Embed Size (px)

Citation preview

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

2016 VTB Group Investor Day

London / May 17, 2016

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

Some of the information in this presentation may contain projections or other forward-looking statements regarding future events or the future

financial performance of JSC VTB Bank ("VTB") and its subsidiaries (together with VTB, the "Group").

Such forward-looking statements are based on numerous assumptions regarding the Group's present and future business strategies and the

environment in which the Group will operate in the future.

We caution you that these statements are not guarantees of future performance and involve risks, uncertainties and other important factors that

we cannot predict with certainty. Accordingly, our actual outcomes and results may differ materially from what we have expressed or forecasted

in the forward-looking statements.

These forward-looking statements speak only as at the date of this presentation and are subject to change without notice. We do not intend to

update these statements to make them conform with actual results.

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

Andrey Kostin

President and Chairman of VTB Bank Management Board

VTB Group Overview

4

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

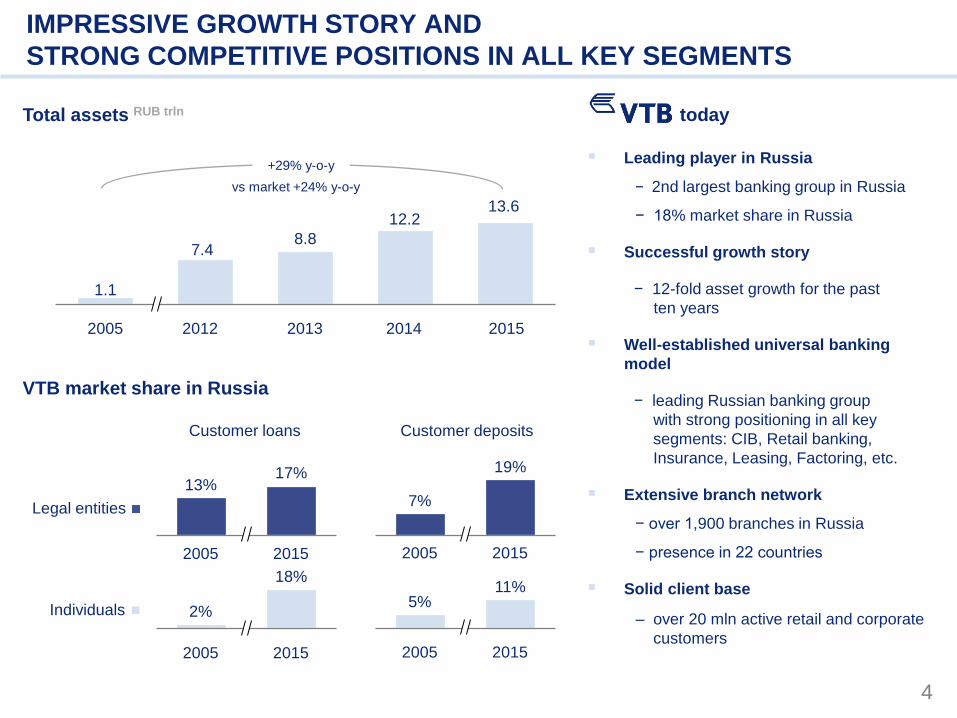

IMPRESSIVE GROWTH STORY AND

STRONG COMPETITIVE POSITIONS IN ALL KEY SEGMENTS

2013

1.1

13.6

2005 2014 2015

8.8

12.2

7.4

2012

Legal entities

Individuals

2015

18%

2005

2%

2015

11%

2005

5%

17% 13%

19%

7%

Customer loans Customer deposits

Total assets RUB trln

VTB market share in Russia

Leading player in Russia

− 2nd largest banking group in Russia

− 18% market share in Russia

Successful growth story

− 12-fold asset growth for the past

ten years

Well-established universal banking

model

− leading Russian banking group

with strong positioning in all key

segments: CIB, Retail banking,

Insurance, Leasing, Factoring, etc.

Extensive branch network

− over 1,900 branches in Russia

− presence in 22 countries

Solid client base

– over 20 mln active retail and corporate

customers

2015 2005 2015 2005

+29% y-o-y

vs market +24% y-o-y

today

5

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

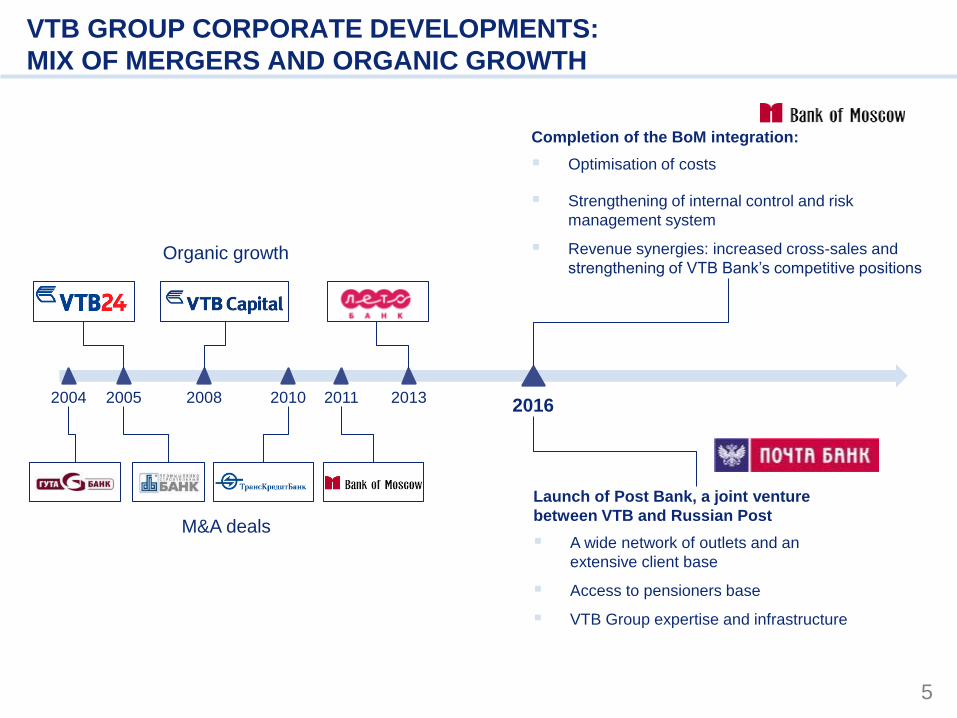

VTB GROUP CORPORATE DEVELOPMENTS:

MIX OF MERGERS AND ORGANIC GROWTH

2016 2004 2005 2008 2010 2011 2013

Launch of Post Bank, a joint venture

between VTB and Russian Post

A wide network of outlets and an

extensive client base

Access to pensioners base

VTB Group expertise and infrastructure

Completion of the BoM integration:

Optimisation of costs

Strengthening of internal control and risk

management system

Revenue synergies: increased cross-sales and

strengthening of VTB Bank’s competitive positions Organic growth

M&A deals

6

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

Retail Business

global business line

Corporate – Investment Banking

global business line

IT Risk

management

Audit and

Compliance Finance Admin HR Legal PR Security

VTB GROUP FLEXIBLE OPERATING MODEL

Assets (1) RUB trln 7.6 44% 3.8 22% 0.8 5%

Large corporate clients

(revenue > RUB 10 bn)

Broad corporate client base with

long term relationships with leading

Russian companies across all

economic sectors

#2 Corporate bank in Russia

#1 Investment bank in Russia

Mid-corporate clients

(revenue RUB 0.3 – RUB 10 bn)

Separate global business line and

profit centre since 2014

Wide regional franchise

Small corporate clients and individuals

(revenue <RUB 0.3 bn)

#2 Retail bank in Russia

Network: 1,648 outlets and

13 thousand ATMs

Post bank

Mid-Corporate Banking

global business line

Corporate Centre

(1) Second number represents share of each global business line in VTB Group’s total assets, %

7

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

SUMMARY

2017 – 2019 New development strategy 2014 – 2016 Strategy of quality growth

Maintaining position of Сorporate-Investment

banking while further improving its efficiency

Outperforming the market growth in Retail

banking, and further increasing the share of Retail

in the Group’s business mix

Prioritising Mid-Corporate banking as a

separate operating segment and profit centre while

further increasing the market share in Russia

Focusing on operating efficiency and stringent

cost control

Enhancement of Group level risk management

and controls

Transitioning the Group to unified functional and

technological platforms

Outperforming the market growth in Retail banking,

and further increasing the share of Retail in the

Group’s business mix

Outperforming the market growth in Mid-Corporate

banking in loans and transaction fee income while

further growing customer base

Maintaining position of Сorporate-Investment

banking while further diversifying CIB business mix

Prioritising investments in technological platform

development and innovations

Further consolidation of VTB Group governance

structure and enhancement of Group level risk

management and controls

Focusing on operating efficiency and stringent cost

control

1

2

3

4

5

6

1

2

3

4

5

6

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

Yuri Soloviev

First Deputy President and Chairman of VTB Bank Management Board

VTB Group Corporate-Investment Banking

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

9

In 2015 CIB managed to achieve

Four-fold year-on-year increase in NOI driven

by strong revenue growth, tight cost control

and a reduction in provisions vs high 2014

base

CIB increased / maintained its leading market

position in loans (~23%), deposits (~14%),

current accounts (~15%) and across all

investment banking products

Improved portfolio mix: increase share of Oil

and Gas, Metals and Mining, Retail, Telecom,

Chemicals and lower exposure to

Construction, Utilities, Public Sector

Year-on-year 30% increase of fees and

commissions driven by cross-sell and new

product development

CIB: 2015 KEY ACHIEVEMENTS

76%

9%

15%

45%

10%

45%

NII

NCI

Other Income

CIB net income and costs dynamics RUB bn

CIB structure of net operating income before

provisions

2014

2015

24.2

101.6

-34.2

29.9

2014 2015

Net operating income Net profit

Other income

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

10

13.6

19.7

23.8 23-24

30-31

2013 2014 2015 2016 (F) 2019 (F)

13.2

19.6

22.8 23-24

29-30

2013 2014 2015 2016 (F) 2019 (F)

CIB: 2013-2019 MARKET IN RUSSIA

CIB loans RUB trln

CIB deposits and current accounts RUB trln

Significant banking market growth in 2013-2016 driven by currency impact, closed international capital market and

low risk appetite of foreign banks to Russia;

We expect slower market growth in 2016-2019 both in lending and deposit / current accounts markets in Russia due

to low investment demand and high interest rates.

~22% CAGR

~8% CAGR

~23% ~7% CAGR CAGR

2016F 2019F 2016F 2019F

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

11

Managed to increase CIB segment loan portfolio by 18% and

ensure strong revenue growth

Maintained strong positions in corporate lending; worked with

more than 400 active client groups

Kept leading position: VTB market share of CIB Russian

credit portfolio rose from 19.3% in 2013 to 23% in 2015

International franchise development: VTB Group established

itself as one of the leading lenders and arrangers of private

financings in Sub-Saharan Africa and arranged some

strategic financing transactions in CEEMEA and Asia

(including debt restructurings, holding company financings

and event driven transactions)

Key 2015 achievements

CIB CREDIT BUSINESS(1): 2014-2015 HIGHLIGHTS

Loan portfolio RUB bn

VTB has extended its presence in infrastructure finance by moving forward with the financing of a landmark toll road

construction project and several new deals in mining, airport and shipping finance

VTB has taken the leading position in terms of volume of deals approved under the Government investment projects

support program (P-1044)

Development of Trade Finance franchise and further build-up relations with counterparties from 55 countries

Since 2013 Trade Finance business volume has been increased by 7.0x

Became one of the key partner banks for Russian Export Credit Agency (EXIAR)

(1) Key products in L&D segment are Credit, Leveraged Finance and Investments, Infrastructure credits and project finance, Trade finance, Leasing

6,748 7,671

5,186 6,139

2014 2015

+18%

CIB loans and advances (net)

Loans and advances to legal entities (net)

+14%

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

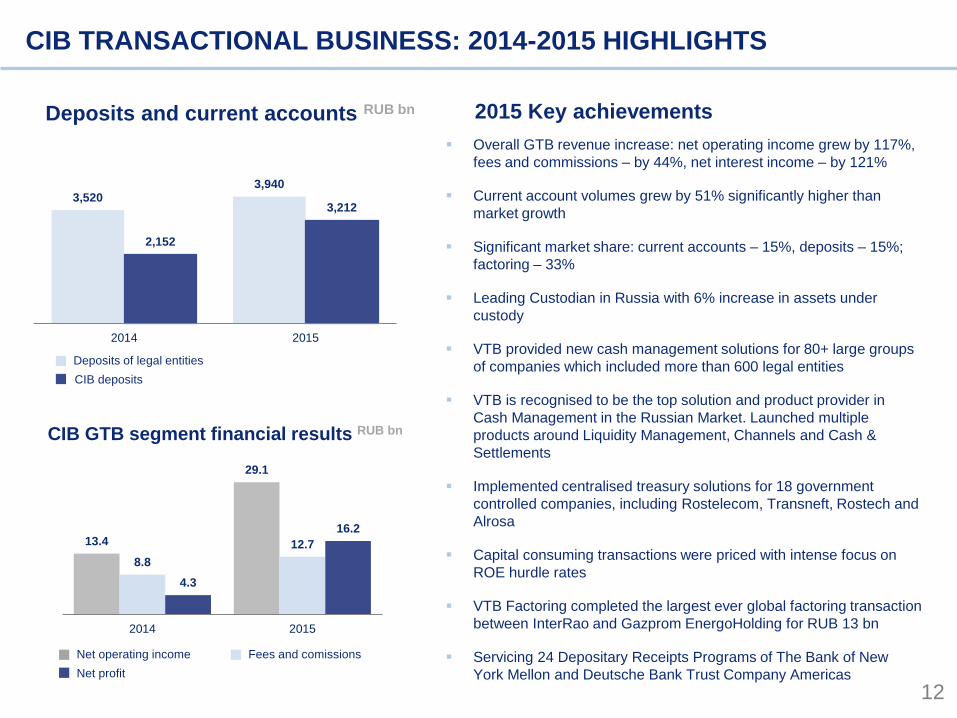

12

CIB GTB segment financial results RUB bn

Deposits and current accounts RUB bn

Overall GTB revenue increase: net operating income grew by 117%,

fees and commissions – by 44%, net interest income – by 121%

Current account volumes grew by 51% significantly higher than

market growth

Significant market share: current accounts – 15%, deposits – 15%;

factoring – 33%

Leading Custodian in Russia with 6% increase in assets under

custody

VTB provided new cash management solutions for 80+ large groups

of companies which included more than 600 legal entities

VTB is recognised to be the top solution and product provider in

Cash Management in the Russian Market. Launched multiple

products around Liquidity Management, Channels and Cash &

Settlements

Implemented centralised treasury solutions for 18 government

controlled companies, including Rostelecom, Transneft, Rostech and

Alrosa

Capital consuming transactions were priced with intense focus on

ROE hurdle rates

VTB Factoring completed the largest ever global factoring transaction

between InterRao and Gazprom EnergoHolding for RUB 13 bn

Servicing 24 Depositary Receipts Programs of The Bank of New

York Mellon and Deutsche Bank Trust Company Americas

2015 Key achievements

CIB TRANSACTIONAL BUSINESS: 2014-2015 HIGHLIGHTS

13.4

29.1

8.8

12.7

4.3

16.2

2014 2015

3,520 3,940

2,152

3,212

2014 2015

Net profit

Net operating income Fees and comissions

CIB deposits

Deposits of legal entities

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

13

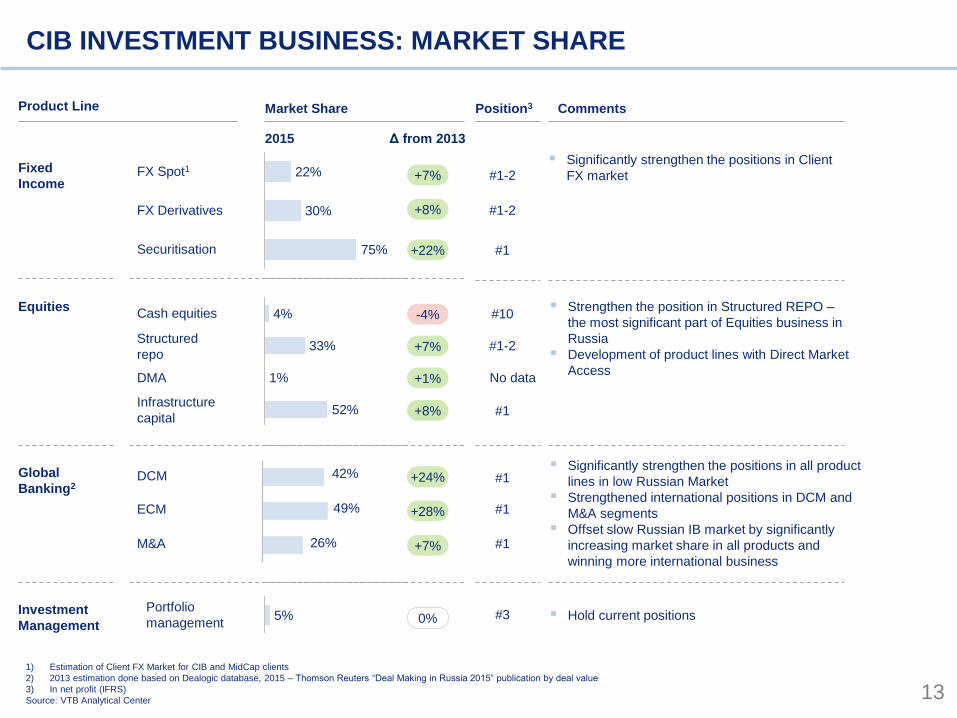

CIB INVESTMENT BUSINESS: MARKET SHARE

Securitisation

FX Derivatives

FX Spot1

Market Share Product Line

Fixed

Income

Equities

Global

Banking2

42%

49%

26%

75%

30%

22%

2015 Δ from 2013

+22%

52%

1%

33%

4% -4%

+7%

+1%

+24%

+28%

+7%

Portfolio

management Investment

Management 5%

+8%

0%

1) Estimation of Client FX Market for CIB and MidCap clients

2) 2013 estimation done based on Dealogic database, 2015 – Thomson Reuters “Deal Making in Russia 2015” publication by deal value

3) In net profit (IFRS)

Source: VTB Analytical Center

+7%

+8%

Significantly strengthen the positions in all product

lines in low Russian Market

Strengthened international positions in DCM and

M&A segments

Offset slow Russian IB market by significantly

increasing market share in all products and

winning more international business

Strengthen the position in Structured REPO –

the most significant part of Equities business in

Russia

Development of product lines with Direct Market

Access

Hold current positions

Comments

DCM

ECM

M&A

Cash equities

Structured

repo

DMA

Infrastructure

capital

Position3

#1

#1

#1

#1

#1

#1-2

#1-2

#10

#1-2

No data

#3

Significantly strengthen the positions in Client

FX market

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

14

FX and Rates:

VTB has been recognised as the best Russian Foreign Exchange Provider every year by Global

Finance magazine

2014 VTB Started trading African and Asian currencies

2015 VTB prints record-high volumes in trading RUBCNY in the onshore interdealer market in China

Local RUB Spot market share in 2015 reaches about 25%, derivatives are over 30%

Technological advances in FX allow VTB to enter into strategic partnerships with Alibaba Group and

Ant Financial Group

Credit Trading:

Over the course of the past year in response to rising capital requirements and secondary liquidity

adjustments Credit trading has significantly reduced balance sheet use for linear/non-linear risk and

has increased the velocity of position turnover

VTB has won 10 CBonds awards, including Best Bond Market Sales and Best Bond Market Trading

Commodities business:

Launch of physical trading and financing in VTBCT Zug. Zug became operating entity and completed

first physical deals in crude oil, oil products and base metals

First official member on Shanghai Gold Exchange

Physical Commodity financing set up in VTB Austria

Fixed Income

IB: 2014-2015 HIGHLIGHTS (1/2)

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

15

The establishment of a ‘true’, integrated Global Equities Product which encompasses Cash Equities,

Equity Derivatives Volatility Trading, Repo, Private Equity & Special Situations (PESS) and Infrastructure

Capital & Project Finance (IC&PF)

Completed the re-organisation of our client franchise ‘flow’ businesses to reflect the prevailing market

opportunity / dynamics while maintaining the scope of our product offering and geographical coverage;

VTBC Broker: develop a robust, scalable, secure, multi-asset class electronic trading platform which is

being pro-actively marketed to clients as we continue to add functionality and new market connectivity;

Market-leading MOEX Repo business combined with our core client-facing strategic EQ financing

business

The PESS portfolio continues to generate significant returns while the team retained their “#1 Private

Equity Firm in Russia” from Private Equity International (#2 in CEE since the category was expanded);

IC&PF are the clear leader in their field within the Russia market. The official opening (in February 2014)

of the new terminal at Pulkovo International Airport in St Petersburg attracted global acclaim

Revenue growth of almost 50% in 2015 vs 2014 despite a highly subdued domestic IB market and

without increasing headcount

Increased market share in the Russian IB market - which hit record levels in 2015 - with clear leadership

across M&A, ECM and DCM activity (verified by ThomsonReuters independent research)

A good balance of domestic and international business (~50% of revenues generated on internationally

related deals)

Development of several profitable niches where VTB has established unique specialist knowledge such

as in taking private London Stock Exchange companies and in running domestic Russian IPOs

Equities

Global Banking

IB: 2014-2015 HIGHLIGHTS (2/2)

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

16

2015 GLOBAL BANKING KEY DEALS

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

17

CIB market position

Product development

Operational efficiency

Maintain market share in lending and deposits / current accounts Russian banking markets

TOP positions in key IB markets (GB, FX, Infrastructure finance)

Leverage domestic dominant position in advisory

Bespoke approach to international markets focusing on high-yield financing solutions and

advisory

Key strategic international regions: Asia (China, India), Africa (Southern and Eastern parts),

Southern Europe

Special focus on growing Russia-China links

d CIB 2016 KEY PRIORITIES

▪ Focus on new product development: commodities, trade finance, project finance, structured

financing solutions

▪ New solutions in Cash management techniques

▪ Direct market Access platform development

▪ Further growth of cross-sell opportunities: increase number of products per one client

▪ Operating platform realignment to decrease share of hard currency CIB denominated costs

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

Mikhail Zadornov

President and Chairman of VTB24 Management Board

VTB Group Retail Banking

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

19

RETAIL BANKING MARKET IN RUSSIA

10%

38%

46%

10.9 10.7

10%

40%

45%

5%

27% 10%

10% 7.7

6% 8%

50%

10%

9%

28%

10.0

53%

11.3

54%

9%

42%

15 - 15.5

43%

10%

6%

32%

Retail loans RUB trln

18.6

82%

18% 19%

19%

14.3

15% 23.2

83%

26.0

85%

17%

81%

17.0

81%

16%

34 - 35

84%

Retail deposits RUB trln

Car loans Credit cards

Cash loans Mortgage

Small business loans RUB trln Small business RUB trln

2.4 2.7

2.9 2.7 2.6

3.1-3.3

2013 2012 2014 2016F 2015 2019F

3.1 3.0

30%

2015

70%

2016F

81%

19% 21%

79%

2.6

2014

69%

31% 31%

69%

2013 2012

2.1 2.4

69%

31%

2019F

3.3-3.5

CAGR

+11%

+10%

+18%

+11%

CAGR

CAGR

CAGR

+4% CAGR

+6%

CAGR

2013 2012 2014 2016F 2015 2019F 2013 2012 2014 2016F 2015 2019F

+13% CAGR

+3% CAGR Current accounts Term deposits

Current accounts Term deposits

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

20

VTB GROUP MARKET POSITION IN RETAIL BUSINESS IN RUSSIA

12.7% 14.4% 15.0%

1.2%

2.7% 2.9%

0.6% 0.9%

18.8% 17.8%

13.9%

7.5% 8.7% 9.2%

1.2%

1.8% 1.8%

11.2% 10.7% 8.7%

5.0% 5.6% 6.7%

0.6% 1.2%

1.2%

5.2%

10.0% 11.3% 1.4%

1.3%

1.7%

Retail loans Retail deposits and current accounts

Small business loans

Small business deposits and current accounts

VTB24

Ex-Bank of Moscow

2012 2015 2016F 2012 2015 2016F

+3.9 p.p. +1.0 p.p.

+2.0 p.p. +0.5 p.p.

2012 2015 2016F

7.9% 6.9%

5.6%

+1.3 p.p.

+1.0 p.p.

2012 2015 2016F

13.1% 11.4%

6.6%

+4.8 p.p. +1.7 p.p.

0.1% 0.2% 0.2%

VTB24

Ex-Bank of Moscow

VTB24

Ex-Bank of Moscow

Leto / Post Bank

VTB24

Ex-Bank of Moscow

Leto / Post Bank

& VTB Bank

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

21

50.8

37.6

16.9

RETAIL BUSINESS CONTINUES TO BE THE KEY CONTRIBUTOR

TO VTB GROUP P&L AND EFFICIENCY

2013 2014 2015

Profitability of VTB Group’s Retail business RUB bn

48% 46% 56% CIR

136.2

157.6

Net operating income

Net profit

166.0

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

22

VTB Group customer base (active customers) in 2015 mln

9.0 1.1

1.9

11.5

10.4

1.3

19.9

Total

customer

base

VTB

Pension

Fund

VTB

Insurance

Banking

customers,

total

BoM Post Bank

(ex-Leto Bank)

VTB24 De-duplication

-0.5

-3.3

VTB GROUP CUSTOMER BASE IN RUSSIA BY ENTITY

De-duplication

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

23

2,544 (29%) 1,679

(19%)

2,526 (29%)

2,290 (25%)

2,466 (28%)

3,133 (35%)

1,253 (14%)

1,932 (21%)

VTB24 CUSTOMER BASE BY SEGMENT

8,789 9,033

VTB24 customer segments (active customers) thsd

2013 2015

Affluent + HNWI

Upper mass

Mass

Lower mass

+7 p.p.

+7 p.p.

-4 p.p.

-10 p.p.

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

24

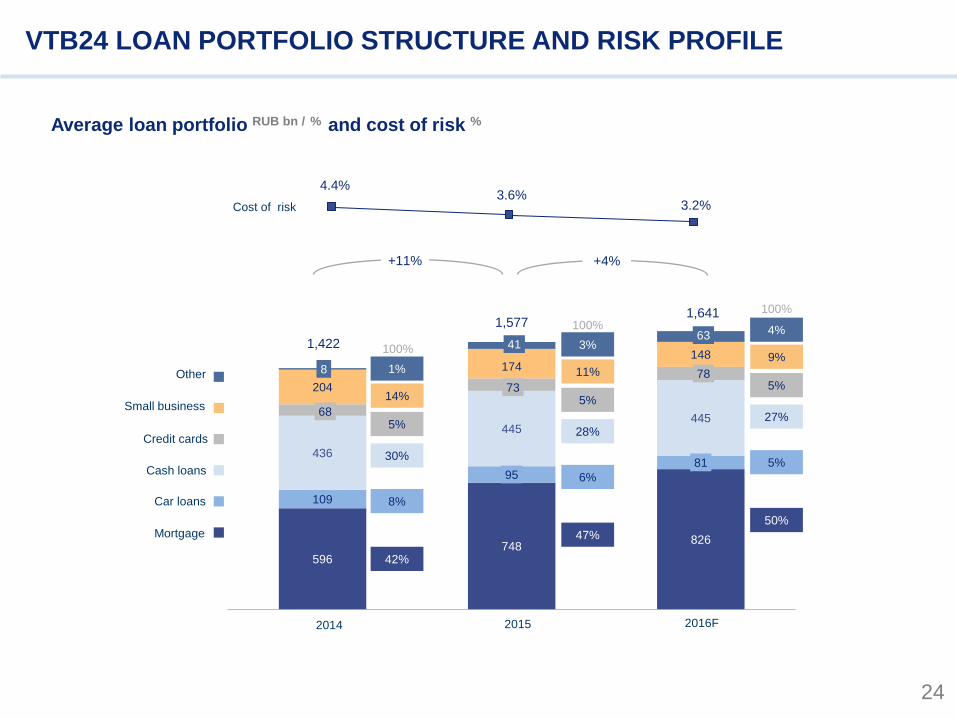

VTB24 LOAN PORTFOLIO STRUCTURE AND RISK PROFILE

Average loan portfolio RUB bn / % and cost of risk %

596 748

826

109

95 81

436

445 445

68

73 78

204

174 148

8

41 63

2015 2016F 2014

1,422

1,577 1,641

Small business

Mortgage

Car loans

Cash loans

Credit cards

Other

+11% +4%

42%

8%

30%

5%

14%

1%

47%

6%

28%

5%

11%

3%

50%

5%

27%

5%

9%

4%

100%

100%

100%

Cost of risk

4.4% 3.6%

3.2%

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

25

10.1 11.0

17.0

2.0

2.0

VTB GROUP BRANCH AND ATM NETWORKS IN RUSSIA

378

530 576 627

646 603 630

2,600

4,312

455

(42%)

2016F

+52%

1,713

309

(45%)

687

2012

537

(50%)

2014

470

(45%)

1,649

2015

Standard offices

Offices with affluent zones

Leto/Post Bank and ex-BoM

Post-office branches

2014

12.1

13.4

2017F 2015

0.4

VTB24

Ex-BoM

Leto/Post Bank

Branch network ATM thsd

+11%

+27%

-4%

+161%

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

26

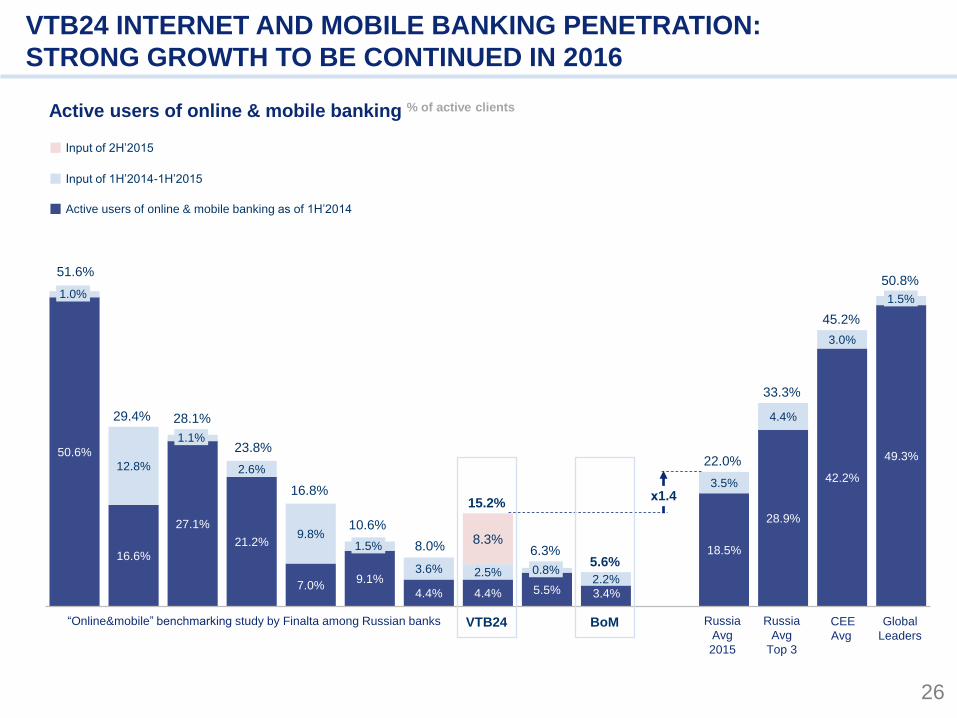

VTB24 INTERNET AND MOBILE BANKING PENETRATION:

STRONG GROWTH TO BE CONTINUED IN 2016

Active users of online & mobile banking % of active clients

50.6%

16.6%

27.1%

21.2%

7.0% 9.1%

4.4% 4.4% 5.5% 3.4%

18.5%

28.9%

42.2%

49.3% 12.8% 2.6%

9.8%

3.6% 2.5% 2.2%

3.5%

4.4%

3.0%

8.3%

45.2%

33.3%

22.0%

BoM

5.6% 6.3%

0.8%

VTB24

15.2%

8.0%

10.6%

Global

Leaders

50.8%

1.5%

CEE

Avg

1.5%

16.8%

23.8%

28.1%

1.1%

29.4%

51.6%

1.0%

х1.4

Active users of online & mobile banking as of 1H’2014

Input of 1H’2014-1H’2015

Input of 2H’2015

“Online&mobile” benchmarking study by Finalta among Russian banks Russia

Avg

2015

Russia

Avg

Top 3

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

27

CRM ACTIVITIES PLAY INCREASINGLY IMPORTANT ROLE IN

SUPPORTING DYNAMIC GROWTH OF RETAIL BUSINESS

2015 2016F

151,969

49%

316,091

54%

+129%

Sales of consumer loans RUB mln

2016F

41%

364,256

449,144

27%

2015

+87%

Sales of credit cards No. of cards

49%

2016F

418,956

2015

195,724

56%

+87%

Sales of affluent bundles

(“Privilege”) No. of bundles

Share of CRM VTB24 business plans for selected products and CRM

+108% +23% +114%

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

28

SHARE OF CLIENTS WITH SALARY ACCOUNTS

Share of clients with salary accounts, 2014 % of active clients

47.0%

42.0%

36.0% 35.0%

32.0% 32.0%

22.0%

19.0%

12.0%

3.0%

29.0%

Russia

Average

BoM VTB24 “Branch productivity” benchmarking study by Finalta among Russian banks

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

29

VTB GROUP RETAIL BUSINESS KEY STRATEGIC INITIATIVES

FOR THE NEXT 3 YEARS

Market share and financial performance

Increase market share (as a Group) both in loans and deposits

+ 5% in loans

+ 5% in deposits and CA

Maintain high level of financial efficiency / profitability (ROE ~18%)

Customers

▪ Increase number of active customers through new customers acquisition and current customers reactivation

▪ Continue developing as a multi-brand model to target different client segments (e.g. focus VTB24 on mass-affluent and affluent segments and Post Bank

on mass segment and retirees)

▪ X-sell: increase number of products per customer

▪ Customer experience: improve customer satisfaction (NPS)

Multi-channel

▪ Continue developing multi-channel model:

Increase sales network - mainly by Post Bank

Increase penetration of Internet and Mobile bank

Increase share of sales in alternative channels (CRM, Internet)

Operational efficiency

▪ Achieve high-level of operational efficiency: number of customers per branch employee, sales per branch employee

▪ Continue further centralisation of back-office functions

Post bank

▪ Successfully realise a joint project with Russian Post

IT

▪ Mid 2017 – completion of VTB24 IT overhaul

▪ YE’2019 – harmonisation of VTB Group retail IT landscape

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

30

Customers

POST BANK OFFICIALLY LAUNCHED IN APRIL 2016

Post Bank logo and branch format

Key numbers (2023): Branches in Post offices

Top-3 retail bank in Russia

15,000

>17 mln

Top-3

Key numbers (2023)

10

41

115

212

225

240

252

25

33

248

164

74

254

194

120

253

225

185

198

76

155

216

132

186

146

205

81

183

223

131

219

240

189

153

153

153

58

75

140

235

193

219

118

141

188

31

6.7

15.6

52% 60%

1

20

2

5

3

25

POST BANK 2016 BUSINESS PLAN

Loan portfolio (gross) RUB bn Customer deposits RUB bn

Net operating income RUB bn

60

103 14

15

4

8

78

126

2015 2016F

Credit cards

POS

Net profit RUB bn

-1.7

0.1

CIR

+62%

2015 2016F

х8.6

Term deposits

Current accounts

+131%

Cash loans

2015 2016F 2015 2016F

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

Herbert Moos

Deputy President and Chairman of VTB Bank Management Board

VTB Group Financial Performance and Outlook

33

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

5.5% 7.9%

12.6%

108.0 98.0

52.0

2013 2014 2015

31.8 38.0 61.2

MACRO ENVIRONMENT SIGNIFICANTLY DETERIORATED

Oil price USD and exchange rate RUB Inflation and CBR key rate

Russian macroeconomic indicators

USD/RUB

(avg)

Oil price

(Urals, avg)

Investments in fixed capital

GDP

Industrial production

Retail turnover

1.3% 0.6%

-3.7%

0.8%

-1.5%

-8.4%

0.4% 1.7%

-3.4%

3.9% 2.7%

-10.0%

2013 2014 2015

6.8% 7.8%

15.6%

2013 2014 2015

(1) In its current form key rate was introduced by the Bank of Russia in September 2013. Average figure for 2013 is calculated based on the period from

September 13, 2013 till December 31, 2013.

-47% -9%

CPI inflation

(avg)

CBR key rate

(avg) (1)

+7.8 p.p. +1 p.p.

34

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

313

534 635

2013 2014 2015

4.7% 5.8% 6.3%

10.9% 9.8%

12.4%

14.7%

12.0%

14.3%

807 998 1,316

1,516 1,217 1,093

2013 2014 2015

VTB SIGNIFICANTLY IMPROVED BALANCE SHEET METRICS

AND CAPITAL

Total assets RUB bn Customer funding RUB bn

8,769

12,191 13,642

2013 2014 2015

4,383 5,669

7,267

2013 2014 2015

BIS Group capital RUB bn NPLs (90+) RUB bn

115.5% 114.8% 105.8%

Total CAR

Tier I ratio

Tier I capital

Total capital

NPL coverage

ratio

151% 157% 139%

LDR +12% +39%

+28% +29%

+25% +11%

NPL ratio

NPL

35

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

99.2

275.4

178.1

2013 2014 2015

1.6%

3.4%

1.8%

PROFITABILITY HIT BY LOWER NIM AND RISE IN CREDIT COSTS

PARTLY OFFSET BY SOLID FEES GROWTH

Net interest income RUB bn Provisions charge (1) RUB bn

Net fee and commission income (NFCI) RUB bn Net profit RUB bn

316.9 347.3

289.1

2013 2014 2015

4.4% 4.0%

2.6%

100.5

0.8 1.7

2013 2014 2015

11.8% 0.1% 0.1%

55.4 63.1

76.2

2013 2014 2015

NIM

Share of NFCI in operating

income before provisions

13% 12% 19%

-17% +10%

+21% +14%

CoR

ROE

-35% +178%

+113%

-99%

(1) Including provision charge for impairment of debt financial assets and provision charge for impairment of other assets, credit related commitments and legal claims.

36

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

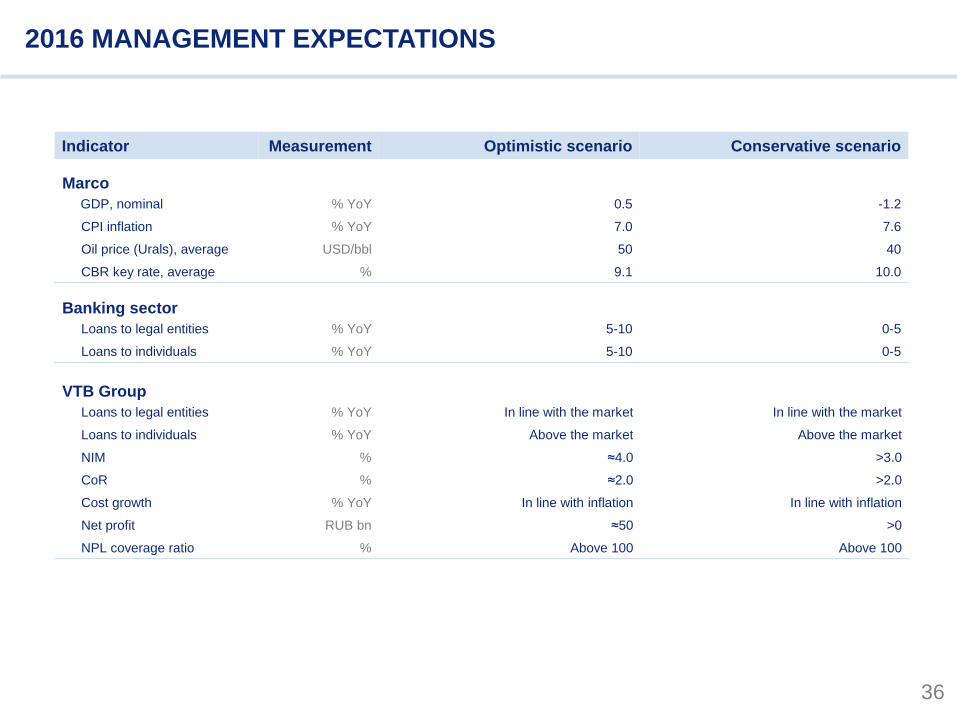

2016 MANAGEMENT EXPECTATIONS

Indicator Measurement Optimistic scenario Conservative scenario

Marco

GDP, nominal % YoY 0.5 -1.2

CPI inflation % YoY 7.0 7.6

Oil price (Urals), average USD/bbl 50 40

CBR key rate, average % 9.1 10.0

Banking sector

Loans to legal entities % YoY 5-10 0-5

Loans to individuals % YoY 5-10 0-5

VTB Group

Loans to legal entities % YoY In line with the market In line with the market

Loans to individuals % YoY Above the market Above the market

NIM % ≈4.0 >3.0

CoR % ≈2.0 >2.0

Cost growth % YoY In line with inflation In line with inflation

Net profit RUB bn ≈50 >0

NPL coverage ratio % Above 100 Above 100

37

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

VTB GROUP MACRO EXPECTATIONS TILL 2019

GDP growth Y-o-Y Oil price (Urals), average USD/bbl

CPI inflation Dec / Dec CBR key policy rate EOP

≈2%

≈2.0-2.5% ≈2.0-2.5%

2017F 2018F 2019F

55 60 60

2017F 2018F 2019F

5.5 – 6.5%

4.5 – 5.5% 4.0 – 5.0%

2017F 2018F 2019F

6.5 – 7.5%

5.5 – 6.5% 5.5 – 6.5%

2017F 2018F 2019F

38

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

12.0 - 12.5 13.0 - 13.5 15.0 - 15.5

2017F 2018F 2019F

RUSSIAN BANKING SECTOR TILL 2019

Loans to legal entities RUB trln Loans to individuals RUB trln

Deposits of legal entities RUB trln Deposits of individuals RUB trln

36 - 37 40 - 41

44 - 45

2017F 2018F 2019F

+10-12%

Y-o-Y avg growth rate

VTB market share

+10-15%

Y-o-Y avg growth rate

VTB market share

32 - 33 36 - 37

40 - 41

2017F 2018F 2019F

28 - 29 31 - 32 34 - 35

2017F 2018F 2019F

VTB market share VTB market share

+10-12%

Y-o-Y avg growth rate +9-11%

Y-o-Y avg growth rate

2015 2019 2015 2019

2015 2019 2015 2019

18% 23%

11% 16%

14%

11%

13%

11%

39

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

VTB GROUP KEY FINANCIAL TARGETS TILL 2019

Indicator Measurement 2017 – 2019

Loans to legal entities % YoY In line with the market

Loans to individuals % YoY Above the market

NIM % ≈4.0

CoR % ≈2.0

CIR % 2019: low 40th

ROE % 2017-2018: >5.0

2019: ≈11.0

NPL coverage ratio % Above 100

40

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

IT AND INFRASTRUCTURE DEVELOPMENT

Key objectives

Productivity increase

Reduced maintenance

cost

Overall improvement of

IT reliability and

security

Reduced time-to-

market Consolidation and virtualisation of IT infrastructure

Product and channel innovation

New data processing center,

integrated infrastructure of

data processing centers in

Russia

Private cloud

and dynamic

capacity

management

Virtualisation of

workstations

Workplace

mobility

Product and channel innovation

Broadening the list of products and

services available through mobile and

internet banking

Omnichannel and seamless customer

experience

New customer interaction channels

Market place (integrated group-wide

product platform)

Organisational setup to support

innovation cycle

Simplification of IT landscape

Unification of corporate support

applications

Centralised IT architecture management

Data analytics

Enhancement of data quality and

granularity through introduction of CDO

function and methodology

MIS improvement through visualisation

tools and mobile analytics

Centralised risk modelling

Cyber security

Development of authentication tools (including biometric authentication)

Introduction of adaptive anti-fraud systems

41

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

10% 3%

6%

10%

9%

62%

222

Future projections2015

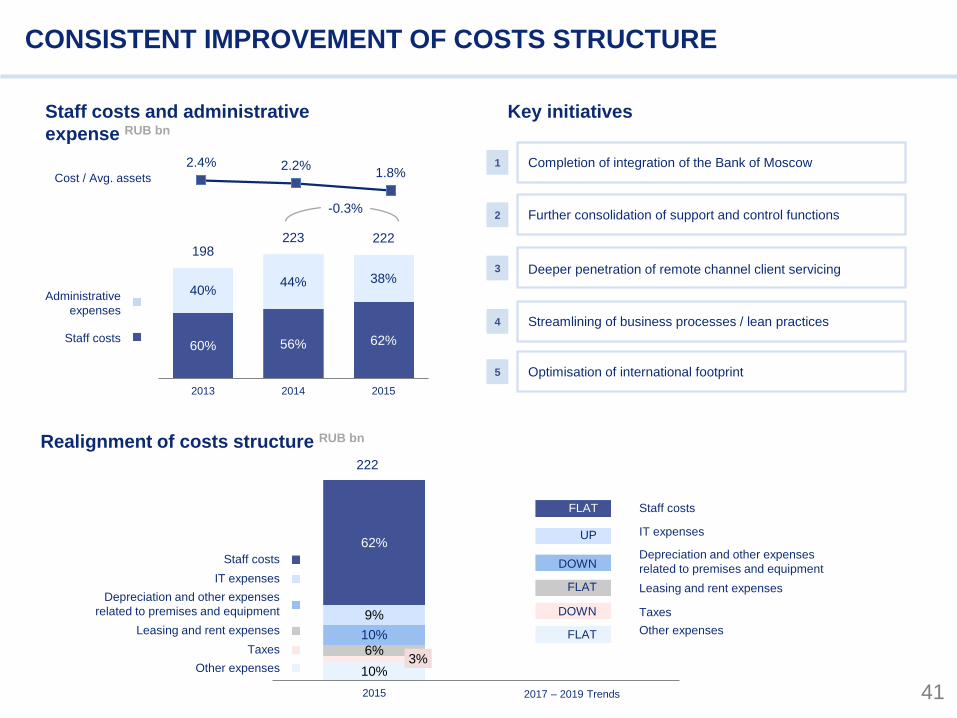

CONSISTENT IMPROVEMENT OF COSTS STRUCTURE

Key initiatives Staff costs and administrative

expense RUB bn

Realignment of costs structure RUB bn

Staff costs

Administrative

expenses

Cost / Avg. assets

62% 56% 60%

38% 44% 40%

222 223 198

201520142013

-0.3%

1.8% 2.2% 2.4%

1 Completion of integration of the Bank of Moscow

2

3

4

5

Further consolidation of support and control functions

Deeper penetration of remote channel client servicing

Streamlining of business processes / lean practices

Optimisation of international footprint

Other expenses

Taxes

Leasing and rent expenses

IT expenses

Depreciation and other expenses

related to premises and equipment

Staff costs

Other expenses

Taxes

Leasing and rent expenses

IT expenses

Depreciation and other expenses

related to premises and equipment

Staff costs

FLAT

DOWN

UP

DOWN

FLAT

FLAT

2017 – 2019 Trends

42

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

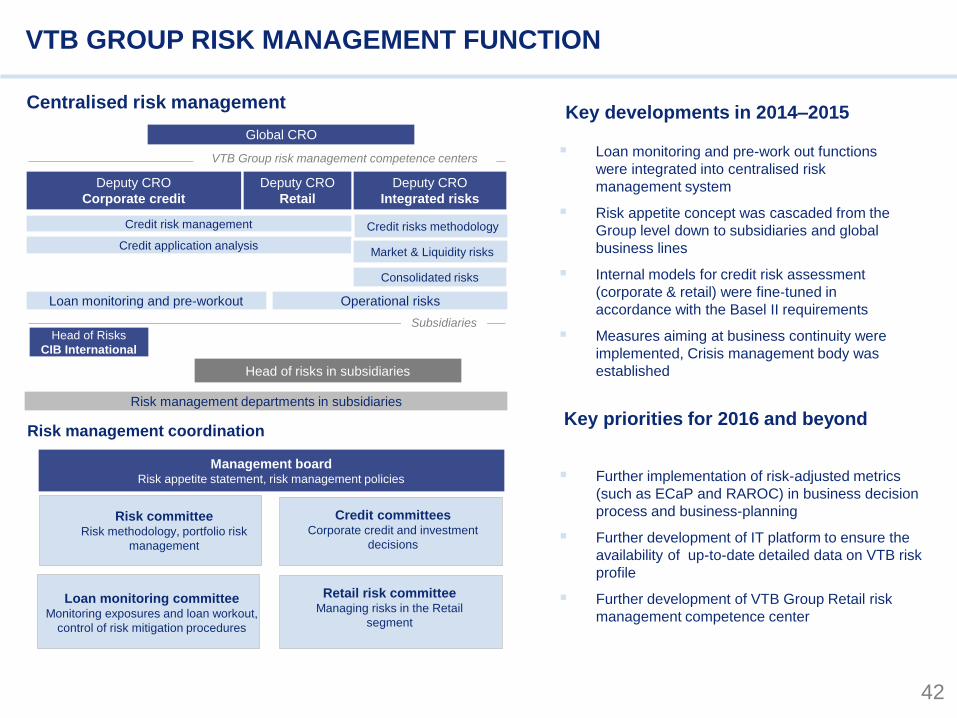

VTB GROUP RISK MANAGEMENT FUNCTION

Loan monitoring and pre-work out functions

were integrated into centralised risk

management system

Risk appetite concept was cascaded from the

Group level down to subsidiaries and global

business lines

Internal models for credit risk assessment

(corporate & retail) were fine‐tuned in

accordance with the Basel II requirements

Measures aiming at business continuity were

implemented, Crisis management body was

established

Global CRO

Deputy CRO

Corporate credit

Deputy CRO

Integrated risks

Deputy CRO

Retail

Credit risk management

Credit application analysis

Consolidated risks

Head of Risks

CIB International

Loan monitoring and pre-workout Operational risks

Head of risks in subsidiaries

VTB Group risk management competence centers

Risk management departments in subsidiaries

Market & Liquidity risks

Subsidiaries

Centralised risk management

Risk management coordination

Key developments in 2014–2015

Key priorities for 2016 and beyond

Further implementation of risk-adjusted metrics

(such as ECaP and RAROC) in business decision

process and business-planning

Further development of IT platform to ensure the

availability of up-to-date detailed data on VTB risk

profile

Further development of VTB Group Retail risk

management competence center

Management board Risk appetite statement, risk management policies

Credit committees Corporate credit and investment

decisions

Loan monitoring committee Monitoring exposures and loan workout,

control of risk mitigation procedures

Retail risk committee Managing risks in the Retail

segment

Credit risks methodology

Risk committee Risk methodology, portfolio risk

management

43

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

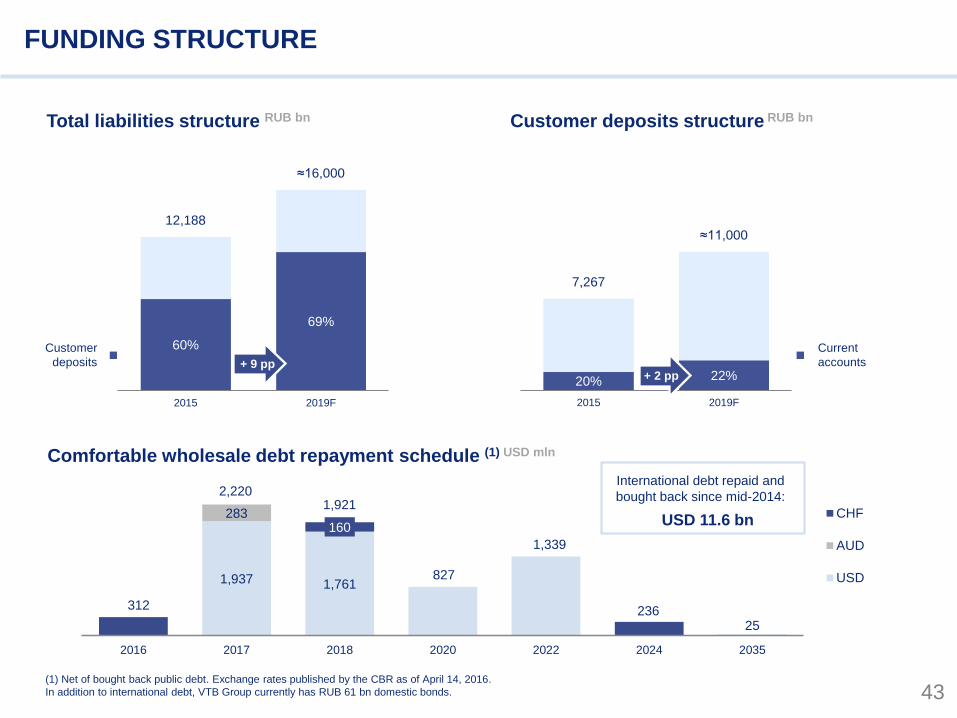

FUNDING STRUCTURE

Total liabilities structure RUB bn Customer deposits structure RUB bn

Comfortable wholesale debt repayment schedule (1) USD mln

1,937 1,761

25

283 160

312

2,220 1,921

827

1,339

236

2016 2017 2018 2020 2022 2024 2035

CHF

AUD

USD

60%

69%

12,188

≈16,000

2015 2019F

Customer

deposits

20% 22%

7,267

≈11,000

2015 2019F

Current

accounts

(1) Net of bought back public debt. Exchange rates published by the CBR as of April 14, 2016.

In addition to international debt, VTB Group currently has RUB 61 bn domestic bonds.

+ 9 pp + 2 pp

International debt repaid and

bought back since mid-2014:

USD 11.6 bn

44

153

153

255

10

41

115

212

225

240

161

11

72

153

51

102

221

221

221

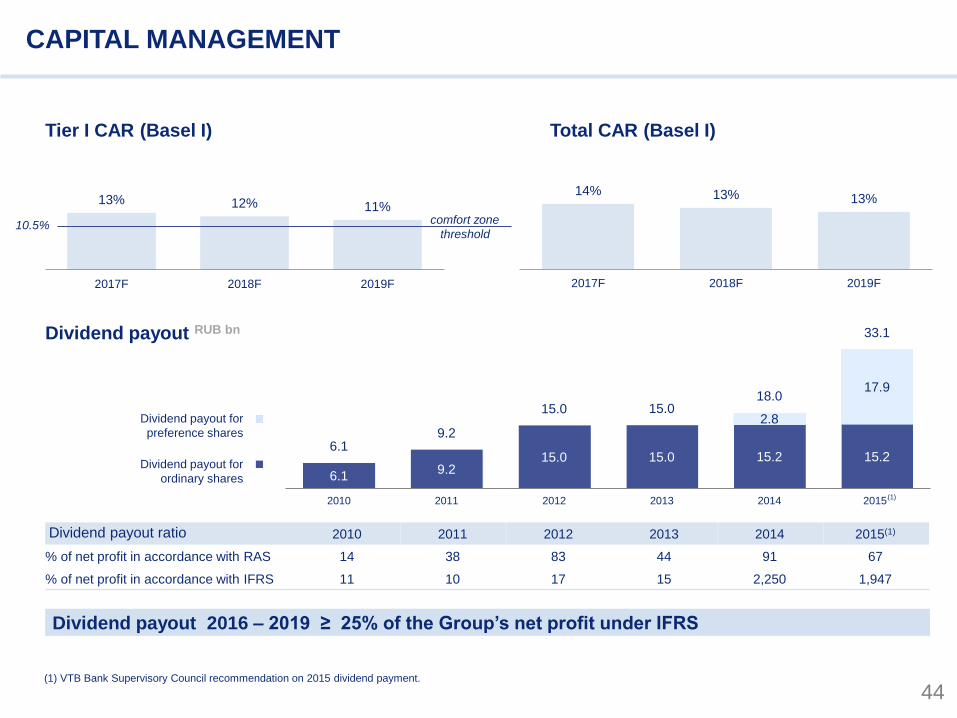

6.1 9.2

15.0 15.0 15.2 15.2

2.8

17.9

6.1 9.2

15.0 15.0 18.0

33.1

2010 2011 2012 2013 2014 2015*

CAPITAL MANAGEMENT

Tier I CAR (Basel I)

13% 12% 11%

2017F 2018F 2019F

10.5% comfort zone

threshold

Dividend payout 2016 – 2019 ≥ 25% of the Group’s net profit under IFRS

Dividend payout RUB bn

14% 13% 13%

2017F 2018F 2019F

Total CAR (Basel I)

Dividend payout ratio 2010 2011 2012 2013 2014 2015(1)

% of net profit in accordance with RAS 14 38 83 44 91 67

% of net profit in accordance with IFRS 11 10 17 15 2,250 1,947

Dividend payout for

preference shares

Dividend payout for

ordinary shares

(1) VTB Bank Supervisory Council recommendation on 2015 dividend payment.

(1)