Embed Size (px)

Citation preview

2017 NONPROFIT OUTLOOK SURVEY:OVERCOMING UNCERTAINTY WITH SUPPORT, STRATEGY, AND OPTIMISM

ABOUT EKS&H

EKS&H is a nationally recognized professional services

firm providing audit, tax, technology, wealth advisory, and

business consulting services to public and private clients

locally, nationally, and internationally. Our commitment

to client service has resulted in sustained growth since we

began in 1978. Working collaboratively, the best measure of

our success is the success of our clients.

Passion is a critical element to success.

The leaders of our nonprofit clients have passion for their

organizations’ missions, which is a large part why they’re

so successful. Similarly, we have a passion to serve these

nonprofit clients. One important element of our service is to

strive to present new, useful, and actionable information that

helps make better strategic decisions. In support of that goal,

we are proud to present the results of our latest Nonprofit

Outlook Survey.

In 2016, measures such as revenue and demand appear to have

improved for most organizations. Growing expenses, however,

tempered some of that success and impacted profitability. When

it comes to the 2017 outlook, many respondents expressed

some major uncertainty, particularly related to the economic

impacts of the changing control of government. In the face of

these unknowns, we are very pleased with the positive outlook

many participants expressed as it relates to revenue, profit, and

demand. We consider this confidence and optimism to be a

wonderful facet of the passion of our nonprofit client leaders.

As always, the economy will have important implications

related to attracting and retaining talent, and that appears to

have grown as an area of focus for 2017. In other good news,

wages are rising, board effectiveness appears to have improved

in many ways, and the attention given to strategically using

technology has also grown since our previous survey.

As always, the results described in the following pages could

not have been compiled without the generous time and effort

of many nonprofit leaders. We thank these individuals for

their participation and invite other nonprofits to participate

in the future.

If this year’s results raise any additional questions or concerns

about the strategic decisions of your organization, please do

not hesitate to reach out to us to discuss. We look forward to

serving you in 2017!

ABOUT THE EKS&H NONPROFIT CLIENT SERVICE TEAM

With more than 50 nonprofit industry-focused professionals

and dedicated audit, tax, and consulting partners, the

Denver-based nonprofit specialty group at EKS&H is

larger than all local nonprofit “niche” firms as well as the

nonprofit groups within the regional/national firms. We

currently serve a wide variety of more than 125 local and

national nonprofit clients, including private and community

foundations; professional associations; and organizations

involved with human services, animals, the environment,

healthcare, religion, education, fundraising, and the arts.

Ann Hinkins, CPA Lisa Meacham, CPA Ryan Sells, CPA Kelly Kozeliski, CPA Craig Choun, CPA Dori Eggett, CPA

2017 NONPROFIT OUTLOOK SURVEY:OVERCOMING UNCERTAINTY WITH SUPPORT,

STRATEGY, AND OPTIMISM

Key Findings

2016 Nonprofit Performance

2017 Nonprofit Outlook

2017 Goals

2017 Challenges

2017 Strategies for Success

Talent and Compensation

Technology and Giving

Board Performance

About the Survey and Participants

3

5

11

17

18

19

19

25

27

28

2

3

2016• Two-thirds of respondents indicated that revenue/support

exceeded expenses.

• Revenue grew for 57% of respondents in 2016 (only 51% expected revenue growth) and demand grew for 55% (only 35% expected demand growth). No organizations reported a decrease in demand.

• However, expenses increased for 62% of respondents, and employment grew for 42% of respondents.

•Asaresult,profitsdecreasedfor42%ofrespondents,andonly32%ofrespondentsgrewprofits.Still,thisresultexceedsthe22%whoexpectedprofitgrowthfor2016.

KEYFINDINGS

2017•Politicalchangesaretranslatingtosignificanteconomic

uncertainty — and uncertainty about how this will impact nonprofits.Morethanhalf(54%)ofrespondentsselected“unknown”todescribetheanticipatedeffectontheirorganizations.

•Nonprofitsaremorepositivethisyearthanthepreviousyearaboutgrowthinrevenue(58%versus51%),profit(41%versus22%), and demand (58% versus 35%), but surprisingly fewer (46% versus 52%) expect increases in costs.

• Almost one-third plan to grow employment. Related to that expectation, retaining talent has become the top goal of 2017, and the scarcity of talent is the second biggest challenge.

• Technology priorities have grown with the greatest increases in tracking impacts/outcomes, improving performance of existing systems, and donor/member relations and analysis.

• Board focus also improved in many areas since the previous year with mission, strategic planning, fundraising, and board member expectations all becoming higher priorities.

4

2016 NONPROFIT PERFORMANCE

REVENUE/SUPPORT EXCEEDING EXPENSES

In 2016, two-thirds of organizations indicated that revenue/support had exceeded

expenses. This represents an eight-point decrease from the percent that reported this

resultin2015andthelowestlevelinthepastfiveyears.Theseresultsforetellsubsequent

responses about the increase in expenses many organizations reported during 2016.

5

20120%

25%

50%

75%

100%REVENUE/SUPPORT EXCEEDING EXPENSES

2013 2014 2015 2016

69%76%

71%75%

67%

2/3 of respondents reported revenue/support exceeded expenses

REVENUE CHANGE

A majority (57%) of respondents indicated that revenue grew in 2016. (This includes one-

quarterofrespondentswhoachievedgrowthgreaterthan10%—mirroringafive-year

high from 2014 — and one-third of respondents who achieved 3% to 9%.) Just over one-

fifthofrespondentsreportednochangeinrevenue,andjustoverone-fifthofrespondents

reported a decrease.

6

0%

100%REVENUE CHANGE

p10%

p3%-10%

Neutral

q3%-10%

q10%

2013 2014 2015 20162012

Revenue pNeutral

Revenue q

201246%18%35%

201366%19%15%

201457%22%21%

201554%20%26%

201657%21%22%

15%

20%

18%

33%

13%24% 25% 20% 25%

32%

21%

13%

9%

34%

20%

15%

11%

32%

22%

10%

11%

42%

19%

8%7%

10%

20%

30%

40%

50%REVENUE SOURCES

Program Revenue(Membership, Tuition,Admissions, Sales of

Products and Services)

0Contributions Special Events Corporate/

FoundationGrants

GovernmentGrants

39%

30%

4%

13% 14%

0%

100%DEMAND CHANGE

p

Neutral

q

2013 2014 2015 20162012

43%

51%

7%

46%

49%

6%

57%

37%

7%

44%

52%

3%

55%

45%

7

REVENUE SOURCES (OTHER THAN INVESTMENT INCOME)

When asked about the source of revenue in 2016, average percentages increased for

program revenue (p3%), corporate/foundation grants (p4%), and government grants

(p1%). Revenue from special events decreased (q6%), and contributions stayed the same.

Note:Duetosignificantfluctuationsanddifferingyear-ends,investmentincomeresults

have been excluded from calculations.

DEMAND CHANGE

2016 represented another year in which more than half of respondents (55%) reported

increases in demand for programs and services. No respondents to this year’s survey

indicated that demand for services decreased. 55% represents a 20-point increase over

the percentage of respondents who expected demand to grow in 2016.

8

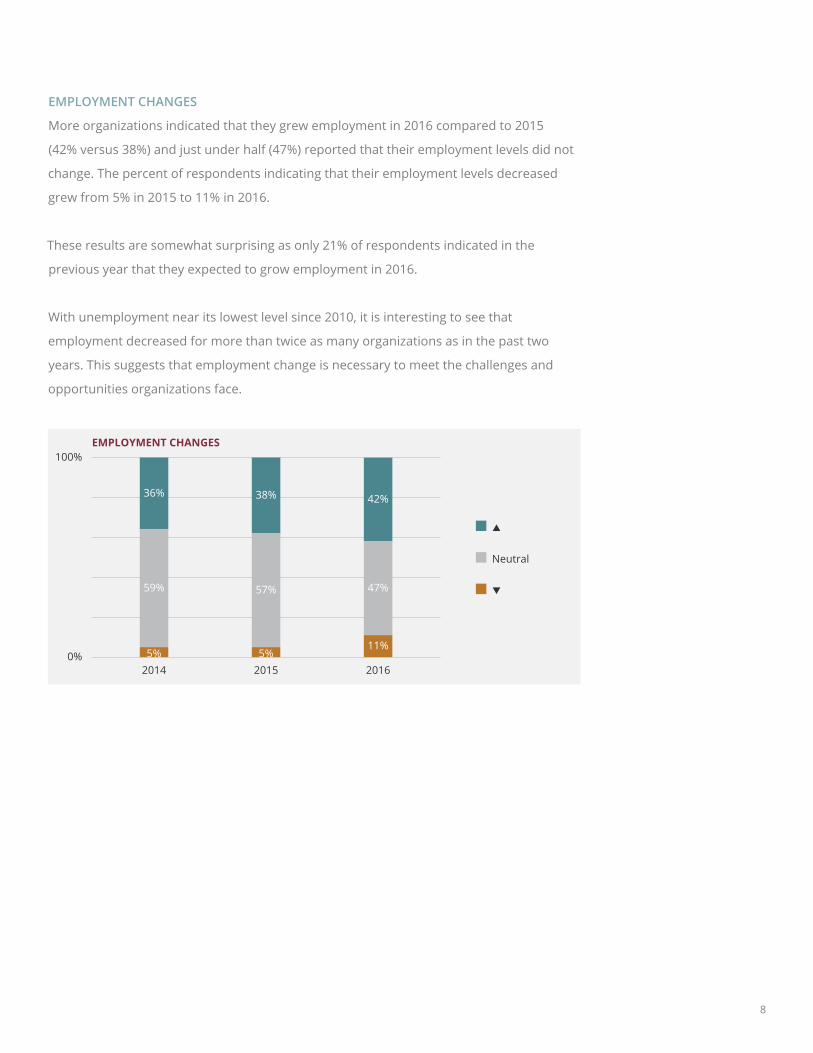

0%

100%EMPLOYMENT CHANGES

p

Neutral

q

2015 20162014

Employment pNeutral

Employment q

201436%59%5%

201538%57%5%

201642%47%11%

36%

59%

5%

38%

57%

5%

42%

47%

11%

EMPLOYMENT CHANGES

More organizations indicated that they grew employment in 2016 compared to 2015

(42% versus 38%) and just under half (47%) reported that their employment levels did not

change. The percent of respondents indicating that their employment levels decreased

grew from 5% in 2015 to 11% in 2016.

These results are somewhat surprising as only 21% of respondents indicated in the

previous year that they expected to grow employment in 2016.

With unemployment near its lowest level since 2010, it is interesting to see that

employment decreased for more than twice as many organizations as in the past two

years. This suggests that employment change is necessary to meet the challenges and

opportunities organizations face.

EXPENSES CHANGE

With growing demand for most participants, it is not surprising that expenses grew for a

majority as well. Representing a six-point increase over 2015, 62% of respondents reported

increasingexpensesin2016.(Thisincludesnearlyone-fifthwhoindicatedcostsincreased

morethan10%.)Withaverageannualinflationfromthepast10yearsbeingaround

2%,someincreaseinexpensescanbeexpected.However,one-quarterofrespondents

indicated no change to expenses, and 13% actually reported a decrease in expenses.

9

0%

100%EXPENSES CHANGE

p10%

p3%-10%

Neutral

q3%-10%

q10%

2013 2014 2015 20162012

Expenses pNeutral

Expenses q

201249%28%23%

201350%27%24%

201450%25%25%

201556%25%20%

201662%25%13%

12% 18% 11% 13% 17%

37% 32% 39%43%

45%

28% 27% 25%25%

25%

20% 17% 17%15%

11%3% 7% 8% 5% 2%

10

PROFIT CHANGES

Essentially,combiningtherevenueresultsandexpenseresultsgivesusprofit,and,likethe

smaller percentage who reported revenue/support exceeded expenses in 2016, a smaller

percentage(32%versus34%in2015and45%in2014)alsoreportedprofitgrowth.

As described previously, there is less and less room to stay the same.

0%

100%PROFIT CHANGES

2015 20162014

Profit pNeutralProfit q

201445%26%29%

201534%30%37%

201632%25%42%

p10%

p3%-10%

Neutral

q3%-10%

q10%

29%

16%

26%

13%

16%

23%

11%

30%

7%

30%

17%

15%

25%

17%

25%

“While many

organizations aim

for breakeven

between income

and expenses,

profits are a

healthy nonprofit

goal. Profits are

important because

they enable an

organization to

reinvest back into

what works and

grow in new and

different ways.”

-Lisa Meacham, CPA,

Audit Partner

Profits grew for 1/3 of respondents

11

2017 NONPROFIT OUTLOOK

POLITICAL IMPACT

A nearly identical percentage of respondents (69% versus 68%) expect the political

environment will have a negative impact on their organizations in 2017. In a reversal of

expectations for 2016, however, more respondents (19% versus 10%) believe the political

environment will have a positive impact on their organizations, and fewer respondents (13%

versus 22%) feel the impact will be unknown.

The somewhat surprisingly low “unknown” category might suggest that people have made

conclusions about the reality they will operate in, politically, for the foreseeable future (and it

is not good for the majority of respondents). It is important to note that potentially dramatic

politicalshiftscanpresentachallenge—oranopportunity—todifferentorganizations,

their programs, and their funding and fundraising prospects.

Respondents were asked how the political environment would impact their organizations

(see sidebar).

0%

25%

50%

75%POLITICAL IMPACT

PositiveUnknownNegative

20172016

10%

19%22%

13%

68% 69%

“Potentially more service demand. We may see a bump from the election since people want to do something:”

“It is unclear currently whether changes will occur in the philanthropic community due to the election. We are also monitoring other policy agendas, which could impact our organization and goals:”

“With the new administration, our government funding could be decreased or eliminated.”

FROM THE RESPONDENTS…

12

ECONOMIC IMPACT

The economic outlook, however, is much more uncertain yet positive. More than half of

survey participants (54%) selected unknown when asked how the economic environment

would impact their organizations in 2017. More than one-third (39%) indicated it would have

a positive impact, and, somewhat remarkably, only 7% of respondents felt the economic

impact would be negative for their organizations.

Respondents were asked how the economic environment would impact their

organizations (see sidebar).

0%

25%

50%

75%ECONOMIC IMPACT

PositiveUnknownNegative

20172016

42%39%37%

54%

22%

7%

FROM THE RESPONDENTS…

“I think that the expected pro-business policies of the new administration will increase the optimism of our benefactors.”

“We are unsure of what will happen with federal funding opportunities in 2017 and beyond, and this could have a negative impact on our organization. Changes to tax codes could impact us either positively or negatively.”

“Local economy is strong impacting program revenue. Current market outlook is expected to support investment returns.”

13

REVENUE/SUPPORT EXCEEDING EXPENSES

Expectationsaboutrevenue/supportexceedingexpensesin2017reflectasignificant

(13-point) jump from expectations for 2016. Impressively, 85% expect revenue/support to

exceed expenses while 15% do not.

With expectation percentages returning to levels similar to those in past years, one must

wonder whether 2016’s outlook was an anomaly.

Itmaybesurprisingtoconsiderthisyear’soptimisticoutlookwhencomparingthedifference

between expectations and reality for 2016; although 72% predicted a positive balance, only

67% achieved that. Adding the political and economic uncertainty expressed, this makes the

18-point increase from 2016 actual to 2017 expectations even more interesting.

20130%

25%

75%

50%

100%REVENUE/SUPPORT EXCEEDING EXPENSES

2014 2015 2016 2017

NoYes

80% 83% 86%

72%

20% 17% 14%

28%

85%

15%

“While some might

anticipate after

organizations

do not meet

expectations in one

year, they would

lower expectations

for the next. But

perhaps a more

positive outlook

reflects lessons

learned and

changes made.”

-Ann Hinkins CPA,

Audit Partner

14

REVENUE AND PROFIT GROWTH OUTLOOK

Mirroring the optimism of the previous response, more participants (58% versus 51%)

expect revenue to grow in 2017. Similarly, many more respondents (41% versus 22%)

expectprofitstoincrease.(Recallthat57%achievedrevenuegrowth,butonly32%

achievedprofitgrowthin2016.)

Respondents were also asked to describe how revenue and support would increase or

why it might decrease (see sidebar).

20150%

25%

50%

75%REVENUE AND PROFIT GROWTH OUTLOOK

Revenue Growth

Profit Growth

2016 2017

58%

41%

22%19%

51%

60%

FROM THE RESPONDENTS…

“2017 is [our organization’s] anniversary, and special events are being planned with projections of additional donors:”

“Expand into new areas, utilize healthcare worker outreach, and price more competitively.”

“Cyclical nature of [our programs]:”

“Engage board in fundraising efforts.”

“…continue to ramp up advertising and community engagement to increase referrals to our program.”

Respondents who expect profit to grow in 2017 nearly doubled from 22% to 41%

15

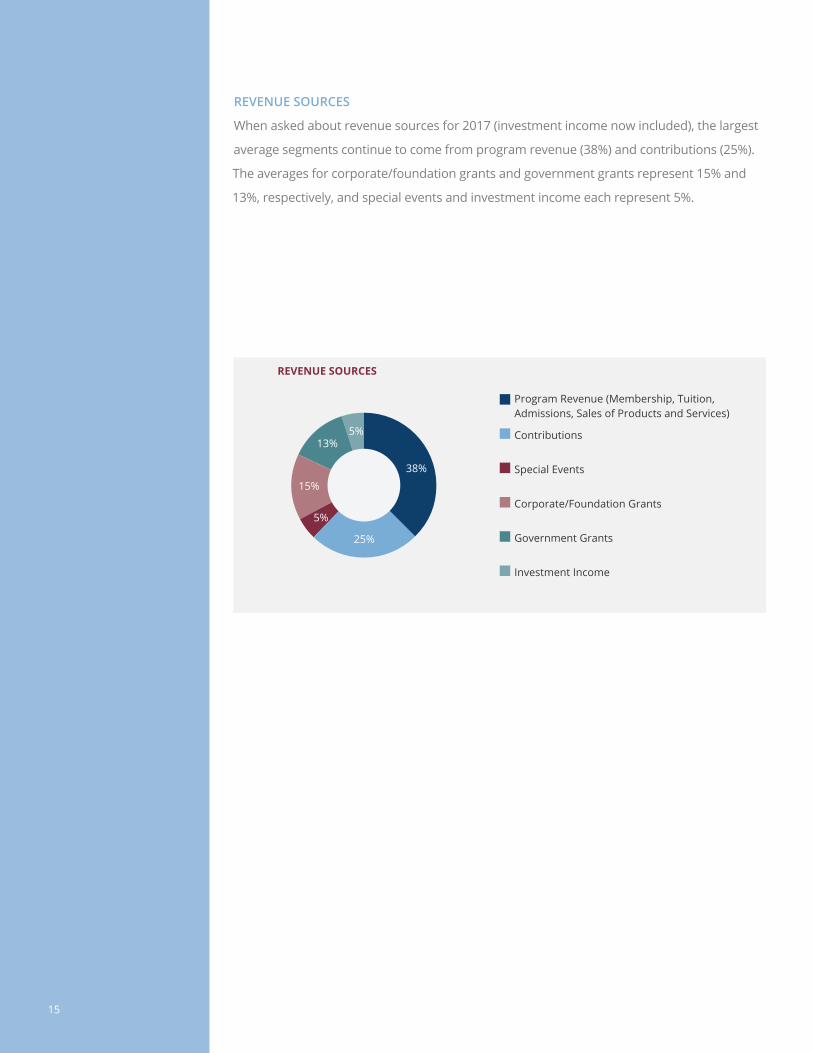

REVENUE SOURCES

When asked about revenue sources for 2017 (investment income now included), the largest

average segments continue to come from program revenue (38%) and contributions (25%).

The averages for corporate/foundation grants and government grants represent 15% and

13%, respectively, and special events and investment income each represent 5%.

REVENUE SOURCES

Special Events

Contributions

Program Revenue (Membership, Tuition,Admissions, Sales of Products and Services)

Government Grants

Corporate/Foundation Grants

Investment Income

5%

5%

15%

13%

38%

25%

16

DEMAND AND EXPENSE GROWTH OUTLOOK

One of the most surprising results in this year’s survey was the deviation of organizations’

expectations for demand and expenses.

More organizations (58%) expect demand to increase (a 23-point increase compared to 2016

expectations), but fewer organizations (46%) expect expenses to increase (down six points

compared to 2016 expectations).

Possibleexplanationsmightbe1)anticipatedefficienciestoberealizedthisyear,2)excess

capacity created in 2016 that will be utilized in 2017, or 3) leaving demand unmet.

20130%

25%

50%

75%DEMAND AND EXPENSE GROWTH OUTLOOK

2014 2015 2016 2017

ExpensesDemand

37%

23%

52%

35%

46%40%

50%

57%52%

58%

17

2017 GOALS

Highlighting the growing concern of competition for talent, retain qualified staff was the

new top goal selected by survey respondents. (It is interesting to note that just three years

agothisgoalwasnoteveninthetopfive.)Thissignificantchangemightbeafacetofthe

expected improved economic environment and its implications on demand for talent or a

concernaboutstrategicandeffectiveorganizationalsuccessionplanningforkeyindividuals.

On the other hand, some things never change: obtain new funding sources/obtain more

funding from current sources and meet annual budget remain critically important goals,

coming in second and third.

Respondents were asked what concrete steps would be taken to achieve top goals

(see sidebar).

2017GOALS 2016 2015 2014 2013

Obtain New Funding Sources/Obtain MoreFunding from Current Sources

Meet Annual BudgetImprove Effectiveness of Fundraising Efforts and Activities

Recruit Qualified StaffStart New/Expand Current Programs

Conduct Long-Term Strategic and Financial PlanningImprove Program Reporting Efficiency and Accuracy

Collaboration with Other Organizations/Entities

2 1 1 1 1

3 2 3 2 34 4 5 4 45 5 7 10 106 6 6 5 67 8 - - -8 7 8 9 79 10 9 8 9

Retain Qualified Staff 1 3 4 6 5

Increase Effectiveness of Board Involvement and Governance 10 9 10 7 8

FROM THE RESPONDENTS…

“Several targeted hires in early 2017; three-year forecast in Q1 2017; fundraising plan in place and progress tracked monthly.”

“We set quarterly goals and have quarterly strategic planning meetings.”

“Strategic planning cycle, exploration of new revenue opportunities, continued build out and deployment of new programs.”

“Continue to improve online recruiting capabilities, re-engage current staff…”

18

2017 CHALLENGES

Unlike the change at the top of this year’s goals, challenge in predicting future funding

continues to be the top challenge since we began surveying in 2008. Two new options,

scarcity of talented job candidates and cybersecurity, started the list impressively at

No. 2 (perhaps echoing the sentiments of the top goal and the importance of succession

planning) and No. 5, respectively. Inadequate access to funding was the only other

challenge that appears to have grown in importance. Interestingly, the challenge of

inefficient, insufficient, or outdated technologydroppedfiveplacessince2016.

Respondents were asked what concrete steps would be taken to manage top challenges

(see sidebar).

2017CHALLENGES 2016 2015 2014 2013

Scarcity of Talented Job CandidatesPotential Loss of Top Management/Talent

Inadequate Access to FundingCybersecurity

Obstacles to New Program ImplementationBoard Effectiveness/Engagement

Inefficient, Insufficient, or Outdated TechnologyIncreased Compliance and Regulation

1 1 1 1 1

5

Challenge in Predicting Future Funding

Challenge in Predicting Cash Flow Needs

2 - - - -3 2 5 4 64 5 3 5 3

- - - -6 4 4 2 47 6 - - -8 3 2 3 59 8 7 8 7

10 7 6 6 2

FROM THE RESPONDENTS…

“Focus on fundraising effort and team; offer training to compliance staff; use staff time to incorporate ‘team problem solving.’”

“New fundraising technology platform; succession planning.”

“Building infrastructure, including technology to help us stay abreast of increasing compliance and regulation requirements.”

19

0%

25%

50%EMPLOYMENT GROWTH OUTLOOK

2014 2015 2016 2017

28%

37%

21%

31%

2017 STRATEGIES FOR SUCCESS

TALENT AND COMPENSATION

EMPLOYMENT GROWTH OUTLOOK

Almost one-third of respondents indicated they plan to grow employment in 2017. This

is similar to percentages from 2014 and 2015 and 10 points higher than the hiring

expectationfor2016.However,itremainssignificantlylower(11points)thanthe42%who

reported actual employment increases in the previous year.

31% of respondents expect to increase hiring

20

25%

50%

75%

100%FUNCTIONAL AREAS FOR INCREASED EMPLOYMENT

Direct Service/Program Management/Member or Constituent Services

0%Fundraising/Development

Administrative

21%26%

79%

FUNCTIONAL AREAS FOR INCREASED EMPLOYMENT

With nearly 80% of respondents indicating that new hires will be made in direct service/

program management/member or constituent services, hiring will clearly be driven by

recipient demand for services. Fundraising/development will be an area of increased

hiringforapproximatelyone-quarterofrespondents,andadministrative will be a focus

ofincreasedemploymentforapproximatelyone-fifthofrespondents.(Thisrepresentsa

reversal in priority from 2016 when 36% expected to increase hiring for administrative

and 22% expected to increase hiring for fundraising/development personnel.)

21

75%50%25%0%

CHALLENGES TO ATTRACTING AND RETAINING TALENT

Advancement Opportunities

Workloads/Staff Resources

Competitive Pay

Cost of Living/Housing

Organizational Culture

Other

67%

67%

40%

31%

4%

8%

CHALLENGES TO ATTRACTING AND RETAINING TALENT

Whenaskedaboutchallengesnonprofitsfacewhenattractingandretainingtalent,the

two top issues from 2016, competitive pay and advancement opportunities, were again

identifiedbythemostrespondents.

However, comparing 2016’s percentages to this year’s, competitive pay seems to be

decreasing as a challenge (67% versus 72% in 2016), and advancement opportunities

seems to be a growing challenge (67% versus 59% in 2016).

22

75%50%25%0%

STRATEGIES FOR ATTRACTING AND RETAINING TALENT

Posting Online or Use ofReferral Sources

Enhanced Training andDevelopment Programs

Flexible/Remote WorkArrangements

Increased Compensation

Increased Benefits

Use of Recruiting Firms

Other

65%

63%

60%

48%

31%

21%

10%

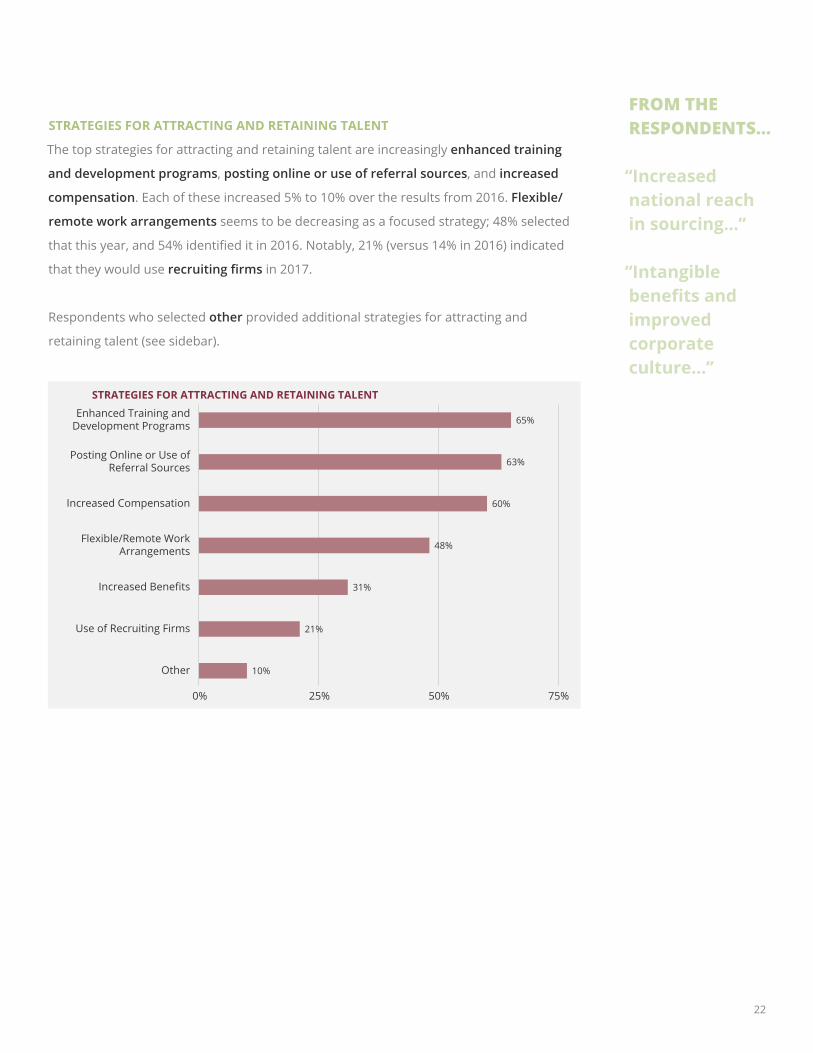

STRATEGIES FOR ATTRACTING AND RETAINING TALENT

The top strategies for attracting and retaining talent are increasingly enhanced training

and development programs, posting online or use of referral sources, and increased

compensation. Each of these increased 5% to 10% over the results from 2016. Flexible/

remote work arrangements seems to be decreasing as a focused strategy; 48% selected

thatthisyear,and54%identifieditin2016.Notably,21%(versus14%in2016)indicated

that they would use recruiting firms in 2017.

Respondents who selected other provided additional strategies for attracting and

retaining talent (see sidebar).

FROM THE RESPONDENTS…FROM THE RESPONDENTS…

“Increased national reachin sourcing…”

“Intangible benefits and improved corporate culture…”

q+6%0%

20%

40%

60%

80%

100%COMPENSATION 2016 2017

q4%-6% q2%-4% No Change p2%-4% p4%-6% p+6%

0% 0% 2% 0% 2% 0%

23%

6%

61%

83%

7% 7% 5% 4%

q+6%0%

10%

20%

30%

40%

50%HEALTHCARE BENEFITS 2016 2017

q4%-6% q2%-4% No Change p2%-4% p4%-6% p+6%

2%4%

0% 0%

4%6%

30% 29%

24% 24%

13%

22%

28%

14%

COMPENSATION

When asked about compensation, the trend is clear (if slight). No respondents indicated

they expect to decrease wages in 2017, and only 6% expect to keep them level (compared

to 23% in 2016). Interestingly, 94% expect to increase wages, 11% expect to increase them

4% or more, and a more stable 83% expect to increase wages 2% to 4%.

HEALTHCARE BENEFITS

Expectationsforchangestohealthcarebenefitsseemtobesimilartothosefromlastyear.

However there may be some moderation: 22% expect increases of 4% to 6% (compared to

13% in 2016) and only 14% expect increases of more than 6% (compared to 28% in 2016).

This moderation may be a result of budget conformity or adjusted participant co-pays,

deductibles, etc.

23

24

BONUS/INCENTIVE COMPENSATION

Mostrespondents,57%,indicatedthattheywillbeofferingsomeformofbonus

compensation in 2017. This represents the highest response compared with previous years’

resultsrangingfrom38%to52%.Somefollow-upquestionsinclude:

• Is it based on individual or organizational

performance?

• Is it seasonal or tied to objectives met?

• Is it available to all employees, only some

departments, or only executive level?

Respondents were also asked to describe

their bonus or incentive compensation

programs (see sidebar).

ORGANIZATION CONTRIBUTION

TO RETIREMENT (% OF EMPLOYEES’

SALARIES)

Forthefirstyear,weaskedwhatpercentageoforganizationscontributetotheir

employees’ retirement. Almost half of respondents indicated that they contribute 4% to

6% of wages. One-third of respondents contribute 1% to 3%. And 15% of respondents

contribute more than 6%. Finally, 7% of respondents contribute nothing to their

employees’ retirement. (Organization executives should consider whether this puts them

atacompetitivedisadvantagetoattractandretainqualifiedstaff,andtheymightneedto

strategize how to overcome that challenge.)

BONUS/INCENTIVE COMPENSATION

Yes No

57%

43%

ORGANIZATION CONTRIBUTION TO RETIREMENT (% OF EMPLOYEES’ SALARIES)

1%-3%

0%

More than 6%

4%-6%

7%

33%

45%

15%

FROM THE RESPONDENTS…

“Bonuses are never guaranteed, but every year we have paid bonuses based on work goals and projects.”

“Awards were given to all staff at the end of calendar year 2016 (i.e., FY17). Additional work was performed by employees as there were up to 5 positions vacant during the first half of the fiscal year.”

“Performance bonuses, based on goals achieved (not related to fundraising goals).”

“Incentive for all employees if certain organizational goals are attained.”

100%80%60%0% 20% 40%

TECHNOLOGY PRIORITIES

Tracking Impact/Outcomes

Improving Performance of Existing Systems

Social Media and Online Presence

Data Quality/Integration and BusinessIntelligence/Analytics

Donor/Member Relations and Analysis

Donation/Income Collection

Outsourcing Technology Support/Strategy

PriorityConsiderationNot a Focus

Remote Access for Employees

Cybersecurity

Program/Service Delivery to Recipients

Banking, Cash Management,and Expense Payment

59%

46%

33%

20%

15%

11%

9%

6%

7%

4%

6%

24%

31%

43%

46%

35%

37%

35%

39%

26%

30%

17%

17%

22%

24%

33%

50%

52%

56%

56%

67%

67%

78%

TECHNOLOGY AND GIVING

TECHNOLOGY PRIORITIES

The biggest change in technology priorities for 2017, as compared to those for 2016, was

tracking impact/outcomes, which increased 25 points to become a priority for almost

80% of respondents. Improving performance of existing systems also increased, by

14 points, to be a priority of two-thirds of respondents. Finally, donor/member relations

and analysis also increased as a technology priority, by 10 points, to 56% of respondents.

Technology priorities that decreased in importance include banking, cash management,

and expense payment, down nine points, and remote access for employees, down seven

points. It may be that these more foundational organizational technologies have already

been addressed by the majority of organizations.

25

26

CAMPAIGN STATUS

Currently Conducting a Capital Campaign(Silent Phase)

Currently Conducting a Capital Campaign(Public Phase)

No Capital Campaign Plans for the Near Future (2-3 years)

Planning a Capital Campaign for the Next Year

16%

14%

11%59%

CAMPAIGN STATUS

Fewer respondents indicated they will be in a capital campaign (public phase), 16%

versus 22% in 2016, and in planning stages, 11% versus 27%. More will be in a capital

campaign (silent phase), 14% versus 8% in 2016, and many more expressed no capital

campaign plans for the near future, 59% versus 43%.

Fewer organizations appear to be in campaign-mode

BOARD PERFORMANCE

PRIORITIES

When it comes to board priorities, many areas seem to be improving and becoming

a greater focus. Comparing the two highest focus categories from 2016 to 2017,

organizational mission is up from 77% to 87%, strategic plans up from 60% to 75%,

fundraising expectations are up from 48% to 60%, and board member expectations

are up from 43% to 65%. One area, however, that has not become a higher priority is

organizational evaluation methods, down from 39% to 35%. Leadership evaluation

methods remained the same at 41%.

Respondents were also asked to share what new strategies were working in relation to

their boards (see sidebar).

PRIORITIES

Organization Mission

Strategic Plan

Fundraising Expectations

Board Member Expectations

Leadership Evaluation Methods

Organization Evaluation Methods

4%

2%

9%

9%

2%

26%

52%

43%

30%

22%

12%

2%

4%

8%

2%

15%

11%

35%

32%

30%

43%

29%

24%

7%

20%

23%

24%

42%

39%

High FocusLow Focus

FROM THE RESPONDENTS…

“Incorporated an individualized ‘board orientation’ for new board members.”

“New financial statements that are easier to read, encouragement to join and participate in a board committee.”

“We formalized a board policy manual.”

27

28

40%35%30%25%0% 5% 10% 15% 20%

ANNUAL REVENUE

$26 Million-$50 Million

$11 Million-$25 Million

$6 Million-$10 Million

More than $100 Million

$51 Million-$100 Million

$1 Million-$5 Million

Less than $1 Million

4%

1%

13%

25%

15%

32%

4%

35%30%25%0% 5% 10% 15% 20%

TOTAL EMPLOYEES

100-249

50-99

250-500

More than 500

25-49

Less than 25

6%

10%

29%

9%

19%

27%

ABOUT THE SURVEY AND PARTICIPANTS

TheEKS&HNonprofitOutlookSurveyhasgrowntobecomeaninformativebarometer

of executives of organizations in Colorado and the western U.S., representing a wide

varietyoftypesandsizesofnonprofits.The2017surveyinvolvedalmost90executive

participants. This report includes results we consider to be meaningful, insightful,

strategic,andactionableinformationfornonprofits.Formoreinformationaboutthe

survey, please contact partners Ann Hinkins at [email protected] or Lisa Meacham

at [email protected], or call us at 303-740-9400.

29

35%15%10%5% 20% 25% 30%

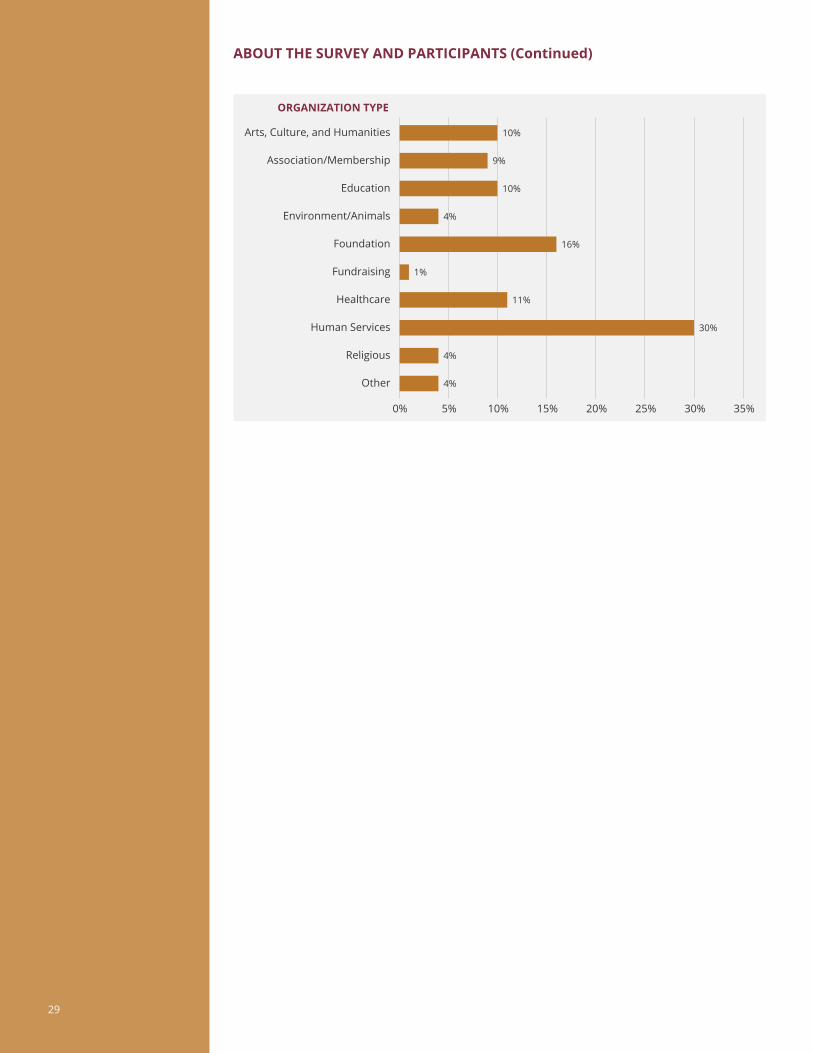

ORGANIZATION TYPE

Education

Foundation

Healthcare

Association/Membership

Arts, Culture, and Humanities

Religious

Environment/Animals

Fundraising

Human Services

Other

0%

10%

9%

10%

4%

16%

1%

11%

4%

4%

30%

ABOUT THE SURVEY AND PARTICIPANTS (Continued)

30

EKS&H SERVICES

EKS&H LLLP (EKS&H) is a nationally recognized professional

servicesfirmprovidingaudit,tax,technology,and

business consulting services to public and private clients

locally, nationally, and internationally. Our commitment

to excellence has resulted in sustained growth since we

began in 1978. Working collaboratively, we know the best

measure of our success is the success of our clients.

Audit and Assurance

•Publicofferingsandprivateplacements

• SEC reporting

•Employeebenefitplans

• Risk advisory

Tax

• Multistate and state and local taxes (SALT)

• Federal credits and opportunities

• International tax and transfer pricing services

• Transaction tax strategy

Business Consulting

• Outsourced accounting

• Transaction services

• Strategic planning

• Specialty tax

Founded: 1978

Locations: Denver, Boulder, Fort Collins, and San Francisco

Employees: Approximately 700

Partners: More than 70

Number of CPAs: 300

Number of Consultants: 100

Business Technology

• Budgeting and forecasting

• Business intelligence

•Dataqualityandintegration

• Enterprise software advisory

• Managed IT and cloud

• Project management

• Security and risk assurance

• Strategy and leadership

• Training

Wealth Advisory

• Family business

•Familyofficeservices

• Financial planning

• Income tax planning and compliance

• Philanthropy guidance

• Wealth transfer planning

303-740-9400 www.EKSH.com