Embed Size (px)

Citation preview

2014

ANNUAL REPORT

PRESS RELEASE DATED MARCH 5, 2015

OVERVIEW OF JACQUET METAL SERVICE GROUP 2

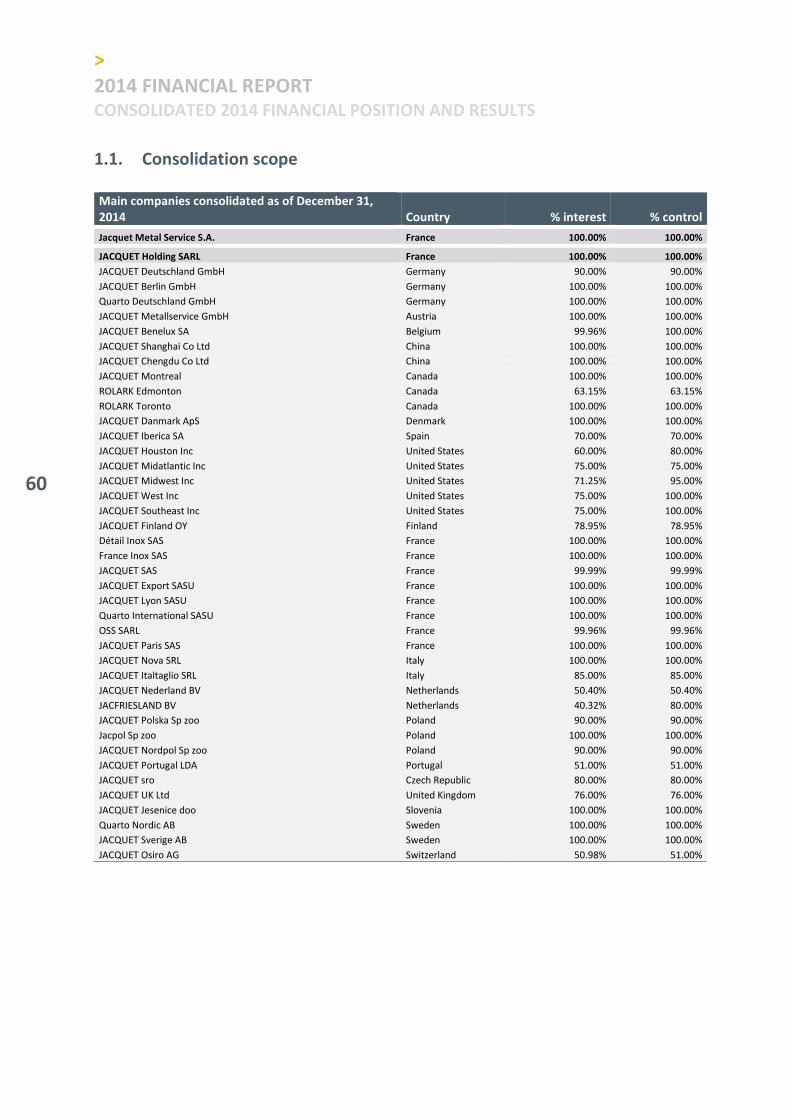

2014 FINANCIAL REPORT 20 1.

2.

3.

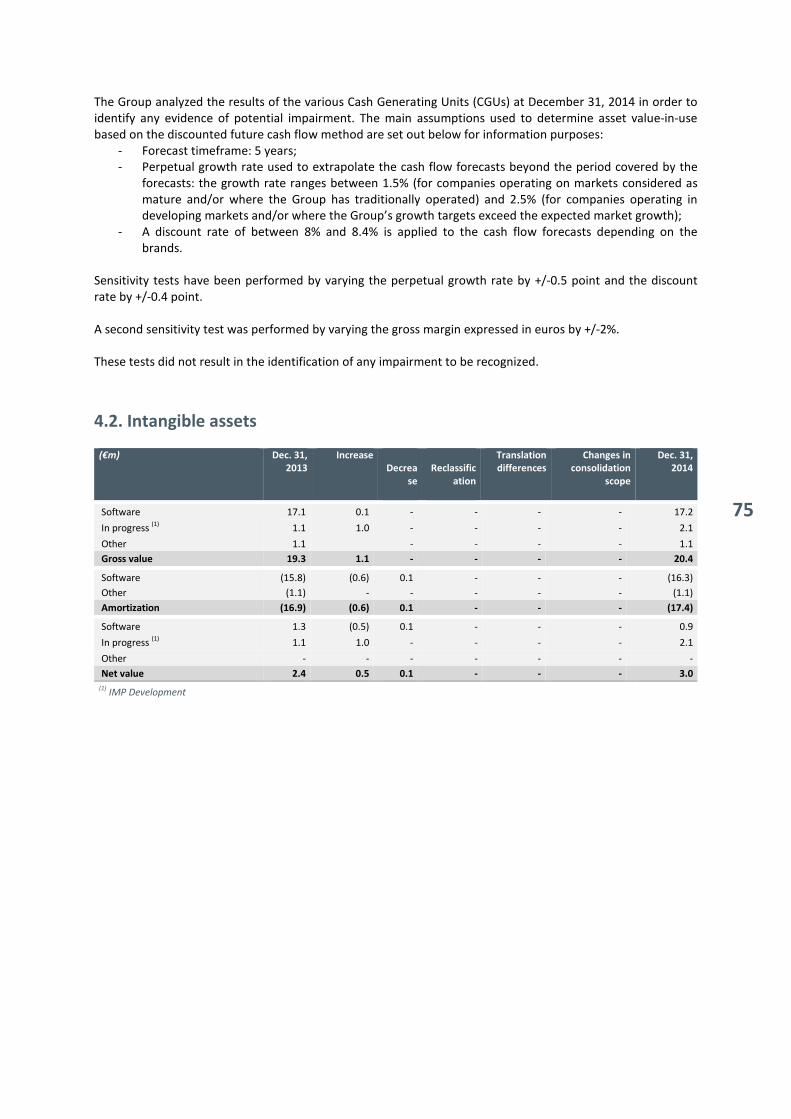

4.

5.

6.

7.

8.

9.

Management report - Information on the Group

Management report - Information on the parent company Jacquet Metal Service S.A.

Consolidated financial position and earnings for 2014

Statutory auditors’ report on consolidated results

2014 Financial Statements - Jacquet Metal Service S.A.

Statutory auditors’ report on the financial statements

Statutory auditors’ special report on regulated agreements and commitments

Chairman’s report concerning the preparation and organization of the Board of Directors’ work

and internal control procedure

Statutory auditors’ report on the report prepared by the Chairman of the Board of Directors

20

35

54

97

99

117

119

123

136

OTHER INFORMATION 138 1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

11.

12.

Person responsible for the annual report and the annual financial report

Auditors

Person responsible for the financial report information and investor relationships

Information on the share issuer

Information on the share capital

Related-party transactions

Information concerning the company, society and the environment

Independent verifier’s report on consolidated social, environmental and societal information

presented in the management report

Group infrastructures

Annual disclosure document

Cross-reference table of the annual report 2014

Cross-reference table of the financial report 2014

138

139

139

140

144

146

147

150

153

154

156

159

This is a free translation into English of Jacquet Metal Service group’s annual report for 2014, which is

issued in the French language, and is provided solely for the convenience of English speaking readers.

2014 ANNUAL RESULTS – PRESS RELEASE DATED MARCH 5, 2015

2014 annual results

• Sales €1,126 million (+8.5% from 2013)

• EBITDA + €58.1 million (5.2% of sales)

• Net income, Group share + €25.2 million

The Board of Directors’ meeting on March 4, 2015, which was chaired by Eric Jacquet, approved the consolidated financial statements for the year ended December 31, 2014.

€m Q4 2014 Q4 2013 2014 2013

Sales 269.3 244.8 1,126.0 1,037.6

Gross margin 71.3 61.5 283.5 242.6

% of sales 26.5% 25.1% 25.2% 23.4%

EBITDA 11.6 6.9 58.1 30.1

% of sales 4.3% 2.8% 5.2% 2.9%

Operating income 10.5 4.4 45.2 18.4

% of sales 3.9% 1.8%

4.0% 1.8%

Net income (Group share) 7.1 0.8 25.2 3.8

2014 sales and earnings

The Group generated sales of €1.13 billion, up 8.5% from 2013, including a price effect of -2.2% and a +10.7% increase in volumes (of which 3.7 percentage points were due to scope effect). The increase in volumes was boosted by the Group’s sustained investment.

The gross margin rate rose 1.8 percentage points to 25.2% of sales, while the gross margin itself amounted to €283.5 million.

Operating expenses excluding scope effect were kept under tight control with a 2.3% increase from 2013 primarily due to the increase in activity and results.

Against this backdrop, EBITDA rose by +93% to €58.1 million (5.2% of sales), while operating income amounted to €45.2 million (4% of sales).

All the brands made a positive contribution to the increase in the Group's revenues as well as to the improvements in the gross margin and EBITDA.

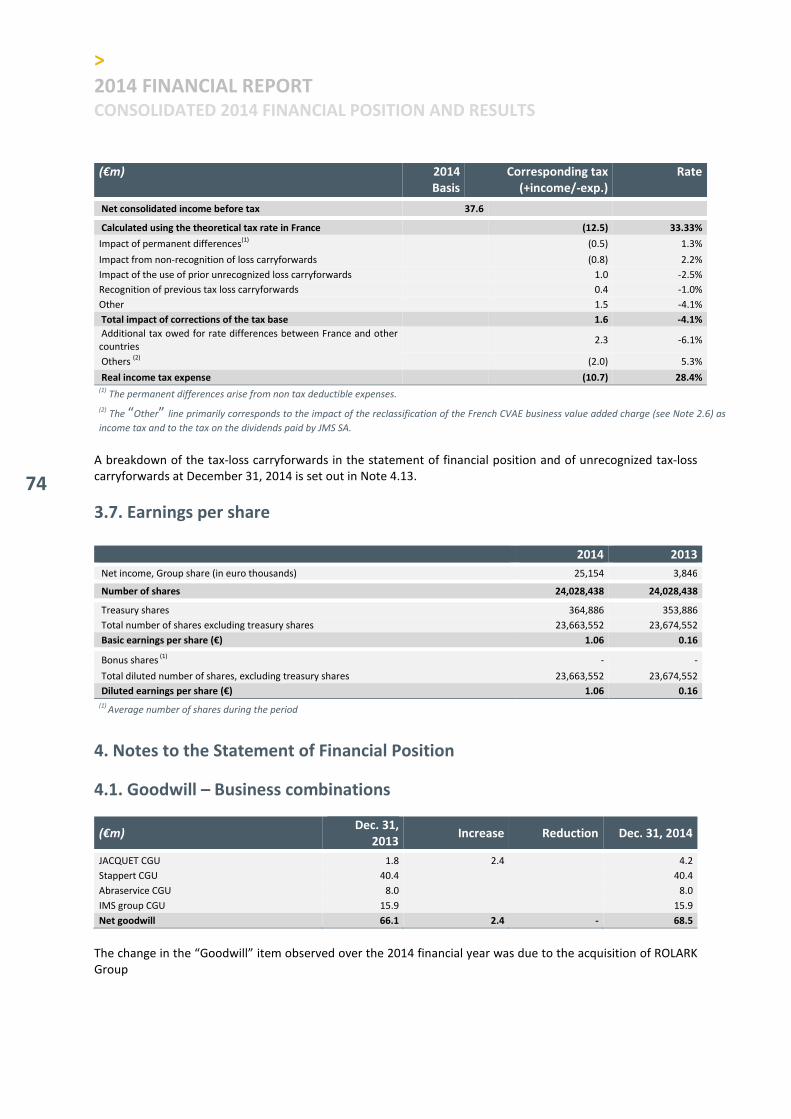

Net income (Group share) amounted to €25.2 million (i.e. €1.05 per share) compared with €3.8 million in 2013.

Early 2015 demand remains favorably oriented while market prices remain low.

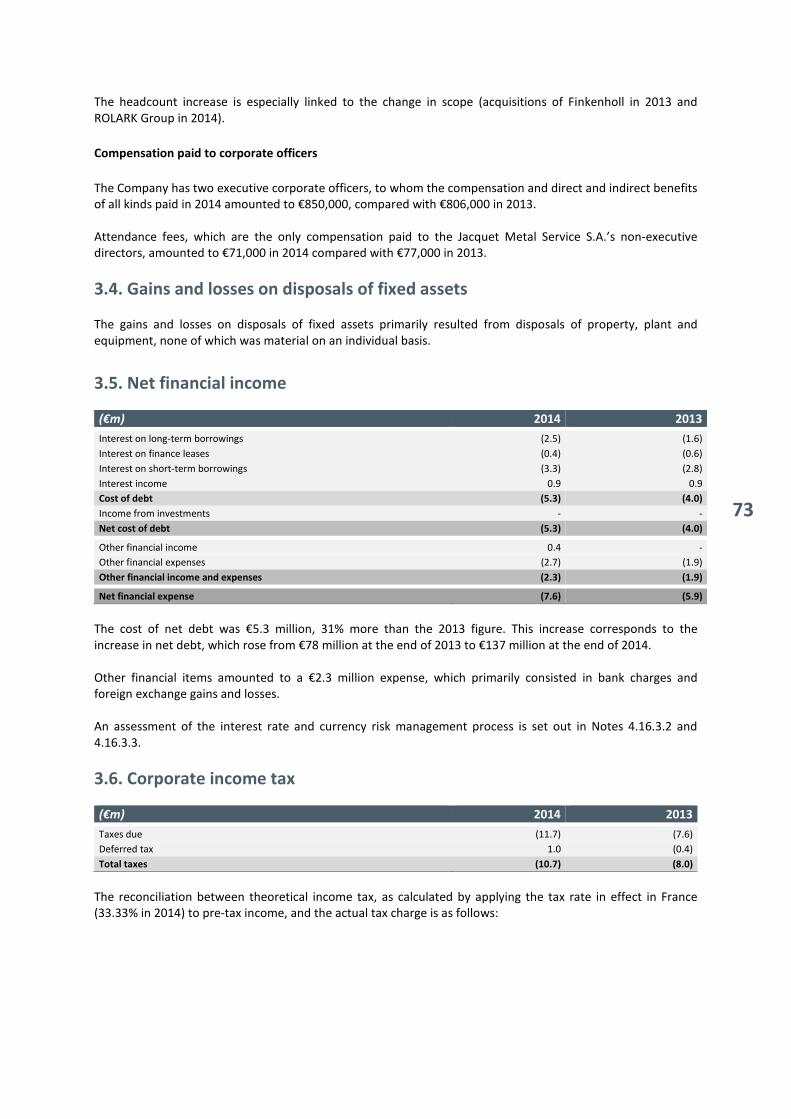

Financial position

Group’s net debt at the end of 2014 amounted to €137.3 million compared with shareholder’s equity of €261.7 million, resulting in a net debt ratio (gearing) of 52.5%.

The Group’s cash flow amounted to €52.7 million in 2014, compared with €25.1 million in 2013.

Inventory increased by €50 million due to the rise in activity and to the projects implemented in 2014. Accordingly, operating working capital amounted to 25% of sales at the end of 2014.

Capital expenditure for the financial year amounted to €14.2 million (primarily related to new finishing capacity) following €14.9 million in 2013.

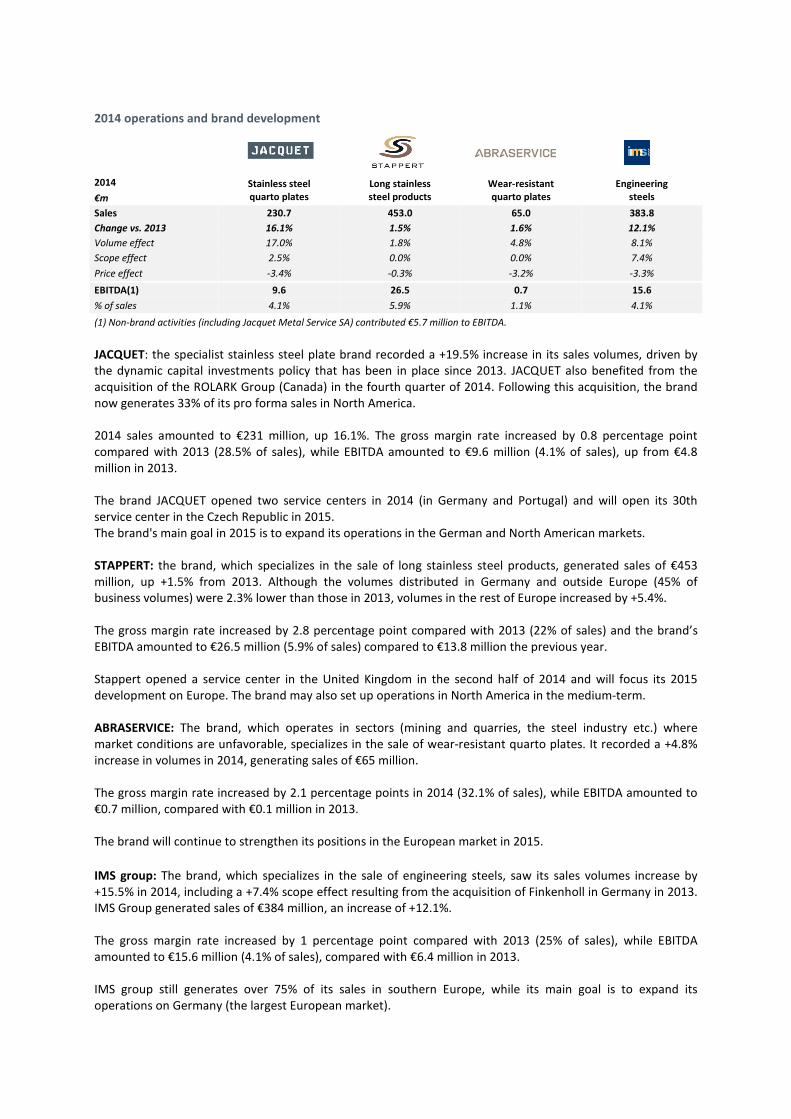

2014 operations and brand development

2014 Stainless steel

quarto plates

Long stainless

steel products

Wear-resistant

quarto plates

Engineering

steels €m

Sales 230.7 453.0 65.0 383.8

Change vs. 2013 16.1% 1.5% 1.6% 12.1%

Volume effect 17.0% 1.8% 4.8% 8.1%

Scope effect 2.5% 0.0% 0.0% 7.4%

Price effect -3.4% -0.3% -3.2% -3.3%

EBITDA(1) 9.6 26.5 0.7 15.6

% of sales 4.1% 5.9% 1.1% 4.1%

(1) Non-brand activities (including Jacquet Metal Service SA) contributed €5.7 million to EBITDA.

JACQUET: the specialist stainless steel plate brand recorded a +19.5% increase in its sales volumes, driven by the dynamic capital investments policy that has been in place since 2013. JACQUET also benefited from the acquisition of the ROLARK Group (Canada) in the fourth quarter of 2014. Following this acquisition, the brand now generates 33% of its pro forma sales in North America. 2014 sales amounted to €231 million, up 16.1%. The gross margin rate increased by 0.8 percentage point compared with 2013 (28.5% of sales), while EBITDA amounted to €9.6 million (4.1% of sales), up from €4.8 million in 2013. The brand JACQUET opened two service centers in 2014 (in Germany and Portugal) and will open its 30th service center in the Czech Republic in 2015. The brand's main goal in 2015 is to expand its operations in the German and North American markets.

STAPPERT: the brand, which specializes in the sale of long stainless steel products, generated sales of €453 million, up +1.5% from 2013. Although the volumes distributed in Germany and outside Europe (45% of business volumes) were 2.3% lower than those in 2013, volumes in the rest of Europe increased by +5.4%. The gross margin rate increased by 2.8 percentage point compared with 2013 (22% of sales) and the brand’s EBITDA amounted to €26.5 million (5.9% of sales) compared to €13.8 million the previous year. Stappert opened a service center in the United Kingdom in the second half of 2014 and will focus its 2015 development on Europe. The brand may also set up operations in North America in the medium-term. ABRASERVICE: The brand, which operates in sectors (mining and quarries, the steel industry etc.) where market conditions are unfavorable, specializes in the sale of wear-resistant quarto plates. It recorded a +4.8% increase in volumes in 2014, generating sales of €65 million. The gross margin rate increased by 2.1 percentage points in 2014 (32.1% of sales), while EBITDA amounted to €0.7 million, compared with €0.1 million in 2013. The brand will continue to strengthen its positions in the European market in 2015.

IMS group: The brand, which specializes in the sale of engineering steels, saw its sales volumes increase by +15.5% in 2014, including a +7.4% scope effect resulting from the acquisition of Finkenholl in Germany in 2013. IMS Group generated sales of €384 million, an increase of +12.1%. The gross margin rate increased by 1 percentage point compared with 2013 (25% of sales), while EBITDA amounted to €15.6 million (4.1% of sales), compared with €6.4 million in 2013. IMS group still generates over 75% of its sales in southern Europe, while its main goal is to expand its operations on Germany (the largest European market).

2

THE GROUP

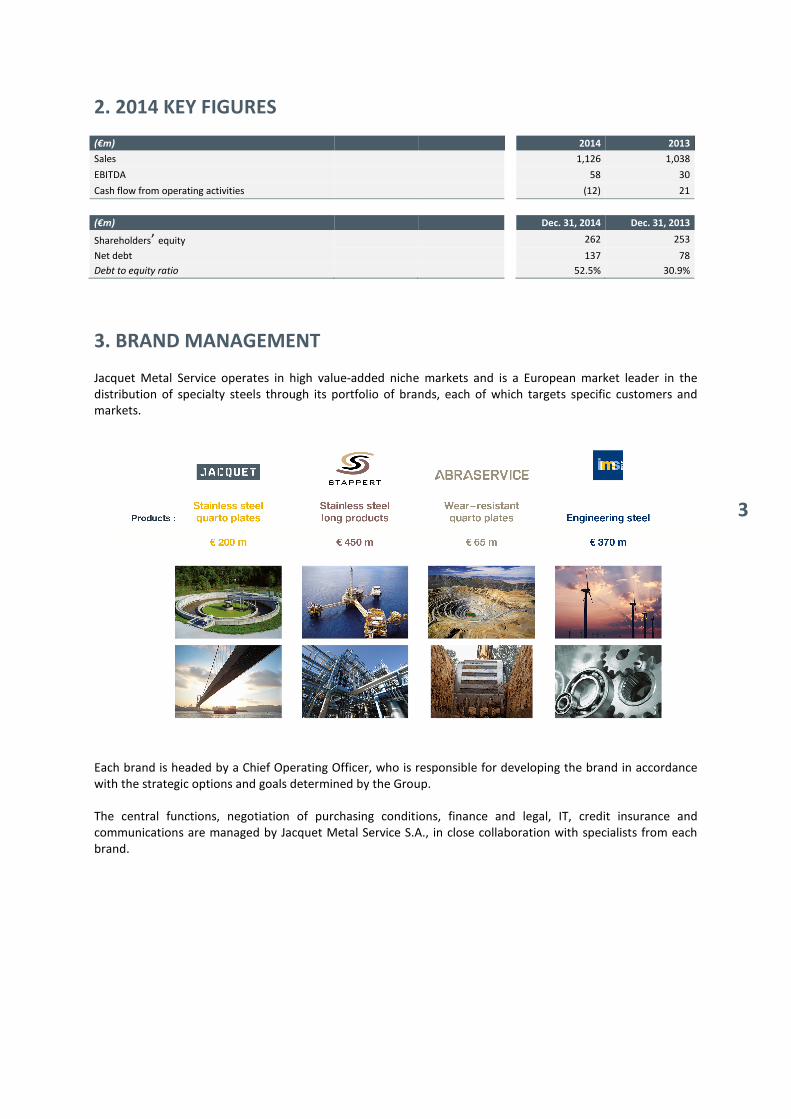

1. A LEADING DISTRIBUTOR OF SPECIALTY STEELS

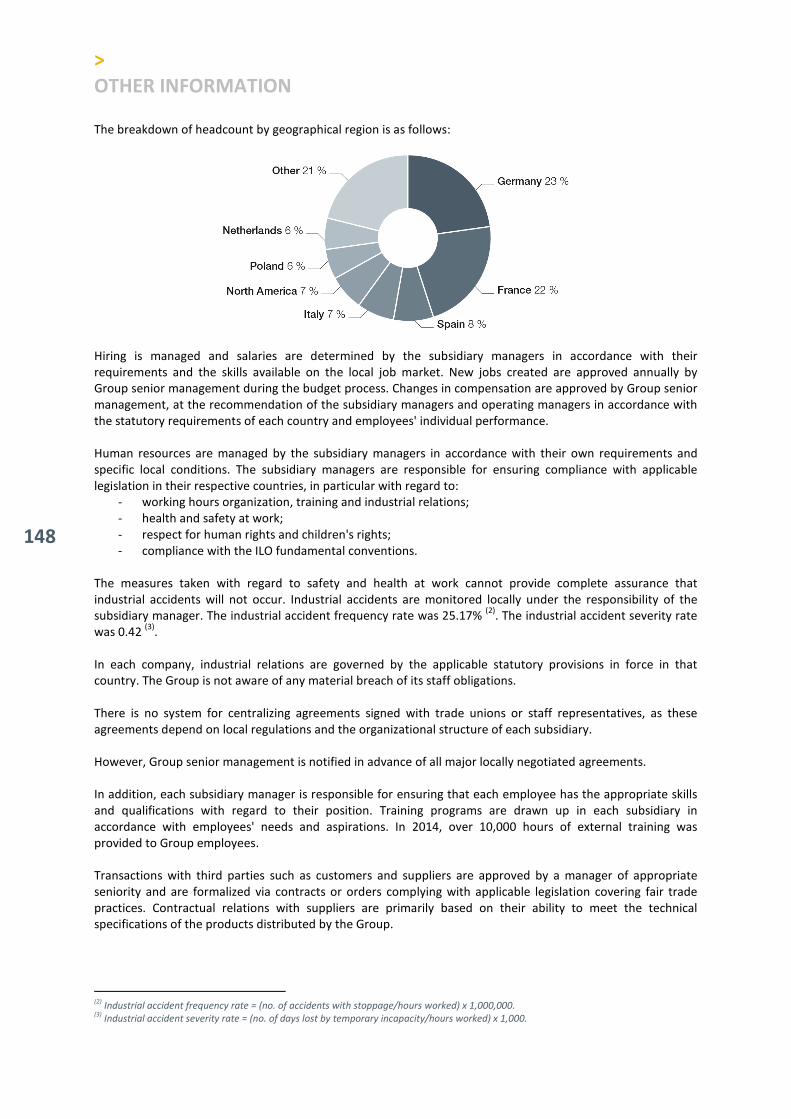

Employees 2,413

Distribution centers 86

Countries 23

A global player Breakdown of sales 2014

Jacquet Metal Service is a European market leader in the distribution of specialty steels and also operates in China and North America. The Group manages and develops a portfolio of brands: JACQUET (stainless steel quarto plates), Stappert (long stainless steel products), Abraservice (wear-resistant quarto plates) and IMS group (engineering steels).

3

2. 2014 KEY FIGURES

(€m) 2014 2013

Sales 1,126 1,038

EBITDA 58 30

Cash flow from operating activities (12) 21

(€m) Dec. 31, 2014 Dec. 31, 2013

Shareholders’ equity 262 253

Net debt 137 78

Debt to equity ratio 52.5% 30.9%

3. BRAND MANAGEMENT Jacquet Metal Service operates in high value-added niche markets and is a European market leader in the distribution of specialty steels through its portfolio of brands, each of which targets specific customers and markets.

Each brand is headed by a Chief Operating Officer, who is responsible for developing the brand in accordance with the strategic options and goals determined by the Group. The central functions, negotiation of purchasing conditions, finance and legal, IT, credit insurance and communications are managed by Jacquet Metal Service S.A., in close collaboration with specialists from each brand.

>

OVERVIEW OF GROUP

4

4. GOVERNANCE

4.1. The Board of Directors As of June 30, 2010 the Company adopted a governance model based on a Board of Directors. The General Meeting of June 26, 2014 appointed the following individuals as directors for a two-year term of office expiring at the end of the General Meeting called to approve the financial statements for the financial year ended December 31, 2015:

- Eric Jacquet, a French national, 56, who has been the Chairman and Chief Executive Officer of Jacquet Metal Service since July 20, 2010. He was previously Chairman and Chief Executive Officer of Jacquet Metals (formerly Jacquet Industries) from that company’s foundation in 1994. Eric Jacquet also held the positions of Vice-Chairman of the Supervisory Board and member of the Strategy Committee of IMS International Metal Service from June 16, 2009 to February 3, 2010. Eric Jacquet has spent his entire career at the Jacquet Metal Service Group, where he held positions including Sales Manager (1980-1985), and Marketing and Export Development Manager (1986-1993). Eric Jacquet is also a member of the Lyon Commercial Court Association of Judges and Former Judges. He was first appointed to the Board of Directors on June 30, 2010.

- Françoise Papapietro (who is considered as an independent director), a French national, 50, spent

most of her career in investment banking (Paribas and Barclays), where she gained expertise in financial transactions (M&A, equity capital transactions and tax engineering). She has also held positions as Head of Institutional and Financial Communications for Infogrames, Chief Executive Officer of Henri Germain and Chief Executive Officer of Loze Partners & Vostok. Françoise Papapietro is an auditor at the French Institute of Advanced National Defense Studies and a Senior Advisor at Leyders Associates. She was first appointed to the Board of Directors on June 29, 2012.

- Gwendoline Arnaud (who is considered as an independent director), a French national, 42, has been a lawyer since 1998. In 2003 she set up her firm specializing in property and business law. Gwendoline Arnaud holds a Master’s Degree in Private Law and a Certificate of Legal Proficiency (CAPA). She was first appointed to the Board of Directors on June 26, 2014.

- Jean Jacquet (who is considered as an independent director), a French national, 82, held the positions

of Chairman of Faïence et Cristal de France until 2012, Chairman and Chief Executive Officer of SOMERGIE (the Metz urban public-private waste management company) until 2011 and Chairman and Chief Executive Officer of TCRM (Metz area public transport system) until 2010. Jean Jacquet represented JSA as a member of the Supervisory Board and member of the Appointment and Compensation Committee of IMS International Metal Service from June 16, 2009 to February 3, 2010. Jean Jacquet began his career at the Renault Group, where he worked until 1984. He was then Chairman and Chief Executive Officer of Unimetal-Ascometal, from 1984 to 1988, and Chairman of the Special Steel Dealers Union (UNAS) from 1988 to 1999. He has also held positions as Chairman of the Supervisory Board of Winwise, Director of the Metz National Engineering School, Chairman of the Inter-Ministerial Development Mission for the development of the Longwy European Hub, Chairman of the Board of Directors of the Metz power plant, Deputy Vice-Chairman of the French National Association of Electricity Concessions and Vice-Chairman of the Metz urban district (now the Metz metropolitan urban district grouping). We would remind you that Jean Jacquet is no relation to Eric Jacquet.

5

Jean Jacquet holds a Law Degree and is a graduate of the Paris Institute of Political Studies. He was first appointed to the Board of Directors on June 30, 2010.

- Henri-Jacques Nougein (who is considered as an independent director), a French national, 67, is an arbitration expert, mediator, amicable liquidation expert and insurance broker (specializing in corporate risk and liability). He is also the Honorary President of the Lyon Commercial Court, former Chairman of the Inter-Professional Mediation and Arbitration Center and Joint Manager of the European Arbitration and Mediation Network. He is the founder and Joint Manager of the Franco-Argentinian Mediation and Arbitration Center, the Franco-Chinese Mediation Center (in partnership with the Shanghai government authorities), and the Franco-Indian Mediation and Arbitration Center (in partnership with the Indian Federation of Chambers of Commerce and Industry). Henri-Jacques Nougein is also a lecturer at Lyon III University (Economic Procedural Law) and is the author of legal and technical research publications. He holds a degree in Private Law and is a graduate of the Lyon Legal Studies Institute, a graduate of the Advanced School of Private Law and a Government Doctor in Law (1976). He was first appointed to the Board of Directors on June 30, 2010.

- Xavier Gailly (who is considered to be an independent director), a Belgian national, 67, spent virtually

his entire career at Fabrique de Fer de Charleroi, which subsequently became Industeel Belgium, a subsidiary of the Arcelor Mittal Group. He held a number of positions in a wide variety of fields (maintenance, capital expenditure, purchasing, production, human resources, etc.), before becoming the company’s Chief Industrial Officer, Executive Director and finally Chief Executive Officer. He was then appointed as Sales Director for Industeel, Arcelor Mittal’s specialty flat steels division. Xavier has been a director or the Chairman of several Arcelor Mittal subsidiaries in Belgium and abroad. He has also held the offices of Director of the Mons Polytechnic Faculty, Director of IGRETEC (inter-district association for the management and performance of technical and economic research, which include 68 towns and cities in the province of Hainaut in Belgium), Vice-Chairman of the Belgian Steel Industry Consortium and Chairman of its French-speaking division. Xavier Gailly is the Chairman of GAMI, a member of the Outlook Committee for the city of Charleroi and a member of the Regional Advisory Committee for CERA (a cooperative financial grouping that includes 415,000 members). He is a civil electrical engineer and a graduate of the Mons Polytechnic Faculty (Belgium). He was first appointed to the Board of Directors on June 30, 2010.

- Jacques Leconte, (who is considered to be an independent director), a French national, 70, was the Director of the Crédit Agricole Sud Rhône-Alpes Business Center. He was specifically in charge of the financing activities for large companies, cooperatives and institutional investors for the Rhône-Alpes regional districts at the Crédit Agricole Regional Development Agency. He has been a director of Jacquet Metals since 2009 and is also a member of the Strategy Committee of Thermcross SA. Jacques Leconte studied geography at university and is a graduate of the Lyon Institute of Political Studies. He was first appointed to the Board of Directors on June 30, 2010.

- Hiscan Patrimonio S.A. (which is considered to be an independent director), a company governed by

Spanish law, represented by Jorge Galera Garcia Montes. Hiscan Patrimonio resigned from its director's office on October 10, 2014.

>

OVERVIEW OF GROUP

6

- JSA, a limited company governed by Belgian Law, controlled by Eric Jacquet and represented by Philippe Goczol. Philippe Goczol, a Belgian national, 48, is also the Deputy Chief Executive Officer of Jacquet Metal Service. He holds several appointments as a legal representative within the JMS Group. Philippe Goczol was a member of IMS International Metal Service’s Supervisory Board and Audit and Risk Committee from June 16, 2009 to February 3, 2010, the date on which he resigned. He was Chief Development Officer for Jacquet Metals from 2001 to 2004 and Chief Executive Officer from 2004 to 2008 Before joining Jacquet Metals, he was a member of the Executive Board and the CEO of Anysteel (2000-2001), and held positions as Sales Director (1999-2000), Proxy (1992-2000) and Commercial Engineer (1988-1992) at Industeel (formerly CLI-Fafer and Fafer). Philippe Goczol is a sales engineer and holds a degree from Mons University (Belgium). He was first appointed to the Board of Directors on June 30, 2010.

To the Company’s knowledge, no member of the Board of Directors has been the subject of an official public sanction, has been sentenced for fraud during the past five years, has been involved in any receivership, has been sanctioned by any statutory or regulatory authorities, including designated professional bodies, or has been the subject of any measure preventing them from directing, managing, administering or controlling a company during the past five years. To the Company’s knowledge, there is no potential conflict of interest between the private interests of the members of the Board of Directors and their duties to the Company. There are no arrangements or agreements with the main shareholders, or with customers or suppliers, pursuant to which a member of the Board of Directors might have been appointed as a director of the Company. There are no family ties between the members of the Board of Directors, including between Eric Jacquet and Jean Jacquet. A list of the offices and positions held by the corporate officers, as well as information on the number of shares they hold in Jacquet Metal Service is disclosed in paragraph 2.15 of the Management Report – Information on the parent company. The remuneration paid to the corporate officers is set out in paragraph 2.13 of the Management Report – Information on the parent company.

7

4.2 Senior management Jacquet Metal Service

Eric Jacquet Chairman & Chief Executive Officer Philippe Goczol Deputy Chief Executive Officer Thierry Philippe Chief Financial Officer, Investor Relations David Farias Chief Executive Officer responsible for the Jacquet and Abraservice brands Patrick Guien IT Director Jean Révérand Group Procurement Director Cédric Chaillol Brand communications and corporate identity manager

Brand operating divisions

David Farias Jacquet - Abraservice Wolfgang Hartmann Stappert José Berthelier IMS group

4.3. The Board of Directors committees Appointment and Compensation Committee

The Appointment and Compensation Committee consists of the following directors appointed by the Board of Directors for the term of their office as director on June 26, 2014:

- Henri-Jacques Nougein, Chairman; - Jacques Leconte; - Jean Jacquet.

Audit and Risk Committee

The Audit and Risk Committee consists of the following directors appointed by the Board of Directors for the term of their office as director on June 29, 2012:

- Jean Jacquet, Chairman; - Françoise Papapietro; - Xavier Gailly.

The offices of the Audit and Risk Committee members were renewed at the Board of Directors meeting on June 26, 2014.

4.4. Honorary Chairman Jacques-Didier Champalbert, the founder of IMS International Metal Service and Honorary Chairman of Jacquet Metal Service, died on April 25, 2014.

>

OVERVIEW OF GROUP

8

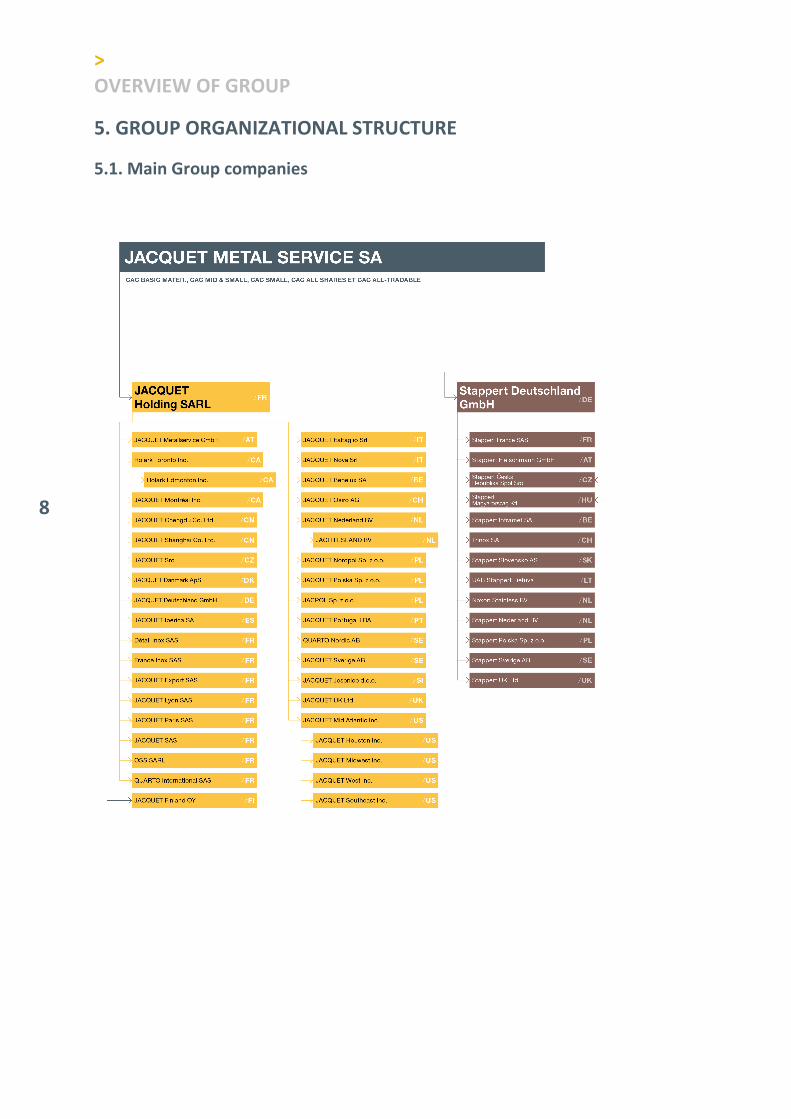

5. GROUP ORGANIZATIONAL STRUCTURE

5.1. Main Group companies

9

>

OVERVIEW OF GROUP

10

5.2. History of the Group

JACQUET Metals

1962 Foundation of Etablissements JACQUET, a company specializing in metal cutting, by Michel Jacquet in Lyon

1993 Eric Jacquet becomes the majority shareholder (51%) in JACQUET SA, the Group’s parent company

1994 Eric Jacquet founds JACQUET Industries, which controls 100% of the Group

1997 JACQUET Industries is listed on the Paris

Stock Exchange second market on October 23

1991-2006 The Group expands into Europe (Netherlands, Poland, UK, Italy and Finland)

2006 JACQUET Industries becomes JACQUET

Metals

2006-2010 The Group establishes its first operations in Asia (Shanghai, China) and the United States (Philadelphia, Houston, Chicago, Los Angeles and Charlotte) 2008-2009 Eric Jacquet and JACQUET Metals acquire

a 33.19% stake in IMS

IMS

1977 Foundation of “International Metal

Service”, which includes the Creusot-Loire steel manufacturer's “commercial companies”

1983 Usinor acquires full control of IMS

1987 IMS is listed on the Paris Stock Exchange

second market on June 11, under the chairmanship

of IMS founder Jacques-Didier Champalbert

1996-2002 The Group expands into Europe (IMS Stalserwis in Poland, IMS SpA in Italy, acquisition of Grupo Aceros Garay, which becomes Aceros IMS (Spain) and foundation of IMS France via the merger of three French companies)

2004 Arcelor sells its shareholding and Chequers Capital Fund acquires control of IMS

2005 Acquisitions in Central Europe (Hungary, the Czech Republic and Slovakia)

2006 Acquisition of Hoselmann (engineering steels in Germany)

2006 Chequers Capital sells its interest. Market placement of the IMS shares

2007 Acquisition of the Cotubel Group

2008 Sale of US subsidiary Astralloy

February 3, 2010 Jacquet Metals launches a public exchange offer (PEO) for the IMS shares.

June 30, 2010 The absorption of JACQUET Metals by IMS on the basis of the issuance of 20 IMS shares for 7 existing JACQUET Metals shares is approved by the General Meetings of Jacquet Metals and IMS.

July 20, 2010 Merger between JACQUET Metals and IMS

2011 - Disposal of IMS France’s aluminum and non-ferrous metals businesses and of Euralliage.

- IMS International Metal Service becomes Jacquet Metal Service.

- Disposal of Produr.

2012 Disposal of Venturi srl (Italy) and Brescia Acciai (Italy).

2013 Acquisition of Finkenholl (Germany) by the IMS group brand.

2014 Acquisition of ROLARK (Canada) by the JACQUET brand.

11

6. INFORMATION ON THE GROUP’S BUSINESS

6.1. The business The Jacquet Metal Service Group’s main business is the purchase, storage and delivery of various categories of products to a customer base that is primarily local and consists of small and medium-sized industrial companies. The Group buys large quantities from specialty steel producers (20 suppliers account for over 50% of Group purchases, with lead times ranging between 1 and 12 months) and sells them to a scattered customer base (60,000 active customers, average invoices of less than €3,000). Jacquet Metal Service provides the following value-added between the producer and the end-customer:

- A wide range of products in stock, which are delivered within short timeframes (order books rarely exceed a few weeks);

- Security of supply and product traceability; - Managing requirements on a just-in-time basis (customized inventory, defined supply strategies); - Competitive sale prices; - Managing price fluctuation on the customer’s behalf; - Cutting and finishing services.

In addition to selling its standard product range, the Group is able to offer its customers the choice of various customized initial processing operations in order to meet the final users' specifications. These services, which are performed at the Group’s warehouses, vary according to the products sold but usually involve light cutting, straightening and bending, folding or drilling operations. These services provide an obvious commercial advantage: they enable the Group to increase customer loyalty by positioning itself as a single contact point, thereby avoiding the use of a sub-contractor. The sales teams account for around 40% of the staff. They consist of sedentary or traveling salespersons whose remit is to follow up and advise customers, while ensuring that the Group’s offering meets their requirements on an ongoing basis.

6.2. Positioning The Group currently operates on four separate markets that form part of the distribution of specialty steels to industry, via four brands:

- JACQUET: stainless steel quarto plates; - Stappert: long stainless steel products; - Abraservice: wear-resistant quarto plates; - IMS group: engineering steels.

The Group’s strategy is to be physically close to its customers on the markets targeted by each Group brand. To date, Jacquet Metal Service is primarily positioned in European markets with the Stappert, Abraservice and IMS group brands. The JACQUET brand is established in Europe, in North America and China.

>

OVERVIEW OF GROUP

12

6.3. The market Sources: Jacquet Metal Service

The global steel market amounted to around 1.66 billion tons in 2014, of which alloy steels (steels containing alloy components such as chrome, nickel, molybdenum and titanium) accounted for around 5% across all product ranges. In the steel alloy category, stainless steels accounted for around 37 million tons across all products, i.e. around 2% of the global steel market. As the specialty steels market covers a large number of product niches, geopolitical situations and types of distribution role, the Group has little quantified information of an official nature. JACQUET and Stappert – stainless steels

Stainless steels are characterized by their strong resistance to corrosion and their stability when treated with fluids or gas. The main sectors that consume stainless steels are industries operating in:

- the chemicals sector (including pharmaceuticals and cosmetics); - the food-processing sector (hygiene restrictions and ease of maintenance); - the gas processing and storage sector (cryogenics, industrial gas); - the water treatment sector (waste water precipitation basins, desalination of sea water, transmission

and supply); - the environmental and decontamination sector (emissions and waste treatment); - the energy sector (hydraulic, nuclear and thermal power plants, etc.).

From 2013 to 2014, the consumption of stainless steel increased by 4% in Europe, 5% in America and 6% in Asia. In 2014, the consumption of stainless steel in Europe increased compared to 2013 by 4%, by 5% in North America and 6% in Asia. The stainless steel sector is characterized by the regular adjustment of the alloys to the increasingly high requirements of various industrial sectors. While there were two main varieties of stainless steel in 1960, JACQUET and Stappert currently stock several dozen, in addition to nickel alloy varieties, whose corrosion resistance is even higher than that of stainless steel. JACQUET – stainless steel quarto plates

The annual global stainless steel quarto plate market represents just over 1.25 million tons, i.e. around 3.9% of the global stainless steel market. It is a typically niche market in this regard and accounts for the bulk of JACQUET’s sales. This market is usually equally divided between projects (direct supply from the producer to the end-customer) and distribution. JACQUET is the leading global distributor of stainless steel quarto plates. Stappert – long stainless steel products

The annual global long stainless steel product market represents around 5.5 million tons. The global stainless steel rod market represents around 3 million tons, while the European market represents around 800,000 tons. Distribution accounts for around 50% of the long stainless steel product market in Europe. Stappert is one of the leading operators on the distribution market.

13

Abraservice – wear-resistant quarto plates

Wear-resistant quarto plates are intended for industrial sectors that face issues related to wear, shock-resistance, friction, temperature or tension that require the use of particularly hard materials, i.e. public works machinery, steel production, mines and quarries, cement plants, dredging, recycling, handling, agricultural machinery and the lifting and transportation of aggregates, etc. The wear-resistant quarto plates distributed by Abraservice meet particularly stringent quality and durability requirements. In addition to its offer, Abraservice also distributes plates with a high elasticity threshold designed for the heavy machinery, telescopic crane and civil engineering sectors. In fact, both categories of products share the same manufacturing methods (“hardened and tempered steels”) and the same shaping processes (pre-manufacturing operations performed by Abraservice, including cutting, drilling, folding and rolling). The annual European wear-resistant steels market is usually estimated at around 350,000 tons, 70% of which is supplied via distribution channels while the remainder is sold directly to end-users by producers. The wear-resistant steel market has struggling to recover since 2012. The European market for high-elasticity steels is usually estimated at around 500,000 tons, 30% of which is supplied via distribution channels. This market has been hit hard since 2012 in Europe. Abraservice is one of the market leaders for the distribution of wear-resistant plates. IMS group – engineering steels

These steels are used to manufacture parts that are subject to stringent engineering specifications. Engineering steels are distributed by the IMS group brand, primarily in the form of seamless rods and tubes, and are produced in accordance with specific standards and specifications that guarantee their suitability for processing by the customer (forging, machining, folding, welding, heat treatment) so as to achieve specific engineering features following their treatment. They are used in many industrial sectors, including: general engineering, public works equipment, agricultural machinery, transportation (engines, automotive drives, heavy goods vehicles and the railway sector), lifting machinery, oil industry and energy (wind turbines, etc.), and machining plants. The engineering steels market includes many forms and categories of products. The annual European engineering alloy steel market is estimated at around 9.5 million tons, including 4.5 million tons of rods. The two largest geographical markets in Europe are Germany and Italy, which jointly account for 60% of the market, followed by France and Spain, which represent 20% of the European market. The distribution sector’s share of the engineering steel rod market is estimated at 50%. IMS group’s market share varies significantly depending on the country, with strong positions in Italy, France and Spain. IMS group still has significant room to expand in other European countries, especially in Germany (first European market).

>

OVERVIEW OF GROUP

14

6.4. Competition JACQUET

The main competitors in the cut plate market, which accounts for most of the volumes distributed by JACQUET, fall into two categories:

- In-house departments of large European steel groups (e.g. Outokumpu, which absorbed the Inoxum Division including the ThyssenKrupp stainless steel businesses in December 2012) in several countries;

- Family-owned companies, which operate in just one country. There are also two kinds of competitors in the trade segment (sale of unprocessed plates), a business where JACQUET implements an opportunistic policy depending on market conditions, i.e.

- Stainless steel producers who have their own in-house distribution network (Acerinox, Outokumpu, Daekyung and Thyssen);

- Companies that are independent from the producers, such as Nichelcrom in Italy and Salzgitter in Germany; As product availability, and therefore inventories, is a key factor in this business, there are few direct competitors in the trading segment.

Stappert

Stappert’s competition breaks down between:

- Operators who are established at the European level, including producers of long stainless steel products who distribute their products via their own distribution network (Schmolz + Bickenbach, Cogne, Valbruna) or distributors who are independent from the producers (Amari, Damstahl, ThyssenKrupp Materials);

- Independent distributors, whose size may be significant at regional or national level but who do not operate on a European scale.

Abraservice

Wear-resistant products are often brand steels that are developed and distributed by steel producers. Abraservice’s main competitor in Europe is SSAB, the Swedish steel producer, which only markets its own products. There are a few independent competitors, whose size can be significant, at regional or national level. They often distribute entry-level products from remote or second-tier producers. IMS group

The engineering steel distribution market includes a small number of major international operators at European level (Schmolz + Bickenbach, ThyssenKrupp Materials, Cogne). IMS group is the only operator that has no production activities. The remainder of the market is divided between a large number of independent distributors, whose size may be significant at regional or national level but who do not operate on a European scale. Competition in the engineering steel distribution segment rarely comes from the actual producers. A large number of those producers do not hold any inventories. The different varieties are often not produced on an ongoing basis and are sold through the order book as soon as they leave the plant. This means that the producers only target major end-users directly.

15

6.5. The customers Specialty steels are used for specific applications by a wide variety of industrial sectors. Larger end-users such as automotive manufacturers are supplied directly by producers. Conversely, Jacquet Metal Service’s core target market consists of a local network of SMEs operating in a wide variety of industrial sectors. The Group supplies over 60,000 active customers based in around 100 countries, while its commercial relationships are based on a large quantity of small orders (less than €3,000 on average). Accordingly, the Group is not dependent on any specific customer. Customers place their orders directly with the Group companies, with no call for tender process. Every customer order is invoiced once the products have been dispatched. A significant portion of the sales are insured by various credit insurance companies. JACQUET's and Stappert's customers primarily operate in the chemicals, food-processing, energy and environmental sectors, as well as the water and gas storage and treatment sectors. Abraservice’s customers are industrial companies that operate in the mining and quarries, public works machinery, handling, lifting and haulage sectors, as well as cement plants. IMS group offers products that display resistance to engineering constraints. Therefore the brand primarily targets industrial companies in the transportation equipment (engines, drives, railways, etc.), energy (wind turbines, petrochemicals and refining, etc.) and more broadly in the general engineering and machining plant sectors. The commercial relationships are recurring and involve a large quantity of small orders, which account for most of the Group’s sales. The order book represents around one month’s sales.

6.6. Purchases The terms and conditions of purchase are negotiated between the main producers’ management teams and the Jacquet Metal Service S.A. managers, working together with the Chief Operating Officer for each brand. By aggregating the volumes for each brand, Jacquet Metal Service provides producers with greater visibility on their business volumes and on the organization of their production schedule. The Group benefits from optimal purchasing terms and conditions in return. The “framework terms and conditions” obtained in this way are disclosed to the subsidiaries involved, which place their orders with the producers directly. The Group is not dependent on a specific supplier and only uses sub-contractors on an occasional basis. A given supplier is only in a position to provide a limited number of stock items. In the case of so-called specialty products distributed on niche markets, the number of suppliers is also limited. In the case of some niche products, the Group purchases its supplies primarily from producers with which it has a close relationship (VDM for nickel alloys, Arcelor Mittal Industeel for the Creusabro range, etc.). The Group also has exclusive agreements for some products and in some countries.

>

OVERVIEW OF GROUP

16

7. OTHER INFORMATION

7.1. IT system All the companies belonging to the JACQUET and Abraservice brands use the Integrated Management Program (IMP), which was developed in-house. This program includes a business application and a localized accounting solution. These centralized tools are one of the keys to an effective and responsive management control process. This IMP is being installed for Stappert brand and will be operational in 2015. The dedicated IT tool provides optimal solutions aimed at simplifying the sales process. It is also an essential tool for implementing purchasing systems based on pooled negotiations. The user interface benefits from the user-friendliness of a full web mode. Every user can access all their brand’s inventories in real-time. “Intra-group” sales are processed automatically. Marketing documents are published in the local language and comply with national presentation specifications. The business application for each brand is available in many languages, which simplifies the day-to-day work of all users throughout the world. For instance, all user interface screens are available in Chinese; when a Chinese employee handles an order in Shanghai in their native tongue, this order can be viewed in French at the Group’s head office. The business application has been developed using state-of-the-art technologies (full web mode on a LAOP Linux-Apache platform, Oracle database, PHP), while all Group websites are connected to the central website via an MPLS and VPN IPsec network. The high degree of scalability of the chosen solution enables the Group’s developments over the coming years to be supported without problems, regardless of the number of users and/or volumes handled. The IMS group and Stappert brands companies primarily use the Stratix IMP and specific IMSX developments, which supplement the logistic functionalities of the Stratix product. Adapting the in-house developed IMP to the long product distribution businesses (Stappert and IMS group brands) required a significant number of changes and the development of additional modules. The main IMP modules have now been developed and the first Stappert Polska website has been rolled out. Local customization and the roll-out of the IMP developed on Stappert brand companies will be operational in 2015.

17

7.2. A unique development method The Group is developing the use of its brands via an unusual and innovative business model in the metal distribution sector. Joint ventures (JVs) are set up with a local partner, who is usually the manager of the JV. This partner invests and receives an equity interest in the JV that ranges between 10 and 49%; the partner commits to recapitalizing the JV at least up to the amount initially invested in the event of losses. The JV benefits from the exclusive right to use the brand and can therefore market the full range of the brand’s products in a specified area. The local partner benefits from a set of resources made available to them by the Group, such as terms and conditions of purchase, a product/market information system tailored to their business, staff training, access to an information network, etc. Every effort is made to enable the local partner to focus on their main goal, i.e. generating profitable sales. Local managers manage their inventories in accordance with the marketing policy that they have determined. Managers' compensation is largely based on the JV’s results. The Group invoices the JV for services performed, primarily management fees and IT services. Where applicable, managers also receive dividends in proportion to the units that they hold.

7.3. Capital expenditure policy This information is provided in paragraph 1.5 “Consolidated financial position/Capital expenditure” in the Management Report – Information on the Group.

7.4. Risk factors This information is provided in paragraph 1.7 “Risk factors” in the Management Report – Information on the Group.

8. STOCK MARKET INFORMATION

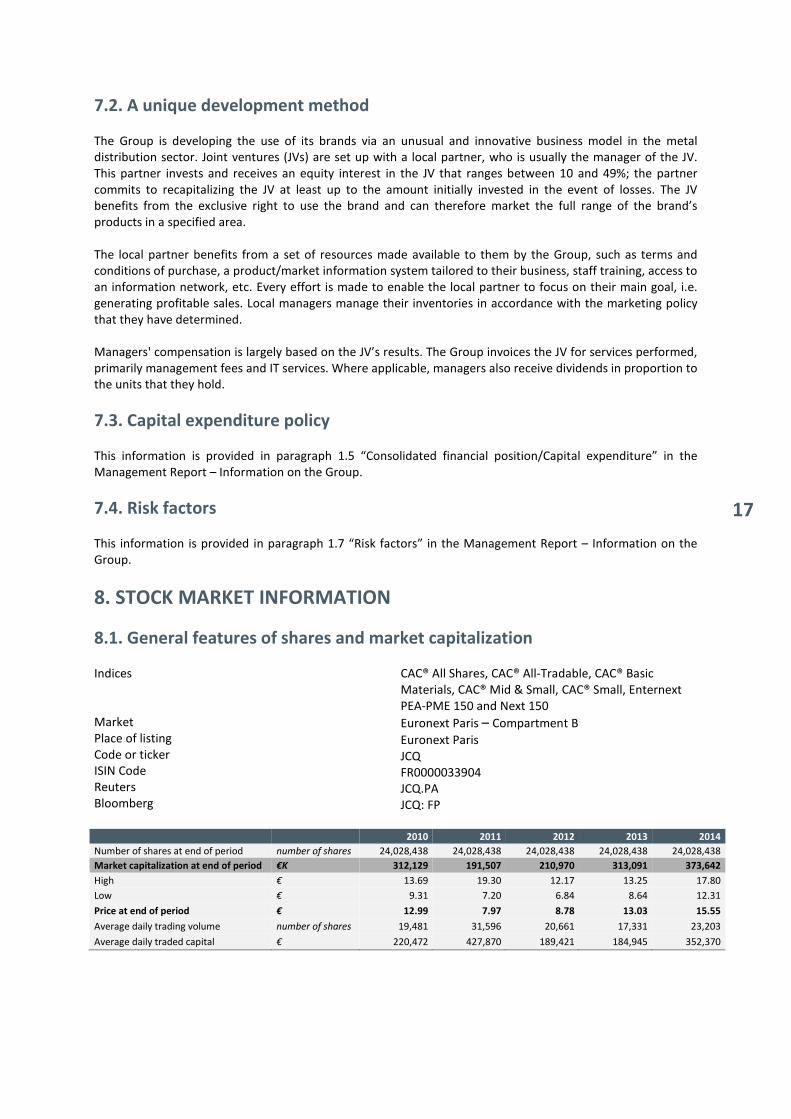

8.1. General features of shares and market capitalization

Indices Market Place of listing Code or ticker ISIN Code Reuters Bloomberg

CAC® All Shares, CAC® All-Tradable, CAC® Basic Materials, CAC® Mid & Small, CAC® Small, Enternext PEA-PME 150 and Next 150

Euronext Paris – Compartment B

Euronext Paris JCQ FR0000033904 JCQ.PA JCQ: FP

2010 2011 2012 2013 2014

Number of shares at end of period number of shares 24,028,438 24,028,438 24,028,438 24,028,438 24,028,438

Market capitalization at end of period €K 312,129 191,507 210,970 313,091 373,642

High € 13.69 19.30 12.17 13.25 17.80

Low € 9.31 7.20 6.84 8.64 12.31

Price at end of period € 12.99 7.97 8.78 13.03 15.55

Average daily trading volume number of shares 19,481 31,596 20,661 17,331 23,203

Average daily traded capital € 220,472 427,870 189,421 184,945 352,370

>

OVERVIEW OF GROUP

18

STOXX® Europe TMI Industrial Metals (indexed to JCQ at Jan. 1, 2014

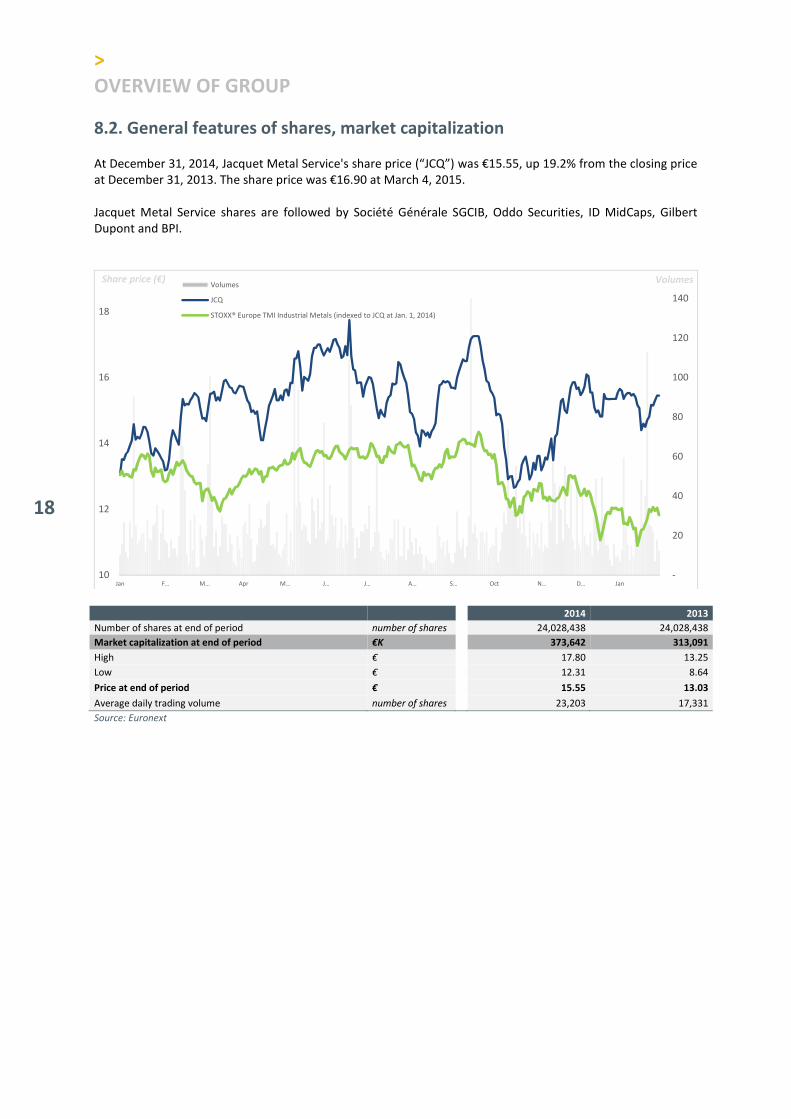

8.2. General features of shares, market capitalization

At December 31, 2014, Jacquet Metal Service's share price (“JCQ”) was €15.55, up 19.2% from the closing price at December 31, 2013. The share price was €16.90 at March 4, 2015. Jacquet Metal Service shares are followed by Société Générale SGCIB, Oddo Securities, ID MidCaps, Gilbert Dupont and BPI.

2014 2013

Number of shares at end of period number of shares 24,028,438 24,028,438

Market capitalization at end of period €K 373,642 313,091

High € 17.80 13.25

Low € 12.31 8.64

Price at end of period € 15.55 13.03

Average daily trading volume number of shares 23,203 17,331

Source: Euronext

-

20

40

60

80

100

120

140

10

12

14

16

18

Jan F… M… Apr M… J… J… A… S… Oct N… D… Jan

Volumes Share price (€)Volumes

JCQ

STOXX® Europe TMI Industrial Metals (indexed to JCQ at Jan. 1, 2014)

19

NewCap

Emmanuel Huynh / Julien Perez Tel: +33 (0)1 44 71 94 94 [email protected]

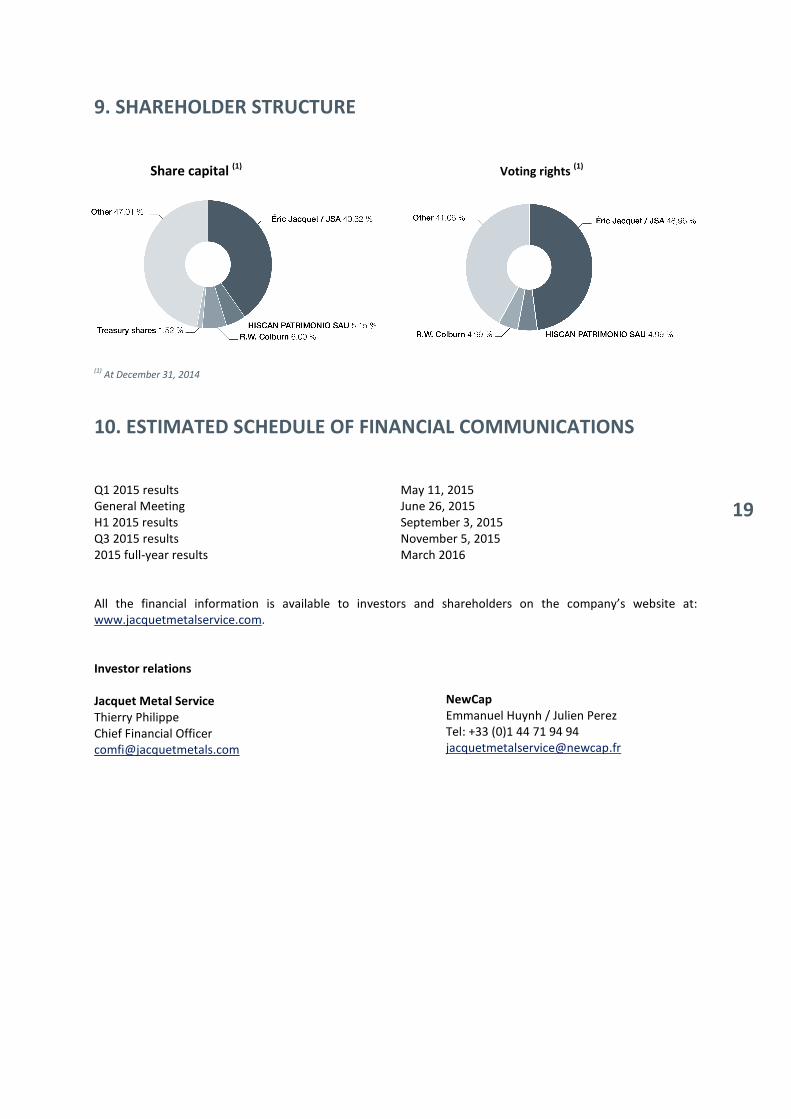

9. SHAREHOLDER STRUCTURE

Share capital (1) Voting rights

(1)

(1)

At December 31, 2014

10. ESTIMATED SCHEDULE OF FINANCIAL COMMUNICATIONS

Q1 2015 results General Meeting H1 2015 results Q3 2015 results 2015 full-year results

May 11, 2015 June 26, 2015 September 3, 2015 November 5, 2015 March 2016

All the financial information is available to investors and shareholders on the company’s website at: www.jacquetmetalservice.com.

Investor relations

Jacquet Metal Service

Thierry Philippe Chief Financial Officer [email protected]

20

2014

FINANCIAL

REPORT

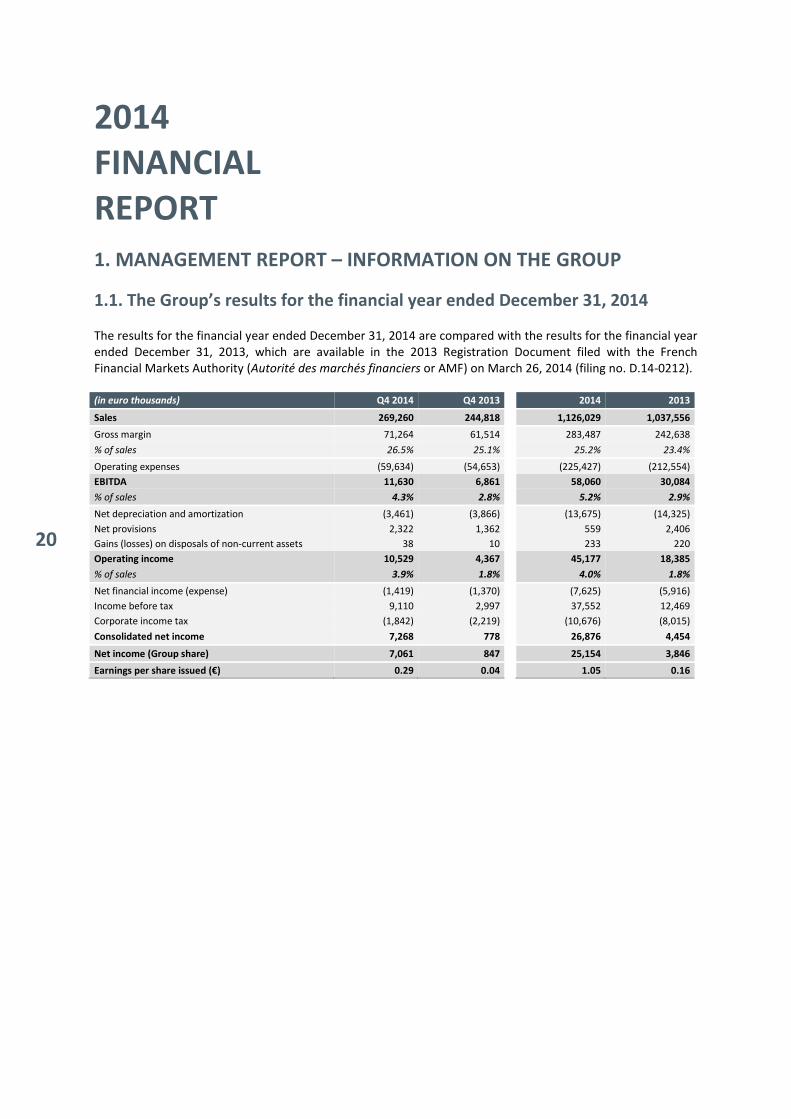

1. MANAGEMENT REPORT – INFORMATION ON THE GROUP

1.1. The Group’s results for the financial year ended December 31, 2014 The results for the financial year ended December 31, 2014 are compared with the results for the financial year ended December 31, 2013, which are available in the 2013 Registration Document filed with the French Financial Markets Authority (Autorité des marchés financiers or AMF) on March 26, 2014 (filing no. D.14-0212). (in euro thousands) Q4 2014 Q4 2013 2014 2013

Sales 269,260 244,818 1,126,029 1,037,556

Gross margin 71,264 61,514 283,487 242,638

% of sales 26.5% 25.1% 25.2% 23.4%

Operating expenses (59,634) (54,653) (225,427) (212,554)

EBITDA 11,630 6,861 58,060 30,084

% of sales 4.3% 2.8% 5.2% 2.9%

Net depreciation and amortization (3,461) (3,866) (13,675) (14,325)

Net provisions 2,322 1,362 559 2,406

Gains (losses) on disposals of non-current assets 38 10 233 220

Operating income 10,529 4,367 45,177 18,385

% of sales 3.9% 1.8% 4.0% 1.8%

Net financial income (expense) (1,419) (1,370) (7,625) (5,916)

Income before tax 9,110 2,997 37,552 12,469

Corporate income tax (1,842) (2,219) (10,676) (8,015)

Consolidated net income 7,268 778 26,876 4,454

Net income (Group share) 7,061 847 25,154 3,846

Earnings per share issued (€) 0.29 0.04 1.05 0.16

21

1.2. 2014 highlights

2014 was characterized by:

- a 10.7% increase in volumes sold ; - average sale prices fell by 2.2% compared with 2013 ; - a €40.8 million rise in the gross margin to €283.5 million, i.e. 25.2% of sales (+1.8 percentage points

compared with 2013) ; - Acquisition of ROLARK Group (Canada) by the JACQUET brand (stainless steel quarto plates)

ROLARK is a Canadian group that has been operating in the stainless steel distribution sector for 30 years and consists of three companies based in Toronto, Edmonton and Montreal. ROLARK has 65 employees and generates sales of CAD 34 million (€25 million). The three ROLARK Group companies have warehouses and finishing facilities, and supplement JACQUET's North American network, which is already established in Philadelphia, Chicago, Houston, Charlotte and Los Angeles. Including ROLARK, the JACQUET brand now has 626 employees and 29 distribution centers in 20 countries. As a result of this acquisition, the brand generated 2014 annual pro forma sales of €250 million, 33% of which was generated in North America.

1.3. Group sales and earnings

Sales 2014 revenues amounted to €1.13 billion, an 8.5% increase compared with 2013. This increase breaks down as follows:

- Volume effect: +10.7% rise in volumes, including 3.7 percentage points related to the acquisition of Finkenholl in August 2013 and Rolark in October 2014 (€5.0 million recognized over 2.5 months);

- Price effect: -2.2%. In 2014, average sale prices decreased by -2.2% compared with 2013 (including -7.8% during first semester and +2.5% during the second semester).

Group sales increased by 10.0% to €269.3 million in the fourth quarter of 2014, including a price effect of +4.3% and volume effect of 5.7% (including 2.8 percentage points due to changes in the consolidation scope).

(€m) Q4 2014 Q4 2013 2014 2013

Sales 269.3 244.8 1,126.0 1,037.6

2014 change vs. 2013 10.0% 8.5%

Price effect 4.3% -2.2%

Volume effect 2.9% 7.0%

Scope effect 2.8% 3.7%

Gross margin The 2014 gross margin amounted to €283.5 million compared with €242.6 million in 2013. This €40.8 million increase was primarily due to:

- an improvement of gross margin rate from 23.4% in 2013 to 25.2% in 2014: + €20.3 million ; - volume increases amounting to €25.5 million ; - a decrease in average sales prices amounting to €5.0 million.

Excluding the impact of inventory provisions, the gross margin rate was 25.6% in 2014 compared to 23.3% in 2013.

>

2014 FINANCIAL REPORT MANAGEMENT REPORT – INFORMATION ON THE GROUP

22

Comparing with the fourth quarter 2013, the gross margin rate rose by 1.4 percentage points in the fourth quarter 2014 to 26.5% of sales. All brands contributed to this improvement. (€m) Q4 2014 Q4 2013 2014 2013

Gross margin 71.3 61.5 283.5 242.6

% of sales 26.5% 25.1% 25.2% 23.4%

Operating income Operating expenses (including net amortization, depreciation and provisions) amounted to €238.5 million compared with €224.5 million in 2013. This €14 million increase was primarily due to:

- a positive consolidation scope effect of €8.9 million, primarily related to the acquisitions of Finkenholl in 2013 and ROLARK Group in 2014;

- a €5.6 million increase relating to higher activity and results;

Excluding scope effect, operating expenses increased by +2.3% compared with 2013. EBITDA amounted to €58.1 million, or 5.2% of sales, compared to 2.9% in 2013. Operating income amounted to €45.2 million (4.0% of sales) compared to €18.4 million in 2013.

Net financial items Net financial expense amounted to €7.6 million compared to €5.9 million in 2013. This evolution is linked to the increase in gross debt (from €127.2 million in 2013 to €172.6 million in 2014). Meanwhile, the average cost of gross debt fell from 3.1% in 2013 to 2.8% on 2014. (€m) Q4 2014 Q4 2013 2014 2013

Net cost of debt (1.3) (1.4) (5.3) (4.0)

Other financial items (0.2) 0.0 (2.3) (1.9)

Net financial income (expense) (1.4) (1.4) (7.6) (5.9)

Net income Net income (Group share) rose from €3.8 million in 2013 to €25.2 million in 2014, corresponding to €1.05 per share. Net income includes a tax charge of €10.7 million, corresponding to a tax rate of 28.4%. (€m) Q4 2014 Q4 2013 2014 2013

Income before tax 9.1 3.0 37.6 12.5

Corporate income tax (1.8) (2.2) (10.7) (8.0)

Income tax rate -20.2% -74.0% -28.4% -64.3%

Consolidated net income 7.3 0.8 26.9 4.5

Minority interests 0.2 (0.1) 1.7 0.6

Net income (Group share) 7.1 0.8 25.2 3.8

% of sales 2.6% 0.3% 2.2% 0.4%

23

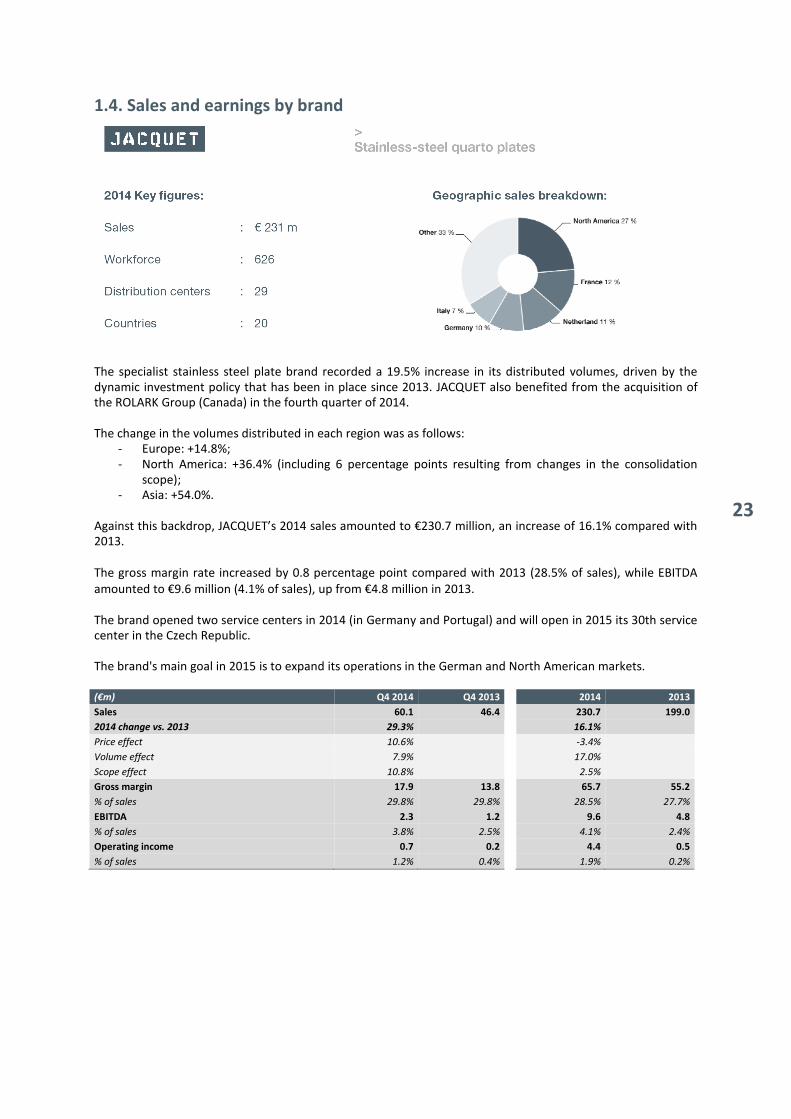

1.4. Sales and earnings by brand The specialist stainless steel plate brand recorded a 19.5% increase in its distributed volumes, driven by the dynamic investment policy that has been in place since 2013. JACQUET also benefited from the acquisition of the ROLARK Group (Canada) in the fourth quarter of 2014. The change in the volumes distributed in each region was as follows:

- Europe: +14.8%; - North America: +36.4% (including 6 percentage points resulting from changes in the consolidation

scope); - Asia: +54.0%.

Against this backdrop, JACQUET’s 2014 sales amounted to €230.7 million, an increase of 16.1% compared with 2013. The gross margin rate increased by 0.8 percentage point compared with 2013 (28.5% of sales), while EBITDA amounted to €9.6 million (4.1% of sales), up from €4.8 million in 2013. The brand opened two service centers in 2014 (in Germany and Portugal) and will open in 2015 its 30th service center in the Czech Republic. The brand's main goal in 2015 is to expand its operations in the German and North American markets. (€m) Q4 2014 Q4 2013 2014 2013

Sales 60.1 46.4

230.7 199.0

2014 change vs. 2013 29.3% 16.1%

Price effect 10.6% -3.4%

Volume effect 7.9% 17.0%

Scope effect 10.8% 2.5%

Gross margin 17.9 13.8 65.7 55.2

% of sales 29.8% 29.8% 28.5% 27.7%

EBITDA 2.3 1.2 9.6 4.8

% of sales 3.8% 2.5% 4.1% 2.4%

Operating income 0.7 0.2 4.4 0.5

% of sales 1.2% 0.4% 1.9% 0.2%

>

2014 FINANCIAL REPORT MANAGEMENT REPORT – INFORMATION ON THE GROUP

24

The specialist long stainless steel products brand recorded sales of €453 million, an increase of 1.5% compared with 2013 (volume effect +1.8%, price effect -0.3%). Although the volumes distributed in Germany and outside Europe (45% of total volumes) fell by 2.3% compared to 2013, volumes in the rest of Europe increased by 5.4%:

- South Eastern Europe (Austria, Czech Republic, Slovakia and Hungary): +3.8%. This region accounts for 26% of the brand’s sales.

- North Eastern Europe (Poland, Lithuania and Sweden): +5.3%. This region accounts for 14% of the brand’s sales.

- Western Europe (Austria, Czech Republic, Slovakia and Hungary): +8.4%. This region accounts for 15% of the brand’s sales.

With an increase of gross margin rate by 2.8 percentage points compared to 2013 (22% of sales), the EBITDA of the brand amounted to €26.5 million (5.9% of sales), compared to €13.8 million a year earlier. Stappert opened a service center in the United Kingdom in the second half of 2014 and will focus its 2015 development on Europe. The brand may also establish operations in North America in the medium-term. (€m) Q4 2014 Q4 2013 2014 2013

Sales 102.3 100.1

453.0 446.3

Change vs. 2013 2.3% 1.5%

Price effect 6.6% -0.3%

Volume effect -4.3% 1.8%

Gross margin 24.0 21.1 99.7 85.7

% of sales 23.4% 21.1% 22.0% 19.2%

EBITDA 5.8 2.9 26.5 13.8

% of sales 5.7% 2.9% 5.9% 3.1%

Operating income 5.1 2.9 23.4 11.0

% of sales 5.0% 2.9% 5.2% 2.5%

25

The brand, which operates in sectors (mining and quarries, the steel industry etc.) where market conditions are unfavorable, specializes in the sale of wear-resistant quarto plates. It recorded a 4.8% increase in volumes in 2014, generating sales of €65 million. The gross margin rate rose by 2.1 percentage points (32.1% of sales in 2014).

EBITDA amounted to €0.7 million, compared with €0.1 million in 2013.

In 2014, Abraservice strengthened its operations by launching new service centers in Portugal, and in Italy and

Great Britain with the coming of new managers (minority shareholders for the subsidiaries they manage).

The brand will focus on strengthening its positioning in the European market in 2015.

(€m) Q4 2014 Q4 2013 2014 2013

Sales 16.3 15.1

65.0 64.0

Change vs. 2013 8.5% 1.6%

Price effect -2.3% -3.2%

Volume effect 10.8% 4.8%

Gross margin 5.4 4.8 20.8 19.1

% of sales 33.0% 32.2% 32.1% 29.9%

EBITDA 0.1 0.3 0.7 0.1

% of sales 0.4% 2.2% 1.1% 0.1%

Operating income (0.0) 0.3 (0.1) (0.4)

% sales -0.1% 1.7% -0.1% -0.6%

>

2014 FINANCIAL REPORT MANAGEMENT REPORT – INFORMATION ON THE GROUP

26

The brand, which specializes in the sale of engineering steels, saw its sales volumes increase by 15.5% in 2014, including a 7.4% consolidation scope effect resulting from the acquisition of Finkenholl in Germany in 2013. Accordingly, the brand generated sales of €384 million, an increase of 12.1%. The gross margin rate rose by 1 percentage point from 2013 to 25% of sales. 2014 EBITDA amounted to €15.6 million, or 4.1% of sales, compared with €6.4 million in 2013. IMS group opened in 2014 a subsidiary in the Netherlands, IMS Nederland. The brand still generates over 75% of its sales in southern Europe. Its main goal is to expand its operations on Germany (the largest European market). (€m) Q4 2014 Q4 2013 2014 2013

Sales 91.8 85.5

383.8 342.3

Change vs. 2013 7.3% 12.1%

Price effect -0.2% -3.3%

Volume effect 7.5% 8.1%

Scope effect 0.0% 7.4%

Gross margin 23.7 21.5 96.1 82.3

% of sales 25.9% 25.1% 25.0% 24.0%

EBITDA 2.0 1.0 15.6 6.4

% of sales 2.2% 1.2% 4.1% 1.9%

Operating income 2.9 (0.2) 12.7 4.2

% of sales 3.2% -0.2% 3.3% 1.2%

27

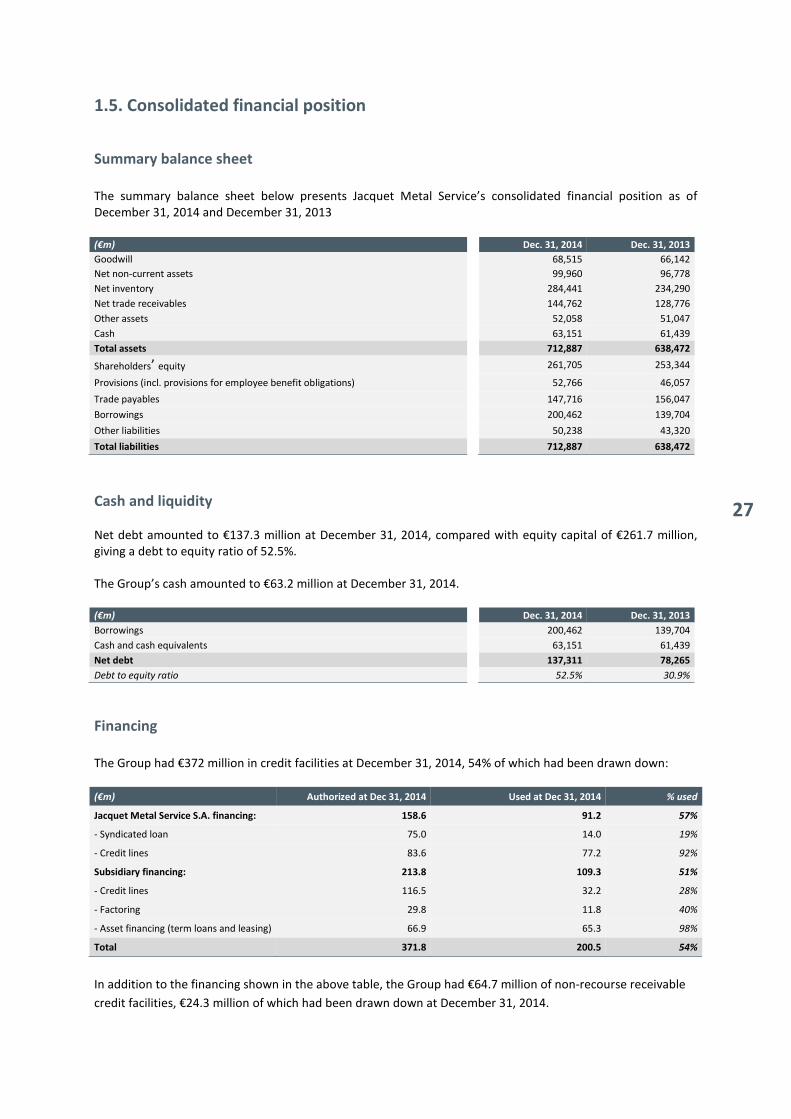

1.5. Consolidated financial position

Summary balance sheet

The summary balance sheet below presents Jacquet Metal Service’s consolidated financial position as of December 31, 2014 and December 31, 2013

(€m) Dec. 31, 2014 Dec. 31, 2013

Goodwill 68,515 66,142

Net non-current assets 99,960 96,778

Net inventory 284,441 234,290

Net trade receivables 144,762 128,776

Other assets 52,058 51,047

Cash 63,151 61,439

Total assets 712,887 638,472

Shareholders’ equity 261,705 253,344

Provisions (incl. provisions for employee benefit obligations) 52,766 46,057

Trade payables 147,716 156,047

Borrowings 200,462 139,704

Other liabilities 50,238 43,320

Total liabilities 712,887 638,472

Cash and liquidity Net debt amounted to €137.3 million at December 31, 2014, compared with equity capital of €261.7 million, giving a debt to equity ratio of 52.5%. The Group’s cash amounted to €63.2 million at December 31, 2014. (€m) Dec. 31, 2014 Dec. 31, 2013

Borrowings 200,462 139,704

Cash and cash equivalents 63,151 61,439

Net debt 137,311 78,265

Debt to equity ratio 52.5% 30.9%

Financing

The Group had €372 million in credit facilities at December 31, 2014, 54% of which had been drawn down:

(€m) Authorized at Dec 31, 2014 Used at Dec 31, 2014 % used

Jacquet Metal Service S.A. financing: 158.6 91.2 57%

- Syndicated loan 75.0 14.0 19%

- Credit lines 83.6 77.2 92%

Subsidiary financing: 213.8 109.3 51%

- Credit lines 116.5 32.2 28%

- Factoring 29.8 11.8 40%

- Asset financing (term loans and leasing) 66.9 65.3 98%

Total 371.8 200.5 54%

In addition to the financing shown in the above table, the Group had €64.7 million of non-recourse receivable

credit facilities, €24.3 million of which had been drawn down at December 31, 2014.

>

2014 FINANCIAL REPORT MANAGEMENT REPORT – INFORMATION ON THE GROUP

28

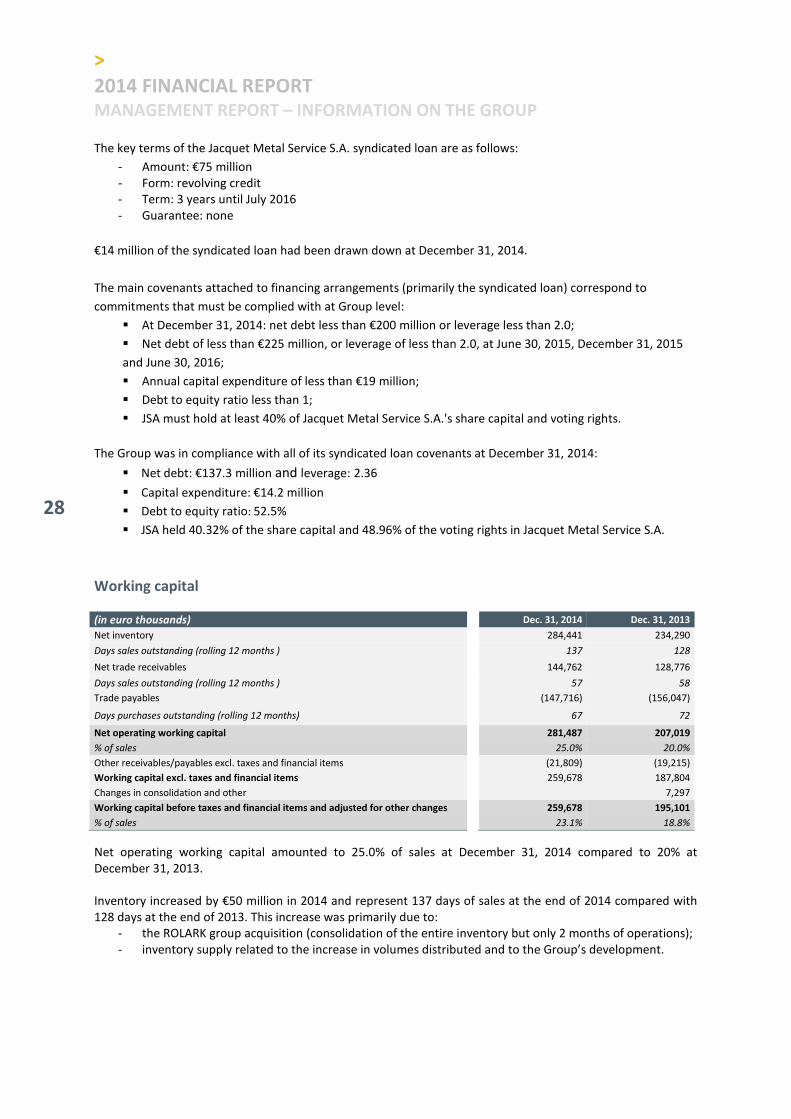

The key terms of the Jacquet Metal Service S.A. syndicated loan are as follows:

- Amount: €75 million - Form: revolving credit - Term: 3 years until July 2016 - Guarantee: none

€14 million of the syndicated loan had been drawn down at December 31, 2014.

The main covenants attached to financing arrangements (primarily the syndicated loan) correspond to

commitments that must be complied with at Group level:

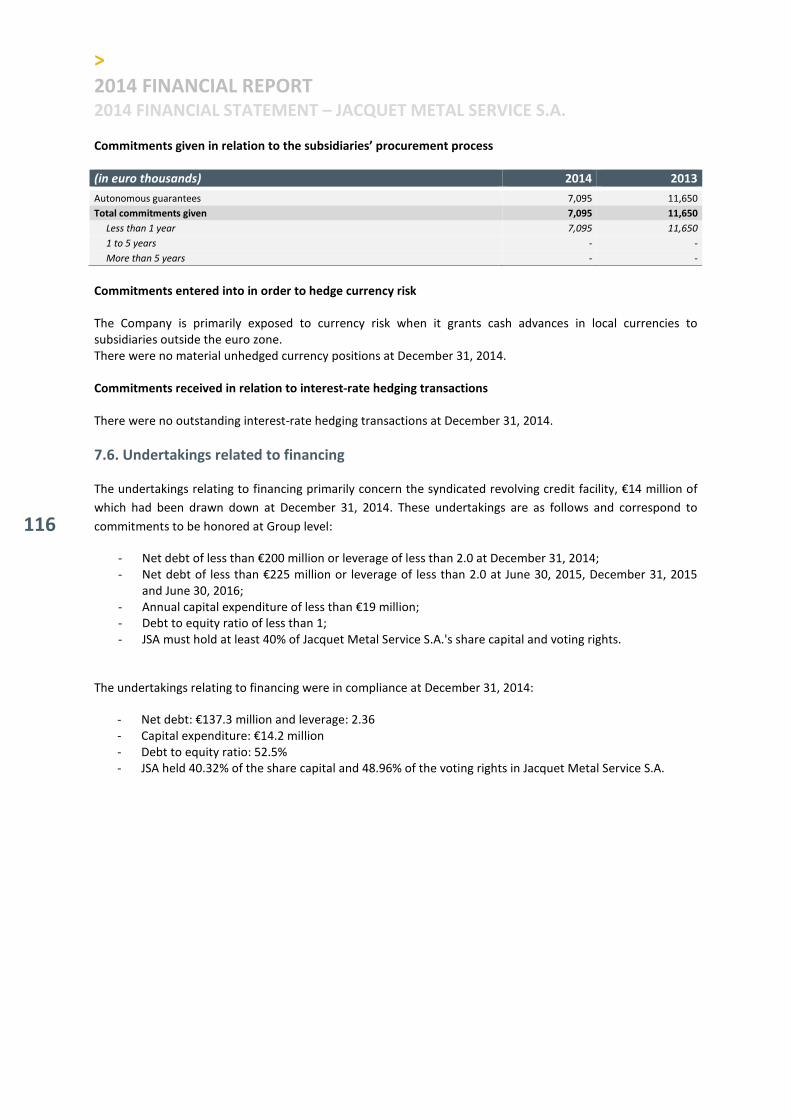

� At December 31, 2014: net debt less than €200 million or leverage less than 2.0;

� Net debt of less than €225 million, or leverage of less than 2.0, at June 30, 2015, December 31, 2015

and June 30, 2016;

� Annual capital expenditure of less than €19 million;

� Debt to equity ratio less than 1;

� JSA must hold at least 40% of Jacquet Metal Service S.A.'s share capital and voting rights.

The Group was in compliance with all of its syndicated loan covenants at December 31, 2014:

� Net debt: €137.3 million and leverage: 2.36

� Capital expenditure: €14.2 million

� Debt to equity ratio: 52.5%

� JSA held 40.32% of the share capital and 48.96% of the voting rights in Jacquet Metal Service S.A.

Working capital (in euro thousands) Dec. 31, 2014 Dec. 31, 2013

Net inventory 284,441 234,290

Days sales outstanding (rolling 12 months ) 137 128

Net trade receivables 144,762 128,776

Days sales outstanding (rolling 12 months ) 57 58

Trade payables (147,716) (156,047)

Days purchases outstanding (rolling 12 months) 67 72

Net operating working capital 281,487 207,019

% of sales 25.0% 20.0%

Other receivables/payables excl. taxes and financial items (21,809) (19,215)

Working capital excl. taxes and financial items 259,678 187,804

Changes in consolidation and other 7,297

Working capital before taxes and financial items and adjusted for other changes 259,678 195,101

% of sales 23.1% 18.8%

Net operating working capital amounted to 25.0% of sales at December 31, 2014 compared to 20% at December 31, 2013. Inventory increased by €50 million in 2014 and represent 137 days of sales at the end of 2014 compared with 128 days at the end of 2013. This increase was primarily due to:

- the ROLARK group acquisition (consolidation of the entire inventory but only 2 months of operations); - inventory supply related to the increase in volumes distributed and to the Group’s development.

29

Trade receivables amounted to €144.8 million at December 31, 2014, an increase of €16 million compared with 2013. This trend is linked to the increase in sales. The average trade receivable collection period was unchanged at 57 days’ sales. Trade payables decreased by €8.3 million to €147.7 million at December 31, 2014, down from €156 million for the previous year. The average trade payable settlement timeframe was 67 days, a decrease of 5 days compared with the end of 2013, which was primarily due to the increase in supplies from outside Europe.

Cash flow (in euro thousands) 2014 2013

Operating cash flow before change in WCR 52,688 25,097

Change in working capital (64,577) (4,296)

Cash flow from operating activities (11,889) 20,801

Capital expenditure (14,249) (14,845)

Asset disposals 533 819

Impact of acquisitions (9,212) (14,208)

Dividends paid to shareholders of Jacquet Metal Service S.A. (13,978) (13,947)

Interest paid (6,865) (5,563)

Other movements (3,386) (596)

Change in net debt (59,046) (27,539)

Net debt brought forward 78,265 50,726

Net debt carried forward 137,311 78,265

The Group’s net debt amounted to €137.3 million. The Group’s Operating cash flow before change in WCR amounted to €52.7 million in 2014, compared with €25.1 million in the previous year. Group capital expenditure amounted to €14.2 million in 2014, which primarily corresponded to new finishing and cutting capacity and the acquisition of ROLARK Group resulted in a €9.2 million increase in debt at December 31, 2014.

Development Brand development consists mainly in opening new service centers in order to cover new geographical regions. The average investment for a warehouse is around €3 million, two-thirds of which corresponds to inventories. Given the nature of its business, i.e. the distribution of specialty steels, capital expenditure primarily involves buildings and finishing capacity (cutting and folding machines, etc.). This development model requires relatively little capital outlay and is implemented at a rate adapted to the economic conditions encountered. It is also low-risk, since inventories and machineries can be rapidly used by other brand warehouses in the event that a service center has a low return on investment. Given the nature of its business, Jacquet Metal Service Group is not required to invest in research and development.

Subsequent events None.

>

2014 FINANCIAL REPORT MANAGEMENT REPORT – INFORMATION ON THE GROUP

30

1.6 Staff information The Group’s headcount at December 31, 2014 was 2,413 (full-time equivalent) employees compared with 2,277 at December 31, 2013.

2014 2013

Full-time equivalent at closing date 2,413 2,277

Average headcount 2,398 2,262

France 519 491

Other countries 1,879 1,771

The Group complies with local statutory working time requirements in accordance with the legislation of each country in which it operates.

1.7. Risk factors The Company's management has reviewed the risks that could have a material adverse impact on its business, financial position or income (or on its ability to meet its targets) and believes that there are no significant risks other than those set out below. Once a quarter, the Group’s senior management meets the brand Chief Operating Officers. The primary purpose of these meetings is to review results, monitor targets, identify growth opportunities and survey risks. This survey is supplemented by a half-yearly report on the risks identified by the subsidiaries. The main risk areas identified relate to:

- The economic environment: change in third parties’ attitudes, changes in prices, especially the prices of raw materials, and market trends;

- Operations: strategic monitoring, choice of acquisitions and their successful integration, business continuity in the event of a crisis and the effectiveness of control processes;

- Human resources: motivation and loyalty of employees, reliance of the Group or its subsidiaries on specific senior executives and key personnel;

- Support functions: performance and adjustments to the IT systems and tools for measuring financial performance.

Risks other than those identified above may exist. Either they have not been identified to date, or their occurrence is not considered likely to have a material adverse impact on the Group.

1.7.1. Risks relating to the Group’s operations 1.7.1.1. IT system risk

All the companies belonging to the JACQUET and Abraservice brands only use the Integrated Management Program (IMP) historically developed by Jacquet Metal Service. This program includes a business application and a localized accounting solution. These centralized tools are one of the keys to effective and responsive financial control. The migration of the Stappert brand to this information system is currently underway, while that of IMS group is scheduled for a later date. Jacquet Metal Service protects its IT architecture against risks of outage or disaster by using several IT rooms. Every item of equipment is installed in two separate inter-connected rooms, enabling ongoing real-time data duplication in both locations. The production rooms are hosted in data centers that provide a high level of service and access security, as well as broadband Internet access.

31

1.7.1.2. Procurement risk

The nature of Jacquet Metal Service’s business guarantees the Company’s independence in terms of any specific supply contract. This strategy is reflected in a diversified procurement policy and a stringent supplier selection process specifically aimed at avoiding dependence on one or more suppliers. 1.7.1.3. Distribution risk

Jacquet Metal Service primarily distributes its products via intermediaries and second-tier distributors, which makes it impossible to monitor the final destination of the products. 1.7.1.4. Risk of industrial accidents

The Group considers that it complies with applicable safety rules and statutory provisions in each country. However, the measures adopted do not provide complete assurance that no industrial accident will occur.

1.7.2. Market risk 1.7.2.1. Country risk

The Group generates over 90% of its sales in Europe and primarily operates in countries that are members of the European Union or are considered to be politically stable. The country risk is therefore considered to be low. 1.7.2.2. Purchase price elasticity risk Purchase prices of stainless steels (JACQUET and Stappert) usually consist of two separate components:

- the base price, which is the outcome of negotiations at the time when the order is placed with each producer; and

- a more variable portion, which depends on the trend in raw material prices. This includes, for example, the scrap surcharge for engineering steels or the alloy surcharge for stainless steels. The alloy surcharge is usually determined at the time of delivery, in accordance with a calculation formula specific to each producer, which factors in the cost of nickel, chromium, titanium, molybdenum and scrap metal, the euro-US dollar exchange rate, etc.

Furthermore, delivery lead times are a major parameter for determining prices. In fact, they are usually not adhered to, and generally range between 1 and 12 months. Given the fluctuations in raw material prices that affect the value chain, purchase prices may be subject to adjustment clauses depending on compliance with delivery lead times. Some agreements may also provide for the final price to be adjusted depending on the actual delivery date, rather than on the theoretical date, while the base price may be revised retroactively by the producer, etc. Lastly, annual price reductions may be provided for in accordance with the volumes purchased and the producer’s overall performance. The Group's gross margin as a percentage of sales varies in accordance with the following factors:

- Changes in the business mix (relative contributions of brands to sales, in view of differences between individual brand margin rates);

- The price levels in absolute value terms; - The impact of price changes on inventory rundown.

Accordingly, Group policy and industry practice tend to pass on any purchase price increases that occur directly to customers, with immediate effect if possible. Conversely, if prices decrease, the Group’s competitive positioning requires it to pass on these price decreases within variable timeframes. The option whether to pass on price increases and decreases results in an inventory price effect and a gross margin effect.

>

2014 FINANCIAL REPORT MANAGEMENT REPORT – INFORMATION ON THE GROUP

32

Changes in base steel prices and in the prices of certain metals used in alloys (nickel, molybdenum, chromium etc.) also impact the gross margin as a percentage of revenues. 1.7.2.3. Risk of changes in metal prices

The Group does not use any financial instruments to hedge fluctuations in the price of the raw materials used as components in the steels that it markets. In the case of some of the metals used (especially molybdenum and chromium), this is due to the lack of a market allowing such a hedging process. In the case of nickel, the lack of hedging is a management decision, as the Group currently considers that such a policy would not necessarily be effective and could even be financially counter-productive, as the related costs may be higher than the profits likely to result. The advisability of implementing such a hedging policy is the subject of periodic reviews. To date, the policy has been to remain exposed to fluctuations in metal prices. The Group is not able to provide relevant and reliable quantified information regarding the elasticity and sensitivity of prices and margins, due to the large number of factors taken into account when setting raw material purchase prices and sale prices.

1.7.2.4. Currency risk

The subsidiaries' raw material purchases are mainly carried out in euros, given the Group’s geographical locations. Accordingly, the Group’s exposure to currency risk primarily concerns purchases in euros made by subsidiaries based outside the euro zone, while other cash flows are expressed in the functional currency of each subsidiary. Jacquet Metal Service S.A. is exposed to currency risk when it grants cash advances in local currencies to subsidiaries outside the euro zone. An assessment of currency risk is set out in Section 4.16.3 of the Notes to the 2014 consolidated financial statements. 1.7.2.5. Interest rate risk

Cash investments primarily consist of term deposits, where the interest-rate risk is limited. Exposure to interest-rate risk primarily relates to the floating-rate debt, which is partly hedged via hedging instruments. An assessment of these risks is set out in Section 4.16.3 of the Notes to the 2014 consolidated financial statements. 1.7.2.6. Liquidity risk

Some loans are subject to compliance with covenants. As explained in Section 5.4 of the Notes to the 2014 consolidated financial statements, such clauses were not applicable at December 31, 2014. The Group has carried out a specific review of its liquidity risk and considers that it is able to meet its future liabilities as they fall due. An assessment of liquidity risk is set out in Section 4.16.3 of the Notes to the 2014 consolidated financial statements. 1.7.2.7. Credit and counterparty risk

The Group's exposure to credit and counterparty risk primarily relates to uninsured trade receivables. The Group is not in a position of commercial dependence on its customers. Moreover, the Group is not dependent on a specific supplier and only uses sub-contractors on an occasional basis. An assessment of these risks is set out in Section 4.16.3 of the Notes to the 2014 consolidated financial statements.

33

1.7.2.8. Equity risk

Jacquet Metal Service S.A. does not hold a share portfolio, except for its treasury shares. The Group held 364,886 treasury shares at December 31, 2014, which represented 1.52% of the share capital and a net value of €5.1 million. A 10% fall in the Jacquet Metal Service share price would result in a €0.5 million decrease in Jacquet Metal Service S.A.’s net financial income. However, any change in Jacquet Metal Service’s share price would have no impact on the Group’s consolidated net income and consolidated shareholders’ equity, as the treasury shares are eliminated from the consolidated shareholders’ equity and any potential impact on net income is neutralized.

1.7.3. Legal risk There are no pending or imminent government, judicial or arbitration proceedings, including any proceedings of which the Company is aware, likely to have a material impact on the Company’s and/or Group's financial position or profitability. Neither have any such proceedings had such an impact over the past 12 months.

1.7.4. Patents The Company does not depend on patents to carry out its business activities.

1.7.5. Sub-contracting There is no dependence on sub-contractors.

1.7.6. Insurance and risk coverage In the case of operational risks, each Jacquet Metal Service Group subsidiary has a risk coverage suited to its operations, through insurance policies taken out locally or by the Group and covering all potential risks, such as:

- Property damage and consequential operating losses; - The liability of corporate officers and directors; - General third-party liability: the Group has taken out a master policy with AIG covering the

consequences of the Company’s and its subsidiaries’ liability for damage caused to third parties up to an amount of €25 million per claim for all types of damage combined, subject to the specific limits per type of risk provided for in the policy.

The Company believes that its insurance cover complies with French and European professional third-party liability insurance standards and is sufficiently broad to cover the standard risks inherent to its operations. However, it cannot guarantee that these policies will cover all the claims that the Group may face. No material potential risk where the consequences were not already included in the 2014 financial statements had been identified at December 31, 2014.

>

2014 FINANCIAL REPORT MANAGEMENT REPORT – INFORMATION ON THE GROUP

34

1.7.7. Environmental risk Given that its operations involve distribution and processing prior to delivery, Jacquet Metal Service does not incur any material environmental risk. In fact, Jacquet Metal Service does not use any particularly hazardous substances and its operations do not have a material impact on the environment. However, further tightening of environmental and safety requirements cannot be ruled out in the future. Furthermore, some of the facilities used by the Group companies have a long industrial history. Accordingly, the Group could be held liable for any pollution, including legacy pollution, identified at facilities currently or previously used by the Group. To date, Jacquet Metal Service has not been informed of any environmental constraints likely to affect the Group’s use of its property, plant and equipment.

35

2. MANAGEMENT REPORT - INFORMATION ON THE JACQUET

METAL SERVICE S.A. PARENT COMPANY Jacquet Metal Service S.A., hereinafter the “Company”, holds equity interests in the Group subsidiaries on a direct or indirect basis. Its main functions are as follows:

- Defining the Group’s strategy and coordinating its development; - Developing and maintaining the information systems; - Controlling, coordinating and negotiating purchasing terms and conditions; - Financial audits, financing management, financial communications and investor relations; - Corporate communications.

The Jacquet Metal Service S.A. financial statements for the year ended December 31, 2014 were prepared in accordance with French statutory requirements and in accordance with the same accounting principles and policies as those applied in the preparation of the previous year's financial statements, except where pension obligations are concerned: Pursuant to the initial application of ANC Recommendation 2013 R02 dated November 7, 2013, Jacquet Metal Service SA has chosen to record for all pensions plans, all aggregate actuarial differences and costs of past unamortized services directly under “retained earnings” as from the beginning of the financial year for all of its pension schemes. The impact is an k€866 increase in provisions, which is offset by a decrease in shareholders’ equity.

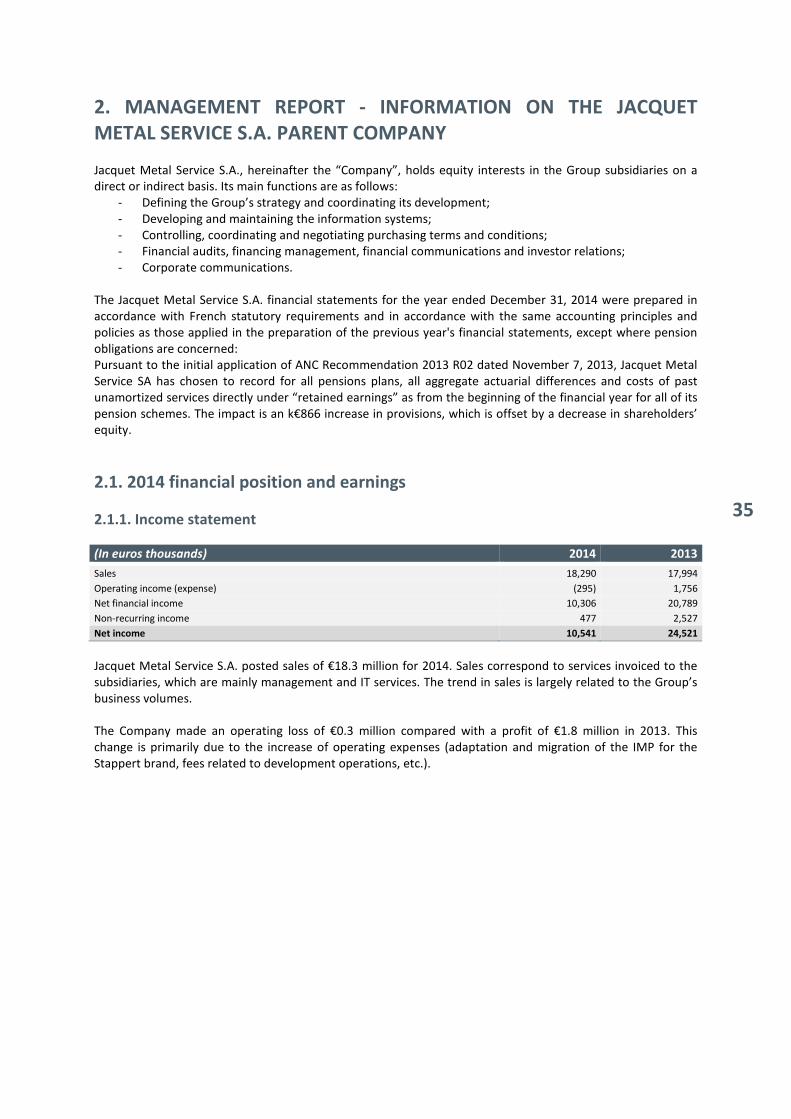

2.1. 2014 financial position and earnings

2.1.1. Income statement

(In euros thousands) 2014 2013

Sales 18,290 17,994

Operating income (expense) (295) 1,756

Net financial income 10,306 20,789

Non-recurring income 477 2,527

Net income 10,541 24,521

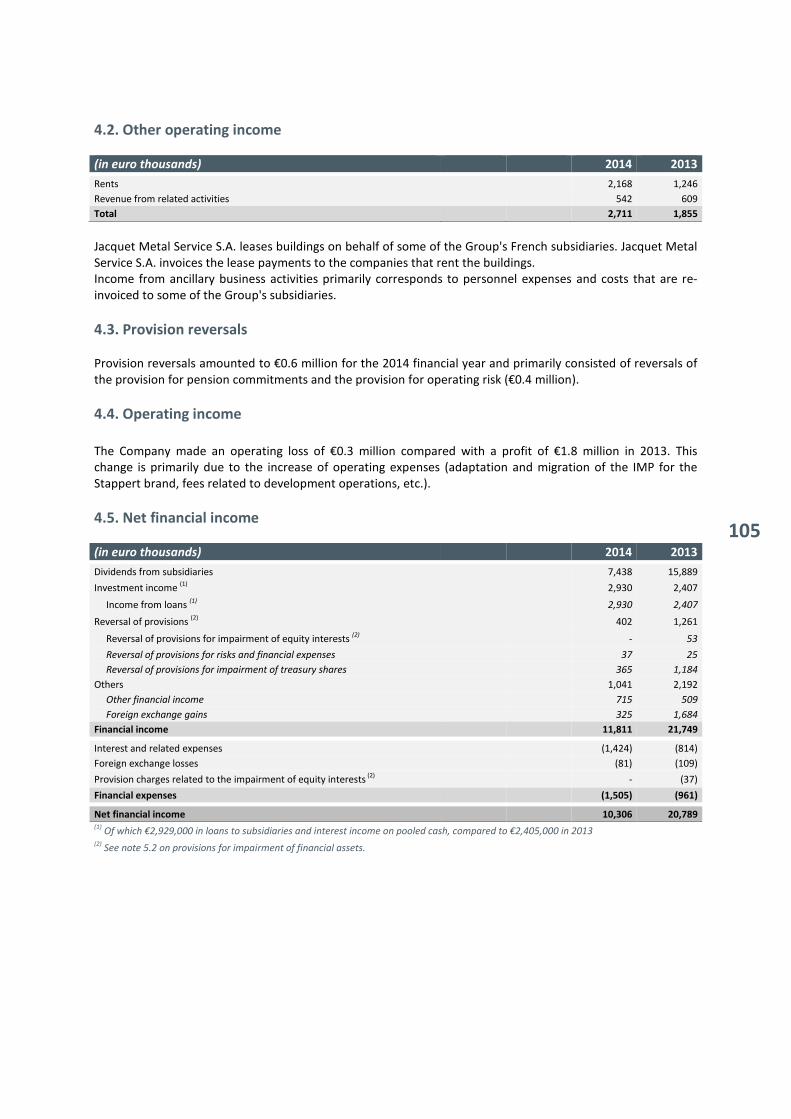

Jacquet Metal Service S.A. posted sales of €18.3 million for 2014. Sales correspond to services invoiced to the subsidiaries, which are mainly management and IT services. The trend in sales is largely related to the Group’s business volumes. The Company made an operating loss of €0.3 million compared with a profit of €1.8 million in 2013. This change is primarily due to the increase of operating expenses (adaptation and migration of the IMP for the Stappert brand, fees related to development operations, etc.).

>

2014 FINANCIAL REPORT MANAGEMENT REPORT – INFORMATION ON THE PARENT COMPANY

JACQUET METAL SERVICE S.A.

36

Financial income amounted to €10.3 million, broken down as follows:

(In euros thousands) 2014 2013

Dividends from subsidiaries 7,438 15,889

Income from investments 982 876

Provision reversals (2) 402 1,261

Other 2,989 3,723

Financial income 11,811 21,749

Interest and related expenses (1) (1,424) (814)

Provision charges (2) - (37)

Other (81) (109)

Financial expenses (1,505) (961)

Net financial income 10,306 20,789 (1)

Including interest on interest-rate swaps

(2) See analysis of financial assets in paragraph 2.1.2.

Non-recurring income (+€477 thousands) primarily consisted of gains on the disposal of treasury shares as part of the liquidity contract and the reversal of accelerated amortization and depreciation.

2.1.2. Statement of financial position

(In euros thousands) Dec. 31, 2014 Dec. 31, 2013

Financial assets 207,705 204,397

Intangible assets and PP&E 2,431 2,143

Cash and cash equivalents 25,243 23,234

Other assets 115,643 80,685

Total assets 351,023 310,459

Shareholders’ equity 211,862 216,351

Debt 117,033 75,670

Other liabilities 22,128 18,438

Total equity and liabilities 351,023 310,459

Financial assets