Embed Size (px)

Citation preview

2009:038

M A S T E R ' S T H E S I S

E-Business Adoption in theBanking Industry in Ghana

Emma Anamuah-Mensah Georgia Marfo

Luleå University of Technology

Master Thesis, Continuation Courses Marketing and e-commerce

Department of Business Administration and Social SciencesDivision of Industrial marketing and e-commerce

2009:038 - ISSN: 1653-0187 - ISRN: LTU-PB-EX--09/038--SE

i

To God Be The Glory Great Things He Has

Done!

ii

iii

ACKNOWLEDGEMENTS

To God Almighty and Our Lord and Saviour Jesus Christ.

We express our profound and deepest gratitude to you. Your grace and mercy have

enabled us to make this milestone. Our reverence to you Father.

To Dr. Anne.Engstrom - our wonderful supervisor

We owe you a special debt of gratitude for your excellent guidance, thorough

supervision and positive criticism that has engineered the production of this work. We

salute you madam! We say God richly bless and increase you abundantly.

To the Staff of the four sampled banks

Our deepest appreciation for your time, efforts and inputs for being used as the case

study in this study. You have our respect Sirs! God bless you all.

To Dr. Kwame Adam- our Friend and Proof Reader

We say special thanks to you for all your energy, time, efforts and contributions. God

bless you.

Finally, to all who shared a word or two with us, encouraged, prayed and supported us

in diverse ways to assist us complete successfully this thesis, we say our Almighty God

bless you with your heart desires for you have helped us to achieve ours.

God Bless Everyone.

While we share the credit of this thesis with all the above-mentioned people,

responsibility for any errors, shortcomings or omissions in this work is solely our own.

iv

DEDICATION

This thesis is dedicated to our husbands;

Mr. Ebow Amanuah Mensah & Mr. Emmanuel Coffie

For Your Love and Support

v

ABSTRACT

This thesis is based on a case study of four banks, in Ghana; two private and two state

banks. The study only sought to examine the adoption of e-Business in the Ghanaian

banking industry with respect to the expected benefits derived by adopting e-business,

the barriers that prevent firms from taking advantage of e-business adoption and the

challenges firms encounter when adopting e-business. The study idea was conceived on

the premise that businesses are always looking for ways of improving their products

and services deliveries and will thus be useful to understand how the adoption of e-

Business can benefit the banking industries in Ghana that is seen to be in the fore-front

of national development. The researchers also wanted to understand how electronic

commerce as a new way of doing business can be introduced effectively in the

Ghanaian banking business especially with the understanding that E-business involves

the fundamental reengineering of business model into a internet based networked

enterprise.

The result of the study indicated that the benefits of e-business are well known to the

banks and represent a formidable force to drive the adoption by many banks in Ghana.

The benefits of e-business are experienced whether or not the bank is state or private.

The various areas where the banks are preparing to use e-business approach includes

familiar and relatively mature electronically-based products in developing markets,

such as telephone banking, credit cards, ATMs, and direct deposit. This means that

most of the banks have recognized the need to change their business process to conform

to changing business trends in order to keep up with competition. Despite the perceived

and experienced benefits of e-business in Ghanaian banking, they also identified

vi

several barriers and challenges that could be described as: economic; technical and

technological; ethical and institutional; and socio-cultural. The results also revealed that

the banks consider technology as the most important challenge to the effective adoption

of e-service in the banking industry in Ghana. The study provides some

recommendations towards improving e-business adoption in Ghanaian banks

vii

TableofContents

ACKNOWLEDGEMENTS ............................................................................................................................. IIIDEDICATION ..................................................................................................................................................IVABSTRACT .......................................................................................................................................................VTABLEOFCONTENTS................................................................................................................................VIITABLEOFTABLES........................................................................................................................................IXCHAPTER1: INTRODUCTION................................................................................................................. 11.1. BACKGROUND......................................................................................................................................................... 11.2. PURPOSEOFSTUDY ............................................................................................................................................... 41.3. RESEARCHQUESTIONS.......................................................................................................................................... 41.4. SIGNIFICANCEOFTHESTUDY.............................................................................................................................. 51.5. SCOPEANDLIMITATIONOFSTUDY.................................................................................................................... 5

CHAPTER2: LITERATUREREVIEW ..................................................................................................... 72.1. THEEVOLUTIONOFE‐BUSINESS........................................................................................................................ 72.2. DEFININGE‐BUSINESS.......................................................................................................................................... 72.3. E‐BUSINESSADOPTION......................................................................................................................................102.4. BENEFITSOFE‐BUSINESSADOPTION .............................................................................................................122.5. BARRIERSTOE‐BUSINESSADOPTION.............................................................................................................142.6. CHALLENGESRELATEDTOTHEADOPTIONOFE‐BUSINESS .......................................................................14

CHAPTER3: CONCEPTUALFRAMEWORK .......................................................................................163.1. INTRODUCTION ....................................................................................................................................................163.1.1. BenefitsofEBusiness ................................................................................................................................ 163.1.2. BarrierstoEBusinessAdoption........................................................................................................... 163.1.3. ChallengesofEBusinessadoption ...................................................................................................... 17

3.2. SUMMARIZATIONOFTHEORIES,CONCEPTSANDFRAMEOFREFERENCEINLINEWITHRESEARCHQUESTIONS.........................................................................................................................................................................173.2.1. ResearchQuestionOne:Whatarethebenefitsthatmaybederivedbyadoptingebusiness ............................................................................................................................................................................ 173.2.2. ResearchQuestionTwo:WhatarethebarrierstotheadoptionofebusinessinbanksinGhana........................................................................................................................................................................... 183.2.3. ResearchQuestionThree:Whatchallengesdobanksfaceinadoptingebusiness........ 19

CHAPTER4: METHODOLOGY ..............................................................................................................224.1. INTRODUCTION ....................................................................................................................................................224.2. RESEARCHPURPOSE ...........................................................................................................................................234.3. RESEARCHAPPROACH........................................................................................................................................234.3.1. StrategiesforResearch............................................................................................................................. 244.3.2. StudyArea ...................................................................................................................................................... 25

4.4. TYPEOFDATAANDDATACOLLECTION .........................................................................................................264.4.1. Typeofdata ................................................................................................................................................... 26

4.5. DATACOLLECTION ..............................................................................................................................................274.5.1. SampleSelection.......................................................................................................................................... 274.5.2. EmpiricalData ............................................................................................................................................. 274.5.3. Secondarydata............................................................................................................................................. 274.5.4. ResearchProtocolsandCasestudydatabase ................................................................................ 28

4.6. DATAANALYSIS ...................................................................................................................................................284.6.1. MethodofAnalysis ...................................................................................................................................... 29

viii

4.7. QUALITYDATA.....................................................................................................................................................304.7.1. ValidityandReliability ............................................................................................................................. 304.7.1.1. Validity........................................................................................................................................................................................ 30

4.7.2. Reliability........................................................................................................................................................ 31CHAPTER5: CASESTUDYANALYSIS .................................................................................................325.1. INTRODUCTION ....................................................................................................................................................325.2. GENERALDESCRIPTIONOFBANKINGINGHANA...........................................................................................325.3. INDIVIDUALCASEANALYSIS ..............................................................................................................................345.3.1. CaseOne:EcobankGhanaLtd. .............................................................................................................. 345.3.1.1. E‐businessAdoptioninEcobankGhanaLtd. ............................................................................................................. 355.3.1.2. Benefitsofe‐businessadoptioninEcobankGhana ................................................................................................ 355.3.1.3. Barrierstotheadoptionofe‐businessinEcobankGhana. .................................................................................. 355.3.1.4. Challengesintheadoptionofe‐businessinEcobank. ........................................................................................... 35

5.3.2. CaseTwo:StanbicBankGhanaLimited(SBG)............................................................................... 365.3.2.1. E‐businessAdoptioninStandbicBankGhana(SBG) ............................................................................................. 365.3.2.2. Benefitsofe‐businessadoptioninStanbicBankGhana ....................................................................................... 365.3.2.3. Barrierstotheadoptionofe‐businessinStanbicBankGhana(SBG)............................................................. 365.3.2.4. Challengesintheadoptionofe‐businessinStanbicBankGhana(SBG)........................................................ 37

5.3.3. CaseThree:AgriculturalDevelopmentBank(ADB).................................................................... 375.3.3.1. E‐businessAdoptioninAgriculturalDevelopmentBank..................................................................................... 385.3.3.2. Benefitsofe‐businessadoptioninAgriculturalDevelopmentBankLtd....................................................... 385.3.3.3. Barrierstotheadoptionofe‐businessinAgriculturalDevelopmentBankLtd ......................................... 385.3.3.4. Challengesintheadoptionofe‐businessinAgriculturalDevelopmentBank(ADB) .............................. 38

5.3.4. CaseFour:GhanaCommercialBank .................................................................................................. 385.3.4.1. E‐businessAdoptioninGhanaCommercialBankLtd............................................................................................ 395.3.4.2. Benefitsofe‐businessadoptioninGhanaCommercialBankLtd ..................................................................... 395.3.4.3. Barrierstotheadoptionofe‐businessinGhanaCommercialBankLtd ........................................................ 395.3.4.4. Challengesintheadoptionofe‐businessinGhanaCommercialbankGhana ............................................. 40

5.4. CROSSCASEANALYSIS .......................................................................................................................................405.4.1. Crosscaseanalysis ...................................................................................................................................... 405.4.2. BankingBusinessCharacteristicsinGhana..................................................................................... 405.4.2.1. BankageandRegionalcoverage..................................................................................................................................... 405.4.2.2. Typeandlocationofcustomers....................................................................................................................................... 435.4.2.3. Reasonsforapplyinge‐business ..................................................................................................................................... 435.4.2.4. E‐servicesandproducts...................................................................................................................................................... 43

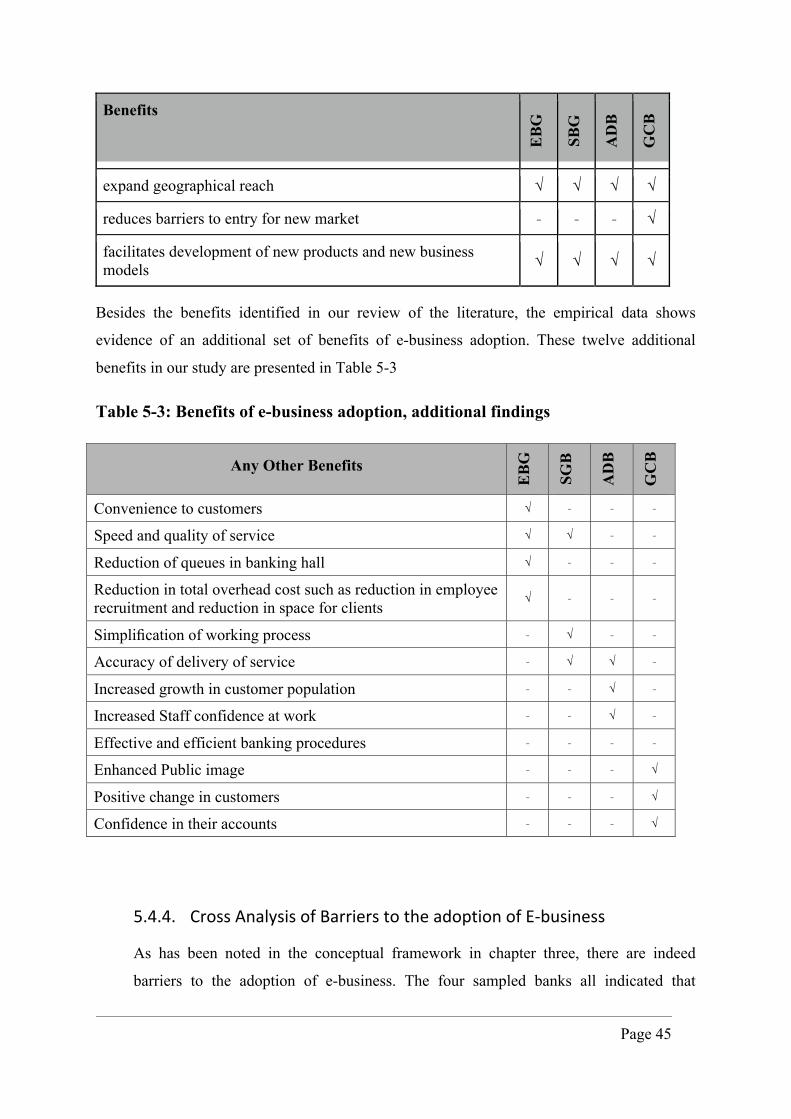

5.4.3. CrossAnalysisofBenefitstotheadoptionofEbusiness............................................................ 435.4.4. CrossAnalysisofBarrierstotheadoptionofEbusiness ........................................................... 45

5.5. CROSSANALYSISOFPERCEIVEDCHALLENGESINTHEADOPTIONOFE‐BUSINESS. .................................47CHAPTER6: CONCLUSIONSANDRECOMMENDATIONS..............................................................496.1. BENEFITSTHATMAYBEDERIVEDBYADOPTINGEBUSINESS ........................................................................496.2. BARRIERSTOTHEADOPTIONOFEBUSINESSINBANKSINGHANA ...............................................................506.3. CHALLENGESTHATBANKSFACEINADOPTINGEBUSINESS ...........................................................................506.4. SUMMARY..............................................................................................................................................................526.5. RECOMMENDATIONS...........................................................................................................................................53

REFERENCES .................................................................................................................................................55APPENDIX ......................................................................................................................................................72

Table of Figures

Figure 2-1: Classification of e-business and e-commerce (adapted from EC 2007) .................8 Figure 3-1: Emerged frame of reference..................................................................................21 Figure 5-1: Ghana map inserted with the Regional distribution of banks and Numbers

showing human population density per square kilometer.................................................42

ix

TableofTables

Table 3-1: A table showing research questions and theories used to answer. .........................20 Table 5-1: Description of the four selected Banks in Ghana ...................................................33 Table 5-2: Benefits of e-business adoption, derived from literature review............................44 Table 5-3: Benefits of e-business adoption, additional findings..............................................45 Table 5-4: Barriers to e-business adoption, derived from literature review ............................46 Table 5-5: Challenges of e-business adoption, derived from literature review .......................48 Table 5-6: Challenges of e-business adoption AdditionalFindings .........................................48

Page 1

Chapter1: Introduction

1.1. BackgroundInformation and Communication Technologies (ICTs) have become an essential part of

our lives. In the past decade, the use of ICT throughout society really took off with the

introduction of the Internet. The Internet started mainly as a network for researchers

that gave the opportunity to share information and ideas. An important step in the

commercialization of the Internet was the announcement of the World Wide Web

(www) in 1991 by Tim Berners-Lee of CERN (Kalakota and Whinston, 1996).

Today, because the Internet can facilitate the quick and efficient movement of

information among trading partners at a greatly reduced cost, (Ministry of Commerce

Barbados, 2005), business via the internet or electronic commerce (E-Commerce) has

become one of the principal means of doing business.

In the World Trade Organization (WTO) Work Programme, E-Commerce is

understood to mean the production, distribution, marketing, sale or delivery of goods

and services by electronic means. Broadly defined, electronic commerce encompasses

all kinds of commercial transactions that are concluded over an electronic medium or

network, essentially, the Internet. Electronic Commerce is a new way of doing

business. According to Payne (2003) it is transacting or enabling the marketing, buying,

and selling of goods and/or information through an electronic media, specifically the

Internet.

Recently authors have begun to delineate more explicitly a difference between e-

commerce and e-Business. E-commerce is emerging as the term used when discussing

the process of transacting business over the Internet. E-Business, on the other hand,

involves the fundamental reengineering of the business model into an Internet based

networked enterprise. The difference in the two terms according to most authors is the

degree to which an organization transforms its business operations and practices

Page 2

through the use of the Internet (Hackbarth & Kettinger 2000;

Mehrtens et.al. 2001; Poon 2000; Poon & Swatman, 1997).

In this study, we will use e-business to describe all electronically based exchanges of

goods, services and information.

According to Basu and Muylle (2007), E-Business has dramatically changed how

companies’ business processes are implemented and has also enhanced industry

structure and shifted the balance of power between corporations and their suppliers and

customers. According to them, companies in every industry have had to evaluate the

opportunities and threats presented by e-Business. By thinking strategically about e-

Business, managers can select technological solutions that support the company’s

business strategies and create value for the company and its customers (Cote et al,

2005).

The Internet is driving the new economy by creating unprecedented opportunities for

countries, companies and individuals around the world. Today CEOs worldwide

recognize the strategic role that the Internet plays in their company’s ability to survive

and compete in the future. (Al-Mudimigh, 2007). Indeed, currently businesses

everywhere need to understand the if,whenand how to use electronic commerce. In

some industries, businesses are learning now that this is no longer an option to

consider, but a requirement for survival. The reach of the underlying information and

communication technologies (ICT) making electronic commerce possible is also

causing unprecedented globalization of business. Businesses in developing countries

will soon be affected as significantly as those elsewhere (Payne, 2003). In this respect,

Kofi Annan former UN Secretary General opined that, the ability of developing

countries to adopt e-business can be another opportunity for accelerate economic

growth and development.

However, according to research conducted, companies and the private sector in Africa

have not been active initiators of e-commerce. For example, a survey in Ghana (part of

a Ghana SCAN-ICT study)1 revealed that about 65% of ICT companies do not have a

1 http://www.uneca.org/aisi/ScanGhana/presentations/The%20Ghana%20Scan-Workshop%20Programme-Final.pdf

Page 3

presence on the Internet and 84% reported that they were not involved in e-commerce.

(Opoku Mensah et al, 2005)

Though there are a growing number of examples of the use of ICT for electronic

business (e-Business) in developing countries the effects to date are small compared to

what is expected to occur (UNCTAD Report, 2002)2.

As the economy of Ghana is picking up the service industry especially the banking

industry are extending their national and regional coverage to be able to provide the

needed financial service. In this development it is expected that the use of the internet

would facilitate the adoption of e-business in the Ghana banking industry as a means of

offering fast, flexible, and cost-effective ways of doing business as well as enhance

their competitiveness. This state of development will be important especially as volume

of trade increases and Ghana and other developed countries require fast transfers of

monies, payments across continents, and many other services that promote growth of

business (Al-Mudimigh, 2007).

As with most developing countries that have pursued economic and structural reforms,

Ghana has been undergoing a process of financial sector restructuring and

transformation as an integral part of a comprehensive strategy for some time (Acquah,

2006). According to Bawumia (2007) banks in Ghana will need to reinvent themselves

in this new conducive but challenging environment. This is important because

electronic transactions will continue to grow and only countries that make a move

towards embracing e-Business will participate in this revenue generation (Akoh, 2001).

Banking in Ghana is one of the industries being radically transformed by ICT

(Frempong, 2007). For example most banks within the main cities of Ghana now

employ cutting edge technologies to roll out their products to their Ghanaian customers.

(Bawumia, 2007).

Banks today are becoming increasingly aware of both the threat and the opportunity

that the Web represents. ICT- mediated services such as automatic teller machines,

electronic fund transfer, electronic smart cards, cell phone banking among others, are

2 UNCTAD Report: "Developing world looks to e-Business for growth" http://www.apnic.net/mailing-lists/s-asia-it/archive/2002/11/msg00048.html

Page 4

transforming the traditional ways of banking and providing competitive edge for banks

that provide those services (Frempong, 2007). But, to be competitive in the Internet

economy, companies need to harness the power of the Internet successfully (Al-

Mudimigh, 2007) hence it is important to understand the benefits, barriers and

challenges related to companies’ adoption of e-business.

1.2. PurposeofstudyIn Ghana banking is one of the service industries crucial to the growth of its emerging

economy. Banking is important in the role it plays in capital mobilization and granting

of financial facilities that is crucial to business development and growth. As businesses

always need to find ways of improving its products and services deliveries it will be

useful to understand how the adoption of e-Business can benefit the banking industry.

The purpose of this study therefore is .to describe the status of adoption of e-business in

banks in Ghana as a means of identifying their special needs for enhancing the

adoptions processes.

The specific objectives to be achieved are to:

• identify the benefits of e-business to the banking industry in Ghana;

• explore barriers to the adoption of e-business in banks in Ghana; and

• describe the challenges encountered in the adoption of e-business.

1.3. ResearchquestionsThe research questions to be addressed by this study will be:

o What are the benefits that may be derived by adopting e-business

o What are the barriers to the adoption of e-business in banks in Ghana,

o What challenges do banks face in adopting e-business

Page 5

1.4. SignificanceoftheStudyThe significance of this study can be seen in the fact that the outcome can be applied in

the development of national policy framework as a guide for e-Business adoption,

which is relevant to the national policy of using the banks to facilitate economic and

social growth. In this respect the study will improve our understanding of the following

issues as they apply in the Ghanaian situation.

o The relevance of e-Business in banking for a developing country like Ghana

o Expected benefits derived by adopting e-business

o The barriers that prevent firms from taking advantage of e-business adoption

o The challenges firms encounter when adopting e-business

1.5. ScopeandLimitationofStudy

In this study, it is assumed that e-Business concerns the recognition of business

opportunities that are based on ICT. The exploitation of these opportunities for e-

Business gives a competitive edge. This study focuses on the ability of firms to

discover and exploit opportunities based on ICT. Again, the emphasis is not on the

processof opportunity recognition itself. Rather, the result (the expected e-Business

benefits) is related to a firm’s ability to recognize opportunities and the benefits it

brings. In other words, which firm characteristics explain the recognition of

opportunities for e-Business leading to its adoption?

This study will only examine the adoption of e-Business in banking with respect to

their;

o benefits

o barriers

o challenges

Page 6

Due mainly to time and budgetary constraints this research will cover only four banks.

Two of which are state-owned banks located in Kumasi, the second largest city and the

other two which are private-owned banks located in Accra, the capital of Ghana.

Page 7

Chapter2: LiteratureReview

In chapter One we set out the outline of our study, stating the pursopse, specific

objectives, scope of study and research questions. In this chapter we present from a

literature survey existing views, knowledge and other information relevant to the theme

of this study but more importantly to the objectives and research questions set for this

study. This literature review was also conducted to help put the research methodology

in a better conceptual framework. In this regard the review focused on: the evolution

and definition of e-business; processes of e-business adoption; benefits, barriers and

challenges to e-business adoption.

2.1. TheEvolutionofe‐BusinessE-Business probably began with electronic data interchange in the 1960s (Zwass,

1996). However, (Melão, 2008) suggests that it was only in the 1990s, primarily via the

Internet, that e-Business has emerged as a core feature of many organizations. In his

opinion, the hope was that e-Business would revolutionize the ways in which

organizations interact with customers, employees, suppliers and partners. Some saw e-

Business as part of a recipe to stay competitive in the global economy.

2.2. Defininge‐BusinessThe term “e-Business” has a very broad application and means different things to

different people. Furthermore, its relation with e-commerce is at the source of many

disagreements. (Melão, 2008) Some authors view e-Business as the evolution of e-

commerce from the buying and selling over the Internet, and argue that the former is a

subset of the latter.( Turban et al., 2006). Others defend that, although related, they are

distinct concepts (Laudon and Traver, 2008). Others use both terms interchangeably to

mean the same thing (Schneider, 2002). (Kalakota and Robinson, 2000) proposed a

definition of e-business that clearly stresses the difference between e-commerce and e-

Page 8

business. More precisely they assume that “e-business is not just about e-commerce

transactions or about buying and selling over the Web; it is the overall strategy of

redefining old business models, with the aid of technology, to maximize customer value

and profits”. Kalakota and Robinson’s definition is of great importance because it

describes e-business as an essential business-reengineering factor that can promote

company’s growth. (European Commission, 2007)

Recently authors have begun to delineate more explicitly a difference between e-

commerce and e-Business. E-commerce is emerging as the term used when discussing

the process of transacting business over the Internet. E-Business, on the other hand,

involves the fundamental reengineering of the business model into an Internet based

networked enterprise. While e-business refers to more strategic focus with an emphasis

on the functions that occur using electronic capabilities, e-commerce is a subset of an

overall e- business strategy. E-commerce aims at adding revenue streams using the

World Wide Web or the Internet to build and enhance relationships with clients and

partners. Often, e-commerce involves the application of knowledge management

systems. On the other hand, e-business involves business processes that span through

the entire value chain: electronic purchasing and supply chain management, processing

orders electronically, handling customer service and cooperating with business

partners. E-business can be conducted using the Web, the Internet, intranets, extranets,

or some combination of these (European Commission, 2007).

Figure 2-1: Classification of e-business and e-commerce (adapted from EC 2007)

Page 9

The difference in the two terms according to most authors is the degree to which an

organization transforms its business operations and practices through the use of the

Internet (Hackbarth & Kettinger, 2000; Mehrtens et.al., 2001; Poon, 2000; Poon &

Swatman, 1997)

Some commonly used definitions of e-Business are presented by;

o Earl (2000) “e-Business is about re-engineering or redesigning business

processes to match customers’ expectations in the new economy”

o El Sawy (2001) “e-Business involves rethinking and redesigning business

processes at both the enterprise and supply chain level to take advantage of

Internet connectivity and new ways of creating value”

o Kalakota and Robinson (2001) “e-Business is the complex fusion of

business processes, enterprise applications, and organisational structure

necessary to create a high performance business model”

o Laudon and Traver (2008) “e-Business refers primarily to the digital

enablement of transactions and processes within a firm, involving only the

information systems under the control of the firm”

o Papazoglou and Ribbers (2006) “e-Business can be defined as the conduct of

automated business transactions by means of electronic communications

networks (e.g., via the Internet and/or possibly private networks) end-to-end”

o Schneider (2002) “business activities conducted using electronic data

transmission technologies such as those used in the Internet and the World

Wide Web”

o Turban et al. (2006) “e-Business refers to a broader definition of e-

commerce], not just the buying and selling of goods and services, but also

servicing customers, collaborating with business partners, and conducting

electronic transactions within an organization”

o Windrum and Berranger (2002) “E-business is the integration of the internet and

related ICTs into the business organization”

Page 10

According to (Melão, 2008) the clear commonalities among these definitions, include

the improvement of business processes and the use of ICT in intranets, extranets and

the Internet to conduct business. He defines e-Business as the use of ICT as an enabler

to (re)design, manage, execute, improve and control business processes both within and

between organizations. Thus, front- and back-office integration and multi-channel

integration become crucial in e-Business, which requires a challenging process

improvement approach to support the necessary organizational, technological and

social changes.

E-Business can describe companies operating in the ICT producing sectors as well as

new emerging sectors and industries such as in the area of digital content. However, at

a more fundamental level, the term e-Business also describes the application of

information and communication technologies to business processes in all sectors of the

economy to reduce costs, to improve customer value and to find new markets for

products and services (Department of Enterprise, Trade and Employment, 2004).

Electronic business methods enable companies to link their internal and external data

processing systems more efficiently and flexibly, to work more closely with suppliers

and partners, and to better satisfy the needs and expectations of their customers. E-

Business refers to more strategic focus with an emphasis on the functions that occur

using electronic capabilities. (Yen-Yi, 2006)

In this study we will, as previously stated, use e-business to describe all electronically

based exchanges of goods, services and information.

2.3. E‐BusinessAdoptionThe organizational adoption of an innovation has been defined as the adoption of an

internally generated or purchased device, system, policy, program, process, product, or

service that is new to the adopting organization (Daft, 1982)

E-business commonly involves integration of the internet and related ICTs into the

business organization and has two facets. One is the integration of the supply chain so

that production and delivery become a seamless process. The other is the creation of

new business models based on open systems of communication between customers,

Page 11

suppliers and partners. Where the integration of the supply chain provides increased

efficiency and significant cost advantages through waste minimization, the

development of new products and services are facilitated by new ways of conducting

business based on internet working between organizations and individuals. (Windrum,

and De Berranger, 2002

It is possible to trace a number of stages through which firms are passing as they

progress towards e-business. Each stage is associated with a higher degree of

internetworking and sophistication in communication modes, progression from

traditional commerce to e-commerce business models which require more radical

restructuring of the internal structures. (Windrum and De Berranger, 2002).

In order to acquire a holistic view of the electronic business adoption phenomenon the

academic and research community has focused its research attention on the analysis of

the electronic business adoption process. Within this framework, a great amount of

effort has been placed on the examination of the electronic business adoption process as

well as on the investigation of the significant factors that affect the specific process.

The results of the specific research attempts and developments have led to the

formulation of certain electronic business adoption models (European Commission,

2007).

The Stages theory has been widely used as a way of examining the adoption and

progression of various aspects of electronic business in organizations. The main

assumption of the Stages theory is that organizations progress towards electronic

business through a number of clearly defined and successive stages or phases. Each

adoption stage or phase is characterized by the existence of distinctive applications,

benefits and problems while it reflects a particular level of maturity in terms of the use

and management of Information Systems and Information Technologies (Taylor and

Murphy, 2004).

It is also assumed that the electronic business adoption process is linear, while the

outcomes and the developments of the progressive process are cumulative. (European

Commission, 2007).

Page 12

Within the Staged adoption models, early stages of electronic business adoption are

typically characterized by gaining access to the Internet followed by the use of

relatively simple applications, such as electronic mail (e-mail), in order to dispense and

gather information. Later, the business starts to publish a wider range of information in

order to market its products or services and perhaps provide after-sales support. The

deployment of electronic commerce practices comes next, allowing the users of the

corporate site to order and/or pay for goods and services. In the most mature stages, the

corporate website is fully integrated with the various back office systems such as

enterprise resource planning (ERP), customer relationship management (CRM), and

integrated supply chain management (SCM) applications (Mendo and Fitzgerald, 2005)

Electronic business can be approached in many different ways, depending on the

specific business process that might be carried out through the Internet. Thus, several

Internet usage profiles or approaches are possible. A company must determine which

profile or combination of profiles best suits its particular business context and strategy.

(Mendo and Fitzgerald, 2005)

2.4. BenefitsofE‐BusinessAdoptionAccording to Basu and Muylle (2007), companies can gain two fundamental types of

benefits from e-Business. These are generally described as:

Value Creation or Value Enhancement for one or more of a company’s stakeholder

groups; and Lower Cost of providing goods and services to the market place.

Examples under Value Creation include Improvement in internal and external

communication through effective e-marketing, Increment of sales through an e-

commerce website integrated with a back office systems and Improvement in supplier

relations and productivity through collaborative workspaces (Basu and Muylle, 2007).

And examples under Lower Cost are: reduction in communication and travel costs

using online meeting tools; shared workspaces and; benefit from license free open

source alternatives to proprietary software (http://www.nb2bc.co.uk/what_is_e-

Business).

Page 13

Businesses also see tremendous opportunities for cost saving, revenue generation,

increased market share, marketing and market access, and improving customer service

through direct links that facilitate speedy enquiry and feedback. Similarly, consumers

can inter alia, access the world market through the virtual economy on the Internet,

choose from a wider variety of products, and shop in the comfort of their homes.

Globalization and specifically liberalization of communication networks have all

facilitated this break-through that further presents a massive boost for international

trade. (Mark Bynoe, 2002)

Akoh (2001) answers the question why firms should go the e-Business way and

outlines the tremendous benefits derived by firms who have already integrated e-

Business in their business processes. According to him it is shown that the cost of a

full-service trading transaction is about $150. It will cost $69 doing the same using a

discount broker and $10 using an online broker! That’s about $140 saving on doing

business on the web.

Ako (2001) states that it will cost all parties (the bank, consumer, service provider, etc.)

$1.27 for a banking transaction (could be as little as making a cash withdrawal) at a

bank branch, $0.27 using an ATM machine and $0.01 banking using the Internet! And

in addition Ako iterates that doing business electronically does not only reduce cost but

tremendously affects the speed and efficiency of businesses.

Windrum and Berranger (2002) suggest that the commercial benefits of e-business lie

in five areas.

Firstly, firms are able to expand their geographical reach. Secondly, important cost

benefits lie in improved efficiency in procurement, production and logistics processes.

Thirdly, there is enormous scope for gaining through improved customer

communications and management. Fourthly, the Internet reduces barriers to entry for

new market entrants and provides an opportunity for small firms to reorient their supply

chain relationships to forge new strategic partnerships

Finally, e-business technology facilitates the development of new types of products and

new business models for generating revenues in different ways.

Page 14

2.5. BarrierstoE‐BusinessAdoptionAccording to Windrum and Berranger (2002 ) it is hypothesized that many of the

factors affecting the successful adoption of new technologies such as e-business are

generic in nature and that the successful adoption of internet technologies in part

depends on how these are used in conjunction with the other technologies and

management practices that form a ‘technology cluster .

However the most critical barrier can be ascribed to the very limited information and

communication infrastructure available in most countries in Africa (Ben Akoh 2001).

Reasons vary widely among sectors and countries and are most commonly related to

lack of applicability to the business, preferences for established business models,

(OECD, 2004)

. Common barriers include: unsuitability for the type of business; enabling factors

(availability of ICT skills, qualified personnel, network infrastructure); cost factors

(ICT equipment and networks, software and re-organisation); security and trust factors

(security and reliability of e-commerce systems, uncertainty of payment methods, legal

frameworks and Intellectual Property Right); and challenges in areas of management

skills, technological capabilities, productivity and competitiveness (OECD, 2004).

Lack of reliable trust and redress systems and cross-country legal and regulatory

differences also impede e-business adoption (OECD, 2004).

It is however important to note that barriers to e-Business adoption work differently

according to organizational type and culture. Areas of training and people development

need to be addressed. (Aranda-Mena and Stewart, 2005).

2.6. ChallengesRelatedtotheAdoptionofE‐BusinessMany writers of e-Business and e-commerce extol the enormous potential and

opportunities provided for consumers and businesses globally. However there are some

drawbacks and the benefits to be derived tend to be overstated. (Mark Bynoe, 2002)

Page 15

While many commentators hold the view that e-commerce has many advantages for

developing countries, the African continent has a number of major challenges to

overcome before it can more fully exploit the benefits of e-commerce. A number of

constraints, specific to doing e-Business in Africa, are apparent (Akoh, 2001). These

include but not limited to the following: Low level of economic development and small

per-capita incomes; limited skills base with which to build e-commerce services; the

number of Internet users needed to build a critical mass of online consumers and; lack

of familiarity with even traditional forms of electronic commerce such as telephone

sales and credit card use (ibid).

Perhaps one of the greatest constraints to the adoption of e-Business as a means to

generate efficiencies is a cultural reluctance to interface with buyers and suppliers

electronically. Such challenges remain major obstacles, limiting the potential benefits

of e-Business (Akoh, 2001). Other challenges are the cost of implementation, security

concerns, perceived customer readiness, lack of knowledge of IT and e-Business, the

relatively high costs associated with investments in ICTs, the lack of technical and

managerial skills and reluctance on the part of companies to network with other

enterprises and lack of executive support and concerns regarding the reliability of

technology (Department of Enterprise, Trade and Employment, 2004).

Page 16

Chapter3: ConceptualFramework

3.1. IntroductionThe previous chapter provided a review of literature relevant to our research questions.

This chapter will provide the conceptualization, which constitutes the frame of

reference for this study. The main aim of this chapter is to select relevant theories and

concepts that will be used in this study. The frame of reference provides guidance in the

collection of data and also helps to fulfill the purpose of describing the adoption of e-

business in banks in Ghana

3.1.1. BenefitsofE‐Business

Benefits expected to be gained from e-Business as an option is a big deciding factor for

a firm’s decision to go the e-Business way. Some of these benefits include value

creation and value enhancement, improvement in internal and external communication

(Basu and Muylle, 2007), cost saving, increased market share, speed and efficiency of

doing business and improvement in customer service (Akoh, 2001). These elements of

benefits are the expected answers to our first research question, “What are the benefits

that may be derived by adopting e-business?”

3.1.2. BarrierstoE‐BusinessAdoption

Windrum and De Berranger (2002) states that factors affecting the successful adoption

of new technologies such as e-business are generic in nature. However reasons vary

widely among sectors and countries. Common barriers include security and trust

factors, unsuitability for the type of business, enabling environment and cost factors.

Other barriers (OECD, 2004) have already been discussed in chapter two. From the

literature cited it is abundantly clear that there are certain issues or factors that

constitute barriers to the smooth adoption of e-business.

Page 17

This addresses our second research question “What are the barriers to the adoption of e-

business in banks in Ghana”

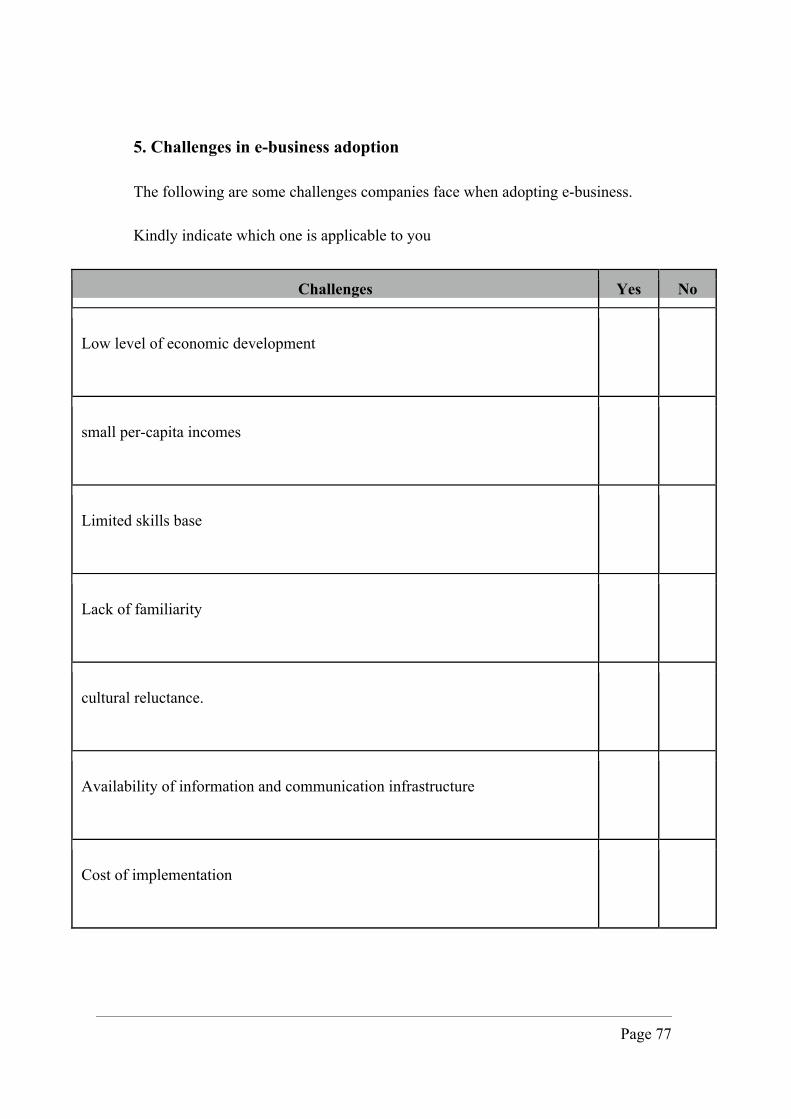

3.1.3. ChallengesofE‐Businessadoption

Though the expected benefits in the adoption of e-business are enormous, firms

adopting this new way of doing business can also expect some challenges as well.

According to (Akoh, 2001) some of these challenges are specific to doing business in

Africa. They include low level of economic development, limited information and

technological infrastructure, culture and high cost of investment. This reference is

formulated in view of our third research question, What challenges do banks face in

adopting e-business ?

3.2. Summarizationoftheories,conceptsandframeofreferenceinlinewithresearchquestions.

3.2.1. ResearchQuestionOne:Whatarethebenefitsthatmaybederivedbyadoptinge‐business

To be able to describe the benefits to the adoption of e-business, the following theory

has been utilised.

o Value creation or value enhancement. (Basu and Muylle, 2007)

o lower cost. (Ben Akoh ( 2001); Windrum &, De Berranger, (2002); Basu and

Muylle (2007), )

o Improvement in internal and external communication. (Windrum & De

Berranger (2002) ; Basu and Muylle (2007) )

o Increment of sales. (Basu and Muylle, 2007)

o Integrated with a back office systems. (Basu and Muylle, 2007)

o Improvement in supplier relations. (Basu and Muylle, 2007)

Page 18

o Improvement in Productivity (Basu and Muylle, 2007)

o Cost saving. (Ben Akoh, 2001), Mark Bynoe, 2002, )

o Revenue generation. (Mark Bynoe, 2002), (Windrum, P. &, De Berranger, P.,

2002 )

o Increased market share. (Mark Bynoe, 2002)

o Marketing and market access. (Mark Bynoe, 2002)

o Improving customer service. (Mark Bynoe, 2002)

o Speed and efficiency. (Ben Akoh ( 2001); Windrum. &, De Berranger ( 2002 )

o Expand geographical reach. (Windrum & De Berranger, 2002 )

o Reduces barriers to entry for new market. (Windrum, P. &, De Berranger, P.

2002 )

o Facilitates development of new products and new business models. (Windrum,

P. &, De Berranger, P. 2002 )

3.2.2. ResearchQuestionTwo:Whatarethebarrierstotheadoptionofe‐businessinbanksinGhana

To be able to describe the barriers to the adoption of e-business, the following theory

has been utilised.

o Lack of applicability to the business. (Windrum and De Berranger,. 2002)

o Preferences for established business models. (Windrum and De Berranger.

2002)

o Unsuitability for the type of business. (OECD,2004)

o Enabling factors. (OECD,2004)

o Cost factors. (OECD,2004)

Page 19

o Security and trust factors (OECD,2004)

o ICT competencies within the firm. (OECD,2004)

o Availability and cost of appropriate interoperable systems. (OECD,2004)

o Network infrastructure and Internet-related support services.. (OECD,2004)

o Cross-country legal and regulatory differences. (OECD,2004)

3.2.3. ResearchQuestionThree:Whatchallengesdobanksfaceinadoptinge‐business

To be able to describe the benefits to the adoption of e-business, the following theory

has been utilised.

o Low level of economic development. (Akoh, 2001)

o small per-capita incomes (Akoh, 2001)

o Limited skills base. (Akoh, 2001)

o Lack of familiarity (Akoh, 2001)

o Cultural reluctance. (Akoh, 2001)

o Availability of information and communication infrastructure (Akoh, 2001)

o Cost of implementation. (DETE, 2004)

o Security concerns. (DETE, 2004)

o Perceived customer readiness. (DETE, 2004)

o Knowledge of IT and e-Business. (Department of Enterprise, Trade and

Employment, 2004)

o High costs associated with investments in ICTs. (Department of Enterprise,

Trade and Employment, 2004)

Page 20

o Lack of technical and managerial skills. (Department of Enterprise, Trade and

Employment, 2004)

o Reluctance on the part of companies to network with other enterprise.

(Department of Enterprise, Trade and Employment, 2004)

o lack of executive support (Department of Enterprise, Trade and Employment,

2004)

o Organizational type and culture. (Aranda-Mena and Stewart, 2005)

The table below summarizes our research questions and theories used to answer them.

Table 3-1: A table showing research questions and theories used to answer.

Research question Theories used to answer

Content

What are the benefits that may be derived by adopting e-business

Basu and Muylle (2007)

Ben Akoh ( 2001)

Windrum &De Berranger (2002)

Mark Bynoe (2002)

Value creation or value enhancement, lower cost, Improvement in internal and external, communication, Increment of sales, Integrated with a back office systems, Improvement in supplier relations, Improvement in Productivity, revenue generation, Increased market share, marketing and market access, improving customer service, speed and efficiency, expand geographical reach, reduces barriers to entry for new market, facilitates development of new products and new business models

What are the barriers to the adoption of e-business in banks in Ghana

Windrum De Berranger (2002)

OECD,(2004)

Lack of applicability to the business, Preferences for established business models, Unsuitability for the type of business, Enabling factors, Cost factors, Security and Trust factors, ICT competencies within the firm,

Availability and cost of appropriate interoperable systems, Network infrastructure and internet-related support services,

Cross-country legal and regulatory differences.

What challenges do banks face in adopting e-business

Akoh, (2001) DETE (2004) Low level of economic development, small per-

capita incomes, Limited skills base, Lack of familiarity, Cultural reluctance, availability of information and communication infrastructure,

Cost of implementation, security concerns, Perceived customer readiness

Page 21

In this study the benefits of e-business are conceptualized as issues or factors perceived

by respondents as beneficial for e-business adoption. Similarly, barriers are those

factors perceived to be impediments to the adoption of e-business. Finally challenges

are conceptualized to be the perceived factors that make it difficult to adopt e-business.

Figure 3-1: Emerged frame of reference

Page 22

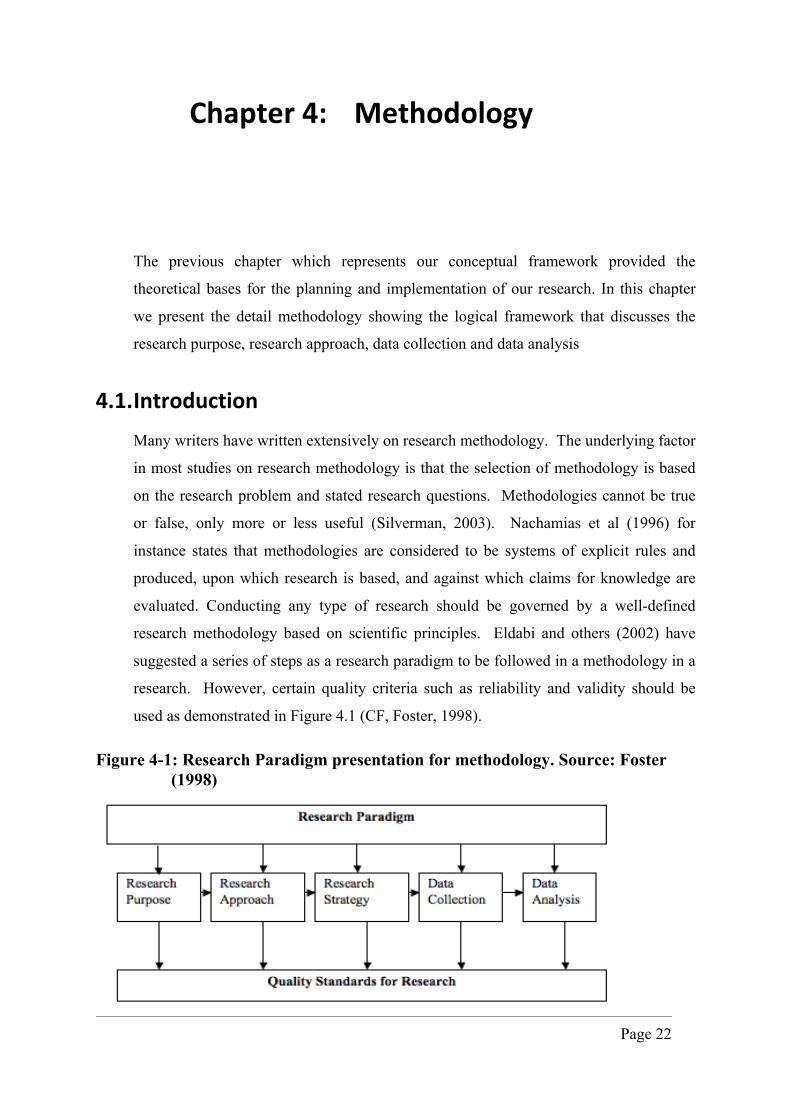

Chapter4: Methodology

The previous chapter which represents our conceptual framework provided the

theoretical bases for the planning and implementation of our research. In this chapter

we present the detail methodology showing the logical framework that discusses the

research purpose, research approach, data collection and data analysis

4.1. IntroductionMany writers have written extensively on research methodology. The underlying factor

in most studies on research methodology is that the selection of methodology is based

on the research problem and stated research questions. Methodologies cannot be true

or false, only more or less useful (Silverman, 2003). Nachamias et al (1996) for

instance states that methodologies are considered to be systems of explicit rules and

produced, upon which research is based, and against which claims for knowledge are

evaluated. Conducting any type of research should be governed by a well-defined

research methodology based on scientific principles. Eldabi and others (2002) have

suggested a series of steps as a research paradigm to be followed in a methodology in a

research. However, certain quality criteria such as reliability and validity should be

used as demonstrated in Figure 4.1 (CF, Foster, 1998).

Figure 4-1: Research Paradigm presentation for methodology. Source: Foster (1998)

Page 23

For the purpose of this research the schematic approach shown in Figure 4.1 will be

adopted.

4.2. ResearchPurposeThe purpose of this thesis is to conduct an exploratory and descriptive research in order

to gather as much information as possible concerning the adoption of e-Business as an

option in a competitive business environment in Ghana. Specifically this will be in

respect of the banking business. According to Yin (1994) exploratory research is

designed to allow a researcher to just look around with respect to some phenomenon,

with the aim to develop suggestive ideas. Exploratory research is often used when a

problem is not well known, or the available knowledge is not absolute. The technique

that is best suited for information gathering when performing an exploratory research is

interview (Yin, 1994). We are employing exploratory study because it gives valuable

insight of the problem and result drawn from this study will be in firm grasp of

essential characters. It has also been demonstrated that exploratory research provides

suggestive ideas through reviewing information from problem area. (Chisnall, 1997)

4.3. ResearchApproachThe research approach in this study is chosen based on the purpose and the research

questions set out to be addressed. In an exploratory research such as this a qualitative

approach will be adopted.

Qualitative data are characterized by the richness and fullness based on the opportunity

to explore a subject. The nature of qualitative study is primarily to understand, not to

explain. Qualitative research implies an emphasis on processes and meanings that are

not measured in terms of quantity amount, intensity or frequency.

The main features of quantitative research approaches have been described by Miles

and Huberman (1994) as shown below.

o The aim of qualitative analysis is a complete, detailed description

o Recommended during earlier phases of research projects

Page 24

o Researcher may only know roughly in advance what he/ she is looking for

o The design emerges as the study unfolds

o Researcher is the data gathering instrument

o Data is in the form of words, pictures or objects.

o Qualitative data is more “rich”, time consuming, and less able to be

generalized

o Researcher tends to become subjectively immersed in the subject matter

We are using the qualitative approach for our study because we want to have a deeper

understanding of e-Business adoption and its ability to give competitive edge. By

using the qualitative approach we will get the opportunity to explore our subject matter.

We are seeking to understand more about e-Business adoption and its competitive

nature and not to explain it.

4.3.1. StrategiesforResearch

Yin (2003) has described five primary strategies for research in social sciences to

collect empirical data. According to him, depending on the character of the research

questions, to which extent the researcher has control over behavioral events and to what

degree the focus is on contemporary event, the research can choose from the following:

o Experiments;

o Survey;

o Analysis of archival records;

o History;

o Case Study.

In our study we have used a case study approach since our research deals with “how”

barriers, benefits and challenges related to e-business adoption in Ghanaian banks can

be described.”. This is because the form of our research question is “how” e-Business

Page 25

adoption has or can help firms to stay ahead of competition in their respective

environments. In this thesis we are using the four banks in Ghana as a case study.

4.3.2. StudyArea

This section describes the banking environment in Ghana with respect to the policy and

legal framework under which the banking industry in Ghana operates.

The banking industry in Ghana is controlled by the Bank of Ghana acting as the central

bank. The total number of registered commercial banks under the bank of Ghana

numbers up to 23 as at January 2008. These comprises 5 state owned banks and 18

other private or multinational banks. In addition to the 23 banks, the sector also

comprises a range of non-bank financial institutions, including several community

banks established to mobilize rural savings.

The past few years have seen a phenomenal growth in the Ghanaian banking sector.

Ghana’s financial sector according to the Bank of Ghana is well-capitalized, very

liquid, profitable and recording strong asset growth. The banking sector has seen major

capital injection partly because of the political stability, attainment of micro and macro-

economic stability and the government’s desire to make Ghana the “financial hub” of

the Sub-region. For instance net interest income for the industry increased by 19% from

¢2.7tn in 2004 to ¢3.2tn in 2005 (George M and Bob-Milliar, 2007). Over the five-year

review period, net profit had increased by about 56%. Industry net profit after tax

margin dipped from 29.64% (2001) to 23.99% (2005). Industry return on equity (ROE)

has decreased steadily from a high of 43.9% in 2001 to 26.9% in 2005, while return on

assets dropped from 5.7% to 3.5 percent giving an indication of the increasing

competitive nature of the banking industry (Pricewater House Coopers, 2006).

The Ghanaian banking sector is now very vibrant and modern. According to

Dr.Mahamadu Bawumia, (the second Deputy Governor of BoG), bank branches in

Ghana increased by 11.3 per cent from 309 to 344 between 2002 and 2004 with 81 new

branches springing up from 2004 and 2006 indicating an increase of 23.5 per cent.

Most banks now employ cutting edge technologies to roll out their products to their

Ghanaian customers. Banking halls are housed in ultra modern buildings, staffed with

well trained ladies and gentlemen. Ghanaians living in the big commercial towns are

Page 26

now spoilt for choice. Twenty three banks are chasing the about 10 per cent of the

bankable segment of the population. Nigerian banks have added to the competition and

are well represented in the new banking sector in Ghana. (George M and Bob-Milliar,

2007).

Because of the very fierce but healthy competition in the banking sector, daily

newspapers are adorned with catchy adverts of re-branded or new products all in an

attempt to lure new customers to their products and services. Many banks in the

commercial centers now work half day on Saturdays, thus making it possible for busy

workers to access banking services at the weekend. (Price-water House Coopers, 2006).

Recent and emerging developments suggest that cost competitiveness, customer

sophistication, technology and regulatory changes will be the main drivers of change in

the industry and the banks that are able to position themselves to embrace these

challenges will emerge winners. (ibid)

The banking sector in Ghana has remained one of the sectors with the brightest

opportunities despite increasing competition (Price-water House Coopers, 2006).

4.4. TypeofDataandDataCollection

4.4.1. Typeofdata

Both primary and secondary data will be used in our study. Primary data that will

provide empirical data will be collected through, interviews, and administration of

structured questionnaires. These will give specific responses to our research questions.

Primary data is recognized as data that is gathered for a specific research in response to

a particular problem through interviews, questionnaires or observations. Secondary

data information is that obtained through various kinds of documents, e.g. Research

reports, annual reports, books and articles.

Most researchers agree that qualitative research should try to use as many different

sources as possible. This is on the general observation that no single source has

complete advantage of all other sources (Yin, 1994; Denscombe, 1998). For instance

according to Denscombe (2000) interviews are suitable when there is the need to gather

Page 27

detailed data and information from very few respondents, but the researcher would

have to decide whether or not the study needs the type of information and if it will be

possible to rely on the information these few respondents would provide the researcher

with.

4.5. Datacollection

4.5.1. SampleSelection

The population of banks sampled from Banks in Kumasi and Accra were categorized

into two main blocks i) two State-owned banks, and ii) Private-owned banks From each

category the sample units will be the managers responsible for e-buisness. A manager

from each bank will be selected from each category.

We have to take a sample because it is often impossible or too much expensive to

collect data from all the potential units. Hence samples are chosen to represent the

relevant attributes of the whole population. In this respect we note the caution by

Graziano and Raulin (1997) that because the samples are not perfectly representative of

the population from which they are drawn, we are unlikely to be able to generalize our

conclusions to the entire population.

4.5.2. EmpiricalData

The empirical data was mainly qualitative description given by the managers of the

sampled banks. This is important to be able to evaluate and describe the adoption of e-

Business application on the target banks. This data will be collected mainly through

the administration of structured questionnaires (see Appendix 1).

4.5.3. Secondarydata

This data was required to describe the environment in which the selected industry

operates. The data was obtained mainly from records and reports of the industry, from

the website, books articles and journals.

Page 28

4.5.4. ResearchProtocolsandCasestudydatabase

In the research protocol, the objectives of the study were restated in question forms to

emphasize the importance of all the components of the research and how the outputs

are expected to contribute to improving knowledge on e-Business adoption in Ghana.

In this respect the research protocol will be done with the following issues in mind

o barriers to the adoption of e-business in banks in Ghana,

o benefits of e-business, and

o challenges encountered in the adoption of e-business

4.6. DataAnalysisData Analysis generally consists of examining, categorizing, tabulation or otherwise

recombining the evidence to address the initial proposition of a study. According to

Yin (1994), the ultimate goal of analyzing data is to treat the evidence fairly, to produce

compelling analytical conclusions and to rule out alternative interpretations. In another

sense data analysis is seen to consist of three concurrent flows of activities (Miles and

Huberman, 1994). These three are data reduction, data display, and conclusion drawing

and verification.

Data reduction as an integral part of data analysis will be carried out to sharpen, sort,

focus, discard, and organized the data in a way that allows for final conclusions to be

drawn and verified. In this sense data reduction refers to the process of selecting,

focusing, simplifying, abstracting, and transforming the raw data (Miles & Huberman,

1994).

Data display refers to an organized assembly of information that permits conclusions,

drawing and action taking. Deductions and conclusion will be drawn from the data to

decide what things mean from the beginning of data collection. We do this by noting

regularities, patterns, explanations, possible configurations, causal flows, and

propositions. However, we hold such conclusions lightly, while maintaining both

openness and degree of skepticism. This is important because according to Chisnall

(1997) the stability and consistency of results derived from research is contingent on

Page 29

the probability that the same results could be obtained if the measures used in the

research were replicated. Essentially, reliability is connected with consistency, accuracy

and predictability of specific research findings. In addition, the role of reliability is to

minimize the errors and biases in this study. Two things that were adopted to increase

reliability in this study are the use of case study protocol and the development of a case

study database.

4.6.1. MethodofAnalysis

In this study the findings have been presented in narrative descriptions and where

possible, tables, charts and figures are also used to indicate trends and pattern that

facilitate discussions

Alvesson and Sköldbery (1994), state the three ways for drawing conclusions. These

are Inductive, Deductive, and Adductive

Inductive method is used to draw conclusions based on empirical findings. This

method is normally used when established theories in the field of study are limited and

the purpose is to form a new theory.

Deductive method is used when drawing conclusion perceived as valid when it is

logically connected. Usually in deductive studies, theories and literature that have been

established already is used as foundation for the new research.

Adductive method is similar to Inductive method. Here the researcher starts with the

empirical facts, just as in the inductive method. However, theoretical pre-conceptions

are not rejected. In adductive method a separate case is interpreted according to the

theoretical pattern as if it was true, would explain the case. The result is then confirmed

based on the new observations. The new observation from the study is then compared

with the theoretical frame of reference.

Based on the explanations above, our method of analysis is based on the deductive

Method. Our research is based on existing literature on e-business.

Page 30

This is in order because it presented to us a foundation upon which to build on by

presenting a guide for our questionnaire that will enable us to collect our data upon

which conclusions could be drawn based on the empirical findings.

4.7. QualityData

4.7.1. ValidityandReliability

Research quality is generally described by the validity and reliability of the research

methodology and data. In this thesis where the research is more of a qualitative

assessment we apply the quality criteria for the purpose of “generating understanding”

of the research issues identified in relation to e-business adoption in Ghanaian banks.

Patton (2001) states that the validity and reliability are two factors that any qualitative

researcher should be concerned about while designing a study, analyzing results and

judging the quality of the study

4.7.1.1. Validity

Validity refers to the extent to which a measure reflects the concept it intends to

measure. If the measures used actually measure what they claim to, and if there are no

logical errors when drawing conclusions from the data, the study is said to be valid

(Trochim, 2005,)

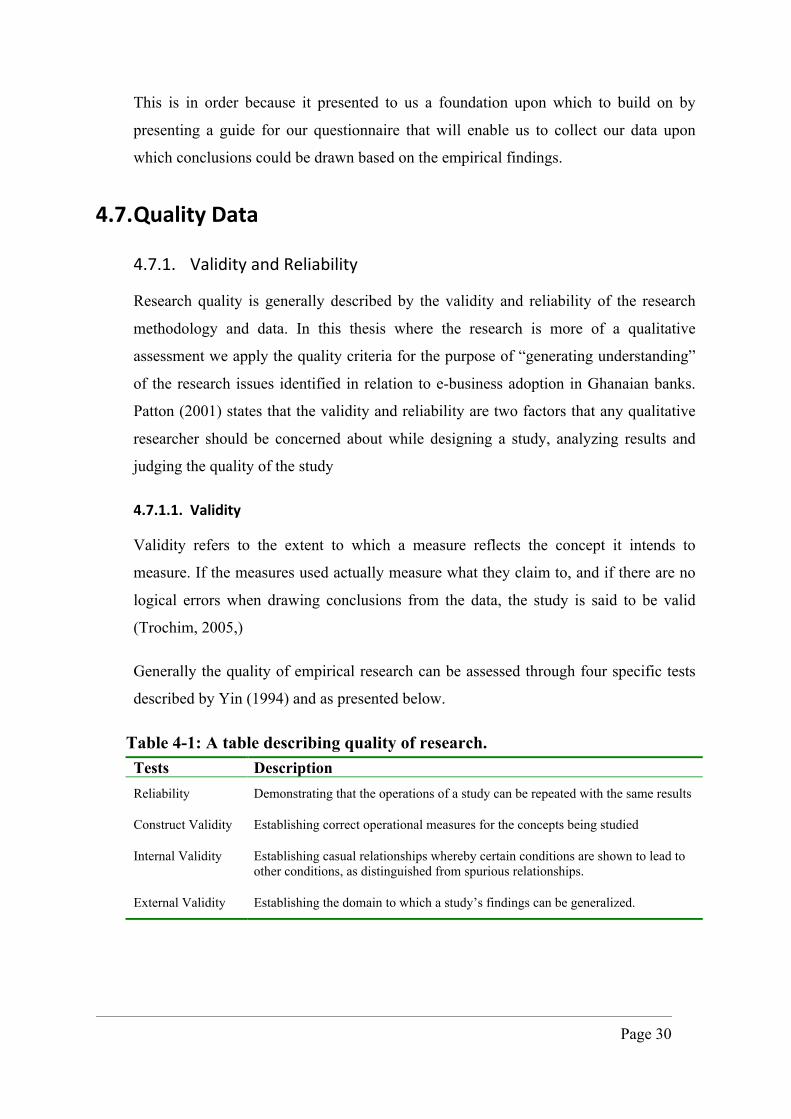

Generally the quality of empirical research can be assessed through four specific tests

described by Yin (1994) and as presented below.

Table 4-1: A table describing quality of research. Tests Description Reliability Demonstrating that the operations of a study can be repeated with the same results

Construct Validity Establishing correct operational measures for the concepts being studied

Internal Validity Establishing casual relationships whereby certain conditions are shown to lead to other conditions, as distinguished from spurious relationships.

External Validity Establishing the domain to which a study’s findings can be generalized.

Page 31

4.7.2. Reliability

Reliability means dependability or consistency (Neumann, 2006: 196). It indicates the

likelihood that a given measurement technique will repeatedly yield the same

description of a given phenomenon. The role of reliability is to minimize the errors and

biases in a study. (Yin, 2003,)

To ensure reliability in this study we mapped out the detailed procedure for sample

selection, selection of research instruments (mainly questionnaire), designing the

questionnaire, and administration of questionnaire. To have a representative sample of

the banks we made an initial visit to their headquarters and obtained information on

their regional coverage and location of branches within the study area. Through

informal contacts we managed to sensitize the selected branches and gave some

indication of the issues that our study seeks to investigate. This helped to design

realistic interview questions. A draft questionnaire was administered to few banks to

test the relevance of the questions and revised before the final administration. To ensure

candid response each respondent was assured of the anonymity of his or her answers.

Similarly to have a better understanding of the issue being addressed the questionnaire

were distributed a couple of weeks before the interviews. Further explanations were

provided in the course of the interview.

However, despite these attempts of maintaining a high reliability in this study, personal

biases on the part of the respondents in answering the questions and on the part of the

researches in recording the answers cannot be ruled out. Hence we cannot be exact on

the influence of attitudes and vales on the respondents and ourselves in the study.

With respect to constructed validity of this study, we have used a combination of

consultations, phone interviews and questionnaire to collect data. The collected data

and recorded notes from the interviews have been captured on a computer in a specified

format.

Page 32

Chapter5: CaseStudyAnalysis

5.1. IntroductionThis chapter deals with the output of the analysis of the questionnaire. Here empirical

data collected on four Ghanaian banks are presented. The data was collected through

personal interview and via emails. Each case is examined individually and a cross case

analysis is also done. The outputs are presented in the form of tables and charts. The

outputs are presented to indicate the responses to the three main questions:

o What are the benefits that may be derived by adopting e-business?

o What are the barriers to the adoption of e-business in banks in Ghana?

o What challenges do banks face in adopting e-business?

Before addressing the research questions, some characteristics of the banks are

presented.

5.2. GeneralDescriptionofBankinginGhanaThe banking industry in Ghana is controlled by the Bank of Ghana acting as the central

bank. The total number of registered commercial banks under the bank of Ghana

numbers up to 23 as at January 2008. These comprises five state owned banks and 18

other private or multinational banks.

Over the past ten years, Ghana has been undergoing the process of financial sector

restructuring and transformation as an integral part of a comprehensive programme to

ensure that the country achieves emerging market status. The recent developments in

the country's banking environment with the liberalization of entry encouraged foreign

banks and investors, noticeably those from Nigeria to consider the country as a good

destination for their investment.

Page 33

Liberalizing entry and encouraging foreign banks and investors into the financial

services industry has increased competition in the banking industry as well as the

introduction of strong business practices, technology, products and risk management

systems. Many of the traditional local banks in Ghana responded to the competition

brought by the foreign banks by rethinking their strategy, and reshaping their focus and

direction in order to be attractive to customers. (Daily Graphic, 2008)

In this study, four banks have been chosen. Two traditional banks (Ghana Commercial

bank and Agricultural Development Bank) and two foreign banks (Ecobank Ghana Ltd

and Stanbic Bank Ghana)

The table below describes these four chosen banks.

Table 5-1: Description of the four selected Banks in Ghana

Ban

k

Typ

e

Age

Ado

pted

Rea

son

ebus

ines

s Pr

oduc

ts

Tar

get

Cus

tom

ers

Reg

iona

l C

over

age

Bra

nche

s

Ecobank Ghana Ltd

Private Owned