Embed Size (px)

Citation preview

2010 NSAA IT Conference

Gaining Audit Efficiency and Insight Through Risk Metrics & Data Analytics

_____________________________________

September 29, 2010April Gunn, CPA, CISAVirginia Auditor of Public Accounts

2010 NSAA IT Conference

Speaker Biography

Virginia Auditor of Public Accounts Audit Director Data Analysis Director Judicial Director

Commonwealth Data Point James Madison University Alumni CPA, CISA Wife, mother of two boys

2010 NSAA IT Conference

Objectives

Provide ways to pinpoint risks of non-compliance using data

How to achieve efficiency through reviewing data as a whole instead of individually

How to automate assigning risk factors to data

Challenges of implementing a risk-based audit approach

2010 NSAA IT Conference

Background

207 District Courts – including General District, Juvenile and Domestic Relations, and Combined

Goal was to visit each court a maximum of every 24 months

Same audit program for years – including only revenue cycle

TONS of data not being used No link between central oversight and local

courts

2010 NSAA IT Conference

Challenge

Incorporate other audit cycles – Expenditures, Payroll

Develop audit using manuals and data analytics combined

Visit ALL District Courts in 9 months Relate to central audit of the Supreme Court Make big picture recommendations to improve

oversight

2010 NSAA IT Conference

Answer

Develop risk metrics using data in addition to known risks

Perform a risk analysis of all courts Determine which courts to test in detail vs.

those to test minimally Create new programs to focus test work

only where necessary

2010 NSAA IT Conference

Process

Determine Risks

Gather Data

Develop reports/queries

Assign risks and Accumulate data

Write new programs

2010 NSAA IT Conference

Risk FactorsRisk Factor Points Assigned

Staff Size Variable

Turnover Variable

Prior year audit findings 4 pts per written finding2 pts per verbal finding

Fraud 10 pts

New Clerk 3 pts

Case to Staff Ratio Variable

Exception Reports 3 pts for cash over/short report2 pts for extended due dates and payroll1 pt for all others

Dismissed Cases Test work performed at all high risk (top 5%)

2010 NSAA IT Conference

Example Script – Staff Size

Open Staff_Count

DEFINE FIELD Staff_Count_RF COMPUTED

5 IF BETWEEN(Staff_Count,0,1.99)

4 IF BETWEEN(Staff_Count,2,2.99)

3 IF BETWEEN(Staff_Count,3,3.99)

2 IF BETWEEN(Staff_Count,4,4.99)

0

END

2010 NSAA IT Conference

2010 NSAA IT Conference

OPEN Staff_Count

DEFINE FIELD Case_to_Staff_RF COMPUTED

1 IF (BETWEEN(Ratio_Cases_to_Staff,439,2619) AND Court_type = 'G')

3 IF (BETWEEN(Ratio_Cases_to_Staff,0,440) AND Court_type = 'G')

3 IF (BETWEEN(Ratio_Cases_to_Staff,2618,5000) AND Court_type = 'G')

0

END

Example Script – Case to Staff

2010 NSAA IT Conference

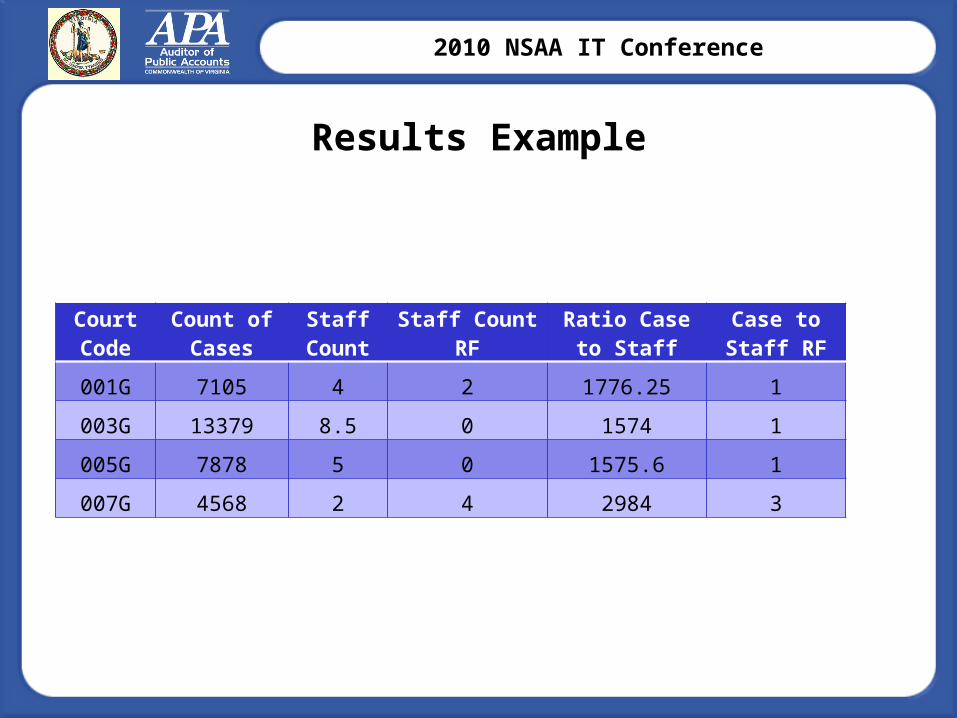

Court Code

Count of Cases

Staff Count Staff Count RF

Ratio Case to Staff

Case to Staff RF

001G 7105 4 2 1776.25 1

003G 13379 8.5 0 1574 1

005G 7878 5 0 1575.6 1

007G 4568 2 4 2984 3

Results Example

2010 NSAA IT Conference

2010 NSAA IT Conference

Example Script – Turnover Ratio

Open turnover

DEFINE FIELD Turnover_RF COMPUTED

1 IF BETWEEN(Percent_Turnover_2009,2.8,12.4)

2 IF BETWEEN(Percent_Turnover_2009,12.3,21.8)

3 IF BETWEEN(Percent_Turnover_2009,21.7,31.2)

4 IF BETWEEN(Percent_Turnover_2009,31.1,40.6)

5 IF BETWEEN(Percent_Turnover_2009,40.5,50.1)

0

END

2010 NSAA IT Conference

Exception Report Descriptions

Revenue Specific accounts codes = code mandated

amount Cash over/short Extended due dates

Expenses Fees paid out = code mandated amount

Experts Court Appointed Attorney Fees Involuntary Mental Commitments

2010 NSAA IT Conference

Exception Report Descriptions

Payroll Bonuses Overtime Leave

Other Systems Access

2010 NSAA IT Conference

Risk Accumulation

Exception reports combined into one table on a summary level

Created script to assign risks 3 pts for Cash Over/Under 2 pts for Payroll and Extended Due Dates 1 pt for all others

Combined all risks into one table by court Calculated a total risk score

2010 NSAA IT Conference

2010 NSAA IT Conference

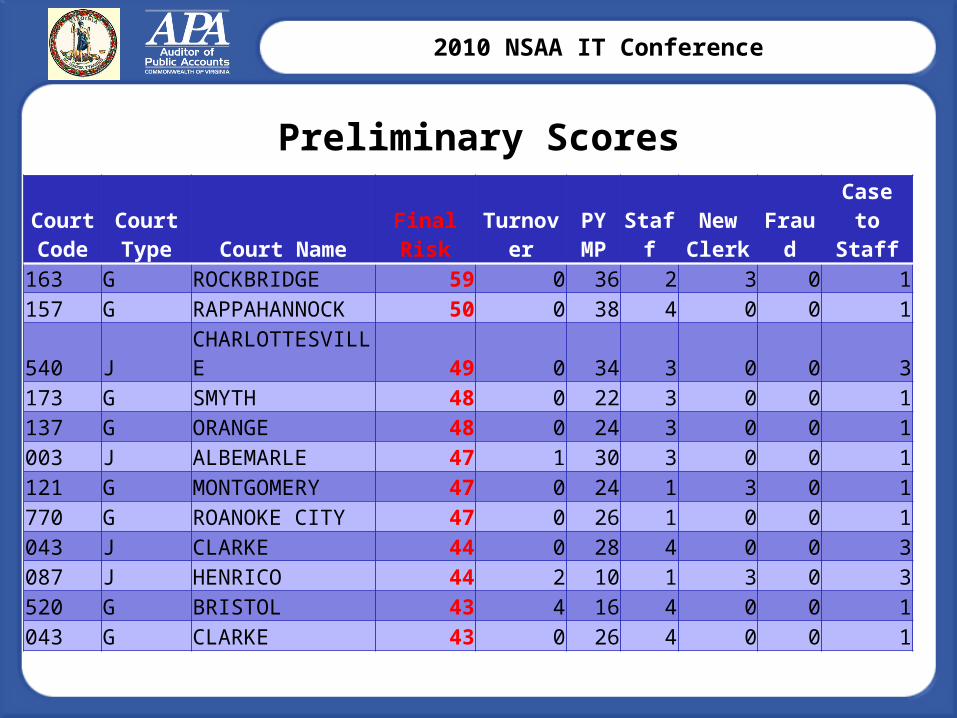

Preliminary Scores

Court Code

Court Type Court Name

Final Risk

Turnover

PY MP

Staff

New Clerk

Fraud

Case to

Staff163 G ROCKBRIDGE 59 0 36 2 3 0 1157 G RAPPAHANNOCK 50 0 38 4 0 0 1

540 JCHARLOTTESVILLE 49 0 34 3 0 0 3

173 G SMYTH 48 0 22 3 0 0 1137 G ORANGE 48 0 24 3 0 0 1003 J ALBEMARLE 47 1 30 3 0 0 1121 G MONTGOMERY 47 0 24 1 3 0 1770 G ROANOKE CITY 47 0 26 1 0 0 1043 J CLARKE 44 0 28 4 0 0 3087 J HENRICO 44 2 10 1 3 0 3520 G BRISTOL 43 4 16 4 0 0 1043 G CLARKE 43 0 26 4 0 0 1

2010 NSAA IT Conference

Additional Considerations

Lapse or Over Coverage Combined Courts splitting Other

2010 NSAA IT Conference

Final Scores/Moving Forward

Established two different audit types Full Audit Internal Control Questionnaire

Tracked findings centrally during audit cycle of six months

Conducted central audit and any follow-up on local findings necessary at same time

2010 NSAA IT Conference

Findings

Leave approvals – questionnaire only No log with cases transferred Weaknesses in transition/payment of

expenses from local to central Data entry errors Many miscommunications from central

oversight

2010 NSAA IT Conference

Lessons Learned

Getting data in a usable format Prepare for “fires” Expect hesitation from client and/or staff Allow time, time, time, and more time

2010 NSAA IT Conference

Other possible applications

Small Purchase Charge Cards Any program where risks can be quantified

Eligibility programs Decentralized clients Internal audit identification – grant awards,

etc Can be supplied to clients for monitoring

internally