Embed Size (px)

Citation preview

8/8/2019 20100719184745eGCC Debt Market Tracker - July2010

http://slidepdf.com/reader/full/20100719184745egcc-debt-market-tracker-july2010 1/10

Chief EconomistDr Jarmo T. Kotilaine

Please refer to the last pagefor important disclaimer

ECONOMIC RESEARCH | JULY 2010

GCC Debt Market Tracker

Debt markets reviveThe second quarter of 2010 marked something o f a revival for the GCC

debt capital markets which had seen a sharp drop is issuance volumes

during Q1. Even as global economic uncertainty continued to deter issuers,

investors received a fillip from ongoing restructuring efforts in the Gulf.

Especially sovereign sukuk experienced a marked turnaround from the

opening months of the year. While the near-term outlook remains highly

uncertain, the Q2 performance high lights the potency of structural drivers

of GCC debt market grow th.

•

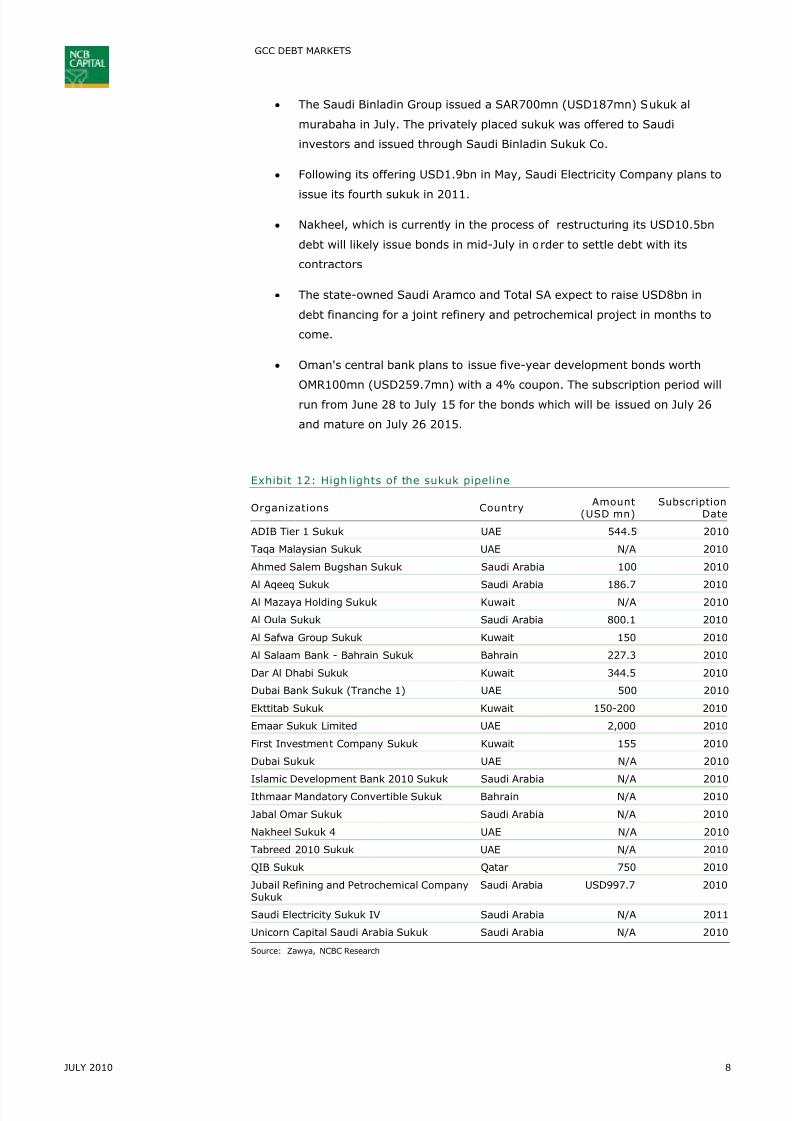

The GCC conventional bond market bounced back in Q2 . In value termsprimary issuances increased by 33% QoQ while the number of issuances more

than doubled. The largest issues came from the Dubai Electricity and Water

Authority (DEWA) and Bahrain-based Gulf International Bank which raised

some USD1bn each. In value terms, conventional government debt issuance

totaled USD12.2bn with Kuwait raising USD1.7bn through seven short-term

issues and Qatar placing USD1.4bn in a new domestic issue.

• Lead by sovereign sukuk, the Islamic bond market surged in value

terms. Total value of offerings in the GCC reached USD3.4bn, a significant

increase over USD1.1bn raised during 2Q09. The largest sovereign sukuk came

from the Government of Qatar which raised USD1.4bn for a tenor of eight

years. The Central Bank of Bahrain also tapped the market with six short-term

issues. By contrast, the corporate sector saw just one sukuk issue worth

USD1.9bn by the Saudi Electricity Company during the quarter. Globally, a total

of 74 sukuk were issued in 2Q10, with 41 coming from Malaysia where the

value of issuance increased almost three-fold from USD2.5bn in 1Q10 to

USD7.4bn in 2Q10. Encouragingly, the tenors of sukuk issues appear to be

growing longer.

• Government issuances emerged as a key market driver. Out of the eight

GCC sukuk issued during 2Q10, seven were sovereign issues from Bahrain and

Qatar. Sovereign sukuk issuance totaled USD1.5bn during 2Q10. The Qatari

government continued its deliberate program of developing domestic debt

capital markets and plans are underway for a secondary market.

• The near-term outlook remains cloudy amidst an uncertain global

economic environment and rising domestic inflationary pressures. The

GCC debt markets face a period of uncertainty because of mounting global

economic risks in the wake of the European sovereign debt crisis and signs of

renewed weakness in the US. In the Gulf region, rising inflation threatens to

push up yield expectations, thereby discouraging new issuance. Nonetheless,

the growing need for long-term financing coupled with low interest rates should

continue to support the market. In terms of new issues, the main worry would

appear to be delays rather than actual cancellations.

8/8/2019 20100719184745eGCC Debt Market Tracker - July2010

http://slidepdf.com/reader/full/20100719184745egcc-debt-market-tracker-july2010 2/10

JULY 2010 2

GCC DEBT MARKETS

Second quarter catch-up

Following a market correction during 1Q10, the GCC debt markets resumed their

expansion during Q2 as restructuring deals announced in recent months, along with

easing sovereign debt fears in the Euro-zone, provided a much needed boost to

investor confidence. In May, Dubai World reached an agreement with its creditors

on USD23.5bn debt restructuring under which the company will pay USD4.4bn

worth of loans over five years and another USD10bn over eight years. Further, the

Dubai Government will convert its USD8.9bn loan to Dubai World into equity. At the

same time, Dubai World’s real-estate arm Nakheel PJSC began returning 40% of its

debt to creditors in the form of cash payments. The company had earlier offered

trade creditors full recovery of their claims – 40% through a cash payment and

60% through a publicly tradable sukuk paying a 10% return annually. The Dubai

government in March pledged to pump USD8bn into Nakheel and said it will take

over the company from Dubai World after the restructuring is complete. Bahrain-

based Gulf Finance House also renegotiated with its creditors a USD100mn debt

which matures in August. Although the overall performance of the Gulf debt capital

markets was far ahead of the disappointing beginning to the year, activity levels

still fell far short of those seen in 2009.

A revival in conventional bonds

Following a slowdown in the first three months of the year, the second quarter of

2010 saw a revival in terms of both the aggregate value and the number of GCC

conventional bond issuances. The total amount issued in 2Q10 was USD6.6bn, upfrom USD3.4bn in 1Q10. The number of offerings more than doubled to 16 from six

in the previous quarter. Although market sentiment improved, both value and

issuances levels remained far short of those seen in 2009, which saw a broad-based

increase in government and corporate activity. During Q2, GCC governments and

central banks issued bonds worth USD5.4bn, of which the Central Bank of Kuwait

accounted for USD1.7bn through short-term issues. Reflecting improving sentiment

in the UAE, the state owned Dubai Electricity and Water Authority (DEWA)

successfully raised USD1bn through five-year bonds.

Exhibit 1: R evival in conventional bond market during 2Q10

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

1 Q 0 7

2 Q 0 7

3 Q 0 7

4 Q 0 7

1 Q 0 8

2 Q 0 8

3 Q 0 8

4 Q 0 8

1 Q 0 9

2 Q 0 9

3 Q 0 9

4 Q 0 9

1 Q 1 0

2 Q 1 0

V a l u e ( U S D m n )

0

5

10

15

20

25

30

Value (LHS) No of deals (RHS)

Source: Bloomberg, NCBC Research

Restructuring deals gave a

welcome boost to investor

confidence in Q2

Conventional bond markets

rebounded after a sharp

decline in 1Q10

8/8/2019 20100719184745eGCC Debt Market Tracker - July2010

http://slidepdf.com/reader/full/20100719184745egcc-debt-market-tracker-july2010 3/10

JULY 2010 3

GCC DEBT MARKETS

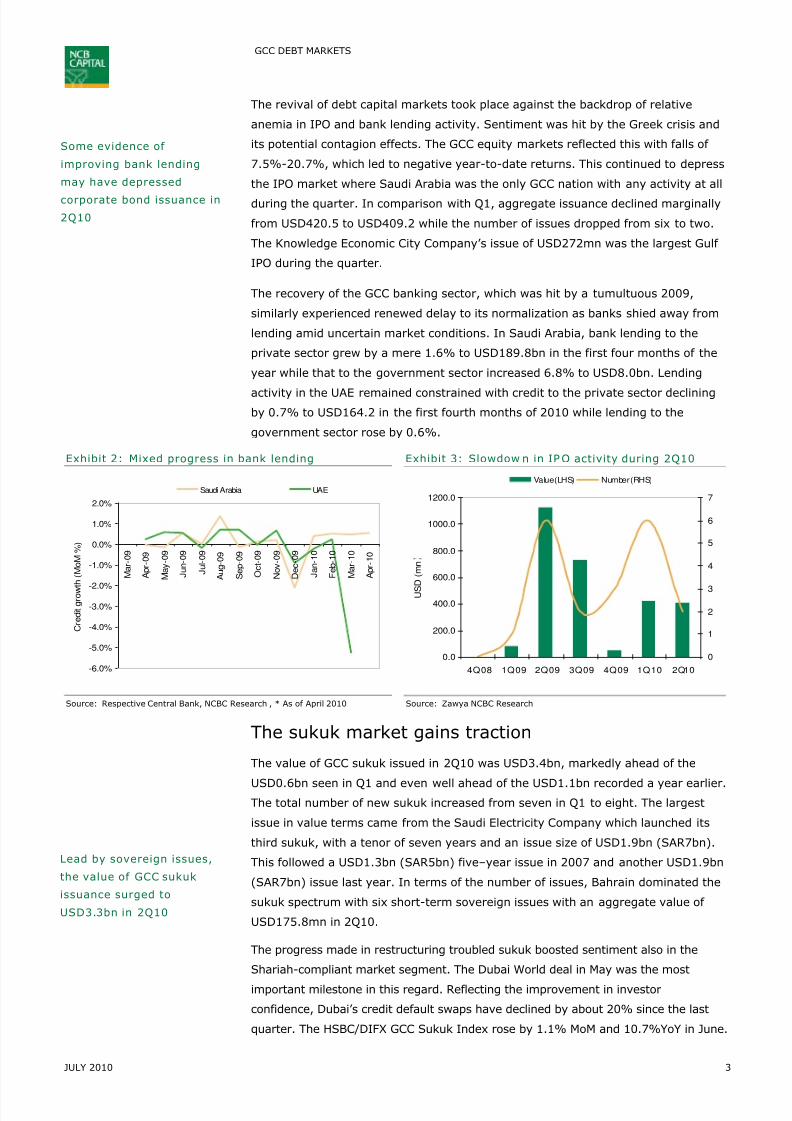

The revival of debt capital markets took place against the backdrop of relative

anemia in IPO and bank lending activity. Sentiment was hit by the Greek crisis and

its potential contagion effects. The GCC equity markets reflected this with falls of

7.5%-20.7%, which led to negative year-to-date returns. This continued to depress

the IPO market where Saudi Arabia was the only GCC nation with any activity at all

during the quarter. In comparison with Q1, aggregate issuance declined marginally

from USD420.5 to USD409.2 while the number of issues dropped from six to two.

The Knowledge Economic City Company’s issue of USD272mn was the largest Gulf

IPO during the quarter.

The recovery of the GCC banking sector, which was hit by a tumultuous 2009,

similarly experienced renewed delay to its normalization as banks shied away from

lending amid uncertain market conditions. In Saudi Arabia, bank lending to the

private sector grew by a mere 1.6% to USD189.8bn in the first four months of the

year while that to the government sector increased 6.8% to USD8.0bn. Lending

activity in the UAE remained constrained with credit to the private sector declining

by 0.7% to USD164.2 in the first fourth months of 2010 while lending to the

government sector rose by 0.6%.

Exhibit 2: Mixed progress in bank lending Exhibit 3: Slowdow n in IPO activity during 2Q10

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

M a r - 0 9

A p r - 0 9

M a y - 0 9

J u n - 0 9

J u l - 0 9

A u g - 0 9

S e p - 0 9

O c t - 0 9

N o v - 0 9

D e c - 0 9

J a n - 1 0

F e b - 1 0

M a r - 1 0

A p r - 1 0

C r e d i t g r o w

t h ( M o M % )

Saudi Arabia UAE

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

4Q 08 1Q 09 2Q 09 3Q 09 4Q 09 1Q 10 2Q10

U S

D ( m n

0

1

2

3

4

5

6

7

Value (LHS) Number (RHS)

Source: Respective Central Bank, NCBC Research , * As of April 2010 Source: Zawya NCBC Research

The sukuk market gains traction

The value of GCC sukuk issued in 2Q10 was USD3.4bn, markedly ahead of the

USD0.6bn seen in Q1 and even well ahead of the USD1.1bn recorded a year earlier.The total number of new sukuk increased from seven in Q1 to eight. The largest

issue in value terms came from the Saudi Electricity Company which launched its

third sukuk, with a tenor of seven years and an issue size of USD1.9bn (SAR7bn).

This followed a USD1.3bn (SAR5bn) five–year issue in 2007 and another USD1.9bn

(SAR7bn) issue last year. In terms of the number of issues, Bahrain dominated the

sukuk spectrum with six short-term sovereign issues with an aggregate value of

USD175.8mn in 2Q10.

The progress made in restructuring troubled sukuk boosted sentiment also in the

Shariah-compliant market segment. The Dubai World deal in May was the most

important milestone in this regard. Reflecting the improvement in investor

confidence, Dubai’s credit default swaps have declined by about 20% since the last

quarter. The HSBC/DIFX GCC Sukuk Index rose by 1.1% MoM and 10.7%YoY in June.

Some evidence of

improving bank lending

may have depressed

corporate bond issuance in

2Q10

Lead by sovereign issues,

the value of GCC sukuk

issuance surged to

USD3.3bn in 2Q10

8/8/2019 20100719184745eGCC Debt Market Tracker - July2010

http://slidepdf.com/reader/full/20100719184745egcc-debt-market-tracker-july2010 4/10

JULY 2010 4

GCC DEBT MARKETS

Exhibit 4: HSBC GCC sukuk total returns Exhibit 5: Dow Jones Citi global sukuk index

80

85

90

95

100

105

110

115

120

Dec-07 Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-1070.0

80.0

90.0

100.0

110.0

120.0

130.0

Jan-09 A pr-09 Jul-09 Oc t-09 Dec -09 Mar-10 Jun-10

Source: Zawya, NCBC Research Source: Zawya, NCBC Research

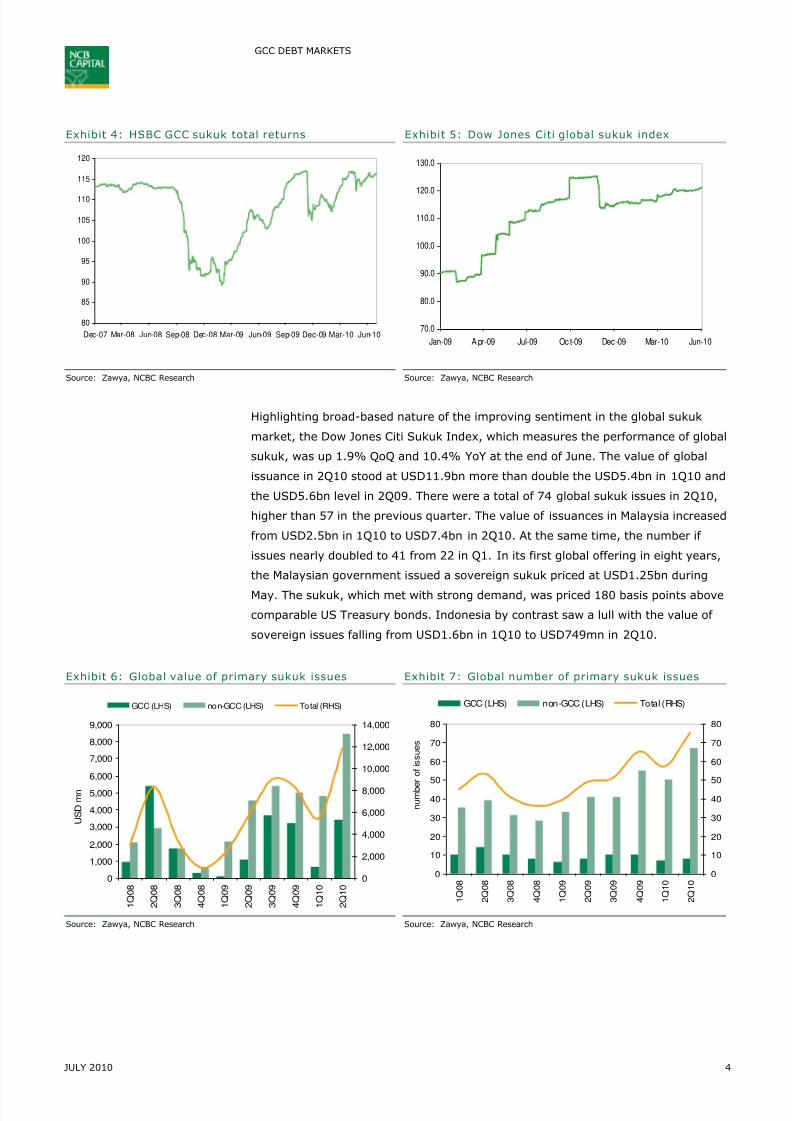

Highlighting broad-based nature of the improving sentiment in the global sukuk

market, the Dow Jones Citi Sukuk Index, which measures the performance of global

sukuk, was up 1.9% QoQ and 10.4% YoY at the end of June. The value of global

issuance in 2Q10 stood at USD11.9bn more than double the USD5.4bn in 1Q10 and

the USD5.6bn level in 2Q09. There were a total of 74 global sukuk issues in 2Q10,

higher than 57 in the previous quarter. The value of issuances in Malaysia increased

from USD2.5bn in 1Q10 to USD7.4bn in 2Q10. At the same time, the number if

issues nearly doubled to 41 from 22 in Q1. In its first global offering in eight years,

the Malaysian government issued a sovereign sukuk priced at USD1.25bn during

May. The sukuk, which met with strong demand, was priced 180 basis points above

comparable US Treasury bonds. Indonesia by contrast saw a lull with the value of

sovereign issues falling from USD1.6bn in 1Q10 to USD749mn in 2Q10.

Exhibit 6: Global value of primary sukuk issues Exhibit 7: Global number of primary sukuk issues

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

1 Q 0 8

2 Q 0 8

3 Q 0 8

4 Q 0 8

1 Q 0 9

2 Q 0 9

3 Q 0 9

4 Q 0 9

1 Q 1 0

2 Q 1 0

U S D m n

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

GCC (LHS) non-GCC (LHS) Total (RHS)

0

10

20

30

40

50

60

70

80

1 Q 0 8

2 Q 0 8

3 Q 0 8

4 Q 0 8

1 Q 0 9

2 Q 0 9

3 Q 0 9

4 Q 0 9

1 Q 1 0

2 Q 1 0

n u m b e

r o f i s s u e s

0

10

20

30

40

50

60

70

80

GCC (LHS) non-GCC (LHS) Total (RHS)

Source: Zawya, NCBC Research Source: Zawya, NCBC Research

8/8/2019 20100719184745eGCC Debt Market Tracker - July2010

http://slidepdf.com/reader/full/20100719184745egcc-debt-market-tracker-july2010 5/10

JULY 2010 5

GCC DEBT MARKETS

A turnaround in government issuance

Government activity has in recent years become an increasingly important driver of

the GCC debt capital markets with issuers such as Qatar and Abu Dhabi playing an

active role in fostering its development. Government issuance once again revived inQ2 after a difficult beginning to the year. Sovereign sukuk accounted for four out of

the total five GCC sukuk issuances during 2Q10. The Central Bank of Bahrain issued

six short-term sukuk valued at an aggregate USD175.8mn while Qatar placed an 8-

year QAR10bn (USD2.75bn) local currency issue, split equally between sukuk and

conventional bonds, with domestic banks. Nine domestic banks participated in the

programme, with the conventional banks buying QAR1bn each and their Islamic

counterparts subscribing to QAR1.25bn each from the issue. The Qatari government

further issued QAR2bn (USD549.7mn) in heavily oversubscribed 5-year domestic

bonds, rolling over old debt. Qatar’s domestic issuances are a part of the

government’s program to develop a local debt market and provide new vehicles tomobilize excess liquidity in the banking sector, partly in a bid to contain inflationary

pressures. The aggregate value of GCC sovereign sukuk issuances in 2Q10 --

USD1.5bn -- was almost eight times the USD0.2bn seen in 1Q10. In addition,

following a USD1.25bn issue of 10-year bonds in March, Bahrain's sovereign wealth

fund Mumtalakat issued a five-year USD750mn bond in June.

The positive trend in sovereign issuance looks set to continue and the Qatar

Exchange may even follow Tadawul’s footsteps and start secondary bond and sukuk

trading later this year. Reflecting the broader positive effect of government activity,

Qatari Diar, the property arm of Qatar’s sovereign wealth fund launched a

USD3.5bn dual tranche bond in July. This was the government’s first international

offering since November 2009 when it raised USD7bn through a multi-tranche bond

sale.

Exhibit 8: GCC sovereign sukuk issues Exhibit 9: GCC corporate sukuk issues

0

500

1,000

1,500

2,000

2,500

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10

V a l u e

( U S D m n )

0

1

2

3

4

5

6

7

8

9

Value (LHS) No of deals (RHS)

0

500

1000

1500

2000

2500

3000

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10

V a l u e ( U S D m n )

0

1

2

3

Value (LHS) No of deals (RHS)

Source: Zawya, NCBC Research Source: Zawya, NCBC Research

By contrast to the recovery in the sovereign space, 2Q10 saw only one corporate

sukuk issuance, highlighting the continued vulnerability of this market to the

uncertain economic backdrop. Corporate involvement in the GCC sukuk market has

been minimal since the beginning of 2009 with the exception of 3Q09 where

USD2.7bn was raised through two corporate issues. Symptomatic of shaky investor

confidence, corporates postponed their bond issuance plans waiting for more

Bahrain and Qatar led the

return of GCC sovereign

issuers to the primary

market in Q2

Corporate sukuk issuance

was depressed during2Q10 as the quarter saw

only a single issue from the

Saudi Electricity Company

8/8/2019 20100719184745eGCC Debt Market Tracker - July2010

http://slidepdf.com/reader/full/20100719184745egcc-debt-market-tracker-july2010 6/10

JULY 2010 6

GCC DEBT MARKETS

favorable market conditions. The Bank of Bahrain and Kuwait, a Bahrain-based

bank delayed its benchmark bond issue which was set to launch in May. Sabic

Capital, a unit of Saudi Basic Industries Corporation also delayed its sukuk sale in

the face of investor expectations of higher yields. The J P Morgan Emerging Markets

Bond Index Plus, which measures the premium investors demand to hold debt of

developing nations over US Treasuries reached an eight-month high of 354.7 basis

points in May.

Secondary market activity depressed

In spite of the primary market revival, secondary trading on Tadawul was

characterized by marked drops in both trading values and volumes. The second

quarter of 2010 saw a significant decline in the number of trades to nine from 57 in

the previous quarter. The total value of registered trades fell to SAR46.6mn from

SAR365.7mn in the preceding three months. By contrast, the total volume of equity

trades was up 33.4% during 2Q10 while turnover increased by 39.8%.

Planned capital spending improves outlook

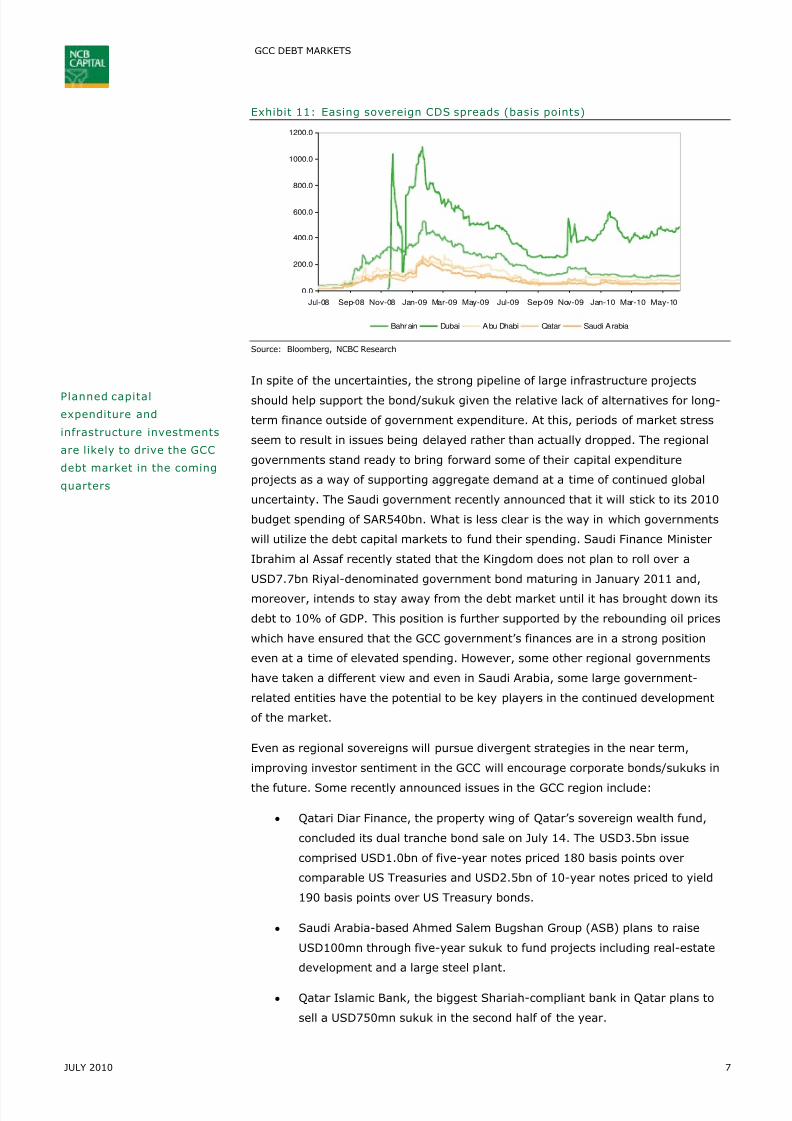

Even as global economic uncertainties will inevitably persist, the steady progress of

corporate restructuring in the region has boosted confidence. Credit default swaps

linked to Dubai government’s debt narrowed by 167 basis points on June 24 from a

year high of 651 on February 15. In spite of the progress, it is far from clear that

the risks associated with the Dubai government-related corporate entities have

been fully identified or dealt with. Dubai Holding and its subsidiaries still owe banks

USD12bn with three-quarters of the total obligations attributable to Dubai Holding’s

two investment companies, Dubai Group LLC and Dubai International Capital LLC.

Echoing the eruption of the Dubai World crisis in November, Dubai International

Capital sought a three-month extension on some of its loan payments in May.

Apart from global concerns, rising inflationary pressures pose an additional

challenge for fixed-income debt instruments. Consumer prices in the GCC region

have been on a fairly consistent upward trend since late last year with Saudi Arabia

leading the way with a rise to a 13-month high of 5.5% in June. Although the

headline figures elsewhere are lower, the basic dynamic is similar, with less and

less relief expected from the real estate market correction while prices pressures

are once again beginning to manifest themselves in food. Steadily increasing

inflationary expectations will likely put pressure on yields expectations as investors

seek compensation for the price pressures. This could act as a dampener for

corporates planning to come out with bond issues in the coming quarters.

Secondary market activity

declined significantly with

the Tadawul registering

only nine trades during

2Q10

Exhibit 10: Sukuk trading on Tadawul

Period Total volume (SAR) Total value (SAR) No of trades

2Q09 11,380,000 11,269,575 27

3Q09 15,230,000 15,043,435 26

4Q09 4,650,000 4,657,000 6

1Q10 367,390,000 365,681,600 57

2Q10 46,600,000 46,576,000 9

Source: Tadawul, NCBC Research

The near-term outlook for

the GCC debt market

remains uncertain amidst

global concerns and rising

inflationary pressures

8/8/2019 20100719184745eGCC Debt Market Tracker - July2010

http://slidepdf.com/reader/full/20100719184745egcc-debt-market-tracker-july2010 7/10

JULY 2010 7

GCC DEBT MARKETS

Exhibit 11: Easing sovereign CDS spreads (basis points)

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

Jul-08 Sep-08 Nov-08 Jan-09 Mar-09 May-09 Jul-09 Sep-09 Nov-09 Jan-10 Mar-10 May-10

Bahrain Dubai Abu Dhabi Qatar Saudi Arabia

Source: Bloomberg, NCBC Research

In spite of the uncertainties, the strong pipeline of large infrastructure projects

should help support the bond/sukuk given the relative lack of alternatives for long-

term finance outside of government expenditure. At this, periods of market stress

seem to result in issues being delayed rather than actually dropped. The regional

governments stand ready to bring forward some of their capital expenditure

projects as a way of supporting aggregate demand at a time of continued global

uncertainty. The Saudi government recently announced that it will stick to its 2010

budget spending of SAR540bn. What is less clear is the way in which governments

will utilize the debt capital markets to fund their spending. Saudi Finance Minister

Ibrahim al Assaf recently stated that the Kingdom does not plan to roll over a

USD7.7bn Riyal-denominated government bond maturing in January 2011 and,

moreover, intends to stay away from the debt market until it has brought down its

debt to 10% of GDP. This position is further supported by the rebounding oil prices

which have ensured that the GCC government’s finances are in a strong position

even at a time of elevated spending. However, some other regional governments

have taken a different view and even in Saudi Arabia, some large government-

related entities have the potential to be key players in the continued development

of the market.

Even as regional sovereigns will pursue divergent strategies in the near term,

improving investor sentiment in the GCC will encourage corporate bonds/sukuks in

the future. Some recently announced issues in the GCC region include:

• Qatari Diar Finance, the property wing of Qatar’s sovereign wealth fund,

concluded its dual tranche bond sale on July 14. The USD3.5bn issue

comprised USD1.0bn of five-year notes priced 180 basis points over

comparable US Treasuries and USD2.5bn of 10-year notes priced to yield

190 basis points over US Treasury bonds.

• Saudi Arabia-based Ahmed Salem Bugshan Group (ASB) plans to raise

USD100mn through five-year sukuk to fund projects including real-estate

development and a large steel plant.

• Qatar Islamic Bank, the biggest Shariah-compliant bank in Qatar plans to

sell a USD750mn sukuk in the second half of the year.

Planned capital

expenditure and

infrastructure investments

are likely to drive the GCC

debt market in the coming

quarters

8/8/2019 20100719184745eGCC Debt Market Tracker - July2010

http://slidepdf.com/reader/full/20100719184745egcc-debt-market-tracker-july2010 8/10

8/8/2019 20100719184745eGCC Debt Market Tracker - July2010

http://slidepdf.com/reader/full/20100719184745egcc-debt-market-tracker-july2010 9/10

JULY 2010 9

GCC DEBT MARKETS

Exhibit 13: Key sukuk and conventional bond issuances in 2Q10

Issuer Issue date Maturity Amount issued(USD mn)

Sovereign sukuk issuance

Qatar Sovereign Sukuk 6/1/2010 6/1/2018 1,373.0

Central Bank of Bahrain (ijarah) 5/18/2010 11/18/2010 26.5

Central Bank of Bahrain (ijarah) 4/26/2010 7/26/2010 31.8

Central Bank of Bahrain (ijarah) 4/20/2010 10/20/2010 26.5

Central Bank of Bahrain (al salam) 4/28/2010 7/28/2010 32.0

Central Bank of Bahrain (al salam) 6/2/2010 9/1/2010 32.0

Central Bank of Bahrain (al salam) 6/30/2010 9/29/2010 32.0 Corporate sukuk issuance

Saudi Electricity Company Sukuk III 5/10/2010 5/10/2017 1,866.8

Sovereign bond and T-bill issuance

Bahrain Treasury Bill 5/10/2010 7/14/2010 66.6

Bahrain Treasury Bill 4/14/2010 7/21/2010 66.6

Bahrain Treasury Bill 4/21/2010 8/4/2010 66.6

Bahrain Treasury Bill 5/5/2010 8/11/2010 66.6

Bahrain Treasury Bill 5/12/2010 8/18/2010 66.6

Bahrain Treasury Bill 5/19/2010 8/25/2010 66.6

Bahrain Treasury Bill 5/26/2010 9/9/2010 66.6

Bahrain Treasury Bill 6/8/2010 9/15/2010 66.6

Bahrain Treasury Bill 6/16/2010 9/22/2010 66.6

Bahrain Treasury Bill 6/23/2010 10/10/2010 53.3

Bahrain Treasury Bill 4/11/2010 12/12/2010 53.3

Bahrain Treasury Bill 6/13/2010 6/9/2011 133.2

Mumtalakat 6/10/2010 6/30/2015 750.0

Kuwait Treasury Bills 6/30/2010 7/27/2010 641.5

Kuwait Treasury Bills 4/27/2010 8/10/2010 242.7

Kuwait Treasury Bills 5/11/2010 8/24/2010 440.4

Kuwait Treasury Bills 5/25/2010 9/5/2010 450.8

Kuwait Treasury Bills 6/6/2010 9/13/2010 443.8

Kuwait Treasury Bills 6/14/2010 12/8/2010 558.3

Kuwait Government Bonds 6/9/2010 4/6/2011 277.4

Kuwait Government Bonds 4/7/2010 4/13/2011 173.4Kuwait Government Bonds 4/14/2010 4/20/2011 294.7

Kuwait Government Bonds 4/21/2010 4/27/2011 242.7

Kuwait Government Bonds 4/28/2010 5/4/2011 433.4

Kuwait Government Bonds 5/5/2010 5/11/2011 208.0

Kuwait Government Bonds 5/12/2010 5/9/2012 114.4

Kuwait Treasury Bills 5/12/2010 7/29/2010 260.1

Kuwait Treasury Bills 4/29/2010 8/2/2010 260.1

Central Bank of Oman CD 5/3/2010 7/14/2010 506.0

Central Bank of Oman CD 6/16/2010 7/21/2010 868.6

Central Bank of Oman CD 6/23/2010 7/28/2010 1,312.0

Qatar Government Bonds 6/1/2010 6/1/2018 1,373.0

Qatar Government Bonds 6/1/2010 6/30/2015 549.7

Corporate bond issuance

Dubai Electricity & Water Authority 6/30/2010 4/22/2015 1,000.0

United Real Estate 6/22/2010 6/22/2013 39.9

United Real Estate 6/22/2010 6/22/2013 98.8

Gulf International Bank 4/27/2010 4/27/2015 934.8

National Bank of Abu Dhabi PJSC 6/21/2010 6/21/2012 44.0

Bank Muscat SAOG 5/31/2010 5/31/2011 39.1

Source: Bloomberg, NCBC Research

8/8/2019 20100719184745eGCC Debt Market Tracker - July2010

http://slidepdf.com/reader/full/20100719184745egcc-debt-market-tracker-july2010 10/10

JULY 2010

GCC DEBT MARKETS

IMPORTANT INFORMATION AND DISCLAIMERS

In the issue of timeliness, the stock prices throughout the report are based on last traded prices (and thus may differ from the adjusted pricesprovided by the exchange post closing).

The authors of this document hereby certify that the views expressed in this document accurately reflect their personal views regarding thesecurities and companies that are the subject of this document. The authors also certify that neither they nor their respective spouses ordependants (if relevant) hold a beneficial interest in the securities that are the subject of this document. Funds managed by NCB Capital andits subsidiaries for third parties may own the securities that are the subject of this document. NCB Capital or its subsidiaries may ownsecurities in one or more of the aforementioned companies, or funds or in funds managed by third parties The authors of this document mayown securities in funds open to the public that invest in the securities mentioned in this document as part of a diversified portfolio over whichthey have no discretion. The Investment Banking division of NCB Capital may be in the process of soliciting or executing fee earningmandates for companies that are either the subject of this document or are mentioned in this document.

This document is issued to the person to whom NCB Capital has issued it. This document is intended for general information purposes only,and may not be reproduced or redistributed to any other person. This document is not intended as an offer or solicitation with respect to thepurchase or sale of any security. This document is not intended to take into account any investment suitability needs of the recipient. Inparticular, this document is not customized to the specific investment objectives, financial situation, risk appetite or other needs of anyperson who may receive this document. NCB Capital strongly advises every potential investor to seek professional legal, accounting andfinancial guidance when determining whether an investment in a security is appropriate to his or her needs. Any investmentrecommendations contained in this document take into account both risk and expected return. Information and opinions contained in thisdocument have been compiled or arrived at by NCB Capital from sources believed to be reliable, but NCB Capital has not independentlyverified the contents of this document and such information may be condensed or incomplete. Accordingly, no representation or warranty,express or implied, is made as to, and no reliance should be placed on the fairness, accuracy, completeness or correctness of the informationand opinions contained in this document. To the maximum extent permitted by applicable law and regulation, NCB Capital shall not be liablefor any loss that may arise from the use of this document or its contents or otherwise arising in connection therewith. Any financialprojections, fair value estimates and statements regarding future prospects contained in this document may not be realized. All opinions andestimates included in this document constitute NCB Capital’s judgment as of the date of production of this document, and are subject tochange without notice. Past performance of any investment is not indicative of future results. The value of securities, the income from them,the prices and currencies of securities, can go down as well as up. An investor may get back less than he or she originally invested.Additionally, fees may apply on investments in securities. Changes in currency rates may have an adverse effect on the value, price orincome of a security. No part of this document may be reproduced without the written permission of NCB Capital. Neither this document norany copy hereof may be distributed in any jurisdiction outside the Kingdom of Saudi Arabia where its distribution may be restricted by law.

Persons who receive this document should make themselves aware, of and adhere to, any such restrictions. By accepting this document, therecipient agrees to be bound by the foregoing limitations.

NCB Capital is authorised by the Capital Market Authority of the Kingdom of Saudi Arabia to carry out dealing, as principal and agent, andunderwriting, managing, arranging, advising and custody, with respect to securities under license number 37-06046. The registered office of which is at Al Mather street in Riyadh, P.O. Box 22216, Riyadh 11495, Kingdom of Saudi Arabia.