Embed Size (px)

DESCRIPTION

2010 Technology Study Plans for 2011. John Van Decker, VP Research Gartner. Table of Contents. Study Overview Top 10 Findings Plans for 2011. Study Demographics. Corporate Perspective. Senior Financial Executives. Source: Gartner FEI April 2010 N = 482 - PowerPoint PPT Presentation

Citation preview

Notes accompany this presentation. Please select Notes Page view. These materials can be reproduced only with written approval from Gartner.Such approvals must be requested via e-mail: [email protected] is a registered trademark of Gartner, Inc. or its affiliates.

2010 Technology StudyPlans for 2011

John Van Decker, VP Research Gartner

Table of Contents

• Study Overview

• Top 10 Findings

• Plans for 2011

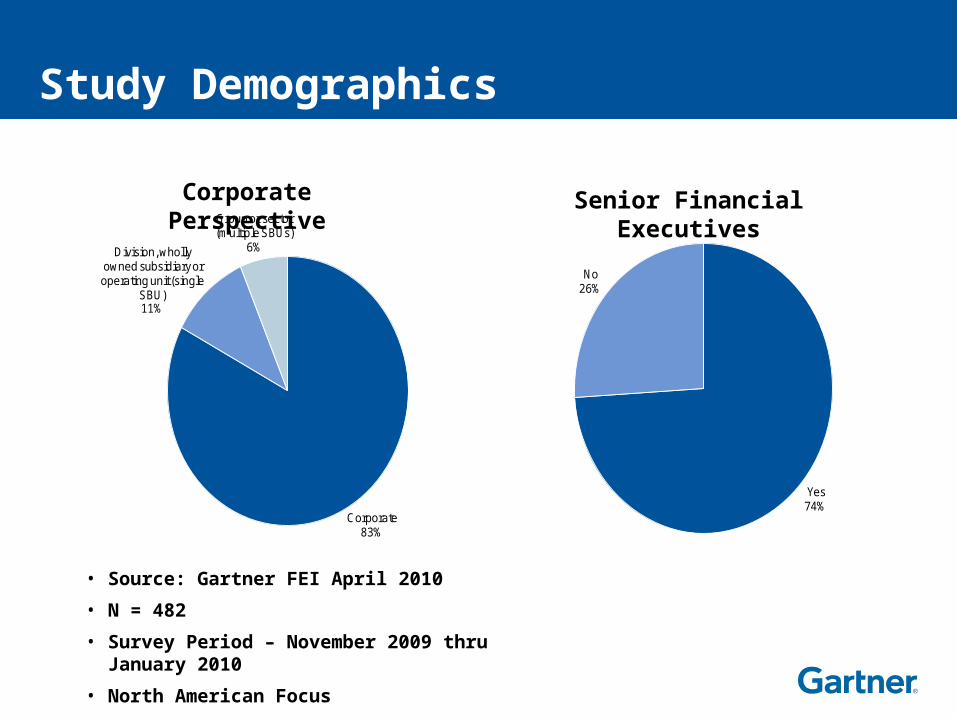

Study Demographics

Corporate83%

Division, wholly owned subsidiary or operating unit (single

SBU)11%

Group or sector (multiple SBUs)

6%

Yes74%

No26%

Corporate Perspective Senior Financial Executives

• Source: Gartner FEI April 2010

• N = 482

• Survey Period – November 2009 thru January 2010

• North American Focus

Study Demographics

Privately held59%

Publicly traded35%

Other6%

1.2

1.2

1.2

1.4

1.7

1.7

1.9

2.1

2.1

2.4

2.8

2.8

3.1

3.1

3.1

3.3

3.5

3.8

4.0

4.0

4.0

4.7

5.0

5.2

7.1

9.7

14.2

0 5 10 15

Higher Education

Mining and Metals

Publishing and Printing

Consumer Goods Manufacturing …

Chemicals

Utilities

Telecommunications

Transportation Services

Healthcare (Provider)

Media and Entertainment

Financial Services (Banking)

Oil and Gas

Wholesale

Healthcare (Pharmaceutical)

Real Estate

Nonprofit (Nongovernmental)

Financial Services (Other)

Distribution

Engineering and Construction

Consumer Goods Manufacturing …

Retail

Aerospace and Defense

Financial Services (Insurance)

Industrial Manufacturing (Process)

Industrial Manufacturing (Discrete)

Professional Services

High-Tech

Percentage of Respondents

IndustriesCorporate Ownership

• Source: Gartner FEI April 2010

• N = 482

• Survey Period – November 2009 thru January 2010

• North American Focus

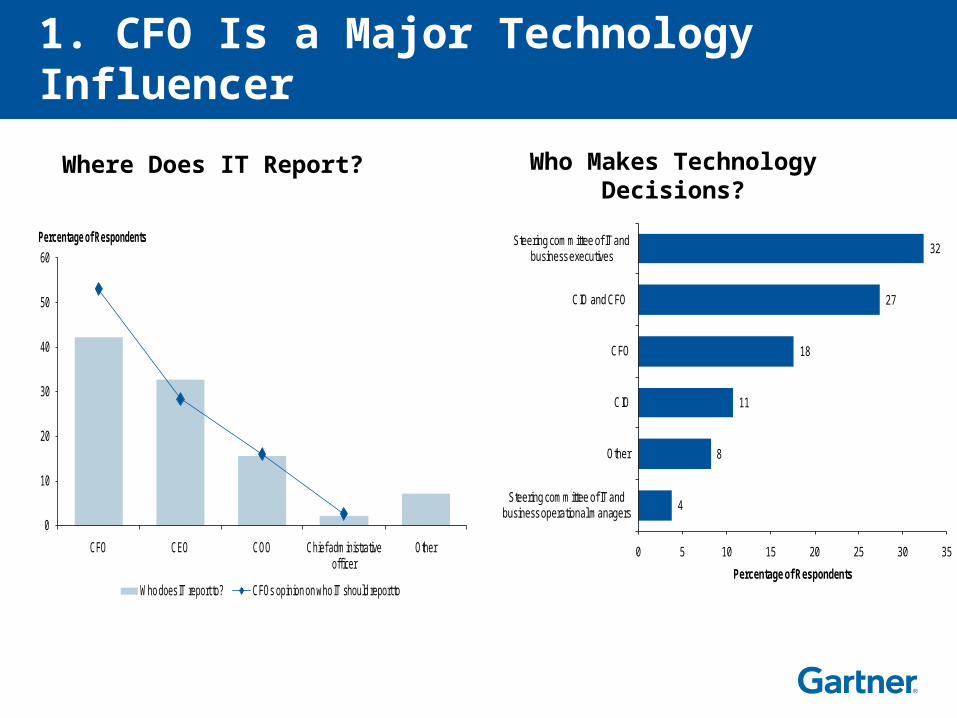

1. CFO Is a Major Technology Influencer

0

10

20

30

40

50

60

OtherChief administrative officer

COOCEOCFO

Who does IT report to? CFOs opinion on who IT should report to

Percentage of Respondents

4

8

11

18

27

32

0 5 10 15 20 25 30 35

Steering committee of IT and business operational managers

Other

CIO

CFO

CIO and CFO

Steering committee of IT and business executives

Percentage of Respondents

Where Does IT Report? Who Makes Technology Decisions?

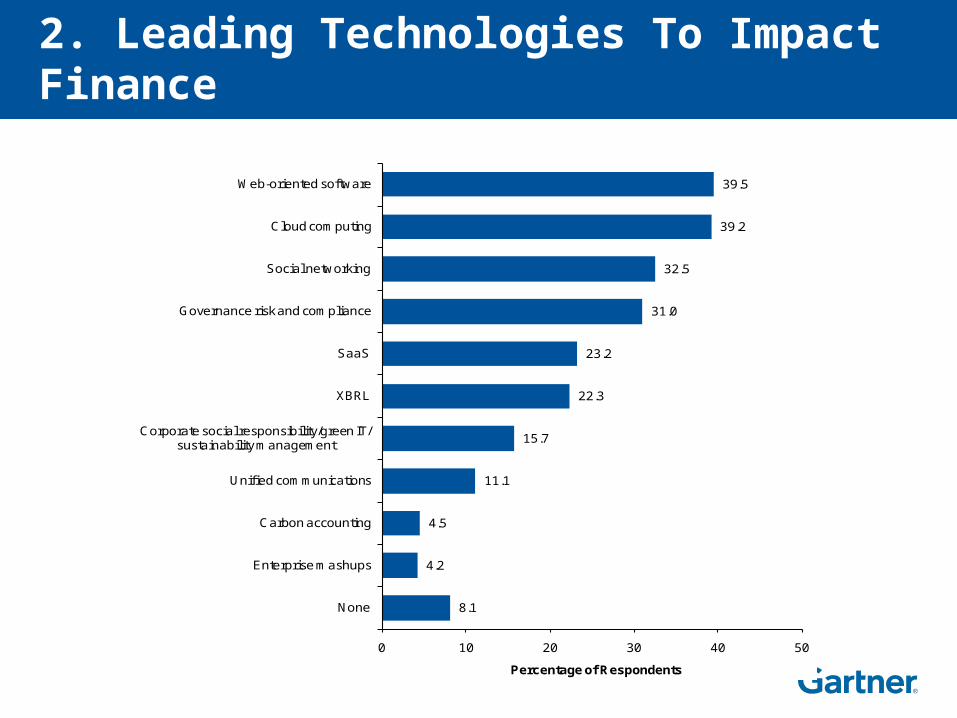

2. Leading Technologies To Impact Finance

39.5

39.2

32.5

31.0

23.2

22.3

15.7

11.1

4.5

4.2

8.1

0 10 20 30 40 50

Web-oriented software

Cloud computing

Social networking

Governance risk and compliance

SaaS

XBRL

Corporate social responsibility/green IT/sustainability management

Unified communications

Carbon accounting

Enterprise mashups

None

Percentage of Respondents

3. ERP Projects Largely Successful

3

10

17

33

37

0 5 10 15 20 25 30 35 40

Failure

Moderately problematic

Highly successful

Neutral

Moderately successful

Percentage of Respondents

12

14

24

51

0 10 20 30 40 50 60

Implement only when installed release is no longer supported

Adopt as new releases become available

Implement to remain within one release of current release

Implement only when substantial new functionality is

provided

Percentage of Respondents

Perception of ERP Implementation

When to Upgrade

4. CFOs Promote "Return to Growth" Strategies for IT

86.1

66.9

62.0

60.2

46.1

40.4

34.0

32.2

30.1

28.3

20.8

8.1

0 20 40 60 80 100

Investing in initiatives with competitive advantage

Deferred new projects

Investigating new technologies

Renegotiating service agreements to reduce maintenance

Moving to more packaged applications

Discontinuing non-mission-critical applications/support

Moving to outsourced applications/support

Pursuing outsourcing

Delegating out to user organizations

Cutting IT spending/staff

Stopped projects in progress

Halting all enhancements

Percentage of Respondents

5. CFOs See the Critical Nature of Improving Data Quality

33

32

31

30

30

27

26

25

24

24

23

19

19

17

9

8

52

53

56

49

55

50

41

52

60

55

55

61

68

55

54

19

0 10 20 30 40 50 60 70 80 90 100

Improving data quality/information integrityso that finance, management andoperational reports are consistent

Identifying the appropriate level of securityfor information and electronic applications

Achieving the expected benefits fromIT investments

Using technology to improve customer metrics(new sales, retention and loyalty)

Prioritizing technology investments

Using technology to drive business change

Upgrading or replacing legacy systems

Aligning business and IT strategy

Optimizing technology platforms tooptimize cost efficiencies

Establishing and maintaining effectivedialogue between IT and users

Increasing the usage of common systemsand shared technology

Identifying how IT can improve or influencebusiness processes

Identifying the appropriate level of technology investment

Developing disaster recovery capabilities

Using IT to assist with governance, riskmanagement and compliance

Other

Percentage of Respondents

Critical

Important

6. CFOs Aren't Yet Sold on XBRL

53.3

37.1

5.4

4.2

- 10 20 30 40 50 60

No decision

External reporting only

External reporting and supplement to internal reporting

External reporting and replacement for certain internal reports

Percent

How Do Organizations Plan to Use XBRL

7. CFOs Are Still Resisting Action on IFRS

46.1

30.4

18.7

2.4

2.4

0 10 20 30 40 50

Not applicable for my organization

All conversion activities to be deferred until closer to the required adoption date

Planning and impact analysis in progress, but implementation to be deferred until

closer to the required adoption date

All conversion activities are in progress

Conversion activities are complete

Percentage of Respondents

Progress of IFRS Projects

43.7

32.5

13.3

5.7

1.8

0 10 20 30 40 50

Not worried

Only begun to size activity

Minor changes to ERP

Changes only in financial reporting

Generally accepted accounting principles to IFRS adjustments in …

Percentage of Respondents

Impact on Business Apps

8. CFOs View Profitability Management as the Top Technological Constraint

19.6

9.1

8.6

7.8

7.4

7.4

7.1

6.6

6.1

5.1

4.3

3.9

3.9

3.4

3.1

1.5

0.7

1.0

8.0

4.3

9.4

7.7

3.1

11.3

11.3

7.2

7.0

8.5

3.4

4.3

3.2

3.4

3.4

3.1

1.7

1.7

6.6

5.1

8.3

6.3

5.4

8.3

10.2

8.0

6.6

3.4

2.0

6.6

1.7

3.4

2.7

1.5

2.9

2.4

0 10 20 30 40

Measuring product and customer profitability

Integrating financial function with enterprise

Integrating strategy with business operations

Enterprisewide view of business relationships

Managing business risk

Ongoing monitoring of business performance

Facilitating analysis and decision making

Knowledge management

Reducing enterprise operating costs

Data quality and information integrity

Developing business plans and budgets

Positioning the company for profitable growth

Managing integration of systems

Consolidating financial processes/instances

Drivers of profitability/cost of service delivery

Modeling business development scenarios

Improving financial value chain areas

Other

Percentage of Respondents

1st

2nd

3rd

9. CFOs Focus on BI and CPM Investments in 2010

53.6

49.1

40.1

38.7

38.7

38.7

38.3

17.6

14.4

7.7

0 10 20 30 40 50 60

Management dashboard

Planning/budgeting/forecasting

Performance measurement/scorecard

Customer and product profitability

Data warehouse

Consolidation and reporting

financial consolidation and reporting

Predictive modeling

Statistical analysis

Other (please specify)

Percentage of Respondents

2.0

21.8

56.4

18.8

1.7

0 10 20 30 40 50 60

Exceptional

Superior

Average

Poor

Failing

Percentage of Respondents

Relative Maturity of BI and CPM Investments

Planned Upgrades in 2010

10.a. Outsourcing Implementations to Grow 24%

0 10 20 30 40 50

Payroll

Travel Planning

HR

Travel Reimbursement

Fixed Assets

Accounts Payable

GL & Accounting

Credit & Collections

Billing and Invoicing

Customer Service

Order Management

Percentage of Respondents

Planned Current

10b. Shared Service Implementations to Grow 23%

0 5 10 15 20 25 30 35 40 45

Payroll

Travel Planning

HR

Travel Reimbursement

Fixed Assets

Accounts Payable

GL & Accounting

Credit & Collections

Billing and Invoicing

Customer Service

Order Management

Percentage of Respondents

Future Plans Current

Recommended Research

"2010 Gartner-FEI Technology Study: The CFO as Technology Influencer“

"2010 Gartner FEI Technology Study: The CFO's Perspective on Data Quality“

"2010 Gartner FEI Technology Study: Planned Shared Services and Outsourcing to Increase“

"2010 Gartner FEI Technology Study: CFOs Green Light IT Investment“

"2010 Gartner-FEI Technology Study: The CFO's Perspective on ERP“

"2010 Gartner FEI Technology Study: U.S. Firms Still Resisting Action on IFRS“

"2010 Gartner FEI Technology Study: GRC, SOX and XBRL“

"2010 FEI Technology Study: CPM and BI Show Improvement From 2009"

2010 Study Performance

• More consistency and quality

• Good survey response

• Leverage work from 2009

• Overall – Major Improvements, Good Performance

• Reports out on time!

Goals for 2011

• Consistency with Gartner CIO Study

• Leverage 2010 study

• 30% increase in responses

• 10% decrease in questions

• Less preparation needed to ensure completing study

• Move off Survey Monkey – internal Gartner support

• Launch on October 1

Timeframe for 2011 Study

• August 1 Determine Survey Vehicle

• August 1 Draft Survey

• September 1Finalize Survey

• October 1 Launch

• January 15 Close

• April 15 Report