Embed Size (px)

Citation preview

2015 Africa Capital Markets Watch

28IPOs in 2015

105 IPOs between 2011 and 2015

$12.7bnIPO and FO proceeds raised in 2015

$41.3bn proceeds raised between 2011 and 2015

47Corporate and sovereign/supranational debt issuances in 2015

489 issuances between 2011 and 2015

$19.3bnCorporate and sovereign/supranational debt capital raised in 2015

$110.2bn raised between 2011 and 2015

www.pwc.co.za/capitalmarketswatch.html

January 2016

About 2015 Africa Capital Markets Watch

This report surveys all new primary market equity initial public offerings (IPOs) and further offers (FOs) by listed companies, as well as high-yield (HY) and investment-grade (IG) debt capital markets activity, in which capital was raised on Africa’s principal stock markets and market segments (including exchanges in Algeria, Botswana, Cameroon, Cape Verde, Côte d’Ivoire, Egypt, Libya, Gabon, Ghana, Kenya, Malawi, Mauritius, Mozambique, Namibia, Nigeria, Morocco, Rwanda, Seychelles, Somalia, South Africa, Sudan, Swaziland, Tanzania, Tunisia, Uganda, Zambia and Zimbabwe).

The report also includes IPO, FO, HY and IG activity of African companies* on international exchanges or non-African companies on African exchanges, on an annual basis. Movements between markets on the same exchange are excluded.

This report covers activity up to 31 December 2015 and captures deals based on their pricing date. All market data is sourced from Dealogic, Bloomberg, The World Federation of Exchanges, Thomson Reuters and the stock markets themselves, unless otherwise stated, and has not been independently verified by PwC.

* Companies incorporated in Africa or with primarily African operations or an African parent.

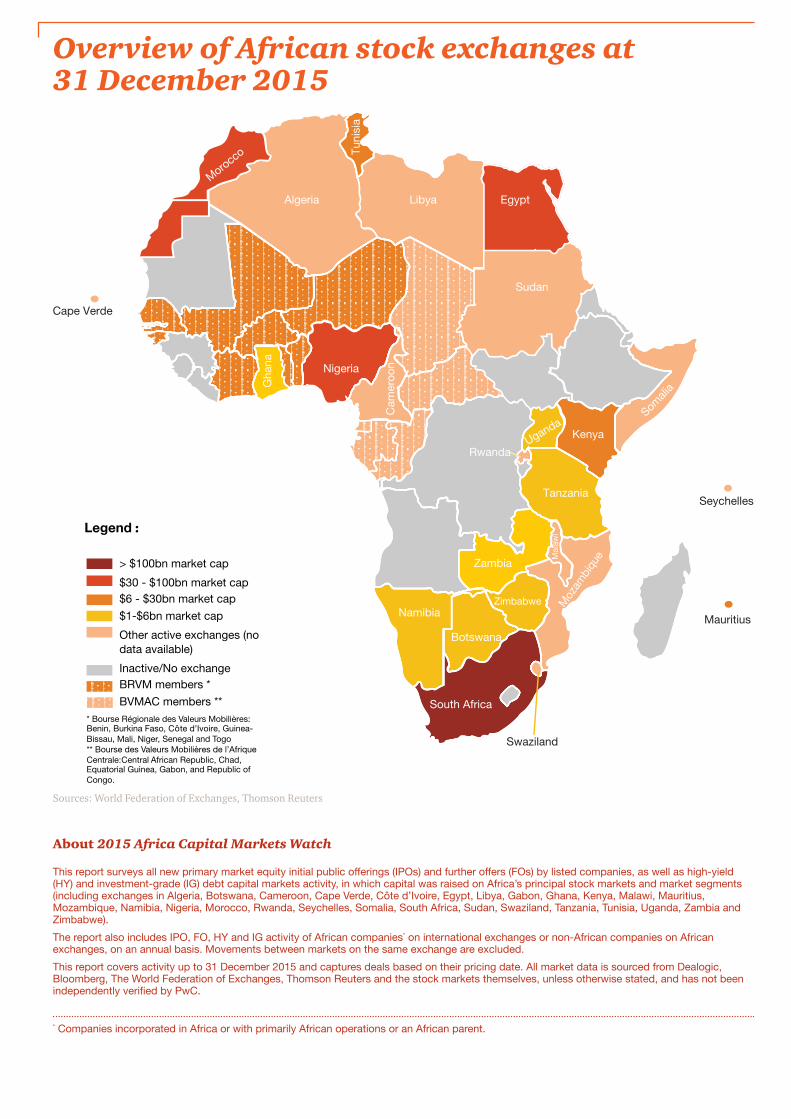

> $100bn market cap

$30 - $100bn market cap $6 - $30bn market cap

$1-$6bn market cap

Other active exchanges (no data available)

Inactive/No exchange BRVM members *

BVMAC members **

Legend :

* Bourse Régionale des Valeurs Mobilières: Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau, Mali, Niger, Senegal and Togo ** Bourse des Valeurs Mobilières de l’Afrique Centrale:Central African Republic, Chad, Equatorial Guinea, Gabon, and Republic of Congo.

Egypt

South Africa

Nigeria

Morocco

Kenya

Tuni

sia

Zimbabwe

Tanzania

Zambia

Botswana

Gha

na

Namibia

Mal

awi

Libya

Mauritius

Seychelles

Algeria

Rwanda

Cape Verde

Moz

ambi

que

Uganda

Sudan

Somali

a

Swaziland

Cam

eroo

n

Overview of African stock exchanges at 31 December 2015

Sources: World Federation of Exchanges, Thomson Reuters

Contents

ContentsForeword 4

Trends in African capital markets in 2015 5

Trends in global equity markets 2006 – 2015 7

African equity markets 9

African IPO market 10

African FO Market 17

African IPOs and FOs: Analysis of cross-border activity 2011 – 2015 21

African debt markets 23

African high-yield debt market 25

African investment-grade debt market 30

Contacts 33

Acknowledgements 33

4 | 2015 Africa Capital Markets Watch

Welcome to PwC’s 2015 Africa Capital Markets Watch. In our second annual publication, we have expanded the scope of our IPO Watch Africa to include an analysis of African equity and debt capital markets transactions that occurred over the past five-year period (2011-2015).

Foreword

Equity capital markets (ECM) transactions included in our report comprise capital raising activities, whether IPOs or FOs, by African companies on exchanges worldwide or those made by non-African companies on African exchanges. Debt capital markets (DCM) transactions analysed include debt funding raised by African companies and public institutions, whether high-yield (HY) or investment-grade (IG) debt.

Between 2011 and 2015, African ECM activity consisted of 105 IPOs and 336 FOs, with 2015 accounting for the largest number of IPOs and FOs in the period with 28 and 91, respectively.

African DCM activity on African exchanges was comparatively muted in 2015, with a decline from 2012 and 2013, years which saw a peak in terms of volume and value of debt capital raised, respectively.

At 31 December 2015, African exchanges had a market capitalisation of approximately $1 trillion, with 23% of this value residing on exchanges outside of South Africa. Though statistics cannot be interpreted in isolation, certain metrics commonly used to analyse global market performance, such as the market capitalisation-to-GDP ratio, suggest that untapped value remains in Africa, with the potential for further sustained growth in African market capitalisation.

Growth across the continent, the outlook for which varies based on the diverse and specific cultural, economic and political circumstances of each country, will require continued investment in various sectors including infrastructure, agriculture, consumer products, telecommunications and financial services, alongside the other industries more traditionally associated with Africa.

In 2015, the capital markets, both local and international, continued to feature as a primary funding source for this growth, in conjunction with private equity investment and mergers & acquisitions (M&A), reflecting the continued appetite from investors with key portfolio allocations targeted towards emerging and frontier markets. Though this upward trend in activity has now been observed over the trailing five-year period, we recognise that uncertainties in the market and economic trends may see a more challenging 2016.

Clifford Tompsett

PwC Global IPO Centre Leader

Nicholas Ganz

PwC Africa Capital Markets Group Leader

Accessing local or international capital markets, especially for first time issuers, involves a steep learning curve with complex regulations and considerations for many areas of the business. When contemplating a move towards the capital markets, companies can begin to prepare by conducting a thorough readiness assessment – from clarification of the market proposition to financial reporting readiness and internal controls, to tax planning and governance matters – to ensure a successfully planned, monitored and executed transaction. Companies may also find that independent capital markets advice can help in navigating the maze of complexities when looking to raise capital.

We hope you find the insights of our expanded capital markets analysis to be both interesting and useful.

PwC | 5

Trends in African capital markets in 2015

Africa remains resilient amidst lower growth expectations

The decline in commodity prices, particularly the oil price; concerns about levels of demand from China, a major trading partner for many African countries; and the relative weakening of local currencies resulted in slower growth projections across a number of economies in 2015. However, Africa continues to have more than just one story, with certain countries expected to continue on a stronger growth trajectory in 2016.

In terms of the continent’s largest economy, Nigeria, PwC’s January 2016 Global Economy Watch suggests growth will rebound to almost 5% in 2016 as tight fuel supplies and power outages abate and a more accommodative monetary and fiscal stance takes hold. Renewed focus on tackling corruption should also help to increase inflows of foreign direct investment (FDI), supported by improved security and better governance.

South Africa, the continent’s most advanced economy, experienced its own challenges at the year end, brought on by surprise political manoeuvres, which have shaken local and global investor confidence, at least for the moment. Nevertheless, the Johannesburg Stock Exchange (JSE) ended the year up nearly 2%, potentially reflecting the depth of liquidity in the market to absorb negative events and the prevalence of traded shares that act as a hedge to South African rand returns.

Active equity markets

Equity issuances by African companies continued to show strong activity in 2015, hitting five-year highs in both volume and value. Industry subsectors such as real estate and food and beverage showed a robust performance in the year, continuing to reflect the megatrends affecting the African continent.

While persistent, record-breaking activity in 2016 is less certain, some significant listings – both primary and secondary – have already been announced, and ECM activity is expected to reflect the continued desire of local companies seeking financing to grow into regional players, as well as private equity investors seeking to capture return through an IPO exit.

Technical advances, strengthened regulation and harmonisation have improved size and liquidity of markets

Harmonisation of East African exchanges and structured collaboration between exchanges (such as the London and Nigerian Stock Exchanges), among others, have allowed these markets to become more liquid and active and to improve turnover ratios.

There is an indication that some activity may currently be impeded by outdated trading, clearing and settlement systems, improvements to which are now on the agenda for many exchanges to handle sizeable capital inflows. This improved efficiency will lower barriers and enhance the attractiveness of African stock markets for equity investors.

During 2015, for instance, the Zimbabwe Stock Exchange transitioned from a manual trading platform to an automated trading platform and has already attracted a new listing in 2016.

In addition, evolution in local regulation has provided the opportunity for pension funds to diversify their expanding portfolios beyond equity investments in traditional sectors, such as banking and oil & gas.

6 | 2015 Africa Capital Markets Watch

Sovereign bonds dominate debt markets

As in each year over the period analysed, sovereign bonds dominated debt markets, accounting for 47% and 44% of the total bond market measured by value in 2015 and over the five-year period, respectively.

As an alternative to high debt servicing costs for local currency debt, African countries have specifically tapped international debt markets over the past years to obtain funding of less costly foreign currency.

However, the development of sovereign yield curves as a means of formally quantifying country risk for these issuances has also driven foreign participation in and pricing of corporate instruments in these countries.

Although the market for corporate bonds remains small and most popular in the financial services and oil & gas sectors, a shift to other sectors may be emerging. In March 2015, for example, East African Breweries became the first non-banking corporate in East Africa to issue a bond in international markets.

End to the record low interest rate environment

Record low interest rates globally created an issuer-friendly debt market over the past five years with sovereign issuances leading the field. However, the increase in interest rates following the end of the US Federal Reserve’s quantitative easing programme has distinctly cooled bond markets.

Furthermore, weakening of local currencies relative to the US dollar and other major funding currencies has made risk management and repayment of these foreign currency denominated bonds more expensive, suggesting that this method of funding may be less attractive during 2016.

PwC | 7

Source: Dealogic, PwC’s Q4 2015 Equity Capital Markets Briefing

PwCQ4 2015

Global money raised via IPOs and FOsThe number of IPOs in 2015 remained fairly stable as compared to 2014 whereas the total amount of money raised through IPOs decreased by 26%

2Quarterly ECM Briefing

Global money raised via IPOs and FOs (10-year overview)

IPO

mon

ey r

aise

d &

# o

f dea

lsF

O m

oney

rai

sed

& #

of

dea

ls

Top countries 2015

Source: Dealogic as of 31 December 2015

Note: included deals > $5m, excluding PIPO’s and transactions on Over-The-Counter exchanges. Top countries have been selected based on money raised in 2015. If IPOs or FOs take place in two or more countries, total money raised is attributed to all countries

$429.1bn

$569.4bn $557.3bn

$841.6bn

$641.2bn

$470.7bn $509.3bn$586.4bn $612.8bn

$681.7bn

3,0013,677

1,965

3,550 3,5462,894

2,5063,038 3,170 3,281

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

$295.8bn

$371.2bn

$105.7bn $120.3bn

$295.8bn

$178.3bn$140.6bn

$194.6bn

$272.5bn

$200.7bn

1,6211,885

567 497

1,2481,036

719 8581,154 1,144

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

US, 31%

China, 12%Hong Kong,

10%UK, 8%

Australia, 5%

Other, 34%

US, 19%

China, 13%

Hong Kong, 11%

UK, 10%Japan,

8%

Other, 39%

Figure 1: Global money raised via IPOs and FOs, 2006 – 2015

Trends in global equity markets 2006 – 2015

by 26%. IPO trends in Africa were more positive in 2015 than globally, though African FOs were more aligned to global trends.

Globally, the number of IPOs in 2015 remained fairly stable as compared to 2014, whereas the total amount of money raised through IPOs decreased

8 | 2015 Africa Capital Markets Watch

Since the beginning of 2013, performance of the FTSE/JSE Africa All Share Index* has tracked a similar course to the FTSE 100 and S&P 500, while the S&P All-Africa Index** tracked the Hang Seng more closely

* The FTSE/JSE Africa All Share Index is a market capitalisation-weighted index and reflects South African rand values. Companies included in this index comprise the top 99% of the total pre free-float market capitalisation of all listed companies on the JSE.

** The S&P All Africa Index is designed to serve as a comprehensive benchmark for the African market, covering companies listed on exchanges in 13 countries – Botswana, Côte d’Ivoire, Egypt, Ghana, Kenya, Mauritius, Morocco, Namibia, Nigeria, South Africa, Tunisia, Zambia and Zimbabwe – as well as companies listed in developed markets that derive the majority of their revenue from the African continent. The index is

weighted by float-adjusted market capitalisation and reflects in US dollar values.

60

90

120

150

S&P All Africa**FTSE/JSE AfricaAll share index*

S&P 500Hang Seng FTSE 100 31 D

ec 2

015

1 Ju

l 201

5

1 Ja

n 20

15

1 Ju

l 201

4

1 Ja

n 20

14

1 Ju

l 201

3

1 Ja

n 20

13

Source: Bloomberg

Figure 2: Global indices, 2013 - 2015

until market gloom began to push it lower in 2015, together with the drop of African currencies against the US dollar. All indices presented in figure 2 share a clear increase in volatility throughout the course of the past year.

Global indices 2013 – 2015

PwC | 9

0

3 000

6 000

9 000

12 000

15 000

201520142013201220110

20

40

60

80

100

120

Value FOs ($m) Value IPOs ($m) Number of ECM transactions

1 101

83

6573

101

119

401 891 1 701 1 991

4 475 5 455 5 102

9 478

10 712

$mill

ion

African equity markets

In line with global trends, 2015 was a challenging year for the African equity markets, with the return of market volatility and emergence of renewed global economic uncertainties, some of which have been closely linked to the ‘Africa Rising’ narrative.

While many economies have faced challenges in traditional sectors, a number have responded by shifting focus and strategy to more stable sectors, as illustrated in our ECM industry sector analysis. African ECM activity in 2015 was driven by continued capital growth in the financials sector (including closed-end funds and real estate).

Other non-commodity sectors, such as renewable energy, real estate, infrastructure, construction,

agriculture, health care and consumer goods, have also become more significant to the growth of African economies.

We continue to analyse trends both on an annual basis, as well as over a five-year time frame, as an indication of broader trends.

Over the past five years, there have been 441 African ECM transactions raising a total of $41.3bn.

The African IPO market also hit a five-year peak in 2015, with a record 28 listings.

2015 showed a steady overall increase in ECM activity of 18% in terms of transaction volume and 14% in terms of transaction value as compared

Figure 3: ECM activity, 2011 – 2015

Source: Dealogic

to 2014. However, 72% of 2015 IPO value and 54% of IPO volume were transacted during the first half of the year, reflective of the relatively higher levels of consumer confidence compared to the second half of 2015.

Proceeds from ECM activity are displayed in US dollars and the 2015 increase shown in figure 3 is tempered by the decreasing US dollar value of proceeds raised in South African rand and other currencies, such as the Egyptian pound. We estimate that on a constant currency basis, the 2015 increase in US dollar-equivalent proceeds would have increased over the prior year by 28% for IPOs and by 36% for FOs.

Note: Data presented in our IPO Watch Africa 2014 report has been adjusted for an additional 2014 IPO (Total Senegal) of $6.6m and two additional 2014 FOs (Curro Holdings of $55m and Taste Holdings of $16m), which were added to the Dealogic dataset after publication. In addition, our methodology for this report has been amended to include outbound capital markets activity in the data for ECM and DCM analyses. Prior periods have been amended to reflect this change in methodology.

10 | 2015 Africa Capital Markets Watch

African IPO trends 2011– 2015

Over the past five years, there have been 105 IPOs by African companies on both African and international exchanges and non-African companies in African exchanges, raising $6.1bn.

Despite the volatility in global equity markets, companies continue to be attracted to African markets, as demonstrated by the steady growth in first-time listings as compared to 2014.

There has been an overall increase of 12% in terms of the number of IPOs and 17% in terms of capital raised.

During 2015, the top four IPOs by proceeds involved companies or exchanges in North Africa. Each of these listings was oversubscribed, suggesting healthy investor demand in the region in the first half of 2015.

0

500

1 000

1 500

2 000

201520142013201220110

5

10

15

20

25

30

Value ($m) Number of IPOs

1 101

17

13

22

25

28

401

891

1 701

1 991

$mill

ion

African IPO market

Figure 4: IPO trends, 2011 – 2015

Source: Dealogic

PwC | 11

In 2015, capital raised from IPOs by companies on the JSE in US dollar terms decreased by 11% as compared to 2014, largely impacted by the weakening of the South African rand during the year; the rand value of IPO capital raised increased 11% over 2014 levels. Capital raised from IPOs by companies on other African exchanges increased slightly by 3% as compared to 2014. In terms of volume, the JSE saw a 33% increase in the number of IPOs as compared to 2014. 2015 was also a good year for the JSE’s Alternative Exchange (AltX), with an increase in listings value of more than double the previous year.

2015 saw a six-fold increase in the value of IPO activity on the Egyptian Exchange, though the bulk of these listings occurred during the first half of the year, against a backdrop of 5% anticipated economic growth and favourable price-to-earnings ratios across the market. After three years with no IPO activity, the Rwanda Stock Exchange welcomed the IPO of the Bank of Kigali in a privatisation of governmental interest in the bank.

In contrast, elsewhere on the continent, 2015 saw a major decrease in IPO capital raised on the Nigerian Stock Exchange and on the Bourse de Tunis as compared to 2014. This decline from 2014 on the Nigerian Stock Exchange is due in large part to the significance of the 2014 IPO of SEPLAT, which was among the top IPOs in 2014 in Africa by value. Similarly, the variance in the Bourse de Tunis activity from 2014 relates to a single significant IPO of Delice Holding, also among the 2014 top 10 African IPOs by value.

During 2015, 68% of total IPO volume transacted and 39% of total IPO value were raised on exchanges in sub-Saharan Africa (SSA), with the remainder made up by North Africa and outbound IPOs.

Over the five-year period as a whole, a similar value of 63% of total IPO volume and a higher 68% of total IPO value were raised in exchanges in SSA countries; the rest was derived from North Africa and outbound IPOs.

The JSE remains a reliable anchor of African capital markets activity, ranking second in the world for exchange regulation and first for ease of raising debt or equity capital, according to the World Economic Forum’s Global Competitiveness Report 2015 – 2016. Since 2011, capital raised from IPOs by companies on the JSE represented 45% of the total African IPO capital and 33% of the total transaction volume.

Over this period, in second place in terms of IPO volume after the JSE was the Bourse de Tunis with 23 issuances, while in second place by capital raised was the Egyptian Exchange with $861m. In third place in terms of volume was the Casablanca Stock Exchange with seven issuances, and third by capital raised was the Nigerian Stock Exchange with $751m, over 70% of which relates to the 2014 SEPLAT IPO.

On average during this period, capital raised per IPO in total over the past five years was $58m, with an average of $77m on the JSE and $46m on other African exchanges.

African IPO data by exchange 2011 – 2015

12 | 2015 Africa Capital Markets Watch

Figure 5: IPOs by African exchange*, 2011 - 2015

2011 2012 2013 2014 2015 Total

Exchange country

Num

ber

of

IPO

s

Cap

ital

ra

ised

($m

)

Num

ber

of

IPO

s

Cap

ital

ra

ised

($m

)

Num

ber

of

IPO

s

Cap

ital

ra

ised

($m

)

Num

ber

of

IPO

s

Cap

ital

ra

ised

($m

)

Num

ber

of

IPO

s

Cap

ital

ra

ised

($m

)

Num

ber

of

IPO

s

Cap

ital

ra

ised

($m

)

South Africa 5 790 5 258 4 261 9 742 12 658 35 2 709

Johannesburg 5 790 3 247 4 261 8 734 9 640 29 2 672

Johannesburg AltX 0 0 2 11 0 0 1 8 3 18 6 37

North Africa

Egypt 0 0 0 0 0 0 1 109 4 752 5 861Tunisia 1 9 2 8 12 191 6 125 2 43 23 376Morocco 3 50 1 3 1 122 1 127 1 74 7 376

Sub-Saharan Africa excluding South AfricaNigeria 0 0 0 0 1 190 1 538 1 23 3 751Kenya 2 76 2 75 0 0 1 7 1 35 6 193Rwanda 2 91 0 0 0 0 0 0 1 39 3 130Botswana 2 68 1 47 0 0 0 0 1 9 4 124BVMAC** 0 0 0 0 1 66 0 0 0 0 1 66Uganda 0 0 1 66 0 0 0 0 0 0 1 66Mauritius 1 10 0 0 0 0 1 29 0 0 2 39Tanzania 1 7 0 0 1 2 2 6 1 15 5 30Mozambique 0 0 0 0 1 11 0 0 0 0 1 11Zambia 0 0 0 0 0 0 1 9 0 0 1 9BRVM*** 0 0 0 0 0 0 1 7 0 0 1 7Ghana 0 0 0 0 0 0 1 1 2 1 3 2

Source: Dealogic

* Data includes IPOs listed on African exchanges and therefore excludes outbound IPOs. Companies listed on two exchanges or more are accounted for on each exchange.

** The BVMAC serves the Central African Republic, Chad, Congo, Equatorial Guinea and Gabon.

*** The BRVM serves the countries of Benin, Burkina Faso, Guinea Bissau, Côte d’Ivoire, Mali, Niger, Senegal and Togo.

PwC | 13

Top 10 African IPOs by value 2015 and 2014

Source: Dealogic

Figure 6: African top 10 IPOs by value, 2015 and 2014

Name Capital

raised $m Sector Country of

operationStock exchange

Top 10 IPOs 2015

Integrated Diagnostics Holdings plc 334 Health care Egypt London

Emaar Misr for Development SAE 299 Financials Egypt Cairo

Edita Food Industries SAE 267 Consumer goods Egypt Cairo/London

Orascom Construction Ltd 185 Industrials United Arab Emirates Cairo/Dubai

Schroder European Real Estate Investment Trust plc

162 Financials United Kingdom Johannesburg/London

Balwin Properties Ltd 131 Financials South Africa Johannesburg

Novus Holdings Ltd 98 Industrials South Africa Johannesburg

Stor-Age Property REIT Ltd 80 Financials South Africa Johannesburg

Capital Appreciation Ltd 75 Financials South Africa Johannesburg

Total Maroc SA 74 Oil & gas Morocco Casablanca

Top 10 IPOs 2014

SEPLAT Petroleum Development Co Ltd 538 Oil & gas Nigeria Lagos/London

Alexander Forbes Group Holdings Ltd 348 Financials South Africa Johannesburg

Residences Dar Saada SA 127 Financials Morocco Casablanca

Arabian Cement Co (Egypt) 109 Industrials Egypt Cairo

Rhodes Food Group Holdings Ltd 100 Consumer goods South Africa Johannesburg

Pivotal Fund Ltd 92 Financials South Africa Johannesburg

Delice Holding SA 67 Consumer goods Tunisia Tunis

Equites Property Fund Ltd 61 Financials South Africa Johannesburg

Tharisa plc 47 Basic materials South Africa Johannesburg

Cartrack Holdings Ltd 44 Industrials South Africa Johannesburg

The top 10 African IPOs by value in 2015 took place in South Africa, Egypt and Morocco.

IPOs of real estate and property companies (within the financials sector) specifically represented a greater share of top 10 IPOs during 2015.

14 | 2015 Africa Capital Markets Watch

Share price performance of 2015 and 2014 top 10 African IPOs

Figure 7 Share price performance of 2015 and 2014 top 10 African IPOs as at 31 December 2015

-64.9

-40.5

-86.9

17.7

27.5

-7.6

-0.7

95

10.6

-20.9

-100%-80% -60% -40% -20% 0% 20% 40% 60% 80% 100%

Cartrack Holdings Ltd

Tharisa plc

Equites Property Fund Ltd

Delice Holding SA

Pivotal Fund Ltd

Rhodes Food Group Holdings Ltd

Arabian Cement Co (Egypt)

Residences Dar Saada SA

Alexander Forbes Group Holdings Ltd

SEPLAT Petroleum Development Co Ltd

11.1

41.7

10

3.8

-3

-9.4

-11.7

10

-51

-27.9

-60%-50%-40%-30%-20%-10% 0% 10% 20% 30% 40% 50%

Total Maroc SA

Capital Appreciation Ltd

Stor-Age Property REIT Ltd

Novus Holdings Ltd

Balwin Properties Ltd

Schroder European Real Estate Investment Trust plc

Orascom Construction Ltd

Edita Food Industries SAE

Emaar Misr for Development SAE

Integrated Diagnostics Holdings plc

The Egyptian Exchange experienced a fourth-quarter decline amid heavy selling by foreign investors and Egyptian financial institutions, reflecting heightened geopolitical tensions introduced by attacks on tourist targets in October 2015.

Unsurprisingly, some of the stocks hardest hit in trading were those in the tourism and real estate sectors, with focus drawn to the outlook for the Egyptian tourism industry as a whole. Both Orascom Construction and Emaar Misr share prices were

impacted heavily as a result, leading to an announcement in January 2016 of Orascom’s intention to delist.

Of the top 10 African IPOs in 2014, SEPLAT’s share performance was hit heavily as a result of the global downturn in oil prices. Tharisa plc also lost ground from its offer price, potentially reflecting global mining sector sentiment, coupled with negative publicity, governance issues and a regulatory shutdown following workplace fatalities.

Meanwhile, Rhodes Food Group exhibited strong results, reflecting its growth through acquisition and the overall attractiveness of the food sector in 2015.

Other JSE shares with global revenue streams, such as Schroder European Real Estate Investment Trust (REIT) and Equities Property Fund, based in Europe and South Africa, respectively, continued to perform well, as local investors continue to seek exposure to companies with non-rand denominated income streams.

Source: Dealogic

2014

2015

PwC | 15

African IPO breakdown by sector 2011 – 2015

Figure 8: IPO breakdown by sector by value, 2011 – 2015 Figure 9: IPO breakdown by sector by volume, 2011 – 2015

FinancialsOil & gasConsumer goodsIndustrialsHealth careConsumer servicesUtilitiesBasic materialsTechnologyTelecommunications

1%1%2%

2011 – 2015 2011 – 2015

3%

5%

6%

9%

11%

11%

51%

4%

6%

3%

2%

8%

4%

13%

12%5%

43%

Source: Dealogic

Over the past five years, the financials sector led the African IPO market with 43% of total volume and 51% of total value, driven in part by an increase in property company listings, which are expected to continue in popularity in 2016, especially given the recent introduction of listed REITs on the Nairobi Securities Exchange. The oil & gas and consumer goods sectors followed in second place, each with a total value of 11%.

When looking at global trends over the same period, the financials sector topped the sector list by total IPO value. In terms of the sector profile of IPOs, Africa shared the greatest similarity with the Asia-Pacific region (with the exception of oil & gas). In both of these regions, financials, industrials and consumer goods contributed significantly to total IPO value.

16 | 2015 Africa Capital Markets Watch

African IPO breakdown by sector in 2015

Figure 10: IPO breakdown by sector by value, 2015

<1%

2%

2015 2015

1%

17%

14%

4%16%

46%

4% 7%

4%

4%

14%

14%

3%

50%

Financials

Oil & gas

Consumer goods

Industrials

Health care

Consumer services

Basic materials

Telecommunications

Source: Dealogic

During 2015, the financials sector continued to dominate the African IPO market at 46% of total value and 50% of total volume, followed by the health care, consumer goods and industrials sectors in terms of value. This is consistent with global IPO trends, where the financials sector proved to be the most active sector in 2015.

Health care ranked second at 17% and consumer goods third at 16% in terms of IPO value in 2015.

Compared to the average over the last five years, 2015 saw a slight decrease in the financials sector and an increase in industrials, consumer goods and health care in terms of value; and the industrials and consumer goods sectors in terms of volume.

Figure 11: IPO breakdown by sector by volume, 2015

PwC | 17

African FO trends 2011 – 2015

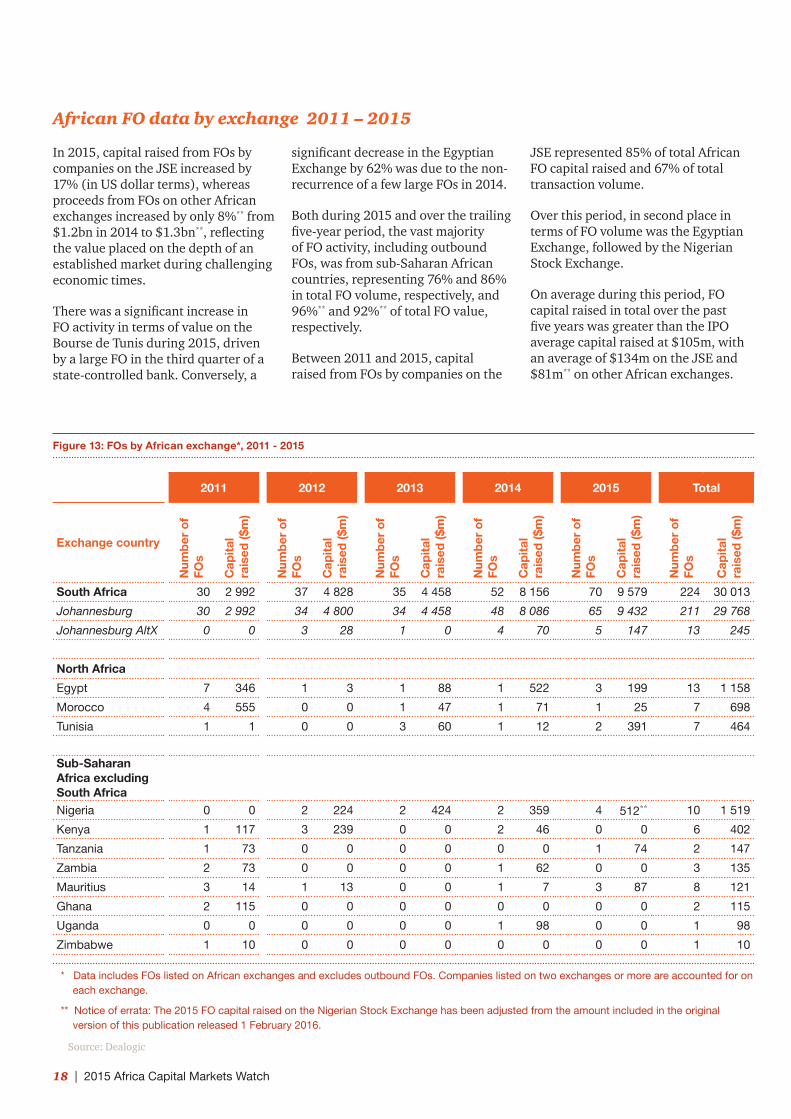

Over the past five years, there have been 336 FOs by African companies, raising $35.2bn on both African and international exchanges.

Though the growth rate of 2015 FO activity did not match that of the prior year, the trend was distinctively positive. During 2015, FO activity increased by 20% in terms of transaction volume and by 13% in terms of value, compared to 2014.

Additionally, total FO capital raised was bolstered by a $2.5bn offer on the JSE by Naspers Ltd in December 2015, which ranked among the top 10 FOs in the entire EMEA region in 2015.

Figure 12: FO trends, 2011 – 2015

African FO Market

0

2 000

4 000

6 000

8 000

10 000

12 000

201520142013201220110

20

40

60

80

100

120

FO Money raised ($m) Number of FOs

4 475

66

52 51

76

91

5 455 5 102

9 478

10 712

$mill

ion

Source: Dealogic

18 | 2015 Africa Capital Markets Watch

African FO data by exchange 2011 – 2015

Figure 13: FOs by African exchange*, 2011 - 2015

2011 2012 2013 2014 2015 Total

Exchange country

Num

ber

of

FOs

Cap

ital

ra

ised

($m

)

Num

ber

of

FOs

Cap

ital

ra

ised

($m

)

Num

ber

of

FOs

Cap

ital

ra

ised

($m

)

Num

ber

of

FOs

Cap

ital

ra

ised

($m

)

Num

ber

of

FOs

Cap

ital

ra

ised

($m

)

Num

ber

of

FOs

Cap

ital

ra

ised

($m

)

South Africa 30 2 992 37 4 828 35 4 458 52 8 156 70 9 579 224 30 013

Johannesburg 30 2 992 34 4 800 34 4 458 48 8 086 65 9 432 211 29 768

Johannesburg AltX 0 0 3 28 1 0 4 70 5 147 13 245

North Africa

Egypt 7 346 1 3 1 88 1 522 3 199 13 1 158

Morocco 4 555 0 0 1 47 1 71 1 25 7 698

Tunisia 1 1 0 0 3 60 1 12 2 391 7 464

Sub-Saharan Africa excluding South AfricaNigeria 0 0 2 224 2 424 2 359 4 512** 10 1 519

Kenya 1 117 3 239 0 0 2 46 0 0 6 402

Tanzania 1 73 0 0 0 0 0 0 1 74 2 147

Zambia 2 73 0 0 0 0 1 62 0 0 3 135

Mauritius 3 14 1 13 0 0 1 7 3 87 8 121

Ghana 2 115 0 0 0 0 0 0 0 0 2 115

Uganda 0 0 0 0 0 0 1 98 0 0 1 98

Zimbabwe 1 10 0 0 0 0 0 0 0 0 1 10

* Data includes FOs listed on African exchanges and excludes outbound FOs. Companies listed on two exchanges or more are accounted for on each exchange.

** Notice of errata: The 2015 FO capital raised on the Nigerian Stock Exchange has been adjusted from the amount included in the original version of this publication released 1 February 2016.

Source: Dealogic

significant decrease in the Egyptian Exchange by 62% was due to the non-recurrence of a few large FOs in 2014.

Both during 2015 and over the trailing five-year period, the vast majority of FO activity, including outbound FOs, was from sub-Saharan African countries, representing 76% and 86% in total FO volume, respectively, and 96%** and 92%** of total FO value, respectively.

Between 2011 and 2015, capital raised from FOs by companies on the

JSE represented 85% of total African FO capital raised and 67% of total transaction volume.

Over this period, in second place in terms of FO volume was the Egyptian Exchange, followed by the Nigerian Stock Exchange.

On average during this period, FO capital raised in total over the past five years was greater than the IPO average capital raised at $105m, with an average of $134m on the JSE and $81m** on other African exchanges.

In 2015, capital raised from FOs by companies on the JSE increased by 17% (in US dollar terms), whereas proceeds from FOs on other African exchanges increased by only 8%** from $1.2bn in 2014 to $1.3bn**, reflecting the value placed on the depth of an established market during challenging economic times.

There was a significant increase in FO activity in terms of value on the Bourse de Tunis during 2015, driven by a large FO in the third quarter of a state-controlled bank. Conversely, a

PwC | 19

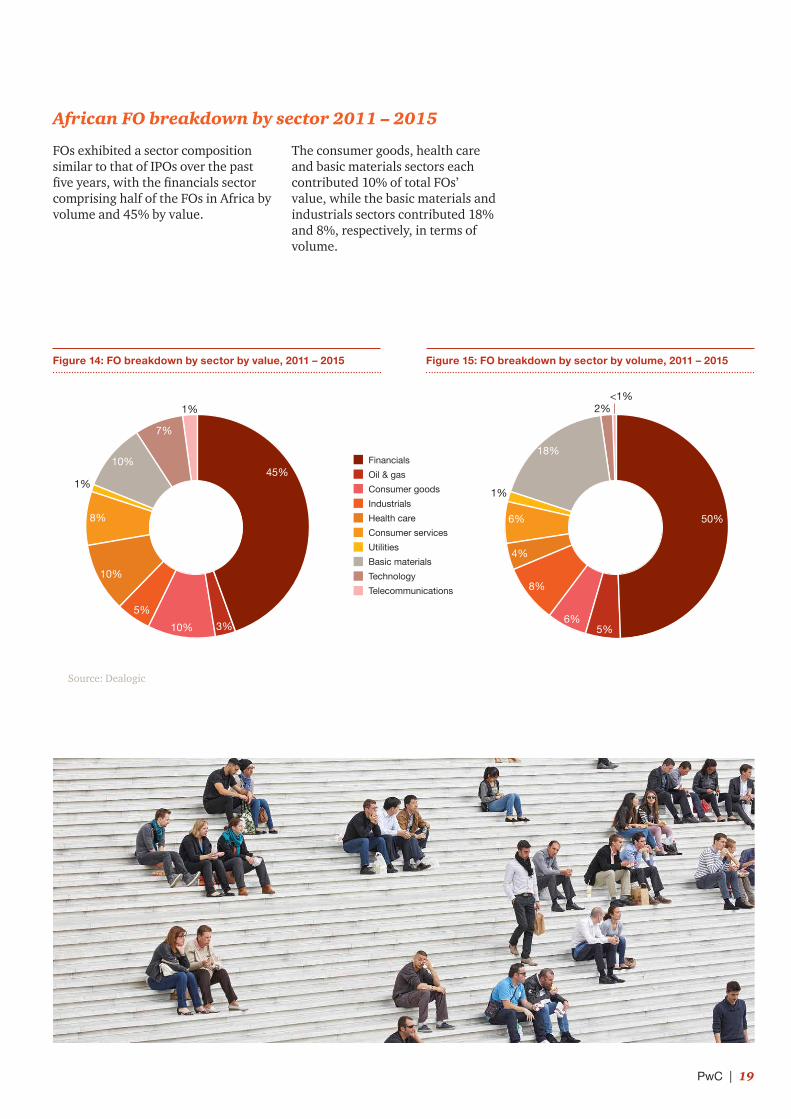

FOs exhibited a sector composition similar to that of IPOs over the past five years, with the financials sector comprising half of the FOs in Africa by volume and 45% by value.

Figure 14: FO breakdown by sector by value, 2011 – 2015 Figure 15: FO breakdown by sector by volume, 2011 – 2015

1%

2015 2015

1%

10%

8%

7%

10%

5%

10% 3%

45%

2%<1%

18%

6%

4%

6%

1%

8%

5%

50%

Financials

Oil & gas

Consumer goods

Industrials

Health care

Consumer services

Utilities

Basic materials

Technology

Telecommunications

Source: Dealogic

The consumer goods, health care and basic materials sectors each contributed 10% of total FOs’ value, while the basic materials and industrials sectors contributed 18% and 8%, respectively, in terms of volume.

African FO breakdown by sector 2011 – 2015

20 | 2015 Africa Capital Markets Watch

During 2015, there was a slight shift in the sector composition of African FO activity, with FOs in the financials sector being lower than their five-year average in terms of value. Conversely, there was a significant increase in the technology sector from 7% on average to 23% in 2015, due in large part to Naspers’ December rights issue of $2.5bn.

3%

2015 2015

3%

2%3%

9%

23%

4%

17%

36%

2% 1%

14%

6%

7%

8%

2% 3%

57%

FinancialsOil & gasConsumer goodsIndustrialsHealth careConsumer servicesBasic materialsTechnologyTelecommunications

Figure 16: FO breakdown by sector by value, 2015

Figure 17: FO breakdown by sector by volume, 2015

Source: Dealogic

The year saw a similar trend to the FO sector breakdown by volume over the past five years, during which the financials sector contributed more than half of the total FOs volume, followed by the basic materials sector at 14%.

African FO breakdown by sector in 2015

PwC | 21

Perhaps the clearest trend that has persisted since 2011 is the interest of African companies in executing dual listings or raising further offers on London’s stock exchanges, largely the Alternative Investment Market (AIM), which has proved a particularly attractive market for companies from emerging economies in Africa and Asia.

One such example is Lekoil, the Nigerian oil & gas exploration group that raised $49 million upon its flotation on the AIM in May 2013. Less than six months later, the group returned to the market to raise a further $100 million at a share price comfortably above its flotation price, enabling further exploration work off the Nigerian coast.

During the same period, the JSE remained popular for inbound IPOs, with only one other inbound listing in Africa – the debut of the United Arab Emirates’ Orascom Construction on the Egyptian Exchange.

The year saw both greater inbound and outbound global cross-border IPO activity than 2014. However, of note was the lack of intra-African cross-border IPO activity in 2015 despite moves towards regional exchange harmonisation. This likely reflects the more common response over the past year to use decreased listing barriers as an opportunity to deepen liquidity of shares via the introduction on other African exchanges, with a view towards future capital raising.

Cross-border activity will also be assisted by the Fast Track listing process for secondary inbound listings on the JSE. Already in 2016, Belgian brewing giant Anheuser-Busch (AB) InBev launched a secondary listing on the JSE through introduction, and Mediclinic International is expected to complete a secondary listing transaction during the year.

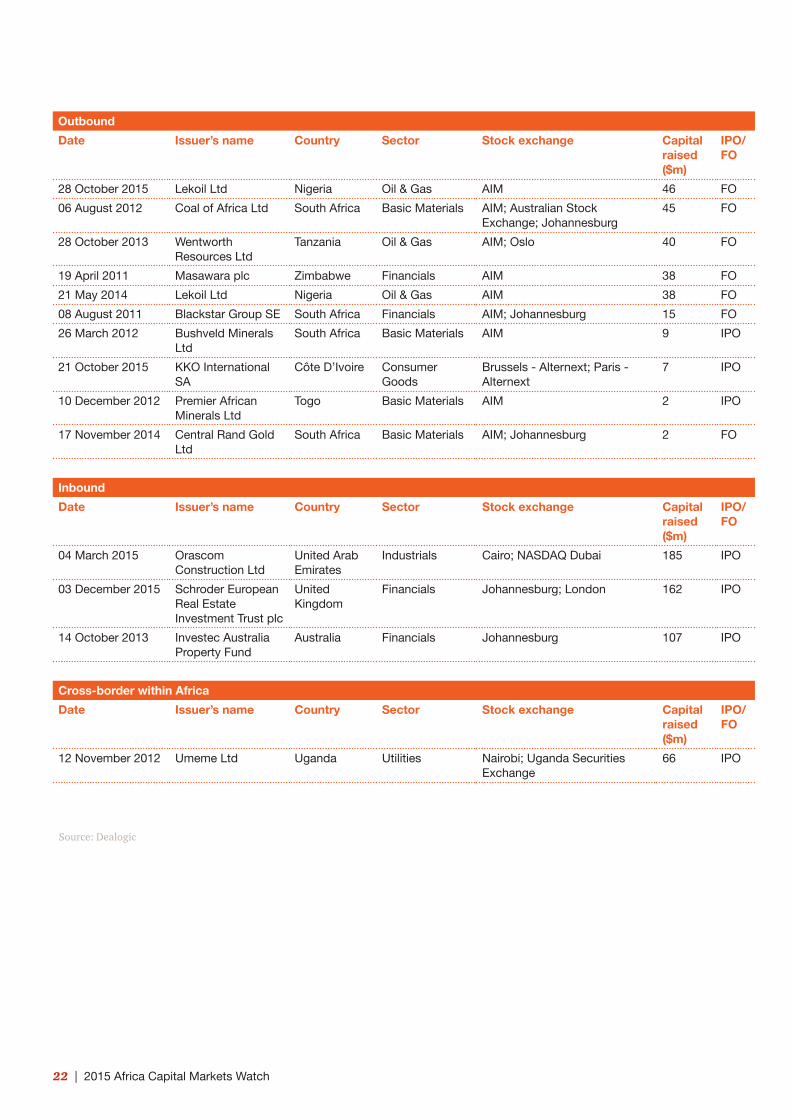

Figure 18: Outbound and Inbound IPOs and FOs, 2011 – 2015

Outbound

Date Issuer’s name Country Sector Stock exchange Capital raised ($m)

IPO/FO

09 April 2014 SEPLAT Petroleum Development Co Ltd

Nigeria Oil & Gas London; Nigerian Stock Exchange

538 IPO

05 May 2015 Integrated Diagnostics Holdings plc

Egypt Health Care London 334 IPO

01 April 2015 Edita Food Industries SAE

Egypt Consumer Goods

Cairo; London 267 IPO

15 May 2014 Aquarius Platinum Ltd

South Africa Basic Materials Australian Stock Exchange; Johannesburg; London

235 FO

08 August 2013 MiX Telematics Ltd South Africa Industrials New York 116 FO

03 November 2011 Coal of Africa Ltd South Africa Basic Materials AIM; Australian Stock Exchange; Johannesburg

106 FO

01 November 2013 Lekoil Ltd Nigeria Oil & Gas AIM 100 FO

11 July 2014 Delta International Property Holdings Ltd

South Africa Financials Bermuda; Johannesburg 87 FO

12 February 2013 Madagascar Oil Ltd Madagascar Oil & Gas AIM 75 FO

01 April 2015 Fastjet plc Tanzania Financials AIM 74 FO

10 August 2011 Elemental Minerals Ltd

South Africa Basic Materials Toronto 64 FO

27 June 2012 Namakwa Diamonds Ltd

South Africa Basic Materials London 56 FO

20 June 2011 Zambeef Products plc

Zambia Consumer Goods

AIM; Zambia 55 FO

17 May 2013 Lekoil Ltd Nigeria Oil & Gas AIM 49 IPO

African IPOs and FOs: Analysis of cross-border activity 2011 – 2015

22 | 2015 Africa Capital Markets Watch

Outbound

Date Issuer’s name Country Sector Stock exchange Capital raised ($m)

IPO/FO

28 October 2015 Lekoil Ltd Nigeria Oil & Gas AIM 46 FO

06 August 2012 Coal of Africa Ltd South Africa Basic Materials AIM; Australian Stock Exchange; Johannesburg

45 FO

28 October 2013 Wentworth Resources Ltd

Tanzania Oil & Gas AIM; Oslo 40 FO

19 April 2011 Masawara plc Zimbabwe Financials AIM 38 FO

21 May 2014 Lekoil Ltd Nigeria Oil & Gas AIM 38 FO

08 August 2011 Blackstar Group SE South Africa Financials AIM; Johannesburg 15 FO

26 March 2012 Bushveld Minerals Ltd

South Africa Basic Materials AIM 9 IPO

21 October 2015 KKO International SA

Côte D’Ivoire Consumer Goods

Brussels - Alternext; Paris - Alternext

7 IPO

10 December 2012 Premier African Minerals Ltd

Togo Basic Materials AIM 2 IPO

17 November 2014 Central Rand Gold Ltd

South Africa Basic Materials AIM; Johannesburg 2 FO

Inbound

Date Issuer’s name Country Sector Stock exchange Capital raised ($m)

IPO/FO

04 March 2015 Orascom Construction Ltd

United Arab Emirates

Industrials Cairo; NASDAQ Dubai 185 IPO

03 December 2015 Schroder European Real Estate Investment Trust plc

United Kingdom

Financials Johannesburg; London 162 IPO

14 October 2013 Investec Australia Property Fund

Australia Financials Johannesburg 107 IPO

Cross-border within Africa

Date Issuer’s name Country Sector Stock exchange Capital raised ($m)

IPO/FO

12 November 2012 Umeme Ltd Uganda Utilities Nairobi; Uganda Securities Exchange

66 IPO

Source: Dealogic

PwC | 23

African debt markets

In our inaugural analysis of the African debt markets, we have focused on the analysis of corporate HY and IG debt, which contributed 99% of the total corporate debt capital raised since 2011, and a brief discussion on supranational and sovereign debt during this five-year period.

It should be noted that DCM activity represents only a portion of the total debt raising activity in Africa, with a large component of debt funding sourced from traditional bank finance or other bilateral lending arrangements with investment funds that take place outside of the capital markets.

African DCM activity has declined since its peak in 2013, when African governments and corporates responded to initial signals of impending US monetary policy tightening by tapping debt markets.

As recently as 2007, South Africa, Egypt and Tunisia were the only African countries with sovereign bonds in issue in international markets. Since then, 15 countries have entered the debt markets, introducing formal credit analysis to guide country risk assessment and paving the way for expanded issuance by African corporates in these countries. Other advances in debt markets included the 2013 launch of a Nigerian over-the-counter trading platform, creating a secondary market for local debt.

While debt issuances have declined in volume and value since 2013, sovereign and supranational (including government agencies) debt, particularly foreign currency-denominated debt, continues to accumulate, introducing the discussion during the past year about the sustainability of the indebtedness of some countries. There are a number of

views on both sides of this discussion, but what is clear is the role this funding has played in encouraging debt market activity on the continent.

Over the past five years, 489 debt transactions have taken place on African debt markets or by African companies on international markets, raising $110.2bn, of which 72% was US dollar-denominated.

Though African debt markets were not as active in 2015 as in the previous two years, the average of proceeds raised in 2015 was $411m per transaction, 26% higher than 2014’s average of $326m and 83% higher than the average per transaction over the past five years of $225m.

Figure 19: DCM activity*, 2011 - 2015

0

5000

10000

15000

20000

25000

30000

201520142013201220110

20

40

60

80

100

120

140

160

Corporate debt value ($m)

Number of transactionsSovereign and Supranational (including government agencies) debt value ($m)

8 352

103

142

129

68

47

7 932

10 100

6 233

5 707

11 39712 346

18 554

15 964

13 593

$mill

ion

* Tranches within a deal are counted as a single issuance.

Source: Dealogic

African debt markets overview

24 | 2015 Africa Capital Markets Watch

Figure 20: Breakdown of corporate debt by value, 2011 - 2015 Figure 21: Breakdown of sovereign and supranational (including government agencies) debt by value, 2011 - 2015

* Investment grade and high-yield designation per Dealogic ** ‘Sovereign’ includes all debt issued by national or provisional governments, and local authorities. *** ‘Supranational’ includes all debt issued by institutions organised at a world or regional level. **** ‘Agency’ refers to issuers that carry out government objectives while not being legally owned by a government itself. Agency debt usually carries an actual or implied government guarantee.

Source: Dealogic

1%

31%

68%

4%

28%

68%

Corporate Bond –Investment Grade*

Corporate Bond –High Yield*

Sovereign,Local Authority**

Supranational***

Short-termDebt

Agency****

PwC | 25

Between 2011 and 2015, there were 38 African corporate HY debt issuances, raising $11.7bn, of which 62% was US dollar denominated and half of which was raised under the US Securities and Exchange Commission’s (SEC) Rule 144A*, reflecting the strong demand for high-yield debt securities by US investors during this period.

In 2015, there was a significant decrease of 57% in HY debt issued by value as compared to 2014, with a similar level of average proceeds raised per transaction of $303m, as compared to $309m on average over the past five years. This decline likely reflects a degree of caution in the market in response to increased volatility during the year, especially from those companies looking to raise debt for planned acquisitions.

HY debt proceeds have been raised predominantly in US dollars during the past five years, comprising 62% of all proceeds, followed by the euro at 23%.

Unlike HY debt raised in more developed markets, characteristics of African HY debt instruments (excluding South Africa) are more commonly vanilla in nature; HY ratings for such debt are largely driven by the ‘ceiling’ on corporate credit ratings imposed by a home country’s own sovereign rating.

Figure 22: African high-yield debt value and volume, 2011 – 2015

Figure 23: African high-yield debt by SEC Rule 144A and volume, 2011 – 2015

Figure 24: African high-yield proceeds by currency, 2011 – 2015

0

500

1 000

1 500

2 000

2 500

3 000

3 500

201520142013201220110

2

4

6

8

10

12

14

16

Value ($m) Volume

2 639

5 5

14

10

4

1 879

3 1962 823

1 210$m

illio

n

50% 50%Not Rule 144ARule 144A

4%

4%3%

4%

23%

62%USD

EUR

GBP

ZARNGN

Others

Source: Dealogic

African high-yield debt market

*SEC Rule 144A provides a non-exclusive safe harbour from the registration requirements of the United States Securities Act of 1933 for sales of securities to “qualified institutional buyers” (QIBs), a term that encompasses banks, insurance companies, certain trust funds, pension plans, corporations and broker-dealers (but not individuals), who meet certain ownership and investment thresholds. Rule 144A offerings have become popular among foreign issuers as they provide a means to raise capital in the US capital markets without being subject to the registration and reporting requirements of a public offering with the SEC.

Trends between 2011 – 2015

26 | 2015 Africa Capital Markets Watch

African high-yield debt credit rating and average yield-to-maturity 2011 – 2015

Figure 25: African high-yield debt credit rating and average yield-to-maturity, 2011 - 2015

* Selection of bond ratings in the table above reflects the availability of ratings information for these issuances. S&P ratings have been used when available, followed by Moody’s when available, followed by Fitch. 11 of the debt issuances have no publicly available rating information.

Source: Dealogic, Bloomberg

Bond ratings* Number of transactions

Average yield-to- maturity (%)

BB+/Ba1 3 6.9

BB 4 6.3

BB-/Ba3 3 9.3

B+ 4 11.7

B 8 8.9

B- 4 10.3

CCC 1 13.4

Data not available 11 9.1

Grand Total/Total Average 38 9.0

PwC | 27

African high-yield debt by exchange nationality 2011 – 2015

Figure 26: African high-yield debt by exchange nationality, 2011 –2015

0

500

1 000

1 500

2 000

2 500

3 000

3 500

20152014201320122011

United States Europe Africa

$mill

ion

220

1 149

80 126154 271

1 885

534

6503 070

2 669

939

Over the past five years, the majority of African HY debt was issued by South African and Nigerian companies, at 42% and 41% by value, respectively.

Our data highlights that a variety of structuring methods and listing destinations have been used in recent issuances. We observe from this data that during the period 2011-2015, HY debt, unlike equity capital, was largely raised outside the continent, with the exception of issuances by Botswanan, Nigerian and South African companies on local exchanges, which accounted for 7% of total proceeds raised, and the Nairobi listing by East African Breweries, accounting for less than 1% of total proceeds.

Source: Dealogic

28 | 2015 Africa Capital Markets Watch

Figure 27: African high-yield debt by deal issuer and exchange nationality, 2011-2015

Deal nationality*

Issuer nationality of incorporation

Exchange nationality Currency code

Number of transactions

USD equivalent

proceeds ($m)

South Africa

South Africa

Irish Stock ExchangeEUR 1 825

USD 1 250

Frankfurt Stock Exchange EUR 1 573

New York Stock Exchange EUR 1 534

Johannesburg Stock Exchange ZAR 6 343

SIX Swiss Exchange CHF 1 115

Austria Luxembourg Stock ExchangeUSD 1 1 050

EUR 2 841

United Kingdom London Stock Exchange GBP 1 454

Nigeria

Nigeria

Irish Stock Exchange USD 7 2 426

Oslo Børs USD 1 575

Nigerian Stock Exchange NGN 2 374

London Stock Exchange USD 1 350

NetherlandsIrish Stock Exchange USD 2 893

London Stock Exchange USD 1 250

United States**

Liberia** New York Stock Exchange USD 1 650

Mauritius Mauritius NASDAQ OMX Nordic (Stockholm) SEK 3 312

Morocco France Luxembourg Stock Exchange USD 1 297

Ghana Ireland Irish Stock Exchange USD 1 253

Togo Nigeria Irish Stock Exchange USD 1 248

Botswana Botswana Johannesburg Stock Exchange ZAR 1 80

Kenya Kenya Nairobi Securities Exchange KES 1 54

Grand Total

38 11 747

* Deal nationality is a calculated nationality that combines the business nationality of the issuing entity with that of the originator or, if undisclosed, the nationality of risk.

** The US deal relates to Royal Caribbean Cruises Ltd, a company incorporated in Liberia with global operations.

Source: Dealogic

PwC | 29

Figure 28: African country credit ratings*, 2011 – 2015

African high-yield debt by industry 2011 – 2015

Over the period 2011-2015, African HY debt was mainly raised by companies in the financials sector, which comprised 58% of total HY debt volume and 47% of total value.

Sector composition for HY debt over this period is similar to that observed for ECM activity during this time.

Figure 29: African high-yield debt by industry, 2011-2015

Industry Volume Value ($m)

Financials 22 5 544

Consumer goods 5 2 236

Basic materials 3 1 891

Industrials 3 704

Oil & gas 1 575

Utilities 2 514

Telecommunications 1 250

Technology 1 33

Total 38 11 747

Source: Thomson Reuters

Source: Dealogic

20152014201320122011

A-

BBB+

BBB

BBB-

BB+

BB

BB-

B+

B

B-

Botswana

Mauritius

South AfricaMorocco

Nigeria

Ghana

Kenya

*Only countries with a sovereign credit rating, which also had HY debt activity during 2011 – 2015, have been presented above.

30 | 2015 Africa Capital Markets Watch

4%

4%4%

22%

66%

USD

ZAR

EUR

GBP

Others

Others

USD

ZAR

EUR

GBP

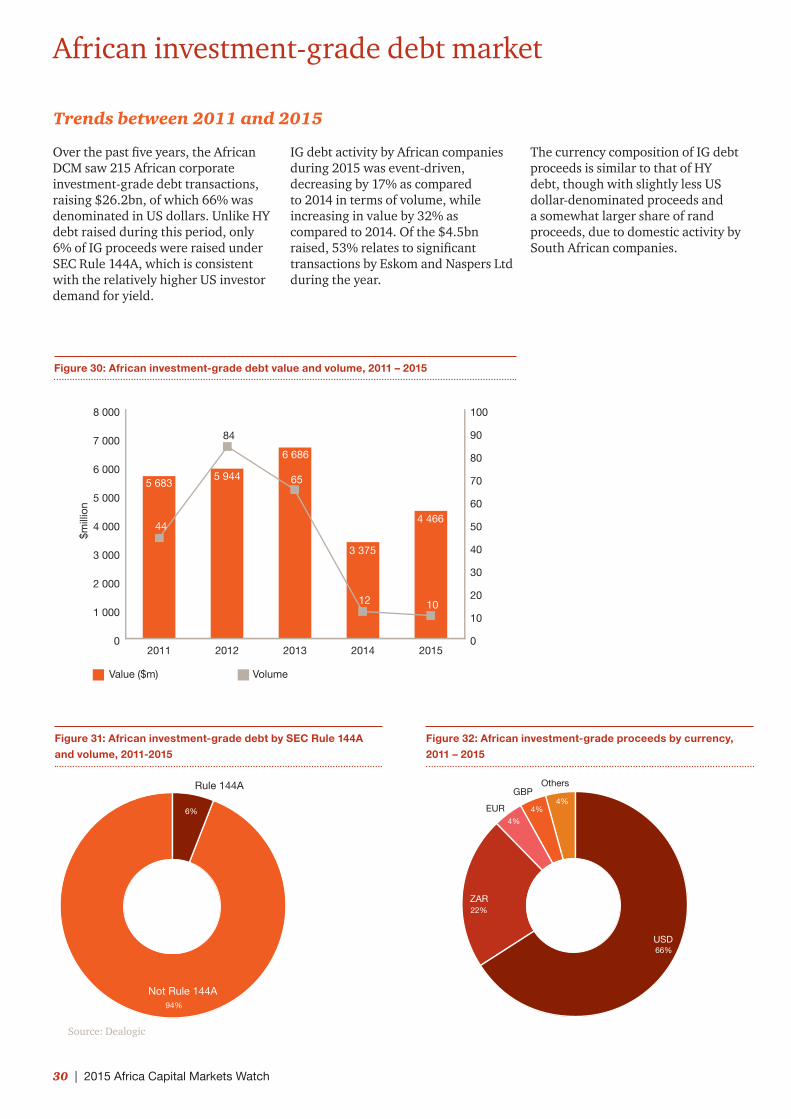

Over the past five years, the African DCM saw 215 African corporate investment-grade debt transactions, raising $26.2bn, of which 66% was denominated in US dollars. Unlike HY debt raised during this period, only 6% of IG proceeds were raised under SEC Rule 144A, which is consistent with the relatively higher US investor demand for yield.

African investment-grade debt market

Figure 30: African investment-grade debt value and volume, 2011 – 2015

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

201520142013201220110

10

20

30

40

50

60

70

80

90

100

Value ($m) Volume

5 683

44

84

65

12 10

5 944

6 686

3 375

4 466

$mill

ion

94%

6%

Not Rule 144ARule 144A

Rule 144A

Not Rule 144A

Figure 31: African investment-grade debt by SEC Rule 144A and volume, 2011-2015

Source: Dealogic

Figure 32: African investment-grade proceeds by currency, 2011 – 2015

IG debt activity by African companies during 2015 was event-driven, decreasing by 17% as compared to 2014 in terms of volume, while increasing in value by 32% as compared to 2014. Of the $4.5bn raised, 53% relates to significant transactions by Eskom and Naspers Ltd during the year.

The currency composition of IG debt proceeds is similar to that of HY debt, though with slightly less US dollar-denominated proceeds and a somewhat larger share of rand proceeds, due to domestic activity by South African companies.

Trends between 2011 and 2015

PwC | 31

Figure 33: African investment-grade proceeds by currency and average yield-to-maturity, 2011 – 2015

Currency code Average yield-to-maturity

NGN 12.76

ZAR 8.67

GBP* 7.38

USD 4.87

EUR 4.11

CNH 3.95

CHF 3.04

Average yield-to-maturity 7.63

* Yield-to-maturity data for debt raised in pounds sterling reflects the subordinated nature of the specific debt instruments.

Source: Dealogic

African investment-grade debt by exchange nationality 2011 – 2015

The story of African IG debt over the past five years is, predictably, a largely South African affair, with issuance across global exchanges dominated by South African companies or subsidiary entities. Exceptions include $2.8bn raised by Morocco’s Groupe OCP on the Irish Exchange.

Figure 34: African investment-grade debts by exchange nationality and value, 2011-2015

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

20152014201320122011

United States Europe Africa

$mill

ion

1 570

2 842

1 003 2 611 128

2 959

288

168

4 113

1 340

2 099

2 7352 669

4 298

Source: Dealogic

32 | 2015 Africa Capital Markets Watch

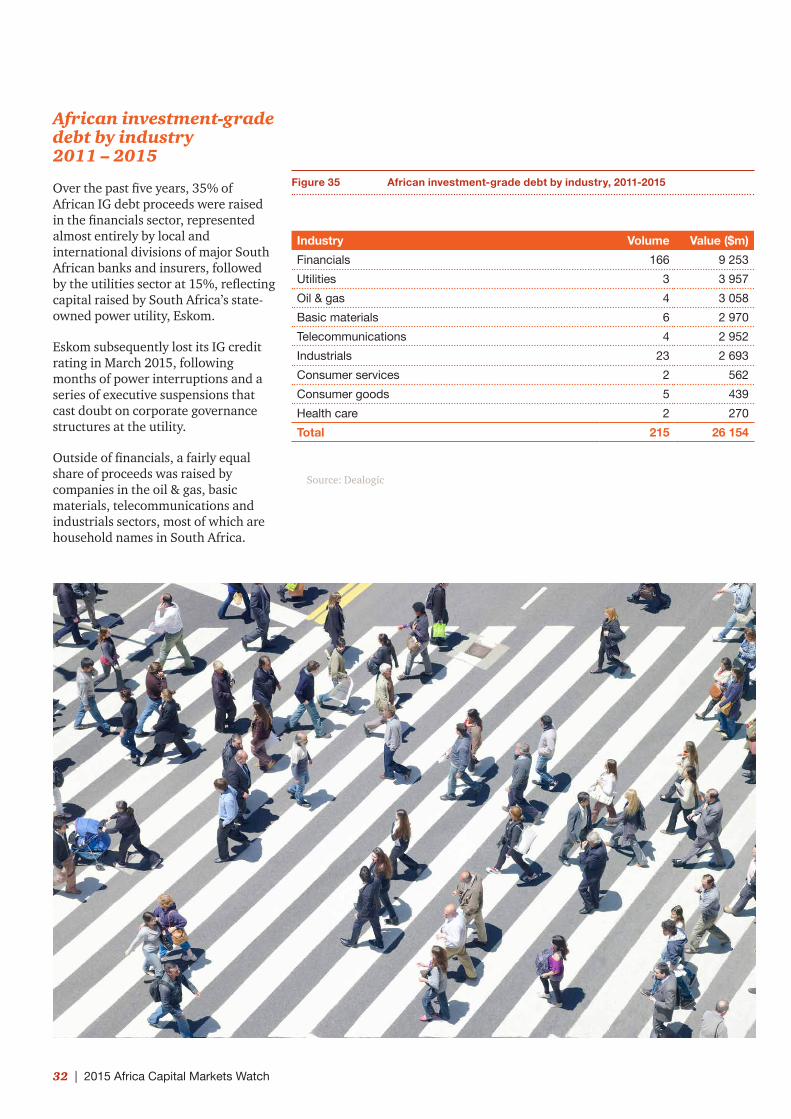

African investment-grade debt by industry 2011 – 2015

Over the past five years, 35% of African IG debt proceeds were raised in the financials sector, represented almost entirely by local and international divisions of major South African banks and insurers, followed by the utilities sector at 15%, reflecting capital raised by South Africa’s state-owned power utility, Eskom.

Eskom subsequently lost its IG credit rating in March 2015, following months of power interruptions and a series of executive suspensions that cast doubt on corporate governance structures at the utility.

Outside of financials, a fairly equal share of proceeds was raised by companies in the oil & gas, basic materials, telecommunications and industrials sectors, most of which are household names in South Africa.

Figure 35 African investment-grade debt by industry, 2011-2015

Industry Volume Value ($m)

Financials 166 9 253

Utilities 3 3 957

Oil & gas 4 3 058

Basic materials 6 2 970

Telecommunications 4 2 952

Industrials 23 2 693

Consumer services 2 562

Consumer goods 5 439

Health care 2 270

Total 215 26 154

Source: Dealogic

PwC | 33

East Africa

André Bonieux [email protected] +230 404 5061

Anthony Murage [email protected] +254 20 285 5347

Francophone Africa & Maghreb

Philippe Couderc [email protected] +212 5229 99801

North Africa

Steve Drake [email protected] +971 4 304 3421

Contacts

West Africa

Omobolanle Adekoya [email protected] +234 (1) 271 1700 ext 3102

Darrell McGraw [email protected] +234 706 401 9361

Southern Africa

Craig Du Plessis [email protected] +27 11 797 4055

Andrew Del Boccio [email protected] +27 11 287 0827

Nicholas Ganz [email protected] +27 11 797 5568

Peter McCrystal [email protected] +27 11 797 5275

Coenraad Richardson [email protected] +27 11 797 4713

We extend our thanks to everyone who contributed to PwC’s 2015 Africa Capital Markets Watch. This marks the first year in the life of the Africa Capital Markets Watch series, and our second look at equity capital markets in Africa. In particular, we would like to thank Andrew Del Boccio, Laure Fine, Chi Le, Alice Tomdio and Christine Van Den Bos for their important contributions.

Acknowledgements

For a deeper discussion about our capital market offerings in Africa, please contact one of our practice leaders below.

Global IPO Centre

Clifford Tompsett [email protected] +44 20 7804 4703

www.pwc.co.za

The information contained in this publication by PwC is provided for discussion purposes only and is intended to provide the reader or his/her entity with general information of interest. The information is supplied on an “as is” basis and has not been compiled to meet the reader’s or his/her entity’s individual requirements. It is the reader’s responsibility to satisfy him or her that the content meets the individual or his/her entity’s requirements. The information should not be regarded as professional or legal advice or the official opinion of PwC. No action should be taken on the strength of the information without obtaining professional advice. Although PwC take all reasonable steps to ensure the quality and accuracy of the information, accuracy is not guaranteed. PwC, shall not be liable for any damage, loss or liability of any nature incurred directly or indirectly by whomever and resulting from any cause in connection with the information contained herein.

©2016 PricewaterhouseCoopers (“PwC”), the South African firm. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers in South Africa, which is a member firm of PricewaterhouseCoopers International Limited (PwCIL), each member firm of which is a separate legal entity and does not act as an agent of PwCIL.

(16-18253)