Embed Size (px)

Citation preview

2022 Tax Filing Season Update

#8030EXAM MATERIAL

8030 Final Exam • 1

2022 TAX FILING SEASON UPDATE (COURSE #8030)

COURSE DESCRIPTION

Each year, income tax return preparation must take into account inflation-related changes to various limits and new tax laws. This course examines those changes and new laws. The 2022 Tax Filing Season Update course is designed to provide valuable information to persons preparing individual Form 1040 income tax returns reflecting clients’ 2021 income. The course discusses new tax law, including various tax extenders, and recent updates for the 2022 filing season, provides a general tax review, and examines important rules governing tax return preparer practices, procedures, and responsibilities. No prerequisites. Course level: Basic. Course #8030 – 8 CPE hours.

LEARNING ASSIGNMENTS AND OBJECTIVES

As a result of studying each assignment, you should be able to meet the objectives listed below each individual assignment.

ASSIGNMENT 1: SUBJECTRecent Updates

Study the course materials from pages 1 to 26Complete the review questions at the end of the chapterAnswer the exam questions 1 to 3

Objectives:

• To identify the inflation adjustments to various federal limits • To recognize the optional standard mileage rates• To recall the required minimum distribution rules applicable to traditional IRAs and retirement

plans

2 • 8030 Final Exam

ASSIGNMENT 2: SUBJECTNew Tax Law and Extenders

Study the course materials from pages 27 to 44Complete the review questions at the end of the chapterAnswer the exam questions 4 to 8

Objectives:

• To recall the health insurance premium tax credit increase brought about by ARPA • To recognize the rules for repayment of COVID-19 related distributions from retirement plans• To identify the rules governing nonitemizers’ permitted adjustment for charitable contributions• To recognize the income tax rules applicable to the Recovery Rebate Credit• To recall the current status of tax extenders

ASSIGNMENT 3: SUBJECTIndividual Income Components

Study the course materials from pages 45 to 70Complete the review questions at the end of the chapterAnswer the exam questions 9 to 13

Objectives:

• To identify the items included in a taxpayer’s taxable earnings• To recall the tax treatment of foreign accounts and trusts• To recall the rules governing contributions to and distributions from IRAs• To recognize the tax treatment of retirement income• To recall the reporting requirements and taxability of unemployment compensation• To recall the rules governing the tax treatment of alimony under post-2018 divorce agreements

ASSIGNMENT 4: SUBJECTProprietorship Income

Study the course materials from pages 71 to 94Complete the review questions at the end of the chapterAnswer the exam questions 14 to 19

Objectives:

• To recognize the items included in self-employment income and expenses• To recognize the difference between a hobby and a business for tax purposes• To recognize the tax deduction for business use of a home• To identify the recordkeeping requirements to substantiate Schedule C entries

8030 Final Exam • 3

ASSIGNMENT 5: SUBJECTIndividual Deductions and Credits

Study the course materials from pages 95 to 120Complete the review questions at the end of the chapterAnswer the exam questions 20 to 24

Objectives:

• To recall the eligibility for, and amount of, standard deductions• To identify the limitations applicable to Schedule A itemized deductions• To recognize the eligibility requirements for and limits applicable to the common tax credits

ASSIGNMENT 6: SUBJECTGeneral Income Tax Review - Part 1

Study the course materials from pages 121 to 140Complete the review questions at the end of the chapterAnswer the exam questions 25 to 30

Objectives:

• To recognize the tax treatment of virtual currency• To recall the applicable alternative minimum taxable income exemption• To identify the qualified business income deduction available to pass-through entities • To recall the rules for taxing the unearned income of dependent children• To identify the broadened § 529 qualified education expenses resulting from the passage of the

Tax Cuts and Jobs Act and the SECURE Act

ASSIGNMENT 7: SUBJECTGeneral Income Tax Review - Part 2

Study the course materials from pages 141 to 166Complete the review questions at the end of the chapterAnswer the exam questions 31 to 36

Objectives:

• To recognize the expanded exclusion from income of student loan indebtedness authorized under the American Rescue Plan Act (ARPA)

• To identify the tax treatment given to Achieving a Better Life Experience Act (ABLE) accounts• To recall the modification of net operating losses imposed under the CARES Act• To identify the tax treatment of employee fringe benefits• To recall the rules governing a taxpayer’s tax withholding and estimated tax payments• To recognize the options available to a taxpayer for paying any tax due or receiving a tax refund

4 • 8030 Final Exam

ASSIGNMENT 8: SUBJECTPractices, Procedures, and Responsibility

Study the course materials from pages 167 to 192Complete the review questions at the end of the chapterAnswer the exam questions 37 to 40

Objectives:

• To identify the red flags indicating possible tax-related identity theft and suggested assistance to its victims

• To recognize the laws and regulations requiring privacy and security of taxpayer data and the best practices tax preparers may implement to help assure it

• To recall the purpose of individual taxpayer identification numbers, their effect on tax credits and how to renew them

• To identify the due diligence requirements imposed on tax return preparers with respect to claiming head of household filing status, EITC, CTC and AOTC

• To recall the e-file requirements

ASSIGNMENT 9:• Complete the Answer Sheet and Course Evaluation and submit to PES

NOTICEThis course and test uses the materials entitled 2022 Tax Filing Season Update © 2021 by Paul J Winn. Displayed by permission of the author. All rights reserved. No part of this course may be reproduced in any form or by any means without the written permission of the copyright holder.

Use of these materials or services provided by Professional Education Services, LP (“PES”) is governed by the Terms and Conditions on PES’ website (www.mypescpe.com). PES provides this course with the understanding that it is not providing any accounting, legal, or other professional advice and assumes no liability whatsoever in connection with its use. PES has used diligent efforts to provide quality information and material to its customers, but does not warrant or guarantee the accuracy, timeliness, completeness, or currency of the information contained herein. Ultimately, the responsibility to comply with applicable legal requirements falls solely on the individual licensee, not PES. PES encourages you to contact your state Board or licensing agency for the latest information and to confirm or clarify any questions or concerns you have regarding your duties or obligations as a licensed professional.

© Professional Education Services, LP 2021

Program Publication Date 6/28/2021

8030 Final Exam • 5

2022 TAX FILING SEASON UPDATE (COURSE #8030)

EXAM INFORMATION

COURSE EXPIRATION DATE: Per AICPA and NASBA standards, this course must be completed within ONE YEAR from the date of purchase.

TEST FORMAT: The following final exam, consisting of 40 multiple choice questions, is based specifically on the material included in this course. The answer sheet must be completed and returned to PES for CPE certification. You will find the answer sheet at the back of this exam packet so that you may easily remove it and use it while taking your test.

LICENSE RENEWAL INFORMATION: The 2022 Tax Filing Season Update course (#8030) qualifies for 8 CPE hours.

PROCESSING: You must score 70% or better to pass. If you mail or fax your exam, when you pass, your Certificate of Completion will be mailed. If you do not pass, we will give you a courtesy call to inform you of this. When completing your exam online, grading is instantaneous. Upon achieving a passing score, the completion certificate is immediately available in your account under “My Completed CPE.” Please note: failed exams may be retaken. Per NASBA and AICPA guidelines, missed questions cannot be indicated until after you pass.

GRADING OPTIONS – Please choose only ONE of the following:

GRADING OPTIONS: Please choose only ONE of the following. If mailing or faxing, make sure to fill out your Answer Sheet completely prior to submitting it.

• ONLINE GRADING –Visit our website at http://www.mypescpe.com. Login to your account (if you are a first-time user, you must set up a new user account). Click on the course title of the exam you wish to take. Once all answers have been selected, click the “Submit/Grade Answers” button at the bottom of the page for instant grading and certification. If you do not see the exam listed, click on “My CPE in Progress.” Click on the “Add Exam to Account” button and follow the instructions.

• MAIL – Your exam will be graded and your certificate of completion mailed to you within one business day. Your certificate will be dated according to the postmark date. Please mail your Answer Sheet to:

Professional Education Services, LP4208 Douglas Blvd., Ste 50

Granite Bay, CA 95746

• FAX – Your exam will be graded and you will be contacted either via phone or fax with your results within 4 business hours of receipt. A copy of your graded exam and certificate of completion will be mailed to you. Your certificate will be dated according to the fax date. If you choose to fax your exam, please do not mail it. Your fax will serve as the original. Please refer to the attached answer sheet for further instructions on fax grading. Fax number (916) 791-4099.

THANK YOU FOR USING PROFESSIONAL EDUCATION SERVICES.

THIS PAGE INTENTIONALLY LEFT BLANK.

8030 Final Exam • 7

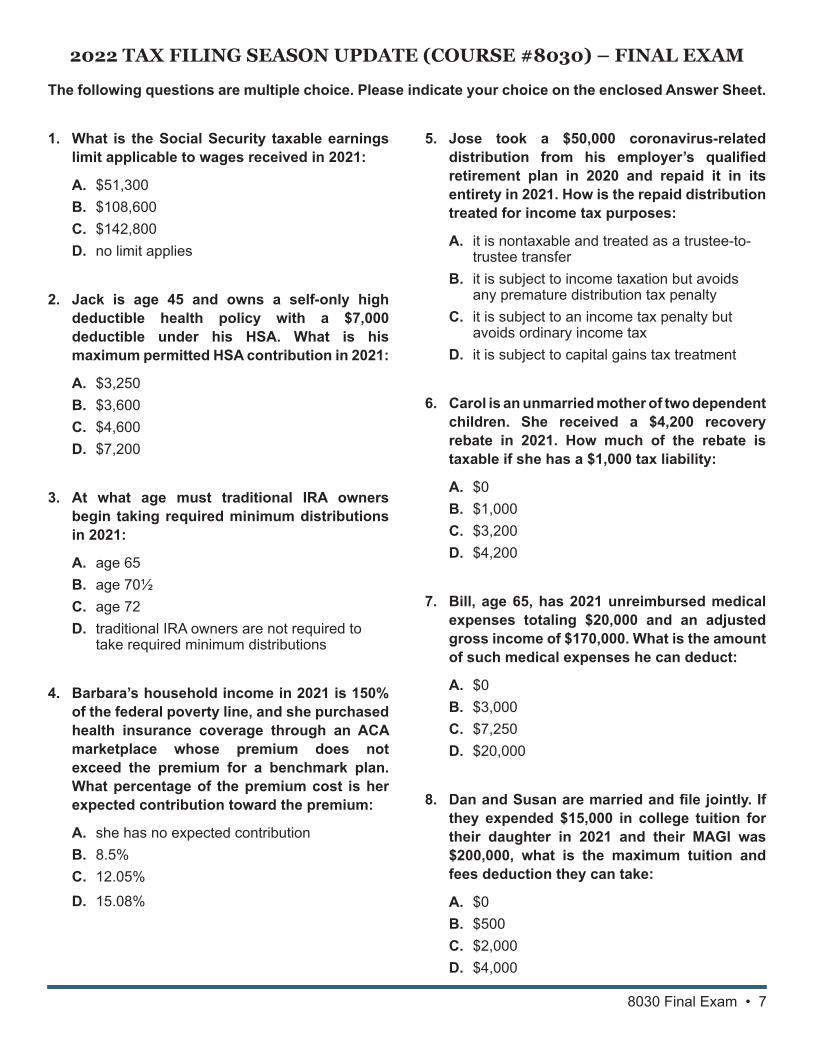

2022 TAX FILING SEASON UPDATE (COURSE #8030) – FINAL EXAM

The following questions are multiple choice. Please indicate your choice on the enclosed Answer Sheet.

1. What is the Social Security taxable earnings limit applicable to wages received in 2021:

A. $51,300B. $108,600C. $142,800D. no limit applies

2. Jack is age 45 and owns a self-only high deductible health policy with a $7,000 deductible under his HSA. What is his maximum permitted HSA contribution in 2021:

A. $3,250B. $3,600C. $4,600D. $7,200

3. At what age must traditional IRA owners begin taking required minimum distributions in 2021:

A. age 65B. age 70½ C. age 72D. traditional IRA owners are not required to

take required minimum distributions

4. Barbara’s household income in 2021 is 150% of the federal poverty line, and she purchased health insurance coverage through an ACA marketplace whose premium does not exceed the premium for a benchmark plan. What percentage of the premium cost is her expected contribution toward the premium:

A. she has no expected contributionB. 8.5%C. 12.05%

D. 15.08%

5. Jose took a $50,000 coronavirus-related distribution from his employer’s qualified retirement plan in 2020 and repaid it in its entirety in 2021. How is the repaid distribution treated for income tax purposes:

A. it is nontaxable and treated as a trustee-to-trustee transfer

B. it is subject to income taxation but avoids any premature distribution tax penalty

C. it is subject to an income tax penalty but avoids ordinary income tax

D. it is subject to capital gains tax treatment

6. Carol is an unmarried mother of two dependent children. She received a $4,200 recovery rebate in 2021. How much of the rebate is taxable if she has a $1,000 tax liability:

A. $0B. $1,000C. $3,200D. $4,200

7. Bill, age 65, has 2021 unreimbursed medical expenses totaling $20,000 and an adjusted gross income of $170,000. What is the amount of such medical expenses he can deduct:

A. $0B. $3,000C. $7,250D. $20,000

8. Dan and Susan are married and file jointly. If they expended $15,000 in college tuition for their daughter in 2021 and their MAGI was $200,000, what is the maximum tuition and fees deduction they can take:

A. $0B. $500C. $2,000D. $4,000

8 • 8030 Final Exam

9. John, a cash method taxpayer, received advance commissions in 2021 for work he will be doing in each of the three following years. In what year(s) must he include the commissions in his income for tax purposes:

A. in 2021B. in 2022, the first year of performing the workC. in each of the years 2022 to 2024, equallyD. in 2024 when the final work is completed

10. Schedule B, Part III, Foreign Accounts and Trusts, must be completed if any of the following apply except:

A. the taxpayer had more than $1,500 of taxable interest or ordinary dividends

B. the taxpayer had a foreign accountC. the taxpayer received a distribution from a

foreign trustD. the taxpayer is claiming the exclusion of

interest from series EE savings bonds

11. What would cause a taxpayer’s contribution to a traditional IRA to be non-deductible:

A. the taxpayer’s ageB. the taxpayer’s additional contribution to a

Roth IRAC. whether the taxpayer’s spouse also made a

contributionD. the taxpayer’s active participation in an

employer’s qualified plan

12. Susan received unemployment benefits amounting to $8,500 in 2021 and repaid $1,500 in the same year. How is the unemployment compensation reported:

A. the total unemployment compensation received must be included in compensation

B. the amount repaid should be subtracted from the total amount of unemployment compensation received and the difference entered on Form 1040, Schedule 1

C. the amount repaid should be deducted on Form 1040 Schedule A

D. no reporting is required since unemployment compensation is not includible in income

13. Jeremy entered into a divorce agreement in 2021 under which he agreed to make annual payments of $100,000. How much of the payments made to his ex-spouse may he deduct:

A. $0B. $25,000C. $50,000D. $100,000

14. Peter is a carpenter employed by Big Construction, Inc. In addition to his work as an employee, he also builds and sells cabinets on a self-employed basis. Accordingly, he must file a Form 1040 and Schedule SE if his net earnings from self-employment are ____ or more.

A. $108.28B. $400C. $600D. $1,000

15. An activity engaged in by a taxpayer is presumed to be carried on for a profit and is, therefore, a business rather than a hobby, if it makes a profit during at least ______ of the last five tax years, including the current year.

A. oneB. twoC. threeD. four

16. Arthur had gross receipts of $8,000 from his hobby and incurred necessary expenses of $10,000. How much of his incurred expenses may he deduct:

A. $0B. $2,000C. $8,000

D. $10,000

8030 Final Exam • 9

17. Which of the following taxpayers may qualify for a home-office deduction for business use of the taxpayer’s home even though the use of the space is not exclusive to the business:

A. Shirley, who uses part of her home in her beauty shop

B. Bob, a self-employed chiropractor, who uses a room in his home to see patients

C. Audrey, who operates a daycare facilityD. Arthur, a statutory employee, who uses a

room in his home to schedule appointments with clients

18. As an alternative to using the actual expense method of determining a home office deduction, a taxpayer may elect to use which of the following:

A. the declining balance methodB. the historical use methodC. the simplified methodD. the average annual use method

19. For what minimum period must a self-employed taxpayer retain business documents supporting her federal tax return:

A. for 6 months following the due date of the return

B. for 2 years following the due date of the return

C. for 3 years following the due date of the return

D. for as long as they are material to the administration of tax law

20. Which of the following would be ineligible to take the standard deduction:

A. Peter, who files as head of householdB. Adrienne, who files as married filing

separately and whose spouse itemizes deductions

C. Harry, who claims the qualified business income deduction

D. Shirley, a dependent

21. A taxpayer’s 16 year-old dependent son earned $7,000 in 2021. What is the standard deduction for him:

A. $7,350B. $12,550C. $1,100D. $0

22. Helen and Jim itemize deductions when they file their income tax return as married filing jointly. If they paid $14,000 in state and local taxes in 2021, what would be the maximum state and local tax deduction they can take on their federal income tax return:

A. $0B. $4,000C. $10,000D. $14,000

23. Bob and Carol refinanced their sole residence, valued at $500,000, in 2021. Under the refinancing arrangement, they refinanced their $300,000 indebtedness for $400,000, receiving $100,000 in cash that they used to pay for their daughter’s wedding. What percent of the interest they pay on the refinanced property are they able to deduct:

A. 25%B. 50%C. 75%D. 100%

24. John and Shirley have one twelve year-old child eligible for the Child Tax Credit, file their tax return as married filing jointly and, at a $160,000 modified adjusted gross income for 2021, they have an AGI that exceeds the threshold at which the increase credit amount begins to phase out by $10,000. For what Child Tax Credit would they be eligible:

A. $0 B. $500C. $2,500D. $3,000

10 • 8030 Final Exam

25. What is the basis of virtual currency received by a taxpayer as payment for goods and services:

A. the fair market value of the virtual currency in U.S. dollars as of the date of receipt

B. the fair market value of the virtual currency in U.S. dollars as of the date it is subsequently traded

C. the cost of the goods and services traded for the virtual currency as of the date of receipt

D. $0

26. As a single taxpayer, Jennifer’s AMTI exemption would be $73,600 if her AMTI did not exceed $523,600. Because her AMTI was $623,600, what is her AMTI exemption:

A. $0B. $23,600C. $48,600D. $73,600

27. Jennifer’s pass-through business has total qualified business income of $100,000 and combined REIT dividends/PTP income of $20,000. Since her taxable income of $150,000, including $10,000 of net capital gain, is below the applicable threshold, what is her pass-through deduction:

A. $20,000B. $24,000C. $28,000D. $30,000

28. Bill and Edna are married and file a joint tax return in 2021. What is their applicable threshold for the § 199A pass-through deduction:

A. $164,925B. $214,925C. $329,800

D. $429,800

29. A child’s 2021 income subject to the Kiddie Tax is taxed in accordance with ________ rates and brackets.

A. the parents’B. married taxpayers’ filing jointlyC. unmarried taxpayers’D. head of household

30. What is the maximum amount that may be withdrawn from a Section 529 Qualified Tuition Plan in 2021 for elementary school tuition that would be considered a qualified education expense:

A. no elementary school tuition would be considered a qualified education expense under a Section 529 plan

B. $10,000C. $25,000D. no limit applies

31. A designated beneficiary of an ABLE account must be ___________ in order to meet the special rules that apply to the increased contribution limit authorized under the Tax Cuts and Jobs Act.

A. an employee for whom no contribution is made for the taxable year to a defined contribution, TSA, or section 457 deferred compensation plan

B. terminally illC. age 55 or olderD. on public assistance

32. Student loan forgiveness in 2021 that would be includible in income except for the passage of the American Rescue Plan Act is tax-free unless:

A. the loan discharge is made on account of services performed

B. the taxpayer has diedC. the taxpayer is in the military and stationed

outside the U.S.D. the taxpayer is disabled

8030 Final Exam • 11

33. Harry experienced a substantial net operating loss in 2021. What is the maximum percent of that loss that may be carried forward:

A. no more than 40% of the taxpayer’s taxable income

B. no more than 60% of the taxpayer’s taxable income

C. no more than 80% of the taxpayer’s taxable income

D. no more than 100% of the taxpayer’s taxable income

34. For which of the following transportation fringe benefit expenses provided in 2021 would an employer receive a tax deduction:

A. transportation in a commuter highway vehicle in connection with travel between the employee’s residence and place of employment

B. transit pass C. qualified parking reimbursement D. qualified bicycle commuting reimbursement

35. How soon following an event that reduces the taxpayer’s withholding allowances must the taxpayer submit a new W-4 Form to his or her employer:

A. within 10 daysB. within 30 daysC. within 60 daysD. within 90 days

36. Susan is eligible for an income tax refund. Which of the following is not an option with respect to the refund:

A. have the funds credited to a TreasuryDirect® online account in order to buy U.S. Treasury marketable securities

B. have the funds credited to her preparer’s account

C. have the funds deposited directly to an IRA

D. receive the funds in a check

37. Which of the following is/are required for a paid tax preparer to comply with the FTC Financial Privacy Rule:

A. to provide a notice to consumers explaining their information collection and sharing practices

B. to have security systems in place to prevent unauthorized access to taxpayer accounts and personal information

C. to develop, implement and maintain an information security program

D. to preserve records and data from destruction, loss, unauthorized alteration or other misuse

38. To which of the following would the IRS issue an Individual Tax Identification Number (ITIN):

A. Harry, an immigrant with a green card, who works at a local grocery store

B. Edna, a foreign national, who has a U.S. tax reporting requirement

C. Shirley, a U.S. prison inmate, who never applied for a Social Security Number

D. Carl, a U.S. citizen, who has foreign investment income

39. In order for a taxpayer to qualify for head of household filing status, the taxpayer must have _________ for the tax year.

A. lived with his or her spouseB. paid more than half the cost of keeping up

the taxpayer’s homeC. paid the entire cost of keeping up the

taxpayer’s home

D. owned a home

12 • 8030 Final Exam

40. Which of the following tax return preparers must file federal income tax returns electronically:

A. Bob, who provides tax assistance under the Volunteer Income Tax Assistance program

B. Ellen, who prepares a return of the employer by whom she is employed

C. Peter, a tax return preparer who expects to file 20 individual income tax returns

D. Lynn, who prepares 20 tax returns as a fiduciary

Congratulations –

you’ve completed the exam!

8030 Final Exam • 13

2022 TAX FILING SEASON UPDATE #8030 (8 CPE HOURS) ANSWER SHEET (6/21)

IMPORTANT NOTE: For certification, this answer sheet must be completed and submitted to PES for grading within ONE YEAR from the date of purchase. Please use BLACK INK and PRINT for quicker processing –

thank you.

Full Name (as it appears on your license) _______________________________________________________________________________

Address (□ Home □ Work ) ___________________________________________________________________________________

City _____________________________________________________ State ______________________________ Zip __________

Daytime Phone ( ) __________________________________________ E-mail ___________________________________________

License Number ______________________ State _______ Exp Date: ____/____ Are you a: □ CPA □ CFP □ EA (check all that apply)

PTIN Number (if applicable) ______________________________________________________________________________________

If course was ordered by another party, please indicate their name here: _____________________________________________

GRADING OPTIONS – Please choose only ONE of the following:ONLINE GRADING – Visit our website at www.mypescpe.com. Login to your account (if you are a first-time user, you must set up a new user account). Click on the course title of the exam you wish to take. If you do not see the exam listed, click on “My CPE in Progress,” then click on the “Add Exam to Account” button and follow the instructions.

Mail – Mail your exam to: PES, 4208 Douglas Blvd., Ste 50, Granite Bay, CA 95746

Fax – Fax your exam to (916) 791-4099 and choose one of the following options: □ Mail my results □ Fax my results (_____)__________________ □ Phone my results (_____)__________________

PLEASE INDICATE YOUR ANSWER BY FILLING IN THE APPROPRIATE CIRCLE

Please complete the attached course evaluation - your opinion is extremely valuable!

14 • 8030 Final Exam

2022 TAX FILING SEASON UPDATE #8030 - COURSE EVALUATION

Rate on a scale of 1-10 with 1 being poor and 10 being excellent.

1. The course met the course objectives described in the promotional material. ______

2. The course was up to date, held my interest, was timely, and effective. ______

3. The course materials were understandable, valuable, and suitable for a correspondence course. ______

4. The amount of advance knowledge and stated prerequisites were appropriate. ______

5. The completion time was appropriate for the number of credits allowed. ______

6. The course met my professional education needs. ______

Please answer the following questions – mark/rate any and all that may apply

1. How would you rate PES’s order desk ______ customer service ______

2. What can PES do to keep you as a valued customer? __________________________________

_____________________________________________________________________________

_____________________________________________________________________________

_____________________________________________________________________________

_____________________________________________________________________________

3. Any other comments regarding this course or our company would be appreciated. ____________

_____________________________________________________________________________

_____________________________________________________________________________

_____________________________________________________________________________

_____________________________________________________________________________

4. What other courses/subjects would you like to see PES offer in the future? __________________

_____________________________________________________________________________

_____________________________________________________________________________

_____________________________________________________________________________

_____________________________________________________________________________

PLEASE MAIL YOUR EVALUATION TO: Professional Education Services, LP

4208 Douglas Blvd., Ste 50 • Granite Bay, CA 95746

THIS PAGE INTENTIONALLY LEFT BLANK.