Embed Size (px)

Citation preview

© 2016 Baker & McKenzie

2016 Luxury & Fashion Industry Conference for Multinationals - Singapore

23 February 2016 | 9:00 am – 1:00 pm |

The St. Regis Singapore

© 2016 Baker & McKenzie

2016 Luxury & Fashion Industry Conference for Multinationals - Singapore

Supply Chain Issues in

ASEAN / TPP / FTA

Eugene Lim, Baker & McKenzie.Wong & Leow

Jaclyn Ho, Baker & McKenzie.Wong & Leow

Supply chain issues in

ASEAN

© 2016 Baker & McKenzie

Optimising the Supply Chain

Integral part of businesses

Competition is driving businesses to be more efficient in their supply

chain operations

Custom duties and indirect tax savings are

low hanging fruits to achieve such cost

savings

© 2016 Baker & McKenzie

From Catwalk to Customer

Design Manufacture and source

Transport and logistics

Warehouse operations

Distribute / Sell

© 2016 Baker & McKenzie

Supply Chain - Basic Building Blocks

1. Customs duties 2. Excise duties 3. Indirect taxes

4. Permanent establishment

5. Transfer pricing 6. Incoterms

© 2016 Baker & McKenzie

Regional Distribution Company

Regional Distribution

Company

Headquarters / IP

Company

(e.g., U.S., Europe)

Manufacturers

(e.g., Europe, China,

ASEAN)

Suppliers

(e.g., various locations)

Distributors / Retail

stores

(e.g., various Asia

Pacific locations)

Customers

(e.g., various Asia

Pacific locations)

IP License

Finished

goods

Raw

materials

Finished

goods Raw

materials

Finished

goods

© 2016 Baker & McKenzie

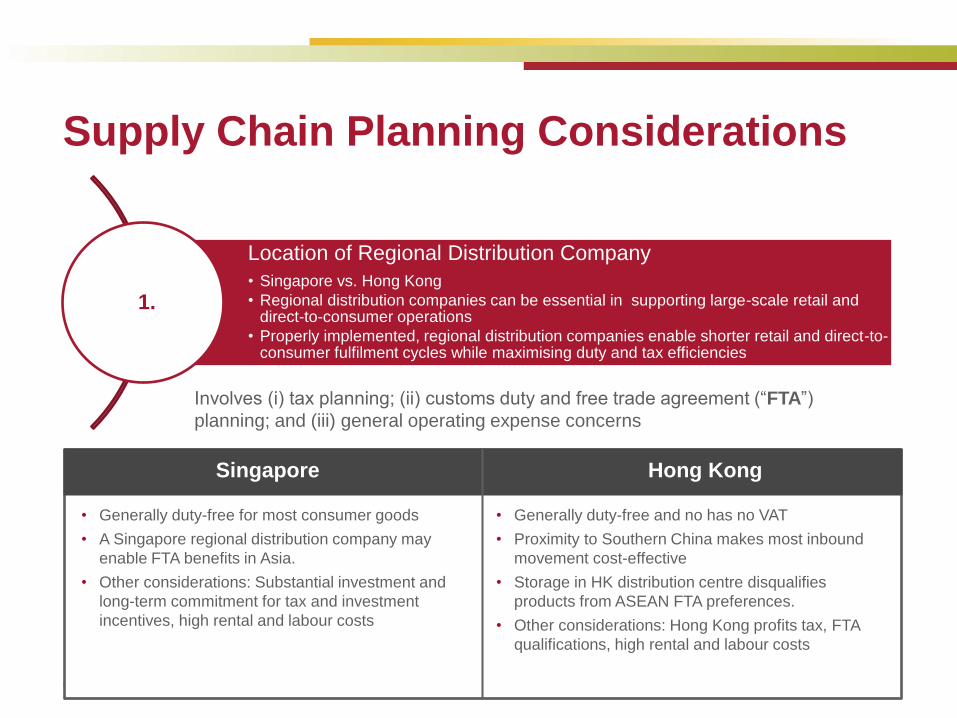

Supply Chain Planning Considerations

Location of Regional Distribution Company

• Singapore vs. Hong Kong

• Regional distribution companies can be essential in supporting large-scale retail and direct-to-consumer operations

• Properly implemented, regional distribution companies enable shorter retail and direct-to-consumer fulfilment cycles while maximising duty and tax efficiencies

1.

Singapore Hong Kong

• Generally duty-free for most consumer goods

• A Singapore regional distribution company may

enable FTA benefits in Asia.

• Other considerations: Substantial investment and

long-term commitment for tax and investment

incentives, high rental and labour costs

• Generally duty-free and no has no VAT

• Proximity to Southern China makes most inbound

movement cost-effective

• Storage in HK distribution centre disqualifies

products from ASEAN FTA preferences.

• Other considerations: Hong Kong profits tax, FTA

qualifications, high rental and labour costs

Involves (i) tax planning; (ii) customs duty and free trade agreement (“FTA”)

planning; and (iii) general operating expense concerns

© 2016 Baker & McKenzie

Supply Chain Planning Considerations

Transfer Pricing

• Principle guiding transactions between associated entities is that the transactions must be at arm’s length.

• Generally, profits follow ownership of functions, assets and risks

Customs and Duties

• Interaction between Asean Economic Community (“AEC”), Trans Pacific Partnership Agreement (“TPP”) and FTAs

• Bonded contract manufacturing regimes to defer custom duties, excise duties and import GST

• How the IP structured may substantially impact indirect tax and customs duty liabilities

2.

3.

© 2016 Baker & McKenzie

Supply Chain Planning Considerations

Manufacturing arrangements

• Contract manufacturing structures 4.

Turnkey Toll

Principal

Manufacturing

Co.

Finished

goods

(purchase)

Raw

materials

(sale)

• Buy-sell relationship

• Manufacturing Co.

bears risk of loss of

inventory

• Availability of bonded

manufacturing

arrangements to defer

custom duties and

import GST

• Treatment of locally-

sourced raw materials

and local sales of

finished goods

Principal

Manufacturing

Co.

Finished

goods

(return)

Raw

materials

(consign)

Tolling

fee

• Consignment

relationship

• Principal bears risk of

loss of inventory

• Availability of bonded

manufacturing

arrangements

• Treatment of locally-

sourced raw materials

and local sales of

finished goods

• Applicability of GST on

tolling fee

© 2016 Baker & McKenzie

Supply Chain Planning Considerations

Distribution arrangements

• Multi-channel retail

• Retail distribution / Wholesale distribution / Licensee distribution

5.

© 2016 Baker & McKenzie

E-Commerce

Manufacturing

Co. / Regional

Distribution Co.

Customer

Website of

brand

owner

Brand’s Own Website

2. Delivery of

goods

1. Order and

payment made

online

Market Place

Manufacturing Co. /

Regional Distribution Co.

(registered dealer on

platform)

Customer

E-

Commerce

platform

4. Delivery of

goods

2. Order and

payment made

online

3. Informs

dealer of order 5. Net

amount

remitted

after

deducting

service

fee

1. Listing of

goods on

website

© 2016 Baker & McKenzie

E-Commerce – Tax Considerations

Which entity will make the sale? To which entities are profits attributable?

“Reverse-charge” mechanism

Permanent establishment issues

Double taxation issues and the applicability of foreign tax credits

Transfer pricing

VAT registration issues – who is the supplier of services and who is liable for compliance?

Customs value impact

1.

2.

3.

4.

5.

6.

7.

Q & A

© 2016 Baker & McKenzie

2016 Luxury & Fashion Industry Conference for Multinationals - Singapore

THANK YOU

23 February 2016 | The St. Regis Singapore