Embed Size (px)

Citation preview

2 0 1 5 A n n u a l R e p o r t

Glatfelter is a global supplier of specialty papers and fiber-based engineered

materials, offering innovation, world-class service and over a century and a half

of technical expertise. Headquartered in York, PA, the company employs over

4,300 people and serves customers in over 100 countries. U.S. operations include

facilities in Pennsylvania and Ohio. International operations include facilities in

Canada, Germany, France, the United Kingdom and the Philippines, and sales and

distribution offices in China and Russia. Glatfelter’s sales approximate $1.7 billion

annually and its common stock is traded on the New York Stock Exchange under the

ticker symbol GLT. Additional information may be found at www.glatfelter.com.

FORWARD-LOOKING STATEMENTS

Certain statements made in this annual report which pertain to future financial and business performance and conditions and other financial

and business matters are “forward-looking statements” within the meaning of the safe harbor provisions of the United States Private

Securities Litigation Reform Act of 1995. These statements are based on management’s current expectations and are subject to numerous

risks, uncertainties and other unpredictable or uncontrollable factors which may cause actual results or performance to differ materially from

the Company’s expectations. Some of the risks, uncertainties and other factors that could cause actual results to differ materially from those

expressed in the forward-looking statements are detailed on page 16 of the accompanying 2015 Annual Report on Form 10-K included

herein and in other filings with the SEC.

1

As Glatfelter entered 2015, we knew that success in a

volatile world economy would demand adaptation and

focused execution. As the year unfolded, we encountered

significant macro-level headwinds that made it difficult

to meet our own and investors’ expectations. A weaker

euro, lower product pricing, the ongoing decline of

the uncoated free sheet market, and geopolitical and

economic issues in Russia/Ukraine combined to restrain

our performance.

In response, Glatfelter PEOPLE remained true to our

strategy of driving growth in our global, fiber-based

engineered materials businesses. We pursued operational

excellence and continuous improvement practices to

reduce costs, improve safety, and better serve customer

needs. A set of aggressive actions was initiated that

helped mitigate the effects of our macro-level challenges.

• $31 million of total cost reductions were achieved,

including a 3.1% workforce reduction, exceeding our

target range.

• Volumes grew in core segments such as tea,

single-serve coffee, technical specialties, and wipes.

• Feminine hygiene shipments increased in the

second half of the year.

• Specialty Papers outperformed the uncoated free

sheet market for the 11th consecutive year.

In addition, Glatfelter PEOPLE achieved another

companywide safety record. We are now approaching

industry top-quartile performance and have the

opportunity to become a safety leader.

During the year, our balance sheet strengthened

as we carefully managed working capital and capital

spending. Higher cash flow supported investments in

compliance-related environmental projects, process

improvement, and growth initiatives. Net debt was

reduced by $46 million, and our dividend was increased

for the third year in a row.

But our many accomplishments were unable

to offset the full impact of the macro-level headwinds.

Adjusted annual earnings in 2015 were down 14%

from the previous year, which impacted our share

price performance.

Dante C. Parrini Chairman and Chief Executive Officer

LOOKING AHEAD

As we look forward to 2016, it’s clear we will

continue to operate in a dynamic global economy.

Glatfelter will leverage the core competencies that have

underpinned our progress and fueled our past success.

• Our close relationships with blue-chip customers

have created binding partnerships that give us leading

positions in global growth markets. Forged over

decades, Glatfelter’s value proposition of providing

premium-quality, value-adding products and services

has engendered loyalty and trust that Glatfelter is their

supplier of choice.

• Our new business development capabilities have

spawned clearly differentiated products that embrace

innovation and specialization to fulfill customer needs.

For example, specialty wipes increased shipments by 44%

over 2014, leveraging an exciting new growth market.

• The scale and diversity of our engineered

materials assets and technical know-how, coupled with

our consistency of service, give global customers the

assurance that Glatfelter will support their needs and

solve their most challenging problems.

D E A R F E L L O W S H A R E H O L D E R S

UNITED STATES SECURITIES AND EXCHANGE COMMISSIONWASHINGTON, D.C. 20549

FORM 10-KÍ Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2015or

‘ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934For the transition period from to

96 South George Street, Suite 520York, Pennsylvania 17401

(Address of principal executive offices)

(717) 225-4711(Registrant’s telephone number, including area code)

Commission file numberExact name of registrant as

specified in its charterIRS Employer

Identification No.State or other jurisdiction ofincorporation or organization

1-03560 P. H. Glatfelter Company 23-0628360 Pennsylvania

Securities registered pursuant to Section 12(b) of the Act:Title of Each Class Name of Each Exchange on which registered

Common Stock, par value $.01 per share New York Stock Exchange

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ‘ No Í.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ‘ No Í.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filingrequirements for the past 90 days. Yes Í No ‘.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data Filerequired to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that theregistrant was required to submit and post such files). Yes Í No ‘.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, tothe best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or anyamendment to this Form 10-K. ‘

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a small reporting company. Seethe definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. Í Largeaccelerated filer ‘ Accelerated filer ‘ Non-accelerated filer ‘ Small reporting company (Do not check if a smaller reporting company).

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes ‘ No Í.

Based on the closing price as of June 30, 2015, the aggregate market value of the Common Stock of the Registrant held by non-affiliates was$940.3 million.

Common Stock outstanding on February 23, 2016 totaled 43,442,171 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the following documents are incorporated by reference in this Annual Report on Form 10-K:

Portions of the registrant’s Proxy Statement to be dated on or about March 31, 2016 are incorporated by reference into Part III.

P. H. GLATFELTER COMPANYANNUAL REPORT ON FORM 10-K

For the Year Ended

DECEMBER 31, 2015Table of Contents

Page

PART IItem 1 Business 1Item 1A Risk Factors 7Item 1B Unresolved Staff Comments 12Item 2 Properties 12Item 3 Legal Proceedings 13

Executive Officers 13Item 4 Mine Safety Disclosures 14

PART IIItem 5 Market for Registrant’s Common Equity,

Related Stockholder Matters and IssuerPurchases of Equity Securities 14Common Stock Prices and Dividends

Declared Information 14Stock Performance Graph 14

Item 6 Selected Financial Data 15Item 7 Management’s Discussion and Analysis of

Financial Condition and Results ofOperations 16Results of Operations 17Liquidity and Capital Resources 25

Critical Accounting Policies and Estimates 28Item 7A Quantitative and Qualitative Disclosures

about Market Risk 29Item 8 Financial Statements and Supplementary

Data 30Report of Independent Registered Public

Accountants 31Statements of Income 33Statements of Comprehensive Income 34Balance Sheets 35Statements of Cash Flows 36Statements of Shareholders’ Equity 37Notes to Consolidated Financial Statements1. Organization 382. Accounting Policies 383. Acquisitions 404. Energy and Related Sales,

Net 415. Gain on Dispositions of Plant,

Equipment andTimberlands 42

6. Asset Impairment Charges 427. Earnings Per Share 428. Accumulated Other

Comprehensive Income 439. Income Taxes 4410. Stock-Based Compensation 4611. Retirement Plans and Other

Post-Retirement Benefits 47

Page

12. Inventories 5013. Plant, Equipment and

Timberlands 5014. Goodwill and Intangible

Assets 5015. Other Long-Term Assets 5016. Other Current Liabilities 5117. Long-Term Debt 5118. Asset Retirement Obligation 5219. Fair Value of Financial

Instruments 5320. Financial Derivatives and

Hedging Activities 5321. Shareholders’ Equity 5422. Share Repurchases 5523. Commitments, Contingencies

and Legal Proceedings 5524. Segment and Geographic

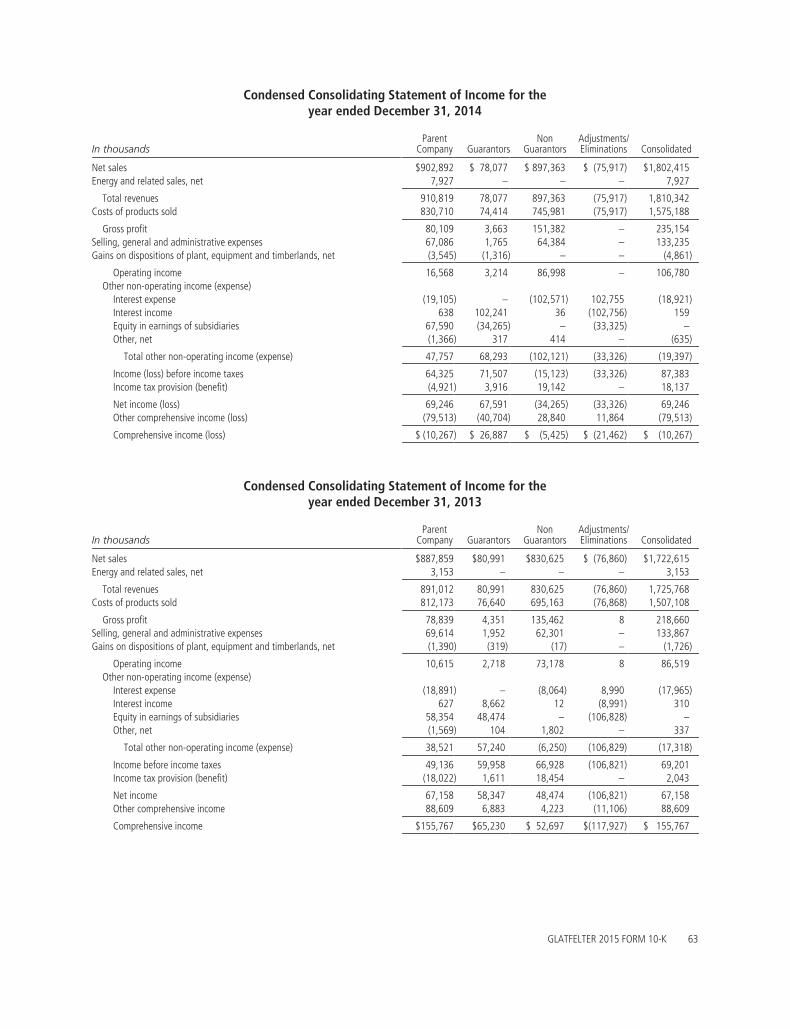

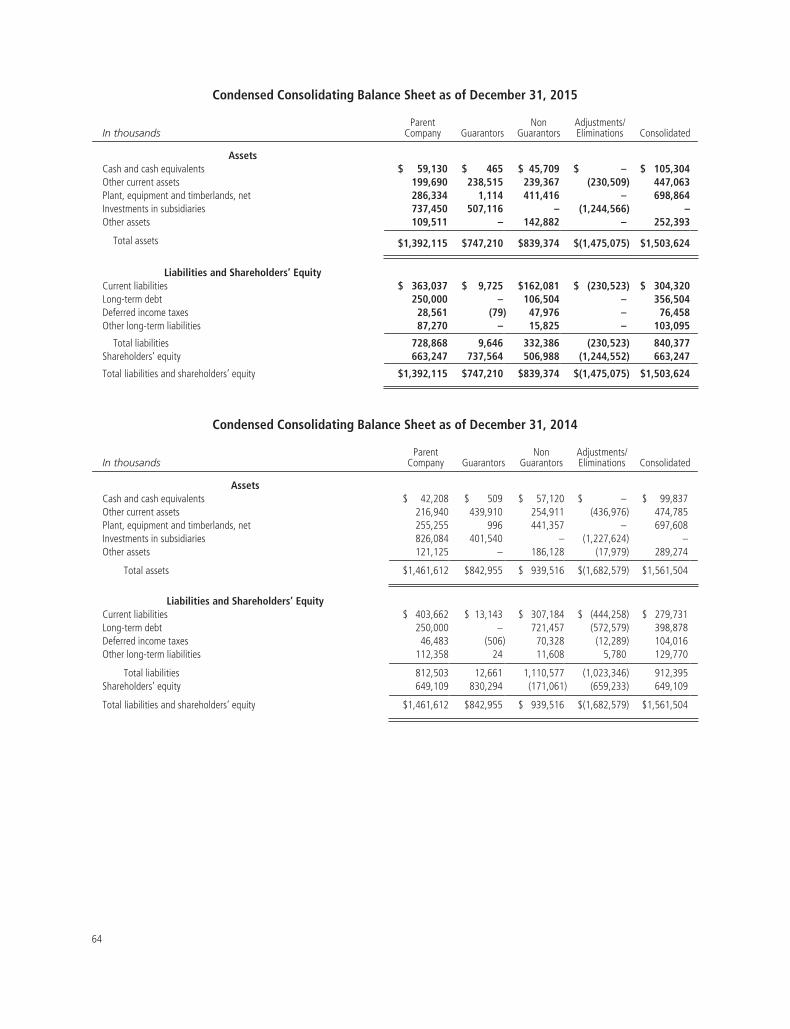

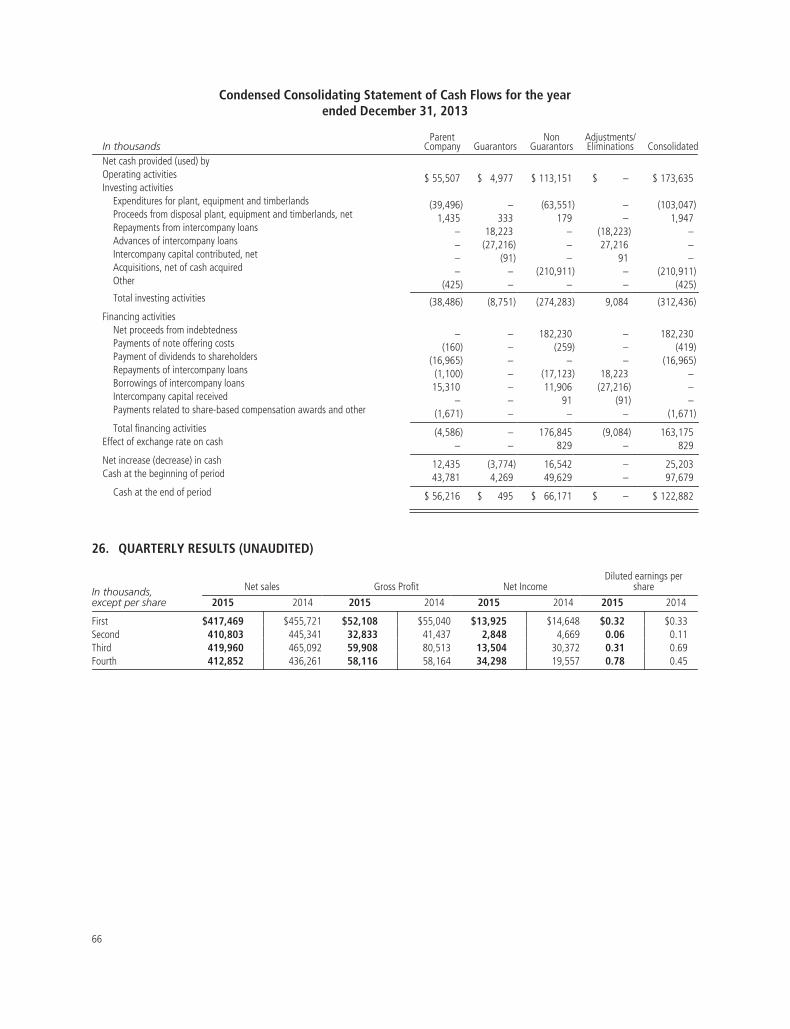

Information 5925. Condensed Consolidating

Financial Statements 6226. Quarterly Results (Unaudited) 66

Item 9 Changes in and Disagreements WithAccountants on Accounting and FinancialDisclosures 67

Item 9A Controls and Procedures 67Item 9B Other Information 67

PART IIIItem 10 Directors, Executive Officers and Corporate

Governance 67Item 11 Executive Compensation 67Item 12 Security Ownership of Certain Beneficial

Owners and Management and RelatedStockholder Matters 67

Item 13 Certain Relationships and RelatedTransactions, and Director Independence 67

Item 14 Principal Accountant Fees and Services 67

PART IVItem 15 Exhibits, Financial Statement Schedules 68

Signatures 71

Schedule II 73

PART I

P. H. Glatfelter Company makes regular filings withthe Securities and Exchange Commission (“SEC”),including this Annual Report on Form 10-K, as well asQuarterly Reports on Form 10-Q and Current Reports onForm 8-K. These filings are available, free of charge, on ourwebsite, www.glatfelter.com, and the SEC’s website atwww.sec.gov. We also provide copies of our SEC filings atno charge upon request to Investor Relations at (717) 225-2719, [email protected], or by mail to Investor Relations,96 South George Street, Suite 520, York, PA, 17401. Inthis filing, unless the context indicates otherwise, the terms“we,” “us,” “our,” “the Company,” or “Glatfelter” referto P. H. Glatfelter Company and subsidiaries.

ITEM 1 BUSINESS

Overview Glatfelter began operations in 1864,and we believe we are one of the world’s leadingmanufacturers of specialty papers and fiber-basedengineered materials. Headquartered in York,Pennsylvania, we own and operate manufacturing facilitiesin Pennsylvania, Ohio, Canada, Germany, the UnitedKingdom, France, and the Philippines and we have salesand distribution offices in Russia and China.

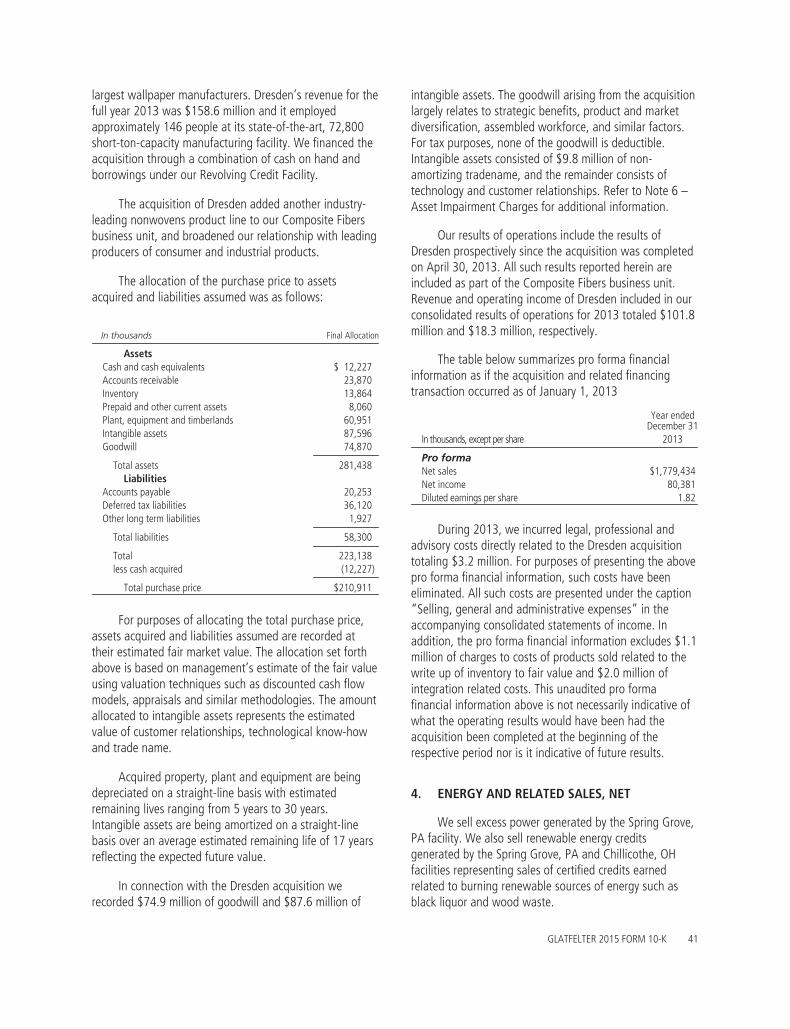

Acquisitions Over the past several years, we havecompleted a number of acquisitions that have diversifiedour revenue, expanded our geographic footprint andenhanced our asset base. The most recent transactionsinclude the April 2013, $211 million acquisition of DresdenPapier GmbH (“Dresden”) and the October 2014, $8.0million acquisition of Spezialpapierfabrik OberschmittenGmbH (“SPO”). Dresden is a leading supplier of nonwovenwall covering products with annual revenues ofapproximately $160 million in the year of acquisition. SPOis a producer of highly technical papers for a wide range ofelectrical applications with annual sales of approximately$33 million. Both of these businesses operate within ourComposite Fibers business unit.

Products Our three business units manufactureand distribute a wide array of specialty papers and fiber-based engineered materials including:

• Composite Fibers with revenue from the sale ofsingle-serve tea and coffee filtration papers,nonwoven wall covering materials, metallizedpapers, composite laminates papers, and manytechnically special papers including substrates forelectrical applications;

• Advanced Airlaid Materials with revenue fromthe sale of airlaid nonwoven fabric-like materialsused in feminine hygiene and adult incontinenceproducts, wipes, and other airlaid applications;and

• Specialty Papers with revenue from the sale ofpapers for carbonless and other forms, envelopes,book publishing, and engineered products such aspapers for high-speed ink jet printing, officespecialty products, greeting cards, packaging,casting, release, transfer, playing card, postal,FDA-compliant food and beverage applications,and other niche specialty applications.

The global growth markets served by the CompositeFibers and Advanced Airlaid Materials business units arecharacterized by attractive growth rates as the result ofemerging products and markets, changing end-userpreferences and evolving demographics. Specialty Papersserves more mature market segments, many of which arein decline.

As a result of our strategy to diversify sources ofrevenue and invest in growth businesses, revenuegenerated from Composite Fibers and Advanced AirlaidMaterials is expected to represent an increasingly greaterproportion of total revenue. Combined, these two businessunits comprised 47% of our total net sales in 2015compared with 30% in 2006.

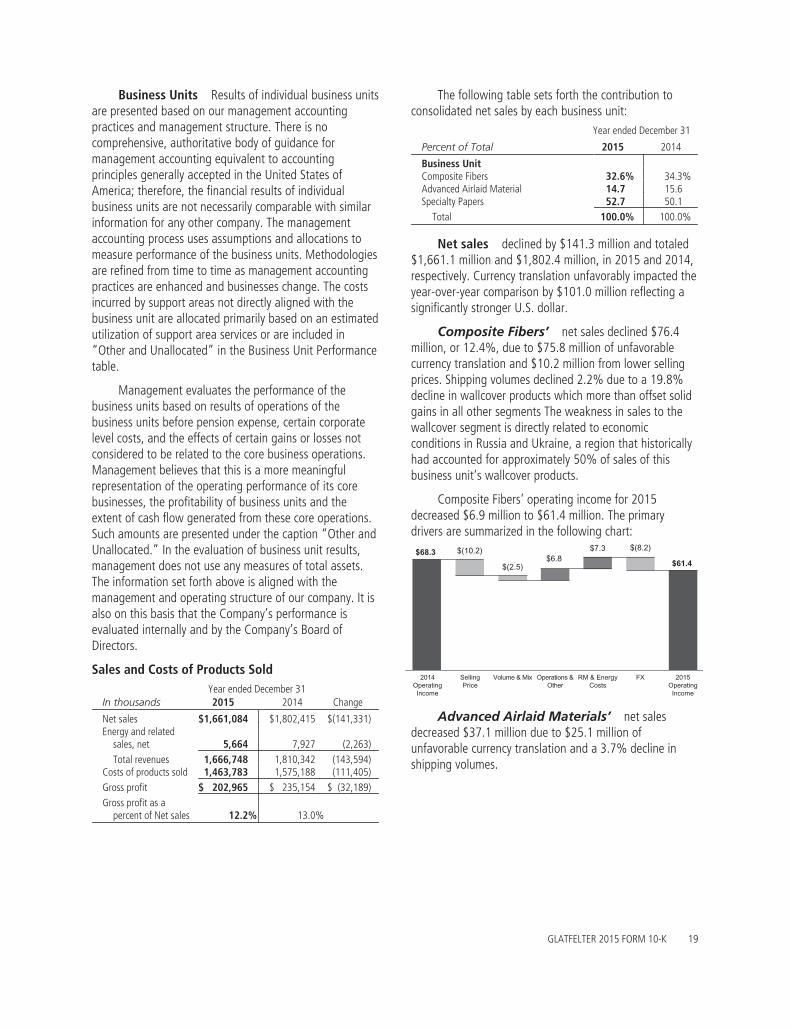

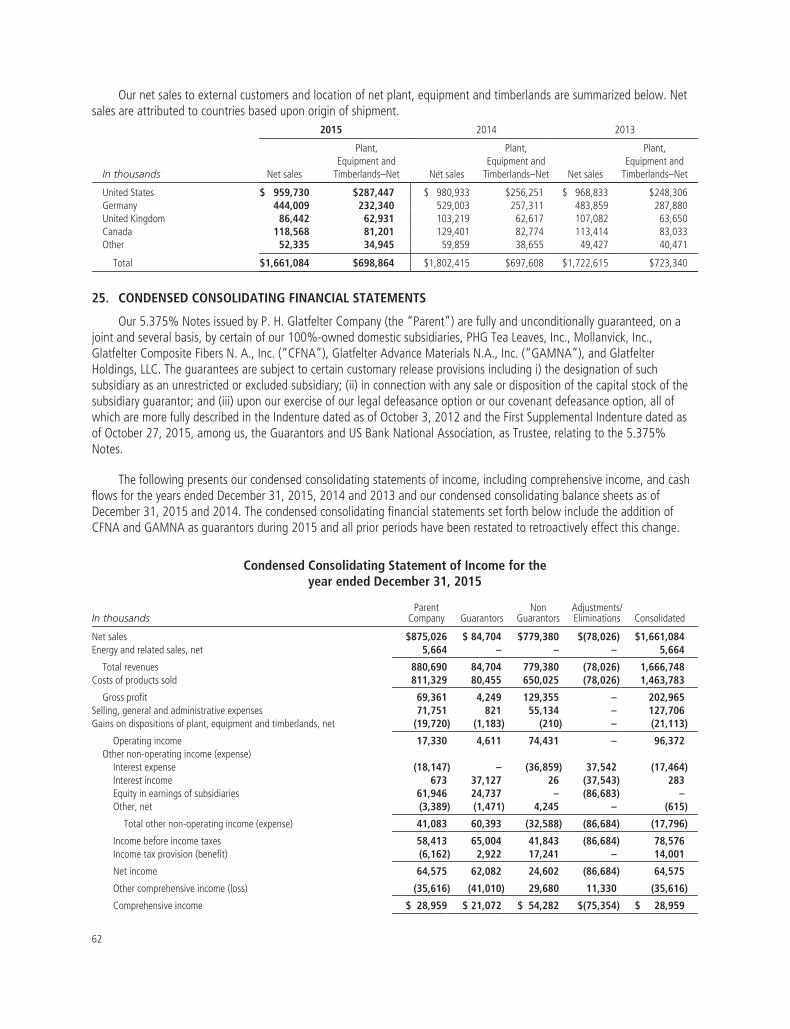

Consolidated net sales and the relative net salescontribution of each of our business units for the pastthree years are summarized below:

Dollars in thousands 2015 2014 2013

Net sales $1,661,084 $1,802,415 $1,722,615Business unit

contributionComposite Fibers 32.6% 34.3% 32.9%Advanced Airlaid

Materials 14.7 15.6 15.6Specialty Papers 52.7 50.1 51.5

Total 100.0% 100.0% 100.0%

Strategy Our strategy is focused on growingrevenues, organically and by acquisition, in our key globalgrowth markets including single-serve coffee and tea,nonwoven wall covering materials, electrical products,hygiene and wipes products, and other technical materials.We partner with leading consumer product companies andother market leaders to provide innovative products withoutstanding performance to meet market requirements.Over the past several years, we have made investments toincrease production capacity and improve our technicalcapabilities to ensure we are best positioned to serve the

GLATFELTER 2015 FORM 10-K 1

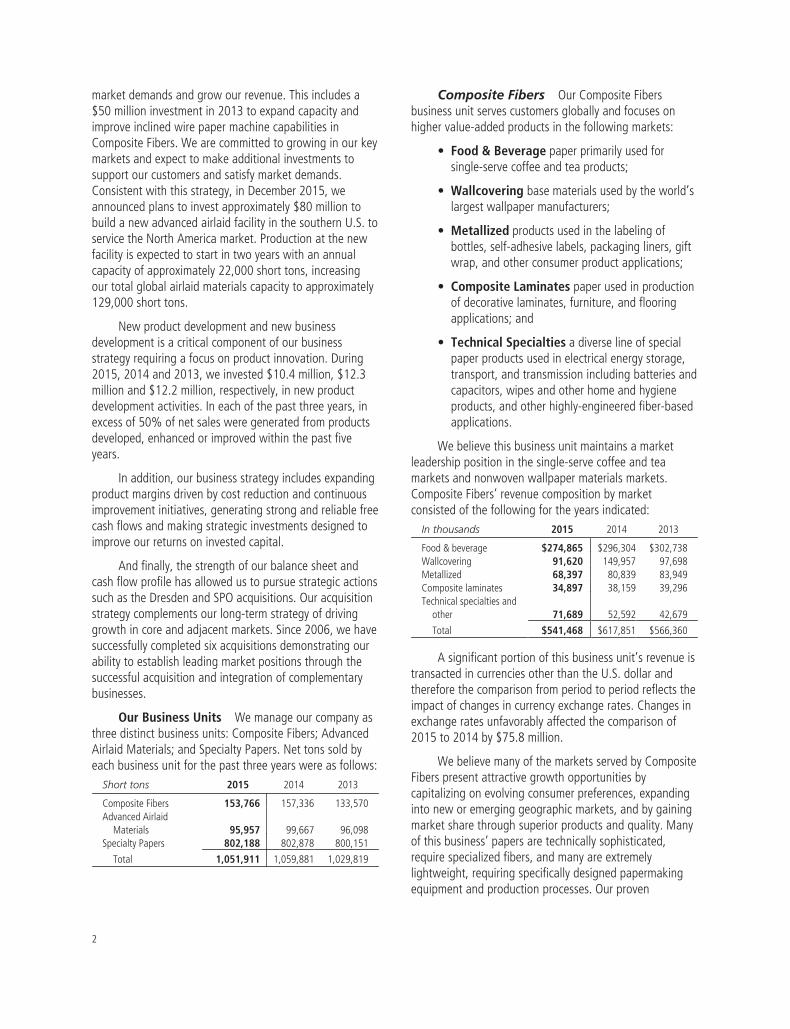

market demands and grow our revenue. This includes a$50 million investment in 2013 to expand capacity andimprove inclined wire paper machine capabilities inComposite Fibers. We are committed to growing in our keymarkets and expect to make additional investments tosupport our customers and satisfy market demands.Consistent with this strategy, in December 2015, weannounced plans to invest approximately $80 million tobuild a new advanced airlaid facility in the southern U.S. toservice the North America market. Production at the newfacility is expected to start in two years with an annualcapacity of approximately 22,000 short tons, increasingour total global airlaid materials capacity to approximately129,000 short tons.

New product development and new businessdevelopment is a critical component of our businessstrategy requiring a focus on product innovation. During2015, 2014 and 2013, we invested $10.4 million, $12.3million and $12.2 million, respectively, in new productdevelopment activities. In each of the past three years, inexcess of 50% of net sales were generated from productsdeveloped, enhanced or improved within the past fiveyears.

In addition, our business strategy includes expandingproduct margins driven by cost reduction and continuousimprovement initiatives, generating strong and reliable freecash flows and making strategic investments designed toimprove our returns on invested capital.

And finally, the strength of our balance sheet andcash flow profile has allowed us to pursue strategic actionssuch as the Dresden and SPO acquisitions. Our acquisitionstrategy complements our long-term strategy of drivinggrowth in core and adjacent markets. Since 2006, we havesuccessfully completed six acquisitions demonstrating ourability to establish leading market positions through thesuccessful acquisition and integration of complementarybusinesses.

Our Business Units We manage our company asthree distinct business units: Composite Fibers; AdvancedAirlaid Materials; and Specialty Papers. Net tons sold byeach business unit for the past three years were as follows:

Short tons 2015 2014 2013

Composite Fibers 153,766 157,336 133,570Advanced Airlaid

Materials 95,957 99,667 96,098Specialty Papers 802,188 802,878 800,151

Total 1,051,911 1,059,881 1,029,819

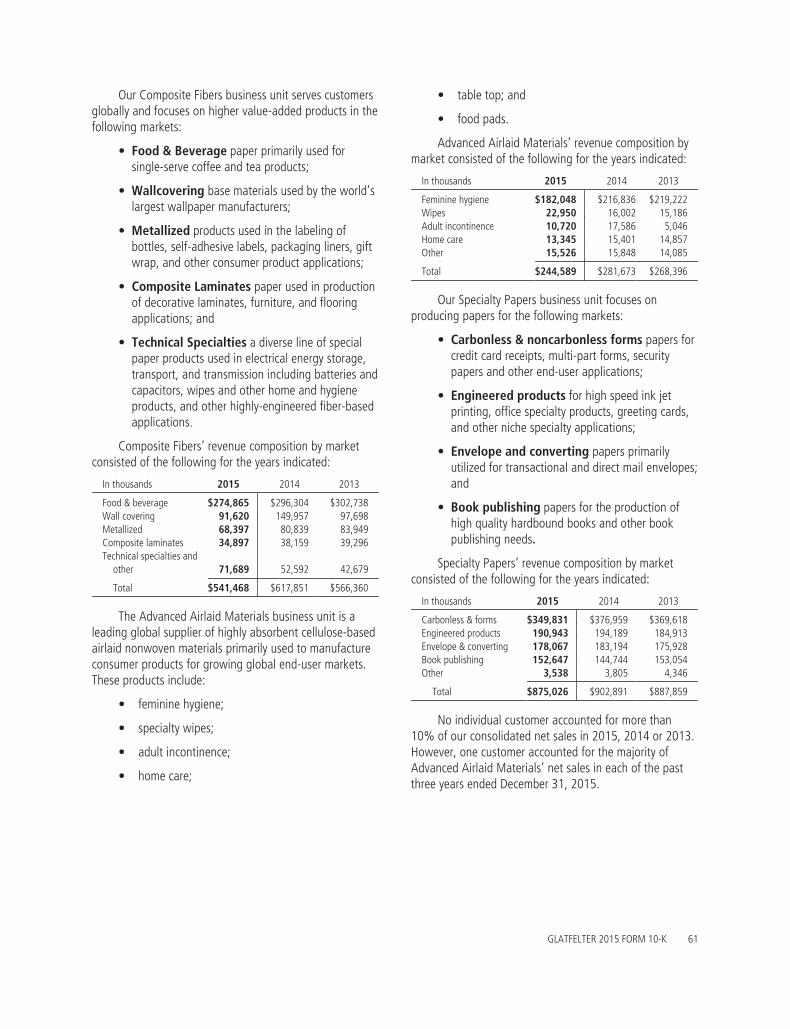

Composite Fibers Our Composite Fibersbusiness unit serves customers globally and focuses onhigher value-added products in the following markets:

• Food & Beverage paper primarily used forsingle-serve coffee and tea products;

• Wallcovering base materials used by the world’slargest wallpaper manufacturers;

• Metallized products used in the labeling ofbottles, self-adhesive labels, packaging liners, giftwrap, and other consumer product applications;

• Composite Laminates paper used in productionof decorative laminates, furniture, and flooringapplications; and

• Technical Specialties a diverse line of specialpaper products used in electrical energy storage,transport, and transmission including batteries andcapacitors, wipes and other home and hygieneproducts, and other highly-engineered fiber-basedapplications.

We believe this business unit maintains a marketleadership position in the single-serve coffee and teamarkets and nonwoven wallpaper materials markets.Composite Fibers’ revenue composition by marketconsisted of the following for the years indicated:

In thousands 2015 2014 2013

Food & beverage $274,865 $296,304 $302,738Wallcovering 91,620 149,957 97,698Metallized 68,397 80,839 83,949Composite laminates 34,897 38,159 39,296Technical specialties and

other 71,689 52,592 42,679

Total $541,468 $617,851 $566,360

A significant portion of this business unit’s revenue istransacted in currencies other than the U.S. dollar andtherefore the comparison from period to period reflects theimpact of changes in currency exchange rates. Changes inexchange rates unfavorably affected the comparison of2015 to 2014 by $75.8 million.

We believe many of the markets served by CompositeFibers present attractive growth opportunities bycapitalizing on evolving consumer preferences, expandinginto new or emerging geographic markets, and by gainingmarket share through superior products and quality. Manyof this business’ papers are technically sophisticated,require specialized fibers, and many are extremelylightweight, requiring specifically designed papermakingequipment and production processes. Our proven

2

capability to produce these demanding products and ourcustomer orientation positions us well to compete in theseglobal markets.

During 2013, we completed the acquisition ofDresden, a leading global supplier of nonwoven wallpaperbase materials. The Dresden acquisition added anotherindustry-leading nonwovens product line to our CompositeFibers business, and broadened our relationship withleading producers of consumer and industrial products.Dresden produces products with superior performance andcharacteristics such as dry strip-ability, higher tearresistance, and no material shrinkage or expansion whenwet. However, since late 2014, demand for and pricing ofDresden’s products has been adversely impacted by thegeopolitical and economic conditions in Russia andUkraine, countries from which Dresden generates asignificant portion of its revenue.

The primary raw materials used in the production ofour lightweight papers are abaca pulp, wood pulp andsynthetic fibers. Abaca pulp is a specialized pulp withlimited sources of availability. Sufficient quantities of abacapulp and its source fiber are required to support growth inthis business unit. Our abaca pulp production process,fulfilled by our Philippine mill, provides a unique advantageto our Composite Fibers business unit. In the event thesupply of abaca fiber becomes constrained or whenproduction demands exceed the capacity of the Philippinesmill, alternative sources and/or substitute fibers are used tomeet customer demands.

The Composite Fibers business unit is comprised offour paper making facilities (Germany, France andEngland), a nonwoven wall cover base mill (Germany),metallizing operations (Wales and Germany) and a pulpmill (the Philippines). The combined attributes of thefacilities are summarized as follows:

ProductionCapacity

(short tons)

Principal RawMaterial(“PRM”)

Estimated AnnualQuantity of PRM

(short tons)

154,000 lightweightand other Abaca pulp 17,300

Wood pulp 95,000Synthetic fiber 22,000

28,000 metallized Base stock 28,00018,000 abaca pulp Abaca fiber 27,000

Composite Fibers’ lightweight products are producedusing highly specialized inclined wire paper machinetechnology and we believe we currently maintainapproximately 25% of the global inclined wire capacity.

In addition to critical raw materials, the cost toproduce Composite Fibers’ products is influenced byenergy. Although the business unit generates all of itssteam needed for production, in 2015, it purchased 75%of its electricity.

In Composite Fibers’ markets, competition is productline specific as the necessity for technical expertise andspecialized manufacturing equipment limits the number ofcompanies offering multiple product lines. The followingchart summarizes key competitors by market segment:

Market segment Competitor

Single serve coffee & tea Ahlstrom, Purico, MB Papelesand Zhejiang Kan

Nonwoven wallcovering Ahlstrom, Technocell, Neu Kaliss,and Goznak

Composite laminates Schweitzer-Maudit, Purico, MBPapeles and Oi Feng

Metallized AR Metallizing, Torras PapelNovelis, Vaassen, GalileoNanotech, and Wenzhou ProtecVacuum Metallizing Co.

Our strategy in Composite Fibers is focused on:

• capitalizing on growing global markets in food &beverage, electrical products and dispersiblewipes;

• maximizing capacity utilization provided by theinvestment in state-of-the-art inclined wiretechnology to support consistent growth of keymarkets;

• enhancing product mix across all markets byutilizing new product and new businessdevelopment capabilities;

• implementing continuous improvementmethodologies to increase productivity, reducecosts and expand capacity; and

• ensuring readily available access to specialized rawmaterial requirements to support projectedgrowth.

As part of our commitment to realizing the growthpotential of certain of this business unit’s markets, in 2013we completed a $50 million investment to expand ourinclined wire capacity by nearly 20%, or approximately10,500 short tons. In addition, the 2014 acquisition of SPOfurthers our strategy of capitalizing on the fast-growingelectrical market by broadening our electrical papersplatform and know-how.

GLATFELTER 2015 FORM 10-K 3

Advanced Airlaid Materials Our AdvancedAirlaid Materials business unit is a leading global supplierof highly absorbent cellulose-based airlaid nonwovenmaterials primarily used to manufacture consumer productsfor growing global end-user markets. These productsinclude:

• feminine hygiene;

• specialty wipes;

• adult incontinence;

• home care;

• table top; and

• food pads.

Advanced Airlaid Materials serves customers who areindustry leading consumer product companies as well asprivate-label converters for feminine hygiene, adultincontinence and specialty wipes products. We believe thisbusiness unit holds leading market share positions in manyof the markets it serves. Advanced Airlaid Materials hasdeveloped long-term customer relationships throughsuperior quality, customer service, and a reputation forquickly bringing product and process innovations tomarket.

Advanced Airlaid Materials’ revenue composition bymarket consisted of the following for the years indicated:

In thousands 2015 2014 2013

Feminine hygiene $182,048 $216,836 $219,222Wipes 22,950 16,002 15,186Adult incontinence 10,720 17,586 5,046Home care 13,345 15,401 14,857Other 15,526 15,848 14,085

Total $244,589 $281,673 $268,396

A significant portion of this business unit’s revenue istransacted in currencies other than the U.S. dollar andtherefore the comparison from period to period reflects theimpact of changes in currency exchange rates. Changes inexchange rates unfavorably affected the comparison of2015 to 2014 by $25.1 million.

The feminine hygiene category accounted for 74% ofAdvanced Airlaid Material’s revenue in 2015. The majorityof sales of this product are to a small group of large,leading global consumer products companies. Thesemarkets are considered to be more growth oriented due topopulation growth in certain geographic regions andchanging consumer preferences. In developing regions,demand is also influenced by increases in disposableincome and cultural preferences. The airlaid wipes market

presents attractive growth opportunities and as a result,we are investing approximately $80 million over the nexttwo years to build a new advanced airlaid facility in theUnited States.

The Advanced Airlaid Materials business unitoperates state-of-the-art facilities in Falkenhagen,Germany and Gatineau, Canada. The Falkenhagen locationoperates three multi-bonded production lines and threeproprietary single-lane festooners. The Gatineau locationconsists of two airlaid production lines employing multi-bonded and thermal-bonded airlaid technologies and twoproprietary single-lane festooners.

The business unit’s two facilities operate with thefollowing combined attributes:

Airlaid ProductionCapacity (short tons)

Principal RawMaterial (“PRM”)

Estimated AnnualQuantity of PRM

(short tons)

107,000 Fluff pulp 75,000

In addition to the cost of critical raw materials,production cost is impacted by energy. Advanced AirlaidMaterials purchases substantially all of the electricity andnatural gas used in its operations. Approximately 90% ofthis business unit’s revenue is earned under contracts withpass-through provisions directly related to the price of keyraw material costs.

Advanced Airlaid Materials continues to be atechnology and product innovation leader in technicallydemanding segments of the airlaid market, most notablyfeminine hygiene. This business unit’s airlaid materialproduction employs multi-bonded and thermal-bondedairlaid technologies as opposed to other methods such ashydrogen-bonding. We believe that its facilities are amongthe most modern and flexible airlaid facilities in the world,allowing it to produce at industry leading operating rates.Its proprietary single-lane festooning technology providesconverting and product packaging which supportsefficiency optimization by the customers convertingprocesses. This business unit’s in-house technical expertise,combined with significant capital investment requirementsand rigorous customer expectations creates large barriersto entry for new competitors.

The following summarizes this business unit’s keycompetitors:Market segment Competitor

Airlaid products Georgia-Pacific LLC, Fitesa,McAirlaid’s GmbH, Domtar

4

The global markets served by this business unit arecharacterized by attractive growth opportunities. To takeadvantage of this, our strategy is focused on:

• maintaining and expanding relationships withcustomers that are market-leading consumerproduct companies as well as companiesdistributing through private label arrangements;

• capitalizing on our product and process innovationcapabilities;

• expanding geographic reach of markets served;

• optimizing the use of existing production capacity;and

• employing continuous improvement methodologiesand initiatives to reduce costs, improve efficienciesand create additional capacity.

Specialty Papers Our North America-basedSpecialty Papers business unit focuses on producing papersfor the following markets:

• Carbonless & non-carbonless forms papersfor credit card receipts, multi-part forms, securitypapers and other end-user applications;

• Engineered products for high speed ink jetprinting, office specialty products, greeting cards,and other niche specialty applications;

• Envelope and converting papers primarilyutilized for transactional and direct mail envelopes;and

• Book publishing papers for the production ofhigh-quality hardbound books and other bookpublishing needs.

This business unit produces both commodity productsand higher-value-added specialty products. SpecialtyPapers’ revenue composition by market consisted of thefollowing for the years indicated:

In thousands 2015 2014 2013

Carbonless & forms $349,831 $376,959 $369,618Engineered products 190,943 194,189 184,913Envelope & converting 178,067 183,194 175,928Book publishing 152,647 144,744 153,054Other 3,538 3,805 4,346

Total $875,026 $902,891 $887,859

Many of the market segments served by SpecialtyPapers are characterized by declining demand resulting inexcess capacity, lower operating rates and pricing pressure.As a result, over the past several years, certain producershave closed, reduced or repurposed production capacity in

an attempt to bring supply balance to the market. Inaddition, foreign producers have created additionalimbalance by shipping product to the U.S. when marketpricing is favorable or the U.S. dollar is stronger.Maintaining the supply and demand balance will requirethe industry to continually remove capacity sufficient tomatch declining demand.

Despite our exposure to declining markets, in each ofthe past eleven years, we have outperformed the broaderuncoated free sheet market in terms of shipping volume.We have been successful at maintaining this businessunit’s shipments by leveraging the flexibility of our assetbase to respond to new product and new businessdevelopment opportunities, efficiently responding tochanging customer demands and delivering superiorcustomer service.

We are one of the leading suppliers of carbonless andbook publishing papers in the United States. Although themarkets for these products are declining, we have beensuccessful in executing our strategy to replace this lostvolume with products such as envelope papers, businessforms, and other value-added specialty engineeredproducts. Specialty Papers’ envelope papers market is alsodeclining, however we have leveraged our customer servicecapabilities and geographic locations to grow our marketshare in each of the last several years.

Specialty Papers’ highly technical engineered productsinclude high speed ink jet printing products, office specialtyproducts, greeting cards, packaging, casting, release,transfer, playing card, postal, FDA-compliant food and otherniche specialty applications. Such products comprise an arrayof distinct business niches that are in a continuous state ofevolution. Many of these products are utilized fordemanding, specialized customer and end-user applications.Some of our products are new and higher growth whileothers are more mature and further along in the product lifecycle. Because many of these products are technicallycomplex and involve substantial customer-supplierdevelopment collaboration, they typically command higherper ton prices and generally exhibit greater pricing stabilityrelative to commodity grade paper products.

The Specialty Papers business unit operates twointegrated pulp and paper making facilities with thefollowing combined attributes:Uncoated ProductionCapacity(short tons)

Principal RawMaterial (“PRM”)

Estimated AnnualQuantity of PRM

(short tons)

820,000 Pulpwood 2,327,250Wood-and other pulps 708,000

GLATFELTER 2015 FORM 10-K 5

This business unit’s pulp mills have a combined pulpmaking capacity of 615,000 tons of bleached pulp peryear. The principal raw material used to produce pulp ispulpwood, including both hardwoods and softwoods.Pulpwood is obtained from a variety of locations includingthe states of Pennsylvania, Maryland, Delaware, NewJersey, New York, West Virginia, Virginia, Kentucky, Ohioand Tennessee. To protect our sources of pulpwood, weactively promote conservation and forest managementamong suppliers and woodland owners.

The Spring Grove facility includes five uncoated papermachines as well as an off-line combi-blade coater and aSpecialty Coater which together provide annual productioncapacity for coated paper of approximately 65,000 tons.The Chillicothe facility operates four paper machinesproducing uncoated and carbonless paper. Two of themachines have built-in coating capability which along withthree additional coaters at the facility provide annualcoated capacity of approximately 126,000 tons.

In addition to critical raw materials, the cost to produceSpecialty Papers’ products is influenced by energy. Althoughthe business unit generates all of its steam needed forproduction at both facilities and generates more power than itconsumes at the Spring Grove, PA facility, it purchasedapproximately 25% of its electricity needed for the Chillicothe,OH mill in 2015. The facilities’ source of fuel is primarily coaland, to a lesser extent, natural gas. As discussed more fullyunder “Environmental Matters,” in order to comply with newair quality regulations, we will be implementing modificationsthat will convert certain boilers to burn natural gas rather thancoal. As a result, the consumption of natural gas will increasesignificantly in late 2016 and beyond.

In Specialty Papers’ markets, competition is product linespecific due to the necessity for technical expertise andspecialized manufacturing for certain products. The followingchart summarizes key competitors by market segment:Market segment Competitor

Carbonless paper Appvion, Inc., and to a lesserextent, Fibria Celulose, KoehlerPaper, Mitsubishi Paper, NekoosaCoated Products and Asia Pulpand Paper Co.

Engineered products Specialty papers divisions ofInternational Paper, DomtarCorp., Packaging Corp, and SappiLimited, among others.

Envelope & converting Domtar and International Paper

Book publishing Domtar Corp., North PacificPaper (NORPAC), Resolute Forestand others

Customer service, product performance, technologicaladvances and product pricing are important competitivefactors with respect to all our products. We believe ourreputation in these areas continues to be excellent.

To be successful in the market environment in whichSpecialty Papers operates, our strategy is focused on:

• new product and new business developmentcapabilities to ensure optimal utilization of ourcapacity and to maximize margins;

• leveraging our flexible operating platform tooptimize product mix by shifting production amongthe machines in our system to more closely matchoutput with changing demand trends;

• utilizing ongoing continuous improvementmethodologies to ensure operational efficienciesand asset reliability; and

• maintaining superior customer service.

Additional financial information for each of ourbusiness units is included in Item 7 – Management’sDiscussion and Analysis of Financial Condition and Resultsof Operations and in Item 8 – Financial Statements andSupplementary Data, Note 24 including geographicrevenue and long-lived asset financial information.

Concentration of Customers For each of thepast three years, no single customer represented morethan 10% of our consolidated net sales. However, asdiscussed in Item 1A Risk Factors, one customer accountedfor the majority of Advanced Airlaid Materials net sales in2015, 2014 and 2013.

Capital Expenditures Our business is capitalintensive and requires significant expenditures for new andenhanced equipment. These capital investments arenecessary to support growth strategies, research anddevelopment initiatives, environmental compliance, and fornormal upgrades or replacements. Capital expenditurestotaled $99.9 million, $66.0 million and $103.0 million, in2015, 2014 and 2013, respectively. For 2016, capitalexpenditures are estimated as follows:

In millions

Normal capital expenditures $ 70 – $ 80Major Projects

AMBU capacity expansion 40 – 45SPBU environmental compliance 40 – 45

Total $150 – $170

Environmental Matters We are subject tovarious federal, state and local laws and regulationsintended to protect the environment as well as human

6

health and safety. At various times, we have incurredsignificant costs to comply with these regulations and wecould incur additional costs as new regulations aredeveloped or regulatory priorities change.

We have incurred and will incur additional materialcapital costs to comply with upcoming air qualityregulations including the U.S. EPA Best Available RetrofitTechnology rule (BART; otherwise known as the RegionalHaze Rule) and the Boiler Maximum Achievable ControlTechnology rule (Boiler MACT). These rules require processmodifications and/or upgrades of air pollution controls onboilers at two of our facilities. We have begun convertingor replacing five coal-fired boilers to natural gas andupgrading site infrastructure to accommodate the newboilers, including connecting to gas supply. The total costof these projects is estimated at $85 million to $90 million,of which $33.0 million has been incurred through the endof 2015. The balance of the related spending should besubstantially completed in 2016.

We are a defendant in the Fox River environmentalmatter. Although this matter is the subject of extensive andongoing litigation, during 2015, we spent $9.7 million forremediation activities, and possibly may spend a similaramount in 2016. For a more complete discussion of thismatter, see Item 8 – Financial Statements andSupplementary Data – Note 23.

Employees As of December 31, 2015, weemployed 4,375 people worldwide, of whichapproximately 75% are unionized. The UnitedSteelworkers International Union and the Office andProfessional Employees International Union represents1,446 hourly employees at our Chillicothe, OH and SpringGrove, PA facilities under labor contracts expiring inAugust 2016 for Chillicothe and January 2017 for SpringGrove. Hourly employees at each of our internationallocations are represented by various unions or workscouncils. We consider the overall relationship with ouremployees to be satisfactory.

Other Available Information The CorporateGovernance page of our website includes the Company’sGovernance Principles, Code of Business Conduct, andbiographies of our Board of Directors and ExecutiveOfficers. In addition, the website includes charters of theAudit, Compensation, Finance, and Nominating andCorporate Governance Committees of the Board ofDirectors. The Corporate Governance page also includesthe Code of Business Ethics for the CEO and SeniorFinancial Officers of Glatfelter, our “whistle-blower” policyand other related material. We satisfy the disclosurerequirement for any future amendments to, or waivers

from, our Code of Business Conduct or Code of BusinessEthics for the CEO and Senior Financial Officers by postingsuch information on our website. We will provide a copy ofthe Code of Business Conduct or Code of Business Ethicsfor the CEO and Senior Financial Officers, without charge,to any person who requests one, by contacting InvestorRelations at (717) 225-2719, [email protected] or by mailto 96 South George Street, Suite 520, York, PA, 17401.

ITEM 1A RISK FACTORS

Our business and financial performancemay be adversely affected by a weakglobal economic environment ordownturns in the target markets that weserve.

Adverse global economic conditions could impact ourtarget markets resulting in decreased demand for ourproducts. Our results could be adversely affected ifeconomic conditions weaken or fail to improve. In theevent of significant currency weakening in the countriesinto which our products are sold, demand for or pricing ofour products could be adversely impacted. Also, there maybe periods during which demand for our products isinsufficient to enable us to operate our production facilitiesin an economical manner. As a result, we may be forced totake machine downtime. The economic environment mayalso cause customer insolvencies which may result in theirinability to satisfy their financial obligations to us. Theseconditions are beyond our control and may have asignificant impact on our sales and results of operations.

Approximately $75 million of our revenue in 2015was earned from customers located in Ukraine, Russia andmembers of the Commonwealth of Independent States(also known as “CIS”). Uncertain geo-political andeconomic conditions in this region and weak currencieshave and may continue to cause weak demand for ourproducts as well as volatility in our customers buyingpatterns.

Approximately 28% of our net sales in 2015 wereshipped to customers in Europe, the demand for which isdependent on economic conditions in this area, or to theextent such customers do business outside of Europe, inother regions of the world. Uncertain economic conditionsin this region may cause weakness in demand for ourproducts as well as volatility in our customers buyingpatterns.

GLATFELTER 2015 FORM 10-K 7

Foreign currency exchange ratefluctuations could adversely affect ourresults of operations.

A significant proportion of our revenue is generatedfrom operations outside of the United States. We own andoperate manufacturing facilities in Canada, Germany,France, the United Kingdom and the Philippines. Asignificant portion of our business is transacted in currenciesother than the U.S. dollar such as euros, British pound,Canadian dollars or Philippine peso. Our euro denominatedrevenue exceeds euro expenses by approximately €120million. With respect to the British pound, Canadian dollar,and Philippine peso, we have greater outflows than inflowsof these currencies, although to a lesser degree. As a result,we are exposed to changes in currency exchange rates andsuch changes could be significant.

Economic weakness, the potential inability of certainEuropean countries to continue to service their sovereigndebt obligations, and the related actions of this region’scentral banks has caused, and could continue to cause, thevalue of the euro to weaken. As a result, our operatingresults could be negatively impacted. In the event that oneor more European countries were to replace the euro withanother currency, business may be adversely affected untilstable exchange rates are established.

Our ability to maintain our products’ pricecompetitiveness is reliant, in part, on the relative strengthof the currency in which the product is denominatedcompared to the currency of the market into which it issold and the functional currency of our competitors.Changes in the rate of exchange of foreign currencies inrelation to the U.S. dollar, and other currencies, mayadversely impact our results of operations and our abilityto offer products in certain markets at acceptable prices.For example, approximately $75 million of our revenue in2015 was earned from shipments to customers located inUkraine, Russia and members of the CIS. Although thesesales are denominated in euros, a significant weakening ofthe customers’ local currencies has and may continue toadversely affect our revenue, our customers’ credit risk andour results of operation.

The cost of raw materials and energy usedto manufacture our products could increaseand the availability of certain raw materialscould become constrained.

We require access to sufficient and reasonably pricedquantities of pulpwood, purchased pulps, pulp substitutes,abaca fiber, synthetic fibers, and certain other rawmaterials.

Our Specialty Papers’ locations are verticallyintegrated manufacturing facilities that can generateapproximately 85% of their annual pulp requirements.

Our Philippine mill purchases abaca fiber to produceabaca pulp, a key material used to manufacture paper forsingle-serve coffee, tea and technical specialty products atour Gernsbach, Scaër, and Lydney facilities. At certaintimes, the supply of abaca fiber has been constrained dueto factors such as weather-related damage to the sourcecrop as well as decisions by land owners to producealternative crops in lieu of those used to produce abacafiber.

Our Advanced Airlaid Materials business unit requiresaccess to sufficient quantities of fluff pulp, the supply ofwhich is subject to availability of certain softwoods.Softwood availability can be limited by many factors,including weather in regions where softwoods areabundant.

The cost of many of our production materials,including petroleum based chemicals and freight charges,are influenced by the cost of oil. In addition, although weare currently converting our boilers to burn natural gas,coal is currently a principal source of fuel for both theSpring Grove and Chillicothe facilities. Natural gas is usedas a source of fuel at Chillicothe and our Composite Fibersand Advanced Airlaid Materials business units’ facilities.

Government rules, regulations and policies have animpact on the cost of certain energy sources, particularlyfor our European operations. We currently benefit from anumber of government sponsored programs related to,among others, green energy or renewable energyinitiatives designed to mitigate the cost of electricity tolarger industrial consumers of power. Any reduction in theextent of government sponsored incentives may adverselyaffect the cost ultimately borne by our operations.

Although we have contractual cost pass-througharrangements with certain Advanced Airlaid Materials’customers, we may not be able to fully pass increased rawmaterials or energy costs on to all customers if the marketwill not bear the higher price or if existing agreements limitprice increases. If price adjustments significantly trailincreases in raw materials or energy prices, our operatingresults could be adversely affected.

8

Our industry is highly competitive andincreased competition could reduce oursales and profitability.

Specialty Papers The primary market for ourSpecialty Papers business unit is the United States, whichhas been adversely affected by capacity exceeding thedemand for products, increased imports from foreigncompetitors and by declining uncoated free sheet demand.As a result, the industry has taken steps to reduce capacity.However, slowing demand or increased competition couldforce us to lower our prices or to offer additional servicesat a higher cost to us, which could reduce our grossmargins and net income. The greater financial resources ofcertain of our competitors may enable them to commitlarger amounts of capital in response to changing marketconditions. Certain competitors may also have the ability todevelop product or service innovations that could put us ata competitive disadvantage.

There have been periods of supply/demand imbalancein our industry which have caused pulp prices and ourproducts’ selling prices to be volatile. The timing andmagnitude of price increases or decreases in these marketshave generally varied by region and by product type. Asustained period of weak demand or excess supply wouldlikely adversely affect pulp prices and our products’ sellingprices. This could have a material adverse effect on ouroperating and financial results.

Some of the other factors that may adversely affectour ability to compete in Specialty Papers markets in whichwe participate include:

• the entry of new competitors into the markets weserve;

• the prevalence of imported product, particularlyuncoated free sheet, into the U.S.;

• the willingness of commodity-based producers toenter our markets when they are unable tocompete or when demand softens in theirtraditional markets;

• the aggressiveness of our competitors’ pricingstrategies, which could force us to decrease pricesin order to maintain market share;

• our failure to anticipate and respond to changingcustomer preferences;

• the impact of electronic-based substitutes forcertain of our products such as carbonless andforms, book publishing, and envelope papers;

• the impact of replacement or disruptivetechnologies;

• changes in end-user preferences;

• our inability to develop new, improved orenhanced products;

• our inability to maintain the cost efficiency of ourfacilities; and

• the cost of regulatory environmental compliancerequirements.

Composite Fibers and Advanced AirlaidMaterials The global markets in which we compete,although growing, are not as large as the markets forSpecialty Papers. As a result, our ability to compete is moresensitive to and may be adversely impacted by thefollowing:

• the entry of new competitors into the markets weserve;

• the aggressiveness of our competitors’ pricingstrategies, which could force us to decrease pricesin order to maintain market share;

• our failure to anticipate and respond to changingcustomer preferences; and

• technological advances or changes that impactproduction of our products.

The impact of any significant changes may result inour inability to effectively compete in the markets in whichwe operate, and as a result our sales and operating resultswould be adversely affected.

We may not be able to develop newproducts acceptable to our existing orpotential customers.

Our business strategy is market focused and includesinvestments in developing new products to meet thechanging needs of our customers or serve new customersand to maintain our market share. Our success willdepend, in part, on our ability to develop and introducenew and enhanced products that keep pace withintroductions by our competitors and changing customerpreferences. If we fail to anticipate or respond adequatelyto these factors, we may lose opportunities for businesswith both current and potential customers. The success ofour new product offerings will depend on several factors,including our ability to:

• anticipate and properly identify our customers’needs and industry trends;

GLATFELTER 2015 FORM 10-K 9

• develop and commercialize new products andapplications in a timely manner;

• price our products competitively;

• differentiate our products from our competitors’products; and

• invest efficiently in research and developmentactivities.

Our inability to develop new products or newbusiness opportunities could adversely impact our businessand ultimately harm our profitability.

We are subject to substantial costs andpotential liability for environmentalmatters.

We are subject to various environmental laws andregulations that govern our operations, including dischargesinto the environment, and the handling and disposal ofhazardous substances and wastes. We are also subject tolaws and regulations that impose liability and clean-upresponsibility for releases of hazardous substances into theenvironment. To comply with environmental laws andregulations, we have incurred, and will continue to incur,substantial capital and operating expenditures. The CleanAir Act, and similar regulations, will impose significantcompliance costs or require significant capital expenditures.Compliance with the Clean Air Act will require processmodifications and/or installation of air pollution controls onboilers at two of our facilities, as well as connecting to gaspipelines. Because of the complexities of this initiative, ourinability to successfully complete all aspects of the projectcould adversely impact the expenditures required or ourresults of operations.

We anticipate that environmental regulation of ouroperations will continue to become more burdensome andthat capital and operating expenditures necessary tocomply with environmental regulations will continue, andperhaps increase, in the future. Because environmentalregulations are not consistent worldwide, our ability tocompete globally may be adversely affected by capital andoperating expenditures required for environmentalcompliance. In addition, we may incur obligations toremove or mitigate any adverse effects on theenvironment, such as air and water quality, resulting frommills we operate or have operated. Potential obligationsinclude compensation for the restoration of naturalresources, personal injury and property damages. SeeItem 1 – Environmental Matters for an additionaldiscussion of expected costs to comply with environmentalregulations.

We have exposure to potential liability forremediation and other costs related to the presence ofpolychlorinated biphenyls (PCBs) in the lower Fox River onwhich our former Neenah, Wisconsin mill was located.During 2015, we incurred $9.7 million for remediationactivities in the downstream portion of the river and it ispossible we may incur a similar amount in 2016. While webelieve this to be a reasonable estimation of our currentexposure, there can be no assurance that we will not berequired to provide significant contributions to fundremediation efforts in the near term and/or ultimately paymaterial amounts to resolve our liability in the Fox Rivermatter. We have financial reserves for environmentalmatters, including the Fox River site, but we cannot becertain that those reserves will be adequate to provide forfuture obligations related to these matters, that our shareof costs and/or damages for these matters will not exceedour available resources, or that such obligations will nothave a long-term, material adverse effect on ourconsolidated financial position, liquidity or results ofoperations.

Our environmental issues are complex and should bereviewed in the context set forth in more detail in Item 8 –Financial Statements and Supplementary Data – Note 23.

The Advanced Airlaid Materials businessunit generates a substantial portion of itsrevenue from one customer serving thehygiene products market, the loss of whichcould have a material adverse effect on ourresults of operations.

The majority of Advanced Airlaid Materials’ net salesof hygiene products are from one customer. In addition,sales to the feminine hygiene market accounted for 74% ofAdvanced Airlaid Materials’ net sales in 2015 and sales areconcentrated within a small group of large customers. Theloss of the large customer or a decline in sales of hygieneproducts could have a material adverse effect on thisbusiness’s operating results. Our ability to effectivelycompete could be affected by technological productionalternatives which could provide substitute products intothis market segment. Customers in the airlaid nonwovenfabric material market, including the hygiene market, mayalso switch to less expensive products, change preferencesor otherwise reduce demand for Advanced AirlaidMaterial’s products, thus reducing the size of the marketsin which it currently sells its products. Any of the foregoingcould have a material adverse effect on our financialperformance and business prospects.

10

Our operations may be impaired and wemay be exposed to potential losses andliability as a result of natural disasters, actsof terrorism or sabotage or similar events.

If we have a catastrophic loss or unforeseenoperational problem at any of our facilities, we could suffersignificant lost production which could impair our ability tosatisfy customer demands.

Natural disasters, such as earthquakes, hurricanes,typhoons, flooding or fire, and acts of terrorism orsabotage affecting our operating activities and majorfacilities could materially and adversely affect ouroperations, operating results and financial condition.

In addition, we own and maintain two dams in YorkCounty, Pennsylvania, that were built to ensure a steadysupply of water for the operation of our facility in SpringGrove which is a primary manufacturing location for ourenvelope papers and engineered products. Each of thesedams is classified as “high hazard” by the Commonwealthof Pennsylvania because they are located in close proximityto inhabited areas. Any sudden failure of a dam, includingas a result of natural disaster or act of terrorism orsabotage, would endanger occupants and residential,commercial and industrial structures, for which we couldbe liable. The failure of a dam could also be extremelydisruptive and result in damage to, or the shutdown of, ourSpring Grove mill. Any losses or liabilities incurred due tothe failure of one of our dams may not be fully covered byor may substantially exceed the limits of our insurancepolicies and could materially and adversely affect ouroperating results and financial condition.

In addition, many of our papermaking operationsrequire a reliable and abundant supply of water. Such millsrely on a local water body or water source for their waterneeds and, therefore, are particularly impacted by droughtconditions or other natural or manmade interruptions towater supplies. At various times and for differing periods,each of our mills has had to modify operations due towater shortages, water clarity, or low flow conditions in itsprincipal water supplies. Any interruption or curtailment ofoperations at any of our paper mills due to drought or lowflow conditions at the principal water source or anothercause could materially and adversely affect our operatingresults and financial condition.

Our pulp mill in Lanao del Norte on the Island ofMindanao in the Republic of the Philippines is locatedalong the Pacific Rim, one of the world’s hazard belts. Byvirtue of its geographic location, this mill is subject tosimilar types of natural disasters discussed above, cyclones,

typhoons, and volcanic activity. Moreover, the area ofLanao del Norte has been a target of suspected terroristactivities. Our pulp mill in Mindanao is located in a ruralportion of the island and is susceptible to attacks or powerinterruptions. The Mindanao mill supplies the abaca pulpused by our Composite Fibers business unit to manufactureour paper for single serve coffee and tea products andcertain technical specialties products. Any interruption, lossor extended curtailment of operations at our Mindanaomill could affect our ability to meet customer demands forour products and materially affect our operating resultsand financial condition.

We have operations in a potentiallypolitically and economically unstablelocation.

Our pulp mill in the Philippines is located in a regionthat is unstable and subject to political unrest. Asdiscussed above, our Philippine pulp mill produces abacapulp, a significant raw material used by our CompositeFibers business unit, and is currently our main provider ofabaca pulp. There are limited suitable alternative sourcesof readily available abaca pulp in the world. In the event ofa disruption in supply from our Philippine mill, there is noguarantee that we could obtain adequate amounts ofabaca pulp, if at all, from alternative sources at areasonable price. Further, there is no assurance theperformance of such alternative materials will be satisfycustomer performance requirements. As a consequence,any civil disturbance, unrest, political instability or otherevent that causes a disruption in supply could limit theavailability of abaca pulp and would increase our cost ofobtaining abaca pulp. Such occurrences could adverselyimpact our sales volumes, revenues and operating results.

Our international operations pose certainrisks that may adversely impact sales andearnings.

We have significant operations and assets located inCanada, Germany, France, the United Kingdom, and thePhilippines. Our international sales and operations aresubject to a number of unique risks, in addition to the risksin our domestic sales and operations, including differingprotections of intellectual property, trade barriers, laborunrest, exchange controls, regional economic uncertainty,differing (and possibly more stringent) labor regulation,risk of governmental expropriation, domestic and foreigncustoms and tariffs, differing regulatory environments,difficulty in managing widespread operations and politicalinstability. These factors may adversely affect our futureprofits. Also, in some foreign jurisdictions, we may be

GLATFELTER 2015 FORM 10-K 11

subject to laws limiting the right and ability of entitiesorganized or operating therein to pay dividends or remitearnings to affiliated companies unless specified conditionsare met. Any such limitations would restrict our flexibility inusing funds generated in those jurisdictions.

We are subject to cyber-security risksrelated to unauthorized or malicious accessto sensitive customer, vendor, company oremployee information as well as to thetechnology that supports our operationsand other business processes.

Our business operations rely upon secure systems formill operations, and data capture, processing, storage andreporting. Although we maintain appropriate data securityand controls, our information technology systems, andthose of our third party providers, could become subject tocyber attacks. Systems such as ours are inherently exposedto cyber-security risks and potential attacks. The result ofsuch attacks could result in a breach of data security andcontrols. Such a breach of our network, systems,applications or data could result in operational disruptionsor damage or information misappropriation including, butnot limited to, interruption to systems availability, denial ofaccess to and misuse of applications required by ourcustomers to conduct business with us, denial of access tothe applications we use to plan our operations, procurematerials, manufacture and ship products and account fororders, theft of intellectual knowhow and trade secrets,and inappropriate disclosure of confidential company,employee, customer or vendor information, could stemfrom such incidents.

Any of these operational disruptions and/ormisappropriation of information could adversely affect ourresults of operations, create negative publicity and couldhave a material effect on our business.

We operate in and are subject to taxationfrom numerous U.S. and foreignjurisdictions.

The multinational nature of our business subjects usto taxation in the U.S and numerous foreign jurisdictions.Due to economic and political conditions, tax rates invarious jurisdictions may be subject to significant change.Our effective tax rates could be affected by changes in taxlaws or their interpretation or changes in the mix ofearnings in jurisdictions with differing statutory tax rates,changes in the valuation of deferred tax assets andliabilities. For example, the European Commission has

opened formal investigations to examine whether decisionsby the tax authorities in certain European countries complywith European Union rules on state aid. The outcome ofthe European Commission’s investigations could requirechanges to existing tax rulings that, in turn, could have animpact on our income taxes and results of operations.

In the event any of the above risk factorsimpact our business in a material way or incombination during the same period, wemay be unable to generate sufficient cashflow to simultaneously fund ouroperations, finance capital expenditures,satisfy obligations and make dividendpayments on our common stock.

In addition to debt service obligations, our business iscapital intensive and requires significant expenditures tosupport growth strategies, research and developmentinitiatives, environmental compliance, and for normalupgrades or replacements. During 2016, we expect our useof cash for capital expenditures, strategic investments andenvironmental compliance projects will exceed cashgenerated from operations. We expect to meet all of ournear and long-term cash needs from a combination ofoperating cash flow, cash and cash equivalents, ourexisting credit facility and other long-term debt. If we areunable to generate sufficient cash flow from these sources,we could be unable to meet our near and long-term cashneeds or make dividend payments.

ITEM 1B UNRESOLVED STAFF COMMENTS

None.

ITEM 2 PROPERTIES

We own substantially all of the land and buildingscomprising our manufacturing facilities located inPennsylvania; Ohio; Canada; the United Kingdom;Germany; France; and the Philippines; as well assubstantially all of the equipment used in ourmanufacturing and related operations. Certain of ouroperations are under lease arrangements including ourmetallized paper production facility located in Caerphilly,Wales, office and warehouse space in Moscow, Russia,Souzou, China and our corporate offices in York,Pennsylvania. All of our properties, other than those thatare leased, are free from any material liens orencumbrances. We consider all of our buildings to be ingood structural condition and well maintained and ourproperties to be suitable and adequate for presentoperations.

12

ITEM 3 LEGAL PROCEEDINGS

We are involved in various lawsuits that we considerto be ordinary and incidental to our business. The ultimateoutcome of these lawsuits cannot be predicted withcertainty; however, except with respect to the Fox Rivermatter referred to below, we do not expect such lawsuits,individually or in the aggregate, will have a materialadverse effect on our consolidated financial position,liquidity or results of operations.

We are one of several defendants in a significantenvironmental matter relating to contamination in the FoxRiver and Bay of Green Bay in Wisconsin. For a discussionthis matter, see Item 8 – Financial Statements andSupplementary Data – Note 23.

EXECUTIVE OFFICERS

The following table sets forth certain informationwith respect to our executive officers and seniormanagement as of February 26, 2016.

Name Age Office with the Company

Dante C. Parrini 51 Chairman and Chief ExecutiveOfficer

John P. Jacunski 50 Executive Vice President and ChiefFinancial Officer

Christopher W. Astley 43 Senior Vice President & BusinessUnit President, AdvancedAirlaid Materials

Brian E. Janki 43 Senior Vice President & BusinessUnit President, Specialty Papers

Martin Rapp 56 Senior Vice President & BusinessUnit President, CompositeFibers

William T. Yanavitch II 55 Senior Vice President, HumanResources and Administration

David C. Elder 47 Vice President, FinanceKent K. Matsumoto 56 Vice President, General Counsel

and Corporate SecretaryMark A. Sullivan 60 Vice President

Officers are elected to serve at the pleasure of theBoard of Directors. Except in the case of officers elected tofill a new position or a vacancy occurring at some otherdate, officers are generally elected at the organizationalmeeting of the Board of Directors held immediately afterthe annual meeting of shareholders.

Dante C. Parrini became Chief Executive Officereffective January 1, 2011 and Chairman of the Board inMay 2011. Prior to this, he was Executive Vice Presidentand Chief Operating Officer, a position he held sinceFebruary 2005. Mr. Parrini joined us in 1997 and haspreviously served as Senior Vice President and GeneralManager, a position he held beginning in January 2003

and prior to that as Vice President responsible for Salesand Marketing.

John P. Jacunski was promoted to Executive VicePresident and Chief Financial Officer in February 2014. Hejoined us in October 2003 and served as Vice Presidentand Corporate Controller. In July 2006 he was promoted toSenior Vice President and Chief Financial Officer.Mr. Jacunski was previously Vice President and ChiefFinancial Officer at WCI Steel, Inc. from June 1999 toOctober 2003. Prior to joining WCI, Mr. Jacunski was withKPMG, an international accounting and consulting firm,where he served in various capacities.

Christopher W. Astley was named Senior VicePresident & Business Unit President, Advanced AirlaidMaterials in January 2015. He joined us in August 2010 asVice President, Corporate Strategy and was promoted toSenior Vice President in February 2014. Prior to joining us,he was an entrepreneur leading a privately held businessfrom 2004 until 2010. Prior to that Mr. Astley heldpositions with Accenture, a global management consultingfirm, and The Coca-Cola Company.

Brian E. Janki serves as Senior Vice President &Business Unit President, Specialty Papers. Prior to joiningus in August 2013 Mr. Janki was employed by Greif astheir Vice President & General Manager, Rigid IndustrialPackaging & Services. During his twelve years with Greif,Mr. Janki held leadership positions including profit/lossresponsibilities for two business units, global responsibilityfor supply chain and sourcing, and transformationalassignments including global oversight of theimplementation of the Greif Business System.

Martin Rapp serves as Senior Vice President &Business Unit President, Composite Fibers. Mr. Rapp joinedus in August 2006 and has lead the Composite Fibersbusiness unit since that time. Prior to this, he was VicePresident and General Manager of Avery Dennison’s RollMaterials Business in Central and Eastern Europe sinceAugust 2002.

William T. Yanavitch II was promoted to SeniorVice President Human Resources and Administration inFebruary 2014. Since joining us in July 2000, he has servedas Vice President, Human Resources. Prior to joining us heworked for Dentsply International and Gould Pumps Inc. invarious leadership capacities.

David C. Elder was named Vice President, Financein December 2011 and continues as our chief accountingofficer. Prior to his promotion, he was our Vice President,Corporate Controller, a position held since joining

GLATFELTER 2015 FORM 10-K 13

Glatfelter in January 2006. Mr. Elder was previouslyCorporate Controller for YORK International Corporation.

Kent K. Matsumoto was appointed Vice President,General Counsel and Corporate Secretary in October 2013.Mr. Matsumoto joined us in June 2012 as Assistant GeneralCounsel and also served as interim General Counsel fromMarch 2013 to October 2013. From July 2008 untilFebruary 2012, he was Associate General Counsel forWolters Kluwer.

Mark A. Sullivan serves as a Vice President.Previously, he was Vice President, Global Supply Chain andInformation Technology since his promotion in November2012. Mr. Sullivan joined us in December 2003 as ChiefProcurement Officer and he was appointed Vice President,Global Supply Chain in February 2005.

ITEM 4 MINE SAFETY DISCLOSURES

Not Applicable

PART II

ITEM 5 MARKET FOR REGISTRANT’SCOMMON EQUITY, RELATEDSTOCKHOLDER MATTERS ANDISSUER PURCHASES OF EQUITYSECURITIES

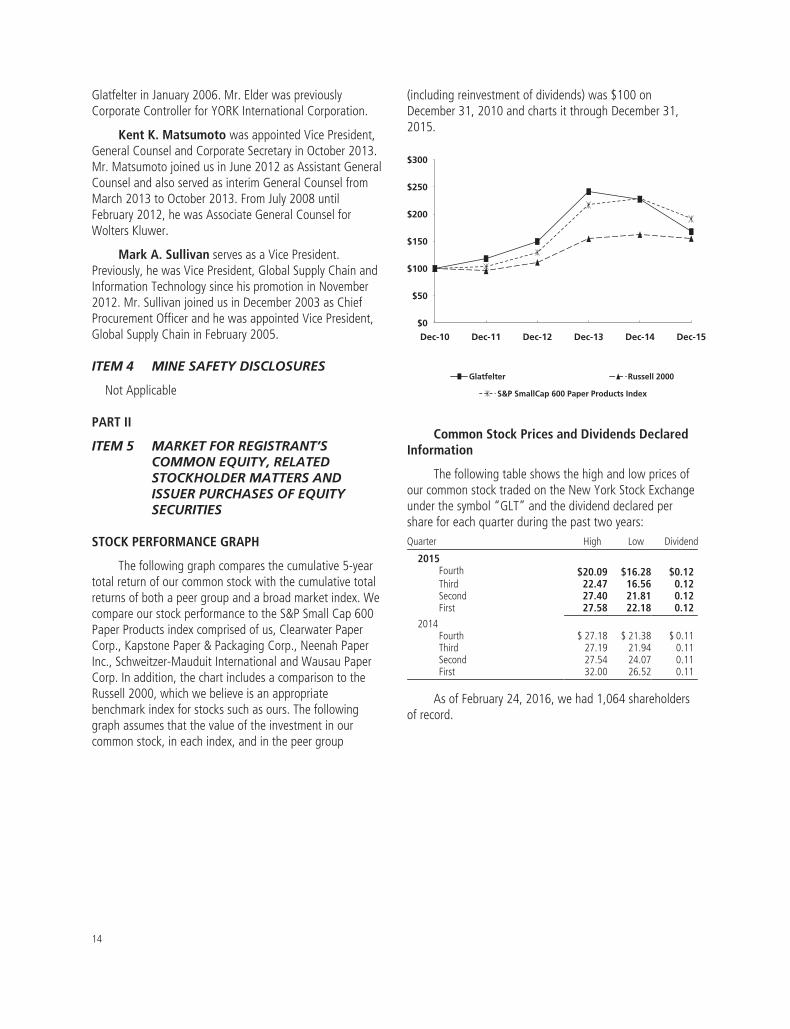

STOCK PERFORMANCE GRAPH

The following graph compares the cumulative 5-yeartotal return of our common stock with the cumulative totalreturns of both a peer group and a broad market index. Wecompare our stock performance to the S&P Small Cap 600Paper Products index comprised of us, Clearwater PaperCorp., Kapstone Paper & Packaging Corp., Neenah PaperInc., Schweitzer-Mauduit International and Wausau PaperCorp. In addition, the chart includes a comparison to theRussell 2000, which we believe is an appropriatebenchmark index for stocks such as ours. The followinggraph assumes that the value of the investment in ourcommon stock, in each index, and in the peer group

(including reinvestment of dividends) was $100 onDecember 31, 2010 and charts it through December 31,2015.

Glatfelter Russell 2000

S&P SmallCap 600 Paper Products Index

$300

$200

$250

$150

$100

$50

$0

Dec-10 Dec-11 Dec-12 Dec-13 Dec-15Dec-14

Common Stock Prices and Dividends DeclaredInformation

The following table shows the high and low prices ofour common stock traded on the New York Stock Exchangeunder the symbol “GLT” and the dividend declared pershare for each quarter during the past two years:Quarter High Low Dividend

2015Fourth $20.09 $16.28 $0.12Third 22.47 16.56 0.12Second 27.40 21.81 0.12First 27.58 22.18 0.12

2014Fourth $ 27.18 $ 21.38 $ 0.11Third 27.19 21.94 0.11Second 27.54 24.07 0.11First 32.00 26.52 0.11

As of February 24, 2016, we had 1,064 shareholdersof record.

14

ITEM 6 SELECTED FINANCIAL DATA

As of or for the year ended December 31Dollars in thousands, except per share 2015 2014 2013 (1) 2012 2011

Net sales $1,661,084 $1,802,415 $1,722,615 $1,577,788 $1,603,154Energy and related sales, net 5,664 7,927 3,153 7,000 9,344

Total revenue 1,666,748 1,810,342 1,725,768 1,584,788 1,612,498

Gains on dispositions of plant, equipmentand timberlands, net 21,113 4,861 1,726 9,815 3,950

Net income $ 64,575 $ 69,246 $ 67,158 $ 59,379 $ 42,694Earnings per share

Basic $ 1.49 $ 1.60 $ 1.56 $ 1.39 $ 0.94Diluted 1.47 1.57 1.52 1.36 0.93

Total assets $1,503,624 $1,561,504 $1,678,410 $1,242,985 $1,136,925Total debt 363,870 404,612 442,325 250,000 227,000

Shareholders’ equity 663,247 649,109 684,476 539,679 490,404Cash dividends declared per common share 0.48 0.44 0.40 0.36 0.36

Depreciation, depletion and amortization 63,236 70,555 68,196 69,500 69,313Capital expenditures 99,889 66,046 103,047 58,752 64,491

Net tons sold 1,051,911 1,059,881 1,029,819 969,833 960,915Number of employees 4,375 4,516 4,403 4,258 4,274

(1) On April 30, 2013, we acquired Dresden Papier GmbH, the results of which are included prospectively from the acquisition date, including $101.8million of net sales and $18.3 million of operating income.

GLATFELTER 2015 FORM 10-K 15

ITEM 7 MANAGEMENT’S DISCUSSION ANDANALYSIS OF FINANCIALCONDITION AND RESULTS OFOPERATIONS

Forward-Looking Statements This AnnualReport on Form 10-K includes forward-looking statementswithin the meaning of the Private Securities LitigationReform Act of 1995. All statements other than statements ofhistorical fact, including statements regarding industryprospects and future consolidated financial position orresults of operations, made in this Report on Form 10-K areforward looking. We use words such as “anticipates”,“believes”, “expects”, “future”, “intends” and similarexpressions to identify forward-looking statements. Forward-looking statements reflect management’s currentexpectations and are inherently uncertain. Our actual resultsmay differ significantly from such expectations. The followingdiscussion includes forward-looking statements regardingexpectations of, among others, non-cash pension expense,environmental costs, capital expenditures and liquidity, all ofwhich are inherently difficult to predict. Although we makesuch statements based on assumptions that we believe to bereasonable, there can be no assurance that actual resultswill not differ materially from our expectations. Accordingly,we identify the following important factors, among others,which could cause our results to differ from any results thatmight be projected, forecasted or estimated in any suchforward-looking statements:

i. variations in demand for our products including theimpact of unplanned market-related downtime,variations in product pricing, or product substitution;

ii. the impact of competition, both domestic andinternational, changes in industry production capacity,including the construction of new mills or newmachines, the closing of mills and incremental changesdue to capital expenditures or productivity increases;

iii. risks associated with our international operations,including local economic and political environmentsand fluctuations in currency exchange rates;

iv. geopolitical events, including the impact of conflictssuch as Russia and Ukraine;

v. our ability to develop new, high value-addedproducts;

vi. changes in the cost or availability of raw materials weuse, in particular pulpwood, pulp, pulp substitutes,caustic soda, and abaca fiber;

vii. changes in energy-related costs and commodity rawmaterials with an energy component;

viii. the impact of unplanned production interruption;

ix. disruptions in production and/or increased costs dueto labor disputes;

x. the impact of exposure to volatile market-basedpricing for sales of excess electricity;

xi. the gain or loss of significant customers and/or on-going viability of such customers;

xii. cost and other effects of environmental compliance,cleanup, damages, remediation or restoration, orpersonal injury or property damages related thereto,such as the costs of natural resource restoration ordamages related to the presence of polychlorinatedbiphenyls (“PCBs”) in the lower Fox River on whichour former Neenah mill was located;

xiii. adverse results in litigation in the Fox River matter;

xiv. the impact of war and terrorism;

xv. the impact of unfavorable outcomes of audits byvarious state, federal or international tax authorities;

xvi. enactment of adverse state, federal or foreign tax orother legislation or changes in government policy orregulation; and

xvii. our ability to finance, consummate and integrateacquisitions.

Introduction We manufacture a wide array ofspecialty papers and fiber-based engineered materials andwe manage our company along three business units:

• Composite Fibers with revenue from the sale ofsingle-serve tea and coffee filtration papers,nonwoven wall covering materials, metallizedpapers, composite laminates papers, and manytechnically special papers including substrates forelectrical applications;