Please refer to the Appendix at the end of this presentation for disclosures.

Where Do We Go From Here?

Global economic recovery (SLOW) US jobs picture remains cloudy Political unrest overseas European debt crisis is still there Presidential election Fiscal Cliff Housing recovery or further decline? Global stock market gyrations

*Please refer to the Appendix at the end of this presentation for disclosures.

BOTTOM LINE:

There is a Lot of Uncertainty Out There!

*Please refer to the Appendix at the end of this presentation for disclosures.

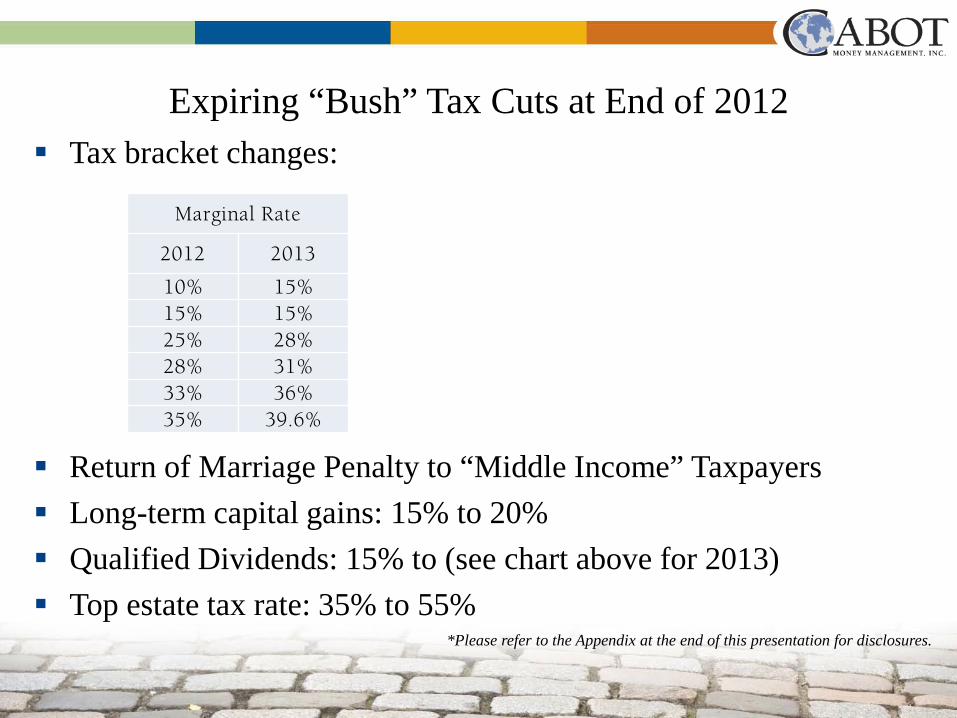

Expiring “Bush” Tax Cuts at End of 2012 Tax bracket changes:

Return of Marriage Penalty to “Middle Income” Taxpayers Long-term capital gains: 15% to 20% Qualified Dividends: 15% to (see chart above for 2013) Top estate tax rate: 35% to 55%

Marginal Rate

2012 2013 10% 15% 15% 15% 25% 28% 28% 31% 33% 36% 35% 39.6%

*Please refer to the Appendix at the end of this presentation for disclosures.

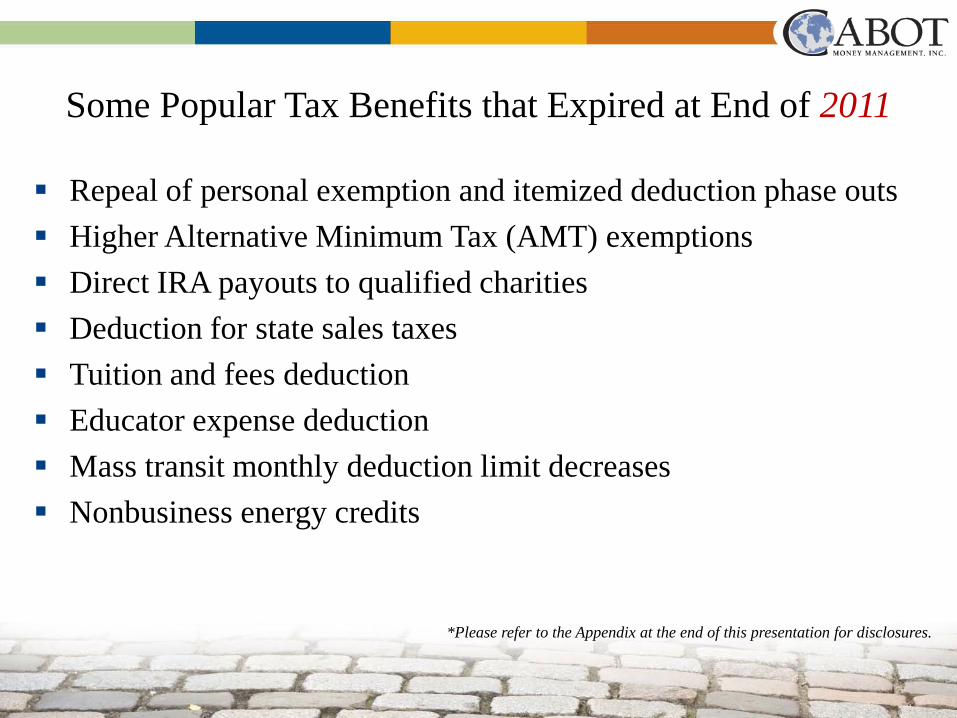

Some Popular Tax Benefits that Expired at End of 2011

Repeal of personal exemption and itemized deduction phase outs Higher Alternative Minimum Tax (AMT) exemptions Direct IRA payouts to qualified charities Deduction for state sales taxes Tuition and fees deduction Educator expense deduction Mass transit monthly deduction limit decreases Nonbusiness energy credits

*Please refer to the Appendix at the end of this presentation for disclosures.

Medicare “Surtax” Begins in 2013

Individuals with modified AGI over $200,000 and families with modified AGI over $250,000 will be affected

Additional 2.8% on investment income Additional 0.9% payroll tax This is part of the Patient Protection and Affordable Care Act

(Obamacare) and is separate from Bush tax cuts For affected taxpayers, long-term capital gain rate could increase

from 15% to 23.8% and qualified dividend rate could increase from 15% to as high as 43.4% if Bush tax cuts are not extended

*Please refer to the Appendix at the end of this presentation for disclosures.

What is the “Fiscal Cliff”?

*Please refer to the Appendix at the end of this presentation for disclosures.

What is the “Fiscal Cliff”?

Combination of: – Tax increases – Mandatory government spending cuts

Impact:* – Reduces deficit by about $600 billion – Projected GDP contraction of about 4% in 2013 (recession) – Unemployment increase of about 1%

* Source: Central Budget Office

*Please refer to the Appendix at the end of this presentation for disclosures.

*Please refer to the Appendix at the end of this presentation for disclosures.

What Will Really Happen?

Probably nothing before the elections Both political parties believe adjustments need to be made, but

negotiations will be contentious. – Not knowing the rules makes tax planning difficult Best case scenario: Agreement will be made as soon as possible

(not likely). Likely scenario: Agreement will be made after elections but

before end of year. Worst case scenario: Agreement will be made in 2013 and rules

will apply retroactively (no opportunity to plan).

*Please refer to the Appendix at the end of this presentation for disclosures.

Likely Scenario?

Compromise is reached after election – Democrats would like to raise just the top two tax brackets

(33% to 36% and 35% to 39.6%) – Republicans would like to extend all Bush tax cuts

Extend most or all Bush tax cuts through 2013 Extend the tax laws that expired at end of 2011 through 2013 Continue temporary payroll tax decrease? Major tax reform during 2013 effective at beginning of 2014

*Please refer to the Appendix at the end of this presentation for disclosures.

Tax Planning Strategies

Plan now, execute later. In most cases, there are few reasons to execute “tax-planning” transactions before the rules are known.

Plan for multiple scenarios:

– Higher tax rates – Lower tax rates – Same tax rates

*Please refer to the Appendix at the end of this presentation for disclosures.

Sample “Higher Tax Rate in 2013” Strategy

You can control the timing of certain income sources. – Capital gains on investments – Stock options – Roth IRA conversions – Sales of real estate that generate capital gains

Accelerate income from these sources into 2012 Defer deductions (if possible) into 2013

– Medical expenses – Charitable contributions

*Please refer to the Appendix at the end of this presentation for disclosures.

Other Strategies

Lower tax rates in 2013? – Defer income into 2013 – Accelerate deductions into 2012 – But depends on your individual situation as well

Same tax rates in 2013? – Depends on your individual situation – Deferring tax payments can be beneficial while your money

can be otherwise used for investing, spending, paying down debt, etc.

*Please refer to the Appendix at the end of this presentation for disclosures.

Plan Around Your Marginal Tax Rate

Determine what your marginal tax rate will be each year. How much will your next dollar of taxable income cost you? – Tax brackets published by IRS – Phaseouts of tax benefits – Alternative Minimum Tax – State income tax rate

Changes in your individual marginal tax rate from year to year will depend on 1) tax laws and 2) your individual income situation.

*Please refer to the Appendix at the end of this presentation for disclosures.

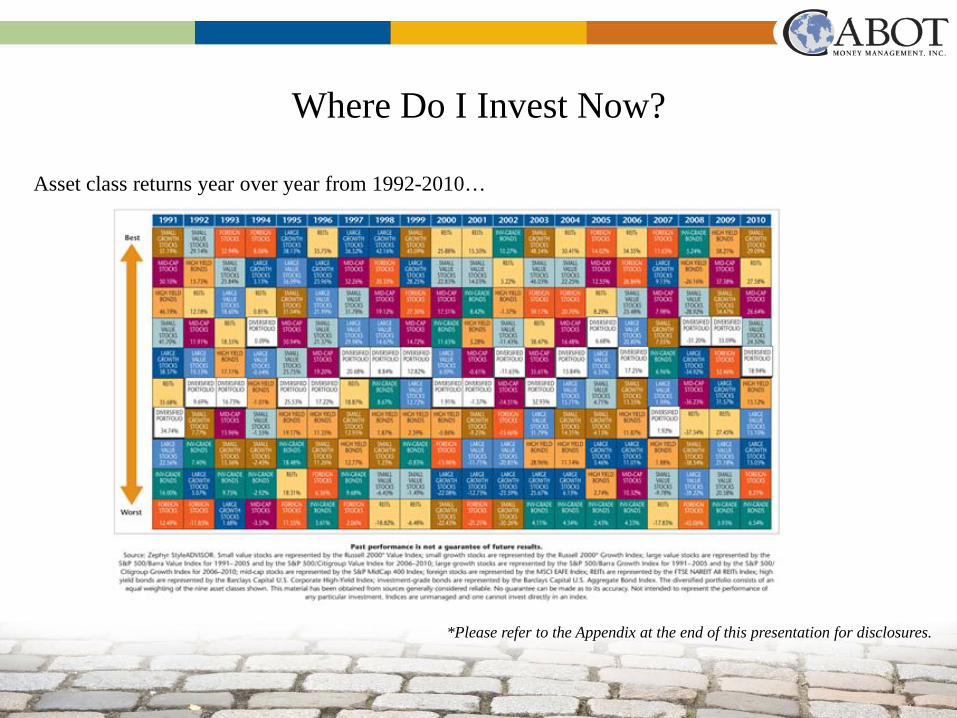

Where Do I Invest Now?

Asset class returns year over year from 1992-2010…

*Please refer to the Appendix at the end of this presentation for disclosures.

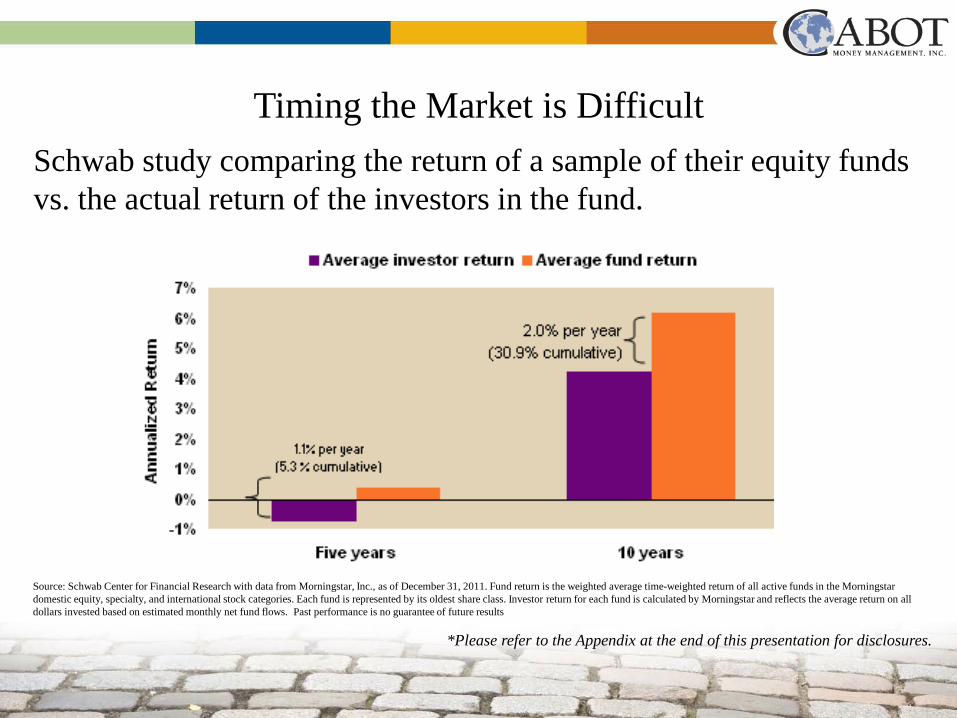

Timing the Market is Difficult Schwab study comparing the return of a sample of their equity funds vs. the actual return of the investors in the fund.

Source: Schwab Center for Financial Research with data from Morningstar, Inc., as of December 31, 2011. Fund return is the weighted average time-weighted return of all active funds in the Morningstar domestic equity, specialty, and international stock categories. Each fund is represented by its oldest share class. Investor return for each fund is calculated by Morningstar and reflects the average return on all dollars invested based on estimated monthly net fund flows. Past performance is no guarantee of future results

*Please refer to the Appendix at the end of this presentation for disclosures.

How Should We Invest?

Develop an allocation based around your goals, not just where you expect the market to go.

College Planning – Amount, timeframe, risk tolerance – Will your kids (or grandchildren) need financial aid?

Retirement – How long do you expect to work? – How much do you need? – Retirement can last for 30+ years; invest with that timeframe in

mind! Short-term purchases

– Amount and timeframe are critical to determine investment objective

*Please refer to the Appendix at the end of this presentation for disclosures.

Develop A Roadmap

The starting point is your current financial situation.

Your goals are the finish line.

Bridge the gap between start and finish.

Which route should you take?

*Please refer to the Appendix at the end of this presentation for disclosures.

Make realistic assumptions for the uncertain variables.

– Historical inflation = 3%

– Investment returns based on historical averages

– Taxes: Current laws with an educated guess about the future

Develop A Roadmap

*Please refer to the Appendix at the end of this presentation for disclosures.

Why Do We Invest?

But, How Much Money is Enough?

– It depends on a few uncertain things: Investment returns

Inflation

Tax policy

– And some certain things: Your asset allocation

Tax minimization

Most importantly – your financial goals!

*Please refer to the Appendix at the end of this presentation for disclosures.

Focus On The Big Picture

Determine an Appropriate Asset Allocation

– Will significantly impact your investment returns over the long-term.

– Investment returns in the short-term are uncertain.

– Performance of a broad asset allocation over the long-term can be estimated with more confidence.

– There is no free lunch. Higher returns come with a price – higher volatility.

*Please refer to the Appendix at the end of this presentation for disclosures.

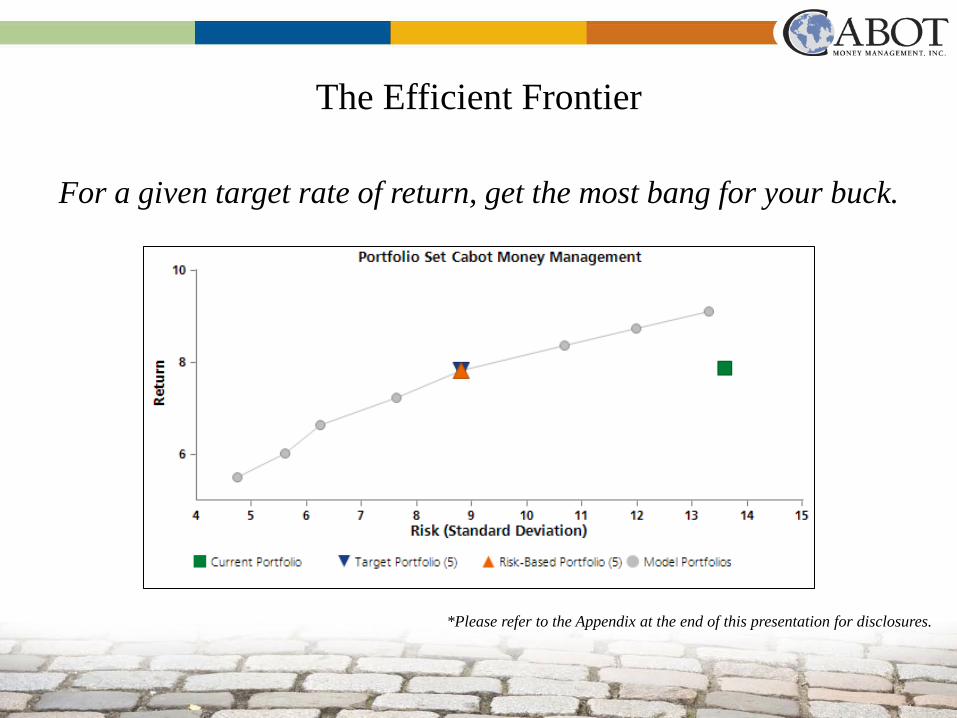

The Efficient Frontier

For a given target rate of return, get the most bang for your buck.

*Please refer to the Appendix at the end of this presentation for disclosures.

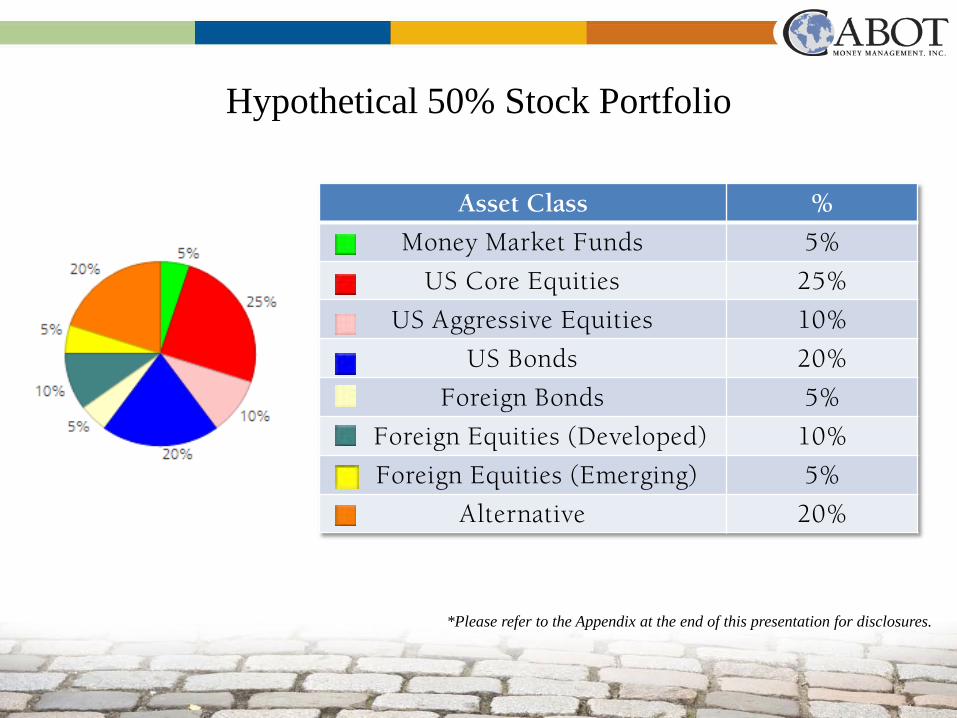

Hypothetical 50% Stock Portfolio

Asset Class %

Money Market Funds 5%

US Core Equities 25%

US Aggressive Equities 10%

US Bonds 20%

Foreign Bonds 5%

Foreign Equities (Developed) 10%

Foreign Equities (Emerging) 5%

Alternative 20%

*Please refer to the Appendix at the end of this presentation for disclosures.

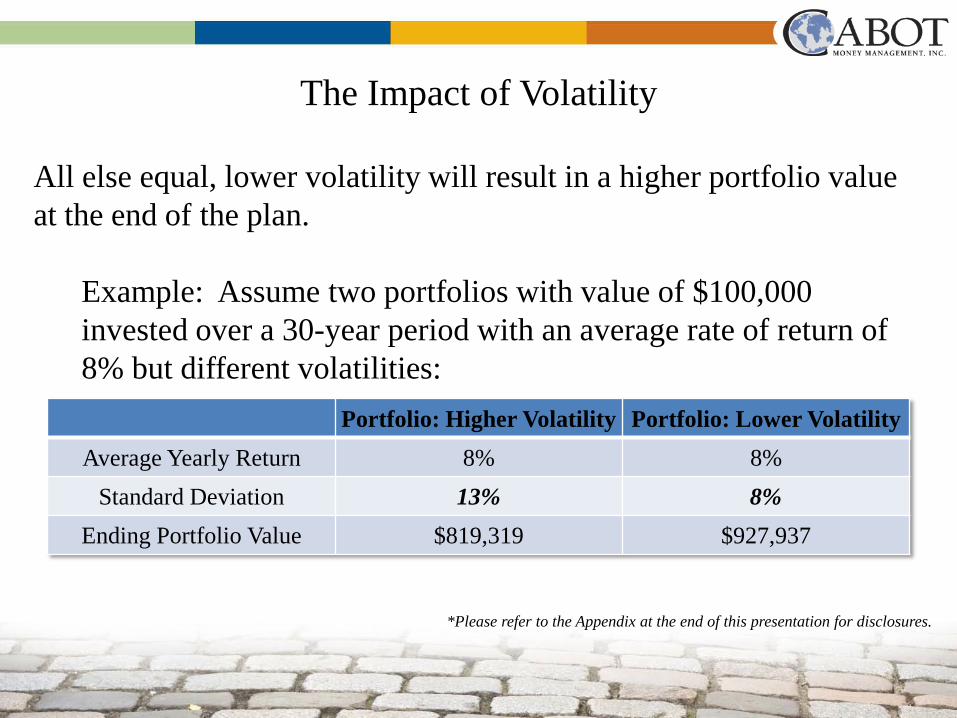

The Impact of Volatility

Portfolio: Higher Volatility Portfolio: Lower Volatility Average Yearly Return 8% 8%

Standard Deviation 13% 8% Ending Portfolio Value $819,319 $927,937

All else equal, lower volatility will result in a higher portfolio value at the end of the plan.

Example: Assume two portfolios with value of $100,000 invested over a 30-year period with an average rate of return of 8% but different volatilities:

*Please refer to the Appendix at the end of this presentation for disclosures.

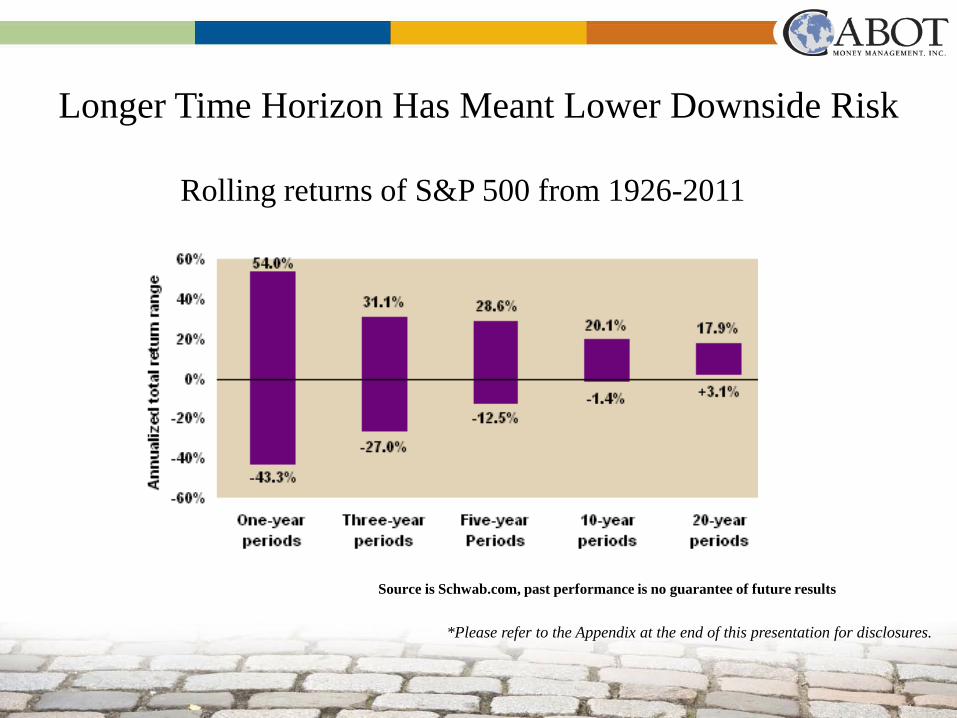

Longer Time Horizon Has Meant Lower Downside Risk

Rolling returns of S&P 500 from 1926-2011

Source is Schwab.com, past performance is no guarantee of future results

*Please refer to the Appendix at the end of this presentation for disclosures.

Putting It All Together

Run Monte Carlo Simulation to find the success rate of your plan – The simulation runs thousands of trials based on the variables: Taxes Inflation Projected investment returns / Asset allocation Goals

– Some of the trials are successful and some are not. A “probability of success” is estimated.

*Please refer to the Appendix at the end of this presentation for disclosures.

If the estimated success rate is not adequate, make adjustments with the things you can control.

– Asset allocation Expected rate of return

Expected volatility

– Goals Change future standard of living

Change current standard of living (saving rate)

Putting It All Together

*Please refer to the Appendix at the end of this presentation for disclosures.

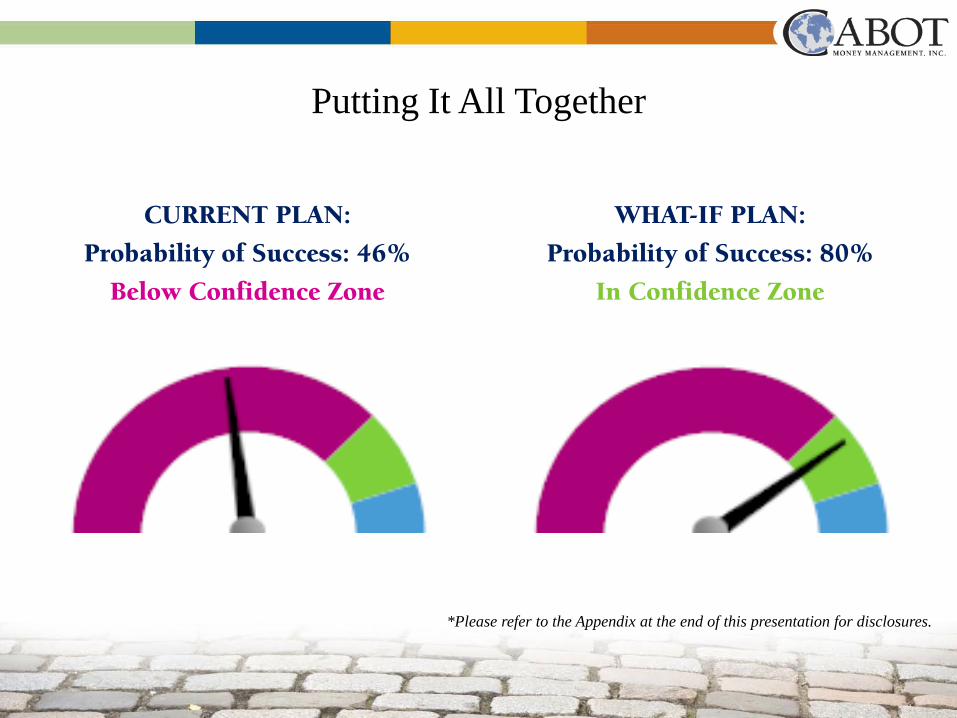

CURRENT PLAN:

Probability of Success: 46%

Below Confidence Zone

WHAT-IF PLAN:

Probability of Success: 80%

In Confidence Zone

Putting It All Together

*Please refer to the Appendix at the end of this presentation for disclosures.

What about your Estate Plan?

What is an estate plan? Road map for you beneficiaries/executor Gives you control of your assets after your death Designates who takes control if you’re incapacitated

*Please refer to the Appendix at the end of this presentation for disclosures.

Critical Estate Planning Documents

Simple Will – Spells out “who gets what”

Durable Power of Attorney (DPOA) – Who makes financial decisions if you can’t?

Health Care Proxy – Who makes medical decisions if you can’t?

Trusts – Dictates how your assets pass on and gives you the

opportunity to control how they are distributed.

*Please refer to the Appendix at the end of this presentation for disclosures.

Highlights of a Trust

Can be Revocable or Irrevocable Terms of Rev Trust become “irrevocable” at the time of death The grantor can dictate how and to whom their assets pass at their

death (or during life) Moving assets to a Trust gives us the ability to plan for the

uncertainty of the estate tax in future years Allows grantor to retain control

*Please refer to the Appendix at the end of this presentation for disclosures.

Revocable Trust

Terms can be changed during grantor’s life Can provide for assets to remain in Trust at death Most Rev Trusts contain provisions for “splitting” the estate at death and preserving the deceased’s estate tax exemption (married couples) Assets held in the Trust (i.e. real estate, investment accounts, etc.) are exempt from probate

*Please refer to the Appendix at the end of this presentation for disclosures.

Irrevocable Trust

Can be created from a Rev Trust at death of Grantor or on its own Excellent way to transfer assets and remove future appreciation

from your estate Examples

– Gift Trust – Charitable Trust – Grantor Retained Annuity Trust – Credit Shelter Trust

*Please refer to the Appendix at the end of this presentation for disclosures.

Estate Taxes

Estate taxes are imposed at death, if your estate exceeds the “threshold”.

Threshold is a moving target ($5,120,000 for 2012, set to revert to $1 million in 2013)

Value of estate over $5,120,000 is taxed at 35% Individual states have their own estate tax ($1 million threshold in

MA)

*Please refer to the Appendix at the end of this presentation for disclosures.

How Do We Manage Estate Taxes?

Develop a plan! – Gifting ($13K per year to any individual) – Estate splitting/balancing for married couples – Transfer assets to Revocable Trust with credit shelter provision – Consider large gifts by funding an irrev. Trust crafted to suit

your needs (removes future appreciation from your estate) – Life insurance owned by Trust to pay taxes – Don’t forget to review the beneficiary designation on any

retirement accounts and insurance policies!

*Please refer to the Appendix at the end of this presentation for disclosures.

SUMMARY

In an uncertain environment, you can do things to minimize the uncertainty:

– Focus on what you can control.

– Remember that the markets historically have gone up more often than they have gone down.

– Diversification still works.

– Create a multi-year tax minimization strategy.

– Develop a roadmap and monitor your progress to gain peace of mind!

*Please refer to the Appendix at the end of this presentation for disclosures.

THANK YOU!

APPENDIX: DISCLOSURES

Past performance is not indicative of future results. Investments are not insured and may lose value.

No amount of asset or sector allocation or diversification can protect against principal loss.

Individual security selection may result in returns that deviate from the security’s corresponding benchmark.

Nothing contained in the presentation should be considered as tax or legal advice.

23rd Annual Investment Conference & Luncheon