Embed Size (px)

Citation preview

11

Investo

r P

resen

tati

on

Jan

uary

2008, H

on

g K

on

g

22

Ag

en

da

11 332

008

CO

SL

Bu

sin

es

s O

utl

oo

k2

008

CO

SL

Bu

sin

es

s O

utl

oo

k

222

00

8

20

08

Ma

cro

Ma

cro

En

vir

on

me

nt

Ou

tlo

ok

En

vir

on

me

nt

Ou

tlo

ok

Re

vie

w o

f 200

7 O

pe

rati

ng

Da

taR

evie

w o

f 200

7 O

pe

rati

ng

Da

ta

33

11R

evie

w o

f 200

7 O

pe

rati

ng

Da

taR

evie

w o

f 200

7 O

pe

rati

ng

Da

ta

44

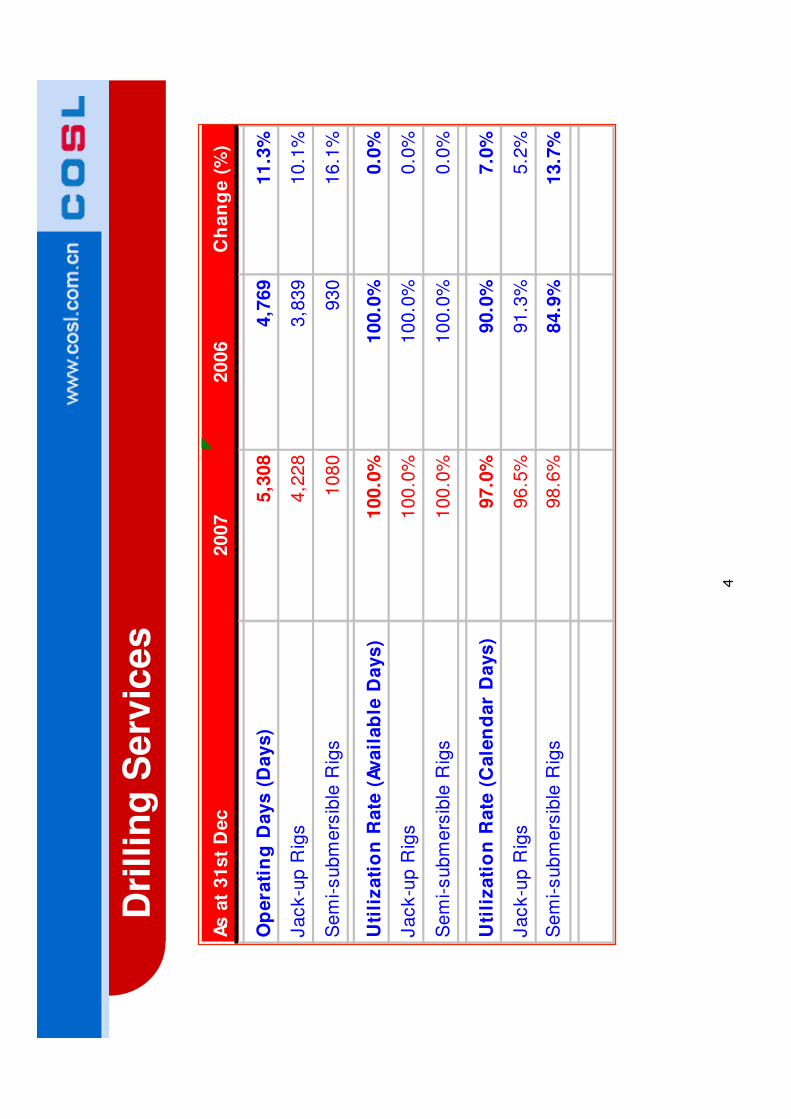

Dri

llin

g S

erv

ice

s

As

at

31s

t D

ec

20

07

20

06

Ch

an

ge (

%)

Op

era

tin

g D

ay

s (

Da

ys)

5,3

08

4,7

69

11

.3%

Ja

ck-u

p R

igs

4,2

28

3,8

39

10

.1%

Se

mi-

sub

me

rsib

le R

igs

108

09

30

16

.1%

Uti

liz

ati

on

Ra

te (

Av

ail

ab

le D

ays

)1

00

.0%

10

0.0

%0

.0%

Ja

ck-u

p R

igs

100

.0%

10

0.0

%0

.0%

Se

mi-

sub

me

rsib

le R

igs

100

.0%

10

0.0

%0

.0%

Uti

liz

ati

on

Ra

te (

Ca

len

da

r D

ays

)97

.0%

90.0

%7

.0%

Ja

ck-u

p R

igs

96

.5%

91.3

%5

.2%

Se

mi-

sub

me

rsib

le R

igs

98

.6%

84.9

%1

3.7

%

55

We

ll S

erv

ice

s

As a

t 31

st

Dec

20

07

200

6C

han

ge(%

)

Lo

gg

ing

(n

o.

of

job

s)

86

58

37

3.3

%

Dri

llin

g f

luid

s (

no

. o

f w

ell

s)

29

02

91

-0.3

%

Dir

ecti

on

al

Dri

llin

g (

no

. o

f jo

bs)

58

12

42

140

.1%

Cem

en

tin

g (

no

. o

f w

ell

s)

47

43

32

42

.8%

Well

Co

mp

leti

on

(n

o.

of

job

s)

152

71

244

22

.7%

Well

Wo

rko

ve

r (t

eam. ...

days

)15

,944

13,3

69

19

%

66

Ma

rin

e S

up

po

rt a

nd

Tra

ns

po

rta

tio

n S

erv

ice

s

As

at

31s

t D

ec

2007

2006

Ch

an

ge

(%

)

Op

era

tin

g D

ays

(D

ays

)24,2

29

23,6

68

2.4

%

Sta

ndby v

essels

13,2

02

13,3

21

-0.9

%

AH

TS

vessels

7,1

72

6,5

54

9.4

%

PS

V v

essels

2,1

45

2,1

13

1.5

%

Util

ity v

essels

1,7

10

1,6

80

1.8

%

Ve

ss

el U

tilizati

on

Rate

(A

vailab

le D

ays

)99.6

%99.1

%0.5

%

Sta

ndby v

essels

99.8

%99.7

%0.1

%

AH

TS

vessels

100.0

%98.8

%1.2

%

PS

V v

essels

99.7

%99.8

%-0

.1%

Util

ity v

essels

96.6

%94.9

%1.7

%

Ve

ss

el U

tilizati

on

Rate

(C

ale

nd

ar

Days

)94.9

%95.1

%-0

.2%

Sta

ndby v

essels

95.2

%96.0

%-0

.8%

AH

TS

vessels

93.9

%93.7

%0.2

%

PS

V v

essels

97.9

%96.5

%1.4

%

Util

ity v

essels

93.7

%92.1

%1.6

%

77

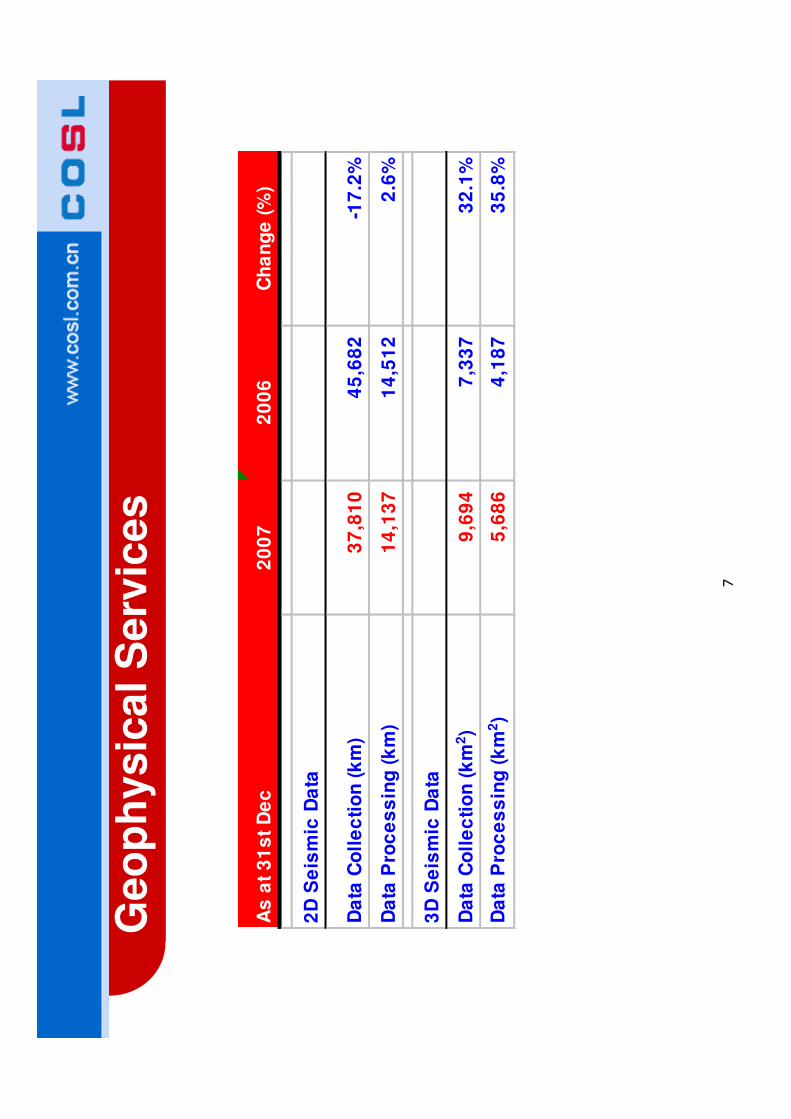

Geo

ph

ysic

al S

erv

ices

As

at

31

st

De

c2

00

72

00

6C

ha

ng

e (

%)

2D

Se

ism

ic D

ata

Da

ta C

oll

ec

tio

n (

km

)3

7,8

10

45

,68

2-1

7.2

%

Da

ta P

roc

es

sin

g (

km

)1

4,1

37

14

,51

22

.6%

3D

Se

ism

ic D

ata

Da

ta C

oll

ec

tio

n (

km

2)

9,6

94

7,3

37

32

.1%

Da

ta P

roc

es

sin

g (

km

2)

5,6

86

4,1

87

35

.8%

88

222

00

8 M

ac

ro E

nvir

on

me

nt

Ou

tlo

ok

20

08 M

ac

ro E

nvir

on

me

nt

Ou

tlo

ok

99

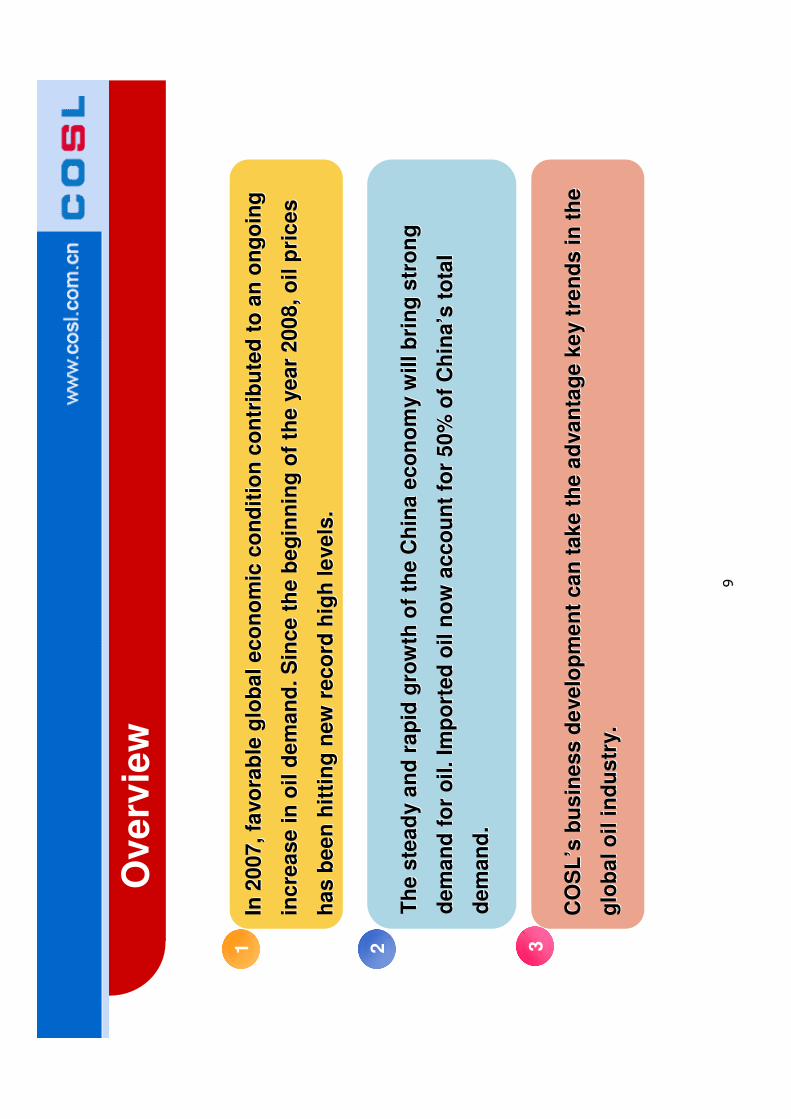

Ov

erv

iew

In 2

00

7,

favo

rab

le g

lob

al

ec

on

om

ic c

on

dit

ion

co

ntr

ibu

ted

to

an

oIn

20

07

, fa

vo

rab

le g

lob

al

ec

on

om

ic c

on

dit

ion

co

ntr

ibu

ted

to

an

on

go

ing

n

go

ing

inc

rea

se

in

oil

de

ma

nd

. S

inc

e t

he

be

gin

nin

g o

f th

e y

ea

r 2

00

8,

oi

inc

rea

se

in

oil

de

ma

nd

. S

inc

e t

he

be

gin

nin

g o

f th

e y

ea

r 2

00

8,

oi l

pri

ce

s

l p

ric

es

ha

s b

ee

n h

itti

ng

new

re

co

rd h

igh

le

ve

ls.

ha

s b

ee

n h

itti

ng

new

re

co

rd h

igh

le

ve

ls.

Th

e s

tea

dy a

nd

ra

pid

gro

wth

of

the

Ch

ina

ec

on

om

y w

ill

bri

ng

str

oT

he

ste

ad

y a

nd

ra

pid

gro

wth

of

the

Ch

ina

ec

on

om

y w

ill

bri

ng

str

on

g

ng

de

ma

nd

fo

r o

il.

Imp

ort

ed

oil

no

w a

cc

ou

nt

for

50

% o

f C

hin

ad

em

an

d f

or

oil

. Im

po

rte

d o

il n

ow

ac

co

un

t fo

r 5

0%

of

Ch

ina

’’ s t

ota

l s

to

tal

de

ma

nd

.d

em

an

d.

CO

SL

CO

SL

’’ ssb

us

ine

ss

de

ve

lop

me

nt

ca

n t

ak

e t

he

ad

va

nta

ge

ke

y t

ren

ds

in

th

e

bu

sin

es

s d

eve

lop

me

nt

ca

n t

ak

e t

he

ad

va

nta

ge

ke

y t

ren

ds

in

th

e

glo

ba

l o

il i

nd

us

try.

glo

ba

l o

il i

nd

us

try.

2 31

1010

Ste

ad

y I

nc

rea

se

in

Cru

de

Oil

De

ma

nd

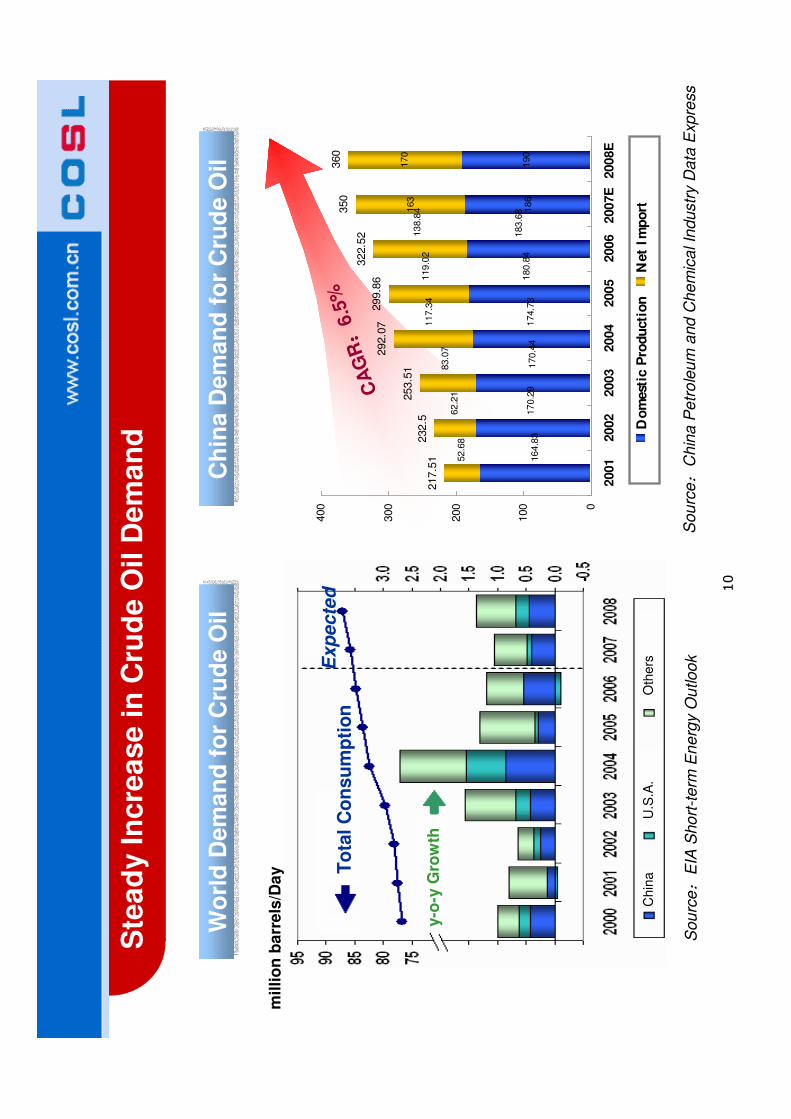

Chin

aU

.S.A

.O

thersExp

ecte

d

y-o

-yG

row

th

To

tal C

on

su

mp

tio

n

mil

lio

n b

arr

els

/Da

y

Sou

rce:

EIA

Sho

rt-t

erm

En

erg

y O

utloo

k

186

190

163

170

217.5

1232.5

253.5

1

292.0

7299.8

6

322.5

2

350

360

183.6

8180.8

4164.8

3170.2

9170.4

4174.7

3

138.8

4119.0

2117.3

4

83.0

762.2

152.6

8

0

100

200

300

400

2001

2002

2003

2004

2005

2006

2007E

2008E

Do

mest

ic P

rodu

cti

on

Net

Imp

ort

CA

GR::::

6.5

%

Sou

rce:

Ch

ina

Pe

tro

leu

m a

nd

Ch

em

ica

l In

dustr

y D

ata

Exp

ress

Wo

rld

Dem

an

d f

or

Cru

de O

ilW

orl

d D

em

an

d f

or

Cru

de O

ilC

hin

a D

em

an

d f

or

Cru

de O

ilC

hin

a D

em

an

d f

or

Cru

de O

il

1111

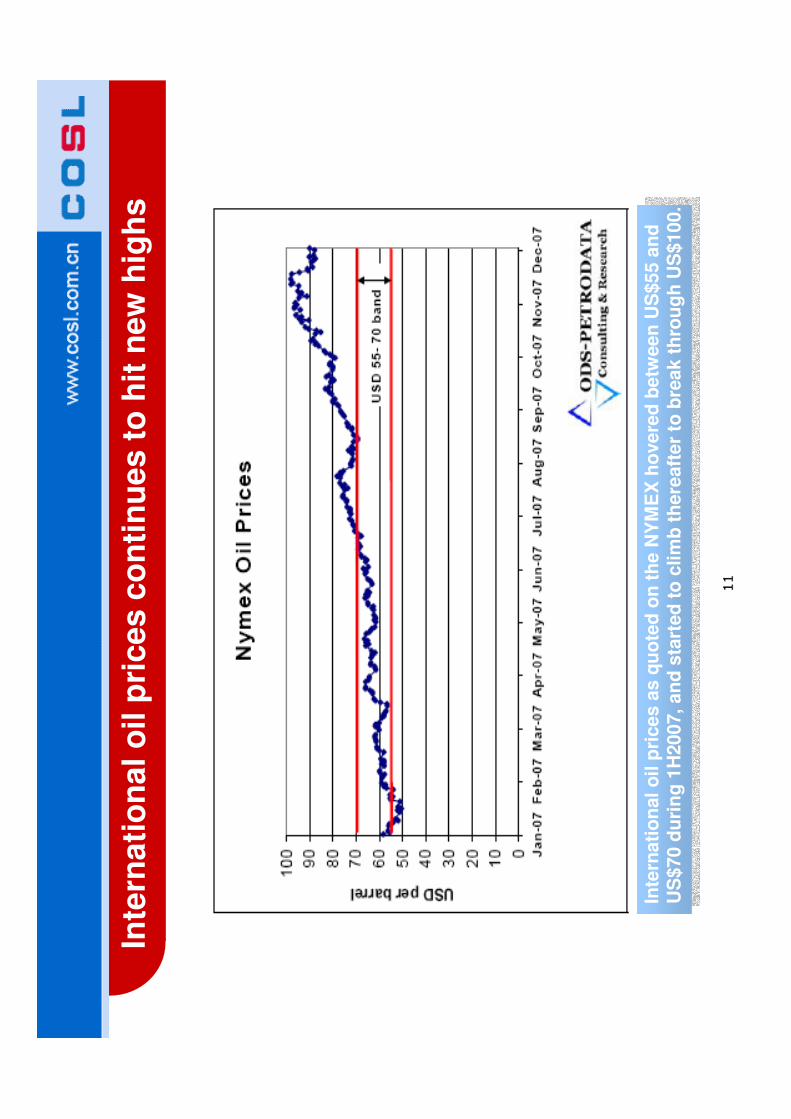

Inte

rnati

on

al o

il p

rices a

s q

uo

ted

on

th

e N

YM

EX

ho

vere

d b

etw

een

US

$55 a

nd

U

S$70 d

uri

ng

1H

2007, an

d s

tart

ed

to

clim

b t

here

aft

er

to b

reak t

hro

ug

h U

S$100.

Inte

rnati

on

al o

il p

rices a

s q

uo

ted

on

th

e N

YM

EX

ho

vere

d b

etw

een

US

$55 a

nd

U

S$70 d

uri

ng

1H

2007, an

d s

tart

ed

to

clim

b t

here

aft

er

to b

reak t

hro

ug

h U

S$100.

Inte

rnati

on

al

oil p

rices c

on

tin

ues t

o h

it n

ew

hig

hs

1212

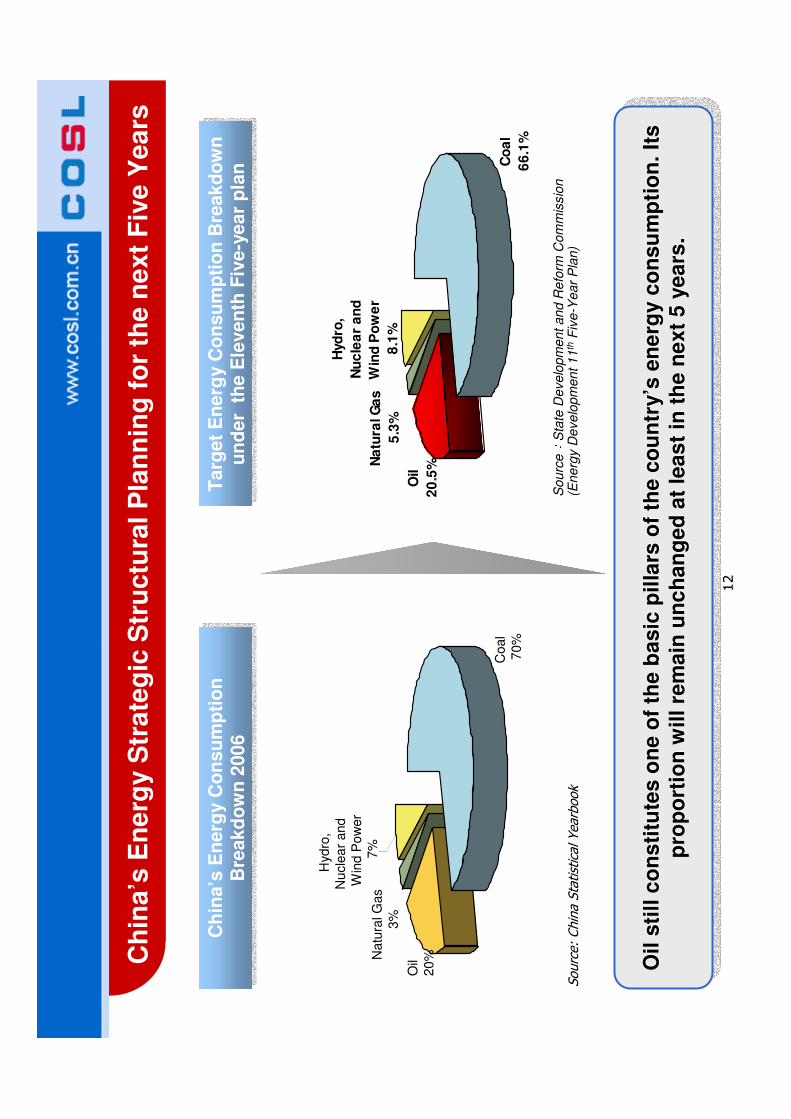

Co

al

66

.1%

Hyd

ro,

Nu

cle

ar

an

d

Win

d P

ow

er

8.1

%

Na

tura

l G

as

5.3

%

Oil

20

.5%

Ch

ina

’s E

ne

rgy S

tra

teg

ic S

tru

ctu

ral P

lan

nin

g f

or

the

ne

xt

Fiv

e Y

ea

rs

Targ

et

En

erg

y C

on

su

mp

tio

n B

reakd

ow

n

un

der

th

e E

leven

th F

ive-y

ear

pla

n

Targ

et

En

erg

y C

on

su

mp

tio

n B

reakd

ow

n

un

der

th

e E

leven

th F

ive-y

ear

pla

nC

hin

a’s

En

erg

y C

on

su

mp

tio

n

Bre

akd

ow

n 2

006

Ch

ina’s

En

erg

y C

on

su

mp

tio

n

Bre

akd

ow

n 2

006

Source: China Statistical Yearbook

Oil

sti

ll c

on

sti

tute

s o

ne

of

the

ba

sic

pil

lars

of

the

co

un

try’s

en

erg

y c

on

su

mp

tio

n.

Its

p

rop

ort

ion

wil

l re

ma

in u

nc

ha

ng

ed

at

lea

st

in t

he

ne

xt

5 y

ea

rs.

Oil

sti

ll c

on

sti

tute

s o

ne

of

the

ba

sic

pil

lars

of

the

co

un

try

Oil

sti

ll c

on

sti

tute

s o

ne

of

the

ba

sic

pil

lars

of

the

co

un

try

’’ s e

ne

rgy c

on

su

mp

tio

n.

Its

s

en

erg

y c

on

su

mp

tio

n.

Its

pro

po

rtio

n w

ill

rem

ain

un

ch

an

ge

d a

t le

as

t in

th

e n

ex

t 5

ye

ars

.p

rop

ort

ion

wil

l re

ma

in u

nc

ha

ng

ed

at

lea

st

in t

he

ne

xt

5 y

ea

rs.

Sourc

e:State Devel

opm

ent and R

efo

rm C

om

mis

sio

n

(Energ

y D

evelo

pm

ent 11

thF

ive-Y

ear

Pla

n)

Coal

70%

Hyd

ro,

Nucle

ar

and

Win

d P

ow

er

7%

Natu

ral G

as

3%

Oil

20%

1313

0

20,0

00

40,0

00

60,0

00

80,0

00

100,0

00

120,0

00

140,0

00

2002

2003

2004

2005

2006

2007E

2008E

2009E

2010E

CAPEX

OPEX OPEXOPEXOPEX

Co

nti

nu

ing

In

cre

as

e i

n W

orl

d

Inve

stm

en

ts i

n M

ari

ne

Oil

an

d G

as

Co

nti

nu

ing

In

cre

as

e i

n W

orl

d

Inve

stm

en

ts i

n M

ari

ne

Oil

an

d G

as

Bri

gh

t F

utu

re f

or

Off

sh

ore

Oil a

nd

Gas E

xp

lora

tio

n

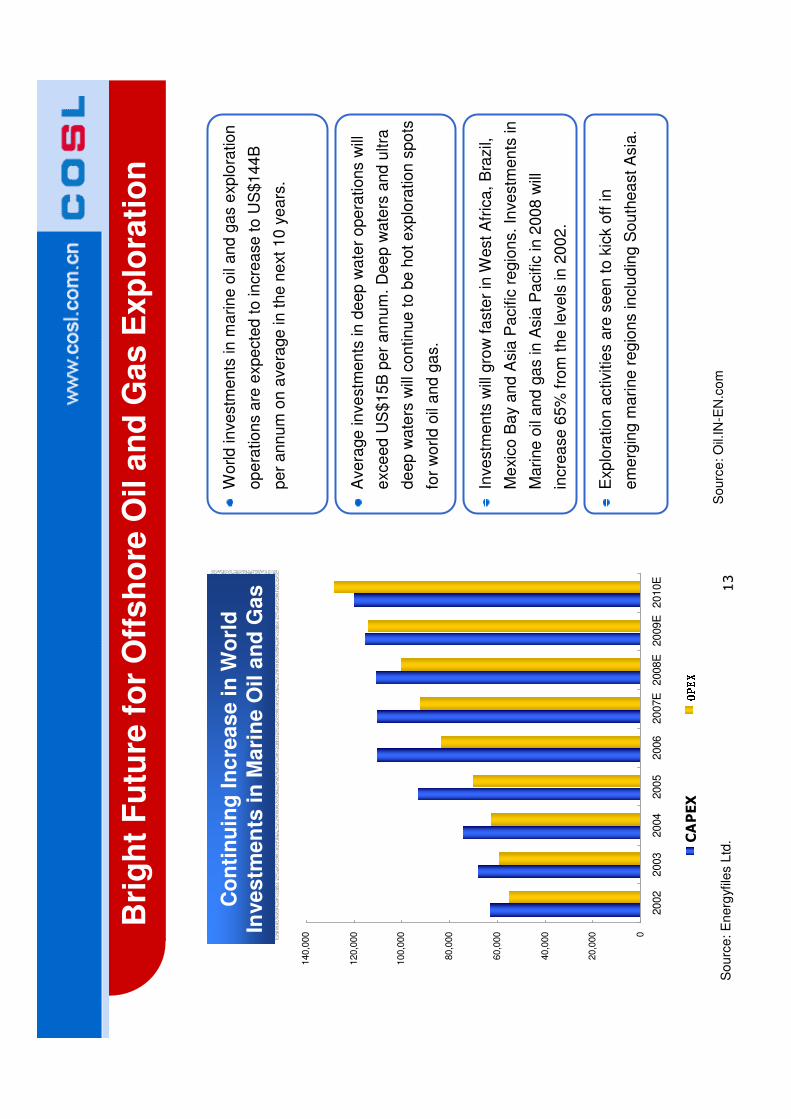

World

in

vestm

en

ts in

ma

rine

oil

and

ga

s e

xplo

ratio

n

op

era

tion

s a

re e

xpe

cte

d t

o in

cre

ase

to

US

$1

44

B

pe

r ann

um

on

ave

rage in

the

ne

xt 1

0 y

ea

rs.

Ave

rage

inve

stm

en

ts in

deep

wa

ter

ope

rations w

ill

exc

eed

US

$15

B p

er

ann

um

. D

ee

p w

ate

rs a

nd

ultra

de

ep

wa

ters

will

co

ntin

ue

to

be

ho

t e

xplo

ratio

n s

po

ts

for

wo

rld

oil

and

ga

s.

Inve

stm

en

ts w

ill g

row

fa

ste

r in

West

Afr

ica

, B

razi

l,

Me

xico

Ba

y and

Asia

Pa

cific

re

gio

ns.

Inve

stm

en

ts in

Ma

rine

oil

and

ga

s in

Asia

Pa

cific

in 2

008

will

incre

ase

65%

fro

m t

he le

vels

in 2

002

.

Exp

lora

tion

activi

tie

s a

re s

een

to

kic

k o

ff in

em

erg

ing m

arine

re

gio

ns in

clu

din

g S

ou

thea

st A

sia

.

Sourc

e: E

nerg

yfile

sLtd

.S

ourc

e: O

il.IN

-EN

.com

1414

840

1,0

50

1,2

35

1,6

79

35

40

45

45

23

33

29

600

1,0

00

1,4

00

1,8

00

2,2

00

2003

2004

2005

2006

2007E

2008E

Pro

du

cti

on

We

llG

as

an

d O

ilfi

eld

So

urc

e:

CN

OO

C L

imit

ed

CO

SL

receiv

es

be

nefi

ts f

rom

dif

fere

nt

sta

ges

in

clu

din

g e

xp

lora

tio

n, d

ev

elo

pm

en

t an

d p

rod

uc

tio

n

CO

SL

receiv

es

be

nefi

ts f

rom

dif

fere

nt

sta

ges

in

clu

din

g e

xp

lora

tio

n, d

ev

elo

pm

en

t an

d p

rod

uc

tio

n

Ch

ina’s

off

sh

ore

op

era

tio

ns

at

full

cap

acit

y

Ch

ina’s

off

sh

ore

op

era

tio

ns

at

full

cap

acit

y

20

03

20

04

20

05

20

06

20

07

E0

50

100

150

200

250

300

350

2006

2007E

2008E

2009E

2010E

RM

B b

Petr

oC

hin

aS

inopec

CN

OO

C

So

urc

e:

CL

SA

sta

tis

tics

Exp

lora

tio

n C

AP

EX

in

Ch

ina

Exp

lora

tio

n C

AP

EX

in

Ch

ina

Bri

gh

t F

utu

re f

or

Off

sh

ore

Oil a

nd

Gas

Ex

plo

rati

on

in

Ch

ina 2

00

8E

1515

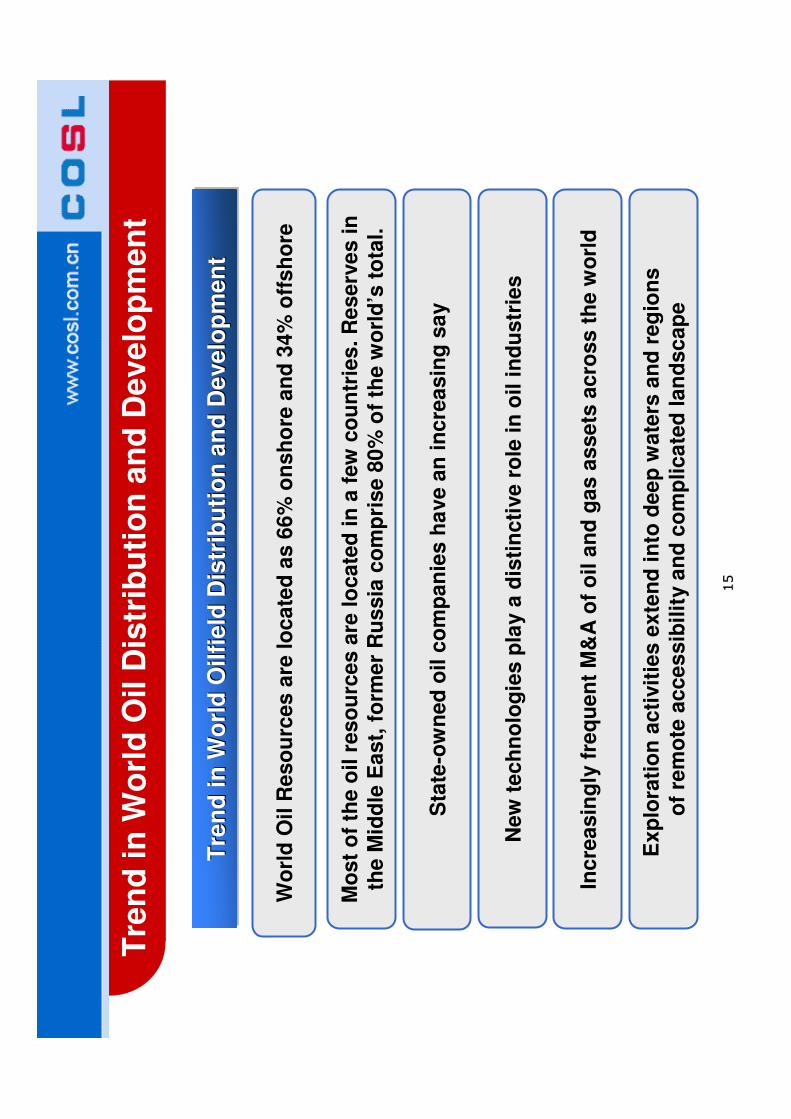

Tre

nd

in

Wo

rld

Oil D

istr

ibu

tio

n a

nd

Dev

elo

pm

en

t

Wo

rld

Oil

Re

so

urc

es

are

lo

ca

ted

as

66

% o

ns

ho

re a

nd

34

% o

ffs

ho

re

Mo

st

of

the

oil

re

so

urc

es

are

lo

ca

ted

in

a f

ew

co

un

trie

s.

Re

se

rve

s i

n

the

Mid

dle

Ea

st,

fo

rme

r R

us

sia

co

mp

ris

e 8

0%

of

the

wo

rld

’s t

ota

l.

Sta

te-o

wn

ed

oil

co

mp

an

ies

ha

ve

an

in

cre

as

ing

sa

y

Tre

nd

in

Wo

rld

Oilfi

eld

Dis

trib

uti

on

an

d D

evelo

pm

en

tT

ren

d i

n W

orl

d O

ilfi

eld

Dis

trib

uti

on

an

d D

evelo

pm

en

tT

ren

d i

n W

orl

d O

ilfi

eld

Dis

trib

uti

on

an

d D

evelo

pm

en

t

New

te

ch

no

log

ies

pla

y a

dis

tin

cti

ve

ro

le i

n o

il i

nd

us

trie

s

Inc

rea

sin

gly

fre

qu

en

t M

&A

of

oil

an

d g

as

as

se

ts a

cro

ss

th

e w

orl

d

Ex

plo

rati

on

ac

tivit

ies

ex

ten

d i

nto

de

ep

wa

ters

an

d r

eg

ion

s

of

rem

ote

ac

ce

ss

ibil

ity a

nd

co

mp

lic

ate

d l

an

ds

ca

pe

1616

Tre

nd

in

Wo

rld

Oil D

istr

ibu

tio

n a

nd

Dev

elo

pm

en

t (c

on

t’d

)

1717

20

08

20

08年 年年年年 年年年

CO

SL

CO

SL发

展展

望发

展展

望发

展展

望发

展展

望发

展展

望发

展展

望发

展展

望发

展展

望

二 二二二二 二二二2

00

8

20

08

CO

SL

C

OS

L B

us

ine

ss O

utl

oo

kB

us

ine

ss O

utl

oo

k33

1818

CO

SL

CO

SL

’’ ssIn

vestm

en

t H

igh

lig

hts

Investm

en

t H

igh

lig

hts

Un

para

llele

d c

om

peti

tive e

dg

e i

n

the o

ffsh

ore

oil

field

serv

ice i

nd

ustr

y

Co

mp

lete

in

du

str

y s

up

ply

c

ha

in

2

5

Hig

h q

ua

lity

cli

en

tele

3

Co

nti

nu

ou

sly

up

gra

din

g

pro

du

cti

on

fa

cil

itie

s a

nd

c

ap

ab

ilit

ies

41C

om

pe

titi

ve

co

st

ad

va

nta

ge

7

Hu

gh

po

ten

tia

l fr

om

new

m

ark

et

se

gm

en

ts a

nd

new

b

us

ine

ss

es

So

un

d f

ina

nc

ial

pe

rfo

rma

nc

e

8

So

lid

co

ntr

ol

on

qu

ali

ty

an

d s

afe

ty s

tan

da

rds

6

Ex

ce

lle

nt

ma

na

ge

me

nt

tea

m a

nd

p

rod

uc

tive

co

rpo

rate

cu

ltu

re

1919

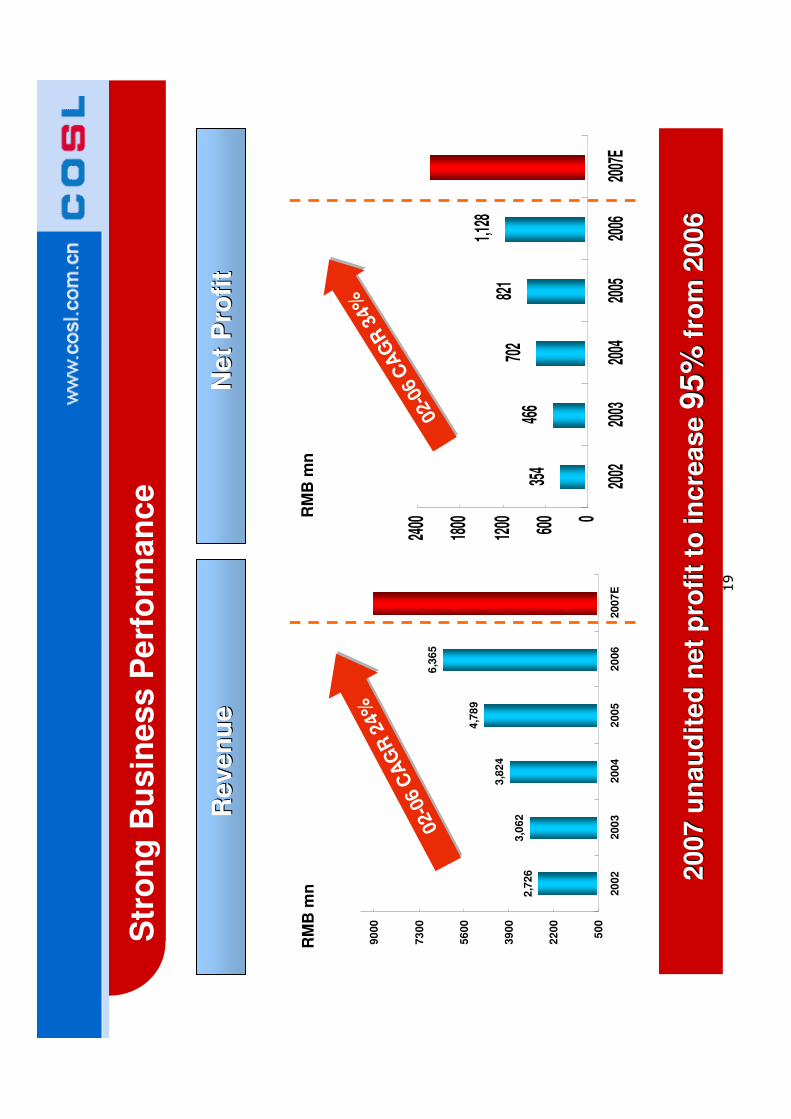

2,7

26

3,0

62

3,8

24

4,7

89

6,3

65

50

0

22

00

39

00

56

00

73

00

90

00

20

02

20

03

20

04

20

05

20

06

20

07

E

02-0

6 C

AG

R 2

4%

02-0

6 C

AG

R 2

4%

RM

B m

n

Re

ve

nu

eR

eve

nu

e

354

466

702

821

1,128

0

600

1200

1800

2400

2002

2003

2004

2005

2006

2007

E

02-0

6 C

AG

R 3

4%

02-0

6 C

AG

R 3

4%

Ne

t P

rofi

tN

et

Pro

fit

RM

B m

n

Str

on

g B

usin

ess P

erf

orm

an

ce

20

07

2

00

7 u

na

ud

ite

du

na

ud

ite

dn

et

pro

fit

to in

cre

as

e

ne

t p

rofi

t to

in

cre

as

e 9

5%

95

%fr

om

20

06

fro

m 2

00

6

2020

Go

als

of

CO

SL

202

0202

0

201

0201

0

Ne

ar-

term

go

al

Ne

ar

Ne

ar --

term

go

al

term

go

al

Lo

ng

-te

rm g

oa

lL

on

gL

on

g-- t

erm

go

al

term

go

al

Be

co

me

a t

op

-no

tch

in

tern

ati

on

al

oil

fie

ld s

erv

ice

pro

vid

ers

Be

co

me

a t

op

Be

co

me

a t

op

-- no

tch

in

tern

ati

on

al

no

tch

in

tern

ati

on

al

oil

fie

ld s

erv

ice

pro

vid

ers

oil

fie

ld s

erv

ice

pro

vid

ers

An

oil

fie

ld s

erv

ice

pro

vid

er

wit

h

str

on

g c

om

pe

ten

ce

s i

n t

he

in

tern

ati

on

al

ma

rke

t

An

oil

fie

ld s

erv

ice

pro

vid

er

wit

h

An

oil

fie

ld s

erv

ice

pro

vid

er

wit

h

str

on

g c

om

pe

ten

ce

s i

n t

he

s

tro

ng

co

mp

ete

nc

es

in

th

e

inte

rna

tio

na

l m

ark

et

inte

rna

tio

na

l m

ark

et

Accele

rate

deve

lopm

ent of

inte

gra

ted

capabili

ties. C

om

pre

hensiv

ely

enhance

pro

fessio

nal c

apabili

ties.

Explo

re n

ew

busin

ess o

pport

uniti

es n

ew

oilf

ield

pro

ductio

n s

erv

ices

Pla

ns

Pla

ns

Expand facili

ties, upgra

de s

erv

ice c

apabili

ty

Str

ength

en d

eep w

ate

r opera

tion c

apabili

ty

Incre

ase in

vestm

ents

in R

&D

to e

nhance

CO

SL’s

technolo

gic

al c

om

petit

iveness

Expand s

cope o

f serv

ice, im

ple

ment glo

bal

deve

lopm

ent st

rate

gie

s

Achie

ve b

reakth

roughs in

technolo

gy,

capacity

expansio

n a

nd c

apabili

ty u

pgra

des

thro

ugh c

apita

l mark

et opera

tions in

clu

din

g

M&

A

2121

Fo

ur

Co

re S

trate

gie

s

Tech

no

log

yT

ech

no

log

y-- d

riven

dri

ven

Co

st

Co

mp

eti

tiven

ess

Co

st

Co

mp

eti

tiven

ess

Inte

gra

tio

nIn

teg

rati

on

GGlo

bal

lob

al

Op

era

tio

nO

pera

tio

n

A u

niq

ue

pu

bli

cly

-lis

ted

in

teg

rate

d o

ilfi

eld

se

rvic

e p

rovid

er

A u

niq

ue

pu

bli

cly

A u

niq

ue

pu

bli

cly

-- lis

ted

in

teg

rate

d o

ilfi

eld

se

rvic

e p

rovid

er

lis

ted

in

teg

rate

d o

ilfi

eld

se

rvic

e p

rovid

er

Str

ate

gic

po

sit

ion

ing

:E

xp

ert

in

co

nve

ntio

nal te

ch

no

logie

sK

ee

n f

ollo

we

r in

ad

va

nce

d a

pp

lica

tio

ns

En

ab

ler

of

hig

hly

eff

icie

nt

op

era

tio

ns

Co

ntr

ibu

tor

to c

ost

red

uctio

n

Pio

ne

er

in in

teg

rate

d s

erv

ice

sP

art

icip

an

t in

glo

ba

l co

mp

etitio

nP

art

ne

r in

win

-win

de

ve

lop

me

nt

Se

rva

nt

for

sh

are

ho

lde

r va

lue

2222

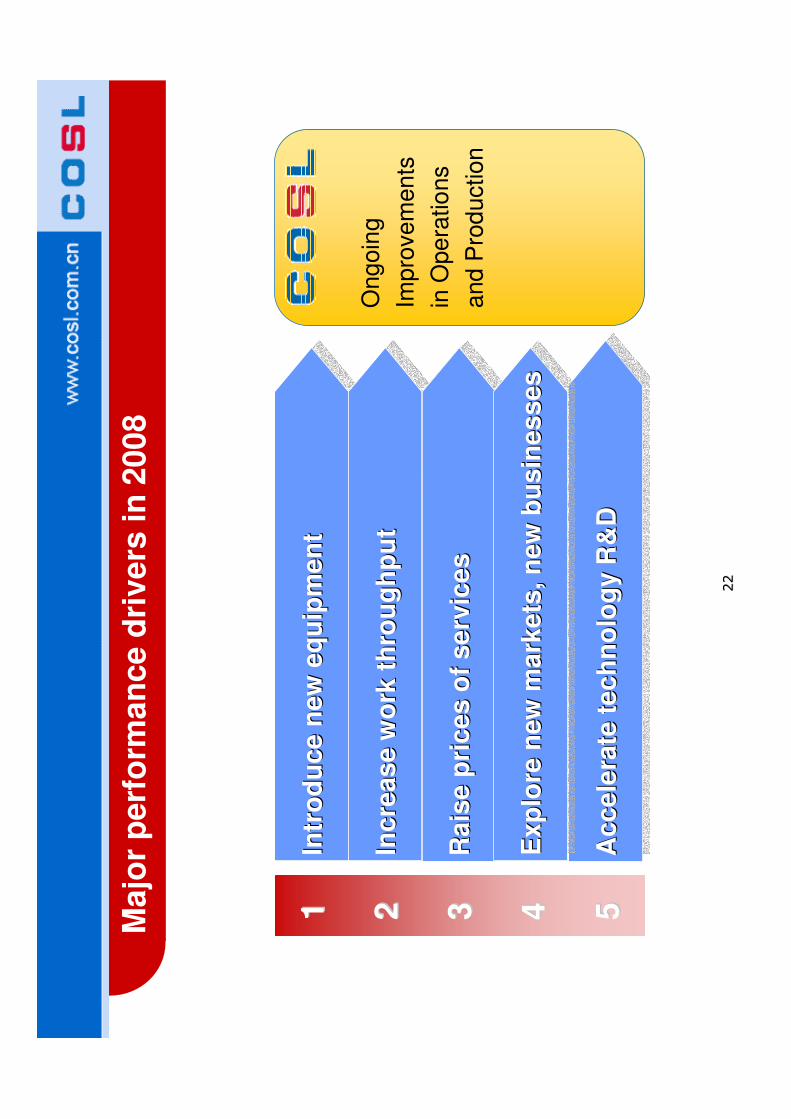

Majo

r p

erf

orm

an

ce d

rivers

in

2008

11In

tro

du

ce

new

eq

uip

me

nt

Intr

od

uce

new

eq

uip

me

nt

Intr

od

uce

new

eq

uip

me

nt

22In

cre

as

e w

ork

th

rou

gh

pu

tIn

cre

as

e w

ork

th

rou

gh

pu

tIn

cre

as

e w

ork

th

rou

gh

pu

t

33R

ais

e p

ric

es o

f se

rvic

es

Ra

ise

pri

ces o

f se

rvic

es

Ra

ise

pri

ces o

f se

rvic

es

44 55A

cc

ele

rate

te

ch

no

log

y R

&D

Ac

ce

lera

te t

ec

hn

olo

gy R

&D

Ac

ce

lera

te t

ec

hn

olo

gy R

&D

Ex

plo

re n

ew

ma

rke

ts, n

ew

bu

sin

es

ses

Ex

plo

re n

ew

ma

rke

ts, n

ew

bu

sin

es

ses

Ex

plo

re n

ew

ma

rke

ts, n

ew

bu

sin

es

ses

Ongoin

g

Impro

vem

ents

in O

pera

tio

ns

and P

rod

uction

2323

CA

PE

X s

inc

e lis

tin

gC

AP

EX

sin

ce

lis

tin

g:

in e

xc

es

s o

f R

MB

10

billio

n:

in e

xc

es

s o

f R

MB

10

billio

n

RM

B M

il’

Bu

sin

es

s d

river

in 2

008:

Intr

od

uce n

ew

eq

uip

men

t

0 0001100 1100110011002200 2200220022003300 3300330033004400 4400440044005500 550055005500 2002 2002200220022003 2003200320032

004 2004200420042005 2005200520052

006 2006200620062007E 2007E 2007E 2007E 2

008E 2008E 2008E 2008E

2424

2010

2010

2009

2009

2008

2008

CO

SL

942 w

ill co

mm

en

ce

op

era

tio

n in

2H; ;;; 4

mo

du

le r

igs o

pera

te f

or

six

mo

re m

on

ths;

5

on

sh

ore

rig

s w

ill

co

mm

en

ce o

pera

tio

n in

C

hin

a a

nd

oth

er

co

un

trie

s

R&

D, b

uild

ing

, p

rocu

re

eq

uip

men

t like

cem

en

tin

g p

um

p, E

LIS

, lift

bo

at

etc

.

Nin

e n

ew

su

pp

ort

ing

v

essels

will co

mm

en

ce

op

era

tio

n in

2H

On

e 8

-str

eam

er

seis

mic

v

essel w

ill co

mm

en

ce

op

era

tio

n in

2Q

Jack-u

p C

OS

L936 w

ill

co

mm

en

ce o

pera

tio

n b

y

year

en

d

R&

D a

nd

pro

cu

re t

oo

ls

for

measu

rem

en

t w

hile

dri

llin

g (

MW

D),

acid

ific

ati

on

an

d

cru

sh

ing

Nin

e n

ew

su

pp

ort

ing

v

essels

will co

mm

en

ce

op

era

tio

n in

1H

. T

wo

hig

h-

po

were

d d

eep

wate

r v

essels

will co

mm

en

ce

op

era

tio

n b

y y

ear

en

d

Jack-u

p C

OS

L937 w

ill

co

mm

en

ce o

pera

tio

n;

4

200-f

eet

jack-u

p r

igs t

o

co

mm

en

ce o

pera

tio

n;

to

op

era

te t

he d

eep

-wate

r ri

gs in

veste

d b

y t

he

pare

nt

co

mp

an

y in

2011

On

e 1

2-s

tream

er

seis

mic

v

essel w

ill co

mm

en

ce

op

era

tio

n

Dri

llin

g

Serv

ice

s

Well

S

erv

ice

s

Mari

ne S

up

po

rt

an

d T

ran

sp

ort

ati

on

S

erv

ice

Geo

ph

ysic

al

Serv

ice

s

Bu

sin

es

s d

rive

r in

20

08

: In

tro

du

ce n

ew

eq

uip

me

nt

(co

nt’

d)

16 o

ffsh

ore

en

gin

eeri

ng

su

pp

ort

ing

vessels

2525

44

48

53

57

62

46

12

16

20

6

11

16

21

2

0

20

40

60

80

100

120

2006

2007E

2008E

2009E

2010E

Cem

en

tin

g P

um

pL

WD

EL

IS L

og

gin

g S

yste

m

70

75

80

95

97

55

4

44

55

55

1

0

20

40

60

80

100

120

2006

2007E

2008E

2009E

2010E

Ch

em

ical

vess

el

Oil

tan

ke

r

Off

sh

ore

wo

rkin

g v

esse

l

Inc

rease

ca

pa

cit

y f

or

dri

llin

g o

pe

rati

on

s

Inc

rease

ca

pa

cit

y f

or

dri

llin

g o

pe

rati

on

sIn

cre

ase

ca

pa

cit

y f

or

well

se

rvic

es

Inc

rease

ca

pa

cit

y f

or

well

se

rvic

es

Inc

rease

ca

pa

cit

y f

or

m

ari

ne

tra

ns

po

rta

tio

n

an

d s

up

po

rt

Inc

rease

ca

pa

cit

y f

or

m

ari

ne

tra

ns

po

rta

tio

n

an

d s

up

po

rt

Inc

rease

ca

pa

cit

y f

or

ge

op

hys

ica

l o

pe

rati

on

s

Inc

rease

ca

pa

cit

y f

or

ge

op

hys

ica

l o

pe

rati

on

s

15

15

16

17

18

44

441

44

4

06

12

18

24

30

2006

2007E

2008E

2009E

2010E

On

sh

ore

Dri

llin

g R

igR

en

ted

De

ep

Wa

ter

Rig

gin

g p

latf

orm

Mo

du

le R

igR

ig p

latf

orm

77

89

44

44

5

8

02468

10

12

14

2006

2007E

2008E

2009E

2010E

Su

rve

yin

g V

es

se

l

Se

ism

ic V

es

se

l

Bu

sin

es

s d

river

in 2

008:

Intr

od

uce n

ew

eq

uip

men

t (c

on

t’d

)

+

2626

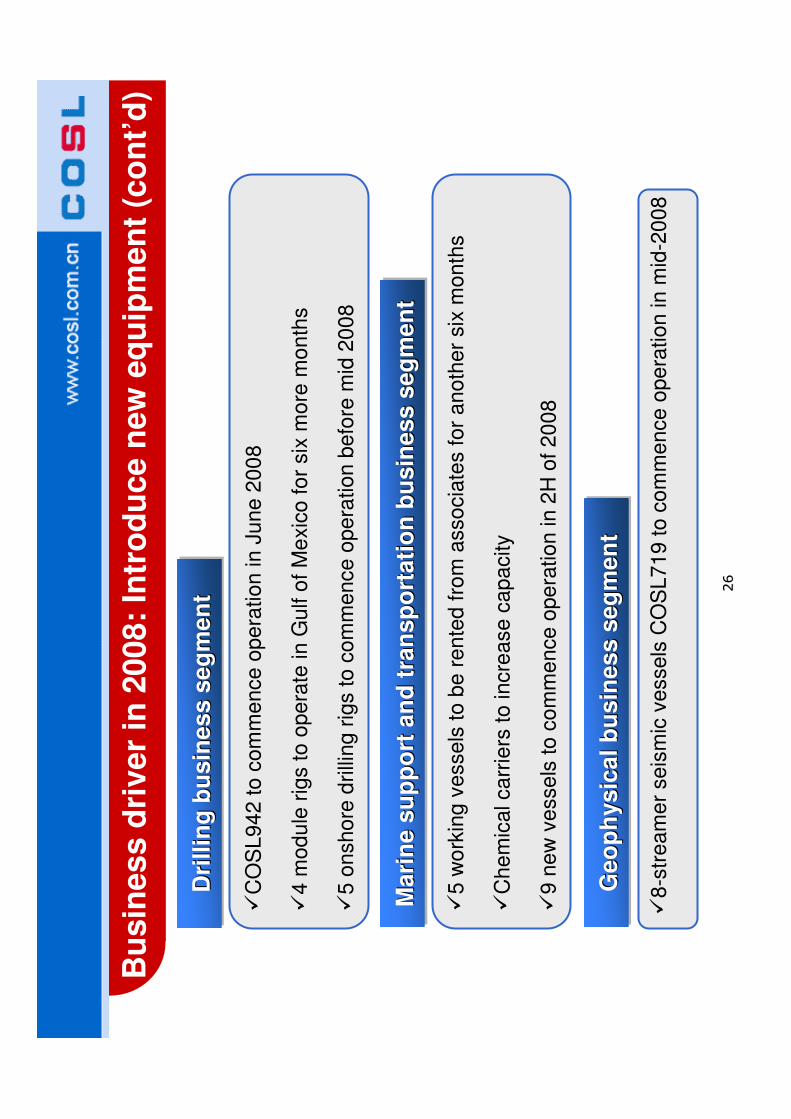

Bu

sin

es

s d

river

in 2

008:

Intr

od

uce n

ew

eq

uip

men

t (c

on

t’d

)

�C

OS

L9

42

to c

om

me

nce

op

era

tio

n in

Ju

ne

20

08

�4

mo

du

le r

igs t

o o

pe

rate

in

Gu

lf o

f M

exic

o f

or

six

mo

re m

on

ths

�5

on

sh

ore

dri

llin

g r

igs t

o c

om

me

nce

op

era

tio

n b

efo

re m

id 2

00

8

Dri

llin

g b

usin

ess s

eg

men

tD

rill

ing

bu

sin

ess s

eg

men

tD

rill

ing

bu

sin

ess s

eg

men

t

�5

wo

rkin

g v

essels

to

be

re

nte

d f

rom

asso

cia

tes f

or

an

oth

er

six

mo

nth

s

�C

he

mic

al ca

rrie

rs t

o in

cre

ase

ca

pa

city

�9

ne

w v

esse

ls t

o c

om

me

nce

op

era

tio

n in

2H

of

20

08

Mari

ne

su

pp

ort

an

d t

ran

sp

ort

ati

on

bu

sin

ess s

eg

men

tMM

ari

ne

ari

ne

su

pp

ort

an

d t

ran

sp

ort

ati

on

bu

sin

ess s

eg

men

tsu

pp

ort

an

d t

ran

sp

ort

ati

on

bu

sin

ess s

eg

men

t

�8

-str

ea

me

r se

ism

ic v

essels

CO

SL

71

9to

co

mm

en

ce

op

era

tio

n in

mid

-20

08

Geo

ph

ysic

al

bu

sin

ess s

eg

men

tG

eo

ph

ysic

al

bu

sin

ess s

eg

men

tG

eo

ph

ysic

al

bu

sin

ess s

eg

men

t

2727

CO

SL

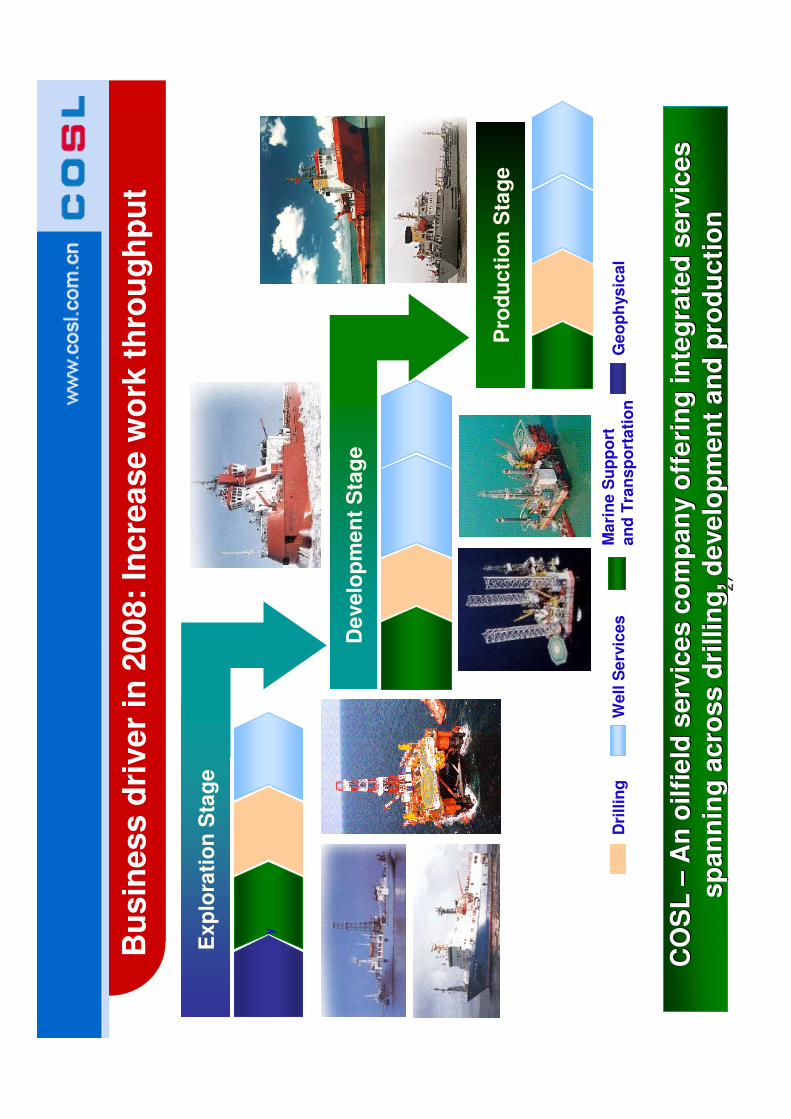

C

OS

L ––

An

oilfi

eld

serv

ice

s c

om

pa

ny o

ffe

rin

g in

teg

rate

d s

erv

ice

s

An

oilfi

eld

serv

ice

s c

om

pa

ny o

ffe

rin

g in

teg

rate

d s

erv

ice

s

sp

an

nin

g a

cro

ss

dri

llin

g, d

eve

lop

me

nt

an

d p

rod

ucti

on

sp

an

nin

g a

cro

ss

dri

llin

g, d

eve

lop

me

nt

an

d p

rod

ucti

on

Ex

plo

rati

on

Sta

ge

Pro

du

cti

on

Sta

ge

y

De

ve

lop

me

nt

Sta

ge

Ge

op

hys

ica

lM

ari

ne

Su

pp

ort

a

nd

Tra

ns

po

rta

tio

nD

rill

ing

We

ll S

erv

ices

Bu

sin

es

s d

river

in 2

008:

Incre

ase w

ork

th

rou

gh

pu

t

2828

Bu

sin

es

s d

river

in 2

008:

Incre

ase w

ork

th

rou

gh

pu

t (c

on

t’d

)

�N

um

ero

us

ma

rke

t o

pp

ort

un

itie

s i

n

dif

fere

nt

sta

ge

s o

f o

ilfi

eld

pro

du

cti

on

�B

es

ide

s i

nc

rea

se

in

wo

rk t

hro

ug

hp

ut

of

log

gin

g,

dir

ec

tio

na

l d

rill

ing

, c

em

en

tin

g

an

d w

ell

co

mp

leti

on

, a

cid

ific

ati

on

, c

rus

hin

g,

sc

ree

n p

ipe

pro

du

cti

on

a

cti

vit

ies

are

ex

pe

cte

d t

o g

row

�U

ptr

en

d i

n C

AP

EX

an

d O

PE

X o

f o

il

co

mp

an

ies

on

oil

fie

ld e

xp

lora

tio

n

�C

NO

OC

an

no

un

ce

d d

isc

ove

ry o

f 1

0

new

oil

an

d g

as

re

se

rve

s i

n N

ov 2

00

7

2929

20,0

00

60,0

00

100,0

00

140,0

00

2002

2003

2004

2005

2006

2007E

25,0

00

50,0

00

75,0

00

2002

2003

2004

2005

2006

2007E

Jack-u

p:

US

D/D

ay

Sem

i-su

bm

ers

ible: :::

US

D/D

ay

Bu

sin

es

s d

river

in 2

008:

Rais

e s

erv

ices p

rices

Uti

lizati

on

to

rem

ain

hig

h d

ue t

o s

tro

ng

dem

an

d,

satu

rate

d c

ap

acit

y,

go

od

cu

sto

mer

rela

tio

nsh

ip a

nd

tig

ht

sch

ed

ule

man

ag

em

en

t

Uti

lizati

on

to

rem

ain

hig

h d

ue t

o s

tro

ng

dem

an

d,

satu

rate

d c

ap

ac

Uti

lizati

on

to

rem

ain

hig

h d

ue t

o s

tro

ng

dem

an

d,

satu

rate

d c

ap

ac

ity,

ity,

go

od

cu

sto

mer

rela

tio

nsh

ip a

nd

tig

ht

sch

ed

ule

man

ag

em

en

tg

oo

d c

usto

mer

rela

tio

nsh

ip a

nd

tig

ht

sch

ed

ule

man

ag

em

en

t

3030

Tap

th

e d

eep

w

ate

r seg

men

t

Exp

an

d f

oo

tho

ld

in o

vers

eas

mark

ets

Ta

rge

ted

So

uth

ea

st

As

ia,

Mid

dle

Ea

st,

Gu

lf

of

Me

xic

o,

Ru

ss

ia a

nd

Afr

ica

Ex

pa

nd

in

to o

ns

ho

re s

erv

ice

s,

leve

rag

ing

o

ur

str

en

gth

in

th

e o

ffs

ho

re m

ark

et.

Ex

pa

nd

pre

se

nc

e i

n t

he

de

ep

wa

ter

se

gm

en

t fo

llo

win

g f

oo

tste

ps

of

oil

co

mp

an

ies

Co

nso

lid

ate

exis

tin

g

mark

et

sh

are

Secu

re f

irst-

mo

ver

ad

van

tag

es in

n

ew

mark

ets

an

d

new

bu

sin

ess

Bu

sin

es

s d

rive

r in

20

08

: E

xp

lore

new

ma

rke

ts, n

ew

bu

sin

es

ses

Pen

etr

ate

in

to

on

sh

ore

mark

ets

3131

�B

reakth

roughs a

chie

ved in d

rilli

ng, w

ell

serv

ices a

nd g

eophys

ical opera

tions in

ove

rseas m

ark

ets

�A

ddin

g m

ore

than U

S 1

00 m

illio

n o

f re

venue to o

nshore

drilli

ng s

erv

ices in b

oth

lo

cal a

nd o

vers

ea m

ark

et

�S

igned a

2-y

ear

geoth

erm

al w

ell

contr

act

with the P

hili

ppin

e N

ational O

il C

om

pany

for

the d

irectional drilli

ng s

erv

ices

RM

B M

n

43.2

%

26.8

%

12.9

%

17.1

%

770

(18.1

%)

Indone

sia

Au

str

alia

Me

xico

Oth

ers

Bre

ak

do

wn

of

Bre

ak

do

wn

of

ove

rse

as

re

ve

nu

e i

n 1

H2

00

7o

ve

rse

as

re

ve

nu

e i

n 1

H2

00

7

RM

B M

n

OOve

rse

as

ma

rke

ts a

dd

ing

mo

me

ntu

mve

rse

as

ma

rke

ts a

dd

ing

mo

me

ntu

m

0

200

400

600

800

1000

1200

2003

2004

2005

20061H2007

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

ove

rse

as

reve

nu

eo

ve

rse

as/

tota

l

Bu

sin

ess d

river

in 2

008:

Ex

plo

re n

ew

mark

ets

, n

ew

bu

sin

esses (

co

nt’

d)

3232

Ma

rke

tM

ark

et --

ori

en

ted

ori

en

ted

CO

SL

CO

SL

’’ sste

ch

no

log

yte

ch

no

log

y-- d

rive

n s

tra

teg

yd

rive

n s

tra

teg

y

Inte

gra

ted

In

teg

rate

d

Inn

ova

tio

nIn

no

va

tio

n

Le

ap

fro

gL

ea

pfr

og

De

ve

lop

me

nt

De

ve

lop

me

nt

Ta

len

tT

ale

nt

ori

en

ted

ori

en

ted

Bu

sin

es

s d

rive

r in

20

08

: A

cc

ele

rate

te

ch

no

log

y R

&D

Intr

oduced p

roprieta

ry E

LIS

loggin

g s

yste

m

into

dom

estic a

nd o

vers

eas m

ark

ets

Esta

blis

hed the first jo

int la

bora

tory

Intr

oduced c

em

enting s

erv

ices to X

injia

ng

Pro

prieta

ry “

Bohailo

w-d

ensity-

hig

h-s

trength

well

cem

enting technolo

gy

wid

ely

applie

d

CO

SL

’ste

ch

no

log

y s

trate

gy

CO

SL

’ste

ch

no

log

y s

trate

gy

CO

SL

’sap

plicati

on

of

tech

no

log

ies

CO

SL

’sap

plicati

on

of

tech

no

log

ies

Con

ven

tiona

l

Cem

en

t

Lo

w-D

en

sity,

Hig

h-S

tren

gth

Cem

en

t

3333

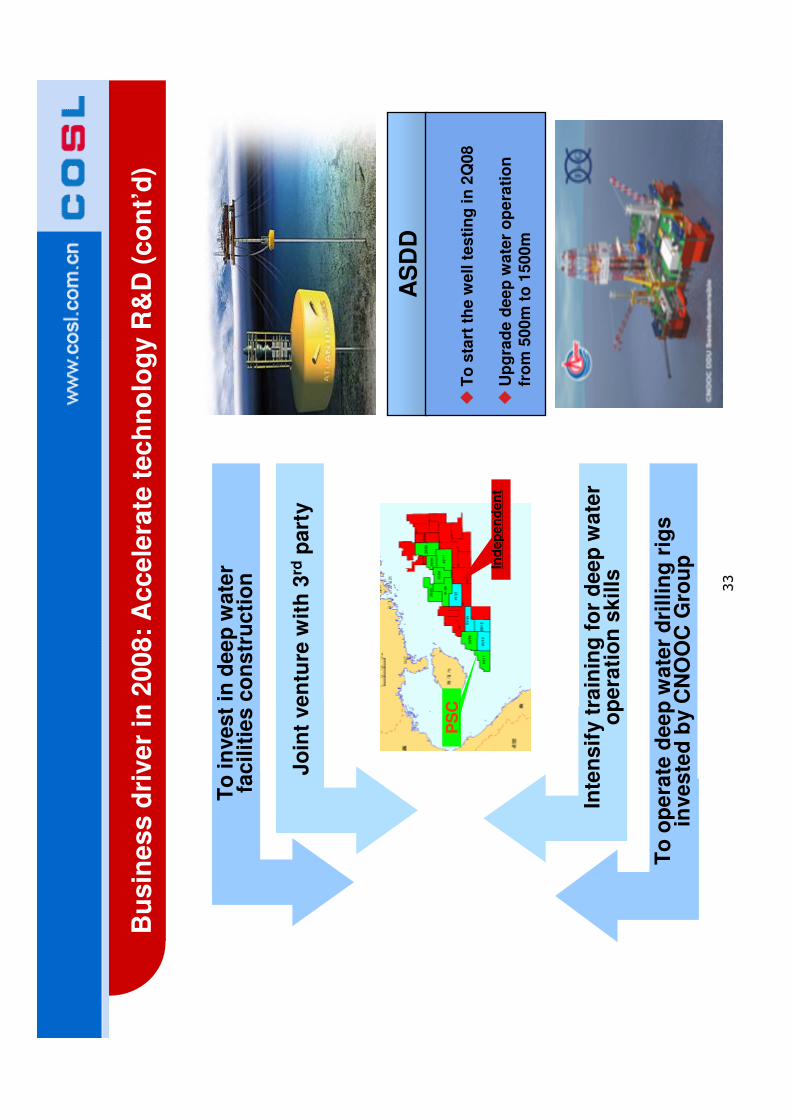

AS

DD

�T

o s

tart

th

e w

ell

tes

tin

g i

n 2

Q08

�U

pg

rad

e d

ee

p w

ate

r o

pe

rati

on

fr

om

50

0m

to

1500

m

PS

C

Ind

ep

en

den

t

Jo

int

ve

ntu

re w

ith

3rd

pa

rty

Inte

ns

ify t

rain

ing

fo

r d

ee

p w

ate

r o

pe

rati

on

sk

ills

To

op

era

te d

ee

p w

ate

r d

rill

ing

rig

s

inve

ste

d b

y C

NO

OC

Gro

up

To

in

ve

st

in d

ee

p w

ate

r fa

cil

itie

s c

on

str

uc

tio

n

Bu

sin

es

s d

rive

r in

20

08

: A

cc

ele

rate

te

ch

no

log

y R

&D

(c

on

t’d

)

3434

Clic

k t

o e

dit

tit

le s

tyle

Th

an

k Y

ou

!

![Defense department-strategic-guidance-010512[1]](https://img.pdfslide.us/doc/110x75/5561860bd8b42ace7d8b4574/defense-department-strategic-guidance-0105121.jpg)