Embed Size (px)

Citation preview

2018 Digital Trends in South Africa

DigitalIntelligenceBriefing

2018 Digital Trends in South Africa2

Digital Intelligence Briefing: 2018 Digital Trends in South Africa

1. Foreword ........................................................................................

2. Executive summary ....................................................................

3. Current state of digital maturity ............................................

4. Customer journeys are the priority as channel choice increases .........................................................................................

5. Social media remains king but content is chasing the throne ..............................................................................................

6. Design-led thinking impeded by a lack of internal process and tech .........................................................................

7. The future is personalised, but not yet automated ........

8. Fit for the future: five areas South African marketers should focus on ............................................................................

9. Appendix: respondent profiles ...............................................

3

4

6

10

13

15

17

20

21

2018 Digital Trends in South Africa 3

This is the second year that we have partnered with Econsultancy to produce a Digital Trends report that focuses on South Africa, assessing the digital maturity of this rapidly changing country.

Based on a wider survey of almost 13,000 marketers, this year we are able to compare not only South Africa to the global base, but also to last year’s local data to assess ongoing trends and developments in the region.

The marketing profession is evolving quickly in South Africa in response to the rate of digital penetration. Improved access to smartphone technology and declining data costs mean that mobile is a significant force for change in the country, and marketers need to learn on their feet.

It is perhaps as a result of this that respondents this year are less assured of their digital capabilities than in 2017, as they learn the extent of the opportunities digital can provide, and benchmark their own strategies against this.

The global 2018 Digital Trends report confirmed that we are now in an era where the customer experience is the focal point of marketing, and this finding is echoed by this South Africa report; marketers in the region are focused on joining up the growing number of touchpoints along the customer journey.

This research reveals that businesses are still challenged by having the right technologies to meet their customers along this journey, and to connect these systems across functions. This is a challenge particularly pertinent in South Africa, where the majority of internet traffic comes from mobile, meaning consumers are harder to track and profile. It is encouraging to see that respondents are increasingly focusing on content as a way of giving the journey consistency, regardless of platform.

Here at Adobe we believe this consistency is vital to a great customer experience, and a strong technology base is the best foundation to ensure this consistency. Recent years have proven that commercial success comes from consistently good experiences – in digitally transforming South Africa, this consistency can be a significant challenge, being met by only a minority of leading businesses.

We hope this report provides you with some insightful data points and analysis which will be useful to your organisation throughout your digital transformation journey.

Foreword by AdobeGrant O’Connor Director, Sub-Sahara Africa Adobe

2018 Digital Trends in South Africa4

Executive summary

Perceptions of digital maturity may have become more realistic

› Companies are positive about their business performance, but less than 20% have mature digital marketing strategies. Only 12% of companies claimed to be digital-first this year; a drop on last year’s 17%. The rate of change in the country is rapid, meaning that marketers may be realising that the goalposts are shifting when it comes to the use of digital within marketing strategies.

› Design-driven marketing has grown in popularity as a strategy in recent years due to increasing evidence that the approach brings tangible business benefits, despite its ROI being challenging to measure. Compared to last year, respondents are less likely to describe their organisations as design-driven, with those responding as such dropping to 54% from 69% last year. Increased awareness of what it means to be design-led across a business, and the challenge of measurement, may have contributed to this drop in confidence.

Optimising journeys across channels is a priority, but it’s hindered by technology

› With opportunities to reach consumers growing significantly as digital channels and platforms are added to the media mix, optimising the customer journey across multiple touchpoints is understandably the most important factor for companies responding to the survey. The vast majority (83%) said this was ‘very important’ to their digital marketing over the next few years.

› Technology is seen as one of the most important prerequisites for CX success; 73% rated the tools to use data to create compelling, personalised, real-time experiences a ‘4’ or ‘5’ on a five-point scale. However, technology is also seen as one of the hardest elements of the customer experience to master.

The 2018 Digital Trends in South Africa report, published by Econsultancy in partnership with Adobe, is based on a sample of almost 230 digital professionals based in South Africa1 who were among around 13,000 respondents taking part in the annual Digital Trends survey.

These are the key findings of the report:

1. The 226 South Africa respondents who took part in the 2018 Digital Trends survey were among a total of nearly 13,000 marketing, creative and technology professionals in the digital industry from all sectors who participated, from countries across EMEA, North America and Asia Pacific.

2018 Digital Trends in South Africa 5

Mobile focus does not yet equal mobile traffic

› South Africa is mobile-led, with over 75% of internet traffic coming from mobile. However, only 9% of companies said mobile optimisation was a top priority for 2018, compared to 20% of agencies. Despite this, optimisation and consistency of the customer journey across touchpoints are both ‘very important’ to the majority of respondents.

Social media remains a focus as companies optimise their content efforts

› Social media engagement is the top digital related priority for companies and agencies in 2018, selected by 27% and 39% respectively. As the number of active users on social platforms, particularly Facebook, continues to grow, marketers are harnessing the power of social conversation and content sharing to increase brand awareness.

› Content marketing is high on the priority list for marketers this year, and with the choice of channels and media increasing, marketers are clearly aware of the need for content to work across varied distribution channels. Seven in ten (71%) see optimising creative workflows to facilitate the rapid creation and deployment of content across multiple platforms as very important for CX success over the next year.

› Companies evidently want to remain close to the content creation process; 86% of respondents agreed that they were bringing content in-house.

Use of emerging technology remains a distant future for the majority

› South African companies are, relative to their international peers, more likely to be using artificial intelligence, though this group is still the minority (20%). Almost half have no plans to use AI, due to a lack of knowledge and resource (42% each), while a larger proportion (47%) haven’t put thought into how they could use the technology in their business.

13%

20%

42%

14%

11%

We exceeded our topbusiness goal by asigni�cant margin

We narrowly exceededour top business goal

We met our topbusiness goal

We narrowly missed outon our top business

goal

We missed our topbusiness goal

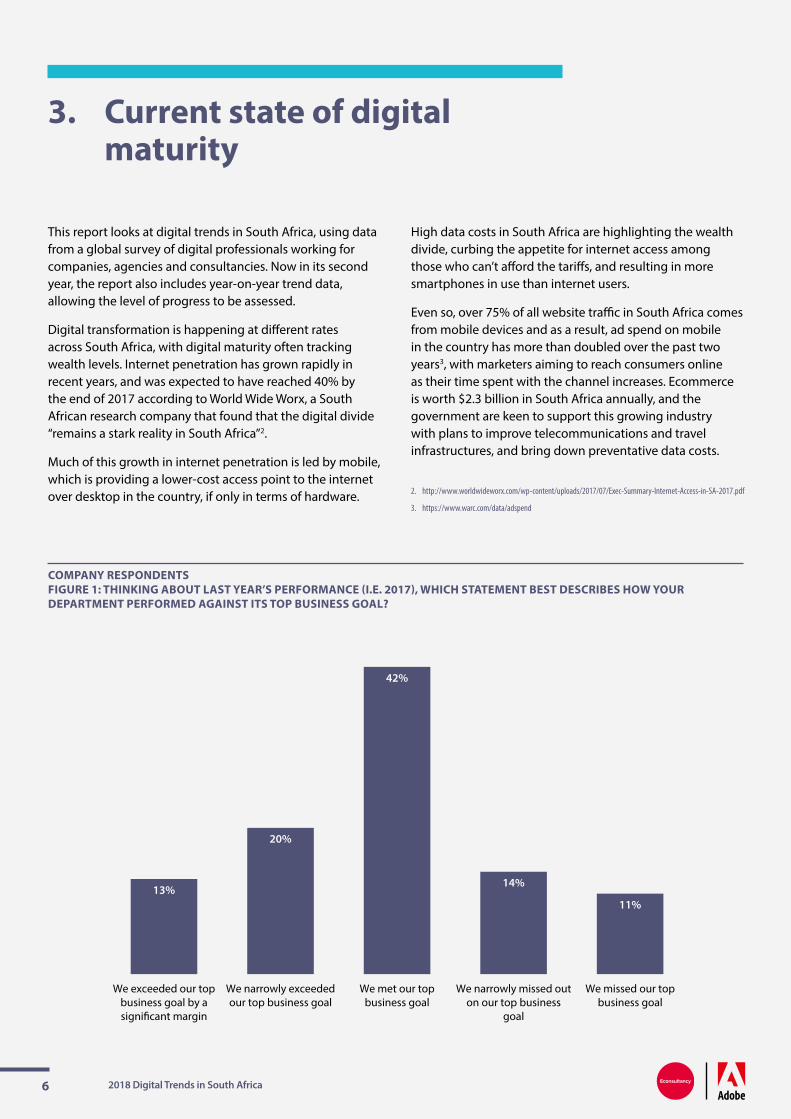

COMPANY RESPONDENTS FIGURE 1: THINKING ABOUT LAST YEAR’S PERFORMANCE (I.E. 2017), WHICH STATEMENT BEST DESCRIBES HOW YOUR DEPARTMENT PERFORMED AGAINST ITS TOP BUSINESS GOAL?

2018 Digital Trends in South Africa6

This report looks at digital trends in South Africa, using data from a global survey of digital professionals working for companies, agencies and consultancies. Now in its second year, the report also includes year-on-year trend data, allowing the level of progress to be assessed.

Digital transformation is happening at different rates across South Africa, with digital maturity often tracking wealth levels. Internet penetration has grown rapidly in recent years, and was expected to have reached 40% by the end of 2017 according to World Wide Worx, a South African research company that found that the digital divide “remains a stark reality in South Africa”2.

Much of this growth in internet penetration is led by mobile, which is providing a lower-cost access point to the internet over desktop in the country, if only in terms of hardware.

High data costs in South Africa are highlighting the wealth divide, curbing the appetite for internet access among those who can’t afford the tariffs, and resulting in more smartphones in use than internet users.

Even so, over 75% of all website traffic in South Africa comes from mobile devices and as a result, ad spend on mobile in the country has more than doubled over the past two years3, with marketers aiming to reach consumers online as their time spent with the channel increases. Ecommerce is worth $2.3 billion in South Africa annually, and the government are keen to support this growing industry with plans to improve telecommunications and travel infrastructures, and bring down preventative data costs.

3. Current state of digital maturity

2. http://www.worldwideworx.com/wp-content/uploads/2017/07/Exec-Summary-Internet-Access-in-SA-2017.pdf

3. https://www.warc.com/data/adspend

28%

33% 33%

6%

We are signi�cantlyoutperforming our

competitors

We are slightly outperformingour competitors

We are slightlyunderperforming against our

competitors

We are signi�cantlyunderperforming against our

competitors

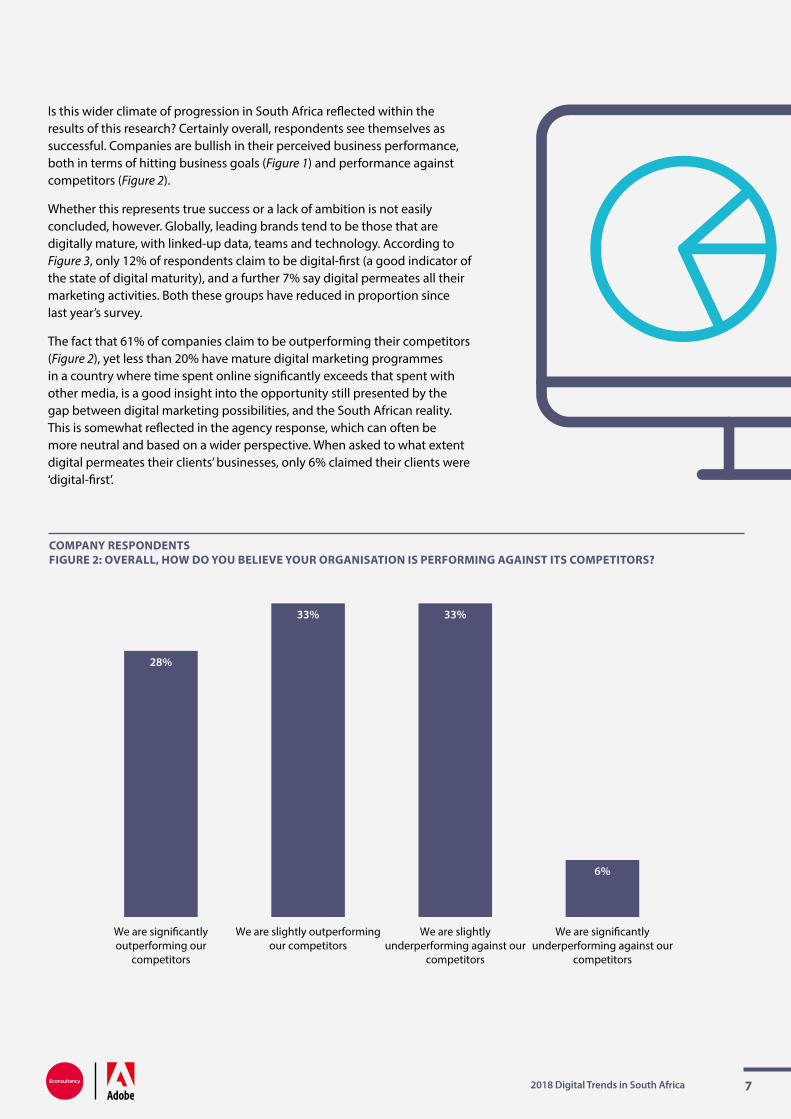

COMPANY RESPONDENTS FIGURE 2: OVERALL, HOW DO YOU BELIEVE YOUR ORGANISATION IS PERFORMING AGAINST ITS COMPETITORS?

2018 Digital Trends in South Africa 7

Is this wider climate of progression in South Africa reflected within the results of this research? Certainly overall, respondents see themselves as successful. Companies are bullish in their perceived business performance, both in terms of hitting business goals (Figure 1) and performance against competitors (Figure 2).

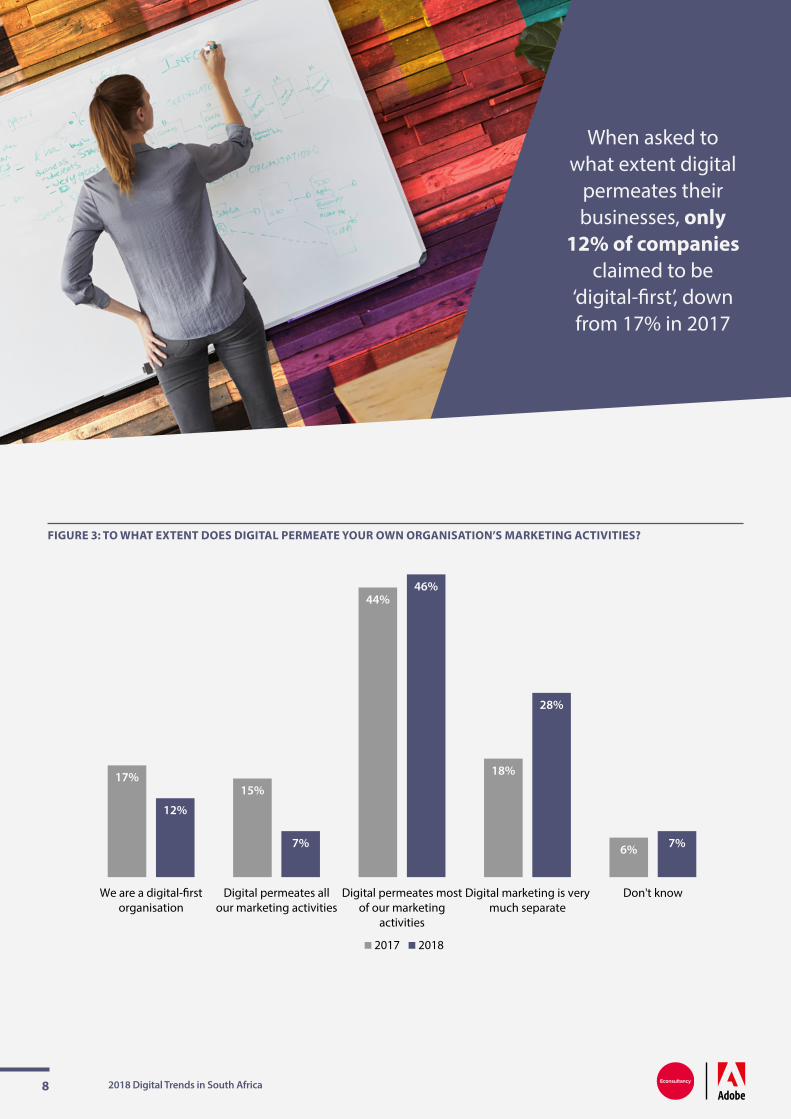

Whether this represents true success or a lack of ambition is not easily concluded, however. Globally, leading brands tend to be those that are digitally mature, with linked-up data, teams and technology. According to Figure 3, only 12% of respondents claim to be digital-first (a good indicator of the state of digital maturity), and a further 7% say digital permeates all their marketing activities. Both these groups have reduced in proportion since last year’s survey.

The fact that 61% of companies claim to be outperforming their competitors (Figure 2), yet less than 20% have mature digital marketing programmes in a country where time spent online significantly exceeds that spent with other media, is a good insight into the opportunity still presented by the gap between digital marketing possibilities, and the South African reality. This is somewhat reflected in the agency response, which can often be more neutral and based on a wider perspective. When asked to what extent digital permeates their clients’ businesses, only 6% claimed their clients were ‘digital-first’.

“

17%15%

44%

18%

6%

12%

7%

46%

28%

7%

We are a digital-�rstorganisation

Digital permeates allour marketing activities

Digital permeates mostof our marketing

activities

Digital marketing is verymuch separate

Don't know

2017 2018

FIGURE 3: TO WHAT EXTENT DOES DIGITAL PERMEATE YOUR OWN ORGANISATION’S MARKETING ACTIVITIES?

2018 Digital Trends in South Africa8

When asked to what extent digital

permeates their businesses, only

12% of companies claimed to be

‘digital-first’, down from 17% in 2017

FIGURE 4: PROPORTION OF COMPANY RESPONDENTS AGREEING (‘STRONGLY’ OR ‘SOMEWHAT’) WITH THESE STATEMENTS

56%

58%

66%

71%

72%

76%

82%

84%

60%

59%

74%

57%

72%

69%

66%

85%

Technology – we have the tools to use data in order to create compelling, personalised, real-time experiences

UX design – we have well-designed user journeys that facilitate clear communication and a seamless transaction

Collaboration – we have tools that allow for streamlined work�ows between creative and content marketers /

web teams

Data – we have access and control over customer and marketing application data

Strategy – we have a cohesive plan, long-term view and executive support for the future of our customer

Process – we have the means and methods to ensure that strategy is carried out e�ciently

Skills – we are combining digital marketing skills with technology

Culture – we have a cross-team approach with the customer at the heart of all initiatives

2017 2018

2018 Digital Trends in South Africa 9

Figure 4 illustrates the typical pillars of digital maturity, and reveals that company culture is strong in South Africa, with 84% companies stating that they have a cross-team approach. This is higher than the average across the rest of the world, where 73% ‘strongly’ or ‘somewhat’ agreed.

However, as is the case globally, this research highlights the fact that technology is a stumbling block for South African marketers. Figure 4 shows that just over half (56%) agree (‘strongly’ or ‘somewhat’) that they have the tools to use data in order to create compelling, personalised, real-time experiences, down from 60% last year. The expense of technology can present a barrier to even large companies, and onboarding technology associated with customer experience can often be accompanied by the pain of integrating or phasing out legacy systems and tools.

Over the next year, three-quarters of respondents are planning to increase their budgets for digital marketing, and this research shows that their focus will be on content and experience management. Customer experience has been high on the marketing agenda globally for the last few years and is seen as the crucial factor in the purchase decisions of consumers in an era of tremendous choice. Impacted by almost every other aspect of marketing, improving the customer experience is a central driving force behind change in digital marketing strategy. As digital marketing efforts reach an increasingly large proportion of the South African population, and choice increases, marketers in South Africa need to put CX first to stay ahead of the competition.

COMPANY RESPONDENTS FIGURE 5: HOW IMPORTANT WILL THE FOLLOWING BE FOR YOUR DIGITAL MARKETING OVER THE NEXT FEW YEARS?

49%

51%

52%

66%

69%

73%

83%

44%

41%

36%

26%

29%

27%

17%

7%

8%

12%

8%

2%

Understanding when and where customers use di�erentdevices

Using o�ine data to optimise the online experience

Using online data to optimise the o�ine experience

Understanding how mobile users research / buy products

Training teams in new techniques, channels and disciplines

Ensuring consistency of message across channels

Optimising the customer journey across multipletouchpoints

Very important Quite important Not important

2018 Digital Trends in South Africa10

Globally, the most successful companies are those that are digitally mature (often assessed on the elements featured in Figure 4), and tend to have seamless customer journeys that link across all touchpoints. Figure 5 shows that companies in South Africa realise the importance of this seamless customer journey, and of consistent messaging across channels.

The previous section discussed how South Africa is currently mobile-led, with many consumers only having access to the internet through their one mobile device. This may explain why understanding when and where customers use different devices is the lowest digital marketing priority for respondents over the coming years, particularly as the telecommunications infrastructure across large parts of South Africa is not yet developed enough to support location-based services.

However, marketers are clearly seeing traffic and engagement through an increased number of channels and media. Figure 5 shows that a large majority (83%) of respondents see optimising the customer journey across multiple touchpoints as ‘very important’ for their digital marketing over the next few years. As the number of channels and touchpoints increases, continued emphasis will need to be placed on ensuring the success of more complex campaigns through consistent and effective integration.

4. Customer journeys are the priority as channel choice increases

83% of respondents see optimising the customer journey across multiple touchpoints as ‘very important’ for their digital marketing over the next few years

“More than half of respondents said they had a fragmented approach with inconsistent integration between technologies

COMPANY RESPONDENTS FIGURE 6: PLEASE RANK THE IMPORTANCE OF THESE ELEMENTS OF THE CUSTOMER EXPERIENCE FROM 1 TO 5, WHERE 5 IS ‘MOST IMPORTANT TO SUCCESS’.

6%

6%

6%

3%

6%

3%

3%

6%

3%

12%

3%

6%

9%

8%

3%

6%

18%

15%

31%

24%

21%

6%

6%

15%

47%

37%

29%

34%

26%

44%

47%

26%

26%

30%

31%

33%

38%

39%

41%

47%

Collaboration – having tools that allow for streamlined work�ows between creative and content marketers / web

teams

UX design – having well-designed user journeys that facilitate clear communication and a seamless transaction

Culture – a cross-team approach with the customer at the heart of all initiatives

Data – having access and control over customer and marketing application data

Skills – combining digital marketing skills with technology

Strategy – the cohesive plan, long-term view and executive support for the future of our customer

Process – having the means and methods to ensure strategy is carried out e�ciently

Technology – the tools to use data to create compelling, personalised, real-time experiences

1 2 3 4 5

2018 Digital Trends in South Africa 11

Most important to the success of CX strategies are the tools and technologies used, according to Figure 6. However, technology was also ranked as one of the hardest elements to master, reflecting the technology concerns discussed in the previous section (Figure 4). This research shows that current capabilities are limited: when asked about their approach to marketing and customer experience technology, more than half (56%) said they had a fragmented approach with inconsistent integration between technologies, compared to an average of 43% across the rest of the world.

COMPANY RESPONDENTS FIGURE 7: HOW IMPORTANT DO YOU THINK THE FOLLOWING INTERNAL FACTORS WILL BE IN DELIVERING A GREAT CUSTOMER EXPERIENCE OVER THE COMING YEAR?

43%

50%

52%

62%

68%

71%

88%

53%

36%

43%

36%

30%

29%

10%

4%

14%

5%

2%

2%

2%

Ongoing and widespread testing of creative variations

Experimentation with channel-speci�c creative formats (e.g.Facebook 360 video, Instagram Stories etc.)

Building more ‘native’ online content such as interactive applications, short-form video etc.

Improving content marketing through immersivestorytelling

Optimising internal collaboration between creative andmarketing teams

Optimising creative work�ows to facilitate the rapidcreation and deployment of content across multiple

platforms

Improving data analysis capabilities to better understandcustomer experience requirements

Very important Quite important Not important

2018 Digital Trends in South Africa12

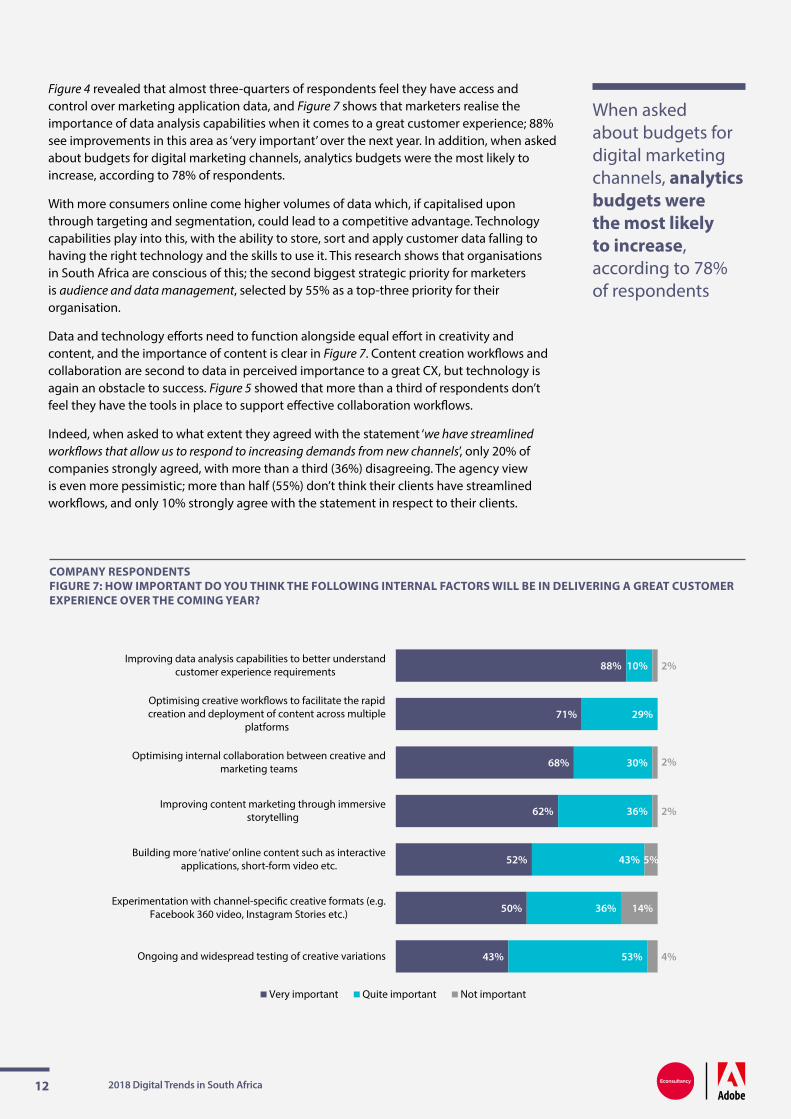

Figure 4 revealed that almost three-quarters of respondents feel they have access and control over marketing application data, and Figure 7 shows that marketers realise the importance of data analysis capabilities when it comes to a great customer experience; 88% see improvements in this area as ‘very important’ over the next year. In addition, when asked about budgets for digital marketing channels, analytics budgets were the most likely to increase, according to 78% of respondents.

With more consumers online come higher volumes of data which, if capitalised upon through targeting and segmentation, could lead to a competitive advantage. Technology capabilities play into this, with the ability to store, sort and apply customer data falling to having the right technology and the skills to use it. This research shows that organisations in South Africa are conscious of this; the second biggest strategic priority for marketers is audience and data management, selected by 55% as a top-three priority for their organisation.

Data and technology efforts need to function alongside equal effort in creativity and content, and the importance of content is clear in Figure 7. Content creation workflows and collaboration are second to data in perceived importance to a great CX, but technology is again an obstacle to success. Figure 5 showed that more than a third of respondents don’t feel they have the tools in place to support effective collaboration workflows.

Indeed, when asked to what extent they agreed with the statement ‘we have streamlined workflows that allow us to respond to increasing demands from new channels’, only 20% of companies strongly agreed, with more than a third (36%) disagreeing. The agency view is even more pessimistic; more than half (55%) don’t think their clients have streamlined workflows, and only 10% strongly agree with the statement in respect to their clients.

When asked about budgets for digital marketing channels, analytics budgets were the most likely to increase, according to 78% of respondents

FIGURE 8: WHICH THREE DIGITAL-RELATED AREAS ARE THE TOP PRIORITIES FOR YOUR ORGANISATION (OR YOUR CLIENTS’) IN 2018?

5%

2%

6%

8%

20%

8%

8%

5%

12%

6%

15%

20%

12%

11%

21%

9%

27%

27%

23%

39%

1%

2%

7%

7%

9%

10%

10%

10%

10%

11%

13%

16%

16%

18%

19%

21%

22%

25%

27%

27%

None of the above

Voice interfaces

Programmatic buying / optimisation

Joining up online and o�ine data

Mobile optimisation

Customer scoring and predictive marketing

Conversion rate optimisation

Marketing automation

Content management

Real-time marketing

Search engine marketing

Social media analytics

Customer journey management

Targeting and personalisation

Multichannel campaign management

Mobile app engagement

Brand building / viral marketing

Video content

Content marketing

Social media engagement

Company respondents Agency respondents

2018 Digital Trends in South Africa 13

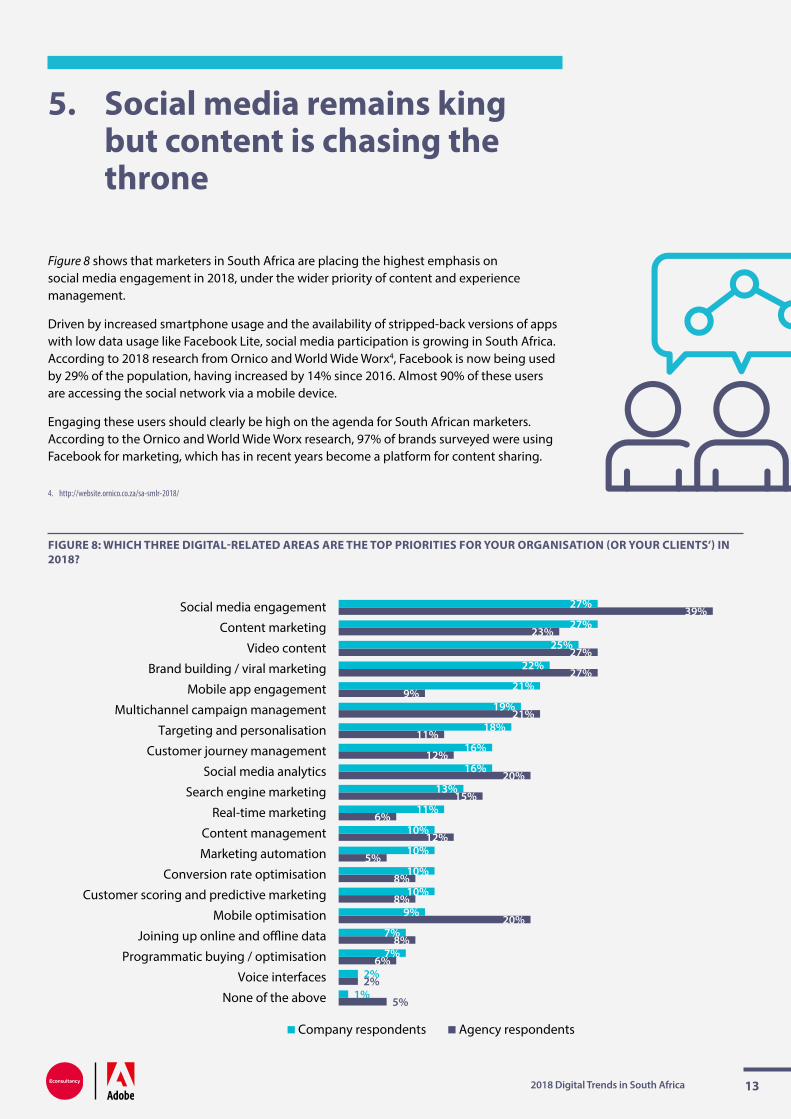

5. Social media remains king but content is chasing the throne

Figure 8 shows that marketers in South Africa are placing the highest emphasis on social media engagement in 2018, under the wider priority of content and experience management.

Driven by increased smartphone usage and the availability of stripped-back versions of apps with low data usage like Facebook Lite, social media participation is growing in South Africa. According to 2018 research from Ornico and World Wide Worx4, Facebook is now being used by 29% of the population, having increased by 14% since 2016. Almost 90% of these users are accessing the social network via a mobile device.

Engaging these users should clearly be high on the agenda for South African marketers. According to the Ornico and World Wide Worx research, 97% of brands surveyed were using Facebook for marketing, which has in recent years become a platform for content sharing.

4. http://website.ornico.co.za/sa-smlr-2018/

COMPANY RESPONDENTS FIGURE 9: ‘WE ARE BRINGING CONTENT CREATION IN-HOUSE’ – AGREE OR DISAGREE

48%

38%

9%

5%

Strongly agree Somewhat agree Somewhat disagree Strongly disagree

2018 Digital Trends in South Africa14

With customer experience a key priority, and content driving digital experiences, marketers are clearly aware of the need to create compelling content that functions across platforms. Seven in ten (71%) strongly agree that optimising creative workflows to facilitate the rapid creation and deployment of content across multiple platforms is very important to delivering a great customer experience over the coming year (Figure 7).

Figure 8 supports this, showing that content marketing is the second most important digital priority for companies this year. Agencies, perhaps keen to capitalise on the opportunities presented by mobile, put more emphasis on social in the first instance, but mobile optimisation and video content were selected by a larger proportion of agencies than companies.

The dominance of mobile in the region means that optimising content and experiences for mobile becomes paramount. It is possible that the experience of agencies is showing through here, with agency respondents realising this importance more than companies. Indeed, agencies were 26% more likely to see understanding how mobile users research/buy products as ‘very important’ to their clients’ digital marketing over the next few years.

It is perhaps a concern then that 86% of companies are bringing content creation in-house (Figure 9). A separate survey of South African marketers by content agency Narrative Media supported these findings, stating that 85% of marketers are directly involved in their brand’s marketing efforts, and 61% see themselves as advanced or expert at content marketing in-house5. The research also found that only 53% of companies were using mobile for content marketing.

While it is positive that confidence around internal marketing skills is high, and that brands are staying close to their messaging, marketers need to ensure that this isn’t to the detriment of customer experience in a mobile-centric customer journey. Though social marketing will be able to reach many mobile users through social media apps, it is still important that optimisation of the content for mobile consumption takes place, particularly for video where factors like audio and screen rotation need to be considered.

Brands also need to be wary of focusing overly on social media and viral marketing, as while good for short-term awareness and of lower cost than other channels, typically campaigns that lead with social have a short-term impact that doesn’t always translate into long-term ROI.

5. http://www.narrativemedia.co.za/digital_magazines/narrative/2017/content-marketer/index.html

32%

37%

24%

7%

23%

31%

40%

6%

Yes, de�nitely Yes, somewhat No, not really Not at all

2017 2018

COMPANY RESPONDENTS FIGURE 10: WOULD YOU DESCRIBE YOUR COMPANY AS A DESIGN-DRIVEN ORGANISATION?

2018 Digital Trends in South Africa 15

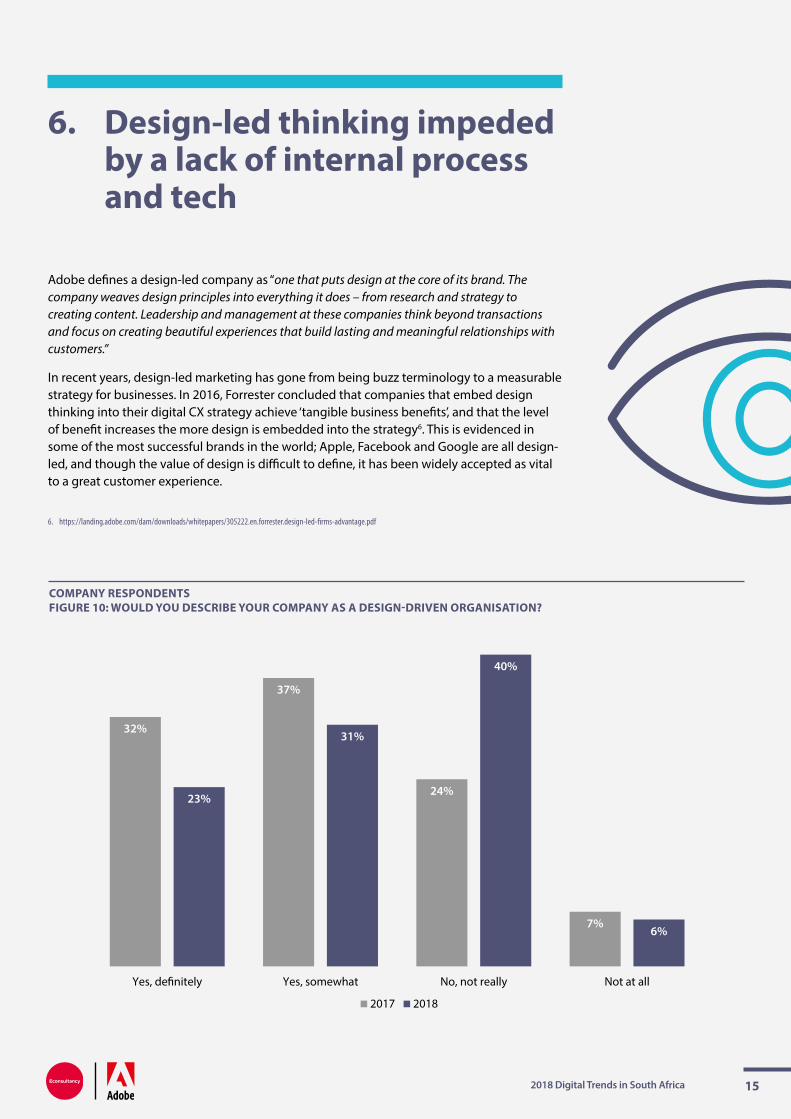

6. Design-led thinking impeded by a lack of internal process and tech

Adobe defines a design-led company as “one that puts design at the core of its brand. The company weaves design principles into everything it does – from research and strategy to creating content. Leadership and management at these companies think beyond transactions and focus on creating beautiful experiences that build lasting and meaningful relationships with customers.”

In recent years, design-led marketing has gone from being buzz terminology to a measurable strategy for businesses. In 2016, Forrester concluded that companies that embed design thinking into their digital CX strategy achieve ‘tangible business benefits’, and that the level of benefit increases the more design is embedded into the strategy6. This is evidenced in some of the most successful brands in the world; Apple, Facebook and Google are all design-led, and though the value of design is difficult to define, it has been widely accepted as vital to a great customer experience.

6. https://landing.adobe.com/dam/downloads/whitepapers/305222.en.forrester.design-led-firms-advantage.pdf

COMPANY RESPONDENTS FIGURE 11: PLEASE INDICATE WHETHER YOU AGREE OR DISAGREE WITH THE FOLLOWING STATEMENTS.

14%

16%

17%

18%

18%

23%

26%

37%

38%

35%

37%

49%

40%

39%

47%

35%

37%

49%

38%

29%

21%

32%

25%

18%

25%

17%

8%

13%

18%

13%

10%

18%

12%

14%

9%

5%

Our CMS facilitates a brand-enhancing digital presence

We have the processes and collaborative work�ows weneed to achieve a design advantage

We have the people we need to engineer good customerexperiences

We have the centralised assets we need to be consistent inour approach to design

We have a consistent approach to design across the wholebusiness

We are investing in design to help di�erentiate our brand

Our design approach is consistent across the digital andphysical worlds

Creativity is highly valued within our organisation

Design-driven companies outperform other businesses

Strongly agree Somewhat agree Somewhat disagree Strongly disagree

2018 Digital Trends in South Africa16

Though the stated focus on customer experience has been consistent over the past year, this research shows a significantly lower proportion of respondents seeing themselves as design-driven than last year (Figure 10), and only 58% think they have well-designed user journeys (Figure 4). Yet, compared to their international peers, South African marketers remain more confident in their abilities, with a higher proportion of respondents saying they are ‘definitely’ design-driven (23% in South Africa versus an average of 17% across the rest of the world) despite the drop in the country’s year-on-year results.

The agency view has also changed demonstrably in the past year, with a similar drop in the proportion of those seeing their clients as ‘definitely’ design-driven, from 31% to 10% this year. With increasing mainstream media coverage of design-driven marketing and ‘design thinking’, it is possible that understanding of what it means to be a design-driven organisation has increased over the past year, resulting in a drop in confidence around current capabilities.

As a notoriously hard-to-measure approach, measurement may be a factor in this drop in confidence. However, the effect of a design-driven strategy appears to be understood by survey respondents. Almost all agree that design-driven companies outperform other businesses (Figure 11), but as with progress towards a good customer experience, it appears that technology and workflows are presenting an obstacle to success.

Figure 11 shows that technology constraints (in this case in terms of content management systems) are hindering the creation of a brand-enhancing digital presence for the majority (51%), and almost half (47%) don’t have the processes and workflows in place to achieve a design advantage. Agencies agree, with a typically more negative outlook; 64% believe their clients don’t have workflows and processes in place, and 56% see issues with their clients’ CMS.

A significantly lower proportion of respondents see themselves as design-driven than last year, with only 58% thinking that they have well-designed user journeys

20%

34%

46%

15%

31%

54%

Yes - we are using it already Yes - we are planning to use it No - we have no plans to use it

South Africa Rest of the world

COMPANY RESPONDENTS FIGURE 12: IS YOUR ORGANISATION USING OR PLANNING TO USE ARTIFICIAL INTELLIGENCE (AI) IN THE NEXT 12 MONTHS?

2018 Digital Trends in South Africa 17

7. The future is personalised, but not yet automated

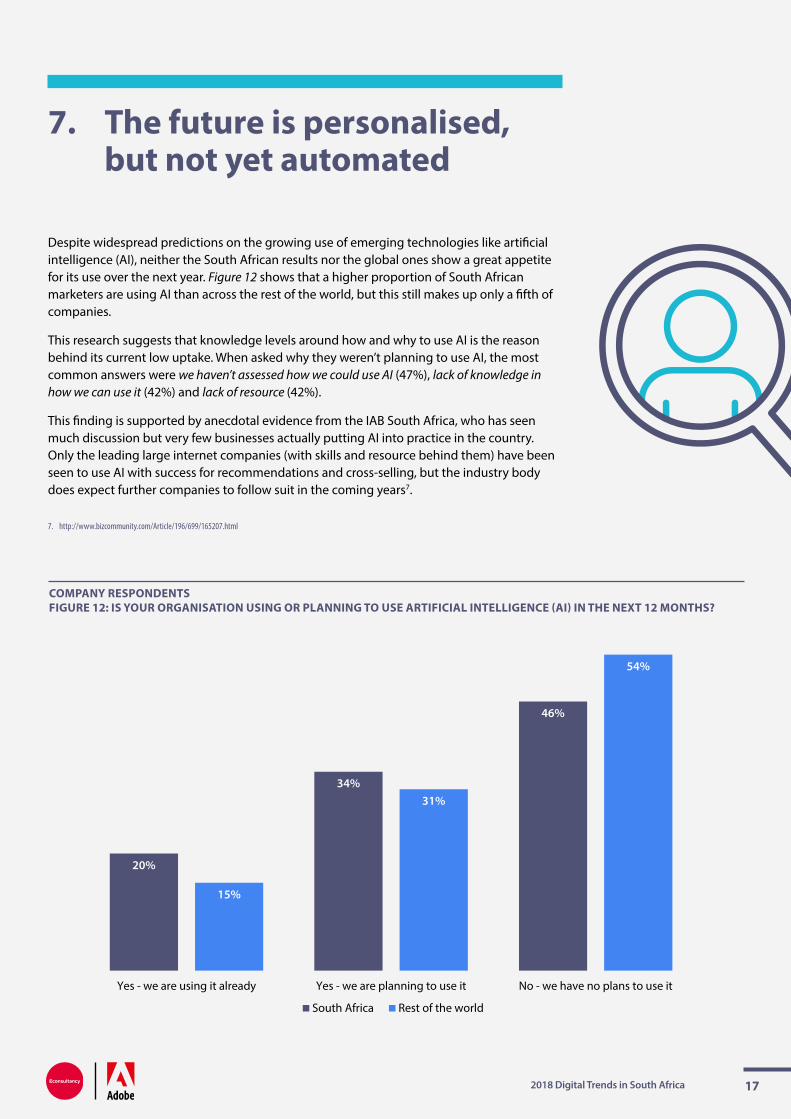

Despite widespread predictions on the growing use of emerging technologies like artificial intelligence (AI), neither the South African results nor the global ones show a great appetite for its use over the next year. Figure 12 shows that a higher proportion of South African marketers are using AI than across the rest of the world, but this still makes up only a fifth of companies.

This research suggests that knowledge levels around how and why to use AI is the reason behind its current low uptake. When asked why they weren’t planning to use AI, the most common answers were we haven’t assessed how we could use AI (47%), lack of knowledge in how we can use it (42%) and lack of resource (42%).

This finding is supported by anecdotal evidence from the IAB South Africa, who has seen much discussion but very few businesses actually putting AI into practice in the country. Only the leading large internet companies (with skills and resource behind them) have been seen to use AI with success for recommendations and cross-selling, but the industry body does expect further companies to follow suit in the coming years7.

7. http://www.bizcommunity.com/Article/196/699/165207.html

A higher proportion of South African marketers

are currently using AI than across the rest

of the world, but this still makes up only a

fifth of companies

2018 Digital Trends in South Africa18

In South Africa’s mobile-led market, one area of AI that has seen increased uptake is the use of bots via Facebook Messenger. As the most-used social platform in the country, Facebook is enabling brands to access consumers who previously would only have been reached through above-the-line channels like TV and out of home. Typically used by large brands that have employed the technique with success in other regions, the tactic is producing returns for marketers.

A recent example is from FMCG behemoth Unilever, who wanted to extend the reach of its Knorr food brand. Knorr created the ‘Dinner On Demand’ chatbot, a Facebook Messenger bot that uses AI, providing recipes based on ingredients users already have in their kitchen. Knorr reached over two million users in two months through the bot, in a first of its kind use of AI in South Africa8.

As AI use cases like Knorr’s become more prevalent, and the uptake of AI across the rest of the world picks up speed, we may see South Africa following suit, though the pace is likely to be slower due to the developing state of the country’s digital marketing industry.

Legacy infrastructure, technologies and dated corporate structures mean the implementation of emerging technologies can be slow, worsened by a smaller cohort of people with the associated skills and knowledge of the tools. Added to this is the fear of job losses associated with automation that could exacerbate the income inequalities already so prevalent. When comparing the digital priorities of marketers in South Africa to those of their international peers, international marketers are 60% more likely to be prioritising automation over the next year.

However, the country certainly cannot afford to ignore emerging technologies; a recent analysis by consulting firm Accenture found that AI has the potential to significantly add to the annual economic growth rates in South Africa by 2035, at 3.5% without AI, compared to 4.5% with9.

8. http://www.mmaglobal.com/smarties-2017/finalists/winners/region:3

9. https://www.accenture.com/t20170810T154838Z__w__/za-en/_acnmedia/Accenture/Conversion-Assets/DotCom/Documents/Local/za-en/Accenture-AI-South-Africa-Ready.pdf

FIGURE 13: LOOKING AHEAD, WHICH OF THESE DO YOU REGARD AS THE MOST EXCITING PROSPECT IN THREE YEARS’ TIME?

2%

4%

13%

20%

20%

9%

32%

1%

5%

10%

12%

14%

23%

35%

Other

Voice interfaces e.g. Amazon Echo, Google Home

Enhanced payment technologiese.g. mobile wallets, e-receipts

Internet of Things / connected devicese.g. wearables, audience tracking

Engaging audiences through virtual or augmented reality

Utilising arti�cial intelligence / bots to drive campaigns andexperiences

Delivering personalised experiences in real time

Company respondents Agency respondents

2018 Digital Trends in South Africa 19

And interest is growing for the future; almost a quarter of respondents said that the use of artificial intelligence/bots to drive campaigns and experiences will be the most exciting prospect in three years’ time, second only to delivering personalised experiences in real time (Figure 13). Added to this is the planned launch of Amazon Echo and Google Home – voice recognition devices that have become popular in developed markets like the UK and US, and likely to drive interest in South Africa once the devices are widely available.

Though Figure 13 shows excitement for technological advances like AI, virtual and augmented reality, the largest proportion remain more focused on the customer experience for the future. Both companies and agencies were most likely to expect delivering personalised experiences in real time to be the most exciting prospect in three years’ time. While targeting, personalisation and real-time marketing were not top of the immediate digital priorities of respondents, when pitted against new and emerging technologies, real-time personalisation emerges the winner.

Personalisation relies on high-quality, high-volume data, and personalisation in real time requires technology capabilities to be on point. We saw in Section 4 that respondents see technology as the most important element for improving the customer experience, but also the hardest to master, so improvements in skills and capabilities will likely be seen around CX technologies before we begin to see innovations like AI become prevalent in South Africa.

2018 Digital Trends in South Africa20

8. Fit for the future: five areas South African marketers should focus on

1. Embrace the social opportunity but don’t forget mobile

As more and more South Africans gain reliable and regular access to the internet, the number of active users on social platforms also increases. Engaging with these new users is a key priority for marketers in the coming years, but for organisations looking to be leaders in their field, the access device of these social users, which in the majority of cases is mobile, must be the focus.

Targeting mobile as a priority channel will allow businesses to reach and engage with consumers not only on social platforms, but through myriad other touchpoints too, and will contribute towards ensuring the consistency of journeys that is so important to the modern marketer.

2. Prepare for digital in every business function

Digitally mature organisations are, more often than not, leaders in their field. For organisations to gain a competitive advantage, they need to set in place processes and strategies that will enable digital to permeate every aspect of their business. Technology should be the focus here, particularly for larger organisation that have further to go in terms of adapting legacy systems and processes to the digital era.

3. Create agile content

With the focus on content creation to improve the customer journey, marketers need to ensure that a balance is maintained between quantity and quality, and optimisation for individual channels versus a cross-channel plan. Marketers are increasingly bringing their content creation in-house, but they should ensure that this isn’t to the detriment of its effectiveness across mobile, which is the dominant channel in the region, but more challenging to market through.

4. Understand the impact of design

There is now a body of evidence to support the idea that businesses that are design-led have an advantage over the rest. Companies should test and learn the effect of design-led strategies and processes on business goals, and attempt to make this a consistent approach across all functions.

5. Don’t ignore emerging technologies

Research has shown that AI could significantly add to the economic future of South Africa. If not using or even planning to use technologies like AI, companies should keep an eye on evolving use cases of these technologies in the country, learning from their international peers and building internal knowledge and skills, so that any future integration of these tools into marketing strategies can be capitalised on from the outset.

FIGURE 14: WHICH OF THE FOLLOWING BEST DESCRIBES YOUR COMPANY OR ROLE?

58%

42%

Client-side (part of an in-house team) Agency / vendor / consultant

FIGURE 15: WHAT BEST DESCRIBES YOUR JOB ROLE?

12%

5%

3%

14%

31%

11%

24%

18%

0%

2%

6%

11%

31%

32%

Other

VP / SVP / EVP

Board level

C-level / general manager

Director / senior director

Junior executive / associate

Manager

Company respondents Agency respondents

2018 Digital Trends in South Africa 21

9. Appendix: respondent profiles

COMPANY RESPONDENTS FIGURE 17: ARE YOU MORE FOCUSED ON B2B OR B2C AS A BUSINESS?

34%

20%

46%

B2C B2B B2B and B2C (equally)

COMPANY RESPONDENTS FIGURE 16: IN WHICH BUSINESS FUNCTION DO YOU WORK?

11%

1%

1%

2%

3%

3%

4%

4%

5%

27%

39%

Other

Web development

Ecommerce

Mobile team

Operations

Analytics team

IT

Customer service

Content / editorial

Marketing

Creative / design

2018 Digital Trends in South Africa22

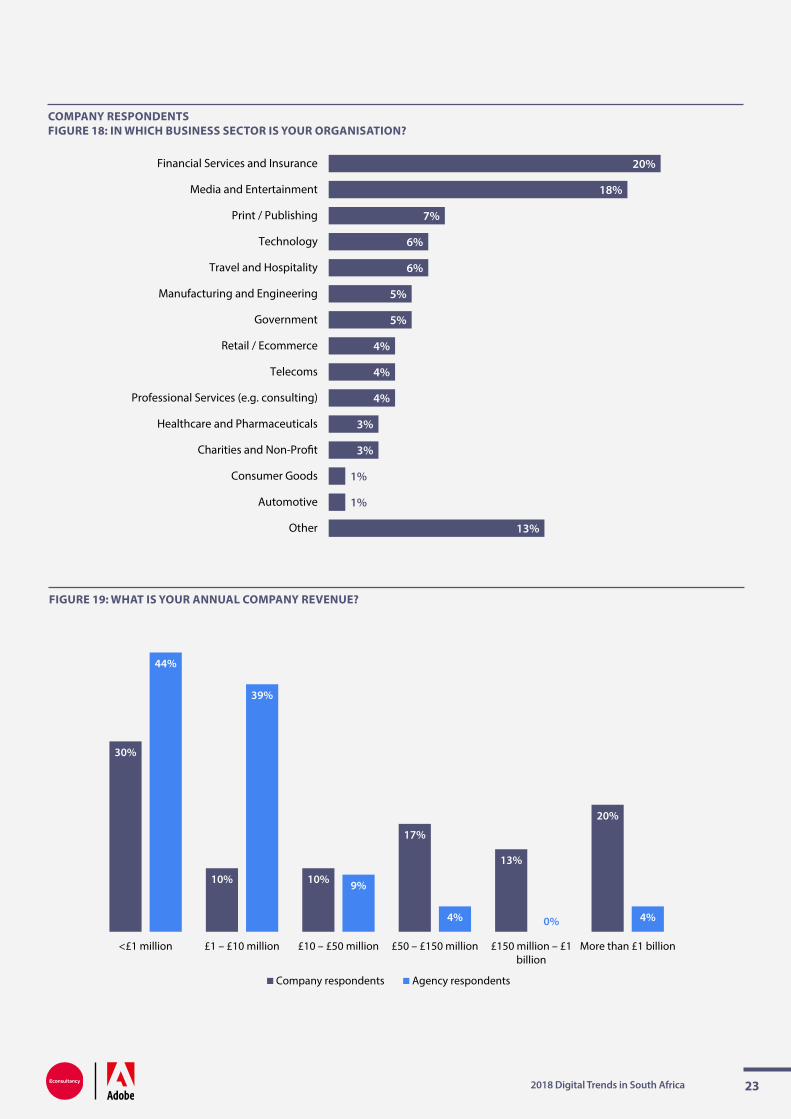

COMPANY RESPONDENTS FIGURE 18: IN WHICH BUSINESS SECTOR IS YOUR ORGANISATION?

13%

1%

1%

3%

3%

4%

4%

4%

5%

5%

6%

6%

7%

18%

20%

Other

Automotive

Consumer Goods

Charities and Non-Pro�t

Healthcare and Pharmaceuticals

Professional Services (e.g. consulting)

Telecoms

Retail / Ecommerce

Government

Manufacturing and Engineering

Travel and Hospitality

Technology

Print / Publishing

Media and Entertainment

Financial Services and Insurance

FIGURE 19: WHAT IS YOUR ANNUAL COMPANY REVENUE?

30%

10% 10%

17%

13%

20%

44%

39%

9%

4% 0% 4%

<£1 million £1 – £10 million £10 – £50 million £50 – £150 million £150 million – £1 billion

More than £1 billion

Company respondents Agency respondents

2018 Digital Trends in South Africa 23

About Econsultancy

Econsultancy’s mission is to help its customers achieve excellence in digital business, marketing and ecommerce through research, training and events.

Founded in 1999, Econsultancy has offices in New York, London and Singapore.

Econsultancy is used by over 600,000 professionals every month. Subscribers get access to research, market data, best practice guides, case studies and elearning – all focused on helping individuals and enterprises get better at digital.

The subscription is supported by digital transformation services including digital capability programmes, training courses, skills assessments and audits. We train and develop thousands of professionals each year as well as running events and networking that bring the Econsultancy community together around the world.

Subscribe to Econsultancy today to accelerate your journey to digital excellence.

Call us to find out more:

› New York: +1 212 971 0630

› London: +44 207 269 1450

› Singapore: +65 6653 1911

About Adobe Experience Cloud

Adobe Experience Cloud is a comprehensive set of cloud services designed to give enterprises everything needed to deliver exceptional customer experiences.

Comprised of Adobe Marketing Cloud, Adobe Advertising Cloud and Adobe Analytics Cloud, Experience Cloud is built on the Adobe Cloud Platform and integrated with Adobe Creative Cloud and Document Cloud.

Leveraging Adobe Sensei’s machine learning and artificial intelligence capabilities, Adobe Experience Cloud combines world-class solutions, a complete extensive platform, comprehensive data and content systems, and a robust partner ecosystem that offer an unmatched expertise in experience delivery.

To learn more about Adobe Experience Cloud, visit http://www.adobe.com/uk/experience-cloud.html.