Embed Size (px)

Citation preview

2013

Investment Products Offered • Are Not FDIC Insured • May Lose Value • Are Not Bank Guaranteed

The information herein reflects prevailing market conditions and our judgments as of the date of this document, which are subject to change. In preparing this document, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. Opinions and estimates may be changed without notice and involve a number of assumptions which may not prove valid. There is no guarantee that any forecasts or opinions in this material will be realized. Information should not be construed as investment advice.

Clouds Parting, Revealing Opportunities

AllianceBernstein.com

Widespread Global Uncertainties…

United States Fiscal Cliff

Presidential and Congressional Election

Supreme Court Ruling on Healthcare

Slow Economic Growth

Brazil Economic Slowdown

China Hard Landing

Leadership Change and Policy Direction

Japan Restructuring Activities

Trade Balance Issues

Bank of Japan (BOJ) Policy/Election

Europe Bank Recapitalization

Greece’s Future in the Euro

Future of the Eurozone

Role of the European Central Bank (ECB)

Move to Fiscal Union

Current analysis does not guarantee future results. As of December 31, 2012 Source: AllianceBernstein

Asia ex Japan Economic

Slowdown

Trade Balance Issues

Presidential Election Mexico

Venezuela Presidential Election

Argentina Policy Risk

EMEA

CMO 1Q 2013 | 1

Economic Slowdown

Arab Spring

CMO 1Q 2013 | 1AllianceBernstein.com

AllianceBernstein.com

…Have Weighed on the Global Economy

Trade Volume Is Trending Down

Historical analysis does not guarantee future results. *PMI: Purchasing Managers’ Index. PMI through December 31, 2012. An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio. Euro-area consumer confidence through August 31, 2012. CEO business confidence through September 30, 2012. Trade volume through September 30, 2012. Cash ratios through December 31, 2012. **Standard deviation: a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. †G7 countries: Canada, France, Germany, Italy, Japan, UK and US. BRIC countries: Brazil, Russia, India and China Source: Deutsche Bank, Eurostat, Haver Analytics, International Monetary Fund (IMF), J.P. Morgan, Markit and AllianceBernstein

Global Manufacturing Output Has Contracted

Global Manufacturing PMI*

–40

–20

0

20

40

01 03 05 07 09 11Year

-ove

r-Ye

ar %

Cha

nge

Confidence Has Declined

Companies Have Slowed Spending

Cash Ratios: S&P 500 Index Companies ex Financials

–50

0

50

100

150

–4

–3

–2

–1

0

1

2

02 03 04 05 06 07 08 09 10 11 12

Index

Sta

ndar

d D

evia

tions

**

Euro-Area Consumer Confidence (Left Scale)

CEO Business Confidence

30

40

50

60

06 07 08 09 10 11 12

Inde

x

2

6

10

14

82 89 96 03 10

Perc

ent

Cash/ Market Cap

Cash/Assets

Exports: G7 + BRIC†

CMO 1Q 2013 | 2 CMO 1Q 2013 | 2AllianceBernstein.com

AllianceBernstein.com

0.0

0.5

1.0

1.5

2.0

Jan 12 Feb 12 Mar 12 Apr 12 May 12 Jun 12 Jul 12 Aug 12 Sep 12 Oct 12 Nov 12 Dec 12

Glo

bal R

isk

Aver

sion

Indi

cato

r*

First Greek

General Election

Some Global Uncertainties Have Been Addressed

Historical analysis does not guarantee future results. Through December 31, 2012 *Incorporates equity index–implied volatilities, bond spreads, currency index–implied volatilities and equity mutual fund flows. **Long-Term Refinancing Operations I was on December 8, 2011. †European Union. ‡Outright Monetary Transactions Source: AllianceBernstein

UPDATED

Through 11/30/12

Received Data From

Guoan Du Mexican Elections

Venezuelan Elections Settled

Japanese Election

China’s Industrial Production and Manufacturing

Expand

China’s Leadership Transition Uneventful Fiscal

Cliff

Obama Reelected

Healthcare Ruling

Spanish Bank

Recaps

EU† Summit (ECB Bond

Buying, Bank

Recaps)

Greece Passes 2013 Austerity

Budget

LTRO II

ECB’s OMT‡ Announcement

US QE3

EU Summit Agreement to Finalize Single

Supervisory Mechanism

Greek Program

US Federal Reserve Sets Numerical Guidelines Based on Inflation and

Unemployment

Draghi’s “Whatever it

Takes to Preserve the Euro” Speech

Second Greek

General Election

LTRO I**

United Kingdom Additional

Asset Purchases

CMO 1Q 2013 | 3 CMO 1Q 2013 | 3AllianceBernstein.com

AllianceBernstein.com CMO 1Q 2013 | 4AllianceBernstein.com

5.8% 0.7%

–6.3%

3.1% 0.0%

–9.0% 0.7%

1.7% 3.5% 4.2%

5.6% 6.8%

–0.4% 1.9%

4Q:2012 Returns

28.7% 7.0%

–1.1%

11.2% 2.2% 2.0%

6.8%

10.9% 18.1% 19.3%

18.2% 17.3%

16.0% 16.4%

Annualized Returns Since February 2009

Returns in US dollars

Markets Performed Better than They Felt in 2012

2012 Returns

Past performance does not guarantee future results. As of December 31, 2012 *Europe, Australasia and the Far East. **Treasury Inflation-Protected Securities. †Global Real Estate Investment Trusts Global high yield, global corporates, Japan and euro-area government bonds in hedged USD terms. All other non-US returns in unhedged USD terms. Please see end of presentation for index information. An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio. Source: Barclays Capital, FactSet, FTSE, MSCI, S&P/Dow Jones and AllianceBernstein

Japan

Global High Yield

US

Euro Area

Emerging-Market Debt Global Corporates

EAFE*

US Small-Cap

Emerging Markets

Equities

Credit

Government Bonds

Commodities Alternatives

Global REITs† TIPS**

Municipals

US Large-Cap

30.2% 10.1%

7.4%

5.0% 2.4%

4.5% 7.3%

10.7% 18.0%

22.6%

24.5% 16.7%

21.5% 24.3%

CMO 1Q 2013 | 4

AllianceBernstein.com CMO 1Q 2013 | 5AllianceBernstein.com

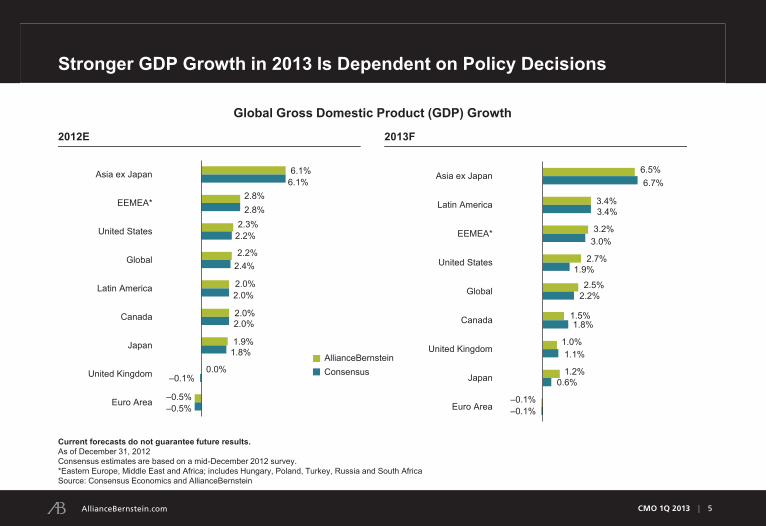

Stronger GDP Growth in 2013 Is Dependent on Policy Decisions

Current forecasts do not guarantee future results. As of December 31, 2012 Consensus estimates are based on a mid-December 2012 survey. *Eastern Europe, Middle East and Africa; includes Hungary, Poland, Turkey, Russia and South Africa Source: Consensus Economics and AllianceBernstein

6.1%

2.8%

2.3%

2.2%

2.0%

2.0%

1.9%

0.0%

–0.5%

6.1%

2.8%

2.2%

2.4%

2.0%

2.0%

1.8%

–0.1%

–0.5%

-3.0% 2.0% 7.0%

Asia ex Japan

EEMEA*

United States

Global

Latin America

Canada

Japan

United Kingdom

Euro Area

6.5%

3.4%

3.2%

2.7%

2.5%

1.5%

1.0%

1.2%

–0.1%

6.7%

3.4%

3.0%

1.9%

2.2%

1.8%

1.1%

0.6%

–0.1%

-3.0% 2.0% 7.0%

Asia ex Japan

Latin America

EEMEA*

United States

Global

Canada

United Kingdom

Japan

Euro Area

2012E

2013F

AllianceBernstein Consensus

Global Gross Domestic Product (GDP) Growth

CMO 1Q 2013 | 5

AllianceBernstein.com CMO 1Q 2013 | 6AllianceBernstein.com

0.5 0.1 0.3

2.8

1.5 1.1

1.7

2.2

0.8

0.4

–0.3

0.8

–0.8 –1.2

0.1

A Broader US Economic Recovery

Public-Sector Growth Has Turned Positive

–12

–8

–4

0

4

8

12

02 03 04 05 06 07 08 09 10 11 12

Perc

ent

Contribution to US GDP Growth Rate Percent

4.6% 2.2% Real GDP

Seasonally Adjusted Annual GDP Growth

Rebound in Early Cyclical Sectors

Historical analysis does not guarantee future results. Left chart through September 30, 2012. Right chart: Historical data are recessional from January 1, 1960, to December 31, 2004. Current data are from July 1, 2009, to June 30, 2012. *Quarter-over-quarter seasonally adjusted annual rate Numbers may not sum due to rounding. Source: Haver Analytics, National Bureau of Economic Research and AllianceBernstein

Government Housing Exports and Investment Imports Consumption

Historical Current

Public Growth

(QoQ SAAR*)

Private Growth

(QoQ SAAR*)

3.1%

3Q:12

CMO 1Q 2013 | 6

AllianceBernstein.com CMO 1Q 2013 | 7AllianceBernstein.com

Housing: Building Permits

90

110

130

150

170

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43Months of Recovery

Inde

x

1991

Current

1983

2001

Housing and Public Spending Improve

Historical analysis does not guarantee future results. Upper left chart through September 30, 2012. Lower left chart through October 31, 2012. Upper right chart through December 31, 2012. Lower right chart through November 1, 2012. Source: Haver Analytics, National Association of Realtors, US Bureau of Economic Analysis, US Census Bureau and US Federal Reserve Board

Housing: Owner-Occupied Housing

95

105

115

125

1 4 7 10 13 16 19 22 25 28 31 34 37 40

1Q:61 4Q:70 Q1:754Q:82 1Q:91 4Q:012Q:09

Number of Months

Inde

x

–1.0

–0.5

0.0

0.5

1.0

1.5

08 09 10 11 12

% C

hang

e (S

AAR

)

Federal

Public Sector: Contribution to Real GDP

Housing: Construction Employment as Share of Total

0

2

4

6

8

10

12

70 76 82 88 94 00 06 12Pe

rcen

t

Unemployment

Construction Participation

State and Local

CMO 1Q 2013 | 7

AllianceBernstein.com CMO 1Q 2013 | 8AllianceBernstein.com

What Stage of the Business Cycle Are We in?

Current analysis does not guarantee future results. July 2009 through December 31, 2012 Source: AllianceBernstein

Early Mid Late

Cycle Length (Duration) Sector Leadership in GDP Labor Markets (Jobless Rate) Wage and Price Trends Household Leverage Nonfinancial Business Leverage Operating Profits Real Profit Margins Monetary Policy Fiscal Policy

Current US Business Cycle

CMO 1Q 2013 | 8

AllianceBernstein.com CMO 1Q 2013 | 9AllianceBernstein.com

Fiscal Cliff Avoided for Now

Fiscal Deal Reduces Tax Cliff

Pending Expenditure Issues: First Quarter

Long-Term Issue of Spending Remains

Debt-ceiling negotiations

Automatic spending cuts

Continuing budget resolution

0

20

40

60

80

100

120

62 68 74 80 86 92 98 04 10 16 22

Per

cent

Current and historical analysis do not guarantee future results. Left chart as of January 8, 2013; bottom right chart as of January 1, 2013 *AllianceBernstein estimates **PEP: Personal Exemption Phaseout. EITC: Earned Income Tax Credit. CTC: Child Tax Credit. AOTC: American Opportunity Tax Credit Numbers may not sum due to rounding. Source: Office of Management and Budget; Urban-Brookings Tax Policy Center (TPC) Microsimulation Model (version 0412-7) and TPC calculations based on Congressional Budget Office and Joint Committee of Taxation (JCT) estimates; and AllianceBernstein

Provision Fiscal Cliff

Fiscal Deal*

Payroll Tax $115 $115

Healthcare Law Provisions 24 24

High-Income Capital Gains and Dividends 8 4

High-Income Rates, Pease and PEP** 44 44

Stimulus Legislation EITC, CTC and AOTC** 27 0

Extenders 75 0

Estate Tax 31 5

Remainder of 2001–2003 Tax Provisions 171 0

Alternative Minimum Tax Patch 40 0

Total $536 $192

Mandatory Spending Post–Fiscal Cliff % of Revenues

Fiscal Cliff vs. Fiscal Deal (USD Billions)

CMO 1Q 2013 | 9

E E

AllianceBernstein.com CMO 1Q 2013 | 10AllianceBernstein.com

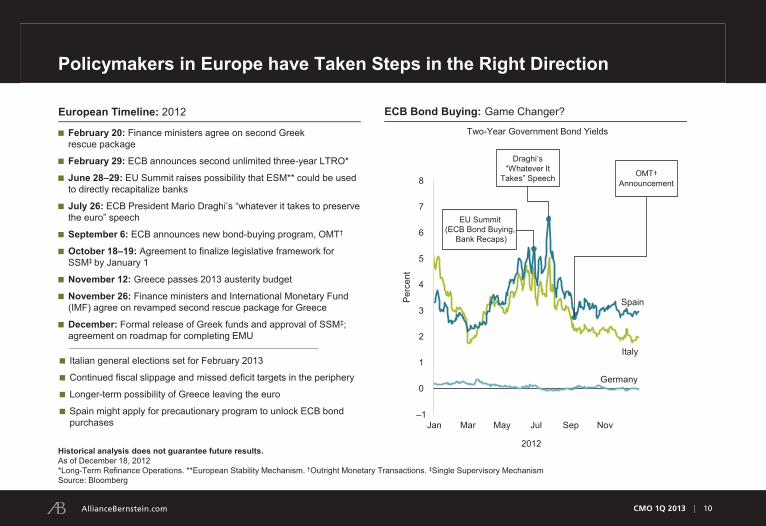

ECB Bond Buying: Game Changer?

Policymakers in Europe have Taken Steps in the Right Direction

Two-Year Government Bond Yields February 20: Finance ministers agree on second Greek rescue package

February 29: ECB announces second unlimited three-year LTRO*

June 28–29: EU Summit raises possibility that ESM** could be used to directly recapitalize banks

July 26: ECB President Mario Draghi’s “whatever it takes to preserve the euro” speech

September 6: ECB announces new bond-buying program, OMT†

October 18–19: Agreement to finalize legislative framework for SSM‡ by January 1

November 12: Greece passes 2013 austerity budget

November 26: Finance ministers and International Monetary Fund (IMF) agree on revamped second rescue package for Greece

December: Formal release of Greek funds and approval of SSM‡; agreement on roadmap for completing EMU

Italian general elections set for February 2013

Continued fiscal slippage and missed deficit targets in the periphery

Longer-term possibility of Greece leaving the euro

Spain might apply for precautionary program to unlock ECB bond purchases

Historical analysis does not guarantee future results. As of December 18, 2012 *Long-Term Refinance Operations. **European Stability Mechanism. †Outright Monetary Transactions. ‡Single Supervisory Mechanism Source: Bloomberg

European Timeline: 2012

CMO 1Q 2013 | 10

–1

0

1

2

3

4

5

6

7

8

Jan Mar May Jul Sep Nov

Germany

Italy

Spain

2012

Perc

ent

EU Summit (ECB Bond Buying,

Bank Recaps)

Draghi’s “Whatever It

Takes” Speech OMT† Announcement

AllianceBernstein.com CMO 1Q 2013 | 11AllianceBernstein.com

European Periphery Starts to Rebalance but Fundamentals Are Still Poor

Historical analysis does not guarantee future results. Current account balances as of September 30, 2012 Change in domestic demand as of June 30, 2012 *Real exchange rate against the rest of the euro area **Greek numbers are for 1Q01 rather than 1Q99. Source: European Commission and Haver Analytics

Domestic Demand Has Been Chronically Weak

Change in Domestic Demand: First Half 2008 to First Half 2012

–24.7 –23.0

–12.5 –11.8

–6.4 –3.5

–0.2 0.8 0.9

3.1 3.2

GreeceIrelandSpain

PortugalItaly

NetherlandsFinlandFrance

BelgiumAustria

Germany

–19.2

3.2 9.9

16.4 7.9

2.6

–5.3

14.2

–0.7

27.7

9.2 3.0 2.0 0.8

–11.0

1.0 2.8 1.9

–10.6

4.7

–20.8

–6.0

Ger

man

y

Fran

ce

Italy

Spa

in

Net

herla

nds

Bel

gium

Aus

tria

Gre

ece*

*

Finl

and

Irela

nd

Por

tuga

l

1Q:99–2Q:08 2Q:08–2Q:12

Peripheral Real Exchange Rates Are More Competitive

–18

–15

–12

–9

–6

–3

0

3

6

07 08 09 10 11 12

Italy

% o

f GD

P; 4

Q M

ovin

g Av

g.

Ireland

Greece

Spain

Portugal

Current Accounts Have Improved on the Surface

Current Account Balances Change in Real Exchange Rate*

CMO 1Q 2013 | 11

AllianceBernstein.com CMO 1Q 2013 | 12AllianceBernstein.com

China: Fundamentals Have Turned Around…

Historical analysis does not guarantee future results. As of November 30, 2012 4Q:2012 industrial production growth assumes an average of October and November. 4Q:2012 GDP is AllianceBernstein forecast at 7.8% year over year. Source: CEIC Data, Direction of Trade Statistics, IMF and AllianceBernstein

Economic Output Remains Solid

Investment Remains Robust

0

2

4

6

8

10

12

14

16

18

0

5

10

15

20

25

00 02 04 06 08 10 12

Year-over-Year % C

hange Year

-ove

r-Ye

ar %

Cha

nge

Industrial Production

(Left Scale)

GDP

10

15

20

25

30

35

40

45

50

55

Jan

Feb

Mar

Apr

May Jun

Jul

Aug

Sep Oct

Nov

Year

-ove

r-Ye

ar %

Cha

nge

Fixed-Asset Investment (FAI)

FAI New Project Starts

2012

CMO 1Q 2013 | 12

AllianceBernstein.com CMO 1Q 2013 | 13AllianceBernstein.com

…but Headwinds Remain

Historical analysis does not guarantee future results. Left chart as of December 31, 2012. Gray arrows are theoretical and reflect desired policy outcomes. Middle chart and right chart as of November 30, 2012. Source: Bernstein Research, CEIC Data and AllianceBernstein

More Consumption Is Needed…

20

25

30

35

40

45

50

55

79 87 95 03 11 19

Perc

ent o

f GD

P

Investment Rate

Consumption Rate

Saving Rate

…but Imports Remain Weak and Vulnerable…

–30

–20

–10

0

10

20

30

40

50

60

70

05 06 07 08 09 10 11 12

Year

-ove

r-Ye

ar P

erce

nt C

hang

e

Real Export Volume

Real Import Volume

…and Domestic Demand Is Weak

–30

–20

–10

0

10

20

30

40

50

60

Jan

11M

ar 1

1M

ay 1

1Ju

l 11

Sep

11

Nov

11

Jan

12M

ar 1

2M

ay 1

2Ju

l 12

Sep

12

Nov

12

Year

-ove

r-Ye

ar P

erce

nt C

hang

e

Imports for Nominal

Domestic Demand

Processing Items for Nominal Exports

Desired Outcomes

CMO 1Q 2013 | 13

E

AllianceBernstein.com CMO 1Q 2013 | 14AllianceBernstein.com

Market Environments Inform Portfolio Strategy

As of December 31, 2012 There is no guarantee that the portfolio strategies presented will yield positive results or that the market environments presented will occur. *Beta is a measure of the volatility, or systemic risk, of a security or a portfolio in comparison to the market as a whole. Source: AllianceBernstein

Financial Crisis/ Recession Risk-On, Risk-Off Recovery/Normalization

Economic Outlook Negative real growth Fears of deflation

1%–2% global GDP growth Fears shift between inflation

and deflation

3%–5% global GDP growth Healthy reflation

Market Volatility High and sustained Frequent shifts between high and low volatility Low and sustained

Market Return Negative Modest High

Investment Focus Preservation Income Appreciation

Bonds Governments Credits High-beta* credit

Real Assets TIPS Real estate Commodities

Equities Defensives US

Stability Global

Cyclical Non-US EM

Currencies Hedged Partially hedged Unhedged/carry exposure

Potential Market Environments and Portfolio Strategies

CMO 1Q 2013 | 14

AllianceBernstein.com CMO 1Q 2013 | 15AllianceBernstein.com

Attractive Equity Potential Has Been Overshadowed by Uncertainty

Long-Term Expected

Return (%)

1.6

5.6

7.2

5.9

2.9

8.8

GlobalSovereigns

Equity RiskPremium

GlobalStocks

Long-Term Average

December 31, 2012

14.3

15.5 Normal

Historical analysis and current forecasts do not guarantee future results. Data do not represent past performance and are not a promise of actual results or range of future results. Left chart as of December 31, 2012. Global sovereign bonds are represented by global, developed, sovereign, seven-year constant-maturity nominal bonds; global stocks by a universe similar to MSCI World. Both are reported in and hedged into US dollars. Source: Lipper, Morningstar, MSCI, Strategic Insight and AllianceBernstein

Investment Flows Reflect Risk Aversion

Net New Flows: Jul 2008–Nov 2012 (USD Millions)

–453,355

400,889

94,887 96,966 234,078

1,038,587

127,937

Act

ive

Equ

ities

Pas

sive

Equ

ities

Com

mod

ities

Alte

rnat

ive

Bal

ance

d/Al

loca

tion

Taxa

ble

Bond

s

Mun

icip

al B

onds

Near-Term Expected

Global Equity Volatility (%)

CMO 1Q 2013 | 15

AllianceBernstein.com CMO 1Q 2013 | 16AllianceBernstein.com

Visibility Has Been Low, but Appears to Be Improving

Past performance is no guarantee of future results. Historical analysis is not a guarantee of future results. Left chart through October 31, 2012. Right chart through December 31, 2012 *Six-month rolling intra-market correlations of returns within the S&P 500 Index. An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio. Correlation is a statistical measure of how two values move in relation to each other. Source: Commodity Research Bureau, Credit Suisse HOLT, Energy Information Administration, IHS Global Insight, S&P, US Federal Reserve, Yahoo! and AllianceBernstein

–0.8

–0.4

0.0

0.4

0.8

67 72 77 82 87 92 97 02 07 12

Inde

x

Crude Oil

US Dollar

Correlation of S&P 500 36-Month Rolling

Macro Currents Have Receded

0.0

0.2

0.4

0.6

0.8

95 97 99 01 03 05 07 09 11

Inde

x

Stock Correlations Have Declined

US Intra-Market Correlations*

CMO 1Q 2013 | 16

AllianceBernstein.com CMO 1Q 2013 | 17AllianceBernstein.com

92%

78% 77% 87% 89%

Wor

ld

Fina

ncia

ls

Res

ourc

es

Def

ensi

ves

Cyc

lical

s

Current Long-Term Range

Valuations Are Compelling and Alpha Opportunities Are Emerging

The Value of Sector Selection

Sizable Valuation Differences Among Stocks

90

95

100

105

110

115

120

125

130

Dec

11

Feb

12

Apr

12

Jun

12

Aug

12

Oct

12

Dec

12

Gro

wth

of U

S$10

0

Dow Industrial

Financials

Consumer Discretionary

Utilities

Information Technology

0

200

400

600

800

95 97 99 01 03 05 07 09 11

Inde

x

High-ROIC Stocks

Global Equity Market

High-ROIC Stocks Have Beaten the Market**

Highest vs. Lowest Price/Book Spread by Supersector†

Market Segment Performance: 2012*

Historical analysis does not guarantee future results. Left and middle charts through December 31, 2012. Right chart as of November 30, 2012 *Sector returns based on the S&P 500 GICS sector indices. An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio **Graph shows performance of a portfolio made up of companies that are in the top 50% of the universe in terms of the following criteria: cash-flow return on capital, asset growth and potential for share-price upside on a discounted cash-flow basis. Portfolio is equally weighted and rebalanced monthly. Global equity market data are based on the equally weighted performance of a broad universe of stocks with a market capitalization in excess of US$1 billion. ROIC: Return on invested capital †Percentile ranks within the fifth (lowest) and 95th (highest) percentile of Q5/Q1 price/book spreads from January 1, 1971, to November 30, 2012. Resources consists of energy, industrial commodities and gold; defensives consists of consumer staples, medical, telecom and utilities; and cyclicals consists of capital equipment, construction and housing, consumer cyclicals, technology and transportation. Source: Center for Research in Security Prices (CRSP), Credit Suisse HOLT, MSCI, S&P/Dow Jones, Thomson Reuters, Worldscope and AllianceBernstein

CMO 1Q 2013 | 17

AllianceBernstein.com CMO 1Q 2013 | 18AllianceBernstein.com

0.2

0.6

1.0

1.4

1.8

66 71 76 81 86 91 96 01 06 11

Rat

io (×

)

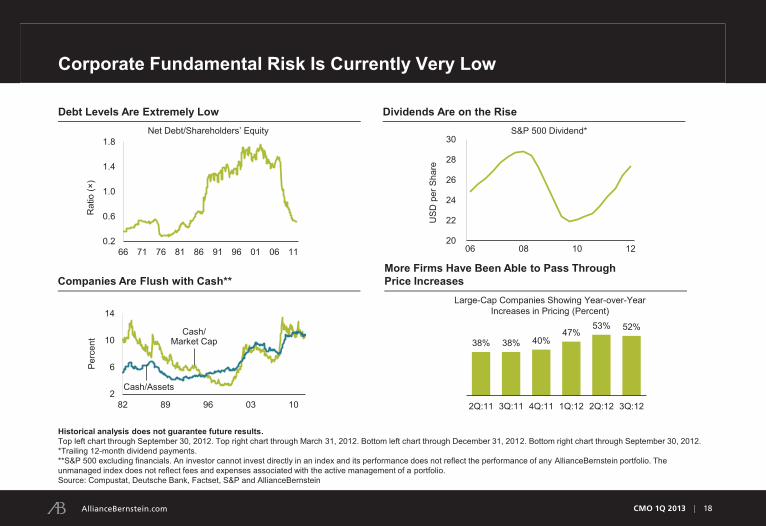

Corporate Fundamental Risk Is Currently Very Low

Historical analysis does not guarantee future results. Top left chart through September 30, 2012. Top right chart through March 31, 2012. Bottom left chart through December 31, 2012. Bottom right chart through September 30, 2012. *Trailing 12-month dividend payments. **S&P 500 excluding financials. An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio. Source: Compustat, Deutsche Bank, Factset, S&P and AllianceBernstein

Net Debt/Shareholders’ Equity

Debt Levels Are Extremely Low

Companies Are Flush with Cash**

20

22

24

26

28

30

06 08 10 12

USD

per

Sha

re

Dividends Are on the Rise

More Firms Have Been Able to Pass Through Price Increases

S&P 500 Dividend*

38% 38% 40% 47%

53% 52%

2Q:11 3Q:11 4Q:11 1Q:12 2Q:12 3Q:12

Large-Cap Companies Showing Year-over-Year Increases in Pricing (Percent)

2

6

10

14

82 89 96 03 10

Per

cent

Cash/ Market Cap

Cash/Assets

CMO 1Q 2013 | 18

AllianceBernstein.com CMO 1Q 2013 | 19AllianceBernstein.com

Current Environment Seems Right for Active Management

Past performance is no guarantee of future results. Upper and lower left charts are illustrative. Right chart through November 30, 2012 *Three-month rolling dispersion of returns within the Bernstein US large-cap universe. Capitalization-weighted; trailing-earnings yields, minus the core consumer price index **Alpha is a measure of performance on a risk-adjusted basis. Six-month rolling premium of top quartile of US large-cap managers versus the S&P 500 Index. An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio. Source: Center for Research in Security Prices, eVestment Alliance, S&P/Dow Jones and AllianceBernstein

–4

–2

0

2

4

6

8

0

10

20

30

40

50

60

95 97 99 01 03 05 07 09 11

Percent Perc

ent

Active Management Has Thrived in High Dispersion

Manager Alpha**

Dispersion (Left Scale)*

Theoretical Dispersion of Returns

Dividends Real Total

Return

Time

Ret

urns

Equities

Time

Ret

urns

Yield

High-Grade Sovereign Bonds

Real Total Return

Return Dispersion vs. Manager Alpha

CMO 1Q 2013 | 19

AllianceBernstein.com CMO 1Q 2013 | 20AllianceBernstein.com

0

20

40

60

80

95 97 99 01 03 05 07 09 11

Perc

ent

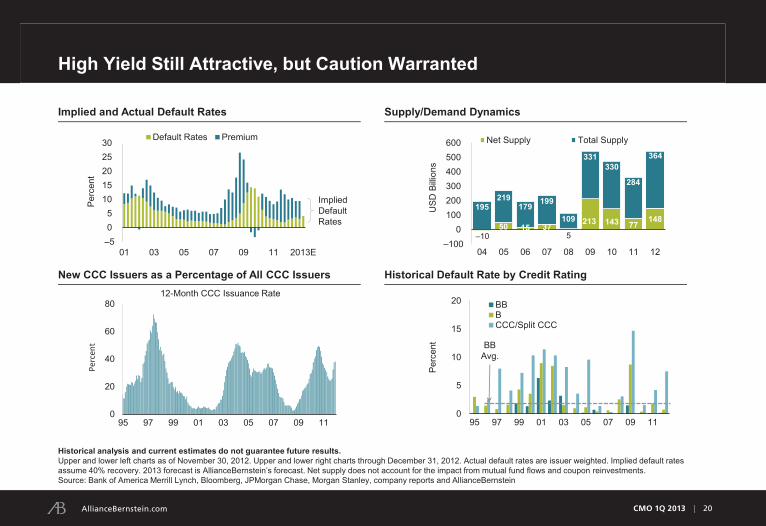

High Yield Still Attractive, but Caution Warranted

Historical analysis and current estimates do not guarantee future results. Upper and lower left charts as of November 30, 2012. Upper and lower right charts through December 31, 2012. Actual default rates are issuer weighted. Implied default rates assume 40% recovery. 2013 forecast is AllianceBernstein’s forecast. Net supply does not account for the impact from mutual fund flows and coupon reinvestments. Source: Bank of America Merrill Lynch, Bloomberg, JPMorgan Chase, Morgan Stanley, company reports and AllianceBernstein

Supply/Demand Dynamics

–10 50 15 37

5

213 143 77 148

195 219

179 199

109

331 330

284

364

–100 0

100200300400500600

04 05 06 07 08 09 10 11 12

USD

Billi

ons

Net Supply Total Supply

New CCC Issuers as a Percentage of All CCC Issuers

12-Month CCC Issuance Rate

Historical Default Rate by Credit Rating

0

5

10

15

20

95 97 99 01 03 05 07 09 11

BBBCCC/Split CCC

BB Avg.

Perc

ent

Implied Default Rates

Implied and Actual Default Rates

–5 05

1015202530

01 03 05 07 09 11 2013E

Default Rates Premium

Perc

ent

CMO 1Q 2013 | 20

AllianceBernstein.com CMO 1Q 2013 | 21AllianceBernstein.com

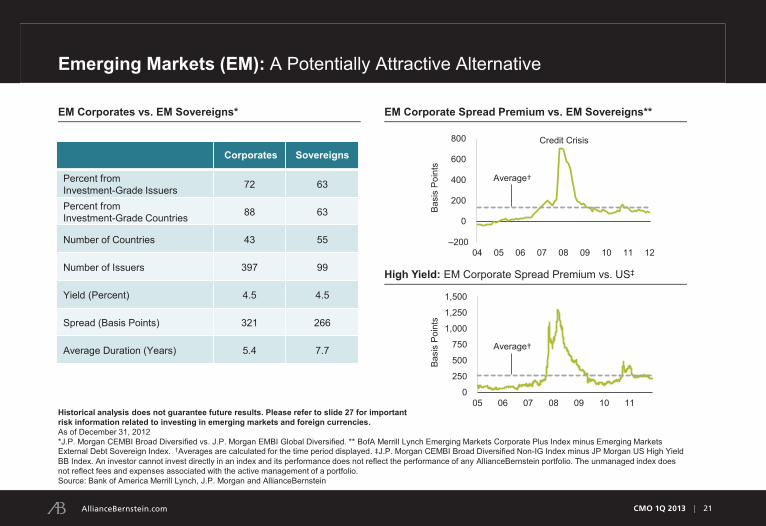

Emerging Markets (EM): A Potentially Attractive Alternative

Historical analysis does not guarantee future results. Please refer to slide 27 for important risk information related to investing in emerging markets and foreign currencies. As of December 31, 2012 *J.P. Morgan CEMBI Broad Diversified vs. J.P. Morgan EMBI Global Diversified. ** BofA Merrill Lynch Emerging Markets Corporate Plus Index minus Emerging Markets External Debt Sovereign Index. †Averages are calculated for the time period displayed. ‡J.P. Morgan CEMBI Broad Diversified Non-IG Index minus JP Morgan US High Yield BB Index. An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio. Source: Bank of America Merrill Lynch, J.P. Morgan and AllianceBernstein

EM Corporates vs. EM Sovereigns*

EM Corporate Spread Premium vs. EM Sovereigns**

High Yield: EM Corporate Spread Premium vs. US‡

Corporates Sovereigns

Percent from Investment-Grade Issuers 72 63

Percent from Investment-Grade Countries 88 63

Number of Countries 43 55

Number of Issuers 397 99

Yield (Percent) 4.5 4.5

Spread (Basis Points) 321 266

Average Duration (Years) 5.4 7.7

–200

0

200

400

600

800

04 05 06 07 08 09 10 11 12

Basi

s Po

ints

Credit Crisis

0

250

500

750

1,000

1,250

1,500

05 06 07 08 09 10 11

Basi

s Po

ints

Average†

Average†

CMO 1Q 2013 | 21

AllianceBernstein.com CMO 1Q 2013 | 22AllianceBernstein.com

Demand for Income Likely to Remain Strong

Historical analysis does not guarantee future results. As of September 30, 2012 *Average from 2005 to December 31, 2012 Source: Barclays Capital; Investment Company Institute; US Federal Reserve, Flow of Funds Accounts of the United States, 3Q:2012; and AllianceBernstein

Municipal Bonds Subject to Redemption: Next 18 Months

8.2%

18.4%

7.8%

10.7%

Investment Grade High Yield

Current Average*

Changes in Municipal Supply and Demand (USD Billions)

155

100

–53

0

69

11

–12

49

09 10 11 12

Net Supply Municipal Fund Flows

CMO 1Q 2013 | 22

AllianceBernstein.com CMO 1Q 2013 | 23AllianceBernstein.com

Municipals Seem Attractive vs. Taxable Bonds

Past performance and historical analysis do not guarantee future results. As of October 31, 2012 There is no guarantee that this, or any, investment strategy will be successful in the short or long term. *Roll is the natural price gain that a bond experiences as it ages, assuming interest rates are unchanged. Source: Barclays Capital, Bloomberg, Delphis Hanover, Municipal Market Data and AllianceBernstein

Yield Plus Roll:* A-Rated Municipals

0.5%

1.7%

2.9% 3.1%

3.4%

2.7%

3.1% 2.9%

2 5 8 9 10 15 20 30

Yield Roll

Maturity (Years)

0

1

2

3

4

5

Short Intermediate Long

After-Tax Yield Curves

A-Rated Corporates 35% Federal + 5% State Tax Yi

eld

(Per

cent

)

A-Rated Municipals 5% State Tax

Adding Short Corporate Bonds to Municipal Portfolios

Income Advantage of BBB-Rated over AAA-Rated Municipals

0

1

2

3

4

87 92 97 02 07 12

Perc

ent

Dec. 31, 2012 1.4%

Average 1.0%

CMO 1Q 2013 | 23

AllianceBernstein.com CMO 1Q 2013 | 24AllianceBernstein.com

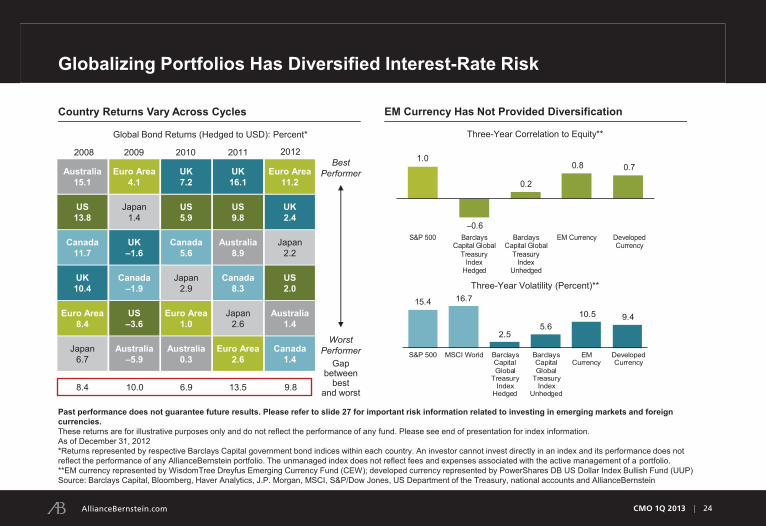

Australia 8.9

Canada 8.3

UK 16.1

Japan 2.6

US 9.8

Globalizing Portfolios Has Diversified Interest-Rate Risk

Euro Area 1.0

US 5.9

Japan 2.9

UK 7.2

Australia 0.3

Canada 5.6

Japan 1.4

UK –1.6

US –3.6

Euro Area 4.1

Australia –5.9

Canada –1.9

2009 2008

UK 10.4

Euro Area 8.4

Australia 15.1

US 13.8

Japan 6.7

Canada 11.7

Euro Area 2.6

2011

9.8 8.4 10.0 6.9

Country Returns Vary Across Cycles

Global Bond Returns (Hedged to USD): Percent*

2010

13.5

Best Performer

Worst Performer

Gap between

best and worst

Past performance does not guarantee future results. Please refer to slide 27 for important risk information related to investing in emerging markets and foreign currencies. These returns are for illustrative purposes only and do not reflect the performance of any fund. Please see end of presentation for index information. As of December 31, 2012 *Returns represented by respective Barclays Capital government bond indices within each country. An investor cannot invest directly in an index and its performance does not reflect the performance of any AllianceBernstein portfolio. The unmanaged index does not reflect fees and expenses associated with the active management of a portfolio. **EM currency represented by WisdomTree Dreyfus Emerging Currency Fund (CEW); developed currency represented by PowerShares DB US Dollar Index Bullish Fund (UUP) Source: Barclays Capital, Bloomberg, Haver Analytics, J.P. Morgan, MSCI, S&P/Dow Jones, US Department of the Treasury, national accounts and AllianceBernstein

2012

Euro Area 11.2

US 2.0

Canada 1.4

Australia 1.4

UK 2.4

Japan 2.2

1.0

–0.6

0.2

0.8 0.7

S&P 500 BarclaysCapital Global

TreasuryIndex

Hedged

BarclaysCapital Global

TreasuryIndex

Unhedged

EM Currency DevelopedCurrency

15.4 16.7

2.55.6

10.5 9.4

S&P 500 MSCI World BarclaysCapitalGlobal

TreasuryIndex

Hedged

BarclaysCapitalGlobal

TreasuryIndex

Unhedged

EMCurrency

DevelopedCurrency

Three-Year Correlation to Equity**

Three-Year Volatility (Percent)**

EM Currency Has Not Provided Diversification

CMO 1Q 2013 | 24

AllianceBernstein.com CMO 1Q 2013 | 25AllianceBernstein.com

The Big Picture

There was much talk about things to fear in 2012

Fundamentals have continued to improve, particularly in the US

In key countries, headwinds have eased, but more work remains

In the “three worlds”* balance remains key, with important emphases:

Safety: be efficient

Income/Cash Flow: be selective

Appreciation: be active

As of December 31, 2012 *Referring to the potential market environments on slide 14 Source: AllianceBernstein

CMO 1Q 2013 | 25

AllianceBernstein.com CMO 1Q 2013 | 26AllianceBernstein.com

Important Mutual Fund Information

Investors should consider the investment objectives, risks, charges and expenses of any Fund/Portfolio carefully before investing. For copies of our prospectus or summary prospectus, which contain this and other information, visit us online at www.alliancebernstein.com or contact your AllianceBernstein Investments representative. Please read the prospectus and/or summary prospectus carefully before investing.

AllianceBernstein Investments, Inc. (ABI) is the distributor of the AllianceBernstein family of mutual funds. ABI is a member of FINRA and is an affiliate of AllianceBernstein L.P., the manager of the funds.

CMO 1Q 2013 | 26

AllianceBernstein.com CMO 1Q 2013 | 27AllianceBernstein.com

Important Risk Information Related to Investing in Emerging Markets and Foreign Currencies

Investing in emerging-market debt poses risks, including those generally associated with fixed-income investments. Fixed-income securities may lose value due to market fluctuations or changes in interest rates. Longer maturity bonds are more vulnerable to rising interest rates. A bond issuer’s credit rating may be lowered due to deteriorating financial condition, which may result in losses and potentially default or failure to meet payment obligations. The default probability is higher in bonds with lower, non-investment-grade ratings (commonly known as “junk bonds”). There are other potential risks when investing in emerging-market debt. Non-US securities may be more volatile because of the associated political, regulatory, market and economic uncertainties; these risks can be magnified in emerging-market securities. Emerging-market bonds may also be exposed to fluctuating currency values. If a bond’s currency weakens against the US dollar, this can negatively affect its value when translated back into US dollar terms.

CMO 1Q 2013 | 27

AllianceBernstein.com CMO 1Q 2013 | 28AllianceBernstein.com

Index Definitions

Barclays Capital Global Aggregate–Corporate Index: Tracks the performance of investment-grade corporate bonds publicly issued in the global market found in the Global Aggregate. (Represents Global Corporates on slide 4.)

Barclays Capital Global Emerging Markets Index: Represents the union of the USD-denominated U.S. Emerging Markets Index and the predominately EUR-denominated Pan Euro Emerging Markets Index, covering emerging markets in the Americas, Europe, Middle East, Africa and Asia. (Represents Emerging-Market Debt on slide 4.)

Barclays Capital Global High Yield Index: Provides a broad-based measure of the global high-yield fixed-income markets. It represents the union of the U.S. High Yield, Pan European High Yield, U.S. Emerging Markets High Yield, CMBS High Yield and Pan European Emerging Markets High Yield Indices. (Represents Global High Yield on slide 4.)

Barclays Capital Global Treasury: Australia Bond Index: Includes fixed-rate, local-currency sovereign debt that makes up the Australian Treasury sector of the Global Aggregate Index.

Barclays Capital Global Treasury: Canada Bond Index: Includes fixed-rate, local-currency sovereign debt that makes up the Canadian Treasury sector of the Global Aggregate Index.

Barclays Capital Global Treasury: Euro Bond Index: Includes fixed-rate, local-currency sovereign debt that makes up the Euro Area Treasury sector of the Global Aggregate Index. (Represents Euro Area Gov’t on slide 4.)

Barclays Capital Global Treasury: Japan Bond Index: Includes fixed-rate, local-currency sovereign debt that makes up the Japanese Treasury sector of the Global Aggregate Index. (Represents Japan Gov’t on slide 4.)

Barclays Capital Global Treasury: United Kingdom Bond Index: Includes fixed-rate, local-currency sovereign debt that makes up the UK Treasury sector of the Global Aggregate Index.

Barclays Capital Municipal Bond Index: A rules-based, market value–weighted index engineered for the long-term tax-exempt bond market. (Represents Municipals on slide 4.)

Barclays Capital U.S. Treasury–U.S. TIPS Index: Consists of inflation-protected securities issued by the US Treasury. (Represents TIPS on slide 4.)

Barclays Capital U.S. Treasury Index: Includes fixed-rate, local-currency sovereign debt that makes up the US Treasury sector of the Global Aggregate Index. (Represents US Gov’t on slide 4.)

Following are definitions of the indices referred to in this presentation. It is important to recognize that all indices are unmanaged and do not reflect fees and expenses associated with the active management of a mutual fund portfolio. Investors cannot invest directly in an index, and its performance does not reflect the performance of any AllianceBernstein mutual fund.

CMO 1Q 2013 | 28

AllianceBernstein.com CMO 1Q 2013 | 29AllianceBernstein.com

Index Definitions (continued)

BofA Merrill Lynch Emerging Markets Corporate Plus Index: This index tracks the performance of US dollar– and Euro–denominated emerging-markets non-sovereign debt publicly issued within the major domestic and Eurobond markets.

DJ-UBS Total Return Commodity Index: Consists of exchange-traded futures on 19 physical commodities that are weighted to account for economic significance and market liquidity. (Represents Commodities on slide 4.)

FTSE EPRA/NAREIT Global Real Estate Index: Designed to represent general trends in eligible real estate equities worldwide. (Represents Global REITs on slide 4.)

J.P. Morgan Corporate Emerging Markets Bond Index–Broad Diversified: This index is a global, liquid corporate emerging-market benchmark that tracks US dollar–denominated corporate bonds issued by emerging-market entities. It includes smaller issues to cover a wider array of corporate bonds.

J.P. Morgan Emerging Markets Bond Index Global Diversified: Limits the weights of countries with larger debt stocks by only including a specified portion of these countries' eligible current face amounts of debt outstanding.

MSCI EAFE Index: A free float–adjusted, market capitalization–weighted index designed to measure developed-market equity performance, excluding the US and Canada. It consists of 22 developed-market country indices. (Represents EAFE on slide 4.)

MSCI Emerging Markets Index: A free float–adjusted, market capitalization–weighted index designed to measure equity-market performance in the global emerging markets. It consists of 21 emerging-market country indices. (Represents Emerging Markets on slide 4.)

Russell 2000 Index: Measures the performance of the small-cap segment of the US equity universe. It is a subset of the Russell 3000 Index representing approximately 8% of the total market capitalization of that index. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. (Represents US Small-Cap on slide 4.)

S&P 500 Index: Includes a representative sample of 500 leading companies in leading industries of the US economy. (Represents US Large-Cap on slide 4.)

The WisdomTree Dreyfus Emerging Currency Fund (CEW): Includes the following constituent currencies: Mexican peso, Brazilian real, Chilean peso, South African rand, Polish zloty, Russian ruble, Turkish new lira, Chinese yuan, South Korean won, Indonesian rupiah, Indian rupee and Malaysian ringgit.

The PowerShares DB US Dollar Index Bullish Fund (UUP): Designed for investors who want a cost-effective and convenient way to track the value of the US dollar relative to a basket of the six major world currencies—the euro, yen, British pound, Canadian dollar, Swedish krona and Swiss franc (collectively, the “Basket Currencies”).

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices, any securities or financial products. This report is not approved, reviewed or produced by MSCI.

CMO 1Q 2013 | 29