Embed Size (px)

Citation preview

Learn how some of the industry’s brightest minds are using and managing data to make smart, fast decisions and drive growth

We hope you enjoyed the 2018 Retail Innovation Summit. From Scott Galloway to Matt Shay, the day was filled with inspiring data-driven insights and learnings. Here is a summary of the key takeaways.

2018 Retail Innovation Summit

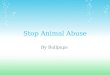

The outlook for retailPaul Greenberg, Founder and CEO of NORA spoke with Australia’s leading retail industry analysts, Ben Gilbert, Head of Consumer Research at UBS, Craig Woolford, Managing Director and Head of Research at Citi and Neil Hendry, Global Head of Consulting at GlobalData. Ben and Craig brought their deep understanding and quantitative analysis of the listed sector of Australian retail, while Neil provided a global perspective. Key takeaways:

1 Australian retail needs to continue innovating to keep up with the accelerating shift in global competition and technology led consumer retail

2 Supply chain and logistics still a key battleground for ecommerce, and retail in general

3 The impact of Amazon on Australian retail has not yet been felt. We overestimated Amazon in the short term, but potentially underestimate them in the long term

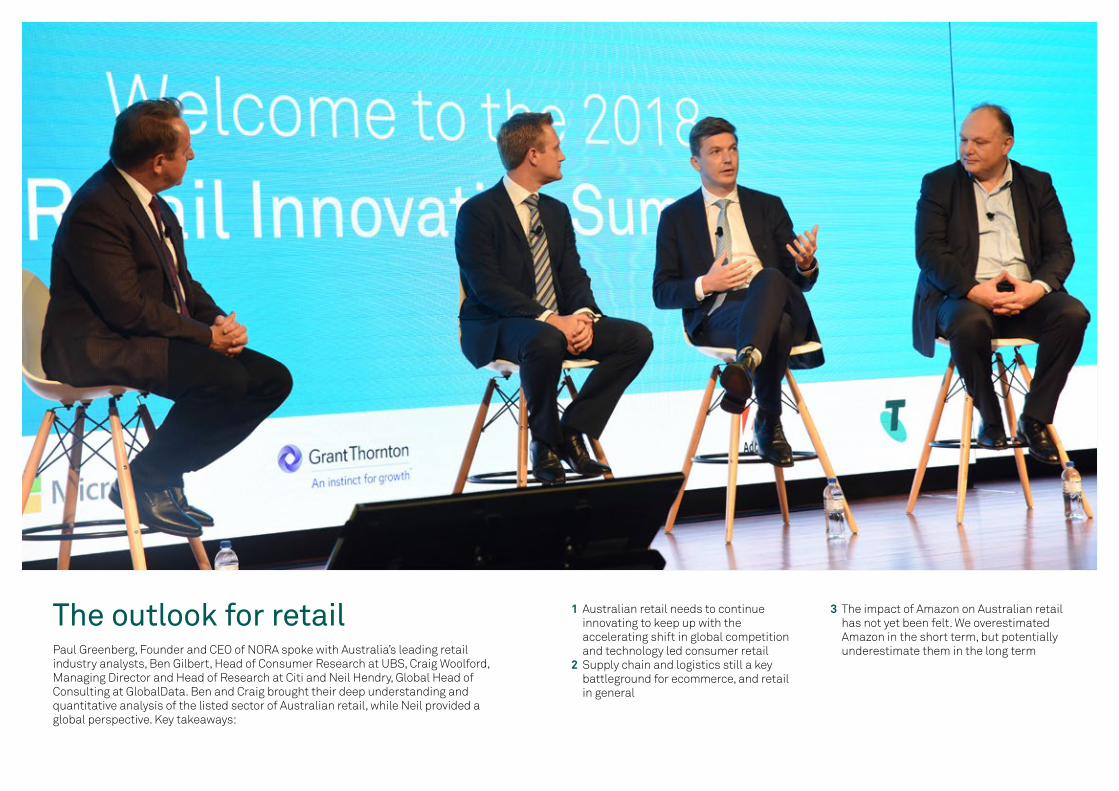

1 Double down on growth channels2 Invest in people3 Design for omnichannel4 Focus on instore customer experience 5 Find your purpose

View presentation

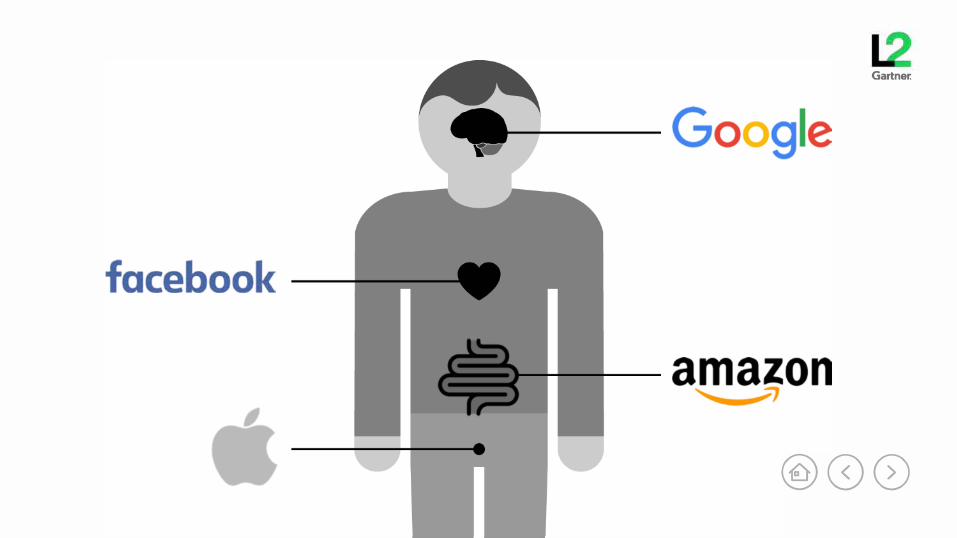

The Four: What to do?Scott Galloway is the Founder of L2 and a Professor of Marketing at NYU Stern. The New York Times best seller deconstructed the strategies of the Four (Apple, Amazon, Facebook, Google) to reveal what brands can do to fight back. Key takeaways:

Leveraging data and insights to transform the customer experienceChristine Corbett is Australia Post’s Group Chief Customer Officer, accountable for all key customer touchpoints including the largest retail network in the country. Key takeaways:

3 Set clear customer priorities4 Empower your workforce to deliver great

customer experiences

View presentation

1 To transform the customer experience, you need to know your customers. Leveraging data and insights is critical to help focus your efforts

2 Understand the market and where the opportunities are

Data-driven customer experienceMarcy Larsen is Retail Solutions Industry Executive at Microsoft. She was joined by Rachel Kelly, Founder and CEO of the Retail Collective, Phil Bonanno, Client Partner at Facebook, Tim Trumper, Advisor at Quantium and Chairman NRMA and Tim Weale, National Retail Solutions Manager at Mirvac. They discussed how data driven technologies and insights are improving customer engagement and helping retailers stay one step ahead. Key takeaways:

1 Experiment using personalised offers with your CRM data, your most loyal customers, and measure the impact

2 Know your customers and your mission – seek the insights from your data to validate

3 Leapfrog building a data culture – collaborate with suppliers and other in the retail ecosystem and analytics firms that come with outside data and algorithms

Data-driven supply chainLuke Ritchie, Partner at GNC Group Consulting led a discussion with Deanna Lomas, Chief Supply Chain Officer at Super Retail Group, Todd Foster, GM Supply Chain and Procurement at Target, Jonathan Aitken, Market Development Manager Digital at Avery Dennison and Gareth Jude, Retail Industry Executive at Telstra on the power of data to transform retail supply chains and create new efficiencies, growth opportunities and benefits for customers. Key takeaways:

1 A broad appetite exists for more data sharing, but often stifled by organisational factors rather than technological ones

2 Technologies such as RFID and blockchain can be transformative for retailers, but Australian retailers have been slow to embrace

3 Amazon’s relentless focus on the customer is expected to drive new expectations and service levels across the logistics sector

4 Bricks-and-mortar retailers must leverage what they have in their arsenal – their stores

Data-driven marketingScott Rigby, Head of Digital Transformation at Adobe discussed the long road ahead for Australian retailers in their data-driven marketing application with Jodie Sangster, CEO of ADMA, Katharina Kuen, Chief Strategist at The Winning Group, Steve Cox, Managing Director at Dymocks Retail and Tom Beeby, Director of Technology at Sapient Raxorfish. Key takeaways:

1 Australian retailers are struggling to find the right talent for digital, particularly inside marketing

2 Retailers are fighting for customer attention. Insights from data and deep customer understanding of human emotions can help win this battle

3 Managing high volumes of data is hard. Extracting actionable insights is even harder. Retailers need to invest in the right set of technology to help drive growth

The InnovatorsGareth Jude, Retail Industry Executive at Telstra chaired a session on how turning an idea into a new business or creating transformative change in an existing business are at the core of what we mean by innovation. We heard from Zoe Ghani, Chief Technology Officer at the Iconic, Kelly Slessor, CEO and Founder at ShopYou and Peter Knock, Executive Director at St Vincent de Paul Society who have done both and who shared the lessons learned along the way. Key takeaways:

1 Innovation challenges vary depending on the maturity of the business model

2 Empower your team to test and learn. Don’t depend on big capex bets

3 Executing a program of innovation depends more on culture, passion and purpose than technology

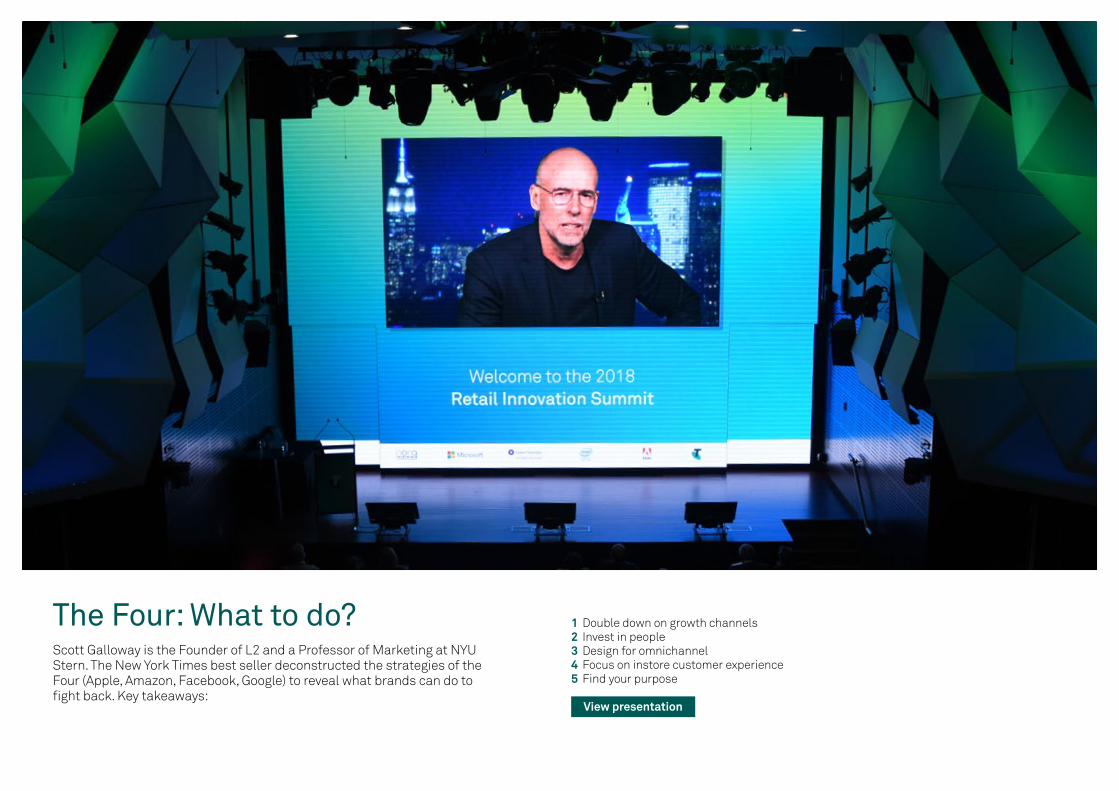

USA and retail – a growing pieMatt Shay is one of the most important figures in global retail, given his position as President and CEO of the National Retail Federation. He shared his industry insights and global perspective on the outlook for retail:

1 Retail is a ‘people business’ and whilst technology is an enabler your people are the competitive advantage

2 Retail is not a zero sum game, and no one retailer will win. The pace of change is accelerating, but so are the opportunities

3 Retail has moved beyond simple transactional retail. Purpose, people and brand position are key

Thank you to our partners

View a video of the key highlights here For more information visit insight.telstra.com.au/retail-innovation-summit-2018

Keynote presentationsScott Galloway and Christine Corbett

THE FOURSCOTT GALLOWAY | FEBRUARY 20TH 2018@profgalloway

Gartner:

@00

$2,794B

2018Source: IMF, Yahoo! Finance.

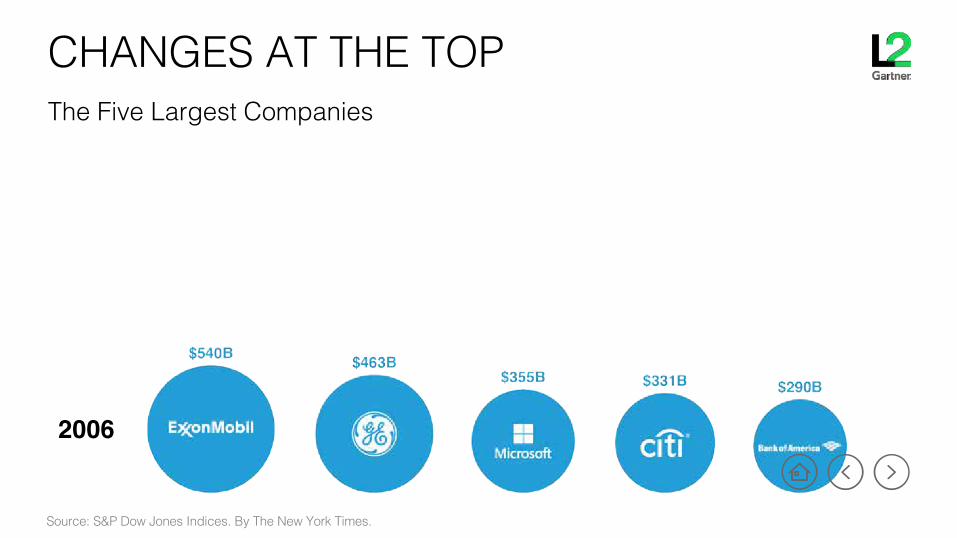

The Five Largest Companies

CHANGES AT THE TOP

Source: S&P Dow Jones Indices. By The New York Times.

now

2006

The chapter I didn’t write?

Big Tech should be broken up.

THE 25 CENT PARKING TICKET

$122M WhatsApp filing fine

$16BWhatsApp acquisition

$2.7B EU Antitrust fine

$95B2016 cash

Target Kroger Costco Walmart

Amazon Whole Foods

$11.23B

$3.07B

-$1.57B -$2.13B

-$5.69B

-$11.13B

June 15, 2017 vs. June 16, 2017Change in Market Cap After Amazon Announced Acquisition of Whole Foods

GROCERY’S ANTI-CHRIST

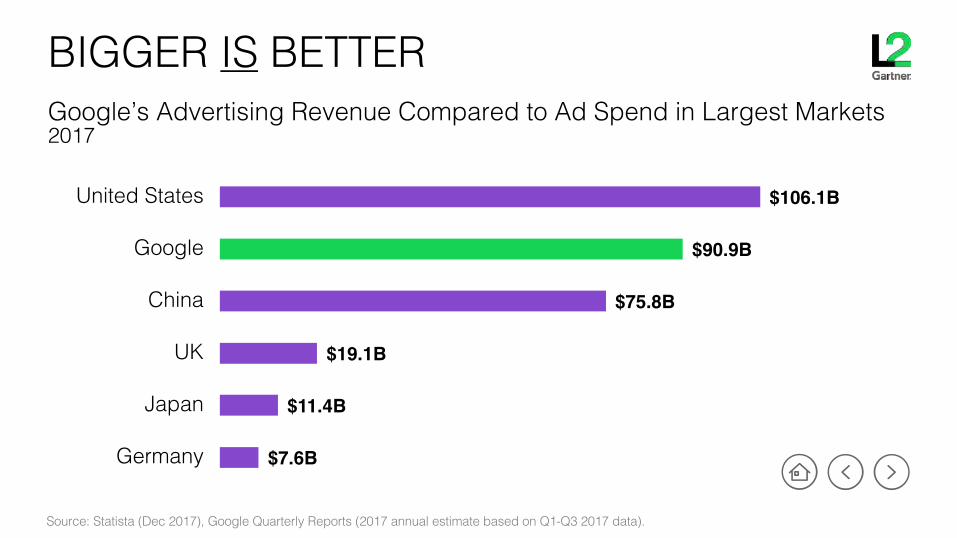

$7.6B

$11.4B

$19.1B

$75.8B

$90.9B

$106.1B

Germany

Japan

UK

China

United States

2017Google’s Advertising Revenue Compared to Ad Spend in Largest Markets

BIGGER IS BETTER

Source: Statista (Dec 2017), Google Quarterly Reports (2017 annual estimate based on Q1-Q3 2017 data).

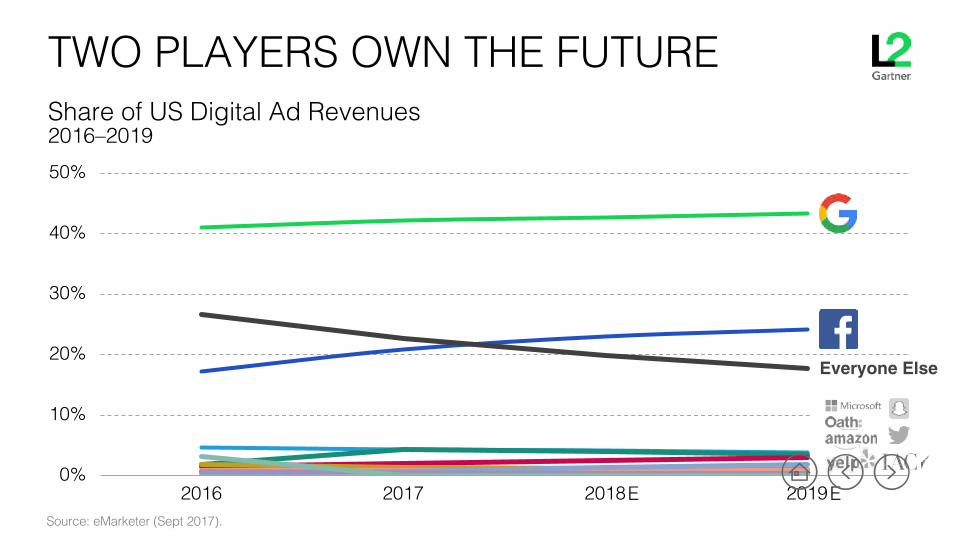

0%

10%

20%

30%

40%

50%

2016 2017 2018 2019

2016 2019Share of US Digital Ad Revenues

TWO PLAYERS OWN THE FUTURE

Source: eMarketer (Sept 2017).

E E

Everyone Else

Internet Television Newspapers Magazines Radio Outdoors1970–2020EAustralian Ad Spend, by Medium

AT THE LOCAL LEVEL

Source: Morgan Stanley Research Estimates.

Forecast

Collected by Global Media/Tech Companies Left for Domestic Media CompaniesAustralia Media Ad Spend

DOWN “UNDER”

Source: CEASA, Morgan Stanley Research Estimates.

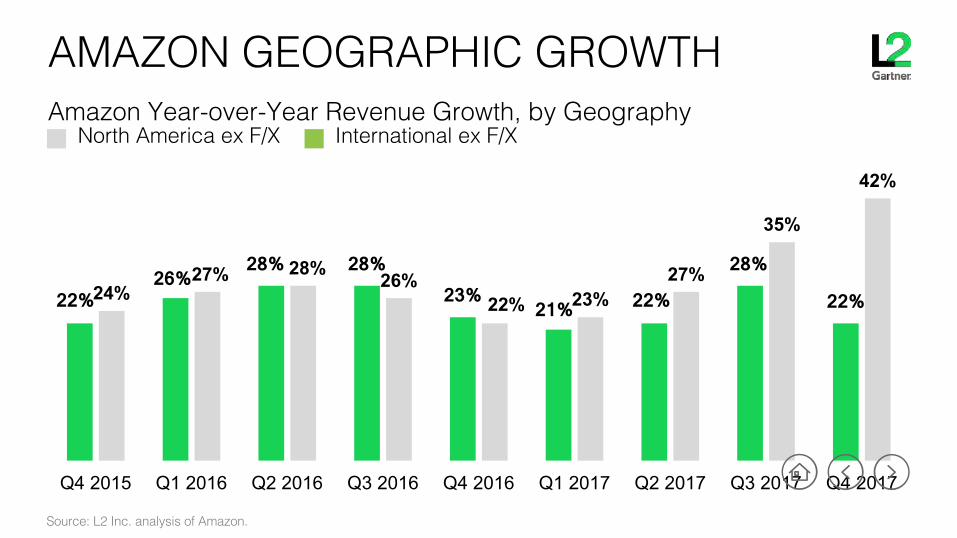

TOTAL CAGR +3%

North America ex F/X International ex F/XAmazon Year-over-Year Revenue Growth, by Geography

AMAZON GEOGRAPHIC GROWTH

Source: L2 Inc. analysis of Amazon.

22% 26%

28% 28% 23%

21% 22%

28%

22% 24%27% 28% 26%

22% 23%27%

35%

42%

Q4 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017

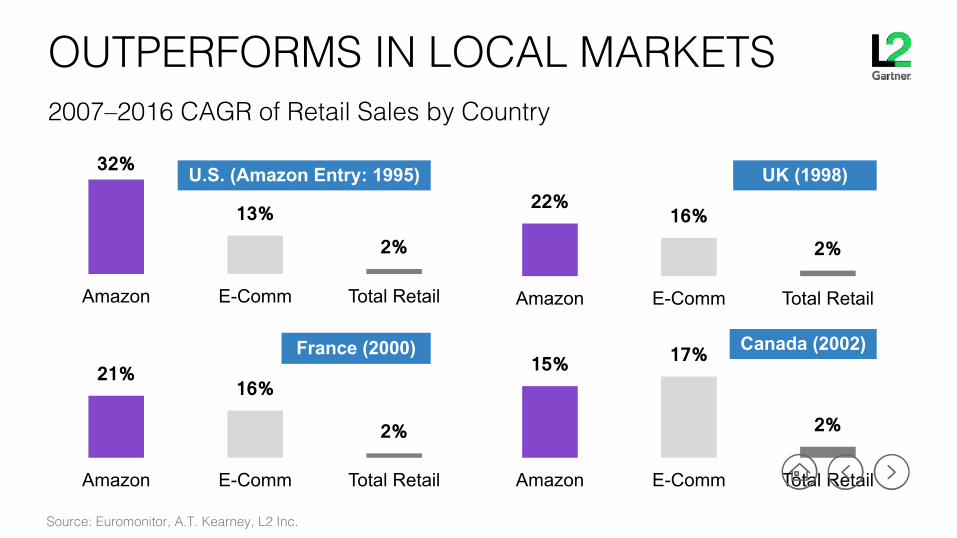

2007–2016 CAGR of Retail Sales by Country

OUTPERFORMS IN LOCAL MARKETS

Source: Euromonitor, A.T. Kearney, L2 Inc.

32%

13% 2%

Amazon E-Comm Total Retail

22% 16%

2%

Amazon E-Comm Total Retail

21% 16%

2%

Amazon E-Comm Total Retail

15% 17%

2%

Amazon E-Comm Total Retail

U.S. (Amazon Entry: 1995)

France (2000)

UK (1998)

Canada (2002)

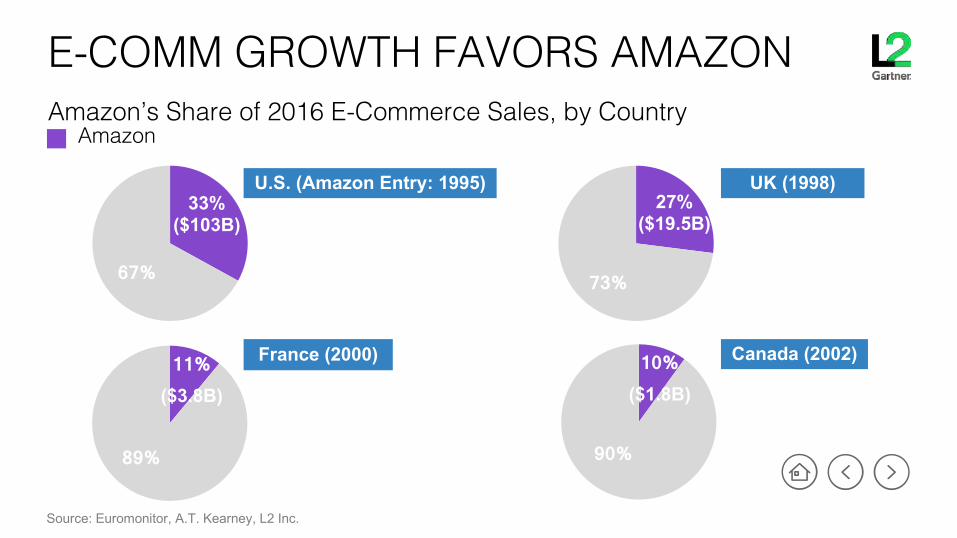

AmazonAmazon’s Share of 2016 E-Commerce Sales, by Country

E-COMM GROWTH FAVORS AMAZON

33%($103B)

67%

27%($19.5B)

73%

11% ($3.8B)

89%

10% ($1.8B)

90%

U.S. (Amazon Entry: 1995)

France (2000)

UK (1998)

Canada (2002)

Source: Euromonitor, A.T. Kearney, L2 Inc.

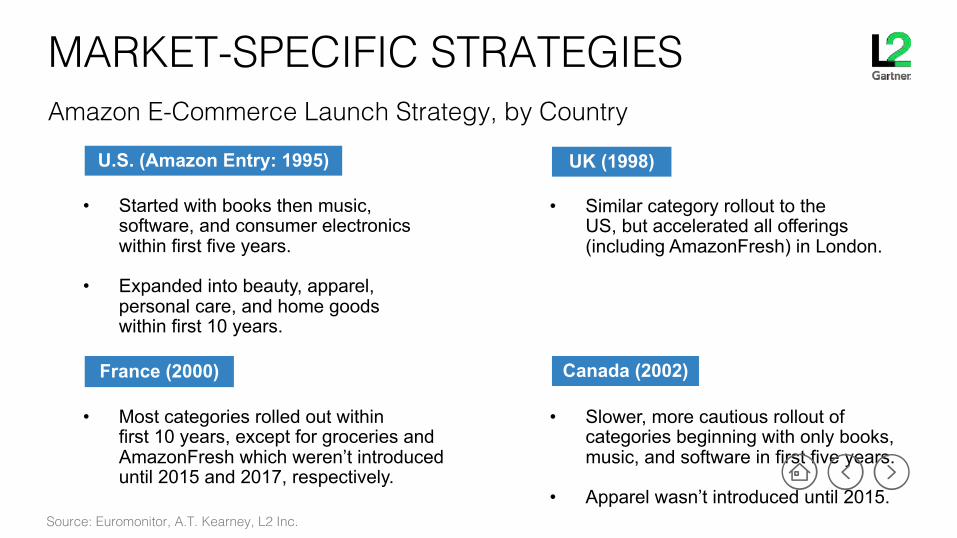

Amazon E-Commerce Launch Strategy, by Country

MARKET-SPECIFIC STRATEGIES

Source: Euromonitor, A.T. Kearney, L2 Inc.

U.S. (Amazon Entry: 1995) UK (1998)

France (2000) Canada (2002)

• Started with books then music, software, and consumer electronics within first five years.

• Expanded into beauty, apparel, personal care, and home goods within first 10 years.

• Similar category rollout to the US, but accelerated all offerings (including AmazonFresh) in London.

• Most categories rolled out within first 10 years, except for groceries and AmazonFresh which weren’t introduced until 2015 and 2017, respectively.

• Slower, more cautious rollout of categories beginning with only books, music, and software in first five years.

• Apparel wasn’t introduced until 2015.

2017Share of Amazon Australia Assortment

AMAZONS AUSTRALIA ASSORTMENT

Source: Citi Research.

Electronics44%

Media19%

Sports & Outdoors11%

Apparel10%

Shoes & Accessories

5%

Tools & Garden5%

Health & Beauty3%

Office Supplies2%Auto Parts

1%

News Announcements Referring to Amazon Australia Launch

AUSTRALIA—WHAT WE’VE HEARD

Source: Euromonitor, A.T. Kearney, L2 Inc.

• Brittain Ladd—former global manager in charge of expanding Fresh and Pantry—says Amazon will “launch as many services as possible in Australia in 2018”

• Rocco Braeuniger, former director of consumables for Amazon Germany, is assigned to the Amazon Australia team.

• Amazon testing Prime Air drone delivery in Australia to overcome same-day delivery challenges

SOME FINAL WORDS

WHAT IS THE PURPOSE OF AN ECONOMY?

1971–2015, USShare of Income Class by Percent of Households

DECLINE OF THE MIDDLE CLASS: US

Source: "The American Middle Class Is Losing Ground," Pew Research Center, December 8, 2015.

1971 1981 1991 2001 2011 2015

100%

75%

50%

25%

Middle Class-11%

Upper Class+7%

Lower Class+4%

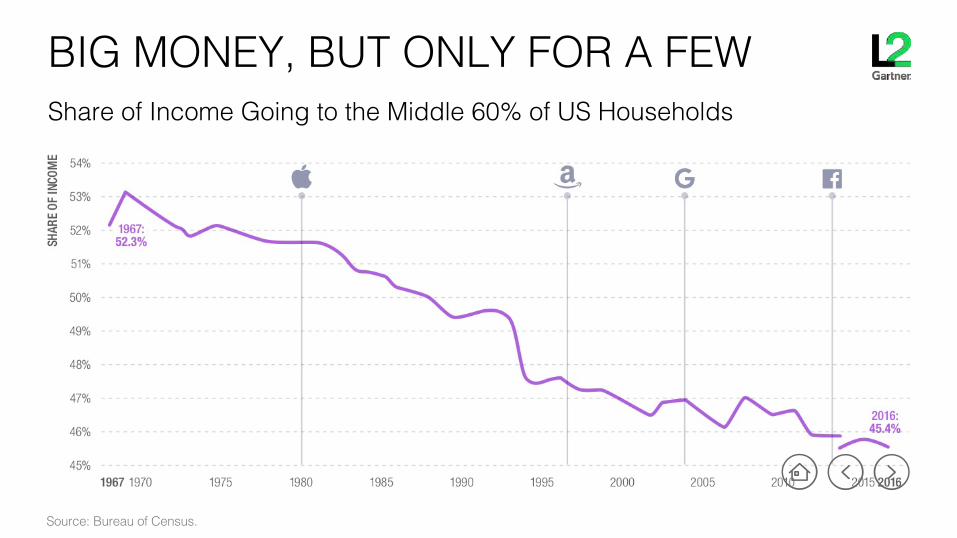

Share of Income Going to the Middle 60% of US Households

BIG MONEY, BUT ONLY FOR A FEW

Source: Bureau of Census.

SEARCH YOUR FEELINGS

@PROFGALLOWAY

Page 2

2017 = $2.3 trillionestimated online retail sales worldwide

2018 = $2.7 trillionestimated online retail sales worldwide

Source: eMarketer retail ecommerce sales worldwide

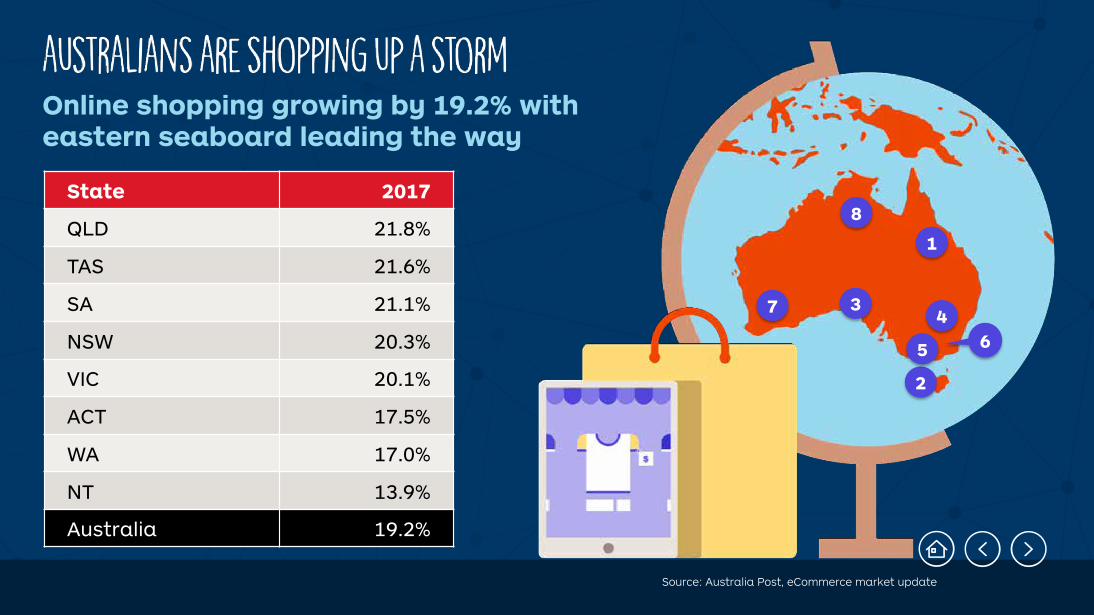

Page 3Source: Australia Post, eCommerce market update

6

1

2

7 4

5

8

Online shopping growing by 19.2% with eastern seaboard leading the way

State 2017

QLD 21.8%

TAS 21.6%

SA 21.1%

NSW 20.3%

VIC 20.1%

ACT 17.5%

WA 17.0%

NT 13.9%

Australia 19.2%

3

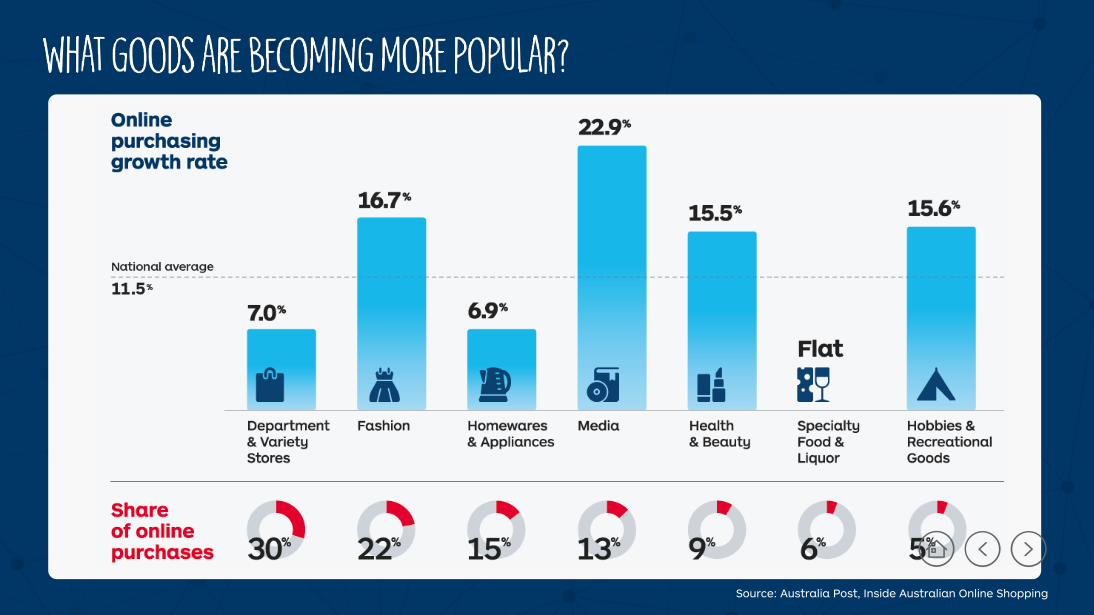

Page 4Source: Australia Post, Inside Australian Online Shopping

9

Top 10 postcodesIn 2016 Australians purchased

• Toowoomba secured the top spot ahead of Point Cook

• 23% of the growth were in the suburbs of Rangeville, Newtown & KearneysSpring – outside Toowoomba City

• Baulkham Hills was the fastest growth postcode in the top 10

• Very remote regions of Australia doubled in rate of growth compared to the previous year.

more goods online11.5%

Rank Growth

1. Toowoomba, 4350 p1 13%

2. Point Cook, 3030 q-1 18%

3. Liverpool, 2170 0 19%

4. Gosford, 2250 p3 18%

5. Mackay, 4740 q-1 5%

6. Cairns, 4870 q-1 9%

7. Baulkham Hills, 2153 p2 24%

8. Hoppers Crossing, 3029 q-2 20%

9. Mandurah, 6210 q-1 11%

10. Bundaberg, 4670 p6 9%

7

8

3

4

1 10

2

56

Page 5Source: Australia Post, Inside Australian Online Shopping

Customer priorities

Creating seamless customer

experiences

Listening to customers and

taking action

Knowing our customers our people

Empowering

Customer priorities Knowing

our customers

Page 8

Up to 3x increase in shopping frequency*

We can significantly increase online shopping

+5%The increase to average basket size with a $25 min basket threshold

Almost double spending online* vs -24% with no minimum

And a $25 minimum spend threshold is enough

Free standard shippingis enough… for now

More retailer choice grows the whole market

Launched

free shipping at over 65 retailers - $25 or more basket size

139% increase in parcel volume – Shipster

subscribers

$82 Average

basket size

Up to 54% Customer

acquisition

Source: Australia Post, Inside Australian Online Shopping*(excl grocery)

We tested the impact of free, fast shipping

with Australian retailers on

420 consumers for 16 weeks

As at Jan 2018

Customer priorities

Listening to customers and

taking action

Page 10

Internal data

Leading Lifestyles

Today’s families

Getting by

BattlersMetrotechs

Aussie Achievers

Golden years

Post Office transactions

NPS Parcel scan data

Marketing activity

Helix personas

Targeted actions

improved NPS results across all personas

Customer priorities

Creating seamless customer

experiences

I’ve ordered my item

It’s on its way

It’s coming today

Receiving my parcel

Sent it back

I have a query

I’ve been carded

Customer priorities our people

Empowering