Embed Size (px)

Citation preview

Bank Name Landesbank Hessen-Thüringen Girozentrale

LEI Code DIZES5CFO5K3I5R58746

Country Code DELa

2016 EU-wide Stress Test

Actual

(starting year)Baseline Scenario Adverse Scenario

(mln EUR, %) 31/12/2015 31/12/2018 31/12/2018

Cumulative 3y: Net interest income 4,204.19 3,438.04

Cumulative 3y: Gains or (-) losses on financial assets and liabilities held for trading or designated at fair value through profit

and loss, net250.27 -547.63

Cumulative 3y: (Impairment or (-) reversal of impairment on financial assets not measured at fair value through profit or loss) -538.39 -985.83

Cumulative 3y: Profit or (-) loss for the year 1,197.30 -818.48

Coverage ratio - Default stock 35.29% 33.56% 38.79%

Common Equity Tier 1 capital 7,563.98 8,042.61 6,229.04

Total Risk exposure amount 54,859.47 55,779.71 61,655.87

Common Equity Tier 1 ratio, % 13.8% 14.4% 10.1%

Fully loaded Common Equity Tier 1 ratio, % 13.1% 14.4% 10.1%

Tier 1 capital 8,171.02 8,463.24 6,649.67

Total leverage ratio exposures 183,275.35 183,275.35 183,275.35

Leverage ratio, % 4.5% 4.6% 3.6%

Fully loaded leverage ratio, % 3.9% 4.4% 3.4%

Total amount of instruments with mandatory conversion into ordinary shares upon a fixed date in the 2016 -2018 period

(cumulative conversions)1 0

Total Additional Tier 1 and Tier 2 instruments eligible as regulatory capital under the CRR provisions that convert into Common

Equity Tier 1 or are written down upon a trigger event2 0

Of which: eligible instruments whose trigger is above CET1 capital ratio in the adverse scenario2 0

1 Conversions not considered for CET1 computation

2 Excluding instruments with mandatory conversion into ordinary shares upon a fixed date in the 2016 -2018 period

2016 EU-wide Stress Test: SummaryLandesbank Hessen-Thüringen Girozentrale

Memorandum items

2016 EU-wide Stress Test:

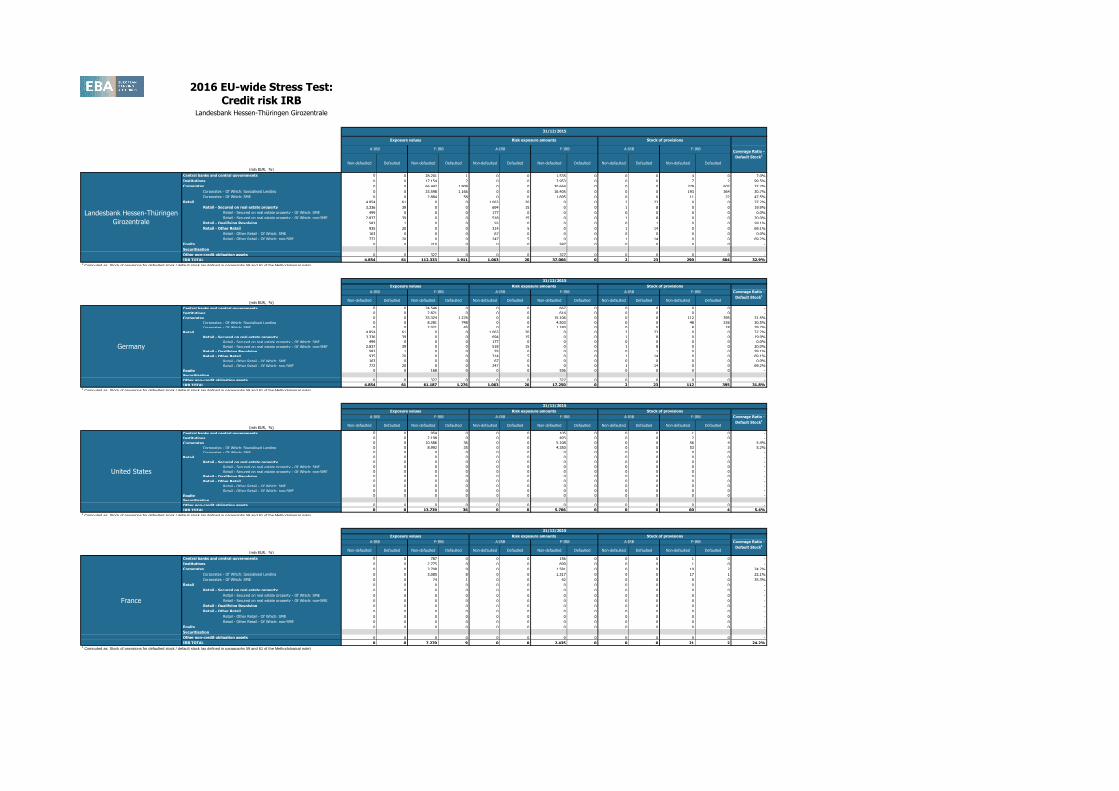

Credit risk IRBLandesbank Hessen-Thüringen Girozentrale

(mln EUR, %)

Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central banks and central governments 0 0 28,201 1 0 0 1,535 0 0 0 4 0 7.0%

Institutions 0 0 17,154 2 0 0 3,953 0 0 0 7 2 99.5%

Corporates 0 0 66,442 1,908 0 0 30,664 0 0 0 279 602 32.7%

Corporates - Of Which: Specialised Lending 0 0 33,598 1,166 0 0 16,405 0 0 0 193 364 30.7%

Corporates - Of Which: SME 0 0 2,884 58 0 0 1,695 0 0 0 11 22 47.5%

Retail 4,854 61 0 0 1,063 20 0 0 2 23 0 0 37.2%

Retail - Secured on real estate property 3,336 39 0 0 694 15 0 0 1 8 0 0 19.9%

Retail - Secured on real estate property - Of Which: SME 499 0 0 0 177 0 0 0 0 0 0 0 0.0%

Retail - Secured on real estate property - Of Which: non-SME 2,837 39 0 0 518 15 0 0 1 8 0 0 20.0%

Retail - Qualifying Revolving 583 1 0 0 55 0 0 0 0 1 0 0 59.1%

Retail - Other Retail 935 20 0 0 314 5 0 0 1 14 0 0 69.1%

Retail - Other Retail - Of Which: SME 163 0 0 0 67 0 0 0 0 0 0 0 0.0%

Retail - Other Retail - Of Which: non-SME 772 20 0 0 247 5 0 0 1 14 0 0 69.2%

Equity 0 0 210 0 0 0 587 0 0 0 0 0 -

Securitisation

Other non-credit obligation assets 0 0 327 0 0 0 327 0 0 0 0 0 -

IRB TOTAL 4,854 61 112,333 1,911 1,063 20 37,066 0 2 23 290 604 32.9%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central banks and central governments 0 0 24,546 0 0 0 667 0 0 0 0 0 -

Institutions 0 0 2,821 0 0 0 614 0 0 0 0 0 -

Corporates 0 0 33,324 1,276 0 0 15,106 0 0 0 112 395 31.5%

Corporates - Of Which: Specialised Lending 0 0 8,281 748 0 0 4,503 0 0 0 48 226 30.5%

Corporates - Of Which: SME 0 0 2,021 45 0 0 1,180 0 0 0 8 18 39.2%

Retail 4,854 61 0 0 1,063 20 0 0 2 23 0 0 37.2%

Retail - Secured on real estate property 3,336 39 0 0 694 15 0 0 1 8 0 0 19.9%

Retail - Secured on real estate property - Of Which: SME 499 0 0 0 177 0 0 0 0 0 0 0 0.0%

Retail - Secured on real estate property - Of Which: non-SME 2,837 39 0 0 518 15 0 0 1 8 0 0 20.0%

Retail - Qualifying Revolving 583 1 0 0 55 0 0 0 0 1 0 0 59.1%

Retail - Other Retail 935 20 0 0 314 5 0 0 1 14 0 0 69.1%

Retail - Other Retail - Of Which: SME 163 0 0 0 67 0 0 0 0 0 0 0 0.0%

Retail - Other Retail - Of Which: non-SME 772 20 0 0 247 5 0 0 1 14 0 0 69.2%

Equity 0 0 168 0 0 0 536 0 0 0 0 0 -

Securitisation

Other non-credit obligation assets 0 0 327 0 0 0 327 0 0 0 0 0 -

IRB TOTAL 4,854 61 61,187 1,276 1,063 20 17,250 0 2 23 112 395 31.8%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central banks and central governments 0 0 954 0 0 0 105 0 0 0 1 0 -

Institutions 0 0 2,198 0 0 0 493 0 0 0 2 0 -

Corporates 0 0 10,586 36 0 0 5,108 0 0 0 56 4 5.4%

Corporates - Of Which: Specialised Lending 0 0 8,992 35 0 0 4,350 0 0 0 53 3 5.2%

Corporates - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Qualifying Revolving 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Equity 0 0 0 0 0 0 0 0 0 0 0 0 -

Securitisation

Other non-credit obligation assets 0 0 0 0 0 0 0 0 0 0 0 0 -

IRB TOTAL 0 0 13,739 36 0 0 5,706 0 0 0 60 4 5.4%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central banks and central governments 0 0 787 0 0 0 156 0 0 0 1 0 -

Institutions 0 0 2,775 0 0 0 699 0 0 0 1 0 -

Corporates 0 0 3,708 9 0 0 1,581 0 0 0 19 2 24.2%

Corporates - Of Which: Specialised Lending 0 0 3,085 8 0 0 1,317 0 0 0 17 1 22.1%

Corporates - Of Which: SME 0 0 74 1 0 0 42 0 0 0 0 0 35.3%

Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Qualifying Revolving 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Equity 0 0 0 0 0 0 0 0 0 0 0 0 -

Securitisation

Other non-credit obligation assets 0 0 0 0 0 0 0 0 0 0 0 0 -

IRB TOTAL 0 0 7,270 9 0 0 2,435 0 0 0 21 2 24.2%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

31/12/2015

Exposure values Risk exposure amounts Stock of provisions

Coverage Ratio -

Default Stock1

A-IRB

Landesbank Hessen-Thüringen

Girozentrale

F-IRB A-IRB F-IRB A-IRB F-IRB

31/12/2015

Exposure values Risk exposure amounts Stock of provisions

Coverage Ratio -

Default Stock1

A-IRB F-IRB A-IRB

Germany

31/12/2015

Exposure values Risk exposure amounts Stock of provisions

F-IRB A-IRB F-IRB

Coverage Ratio -

Default Stock1

A-IRB F-IRB A-IRB F-IRB A-IRB F-IRB

United States

31/12/2015

Exposure values Risk exposure amounts Stock of provisions

Coverage Ratio -

Default Stock1

A-IRB F-IRB

France

A-IRB F-IRB A-IRB F-IRB

2016 EU-wide Stress Test:

Credit risk IRBLandesbank Hessen-Thüringen Girozentrale

(mln EUR, %)Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central banks and central governments 0 0 600 0 0 0 55 0 0 0 0 0 -

Institutions 0 0 2,014 0 0 0 548 0 0 0 0 0 -

Corporates 0 0 4,082 0 0 0 1,487 0 0 0 17 0 36.6%

Corporates - Of Which: Specialised Lending 0 0 3,161 0 0 0 1,072 0 0 0 13 0 -

Corporates - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Qualifying Revolving 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Equity 0 0 0 0 0 0 0 0 0 0 0 0 -

Securitisation

Other non-credit obligation assets 0 0 0 0 0 0 0 0 0 0 0 0 -

IRB TOTAL 0 0 6,696 0 0 0 2,090 0 0 0 17 0 36.6%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central banks and central governments 0 0 56 0 0 0 0 0 0 0 0 0 -

Institutions 0 0 854 0 0 0 188 0 0 0 0 0 -

Corporates 0 0 1,926 63 0 0 776 0 0 0 6 29 46.2%

Corporates - Of Which: Specialised Lending 0 0 1,091 62 0 0 467 0 0 0 4 28 46.3%

Corporates - Of Which: SME 0 0 2 0 0 0 1 0 0 0 0 0 -

Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Qualifying Revolving 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Equity 0 0 0 0 0 0 0 0 0 0 0 0 -

Securitisation

Other non-credit obligation assets 0 0 0 0 0 0 0 0 0 0 0 0 -

IRB TOTAL 0 0 2,836 63 0 0 964 0 0 0 6 29 46.2%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central banks and central governments 0 0 32 0 0 0 5 0 0 0 0 0 -

Institutions 0 0 55 0 0 0 9 0 0 0 0 0 -

Corporates 0 0 2,844 105 0 0 1,371 0 0 0 10 34 32.8%

Corporates - Of Which: Specialised Lending 0 0 2,306 0 0 0 1,164 0 0 0 8 0 -

Corporates - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Qualifying Revolving 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Equity 0 0 0 0 0 0 0 0 0 0 0 0 -

Securitisation

Other non-credit obligation assets 0 0 0 0 0 0 0 0 0 0 0 0 -

IRB TOTAL 0 0 2,931 105 0 0 1,385 0 0 0 10 34 32.8%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central banks and central governments 0 0 25 0 0 0 15 0 0 0 0 0 -

Institutions 0 0 1,084 0 0 0 288 0 0 0 1 0 -

Corporates 0 0 476 2 0 0 189 0 0 0 2 0 7.6%

Corporates - Of Which: Specialised Lending 0 0 94 0 0 0 49 0 0 0 1 0 -

Corporates - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Qualifying Revolving 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Equity 0 0 0 0 0 0 0 0 0 0 0 0 -

Securitisation

Other non-credit obligation assets 0 0 0 0 0 0 0 0 0 0 0 0 -

IRB TOTAL 0 0 1,586 2 0 0 492 0 0 0 3 0 7.6%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

31/12/2015

Exposure values Risk exposure amounts Stock of provisions

Coverage Ratio -

Default Stock1

A-IRB F-IRB A-IRB F-IRB A-IRB F-IRB

United Kingdom

31/12/2015

Exposure values Risk exposure amounts Stock of provisions

Coverage Ratio -

Default Stock1

A-IRB F-IRB

Netherlands

31/12/2015

Exposure values Risk exposure amounts

A-IRB F-IRB A-IRB F-IRB

Stock of provisions

Coverage Ratio -

Default Stock1

A-IRB F-IRB A-IRB F-IRB A-IRB F-IRB

Luxembourg

31/12/2015

Exposure values Risk exposure amounts Stock of provisions

Coverage Ratio -

Default Stock1

A-IRB F-IRB

Switzerland

A-IRB F-IRB A-IRB F-IRB

2016 EU-wide Stress Test:

Credit risk IRBLandesbank Hessen-Thüringen Girozentrale

(mln EUR, %)Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central banks and central governments 0 0 535 0 0 0 225 0 0 0 0 0 -

Institutions 0 0 338 0 0 0 81 0 0 0 0 0 -

Corporates 0 0 565 124 0 0 523 0 0 0 7 48 38.8%

Corporates - Of Which: Specialised Lending 0 0 425 113 0 0 467 0 0 0 6 37 32.8%

Corporates - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Qualifying Revolving 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Equity 0 0 0 0 0 0 0 0 0 0 0 0 -

Securitisation

Other non-credit obligation assets 0 0 0 0 0 0 0 0 0 0 0 0 -

IRB TOTAL 0 0 1,438 124 0 0 828 0 0 0 7 48 38.8%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central banks and central governments 0 0 14 0 0 0 1 0 0 0 0 0 -

Institutions 0 0 1,367 0 0 0 180 0 0 0 0 0 -

Corporates 0 0 141 0 0 0 66 0 0 0 1 0 36.6%

Corporates - Of Which: Specialised Lending 0 0 101 0 0 0 32 0 0 0 1 0 -

Corporates - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Qualifying Revolving 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Equity 0 0 0 0 0 0 0 0 0 0 0 0 -

Securitisation

Other non-credit obligation assets 0 0 0 0 0 0 0 0 0 0 0 0 -

IRB TOTAL 0 0 1,522 0 0 0 246 0 0 0 1 0 36.6%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central banks and central governments 0 0 129 0 0 0 20 0 0 0 0 0 -

Institutions 0 0 389 0 0 0 79 0 0 0 1 0 -

Corporates 0 0 873 51 0 0 524 0 0 0 6 0 36.6%

Corporates - Of Which: Specialised Lending 0 0 398 0 0 0 239 0 0 0 3 0 -

Corporates - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Secured on real estate property - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Qualifying Revolving 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Retail - Other Retail - Of Which: non-SME 0 0 0 0 0 0 0 0 0 0 0 0 -

Equity 0 0 0 0 0 0 0 0 0 0 0 0 -

Securitisation

Other non-credit obligation assets 0 0 0 0 0 0 0 0 0 0 0 0 -

IRB TOTAL 0 0 1,391 51 0 0 624 0 0 0 7 0 36.6%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

31/12/2015

Exposure values Risk exposure amounts Stock of provisions

Coverage Ratio -

Default Stock1

A-IRB F-IRB A-IRB F-IRB A-IRB F-IRB

Spain

31/12/2015

Exposure values Risk exposure amounts Stock of provisions

Coverage Ratio -

Default Stock1

A-IRB F-IRB

Canada

31/12/2015

Exposure values Risk exposure amounts

A-IRB F-IRB A-IRB F-IRB

Austria

Stock of provisions

Coverage Ratio -

Default Stock1

A-IRB F-IRB A-IRB F-IRB A-IRB F-IRB

2016 EU-wide Stress Test:

Credit risk IRBLandesbank Hessen-Thüringen Girozentrale

(mln EUR, %)

Central banks and central governments

Institutions

Corporates

Corporates - Of Which: Specialised Lending

Corporates - Of Which: SME

Retail

Retail - Secured on real estate property

Retail - Secured on real estate property - Of Which: SME

Retail - Secured on real estate property - Of Which: non-SME

Retail - Qualifying Revolving

Retail - Other Retail

Retail - Other Retail - Of Which: SME

Retail - Other Retail - Of Which: non-SME

Equity

Securitisation

Other non-credit obligation assets

IRB TOTAL1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)

Central banks and central governments

Institutions

Corporates

Corporates - Of Which: Specialised Lending

Corporates - Of Which: SME

Retail

Retail - Secured on real estate property

Retail - Secured on real estate property - Of Which: SME

Retail - Secured on real estate property - Of Which: non-SME

Retail - Qualifying Revolving

Retail - Other Retail

Retail - Other Retail - Of Which: SME

Retail - Other Retail - Of Which: non-SME

Equity

Securitisation

Other non-credit obligation assets

IRB TOTAL1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)

Central banks and central governments

Institutions

Corporates

Corporates - Of Which: Specialised Lending

Corporates - Of Which: SME

Retail

Retail - Secured on real estate property

Retail - Secured on real estate property - Of Which: SME

Retail - Secured on real estate property - Of Which: non-SME

Retail - Qualifying Revolving

Retail - Other Retail

Retail - Other Retail - Of Which: SME

Retail - Other Retail - Of Which: non-SME

Equity

Securitisation

Other non-credit obligation assets

IRB TOTAL1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)

Central banks and central governments

Institutions

Corporates

Corporates - Of Which: Specialised Lending

Corporates - Of Which: SME

Retail

Retail - Secured on real estate property

Retail - Secured on real estate property - Of Which: SME

Retail - Secured on real estate property - Of Which: non-SME

Retail - Qualifying Revolving

Retail - Other Retail

Retail - Other Retail - Of Which: SME

Retail - Other Retail - Of Which: non-SME

Equity

Securitisation

Other non-credit obligation assets

IRB TOTAL1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Landesbank Hessen-Thüringen

Girozentrale

Germany

United States

France

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

0.0% 5 31.8% 0.0% 7 31.7% 0.0% 8 31.7% 0.0% 7 43.0% 0.0% 11 44.5% 0.0% 14 45.0%

0.1% 12 70.6% 0.1% 14 65.3% 0.1% 16 62.9% 0.1% 13 72.5% 0.1% 18 69.6% 0.1% 21 67.4%

0.2% 1,075 35.3% 0.2% 1,172 34.5% 0.1% 1,271 34.4% 0.3% 1,237 39.8% 0.3% 1,453 40.2% 0.2% 1,637 41.6%

0.1% 637 31.7% 0.1% 676 30.8% 0.1% 714 30.4% 0.2% 742 37.0% 0.2% 867 38.1% 0.1% 981 40.4%

0.5% 44 47.1% 0.5% 53 46.8% 0.5% 63 46.9% 0.7% 50 51.1% 0.7% 64 52.3% 0.6% 76 53.2%

0.4% 51 48.7% 0.4% 74 48.2% 0.5% 99 48.1% 0.4% 58 53.8% 0.6% 94 56.4% 0.8% 139 58.6%

0.3% 26 37.1% 0.3% 37 36.7% 0.3% 51 36.8% 0.3% 29 40.9% 0.5% 48 42.7% 0.6% 71 44.6%

0.7% 4 33.6% 0.7% 7 33.6% 0.7% 11 33.5% 0.9% 4 37.3% 1.0% 10 38.5% 1.2% 15 39.5%

0.2% 22 37.8% 0.2% 30 37.5% 0.3% 40 37.9% 0.2% 25 41.7% 0.3% 38 44.0% 0.5% 56 46.2%

0.4% 3 68.6% 0.5% 7 71.2% 0.6% 10 72.3% 0.5% 4 76.0% 0.7% 9 84.0% 1.0% 16 88.9%

0.7% 22 70.7% 0.8% 29 70.5% 0.8% 37 70.4% 0.8% 25 78.2% 1.1% 37 83.1% 1.4% 52 86.5%

1.4% 2 57.4% 1.3% 5 59.7% 1.4% 7 60.2% 1.7% 3 63.7% 1.9% 6 70.6% 2.3% 10 74.3%

0.5% 20 72.8% 0.7% 25 72.9% 0.7% 31 73.1% 0.6% 22 80.6% 1.0% 31 86.2% 1.2% 42 90.0%

0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0%

0.0% 0 40.0% 0.0% 0 42.0% 0.0% 0 42.7% 0.0% 0 40.0% 0.0% 0 42.0% 0.0% 0 42.7%

0.2% 1,143 35.9% 0.1% 1,267 35.4% 0.1% 1,395 35.4% 0.2% 1,316 40.5% 0.2% 1,576 41.2% 0.2% 1,812 42.9%

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

0.0% 1 20.8% 0.0% 1 21.8% 0.0% 2 22.2% 0.0% 1 23.7% 0.0% 2 24.9% 0.0% 2 25.2%

0.0% 0 25.6% 0.0% 0 26.7% 0.0% 0 27.0% 0.0% 0 33.4% 0.0% 0 34.7% 0.0% 1 35.1%

0.3% 670 37.1% 0.2% 737 36.4% 0.2% 808 36.6% 0.4% 802 42.9% 0.3% 948 43.7% 0.2% 1,080 45.7%

0.2% 315 32.5% 0.2% 329 31.7% 0.2% 346 31.5% 0.4% 392 40.0% 0.4% 459 42.3% 0.2% 529 46.6%

0.5% 38 45.1% 0.5% 49 45.8% 0.5% 58 46.5% 0.7% 45 50.8% 0.7% 60 52.1% 0.6% 72 52.9%

0.4% 51 48.7% 0.4% 74 48.2% 0.5% 99 48.1% 0.4% 58 53.8% 0.6% 94 56.4% 0.8% 139 58.6%

0.3% 26 37.1% 0.3% 37 36.7% 0.3% 51 36.8% 0.3% 29 40.9% 0.5% 48 42.7% 0.6% 71 44.6%

0.7% 4 33.6% 0.7% 7 33.6% 0.7% 11 33.5% 0.9% 4 37.3% 1.0% 10 38.5% 1.2% 15 39.5%

0.2% 22 37.8% 0.2% 30 37.5% 0.3% 40 37.9% 0.2% 25 41.7% 0.3% 38 44.0% 0.5% 56 46.2%

0.4% 3 68.6% 0.5% 7 71.2% 0.6% 10 72.3% 0.5% 4 76.0% 0.7% 9 84.0% 1.0% 16 88.9%

0.7% 22 70.7% 0.8% 29 70.5% 0.8% 37 70.4% 0.8% 25 78.2% 1.1% 37 83.1% 1.4% 52 86.5%

1.4% 2 57.4% 1.3% 5 59.7% 1.4% 7 60.2% 1.7% 3 63.7% 1.9% 6 70.6% 2.3% 10 74.3%

0.5% 20 72.8% 0.7% 25 72.9% 0.7% 31 73.1% 0.6% 22 80.6% 1.0% 31 86.2% 1.2% 42 90.0%

0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0%

0.0% 0 40.0% 0.0% 0 42.0% 0.0% 0 42.7% 0.0% 0 40.0% 0.0% 0 42.0% 0.0% 0 42.7%

0.2% 722 37.8% 0.2% 812 37.3% 0.2% 910 37.6% 0.3% 861 43.5% 0.3% 1,045 44.6% 0.2% 1,222 46.9%

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

0.0% 1 - 0.0% 1 - 0.0% 1 - 0.0% 1 - 0.0% 1 - 0.0% 1 -

0.0% 3 84.2% 0.0% 3 88.8% 0.0% 3 89.4% 0.1% 3 93.5% 0.1% 4 95.6% 0.0% 4 96.8%

0.1% 70 11.1% 0.1% 78 13.4% 0.0% 83 14.1% 0.1% 74 12.6% 0.1% 95 18.1% 0.1% 111 20.9%

0.1% 65 10.6% 0.1% 72 13.0% 0.0% 77 13.6% 0.1% 69 12.0% 0.1% 88 17.6% 0.1% 102 20.5%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 74 11.3% 0.1% 82 13.7% 0.0% 87 14.4% 0.1% 78 13.0% 0.1% 100 18.7% 0.1% 116 21.5%

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

0.0% 1 56.1% 0.0% 1 59.6% 0.0% 1 60.7% 0.1% 1 60.7% 0.1% 2 63.8% 0.1% 2 64.8%

0.1% 1 37.4% 0.1% 1 39.5% 0.1% 1 40.3% 0.1% 1 45.0% 0.1% 1 47.3% 0.1% 1 48.0%

0.1% 27 44.8% 0.1% 32 43.9% 0.1% 36 43.4% 0.2% 30 46.6% 0.2% 38 46.5% 0.1% 44 47.1%

0.1% 24 44.4% 0.1% 28 43.3% 0.1% 32 42.8% 0.2% 26 46.1% 0.2% 34 45.9% 0.1% 39 46.5%

0.1% 1 47.3% 0.1% 1 46.1% 0.1% 1 45.3% 0.2% 1 48.3% 0.2% 1 49.3% 0.2% 1 49.5%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 29 44.8% 0.1% 34 43.9% 0.1% 38 43.5% 0.2% 32 46.9% 0.2% 41 47.0% 0.1% 47 47.7%

Baseline Scenario Adverse Scenario

31/12/2017 31/12/2018 31/12/2016 31/12/2017 31/12/201831/12/2016

Baseline Scenario Adverse Scenario

31/12/2016 31/12/2017 31/12/2018

Baseline Scenario Adverse Scenario

31/12/2016 31/12/2017 31/12/2018

31/12/2016 31/12/2017 31/12/2018 31/12/2016 31/12/2017 31/12/2018

Baseline Scenario Adverse Scenario

31/12/2018 31/12/2016 31/12/2017 31/12/201831/12/2016 31/12/2017

2016 EU-wide Stress Test:

Credit risk IRBLandesbank Hessen-Thüringen Girozentrale

(mln EUR, %)

Central banks and central governments

Institutions

Corporates

Corporates - Of Which: Specialised Lending

Corporates - Of Which: SME

Retail

Retail - Secured on real estate property

Retail - Secured on real estate property - Of Which: SME

Retail - Secured on real estate property - Of Which: non-SME

Retail - Qualifying Revolving

Retail - Other Retail

Retail - Other Retail - Of Which: SME

Retail - Other Retail - Of Which: non-SME

Equity

Securitisation

Other non-credit obligation assets

IRB TOTAL1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)

Central banks and central governments

Institutions

Corporates

Corporates - Of Which: Specialised Lending

Corporates - Of Which: SME

Retail

Retail - Secured on real estate property

Retail - Secured on real estate property - Of Which: SME

Retail - Secured on real estate property - Of Which: non-SME

Retail - Qualifying Revolving

Retail - Other Retail

Retail - Other Retail - Of Which: SME

Retail - Other Retail - Of Which: non-SME

Equity

Securitisation

Other non-credit obligation assets

IRB TOTAL1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)

Central banks and central governments

Institutions

Corporates

Corporates - Of Which: Specialised Lending

Corporates - Of Which: SME

Retail

Retail - Secured on real estate property

Retail - Secured on real estate property - Of Which: SME

Retail - Secured on real estate property - Of Which: non-SME

Retail - Qualifying Revolving

Retail - Other Retail

Retail - Other Retail - Of Which: SME

Retail - Other Retail - Of Which: non-SME

Equity

Securitisation

Other non-credit obligation assets

IRB TOTAL1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)

Central banks and central governments

Institutions

Corporates

Corporates - Of Which: Specialised Lending

Corporates - Of Which: SME

Retail

Retail - Secured on real estate property

Retail - Secured on real estate property - Of Which: SME

Retail - Secured on real estate property - Of Which: non-SME

Retail - Qualifying Revolving

Retail - Other Retail

Retail - Other Retail - Of Which: SME

Retail - Other Retail - Of Which: non-SME

Equity

Securitisation

Other non-credit obligation assets

IRB TOTAL1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

United Kingdom

Netherlands

Luxembourg

Switzerland

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

0.0% 0 39.5% 0.0% 0 41.5% 0.0% 0 42.1% 0.0% 0 41.4% 0.0% 0 43.5% 0.0% 0 44.2%

0.1% 0 34.3% 0.1% 0 36.3% 0.1% 0 37.1% 0.1% 0 43.2% 0.1% 0 45.4% 0.1% 1 46.1%

0.1% 21 23.6% 0.1% 25 25.4% 0.1% 28 25.6% 0.1% 22 24.1% 0.1% 28 27.0% 0.1% 33 29.4%

0.0% 14 10.0% 0.0% 15 11.4% 0.0% 16 11.7% 0.0% 14 10.3% 0.1% 17 15.0% 0.1% 19 18.0%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 21 23.7% 0.1% 25 25.6% 0.1% 29 25.8% 0.1% 22 24.4% 0.1% 29 27.2% 0.1% 34 29.7%

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.0% 0 34.9% 0.0% 0 36.8% 0.0% 0 37.6% 0.0% 0 42.5% 0.0% 0 44.6% 0.0% 0 45.3%

0.1% 42 54.2% 0.1% 43 52.9% 0.1% 44 51.7% 0.1% 44 56.7% 0.1% 47 55.0% 0.1% 49 54.6%

0.1% 40 54.5% 0.1% 40 53.3% 0.1% 41 52.0% 0.1% 42 57.0% 0.1% 44 55.4% 0.1% 45 55.0%

0.6% 0 43.2% 0.6% 0 45.6% 0.6% 0 46.4% 0.9% 0 48.1% 0.9% 0 50.6% 0.8% 0 51.5%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 42 54.2% 0.1% 43 52.9% 0.1% 44 51.7% 0.1% 44 56.7% 0.1% 47 55.0% 0.1% 49 54.6%

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

0.0% 0 44.8% 0.0% 0 47.2% 0.0% 0 48.1% 0.0% 0 49.4% 0.0% 0 51.9% 0.0% 0 52.7%

0.0% 0 27.1% 0.0% 0 28.6% 0.0% 0 29.3% 0.0% 0 37.6% 0.0% 0 39.2% 0.0% 0 39.8%

0.1% 48 32.3% 0.1% 51 32.3% 0.1% 55 32.3% 0.2% 49 32.4% 0.2% 57 32.7% 0.1% 61 33.3%

0.1% 11 28.0% 0.1% 14 30.0% 0.1% 18 30.6% 0.2% 13 30.1% 0.3% 19 32.4% 0.1% 23 34.3%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 48 32.3% 0.1% 51 32.3% 0.1% 55 32.3% 0.2% 49 32.4% 0.2% 57 32.7% 0.1% 61 33.3%

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

0.0% 0 - 0.0% 0 - 0.0% 0 - 0.0% 0 - 0.0% 0 - 0.0% 0 -

0.0% 1 24.1% 0.0% 1 26.1% 0.0% 1 26.8% 0.0% 1 31.5% 0.0% 1 32.1% 0.0% 1 33.8%

0.1% 3 29.4% 0.1% 3 33.0% 0.1% 3 33.7% 0.1% 3 31.7% 0.1% 3 36.1% 0.1% 4 37.7%

0.1% 1 23.3% 0.1% 1 23.4% 0.1% 1 23.3% 0.1% 1 23.0% 0.1% 1 24.6% 0.1% 2 27.0%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.0% 3 29.3% 0.0% 4 32.7% 0.0% 4 33.4% 0.0% 4 31.7% 0.1% 4 35.8% 0.0% 5 37.4%

Baseline Scenario Adverse Scenario

31/12/2016 31/12/2017 31/12/2018 31/12/2016 31/12/2017 31/12/2018

Baseline Scenario Adverse Scenario

31/12/2018 31/12/2016 31/12/2017 31/12/2018

Baseline Scenario Adverse Scenario

31/12/2016 31/12/2017

31/12/2016 31/12/2017 31/12/2018 31/12/2016 31/12/2017 31/12/2018

Baseline Scenario Adverse Scenario

31/12/2018 31/12/2016 31/12/2017 31/12/201831/12/2016 31/12/2017

2016 EU-wide Stress Test:

Credit risk IRBLandesbank Hessen-Thüringen Girozentrale

(mln EUR, %)

Central banks and central governments

Institutions

Corporates

Corporates - Of Which: Specialised Lending

Corporates - Of Which: SME

Retail

Retail - Secured on real estate property

Retail - Secured on real estate property - Of Which: SME

Retail - Secured on real estate property - Of Which: non-SME

Retail - Qualifying Revolving

Retail - Other Retail

Retail - Other Retail - Of Which: SME

Retail - Other Retail - Of Which: non-SME

Equity

Securitisation

Other non-credit obligation assets

IRB TOTAL1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)

Central banks and central governments

Institutions

Corporates

Corporates - Of Which: Specialised Lending

Corporates - Of Which: SME

Retail

Retail - Secured on real estate property

Retail - Secured on real estate property - Of Which: SME

Retail - Secured on real estate property - Of Which: non-SME

Retail - Qualifying Revolving

Retail - Other Retail

Retail - Other Retail - Of Which: SME

Retail - Other Retail - Of Which: non-SME

Equity

Securitisation

Other non-credit obligation assets

IRB TOTAL1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

(mln EUR, %)

Central banks and central governments

Institutions

Corporates

Corporates - Of Which: Specialised Lending

Corporates - Of Which: SME

Retail

Retail - Secured on real estate property

Retail - Secured on real estate property - Of Which: SME

Retail - Secured on real estate property - Of Which: non-SME

Retail - Qualifying Revolving

Retail - Other Retail

Retail - Other Retail - Of Which: SME

Retail - Other Retail - Of Which: non-SME

Equity

Securitisation

Other non-credit obligation assets

IRB TOTAL1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Spain

Canada

Austria

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

0.1% 1 48.1% 0.1% 1 50.5% 0.1% 2 51.3% 0.4% 2 55.3% 0.4% 4 58.1% 0.4% 6 59.0%

0.1% 0 45.9% 0.1% 0 48.4% 0.1% 0 49.3% 0.2% 0 52.6% 0.2% 0 55.2% 0.2% 0 56.1%

0.8% 59 36.8% 0.6% 62 35.8% 0.5% 65 35.2% 0.9% 60 36.7% 0.9% 65 35.6% 0.8% 69 34.7%

1.0% 47 31.4% 0.8% 50 30.8% 0.6% 52 30.4% 1.2% 48 31.4% 1.1% 52 30.7% 1.0% 56 30.2%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.5% 60 36.9% 0.4% 64 36.0% 0.3% 67 35.5% 0.7% 62 37.2% 0.7% 69 36.5% 0.6% 75 36.1%

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.0% 0 27.0% 0.0% 0 28.6% 0.0% 0 29.3% 0.0% 0 37.5% 0.0% 0 39.4% 0.0% 0 40.0%

0.1% 1 10.7% 0.0% 1 9.2% 0.0% 1 8.5% 0.1% 1 10.2% 0.1% 1 10.0% 0.1% 1 10.2%

0.0% 1 22.4% 0.0% 1 23.6% 0.0% 1 23.9% 0.0% 1 22.9% 0.1% 1 23.9% 0.1% 1 24.2%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 1 10.7% 0.0% 1 9.2% 0.0% 1 8.6% 0.1% 1 10.2% 0.1% 1 10.0% 0.1% 1 10.2%

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

0.0% 0 28.9% 0.0% 0 30.3% 0.0% 0 30.8% 0.0% 0 33.2% 0.0% 0 34.9% 0.0% 0 35.4%

0.0% 1 28.9% 0.0% 1 30.3% 0.0% 1 30.8% 0.0% 1 33.3% 0.0% 1 34.9% 0.0% 1 35.5%

0.3% 8 38.2% 0.2% 10 40.0% 0.2% 12 41.2% 0.4% 9 40.9% 0.4% 13 44.1% 0.2% 15 46.7%

0.3% 4 35.0% 0.3% 5 36.1% 0.3% 6 37.1% 0.5% 5 36.9% 0.5% 7 40.0% 0.3% 9 42.8%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.2% 9 38.0% 0.2% 11 39.8% 0.2% 13 41.0% 0.3% 10 40.8% 0.3% 13 43.9% 0.2% 16 46.5%

Baseline Scenario Adverse Scenario

31/12/2016 31/12/2017 31/12/2018 31/12/2016 31/12/2017 31/12/2018

Baseline Scenario Adverse Scenario

31/12/2018 31/12/2016 31/12/2017 31/12/2018

Baseline Scenario Adverse Scenario

31/12/2016 31/12/2017

31/12/2016 31/12/2017 31/12/2018 31/12/2016 31/12/2017 31/12/2018

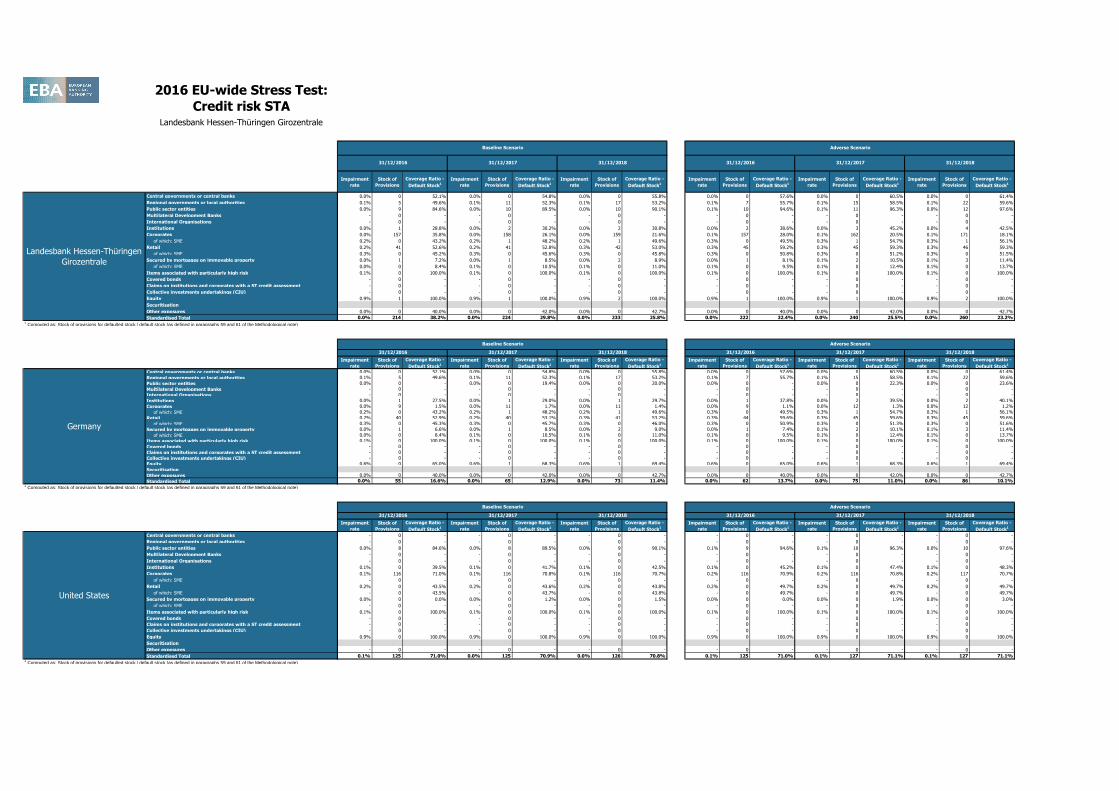

2016 EU-wide Stress Test:

Credit risk STALandesbank Hessen-Thüringen Girozentrale

Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central governments or central banks 1,382 0 38 0 0 0 0.0%

Regional governments or local authorities 11,327 0 20 0 0 0 0.0%

Public sector entities 1,991 0 205 0 9 0 0.0%

Multilateral Development Banks 231 0 0 0 0 0 0.0%

International Organisations 577 0 0 0 0 0 0.0%

Institutions 16,959 0 778 0 1 0 0.0%

Corporates 2,093 165 1,835 109 27 129 71.4%

of which: SME 106 0 99 0 0 0 0.0%

Retail 128 66 97 79 6 4 6.8%

of which: SME 5 0 3 0 0 0 0.0%

Secured by mortgages on immovable property 1,382 0 483 0 0 0 0.0%

of which: SME 126 0 36 0 0 0 0.0%

Items associated with particularly high risk 62 0 93 0 0 0 0.0%

Covered bonds 186 0 19 0 0 0 0.0%

Claims on institutions and corporates with a ST credit assessment 0 0 0 0 0 0 0.0%

Collective investments undertakings (CIU) 0 0 0 0 0 0 0.0%

Equity 918 0 996 0 0 0 0.0%

Securitisation

Other exposures 368 0 365 0 0 0 0.0%

Standardised Total 37,602 231 4,928 188 42 133 54.1%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central governments or central banks 937 0 30 0 0 0 0.0%

Regional governments or local authorities 7,477 0 13 0 0 0 0.0%

Public sector entities 933 0 28 0 0 0 0.0%

Multilateral Development Banks 0 0 0 0 0 0 0.0%

International Organisations 0 0 0 0 0 0 0.0%

Institutions 15,567 0 466 0 1 0 0.0%

Corporates 1,466 0 1,191 6 6 2 0.0%

of which: SME 106 0 99 0 0 0 0.0%

Retail 126 64 96 77 5 4 6.8%

of which: SME 5 0 3 0 0 0 0.0%

Secured by mortgages on immovable property 1,381 0 483 0 0 0 0.0%

of which: SME 126 0 36 0 0 0 0.0%

Items associated with particularly high risk 23 0 35 0 0 0 0.0%

Covered bonds 186 0 19 0 0 0 0.0%

Claims on institutions and corporates with a ST credit assessment 0 0 0 0 0 0 0.0%

Collective investments undertakings (CIU) 0 0 0 0 0 0 0.0%

Equity 859 0 925 0 0 0 0.0%

Securitisation

Other exposures 368 0 365 0 0 0 0.0%

Standardised Total 29,324 64 3,651 82 12 6 10.1%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central governments or central banks 0 0 0 0 0 0 0.0%

Regional governments or local authorities 0 0 0 0 0 0 0.0%

Public sector entities 843 0 163 0 8 0 0.0%

Multilateral Development Banks 0 0 0 0 0 0 0.0%

International Organisations 0 0 0 0 0 0 0.0%

Institutions 120 0 23 0 0 0 0.0%

Corporates 73 160 69 50 3 114 71.1%

of which: SME 0 0 0 0 0 0 0.0%

Retail 0 0 0 0 0 0 9.5%

of which: SME 0 0 0 0 0 0 9.5%

Secured by mortgages on immovable property 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Items associated with particularly high risk 3 0 4 0 0 0 0.0%

Covered bonds 0 0 0 0 0 0 0.0%

Claims on institutions and corporates with a ST credit assessment 0 0 0 0 0 0 0.0%

Collective investments undertakings (CIU) 0 0 0 0 0 0 0.0%

Equity 50 0 50 0 0 0 0.0%

Securitisation

Other exposures 0 0 0 0 0 0 0.0%

Standardised Total 1,089 160 309 50 10 114 71.0%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

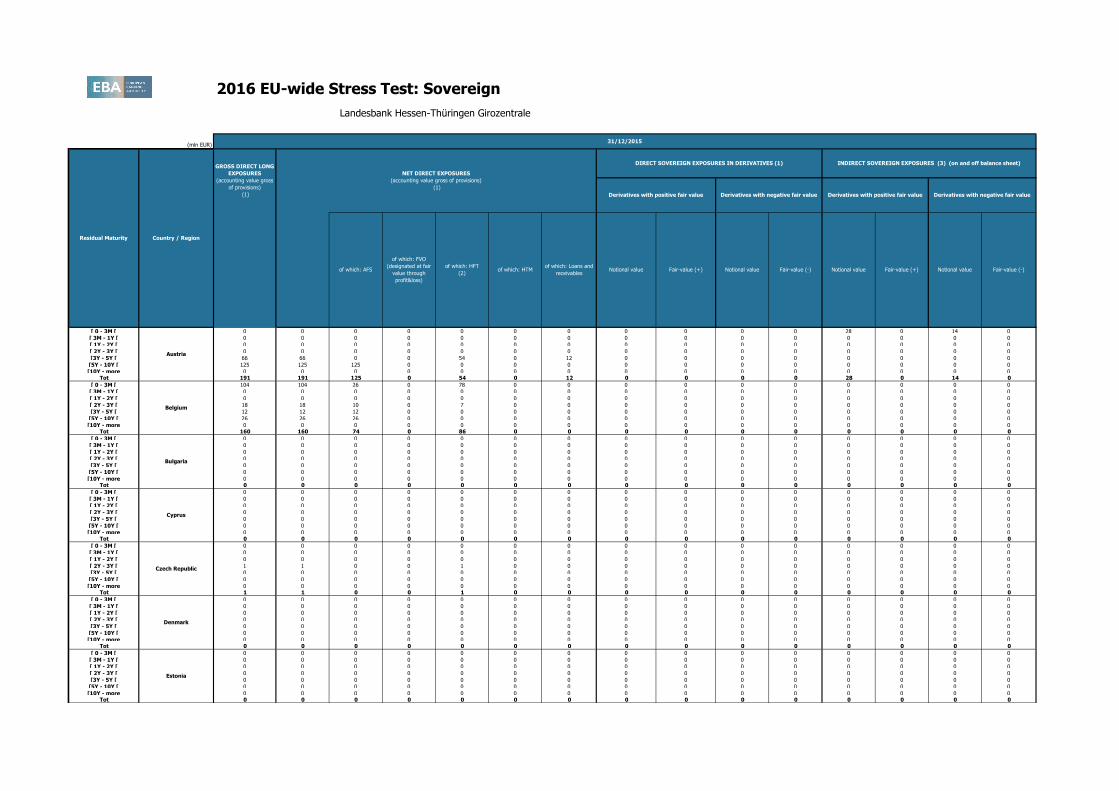

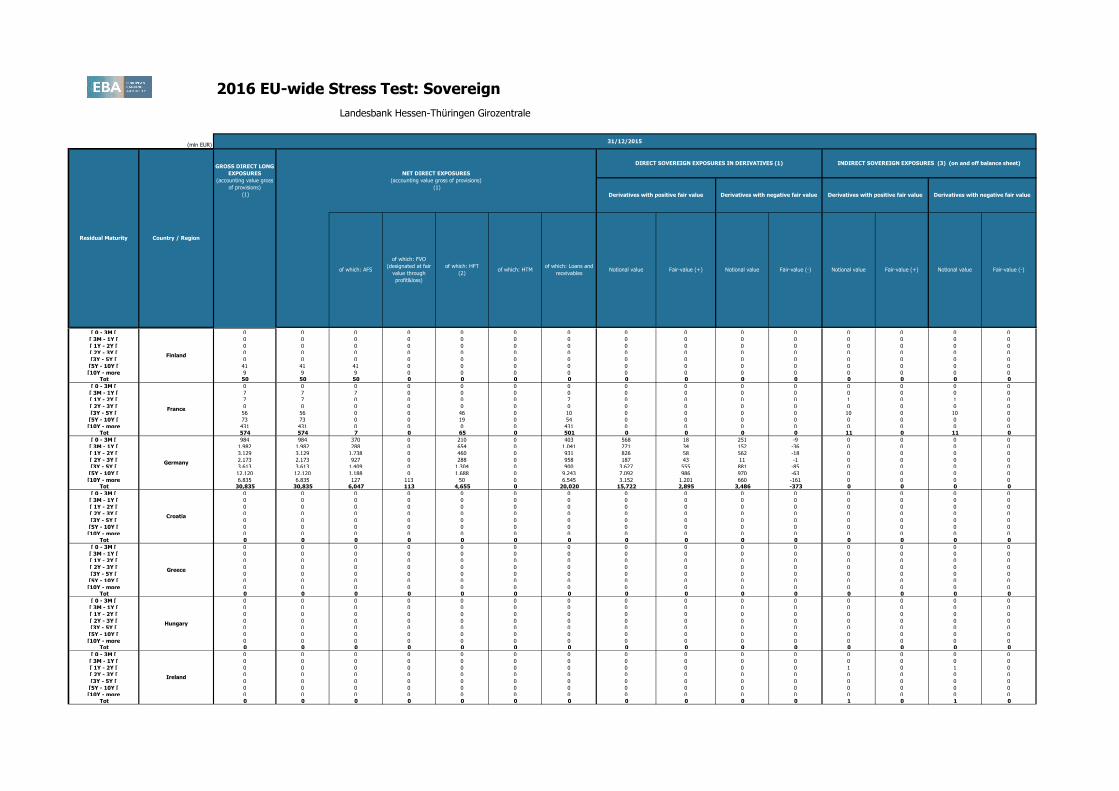

Landesbank Hessen-Thüringen

Girozentrale

31/12/2015

Exposure values Risk exposure amounts Stock of provisions

Coverage Ratio -

Default Stock1

Germany

31/12/2015

31/12/2015

Exposure values Risk exposure amounts Stock of provisionsCoverage Ratio -

Default Stock1

United States

Exposure values Risk exposure amounts Stock of provisionsCoverage Ratio -

Default Stock1

2016 EU-wide Stress Test:

Credit risk STALandesbank Hessen-Thüringen Girozentrale

Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central governments or central banks 0 0 0 0 0 0 0.0%

Regional governments or local authorities 0 0 0 0 0 0 0.0%

Public sector entities 0 0 0 0 0 0 0.0%

Multilateral Development Banks 0 0 0 0 0 0 0.0%

International Organisations 0 0 0 0 0 0 0.0%

Institutions 54 0 27 0 0 0 0.0%

Corporates 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Retail 0 0 0 0 0 0 6.3%

of which: SME 0 0 0 0 0 0 0.0%

Secured by mortgages on immovable property 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Items associated with particularly high risk 0 0 0 0 0 0 0.0%

Covered bonds 0 0 0 0 0 0 0.0%

Claims on institutions and corporates with a ST credit assessment 0 0 0 0 0 0 0.0%

Collective investments undertakings (CIU) 0 0 0 0 0 0 0.0%

Equity 0 0 0 0 0 0 0.0%

Securitisation

Other exposures 0 0 0 0 0 0 0.0%

Standardised Total 54 0 27 0 0 0 6.3%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central governments or central banks 0 0 0 0 0 0 0.0%

Regional governments or local authorities 0 0 0 0 0 0 0.0%

Public sector entities 0 0 0 0 0 0 0.0%

Multilateral Development Banks 0 0 0 0 0 0 0.0%

International Organisations 0 0 0 0 0 0 0.0%

Institutions 7 0 2 0 0 0 0.0%

Corporates 83 6 55 1 3 5 93.1%

of which: SME 0 0 0 0 0 0 0.0%

Retail 0 0 0 0 0 0 5.8%

of which: SME 0 0 0 0 0 0 0.0%

Secured by mortgages on immovable property 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Items associated with particularly high risk 0 0 0 0 0 0 0.0%

Covered bonds 0 0 0 0 0 0 0.0%

Claims on institutions and corporates with a ST credit assessment 0 0 0 0 0 0 0.0%

Collective investments undertakings (CIU) 0 0 0 0 0 0 0.0%

Equity 9 0 21 0 0 0 0.0%

Securitisation

Other exposures 0 0 0 0 0 0 0.0%

Standardised Total 100 6 78 1 3 5 89.1%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central governments or central banks 0 0 0 0 0 0 0.0%

Regional governments or local authorities 0 0 0 0 0 0 0.0%

Public sector entities 0 0 0 0 0 0 0.0%

Multilateral Development Banks 0 0 0 0 0 0 0.0%

International Organisations 0 0 0 0 0 0 0.0%

Institutions 147 0 56 0 0 0 0.0%

Corporates 141 0 132 0 9 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Retail 0 0 0 0 0 0 6.3%

of which: SME 0 0 0 0 0 0 0.0%

Secured by mortgages on immovable property 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Items associated with particularly high risk 0 0 0 0 0 0 0.0%

Covered bonds 0 0 0 0 0 0 0.0%

Claims on institutions and corporates with a ST credit assessment 0 0 0 0 0 0 0.0%

Collective investments undertakings (CIU) 0 0 0 0 0 0 0.0%

Equity 0 0 0 0 0 0 0.0%

Securitisation

Other exposures 0 0 0 0 0 0 0.0%

Standardised Total 288 0 188 0 9 0 10.5%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

31/12/2015

France

31/12/2015

Exposure values Risk exposure amounts Stock of provisionsCoverage Ratio -

Default Stock1

United Kingdom

31/12/2015

Exposure values Risk exposure amounts Stock of provisionsCoverage Ratio -

Default Stock1

Netherlands

Exposure values Risk exposure amounts Stock of provisionsCoverage Ratio -

Default Stock1

2016 EU-wide Stress Test:

Credit risk STALandesbank Hessen-Thüringen Girozentrale

Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central governments or central banks 0 0 0 0 0 0 0.0%

Regional governments or local authorities 0 0 0 0 0 0 0.0%

Public sector entities 0 0 0 0 0 0 0.0%

Multilateral Development Banks 0 0 0 0 0 0 0.0%

International Organisations 0 0 0 0 0 0 0.0%

Institutions 0 0 0 0 0 0 0.0%

Corporates 5 0 4 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Retail 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Secured by mortgages on immovable property 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Items associated with particularly high risk 5 0 7 0 0 0 0.0%

Covered bonds 0 0 0 0 0 0 0.0%

Claims on institutions and corporates with a ST credit assessment 0 0 0 0 0 0 0.0%

Collective investments undertakings (CIU) 0 0 0 0 0 0 0.0%

Equity 0 0 0 0 0 0 0.0%

Securitisation

Other exposures 0 0 0 0 0 0 0.0%

Standardised Total 10 0 12 0 0 0 0.0%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central governments or central banks 0 0 0 0 0 0 0.0%

Regional governments or local authorities 0 0 0 0 0 0 0.0%

Public sector entities 0 0 0 0 0 0 0.0%

Multilateral Development Banks 0 0 0 0 0 0 0.0%

International Organisations 0 0 0 0 0 0 0.0%

Institutions 0 0 0 0 0 0 0.0%

Corporates 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Retail 0 0 0 0 0 0 5.9%

of which: SME 0 0 0 0 0 0 0.0%

Secured by mortgages on immovable property 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Items associated with particularly high risk 0 0 0 0 0 0 0.0%

Covered bonds 0 0 0 0 0 0 0.0%

Claims on institutions and corporates with a ST credit assessment 0 0 0 0 0 0 0.0%

Collective investments undertakings (CIU) 0 0 0 0 0 0 0.0%

Equity 0 0 0 0 0 0 0.0%

Securitisation

Other exposures 0 0 0 0 0 0 0.0%

Standardised Total 1 0 0 0 0 0 5.9%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central governments or central banks 0 0 0 0 0 0 0.0%

Regional governments or local authorities 0 0 0 0 0 0 0.0%

Public sector entities 0 0 0 0 0 0 0.0%

Multilateral Development Banks 0 0 0 0 0 0 0.0%

International Organisations 0 0 0 0 0 0 0.0%

Institutions 15 0 3 0 0 0 0.0%

Corporates 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Retail 0 0 0 0 0 0 6.3%

of which: SME 0 0 0 0 0 0 0.0%

Secured by mortgages on immovable property 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Items associated with particularly high risk 0 0 0 0 0 0 0.0%

Covered bonds 0 0 0 0 0 0 0.0%

Claims on institutions and corporates with a ST credit assessment 0 0 0 0 0 0 0.0%

Collective investments undertakings (CIU) 0 0 0 0 0 0 0.0%

Equity 0 0 0 0 0 0 0.0%

Securitisation

Other exposures 0 0 0 0 0 0 0.0%

Standardised Total 15 0 3 0 0 0 6.3%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

31/12/2015

Luxembourg

31/12/2015

Exposure values Risk exposure amounts Stock of provisionsCoverage Ratio -

Default Stock1

Switzerland

31/12/2015

Exposure values Risk exposure amounts Stock of provisionsCoverage Ratio -

Default Stock1

Spain

Exposure values Risk exposure amounts Stock of provisionsCoverage Ratio -

Default Stock1

2016 EU-wide Stress Test:

Credit risk STALandesbank Hessen-Thüringen Girozentrale

Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central governments or central banks 0 0 0 0 0 0 0.0%

Regional governments or local authorities 0 0 0 0 0 0 0.0%

Public sector entities 0 0 0 0 0 0 0.0%

Multilateral Development Banks 0 0 0 0 0 0 0.0%

International Organisations 0 0 0 0 0 0 0.0%

Institutions 0 0 0 0 0 0 0.0%

Corporates 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Retail 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Secured by mortgages on immovable property 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Items associated with particularly high risk 0 0 0 0 0 0 0.0%

Covered bonds 0 0 0 0 0 0 0.0%

Claims on institutions and corporates with a ST credit assessment 0 0 0 0 0 0 0.0%

Collective investments undertakings (CIU) 0 0 0 0 0 0 0.0%

Equity 0 0 0 0 0 0 0.0%

Securitisation

Other exposures 0 0 0 0 0 0 0.0%

Standardised Total 0 0 0 0 0 0 0.0%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Non-defaulted Defaulted Non-defaulted Defaulted Non-defaulted Defaulted

Central governments or central banks 0 0 0 0 0 0 0.0%

Regional governments or local authorities 0 0 0 0 0 0 0.0%

Public sector entities 0 0 0 0 0 0 0.0%

Multilateral Development Banks 0 0 0 0 0 0 0.0%

International Organisations 0 0 0 0 0 0 0.0%

Institutions 0 0 0 0 0 0 0.0%

Corporates 4 0 4 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Retail 0 0 0 0 0 0 9.5%

of which: SME 0 0 0 0 0 0 0.0%

Secured by mortgages on immovable property 0 0 0 0 0 0 0.0%

of which: SME 0 0 0 0 0 0 0.0%

Items associated with particularly high risk 0 0 0 0 0 0 0.0%

Covered bonds 0 0 0 0 0 0 0.0%

Claims on institutions and corporates with a ST credit assessment 0 0 0 0 0 0 0.0%

Collective investments undertakings (CIU) 0 0 0 0 0 0 0.0%

Equity 0 0 0 0 0 0 0.0%

Securitisation

Other exposures 0 0 0 0 0 0 0.0%

Standardised Total 4 0 4 0 0 0 9.6%1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

31/12/2015

Canada

31/12/2015

Exposure values Risk exposure amounts Stock of provisionsCoverage Ratio -

Default Stock1

Austria

Exposure values Risk exposure amounts Stock of provisionsCoverage Ratio -

Default Stock1

2016 EU-wide Stress Test:

Credit risk STALandesbank Hessen-Thüringen Girozentrale

Central governments or central banks

Regional governments or local authorities

Public sector entities

Multilateral Development Banks

International Organisations

Institutions

Corporates

of which: SME

Retail

of which: SME

Secured by mortgages on immovable property

of which: SME

Items associated with particularly high risk

Covered bonds

Claims on institutions and corporates with a ST credit assessment

Collective investments undertakings (CIU)

Equity

Securitisation

Other exposures

Standardised Total1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Central governments or central banks

Regional governments or local authorities

Public sector entities

Multilateral Development Banks

International Organisations

Institutions

Corporates

of which: SME

Retail

of which: SME

Secured by mortgages on immovable property

of which: SME

Items associated with particularly high risk

Covered bonds

Claims on institutions and corporates with a ST credit assessment

Collective investments undertakings (CIU)

Equity

Securitisation

Other exposures

Standardised Total1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Central governments or central banks

Regional governments or local authorities

Public sector entities

Multilateral Development Banks

International Organisations

Institutions

Corporates

of which: SME

Retail

of which: SME

Secured by mortgages on immovable property

of which: SME

Items associated with particularly high risk

Covered bonds

Claims on institutions and corporates with a ST credit assessment

Collective investments undertakings (CIU)

Equity

Securitisation

Other exposures

Standardised Total1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Landesbank Hessen-Thüringen

Girozentrale

Germany

United States

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

0.0% 0 52.1% 0.0% 0 54.8% 0.0% 0 55.8% 0.0% 0 57.6% 0.0% 0 60.5% 0.0% 0 61.4%

0.1% 5 49.6% 0.1% 11 52.3% 0.1% 17 53.2% 0.1% 7 55.7% 0.1% 15 58.5% 0.1% 22 59.6%

0.0% 9 84.6% 0.0% 10 89.5% 0.0% 10 90.1% 0.1% 10 94.6% 0.1% 11 96.3% 0.0% 12 97.6%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.0% 1 28.8% 0.0% 2 30.2% 0.0% 2 30.8% 0.0% 2 38.6% 0.0% 3 45.2% 0.0% 4 42.5%

0.0% 157 35.8% 0.0% 158 26.1% 0.0% 159 21.6% 0.1% 157 28.0% 0.1% 162 20.5% 0.1% 171 18.1%

0.2% 0 43.2% 0.2% 1 48.2% 0.2% 1 49.6% 0.3% 0 49.5% 0.3% 1 54.7% 0.3% 1 56.1%

0.2% 41 52.6% 0.2% 41 52.8% 0.3% 42 53.0% 0.3% 45 59.2% 0.3% 45 59.3% 0.3% 46 59.3%

0.3% 0 45.2% 0.3% 0 45.6% 0.3% 0 45.8% 0.3% 0 50.8% 0.3% 0 51.2% 0.3% 0 51.5%

0.0% 1 7.2% 0.0% 1 8.5% 0.0% 2 8.9% 0.0% 1 8.1% 0.1% 2 10.5% 0.1% 3 11.4%

0.0% 0 8.4% 0.1% 0 10.5% 0.1% 0 11.0% 0.1% 0 9.5% 0.1% 0 12.4% 0.1% 0 13.7%

0.1% 0 100.0% 0.1% 0 100.0% 0.1% 0 100.0% 0.1% 0 100.0% 0.1% 0 100.0% 0.1% 0 100.0%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.9% 1 100.0% 0.9% 1 100.0% 0.9% 2 100.0% 0.9% 1 100.0% 0.9% 1 100.0% 0.9% 2 100.0%

0.0% 0 40.0% 0.0% 0 42.0% 0.0% 0 42.7% 0.0% 0 40.0% 0.0% 0 42.0% 0.0% 0 42.7%

0.0% 214 38.2% 0.0% 224 29.8% 0.0% 233 25.8% 0.0% 222 32.4% 0.0% 240 25.5% 0.0% 260 23.2%

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

0.0% 0 52.1% 0.0% 0 54.8% 0.0% 0 55.8% 0.0% 0 57.6% 0.0% 0 60.5% 0.0% 0 61.4%

0.1% 5 49.6% 0.1% 11 52.3% 0.1% 17 53.2% 0.1% 7 55.7% 0.1% 15 58.5% 0.1% 22 59.6%

0.0% 0 - 0.0% 0 19.4% 0.0% 0 20.0% 0.0% 0 - 0.0% 0 22.3% 0.0% 0 23.6%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.0% 1 27.5% 0.0% 1 29.0% 0.0% 1 29.7% 0.0% 1 37.8% 0.0% 2 39.5% 0.0% 2 40.1%

0.0% 9 1.5% 0.0% 11 1.7% 0.0% 11 1.4% 0.0% 9 1.1% 0.0% 12 1.3% 0.0% 12 1.2%

0.2% 0 43.2% 0.2% 1 48.2% 0.2% 1 49.6% 0.3% 0 49.5% 0.3% 1 54.7% 0.3% 1 56.1%

0.2% 40 52.9% 0.2% 40 53.1% 0.3% 41 53.2% 0.3% 44 59.6% 0.3% 45 59.6% 0.3% 45 59.6%

0.3% 0 45.3% 0.3% 0 45.7% 0.3% 0 46.0% 0.3% 0 50.9% 0.3% 0 51.3% 0.3% 0 51.6%

0.0% 1 6.6% 0.0% 1 8.5% 0.0% 2 9.0% 0.0% 1 7.4% 0.1% 2 10.1% 0.1% 3 11.4%

0.0% 0 8.4% 0.1% 0 10.5% 0.1% 0 11.0% 0.1% 0 9.5% 0.1% 0 12.4% 0.1% 0 13.7%

0.1% 0 100.0% 0.1% 0 100.0% 0.1% 0 100.0% 0.1% 0 100.0% 0.1% 0 100.0% 0.1% 0 100.0%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.6% 0 65.0% 0.6% 1 68.3% 0.6% 1 69.4% 0.6% 0 65.0% 0.6% 1 68.3% 0.6% 1 69.4%

0.0% 0 40.0% 0.0% 0 42.0% 0.0% 0 42.7% 0.0% 0 40.0% 0.0% 0 42.0% 0.0% 0 42.7%0.0% 55 16.6% 0.0% 65 12.9% 0.0% 73 11.4% 0.0% 62 13.7% 0.0% 75 11.0% 0.0% 86 10.1%

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.0% 8 84.6% 0.0% 8 89.5% 0.0% 9 90.1% 0.1% 9 94.6% 0.1% 10 96.3% 0.0% 10 97.6%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 0 39.5% 0.1% 0 41.7% 0.1% 0 42.5% 0.1% 0 45.2% 0.1% 0 47.4% 0.1% 0 48.3%

0.1% 116 71.0% 0.1% 116 70.8% 0.1% 116 70.7% 0.2% 116 70.9% 0.2% 116 70.8% 0.2% 117 70.7%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.2% 0 43.5% 0.2% 0 43.6% 0.2% 0 43.8% 0.2% 0 49.7% 0.2% 0 49.7% 0.2% 0 49.7%

- 0 43.5% - 0 43.7% - 0 43.8% - 0 49.7% - 0 49.7% - 0 49.7%

0.0% 0 0.0% 0.0% 0 1.2% 0.0% 0 1.5% 0.0% 0 0.0% 0.0% 0 1.9% 0.0% 0 3.0%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 0 100.0% 0.1% 0 100.0% 0.1% 0 100.0% 0.1% 0 100.0% 0.1% 0 100.0% 0.1% 0 100.0%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0% 0.9% 0 100.0%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 125 71.0% 0.0% 125 70.9% 0.0% 126 70.8% 0.1% 125 71.0% 0.1% 127 71.1% 0.1% 127 71.1%

31/12/2018

31/12/2016 31/12/2017 31/12/2018

Baseline Scenario Adverse Scenario

31/12/2016 31/12/2017 31/12/2018 31/12/2016 31/12/2017

Baseline Scenario Adverse Scenario

Baseline Scenario Adverse Scenario

31/12/2016 31/12/2017 31/12/2018

31/12/2018 31/12/2016 31/12/2017 31/12/201831/12/2016 31/12/2017

2016 EU-wide Stress Test:

Credit risk STALandesbank Hessen-Thüringen Girozentrale

Central governments or central banks

Regional governments or local authorities

Public sector entities

Multilateral Development Banks

International Organisations

Institutions

Corporates

of which: SME

Retail

of which: SME

Secured by mortgages on immovable property

of which: SME

Items associated with particularly high risk

Covered bonds

Claims on institutions and corporates with a ST credit assessment

Collective investments undertakings (CIU)

Equity

Securitisation

Other exposures

Standardised Total1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Central governments or central banks

Regional governments or local authorities

Public sector entities

Multilateral Development Banks

International Organisations

Institutions

Corporates

of which: SME

Retail

of which: SME

Secured by mortgages on immovable property

of which: SME

Items associated with particularly high risk

Covered bonds

Claims on institutions and corporates with a ST credit assessment

Collective investments undertakings (CIU)

Equity

Securitisation

Other exposures

Standardised Total1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

Central governments or central banks

Regional governments or local authorities

Public sector entities

Multilateral Development Banks

International Organisations

Institutions

Corporates

of which: SME

Retail

of which: SME

Secured by mortgages on immovable property

of which: SME

Items associated with particularly high risk

Covered bonds

Claims on institutions and corporates with a ST credit assessment

Collective investments undertakings (CIU)

Equity

Securitisation

Other exposures

Standardised Total1 Computed as: Stock of provisions for defaulted stock / default stock (as defined in paragraphs 59 and 61 of the Methodological note)

France

United Kingdom

Netherlands

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 49.6% - 0 49.8% - 0 49.9% - 0 54.6% - 0 54.6% - 0 54.6%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 0 17.2% 0.1% 0 19.0% 0.1% 0 19.5% 0.1% 0 18.9% 0.1% 0 21.1% 0.1% 0 22.2%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 0 49.4% 0.1% 0 49.2% 0.1% 0 49.1% 0.1% 0 54.3% 0.1% 0 54.0% 0.1% 0 53.8%

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.0% 0 45.2% 0.0% 0 47.6% 0.0% 0 48.5% 0.1% 0 50.5% 0.1% 0 53.1% 0.1% 0 53.9%

0.1% 8 90.9% 0.1% 8 89.0% 0.1% 8 87.1% 0.2% 8 90.7% 0.2% 8 88.5% 0.2% 8 86.8%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.2% 0 32.8% 0.2% 0 33.2% 0.2% 0 33.4% 0.2% 0 37.5% 0.2% 0 38.0% 0.2% 0 38.2%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 0 11.6% 0.1% 0 13.1% 0.1% 0 13.6% 0.1% 0 13.2% 0.1% 0 15.2% 0.1% 0 16.2%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

1.6% 0 100.0% 1.6% 0 100.0% 1.6% 0 100.0% 2.0% 0 100.0% 2.0% 0 100.0% 1.7% 0 100.0%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.1% 8 88.3% 0.1% 8 86.5% 0.1% 8 84.8% 0.2% 8 88.3% 0.2% 8 86.3% 0.2% 9 84.7%

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

Impairment

rate

Stock of

Provisions

Coverage Ratio -

Default Stock1

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.0% 0 40.2% 0.0% 0 42.4% 0.0% 0 43.2% 0.1% 0 45.7% 0.1% 0 48.0% 0.1% 0 48.8%

0.0% 9 5.6% 0.0% 9 3.8% 0.0% 9 3.5% 0.0% 9 5.8% 0.0% 9 7.0% 0.0% 9 7.2%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 47.6% - 0 47.7% - 0 47.8% - 0 53.0% - 0 53.0% - 0 53.0%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.0% 0 4.6% 0.0% 0 6.0% 0.0% 0 6.4% 0.0% 0 5.1% 0.0% 0 7.2% 0.0% 0 8.3%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

1.6% 0 100.0% 1.6% 0 100.0% 1.6% 0 100.0% 2.0% 0 100.0% 2.0% 0 100.0% 1.7% 0 100.0%

- 0 - - 0 - - 0 - - 0 - - 0 - - 0 -

0.0% 9 10.2% 0.0% 9 7.9% 0.0% 10 7.5% 0.0% 9 11.7% 0.0% 10 12.2% 0.0% 10 12.4%

Baseline Scenario Adverse Scenario

31/12/2018 31/12/2016 31/12/2017 31/12/2018

Baseline Scenario Adverse Scenario

31/12/2016 31/12/2017

31/12/2018 31/12/2016 31/12/2017 31/12/2018

Baseline Scenario Adverse Scenario

31/12/2016 31/12/2017

31/12/2018 31/12/2016 31/12/2017 31/12/201831/12/2016 31/12/2017

2016 EU-wide Stress Test:

Credit risk STALandesbank Hessen-Thüringen Girozentrale

Central governments or central banks

Regional governments or local authorities

Public sector entities

Multilateral Development Banks

International Organisations

Institutions

Corporates

of which: SME

Retail

of which: SME

Secured by mortgages on immovable property

of which: SME

Items associated with particularly high risk

Covered bonds

Claims on institutions and corporates with a ST credit assessment

Collective investments undertakings (CIU)

Equity