Embed Size (px)

Citation preview

2021-2022Budget Workshop

February 22, 2021

Agenda

● Historical Financial Data

● 2021-2022 Budget Parameters

● Preliminary Five-Year Financial Plan

● Fund Balance Discussion

Impact of HB3 on GCISD Total Funding

2019-2020(old law)

2019-2020(new law) Difference

1 M&O Tax Collections $162,717,907 $151,765,740 ($10,951,357)

2 Recapture (64,377,182) (49,711,052) 14,666,130

3 M&O Tax Collections remaining in GCISD $98,340,725 $102,054,688 $3,714,773

4 Total State Aid $9,551,701 $9,289,229 ($262,472)

5 Total GCISD Funding $107,892,426 $111,343,917 $3,452,301

Historical Financial Data

Year Cost of Living Increase

StartingTeacher

Pay Other

2020-2021 1% of Midpoint+Equity Adjustments $54,000 One-time payment—Greater of 1% or $500

2019-2020 Teachers with 1-5 Years – 3% of MidpointTeachers with 5+ Years – 3% of Midpoint +$500All other employees – 2% of Midpoint

$53,500 TASB Compensation Study and HB3 Requirements

2018-2019 2.5% of Midpoint + Equity Adjustments $51,500 TASB Compensation Study

2017-2018 2% of Midpoint $50,000 One-time payment – Greater of 1% or $500Auxiliary adjustment: raised minimum to $10.50/ hour plus 2%

2016-2017 2% $50,000

Historical Financial Data

q General Operating Fund Balance-

q As of 6/30/20 - $58,145,036

q 31.2% of Annual Operating Expenditures

q Fund Balance Policy = 20% of Annual Operating Expenditures

$0.00$10.00$20.00$30.00$40.00$50.00$60.00$70.00

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

2015

-16

2016

-17

2017

-18

2018

-19

2019

-20

Milli

ons

Fund Balance History

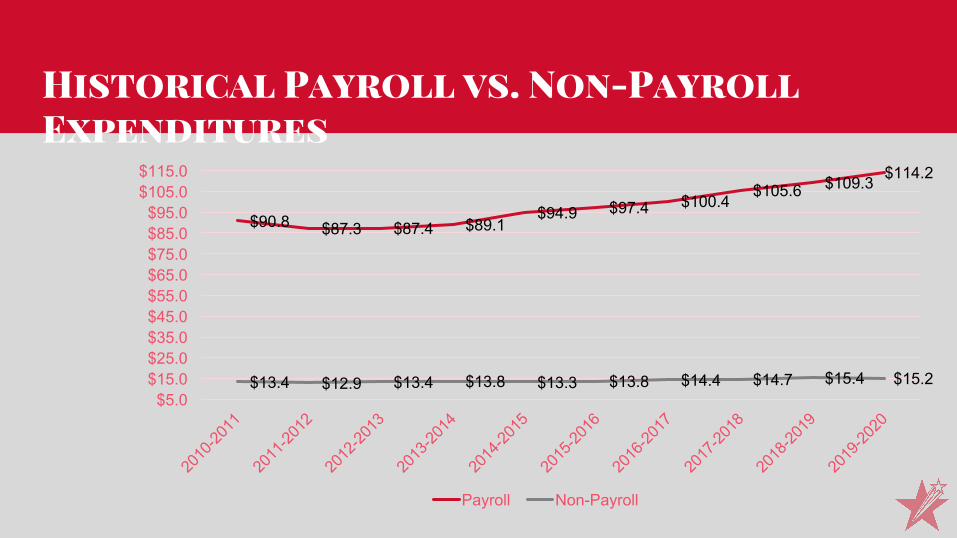

Historical Payroll vs. Non-Payroll Expenditures

$90.8 $87.3 $87.4 $89.1$94.9 $97.4 $100.4 $105.6 $109.3 $114.2

$13.4 $12.9 $13.4 $13.8 $13.3 $13.8 $14.4 $14.7 $15.4 $15.2$5.0

$15.0$25.0$35.0$45.0$55.0$65.0$75.0$85.0$95.0

$105.0$115.0

Payroll Non-Payroll

Historical Financial Data

Fiscal Year Amended Budget

Actual Operating Results

2019-2020 ($5,251,244) $1,025,313

2018-2019 ($6,070,718) $185,275

2017-2018 ($4,399,427) $993,030

2016-2017 ($83,043) $2,734,144

2015-2016 ($9,256,224) ($2,803,542)

2014-2015 ($4,583,688) $276,832

2013-2014 ($8,389,244) $2,885,998

2012-2013 ($5,986,602) ($521,487)

2011-2012 $5,373,624 $9,493,117

2010-2011 $1,146,977 $7,890,871

GCISD Robin Hood Payment History

$0

$10

$20

$30

$40

$50

$60

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Milli

ons

Year Amount

2012 $28,968,997

2013 $27,857,927

2014 $24,248,621

2015 $24,412,421

2016 $25,140,386

2017 $30,665,351

2018 $44,223,887

2019 $53,798,333

2020 $49,715,634

2021* $53,830,394

Since Robin Hood was implemented in 1994, GCISD has paid over $784.1 Million to the State.

*Projected

2020-2021 Enrollment Data

Grade ProjectionsPEIMS

Snapshot

Differencefrom

Projections As of 2/22/21

Difference from

ProjectionsPre-K/EE 241 229 (12) 247 6

K 872 740 (132) 742 (130)

1 932 871 (61) 876 (56)

2-5 3,788 3,621 (96) 3,603 (185)

6-8 3,022 2,912 (110) 2,906 (116)

9-12 4,276 4,238 (39) 4,222 (54)

Total 13,131 12,611 (450) 12,596 (535)

iUprep 1,175 1,208 33 1,152 (23)

Grand Total 14,306 13,819 (417) 13,748 (558)

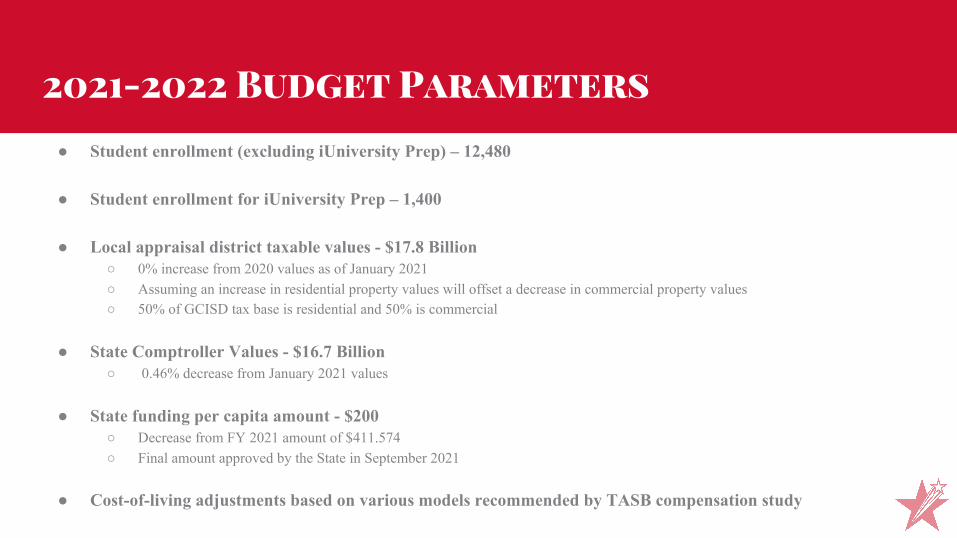

2021-2022 Budget Parameters

● Student enrollment (excluding iUniversity Prep) – 12,480

● Student enrollment for iUniversity Prep – 1,400

● Local appraisal district taxable values - $17.8 Billion ○ 0% increase from 2020 values as of January 2021○ Assuming an increase in residential property values will offset a decrease in commercial property values○ 50% of GCISD tax base is residential and 50% is commercial

● State Comptroller Values - $16.7 Billion○ 0.46% decrease from January 2021 values

● State funding per capita amount - $200○ Decrease from FY 2021 amount of $411.574○ Final amount approved by the State in September 2021

● Cost-of-living adjustments based on various models recommended by TASB compensation study

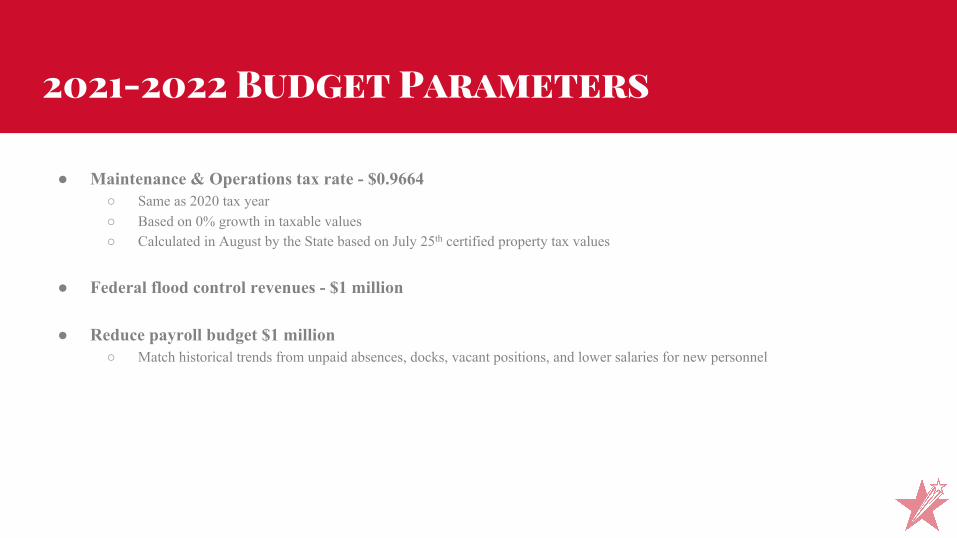

2021-2022 Budget Parameters

● Maintenance & Operations tax rate - $0.9664○ Same as 2020 tax year○ Based on 0% growth in taxable values○ Calculated in August by the State based on July 25th certified property tax values

● Federal flood control revenues - $1 million

● Reduce payroll budget $1 million○ Match historical trends from unpaid absences, docks, vacant positions, and lower salaries for new personnel

Five-Year Projection Assumptions: Student Data

2020-2021 2021-2022 2022-2023 2023-2024 2024-2025

1 Enrollment (Excluding iUprep) 12,611 12,480 12,351 12,337 12,329

2 iUniversity Prep Enrollment 1,208 1,400 1,500 1,600 1,700

3 TOTAL ENROLLMENT 13,819 13,880 13,851 13,937 14,029

4 Change from Prior Year 61 (29) 86 92

5 Average Daily Attendance (ADA) 13,357.89 13,196.23 13,161.16 13,244.82 13,334.68

6 Change from Prior Year (161.66) (35.07) 83.66 89.86

Note: All student population counts for allotments remain the same in all years.

Five-Year Projection Assumptions: Other Data Elements

2020-2021 2021-2022 2022-2023 2023-2024 2024-2025

1 Taxable Value Growth -- 0% 1% 2% 2%

2 CPTD Values $16.8 B $16.7 B $16.9 B $17.2 B $17.6 B

3 M&O Tax Rate $0.9664 $0.9664 $0.9538 $0.9414 $0.9292

4 Per Capita Rate $411.574 $200 $400 $200 $400

5 Cost of Living Adjustments -- 1% 1% 1% 1%

6 Inflation for Non-Payroll Costs -- 2% 2% 2% 2%

7 Teacher FTE Reductions -- 6 6 -- --

Note: Projections are based on current law.

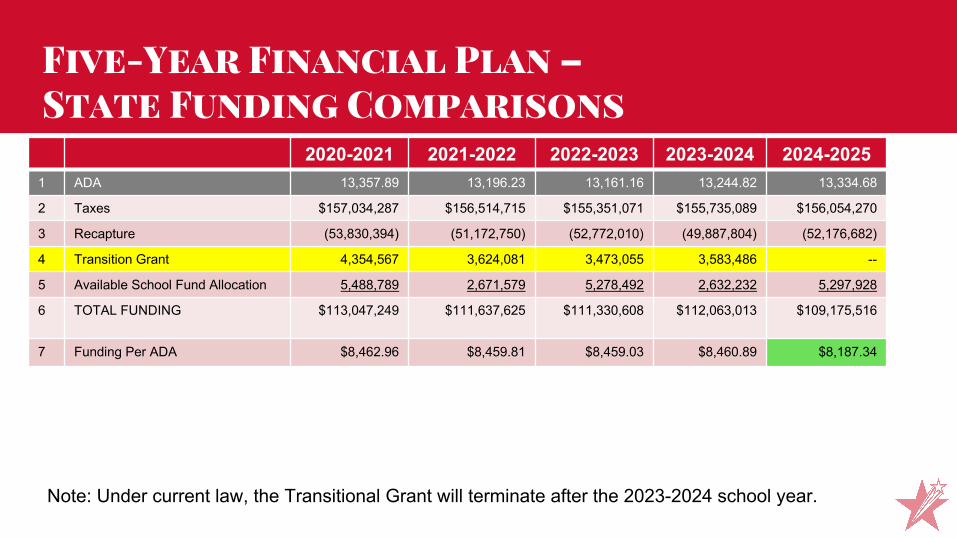

Five-Year Financial Plan –State Funding Comparisons

2020-2021 2021-2022 2022-2023 2023-2024 2024-20251 ADA 13,357.89 13,196.23 13,161.16 13,244.82 13,334.68

2 Taxes $157,034,287 $156,514,715 $155,351,071 $155,735,089 $156,054,270

3 Recapture (53,830,394) (51,172,750) (52,772,010) (49,887,804) (52,176,682)

4 Transition Grant 4,354,567 3,624,081 3,473,055 3,583,486 --

5 Available School Fund Allocation 5,488,789 2,671,579 5,278,492 2,632,232 5,297,928

6 TOTAL FUNDING $113,047,249 $111,637,625 $111,330,608 $112,063,013 $109,175,516

7 Funding Per ADA $8,462.96 $8,459.81 $8,459.03 $8,460.89 $8,187.34

Note: Under current law, the Transitional Grant will terminate after the 2023-2024 school year.

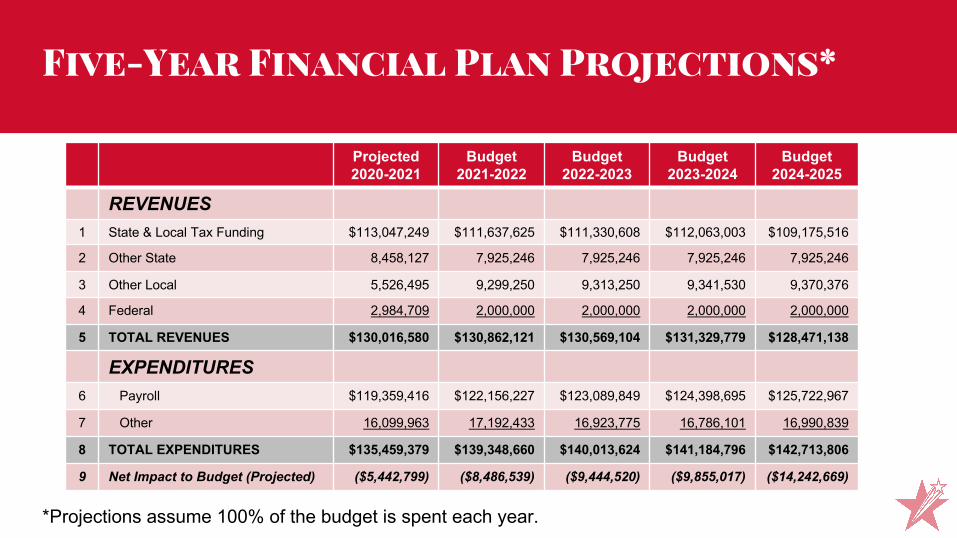

Five-Year Financial Plan Projections*

Projected2020-2021

Budget2021-2022

Budget2022-2023

Budget2023-2024

Budget2024-2025

REVENUES1 State & Local Tax Funding $113,047,249 $111,637,625 $111,330,608 $112,063,003 $109,175,516

2 Other State 8,458,127 7,925,246 7,925,246 7,925,246 7,925,246

3 Other Local 5,526,495 9,299,250 9,313,250 9,341,530 9,370,376

4 Federal 2,984,709 2,000,000 2,000,000 2,000,000 2,000,000

5 TOTAL REVENUES $130,016,580 $130,862,121 $130,569,104 $131,329,779 $128,471,138

EXPENDITURES6 Payroll $119,359,416 $122,156,227 $123,089,849 $124,398,695 $125,722,967

7 Other 16,099,963 17,192,433 16,923,775 16,786,101 16,990,839

8 TOTAL EXPENDITURES $135,459,379 $139,348,660 $140,013,624 $141,184,796 $142,713,806

9 Net Impact to Budget (Projected) ($5,442,799) ($8,486,539) ($9,444,520) ($9,855,017) ($14,242,669)

*Projections assume 100% of the budget is spent each year.

Five-Year Financial Plan-Fund Balance Analysis

2020-2021 2021-2022 2022-2023 2023-2024 2024-2025

1 Beginning Fund Balance $58,145,036 $52,702,237 $44,215,699 $34,771,180 $24,916,162

2 Net Change (Projected)* (5,442,799) (8,486,538) (9,444,519) (9,855,018) (14,242,669)

3 Ending Fund Balance $52,702,237 $44,215,699 $34,771,180 $24,916,162 $10,673,493

4 Targeted Fund Balance(20% of Operating Costs) $37,857,955 $38,104,282 $38,557,127 $38,214,520 $38,978,098

5 Target Overage/(Shortage) $14,844,282 $6,111,417 ($3,785,947) ($13,298,358) ($28,304,605)

*Projections assume 100% of the budget is spent.

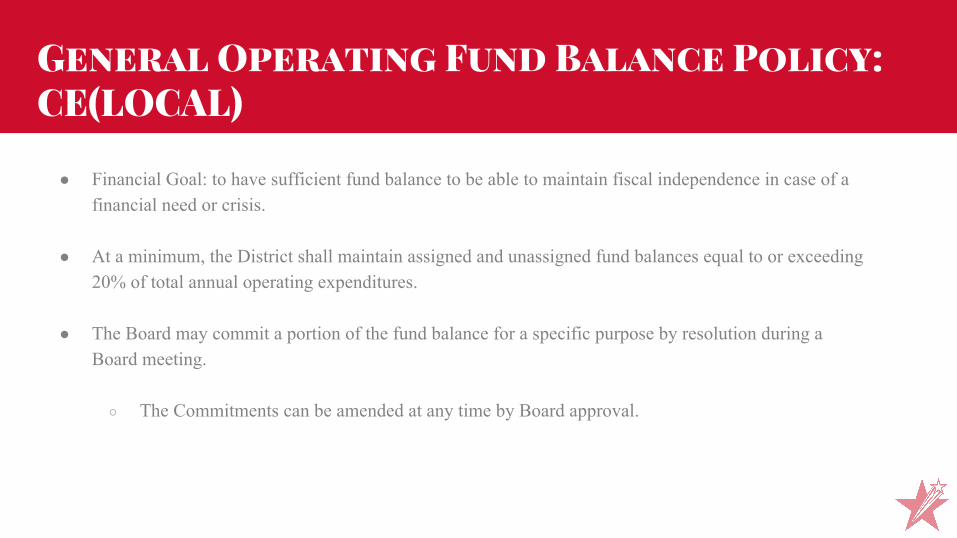

General Operating Fund Balance Policy: CE(LOCAL)

● Financial Goal: to have sufficient fund balance to be able to maintain fiscal independence in case of a financial need or crisis.

● At a minimum, the District shall maintain assigned and unassigned fund balances equal to or exceeding 20% of total annual operating expenditures.

● The Board may commit a portion of the fund balance for a specific purpose by resolution during a Board meeting.

○ The Commitments can be amended at any time by Board approval.

2019-2020 Ending Fund Balance Classifications

Non-Spendable Fund BalanceInventories $311,505

Prepaid Items 228,918

Total Non-Spendable Fund Balance $540,423

Committed Fund Balance*Major Maintenance Expenditures $4,000,000

Potential Claims & Judgements 500,000

Self Insurance Workers Comp Plan Claims 500,000

LEAD 2.0 Strategic Plan 2,524,734

Future Compensation Adjustments 5,000,000

Total Committed Fund Balance $12,524,734

Assigned & Unassigned Fund Balance

Assigned Fund Balance $6,280,823

Unassigned Fund Balance $38,799,056

Total Fund Balance $58,145,036

*Committed by resolution with Board approval.

Why is maintaining a General Operating Fund Balance Important?

v Measures the District’s financial stability

v CASH FLOW - Provides flexibility when District’s revenues are not received and expenditures are not incurred in equal monthly amounts.

v Tax revenues collected during the months of November through January

v Financial Goal of GCISD – to have sufficient fund balance to be able to maintain fiscal independence in case of a financial need or crisis.

v Lower revenues (tax collections reduced/delayed, State funding reduced/delayed) or

v Higher expenditures (unfunded State mandates, gas and utility price fluctuations, contract increases)

v Unanticipated emergency, natural disaster, pandemic, etc.

Why is maintaining a General Operating Fund Balance Important?

v Fund balance should be used for “non-recurring” or “one time” expenditures and never used for “recurring expenditures” such as salaries.

v Pursuant to the Government Finance Officers Association “It is essential that governments maintain adequate levels of fund balance to mitigate current and future risks (e.g. revenue shortfalls and unanticipated expenditures).”

v Adequate fund balance is “Best Practice” of the following:

v Government Finance Officers Association

v Texas Education Agency

v Bond Rating Agencies

What is an Adequate Fund Balance?

Government Finance Officers Association recommends at a minimum at least 2 months of General Fund revenues or expenditures

Texas Education Agency Financial Integrity Rating System of Texas (FIRST) ratings require an aggregate assigned & unassigned fund balance of more than 75 days (approximately 20%) of operational expenditures in order to receive “Superior Achievement” status.

GCISD Board Policy CED(LOCAL) requires at a minimum, the District shall maintain assigned and unassigned fund balances equal to or exceeding 20% of total annual operating expenditures.

What is an Adequate Fund Balance?

Bond Rating Agencies use fund balance as a measure of school districts’ financial solvency

Texas School District Medians for Moody’s Ratings-Fund Balance as a Percentage of Operating Revenues*

Description “Aaa” “Aa1” “Aa2” “Aa3”

Number of Texas Public School Districts Rated 8 25 43 67

General Fund Balance as a % of General Fund Revenues 35.7% 35.2% 35.3% 35.6%

GCISD 2019-2020 Fund Balance 32.29% of Total Revenues (less TIF)

*Source: BOK Financial Securities

What is an Adequate Fund Balance?

$0

$50

$100

$150

$200

$250

Milli

ons

Cash In Cash Out

2019-2020 Cash In* Cash Out* Difference

July $41.9 $39.5 $2.4

August 38.9 42.6 (3.7)

September 16.7 24.3 (7.6)

October 23.1 30.2 (7.1)

November 57.1 57.1 --

December 114.7 126.8 (12.1)

January 236.4 235.6 0.8

February 89.6 88.6 1.0

March 89.5 73.2 16.3

April 53.8 49.9 3.9

May 21.8 22.2 (0.4)

June 53.6 46.4 7.2

*Amounts in Millions.

2019-2020 Cash Flow

Questions??