Embed Size (px)

Citation preview

8/4/2019 20110916 weekly

http://slidepdf.com/reader/full/20110916-weekly 1/10

Markets for the Week ending

16-Sep-2011 1.00 0.09 1.50 0.50 - 0.10 4.75 2.25 21.50

9-Sep-2011 1.00 0.09 1.50 0.50 - 0.10 4.75 2.25 21.50

30-Jun-2011 1.00 0.07 1.25 0.50 0.25 0.10 4.75 2.25 21.50

31-Dec-2010 1.00 0.13 1.00 0.50 0.25 0.10 4.75 2.25 18.50

weekly change - - - - - - - - -

YTD change - (0.04) 0.50 - (0.25) - - - 3.00

1yr forward (OIS) (0.22) (0.03) (0.21) (0.14) 0.03 (1.40)

16-Sep-2011 1.04 1.56 2.28 2.92 2.11 0.00 0.17 0.92 2.06

9-Sep-2011 0.79 1.29 2.11 2.81 2.11 0.01 0.17 0.80 1.92

30-Jun-2011 1.59 2.33 3.11 3.55 2.52 0.02 0.46 1.76 3.16

31-Dec-2010 1.68 2.42 3.12 3.53 2.41 0.13 0.60 2.01 3.30

52-week closing high 1.94 2.90 3.50 3.87 2.70 0.17 0.85 2.40 3.74

52-week closing low 0.79 1.29 2.11 2.81 2.09 (0.01) 0.17 0.80 1.92 weekly change 0.25 0.26 0.17 0.11 0.01 (0.01) - 0.12 0.14

QTD change (0.56) (0.78) (0.83) (0.63) (0.40) (0.01) (0.29) (0.84) (1.10)

YTD change (0.64) (0.87) (0.84) (0.61) (0.30) (0.12) (0.43) (1.09) (1.23)

change from 52wk high (0.91) (1.34) (1.22) (0.95) (0.59) (0.16) (0.68) (1.48) (1.68)

change from 52wk low 0.25 0.26 0.17 0.11 0.03 0.01 - 0.12 0.14

China

Reserve

Requirement

US 10yr

September 16,

Royal Bank

of Australia

China

Rediscount

Rate Braz

Bank of

Canada

U.S. Federal

Reserve

European

Central Bank

Bank of

England

Swiss Bank

Rate

Bank of

Japan

US 2yr US 5yrGoC 10yr GoC 30yr RRB BEIR

Monetary Policy

North American

Bond Yields GoC 2yr GoC 5yr US 3mth

16-Sep-2011 0.91 0.92 1.04 1.02 0.89 0.89 1.02 1.00 2.67

9-Sep-2011 0.91 0.93 1.05 1.03 0.89 0.90 1.03 1.01 2.65 30-Jun-2011 0.73 0.81 0.82 0.87 0.76 0.76 0.86 0.84 2.29

31-Dec-2010 0.67 0.80 0.78 0.87 0.74 0.73 0.87 0.85 2.15

52-week closing high 0.92 0.94 1.05 1.03 0.91 0.91 1.04 1.02 2.78

52-week closing low 0.64 0.73 0.72 0.79 0.65 0.65 0.78 0.77 2.03

weekly change (0.00) (0.01) (0.01) (0.01) (0.00) (0.01) (0.01) (0.01) 0.02

QTD change 0.18 0.11 0.22 0.15 0.12 0.13 0.15 0.16 0.38

YTD change 0.24 0.12 0.26 0.15 0.15 0.16 0.15 0.15 0.52

change from 52wk high (0.01) (0.03) (0.01) (0.01) (0.02) (0.02) (0.02) (0.02) (0.11)

change from 52wk low 0.27 0.19 0.31 0.23 0.24 0.24 0.23 0.23 0.64

16-Sep-2011 1.01 2.48 1.86 2.60 5.51 5.29 11.18 21.19 1.01

9-Sep-2011 1.01 2.26 1.77 2.48 5.41 5.16 11.14 20.56 1.01

30-Jun-2011 1.73 3.38 3.03 3.41 4.88 5.45 10.90 16.34 1.14

31-Dec-2010 1.72 3.40 2.96 3.36 4.82 5.45 6.60 12.47 1.13

52-week closing high 2.16 3.88 3.49 3.78 6.20 6.32 13.38 25.68 1.36

52-week closing low 0.87 2.19 1.74 2.48 3.73 3.98 5.53 8.78 0.85

weekly change 0.00 0.22 0.09 0.12 0.10 0.13 0.04 0.64 0.01

QTD change (0.72) (0.90) (1.16) (0.81) 0.63 (0.16) 0.28 4.85 (0.13)

YTD change (0.71) (0.91) (1.10) (0.76) 0.70 (0.17) 4.58 8.72 (0.12)

Moody's

Corp Avg -

US 10s

JapanGreece A

10yr Quebec long Quebec long BClong Ontario

Spain Portugal

Credit Spreads 10yr Ontario

International 10yr Rates Swiss UK Germany France Italy

long MB long NB long NS

Co

change from 52wk high (1.15) (1.40) (1.63) (1.18) (0.68) (1.03) (2.20) (4.49) (0.34) change from 52wk low 0.14 0.30 0.12 0.12 1.78 1.31 5.65 12.41 0.17

8/4/2019 20110916 weekly

http://slidepdf.com/reader/full/20110916-weekly 2/10

Markets for the Week ending

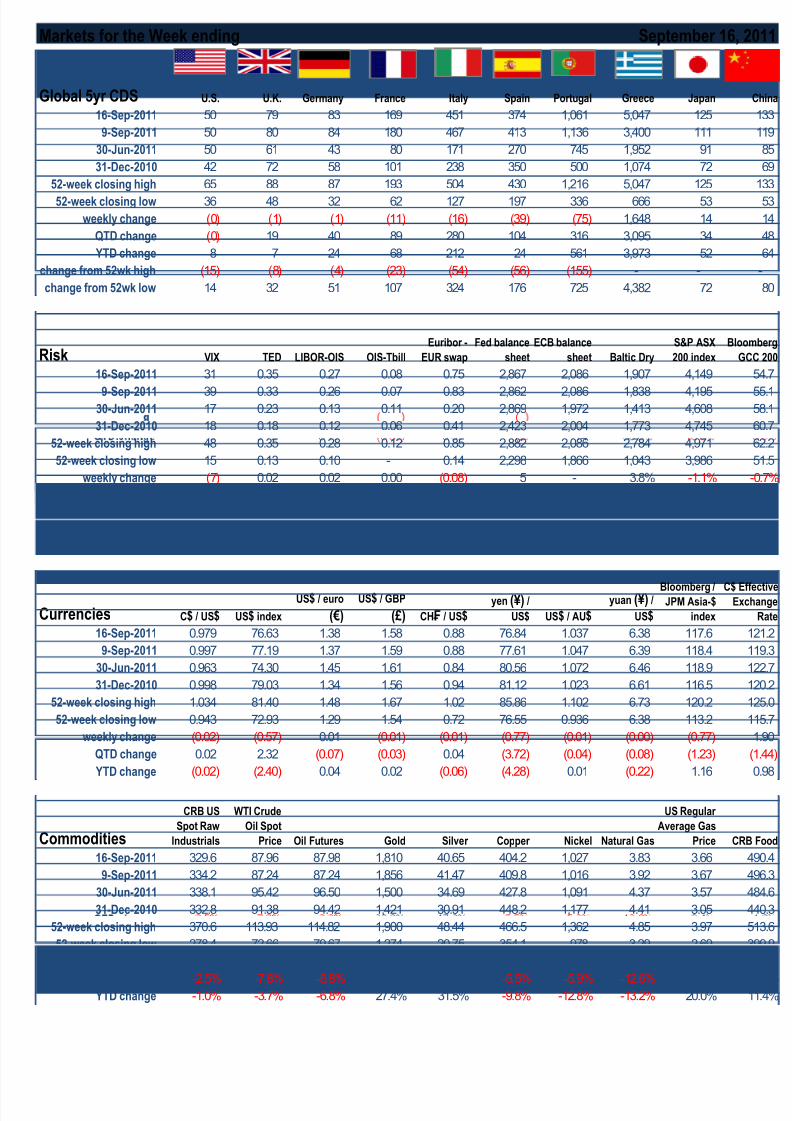

16-Sep-2011 50 79 83 169 451 374 1,061 5,047 125

9-Sep-2011 50 80 84 180 467 413 1,136 3,400 111

30-Jun-2011 50 61 43 80 171 270 745 1,952 91

31-Dec-2010 42 72 58 101 238 350 500 1,074 72

52-week closing high 65 88 87 193 504 430 1,216 5,047 125

52-week closing low 36 48 32 62 127 197 336 666 53

weekly change (0) (1) (1) (11) (16) (39) (75) 1,648 14

QTD change (0) 19 40 89 280 104 316 3,095 34

YTD change 8 7 24 68 212 24 561 3,973 52

change from 52wk high (15) (8) (4) (23) (54) (56) (155) - -

change from 52wk low 14 32 51 107 324 176 725 4,382 72

16-Sep-2011 31 0.35 0.27 0.08 0.75 2,867 2,086 1,907 4,149

9-Sep-2011 39 0.33 0.26 0.07 0.83 2,862 2,086 1,838 4,195 30-Jun-2011 17 0.23 0.13 0.11 0.20 2,869 1,972 1,413 4,608

31-Dec-2010 18 0.18 0.12 0.06 0.41 2,423 2,004 1,773 4,745

52-week closing high 48 0.35 0.28 0.12 0.85 2,882 2,086 2,784 4,971

52-week closing low 15 0.13 0.10 - 0.14 2,298 1,866 1,043 3,986

weekly change (7) 0.02 0.02 0.00 (0.08) 5 - 3.8% -1.1%

QTD chan e 15 0.12 0.15 0.03 0.55 2 114 35.0% -10.0%

Japan

S&P ASX

200 indexOIS-Tbill

Global 5yr CDS U.S. U.K.

Risk VIX TED

September 16,

Germany France Italy Spain Portugal Greece

LIBOR-OIS

Euribor -

EUR swap

Fed balance

sheet

ECB balance

sheet Baltic Dry

Blo

G

. . . . . .

YTD change 13 0.17 0.15 0.02 0.35 444 82 7.6% -12.6%

change from 52wk high (17) - (0.01) (0.05) (0.09) (15) - -31.5% -16.5%

change from 52wk low 17 0.22 0.18 0.08 0.62 569 220 82.8% 4.1%

16-Sep-2011 0.979 76.63 1.38 1.58 0.88 76.84 1.037 6.38 117.6

9-Sep-2011 0.997 77.19 1.37 1.59 0.88 77.61 1.047 6.39 118.4

30-Jun-2011 0.963 74.30 1.45 1.61 0.84 80.56 1.072 6.46 118.9

31-Dec-2010 0.998 79.03 1.34 1.56 0.94 81.12 1.023 6.61 116.5

52-week closing high 1.034 81.40 1.48 1.67 1.02 85.86 1.102 6.73 120.2

52-week closing low 0.943 72.93 1.29 1.54 0.72 76.55 0.936 6.38 113.2

weekly change (0.02) (0.57) 0.01 (0.01) (0.01) (0.77) (0.01) (0.00) (0.77)

QTD change 0.02 2.32 (0.07) (0.03) 0.04 (3.72) (0.04) (0.08) (1.23)

YTD change (0.02) (2.40) 0.04 0.02 (0.06) (4.28) 0.01 (0.22) 1.16

16-Sep-2011 329.6 87.96 87.98 1,810 40.65 404.2 1,027 3.83 3.66

9-Sep-2011 334.2 87.24 87.24 1,856 41.47 409.8 1,016 3.92 3.67

30-Jun-2011 338.1 95.42 96.50 1,500 34.69 427.8 1,091 4.37 3.57

31-Dec-2010 332.8 91.38 94.42 1,421 30.91 448.2 1,177 4.41 3.05

52-week closing high 370.6 113.93 114.82 1,900 48.44 466.5 1,362 4.85 3.97

52-week closing low 278.4 72.66 79.67 1,274 20.75 354.1 978 3.29 2.69

weekly change -1.4% 0.8% 0.8% -2.5% -2.0% -1.4% 1.0% -2.3% -0.4%

Currencies C$ / US$ US$ index

yuan (¥) /

US$

C$ EEx

Commodities

CRB US

Spot Raw

Industrials

WTI Crude

Oil Spot

Price Oil Futures Gold Silver Copper Nickel Natural Gas CR

US$ / euro

(€)

US$ / GBP

(£) CH₣ / US$yen (¥) /

US$ US$ / AU$

Bloomberg /JPM Asia-$

index

US Regular

Average Gas

Price

QTD change -2.5% -7.8% -8.8% 20.6% 17.2% -5.5% -5.9% -12.6% 2.4% YTD change -1.0% -3.7% -6.8% 27.4% 31.5% -9.8% -12.8% -13.2% 20.0%

8/4/2019 20110916 weekly

http://slidepdf.com/reader/full/20110916-weekly 3/10

Markets for the Week ending

16-Sep-2011 12,274 696 1,216 11,509 2,622 38.7 673 714 599

9-Sep-2011 12,388 706 1,154 10,992 2,468 36.2 639 674 569

30-Jun-2011 13,301 764 1,321 12,414 2,774 48.3 734 827 669

31-Dec-2010 13,443 769 1,258 11,578 2,653 52.2 697 784 639

52-week closing high 14,271 819 1,364 12,811 2,874 55.6 758 865 694

52-week closing low 11,671 666 1,119 10,595 2,303 35.1 617 648 552

weekly change -0.9% -1.4% 5.4% 4.7% 6.3% 6.8% 5.3% 6.0% 5.2%

QTD change -7.7% -8.9% -7.9% -7.3% -5.5% -19.9% -8.4% -13.7% -10.5%

YTD change -8.7% -9.4% -3.3% -0.6% -1.2% -25.9% -3.4% -8.8% -6.3%

change from 52wk high -14.0% -15.0% -10.8% -10.2% -8.7% -30.5% -11.3% -17.4% -13.7%

change from 52wk low 5.2% 4.5% 8.6% 8.6% 13.9% 10.2% 9.0% 10.3% 8.5%

16-Sep-2011 4,000 4,654 5,664 4,452 1,767 5,368 5,574 14,547 8,864

9-Sep-2011 3,880 4,553 5,496 4,416 1,818 5,215 5,190 14,020 8,738 30-Jun-2011 4,531 5,505 7,004 4,842 2,083 5,946 7,376 20,187 9,816

31-Dec-2010 4,290 5,226 6,391 4,938 2,062 5,900 6,914 20,173 10,229

52-week closing high 4,707 5,776 7,401 5,136 2,177 6,091 7,528 23,178 10,858

52-week closing low 3,839 4,421 5,320 4,295 1,746 5,007 5,072 13,474 8,519

weekly change 3.1% 2.2% 3.1% 0.8% -2.8% 2.9% 7.4% 3.8% 1.4%

TD chan e -11.7% -15.5% -19.1% -8.0% -15.2% -9.7% -24.4% -27.9% -9.7%

Nikkei 225

Russell

Large-Cap

Value

FTSE 100 DAX 30

MSCI

Europe

MSCI Pacific

Rim

MSCI

Emerging

MarketsMSCI EAFE

North American

Equities S&P/TSX S&P/TSX 60 S&P 500

Dow Jones

Industrials Nasdaq

FTSE MIB 40 S

KBW Bank

index

Russell

Large-Cap

Russell

Small-Cap

La

International

Equities MSCI World

September 16,

- . - . - . - . - . - . - . - . - .

YTD change -6.8% -10.9% -11.4% -9.8% -14.3% -9.0% -19.4% -27.9% -13.3%

change from 52wk high -15.0% -19.4% -23.5% -13.3% -18.8% -11.9% -26.0% -37.2% -18.4%

change from 52wk low 4.2% 5.3% 6.5% 3.7% 1.2% 7.2% 9.9% 8.0% 4.1%

16-Sep-2011 2,684 3,883 1,208 912 1,681 1,544 654 135 921

9-Sep-2011 2,671 4,053 1,196 888 1,665 1,544 634 150 928

30-Jun-2011 3,085 3,689 1,423 1,069 1,739 1,737 761 159 933

31-Dec-2010 3,140 4,101 1,297 1,095 1,674 1,666 488 230 844

52-week closing high 3,504 4,208 1,431 1,139 1,797 1,812 809 271 949

52-week closing low 2,596 3,455 1,178 874 1,573 1,509 442 129 830

weekly change 0.5% -4.2% 1.0% 2.7% 1.0% 0.0% 3.1% -10.0% -0.8%

QTD change -13.0% 5.2% -15.1% -14.7% -3.3% -11.1% -14.1% -15.3% -1.2%

YTD change -14.5% -5.3% -6.8% -16.7% 0.4% -7.3% 34.0% -41.4% 9.2%

16-Sep-2011 499 217 276 298 319 174 382 402 124

9-Sep-2011 479 208 260 279 309 164 369 376 119

30-Jun-2011 559 246 322 318 323 207 411 411 134

31-Dec-2010 507 240 301 296 304 215 365 405 129

52-week closing high 598 255 335 329 334 231 421 439 136

52-week closing low 404 199 251 257 286 161 346 358 115

weekly change 4.0% 4.5% 6.4% 6.9% 3.4% 6.0% 3.7% 7.1% 4.5%

Telecom

Telecom

Energy Materials Industrials Cons Disc

Cons

Staples Financials

Energy Materials Industrials Cons Disc

Cons

Staples Financials Healthcare Tech

S&P/TSX sectors Healthcare Tech

S&P 500 sectors

QTD change -10.9% -11.6% -14.2% -6.2% -1.0% -15.9% -7.0% -2.1% -7.3% YTD change -1.6% -9.3% -8.3% 0.9% 5.2% -19.0% 4.8% -0.5% -3.3%

8/4/2019 20110916 weekly

http://slidepdf.com/reader/full/20110916-weekly 4/10

Markets for the Week ending September 16, 2011

1.0

1.5

2.0

Bank of Canada U.S. Federal Reserve European Central Bank

‐

0.5

1.0

16‐Sep 16‐Nov 16‐Jan 16‐Mar 16‐May 16‐Jul 16‐Se

GoC 2yr GoC 5yr GoC 10yr GoC 30yr BoC

3.0

3.5

4.0

GoC 2yr GoC 5yr GoC 10yr GoC 30yr BoC

2.0

2.5

3.0

0.5

1.0

1.5

2.5

2.6

GoC 10yr

‐

0.5

5‐Mar 5‐Apr 5‐May 5‐Jun 5‐Jul 5‐Aug 5‐Sep

2.2

2.3

2.4

2.5

2.0

2.1

2.2

15‐Aug 22‐Aug 29‐Aug 5‐Sep 12‐Sep

8/4/2019 20110916 weekly

http://slidepdf.com/reader/full/20110916-weekly 5/10

Markets for the Week ending September 16, 2011

1.0

2.0

3.0

4.0

5.0

Germany (2yr) France (2yr) Italy (2yr) Spain (2yr)

‐

1.0

.

5‐Mar 5‐Apr 5‐May 5‐Jun 5‐Jul 5‐Aug 5‐Sep

40

60

80

Swiss (2yr) Portugal (2yr) Greece (2yr)

‐

20

40

5‐Mar 5‐Apr 5‐May 5‐Jun 5‐Jul 5‐Aug 5‐Sep

400

SOVX WEST EUROPEAN SOV CDS CDX EM SOV 5YR

1,000200

100

200

300

16‐Sep 16‐Oct 16‐Nov 16‐Dec 16‐Jan 16‐Feb 16‐Mar 16‐Apr 16‐May 16‐Jun 16‐Jul 16‐Aug 16‐Sep

SOVX WEST EUROPEAN SOV CDS CDX EM SOV 5YR

250

500

750

1,000

50

100

150

200

‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐ ‐

EUROPE IG CORP CDS 5YR EUROPE XOVER (HY) CORP CDS

250 50

16‐Sep 16‐Oct 16‐Nov 16‐Dec 16‐Jan 16‐Feb 16‐Mar 16‐Apr 16‐May 16‐Jun 16‐Jul 16‐Aug 16‐Sep

150

300

450

600

100

200

300

400

EUROPE SNR FIN CDS 5YR EUROPE SUB FIN CDS 5YR

‐

150

‐

100

16‐Sep 16‐Oct 16‐Nov 16‐Dec 16‐Jan 16‐Feb 16‐Mar 16‐Apr 16‐May 16‐Jun 16‐Jul 16‐Aug 16‐Sep

600

800

125

150

CDX NA IG 5YR CDX NA HY 5YR

200

400

600

75

100

125

16‐Sep 16‐Oct 16‐Nov 16‐Dec 16‐Jan 16‐Feb 16‐Mar 16‐Apr 16‐May 16‐Jun 16‐Jul 16‐Aug 16‐Sep

8/4/2019 20110916 weekly

http://slidepdf.com/reader/full/20110916-weekly 6/10

Markets for the Week ending September 16, 2011

13,00

14,00

1,300

1,400

S&P 500 S&P/TSX

10,00

11,00

12,00

13,00

1,000

1,100

1,200

1,300

‐ ‐ ‐ ‐ ‐ ‐ ‐

12,500

12,750

13,000

S&P/TSX

10,001,000

16‐Sep 16‐Nov 16‐Jan 16‐Mar 16‐May 16‐Jul 16‐Sep

11,500

11,750

12,000

12,250

12,500

1,200

1,225

1,250

S&P 500

11,500

15‐Aug 22‐Aug 29‐Aug 5‐Sep 12‐Sep

1,100

1,125

1,150

1,175

,

15‐Aug 22‐Aug 29‐Aug 5‐Sep 12‐Sep

101.5

102.0

102.5

103.0

US$ / C$

1,100

15‐Aug 22‐Aug 29‐Aug 5‐Sep 12‐Sep

100.0

100.5

101.0

101.5

15‐Aug 22‐Aug 29‐Aug 5‐Sep 12‐Sep

8/4/2019 20110916 weekly

http://slidepdf.com/reader/full/20110916-weekly 7/10

Weekly Recap

Monday September 12

- Chinese exports up 24.5% YoY, beating expectations of 21.9%; Chinese imports up 30.2% YoY vs anticipated 21%; so trade balance

unexpectedly fell to $17.8B vs $24.6B expected for August

- Italian industrial production down 4.6% YoY through July; Egyptian CPI 8% YoY, 7% on core; Spanish housing transactions down 35% Y

- C$ briefly traded below par on risk-off trade, as Euribor-OIS, USD LIBOR and ECB deposit facility usage all at yearly highs; 10yr Italian

bonds back north of 5.50%; Greek 1yr bonds at 139%- US Treasury sold $32 billion in 3-year bonds at a yield of 0.334% (which is actually below 3mth LIBOR); bid-to-cover was 3.15

- French bank stocks down 10-12%, with expectations of imminent downgrade by Moodys; Italian financials down over 5%, including Intes

whose trading was halted when it was down 8%; many European lenders trading at 50% of book value, as investors’ suspicion of accura

of book value increases (are those net assets really worth what companies claim? Nomura analysts estimate that the 90 banks that

underwent European stress tests would face capital shortfall of 350 billion euros if PIIGS govt bonds were marked to market)

- Gold stocks and banks weigh on TSX; Shares in Goldman drop out of triple digit range for first time since March 2009

- Rumours that China will buy Italian bonds drives late-day equity rally (but China is no white-knight; if they buy European bonds, its in an

effort to keep the EUR elevated and maintain their favourable trade terms; by intervening in this way, China would be protecting its trade

surplus with Europe, which reduces eurozone aggregate demand, which makes problem of too much debt even worse and makes auste

measures bite even harder, which means debt trajectories will get worse instead of better; i.e. no solution, just more can-kicking)

Tuesday September 13

- French and UK inflation a bit higher than expected; use of ECB deposit facility surged to €198 billion on Monday

- Italian bond auction wasn’t particularly successful; sold €3.9 billion of 5-year notes at 5.60% (up from 4.93% at previous 5yr auction in J

also sold €1.2 billion of 4% 9-year bonds at a 10-point discount price of 90.2.

- Rumours-on / rumours-denied drive risk-on / risk-off trade; WSJ says BNP no longer has access to $ funding markets, which BNP then

denies; & how many times can we rally on the same rumour --- of China buying European sovereign debt? & why is every rumour of a

Merkel-Sarkozy emergency meeting a market-moving news-item? And now rumours of Russia buying euro common bonds?!

- Ceridian UCLA Pulse of Commerce index remains in idle, down 1.4% in August after falling 0.2% in July

- US Census Bureau reported 15.1% of people living in poverty in 2010, matching 1993 and 1983 as highest ratio since the ‘60s

- US Treasury auctioned $27 billion 4-week bills and $21 billion 10-year bonds, the latter at a yield of 2.00%

Wednesday September 14

- BRICs may be discussing co-ordinating purchases of Eurozone debt

- Eurozone industrial production softer than expected in July but still up 4.2% YoY; Canadian capacity utilization didn’t drop as much as

expected, falling to 78.4% from 79%; US PPI as expected (headline flat in August, but up 6.5% YoY; core up 2.5% YoY); US retail sales

bit softer, up just 0.1% in August ex-autos&gas and flat on the headline (retail sales ex-gas up 5.7% YoY)

- Canadian auctioned $3.5 billion of 2-year bonds, and US Treasury auctioned off $13 billion of 30-year bonds at 3.31%

Thursday September 15

- UK retail sales negative YoY; Eurozone CPI as expected (2.5% YoY, 1.2% YoY core); US CPI higher than expected (3.8% YoY, 2.0% Y

core); weekly jobless claims higher than forecast yet again; Empire even worse than last month, in contrast to hope of less soft # ; Philly

Fed managed to do in September what Empire didn’t, retracing half of its August plunge; industrial production up a bit in August but CAP

lower than expected (77.4); Bloomberg weekly consumer comfort index 2nd-worst print since August 2010; RBNZ left rates unch @ 2.5%- But economic data, which was pretty much disappointing across the board, takes back seat to globally-co-ordinated announcement by

central banks to create (or, for ECB, expand) programs to lend in $$s --- gold down almost $150 since Sept 6 to $1775; stocks up; yields

up; spreads in; don’t expect the risk-on to last --- this swap announcement is an acknowledgment of the weakness of funding markets in

Europe --- how can that be good news? And it comes 2 days after BNP categorically “confirmed that it is fully able to obtain USD funding

the normal course of business”; right, that’s why this new program was necessary!; (comes on 3-year anniversary of LEH failure)

- RIMM trounced after-hours after disappointing earnings report

Friday September 16

- Canadian international securities transactions showed net bond buying in July;

- UoM consumer sentiment ticked up on current conditions, but future expectations hit lowest level since 1980

- Relatively quiet day; S&P 500 makes posts its 5 th straight green day

8/4/2019 20110916 weekly

http://slidepdf.com/reader/full/20110916-weekly 8/10

Non-Mainstream News and Views

Quote of the Week1:“[Trichet & Co.] were wrong. They now have a choice. They can admit that they were wrong. Then they will probably have to resign, and then snubbed worldwide. Nobody likes a loser. Alternatively, they can double down. Their reputations right now are underwater. What do they havelose reputation-wise by saying more absurd nonsense? And there is a chance that tomorrow the confidence fairy will appear, wave her magicwand, and the V-shaped recovery will start.... they are reputationally-bankrupt zombies gambling for resurrection.”Brad DeLong. http://delong.typepad.com/sdj/2011/09/understanding-trichet-and-conpany-a-note.html

QOTW2:David Rosenberg: “Assuming that the House Republicans do not accept the Obama spending measures, and half of the tax relief goes intosavings and debt reduction, then we are talking about the grand total of $35 billion of net new stimulus from this "jobs plan". That's... because smuch of it is merely extending what is already in the system. At an annual rate, that is a 0.2% boost to baseline GDP growth.”

An e-book with many distinguished contributors, published by Wharton: Life in the eurozone, with or without sovereign defaulthttp://finance.wharton.upenn.edu/FIC/FICPress/eurozone.pdf

George Magnus of UBS:“In the Eurozone, it is hard to keep track of the moving parts, which include: faltering economic growth in the core and recession in the periphery stressed bank liquidity and funding markets, and total reliance on a reluctant and split ECB to purchase sovereign bonds so as to prevent

contagion parliamentary approval of the redesign of the EFSF, and possible changes to economic governance allowing existing institutions to play a

stronger crisis management role the terms of the IMF’s next loan tranche to a non-compliant Greece, the Finns’ demands for adequate collateral, the implementation of the

Greek debt swap terms, and how and when a Greek default might be managed.”http://www.bearmarketinvestments.com/ubs-george-magnus-says-european-viability-is-far-from-assured

Buttonwood on shorter cycles“Economists are pretty reluctant to forecast a recession, despite some fairly gloomy data, the damaging effect on confidence of the euro zonecrisis and the message sent by ultra-low bond yields. Of course, economists are generally hopeless at predicting recessions”http://www.economist.com/blogs/buttonwood/2011/09/global-economy

Willem Buiter of Citibank, via Buttonwood’s notebook:“Greece's exit would create a powerful and highly visible precedent. As soon as Greece has exited, we expect the markets will focus on thecountry or countries most likely to exit next from the euro area. Any non-captive/financially sophisticated owner of a deposit account.... willwithdraw his deposits from countries deemed at risk - even a small risk - of exit. Any non-captive depositor who fears a non-zero risk of the futintroduction of a New Escudo, a New Punt, a New Peseta or a New Lira would withdraw his deposits at the drop of a hat and deposit them in thhandful of countries likely to remain in the euro area no matter what - Germany, Luxembourg, the Netherlands, Austria and Finland. The fundistrike and deposit run out of the periphery euro area member states (defined very broadly) would create financial havoc and most likely causefinancial crisis followed by a deep recession in the euro area broad periphery.”http://www.economist.com/blogs/buttonwood/2011/09/european-debt-crisis

Bill O’Donnell and John Briggs of RBS:

“I’m not surprised by the pervasive pessimism given what history tells us about deleveraging processes. McKinsey Global Institute cites historythat suggests the sovereign de-levering process takes around 6-7 years to work through, once started. They then add that the debt problems ithe developed world today are more diffuse and deep than they’ve ever been before. Meanwhile, taxpayers are smart and know that any fiscalbone thrown them today will most likely be snatched back in the future.... The only logical outcome to the looming sovereign and householddeleveraging here in the US is a lower standard of living. Yeah, we lived beyond our means for years but nobody likes to go backwards after gsteadily forward for much of their adult lives. It’s just one of those things where change matters more to consumer psychology than level, and Ihighly doubt that Twisting the Fed’s balance sheet is going to do much to alter consumer, bank or business perceptions. These are just theconditions to foster recessions and that risk will no doubt keep bond yields low for an extended period. For example, we recently printed 10yr yields at levels not seen since 1950. Recall that the Fed capped rates for 9 years from 1942 to 1951 so there is precedent for a Japan-likecompression in rates that persists for years. Anchoring short rates through mid-2013 (at least) was just a hat tip to the realities of our time and aacknowledgement that time (a lot of it most likely) is the next best healer as the Fed throws their arm out and the administration is forced to bowthe realities of a bloated budget. Treasuries are thus one of the best places to be for this long haul. Buy dips when offered up.”

http://pragcap.com/deep-thoughts-by-rbs

8/4/2019 20110916 weekly

http://slidepdf.com/reader/full/20110916-weekly 9/10

Jefferies chief market strategist Devid Zervos“The bottom line is that it looks like a Lehman like event is about to be unleashed on Europe WITHOUT an effective TARP like structure fully inplace. Now maybe, just maybe, they can do what the US did and build one on the fly – wiping out a few institutions and then using an expandedEFSF/Eurobond structure to prevent systemic collapse. But politically that is increasingly feeling like a long shot. Rather it looks like we will get TARPs – one for each country. That is going to require a US style socialization of each banking system – with many WAMUs, Wachovias, AIGsand IndyMacs along the way. The road map for Europe is still 2008 in the US, with the end game a country by country socialization of their commercial banks. The fact is that the Germans are NOT going to pay for pan European structure to recap French and Italian banks - eventhough it is probably a more cost effective solution for both the German banks and taxpayers. Where the losses WILL occur is at the ECB, whethe Germans are on the hook for the largest percentage of the damage. And these will not just be SMP losses and portfolio losses. It will also brepo losses associated with failed NON-GERMAN banks. Of course in the PIG nations, the ability to create a TARP is a non-starter – they cannraise any euro funding. The most likely scenario for these countries is full bank nationalization followed by exit and currency reintroduction.”http://www.zerohedge.com/news/jefferies-describes-endgame-europe-finished

Michael Pettis: Why U.S. and Europe are not turning Japanese; but why recent Japanese history is relevant for China.“Japan’s problem was that during the 1980s it was so addicted to investment-led growth and artificially cheap financing that it misallocated caon a massive scale and failed to include the resulting implicit losses in its GDP calculations. Especially after the Plaza Accord, Japan went oninvestment binge that left it with a huge amount of wasted capital. Because of this overinvestment Japan grossly overstated its true GDP durimuch of the 1980s.... This is not the problem that that the US or Europe is suffering from. They suffer from a typical debt-fueled overconsumpboom, whereas Japan suffered from a typical debt-fueled over-investment boom, and Japan’s period of over-investment was much, much moextreme (centralized investment booms can last much longer and go much further than decentralized consumption booms). This is why I thinthe Japanese experience tells us almost nothing about what Europe and the US will go through. On the other hand, it might tell us a lot about

what China will go through.”http://mpettis.com/2011/09/big-in-japan/

International Finance Review: US banks have become the unlikely saviours of their ailing European counterparts, signing private agreements lend them billions of dollars in recent weeks after an exodus of nervous money market funds left many without ready access to short-term fundhttp://www.ifre.com/us-banks-privately-lending-billions-to-support-european-lenders/1606560.article

Surprise, surprise: IMF’s research department says contractionary policies are contractionary; i.e. austerity doesn’t workhttp://www.imf.org/external/pubs/ft/fandd/2011/09/Ball.htm

George Soros on whether the euro has a futurehttp://www.nybooks.com/articles/archives/2011/oct/13/does-euro-have-future/

OECD composite leading indicators signal widespread slowdown in economic activityhttp://www.oecd.org/dataoecd/44/5/48658623.pdf

Kyle Bass of Hayman Capital Partners on CNBC

http://paul.kedrosky.com/archives/2011/09/kyle-bass-on-the-euro.html

Satyajit Das believes the world is experiencing an enormous debt bubble that took over 30 years to build and will take nearly as long to end.http://video.cnbc.com/gallery/?video=3000045528

8/4/2019 20110916 weekly

http://slidepdf.com/reader/full/20110916-weekly 10/10

The European Dis-Union

EU President Herman Van Rompuy:

"The euro has never had the infrastructure that it requires."

Former German Chancellor Gerhard Schroeder:

"The current crisis makes it relentlessly clear that we cannot have a common currency zone without a common fiscal, economic and so

policy"

German President Christian Wulff:

"I regard the huge buy-up of bonds of individual states by the ECB as legally and politically questionable. Article 123 of the Treaty on th

EU’s workings prohibits the ECB from directly purchasing debt instruments, in order to safeguard the central bank’s independence"

Prince Hermann Otto zu Solms-Hohensolms-Lich, the Bundestag's Deputy President:

"We must consider whether it would not be better for the currency union and for Greece itself to go for debt restructuring and an exit fro

the euro"

Polish finance minister Jacek Rostowski:

"European elites, including German elites, must decide if they want the euro to survive - even at a high price - or not. If not, we shouldprepare for a controlled dismantling of the currency zone."

Bank of England Governor Mervyn King:

"Dealing with a banking crisis was difficult enough, but at least there were public-sector balance sheets on to which the problems could

moved. Once you move into sovereign debt, there is no answer; there's no backstop."

Daniel Dăianu, liberal Member of the European Parliament (MEP) and former Finance Minister of Romania:

“Fundamentally, I’m in favour of issuing eurobonds. However, my reading of the crisis is that just imposing stronger fiscal rules and deb

breaks is quite insufficient. And this is not related to the current state of the Single Currency, in my view; it’s rather about the whole

construction of the Eurozone. One has to think about the flaws of the Eurozone. And I’m referring to the lack of a common treasury. Not

only world experience, but also theory indicates that an economic union cannot function properly unless a single currency is underpinne

simultaneously by – not simply fiscal rules – but by fiscal integration. Fiscal integration is not equivilant to fiscal rules. An economic unio

needs mechanisms for dealing with assymetric shocks. Dealing with assymetric shocks boils down to what national governments can d