Embed Size (px)

Citation preview

›2018 TD Securities Engineering & Construction Conference

›Sylvain Girard, EVP and CFO›March 27th, 2018

Forward-looking statementsReference in this presentation, and hereafter, to the “Company” or to “SNC-Lavalin” means, as the context may require, SNC-Lavalin Group Inc. and all or some of itssubsidiaries or joint arrangements, or SNC-Lavalin Group Inc. or one or more of its subsidiaries or joint arrangements.

Statements made in this presentation that describe the Company’s or management’s budgets, estimates, expectations, forecasts, objectives, predictions, projections of thefuture or strategies may be “forward-looking statements”, which can be identified by the use of the conditional or forward-looking terminology such as “aims”, “anticipates”,“assumes”, “believes”, “cost savings”, “estimates”, “expects”, “goal”, “intends”, “may”, “plans”, “projects”, “target”, “should”, “synergies”, “vision”, “will”, or the negative thereofor other variations thereon. Forward-looking statements also include any other statements that do not refer to historical facts. Forward-looking statements also includestatements relating to the following: (i) future capital expenditures, revenues, expenses, earnings, economic performance, indebtedness, financial condition, losses andfuture prospects; and (ii) business and management strategies and the expansion and growth of the Company’s operations. All such forward-looking statements are madepursuant to the “safe-harbour” provisions of applicable Canadian securities laws. The Company cautions that, by their nature, forward-looking statements involve risks anduncertainties, and that its actual actions and/or results could differ materially from those expressed or implied in such forward-looking statements, or could affect the extentto which a particular projection materializes. Forward-looking statements are presented for the purpose of assisting investors and others in understanding certain keyelements of the Company’s current objectives, strategic priorities, expectations and plans, and in obtaining a better understanding of the Company’s business andanticipated operating environment. Readers are cautioned that such information may not be appropriate for other purposes.

Forward-looking statements made in this presentation are based on a number of assumptions believed by the Company to be reasonable as at the date hereof. Theassumptions are set out throughout the Company’s 2017 Management Discussion and Analysis (MD&A). The 2018 outlook also assumes that the federal charges laidagainst the Company and its indirect subsidiaries SNC-Lavalin International Inc. and SNC-Lavalin Construction Inc. on February 19, 2015, will not have a significantadverse impact on the Company’s business in 2018. If these assumptions are inaccurate, the Company’s actual results could differ materially from those expressed orimplied in such forward-looking statements. In addition, important risk factors could cause the Company’s assumptions and estimates to be inaccurate and actual results orevents to differ materially from those expressed in or implied by these forward-looking statements. These risk factors are set out in the Company’s 2017 MD&A.

›The 2018 outlook referred to in this presentation is forward-looking information and is based on the methodology described in the Company’s 2017 MD&A under theheading “How We Budget and Forecast Our Results” and is subject to the risks and uncertainties described in the Company’s public disclosure documents. The purpose ofthe 2018 outlook is to provide the reader with an indication of management’s expectations, at the date of this presentation, regarding the Company’s future financialperformance and readers are cautioned that this information may not be appropriate for other purposes.

2

Non-IFRS financial measures and additional IFRS measures›The Company reports its financial results in accordance with IFRS. However, the following non-IFRS measures and additional IFRS measures are used by the Company:Adjusted net income from E&C, Adjusted diluted EPS from E&C, Adjusted net income from Capital, Adjusted diluted EPS from Capital, Adjusted consolidated diluted EPS,EBITDA, Adjusted E&C EBITDA, Segment EBIT and Revenue backlog. Additional details for these non-IFRS measures and additional measures can be found below and inSNC-Lavalin’s MD&A, which is available in the Investors section of the Company’s website at www.snclavalin.com. Non-IFRS financial measures do not have anystandardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. Management believes that, in addition toconventional measures prepared in accordance with IFRS, these non-IFRS measures provide additional insight into the Company’s financial results and certain investorsmay use this information to evaluate the Company’s performance from period to period. However, these non-IFRS financial measures have limitations and should not beconsidered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

A global fully integrated professional services & project management company leader

3

SNC-Lavalin is a global fully integrated professional services and project management company, and a major player in the ownership of infrastructure

From offices around the world,SNC-Lavalin’s employees are proud to build what matters, providing comprehensive end-to-end project solutions to clients in four industry sectors

Founded in

1911

Employees

50,000+

Revenue

$9.3B

Listed on TSX

“SNC”Since 1986

Investment Grade Credit Rating1

BBB

1 Per S&P and DBRS.

4

Atkins is one of the world’s most respected design, engineering and

project management consultancies

Their core business is helping our clients to plan, design and enable major

capital programs

›Atkins operates in a significant part of the value chain – providing solutions for the complete journey of

capital programs

2017Revenue(6 months)

$1.8B

2017Segment EBIT

(6 months)

11.4%

SNC-Lavalin acquired Atkins on July 3, 2017

52%

23%

14%

11%

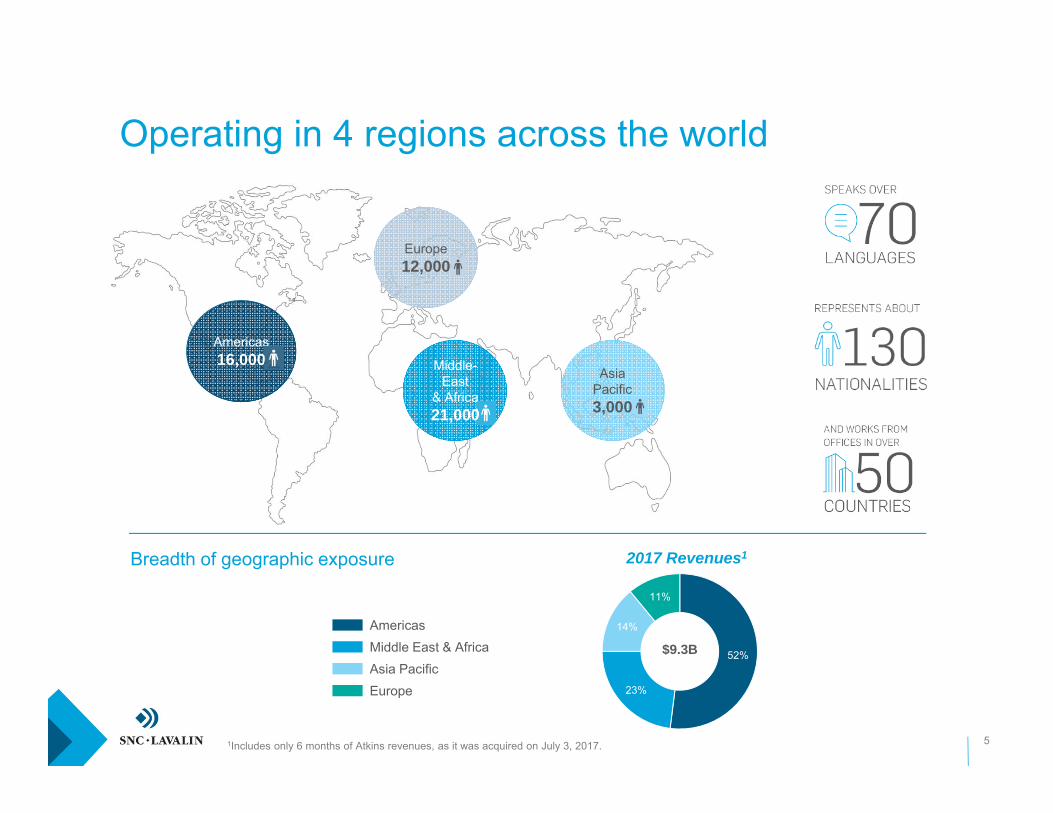

Operating in 4 regions across the world

5

Breadth of geographic exposure

Americas16,000

Europe12,000

Asia Pacific3,000

Middle-East

& Africa21,000

2017 Revenues1

$9.3B

Americas Middle East & AfricaAsia PacificEurope

1Includes only 6 months of Atkins revenues, as it was acquired on July 3, 2017.

31%

19%12%

4%

2%

32%

36%

23%

14%

5%

3%

19%

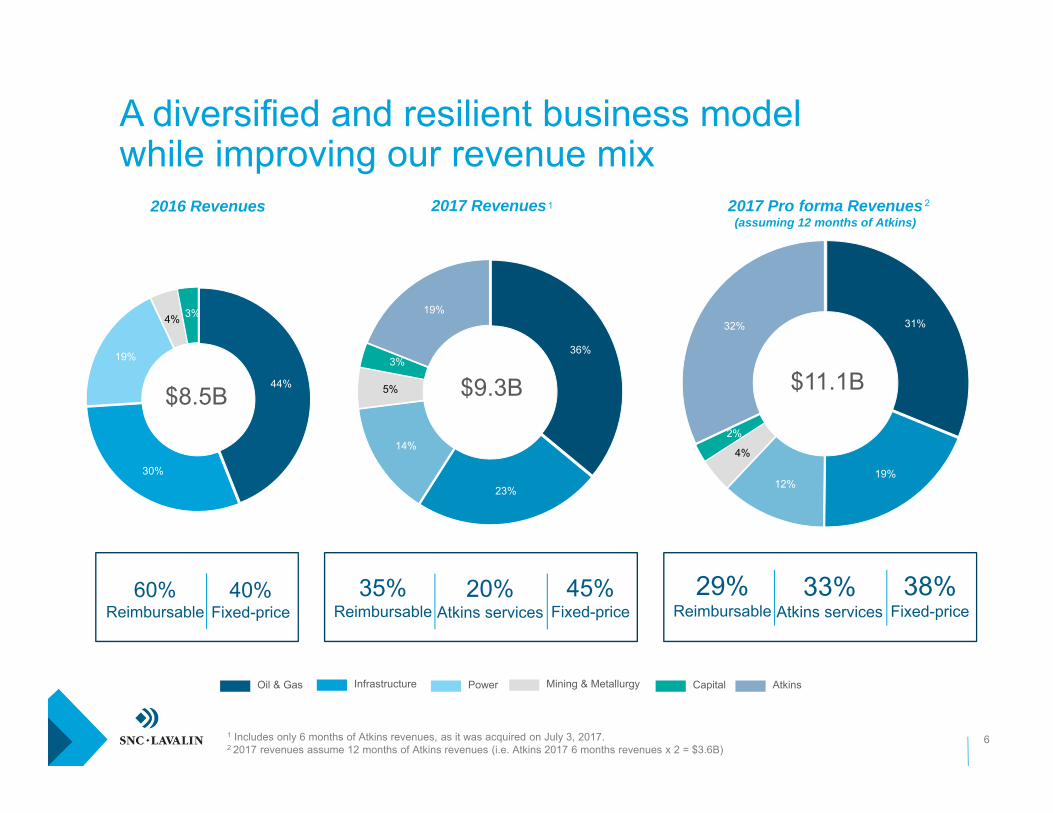

A diversified and resilient business modelwhile improving our revenue mix

6

2017 Revenues

Oil & Gas Infrastructure Power Mining & Metallurgy Capital

$9.3B

1

1 Includes only 6 months of Atkins revenues, as it was acquired on July 3, 2017.2 2017 revenues assume 12 months of Atkins revenues (i.e. Atkins 2017 6 months revenues x 2 = $3.6B)

Atkins

44%

30%

19%

4% 3%

2016 Revenues 2017 Pro forma Revenues (assuming 12 months of Atkins)

2

$8.5B $11.1B

29%Reimbursable

33%Atkins services

38%Fixed-price

35%Reimbursable

20%Atkins services

45%Fixed-price

60%Reimbursable

40%Fixed-price

7

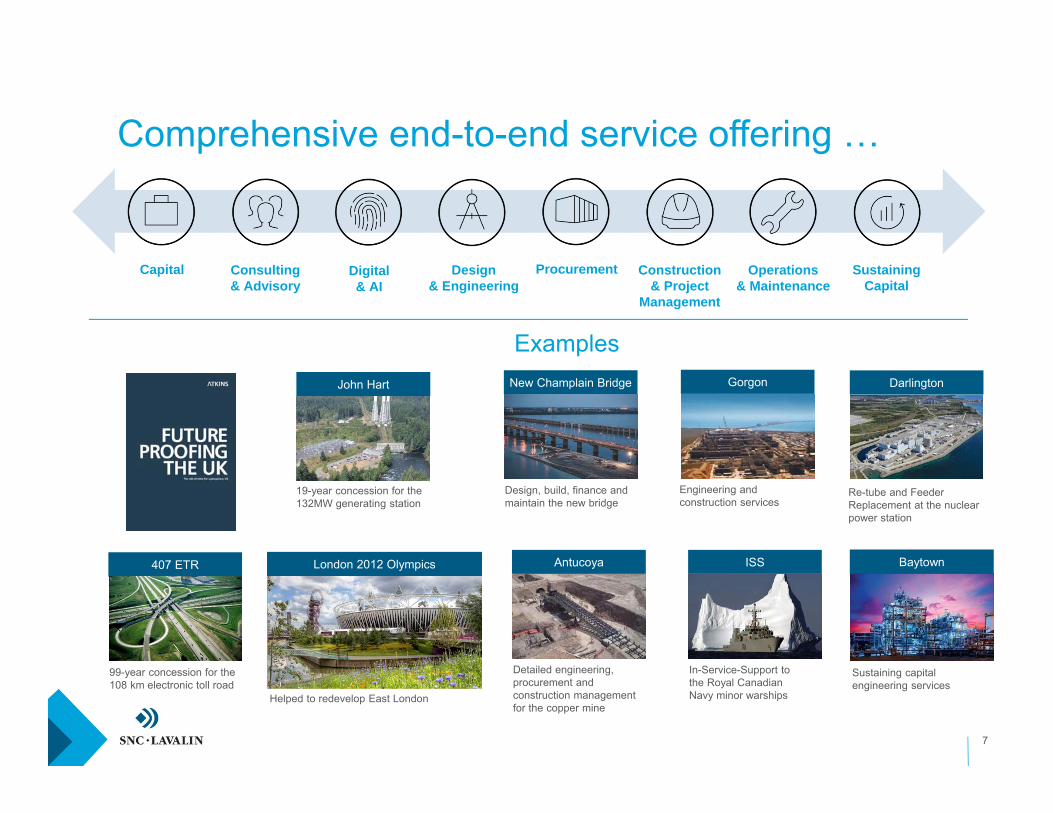

Comprehensive end-to-end service offering …

Capital Consulting& Advisory

Procurement Construction& Project

Management

Operations& Maintenance

Design& Engineering

Sustaining Capital

Digital& AI

John Hart

19-year concession for the 132MW generating station

407 ETR

99-year concession for the 108 km electronic toll road

Darlington

Re-tube and Feeder Replacement at the nuclear power station

New Champlain Bridge

Design, build, finance and maintain the new bridge

Gorgon

Engineering and construction services

Antucoya

Detailed engineering, procurement and construction management for the copper mine

Helped to redevelop East London

London 2012 Olympics ISS

In-Service-Support to the Royal Canadian Navy minor warships

Baytown

Sustaining capital engineering services

Examples

8

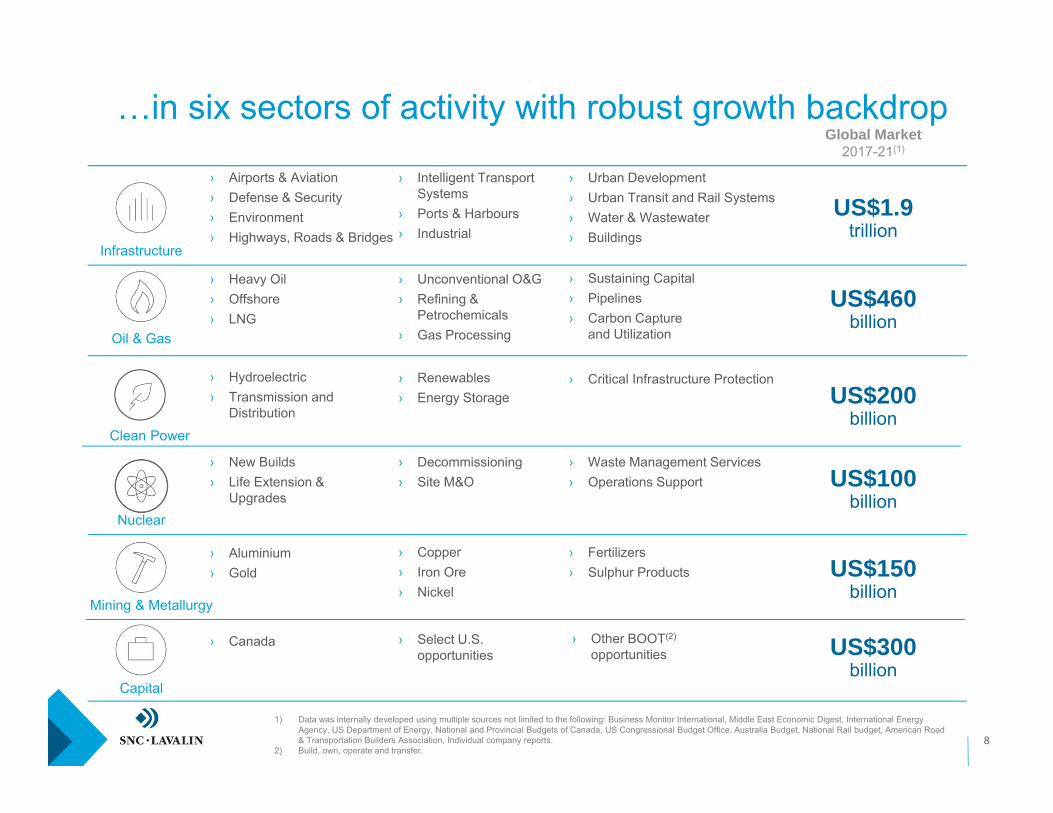

US$300billion

US$150billion

US$100billion

US$460billion

US$1.9trillion

…in six sectors of activity with robust growth backdropGlobal Market

2017-21(1)

› Airports & Aviation› Defense & Security› Environment› Highways, Roads & Bridges

› Urban Development› Urban Transit and Rail Systems› Water & Wastewater › Buildings

› Intelligent Transport Systems

› Ports & Harbours› Industrial

› Heavy Oil› Offshore› LNG

› Unconventional O&G› Refining &

Petrochemicals› Gas Processing

› Sustaining Capital› Pipelines› Carbon Capture

and Utilization

› New Builds› Life Extension &

Upgrades

› Hydroelectric› Transmission and

Distribution

› Renewables› Energy Storage

› Aluminium› Gold

› Copper› Iron Ore› Nickel

› Fertilizers› Sulphur Products

› Canada

1) Data was internally developed using multiple sources not limited to the following: Business Monitor International, Middle East Economic Digest, International Energy Agency, US Department of Energy, National and Provincial Budgets of Canada, US Congressional Budget Office, Australia Budget, National Rail budget, American Road & Transportation Builders Association, Individual company reports.

2) Build, own, operate and transfer.

Infrastructure

Oil & Gas

Clean Power

Mining & Metallurgy

Capital

› Select U.S. opportunities

› Other BOOT(2)

opportunities

Nuclear

› Decommissioning› Site M&O

› Waste Management Services› Operations Support

US$200billion

› Critical Infrastructure Protection

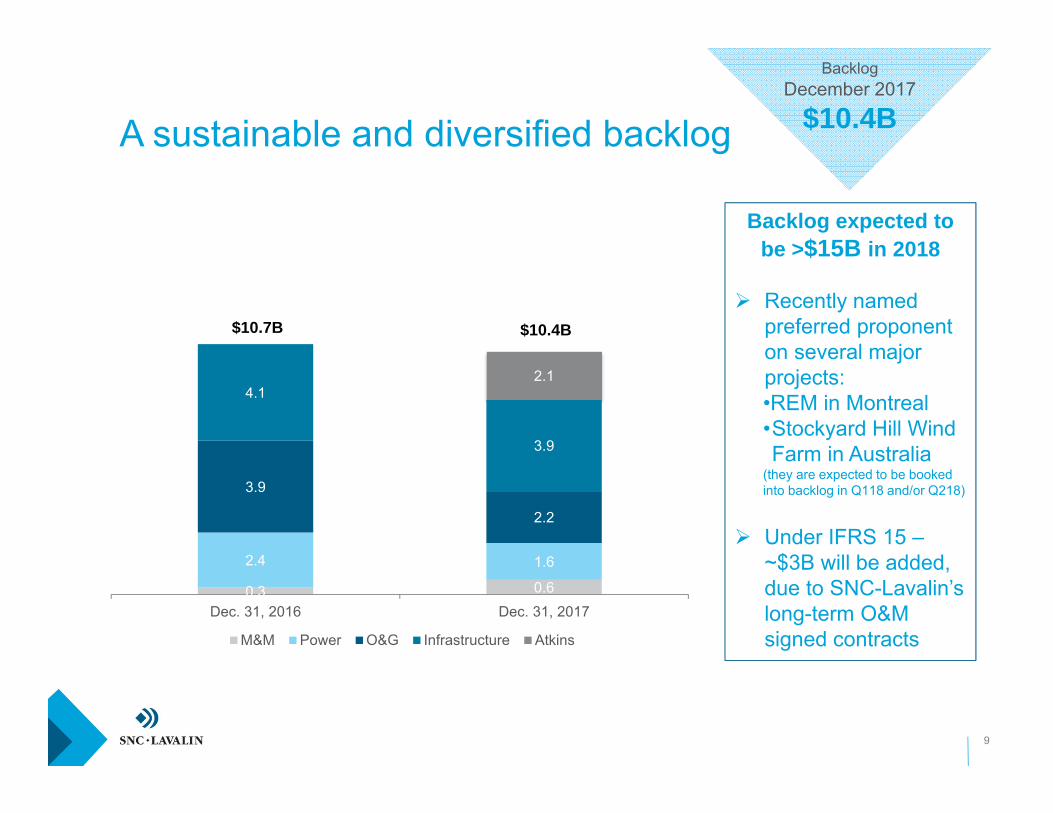

0.3 0.6

2.4 1.6

3.9

2.2

4.1

3.9

2.1

Dec. 31, 2016 Dec. 31, 2017

M&M Power O&G Infrastructure Atkins

9

A sustainable and diversified backlog

BacklogDecember 2017

$10.4B

$10.7B $10.4B

Backlog expected to be >$15B in 2018

Recently named preferred proponent on several major projects:•REM in Montreal•Stockyard Hill Wind Farm in Australia

(they are expected to be booked into backlog in Q118 and/or Q218)

Under IFRS 15 –~$3B will be added, due to SNC-Lavalin’s long-term O&M signed contracts

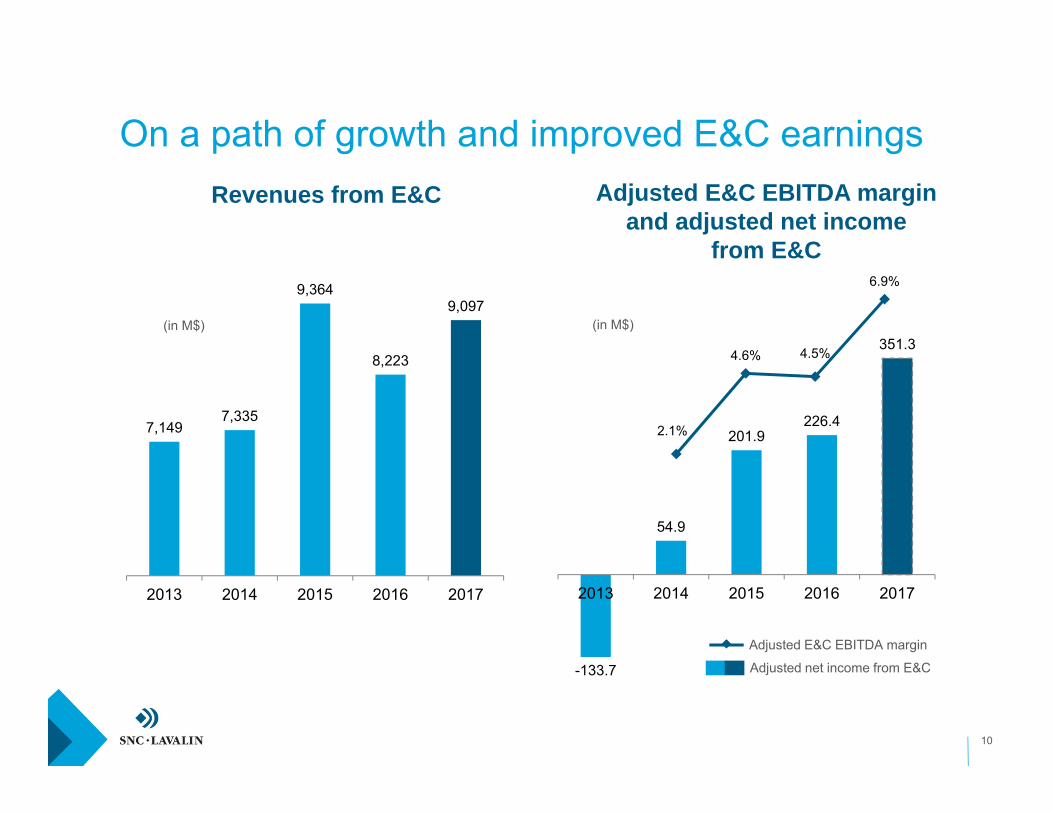

7,1497,335

9,364

8,223

9,097

2013 2014 2015 2016 2017

(in M$)

On a path of growth and improved E&C earnings

10

-133.7

54.9

201.9226.4

351.3

2013 2014 2015 2016 2017

(in M$)

Revenues from E&C Adjusted E&C EBITDA margin and adjusted net income

from E&C

2.1%

4.6% 4.5%

6.9%

Adjusted net income from E&C

Adjusted E&C EBITDA margin

11

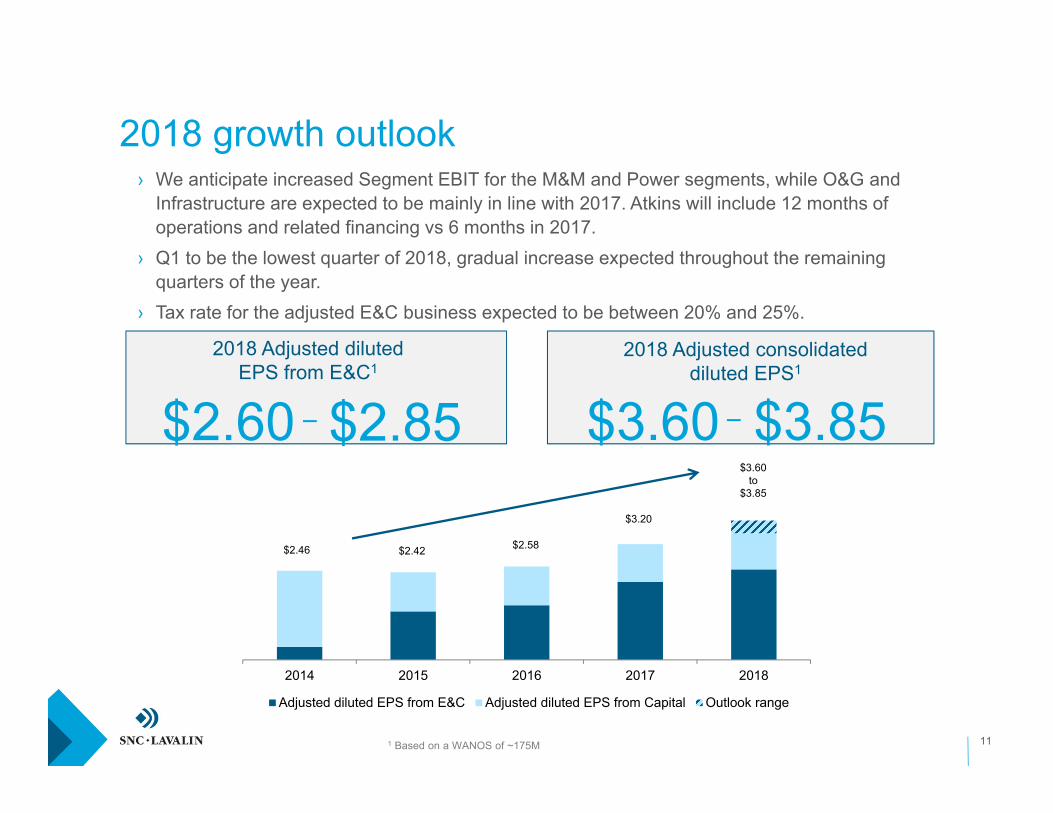

2018 Adjusted dilutedEPS from E&C1

$2.60 $2.85

2018 growth outlook› We anticipate increased Segment EBIT for the M&M and Power segments, while O&G and

Infrastructure are expected to be mainly in line with 2017. Atkins will include 12 months of operations and related financing vs 6 months in 2017.

› Q1 to be the lowest quarter of 2018, gradual increase expected throughout the remaining quarters of the year.

› Tax rate for the adjusted E&C business expected to be between 20% and 25%.

2018 Adjusted consolidateddiluted EPS1

$3.60 $3.85

2014 2015 2016 2017 2018

Adjusted diluted EPS from E&C Adjusted diluted EPS from Capital Outlook range

$2.46 $2.42 $2.58

$3.20

$3.60to

$3.85

1 Based on a WANOS of ~175M

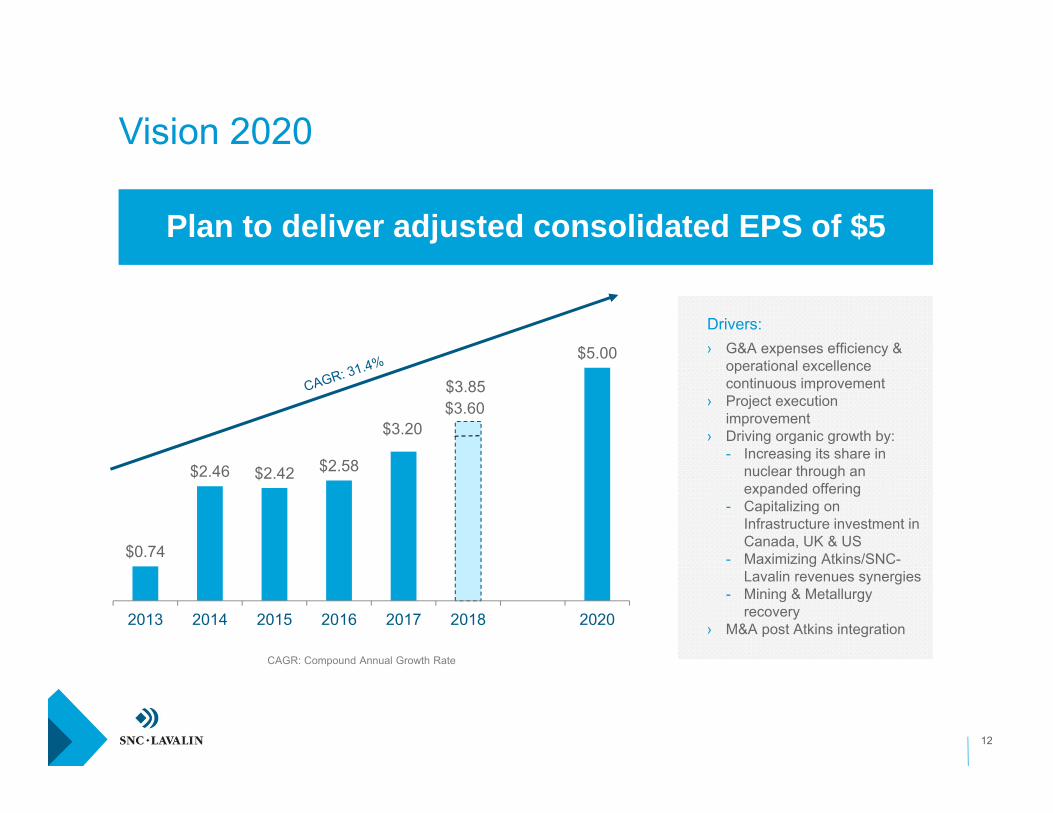

Plan to deliver adjusted consolidated EPS of $5

12

CAGR: Compound Annual Growth Rate

Drivers:› G&A expenses efficiency &

operational excellence continuous improvement

› Project execution improvement

› Driving organic growth by:- Increasing its share in

nuclear through an expanded offering

- Capitalizing on Infrastructure investment in Canada, UK & US

- Maximizing Atkins/SNC-Lavalin revenues synergies

- Mining & Metallurgy recovery

› M&A post Atkins integration

$0.74

$2.46 $2.42 $2.58

$3.20

$3.85

$5.00

2013 2014 2015 2016 2017 2018 2020

$3.60

Vision 2020

13

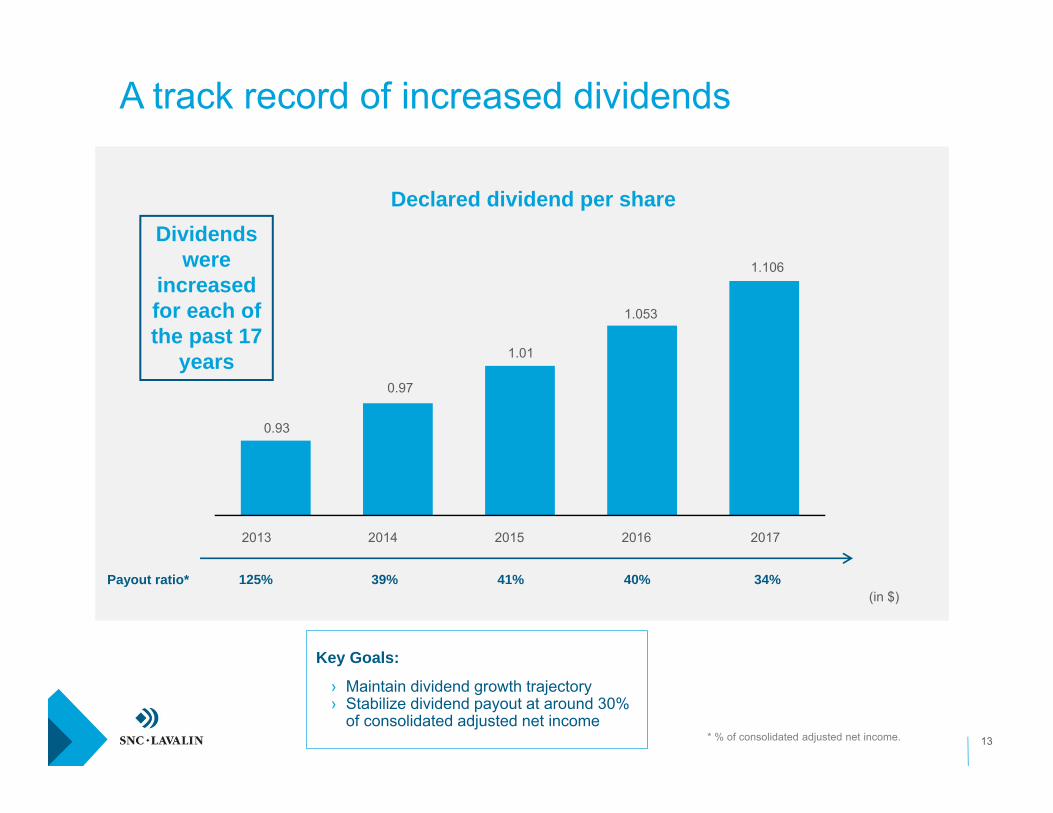

1.053

20152014

1.01

0.97

0.93

2013

1.106

20172016

Payout ratio* 125% 40%41%39% 34%(in $)

A track record of increased dividends

Dividends were

increased for each of the past 17

years

Declared dividend per share

* % of consolidated adjusted net income.

Key Goals:

› Maintain dividend growth trajectory› Stabilize dividend payout at around 30%

of consolidated adjusted net income

14

1 The Integrity Regime, in effect since July 2015, bars companies and their related legal entities from bidding on government contracts if they are charged with or convicted of certain criminal or administrative charges

September 2016Reached a compliance agreement with the Commissioner of Canada Elections in relation to an investigation by the Commissioner into certain reimbursements

September 2016Reached a compliance agreement with the Commissioner of Canada Elections in relation to an investigation by the Commissioner into certain reimbursements

5

December 2015SNC-Lavalin announces the first-ever administrative agreement with the Government of Canada under the Integrity Regime1

December 2015SNC-Lavalin announces the first-ever administrative agreement with the Government of Canada under the Integrity Regime1

February 2015Received Authorization From AMF to Contract With Public Authorities in Quebec

February 2015Received Authorization From AMF to Contract With Public Authorities in Quebec

October 2015Reached a settlement with the African Development Bank Group (AfDB) regarding allegations of sanctionable practices

October 2015Reached a settlement with the African Development Bank Group (AfDB) regarding allegations of sanctionable practices

21 3

May 2016Participation in the Quebec government's Voluntary Reimbursement Program. The program was put into force by the Government of Quebec in November 2015

May 2016Participation in the Quebec government's Voluntary Reimbursement Program. The program was put into force by the Government of Quebec in November 2015

4

Our ethics and compliance

program is an integral part ofdaily activities

Fostering an ethical culture to prevent the likelihood of wrongdoing and compliance violations from occurring

Providing internal controls and other sources to identify misconduct and evaluate adherence

Involving measures to take corrective action in response to misconduct

1)Feb-15

2)Oct-15

3)Dec-15

4)May-16

5)Sep-16

Ethics & compliance integrated in the way we work

December 2017Reached an agreement with all the public bodies of Quebec that have received its offer under the Voluntary Reimbursement Program

December 2017Reached an agreement with all the public bodies of Quebec that have received its offer under the Voluntary Reimbursement Program

6

6)Dec-17

Ethics & compliance update

February 2018Based on the consultation conducted in fall 2017, the Government of Canada intends to introduce legislation for Canadian Deferred Prosecution Agreements, to be implemented through Judicial Remediation Orders

February 2018Based on the consultation conducted in fall 2017, the Government of Canada intends to introduce legislation for Canadian Deferred Prosecution Agreements, to be implemented through Judicial Remediation Orders

77)

Feb-18

15

Investment in the global infrastructure sector is expected to grow, with the North American market particularly attractive

SNC-Lavalin: a unique platform to invest in the high growth infrastructure and power sector

1

2

4

3

6

5

Why

SN

C-L

aval

in

Leading international E&C firm of scale, the largest E&C firm in Canada and globally recognised

Optimally placed to capture market growth due to its diversified sector mix, extensive international presence and its competitive advantage from its presence across the value chain

SNC-Lavalin provides high visibility of revenues driven by a diversified backlog and complemented by a portfolio of prime infrastructure concessions which provide stable cashflows

Established track record of financial performance and strong balance sheet discipline that consistently delivers shareholder returns (strong track record of increased dividends)

Experienced management who have developed SNC-Lavalin into a well respected global brand and fostered a culture of Ethics excellence

16

SNC-Lavalin: a discounted share priceSNC-Lavalin Peers

GroupAverage1

PeersGroup incl.

Canadian peersAverage2

Share price3 $55.37

Less H4074 (25.91)

Less Other Concessions4

(2.82)

Adjusted E&C price $26.64

2018 adjusted EPS from E&C consensus4

$2.74

E&C P/E multiple 9.7 14.3 14.9

1 Includes Fluor, Jacobs, Wood, Balfour Beatty, WorleyParsons, CB&I and Aecom2 Incudes peers group + WSP and Stantec3 Close as at March 23, 20184 Street consensus as at March 23, 2018

SNC-Lavalin’s E&C P/E multiple ~ 5 times lower than peers

Appendix

18

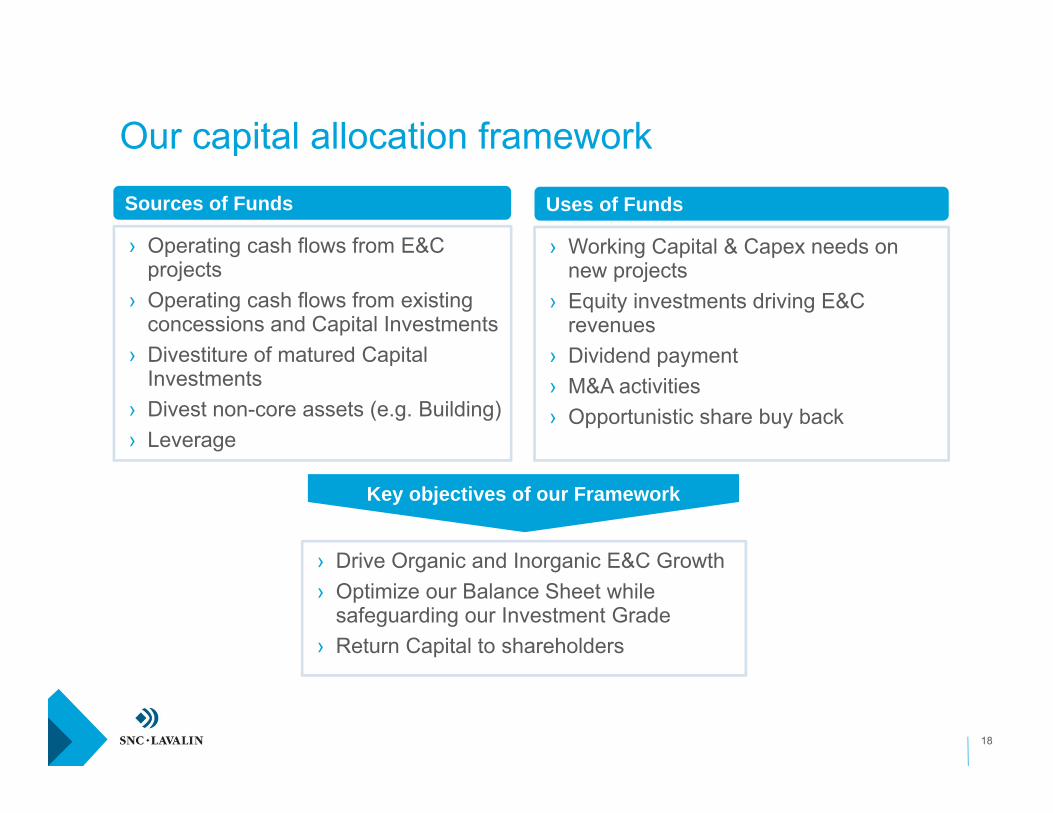

› Operating cash flows from E&C projects

› Operating cash flows from existing concessions and Capital Investments

› Divestiture of matured Capital Investments

› Divest non-core assets (e.g. Building)› Leverage

Sources of Funds

› Working Capital & Capex needs on new projects

› Equity investments driving E&C revenues

› Dividend payment› M&A activities› Opportunistic share buy back

Uses of Funds

› Drive Organic and Inorganic E&C Growth› Optimize our Balance Sheet while

safeguarding our Investment Grade› Return Capital to shareholders

Key objectives of our Framework

Our capital allocation framework

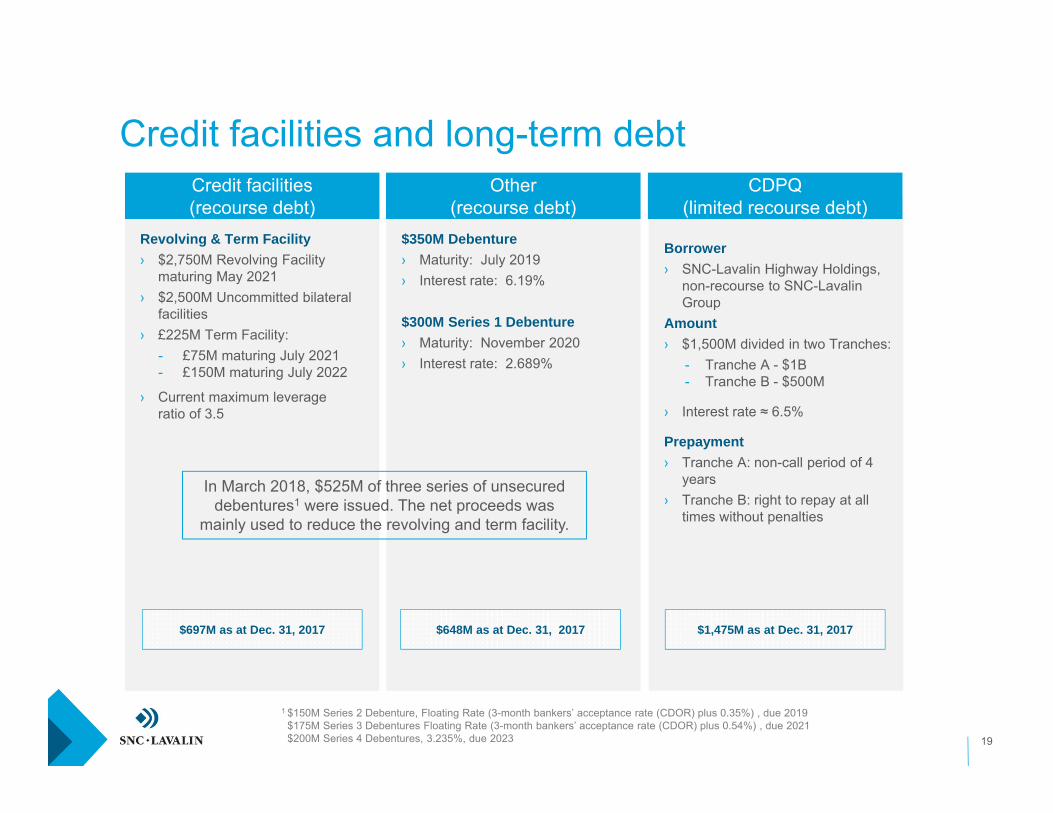

$350M Debenture› Maturity: July 2019› Interest rate: 6.19%

$300M Series 1 Debenture› Maturity: November 2020› Interest rate: 2.689%

Borrower› SNC-Lavalin Highway Holdings,

non-recourse to SNC-Lavalin Group

Amount› $1,500M divided in two Tranches:

- Tranche A - $1B- Tranche B - $500M

› Interest rate ≈ 6.5%

Prepayment› Tranche A: non-call period of 4

years› Tranche B: right to repay at all

times without penalties

19

Revolving & Term Facility› $2,750M Revolving Facility

maturing May 2021› $2,500M Uncommitted bilateral

facilities› £225M Term Facility:

- £75M maturing July 2021- £150M maturing July 2022

› Current maximum leverage ratio of 3.5

$648M as at Dec. 31, 2017

Credit facilities(recourse debt)

Other(recourse debt)

CDPQ(limited recourse debt)

Credit facilities and long-term debt

$697M as at Dec. 31, 2017 $1,475M as at Dec. 31, 2017

In March 2018, $525M of three series of unsecured debentures1 were issued. The net proceeds was

mainly used to reduce the revolving and term facility.

1 $150M Series 2 Debenture, Floating Rate (3-month bankers’ acceptance rate (CDOR) plus 0.35%) , due 2019$175M Series 3 Debentures Floating Rate (3-month bankers’ acceptance rate (CDOR) plus 0.54%) , due 2021$200M Series 4 Debentures, 3.235%, due 2023

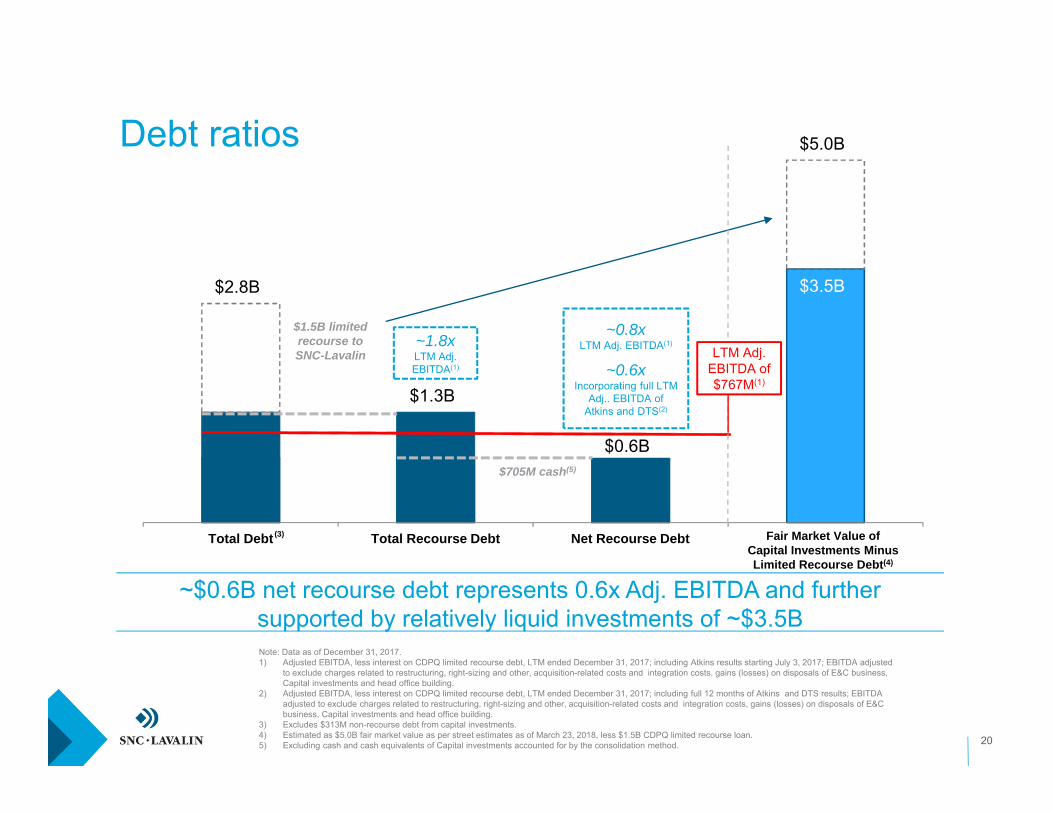

$3.5B $2.8B

$1.3B

$0.6B

$5.0B

Total Debt Total Recourse Debt Net Recourse Debt

20

$1.5B limited recourse to SNC-Lavalin

$705M cash(5)

~$0.6B net recourse debt represents 0.6x Adj. EBITDA and further supported by relatively liquid investments of ~$3.5B

LTM Adj. EBITDA of $767M(1)

Fair Market Value of Capital Investments Minus Limited Recourse Debt(4)

Note: Data as of December 31, 2017.1) Adjusted EBITDA, less interest on CDPQ limited recourse debt, LTM ended December 31, 2017; including Atkins results starting July 3, 2017; EBITDA adjusted

to exclude charges related to restructuring, right-sizing and other, acquisition-related costs and integration costs, gains (losses) on disposals of E&C business, Capital investments and head office building.

2) Adjusted EBITDA, less interest on CDPQ limited recourse debt, LTM ended December 31, 2017; including full 12 months of Atkins and DTS results; EBITDA adjusted to exclude charges related to restructuring, right-sizing and other, acquisition-related costs and integration costs, gains (losses) on disposals of E&C business, Capital investments and head office building.

3) Excludes $313M non-recourse debt from capital investments.4) Estimated as $5.0B fair market value as per street estimates as of March 23, 2018, less $1.5B CDPQ limited recourse loan.5) Excluding cash and cash equivalents of Capital investments accounted for by the consolidation method.

~1.8xLTM Adj. EBITDA(1)

~0.8xLTM Adj. EBITDA(1)

~0.6xIncorporating full LTM

Adj.. EBITDA of Atkins and DTS(2)

(3)

Debt ratios

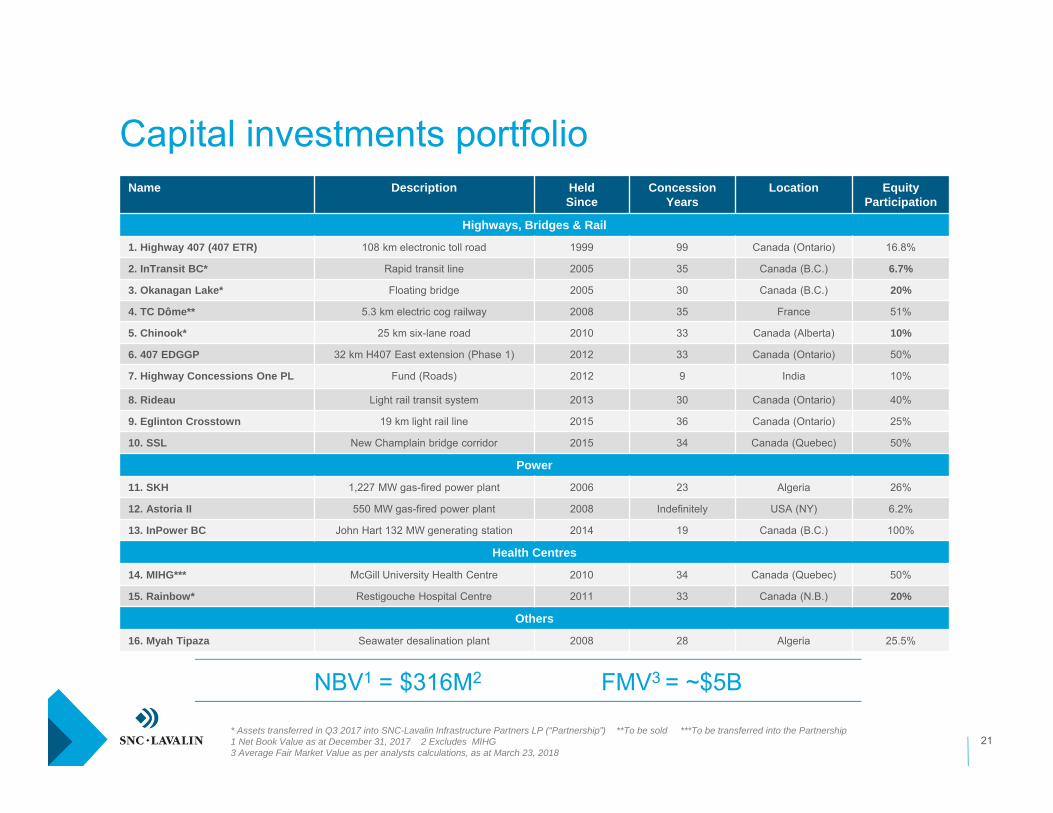

Name Description HeldSince

ConcessionYears

Location EquityParticipation

Highways, Bridges & Rail

1. Highway 407 (407 ETR) 108 km electronic toll road 1999 99 Canada (Ontario) 16.8%

2. InTransit BC* Rapid transit line 2005 35 Canada (B.C.) 6.7%

3. Okanagan Lake* Floating bridge 2005 30 Canada (B.C.) 20%

4. TC Dôme** 5.3 km electric cog railway 2008 35 France 51%

5. Chinook* 25 km six-lane road 2010 33 Canada (Alberta) 10%

6. 407 EDGGP 32 km H407 East extension (Phase 1) 2012 33 Canada (Ontario) 50%

7. Highway Concessions One PL Fund (Roads) 2012 9 India 10%

8. Rideau Light rail transit system 2013 30 Canada (Ontario) 40%

9. Eglinton Crosstown 19 km light rail line 2015 36 Canada (Ontario) 25%

10. SSL New Champlain bridge corridor 2015 34 Canada (Quebec) 50%

Power

11. SKH 1,227 MW gas-fired power plant 2006 23 Algeria 26%

12. Astoria II 550 MW gas-fired power plant 2008 Indefinitely USA (NY) 6.2%

13. InPower BC John Hart 132 MW generating station 2014 19 Canada (B.C.) 100%

Health Centres

14. MIHG*** McGill University Health Centre 2010 34 Canada (Quebec) 50%

15. Rainbow* Restigouche Hospital Centre 2011 33 Canada (N.B.) 20%

Others

16. Myah Tipaza Seawater desalination plant 2008 28 Algeria 25.5%

Capital investments portfolio

NBV1 = $316M2 FMV3 = ~$5B

* Assets transferred in Q3 2017 into SNC-Lavalin Infrastructure Partners LP (“Partnership”) **To be sold ***To be transferred into the Partnership1 Net Book Value as at December 31, 2017 2 Excludes MIHG 3 Average Fair Market Value as per analysts calculations, as at March 23, 2018

21

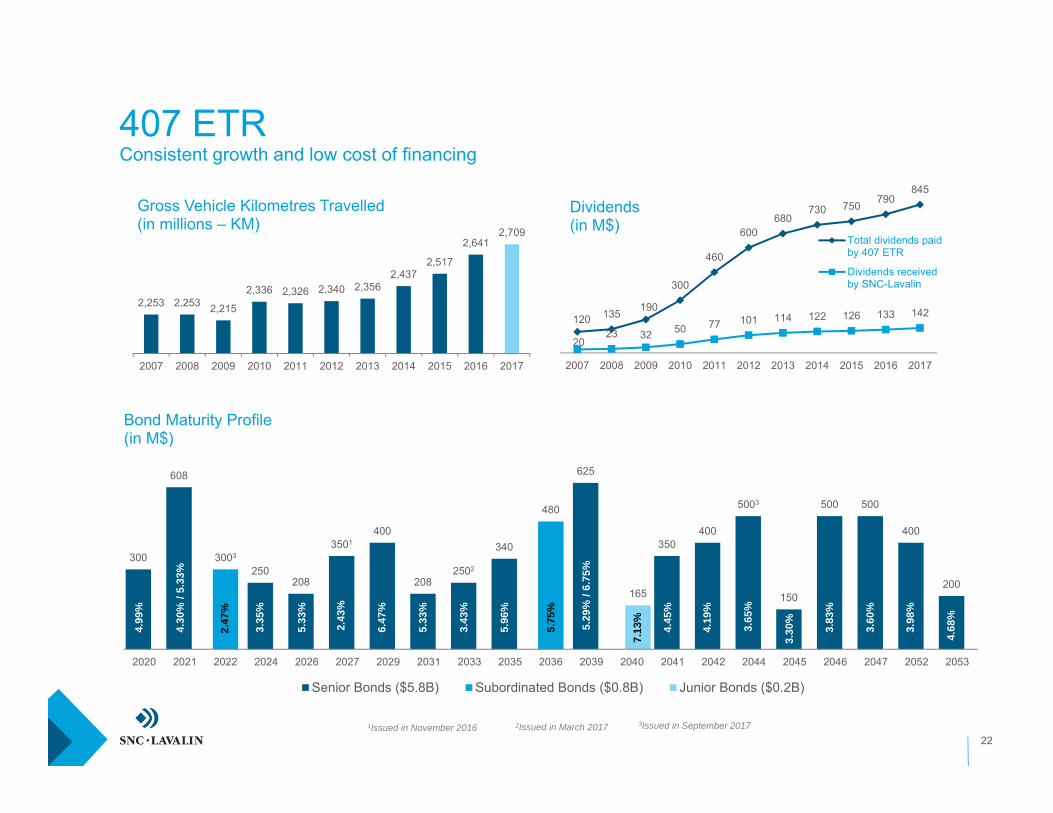

407 ETRConsistent growth and low cost of financing

22

120 135 190

300

460

600680

730 750 790845

2023 32 50 77 101 114 122 126 133 142

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Dividends (in M$)

Total dividends paidby 407 ETR

Dividends receivedby SNC-Lavalin

300

608

250208

3501400

2082502

340

625

350400

5003

150

500 500

400

200

3003

480

165

2020 2021 2022 2024 2026 2027 2029 2031 2033 2035 2036 2039 2040 2041 2042 2044 2045 2046 2047 2052 2053

Bond Maturity Profile(in M$)

Senior Bonds ($5.8B) Subordinated Bonds ($0.8B) Junior Bonds ($0.2B)

4.99

%

4.30

% /

5.33

%

3.35

%

5.33

%

6.47

%

5.33

%

5.96

%

5.75

%

7.13

%

4.45

%

4.19

%

3.30

%

3.83

%

3.98

%

4.68

%

3.60

%

5.29

% /

6.75

%

2.43

%

2,253 2,253 2,215

2,336 2,326 2,340 2,3562,437

2,517

2,6412,709

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Gross Vehicle Kilometres Travelled(in millions – KM)

1Issued in November 2016 2Issued in March 2017

3.43

%

2.47

%

3.65

%

3Issued in September 2017

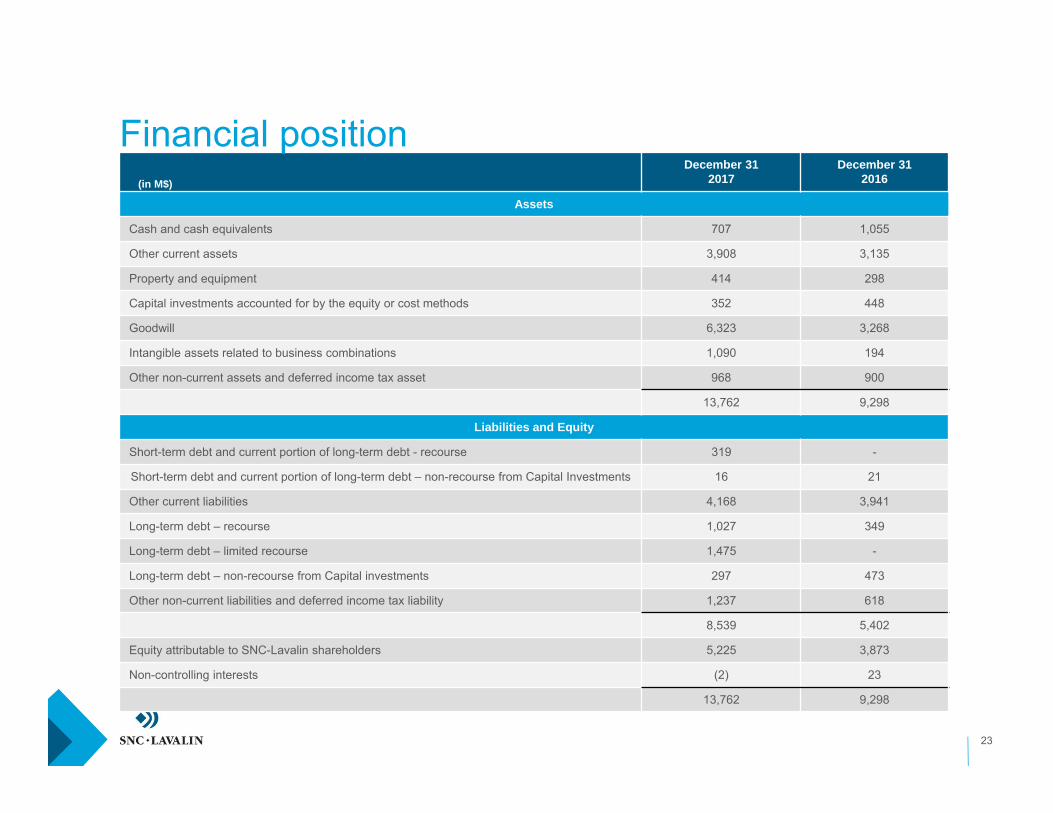

December 312017

December 312016

Assets

Cash and cash equivalents 707 1,055

Other current assets 3,908 3,135

Property and equipment 414 298

Capital investments accounted for by the equity or cost methods 352 448

Goodwill 6,323 3,268

Intangible assets related to business combinations 1,090 194

Other non-current assets and deferred income tax asset 968 900

13,762 9,298

Liabilities and Equity

Short-term debt and current portion of long-term debt - recourse 319 -

Short-term debt and current portion of long-term debt – non-recourse from Capital Investments 16 21

Other current liabilities 4,168 3,941

Long-term debt – recourse 1,027 349

Long-term debt – limited recourse 1,475 -

Long-term debt – non-recourse from Capital investments 297 473

Other non-current liabilities and deferred income tax liability 1,237 618

8,539 5,402

Equity attributable to SNC-Lavalin shareholders 5,225 3,873

Non-controlling interests (2) 23

13,762 9,298

Financial position

23

(in M$)

Our values

24

Our values are the essence of our Company’s identity. They represents how we act, speak and behave together, and how we engage with our clients and stakeholders.

SAFETY› We put safety at the heart of everything we do, to safeguard people, assets and the

environment

INTEGRITY› We do the right thing, no matter what, and are accountable for our actions

COLLABORATION› We work together and embrace each other’s unique contribution to deliver amazing results

for all

INNOVATION› We redefine engineering by thinking boldly, proudly and differently

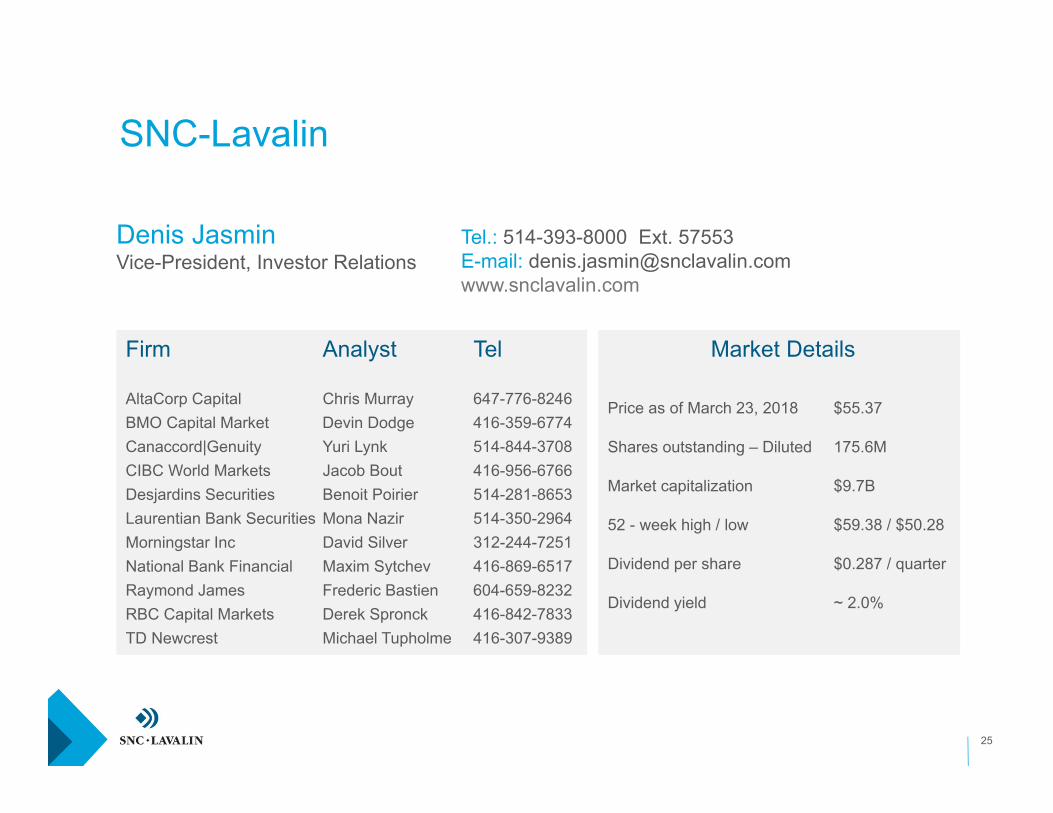

Firm Analyst Tel

AltaCorp Capital Chris Murray 647-776-8246BMO Capital Market Devin Dodge 416-359-6774Canaccord|Genuity Yuri Lynk 514-844-3708CIBC World Markets Jacob Bout 416-956-6766Desjardins Securities Benoit Poirier 514-281-8653Laurentian Bank Securities Mona Nazir 514-350-2964Morningstar Inc David Silver 312-244-7251National Bank Financial Maxim Sytchev 416-869-6517Raymond James Frederic Bastien 604-659-8232RBC Capital Markets Derek Spronck 416-842-7833TD Newcrest Michael Tupholme 416-307-9389

Price as of March 23, 2018 $55.37

Shares outstanding – Diluted 175.6M

Market capitalization $9.7B

52 - week high / low $59.38 / $50.28

Dividend per share $0.287 / quarter

Dividend yield ~ 2.0%

25

Tel.: 514-393-8000 Ext. 57553E-mail: [email protected]

SNC-Lavalin

Denis JasminVice-President, Investor Relations

Market Details