Embed Size (px)

Citation preview

for the National Australia Bank Group Superannuation Fund A

2014Annual Report

This report is issued by National Australia Bank Superannuation Fund Pty Ltd ABN 99 065 048 928 AFSL 24 1720 (Trustee), the trustee of the National Australia Bank Group Superannuation Fund A (NABGSF) ABN 59 929 570 050 (Fund).

The administrator of the Fund is Plum Financial Services Limited ABN 35 081 812 731 AFSL 243356 (Plum).

Preparation date: 07 October 2014

Contents

What is covered in this report

1. A year in review ............................................................................................................................................................. 4

2. Looking out for your interests ...................................................................................................................................... 5

3. Legislative updates ........................................................................................................................................................ 7

4. Fund developments ....................................................................................................................................................... 8

5. Administering your account ......................................................................................................................................... 9

6. How your money is invested ....................................................................................................................................... 11

7. Investment option profiles ......................................................................................................................................... 14

8. Fund accounts ...............................................................................................................................................................17

9. How to contact Plum ................................................................................................................................................... 20

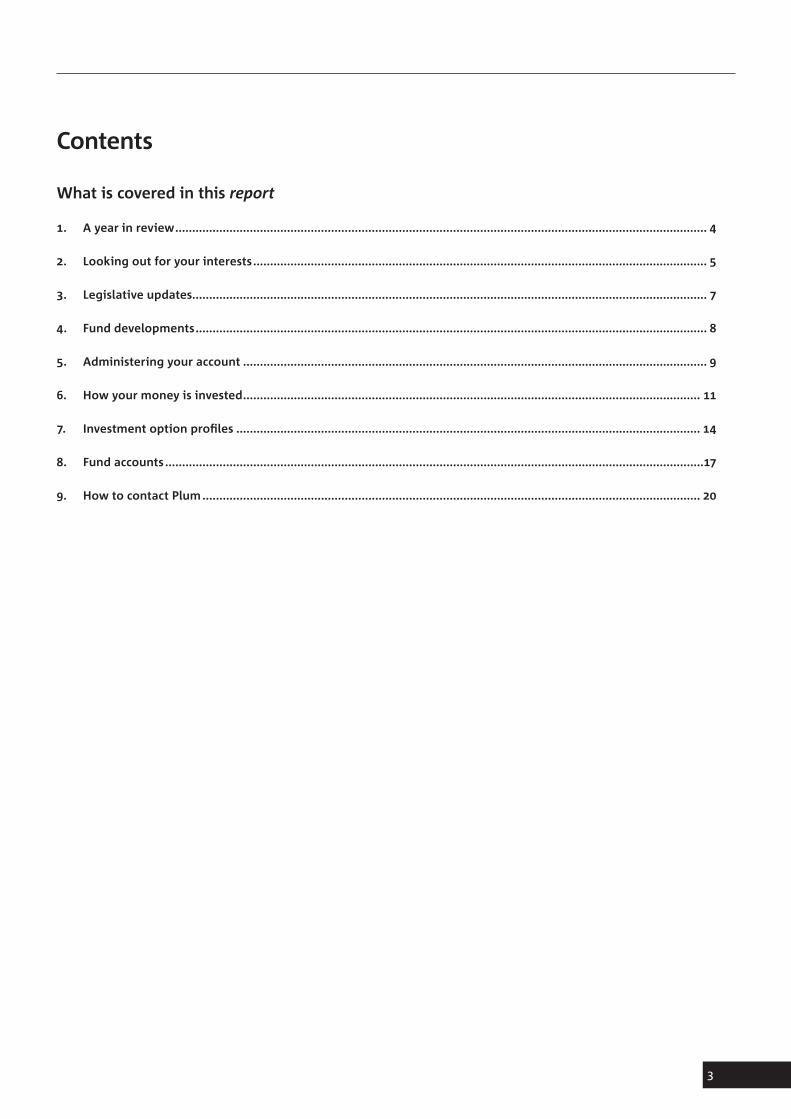

1. A year in review

Investments Of course, it is important to remember that the focus should not be on returns over a single year, but on the longer term performance of your investments.

We offer a range of investment options, which are diversified across many different asset classes and targeting differing levels of risk and return. We encourage you to visit nabgsf.com.au where you can view our publication on investing which may be of use when making your investment decisions, as well as additional information on investments and market performance.

Plum also offers a financial advice service which is available to all members. So if you feel you need some advice on your investments, or have questions about any other aspect of your superannuation, please contact Plum on 1300 55 7586.

Performance of the Fund’s assets over time periods to 30 June 2014

Investment option

2013/2014 Return #

3 year compound annualised

return

5 year compound annualised

return

10 year compound annualised

return

Since inception compound

annualised return (refer notes)

NABGSF MySuper***

2.89% n.a. n.a. n.a. n.a.

High Growth* 16.69% 10.89% 10.17% 7.80% 7.89%

Growth* 13.95% 9.43% 8.90% 6.99% 7.23%

Balanced* 10.15% 8.13% 8.29% 6.86% 7.03%

Capital Stable* 7.82% 6.88% 7.26% 6.23% 6.39%

Cash* 2.80% 3.46% 3.75% 4.89% 4.97%

Fixed Interest** 5.30% 6.16% 7.42% 5.52% 5.50%

Australian Shares**

18.33% 10.45% 11.28% 8.91% 8.87%

Overseas Shares**

19.85% 12.66% 10.33% 4.75% 4.73%

* The option commenced 1 July 1999, and as such the since inception return is a compound annualised return since that date.

**The option commenced 9 June 2004, and as such the since inception return is a compound annualised return since that date.

*** This option commenced 1st January 2014 and as such the 2013/2014 return is the 6 month return for the period ending 30 June 2014.

# The investment returns reflect the earnings of the option after allowing for taxes and investment expenses and are based on the last unit price declared in each financial year.

2. Looking out for your interests

The Trustee directors have a variety of work and life experiences which help them represent your interests.Made up of NAB representatives and member representatives who are personally responsible for any decisions they make, their duties include:

• providing investment choice;

• ensuring your interests are maintained; and

• keeping you informed of any changes.

We have appointed Plum Financial Services Limited to carry out the day-to-day administration of the National Australia Bank Group Superannuation Fund A (Fund).

Meet the BoardThe directors are:

NAB representativesGeoff Webb – Chair

• Bachelor of Economics (Honours);

• Associate of the Institute of Actuaries (London);

• Associate of the Institute of Actuaries of Australia;

• Graduate of the Advanced Management Programme, Melbourne Business School;

• Graduate of the Australian Institute of Company Directors; and

• Association of Superannuation Funds of Australia (ASFA) – Certificate of Trusteeship.

Greg Braddy

• Associate, Institute of Chartered Accountants Australia; and

• Bachelor of Business Studies (Accounting).

Bob Brice

• Bachelor of Business Banking and Finance;

• Graduate Diploma in Applied Finance and Investments;

• Graduate Diploma of Financial Planning; and

• Master Applied Finance.

Jim Young

• Bachelor of Special Education;

• Master of Business Administration;

• Trained Primary Teachers Certificate; and

• Australian Institute of Superannuation Trustees – Induction.

Member representativesJulie Kurkowski

• Masters and Law degree;

• Graduate of the Australian Institute of Company Directors;

• Bachelor of Arts (Hons); and

• Australian Institute of Superannuation Trustees – Induction.

Warwick Lee

• Bachelor of Economics;

• Bachelor of Law;

• Graduate Diploma of Financial Planning;

• Certificate of Superannuation Management (Association of Superannuation Funds of Australia – ASFA); and

• Association of Superannuation Funds of Australia (ASFA) – Certificate of Trusteeship.

Sharon Sims

• Advanced Diploma of Financial Planning;

• Australian Institute of Superannuation Trustees – induction; and

• Australian Property Institute – Certificate in Property Lending.

Patrick Nolan

• Bachelor of Arts;

• Bachelor of Business (Banking and Finance);

• Graduate Diploma of Business (Accounting);

• Australian Institute of Superannuation Trustees – Induction; and

• Graduate of the Australian Institute of Company Directors.

Trustee meeting attendance

Trustee Director

No. meetingsNo. of meetings

attended

Geoff Webb (Chairman)

4 4

Greg Braddy 4 4

Bob Brice 4 4

Julie Kurkowski 4 4

Warwick Lee 4 4

Janelle Mason 0 0

Patrick Nolan 4 4

Sharon Sims 3 3

Jim Young 4 4

Audit and Risk Committee Attendance

Committee Member

No. meetingsNo. of meetings

attended

Greg Braddy (Chairman)

3 3

Bob Brice 3 3

Patrick Nolan 3 3

Trustee director movementsDuring this year Ms. Janelle Mason resigned as a Member Elected Trustee Director and was replaced by Ms. Sharon Sims as per Rule 18 of the Election Rules. The Election Rules are published on the Fund's website under Forms and Publications.

Member Elected Trustee Directors (Directors of the Corporate Trustee) hold office until 31st December 2014 at which time an election is due to be held. Further information will be provided to members by November 2014 regarding this matter.

The removal of a member-representative director shall be either when/he she ceases to be a member, ceases to be an ‘eligible’ person or when the majority of members call for his/her removal.

If there is a casual vacancy for a member-representative director, the unsuccessful candidate at the previous election who received the highest number of votes will be invited to fill the vacancy until the next election.

The NAB representative Trustees (also directors of the Corporate Trustee), are appointed at the discretion of NAB Limited.

Trustee Indemnity InsuranceTrustee insurance to further secure the assets of the Fund and to cover any undue risks associated with the actions of the Trustee and others associated with the administration of the Fund is held with Lloyd’s of London.

Annual auditEach year we are audited by an independent company.

We’re pleased to report we’ve met all our obligations and received a clean audit report.

3. Legislative Change

The Stronger Super Reforms have arrivedAustralian superannuation funds have invested significantly to comply with these reforms, some of which are designed to improve member services.

Introduction of MySuper (effective 1st January 2014)

NABGSF MySuper is a simple and cost effective default investment option for members who do not make an active choice on how their super is invested. NABGSF MySuper is also available for most existing members upon request.

The introduction of the new NABGSF MySuper investment option means members now have a ninth investment option to choose from.

MySuper regulations also meant the way we charged fees in the past had to be changed. The Fund was no longer allowed to charge fees based on a percentage of Fund Salary and have introduced a weekly charge plus a percentage charge based on a member’s account balance. The Trustee acknowledges for some members this may increase their overall fee costs, however the overall fee income derived across the entire Fund membership (designed to cover fund operating costs only) will not increase and some members will pay less.

The MySuper regulations also required a change in the way insurance premiums are deducted. The previous charge based on a percentage of Fund Salary also has been replaced by a direct premium based on a member’s age and level of cover which is designed to reflect more fairly on a member’s perceived level of risk rather than their Fund Salary.

If you were invested 100% in the Growth investment option on the 31st December 2013 your account balance at that date as well as any future contributions made on your behalf will be invested in NABGSF MySuper unless you took the opportunity provided to ‘opt out’ of this event (except for Defined Benefit Members).

Superstream (electronic rollovers) (effective 1st January 2014)

Superstream now requires money to be transferred between funds (rollovers) electronically within 3 days improving the previous paper based / cheque and mailing system (not including transfers to Self Managed Superannuation Funds). This will significantly improve efficiency, reliability and overall member experience.

Statutory ReportingSuperannuation funds have also invested heavily complying with new requirements to report a significant amount of additional fund related data to the Australian Prudential Regulation Authority (APRA) for use in research and publication in members’ best interests.

Increase in the Superannuation Guarantee Charge (SG)(effective 1st July 2014)

The compulsory contribution rate for employers increased from 9.25% to 9.5% of employees’ Ordinary Time Earnings (OTE).

This rise also coincided with a delayed introduction of the rise of the SG rate to 12% until 2022/2023.

*Excess non-concessional contribution withdrawalsIndividuals who make contributions exceeding their non-concessional contribution cap from 1 July 2013 will have the option to withdraw the excess amount, plus earnings on the excess. No tax will be payable on the excess amount withdrawn. However, withdrawn earnings will be taxed at the individual’s marginal tax rate. If no election is made to withdraw the excess contributions, the excess will be taxed under the existing regime at the top marginal tax rate.

Changes to the Annual Contribution Caps(effective 1st July 2014)

The Concessional Contribution Cap (CCC) has increased from $25,000 p.a. to $30,000 p.a and from the same base to $35,000 p.a for those members who are aged 50 and above on 30th June 2015. It is proposed that the CCC will be $35,000 p.a for all members from 2015 / 2016.

To remain at 6 times the CCC, the Non-Concessional Contribution Cap has increased from $150,000 to $180,000 p.a.

*Abolition of the Low Income Superannuation ContributionIntroduced for the 2012 / 2013 financial year, this is to be abolished from the 2014 / 2015 year. The scheme aimed to effectively refund the 15% tax applied to concessional (employer) contributions for members on an income level of $37,000 p.a. or less (capped at $500 p.a)

Medicare Superannuation Lump Sum Tax Changes (effective 1st July 2014)

The Government has increased the Medicare levy for most Australians from 1.5% to 2% to fund the National Disability Insurance Scheme. This higher rate will also apply to taxable lump sum superannuation benefits and income stream payments.

*Income Tax ChangesA 2% temporary levy will apply to person’s whose income exceeds $180,000 p.a. as a temporary national debt relief measure. *Announced as part of the Government’s 2014 Federal Budget which are yet to be legislated at the time of writing.

Operational risk reserve (ORR)As part of the Stronger Super reforms, the government introduced a new requirement for super funds to keep a financial reserve to cover any losses that members incur due to a breakdown in operations.

The ORR is invested in the investment option shown below.

Operational risk reserve investment strategy

Option Proportion (%)

Growth 100%

The balance of the ORR at the end of the last three financial years is summarised below:

Year ended 30 June

Plan reserve ($)

2014 $4,976,881

2013 n.a.

2012 n.a.

4. Fund developments

Your Fund has undergone many new changes during the year, some of which were designed to improve the Fund in terms of services and benefits, whilst some were to comply with regulatory change.

The major changes included:

• A new investment strategy for default contributions (NABGSF MySuper);

• New regulatory standards in relation to the type of fees that can be charged fees which changed the basis for charging fees in NABGSF;

• Changes to the basis of charging insurance premiums from being based on Fund Salary to a direct cost based on age and level of cover;

• Changes in the definition of Total and Permanent Disablement;

• Removal of the Partial Disablement benefit;

• Changes to the cover provided under the Extra Cover Death, Disablement and Temporary Disablement options; and

• Unit Prices being calculated on a daily basis (previously weekly).

In addition to these changes the Trustee also arranged with Plum Financial Services Limited to fully integrate its previous stand alone administration team within the Plum organisation (known as the Plum ‘full service model’). By doing so, it is envisaged that Fund members will enjoy enhanced website content and functionality whilst gaining access to Plum’s member education and communication capability.

Your Trustee communicated these changes during the year.

5. Administering your account

Retained Benefits Account facilityShould you leave NAB, the Fund has a Retained Benefits Account (RBA) facility that allows you to maintain your membership of the Fund, including continuation of your Death and Total and Permanent Disablement cover. The RBA can accept your leaving service benefit and any subsequent contributions from you, your spouse or your future employers. It can also accept superannuation lump sums you may wish to transfer from other funds.

There is no maximum investment in the RBA; however there is a minimum investment of $5,000. Withdrawals of unrestricted non-preserved monies may be made with a minimum withdrawal amount of $5,000 applying and subject to the minimum investment being maintained.

The fee applicable to the RBA facility compares favourably against other similar products. There are no entry or exit fees, with a low administration fee of $1.75 per week and a management fee of 0.14% p.a. based on your account balance. In addition, investments costs between 0.11% and 0.86% (indicative only) are deducted prior to the unit prices being issued and earnings credited to members’ account.

Further details are included in the RBA booklet available at nabgsf.com.au/publications

Spouse Account FacilityThe Fund also has a Spouse Account facility to enable members’ spouses to join the Fund.

The Fund can accept a Spouse of an existing member as a member upon receipt of a spouse contribution from the existing member. From there, the Fund can accept personal or employer contributions for the spouse as well as spouse contributions paid by their spouse. In some cases, a member may be eligible for a maximum tax offset (rebate) of $540 where they contribute a spouse contribution to their low income or non-working spouse’s account. Superannuation lump sums transferred from other funds may also be accepted.

Fees charged for spouse accounts are identical as those for RBA members as outlined above.

Further details are included in the Spouse Account booklet available at nabgsf.com.au/publications

InsuranceThe Fund has a strong emphasis on helping to provide adequate insurance cover to NAB employees. This is why the Fund provides standard cover for death and disablement to employee members. The Fund also offers employee members the option to choose a higher level of insurance cover so as to increase your level of financial protection. You may apply for additional death and permanent disablement disability insurance cover in units of $50,000 (up to a maximum 20 units i.e. $1m) and an extra temporary disability (salary continuance) cover.

All members* are provided with standard cover in the National Australia Bank Group Superannuation Fund and you’re covered 24 hours a day, 7 days a week. The cost of providing the standard cover is met by the deduction of premiums from your retirement account which are based on your age and level of cover.

*Not including RBA members, Spouse Account members, members who choose under Choice of Fund legislation to have future contributions directed to another fund, members re-joining this Fund or joining for the first time following a period of contributions directed to another Fund, members who have chosen to opt out of insurance cover or members who have a current restriction applied to their standard cover.

You receive a benefit on:

• death, or

• total & permanent disability (TPD), or

• partial disability, (subject to disability occurring prior to 1st January 2014) and/or

• temporary disability (also known as two year salary continuance).

Under these flexible arrangements you may also select ‘no cover’, which means that you are not covered for any insured benefit for death or disability. If you die or become disabled, only your leaving service benefit will be paid. If you wish to opt out of insurance cover altogether, you must complete an Opting Out of Insurance Cover form.

Before you opt out of insurance cover, we strongly recommend you discuss this decision with your family and/or licensed financial adviser.

Further details regarding death and disablement benefits are available at nabgsf.com.au/publications

Contributions tax and surchargeMost types of concessional contributions made into a regulated superannuation fund are taxed at the rate of 15%. This includes employer contributions (including superannuation guarantee), before-tax member contributions (salary sacrifice) and any untaxed elements rolled over into the Fund.

The Government abolished the superannuation surcharge effective 1 July 2005 and as a result no surcharge is payable in respect of superannuation contributions made on or after 1 July 2005. However, assessments in relation to prior periods continue to be processed by the Australian Taxation Office (ATO) and any surcharge is payable after the Trustee receives an assessment from the ATO.

The surcharge is deducted from your account through the selling of units and reported in your six-monthly Member benefit statement.

Excess contributions taxContribution caps, or limits, apply to the total amount of superannuation contributions that you can make each financial year before additional tax is payable. As members are responsible for monitoring contributions made to all of their superannuation accounts it is important that you understand your contributory commitments and the tax consequences of exceeding the caps.

The ATO is responsible for determining whether you have exceeded the annual caps and will determine whether you have to pay excess contributions tax.

The ATO will issue an excess contributions tax assessment if you have exceeded the caps.

You can choose to withdraw excess contributions from your super account, plus earnings (if any). Any excess concessional contributions and earnings you withdraw will be taxed at your marginal tax rate, plus an interest charge.

Use of derivativesDerivatives are an investment technique used in some investment options.

They are contracts that have a value derived from another source such as an asset market index or interest rate.

There are many types of derivatives including swap options and futures. They are a common tool used to manage risk or improve returns.

Some derivatives allow investment managers to earn large returns from small movements in the underlying asset’s price. However, they can lose large amounts if the price of the underlying asset moves against them.

The investment managers are not permitted to use financial derivatives to leverage the performance of the portfolio beyond that which could be obtained if derivatives were not used. We will obtain and consider a "Part B" Derivative Risk Statement from each of the investment managers who invest NABGSF assets in derivatives.

At no time in the reporting period did our use of the derivative charge ratio exceed 5%.

Fund rule changesThe Fund rules were amended to comply with section 29TC of the Superannuation Industry (Supervision) (SIS) Act 1993 for the purposes of the introduction of NABGSF MySuper on 1st January 2014.

The amendments were approved by the Trustee and NAB’s Board in May 2013.

SIS complianceNo penalty was imposed against us or any director under the Superannuation Industry (Supervision) (SIS) Act 1993 during the reporting period.

Eligible rollover funds (ERFs)ERFs are approved by the Australian Prudential Regulation Authority (APRA). They are designed to hold unclaimed money and generally have more conservative investments than other superannuation funds, which may result in lower returns.

Once 60 days have elapsed after termination date without member response, unpaid benefit amounts are paid:

1. where the benefit payment is $5,000 or more into the Fund’s Retained Benefits Account.

2. where the benefit payment is less than $5,000 into the Australian Eligible Rollover Fund.

The ERF will hold your transferred benefit until you claim it. You will not have any claim against us once your benefit has been transferred to an ERF because your Fund membership will have ceased. Your insurance cover (if any) will cease. The rules of the ERF will govern your benefit once it has been transferred.

Our current ERF is the Australian Eligible Rollover Fund which can be contacted on 1800 677 424 or by writing to:

Australian Eligible Rollover Fund Locked Bag 5429 PARRAMATTA NSW 2124

If your benefit is transferred to an ERF and if we can provide the ERF with your contact details, the ERF will provide you with its current Product Disclosure Statement (PDS). Alternatively, you can contact the ERF for a copy of its PDS.

The ERF will apply a different fee structure than that of the Fund. Specifically, the ERF is required to protect your benefit. This means that, generally, administration charges cannot exceed investment earnings on your account in a reporting period. However, indirect management fees may be deducted from gross fund earnings. You should refer to the ERF’s PDS for circumstances in which fees may apply.

Temporary residentIf you are a former temporary resident, your lump sum benefit is taken to be unclaimed super monies if:

• you held a temporary visa that has ceased to have effect and you have left Australia;

• it has been at least six months since the visa ceased to be in effect and/or you left Australia;

• the Fund has received a Temporary Resident Notification from the ATO instructing the monies be transferred;

• you are neither an Australian citizen nor a New Zealand citizen;

• you are not a permanent resident or currently the holder of a temporary, permanent or prescribed visa; and

• you do not have an undetermined application for a permanent visa.

If you are a former temporary resident who has left Australia and your visa has expired or been cancelled, you can claim your superannuation from the Fund as a Departing Australia Superannuation Payment (DASP). Contact Plum on 1300 55 7586 for further information on how to initiate a DASP.

However, if you do not claim your benefit within six months of becoming eligible to do so, we will pay your benefit to the ATO if we receive a written notice from the ATO directing payment to be made. In this event, you have a right to apply to the Commissioner of Taxation for payment of the DASP.

The Australian Securities and Investments Commission (ASIC) has provided relief to superannuation trustees to the effect that a trustee is not obliged to notify, or give an exit statement to, a former temporary resident where the trustee pays unclaimed superannuation to the ATO in accordance with the applicable legislation requirements. We wish to rely on this relief. Consequently, members who are departed former temporary residents will not be notified in the event of their benefits being transferred to the ATO in these circumstances.

6. How your money is invested

Investment objectivesThe Fund has an investment strategy and spread of assets aimed to accumulate better than market average investment returns to members accounts over the medium to long term.

Investment mixThe Fund offers nine investment options to choose from. Members can choose just one of the options or any combination of those options. Each option has an approved investment strategy with five of the options having a different type and mix of assets and the four remaining options investing in a single sector.

The options are:

• NABGSF MySuper

• High Growth

• Growth

• Balanced

• Capital Stable

• Cash

• Fixed Interest

• Australian Shares

• Overseas Shares

If you do not select an option then your superannuation benefit will be invested in the default option, being the NABGSF MySuper option.

Investment return rateThe investment return rate is applied through the movements in unit prices. Unit prices are applied to Category 1 members’ accounts and some resignation benefits of Category 3 members. This rate is also applied to amounts brought into the Fund from external sources (eg. rollovers).

Unit prices are updated daily and not at year-end.

Diversify to reduce volatility and other risksDiversification is a sound way to reduce short-term volatility. It also helps you manage the risk of not being able to buy or sell assets when you want to. The more you diversify the less impact any one investment can have on your portfolio.

One of the most effective ways of reducing volatility is to diversify across a range of asset classes. Asset classes are groups of similar types of investments. Each class has its risks and benefits, and goes through its own market cycle. A market cycle can take a couple of years or many years; it’s different each time. Investing for the minimum time or longer improves your chances of achieving the return you expect. However, returns can’t be guaranteed. You need to be prepared for all sorts of return outcomes when investing.

Implemented asset consultantWe have appointed JANA Investment Advisers Pty Ltd (ABN 97 006 717 568) (JANA) to be our implemented asset consultant. JANA is responsible for advising the Trustee on our entire investment menu, providing regular insight and updates on the performance of our investment options.

JANAJANA is an Australian Financial Services Licence Holder and is a wholly owned subsidiary of National Australia Bank Limited (NAB). JANA Investment Advisers was established in 1987 with the objective of providing high quality independent advice to institutional clients on all aspects of investments and asset management. The firm has since grown to become one of the leading investment consultants in Australia, with over A$300 billion funds under advice and A$30 billion funds under management at (31st December 2013). JANA’s core business continues to be the provision of investment and asset consulting advice to institutional clients from its offices in Melbourne and Sydney. JANA's Board of Directors comprises four JANA Executives and three from National Wealth Management, a division of NAB.

JANA’s investment philosophy drives their capital markets and manager research programme. The key elements of that philosophy can be summarised as follows:

• JANA believes it is possible to reduce risk and outperform over the long term by taking advantage of occasional large divergences from fair value in investment markets.

• Through diligent hands-on research, their track record demonstrates that is possible to select managers capable of outperforming over the long term. While above-average ability in security selection is a prerequisite in most asset classes, managers must also exhibit a disciplined process and style and this should be reflected in the qualities and mindset of its personnel.

• To be of real value, research needs to be implemented with full commitment and not sit on the fence.

Frequent switchingYou should not invest in the Fund if you intend to switch your investments frequently in the pursuit of short-term gains.

We monitor all investment options for abnormal activity because this sort of activity can have adverse impacts for other members.

To maintain equity, the Trustee has the right to deal with members who frequently switch by:

• delaying, limiting or rejecting their future switch requests;

• cancelling membership; or

• transferring their account balance to the Australian Eligible Rollover Fund.

Investment managersThe majority of the Fund's assets are invested in the MLC investment platform via a Life Insurance policy issued by MLC Limited, however some assets are invested directly with individual investment managers, those being:

Investment managers as at 30 June 2014

AMP Capital Investors Limited

LGT Capital – Crown Global Secondaries

GPT Group

Etihad Stadium Trust

Lend Lease Real Estate Investments Limited

Macquarie Goodman Funds Management Ltd

MLC Limited

Standard risk measureWe use the Standard Risk Measure (SRM) to help you compare the investment risk across the investment options we offer. The SRM is the estimated number of negative annual returns in any 20 year period. Because it is an estimate, the actual number of negative returns may be different. The SRM is based on industry guidelines, however it isn’t a complete assessment of investment risk. For example is doesn’t:

• capture the size of a possible negative return or the potential for sufficient positive returns to meet your objectives, and

• take into account the impact of fees and tax. These can increase the chance of a negative return.

For more information on how we calculate the Standard Risk Measure please go to nabgsf.com.au

Risk band Risk labelEstimated number of negative returns

in any 20 year period

1 Very low Less than 0.5

2 Low 0.5 to less than 1

3 Low to medium 1 to less than 2

4 Medium 2 to less than 3

5 Medium to high 3 to less than 4

6 High 4 to less than 6

7 Very high 6 or greater

Fund reservesThe Fund manages an operational reserve and allocates its assets in the Growth option. The reserves include defined benefit reserves, death and disability reserves, an Operational Risk Reserve and any other reserve determined by the Actuary.

The reserves are monitored by the Fund’s Actuary who undertakes a formal investigation and provides a report to the Trustee every three years.

UnitisationUnitisation is the pricing method used to credit investment returns to superannuation benefits. Unitisation was introduced to allow for the accurate and timely tracking of returns for each option. Fund earnings are allocated to member accounts through movements in the respective unit prices. The Fund values the units daily with the unit price of each option varying with the value of the underlying assets in each option. Additional units are allocated when contributions are made and when funds are rolled into members’ accounts. Unit prices are quoted to four decimal places and members are able to monitor the change in unit prices at nabgsf.com.au

Your benefit in the Fund is quoted in terms of units held and these multiplied by the applicable unit price(s), will give you your superannuation benefit.

Investment optionsSet out following are details of each of the investment options offered by the Fund, including performance at financial year end.

7. Investment option profiles

Information current as at 30 June 2014

Investment option

**NABGSF MySuper High Growth option Growth option

Investment strategy

Invest primarily in growth assets such as equities and property with some exposure to alternative assets and defensive assets such as fixed interest and cash.

Invest primarily in growth assets such as equities and property with some exposure to alternative assets.

Invest primarily in growth assets such as equities and property with some exposure to alternative assets and defensive assets such as fixed interest and cash.

Investment objective

To earn 3% above CPI over rolling 10 year periods. The suggested minimum timeframe is 5 years.

To earn 4% above the CPI over rolling 5 year periods. The suggested minimum investment timeframe is 5 years.

To earn 3% above CPI over rolling 3-5 year periods. The suggested minimum investment timeframe is 5 years.

Net investment return*

Year ended

2014 (30 June) 2.89% 2014 (30 June) 16.69%

2013 (26 June) 18.07%

2012 (27 June) -1.04%

2011 (29 June) 6.61%

2010 (30 June) 11.67%

2014 (30 June) 13.95%

2013 (26 June) 13.58%

2012 (27 June) 1.26%

2011 (29 June) 6.54%

2010 (30 June) 9.71%

Compound return (p.a.)

Since inception (6 months) 2.89%

3yr 10.89%

5yr 10.17%

10yr 7.80%

Since inception (15 year) 7.89%

3yr 9.43%

5yr 8.90%

10yr 6.99%

Since inception (15 year) 7.23%

Estimated number of negative annual returns in 20 years

Approximately 4 years in 20 Approximately 5 years in 20 Approximately 4 years in 20

Risk label1 High High High

*The net investment return reflects the earnings of the option after allowing for taxes and investment expenses.

** This option commenced on 1st January 2014 and as such the 2014 return is the 6 month return for the period ending 30 June 2014

1. For more information about this risk, please refer to the Standard risk measure section.

Information current as at 30 June 2014

Investment option

Balanced option Capital Stable option Cash option

Investment strategy

Invest approximately half in growth assets such as equities and property with the remainder in defensive assets such as fixed interest and cash, with some exposure to alternative assets.

Invest primarily in defensive assets such as fixed interest and cash with some exposure to growth assets such as equities and property.

Invest in cash, cash equivalents and short term debt instruments.

Investment objective

To earn 2.5% above CPI over rolling 3 year periods. The suggested minimum investment timeframe is 3 years.

To earn 1.5% above CPI over rolling 5 year periods, and to limit the chance of making a loss in any one year by investing a greater proportion in historically lower risk assets.

To earn an investment return equal to the UBS Australian Bank Bill Index, which is one of the benchmarks used in financial markets to measure the performance of cash-type investments. There is no recommended minimum investment timeframe.

Net investment return*

Year ended

2014 (30 June) 10.15%

2013 (26 June) 10.95%

2012 (27 June) 3.44%

2011 (29 June) 7.24%

2010 (30 June) 9.84%

2014 (30 June) 7.82%

2013 (26 June) 8.15%

2012 (27 June) 4.69%

2011 (29 June) 7.11%

2010 (30 June) 8.56%

2014 (30 June) 2.80%

2013 (26 June) 3.44%

2012 (27 June) 4.15%

2011 (29 June) 4.48%

2010 (30 June) 3.87%

Compound return (p.a.)

3yr 8.13%

5yr 8.29%

10yr 6.86%

Since inception (15 year) 7.03%

3yr 6.88%

5yr 7.26%

10yr 6.23%

Since inception (15 year) 6.39%

3yr 3.46%

5yr 3.75%

10yr 4.89%

Since inception (15 year) 4.97%

Estimated number of negative annual returns in 20 years

Approximately 3 years in 20 Approximately 1 years in 20 Not expected

Risk label1 High Medium Very low

*The net investment return reflects the earnings of the option after allowing for taxes and investment expenses.

1. For more information about this risk, please refer to the Standard risk measure section.

Information current as at 30 June 2014

Investment option

Fixed Interest option Australian Shares option Overseas Shares option

Investment strategy

Invest solely in fixed interest securities.

Invest solely in Australian based equities.

Invest solely in overseas based equities.

Investment objective

To earn investment returns of 1% (after fees) above the cash rate per annum over rolling 3 year periods. The suggested minimum investment timeframe is 3 years.

To outperform the S&P ASX 300 Index over rolling 3 year periods. The suggested minimum investment timeframe is 5 years.

To outperform the MSCI All Country World Index (in Australian dollar) over rolling 3 year periods. The suggested minimum investment timeframe is 5 years.

Net investment return*

Year ended

2014 (30 June) 5.30%

2013 (26 June) 4.99%

2012 (27 June) 8.22%

2011 (29 June) 8.17%

2010 (30 June) 10.54%

2014 (30 June) 18.33%

2013 (26 June) 20.03%

2012 (27 June) -5.13%

2011 (29 June) 8.05%

2010 (30 June) 17.21%

2014 (30 June) 19.85%

2013 (26 June) 20.52%

2012 (27 June) -1.00%

2011 (29 June) 3.34%

2010 (30 June) 10.62%

Compound return (p.a.)

3yr 6.16%

5yr 7.42%

10yr 5.52%

Since inception (10+ year) 5.50%

3yr 10.45%

5yr 11.28%

10yr 8.91%

Since inception (10+ year) 8.87%

3yr 12.66%

5yr 10.33%

10yr 4.75%

Since inception (10+ year) 4.73%

Estimated number of negative annual returns in 20 years

Approximately 2 years in 20 Approximately 6 years in 20 Approximately 6 years in 20

Risk label1 Medium to high Very high Very high

*The net investment return reflects the earnings of the option after allowing for taxes and investment expenses.

1. For more information about this risk, please refer to the Standard risk measure section.

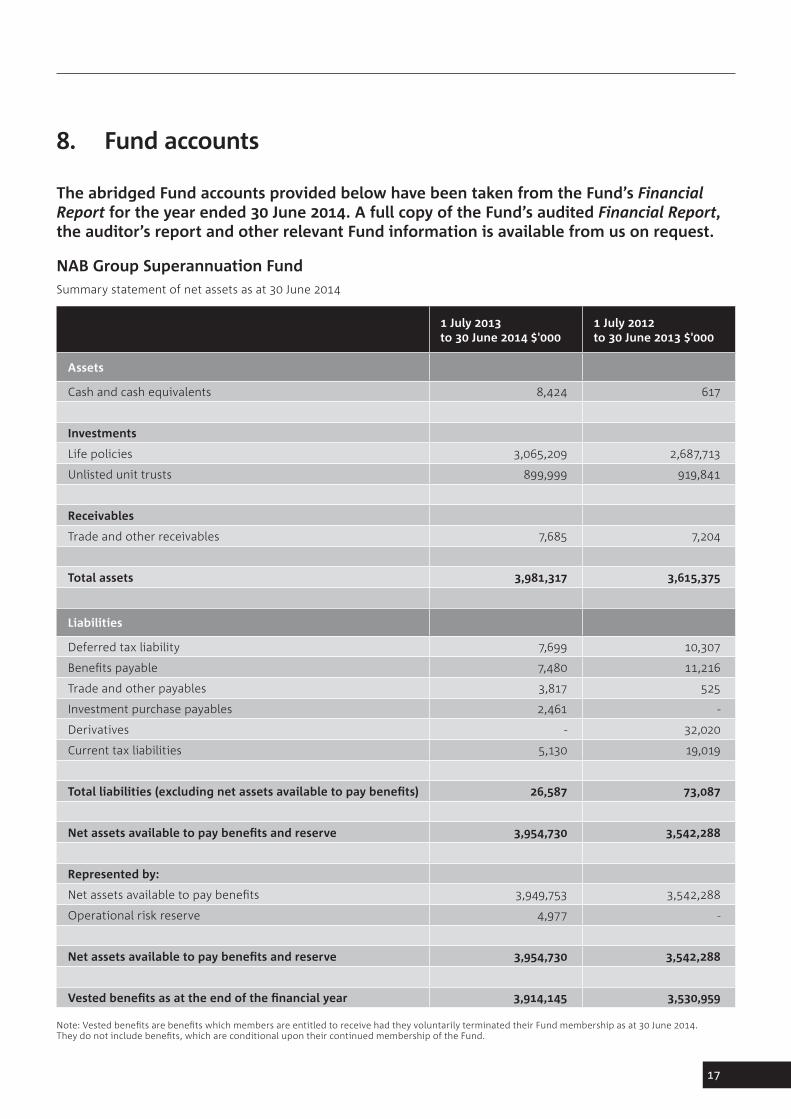

8. Fund accounts

The abridged Fund accounts provided below have been taken from the Fund’s Financial Report for the year ended 30 June 2014. A full copy of the Fund’s audited Financial Report, the auditor’s report and other relevant Fund information is available from us on request.

NAB Group Superannuation FundSummary statement of net assets as at 30 June 2014

1 July 2013 to 30 June 2014 $'000

1 July 2012 to 30 June 2013 $'000

Assets

Cash and cash equivalents 8,424 617

Investments

Life policies 3,065,209 2,687,713

Unlisted unit trusts 899,999 919,841

Receivables

Trade and other receivables 7,685 7,204

Total assets 3,981,317 3,615,375

Liabilities

Deferred tax liability 7,699 10,307

Benefits payable 7,480 11,216

Trade and other payables 3,817 525

Investment purchase payables 2,461 -

Derivatives - 32,020

Current tax liabilities 5,130 19,019

Total liabilities (excluding net assets available to pay benefits) 26,587 73,087

Net assets available to pay benefits and reserve 3,954,730 3,542,288

Represented by:

Net assets available to pay benefits 3,949,753 3,542,288

Operational risk reserve 4,977 -

Net assets available to pay benefits and reserve 3,954,730 3,542,288

Vested benefits as at the end of the financial year 3,914,145 3,530,959

Note: Vested benefits are benefits which members are entitled to receive had they voluntarily terminated their Fund membership as at 30 June 2014. They do not include benefits, which are conditional upon their continued membership of the Fund.

Summary statement of movements in net assets for the year ended 30 June 2014.

1 July 2013 to 30 June 2014 (000’s)

1 July 2012 to 30 June 2013 (000’s)

Investment income

Interest 343 3,415

Dividend and distribution income 30,041 51,289

Other investment income 544 4,176

Changes in the net market values of investments 450,682 386,188

Net investment revenue 481,610 445,068

Contribution revenue

Employer contributions 248,650 249,672

Members' contributions 13,924 12,707

Government co-contributions 205 46

Transfers from other funds 57,779 54,036

Total contribution revenue 320,558 316,461

Other income

Group life insurance proceeds 10,283 9,535

Other revenue 182 3,772

Total other income 10,465 13,307

Total revenue 812,633 774,836

Less

Benefits paid 353,931 322,589

Expenses

Administration fees 4,534 -

Group life insurance premiums 13,224 10,976

Other general administration expenses 3,118 4,013

Superannuation contributions surcharge 24 5

Direct investment expenses 7 1,568

Custody expenses 760 778

Other trustee fees 58 14

Total expenses 21,725 17,354

Change in net assets before income tax 436,977 434,893

Income tax expense 24,535 58,957

Change in net assets after income tax 412,442 375,936

Net assets available to pay benefits and reserve at the beginning of the year

3,542,288 3,166,352

Net assets available to pay benefits and reserve at the end of the year

3,954,730 3,542,288

Fund assets shown according to the category of investment groups are:

1 July 2013 to 30 June 2014 (000’s)

1 July 2012 to 30 June 2013 (000’s)

Commonwealth, State or Territory securities or securities of a public authority thereof

- -

Securities issued by the government of a foreign country or by a public authority thereof

- -

Other fixed interest securities - -

Fixed interest held through unit trusts/life policy 289,080 327,488

Property held through unit trusts/life policy 466,103 248,386

Private equity through unit trusts/life policy 20,595 33,686

Australian shares traded on a securities exchange - -

Australian shares held through unit trusts/life policy 1,215,139 1,062,028

Foreign country shares traded on a securities exchange - -

Foreign country shares held through unit trusts/life policy 1,165,297 1,043,099

Cash or interest bearing deposit 417,270 298,494

Alternative investments held through unit trusts/life policy 391,298 586,755

Deferred tax assets - -

Other assets 426 15,439

3,965,208 3,615,375

9. How to contact Plum

Call Plum on 1300 55 7586 between 8am and 7pm AEST (8pm daylight savings time), Monday to Friday if you have any queries or concerns about your superannuation.

More informationIf you would like more information or documents such as a PDS, Annual Report or Actuarial Report or any other information about the Fund, please contact Plum on 1300 55 7586 or visit nabgsf.com.au

You can also write to Plum at:

Plum Financial Services Limited GPO Box 63 Melbourne VIC 3001

Prefer an email alert?Would you prefer to receive an email alert when your Member benefit statement is available to download from the website?

• simply log on to nabgsf.com.au

• select Receive my bi-annual statements online.

or

Phone Plum on 1300 55 7586 between 8am and 7pm AEST (8pm daylight savings time), Monday to Friday.

This page has been left blank intentionally.

This page has been left blank intentionally.

This page has been left blank intentionally.

Important information

An interest in the National Australia Bank Group Superannuation Fund A ABN 59 929 570 050 (Fund) is issued by National Australia Bank Superannuation Fund Pty Ltd ABN 99 065 048 928 AFSL 24 1720 (Trustee). The Fund Administrator is Plum Financial Services Limited ABN 35 081 812 731 AFSL 243356 (Administrator). This material has been prepared by the Administrator and it contains information that is general in nature. The information does not take into account your objectives, financial situation or needs. Before acting on the information you should consider whether it is appropriate having regard to your personal circumstances and seek professional advice. The Administrator recommends that you consider the Fund’s Product Disclosure Statement (PDS) before you make any decisions about your superannuation. To obtain a copy of the Fund’s PDS, please contact Plum on 1300 55 7586.

Neither the Administrator, the Trustee, nor any other company in the National Australia Group of companies accepts liability whatsoever for any decision that is made on the basis of or in reliance of the information contained in this material. Please note that the information contained in this material is current at 07 October 2014. Any changes in law or policy subsequent to this date have not been incorporated.

©2014 National Australia Bank Limited ABN 12 004 044 937 AFSL and Australian Credit Licence 230686 A110801-0814

![Australian EXP TRIATE...Australian Expatriate Superannuation Fund Investment Guide 3Disclaimer This Investment Guide was prepared by Tidswell Financial Services Ltd [Trustee/Tidswell],](https://img.pdfslide.us/doc/110x75/5fef1a9ccf89674f960337b0/australian-exp-triate-australian-expatriate-superannuation-fund-investment-guide.jpg)