Embed Size (px)

Citation preview

2018 TAX UPDATE

Scott HensleyNovember 8, 2018

Stancil PCCPAs · Advisors

4909 Windy Hill DriveRaleigh, NC 27609

919-872-1260

© 2018 Stancil PC All Rights Reserved

Individual Income Tax Changes The New Qualified Business Income Tax Deduction Changes to Business Deductions and Tax Rates Planning Opportunities

TOPICS TO BE COVERED TODAY

© 2018 Stancil PC All Rights Reserved 3

The 2018 Tax Update

5

INDIVIDUAL INCOME TAX CHANGES

6

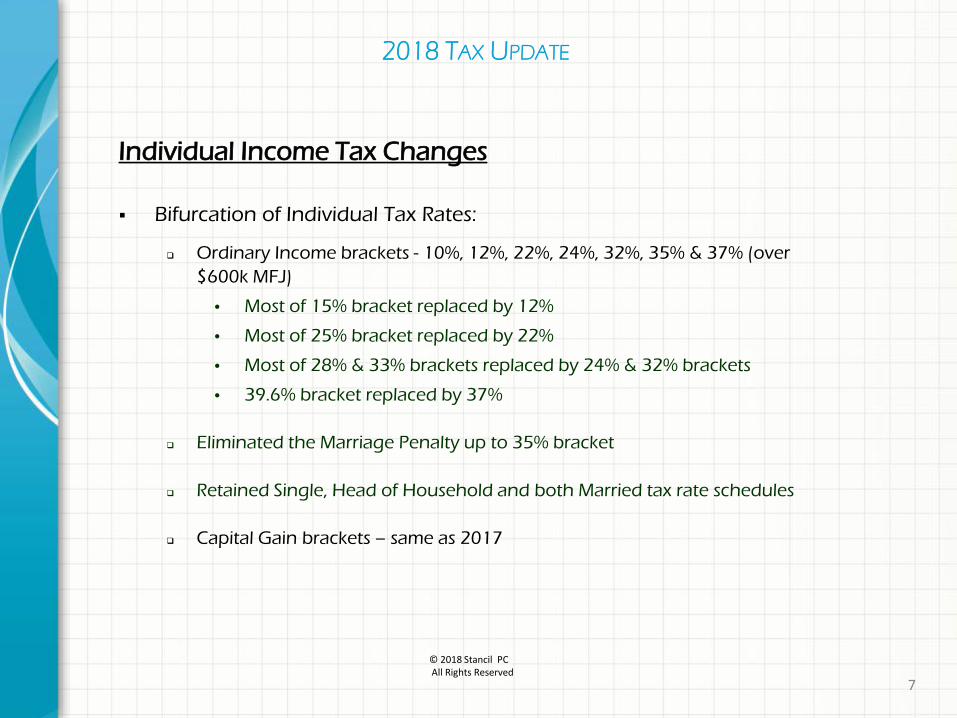

Individual Income Tax Changes

Bifurcation of Individual Tax Rates:

Ordinary Income brackets - 10%, 12%, 22%, 24%, 32%, 35% & 37% (over $600k MFJ)

• Most of 15% bracket replaced by 12%

• Most of 25% bracket replaced by 22%

• Most of 28% & 33% brackets replaced by 24% & 32% brackets

• 39.6% bracket replaced by 37%

Eliminated the Marriage Penalty up to 35% bracket

Retained Single, Head of Household and both Married tax rate schedules

Capital Gain brackets – same as 2017

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved

7

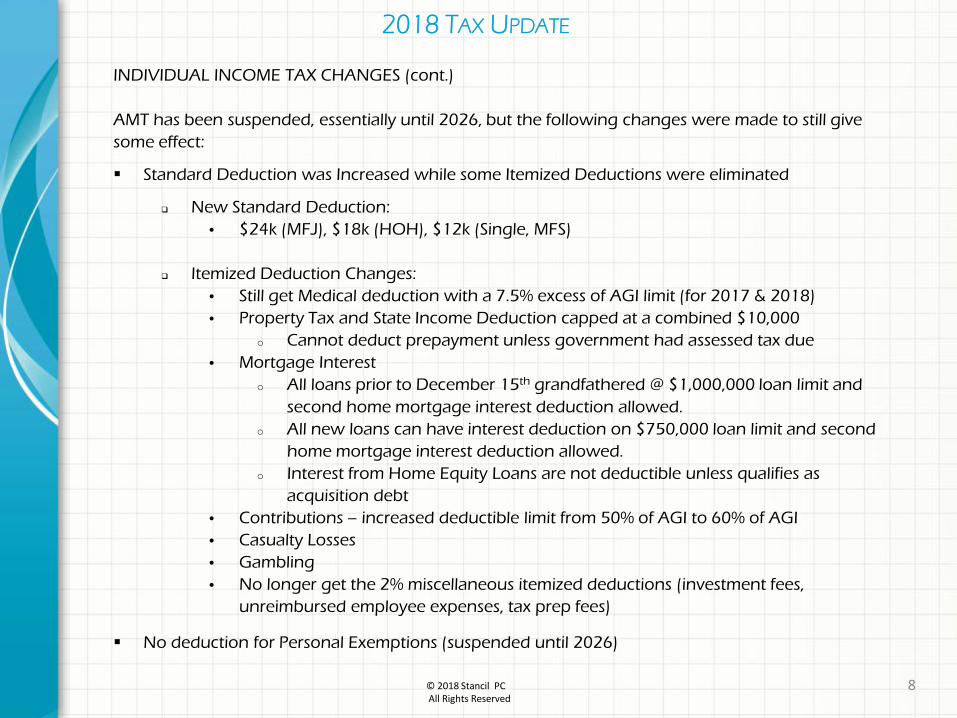

INDIVIDUAL INCOME TAX CHANGES (cont.)

AMT has been suspended, essentially until 2026, but the following changes were made to still give some effect:

Standard Deduction was Increased while some Itemized Deductions were eliminated

New Standard Deduction:• $24k (MFJ), $18k (HOH), $12k (Single, MFS)

Itemized Deduction Changes:• Still get Medical deduction with a 7.5% excess of AGI limit (for 2017 & 2018)• Property Tax and State Income Deduction capped at a combined $10,000

o Cannot deduct prepayment unless government had assessed tax due• Mortgage Interest

o All loans prior to December 15th grandfathered @ $1,000,000 loan limit and second home mortgage interest deduction allowed.

o All new loans can have interest deduction on $750,000 loan limit and second home mortgage interest deduction allowed.

o Interest from Home Equity Loans are not deductible unless qualifies as acquisition debt

• Contributions – increased deductible limit from 50% of AGI to 60% of AGI• Casualty Losses• Gambling• No longer get the 2% miscellaneous itemized deductions (investment fees,

unreimbursed employee expenses, tax prep fees)

No deduction for Personal Exemptions (suspended until 2026)

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved

8

INDIVIDUAL INCOME TAX CHANGES (cont.)

Other Notable Changes to Itemized Deductions/Standard Deduction:

Contributions:

Cannot deduct contributions to Colleges for right to purchase tickets

May STILL make qualified contributions from IRA to charity if 70 ½ or older

• Allowed to do so up to $100,000

• Major planning technique going forward for people that cannot itemize

Even though unreimbursed employee expenses are no longer deductible as an itemized deduction, an employee may still exclude all reimbursed employee expenses that are paid through an accountable plan.

Major planning technique for jobs where employees absorb most of cost

Higher Child and Dependent Credit to replace personal exemptions

Increase Refundable child credit to $2,000 for all qualifying children under 17

New $500 non-refundable credit for all other dependents

Phaseout of the credits starts at $400,000 MAGI and completely phases out at $440,000 MAGI

No longer phaseout of Itemized Deductions if income is too high

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved 9

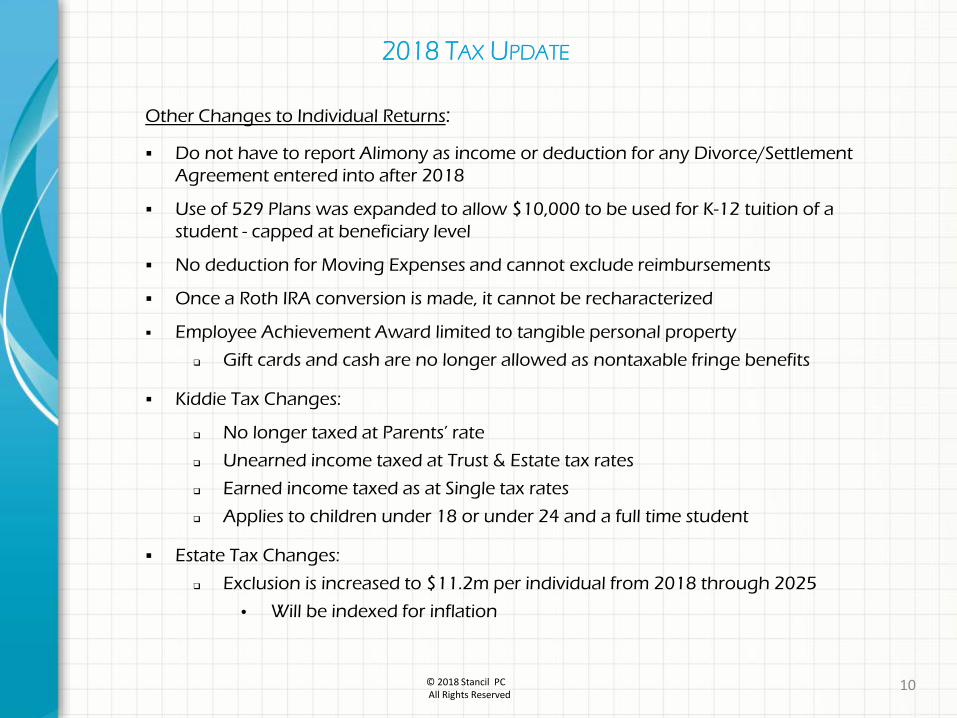

Other Changes to Individual Returns:

Do not have to report Alimony as income or deduction for any Divorce/Settlement Agreement entered into after 2018

Use of 529 Plans was expanded to allow $10,000 to be used for K-12 tuition of a student - capped at beneficiary level

No deduction for Moving Expenses and cannot exclude reimbursements

Once a Roth IRA conversion is made, it cannot be recharacterized

Employee Achievement Award limited to tangible personal property

Gift cards and cash are no longer allowed as nontaxable fringe benefits

Kiddie Tax Changes:

No longer taxed at Parents’ rate

Unearned income taxed at Trust & Estate tax rates

Earned income taxed as at Single tax rates

Applies to children under 18 or under 24 and a full time student

Estate Tax Changes:

Exclusion is increased to $11.2m per individual from 2018 through 2025

• Will be indexed for inflation

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved

10

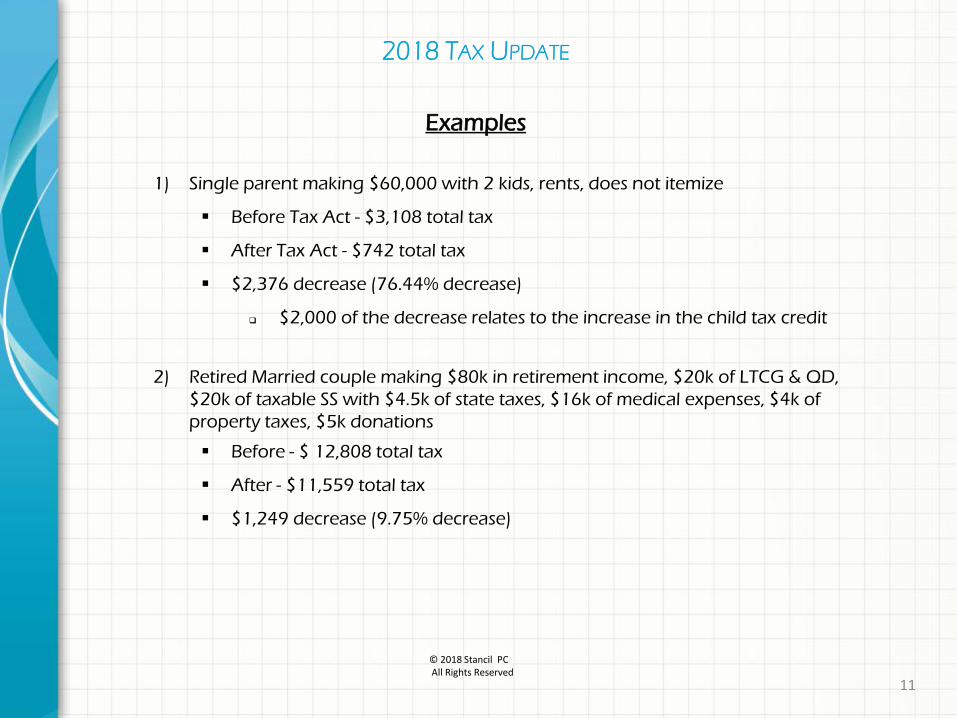

1) Single parent making $60,000 with 2 kids, rents, does not itemize

Before Tax Act - $3,108 total tax

After Tax Act - $742 total tax

$2,376 decrease (76.44% decrease)

$2,000 of the decrease relates to the increase in the child tax credit

2) Retired Married couple making $80k in retirement income, $20k of LTCG & QD, $20k of taxable SS with $4.5k of state taxes, $16k of medical expenses, $4k of property taxes, $5k donations

Before - $ 12,808 total tax

After - $11,559 total tax

$1,249 decrease (9.75% decrease)

2018 TAX UPDATE

Examples

© 2018 Stancil PC All Rights Reserved

11

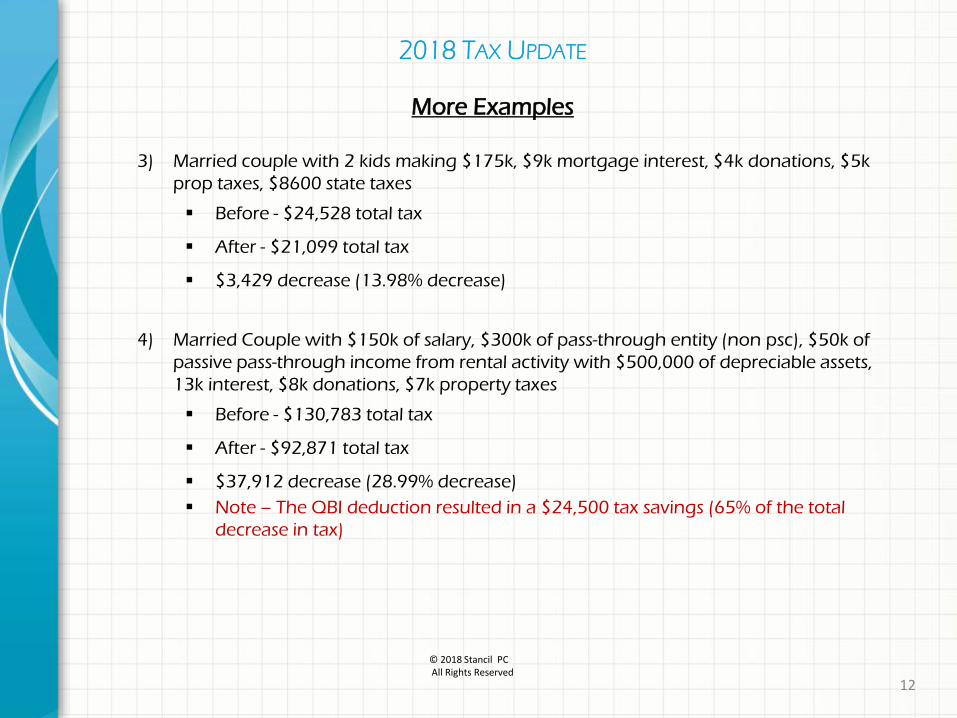

3) Married couple with 2 kids making $175k, $9k mortgage interest, $4k donations, $5k prop taxes, $8600 state taxes

Before - $24,528 total tax

After - $21,099 total tax

$3,429 decrease (13.98% decrease)

4) Married Couple with $150k of salary, $300k of pass-through entity (non psc), $50k of passive pass-through income from rental activity with $500,000 of depreciable assets, 13k interest, $8k donations, $7k property taxes

Before - $130,783 total tax

After - $92,871 total tax

$37,912 decrease (28.99% decrease) Note – The QBI deduction resulted in a $24,500 tax savings (65% of the total

decrease in tax)

2018 TAX UPDATE

More Examples

© 2018 Stancil PC All Rights Reserved

12

THE NEW QUALIFIED BUSINESS INCOMETAX DEDUCTION (199A)

13

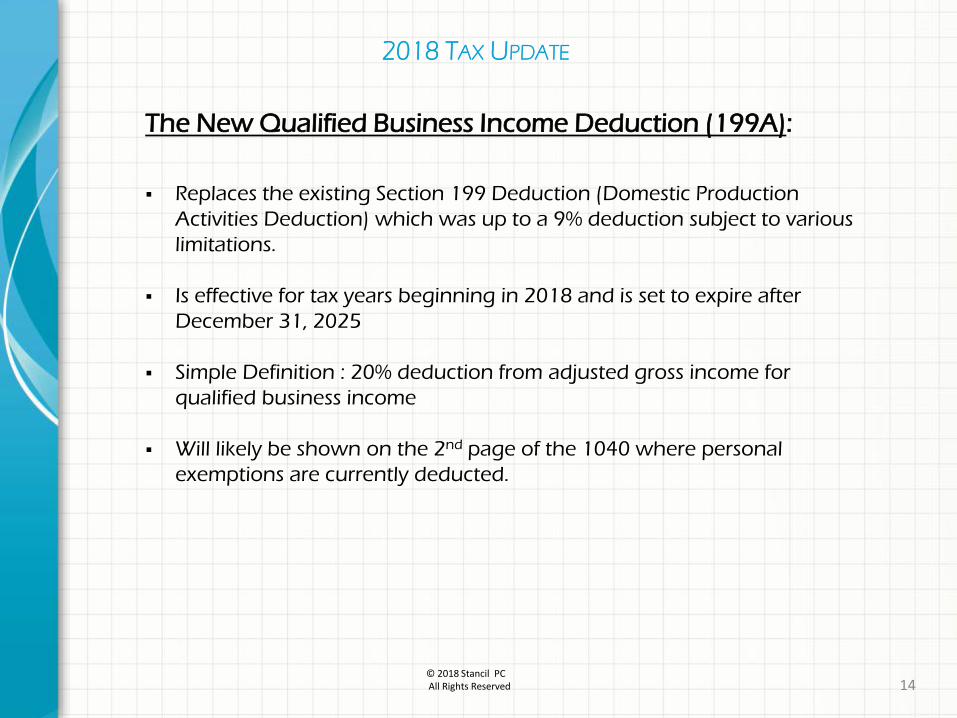

The New Qualified Business Income Deduction (199A):

Replaces the existing Section 199 Deduction (Domestic Production Activities Deduction) which was up to a 9% deduction subject to various limitations.

Is effective for tax years beginning in 2018 and is set to expire after December 31, 2025

Simple Definition : 20% deduction from adjusted gross income for qualified business income

Will likely be shown on the 2nd page of the 1040 where personal exemptions are currently deducted.

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved 14

The New Qualified Business Income Deduction (199A) (cont.)

The deduction is only for business income

Sole Proprietorships (Schedule C) Real Estate (Schedule E) Partnerships S-Corporations Trusts & Estates, REITS and Qualified Cooperatives

No deduction for wage earners

Some wage earners may wish to evaluate feasibility and tax implications of becoming self-employed

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved

15

The New Qualified Business Income Deduction (199A) (cont.)

Key Definition – Specified Service Trade or Business – taken from IRC Section 1202(e)(3)(A)

“Any trade or business involving the service in the fields of health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services or any trade or business where the principal asset of such trade or business is the reputation or skill of one or more its employees.”

Two professions were excluded – Architects and Engineers

Why does being a specified service business matter?

Deduction is phased-out as taxable income exceeds $315,000 for Marrieds and $157,500 for all other filing statuses.

No phase-out range exists for non-service businesses.

Phase out range is $315,000 - $415,000 for Marrieds and $157,500 -$207,500 for all other filing statuses.

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved

16

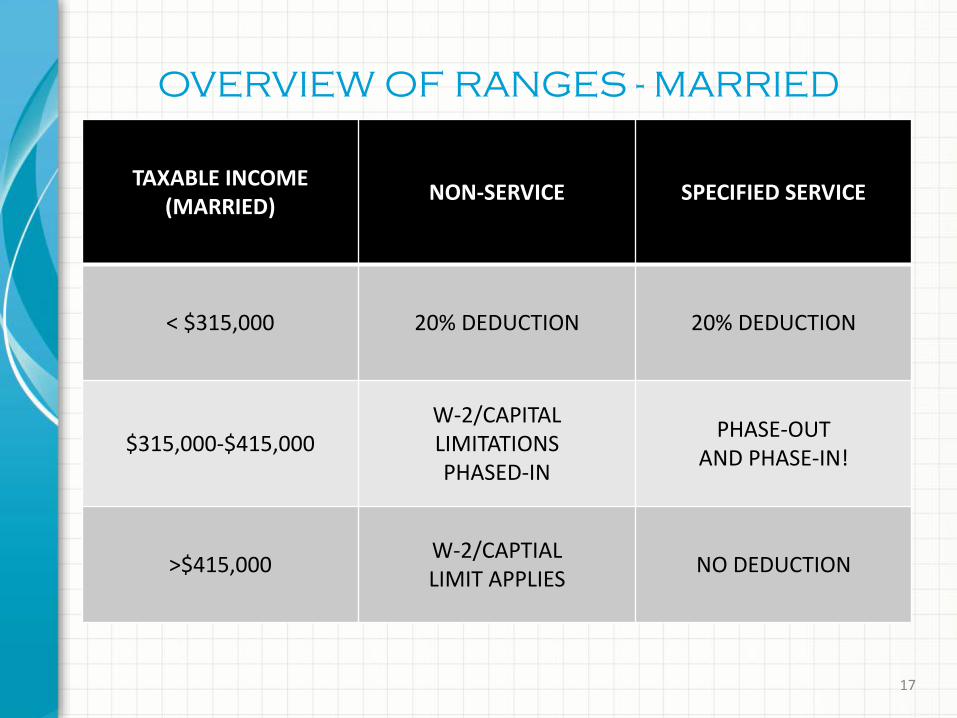

TAXABLE INCOME (MARRIED) NON-SERVICE SPECIFIED SERVICE

< $315,000 20% DEDUCTION 20% DEDUCTION

$315,000-$415,000W-2/CAPITAL LIMITATIONS PHASED-IN

PHASE-OUTAND PHASE-IN!

>$415,000 W-2/CAPTIALLIMIT APPLIES NO DEDUCTION

OVERVIEW OF RANGES - MARRIED

17

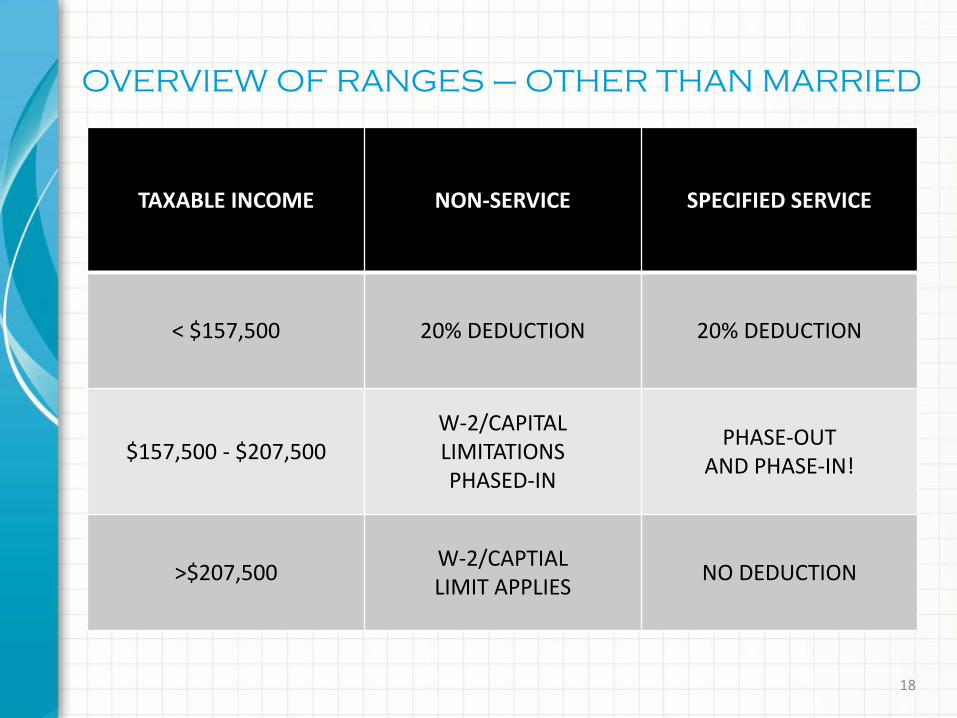

TAXABLE INCOME NON-SERVICE SPECIFIED SERVICE

< $157,500 20% DEDUCTION 20% DEDUCTION

$157,500 - $207,500W-2/CAPITAL LIMITATIONS PHASED-IN

PHASE-OUTAND PHASE-IN!

>$207,500 W-2/CAPTIALLIMIT APPLIES NO DEDUCTION

OVERVIEW OF RANGES – OTHER THAN MARRIED

18

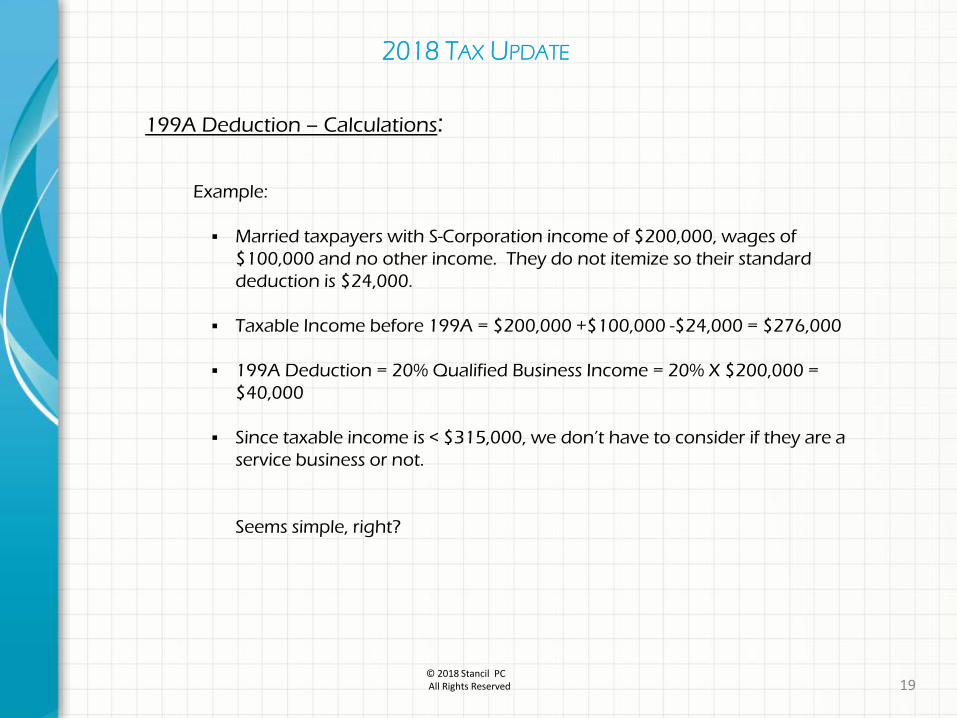

199A Deduction – Calculations:

Example:

Married taxpayers with S-Corporation income of $200,000, wages of $100,000 and no other income. They do not itemize so their standard deduction is $24,000.

Taxable Income before 199A = $200,000 +$100,000 -$24,000 = $276,000

199A Deduction = 20% Qualified Business Income = 20% X $200,000 = $40,000

Since taxable income is < $315,000, we don’t have to consider if they are a service business or not.

Seems simple, right?

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved 19

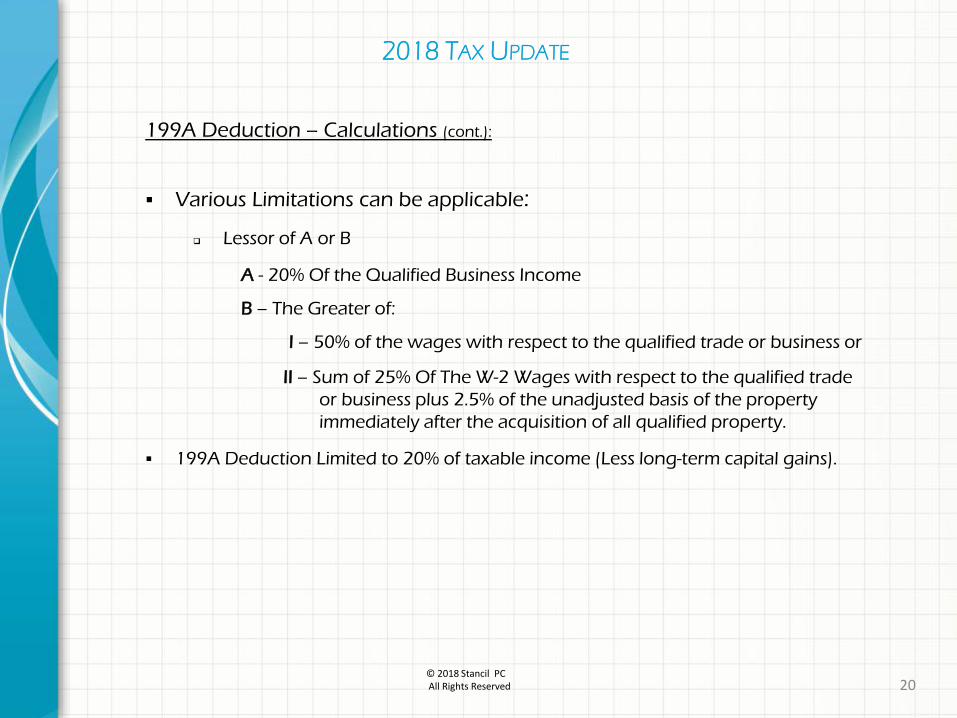

199A Deduction – Calculations (cont.):

Various Limitations can be applicable:

Lessor of A or B

A - 20% Of the Qualified Business Income

B – The Greater of:

I – 50% of the wages with respect to the qualified trade or business or

II – Sum of 25% Of The W-2 Wages with respect to the qualified trade or business plus 2.5% of the unadjusted basis of the property immediately after the acquisition of all qualified property.

199A Deduction Limited to 20% of taxable income (Less long-term capital gains).

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved 20

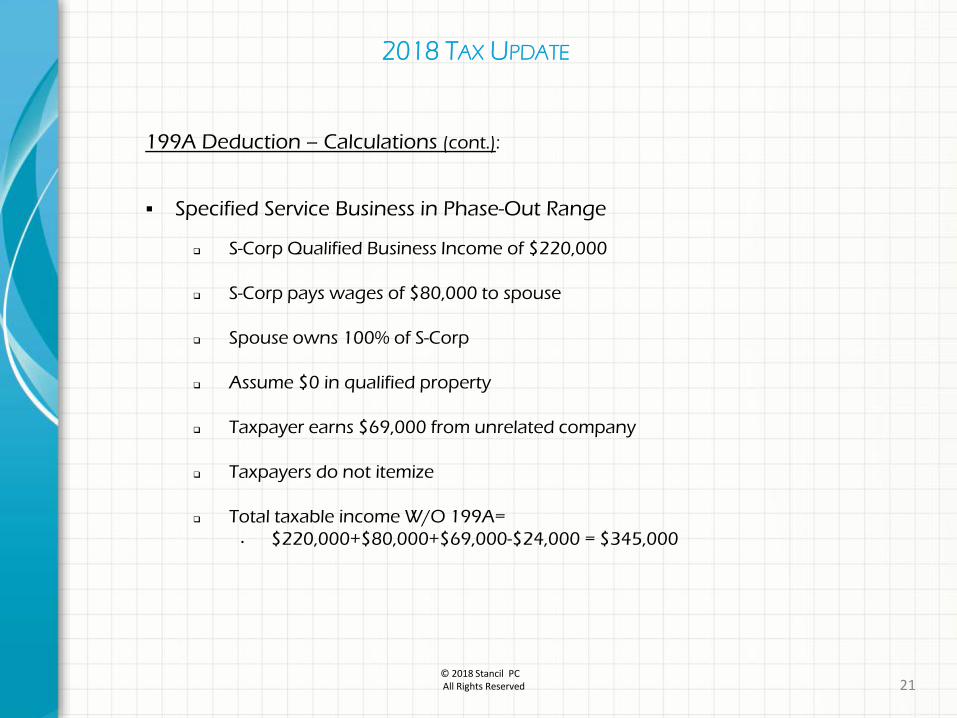

199A Deduction – Calculations (cont.):

Specified Service Business in Phase-Out Range

S-Corp Qualified Business Income of $220,000

S-Corp pays wages of $80,000 to spouse

Spouse owns 100% of S-Corp

Assume $0 in qualified property

Taxpayer earns $69,000 from unrelated company

Taxpayers do not itemize

Total taxable income W/O 199A=• $220,000+$80,000+$69,000-$24,000 = $345,000

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved 21

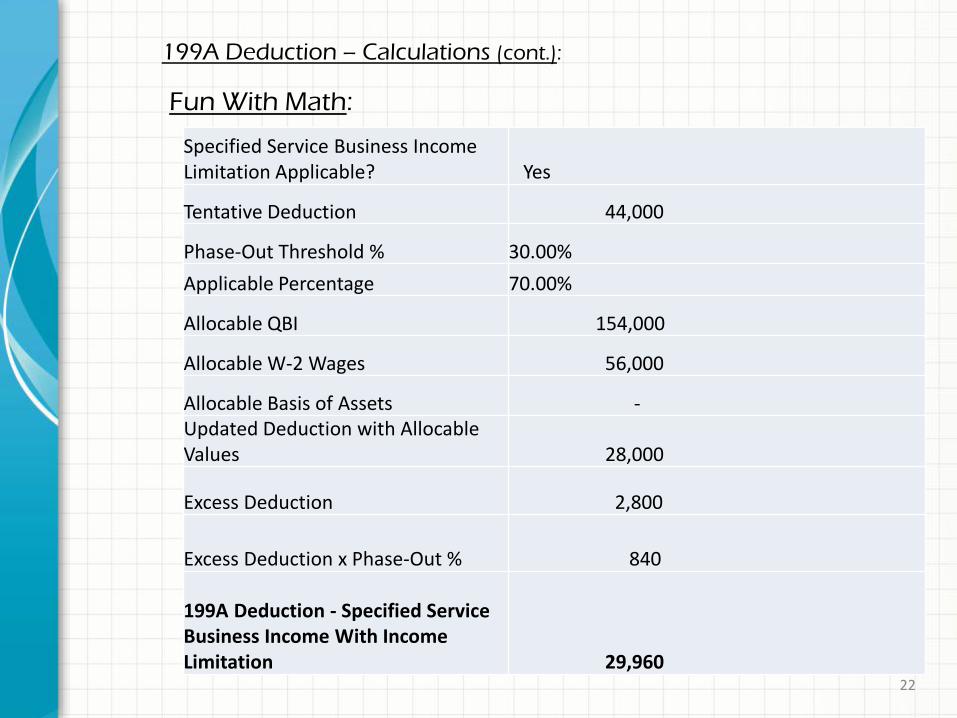

Specified Service Business Income Limitation Applicable? Yes

Tentative Deduction 44,000

Phase-Out Threshold % 30.00%Applicable Percentage 70.00%

Allocable QBI 154,000

Allocable W-2 Wages 56,000

Allocable Basis of Assets -Updated Deduction with Allocable Values 28,000

Excess Deduction 2,800

Excess Deduction x Phase-Out % 840

199A Deduction - Specified Service Business Income With Income Limitation 29,960

Fun With Math:

199A Deduction – Calculations (cont.):

22

199A Deduction – Calculations (cont.):

The previous example represents the most complicated case for one business.

We have developed an Excel based model to calculate the 199A deduction prior to the release of the actual IRS forms and tax software

In the prior example, the W-2 and capital tests were phasing in and the taxable income limits were phasing out the deduction. The overall deduction was limited due to insufficient wages paid by the S-Corp and taxable income > $315,000

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved

23

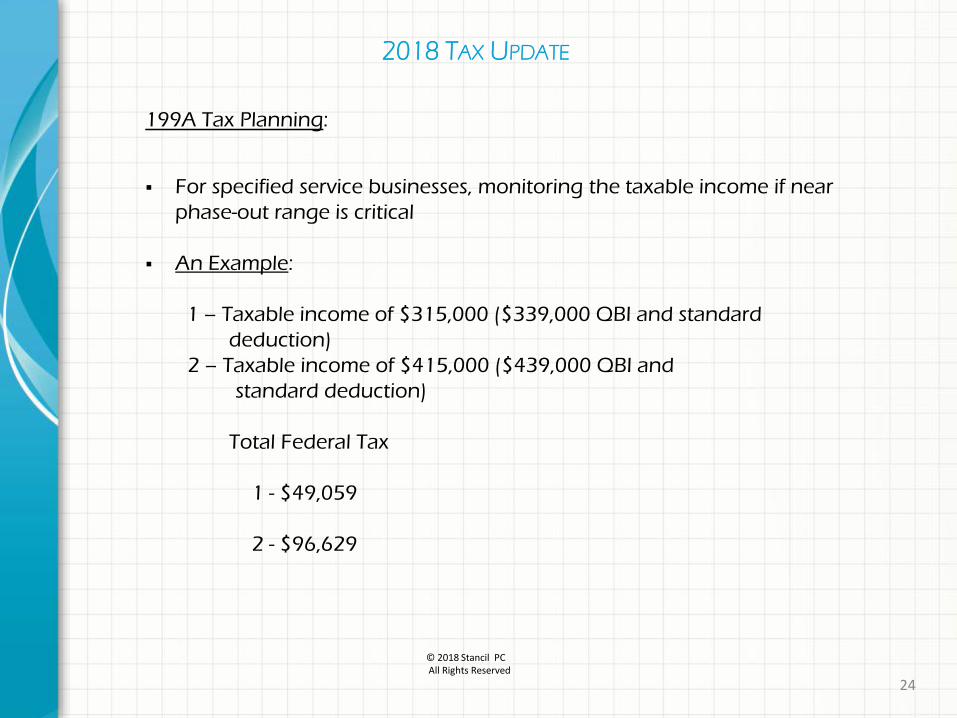

199A Tax Planning:

For specified service businesses, monitoring the taxable income if near phase-out range is critical

An Example:

1 – Taxable income of $315,000 ($339,000 QBI and standard deduction)

2 – Taxable income of $415,000 ($439,000 QBI andstandard deduction)

Total Federal Tax

1 - $49,059

2 - $96,629

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved

24

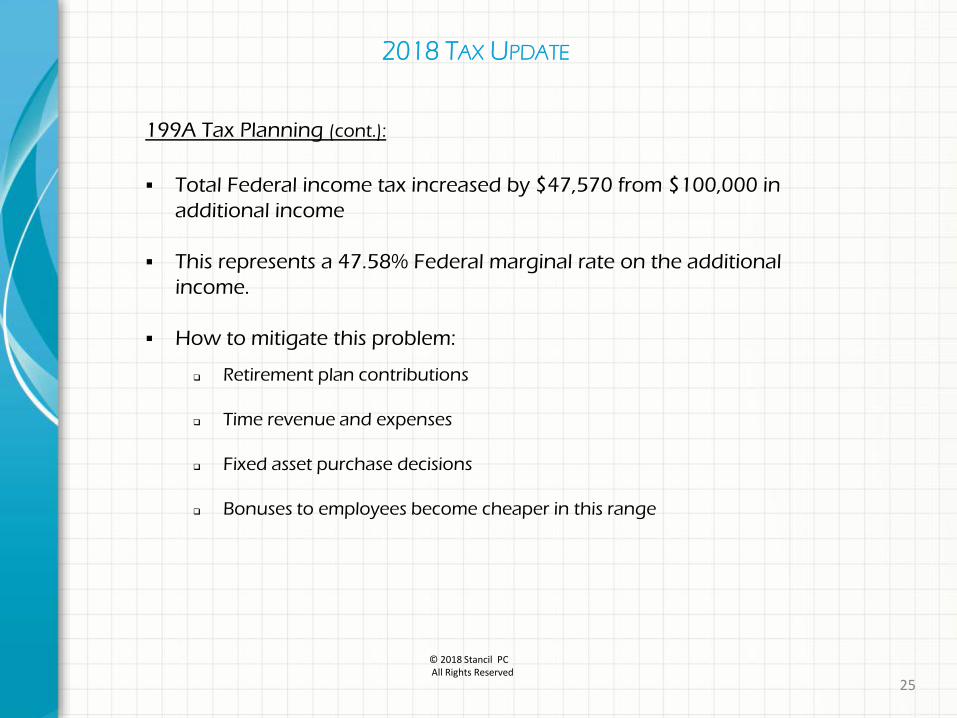

199A Tax Planning (cont.):

Total Federal income tax increased by $47,570 from $100,000 in additional income

This represents a 47.58% Federal marginal rate on the additional income.

How to mitigate this problem:

Retirement plan contributions

Time revenue and expenses

Fixed asset purchase decisions

Bonuses to employees become cheaper in this range

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved

25

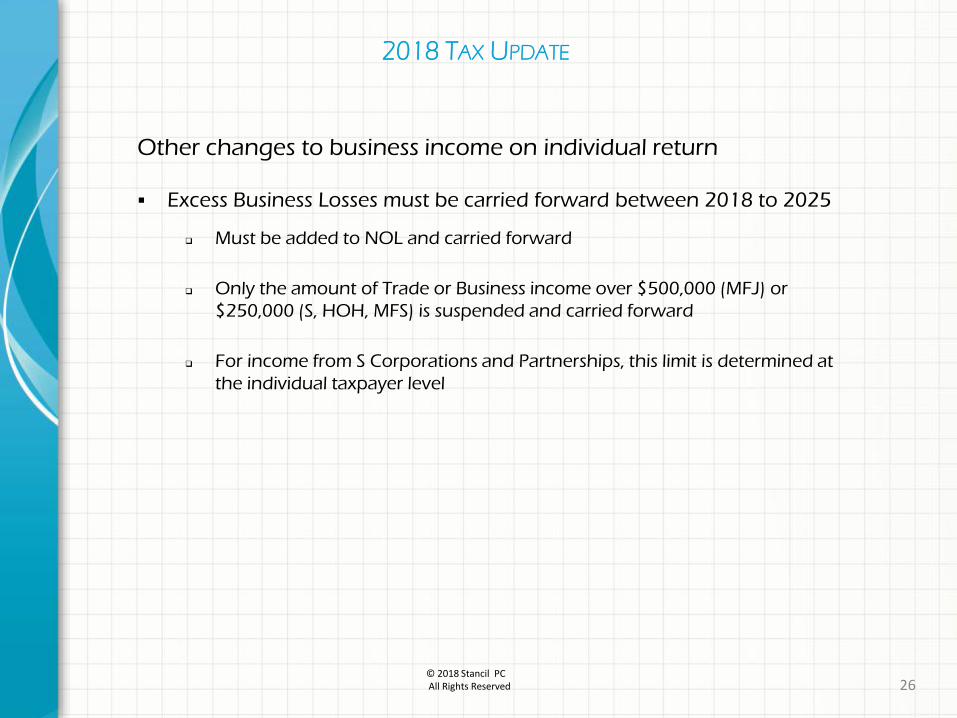

Other changes to business income on individual return

Excess Business Losses must be carried forward between 2018 to 2025

Must be added to NOL and carried forward

Only the amount of Trade or Business income over $500,000 (MFJ) or $250,000 (S, HOH, MFS) is suspended and carried forward

For income from S Corporations and Partnerships, this limit is determined at the individual taxpayer level

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved 26

CHANGES TO BUSINESS DEDUCTIONSAND TAX RATES

27

Changes to Business Deductions and Tax Rates

Depreciation Deduction Changes

Bonus depreciation is 100% for assets bought 9/28/17 – 12/31/22

2023 – 80%, 2024 - $60%, 2025 – 40%, 2026 – 20%

Still may use 50% for first year after 9/28/17 if elect

Allowed for New & Used property

179 expense - $1m maximum and phases out starting at $2.5m of purchases

Now includes Roofs, HVACs, Security Systems, Fire Protection & Alarm Systems that are placed in service after the nonresidential property is placed in service (basically, replacement items)

Qualified Improvement Property category replaces Leasehold Improvement, Qualified Restaurant and Qualified Retail property

Depreciable life is 15 years

Applies to all non-structural internal improvements to Non-residential Real property that happens after the building was placed in service

May take Bonus Depreciation or179 expense

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved

28

Changes to Business Deductions and Tax Rates (cont.):

C Corporation tax rate changes to 21% for years starting after 1/1/2018

If your company has a fiscal year end instead of December 31, then must prorate the tax rate for before and after January 1, 2018

Repealed AMT

NOL’s can only be carried forward and limited to 80% of taxable income

Interest Expense of a business is limited to Interest Income plus 30% of Business Adjusted Taxable Income

Excess is carried over for unlimited number of years

Applied at the entity level for pass through entities

Exceptions:

• Average Gross Receipts for 3 prior years < $25m

• Elect to be Real Property trade or business but then cannot use Bonus Depreciation

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved

29

Changes to Business Deductions and Tax Rates (cont.):

New Small Business Rules (applies to all businesses) – effective for years beginning after 2017

If average gross receipts for prior 3 years is under $25,000,000 then may do the following:

• Use the Cash Basis of accounting

• Expense inventory instead of capitalizing

• Not required to use 263A inventory capitalization

• Not required to use Percent Complete method

For accrual method businesses, the revenue must be recognized no later than it is recognized on the applicable financial statements that are prepared.

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved 30

Other Miscellaneous Changes to note:

Like Kind Exchanges only apply to Real Property

No deduction allowed for Entertainment expenses May still take 50% deduction for meals (food and beverage)

No deduction allowed for Membership Dues May deduct dues to Associations and other Clubs so long as they do not provide access

for entertainment

Net Operating Losses can only be carried forward and limited to 80% of taxable income

Employers limited on the following: 50% deduction allowed for costs of eating facilities that are on site

• 0% allowed started in 2026

No deduction for Transportation Fringes (parking, transit passes)

No deduction for Meals provided on premises starting in 2026

No deduction for Sexual Harassment Settlements or Attorney Fees relating to such

Carried Interest – Must hold the ownership of carried interest in a partnership for 3 years to obtain Long-term Gain treatment

2018 TAX UPDATE

© 2018 Stancil PC All Rights Reserved 31

PLANNING OPPORTUNITIES

32

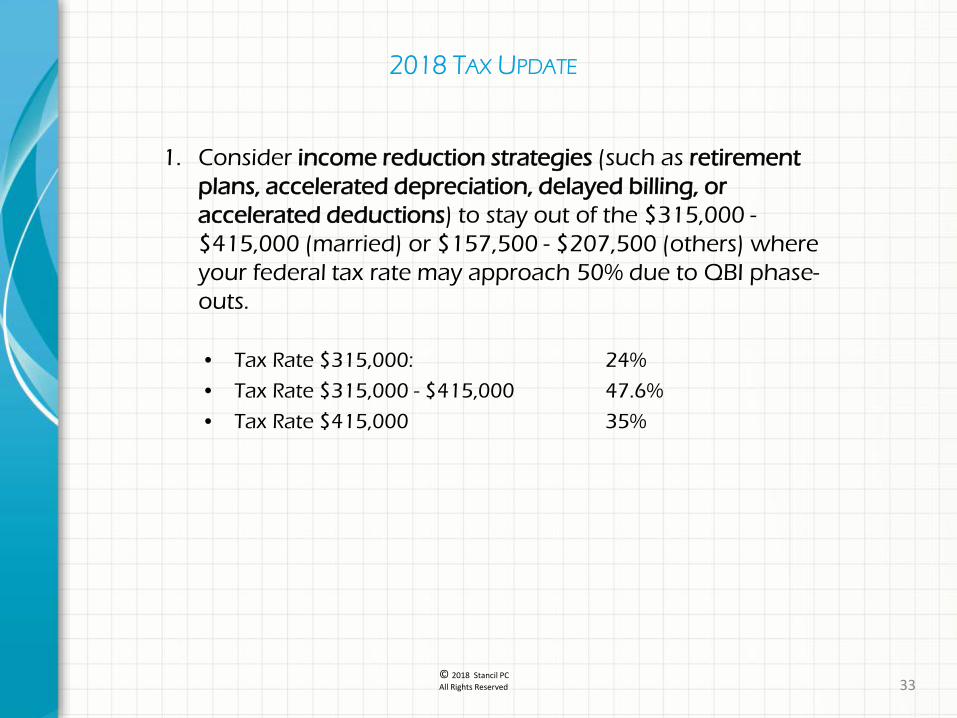

1. Consider income reduction strategies (such as retirement plans, accelerated depreciation, delayed billing, or accelerated deductions) to stay out of the $315,000 -$415,000 (married) or $157,500 - $207,500 (others) where your federal tax rate may approach 50% due to QBI phase-outs.

• Tax Rate $315,000: 24%

• Tax Rate $315,000 - $415,000 47.6%

• Tax Rate $415,000 35%

© 2018 Stancil PC All Rights Reserved

2018 TAX UPDATE

33

© 2018 Stancil PC All Rights Reserved

2018 TAX UPDATE

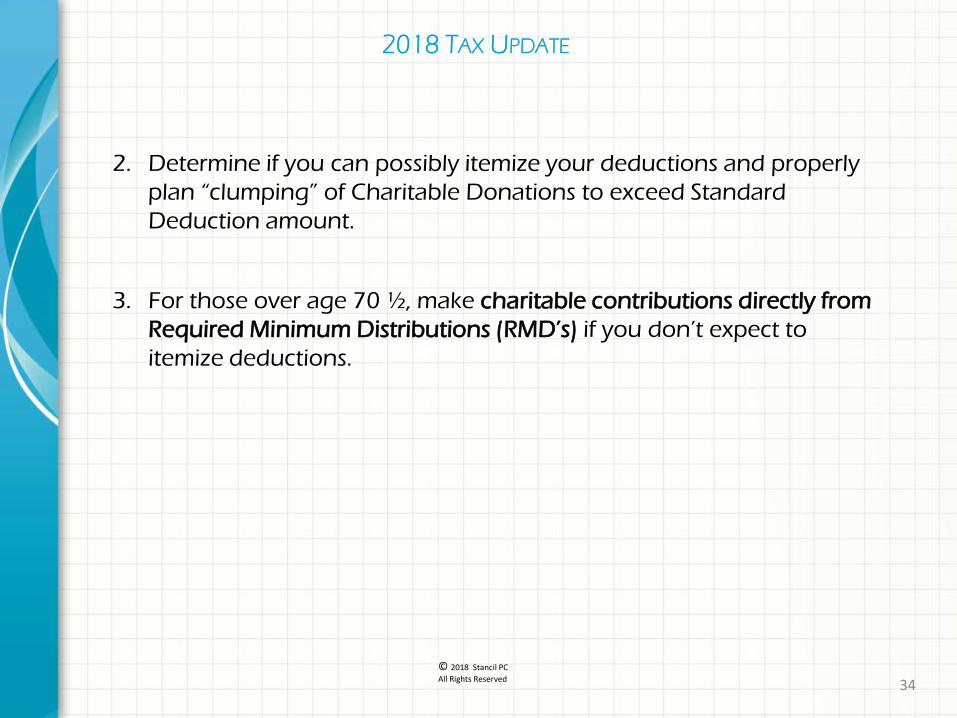

2. Determine if you can possibly itemize your deductions and properly plan “clumping” of Charitable Donations to exceed Standard Deduction amount.

3. For those over age 70 ½, make charitable contributions directly from Required Minimum Distributions (RMD’s) if you don’t expect to itemize deductions.

34

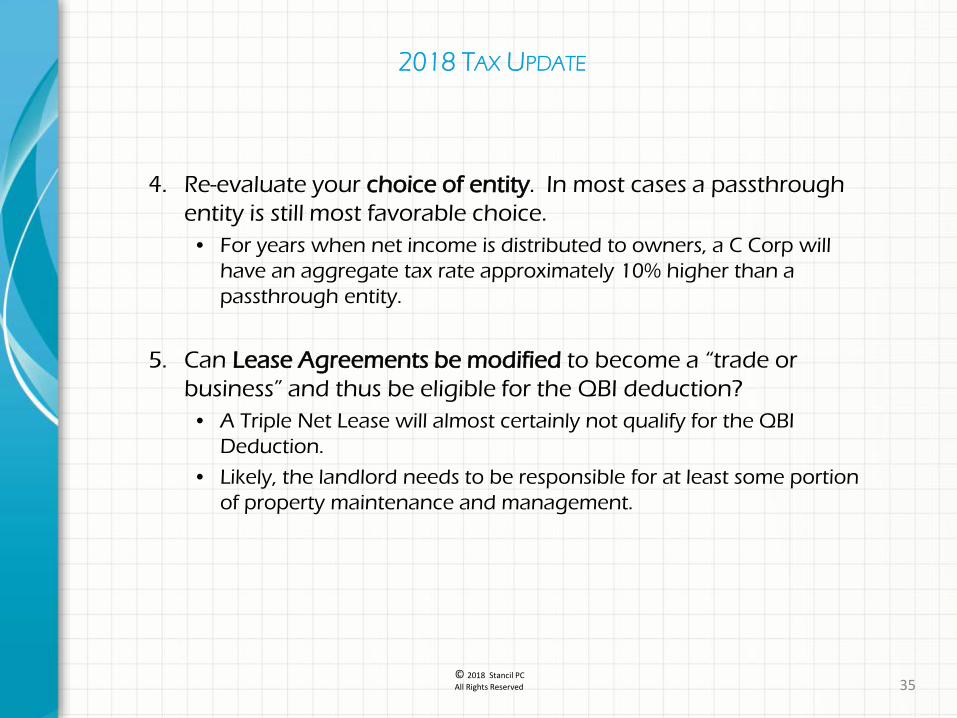

4. Re-evaluate your choice of entity. In most cases a passthrough entity is still most favorable choice.

• For years when net income is distributed to owners, a C Corp will have an aggregate tax rate approximately 10% higher than a passthrough entity.

5. Can Lease Agreements be modified to become a “trade or business” and thus be eligible for the QBI deduction?

• A Triple Net Lease will almost certainly not qualify for the QBI Deduction.

• Likely, the landlord needs to be responsible for at least some portion of property maintenance and management.

© 2018 Stancil PC All Rights Reserved

2018 TAX UPDATE

35

THANK YOU FOR ATTENDING

BYSCOTT HENSLEY

NOVEMBER 2018

STANCIL PCCPAS · ADVISORS

4909 WINDY HILL DRIVERALEIGH, NC 27609

919-872-1260

________________________________________________________________________© 2018 Stancil PC All Rights Reserved 36