Embed Size (px)

Citation preview

2013 ANNUAL REPORT

HYUNDAI MARINE&FIREINSURANCE

Hyundai Marine & Fire Insurance Co., Ltd.163 Sejong-daero, Jongno-gu, Seoul, Korea | Tel: (82)1588-5656 | www.hi.co.kr

HYU

ND

AI IN

SUR

AN

CE 2013 ANN

UAL R

EPO

RT

HYU

ND

AI M

AR

INE

&FIR

E INSU

RA

NCE 2013 AN

NU

AL REP

OR

T

03Hyundai Marine & Fire Insurance

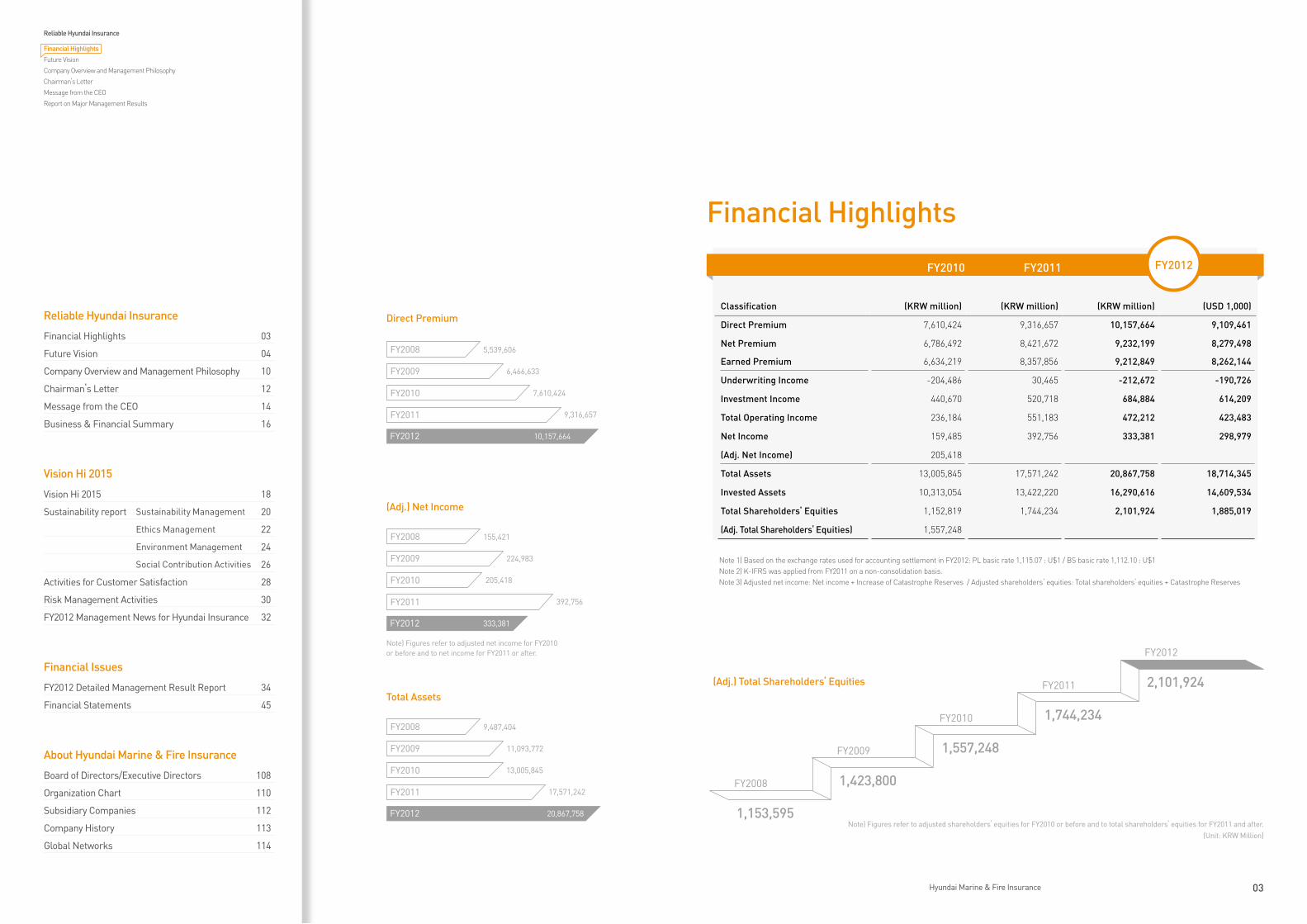

(Adj.) Total Shareholders’ Equities

FY2008

FY2012

FY2011

FY2009

FY2010

1,153,595

2,101,924

1,744,234

1,423,800

1,557,248

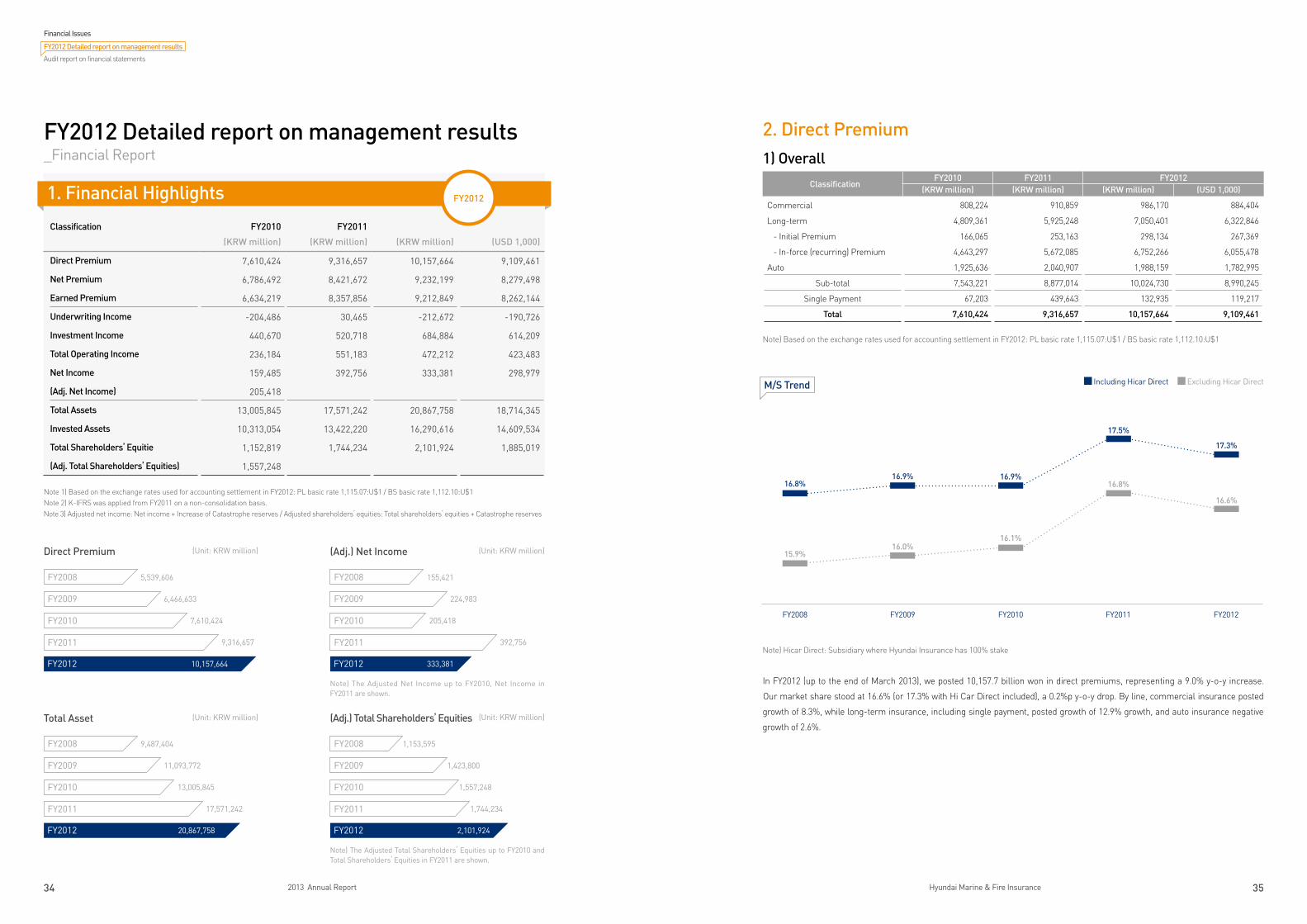

Financial Highlights

FY2010 FY2011

Classification (KRW million) (KRW million) (KRW million) (USD 1,000)

Direct Premium 7,610,424 9,316,657 10,157,664 9,109,461

Net Premium 6,786,492 8,421,672 9,232,199 8,279,498

Earned Premium 6,634,219 8,357,856 9,212,849 8,262,144

Underwriting Income -204,486 30,465 -212,672 -190,726

Investment Income 440,670 520,718 684,884 614,209

Total Operating Income 236,184 551,183 472,212 423,483

Net Income 159,485 392,756 333,381 298,979

(Adj. Net Income) 205,418

Total Assets 13,005,845 17,571,242 20,867,758 18,714,345

Invested Assets 10,313,054 13,422,220 16,290,616 14,609,534

Total Shareholders’ Equities 1,152,819 1,744,234 2,101,924 1,885,019

(Adj. Total Shareholders’ Equities) 1,557,248

FY2012

(Unit: KRW Million)Note) Figures refer to adjusted shareholders’ equities for FY2010 or before and to total shareholders’ equities for FY2011 and after.

Note 1) Based on the exchange rates used for accounting settlement in FY2012: PL basic rate 1,115.07 : U$1 / BS basic rate 1,112.10 : U$1Note 2) K-IFRS was applied from FY2011 on a non-consolidation basis.Note 3) Adjusted net income: Net income + Increase of Catastrophe Reserves / Adjusted shareholders’ equities: Total shareholders’ equities + Catastrophe Reserves

Direct Premium

FY2008

FY2009

FY2010

FY2011

FY2012

5,539,606

6,466,633

7,610,424

9,316,657

10,157,664

Total Assets

FY2008

FY2009

FY2010

FY2011

FY2012

9,487,404

11,093,772

13,005,845

17,571,242

20,867,758

(Adj.) Net Income

FY2008

FY2009

FY2010

FY2011

FY2012

155,421

224,983

205,418

392,756

333,381

Note) Figures refer to adjusted net income for FY2010 or before and to net income for FY2011 or after.

Reliable Hyundai Insurance

Financial Highlights 03

Future Vision 04

Company Overview and Management Philosophy 10

Chairman’s Letter 12

Message from the CEO 14

Business & Financial Summary 16

Vision Hi 2015

Vision Hi 2015 18

Sustainability report Sustainability Management 20

Ethics Management 22

Environment Management 24

Social Contribution Activities 26

Activities for Customer Satisfaction 28

Risk Management Activities 30

FY2012 Management News for Hyundai Insurance 32

Financial Issues

FY2012 Detailed Management Result Report 34

Financial Statements 45

About Hyundai Marine & Fire Insurance

Board of Directors/Executive Directors 108

Organization Chart 110

Subsidiary Companies 112

Company History 113

Global Networks 114

Reliable Hyundai Insurance

Financial Highlights

Future Vision

Company Overview and Management Philosophy

Chairman’s Letter

Message from the CEO

Report on Major Management Results

04 2013 Annual Report 05Hyundai Marine & Fire Insurance

Righteous management

The leading insurance company creating best service for customers by righteous management. We always follow the right path and strive to grow with our customers by providing them with a first-rate service.

We trust in following the right path and believe that it is the best way to repay our customers

for putting their trust in us. We have built up a solid tradition of excellence since our

establishment in 1955 and are refreshing our resolve to provide satisfactory services to all

our customers for the next 100 years based on such a tradition.

Reliable Hyundai Insurance

Financial Highlights

Future Vision

Company Overview and Management Philosophy

Chairman’s Letter

Message from the CEO

Report on Major Management Results

06 2013 Annual Report 07Hyundai Marine & Fire Insurance

Customer satisfaction

Customers’ trust and satisfaction – Our most valuable assets

Hyundai Marine & Fire Insurance will always act as your trusted partner for life.

We conduct first-rate management that leave our customers satisfied by developing

creative products suited to customers’ needs, planning exemplary insurance aimed at

securing our customers a prosperous future, and providing positive and differentiated

compensation.

Reliable Hyundai Insurance

Financial Highlights

Future Vision

Company Overview and Management Philosophy

Chairman’s Letter

Message from the CEO

Report on Major Management Results

08 2013 Annual Report 09Hyundai Marine & Fire Insurance

Hyundai Insurance leads hope with hearty challenge for a better tomorrow! We at Hyundai Marine & Fire Insurance do all we can to give hope to the less privileged.

We engage in social contribution activities to repay our customers for putting their trust

in us. We return a given portion of our profit to the community in an effort to build a

society where everyone is happy. Hyundai Insurance dreams of a respectable company

stepping forward for the happy future – That is how we envision ourselves.

Social contribution

Reliable Hyundai Insurance

Financial Highlights

Future Vision

Company Overview and Management Philosophy

Chairman’s Letter

Message from the CEO

Report on Major Management Results

10 2013 Annual Report 11Hyundai Marine & Fire Insurance

Since the company’s establishment in 1955 as the country’s first company dedicated to marine insurance, we have grown into

a leader in the non-life insurance industry. We have been able to accomplish such a feat through indomitable earnestness,

creative will, a daring spirit of challenge, and our customers’ trust. We regard customer satisfaction as our highest value and

have always striven to realize our customers’ happiness. We aim to be a world-class insurance company that grows with its

customers based on our solid tradition of excellence. We will help build a hopeful future by contributing to society.

Management PhilosophyWe will play a leading role in the financial industry with creativity and powerful driving force, place priority on customers’

satisfaction, and contribute to the making of a more affluent society and the development of the national economy.

Enterprising Spirit of Challenge

Unwavering Love of Customers

Fervent Passion

Creative Will

Hyundai Marine& Fire Insurance

Leading Korean Non-life Insurance Industry

Reliable Hyundai Insurance

Financial Highlights

Future Vision

Company Overview and Management Philosophy

Chairman’s Letter

Message from the CEO

Report on Major Management Results

12 2013 Annual Report 13Hyundai Marine & Fire Insurance

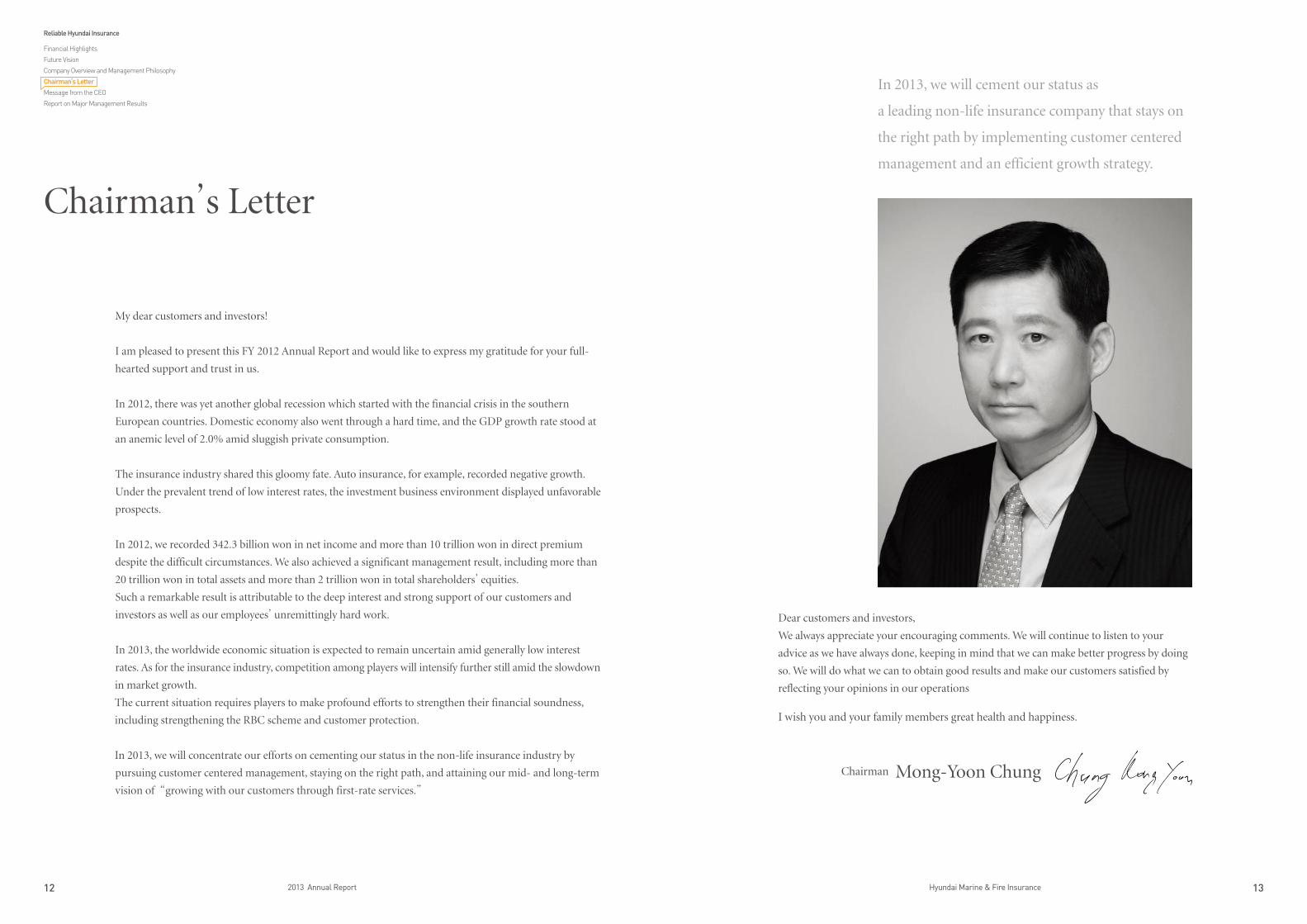

Chairman’s Letter

My dear customers and investors!

I am pleased to present this FY 2012 Annual Report and would like to express my gratitude for your full-

hearted support and trust in us.

In 2012, there was yet another global recession which started with the financial crisis in the southern

European countries. Domestic economy also went through a hard time, and the GDP growth rate stood at

an anemic level of 2.0% amid sluggish private consumption.

The insurance industry shared this gloomy fate. Auto insurance, for example, recorded negative growth.

Under the prevalent trend of low interest rates, the investment business environment displayed unfavorable

prospects.

In 2012, we recorded 342.3 billion won in net income and more than 10 trillion won in direct premium

despite the difficult circumstances. We also achieved a significant management result, including more than

20 trillion won in total assets and more than 2 trillion won in total shareholders’ equities.

Such a remarkable result is attributable to the deep interest and strong support of our customers and

investors as well as our employees’ unremittingly hard work.

In 2013, the worldwide economic situation is expected to remain uncertain amid generally low interest

rates. As for the insurance industry, competition among players will intensify further still amid the slowdown

in market growth.

The current situation requires players to make profound efforts to strengthen their financial soundness,

including strengthening the RBC scheme and customer protection.

In 2013, we will concentrate our efforts on cementing our status in the non-life insurance industry by

pursuing customer centered management, staying on the right path, and attaining our mid- and long-term

vision of “growing with our customers through first-rate services.”

Dear customers and investors,

We always appreciate your encouraging comments. We will continue to listen to your

advice as we have always done, keeping in mind that we can make better progress by doing

so. We will do what we can to obtain good results and make our customers satisfied by

reflecting your opinions in our operations

I wish you and your family members great health and happiness.

Chairman Mong-Yoon Chung

In 2013, we will cement our status as

a leading non-life insurance company that stays on

the right path by implementing customer centered

management and an efficient growth strategy.

Reliable Hyundai Insurance

Financial Highlights

Future Vision

Company Overview and Management Philosophy

Chairman’s Letter

Message from the CEO

Report on Major Management Results

14 2013 Annual Report 15Hyundai Marine & Fire Insurance

Dear customers and investors, We expect to see diverse changes in FY2013.

Uncertainty both in and out of the country will continue to prevail amid

the southern European financial crisis and the economic slowdown of the

United States and China. Low growth and low interest rates will continue

for the time being. It appears that we should take preemptive steps in

conjunction with forthcoming changes in the relevant systems, such as

reducing customer complaints and strengthening the RBC scheme.

To deal with such changes, we will adopt the three following management

guidelines in 2013:

First, we will carry out business based on principle and rules.

Second, we will strengthen our sales capability with the focus on efficiency

and profit. We will ensure that a profit-oriented sales structure takes root.

We will also strive to execute distribution expenses and run the organization

more efficiently.

Third, we will push ahead with the innovation of products and services in

a customer centered way. We will continue to establish a more convenient

business process for customers and enhance the level of customers’

satisfaction with differentiated products and our claims service.

Please rest assured that we will do our best to obtain better management

results by carrying out the said management guidelines thoroughly in 2013.

Thank you.

CEO Message

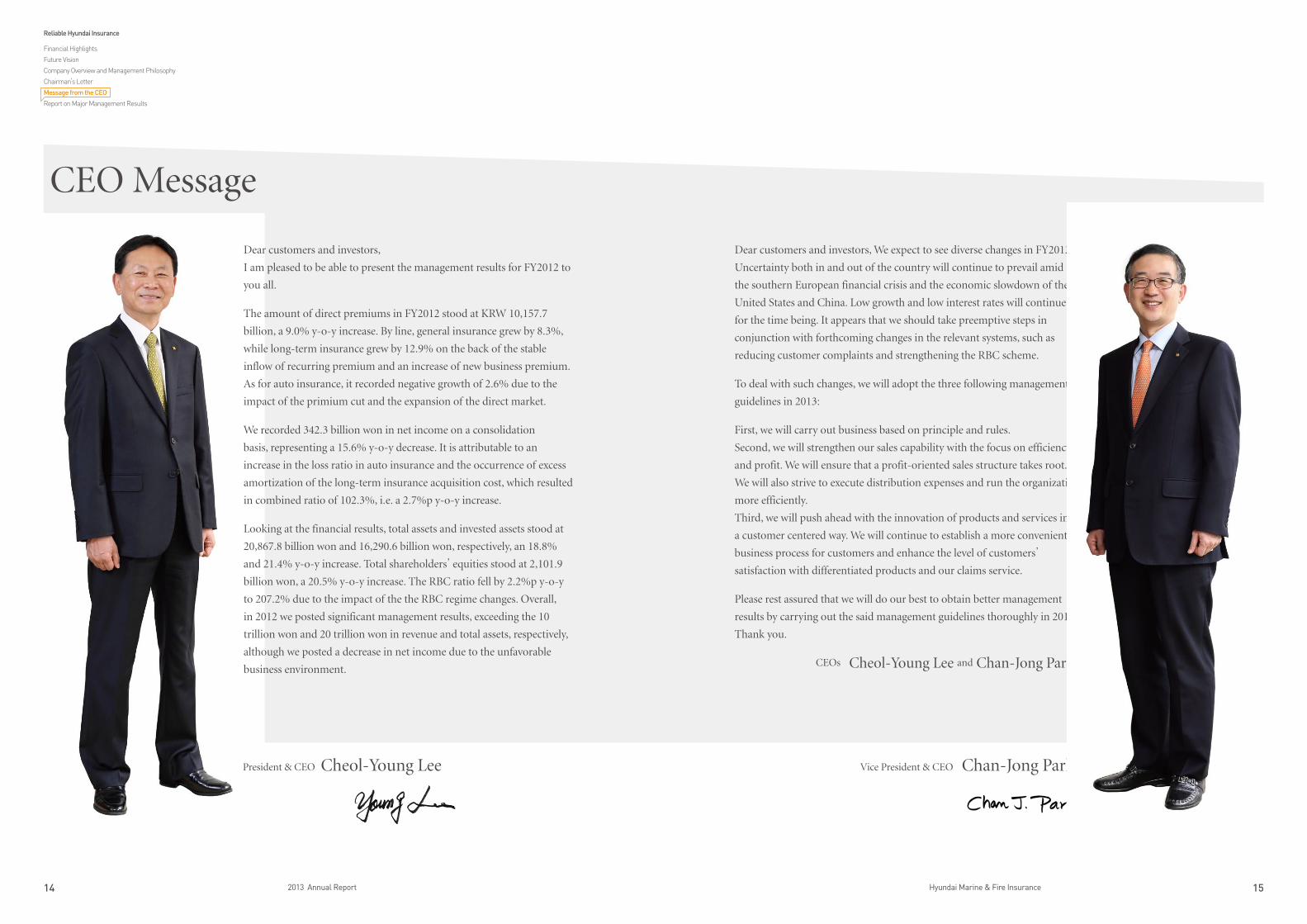

Dear customers and investors,

I am pleased to be able to present the management results for FY2012 to

you all.

The amount of direct premiums in FY2012 stood at KRW 10,157.7

billion, a 9.0% y-o-y increase. By line, general insurance grew by 8.3%,

while long-term insurance grew by 12.9% on the back of the stable

inflow of recurring premium and an increase of new business premium.

As for auto insurance, it recorded negative growth of 2.6% due to the

impact of the primium cut and the expansion of the direct market.

We recorded 342.3 billion won in net income on a consolidation

basis, representing a 15.6% y-o-y decrease. It is attributable to an

increase in the loss ratio in auto insurance and the occurrence of excess

amortization of the long-term insurance acquisition cost, which resulted

in combined ratio of 102.3%, i.e. a 2.7%p y-o-y increase.

Looking at the financial results, total assets and invested assets stood at

20,867.8 billion won and 16,290.6 billion won, respectively, an 18.8%

and 21.4% y-o-y increase. Total shareholders’ equities stood at 2,101.9

billion won, a 20.5% y-o-y increase. The RBC ratio fell by 2.2%p y-o-y

to 207.2% due to the impact of the the RBC regime changes. Overall,

in 2012 we posted significant management results, exceeding the 10

trillion won and 20 trillion won in revenue and total assets, respectively,

although we posted a decrease in net income due to the unfavorable

business environment.CEOs Cheol-Young Lee and Chan-Jong Park

Vice President & CEO Chan-Jong ParkPresident & CEO Cheol-Young Lee

Reliable Hyundai Insurance

Financial Highlights

Future Vision

Company Overview and Management Philosophy

Chairman’s Letter

Message from the CEO

Report on Major Management Results

16 2013 Annual Report 17Hyundai Marine & Fire Insurance

Business & Financial Summary

In FY2012, the non-life insurance industry collected direct premium of about KRW 63 trillion with growth of

about 12% compared to the previous year. Commercial insurance grew 12%, thanks to a consistent increase

of group accident insurance and casualty insurance. As for auto insurance, it recorded negative growth of

1.5% due to the impact of a premium cut and the expansion of the online market. Long-term insurance

posted robust y-o-y growth of 17% on the back of a strong rise of the initial premium, particularly in the

healthcare types amid a stable inflow of recurring premiums.

Looking at our performance in 2012, we posted 10,157.7 billion won in direct premiums, showing a 9.0%

y-o-y increase, with long-term insurance playing a central role. By line, we recorded an 8.3% y-o-y increase

in general insurance as a result of positive efforts made to attract new customers. Auto insurance recorded

negative growth of 2.6%.

We posted a monthly average of initial premium of 24.8 billion won, a 17.8% y-o-y increase and 16 billion

won in monthly converted new business premiums, a 3.7% increase over the preceding year. As for

recurring premiums, we posted 6,752.3 billion won, a 19% y-o-y increase, as a result of our efforts to

improve the persistency rate. In long-term healthcare type insurance with a high profit margin , we recorded

a 41.7% y-o-y increase in terms of monthly converted average initial premiums with 45.3% of proportion in

our long-term portfolio. As regards profit and loss, we recorded a combined ratio of 102.3% with a loss of

212.7 billion won in the underwriting. The loss is attributable to the expense ratio of 19.2%, a 1.8%p y-o-y

increase, associated with an excess amortization of the long-term insurance acquisition cost.

As regards the loss ratio, we posted 83.1%, a 0.9%p y-o-y increase. In general insurance, our loss ratio

stood at 69.8% due to various factors including claims caused by typhoon and other natural disasters. In

auto insurance, our loss ratio stood at 83.4%, i.e.a 2.7%p y-o-y increase, which resulted from a decrease

in per-unit earned premiums associated with premium cut and heavy snow. For long-term insurance, our

loss ratio stood at 83.7%, showing a modest increase over the preceding year, due to an increase in the risk

loss ratio

In the investment sector, we maintained the level of 77% concerning the composition ratio of interest-

bearing assets in invested assets. We held on to the investment strategy of putting priority on risk

management by minimizing risky assets. As of the end of March 2013, our invested assets stood at 16,290.6

billion won, i.e. an increase of 3 trillion won over the same period of the preceding year. In investment

income, we posted 684.9 billion won, which was mainly attributable to an increase in gain on the valuation/

disposition of marketable securities. We also posted a 4.7% return on investment.

As a result of the aforesaid, we posted 342.3 billion won in net profit on a consolidation basis (or 333.4 billion

won on a separate basis) and 19% in ROE. We recorded 2,101.9 billion won in total shareholders’ equities.

As for the RBC ratio, we recorded 207.2%, i.e. a 2.2%p decrease, due to the strengthening of the RBC

scheme.

We accredited the credit rating of “A stable,” an upgrade from the “A-Positive” of the preceding year, from

A.M. Best, a world-class credit rating agency specializing in insurance businesses, apparently in recognition

of the continuous improvements we have made in terms of business performance, our investment strategy’

s focus on risk management and a sufficient solvency margin.

Most observers predict that the world economic environment will remain uncertain in 2013. Insurance

industry is in a difficult situation due to the forthcoming change in the RBC scheme which is designed

to strengthen the qualitative aspect of capital and reduce the customer complaints. Under such

circumstances, we at Hyundai Marine & Fire Insurance will deal with such changes with maintaining

enthusiastic attitude and differentiated competitiveness in business, and set up effective strategies to boost

profitability and growth at the same time.

In FY2012, the non-life insurance industry posted direct premium of about KRW 63 trillion with growth of about 12% compared to the

previous year. Commercial insurance grew 12%, thanks to a consistent increase of group accident insurance and casualty insurance. As

for auto insurance, it recorded negative growth of 1.5% due to the impact of a drop in the premium rate and the expansion of the online

market. Non-life insurance posted robust y-o-y growth of 17% on the back of a strong rise in the number of new contracts, particularly

those in personal insurance amid a stable inflow of recurring premiums.

Reliable Hyundai Insurance

Financial Highlights

Future Vision

Company Overview and Management Philosophy

Chairman’s Letter

Message from the CEO

Report on Major Management Results

18 2013 Annual Report 19Hyundai Marine & Fire Insurance

VISION Hi 2015

To realize our new vision, Hyundai Insurance has chosen mid and long-term strategic tasks for each business division

in line with our 4 major management strategy directions and 12 key strategies.

Based on the momentum gathered through the promotion of 47 strategic measures in the preceding year, we selected and pushed

ahead with 45 strategic measures in 2012 in consideration of their importance and urgency among those to be promoted by each division

by 2015. We successfully concluded the one-year-long FY2012 mid- and long-term strategic measures, in which a total of 200-plus

employees took part, through the kickoff in April 2012, interim checks and progress appraisals, and the final report session in March

2013.

The ongoing mid- and long-term strategic measures, which were implemented for successful accomplishment of the company’s Vision

Hi 2015, may reap good results thanks to the positive efforts made by the relevant director and project members in 2012, the second year

of the project, despite the many difficulties, including rapidly changing external conditions. We will continue to push forward with these

measures, positively using our accumulated know-how and reflecting changes in the relevant environment.

We shall bolster basic competitiveness as an insurer to achieve our “Vision Hi 2015” and become a ‘Leading insurance

company creating the best services for customers’ by concentrating all our capabilities on maximizing customer

values along with internally solid growth.

“The leading insurance company creating best service for customers”We at Hyundai Insurance established our mid and long-term vision, “Hi 2010, Insurer with Korea’s Top Competitiveness” and have been

doing our best in all sectors. As a result, we have grown remarkably in business revenue and other fields. Nonetheless, the future is

uncertain because of changes in the business environment including the saturation of the insurance market, entry of new insurers

into the insurance market, continuous sales channel diversification, and consumer protection consolidation trend. These present new

challenges and tasks that we must overcome.

We have established a new mid and long-term vision dubbed “Hi 2015,” proclaiming it both internally and externally in April 2011 to

proactively cope with the upcoming environmental changes and to continuously grow as a company. Under the newly adopted vision,

namely, “the leading insurance company creating best service for customers”, we will provide high-quality insurance products and

services, faithfully holding on to our role of contributing to customers’ happiness and social security as an insurance business, and

continuing to grow accordingly.

To that end, we have set the following mid-and long-term management strategies: strengthening core business competitiveness,

improving business infrastructure, maximizing customer value, and preparing new growth engines. Under these strategies, we will strive

to remain at the top in terms of overall sales, profitability, and competitiveness, push forward with business more efficiently, and continue

to provide services in a way that will enhance the quality of our customers’ lives. We will also strive to continue to grow by strengthening

the basis for new growth and overcoming the limitations of the insurance market.

12 key strategies to realize 4 major mid- and long-term management strategy directions

01 Development of products leading the market and consolidation of

UW/contract management competence

02 Bolstering sales competitiveness in the open-type,

multi-channel structure

03 Maintaining top-level claim competiveness in the industry

04 Consolidation of assets management competence to realize

long-term, stable investment returns

05 Establishment of Hyundai Insurance’s own new culture and

nurturing of talented people

06 Risk management competences strengthening suitable for

business portfolio and assets increase

07 IT infrastructure enhancement to make the business

process efficient

08 Consolidation of brand image to enhance customer trust

and loyalty

09 Enhancing of total customer services to offer values

beyond risk security

10 Reinforcing of social responsibility management as

the leading insurer

11 Boosting of global business on a step-by-step basis to

overcome the domestic market limitations

12 Consolidation of response to secure new growth opportunities

New Vision and Management Strategy of Hyundai Insurance

New Vision and Management Strategy

Vision Hi 2015

Report on Sustainability

Activities for Customer Satisfaction

Risk Management Activities

FY2012 Management News

20 2013 Annual Report 21Hyundai Marine & Fire Insurance

We place priority on customer satisfaction, fulfill our economic, social, and

environmental responsibilities toward stakeholders and the country, and pursue

balanced development among economic, social, and environmental aspects through

corporate activities and the creation of values. Our sustainable management is

focused on efforts to promote practical methods with a view to attaining our mid-

and long-term visions based on our management philosophy.

Sustainable management

strategy

Sustainability Management

First, we will focus on staying on the right path. As a business dedicated to ensuring security in the future, we stress

mid- and long-term risk management rather than short-term results, which

requires a sound ethical mindset and behavior on the part of our employees.

Second, we will put priority on the efficiency of our operation. Employees will be reminded to innovate themselves so as not to fall into the

trap of inefficiency and carelessness in order that the company will continue

to grow. This is also an effective way of enhancing shareholder value.

Third, customer satisfactions comes to our priority. The most basic element of sustainable management is to provide ultimate satisfaction

to customers, who are our most important stakeholders, and to develop diverse products

and services that reflect customers’ needs.

Fourth, win-win management comes next. A business takes root in the community and grows on the nutrition provided by it. A business can achieve

sustainable development when striving for joint prosperity with the community by adopting the latter as

an important stakeholder. Such an effort includes paying attention to our surroundings and providing

them with protective support.

Fifth, the management of human resources is no less important.It goes without saying that efforts should be made to strengthen employees’ capabilities in order for a

business to engage in creative management activities. Training talented employees with earnestness

and an ownership mindset is the most basic thing that a business must do.

System for promoting sustainable management

righteous management· Risk management

· Ethical management

Efficient management· Innovative management

· Shareholder value enhancement

Customer management· Customer satisfaction

Human resources management· Employees

· Hi planners

Win-win management· Partners

· Society

· Environment

VisionMid- and long-term

objectives

Management philosophy

A perpetual concept

Sustainable management

strategyConcrete methods

of execution

Righteousmanagement

Efficient management

Customer management

Win-win management

Human resources

management

For Tomorrow

Vision Hi 2015

Report on Sustainability Sustainability Management

Activities for Customer Satisfaction

Risk Management Activities

FY2012 Management News

Sustainability Report

22 2013 Annual Report 23Hyundai Marine & Fire Insurance

Sustainability Report

Ethics ManagementUnder the motto of ethical management, we carry out management activities in a way that engenders a sense of trust in our customers

and put customer satisfaction, which is a core element of our management philosophy, into practice through the transparent and fair

handling of business. We are committed to developing a corporate culture focusing on fair and free competition. Our business ethics

require that we provide customers and society with affluence and stability. We are building the base for sustainable management through

ethical management.

We have done our best to practice ethical management, fulfilling all our responsibilities and obligations toward customers, employees,

shareholders, subcontractors, country and society based on our Ethics Charter and Code of Conduct. Our Compliance Officer, appointed

by the Board of Directors, deals with matters relating to compliance and internal control so that our ethical management may be

conducted concretely and effectively.

Within the Company, matters relating to ethical management are controlled by the Compliance Department under the instructions of

the Compliance Officer, with a team composed of 139 compliance managers charged with carrying out matters relating to compliance-

related internal control activities.

Compliance programs ● Periodic campaigns are conducted for the continued promotion of ethical management.● Voluntary programs are adopted to ensure fair transactions with the aim of achieving effective management results through fair and free

competition. We observe the competition laws and execute self-regulated fair transaction rules under the control of the Compliance

Officer. We observe The Personal Information Protection Act by enacting the relevant in-house rules and carrying out activities for

checking and improving the relevant system under the control of the Compliance Officer. We have also established a system to prevent

money laundering involving through financial companies.● We regularly carry out company-wide activities relating to ethics, compliance, and accident prevention through ‘Hi-Compliance Day’

(a departmental-level internal control activity) events and operate a system for the evaluation of self-regulated internal control.● Each department is required to designate an employee in charge of compliance so that ethics and compliance-related matters may be

reflected properly in our overall operation. We also strive to enhance the level of employees’ awareness of ethical and compliance-related

issues through educational sessions.

Compliance and ethics management activities

Our Ethics Charter We at Hyundai Marine & Fire Insurance have set the criteria for ethical decision making and behavior as follows based on our

management philosophy and ethical management-related values and hereby resolve to put them into practice at all times:

● We shall deal with all our customers honestly, respect their opinions, put priority on customer satisfaction, and enhance

customer value.

● We shall disclose Company-related information to our shareholders transparently and fairly. We shall protect our shareholders’

rights and interests through sound management.

● We shall develop the corporate culture in such a way as to recognize human dignity and values based on mutual trust, and

adhere firmly to the basics and principles. ● We shall engage in fair and free competition with other businesses and conduct reasonable business transactions for mutual

development and coexistence.

● We shall provide abundance and stability to the community and contribute to the development of society and the country’s

economy by creating jobs and faithfully paying our taxes.

Trust of Hi

Vision Hi 2015

Report on Sustainability Ethics Management

Activities for Customer Satisfaction

Risk Management Activities

FY2012 Management News

24 2013 Annual Report 25Hyundai Marine & Fire Insurance

Green FinanceEnhancement of the company’s image as an eco-friendly business

As corporate that fulfills its social responsibilities, we make concerted efforts to draw attention to environmental issues, enhance our

image as an eco-friendly business, and establish our status as a business engaging in sustainable activities.

We develop and sell green insurance products to put environmental management into practice, while making diverse efforts to reduce

energy consumption in the name of low carbon, green growth. We operate the eco-Friendly Management Committee and the Hyundai

Insurance Research Center(HIRC) to carry out eco-friendly management positively and be better prepared against environmental risks

relating to climate change.

We are doing our best to save energy wherever possible. We manage energy use in an effort to minimize the environmental burden

occasioned by corporate activities, setting the indoor temperature of our buildings no higher than 20˚C in winter and taking part in the

campaign to reduce power consumption during peak hours. Every year, we distribute energy-saving guidelines throughout the Company

as a part of our participation in the nationwide energy-saving campaign in this era of high oil prices.

In July 2010, HIRC has established to

proactively cope with climate change by

recognizing it as both a risk and opportunity

simultaneously, as well as support

the company’s realization of its social

responsibilities and develop the insurance

industry through research regarding traffic

safety, a major area of non-life insurance

recently.

We started the climate information service

in December 2010 to help reduce safety or

traffic accidents caused by heavy rainfall,

blizzards or cold waves. The service

includes periodic provision of detailed

climate information to customer businesses

via e-mail and SMS-based provision of

information on inclement weather, such as

downpours, heavy snowfall or cold waves to

customers in the affected areas.

Our HIRC provides information on the

impending danger of flooding, using facilities

installed in areas frequently affected by

floods, on a real-time basis in an effort to

prevent accidents and minimize damages.

Environment Management

Weather Management CertificationContents : Certification concerning the creation of added value through diverse use

of weather information by a business (or institution) and ensuring safety

from adverse weather disasters.

Provider : KMA(Korea Meteorological Administration)

Validity of certification : October 26, 2012 - October 25, 2015 (for three years)

Green Finance

We obtained a weather management certification from the Korea Meteorological

Administration (KMA), the first of its kind awarded to a financial business, in

recognition of the aforementioned activities.

We also strive to contribute to society with the development of diverse products

and services designed to realize environmental management. We do what we can

to meet the demand for businesses’ positive environmental management and

meet customers’ eco-friendly service needs by offering Hi Life Power Eco Driver’s

Insurance, Hi Belief Bicycle Casualty Insurance, and storm and Flood Insurance.

We developed Hicar Eco Auto Insurance, a product utilizing used car parts, the

first of its kind adopted by an insurance business, and won an exclusive license for

it. We replaced the printed materials used for insurance contracts related to the

Hicar Green Service , such as the terms and conditions and insurance policy, with

e-mail and reflected the amount thus saved in the insurance premium charged to

customers.

As the first Korean insurance company to sign up to the UN Environmental Program

Financial Initiative (UNEP FI), we are carrying out environmentally-related activities,

including the dissemination of sustainable management. In 1995, we issued a

statement on the importance of environmental issues and the role of insurance

businesses in addressing them in Geneva.

In 2005, we became the first Korean insurance company to announce its support

for the Carbon Disclosure Project (CDP) and have since participated in the relevant

activities. In 2012, we announced our support for the CDP Water Disclosure and have

made efforts to contribute to programs related to climate change and environmental

preservation.

Vision Hi 2015

Report on Sustainability Environment Management

Activities for Customer Satisfaction

Risk Management Activities

FY2012 Management News

Sustainability Report

26 2013 Annual Report 27Hyundai Marine & Fire Insurance

Sustainability Report

Traffic/safety accident prevention activities We carry out activities aimed at protecting people from the kinds of accidents that can occur in everyday life.

[Hicar women drivers’ class] We run a class for novice women drivers, teaching them how to prevent traffic accidents and

park a car in a small space.

[Hi-Mom 119 class] This class aims to teach children how to avoid accidents in their everyday lives and how to act decisively

in moments of danger.

[Helping children avoid a traffic accident] We run a program aimed at teaching children how to get home safely without a

traffic accident after school. We provide a traffic safety map about the areas close to their school in an effort to help children

avoid traffic accidents. We also carry out other programs, such as the Children’s Traffic Safety Concert, which is designed to

raise awareness of the potential dangers posed by road traffic, particularly where children are concerned.

Support for future generations to follow the path of virtueWe work together with experts to assist young people and

tackle social issues relating to them through the following

programs:

[Very Minor Confessions] This program was set up to prevent

school violence through the invigoration of communication.

It comprises Confessions to Make, which is run online and

offline; a session in which celebrities are invited to discuss

school violence; and Healing Camp, which is designed to heal

victims of school violence or trauma. It is carried out with the

positive participation of students, teachers, and parents.

[T-um Class] This long-term program (a total of 16 sessions

have been conducted so far) aims to develop the personality

of children accommodated in special facilities with the help

of experts. The program helps young people to improve their

sense of pride and sociability and make a plan for a hopeful

future.

We share hope with neighborsWe do our best to help needy neighbors and build a better

future.

[Hi-Life voluntary activities / Disaster Aid Committee] The

Company encourages employees and Hi Planners to engage in

voluntary activities and provides support for their activities. Our

Hi-Life Volunteers, launched in 2005, carry out activities in more

than 30 facilities and national parks nationwide. We also operate

the Disaster Aid Committee to provide relief to the needy.

[Ashoka Support] Hyundai Marine & Fire Insurance is a

founding partner of Ashoka Korea, which is well known for its

discovery of and provision of support to social entrepreneurs.

We concur with Ashoka’s philosophy of pursuing a society in

which more and more people take the initiative with a view

to changing the world. We carry out activities as a partner of

Ashoka Korea based on the belief that our activities will bring

about positive changes in our society.

[Financial donations] Our employees voluntarily donate part

of their monthly salary to provide financial support for children

whose parent(s) have lost their lives in a traffic accident.

[Charity Bazaar] Every year our employees and Hi Planners

donate used articles and sell them at the Charity Bazaar. They

spend the proceeds on helping needy neighbors.

Heart Plus

Social Contribution Activities

Challenge for tomorrow We at Hyundai Marine & Fire Insurance pursue sustainable and shared growth and do our best to fulfill our social responsibilities. We make

a point of returning a given percentage of our profits to society so that all people may live a happier life. We expect that the actions we have

taken to help create a more humane society where people share happiness together will blossom into new hope.

Vision Hi 2015

Report on Sustainability Social Contribution Activities

Activities for Customer Satisfaction

Risk Management Activities

FY2012 Management News

28 2013 Annual Report 29Hyundai Marine & Fire Insurance

7 Heart Service01 Customer Satisfaction Service

02 Automobile Claims (Family Heart Service)

03 Long-Term Insurance Claims (Smart Heart Service)

04 Emergency Mobilizations (Plus Heart Service)

05 Emergency Claims (Speed Heart Service)

06 Call Center (Sense Heart Service)

07 Risk Management Service

Meticulous efforts on behalf of our customers In 1996, we became the first insurance business to announce the Customer Satisfaction Management Charter. Since then, our employees

and Hi Planners have made concerted efforts to deliver differentiated customer satisfaction management under the motto of “Hyundai

Marine & Fire Insurance, a company loved by customers for its first-rate service and humane approach.”

We have adopted the 7 Heart Service as our service identity in an effort to put the principle of better customer service into practice.

Under the said service identity, we do our best to convey our readiness to serve our customers at the seven leading contact points: auto

compensation, long-term compensation, coming to the client’s aid, rushing to the scene, call center, Hi Planners, and counters.

As a result of such efforts, our name was admitted to the Hall of Fame, the Korea Management Grand Prize in the category of customer

satisfaction management in 2012.

● Customer assurance SMS information service (information on receipt of report; fax number; employee in charge)● Customized service to inform the client of the end of indemnity (via SMS, location message service (LMS), post, email)● Fax receiving confirmation inquiry of sent document ● Real-time indemnity processing information system from homepage● Mobile-based information system on the real-time compensation handling process● Indemnity consulting on the Internet

04. Emergency Mobilization (Plus Heart Service)● Hicar service (emergency mobilization and vehicle care service) ● Free mobile inspection during summer and winter

05. Emergency Claims (Speed Heart Service)● Hicar emergency claims ● System for identification of the customer’s location and the team coming to the client’s aid● Premium partner repair center information service (SMS service for the closest partner company and information on the person mobilized on-site) ● Customer assurance and information on the accident handling procedure

06. Call Center (Sense Heart Service)● Receipt of the report on a car accident and request for coming to the client’s aid (all year round)● Contract-related counseling and document issuance (documents that a customer needs to prepare, e.g. insurance policy or subscription certificate)● Security call service for elderly living alone● Call-back service

07. Risk Management Service● Risk management seminars● Risk assessment services for corporate customers● Risk management information offerin

01. Customer Satisfaction Service● Hi-Class Service for premium customers● Premium Customer’s Day● Music CD offering to premium customers● Free legal/tax service● Hicar driving lessons for women● Hi mom 119 class● Customer consultant● Hi-VOC (voice of customers) system● Online convenience system via homepage/smart customer center

02. Automobile Claims (Family Heart Service)● Smart Hi-UP service (mobile-based compensation handling system, real-time Claim payment)● Real-time mobile-based accident inquiry service for customers (transmission of a photo of the accident scene via e-mail and inquiry about employee in charge, etc)● Real-time indemnity processing information system from homepage● Post-accident care● Customized service to inform the client of the end of indemnity (via location message service (LMS), post, email)● On-site claim adjustment and payment service for petty car accident claims● Zero Complaint Day to solve customer complaints● Indemnity consulting on the Internet● Education and compensation consulting to prevent accidents for corporations

03. Long-Term Insurance Claims (Smart Heart Service)● Smart phone information service (information on documents to be submitted; consent to personal information handling; payment details)● Accident acceptance service from homepage (file loading, allocating fax number per insured person)● Long-term insurance accident consulting● Mobile accident acceptance service● LMS informing the client of the required documents● Planner touch service for customers with accident experience● Post-accident care

7 Heart Service programs

Activities for Customer Satisfaction

Vision Hi 2015

Report on Sustainability

Activities for Customer Satisfaction

Risk Management Activities

FY2012 Management News

30 2013 Annual Report 31Hyundai Marine & Fire Insurance

Effective response to financial environment and system changesWith the increasingly complicated nature of the financial system, risk management is becoming ever more important

amid uncertainty over global financial markets and the world economy and the ongoing problems of domestic savings

banks. The situation requires the sophistication and specialization of risk management in conjunction with the need

to deal more efficiently with changes in the financial environment and systems, such as compulsory execution of the

Risk-based Capital (RBC) system and enactment of the International Financial Reporting Standard (IFRS).

Risk Management Activities

1) RBC : Risk Based Capital 2) IFRS : International Financial Reporting Standards

Organization · Secure independence of risk management. · Consolidate specialist manpower.

Regulation · Establish the risk perceiving, measuring, analyzing, controlling, and monitoring system.

Premanagement · Consolidate the investment proposal analysis. · Pursue earnings considering the risk. · Tactical Asset Allocation.

Postmanagement · Select risk Mgt. indicators. · Establish the RAPM system.

Analysis · Develop analysis indicators. · Various sensitivity analyzing and reporting systems · Secure model conformance. · Accumulate and computerize risk data.

System · Establish market, credit, interest rate, insurance, and operation risk systems. · Build an integrated risk system.

Vision Hi 2015

Report on Sustainability

Activities for Customer Satisfaction

Risk Management Activities

FY2012 Management News

Adva

ncem

ent of risk

Mgt

. s

ystem

Risk Mgt. s

yste

m

Consolidation of risk

analyzing capabilityBalance between

earnings and risks

Advancement of risk

management

In consideration of such a need for risk management activities, we strive to operate a risk-based strategic management system, looking

for ways to strike a balance between risk and profit and adopting sophisticated risk management organizations, regulations, and systems.

To achieve this, we make a point of establishing a basic risk management plan and pushing ahead with specific objectives and measures

every year based on a risk management master plan.

Risk Management SystemHyundai Insurance is committed to minimizing

losses and enhancing corporate sustainability

amid all financial risks (interest rate, insurance,

market, credit, liquidity) and non-financial risks

(operation, reputation, laws) that may occur in

the course of business operation.

We have developed risk management systems

(ALM system, market risk management

system, credit risk management system, and

DFA system) to measure and analyze each

potential risk and operate the systems. We

completed our project of improving the market

risk management system in 2010 and laid the

foundation for integrated risk management and

consolidated market risk management.

Especially, in 2012, we established the Self Risk

Assessment System in an effort to enhance

the efficiency of self-regulatory efforts to

diagnose the risk management level and

improve vulnerable sectors. We plan to use

the said system as the basis for the operation

risk management system that we are about

to establish. Hyundai Insurance is committed

to continually improving and upgrading the

risk management system, coping with the

risk-concentrated supervision system, and

consolidating the enterprise risk management

base.

Risk-Oriented Management SystemHyundai Insurance has bolstered the risk Mgt. system, risk analysis and control

competence. The Risk Mgt. Committee affiliated with the board of directors

establishes a enterprise risk Mgt. strategy each year, deliberates on the company’

s key management strategy including risk-based business plans, asset Mgt.

plans, and reinsurance special terms and conditions revision. Thus, a risk-

concentrated management system has been built. The Committee is regularly

reported the risk status each quarter; when key issues occur, a provisional

meeting of the Committee is held. The Committee consists of at least 2 directors

or more nominated by the board, including the CEO.

The Risk Management Operation Committee affiliated with the Risk Management

Committee carries out the establishment of detailed policies on the decisions

of the Risk Management Committee, prior negotiation on the agenda, post-

management and inspection of action results, and review of risks in investment

proposals. The Risk Management Operation Committee consists of officer

from the department exclusively in charge of risk management and officers in

underwriting, and asset management divisions; in principle the meeting is held

prior to the Risk Management Committee meeting.

For efficient and practical risk management, Hyundai Insurance nominates risk

management departments per risk to manage the relevant risks. The former

cyclically inspects company-wide risks and reports the results to the Committee.

Furthermore, the department measures and analyzes the entire company’s risk

extent and that of each division and regularly carries out the stress test. The

department is also equipped with a system to measure, report, and cope with the

risk volatility early in case the management or environment rapidly changes. In

addition, the department continually conducts education and seminars on the risk

system, environmental changes, and risk management and makes an effort to

promote a risk-concentrated management culture.

While we at Hyundai Insurance constantly endeavor for risk-based management

culture promotion, we shall strengthen the risk system response and internal risk

management and enhance capital appropriateness by consolidating risk-based

insurance and asset portfolio management. At the same time, Hyundai Insurance

is committed to the solidification of a stable financial company base to cope

proactively with the global financial crisis by bolstering crisis situation analysis.

▶ Risk Management Strategy FrameworkFramework

32 2013 Annual Report 33Hyundai Marine & Fire Insurance

2013Apr • Hold on opening ceremony of the Qingdao Branch of Hyundai Insurance (China) Co., Ltd.

• Awarded the excellent call center certification for

5 consecutive years in the call center sector of non-life

insurance by 2012 Korea Service Quality Index

May • Hold on agreement ceremony for <Very Minor Confession>, a project for the prevention of school violence

• Hold the 1st customer consultant organization ceremony

Jun • Conducted 2012 internship program

Jul • Ranked No.1 in the long-term insurance sector for 4 consecutive years and in the automobile insurance

sector for 8 consecutive years by 2012 Global Customer

Satisfaction Index

Jan • Hold a completion ceremony for Bupyeong building

Feb • Hold a inauguration of the new CEOs

Mar • Launched Ashoka Korea

• Launched children’s transportation safety certification programs

• Awarded the Grand Prize in the product development and

marketing support sectors by 2012 Seoul Economy Daily

Aug • Hosted the first counseling concert of <Very Minor Confession> to make

Sept • Launched the claim service team for the 2012 World Conservation Congress

• Supported the campaign, 2012 Zero Injuries to Children

in Traffic Accidents

Oct • Awarded 2012 Korea 100 Best Companies to Work for (for 5 consecutive years, 10 times)

• Awarded Grand Prize in 2012 Global Excellent Awards in

Customer Satisfaction sector (7 times)

• Ranked No.1 in the non-life insurance sector of Korea

Sustainability Index for 3 consecutive years

• Rated A (stable) by A.M. Best

• Chosen as the first certified weather management

company in a financial business

Nov • Inducted to the Hall of Fame in 2012 Korea Management Grand Awards in Customer Satisfaction sector

• Awarded the 2012 Harald Economy Insurance Grand Prize

in innovative social contribution sector

• Awarded the 2012 Money Today Financial Innovation Grand Prize

• Rated BBB+ (Positive) by S&P

Dec • Agreement ceremony for <T-um Class>, a social contribution activity

• Chosen as 2012 excellent financial product by Financial

Supervisory Service (100 Years Age Nursing Insurance)

FY2012 NEWS

Vision Hi 2015

Report on Sustainability

Activities for Customer Satisfaction

Risk Management Activities

FY2012 Management News

2013

yundai Marine & Fire Insurance

34 2013 Annual Report 35Hyundai Marine & Fire Insurance

2. Direct Premium1) Overall

Note) Based on the exchange rates used for accounting settlement in FY2012: PL basic rate 1,115.07:U$1 / BS basic rate 1,112.10:U$1

Note) Hicar Direct: Subsidiary where Hyundai Insurance has 100% stake

In FY2012 (up to the end of March 2013), we posted 10,157.7 billion won in direct premiums, representing a 9.0% y-o-y increase.

Our market share stood at 16.6% (or 17.3% with Hi Car Direct included), a 0.2%p y-o-y drop. By line, commercial insurance posted

growth of 8.3%, while long-term insurance, including single payment, posted growth of 12.9% growth, and auto insurance negative

growth of 2.6%.

Classification FY2010 FY2011

(KRW million) (KRW million) (KRW million) (USD 1,000)

Direct Premium 7,610,424 9,316,657 10,157,664 9,109,461

Net Premium 6,786,492 8,421,672 9,232,199 8,279,498

Earned Premium 6,634,219 8,357,856 9,212,849 8,262,144

Underwriting Income -204,486 30,465 -212,672 -190,726

Investment Income 440,670 520,718 684,884 614,209

Total Operating Income 236,184 551,183 472,212 423,483

Net Income 159,485 392,756 333,381 298,979

(Adj. Net Income) 205,418

Total Assets 13,005,845 17,571,242 20,867,758 18,714,345

Invested Assets 10,313,054 13,422,220 16,290,616 14,609,534

Total Shareholders’ Equitie 1,152,819 1,744,234 2,101,924 1,885,019

(Adj. Total Shareholders’ Equities) 1,557,248

FY2012 Detailed report on management results _Financial Report

1. Financial Highlights

Note 1) Based on the exchange rates used for accounting settlement in FY2012: PL basic rate 1,115.07:U$1 / BS basic rate 1,112.10:U$1Note 2) K-IFRS was applied from FY2011 on a non-consolidation basis.Note 3) Adjusted net income: Net income + Increase of Catastrophe reserves / Adjusted shareholders’ equities: Total shareholders’ equities + Catastrophe reserves

FY2012

(Unit: KRW million)Direct Premium

FY2008

FY2009

FY2010

FY2011

FY2012

5,539,606

6,466,633

7,610,424

9,316,657

10,157,664

(Unit: KRW million)(Adj.) Net Income

FY2008

FY2009

FY2010

FY2011

FY2012

155,421

224,983

205,418

392,756

333,381

Note) The Adjusted Net Income up to FY2010, Net Income in FY2011 are shown.

(Unit: KRW million)(Adj.) Total Shareholders’ Equities

FY2008

FY2009

FY2010

FY2011

FY2012

1,153,595

1,423,800

1,557,248

1,744,234

2,101,924

Note) The Adjusted Total Shareholders’ Equities up to FY2010 and Total Shareholders’ Equities in FY2011 are shown.

Total Asset

FY2008

FY2009

FY2010

FY2011

FY2012

9,487,404

11,093,772

13,005,845

17,571,242

20,867,758

(Unit: KRW million)

ClassificationFY2010 FY2011 FY2012

(KRW million) (KRW million) (KRW million) (USD 1,000)

Commercial 808,224 910,859 986,170 884,404

Long-term 4,809,361 5,925,248 7,050,401 6,322,846

- Initial Premium 166,065 253,163 298,134 267,369

- In-force (recurring) Premium 4,643,297 5,672,085 6,752,266 6,055,478

Auto 1,925,636 2,040,907 1,988,159 1,782,995

Sub-total 7,543,221 8,877,014 10,024,730 8,990,245

Single Payment 67,203 439,643 132,935 119,217

Total 7,610,424 9,316,657 10,157,664 9,109,461

M/S Trend Including Hicar Direct Excluding Hicar Direct

16.8%

15.9%

16.9%

16.0%

16.9%

16.1%

17.5%

16.8%

17.3%

16.6%

FY2008 FY2009 FY2010 FY2011 FY2012

Financial Issues

FY2012 Detailed report on management results

Audit report on financial statements

36 2013 Annual Report 37Hyundai Marine & Fire Insurance

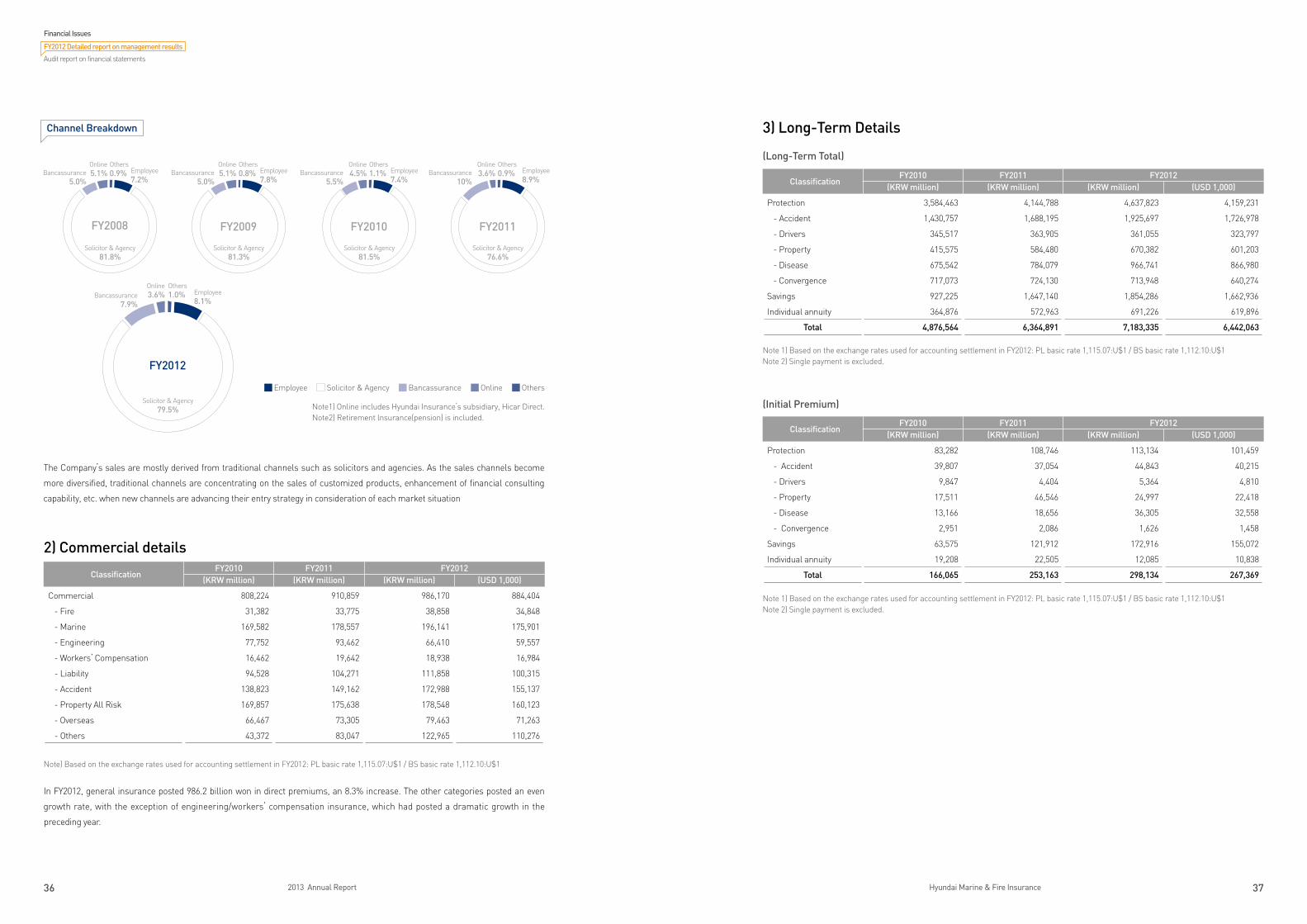

The Company’s sales are mostly derived from traditional channels such as solicitors and agencies. As the sales channels become

more diversified, traditional channels are concentrating on the sales of customized products, enhancement of financial consulting

capability, etc. when new channels are advancing their entry strategy in consideration of each market situation

2) Commercial details

Note) Based on the exchange rates used for accounting settlement in FY2012: PL basic rate 1,115.07:U$1 / BS basic rate 1,112.10:U$1

In FY2012, general insurance posted 986.2 billion won in direct premiums, an 8.3% increase. The other categories posted an even

growth rate, with the exception of engineering/workers’ compensation insurance, which had posted a dramatic growth in the

preceding year.

ClassificationFY2010 FY2011 FY2012

(KRW million) (KRW million) (KRW million) (USD 1,000)

Commercial 808,224 910,859 986,170 884,404

- Fire 31,382 33,775 38,858 34,848

- Marine 169,582 178,557 196,141 175,901

- Engineering 77,752 93,462 66,410 59,557

- Workers’ Compensation 16,462 19,642 18,938 16,984

- Liability 94,528 104,271 111,858 100,315

- Accident 138,823 149,162 172,988 155,137

- Property All Risk 169,857 175,638 178,548 160,123

- Overseas 66,467 73,305 79,463 71,263

- Others 43,372 83,047 122,965 110,276

Channel Breakdown

Employee Solicitor & Agency Bancassurance Online Others

Note1) Online includes Hyundai Insurance’s subsidiary, Hicar Direct. Note2) Retirement lnsurance(pension) is included.

3) Long-Term Details

(Long-Term Total)

Note 1) Based on the exchange rates used for accounting settlement in FY2012: PL basic rate 1,115.07:U$1 / BS basic rate 1,112.10:U$1Note 2) Single payment is excluded.

(Initial Premium)

Note 1) Based on the exchange rates used for accounting settlement in FY2012: PL basic rate 1,115.07:U$1 / BS basic rate 1,112.10:U$1Note 2) Single payment is excluded.

ClassificationFY2010 FY2011 FY2012

(KRW million) (KRW million) (KRW million) (USD 1,000)

Protection 3,584,463 4,144,788 4,637,823 4,159,231

- Accident 1,430,757 1,688,195 1,925,697 1,726,978

- Drivers 345,517 363,905 361,055 323,797

- Property 415,575 584,480 670,382 601,203

- Disease 675,542 784,079 966,741 866,980

- Convergence 717,073 724,130 713,948 640,274

Savings 927,225 1,647,140 1,854,286 1,662,936

Individual annuity 364,876 572,963 691,226 619,896

Total 4,876,564 6,364,891 7,183,335 6,442,063

ClassificationFY2010 FY2011 FY2012

(KRW million) (KRW million) (KRW million) (USD 1,000)

Protection 83,282 108,746 113,134 101,459

- Accident 39,807 37,054 44,843 40,215

- Drivers 9,847 4,404 5,364 4,810

- Property 17,511 46,546 24,997 22,418

- Disease 13,166 18,656 36,305 32,558

- Convergence 2,951 2,086 1,626 1,458

Savings 63,575 121,912 172,916 155,072

Individual annuity 19,208 22,505 12,085 10,838

Total 166,065 253,163 298,134 267,369

FY2009

Others0.8%

Online5.1%Bancassurance

5.0%

Solicitor & Agency81.3%

Employee7.8%

Employee7.2%

Others0.9%

Online5.1%Bancassurance

5.0%

FY2008

Solicitor & Agency81.8%

FY2010

Others1.1%

Online4.5%Bancassurance

5.5%

Solicitor & Agency81.5%

Employee7.4%

FY2011

Others0.9%

Online3.6%Bancassurance

10%

Solicitor & Agency76.6%

Employee8.9%

FY2012

Others1.0%

Online3.6%Bancassurance

7.9%

Solicitor & Agency79.5%

Employee8.1%

Financial Issues

FY2012 Detailed report on management results

Audit report on financial statements

38 2013 Annual Report 39Hyundai Marine & Fire Insurance

Long-term insurance, a driver of sales growth, also posted a high growth rate in FY 2012, 12.9% higher than the previous year. We

posted a growth rate of 17.8% for initial premiums. We posted growth of 4.0% and 28.1% in protection type and saving type, including

individual annuity, respectively, mainly on the back of briskness of healthcare insurance, which showed a 41.7% y-o-y increase,

despite the slowdown in property insurance. Recurring premiums recorded a high growth rate of 19.0% from the previous year due

to the improvement in persistency ratio. In regards to the product mix, protection products accounted for 64.6%, savings products for

25.8%, and annuity for 9.6%. The proportion of protection products, who has more profit margin, is still high. Within the protection

insurance products, accident insurance including coverage for medical expenses comprised the highest portion.

3. Operating Income1) Underwriting Efficiency

Note 1) The figures above are ratios against earned premiums. Sales expense is the amount after the amortization of the acquisition cost.Note 2) K-IFRS was applied from FY2011; its performance is based on a separate standard.

ClassificationFY2010 FY2011 FY2012

(K-GAAP) (K-IFRS) (K-IFRS)

Loss ratio 79.8% 82.2% 83.1%

- Commercial 58.8% 69.2% 69.8%

- Long-term 81.2% 83.3% 83.7%

- Automobile 79.0% 80.8% 83.4%

Expense ratio 22.5% 17.4% 19.2%

- Personnel cost 4.3% 2.8% 2.8%

- Maintenance cost 5.7% 4.7% 4.7%

- Distribution cost 12.6% 11.2% 12.7%

- Others 0.1% -1.3% -1.0%

Combined ratio 102.4% 99.6% 102.3%

Product Mix

Our overall combined ratio rose by 2.7%p y-o-y to 102.3%, with a 0.9%p y-o-y increase in the loss ratio and a 1.8%p increase in the

expense ratio. The loss ratio in general insurance recorded a 0.6%p y-o-y increase due to the occurrence of high-cost accidents,

including typhoons. The loss ratio in long-term insurance recorded a 0.4%p y-o-y increase due to an increase in the risk loss ratio.

Auto insurance recorded a 2.7%p y-o-y increase due to a drop in per-unit premium and heavy snow. The expense ratio recorded

a 1.8%p y-o-y increase due to an excess amortization of the long-term insurance acquisition cost despite the effort to reduce

expenses.

2) Long-Term Risk Loss Ratio

Note 1) Based on the exchange rates used for accounting settlement in FY2012: PL basic rate 1,115.07:U$1 / BS basic rate 1,112.10:U$1Note 2) Based on the direct premium and including IBNR.Note 3) K-IFRS was applied from FY2011 on a non-consolidation basis.

ClassificationFY2010 FY2011 FY2012

(KRW million) (KRW million) (KRW million) (USD 1,000)

Risk premium (a) 1,146,242 1,329,543 1,473,764 1,321,681

Amount of loss incurred (b) 948,409 1,066,123 1,214,288 1,088,982

Risk loss ratio (b/a) 82.7% 80.2% 82.4% 82.4%

Risk margin (a-b) 197,833 263,420 259,475 232,699

Combined Ratio Trend

Loss Ratio

FY2008(K-GAAP)

FY2009(K-GAAP)

FY2010(K-GAAP)

FY2011(K-IFRS)

FY2012(K-IFRS)

75.8%

78.2%

79.8%

82.2%

83.1%

Combined Ratio

FY2008

FY2009

FY2010

FY2011

FY2012

102.8%

101.5%

102.4%

99.6%

102.3%

Expense ratio

FY2008

FY2009

FY2010

FY2011

FY2012

27.0%

23.3%

22.5%

17.4%

19.2%

Accident

Drivers

Property

Disease

Convergence

Savings

Individual annuity

Protection

FY2008

Individual annuity6.0%

Savings15.7%

Convergence20.2%

Disease17.0%

Property11.7%

Drivers9.9%

Accident19.4%

Protection78.3%

FY2012

Individual annuity9.6%

Savings25.8%

Convergence9.9% Disease

13.5%

Property9.3%

Drivers5.0%

Accident26.8%

Protection64.6%

FY2009

Individual annuity6.3%

Savings15.4%

Convergence17.4%

Disease15.4%

Property9.4%

Drivers7.6%

Accident28.5%

Protection78.3%

FY2010

Individual annuity7.5%

Savings19.0%

Convergence14.7%

Disease13.9%

Property8.5%

Drivers7.1%

Accident29.3%

Protection73.5%

FY2011

Individual annuity9.0%

Savings25.9%

Convergence11.4% Disease

12.3%

Property9.2%

Drivers5.7%

Accident26.5%

Protection65.1%

Long-Term Risk Margin (Unit: KRW million)

Risk MarginLoss Ratio

259,47577.6%

82.9% 82.7%

80.2%

82.4%

FY2008 FY2009 FY2010 FY2011 FY2012

159,380163,396

197,833

263,420

Financial Issues

FY2012 Detailed report on management results

Audit report on financial statements

40 2013 Annual Report 41Hyundai Marine & Fire Insurance

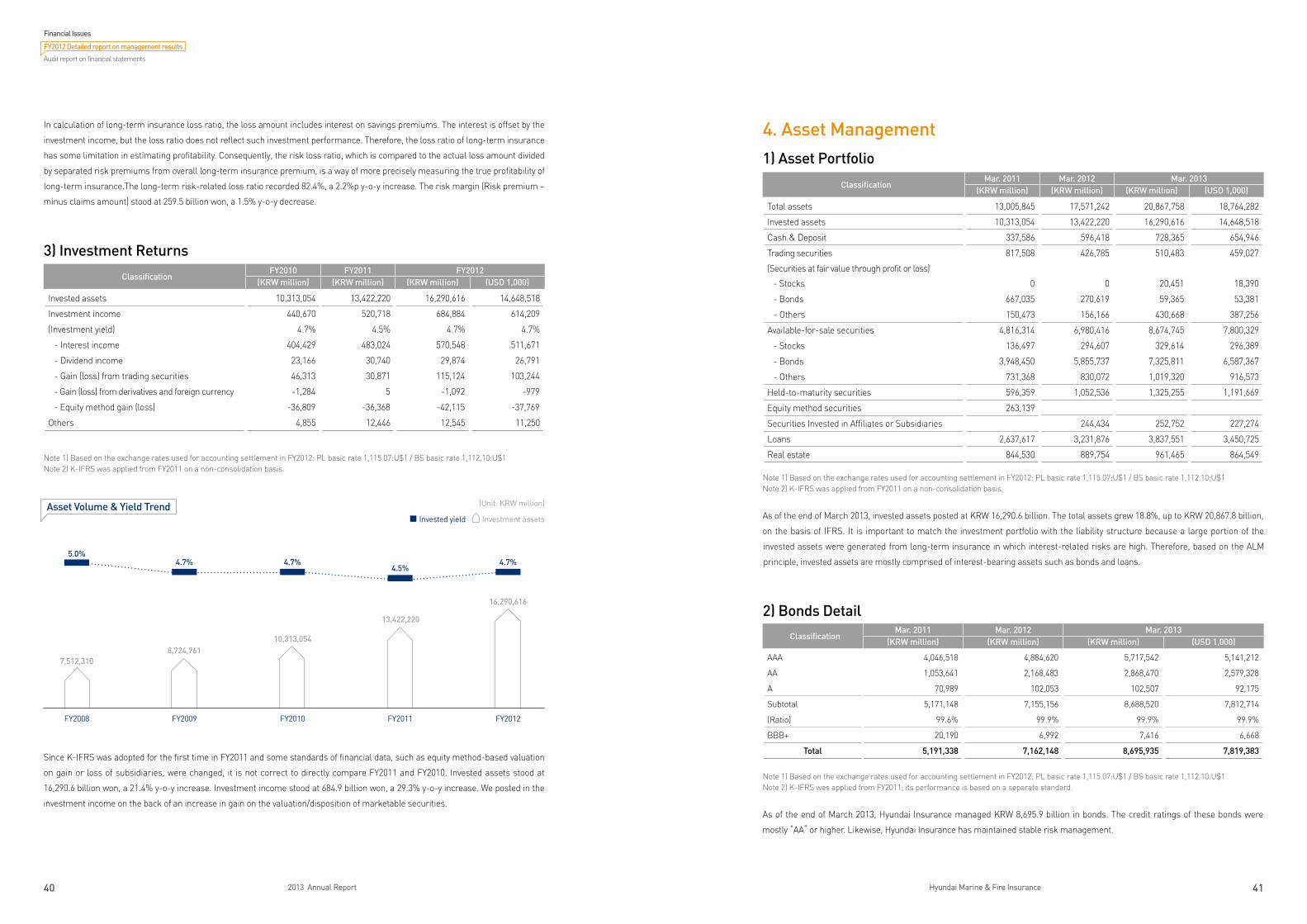

In calculation of long-term insurance loss ratio, the loss amount includes interest on savings premiums. The interest is offset by the

investment income, but the loss ratio does not reflect such investment performance. Therefore, the loss ratio of long-term insurance

has some limitation in estimating profitability. Consequently, the risk loss ratio, which is compared to the actual loss amount divided

by separated risk premiums from overall long-term insurance premium, is a way of more precisely measuring the true profitability of

long-term insurance.The long-term risk-related loss ratio recorded 82.4%, a 2.2%p y-o-y increase. The risk margin (Risk premium –

minus claims amount) stood at 259.5 billion won, a 1.5% y-o-y decrease.

3) Investment Returns

Note 1) Based on the exchange rates used for accounting settlement in FY2012: PL basic rate 1,115.07:U$1 / BS basic rate 1,112.10:U$1Note 2) K-IFRS was applied from FY2011 on a non-consolidation basis.

Since K-IFRS was adopted for the first time in FY2011 and some standards of financial data, such as equity method-based valuation

on gain or loss of subsidiaries, were changed, it is not correct to directly compare FY2011 and FY2010. Invested assets stood at

16,290.6 billion won, a 21.4% y-o-y increase. Investment income stood at 684.9 billion won, a 29.3% y-o-y increase. We posted in the

investment income on the back of an increase in gain on the valuation/disposition of marketable securities.

ClassificationFY2010 FY2011 FY2012

(KRW million) (KRW million) (KRW million) (USD 1,000)

Invested assets 10,313,054 13,422,220 16,290,616 14,648,518

Investment income 440,670 520,718 684,884 614,209

(Investment yield) 4.7% 4.5% 4.7% 4.7%

- Interest income 404,429 483,024 570,548 511,671

- Dividend income 23,166 30,740 29,874 26,791

- Gain (loss) from trading securities 46,313 30,871 115,124 103,244

- Gain (loss) from derivatives and foreign currency -1,284 5 -1,092 -979

- Equity method gain (loss) -36,809 -36,368 -42,115 -37,769

Others 4,855 12,446 12,545 11,250

4. Asset Management1) Asset Portfolio

Note 1) Based on the exchange rates used for accounting settlement in FY2012: PL basic rate 1,115.07:U$1 / BS basic rate 1,112.10:U$1Note 2) K-IFRS was applied from FY2011 on a non-consolidation basis.

As of the end of March 2013, invested assets posted at KRW 16,290.6 billion. The total assets grew 18.8%, up to KRW 20,867.8 billion,

on the basis of IFRS. It is important to match the investment portfolio with the liability structure because a large portion of the

invested assets were generated from long-term insurance in which interest-related risks are high. Therefore, based on the ALM

principle, invested assets are mostly comprised of interest-bearing assets such as bonds and loans.

2) Bonds Detail

Note 1) Based on the exchange rates used for accounting settlement in FY2012: PL basic rate 1,115.07:U$1 / BS basic rate 1,112.10:U$1Note 2) K-IFRS was applied from FY2011; its performance is based on a separate standard.

As of the end of March 2013, Hyundai Insurance managed KRW 8,695.9 billion in bonds. The credit ratings of these bonds were

mostly “AA” or higher. Likewise, Hyundai Insurance has maintained stable risk management.

ClassificationMar. 2011 Mar. 2012 Mar. 2013

(KRW million) (KRW million) (KRW million) (USD 1,000)

Total assets 13,005,845 17,571,242 20,867,758 18,764,282

Invested assets 10,313,054 13,422,220 16,290,616 14,648,518

Cash & Deposit 337,586 596,418 728,365 654,946

Trading securities

(Securities at fair value through profit or loss)

817,508 426,785 510,483 459,027

- Stocks 0 0 20,451 18,390

- Bonds 667,035 270,619 59,365 53,381

- Others 150,473 156,166 430,668 387,256

Available-for-sale securities 4,816,314 6,980,416 8,674,745 7,800,329

- Stocks 136,497 294,607 329,614 296,389

- Bonds 3,948,450 5,855,737 7,325,811 6,587,367

- Others 731,368 830,072 1,019,320 916,573

Held-to-maturity securities 596,359 1,052,536 1,325,255 1,191,669

Equity method securities 263,139

Securities Invested in Affiliates or Subsidiaries 244,434 252,752 227,274

Loans 2,637,617 3,231,876 3,837,551 3,450,725

Real estate 844,530 889,754 961,465 864,549

ClassificationMar. 2011 Mar. 2012 Mar. 2013

(KRW million) (KRW million) (KRW million) (USD 1,000)

AAA 4,046,518 4,884,620 5,717,542 5,141,212

AA 1,053,641 2,168,483 2,868,470 2,579,328

A 70,989 102,053 102,507 92,175

Subtotal 5,171,148 7,155,156 8,688,520 7,812,714

(Ratio) 99.6% 99.9% 99.9% 99.9%

BBB+ 20,190 6,992 7,416 6,668

Total 5,191,338 7,162,148 8,695,935 7,819,383

(Unit: KRW million)

FY2008 FY2009 FY2010 FY2011 FY2012

5.0%4.7% 4.7%

4.5%4.7%

7,512,3108,724,761

10,313,054

13,422,220

16,290,616

Asset Volume & Yield TrendInvestment assetsInvested yield

Financial Issues

FY2012 Detailed report on management results

Audit report on financial statements

42 2013 Annual Report 43Hyundai Marine & Fire Insurance

3) Loan Details

As of Mar. 31, 2013

Note 1) Before deducting bad debt reserves and deferred auxiliary revenueNote 2) K-IFRS was applied from FY2011; its performance is based on a separate standard.

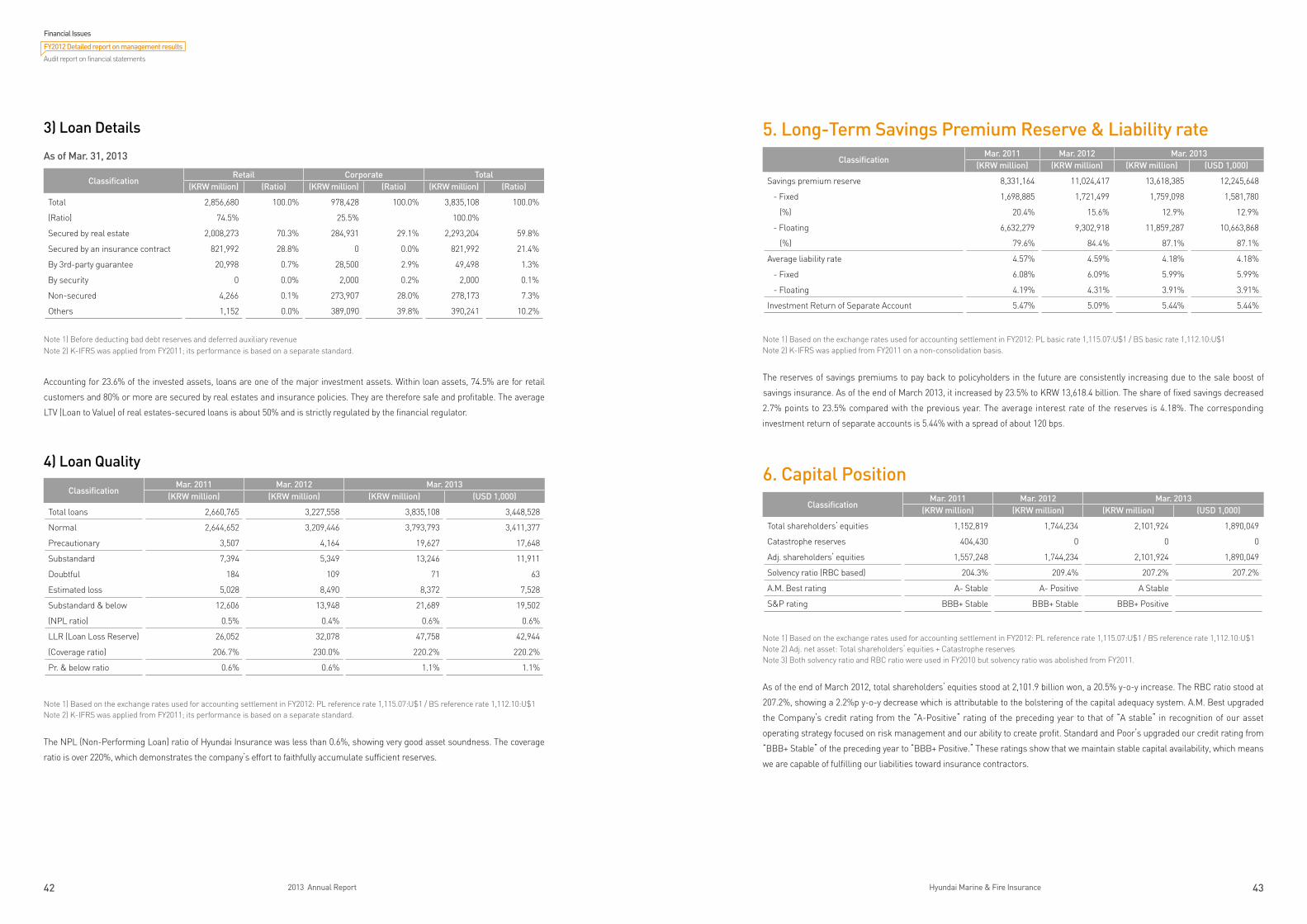

Accounting for 23.6% of the invested assets, loans are one of the major investment assets. Within loan assets, 74.5% are for retail

customers and 80% or more are secured by real estates and insurance policies. They are therefore safe and profitable. The average

LTV (Loan to Value) of real estates-secured loans is about 50% and is strictly regulated by the financial regulator.

4) Loan Quality

Note 1) Based on the exchange rates used for accounting settlement in FY2012: PL reference rate 1,115.07:U$1 / BS reference rate 1,112.10:U$1Note 2) K-IFRS was applied from FY2011; its performance is based on a separate standard.

The NPL (Non-Performing Loan) ratio of Hyundai Insurance was less than 0.6%, showing very good asset soundness. The coverage

ratio is over 220%, which demonstrates the company’s effort to faithfully accumulate sufficient reserves.

ClassificationMar. 2011 Mar. 2012 Mar. 2013

(KRW million) (KRW million) (KRW million) (USD 1,000)

Total loans 2,660,765 3,227,558 3,835,108 3,448,528

Normal 2,644,652 3,209,446 3,793,793 3,411,377

Precautionary 3,507 4,164 19,627 17,648

Substandard 7,394 5,349 13,246 11,911

Doubtful 184 109 71 63

Estimated loss 5,028 8,490 8,372 7,528

Substandard & below 12,606 13,948 21,689 19,502

(NPL ratio) 0.5% 0.4% 0.6% 0.6%

LLR (Loan Loss Reserve) 26,052 32,078 47,758 42,944

(Coverage ratio) 206.7% 230.0% 220.2% 220.2%

Pr. & below ratio 0.6% 0.6% 1.1% 1.1%

ClassificationRetail Corporate Total

(KRW million) (Ratio) (KRW million) (Ratio) (KRW million) (Ratio)

Total 2,856,680 100.0% 978,428 100.0% 3,835,108 100.0%

(Ratio) 74.5% 25.5% 100.0%

Secured by real estate 2,008,273 70.3% 284,931 29.1% 2,293,204 59.8%

Secured by an insurance contract 821,992 28.8% 0 0.0% 821,992 21.4%

By 3rd-party guarantee 20,998 0.7% 28,500 2.9% 49,498 1.3%

By security 0 0.0% 2,000 0.2% 2,000 0.1%

Non-secured 4,266 0.1% 273,907 28.0% 278,173 7.3%

Others 1,152 0.0% 389,090 39.8% 390,241 10.2%

5. Long-Term Savings Premium Reserve & Liability rate

Note 1) Based on the exchange rates used for accounting settlement in FY2012: PL basic rate 1,115.07:U$1 / BS basic rate 1,112.10:U$1Note 2) K-IFRS was applied from FY2011 on a non-consolidation basis.

The reserves of savings premiums to pay back to policyholders in the future are consistently increasing due to the sale boost of

savings insurance. As of the end of March 2013, it increased by 23.5% to KRW 13,618.4 billion. The share of fixed savings decreased

2.7% points to 23.5% compared with the previous year. The average interest rate of the reserves is 4.18%. The corresponding

investment return of separate accounts is 5.44% with a spread of about 120 bps.

6. Capital Position

Note 1) Based on the exchange rates used for accounting settlement in FY2012: PL reference rate 1,115.07:U$1 / BS reference rate 1,112.10:U$1Note 2) Adj. net asset: Total shareholders’ equities + Catastrophe reservesNote 3) Both solvency ratio and RBC ratio were used in FY2010 but solvency ratio was abolished from FY2011.

As of the end of March 2012, total shareholders’ equities stood at 2,101.9 billion won, a 20.5% y-o-y increase. The RBC ratio stood at

207.2%, showing a 2.2%p y-o-y decrease which is attributable to the bolstering of the capital adequacy system. A.M. Best upgraded

the Company’s credit rating from the “A-Positive” rating of the preceding year to that of “A stable” in recognition of our asset

operating strategy focused on risk management and our ability to create profit. Standard and Poor’s upgraded our credit rating from

“BBB+ Stable” of the preceding year to “BBB+ Positive.” These ratings show that we maintain stable capital availability, which means

we are capable of fulfilling our liabilities toward insurance contractors.

ClassificationMar. 2011 Mar. 2012 Mar. 2013

(KRW million) (KRW million) (KRW million) (USD 1,000)

Savings premium reserve 8,331,164 11,024,417 13,618,385 12,245,648

- Fixed 1,698,885 1,721,499 1,759,098 1,581,780

(%) 20.4% 15.6% 12.9% 12.9%

- Floating 6,632,279 9,302,918 11,859,287 10,663,868

(%) 79.6% 84.4% 87.1% 87.1%

Average liability rate 4.57% 4.59% 4.18% 4.18%

- Fixed 6.08% 6.09% 5.99% 5.99%

- Floating 4.19% 4.31% 3.91% 3.91%

Investment Return of Separate Account 5.47% 5.09% 5.44% 5.44%

ClassificationMar. 2011 Mar. 2012 Mar. 2013

(KRW million) (KRW million) (KRW million) (USD 1,000)

Total shareholders’ equities 1,152,819 1,744,234 2,101,924 1,890,049

Catastrophe reserves 404,430 0 0 0

Adj. shareholders’ equities 1,557,248 1,744,234 2,101,924 1,890,049

Solvency ratio (RBC based) 204.3% 209.4% 207.2% 207.2%

A.M. Best rating A- Stable A- Positive A Stable

S&P rating BBB+ Stable BBB+ Stable BBB+ Positive

Financial Issues

FY2012 Detailed report on management results

Audit report on financial statements

44 2013 Annual Report 45Hyundai Marine & Fire Insurance

7. Shareholders’Dividend

Note 1) Based on the exchange rates used for accounting settlement in FY2012: PL basic rate 1,115.07:U$1 / BS basic rate 1,112.10:U$1Note 2) K-IFRS was applied from FY2011; its performance is based on a separate standard.

In FY2012, we posted net income of 333.4 billion won, a 15.2% y-o-y decrease. Dividend per share stood at 1,050 won, a 22%

decrease from the 1,350 won of the preceding year due to the decrease in net profits. Total amount of dividend paid came to 84.4

billion won. Dividend payout ratio stood at 25.3%.

ClassificationFY2010 FY2011 FY2012

(KRW million) (KRW million) (KRW million) (USD 1,000)

Net income 159,485 392,756 333,381 298,979

Total dividend 56,290 108,560 84,435 75,722

Dividend per share (KRW) 700 1,350 1,050

Dividend rate per par value 140.0% 270.0% 210.0%

Payout ratio 35.3% 27.6% 25.3%

Dividend yield 2.4% 4.0% 3.3%

Total dividend

FY2008

FY2009

FY2011

FY2012

FY2010

39,996

56,290

56,290

108,560

84,435

Payout ratio

FY2008

FY2009

FY2011

FY2012

FY2010

34.7%

30.5%

35.3%

27.6%

25.3%

Dividend per par value

FY2008

FY2009

FY2011