Embed Size (px)

Citation preview

4th August 2017

2017 Half-Yearly ResultsPresentation

2017 Half-Yearly Results 2

1. 2017 Half-Yearly Highlights

2. Investment Properties

3. Development Properties

4. Financial Highlights

5. Outlook

6. Q&A

Speakers: Robert Wong, Chief Executive & Simon Dixon, Chief Financial Officer

Agenda

2017 Half-Yearly Results 3

Key figures

Profit1: US$3,125m (1H 2016: US$1,263m)

Net debt: US$1.9bn (Dec 2016: US$2.0bn)

NAV per share: US$14.54 (Dec 2016: US$13.30)

Interim dividend per share: US¢6 (1H 2016: US¢6)

Highlights

Underlying 1H profit1 up 32% YoY and 14% HoH

Positive performance from investment properties

Higher sales completions of development properties in

mainland China and Singapore

New property developments in Singapore, Nanjing and

Wuhan

2017 Half-Yearly Highlights

US$517mUnderlying profit

US$34bnShareholders’ funds

393455

517

1H 2016 2H 2016 1H 2017

3031

34

Jun 2016 Dec 2016 Jun 2017

+32% YoY +9% HoH

1 Attributable to Shareholders of the Company

42017 Half-Yearly Results

Investment Properties

2017 Half-Yearly Results 5

Investment Properties Overview

Investment properties are primarily located in Hong Kong and Singapore

8,618*

Total

TOTAL COMPLETED AREA (HKL’s share)

6,810

1,202

606

Office

Retail

Hotel

(000’s sq. ft NFA)

446TOTAL

OTHERS

1,781Total

88TOTAL

HONG KONG

4,139

590

143

MACAU98

151

HANOI75

8

BANGKOK27

61

SINGAPORE1,652

129

70

161

215

249TOTAL

4,872TOTAL

83TOTAL

JAKARTA663

66

729TOTAL

PHNOM PENH184

89

97

370TOTAL

*Equivalent to 800,000 sq. m.

2017 Half-Yearly Results 6

Accounting

1H 2016 2H 2016 1H 2017

Average net rent(HK$ psf/month)

103 103 106

Period-end vacancy 3.1% 2.2% 1.5%

Weighted average lease expiry (years)

4.0 3.8 4.0

2H 2017 2018 2019

Total lettable office area subject to expiration/rent revisions(’000 sq. ft)

328 1,255 1,037

% of area subject to expiration/rent revisions

8% 30% 25%

- Expiration 5% 17% 19%

- Rent revisions 3% 13% 6%

Average expiring net rent(HK$ psf/month)

94.3 103.0 116.3

AVERAGE RENTS & VACANCY

EXPIRATION AND INTERIM RENT REVISIONS

Positive rental reversions and lower vacancy as market supply remained tight

Hong Kong Portfolio – Office

40%

30%

7%

6%

2%

1%

14%

OFFICE TENANT PROFILE

Trading

Banks and Other Financial Services

Legal

Government Others

Property

2017 Half-Yearly Results 7

1H 2016 2H 2016 1H 2017

Average net rent(HK$ psf/month)

216 220 224

Period-end vacancy 0% 0% 0.6%

Weighted average lease expiry (years)

2.6 2.8 2.7

AVERAGE RENTS & VACANCY

Higher rents due to positive 2016 reversions

Hong Kong Portfolio – Retail

49%

31%

15%

5%

RETAIL TENANT PROFILE

Fashion & Accessories

Jewellery & Watches Others

Food & Beverages

2017 Half-Yearly Results 8

2H 2017 2018 2019

HKL’s Share: Total lettable office area subject to expiration/rent revisions (’000 sq. ft)

23 713 318

% of area subject to expiration/rent revisions

1% 43% 19%

- Expiration 1% 5% 12%

- Rent revisions - 38% 7%

Average expiring gross rent(S$ psf/month)

10.1 9.0 9.8

Low vacancy rate

Singapore Portfolio – Office

1H 2016 2H 2016 1H 2017

Average gross rent(S$ psf/month)

9.4 9.2 9.1

Period-end vacancy 1.0% 0.1% 0.2%

Weighted average lease expiry (years)

5.3 4.9 4.5

73%

7%

5%

5%

3%2%

5%

OFFICE TENANT PROFILE EXPIRATION AND INTERIM RENT REVISIONS

AVERAGE RENTS & VACANCY

Banks and Other Financial Services

Legal

Natural Resources

Accounting

IT Services & Consultancy

Property

Others

2017 Half-Yearly Results 9

Rest of Asia Portfolio

Beijing – WF CENTRAL (84%-owned)

Prestigious retail centre, which includes an exclusive luxury hotel (Mandarin Oriental)

43,000 sq. m. NFA

Open: Q4 2017 (hotel in 2018)

Pre-leasing commitments from a diverse range of tenants

Jakarta – Jakarta Land (50%-owned)

Existing portfolio features 135,000 sq. m. NFA

Average gross rent: US$26 psm per month (1H 2016: US$25 psm per month)

Occupancy: 92%

WTC 3: On schedule to complete in 2018

Phnom Penh – EXCHANGE SQUARE (100%-owned)

Completed in early 2017

Space in the 26,000 sq. m. mixed-use complex is being taken up by tenants

MAINLAND CHINA SOUTHEAST ASIA

Modest exposure outside Hong Kong and Singapore

2017 Half-Yearly Results 10

JV with IOI Properties (33%-owned)

Located within the Marina Bay Financial District of Singapore

Site area: 1.1 ha

Two office towers

1.26 million sq. ft (117,000 sq. m.) NFA office

30,000 sq. ft (2,800 sq. m.) NFA retail podium

Connected to HKL’s existing portfolio in the district

New Project in Singapore

SINGAPORE

Expanding our portfolio of prime investment properties in Singapore’s Marina Bay Financial District

© Urban Redevelopment Authority. All rights reserved.

112017 Half-Yearly Results

Development Properties

2017 Half-Yearly Results 12

Development Properties Overview

The development properties portfolio spans six countries and 11 cities, with a key focus on mainland China and Singapore

824 TOTAL

THE PHILIPPINES163

661

667TOTAL

INDONESIA31

636

285TOTAL

SINGAPORE-

285

6,752Total

TOTAL DEVELOPABLE AREA (HKL’s share)

2,061

4,691

Constructed

Under construction/ to be developed

(000’s sq. m. GFA)4,941TOTAL

MAINLAND CHINA

1,867

3,074

19TOTAL

THAILAND-

19

16TOTAL

VIETNAM-

16

2017 Half-Yearly Results 13

CHENGDU

CHONGQING WUHAN

NANJING

SHANGHAI

Mainland China Portfolio – Overview

Six projects

Total GFA 6.1 million sq. m.

(HKL’s share: 4.1 million sq. m.)

WE City

Total GFA 898,000 sq. m.

(HKL’s share: 449,000 sq. m.)

BEIJING

Maple Place (90%-owned)

Central Park (40%-owned)

Parkville

Total GFA 227,000 sq. m.

(HKL’s share: 113,000 sq. m.)

Conditionally acquired

New 50% JV

Total GFA 494,000 sq. m.

(HKL’s share: 247,000 sq. m.)

New 33% JV

Total GFA 217,000 sq. m.

(HKL’s share: 72,000 sq. m.)

IMAGE TO BE CONFIRMED

IMAGE TO BE CONFIRMED

2017 Half-Yearly Results 14

REVENUE RECOGNISED* CONTRACTED SALES* SOLD BUT UNRECOGNISED SALES*

Mainland China Portfolio

Increase in overall contracted sales and improved profit contribution as a result of positive market sentiment and further completions

-

100

200

300

400

500

600

1H 2016 2H 2016 1H 2017

-

100

200

300

400

500

600

700

800

1H 2016 2H 2016 1H 2017

US$m US$m

-

200

400

600

800

1,000

1,200

1,400

1,600

30 Jun 16 31 Dec 16 30 Jun 17

US$m

$350m$326m

$520m

$432m

$673m$701m

$885m

$1,083m

$1,421m

Chongqing Chengdu

Shanghai Beijing

Sales to be recognised next 6 months

Sales to be recognised after next 6 months

Chongqing Chengdu

Shanghai Beijing

* The above analysis includes share of Joint Ventures & Associates

2017 Half-Yearly Results 15

SOL ACRES

Singapore Portfolio – Overview

LAKEVILLE

699 units

674,000 sq. ft. GFA (63,000 sq. m.)

Completed in 2017

100% sold

LAKE GRANDE

710 units

537,000 sq. ft. GFA(50,000 sq. m.)

Completion: 2019

Pre-sold: 87%

MARGARET DRIVE

315 units

238,000 sq. ft. GFA(22,000 sq. m.)

Completion: 2020

IMAGE TO BE UPDATED

EUNOSVILLE

Conditionally acquired

1,399 units (estimated)

1.05 million sq. ft. GFA (98,000 sq. m.)

Completion: 2021

1,327 units

1.24 million sq. ft. GFA (115,000 sq. m.)

Completion: 2018

Pre-sold: 73%

IMAGE TO BE UPDATED

2017 Half-Yearly Results 16

REVENUE RECOGNISED CONTRACTED SALES SOLD BUT UNRECOGNISED SALES

Singapore Portfolio

An increase in revenue and profit contribution arising from the 1H completion of LakeVille

0

100

200

300

400

500

600

700

1H 2016 2H 2016 1H 2017

0

100

200

300

400

500

600

1H 2016 2H 2016 1H 2017

0

200

400

600

800

1,000

1,200

1,400

30 Jun 16 31 Dec 16 30 Jun 17

$158m

$529m

$268m

$1,394m

$1,294m

$997m

US$m US$m US$m

$6m

$555m

$615m

Hallmark Residence J Gateway

LakeVille

Hallmark Residence LakeVille

Sol Acres Lake Grande

Sales to be recognised next 6 months

Sales to be recognised after next 6 months

2017 Half-Yearly Results 17

Rest of Asia Portfolio

Nava Park (49%-owned)

Site area: 67 ha; GFA: 802,000 sq. m.

653 units launched for sales (67% pre-sold)

Anandamaya (40%-owned)

Site area: 1.3 ha; GFA: 116,000 sq. m.

509 units, 94% pre-sold

Completion: 2018

Asya (25%-owned)

Previously known as Jakarta Garden City

Site area: 67 ha; GFA: 907,000 sq. m.

East of central Jakarta

Multiple phases

Construction start: 2017

The Nassim (50%-owned)

Site area: 0.6 ha; GFA: 31,000 sq. m.

238 units, 97% pre-sold

Completion: 2018

Two Roxas Triangle (40%-owned)

Site area: 0.5 ha; GFA: 98,000 sq. m.

182 units, 99% pre-sold

Completion: 2018

Mandani Bay (40%-owned)

Site area: 20 ha; GFA: 1.2 million sq. m.

Phase 1: 1,226 units, 78% pre-sold

Completion: 2035

INDONESIA VIETNAM THE PHILIPPINES

Performance within expectations

182017 Half-Yearly Results

New Projects

WUHAN NANJING SINGAPORE

Wuhan Salon Phase 2 (50%-owned)

Conditionally acquired

JV with Zall Group

Mixed-use project

GFA: 494,000 sq. m.

Completion: 2021

Nanjing (33%-owned)

JV with CMSK and Country Garden

Mixed-use project

GFA: 217,000 sq. m.

Completion: 2021

Eunosville, MCL Land

Conditionally acquired

Residential project

GFA: 1.05 million sq. ft. (98,000 sq. m.)

1,399 units

Completion: 2021

Four new projects have been added to the portfolio

BANGKOK

The Esse at Sukhumvit 36 (49%-owned)

JV with Singha Estate

Residential project

GFA: 38,000 sq. m.

338 units

Completion: 2020

192017 Half-Yearly Results

Financial Highlights

2017 Half-Yearly Results 20

FY2016 (US$m) 1H 2017 1H 2016 %YoY

1,994 Revenue 1,297 783 66

(1,023) Net operating costs (787) (327) 141

971 Operating profit 510 456 12

117 Share of results of joint ventures 135 60 125

(69) Net financing charges (36) (33) 9

(168) Tax (91) (89) 2

(3) Non-controlling interests (1) (1) -

848 Underlying profit 517 393 32

2,498 Non-trading items 2,608 870 200

3,346 Profit attributable to shareholders 3,125 1,263 147

1H Revenue and underlying profit up year-on-year

Consolidated Profit and Loss Account

2017 Half-Yearly Results 21

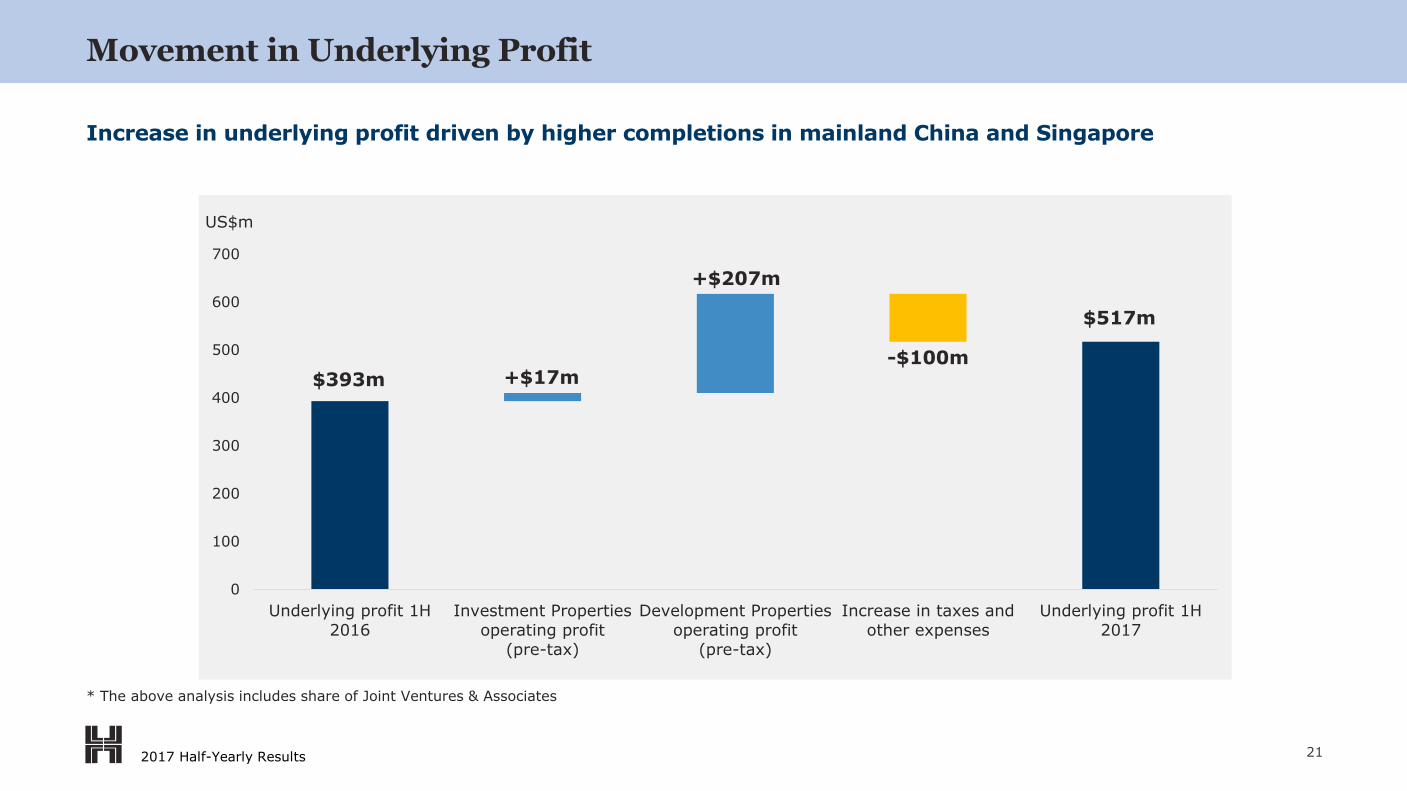

Movement in Underlying Profit

Increase in underlying profit driven by higher completions in mainland China and Singapore

US$m

$393m

$517m

+$17m

+$207m

-$100m

0

100

200

300

400

500

600

700

Underlying profit 1H

2016

Investment Properties

operating profit(pre-tax)

Development Properties

operating profit(pre-tax)

Increase in taxes and

other expenses

Underlying profit 1H

2017

* The above analysis includes share of Joint Ventures & Associates

2017 Half-Yearly Results 22

Operating Profit by Segment and Region

INVESTMENT PROPERTIES* DEVELOPMENT PROPERTIES*

Hong Kong and mainland China remain as the largest profit contributors

$404m

$6m

$62m

$15m

$487m

$430m

$5m

$59m

$10m

$504m

$0

$150

$300

$450

$600 1H 2016 1H 2017

US$m US$m

-$3m

$103m

$1m

-$2m

$99m

-$1m

$232m

$74m

$1m

$306m

-$100

$0

$100

$200

$300

$400

$500

$600 1H 2016 1H 2017

Hong Kong MainlandChina & Macau

Singapore Rest of Asia Total Hong Kong MainlandChina

Singapore Rest of Asia Total

* The above analysis includes share of Joint Ventures & Associates

2017 Half-Yearly Results 23

Consolidated Cash Flow

Strong operating cashflows

FY2016 (US$m) 1H 2017 1H 2016 %YoY

1,096 Operating activities 573 468 22%

(245) Investing activities (175) (81) 116%

(442) Financing activities (433) (372) 16%

409 Net cash inflow/(outflow) (35) 15 -333%

1,566Cash and cash equivalents atbeginning of the period

1,898 1,566 21%

(77) Effect of exchange rate changes 29 (22) -232%

1,898Cash and cash equivalents at end of the period

1,892 1,559 21%

(3,906)Gross debt (excluding bank overdrafts)

(3,774) (3,881) -3%

(2,008) Net debt at end of the period (1,882) (2,322) -19%

2017 Half-Yearly Results 24

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

30-Jun-16 31-Dec-16 1H 2017

Hong Kong Mainland China & Macau

Singapore Rest of Asia

Mainland China

Rest of Asia

Properties Carrying Values

INVESTMENT PROPERTIES - TOTAL VALUE* DEVELOPMENT PROPERTIES – NET INVESTMENT*

Cap rate compression and higher market rents in Hong Kong

30 Jun 2016

31 Dec 2016

30 Jun 2017

$30,390m$31,892m

$34,606m

US$m

30 Jun 2016

31 Dec 2016

30 Jun 2017

US$m

Pre-sale proceeds

Singapore

$3,067m

$2,416m$2,746m

* The above analysis includes share of Joint Ventures & Associates

2017 Half-Yearly Results 25

0

500

1,000

1,500

2,000

2,500

3,000

2017 2018 2019 2020 2021 2022+

Bank facilities (drawn & undrawn) Bonds*

Treasury Management

MATURITY PROFILE OF COMMITTED FACILITIES / BONDS (AS AT 30 JUN 17)

Financial position and liquidity remain strong

US$m

$574m

$1,095m

$665m

$302m

$790m

$2,841m

* Issued under MTN Programme which are at face value

31 DEC 2016 30 JUN 2017

Net debt (US$m) 2,008 1,882

Net gearing 6% 5%

Average tenor of debt (years)

6.4 6.1

Average interest cost

3.4% 3.6%

Credit ratings

- S&P A A

- Moody’s A3 A3

262017 Half-Yearly Results

Outlook

2017 Half-Yearly Results 27

Outlook

Investment properties are expected to continue to generate stable returns

Opening of WF Central in Beijing in 2H 2017

Continue to look for attractive opportunities to construct prime investment properties in key gateway cities in Asia

Strong mainland China contribution expected to continue

No further sales completions expected in Singapore until 2018

The Group remains active in seeking development opportunities in mainland China and Southeast Asia

Net gearing expected to increase due to recent investments

Balance sheet remains strong, with capacity to further invest in new projects

Maintain disciplined approach to assessing future opportunities

INVESTMENT PROPERTIES DEVELOPMENT PROPERTIES FINANCIAL

Solid full year performance expected

282017 Half-Yearly Results

Appendix

2017 Half-Yearly Results 29

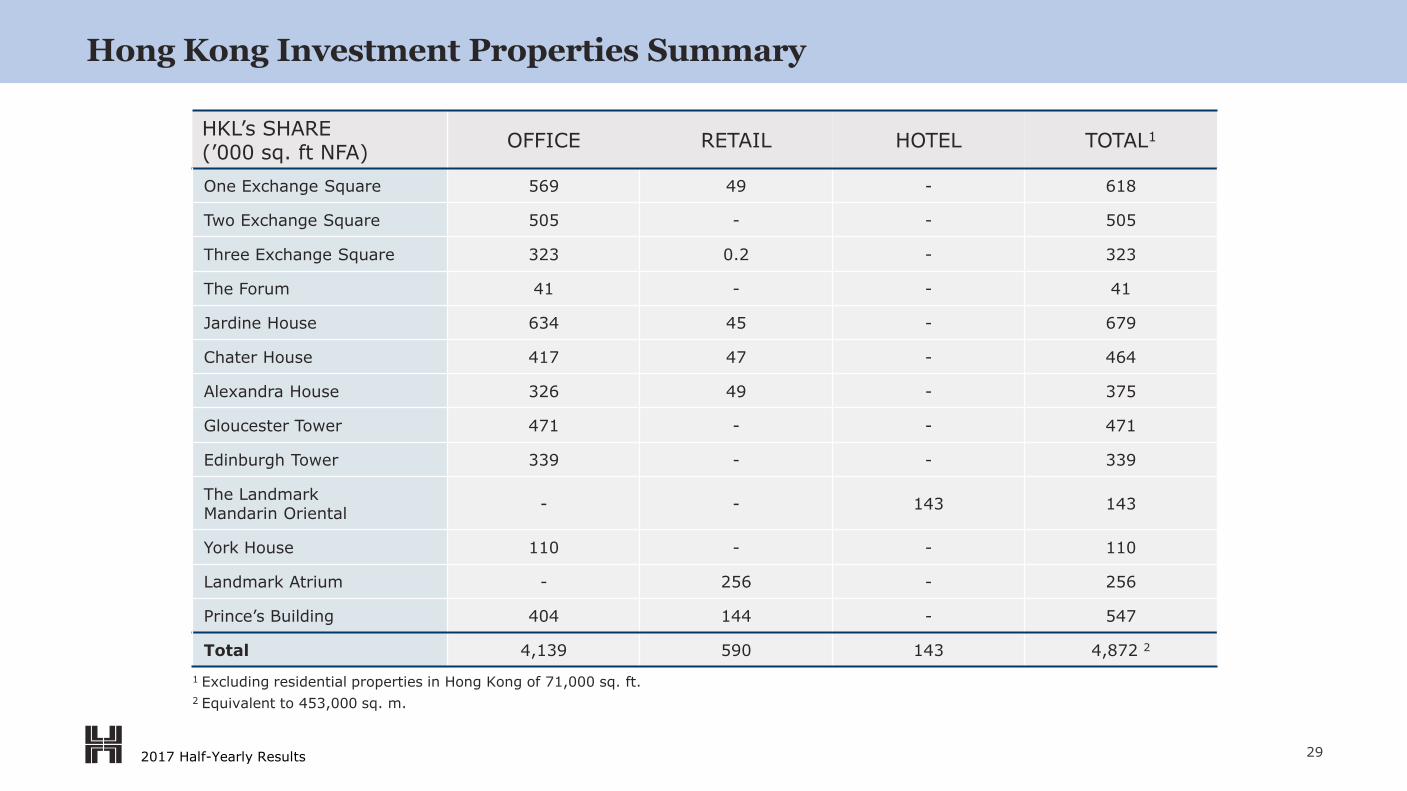

HKL’s SHARE(’000 sq. ft NFA)

OFFICE RETAIL HOTEL TOTAL1

One Exchange Square 569 49 - 618

Two Exchange Square 505 - - 505

Three Exchange Square 323 0.2 - 323

The Forum 41 - - 41

Jardine House 634 45 - 679

Chater House 417 47 - 464

Alexandra House 326 49 - 375

Gloucester Tower 471 - - 471

Edinburgh Tower 339 - - 339

The LandmarkMandarin Oriental

- - 143 143

York House 110 - - 110

Landmark Atrium - 256 - 256

Prince’s Building 404 144 - 547

Total 4,139 590 143 4,872 2

Hong Kong Investment Properties Summary

1 Excluding residential properties in Hong Kong of 71,000 sq. ft.

2 Equivalent to 453,000 sq. m.

2017 Half-Yearly Results 30

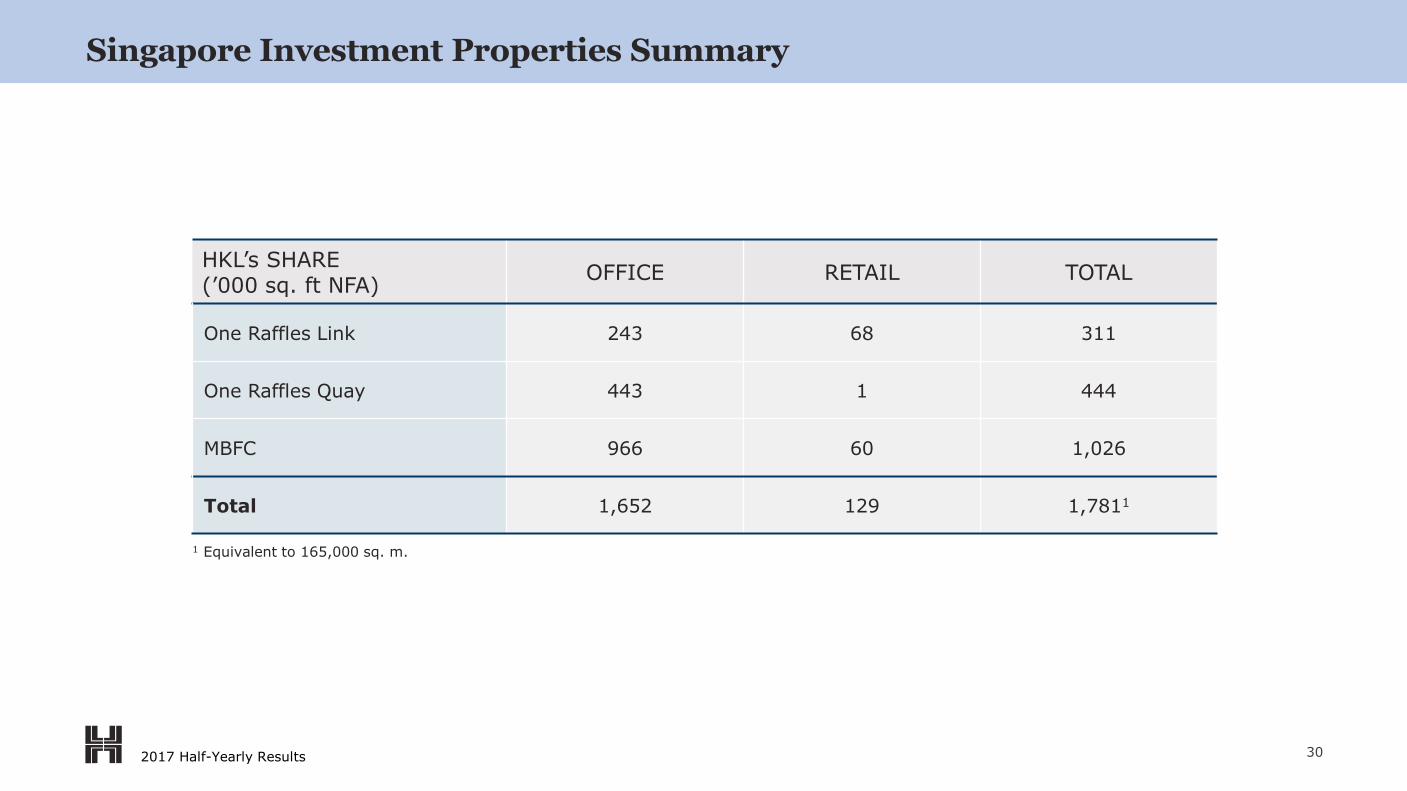

Singapore Investment Properties Summary

HKL’s SHARE(’000 sq. ft NFA)

OFFICE RETAIL TOTAL

One Raffles Link 243 68 311

One Raffles Quay 443 1 444

MBFC 966 60 1,026

Total 1,652 129 1,7811

1 Equivalent to 165,000 sq. m.

2017 Half-Yearly Results 31

Other Investment Properties Summary

HKL’s SHARE(’000 sq. ft NFA)

OFFICE RETAIL HOTEL TOTAL

Macau - 98 151 249

Jakarta 663 66 - 729

Hanoi 75 8 - 83

Bangkok 27 61 - 88

Phnom Penh 184 89 97 370

Others 70 161 215 446

Total 1,019 483 463 1,9651

1 Equivalent to 182,000 sq. m.

2017 Half-Yearly Results 32

HKL’s SHARE

PROJECT INTERESTYEAR OF

ACQUISITIONSITE AREA

(ha)

DEVELOPABLE AREA

(m sq. m.)

CONSTRUCTED(m sq. m.)

UNDER CONSTRUCTION

(m sq. m.)

TO BE DEVELOPED(m sq. m.)

Yorkville South, Chongqing

100% 2010 38.6 0.88 0.51 0.16 0.21

Yorkville North, Chongqing

100% 2011 53.8 1.09 0.33 0.20 0.56

Bamboo Grove,Chongqing

50% 2005 77.9 0.72 0.66 0.06 -

New BambooGrove, Chongqing

50% 2015 34.8 0.32 - 0.20 0.12

Landmark Riverside, Chongqing

50% 2009 22.2 0.50 0.15 0.14 0.20

Central Avenue, Chongqing

50% 2013 40.2 0.55 0.04 0.16 0.36

WE City, Chengdu

50% 2010 19.0 0.45 0.15 0.12 0.17

Parkville, Shanghai

50% 2015 8.7 0.11 0.02 0.10 -

Wuhan1 50% 2017 16.4 0.25 - - 0.25

Nanjing 33% 2017 19.9 0.07 - - 0.07

Total 331.6 4.94 1.87 1.13 1.94

Mainland China Development Properties Summary

1 Conditionally acquired

2017 Half-Yearly Results 33

HKL’s SHARE

PROJECT INTERESTYEAR OF

ACQUISITIONSITE AREA

(ha)

DEVELOPABLE AREA

(m sq. m.)

CONSTRUCTED(m sq. m.)

UNDER CONSTRUCTION

(m sq. m.)

TO BE DEVELOPED(m sq. m.)

Sol Acres 100% 2014 3.3 0.12 - 0.12 -

Lake Grande 100% 2015 1.8 0.05 - 0.05 -

Margaret Drive 100% 2017 0.5 0.02 - - 0.02

Eunosville1 100% 2017 3.5 0.1 - - 0.10

Total 9.1 0.29 - 0.17 0.12

Singapore Development Properties Summary

1 Conditionally acquired

2017 Half-Yearly Results 34

HKL’s SHARE

PROJECT INTERESTYEAR OF

ACQUISITIONSITE AREA

DEVELOPABLE AREA

(m sq. m.)

CONSTRUCTED(m sq. m.)

UNDER CONSTRUCTION

(m sq. m.)

TO BE DEVELOPED(m sq. m.)

Nava Park, Indonesia

49% 2012 67.5 0.39 0.03 0.03 0.33

Anandamaya Residences, Indonesia

40% 2013 1.4 0.05 - 0.05 -

Asya, Indonesia 25% 2016 67.3 0.23 - - 0.23

Two Roxas Triangle, thePhilippines

40% 1995 0.4 0.04 - 0.04 -

Mandani Bay, the Philippines

40% 2013 19.6 0.48 - 0.03 0.44

Northpine, the Philippines

40% 1996-2016 150.7 0.31 0.16 0.01 0.13

The Nassim, Vietnam

50% 2014 0.6 0.02 - 0.02 -

The Esse at Sukhumvit 36, Thailand

49% 2017 0.4 0.02 - - 0.02

Total 307.9 1.52 0.19 0.18 1.15

Other Development Properties Summary

2017 Half-Yearly Results 35

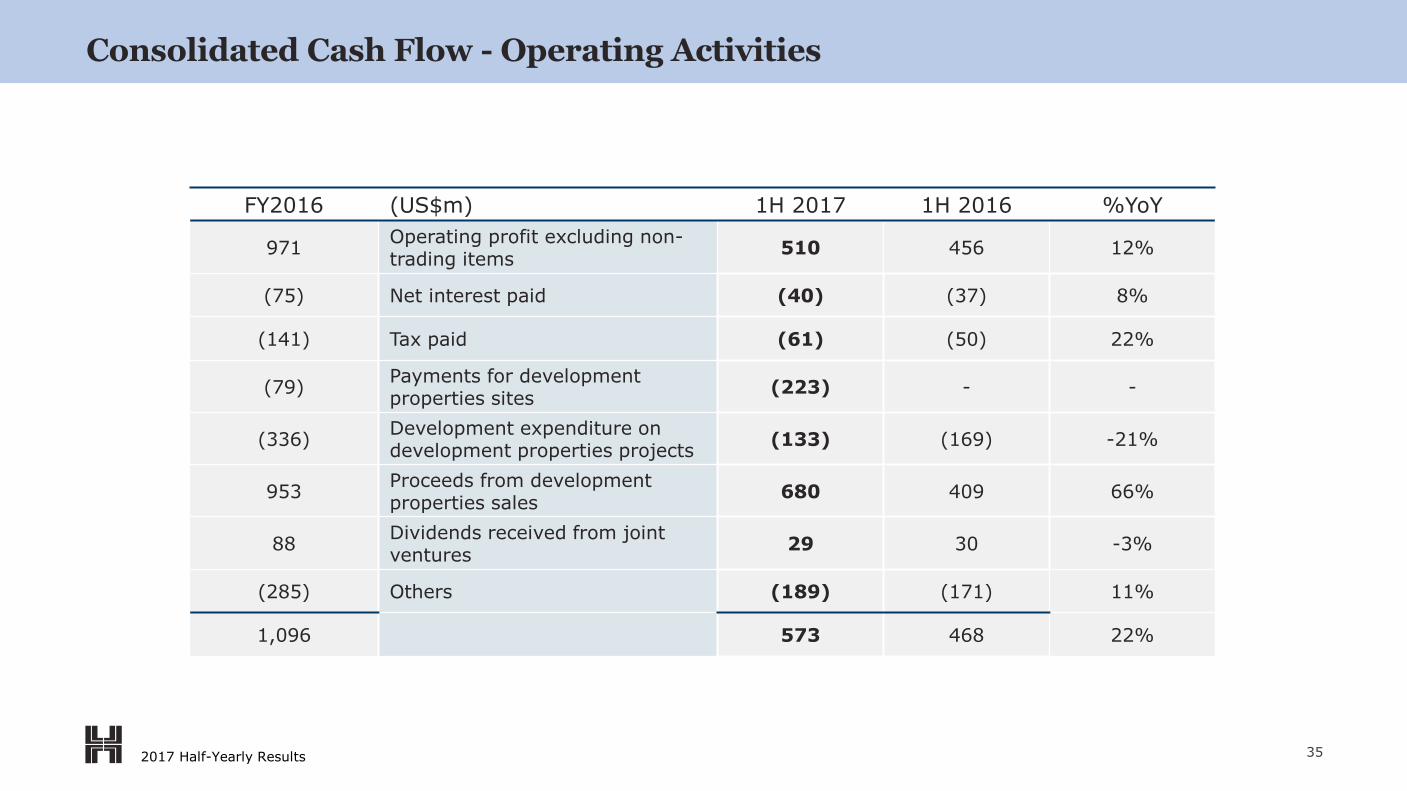

Consolidated Cash Flow - Operating Activities

FY2016 (US$m) 1H 2017 1H 2016 %YoY

971Operating profit excluding non-trading items

510 456 12%

(75) Net interest paid (40) (37) 8%

(141) Tax paid (61) (50) 22%

(79) Payments for development properties sites

(223) - -

(336)Development expenditure on development properties projects

(133) (169) -21%

953Proceeds from development properties sales

680 409 66%

88Dividends received from joint ventures

29 30 -3%

(285) Others (189) (171) 11%

1,096 573 468 22%

2017 Half-Yearly Results 36

FY2016 (US$m) 1H 2017 1H 2016

Investment properties

27,712 - Subsidiaries 30,360 26,079

4,180 - Joint ventures 4,246 4,311

31,892 34,606 30,390

Development properties

2,218 - Subsidiaries 1,972 2,746

1,835 - Joint ventures 2,461 1,818

4,053 4,433 4,564

(2,623) Others (2,904) (2,858)

33,322 Gross assets (excluding cash) 36,135 32,096

Financed by:

31,314 - Total equity 34,253 29,774

2,008 - Net debt 1,882 2,322

33,322 36,135 32,096

Consolidated Balance Sheet

2017 Half-Yearly Results 37

1H 2016 2H 2016 1H 2017

Hong Kong Office –Exchange Square 1 & 2

3.60% 3.50% 3.25%

Hong Kong Retail –Landmark Atrium

4.50% 4.50% 4.50%

Singapore Office –MBFC

3.50% 3.50% 3.25%

CAPITALISATION RATES

Investment Property – Basis of Valuation

2017 Half-Yearly Results 38

Treasury Management

LIQUIDITY AS AT 30 JUN 2017 (All figures in US$ billion)

Liquidity as at 31 DEC 2016

HK$1 S$2 US$ RMB TOTAL

Committed lines 6.5 4.5 1.3 - 0.5 6.3

Gross debt 3.9 3.1 0.4 - 0.3 3.8

Available lines 2.6 1.4 0.9 - 0.2 2.5

Cash 1.9 - 0.4 0.5 1.0 1.9

Available liquidity

4.5 1.4 1.3 0.5 1.2 4.4

1 HK$ debt includes US$ debt swapped into HK$

2 S$ debt includes HK$ debt swapped into S$

2017 Half-Yearly Results 39

Treasury Management

DEBT MANAGEMENT AND HEDGING POLICIES AS AT 30 JUN 2017

0

10

20

30

40

50

60

70

80

90

100

Type of Facilities Currency Interest Rate

Banks 54%

Bonds 46%

Fixed 57%

Floating 43%

HK$82%

S$ 10%

%

RMB 8%

1

![4PNYH[PVU VY 4VKLYUPZH[PVU& - Intec Systems Limited · (un\shy1: 1h]h:jypw[ ?7(.,: 1h]h 1:- 1h]h :wypun 4=* 1h]h =hhkpu 1h]h 'sbnfxpsl -bohvbhf #btjt 'jstu 3fmfbtf,ocation!s better](https://img.pdfslide.us/doc/110x75/5f63751302c9503c893ede57/4pnyhpvu-vy-4vklyupzhpvu-intec-systems-limited-unshy1-1hhjypw-7.jpg)