Embed Size (px)

Citation preview

March 2013

2012 Annual Results

Presentation

Disclaimer

2

Forward-Looking Statements

This presentation contains certain forward-looking statements with respect to the financial condition, results of operations and business of Lianhua Supermarket, the chain retailing industry in the PRC and certain of the plans and objectives of the management of Lianhua Supermarket. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results or performance of Lianhua Supermarket to be materially different from any future results or performance expressed or implied by such forward-looking statements. Such forward-looking statements were based on the assumptions regarding Lianhua Supermarket’s present and future business strategies and the political and economic environment in which Lianhua Supermarket and its subsidiaries will operate in the future. Reliance should not be placed on these forward-looking statements, which reflect the view of Lianhua Supermarket’s management as of the date of this presentation only.

Agenda

3

3

2

1 Market Overview

2 Financial Review

3 Business Review

4 Business Strategy

5 Q & A

Market Overview

Growth of Disposable Income of Urban Residents

5

Market Overview

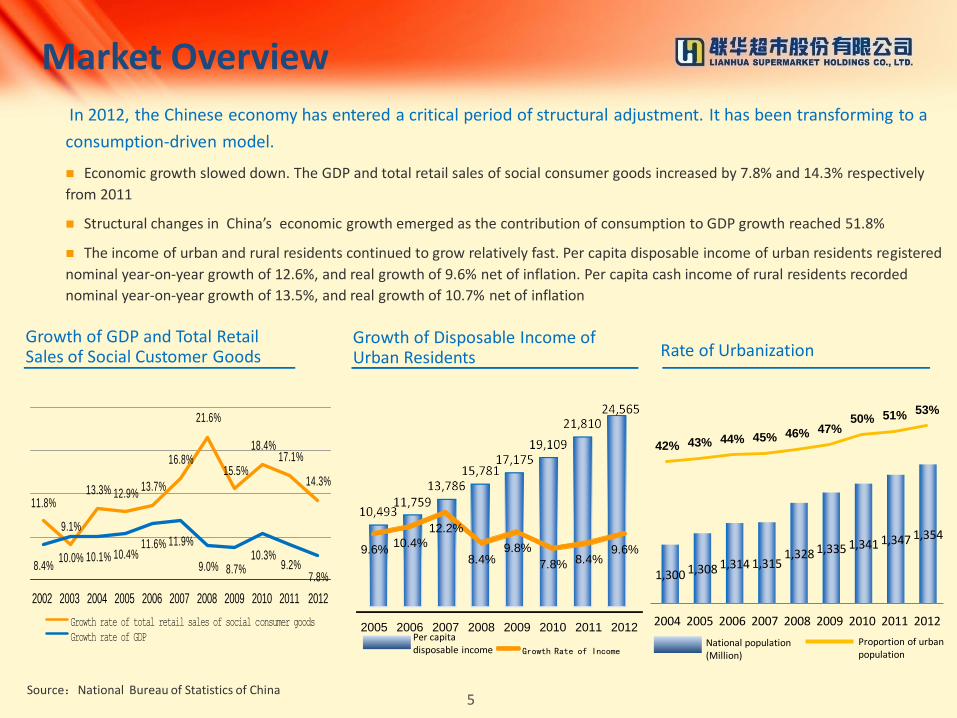

In 2012, the Chinese economy has entered a critical period of structural adjustment. It has been transforming to a

consumption-driven model.

Economic growth slowed down. The GDP and total retail sales of social consumer goods increased by 7.8% and 14.3% respectively

from 2011

Structural changes in China’s economic growth emerged as the contribution of consumption to GDP growth reached 51.8%

The income of urban and rural residents continued to grow relatively fast. Per capita disposable income of urban residents registered

nominal year-on-year growth of 12.6%, and real growth of 9.6% net of inflation. Per capita cash income of rural residents recorded

nominal year-on-year growth of 13.5%, and real growth of 10.7% net of inflation

Per capita disposable income

Growth of GDP and Total Retail Sales of Social Customer Goods Rate of Urbanization

National population (Million)

Proportion of urban population

1,300 1,308 1,314 1,315 1,328 1,335 1,341 1,347 1,354

42% 43% 44% 45% 46% 47% 50% 51% 53%

2004 2005 2006 2007 2008 2009 2010 2011 2012

11.8%

9.1%

13.3% 12.9%13.7%

16.8%

21.6%

15.5%

18.4%17.1%

14.3%

8.4%10.0% 10.1% 10.4%

11.6% 11.9%

9.0% 8.7%10.3%

9.2%7.8%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Growth rate of total retail sales of social consumer goods

Growth rate of GDP

Source:National Bureau of Statistics of China

9.6% 10.4%

12.2%

8.4% 9.8%

7.8% 8.4% 9.6%

2005 2006 2007 2008 2009 2010 2011 2012

Growth Rate of Income

0%

5%

10%

15%

20%

25%

Consumer Price Index

6

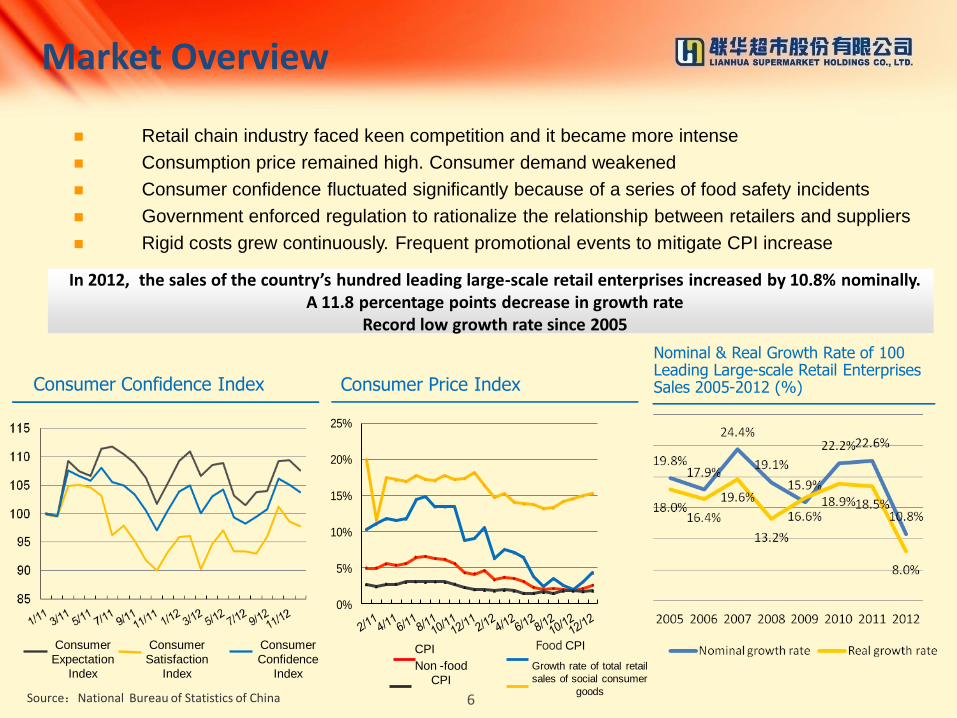

Retail chain industry faced keen competition and it became more intense

Consumption price remained high. Consumer demand weakened

Consumer confidence fluctuated significantly because of a series of food safety incidents

Government enforced regulation to rationalize the relationship between retailers and suppliers

Rigid costs grew continuously. Frequent promotional events to mitigate CPI increase

Nominal & Real Growth Rate of 100 Leading Large-scale Retail Enterprises Sales 2005-2012 (%)

Market Overview

Non -food

CPI

Food CPI

Growth rate of total retail

sales of social consumer

goods

CPI

Source:National Bureau of Statistics of China

Consumer

Expectation

Index

Consumer

Satisfaction

Index

Consumer

Confidence

Index

Consumer Confidence Index

In 2012, the sales of the country’s hundred leading large-scale retail enterprises increased by 10.8% nominally. A 11.8 percentage points decrease in growth rate

Record low growth rate since 2005

Financial Review

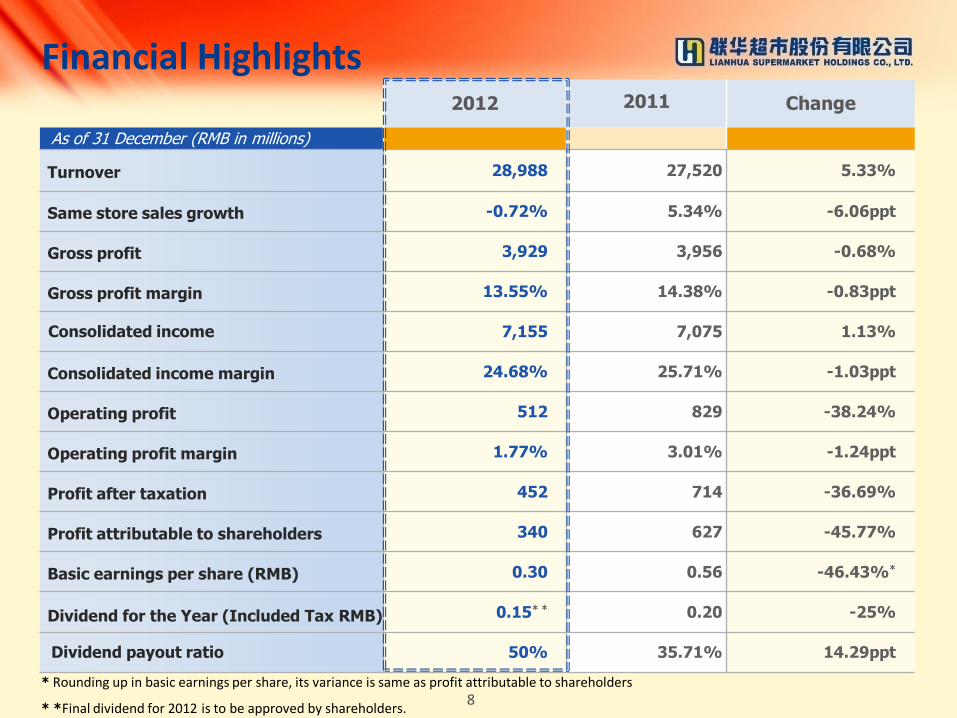

2012 2011 Change

As of 31 December (RMB in millions)

Turnover 28,988 27,520 5.33%

Same store sales growth -0.72% 5.34% -6.06ppt

Gross profit 3,929 3,956 -0.68%

Gross profit margin 13.55% 14.38% -0.83ppt

Consolidated income 7,155 7,075 1.13%

Consolidated income margin 24.68% 25.71% -1.03ppt

Operating profit 512 829 -38.24%

Operating profit margin 1.77% 3.01% -1.24ppt

Profit after taxation 452 714 -36.69%

Profit attributable to shareholders 340 627 -45.77%

Basic earnings per share (RMB) 0.30 0.56 -46.43%*

Dividend for the Year (Included Tax RMB) 0.15* * 0.20 -25%

Dividend payout ratio 50% 35.71% 14.29ppt

Financial Highlights

8 * Rounding up in basic earnings per share, its variance is same as profit attributable to shareholders

* *Final dividend for 2012 is to be approved by shareholders.

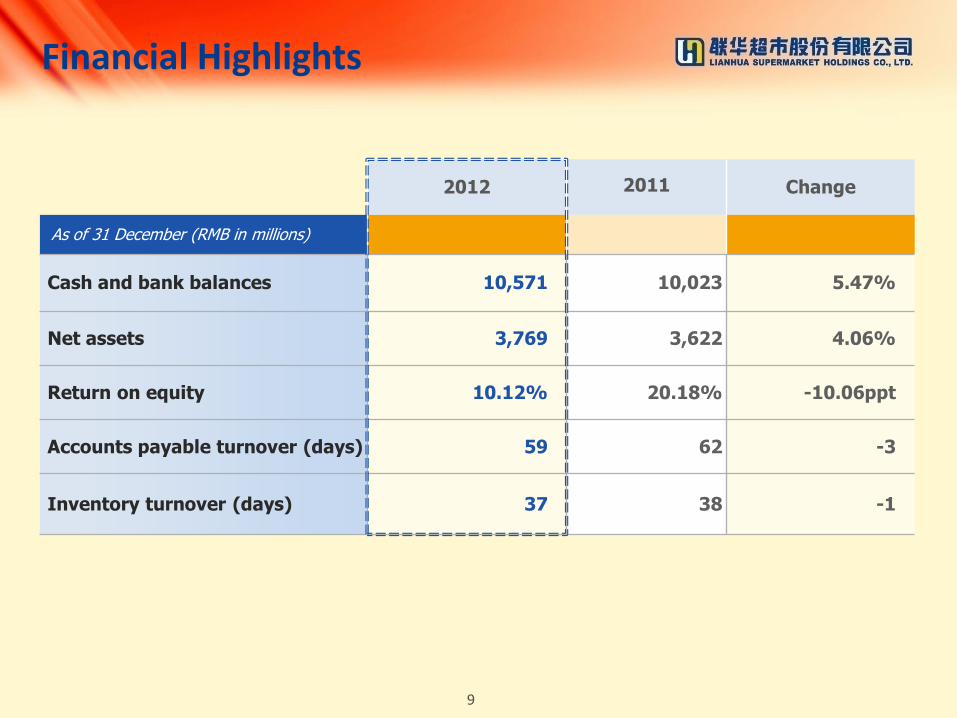

2012 2011 Change

As of 31 December (RMB in millions)

Cash and bank balances 10,571 10,023 5.47%

Net assets 3,769 3,622 4.06%

Return on equity 10.12% 20.18% -10.06ppt

Accounts payable turnover (days) 59 62 -3

Inventory turnover (days) 37 38 -1

Financial Highlights

9

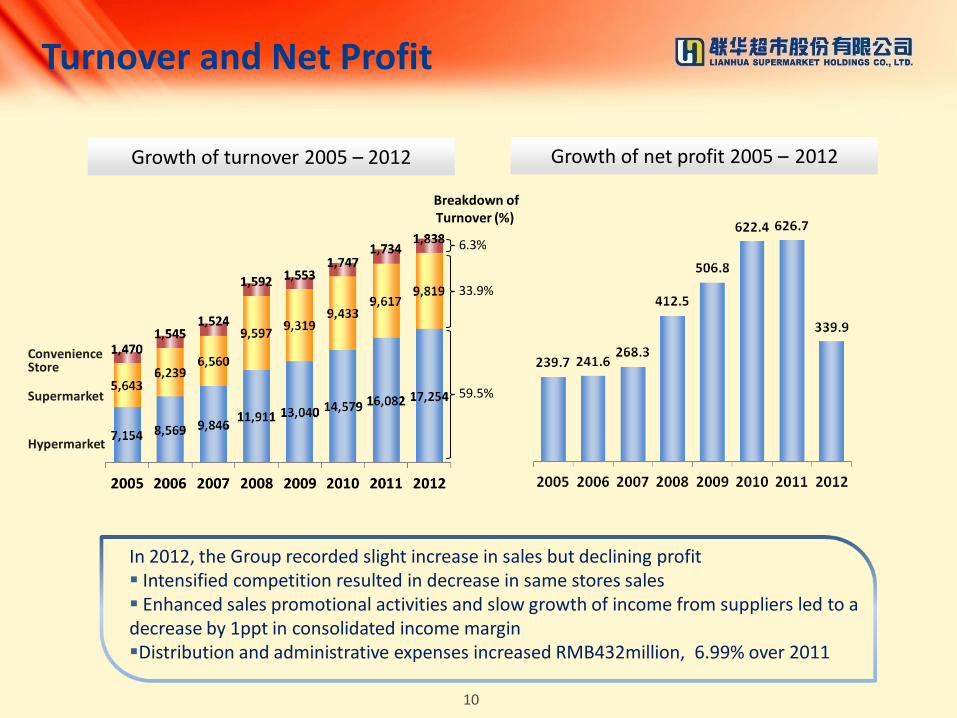

Growth of turnover 2005 – 2012

59.5%

6.3%

33.9%

Turnover and Net Profit

10

Growth of net profit 2005 – 2012

In 2012, the Group recorded slight increase in sales but declining profit Intensified competition resulted in decrease in same stores sales Enhanced sales promotional activities and slow growth of income from suppliers led to a decrease by 1ppt in consolidated income margin Distribution and administrative expenses increased RMB432million, 6.99% over 2011

Convenience Store

Supermarket

Hypermarket

Breakdown of Turnover (%)

2012 2011 Change

As of 31 December (RMB in millions)

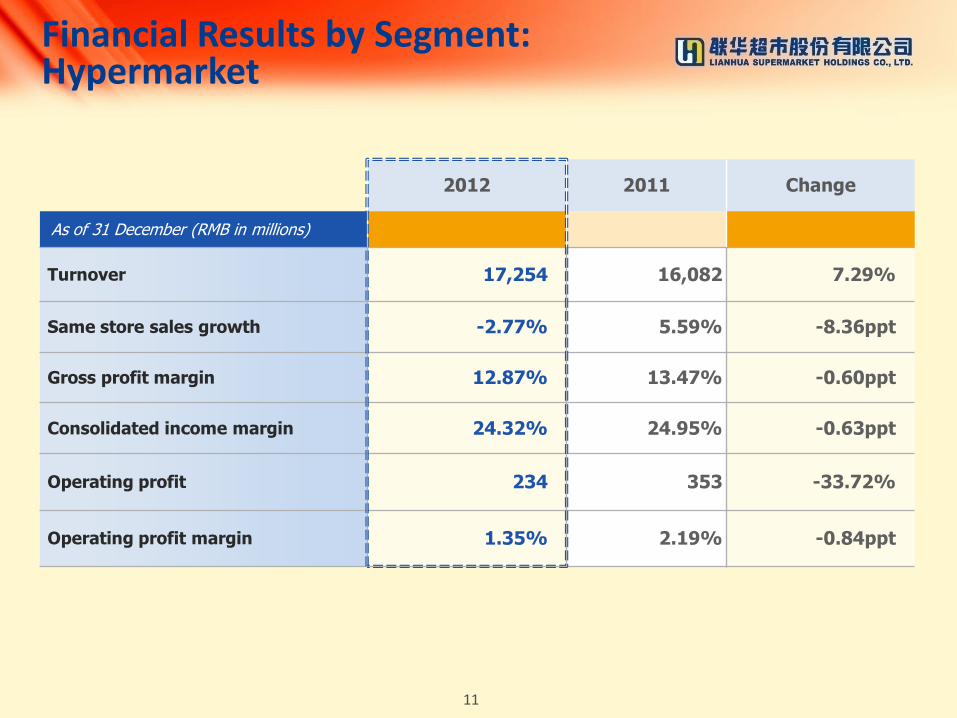

Turnover 17,254 16,082 7.29%

Same store sales growth -2.77% 5.59% -8.36ppt

Gross profit margin 12.87% 13.47% -0.60ppt

Consolidated income margin 24.32% 24.95% -0.63ppt

Operating profit 234 353 -33.72%

Operating profit margin 1.35% 2.19% -0.84ppt

Financial Results by Segment: Hypermarket

11

2012 2011 Change

As of 31 December (RMB in millions)

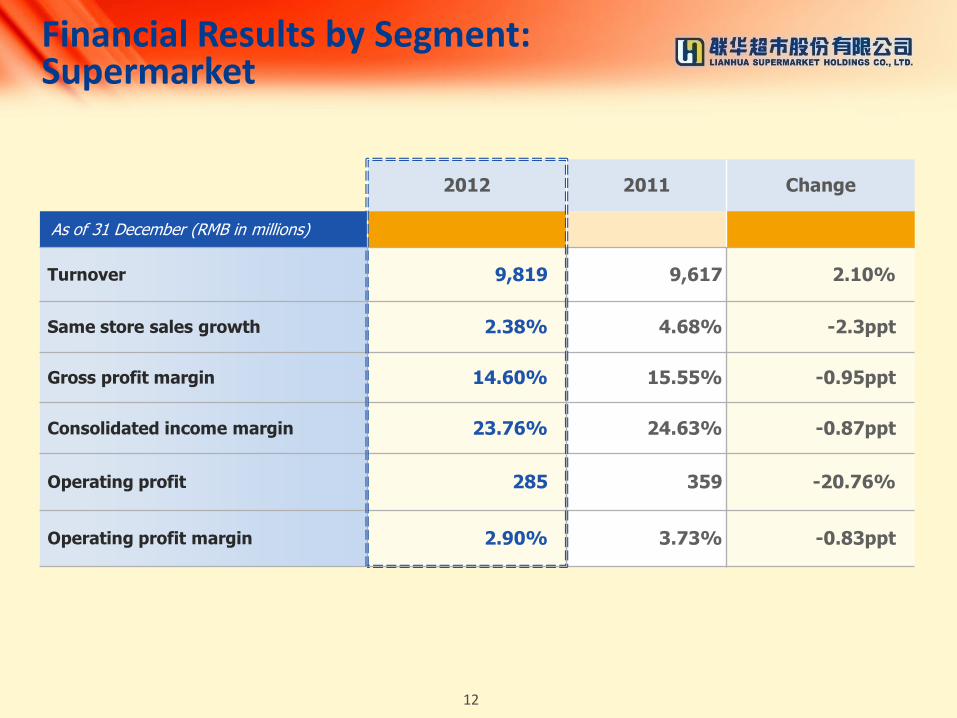

Turnover 9,819 9,617 2.10%

Same store sales growth 2.38% 4.68% -2.3ppt

Gross profit margin 14.60% 15.55% -0.95ppt

Consolidated income margin 23.76% 24.63% -0.87ppt

Operating profit 285 359 -20.76%

Operating profit margin 2.90% 3.73% -0.83ppt

Financial Results by Segment: Supermarket

12

2012 2011 Change

As of 31 December (RMB in millions)

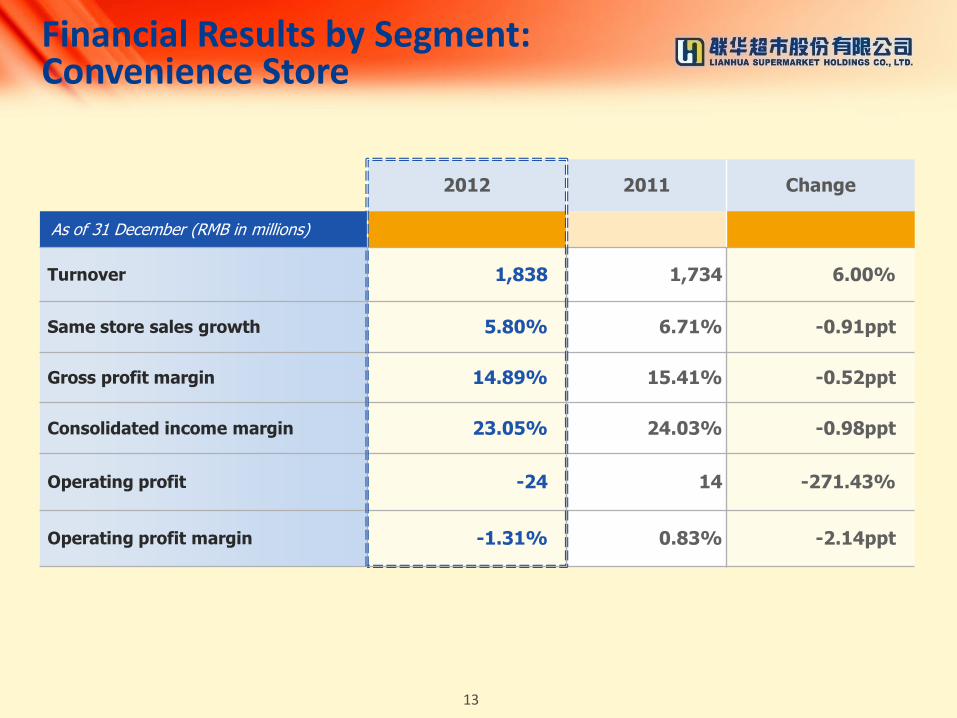

Turnover 1,838 1,734 6.00%

Same store sales growth 5.80% 6.71% -0.91ppt

Gross profit margin 14.89% 15.41% -0.52ppt

Consolidated income margin 23.05% 24.03% -0.98ppt

Operating profit -24 14 -271.43%

Operating profit margin -1.31% 0.83% -2.14ppt

Financial Results by Segment: Convenience Store

13

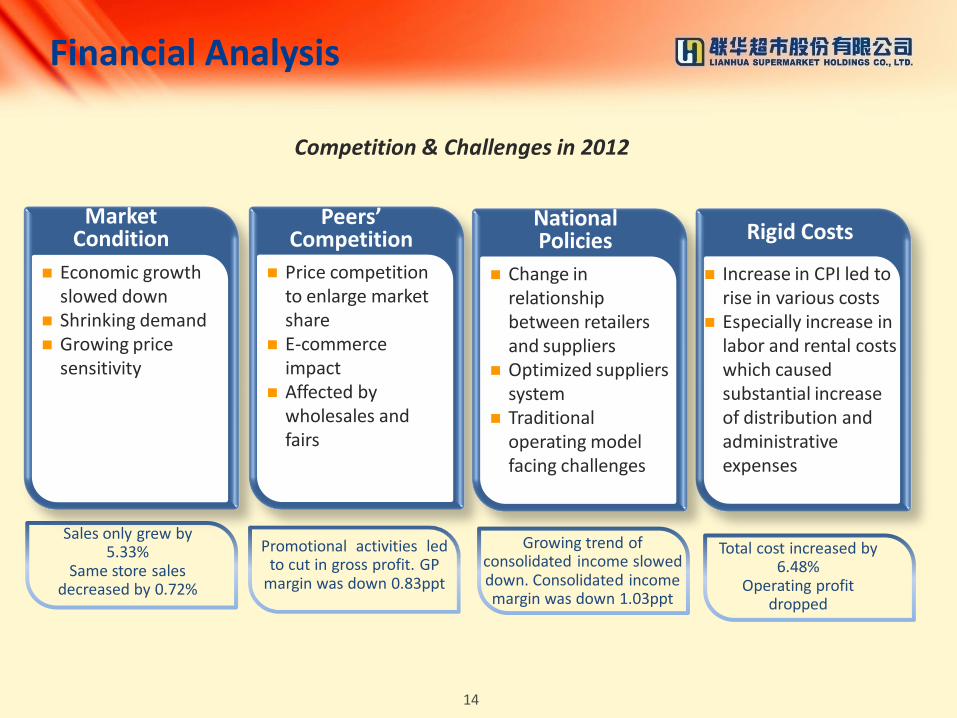

Competition & Challenges in 2012

经济增速放缓

市场需求萎缩

价格敏感上升

添加内容

Market Condition

Rigid Costs

Price competition to enlarge market share

E-commerce impact

Affected by wholesales and fairs

Economic growth slowed down

Shrinking demand Growing price

sensitivity

Change in relationship between retailers and suppliers

Optimized suppliers system

Traditional operating model facing challenges

Increase in CPI led to rise in various costs

Especially increase in labor and rental costs which caused substantial increase of distribution and administrative expenses

Financial Analysis

Sales only grew by 5.33%

Same store sales decreased by 0.72%

Promotional activities led to cut in gross profit. GP

margin was down 0.83ppt

Growing trend of consolidated income slowed down. Consolidated income margin was down 1.03ppt

Total cost increased by 6.48%

Operating profit dropped

14

Peers’ Competition

National Policies

Business Review

16

Open 12 new stores

Enhance success rate in outlet development and explore new businesses

continued to consolidate market share in Eastern China in line with its strategic goal of “Becoming a Regional Leader”

Open 226 new stores Directly-operated: 78 Franchised: 148

Accelerated transformation of existing stores

Explored the development of high- end outlets

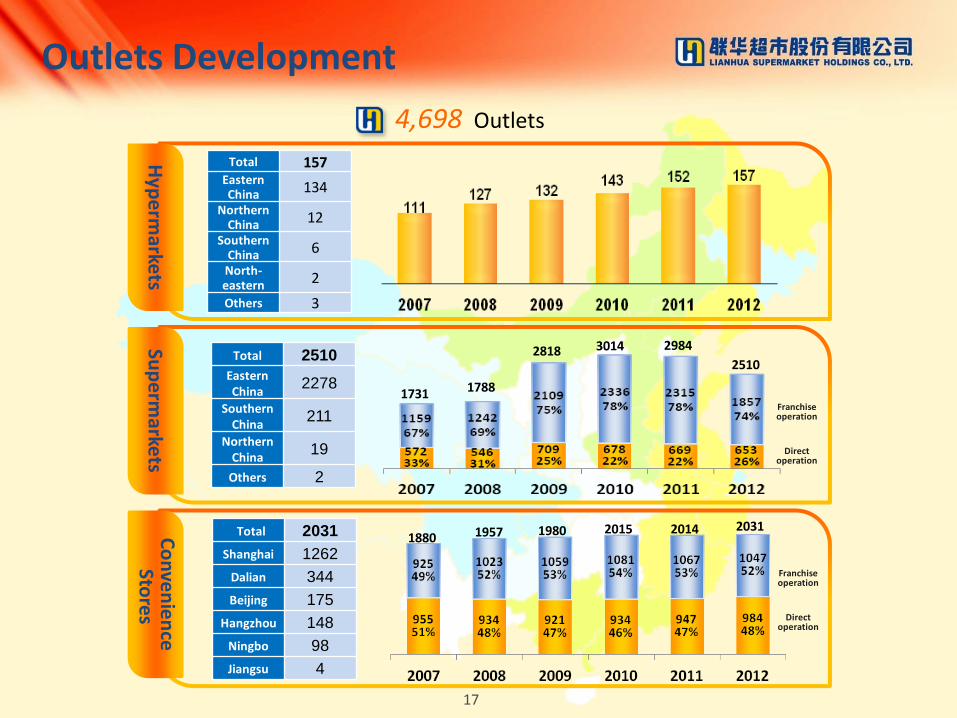

As of 31 December 2012, the Group has a total of 4,698 outlets

Approximately 84% were located in Eastern China

Outlet Development

Convenience Stores

Open 156 new stores Directly-operated: 21 Franchised: 135

Strictly monitored and controlled outlets quality

Maintained the scale of directly-operated stores and accelerated optimization of franchised stores

Hypermarkets Supermarkets

Outlets Development

4,698 Outlets

1731 1788

2818 3014 2984

2510

1980 2015 2014 2031 1957 1880

Total 157 Eastern China 134

Northern China 12

Southern China 6

North-eastern 2

Others 3

Hyp

erm

arkets

Total 2510

Eastern China

2278

Southern China

211

Northern China

19

Others 2

Sup

erm

arkets

Co

nve

nie

nce

Sto

res

Total 2031

Shanghai 1262

Dalian 344

Beijing 175

Hangzhou 148

Ningbo 98

Jiangsu 4

Franchise operation

Direct operation

Franchise operation

Direct operation

17

Outlet Development

Shanghai: 2902

Jiangsu:402

Zhejiang :525

Maintaining leading position in Eastern China

18

Cope with challenges through structure optimization

Driving sales growth with promotions and marketing efforts

Focused on daily necessities with a

series of large scale promotions

Launched large scale marketing

events with strategic allies of

suppliers

Enhanced member loyalty with

tailored marketing efforts

Cope with challenges through proactive marketing and promotions

Expanded direct purchase from farms

to improve the quality and price

perception of fresh produce

Focused substantial resources on key

outlets and increased their revenue

contribution

Expanded the procurement and sales

of imported merchandise and private

label products to improve gross profit

19

Cope with challenges through innovation

Exploring synergies of online and

offline business in E-commerce

Positive feedbacks on four newly

opened "Sakura Kobo“ cosmeceutical

stores

Completed the roof of main structure

of Jiangqiao logistics center and

launched new fresh produce

processing and distribution center in

Zhejiang Province

Strengthening competitiveness through innovation

Trials of large scale hypermarket outlets offering more functions to customers

Tightened the management of franchised supermarkets and opened more high-end convenient stores

Upgraded membership system and improved information analysis abilities-making progress on membership system construction

Cope with challenges through transformation

20

Improve information and technology system

Extended B2B platform to all

three main business

segments

Completed the upgrade of

the information systems in

franchised stores to provide

extra “Guarantee” for food

safety

Established intelligent asset

engineering management

system

Optimized unified

settlement system and

realized supplier information

sharing to strengthen

business analysis capability

Centralised cash

management and put in

place effective budgeting

plan to increase the

utilization efficiency of

capital.

Improving operations with internal reforms

Accelerated the functional and organizational integration of procurement system

Optimized business flow,

logistics, information, and operation systems; Standardized and optimized the process to increase efficiency

Leverage economy of scale

Strengthen unified settlement system

21

Improving operational standards & Strengthening internal control

Refined and optimized channel fees from suppliers

Improve self-operation of selling fresh

produce

Strengthen “Central Kitchen” to centralize

food processing

Pushing forward new operation models

Establish food safety laboratories in certain

hypermarket stores and increased the

frequency of spot checks

Utilized information system to get better

and accurate supplier information

Installed a pork and vegetable tracking

system

Strengthened quality control Emphasizing on performance & efficiency

22

Standardized and streamlined income

from suppliers based on regulations

from Six ministries and commissions

Improve business model achieve win-

win for all parties

Tightened performance and compensation linkage

Enhanced training on key positions and job rotation system

Cultivated highly skilled front-line staff in order to improve the overall quality of employees

Business Strategy

Business Strategy

Improve profitability through innovation

Optimize business structure and consolidate competitive advantages

Reform to make breakthroughs and

optimize the system

Tighten cost

control and improve

efficiency

24

Optimize development structure, tighten property management standards for searching new outlets and

provide better training and supports to new outlets

Optimize franchise outlet structure and gradually increase the proportion of franchised stores in

convenience store segment

Optimize pricing structure, focusing on growing sales and gross margin at the same pace

Optimize merchandise structure , aiming to increase the consolidated income level

Optimize suppliers structure, making adjustment on certain operational procedures

Business Strategy

25

Optimize business structures and consolidate competitive advantages

Focus on fresh produce, increasing direct sourcing from farms

Strengthen the link between production and marketing; optimize merchandises management

based on the positioning of stores

Unify business management platform and make full use of information system

Accelerate the construction of Jiangqiao logistics center and aim to put into trial operation by the

end of 2013

Reform to make breakthroughs and optimize the system

Focus on boosting sales, improve profit model and optimize profit stream

Change management philosophy, clarify strategies for different merchandise, focus on sales

increase of core merchandise categories and items

Continue to expand members and improve the comprehensiveness of the database, enhancing

marketing campaign targeting members

Push forward the development of new business and create synergies with existing segments

Business Strategy

26

Improve profitability through innovation

Lower management costs by structure optimization and providing better services to frontline

Optimize workflow and strictly control expenses

Improve cash management by leveraging the centralized cash management

Tighten cost control and improve efficiency

Q & A

Thank you!