Embed Size (px)

Citation preview

2020 OMS-MISO Survey ResultsFurthering our joint commitment to regional resource assessment and

transparency in the MISO region, OMS and MISO are pleased to

announce the results of the 2020 OMS-MISO Survey

June 2020

Projections and data do not account for impacts of recent and future tariff filings, including those related to Resource Availability & Need, and CoViD-19

Updates: - Slide 14 in the appendix added as an aid to slide 4 explaining stacked bars

- Slides 7 and 8 footnotes edited to re-emphasize that cross-zone transactions reported are

included in values shown

- Slides 5, 9 and 10 footnotes indicate ELCC applies to wind and 50% for solar

- Slides 9 and 10 “expected capacity credit” changed to “current new resource capacity credit”

- Slide 11 footnote indicates only resources within the zone are shown

- Slide 13 reference to GIA removed from unavailable resources indicating non-queue units

not counted

Region projected to have adequate resources in 2021, but

continued action needed to ensure sufficiency going forward

• MISO is projected to have 0.8 GW of firm capacity in excess of the 2021

regional Planning Reserve Margin (PRM), based on responses from

over 94% of MISO load and other non-LSE market participants. This

range could reach 7.2 GW if all potential resources are realized.

• Compared to last year, margins are tighter for both the first year and the

full-five year period of the survey. This is primarily driven by an increased

PRM and modest load growth.

• Since the 2019 Survey, additional resources help maintain the regional

balance, but some zones (2, 4, 6, and 7) show potential risk

• Projected demand growth rate rose just slightly, averaging over 0.3% per

year compared to 0.2% in 2019 Survey

• 2020 Survey marks first year using new OMS-MISO Survey module in

the Module E Capacity Tracking tool, which streamlines process for

respondents and MISO and improves data security

2

MISO Resource Adequacy Requirements

3

• Load serving entities within each

zone must have sufficient

resources to meet load and

required reserves

• Surplus resources may be

shared among load serving

entities with resource shortages

to meet reserve requirements

4.7

2.70.8

1.88.6 11.6

12.112.3

2021 2022 2023 2024 2025

Projected 0.8 GW regional surplus of committed resources in

2021, increasing need for firming additional resources thereafter

4

Projected Regional Installed Capacity (ICAP) Position

GW of surplus/deficit (% Reserves)

7.2 (23.8%)

11.2 (26.9%)

-3.5 (15.3%)

-5.6 (13.5%)-6.8 (12.6%)

• Appendix slide 14 added to further explain the ranges depicted above

• Regional outlook includes projected constraints on capacity, including the Sub-regional Power Balance Constraint (SRPBC)

• These figures will change as future capacity plans are solidified by load serving entities, state commissions, and local regulators

• Potential New Capacity represents capacity in the MISO Generator Interconnection Queue at projected queue certainty factors, updated since

the 2019 Survey (see slides 15 and 16), as of April 23, 2020

• Potentially Unavailable Resources includes potential retirements and capacity which may be constrained by future firm sales across the SRPBC

0.8 (18.6%) -0.4 (17.7%)

12.5 (27.9%)

10.0 (25.9%)

Potential New Capacity

Potentially Unavailable Resources

Committed Capacity Projections

1 d

ay in

10 P

lan

nin

g R

eserv

e M

arg

in P

RM

(18.0

%)

11.1 (26.6%)

4.54.6

4.3

3.1

1.1

0.3

1.1

1.1

2.1 2.1 1.60.8

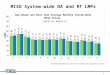

2021 supply balance is slightly lower due to changes in Planning

Reserve Margin, retirements and Load Modifying Resources

5

2021 Regional Outlook

Committed Capacity Projection Changes since 2019 OMS MISO SurveyGW (ICAP)

ForecastedRegional Surpluses:

2019 OMS-MISO Survey

ForecastedRegional Surplus:

2020 OMS-MISO Survey

Increased Reserve Requirement due to Resource and

Load Changes

Forecasted Load

Reductions

Increased Availability of

Resources since 2019

New resources include resources with newly signed Interconnection Agreements; wind at ELCC, solar at 50%

Increased availability results from potential resources from 2019 survey that are now committed resources

LMRs – Load Modifying Resources are Demand Response (DR) and Behind the Meter Generation (BTMG)

Changes in Load

Modifying Resources

New Firm Retirements Since 2019

New Resources Since 2019

1 d

ay i

n 1

0 P

RM

2.5

2.30.8

1.9 1.3

0.3

0.71.4

4.8 5.5

2020 2021 2022 2023 2024

Margins based on Committed Capacity are tighter

than last survey across all five years

66

Projected Capacity PositionICAP GW (% Reserves)

7.2 (23.8%)

11.2 (26.9%)

-3.5 (15.3%)-5.6 (13.5%)

-6.8 (12.6%)

0.8 (18.6%) -0.4 (17.7%)

12.5 (27.9%)10.0 (25.9%)11.1 (26.6%)

5.8 (21.4%)

4.1 (20.0%)

1.2 (17.7%)-1.3 (15.8%)

-2.3 (15.0%)

3.0 (19.2%) 1.1 (17.7%)

3.4 (19.5%)

6.7 (22.1%) 6.8 (22.2%)

2020 Survey

As Reported

2019 Survey

As Reported

Potential New Capacity

Potentially Unavailable Resources

Committed Capacity Projections

4.72.7

0.8

1.8 8.6 11.612.1 12.3

2021 2022 2023 2024 2025

• Appendix slide 14 added to further explain the ranges depicted above

0.8

6.5

In 2021, regional surpluses and transmission are

sufficient to cover zones with potential resource deficits

7

1 2 3 4 6 7 8 9

2021 Outlook (ICAP GW)

Lower MIMN, MT,

ND, SD,

West WI

East WI

and

Upper MI

IA IL IN

and KY

AR LA and

TX

1.8 to 2.3

-0.8 to -0.4

1.1 to 1.2

-2.3

4.8 to 4.9

1.3

5MO

10MS

-1.1

1.3 to 1.4

7.2 (23.8%)

0.8 (18.6%)0.0 to -0.1

0.8

Potential Capacity Projection

Committed Capacity Projection

0.4 to 0.51

day i

n 1

0 P

RM

1.0

1 day in 10

PRM (18.0%)

2021 Outlook,

ICAP GW (% Reserves)

• Regional surpluses and potential resources will be critical for all zones to serve their deficits while meeting local requirements

• Positions include reported contractual inter-zonal transfers, but do not reflect other possible transfers between zones

• Exports from Zones 8, 9, and 10 were limited by the Sub-regional Power Balance Constraint

0.6

1.91 day in 10

PRM (18.0%)

Continued focus on load growth changes and generation

additions and retirements will improve out-year uncertainty

8

10.0 (25.9%)

2025 Outlook,

ICAP GW (% Reserves)

-0.4

0.9 to 1.6

-3.4

3.5 to 4.9

0.7 to 1.1

-1.6

0.9 to 1.8

-0.4-6.8 (12.6%)

0.1

-3.0

1.2

1.7

-0.7

1.0

Potential Capacity Projection

Committed Capacity Projection 1 2 3 4 6 7 8 9Lower MIMN, MT,

ND, SD,

West WI

East WI

and

Upper MI

IA IL IN

and KY

AR LA and

TX

5MO

10MS

1 d

ay i

n 1

0 P

RM

2025 Outlook (ICAP GW)

• Regional surpluses and potential resources will be critical for all zones to serve their deficits while meeting local requirements

• Positions include reported contractual inter-zonal transfers, but do not reflect other possible transfers between zones

• Exports from Zones 8, 9, and 10 were limited by the Sub-regional Power Balance Constraint

5.0

14.3

18.219.6

20.6

0

5

10

15

20

25

2021 2022 2023 2024 2025

9

• Potential New Capacity represents capacity in the MISO Generator Interconnection Queue at projected queue

certainty factors as of April 23, 2020. Wind and solar resources are modeled shown at expected current new

resource capacity credit (ELCC for Wind, 50% for solar)

Future resource ranges will shift as planned generation

interconnections are firmed up

Not Started Phase 1 Phase 2 Phase 3Generator Interconnection Agreement Phase

Signed Generator Interconnection Agreement

Included in potential capacity1

Included in committed capacity

1“Potential capacity”

values shown here are

higher than amounts

shown on pg 4 because

they do not factor in

SRPBC limitations.

Forecasted resource mix changes continue to underpin a

number of initiatives in the MISO stakeholder process

10

• Wind and solar resources shown at expected current new resources capacity credit (ELCC for Wind, 50% for solar)

• Potential New Capacity represents the capacity in the MISO Generator Interconnection Queue at projected queue

certainty factors (see slide 15), as of April 23, 2020

2005 Capacity Mix 2025 Capacity Mix (Existing, Certain and

Potential New Resources)

Coal76%

Natural Gas and Other

Gases7%

Nuclear13%

Other4%

Coal31%

Natural Gas and Other Gases

42%

Nuclear8%

Solar3%

Wind3%

Other5%

DR/BTMG/EE8%

New generation and load modifying resources continue

to be important in meeting local resource needs

11• Includes only projected capacity resources within the zone, i.e. does not include imports and interzonal transfers

• Potential Capacity includes both new generation and potential retirements

• Load Modifying Resources include Demand Response (DR) and Behind the Meter Generation (BTMG)

-

5

10

15

20

25

30

Zone 1 Zone 2 Zone 3 Zone 4 Zone 5 Zone 6 Zone 7 Zone 8 Zone 9 Zone 10

2021 Local Clearing Requirement outlook (ICAP GW)

Committed Capacity Potential Capacity

Behind the Meter Generation Demand Response

Local Clearing Requirement

-

5

10

15

20

25

30

Zone 1 Zone 2 Zone 3 Zone 4 Zone 5 Zone 6 Zone 7 Zone 8 Zone 9 Zone 10

2025 Local Clearing Requirement outlook (ICAP GW)

Committed Capacity Potential Capacity

Behind the Meter Generation Demand Response

Local Clearing Requirement

Appendix

Understanding Resource Projections

• Committed Capacity Projections - resources committed to serving MISO load

• Resources within MISO utilities’ rate base

• New generators with signed interconnection agreements

• External resources with firm contracts to MISO load

• Non-rate base units without announced retirements or commitments to non-MISO load

• Potential Capacity Projections - resources that may be available to serve MISO load but do not have firm commitments to do so

• Potential retirements or suspensions

• Capacity in the MISO Generator Interconnection Queue at their expected current new resource capacity credit and projected queue certainty factors

• Unavailable resources are not included in the survey totals

• Resources with firm commitments to non-MISO load

• Resources with finalized retirements or suspensions

• Potential new generators without a signed Generator Interconnection Agreement or generators which have not entered the MISO Generator Interconnection Queue

13

-2.3

-6.8

4.5

12.3

0.8

4.7

1.8

0.8

Interpreting the range of resource balances shown

in the Survey summary

14

Potential New Capacity

Potentially Unavailable Resources

Committed Capacity Projections

Examples from MISO Region balance forecast on slides 4 and 6

Balance with only Committed

2025 Forecast

2021 Forecast

Add Potentially Unavailable

Add Potential New

Full range shown on p.4

5.5

7.2

-6.8

10.0

Balance with all 3 resources

Balance with only Committed

Balance with Committed plus Potentially Unavailable

Balance with all 3 resources

Balance with only Committed

Balance with Committed plus Potentially Unavailable

Balance with only Committed

Add Potentially Unavailable

Add Potential New

Full range shown on p.4

2020 OMS-MISO Survey Queue Treatment

Apply Capacity

Credit

Wind 16.6%

Solar 50%

All other 100%

Apply DPP Study Phase

Weighting

Not Started and

Phase 1= 10%

Phase 2 = 75% Non-Intermittent, 50%

Intermittent

GIA in Progress and Phase 3 = 90%

Requested In-Service Date

If requested in-service date is

prior to the first Survey year,

projects moved to their DPP

study cycle end date, unless an updated date

provided in the OMS-MISO

Survey

DPP Study Cycle Not Started

If DPP Study Cycle not

started, the requested in-

service dates are moved to the

DPP study cycle end date plus 2

years unless updated date

provided in the OMS-MISO

Survey

15

• DPP Study Phase Weighting is applied to recognize that as projects move through the queue process they generally

become more certain

• In-service adjusted if the DPP Study Cycle Not Started to recognize that a project likely can’t get capacity credit until at

least the end of the DPP study cycle and additional 2 years to to reflect expected GIA dates and construction timelines

• Yellow denotes changes form last year

Updated Queue Weights account for very

few phase 3 and low phase 2 withdrawals

2019 DPP Study Phase Weighting

Not Started/Phase 1 = 10%

Phase 2 = 50% Non-Intermittent / 25% Intermittent

Phase 3 = 75% Non-Intermittent / 50% Intermittent

GIA in Progress = 90%

16

2020 Proposed Weighting

Not Started/Phase 1 = No Change

Phase 2 = 75% Non-Intermittent / 50% Intermittent

GIA in Progress, Phase 3 = 90%

»

2019 by MW

• Yellow denotes changes form last year