Embed Size (px)

Citation preview

Internal market,

industry,

entrepreneurship and SMEs

2016 SBA Fact Sheet

France

Key points

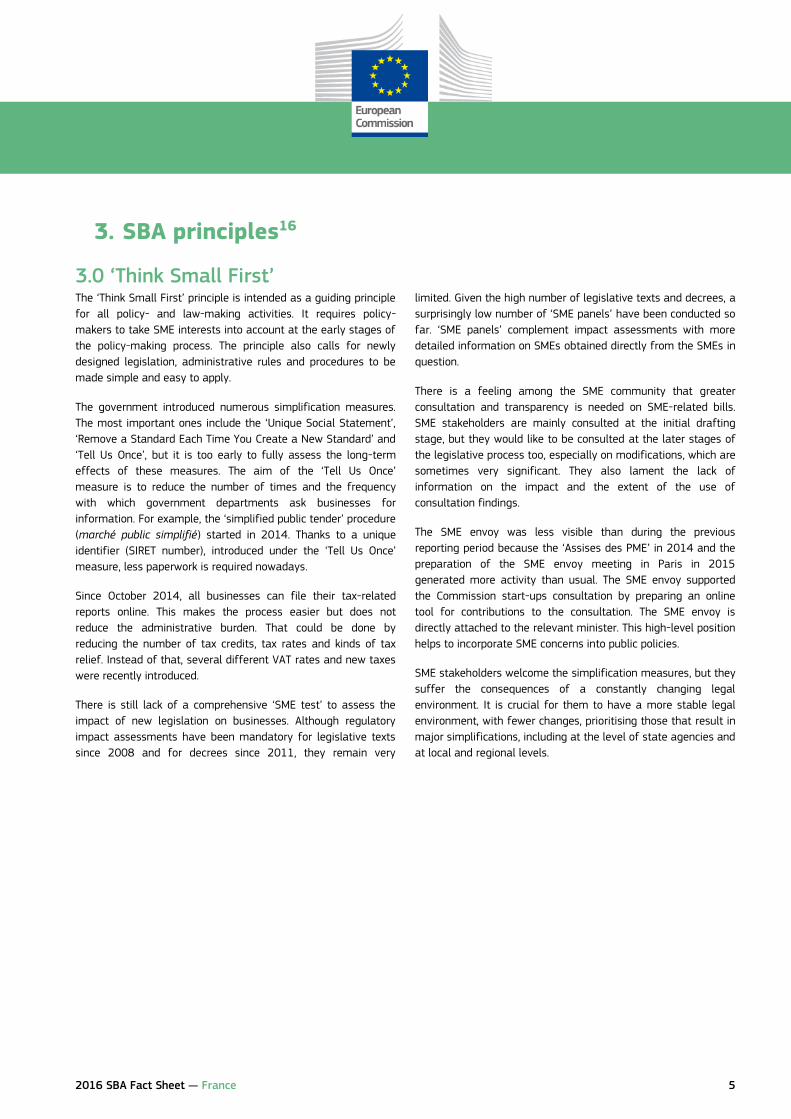

Past & future SME performance1: SMEs in France are recovering from the crisis. Their labour productivity is 27 % higher than the EU

average. Between 2010 and 2015, the added value of French SMEs increased by 4 %. Employment increased only in microcompanies,

by 2 %, while in small companies it fell by 1 % and in medium-sized companies by 4 %. Overall, SME employment stagnated during

this period. In 2015, the number of business registrations fell by 3 % compared to 2014. The number of bankruptcies increased by

1 %. From 2016 onwards, the current moderate growth in SME added value and employment is expected to accelerate. Between

2015 and 2017, added value is forecast to increase by 7 % and employment by 3 %. This corresponds to the creation of 281 000

jobs in SMEs within two years.

Implementing the Small Business Act for Europe (SBA): France’s SBA profile is balanced, with performance in most of the SBA areas

broadly in line with the EU average. Good framework conditions are in place, in particular for SME participation in public procurement.

French policy-makers have been increasingly more attentive to SME policy, with the most significant progress made in recent years in

the area of Access to finance. The ‘Industry for the Future’ programme, the tax incentives encouraging companies to invest and the

incentives to recruit have benefited French SMEs. A large number of measures aim to simplify administrative tasks for SMEs.

SME policy priorities: Regulatory burden and legislative instability continue to be causes for concern. A stable legal environment is

crucial for French SMEs. The focus needs to be on a smaller number of changes, prioritising those that simplify matters a lot,

including at the level of state agencies and at local and regional levels. Remaining barriers that recent or ongoing reforms do not

sufficiently address, in particular regarding business services and regulated professions, need to be removed. A comprehensive,

widespread ‘SME test’ for the assessment of the impact of new legislation on businesses remains to be introduced. The links between

the education sector and the labour market need to be tightened. Innovation policy schemes could be simplified and made more

efficient.

About the SBA fact sheets The Small Business Act for Europe (SBA) is the EU’s flagship policy initiative to support small and medium-sized enterprises (SMEs). It comprises a

set of policy measures organised around 10 principles ranging from Entrepreneurship and ‘Responsive administration’ to Internationalisation. To

improve the governance of the SBA, the 2011 review of it called for better monitoring. Published annually, the SBA fact sheets aim to improve the

understanding of recent trends and national policies affecting SMEs. Since 2011, each EU Member State has appointed a high-ranking

government official as its national SME envoy. SME envoys spearhead the implementation of the SBA agenda in their countries.

2016 SBA Fact Sheet — France 2

Table of Contents Key points ..................................................................................................................................................................................................................................................................... 1

1. SMEs — basic figures ....................................................................................................................................................................................................................................... 2 2. SBA profile ............................................................................................................................................................................................................................................................. 3 3. SBA principles ....................................................................................................................................................................................................................................................... 5

3.0 ‘Think Small First’ ............................................................................................................................................................................................................................................. 5 3.1 Entrepreneurship............................................................................................................................................................................................................................................... 6 3.2 ‘Second chance’ ................................................................................................................................................................................................................................................. 7 3.3 ‘Responsive administration’ ........................................................................................................................................................................................................................ 8 3.4 State aid & public procurement ............................................................................................................................................................................................................... 9 3.5 Access to finance........................................................................................................................................................................................................................................... 10 3.6 Single market .................................................................................................................................................................................................................................................. 11 3.7 Skills & innovation ........................................................................................................................................................................................................................................ 12 3.8 Environment ..................................................................................................................................................................................................................................................... 13 3.9 Internationalisation ...................................................................................................................................................................................................................................... 14

4. Interesting initiative ....................................................................................................................................................................................................................................... 15

1. SMEs — basic figures

Class size Number of enterprises Number of persons employed Value added

France EU-28 France EU-28 France EU-28

Number Share Share Number Share Share Billion € Share Share

Micro 2 858 954 95.1 % 92.8 % 4 477 703 29.5 % 29.5 % 238.3 26.1 % 21.2 %

Small 123 807 4.1 % 6.0 % 2 845 564 18.7 % 20.2 % 151.2 16.6 % 18.0 %

Medium-sized 19 755 0.7 % 1.0 % 2 255 982 14.8 % 17.0 % 138.3 15.1 % 18.2 %

SMEs 3 002 516 99.9 % 99.8 % 9 579 249 63.0 % 66.8 % 527.8 57.8 % 57.4 %

Large 4 457 0.1 % 0.2 % 5 613 950 37.0 % 33.2 % 385.5 42.2 % 42.6 %

Total 3 006 973 100.0 % 100.0 % 15 193 199 100.0 % 100.0 % 913.4 100.0 % 100.0 %

These are estimates for 2015 produced by DIW Econ, based on 2008-2013 figures from the Structural Business Statistics Database (Eurostat). The data cover the ‘non-financial business economy’, which includes industry, construction, trade, and services (NACE Rev. 2 sections B to J, L, M and N), but not enterprises in agriculture, forestry and fisheries and the largely non-market service sectors such as education and health. The advantage of using Eurostat data is that the statistics are harmonised and comparable across countries. The

disadvantage is that for some countries the data may be different from those published by national authorities.2

SMEs play a key role in ensuring jobs and growth in the French

as well as in the overall EU ‘non-financial business economy’.

Their share of added value equals the EU average of 58 % and

they account for 63 % of total employment in France. However,

SME labour productivity, calculated as the ratio of added value

to employment, is 27 % higher than the EU average, amounting

to approximately EUR 55 000 per person in 2015. Wholesale and

retail trade and manufacturing are the most important sectors

for SMEs, as in most Member States. In France, these sectors

account for a combined 40 % of total SME added value and

41 % of SME employment.

Between 2010 and 2015, SME added value increased by 4 %.

This is roughly equivalent to its growth in the ‘non-financial

business economy’ as a whole. Employment increased only in

micro firms however, by 2 %. This was favoured by the

introduction of a new business status in 2009, that of ‘auto-

entrepreneur’. It was widely adopted at first, but since the end of

2014 has fallen out of favour due to registration changes.3,4

Employment in small companies fell by 1 % and in medium-

sized companies by 4 %. Overall, SME employment stagnated.

As in most other Member States, SMEs in the manufacturing

sector in France perform worse than SMEs on average. Between

2010 and 2015, added value increased by 2 % and employment

dropped by 7 %. The automobile sector, consumer electronics

and other industry sectors were contributing factors in this

regard. Among other reasons, this is due to a lack of investment

in research and development and a general lack of funding.5

However, since 2012, government intervention — which includes

2016 SBA Fact Sheet — France 3

state support for low-paid workers and for the manufacturing of

high-value goods — along with the depreciation of the euro and

low energy costs, have all combined to result in improved

growth.6

Between 2010 and 2015, the added value of wholesale and

retail trade SMEs increased by 6 %. At the same time, added

value in large firms dropped by 5 %. Employment in this sector

nearly stagnated both in SMEs and in large firms. The increase in

SME added value is largely due to increased productivity as a

result of greater IT innovation, e.g. online trading, logistics and

network organisation. It is also the result of longer working hours

than in large established companies.7

Between February 2015 and January 2016 there were 529 338

business registrations. This is a fall of 3 % compared to the

previous period.8 The total number of bankruptcies in 2015 was

63 108, a 1 % increase compared to the previous year.9 There

was a marked difference between the number of bankruptcies in

micro-businesses, which rose by 2 %, and bankruptcies in small

and medium companies, which dropped by 6 %.10

The observed business demography dynamics are partly a

consequence of regulatory changes related to the ‘auto-

entrepreneur’ business status. This business-friendly initiative

was widely adopted after its introduction in 2009, but became

less popular when reforms in 2014 made registration more

complicated and introduced other requirements, such as

mandatory training.11 As a result, ‘micro-entrepreneur’

registrations fell by 20 % while other company registrations

increased.12 In 2015, only 42 % of all business registrations

were ‘micro-entrepreneur’ registrations, compared to more than

50 % in previous years.13

From 2016 onwards, the pace of the current moderate increase

in SME added value and SME employment is expected to

accelerate. Between 2015 and 2017, added value is forecast to

increase by 7 % and employment by 3 %. This corresponds to

the creation of 281 000 jobs in SMEs within two years.

2. SBA profile14

France’s SBA profile continues to be balanced, with performance

in most areas broadly in line with the EU average. Solid

framework conditions remain in place, in particular for SME

participation in public procurement. Opportunities provided by

the single market remain unseized however. Overall, progress

has been made in implementing the SBA since 2008.

French policy-makers have been paying more and more

attention to SME policy. Although France does not have a

specific strategy for implementing the SBA, progress has been

made in the implementation of most of the SBA principles. A

number of policy measures to improve the business environment

have been adopted. These include the ‘Bill for growth, activity

and equality of economic opportunities’ (Loi pour la croissance,

l’activité et l’égalité des chances économiques).

In 2015 and the first quarter of 2016, France implemented four

policy measures relating to 3 of the 10 SBA policy areas. There

is a broad consensus that the most significant progress was

made in Access to finance. The ‘Industry for the Future’

programme, the tax incentives to encourage companies to invest

and the incentives to recruit staff have benefited French SMEs.

Many measures aim to simplify administrative tasks for SMEs.

Most of them, adopted as part of the simplification programme,

have already been implemented. While SMEs welcome these

efforts, they also suffer the consequences of a constantly

changing legal environment. They would benefit from a more

stable legal environment, with fewer changes, prioritising those

that result in major simplifications, including at the level of state

agencies and at local and regional levels.

There is still lack of a comprehensive ‘SME test’ to assess the

impact of new legislation on businesses. Although regulatory

impact assessments have been mandatory for legislative texts

since 2008 and for decrees since 2011, they remain very

limited. SME stakeholders also say that they lack information on

the impact and the extent of the use of consultation findings.

2016 SBA Fact Sheet — France 4

The vocational training system does not meet the needs of SMEs

either. Trainees and apprentices are not yet sufficiently prepared

in terms of skills and understanding of the business

environment. The apprenticeship system is regarded as rather

inflexible in terms of the needs of start-ups and SMEs. The

significant administrative burdens attendant upon setting up

apprenticeship contracts continue to make it difficult to set up

new apprenticeships. However, the number of apprenticeship

contracts increased by 4.2 % in 2015 compared to 2014 and the

government recently reaffirmed its goal of reaching the target

of 500 000 apprentices by 2017. French employees can also

choose to train themselves, using their personal training account

(CPF — compte personnel de formation). 200 000 employees

were trained and more than 1 million accounts opened in 2015.

The government plans to integrate the CPF into the personal

activity account (CPA — compte personnel d’activité) to extend

the training programme to self-employed people and public

servants.

A number of administrative services exist to help SMEs expand

across national borders. However, the multiplicity of

administrative services and the general lack of coordination

among these services prevent SMEs from seizing opportunities

the single market and markets beyond the EU provide.

SBA performance of France: state of play and development from 2008 to 201615

2016 SBA Fact Sheet — France 5

3. SBA principles16

3.0 ‘Think Small First’ The ‘Think Small First’ principle is intended as a guiding principle

for all policy- and law-making activities. It requires policy-

makers to take SME interests into account at the early stages of

the policy-making process. The principle also calls for newly

designed legislation, administrative rules and procedures to be

made simple and easy to apply.

The government introduced numerous simplification measures.

The most important ones include the ‘Unique Social Statement’,

‘Remove a Standard Each Time You Create a New Standard’ and

‘Tell Us Once’, but it is too early to fully assess the long-term

effects of these measures. The aim of the ‘Tell Us Once’

measure is to reduce the number of times and the frequency

with which government departments ask businesses for

information. For example, the ‘simplified public tender’ procedure

(marché public simplifié) started in 2014. Thanks to a unique

identifier (SIRET number), introduced under the ‘Tell Us Once’

measure, less paperwork is required nowadays.

Since October 2014, all businesses can file their tax-related

reports online. This makes the process easier but does not

reduce the administrative burden. That could be done by

reducing the number of tax credits, tax rates and kinds of tax

relief. Instead of that, several different VAT rates and new taxes

were recently introduced.

There is still lack of a comprehensive ‘SME test’ to assess the

impact of new legislation on businesses. Although regulatory

impact assessments have been mandatory for legislative texts

since 2008 and for decrees since 2011, they remain very

limited. Given the high number of legislative texts and decrees, a

surprisingly low number of ‘SME panels’ have been conducted so

far. ‘SME panels’ complement impact assessments with more

detailed information on SMEs obtained directly from the SMEs in

question.

There is a feeling among the SME community that greater

consultation and transparency is needed on SME-related bills.

SME stakeholders are mainly consulted at the initial drafting

stage, but they would like to be consulted at the later stages of

the legislative process too, especially on modifications, which are

sometimes very significant. They also lament the lack of

information on the impact and the extent of the use of

consultation findings.

The SME envoy was less visible than during the previous

reporting period because the ‘Assises des PME’ in 2014 and the

preparation of the SME envoy meeting in Paris in 2015

generated more activity than usual. The SME envoy supported

the Commission start-ups consultation by preparing an online

tool for contributions to the consultation. The SME envoy is

directly attached to the relevant minister. This high-level position

helps to incorporate SME concerns into public policies.

SME stakeholders welcome the simplification measures, but they

suffer the consequences of a constantly changing legal

environment. It is crucial for them to have a more stable legal

environment, with fewer changes, prioritising those that result in

major simplifications, including at the level of state agencies and

at local and regional levels.

2016 SBA Fact Sheet — France 6

3.1 Entrepreneurship

France performs broadly in line with the EU average in this area,

although individual indicators vary considerably. For example,

while entrepreneurship education at basic school level is among

the 10 lowest-scoring in the EU, it is among the 10 highest-

scoring performers at post-secondary level. However, it needs to

do more to improve cooperation between educational institutions

and private sector. France is also among the lowest-scoring

performers in the EU on early-stage entrepreneurial activity and

the established business ownership rate (i.e. the proportion of

the population that owns an operating business). On the other

hand, opportunity-driven entrepreneurial activity (as opposed to

not finding another option for work) was the highest in the EU.

Since 2008, a number of policy measures have been

implemented to promote entrepreneurial activity. The status of

‘auto-entrepreneur’ was introduced, simplifying administrative

tasks. The New Programme of Support for Starting or Taking

Over a Company (Nouvel Accompagnement à la Création et à la

Reprise d’Entreprise) was set up, supporting unemployed people

willing to start or take over a company. That status of ‘private

entrepreneur with limited responsibility’ (EIRL - entrepreneur

individuel à responsabilité limitée) was introduced. This allows

individual entrepreneurs to distinguish between their personal

assets and their business assets. Various action plans were also

put in place, such as the female entrepreneurship action plan.

However, the PINEL law, adopted in June 2014, has increased

the administrative and financial burden for those with ‘auto-

entrepreneur’ status. In 2015 compared to 2014, the number of

new ‘auto-entrepreneur’ status registrations decreased by one

fifth. This was the first such decrease since ‘auto-entrepreneur’

status was introduced in 2009. With its draft law on

transparency, the fight against corruption and modernising the

economy, the government intends to address some of the issues

outlined above. The measures are intended to simplify the

obligation of micro-entrepreneurs to have a double bank account

and the mandatory training (depending on the level of

experience) and qualification required (depending on the sector

in question) for some micro-entrepreneurs.

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Entrepreneurship education at post-secondary levels (1-5); 2014; France:2.92; EU avg: 2.78

Entrepreneurship education at basic school (1-5) ; 2014; France: 1.75; EUavg: 2.09

Media attention given to entrepreneurship (%); 2014; France: 38.98; EUavg: 53.3

High status given to successful entrepreneurship (%); 2014; France: 70.43;EU avg: 66.6

Entrepreneurship as a desirable career choice (%); 2014; France: 59.05;EU avg: 56.9

Degree to which school education helped develop an entrepreneurialattitude; 2012; France: 50; EU avg: 50

Entrepreneurial intentions (percentage of adults who intend to start abusiness within 3 years); 2014; France: 14.2; EU avg: 12.1

Opportunity-driven entrepreneurial activity (%); 2014; France: 69.15; EUavg: 47.9

Established business ownership rate (%); 2014; France: 2.94; EU avg: 6.7

Early stage entrepreneurial activity for female population (%); 2014; France:4.03; EU avg: 5.45

Early stage entrepreneurial activity (%); 2014; France: 5.34; EU avg: 7.8

Note: Data bars pointing right show better performance than the EU average and data bars pointing left show weaker performance.

Variation from the EU average (measured in standard deviations, EU average=0)

2016 SBA Fact Sheet — France 7

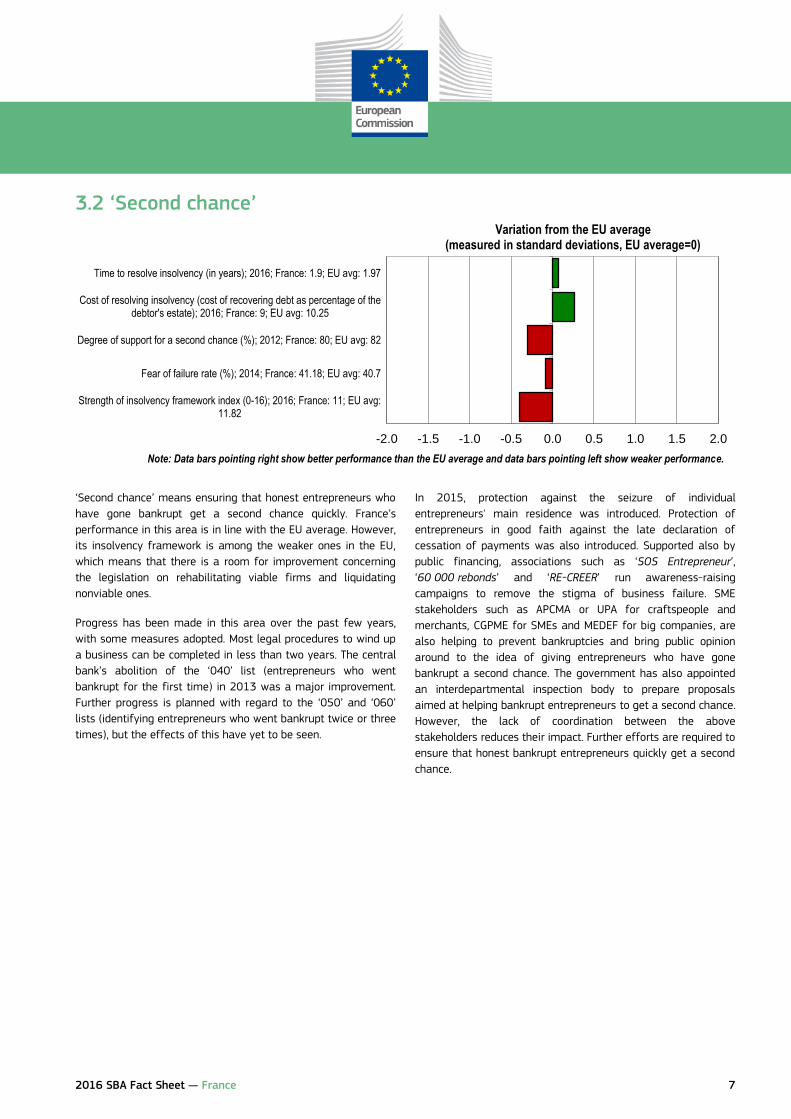

3.2 ‘Second chance’

‘Second chance’ means ensuring that honest entrepreneurs who

have gone bankrupt get a second chance quickly. France’s

performance in this area is in line with the EU average. However,

its insolvency framework is among the weaker ones in the EU,

which means that there is a room for improvement concerning

the legislation on rehabilitating viable firms and liquidating

nonviable ones.

Progress has been made in this area over the past few years,

with some measures adopted. Most legal procedures to wind up

a business can be completed in less than two years. The central

bank’s abolition of the ‘040’ list (entrepreneurs who went

bankrupt for the first time) in 2013 was a major improvement.

Further progress is planned with regard to the ‘050’ and ‘060’

lists (identifying entrepreneurs who went bankrupt twice or three

times), but the effects of this have yet to be seen.

In 2015, protection against the seizure of individual

entrepreneurs' main residence was introduced. Protection of

entrepreneurs in good faith against the late declaration of

cessation of payments was also introduced. Supported also by

public financing, associations such as ‘SOS Entrepreneur’,

‘60 000 rebonds’ and ‘RE-CREER’ run awareness-raising

campaigns to remove the stigma of business failure. SME

stakeholders such as APCMA or UPA for craftspeople and

merchants, CGPME for SMEs and MEDEF for big companies, are

also helping to prevent bankruptcies and bring public opinion

around to the idea of giving entrepreneurs who have gone

bankrupt a second chance. The government has also appointed

an interdepartmental inspection body to prepare proposals

aimed at helping bankrupt entrepreneurs to get a second chance.

However, the lack of coordination between the above

stakeholders reduces their impact. Further efforts are required to

ensure that honest bankrupt entrepreneurs quickly get a second

chance.

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Strength of insolvency framework index (0-16); 2016; France: 11; EU avg:11.82

Fear of failure rate (%); 2014; France: 41.18; EU avg: 40.7

Degree of support for a second chance (%); 2012; France: 80; EU avg: 82

Cost of resolving insolvency (cost of recovering debt as percentage of thedebtor's estate); 2016; France: 9; EU avg: 10.25

Time to resolve insolvency (in years); 2016; France: 1.9; EU avg: 1.97

Note: Data bars pointing right show better performance than the EU average and data bars pointing left show weaker performance.

Variation from the EU average (measured in standard deviations, EU average=0)

2016 SBA Fact Sheet — France 8

3.3 ‘Responsive administration’

‘Responsive administration’ means public administration being

responsive to the needs of SMEs. France continues to be broadly

in line with the EU average in this area. However, fast-changing

legislation and policies made doing business difficult for 89 % of

French respondents in 2015. This figure is the second highest in

the EU and only one percentage point less than in 2013. The

2015 figure for the complexity of administrative procedures

making it hard to do business is also 89 %, 6 percentage points

worse than the 2013 figure of 83 %. The time it takes to

transfer property is more than double the EU average. On the

positive side, the score for the burden of government

regulations, which remains below the EU average, has continued

to improve slowly but steadily since 2008. The people working

for French government agencies are regarded as competent and

effective in supporting new and growing companies. Proof of this

is that France is among the best four performers in the EU on

this indicator.

Overall, a progress has been made in this area since 2008. It has

been made possible to register a business using an online

platform. Among other important measures is the ‘silence is

consent’ principle, being introduced gradually. The government

has also unveiled an ambitious plan to rewrite the labour code.

During 2015 and the first quarter of 2016, about 140 measures

were created to simplify administrative tasks for SMEs. However,

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Competency and effectiveness of government staff in supporting new andgrowing firms (1-5); 2014; France: 3.33; EU avg: 2.7

Burden of government regulations (1=burdensome, 7=not burdensome); 2015;France: 2.92; EU avg: 3.24

Start-up procedures (number); 2016; France: 5; EU avg: 4.93

Licenses and permit systems (1=lowest level of complexity, 26=highest level ofcomplexity); 2011; France: 13; EU avg: 15.77

SMEs interacting online with public authorities (%); 2013; France: 95.57; EUavg: 87.85

The complexity of administrative procedures is a problem for doing business(percentage of respondents who agree); 2015; France: 89; EU avg: 62

Fast-changing legislation and policies are a problem for doing business(percentage of respondents who agree); 2015; France: 89; EU avg: 64

Cost of enforcing contracts (percentage of claim); 2016; France: 17.4; EU avg:21.88

Time it takes to pay taxes (hours per year); 2016; France: 137; EU avg: 185.55

Number of tax payments per year; 2016; France: 8; EU avg: 10.89

Cost required to transfer property (percentage of property value); 2016; France:6.1; EU avg: 4.46

Time required to transfer property (in calendar days); 2016; France: 49; EU avg:23.04

Paid-in minimum capital (percentage of income per capita); 2016; France: 0; EUavg: 10.66

Cost of starting a business (in euros); 2015; France: 84; EU avg: 315.74

Time to start a business (in calendar days); 2015; France: 4; EU avg: 3.35

Note: Data bars pointing right show better performance than the EU average and data bars pointing left show weaker performance.

Variation from the EU average (measured in standard deviations, EU average=0)

2016 SBA Fact Sheet — France 9

despite the simplification programme and the measures

designed to smoothen the impact of the size-related criteria in

regulations that impede companies’ growth, regulatory burden

continues to be an important area of concern for French

companies.

Most of the measures adopted in the context of the

simplification programme have been implemented, but efforts

need to be pursued. Remaining barriers that recent or ongoing

reforms do not sufficiently address, in particular regarding

business services and regulated professions, need to be

removed.

3.4 State aid & public procurement

France’s performance in this area continues to be above the EU

average. It is among the seven best performers in the EU. It has

the second highest percentage of businesses participating in

public tenders, with even greater participation in 2015 (54 %)

than in 2013 (50 %).

Overall, progress has been made in this area since 2008. One of

the most significant policy measures has been the modification

of the rules on procurement, to allow more SMEs, especially

those recently set up, participate in public tenders. Since the

simplified procurement procedure was introduced in 2014, about

20 000 simplified procurement procedures have been carried

out.

Several ombudsmen have been appointed, including one for

subcontractors to improve their relationship with large

companies and spread good practices across public services in

order to increase SME participation in public procurement.

Despite the ombudsmen’s efforts, many companies, in particular

subcontractors, are still paid late.

No significant new policy measures related to public

procurement were implemented or announced during 2015 and

the first quarter of 2016.

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Percentage of businesses submitting proposals in a public electronic tendersystem (e-procurement) (%); 2013; France: 18.61; EU avg: 12.85

Average delay in payments from public authorities (in days); 2015; France:19; EU avg: 12.58

Percentage of businesses participating in public tenders (%); 2015; France:54; EU avg: 37

Percentage SMEs account for in the total value of public contracts awarded(%); 2013; France: 31; EU avg: 29

Note: Data bars pointing right show better performance than the EU average and data bars pointing left show weaker performance.

Variation from the EU average (measured in standard deviations, EU average=0)

2016 SBA Fact Sheet — France 10

3.5 Access to finance

France performs in line with the EU average in this area. Access

to public financial support including guarantees, measured by

the percentage of French respondents that indicated a

deterioration, significantly improved in 2015 compared to 2014.

This happened across the EU however, keeping France below the

EU average on this indicator. The willingness of banks to provide

a loan, measured by the percentage of respondents that

indicated a deterioration, has continued to gradually increase

over the last four years. The situation also improved with regard

to the percentage of rejected loan applications and unacceptable

loan offers, which fell from 13.6 % in 2013 to 10.8 % in 2015.

However, the cost of small loans compared to large loans has

been increasing since 2013, when small loans were 15 % more

expensive than large loans. In 2015 they were nearly 24 % more

expensive than large loans of over EUR 1 million.

Since 2008, a considerable number of funding measures have

been implemented. These include the recovery plan of

2008/2009 and reinforcement of the lending capacity of the

public investment bank ‘Bpifrance’. The creation of a large

national loan of EUR 47 billion, ‘Investment for the Future’, was

an important step towards modernising the French industrial

base and making companies, especially SMEs, more competitive.

The competitiveness and employment tax credit (CICE — Crédit

d’impôt pour la compétitivité et l’emploi), was introduced in

2013, reducing labour costs for SMEs. Ombudsmen help

subcontractors who get into financial difficulties due to late

payments from large companies. However, despite the progress

made, it is still difficult to access finance without the support of

the public investment bank ‘Bpifrance’.

During 2015 and the first quarter of 2016, a number of

additional measures were implemented:

− In April 2015, an exceptional time-limited tax incentive was

introduced to encourage companies to invest during a one-

year period (initially until April 2016, prolonged until April

2017), enabling them to amortise their eligible investments

for up to 140 % of their face value. Prolonging this

measure is a great help for SMEs, since it takes them more

time to initiate larger investments.

− The aim of the ‘Industry for the Future’ policy framework is

to modernise the industrial base and turn traditional

business models into disruptive ones. Under this measure,

adopted in May 2015, targeted loans totalling

EUR 2.2 billion and tax incentives of EUR 5 billion over 6

years are envisaged in order to accelerate the digital

transition of SMEs. The nine industrial solutions address

issues such as green mobility, the internet of things and

future medicine with set objectives and roadmaps.

− In January 2016, the government put in place financial

support, corresponding to the amount of the social charges

the employer pays annually on the minimum wage, for

SMEs recruiting unemployed people. This financial support,

provided as a cash refund on the basis of the employer’s

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Business angels funding for new and growing firms (1-5); 2014; France: 2.75;EU avg: 2.67

Equity funding for new and growing firms (1-5); 2014; France: 2.7; EU avg: 2.73

Willingness of banks to provide a loan (percentage of respondents that indicateda deterioration); 2015; France: 19.86; EU avg: 13.01

Access to public financial support including guarantees (percentage ofrespondents that indicated a deterioration); 2015; France: 21.03; EU avg: 13.76

Rejected loan applications and unacceptable loan offers (percentage of loanapplications by SMEs); 2015; France: 10.82; EU avg: 9.64

Cost of borrowing for small loans relative to large loans (%); 2015; France:23.68; EU avg: 25.22

Bad debt loss (percentage of total turnover); 2015; France: 1.8; EU avg: 3.76

Total amount of time it takes to get paid (days); 2015; France: 48.67; EU avg:34.96

Strength of legal rights index (0-12); 2016; France: 4; EU avg: 5.75

Venture capital investments (percentage of GDP); 2014; France: 0.04; EU avg:0.03

Note: Data bars pointing right show better performance than the EU average and data bars pointing left show weaker performance.

Variation from the EU average (measured in standard deviations, EU average=0)

2016 SBA Fact Sheet — France 11

declaration, is available in 2016, for the two first years of

an employee’s contract. SMEs must apply for this tax credit.

The government also announced that in 2017 it would consider

making the attractive competitiveness and employment tax

credit (whose resulting reduction of labour costs is estimated to

be EUR 13 billion in 2016) permanent. This would make it less

complicated to implement.

3.6 Single market

France’s performance in this area is below the EU average.

Despite significant improvement since 2008, its score is the fifth

lowest in the EU. The number of pending infringement

proceedings is among the four highest in the EU. It has yet to

seize significant single market opportunities, such as in exporting

goods to other EU countries. Namely, the percentage of other

Member States’ SMEs exporting within the EU (17.3 %) was

more than double that of French SMEs (7.8 %).

A number of administrative services exist to help SMEs expand

across national borders. However, the multiplicity of

administrative services and the general lack of coordination

among these services result in suboptimal supporting

environment. The support system is thus complex, which means

that it is harder for SMEs than for large companies to do cross-

border business.

No significant new single market policy measures were

implemented in 2015 and the first quarter of 2016.

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Market access for new and growing firms without being unfairly blocked byestablished firms (1-5); 2014; France: 2.23; EU avg: 2.78

Easy market access for new and growing firms (1-5); 2014; France: 3.32;EU avg: 2.78

Intra-EU online exporters (% of SMEs); 2015; France: 7.94; EU avg: 7.52

SMEs with intra-EU imports of goods (percentage of SMEs in industry);2013; France: 4.67; EU avg: 25.95

SMEs with intra-EU exports of goods (percentage of SMEs in industry);2013; France: 7.81; EU avg: 17.3

Public contracts secured abroad by SMEs (percentage of total value ofpublic contracts); 2013; France: 1; EU avg: 2.6

Number of pending infringement proceedings; 2015; France: 51; EU avg: 27

Average transposition delay for overdue directives (in months); 2015;France: 8.6; EU avg: 7.46

Note: Data bars pointing right show better performance than the EU average and data bars pointing left show weaker performance.

Variation from the EU average (measured in standard deviations, EU average=0)

2016 SBA Fact Sheet — France 12

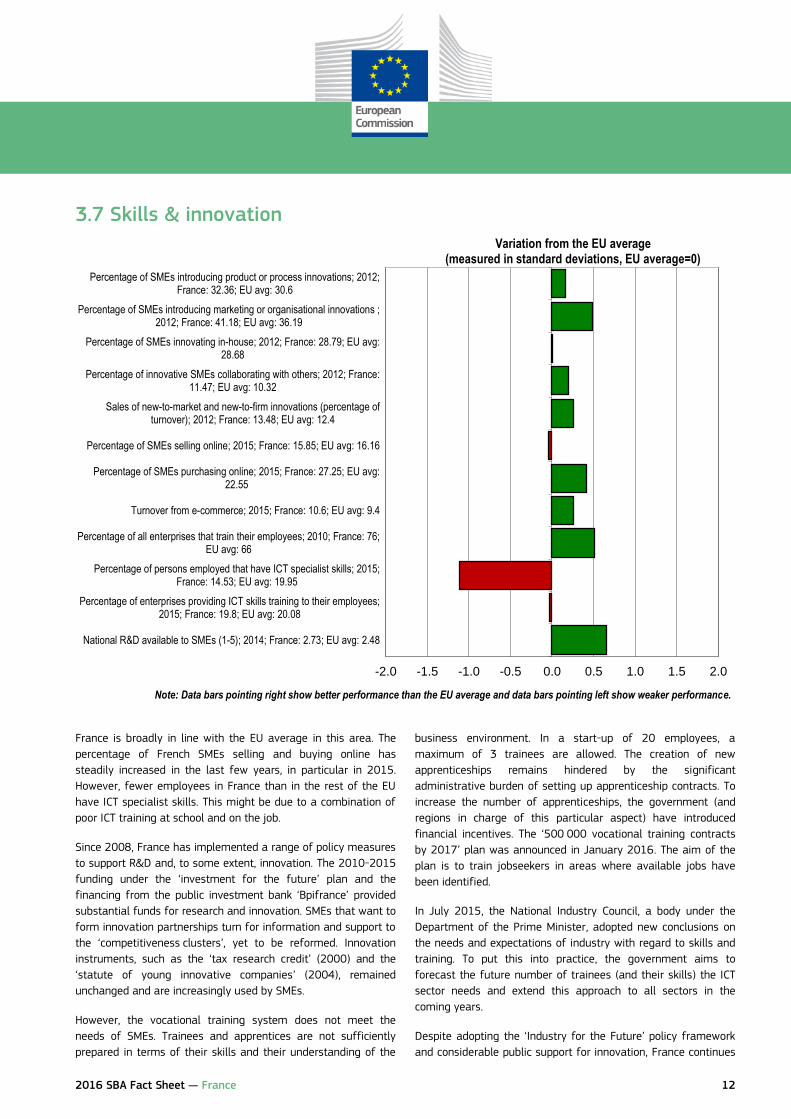

3.7 Skills & innovation

France is broadly in line with the EU average in this area. The

percentage of French SMEs selling and buying online has

steadily increased in the last few years, in particular in 2015.

However, fewer employees in France than in the rest of the EU

have ICT specialist skills. This might be due to a combination of

poor ICT training at school and on the job.

Since 2008, France has implemented a range of policy measures

to support R&D and, to some extent, innovation. The 2010-2015

funding under the ‘investment for the future’ plan and the

financing from the public investment bank ‘Bpifrance’ provided

substantial funds for research and innovation. SMEs that want to

form innovation partnerships turn for information and support to

the ‘competitiveness clusters’, yet to be reformed. Innovation

instruments, such as the ‘tax research credit’ (2000) and the

‘statute of young innovative companies’ (2004), remained

unchanged and are increasingly used by SMEs.

However, the vocational training system does not meet the

needs of SMEs. Trainees and apprentices are not sufficiently

prepared in terms of their skills and their understanding of the

business environment. In a start-up of 20 employees, a

maximum of 3 trainees are allowed. The creation of new

apprenticeships remains hindered by the significant

administrative burden of setting up apprenticeship contracts. To

increase the number of apprenticeships, the government (and

regions in charge of this particular aspect) have introduced

financial incentives. The ‘500 000 vocational training contracts

by 2017’ plan was announced in January 2016. The aim of the

plan is to train jobseekers in areas where available jobs have

been identified.

In July 2015, the National Industry Council, a body under the

Department of the Prime Minister, adopted new conclusions on

the needs and expectations of industry with regard to skills and

training. To put this into practice, the government aims to

forecast the future number of trainees (and their skills) the ICT

sector needs and extend this approach to all sectors in the

coming years.

Despite adopting the ‘Industry for the Future’ policy framework

and considerable public support for innovation, France continues

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

National R&D available to SMEs (1-5); 2014; France: 2.73; EU avg: 2.48

Percentage of enterprises providing ICT skills training to their employees;2015; France: 19.8; EU avg: 20.08

Percentage of persons employed that have ICT specialist skills; 2015;France: 14.53; EU avg: 19.95

Percentage of all enterprises that train their employees; 2010; France: 76;EU avg: 66

Turnover from e-commerce; 2015; France: 10.6; EU avg: 9.4

Percentage of SMEs purchasing online; 2015; France: 27.25; EU avg:22.55

Percentage of SMEs selling online; 2015; France: 15.85; EU avg: 16.16

Sales of new-to-market and new-to-firm innovations (percentage ofturnover); 2012; France: 13.48; EU avg: 12.4

Percentage of innovative SMEs collaborating with others; 2012; France:11.47; EU avg: 10.32

Percentage of SMEs innovating in-house; 2012; France: 28.79; EU avg:28.68

Percentage of SMEs introducing marketing or organisational innovations ;2012; France: 41.18; EU avg: 36.19

Percentage of SMEs introducing product or process innovations; 2012;France: 32.36; EU avg: 30.6

Note: Data bars pointing right show better performance than the EU average and data bars pointing left show weaker performance.

Variation from the EU average (measured in standard deviations, EU average=0)

2016 SBA Fact Sheet — France 13

to lag behind the innovation leaders. The proliferation and

instability of innovation policy schemes raise concerns in terms

of their overall coordination, consistency and efficiency. This

particularly affects SMEs.17

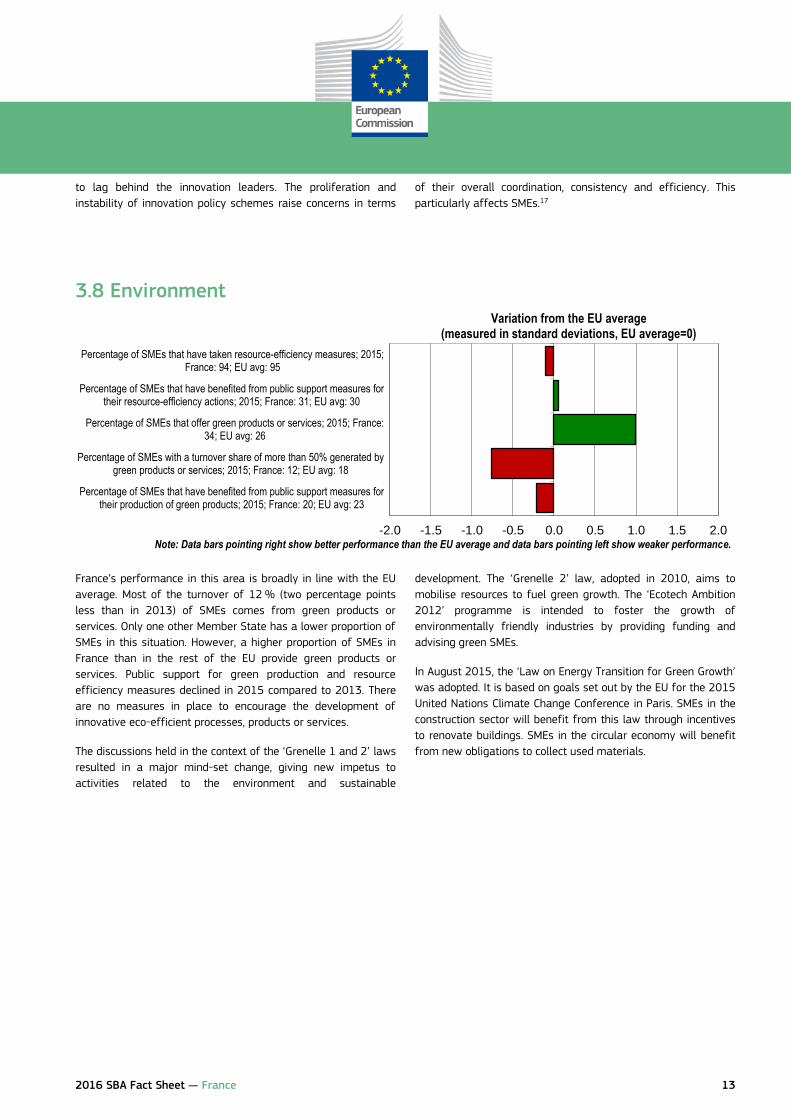

3.8 Environment

France’s performance in this area is broadly in line with the EU

average. Most of the turnover of 12 % (two percentage points

less than in 2013) of SMEs comes from green products or

services. Only one other Member State has a lower proportion of

SMEs in this situation. However, a higher proportion of SMEs in

France than in the rest of the EU provide green products or

services. Public support for green production and resource

efficiency measures declined in 2015 compared to 2013. There

are no measures in place to encourage the development of

innovative eco-efficient processes, products or services.

The discussions held in the context of the ‘Grenelle 1 and 2’ laws

resulted in a major mind-set change, giving new impetus to

activities related to the environment and sustainable

development. The ‘Grenelle 2’ law, adopted in 2010, aims to

mobilise resources to fuel green growth. The ‘Ecotech Ambition

2012’ programme is intended to foster the growth of

environmentally friendly industries by providing funding and

advising green SMEs.

In August 2015, the ‘Law on Energy Transition for Green Growth’

was adopted. It is based on goals set out by the EU for the 2015

United Nations Climate Change Conference in Paris. SMEs in the

construction sector will benefit from this law through incentives

to renovate buildings. SMEs in the circular economy will benefit

from new obligations to collect used materials.

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Percentage of SMEs that have benefited from public support measures fortheir production of green products; 2015; France: 20; EU avg: 23

Percentage of SMEs with a turnover share of more than 50% generated bygreen products or services; 2015; France: 12; EU avg: 18

Percentage of SMEs that offer green products or services; 2015; France:34; EU avg: 26

Percentage of SMEs that have benefited from public support measures fortheir resource-efficiency actions; 2015; France: 31; EU avg: 30

Percentage of SMEs that have taken resource-efficiency measures; 2015;France: 94; EU avg: 95

Note: Data bars pointing right show better performance than the EU average and data bars pointing left show weaker performance.

Variation from the EU average (measured in standard deviations, EU average=0)

2016 SBA Fact Sheet — France 14

3.9 Internationalisation

France’s performance in this area is broadly in line with the EU

average. Since 2008, UBIFRANCE, the main French agency for

export promotion, has been strengthened with additional means

to support 10 000 companies (2009), the merger with similar

services located abroad from the Ministry of the Economy

(2011), and the merger with the French Agency for International

Investment into the ‘Business France’ agency (2015). These

measures helped increase the number of exporting companies

for the fourth consecutive year, with 4 000 additional exporting

companies in 2015.18 However, the overall number of companies

exporting to foreign markets remains relatively low, at 125 000

in 2015.

For years now, SME stakeholders have been voicing their

concerns about the multiplicity of operators helping companies

to expand across national borders. This considerably weakens

the capacity of SMEs to seek support for internationalisation.

The lack of fluency in foreign languages also prevents SMEs

from expanding across national borders.

During 2015 and the first quarter of 2016, no significant new

policy measures were adopted or announced.

-2.0 -1.5 -1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Cost to import for documentary compliance (in USD); 2016; France: 0; EUavg: 6.61

Time to import for documentary compliance (in hours); 2016; France: 1; EUavg: 1.07

Cost to export for documentary compliance (in USD); 2016; France: 0; EUavg: 16.43

Time to export for documentary compliance (in hours); 2016; France: 1; EUavg: 1.39

SMEs with extra-EU imports of goods (percentage of SMEs in industry);2013; France: 7.5; EU avg: 11.08

SMEs with extra-EU exports of goods (percentage of SMEs in industry);2013; France: 8.87; EU avg: 9.95

Note: Data bars pointing right show better performance than the EU average and data bars pointing left show weaker performance.

Variation from the EU average (measured in standard deviations, EU average=0)

2016 SBA Fact Sheet — France 15

4. Interesting initiative

Below is an example of an initiative from France to show what governments can do to support SMEs:

The ‘Industry for the Future’ framework – modernising the French industrial base

The aim of the ‘Industry for the Future’ policy framework is to modernise the industrial base and turn traditional business models into

disruptive ones.

Launched in May 2015, it is a cross-cutting programme that revolves around the corresponding nine industrial solutions. It is based

on the following five principles:

- expanding the French technological offer

- supporting businesses throughout the transformation phase

- providing staff training

- supporting international cooperation on standards

- promoting French ‘Industry for the Future’.

In 2015, over 500 industrial SMEs benefited from individual assessments (1500 in 2016). The nine plans, with set multiannual

roadmaps and objectives, focus on production methods (making them more efficient, using new resources and integrating them into

the circular economy), making cities green, green mobility, future transportation, future medicine, big data, the internet of things, safe

internet use and future food products.

Targeted loans totalling EUR 2.2 billion and tax incentives of EUR 5 billion over 6 years are envisaged to boost the digital transition of

SMEs as part of the drive to modernise the French industrial base.

References:

http://www.economie.gouv.fr/nouvelle-france-industrielle/accueil

http://www.economie.gouv.fr/vous-orienter/industrie/nouvelle-france-industrielle

http://www.economie.gouv.fr/files/files/PDF/industrie-du-futur_dp.pdf

http://www.localtis.info/cs/ContentServer?pagename=Localtis/LOCActu/ArticleActualite&cid=1250270068524

2016 SBA Fact Sheet — France 16

Important remarks

The European Commission Directorate-General for Internal Market, Industry, Entrepreneurship and SMEs (DG GROW) produces the

SBA fact sheets as part of the SME Performance Review (SPR), its main vehicle for economic analysis of SME issues. They

combine the latest available statistical and policy information. Produced annually, the fact sheets help to organise the available

information to facilitate SME policy assessments and monitor SBA implementation. They take stock and record progress. They are

not an assessment of Member State policies. Rather, they should be regarded as an additional source of information to improve

evidence-based policy-making. For example, they cite only policy measures national SME policy experts consider relevant. They do

not and cannot reflect all measures the government has taken over the reference period. There is more policy information on a

database accessible from the SPR website.

SME Performance Review:

http://ec.europa.eu/growth/smes/business-friendly-environment/performance-review/index_en.htm

Small Business Act:

http://ec.europa.eu/growth/smes/business-friendly-environment/small-business-act/index_en.htm

European Small Business Portal:

http://ec.europa.eu/small-business/index_en.htm

Endnotes

1 The two graphs below present the trend over time for the variables. They consist of index values for the years since 2008, with the base year 2008 set at a value of 100. As from 2014, the graphs show estimates of the development over time, produced by DIW Econ on the basis of 2008-2013 figures from Eurostat’s Structural Business Statistics Database. The data cover the ‘non-financial business economy’, which includes industry, construction, trade and services (NACE Rev. 2 sections B to J, L, M and N). They do not cover enterprises in agriculture, forestry and fisheries or largely non-market service sectors such as education and health. A detailed methodology can be consulted at: http://ec.europa.eu/growth/smes/business-friendly-environment/performance-review/index_en.htm

2 These statistics use the Eurostat definition of a company, which focuses on the ‘legal entity’. This differs from France’s definition, which uses the concept of ‘economic groups’. Differences between statistics provided by France’s National Institute for Statistics and Economic Studies (INSEE) and the data above are due to the different concepts.

3 http://www.insee.fr/fr/themes/info-rapide.asp?id=41&date=20160212; last accessed 24.03.2016.

4 Law of 18 June 2014, called the Pinel law; http://www.economie.gouv.fr/chronique-projet-de-loi-artisanat-au-commerce-et-tres-petites-entreprises; last accessed 24.03.2016.

5 http://www.lefigaro.fr/assets/pdf/Rapport-LG.pdf; last accessed 24.03.2016.

6 http://lekiosque.finances.gouv.fr/fichiers/Etudes/Thematiques/A2015.pdf; last accessed 24.03.2016.

7 http://www.insee.fr/fr/ffc/docs_ffc/ENTFRA13.pdf (pp. 29 & 146); last accessed 24.03.2016.

8 http://www.insee.fr/fr/themes/info-rapide.asp?id=41&date=20160212; last accessed 24.03.2016.

9 https://www.banque-france.fr/economie-et-statistiques/stats-info/detail/defaillances-dentreprises.html; last accessed 24.03.2016.

10 https://www.banque-france.fr/economie-et-statistiques/stats-info/detail/defaillances-dentreprises.html; last accessed 24.03.2016.

2016 SBA Fact Sheet — France 17

11 Law of 18 June 2014, called the Pinel law; http://www.economie.gouv.fr/chronique-projet-de-loi-artisanat-au-commerce-et-tres-petites-entreprises; last accessed 24.03.2016.

12 http://www.insee.fr/fr/themes/info-rapide.asp?id=41&date=20160212; last accessed 24.03.2016.

13 http://www.insee.fr/fr/themes/info-rapide.asp?id=41&date=20160212; last accessed 24.03.2016.

14 The 2016 SBA fact sheets benefited substantially from input from the European Commission’s Joint Research Centre (JRC) in Ispra, Italy. The JRC made major improvements to the methodological approach, statistical work on the dataset and the visual presentation of the data.

15 The quadrant chart combines two sets of information. Firstly, it shows current performance based on data for the latest available years. This information is plotted along the X-axis, measured in standard deviations of the simple, non-weighted arithmetical average for the EU-28. Secondly, it shows progress over time, i.e. the average annual growth rates from 2008 to 2016. These are measured against the individual indicators which make up the SBA area averages. This means that the location of a particular SBA area average in any of the four quadrants provides information not only about where the country is located in this SBA area relative to the EU average at a given point in time, but also about the extent of progress made between 2008 and 2016. All SBA principles, with the exception of the ‘Think Small First’ principle, for which there is not enough statistical data available, are calculated as composite indicators following the OECD/JRC Handbook guide. A detailed methodology can be consulted at: http://ec.europa.eu/growth/smes/business-friendly-environment/performance-review/index_en.htm

16 The policy measures presented in this SBA fact sheet are only a selection of the measures the government took in 2015 and the first quarter of 2016. The national SME policy expert that CARSA Spain (DG GROW’s lead contractor for the 2016 SBA fact sheets) contracted made the selection. The experts were asked to select only the measures they considered the most important, i.e. the ones expected to have the highest impact in the SBA area in question. The complete range of measures the experts compiled in producing this year’s fact sheets will be published alongside the fact sheets in a policy database on the DG GROW website.

17 http://ec.europa.eu/europe2020/pdf/csr2016/cr2016_france_en.pdf

18 http://www.ambafrance-de.org/La-France-dans-les-echanges-internationaux-Presentation-des-chiffres-2015-du