Embed Size (px)

Citation preview

Walter A. (Tony) Maull, Jr.703-747-1838

Paul Feeko703-747-1274

Steve Glover202-955-8593

Anita Antenucci703-714-1707

Greg Ager703-736-0020

2007 M&A Hot Topics Briefing2007 M&A Hot Topics BriefingBest Practices Forum – Part 1

0704-0823629_MCL

1

TopicsSlide Number

State of M&A Market 4Trends in Valuation, Deal Pricing and Financing 26Sell Side Strategies 46Buy Side Strategies 56

0704-0823629_MCL

2

Introductions

Gibson, DunnLegal due diligenceStructuringM&A and securities lawContractingLitigation

Houlihan LokeyUpdata Advisors

Transaction strategyPricingMarketing (Offering Memo)NegotiationFinancing

Independent AuditorsAudited financials

Ernst & YoungBuy/Sell-side diligenceFinancial carve-outTax planning and structuringOperational separationValuation and modeling

0704-0823629_MCL

3

State of the M&A MarketState of the M&A Market

0704-0823629_MCL

4

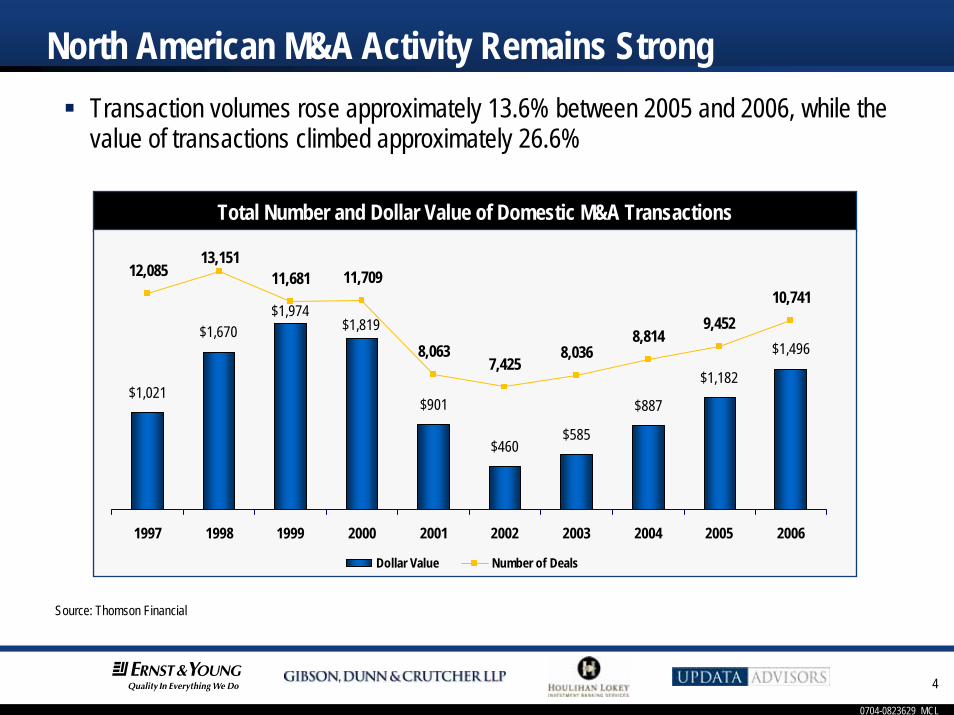

North American M&A Activity Remains StrongTransaction volumes rose approximately 13.6% between 2005 and 2006, while the value of transactions climbed approximately 26.6%

Total Number and Dollar Value of Domestic M&A Transactions

$1,021

$1,670

$901

$460$585

$887

$1,182

$1,496$1,819

$1,974

12,08513,151

11,681 11,709

8,0637,425

8,0368,814

9,45210,741

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Dollar Value Number of Deals

Source: Thomson Financial

0704-0823629_MCL

5

North American Deal Size IncreasingAverage transaction size has risen by 162% from $138 million to $362 million in 2006. Average transaction size rose 17.5% from 2005 to 2006

Average Size of Announced M&A Deals

$171

$283

$348

$252

$138$170

$258$308

$362$383

$0

$100

$200

$300

$400

$500

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

162%

In M

illion

s

Source: Thomson Financial

0704-0823629_MCL

6

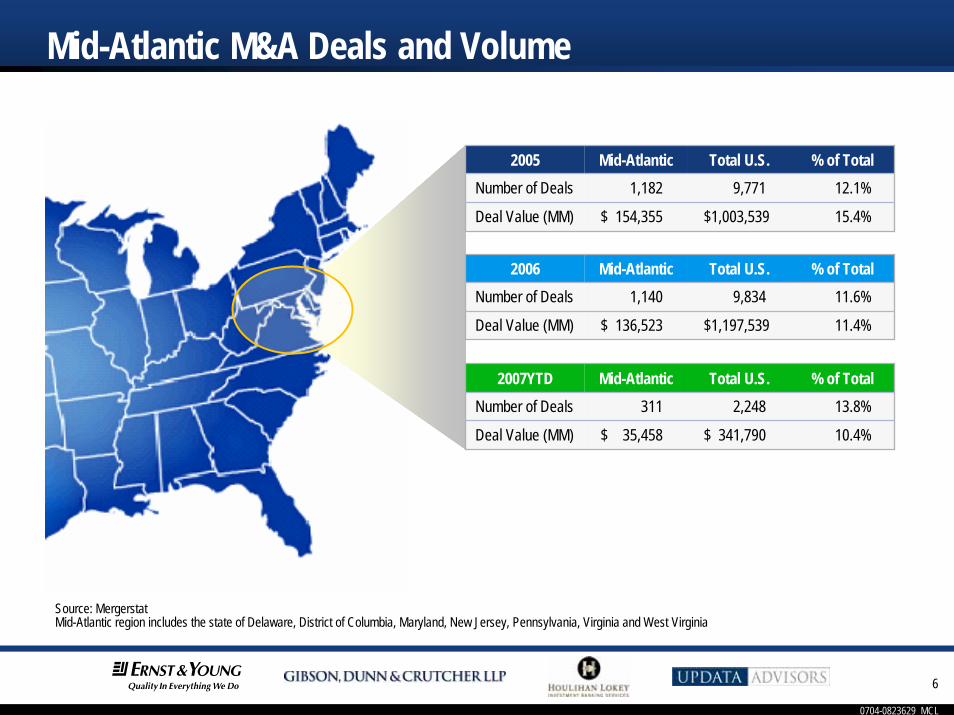

Source: MergerstatMid-Atlantic region includes the state of Delaware, District of Columbia, Maryland, New Jersey, Pennsylvania, Virginia and West Virginia

Mid-Atlantic M&A Deals and Volume

2005 Mid-Atlantic Total U.S. % of TotalNumber of Deals 1,182 9,771 12.1%

Deal Value (MM) $ 154,355 $1,003,539 15.4%

2007YTD Mid-Atlantic Total U.S. % of TotalNumber of Deals 311 2,248 13.8%

Deal Value (MM) $ 35,458 $ 341,790 10.4%

2006 Mid-Atlantic Total U.S. % of TotalNumber of Deals 1,140 9,834 11.6%

Deal Value (MM) $ 136,523 $1,197,539 11.4%

0704-0823629_MCL

7

2006 M&A Market HighlightsMega-Deals Get the Headlines, but Middle-Market Transactions Predominate– Over 90% of all M&A transactions since 1997 have been under $500 million.– However, the percentage of transactions in excess of $500 million has increased from 5.4% in 2002

to 11.4% in 2006.

Total Number of U.S. M&A Transactions by Deal Size

5,620 6,146

4,4203,212 2,914 2,906 2,815 3,083 3,182

1,0281,126

1,0821,039

669 616 710 781893 980

448479

531531

296204 232 357

458 537

4,998

0

2,000

4,000

6,000

8,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Under $100.0 Million $100.0 - $499.9 Million Over $500.0 Million

Deals

Ann

ounc

ed

Source: Mergerstat

0704-0823629_MCL

8

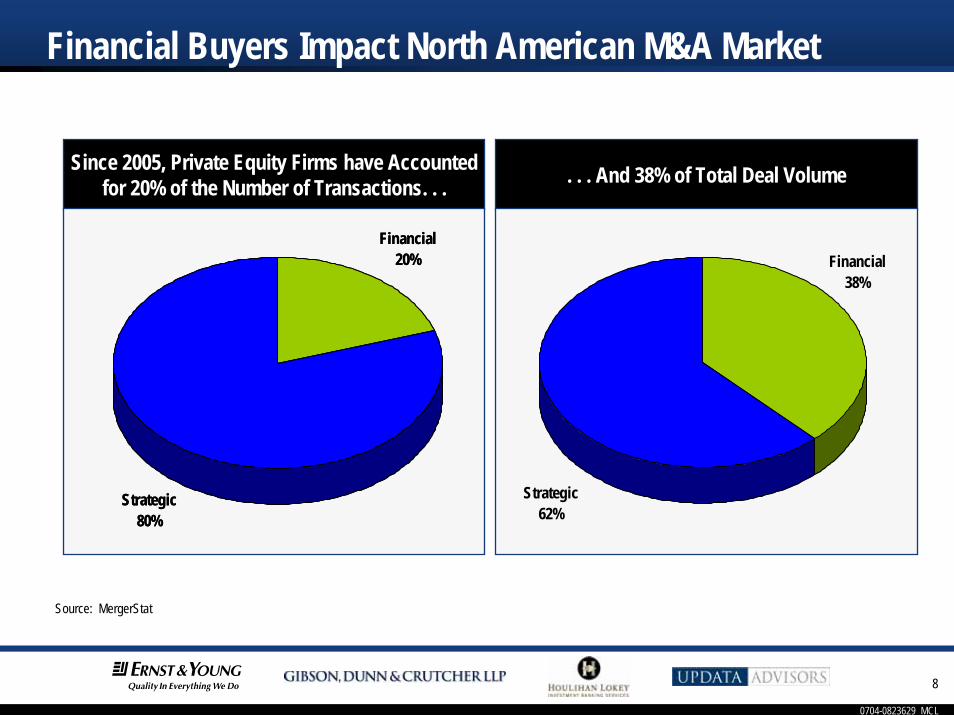

Financial Buyers Impact North American M&A Market

Source: MergerStat

Since 2005, Private Equity Firms have Accounted for 20% of the Number of Transactions. . .

Since 2005, Private Equity Firms have Accounted for 20% of the Number of Transactions. . . . . . And 38% of Total Deal Volume. . . And 38% of Total Deal Volume

Financial20%

Strategic80%

Financial20%

Strategic80%

Financial38%

Strategic62%

0704-0823629_MCL

9

Favorable Interest Rate Environment Means Easy Credit

10-Year Treasury Note Rate10-Year Treasury Note Rate

0

2

4

6

8

10

12

14

16

18

70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06

Avg 7.55%

%

0704-0823629_MCL

10

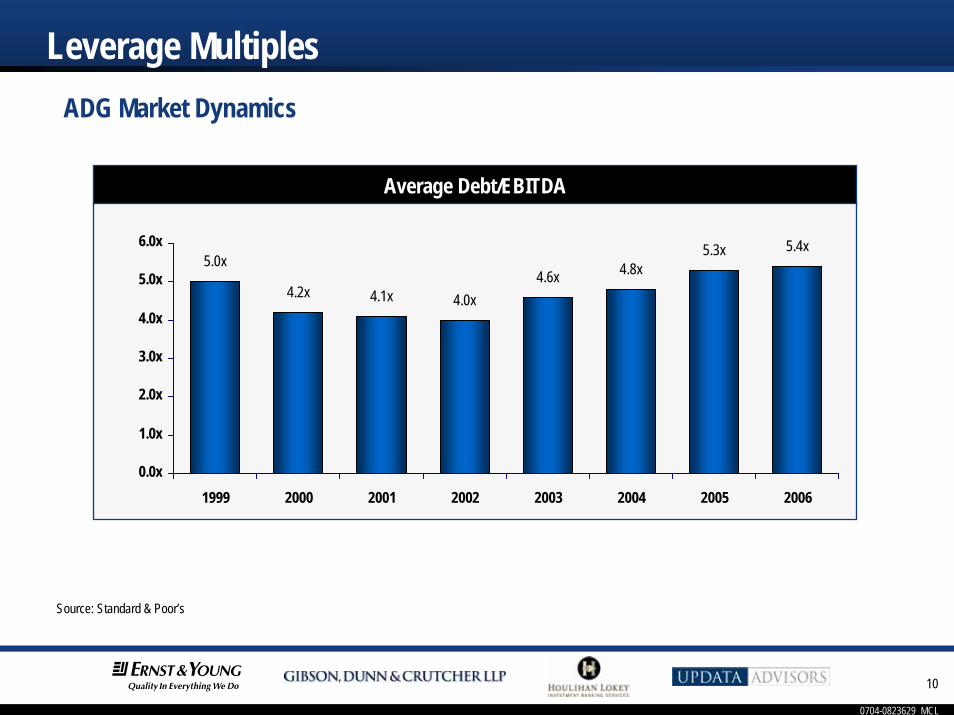

Leverage MultiplesADG Market Dynamics

Source: Standard & Poor’s

Average Debt/EBITDA

5.0x

4.2x 4.1x 4.0x4.6x 4.8x

5.3x 5.4x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

1999 2000 2001 2002 2003 2004 2005 2006

0704-0823629_MCL

11

Strong Supply of Aggressive Private Capital in the USSince 2000, there has been nearly $900 billion in capital committed to U.S. private equity funds, yet only $480 billion of this equity has been invested.There remains a capital overhang of over $400 billion.

Source: VentureXpert

Average Size of Announced M&A DealsAverage Size of Announced M&A Deals

$52$76

$143

$60

$99

$218

$185

$149$125

$60

$121

$56$52$54

$25 $28$45

$90

$146

$63$47

$63

$0

$50

$100

$150

$200

$250

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

PE Funds Raised Invested Capital

$ Billi

ons

$ Billi

ons

0704-0823629_MCL

12

Driving Today’s M&A ActivityHedge Fund Growth– Hedge fund growth has been unrelenting over the past decade. Assets now exceed $1.3 trillion

Hedge Fund Growth (1997– 2006)

Source: HFRI.*Data is YTD Q3 2006.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

0

200

400

600

800

1,000

1,200

1,400

1,600

Num

ber o

f Hed

ge F

unds Assets, $Billions

0704-0823629_MCL

13

Top 15 Megadeals in 2006

Note: PE Deals are highlightedSource: Mergerstat

Date Seller Name Buyer NameEnterprise Value ($B)

04/03/06 General Motors/ GMAC General Motors Acceptance Corp. /Private Group led by Cerberus Capital Management

253.4$

08/28/06 SanPaolo-IMI Banca Intesa 106.3$

03/05/06 BellSouth AT&T 102.2$

05/07/06 Golden West Financial Wachovia 73.2$

02/27/06 SUEZ Gaz de France 61.7$

11/19/06 Equity Office The Blackstone Group 34.7$

11/07/06 America Telecom America Movil 34.0$

01/27/06 Arcelor Mittal Steel 33.2$

07/24/06 HCA HCA /Private Group led by Bain Capital, Kohlberg Kravis Roberts & Co, Merrill Lynch Global Private Equity and HCA founder

31.8$

11/10/06 Daewoo Engineering & Construction Daewoo Engineering & Construction /Consortium led by South Korean airline Kumho Asiana Group

30.8$

04/03/06 Banca Nazionale del Lavoro BNP Paribas 28.7$

11/28/06 Scottish Power Iberdrola 28.2$

10/02/06 Harrah's Entertainment Texas Pacific Group/ Apollo Management 27.2$

11/16/06 Clear Channel Communications Thomas H. Lee Partners/ Bain Capital 26.6$

04/07/06 British Airports Authority Airport Development & Investment 24.9$

896.8$

0704-0823629_MCL

14

Date Seller Name Buyer NameEnterprise Value ($B)

06/12/05 Bayerische Hypo- und Vereinsbank UniCredito Italiano 146.4$

01/28/05 Gillette Procter & Gamble 61.1$

06/30/05 MBNA Bank of America 47.4$

12/12/05 Burlington Resources ConocoPhillips 36.0$

10/31/05 O2 Telefonica 33.6$

09/12/05 Ford Motor/Hertz The Carlyle Group / Clayton, Dubilier & Rice / Merrill Lynch Global Private Equity

25.1$

12/05/05 Guidant Boston Scientific 25.0$

01/31/05 AT&T SBC Communications 23.0$

08/23/05 Autoroutes du Sud de la France Vinci SA 22.9$

11/13/05 Georgia-Pacific Koch Industries 20.3$

04/21/05 Allied Domecq Pernod Ricard 18.2$

09/28/05 Millhouse Capital/Siberian Oil Gazprom 18.0$

02/28/05 May Department Stores Federated Department Stores 17.7$

04/04/05 Unocal CHEVRONTEXACO 17.6$

11/30/05 TDC TDC/Consortium led by Apax Partners 15.3$

527.7$

Top 15 Megadeals in 2005

Note: PE Deals are highlightedSource: Mergerstat

0704-0823629_MCL

15

Source: Factset*

North American Software & Services M&A Activity

*Only North American sellers in the computer software, supplies and services sector are included in the Technology M&A statistics. *Based on deals closed in a given year. *Deal size refers to target enterprise value

Tech M&A Total Deal Value vs. NASDAQ Composite

$24 $28

$145

$33$25

$39 $42

$69$65

$134

$62

$0

$20

$40

$60

$80

$100

$120

$140

$160

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 20060

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000Deal Value NASDAQ Composite

Total # of Deals 575 745 897 1592 2731 1645 1229 1167 1334 1456 1364

Ave Deal Value $MM $87 $90 $156 $197 $140 $61 $60 $103 $99 $134 $170

Tota

l Tra

nsac

tion

Valu

e ($B

) NASDAQ Composite Level

0704-0823629_MCL

16

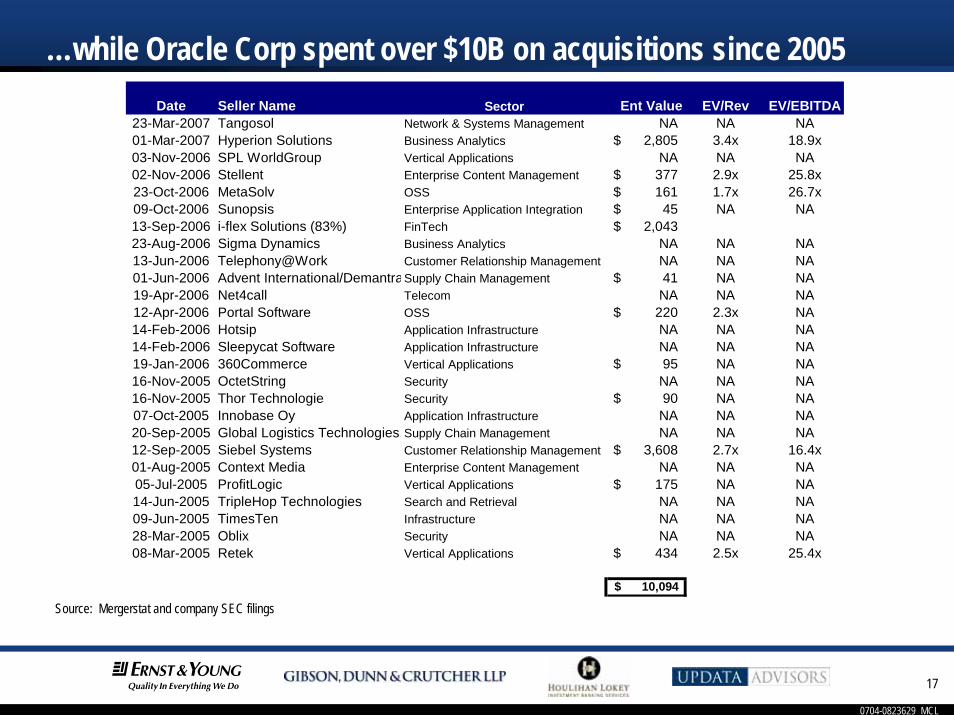

Source: Mergerstat and company SEC filings

Mega-Buyer: IBM Corp Spent Nearly $7B on Acquisitions Since 2005Date Seller Name Sector Ent Value EV/Rev EV/ EBITDA

29-Jan-2007 Softek Storage Solutions Corp. Storage NA NA NA08-Dec-2006 Ementor ASA Hardware NA NA NA05-Dec-2006 Consul Risk Management, Inc. Security NA NA NA28-Nov-2006 Vallent Corp. Application Software NA NA NA20-Oct-2006 Palisades Technology Partners FinTech NA NA NA29-Sep-2006 Valchemy, Inc. Specialty Consulting NA NA NA07-Sep-2006 Global Value Solutions SA IT Services NA NA NA23-Aug-2006 Internet Security Systems, Inc. Security 1,050$ 3$ 13$ 10-Aug-2006 FileNet Corp. Application Software 1,172$ 3$ 16$ 03-Aug-2006 MRO Software, Inc. Application Software 563$ 3$ 15$ 02-Aug-2006 Webify Solutions, Inc. Infrastructure NA NA NA18-May-2006 Rembo Technology SARL Infrastructure NA NA NA02-May-2006 BuildForge, Inc. Infrastructure NA NA NA21-Apr-2006 Unicorn Solutions, Inc. Infrastructure NA NA NA16-Mar-2006 Language Analysis Systems, Inc. Application Software NA NA NA08-Feb-2006 Viacore, Inc. IT Services NA NA NA25-Jan-2006 CIMS Lab, Inc. Application Software NA NA NA10-Jan-2006 Classic Blue IT Services NA NA NA21-Dec-2005 Micromuse, Inc. Infrastructure 743$ 5$ 36$ 20-Dec-2005 Bowstreet, Inc. Infrastructure NA NA NA16-Nov-2005 Collation, Inc. Infrastructure 46$ 9$ NA09-Nov-2005 Network Solutions Pvt Ltd. IT Services 39$ 1$ NA01-Nov-2005 iPhrase Systems, Inc. Application Software NA NA NA18-Oct-2005 DataPower Technology, Inc. Application Software NA NA NA30-Sep-2005 Adaptec, Inc. Hardware 23$ NA NA02-Aug-2005 DWL, Inc. Application Software 104$ 4$ NA19-Jul-2005 PureEdge Solutions, Inc. Application Software NA NA NA29-Jun-2005 Global Value Services Application Software NA NA NA23-Jun-2005 Meiosys, Inc. Infrastructure NA NA NA16-Jun-2005 Isogon Corp. Infrastructure 75$ NA NA10-May-2005 Gluecode Software, Inc. Application Software NA NA NA26-Apr-2005 Healthlink, Inc. Infrastructure NA NA NA14-Mar-2005 Ascential Software Corp. Application Software 938$ 3$ 30$ 02-Feb-2005 Equitant FinTech 40$ NA NA25-Jan-2005 Corio, Inc. IT Services 184$ 3$ (41)$ 07-Jan-2005 SRD, Inc. Application Software 69$ NA NA

5,045$

0704-0823629_MCL

17

Date Seller Name Sector Ent Value EV/Rev EV/EBITDA23-Mar-2007 Tangosol Network & Systems Management NA NA NA01-Mar-2007 Hyperion Solutions Business Analytics 2,805$ 3.4x 18.9x03-Nov-2006 SPL WorldGroup Vertical Applications NA NA NA02-Nov-2006 Stellent Enterprise Content Management 377$ 2.9x 25.8x23-Oct-2006 MetaSolv OSS 161$ 1.7x 26.7x09-Oct-2006 Sunopsis Enterprise Application Integration 45$ NA NA13-Sep-2006 i-flex Solutions (83%) FinTech 2,043$ 23-Aug-2006 Sigma Dynamics Business Analytics NA NA NA13-Jun-2006 Telephony@Work Customer Relationship Management NA NA NA01-Jun-2006 Advent International/DemantraSupply Chain Management 41$ NA NA19-Apr-2006 Net4call Telecom NA NA NA12-Apr-2006 Portal Software OSS 220$ 2.3x NA14-Feb-2006 Hotsip Application Infrastructure NA NA NA14-Feb-2006 Sleepycat Software Application Infrastructure NA NA NA19-Jan-2006 360Commerce Vertical Applications 95$ NA NA16-Nov-2005 OctetString Security NA NA NA16-Nov-2005 Thor Technologie Security 90$ NA NA07-Oct-2005 Innobase Oy Application Infrastructure NA NA NA20-Sep-2005 Global Logistics Technologies,Supply Chain Management NA NA NA12-Sep-2005 Siebel Systems Customer Relationship Management 3,608$ 2.7x 16.4x01-Aug-2005 Context Media Enterprise Content Management NA NA NA05-Jul-2005 ProfitLogic Vertical Applications 175$ NA NA14-Jun-2005 TripleHop Technologies Search and Retrieval NA NA NA09-Jun-2005 TimesTen Infrastructure NA NA NA28-Mar-2005 Oblix Security NA NA NA08-Mar-2005 Retek Vertical Applications 434$ 2.5x 25.4x

10,094$

Source: Mergerstat and company SEC filings

…while Oracle Corp spent over $10B on acquisitions since 2005

0704-0823629_MCL

18

Source: Updata Proprietary Tech M&A DatabasePrivate Equity deals are highlighted

Date Seller BuyerDeal Value

($B) Sector02-Apr-07 First Data Corp Kohlberg Kravis Roberts $26.2 Financial Technology23-Mar-07 Kronos Hellman & Friedman $1.8 Application Software20-Mar-07 Affiliated Computer Services Cerberus Capital $5.9 IT Services15-Mar-07 WebEx Cisco $3.2 Application Software01-Mar-07 Hyperion Solutions Oracle $3.3 Application Software14-Feb-07 TALX Equifax $1.2 IT Services12-Feb-07 Witness Systems Verint Systems $1.1 Application Software05-Feb-07 Investors Financial Services State Street Corp $4.4 Financial Technology29-Jan-07 Egg Banking Citigroup $1.1 Financial Technology29-Jan-07 Altiris Symantec $1.0 Infrastructure Software25-Jan-07 UGS Siemens $2.1 Application Software10-Jan-07 Kodak Health Group Onex Healthcare $2.4 Application Software

Megadeals: 12 Global Software & Services Deals in 2007 YTD >$1 Billion

0704-0823629_MCL

19

Source: Updata Proprietary Tech M&A Database

Date Seller BuyerDeal Value

($B) Sector20-Dec-06 Digitas Publicis Groupe $1.3 IT Services20-Dec-06 John H. Harland M&F Worldwide $1.5 Financial Technology

12-Dec-06 Sabre HoldingsSilver Lake Partners and Texas Pacific Group $4.3 Internet

07-Dec-06 Worldspan Travelport $1.4 Internet30-Nov-06 Digital Insight Intuit $1.4 Financial Technology06-Nov-06 Per-Se Technologies McKesson $1.3 IT Healthcare26-Oct-06 Kanbay Capgemini $1.3 IT Services10-Oct-06 YouTube Google $1.7 Internet26-Sep-06 Emdeon Business Services General Atlantic $1.5 IT Services01-Sep-06 Intergraph Corporation Texas Pacific Group $1.3 Application Software23-Aug-06 Internet Security Systems, Inc IBM $1.3 Security21-Aug-06 WM-data LogicaCMG $1.7 IT Services10-Aug-06 FileNet IBM $1.6 Application Software25-Jul-06 Mercury Interactive Hewlett-Packard $5.0 Infrastructure Software30-Jun-06 Travelport Blackstone Group $4.3 Internet29-Jun-06 RSA Security EMC Corporation $2.3 Security

31-May-06 West CorporationThomas H. Lee Partners and Quadrangle Group $3.3 IT Services

15-May-06 SSA Global Technologies Infor $1.4 Application Software

17-Apr-06 Flextronics Software Dev Business Kohlberg Kravis Roberts $1.1 IT Services

Megadeals: 19 Global Software & Services Deals in 2006 >$1 Billion

0704-0823629_MCL

20

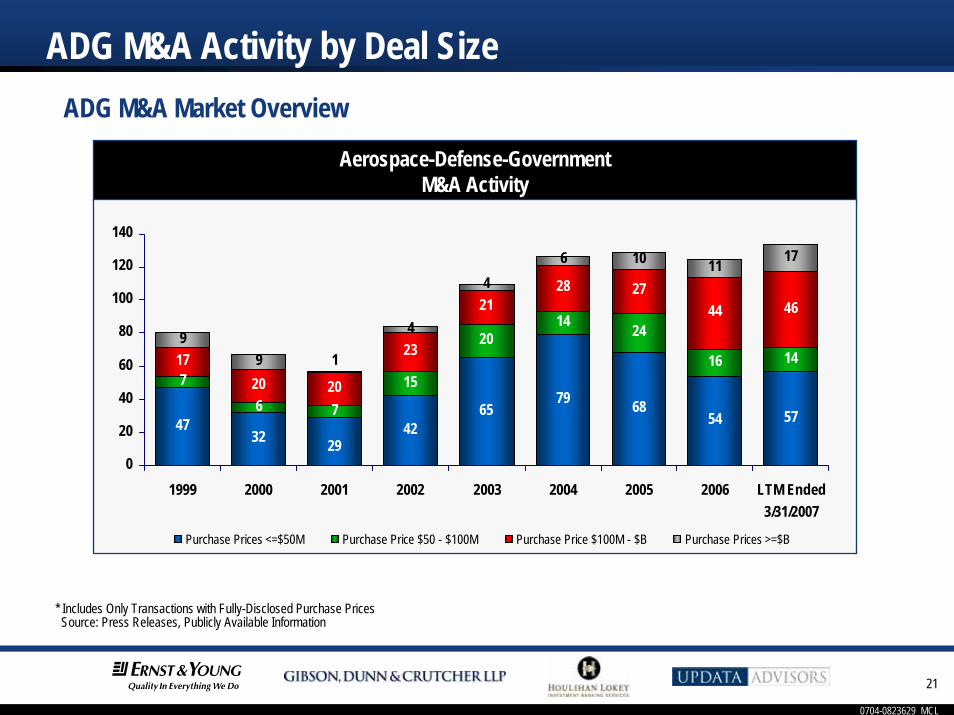

Sustained Heightened Level of ADG M&A Activity

* LTM as of March 31, 2007SOURCE: Press Releases, Publicly Available Information

ADG M&A Market Overview

Aerospace-Defense-GovernmentM&A Activity

84 77 80 87 86 110 121 12135 42 39

58 76 10298

143 12957 71

4764

7992

90

87 93

670

50

100

150

200

250

300

350

400

1999 2000 2001 2002 2003 2004 2005 2006 LTM

Aerospace Defense Government Services

176 190153

202

242280 298

351 343

0704-0823629_MCL

21

ADG M&A Activity by Deal Size

* Includes Only Transactions with Fully-Disclosed Purchase PricesSource: Press Releases, Publicly Available Information

ADG M&A Market Overview

Aerospace-Defense-GovernmentM&A Activity

4732 42

6579 68

54 57

76 7

15

2014 24

16 141720 20

23

2128 27

44 46

99

4

6 10 11 17

29

4

1

0

20

40

60

80

100

120

140

1999 2000 2001 2002 2003 2004 2005 2006 LTM Ended3/31/2007

Purchase Prices <=$50M Purchase Price $50 - $100M Purchase Price $100M - $B Purchase Prices >=$B

0704-0823629_MCL

22

2006 ADG Transaction AnalysisADG Market Dynamics

Source: Press Releases, Company Filings Source: Press Releases, Company Filings

Transactions by Buyer TypeTransactions by Buyer Type Transactions by Form of ConsiderationTransactions by Form of Consideration

Domestic Private Buyer24%

Foreign Buyer11%

Private Equity

12%

Domestic Public Buyer53%

Stock12%

Cash69%

Mixed19%

0704-0823629_MCL

23

Most Active ADG Acquirers

Source: Press Releases, Publicly Available Information

10 Most Active ADG Buyers

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46

QinetiQ

CACI

Smiths Group plc

DRS Technologies

BAE Systems

Lockheed Martin

Curtiss-Wright

General Dynamics

Cobham plc

SAIC

L-3 Communications

Number of Transactions Announced

2002 2003 2004 2005 2006 2007

ADG M&A Market Overview

0704-0823629_MCL

24

Top Government Services AcquirersADG M&A Market Overview

Source: Press Releases, Publicly Available Information

Top Government Services Acquirers

0 2 4 6 8 10 12 14

ManTech International

SRA International

MTC Technologies

CACI International

General Dynamics

BAE Systems

Alion Science & Technology

QinetiQ Group plc

SAIC

Number of Transactions2004 2005 2006 2007

0704-0823629_MCL

25

Trends in Valuation, Deal Pricing and FinancingTrends in Valuation, Deal Pricing and Financing

0704-0823629_MCL

26

Trends In AuctionsBuyers are more cautious:– Heightened level of due diligence– Buyers are becoming very selective in pursuing deals

Active M&A market:– More books, more rounds, more participants

Resulting Process Trends:– Harder to get exclusivity, if granted at all – generally requires commitment of time, money and

resources including significant diligence, contract markup– Pricing is higher and deal terms are more seller favorable– Although overall process is longer, time from selection to execution of contract is short

0704-0823629_MCL

27

2006 M&A Market HighlightsTransaction Multiples on the Rise– Enterprise Value/EBITDA transaction multiples remain well above historical averages.– Competition among private equity and strategic buyers has driven the multiples being paid for

attractive targets.

Median EV/EBITDA Multiples

Medi

an E

V/EB

ITDA

Mul

tiples

Source: FactSet Mergerstat, LLCExcludes negative EV/EBITDA multiples and multiples larger than 25.0x.

9.7x8.9x 8.7x 8.6x

7.7x 7.6x8.4x

9.9x 10.5x 10.2x

0.0x

4.0x

8.0x

12.0x

16.0x

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

0704-0823629_MCL

28

Driving Today’s M&A ActivityAbundant Capital Lowers Equity Contributions and Enhances Returns– Given the steady increase in available leverage, private equity firms have been able to reduce the

amount of equity contributed to transactions.

Average Equity Contribution to Leveraged Buyouts1997 – 2006

3.3% 3.5% 4.1% 3.9% 5.5% 2.7% 4.7% 2.7% 2.3% 2.5%

30.0% 31.7%35.7% 37.8%

40.6%40.0% 39.5%

35.1%32.1%

36.1%

0%

10%

20%

30%

40%

50%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Rollover Equity Contributed Equity

Equi

ty at

a Pe

rcen

t of T

otal

Serv

ices

Equi

ty at

a Pe

rcen

t of T

otal

Serv

ices

Source: Standard & Poor’s Q4 2006 Leveraged Buyout Review.

0704-0823629_MCL

29

2006 M&A Market HighlightsBut Acquisition Premiums have Moderated– Though transaction multiples have risen, premiums paid remain below the 1997-2001 period

Average Acquisition Premiums

32.7% 32.1%

40.8%

34.1%

24.5%30.3%

25.3%22.9%

25.4%

34.8%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Acqu

isitio

n Pr

emiu

m

Source: FactSet Mergerstat, LLCPremium is relative to target share price 4 weeks prior to announcement for deals with U.S. targets valued over $50 million.Excludes negative premiums and premiums over 100%.

0704-0823629_MCL

30

2006 M&A Market HighlightsCash Continues to be the Favored form of Consideration– High corporate cash balances, coupled with the relatively low cost and ready availability of debt

financing and the demise of “pooling-of-interests” accounting, have reduced the attractiveness of stock-for-stock deals.

M&A Consideration by Dollar Volume Activity

27% 26%18%

27% 21% 22% 24% 26% 23%

33% 30% 30%32%

27%22% 18% 18% 19%

16%

40% 44% 46% 49% 45%56% 59% 57% 55% 61%

24%0%

20%

40%

60%

80%

100%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Cash/Stock Stock Cash

Source: FactSet Mergerstat, LLC

0704-0823629_MCL

31

Size MattersLarger companies continue to be valued at a significant premium to middle-market companies

Median EV/EBITDA Multiples

Source: FactSet Mergerstat, LLCExcludes negative EV/EBITDA multiples and multiples larger than 25.0x.

8.4x9.5x

8.9x

7.7x6.9x6.9x

7.7x8.2x9.0x

8.1x

10.5x11.4x11.5x

9.2x8.3x

10.3x

8.9x9.4x10.2x

11.1x11.9x11.8x

11.4x11.1x

9.0x8.7x

11.1x10.3x

11.3x12.2x

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Under $250.0 Million $250.0 - $499.9 Million Over $500.0 Million

35.6%

37.8%27.2% 44.2%

26.1%

30.4%

44.2%

28.1% 24.2%41.7%

0704-0823629_MCL

32

ADG M&A Transaction Pricing DynamicsADG Market Dynamics

*Quartile information based on 262 ADG transactions from 1/1/01 - 3/31/2007 that disclosed pricing information

Transaction Dynamics• Targets offered access to “systems” credentials and specific programs/customers• Involvement in high percentage of classified work and/or many high level clearances• Deals involve larger and more highly-valued strategic buyers• Larger targets (rev > $100 million)• Consideration often involves stock• Targets had distinguished capabilities and/or IP• Differentiated technical depth, delivery model and solutions orientation

• Targets have focused business and often have above average growth and performance attributes

• Customer base is more varied but with some involvement in priority markets• Strong technical qualifications/technology/intellectual property• Larger percentage of cash transactions• Targets most often have had > $50 million in revenue• Predominately strategic acquisitions by larger/public buyers

• Less IT or engineering focused, more “staffing” oriented work• Smaller acquisition targets• Predominately cash or mixture cash and stock (some with earn-outs)• 8(a) and SDB companies as targets• Unrepresented sellers• Private buyers

13.4x

9.9x

8.3x

5.5x

EBITDA Multiple*

9.1x

0704-0823629_MCL

33

ADG Deal Pricing TrendsADG Market Dynamics

ADG Median EBITDA MultiplesADG Median EBITDA Multiples

7.9x

5.0x

7.8x8.3x 8.5x

0.0x1.0x2.0x3.0x4.0x5.0x6.0x7.0x8.0x9.0x

1986-1989 1990-1995 1996-1999 2000-2004 2005-Present*

EV/E

BITD

A

0704-0823629_MCL

34

ADG prices off of adjusted EBITDA ADG Buyer Pricing Driven off of EBITDA

“Adjusted” EBITDA takes into account:– Forward-looking performance (i.e. NFY/run rate)– Pro forma performance (acquisitions, discontinued ops)– Removal of non-recurring or extraordinary items

• One-time expenses• Costs eliminated post transaction (i.e. owner compensation)• Normalized expenses (i.e. R&D, marketing, etc.)

Subtract price associated strictly with tax benefits (e.g. 338(h)10)

0704-0823629_MCL

35

Transaction Size Impacts Deal PricingADG Market Dynamics

* Includes Only Fully-Disclosed TransactionsSource: Press Releases, Publicly Available Information

Median Revenue Multiples for ADG M&A Announced DealsMedian Revenue Multiples for ADG M&A Announced Deals

0.54x 0.57x0.81x 0.81x

1.04x 0.94x

1.22x1.09x

1.96x

1.39x1.19x

2.71x

1.94x

0.73x

1.22x1.16x

1.41x

0.78x

0.90x

1.22x1.00x

1.00x0.75x0.88x

1.00x1.32x

1.31x

0.97x1.19x

1.44x1.50x

1.02x1.49x

1.94x

1.29x1.18x

0.00x

0.50x

1.00x

1.50x

2.00x

2.50x

3.00x

1999 2000 2001 2002 2003 2004 2005 2006 LTM Ended4/17/2006

Purchased Price<$50M Purchase Price $50M - $100M Purchase Price $100M - $1B Purchase Price >=$1B

EV/R

even

ue

0704-0823629_MCL

36

Most Active ADG SubsectorsADG M&A Market Dynamics

January 2006 - March 2007 M&A Announcements by Subsector

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80

Land Vehicles

MOW

Federal IT

Aviation & Airport Services

MRO

ISR

Homeland Security

C4

Professional Services

Tier 3

Number of Transactions

2006 2007Source: Press Releases, Publicly Available Information

0704-0823629_MCL

37

Historical Valuation: Aerospace & DefenseADG Market Dynamics

* LTM as of March 31, 2007

10.6x 10.9x 10.9x 10.8x

6.5x

8.0x7.9x 8.1x

11.0x 10.8x10.3x

9.2x

7.9x

10.2x10.2x10.1x10.6x

9.3x

7.3x7.7x

9.3x

7.5x

8.5x

7.7x

6.6x7.1x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007*

EV/E

BITD

AEV

/EBI

TDA

Average Defense = 9.5xAverage Aerospace = 8.6x

0704-0823629_MCL

38

Historical Valuation: Federal ITADG Market Dynamics

* LTM as of March 31, 2007

EV/E

BITD

A

7.0x

9.4x 8.8x7.9x 7.5x

10.6x

13.1x14.3x 14.7x

16.2x

13.5x

10.5x9.2x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007*

Average Government = 11.0x

0704-0823629_MCL

39

Other Considerations Impact Deal Pricing338(h)10 Example

Source: Houlihan Lokey Howard & Zukin

Buyer TargetTransaction EBITDA

MultipleAdjusted “Operating”

EBITDA MultipleSRA International Galaxy 11.8x 9.6x

Mantech Gray Hawk 16.3x 12.3x

MTC Technologies Management Technology Inc. 12.5x 10.1x

Pro Forma Acquisition Example

Buyer TargetTransaction EBITDA

MultipleAdjusted “Operating”

EBITDA MultipleQinetiQ Apogen 12.5x 11.1x

0704-0823629_MCL

40

Hot M&A Sectors: US IT Deals by Sub Sector

2006 Sectors by # of Deals

2005 Sectors by # of Deals 2005 Sectors by Volume

2006 Sectors by Volume

Source: Updata Advisors Proprietary Database

Security SW6%

Fin Tech13%

Internet12% Application

SW30%

Infrastructure SW12%

Commercial IT Services

23%

Government IT Services

4% Security SW2%

Fin Tech23%

Internet13%

Application SW36%

Infrastructure SW9%

Commercial IT Services

11%

Government IT Services

6%

Security SW6%

FinTech8%

Internet12% Application

28%

Infrastructure SW14%

Commercial IT Services

28%

Government IT Services

4% Security SW7%

Fin Tech8%

Internet20%

Application SW24%

Infrastructure16%

Commercial IT Services

22%

Government IT Services

3%

0704-0823629_MCL

41

Source: Factset**Only North American sellers in the computer software, supplies and services sector are included in the Technology M&A statistics. All divestitures and minority sales are excluded. Based on deals announced in a given year

Software M&A Valuations in North America

Computer Software and ServicesMedian EV / Revenue Multiples

1.9x2.2x

3.4x

5.1x

1.6x 1.4x 1.5x 1.7x

2.5x 2.4x2.1x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

1,3641,4561,3341,1671,2291,6452,7311,592897745575

0704-0823629_MCL

42

Source: Updata Proprietary Tech M&A Database

333 68 139

262 50

146 130299 60 147

295 42

82 129278 58 129

281 37

75 150

Valuation Metrics: IT Deals by Sub Sector

Global IT: Median Transaction Multiple

4.0x 3.8x

2.0x 2.0x1.7x

1.2x0.9x

5.0x 5.0x

3.5x 3.5x

2.4x

1.5x1.2x

0.9x

5.0x 4.9x

3.8x 3.6x

2.6x

1.6x1.1x 0.9x

2.8x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

Security SW InfrastructureSW

Interne FIN Tech SWand Services

Application SW Telecom Government ITServices

Commercial ITServices

CY 2005 CY 2006 LTM Q1/07

Medi

an E

V / R

even

ue

0704-0823629_MCL

43

North America Technology Deals—Method of Payment

North America Technology Deals—Method of Payment

26%

48%

26%25%

57%

18%

0%

10%

20%

30%

40%

50%

60%

Combo Cash Stock

2005 2006

Source: FactSet*Only North American sellers in the computer software, supplies and services sector are included in the Technology M&A statistics. All divestitures and minority sales are excluded. Based on deals announced in a given year

Public Company Premiums and Methods of Payment

Source: FactSet1 Day, 5 Day and 30 Day columns represent the premium calculated based on the offer price to the target’s share price 1 day, 5 days and 30 days prior to the date the transaction was announced.*Only North American sellers in the computer software, supplies and services sector are included in the Technology M&A statistics. All divestitures and minority sales are excluded. Based on deals announced in a given year

North America Technology M&A PremiumsNorth America Technology M&A Premiums

22%

32%

26%

19%25%

21%

0%

10%

20%

30%

40%

50%

60%

1 Day 5 Day 30 Day

2005 2006

0704-0823629_MCL

44

Source: Factset*

Valuation Multiples Paid By Financial Sponsors In Software and Services

* Only North American sellers in the computer software, supplies and services sector are included in the Technology M&A statistics. * Acquisition purpose is financial. Based on deals closed in a given year.* NASDAQ composite is based on the first trading day in July.

Median EV / Revenue Multiples Paid for Computer Software and Services Companies in North America

0.8x

1.8x

1.6x

0.6x

0.9x

1.7x1.8x 1.9x

1.5x

0.0x

0.2x

0.4x0.6x

0.8x

1.0x

1.2x

1.4x1.6x

1.8x

2.0x

1998 1999 2000 2001 2002 2003 2004 2005 2006

Medi

an E

V / R

even

ue

0704-0823629_MCL

45

Sell Side StrategiesSell Side Strategies

0704-0823629_MCL

46

Sell Side StrategiesIncrease competitive tensionAvoid surprises from bidders’ diligenceControl information releaseMeet public timetables and manage shareholder expectationsLimit reps, warranties, indemnificationsOptimize Transition Services Agreement (TSA) structureStay focused on businessGet it done quicklyJudicious on who you spend time with

0704-0823629_MCL

47

Sellside DynamicAttractive valuationsAging Venture Capital portfoliosDesire to boost returns to aid fundraisingPrivate company with a need to satisfy shareholder liquidity requirements and succession and estate-planning issuesSubsidiaries of public companies that are shedding non-core operationsBusiness owners now educated as to the value of competitive processPublic companies that are better off private

0704-0823629_MCL

48

Example Sale Process TimelineAuction Process

Pre-Market Preparation

Marketing Phase I

Marketing Phase II Documentation Closing

Months 1-2 Months 2-3 1/2 Months 3-5 Months 4-7 Months 5-9

Strategy Phase & Preparation Marketing Evaluate Offers Signing Oversight & Closing

Review shareholder objectivesReview sequencing & timingConfirmatory due diligenceDevelop positioning strategyPrepare information memorandumCompile data room materialsFinalize prospective buyers list

Contact prospective buyersPrepare management presentationDistribute information memorandum to interested partiesEvaluate preliminary indications

Give management presentationsLaunch online data roomEvaluate proposalsSelect final candidatesDiligence

Final DiligenceNegotiate transactionExecute contract

HSRITARFCCFOCIClosingCFIUSFinancing

4-8 Weeks 4-6 Weeks 4-6 Weeks 1-6 Weeks 4-8 Weeks

0704-0823629_MCL

49

Sale Strategy AlternativesAuction Process

Potential StrategiesOne-Off Preemptive

3-6 MonthsControlled Auction

6-9 MonthsBroad Auction

6-9 Months

Exchange informationCommence negotiations

Develop positioning strategyPrepare targeted list of buyersMake discrete inquiriesSolicit indications of interestOrchestrate due diligenceNegotiate and close

Public announcement about alternatives explorationActive and passive approach to evaluating interest

Maximize confidentialityMay limit full value exploration

Prioritizes confidentialityFull exploration of valueEfficient, orchestrated process through transaction closeMaximize flexibility of soft terms

Employees & customers’ knowledge must be managed throughout processLarger process consumes more time and resources

0704-0823629_MCL

50

Process Overview Stages & ExampleAuction Process

Source: Houlihan Lokey Howard & Zukin

Number of Buyers Participating in Various Stages of the Deal ProcessHigh Low Mean Median

Initial Contact

Sent Teaser

Sent NDA

Sent Book

1st Round Bids

2nd Round Bids

100% 100% 100% 100%

94% 53% 76% 81%

78% 36% 62% 63%

78% 26% 45% 45%

22% 4% 12% 13%

15% 1% 4% 3%

0704-0823629_MCL

51

Preparation for SaleLong lead time planning issues– Documentation of internal controls– Audited financials– Other accounting issues– Options backdating problems– Stockholder disputes– Other litigation– Capital structure problems– Personal financial planning– Tax: 338(h)10, 380(g), NOL Transferability, Dividend vs. capital gain treatment– Assign ability of contracts

0704-0823629_MCL

52

AuctionsWhen do you organize a formal auction, and when do you take a less formal approach?

0704-0823629_MCL

53

Trends in Structuring AuctionsShortening the time frame for bids, shortening the number of rounds. What do you do when the auction is going slowly? What if the business underperforms during the sales process?How do you deal with low ball bids, contingent bids and requests for additional information?

0704-0823629_MCL

54

Sell Side Communications and InformationHow do you protect your confidential information during the sales process? How do you maintain good customer relations and employee morale during a sales process?When can the selling management team talk to a buyer about employment arrangements? If I get close with a buyer and it doesn’t go through – how do I protect my employees and my customers? How do I protect myself from this becoming a competitive intelligence exercise for others? How should I handle communications to the rank and file about what management is undertaking?

0704-0823629_MCL

55

Buy Side StrategiesBuy Side Strategies

0704-0823629_MCL

56

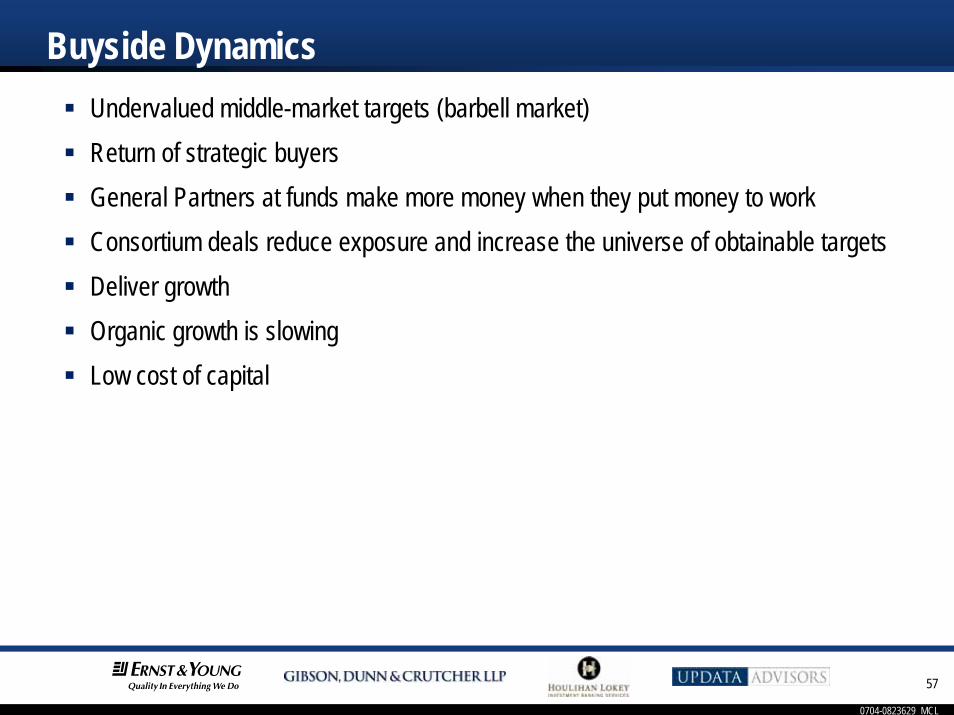

Buy Side StrategiesHighlight liabilities and risksChallenge run rates and forecastsUnderstand sustainabilityMaximize reps, warranties, indemnificationsDevelop advantage versus other biddersFocus resources on high probability outcomesEarnoutsLeave room to adjust bid

0704-0823629_MCL

57

Buyside DynamicsUndervalued middle-market targets (barbell market)Return of strategic buyersGeneral Partners at funds make more money when they put money to workConsortium deals reduce exposure and increase the universe of obtainable targetsDeliver growthOrganic growth is slowingLow cost of capital

0704-0823629_MCL

58

Short Circuiting an AuctionExclusivesShow stopper bids

0704-0823629_MCL

59

Buyside Due DiligenceBain & Company surveyed 250 senior managers with M&A responsibilities. And reported the following in November of 2006. – 50% reported that due diligence overlooked significant problems– 50% reported that targets had been dressed up– 66% overestimated the synergies available from acquisitions– Only 30% were satisfied with their due diligence process– 33% acknowledged they had not walked away from deals despite nagging doubts

Walter A. (Tony) Maull, Jr.703-747-1838

Paul Feeko703-747-1274

Steve Glover202-955-8593

Anita Antenucci703-714-1707

Greg Ager703-736-0020

2007 M&A Hot Topics Briefing2007 M&A Hot Topics BriefingBest Practices Forum – Part 2

0704-0823629_MCL

1

TopicsSlide Number

Special Public Company Issues 3

0704-0823629_MCL

2

Special Public Company IssuesSpecial Public Company Issues

0704-0823629_MCL

3

Special Public Company IssuesThe seller's board has a duty to consider offers and explore alternatives. But it does not have a duty to sell the company. Once it decides to sell, it has a duty to maximize sales proceeds. An auction is not required. But board decisions about how to structure sales process are coming under increasing scrutiny.

Duty to Auction(“Revlon duty”)

If directors decide to sell the company, they must act reasonably and on a fully informed basis to ensure that the transaction offers the greatest value reasonably obtainable for the stockholders (the “Revlon duty”). – The crux of the duty to maximize stockholder value is that the directors play a direct and active role in

investigating all reasonable alternatives, make a fully informed decision and have a reasonable basis to conclude that the selected transaction offers stockholders the greatest value reasonably obtainable for their shares.

There is flexibility in deciding best way to accomplish this:– Formal auction– Informal market check– Post-signing market check

0704-0823629_MCL

4

Special Public Company IssuesIf management will participate in a buy-out, the target company should establish a special committee to consider the proposed transaction. The special committee should control decision-making. What should the special committee do if a buyer and a management team attempt to pre-empt the process?What is the role of fiduciary outs, no shops, go shops and break-up fees? Can the buyer lock-up target stockholders in advance?

Special Committee Considerations in a Management Buy-out If the board decides to sell the company after receiving a management buy-out offer, it should consider how to make the playing field as level as possible for other interested parties.Issues to consider in this regard:– Management will likely have a head start on other bidders– Has management already signed an exclusivity arrangement?– Management change in control provisions– Management may be unwilling to work with/for other interested parties

• Management has a fiduciary obligation to assist in a sale process and to provide information, but might not have an obligation to remain employed with the company.

0704-0823629_MCL

5

Special Public Company IssuesReverse break-up fees.How should the target respond to arbitrageur and hedge fund pressure? Role of the public relations firm. How should the parties deal with the threat of litigation by stockholders? What about other litigation threats?As legal matter, obligations of private company board are very similar to those of public company board. So the same issues can come up in that context as well.

0704-0823629_MCL

6

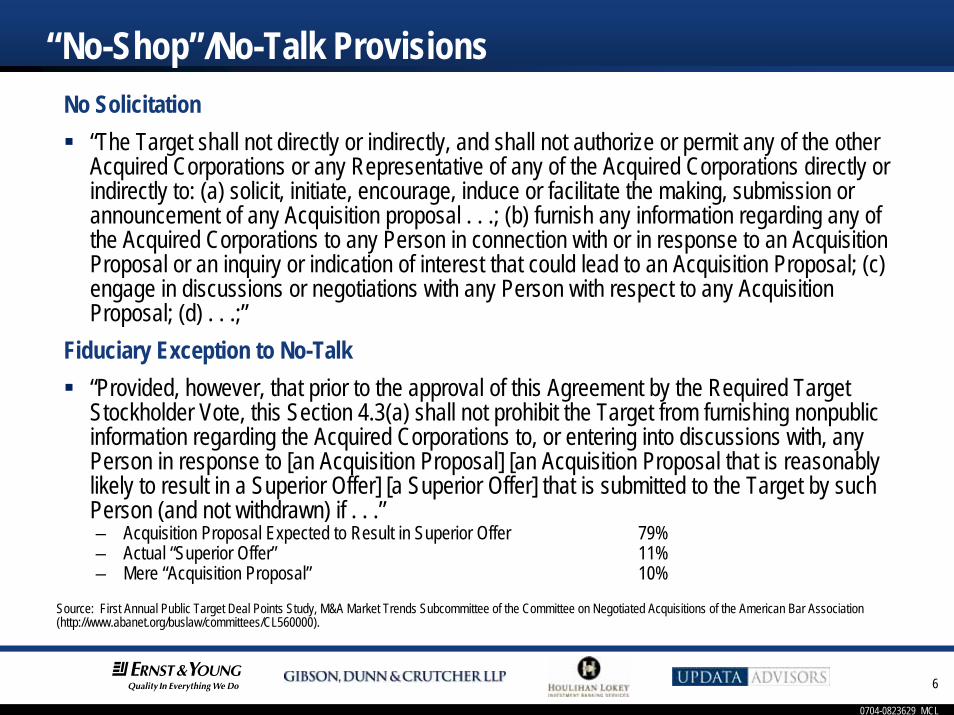

“No-Shop”/No-Talk ProvisionsNo Solicitation

“The Target shall not directly or indirectly, and shall not authorize or permit any of the other Acquired Corporations or any Representative of any of the Acquired Corporations directly or indirectly to: (a) solicit, initiate, encourage, induce or facilitate the making, submission or announcement of any Acquisition proposal . . .; (b) furnish any information regarding any of the Acquired Corporations to any Person in connection with or in response to an Acquisition Proposal or an inquiry or indication of interest that could lead to an Acquisition Proposal; (c) engage in discussions or negotiations with any Person with respect to any Acquisition Proposal; (d) . . .;”

Fiduciary Exception to No-Talk“Provided, however, that prior to the approval of this Agreement by the Required Target Stockholder Vote, this Section 4.3(a) shall not prohibit the Target from furnishing nonpublic information regarding the Acquired Corporations to, or entering into discussions with, any Person in response to [an Acquisition Proposal] [an Acquisition Proposal that is reasonably likely to result in a Superior Offer] [a Superior Offer] that is submitted to the Target by such Person (and not withdrawn) if . . .”– Acquisition Proposal Expected to Result in Superior Offer 79%– Actual “Superior Offer” 11%– Mere “Acquisition Proposal” 10%

Source: First Annual Public Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/buslaw/committees/CL560000).

0704-0823629_MCL

7

Target Fiduciary (Superior Offer) Termination Right (“FTR”)The board of a company being sold should consider whether it should have the right to terminate the purchase agreement in favor of a superior offer.

Source: First Annual Public Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/buslaw/committees/CL560000).

FTR No FTRAll Cash Public Target 86% 14%

Part Cash/Part Stock Public Target 74% 26%

All Stock 63% 37%

0704-0823629_MCL

8

Termination FeesThe purchase agreement may provide that the acquirer has the right to a termination or break-up fee if the target exercises its fiduciary out and terminates the agreement in favor of a superior offer.

Transaction Size 2004 2005$50 Million to $250 Million 3.6% 3.4%

$250 Million to $500 Million 2.9% 6.5%

$500 Million to $1 Billion 3.3% 3.2%

Over $1 Billion 3.1% 2.8%

Median Transaction Fees

Source: Houlihan Lokey Termination Fee Study

0704-0823629_MCL

9

Go-Shop Provisions“Go-Shop” provisions have been used in an increasing number of recent deals.– Buyer receives exclusivity in exchange for agreeing to a “Go-Shop” period.– Affords target 20-30 days after signing definitive agreement to find a superior offer.– Smaller break-up fee payable during the “Go-Shop” period (1/2 to 1/3 the full break-up fee).– Do they work? Private equity buyers may not want to “jump” another sponsor's deal.

0704-0823629_MCL

10

Reverse Break-Up FeesReverse break-up fees have also been used in recent transactions.– Compensates seller for a failed transaction or failure to secure funding– Increasingly common in larger/higher profile transactions– Reverse break-up fees are often tied to HSR/regulatory approval in similar industry transactions.

Walter A. (Tony) Maull, Jr.703-747-1838

Paul Feeko703-747-1274

Steve Glover202-955-8593

Anita Antenucci703-714-1707

Greg Ager703-736-0020

2007 M&A Hot Topics Briefing2007 M&A Hot Topics BriefingBest Practices Forum – Part 3

0704-0823629_MCL

1

TopicsSlide Number

Structuring and Papering the Deal 13Case Studies (discussion only)Biographies 37

0704-0823629_MCL

2

Structuring and Papering the DealStructuring and Papering the Deal

0704-0823629_MCL

3

Structuring and Papering the DealPrice adjustments and working capital adjustments Special representation and warranty problems. Defense contractors and FCPA issues. Adequacy of ownership of intellectual property. Sarbanes Oxley problems. Financial statement inadequacies. Defenses against sand-bagging. Indemnification and escrow provisions. Caps, baskets, time limitations and carve-outs. Is there really such a thing as a market standard? How is the market changing?

0704-0823629_MCL

4

Structuring and Papering the DealConditions to closing: MAC outs; HSR and antitrust issues; comfort regarding customers, suppliers. Negotiating employment arrangements with the management team. When do you lock them in? How do you deal with options and other employment benefits?How do you deal with targets that have complicated and arcane capital structures? What if it is not clear how to allocate purchase price among different classes of equity and options?

0704-0823629_MCL

5

Principal IndemnificationBuyers and sellers often debate scope of D&O indemnification. One big issue—should the buyer indemnify the target’s directors and officers directly?“Indemnification of Officers and Directors. – All rights to indemnification existing in favor of those Persons who are directors and officers of the Target

as of the date of this Agreement (the “Indemnified Persons”) for their acts and omissions occurring prior to the Effective Time, as provided in the Target’s bylaws (as in effect as of the date of this Agreement) and as provided in the indemnification agreements between the Target and said Indemnified Persons (as in effect as of the date of this Agreement) in the forms disclosed by the Target to the Buyer prior to the date of this Agreement, shall survive the Merger and shall be observed by the Surviving Corporation to the fullest extent available under Delaware law for a period of __ years from the Effective Time.

Direct Buyer Indemnity– Without limiting the foregoing provisions, during the period ending on the ___ anniversary of the Effective

Time, the Buyer will indemnify and hold harmless each Indemnified Person against and from any costs, expenses, judgments … in connection with any Proceeding … to the extent such Proceeding arises out of or pertains to: (i) any action or omission or alleged action or omission in such Indemnified Person’s capacity as a director, officer or employee of the Target or any of its Subsidiaries; or (ii) any of the transactions contemplated by this Agreement.”

*100% of the deals in the sample included some form of director and officer indemnification First Annual Public Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/buslaw/committees/CL560000).

No “Direct Buyer Indemnity” 75%Includes “Direct Buyer Indemnity” 25%

0704-0823629_MCL

6

Indemnification—BasketsTrue Deductible– Seller is only responsible for amounts exceeding the basket amount

First Dollar/Tipping Basket– Seller is responsible for all damages once the damages reach the threshold basket amount

Hybrid ApproachesExclusions– Breaches of covenants– Specific Indemnities– Fundamental representations and warranties– Fraud and intentional misrepresentation

Source: Houlihan Lokey

0704-0823629_MCL

7

Indemnification—BasketsBaskets

96% of transactions had baskets– Deductible Form 56%– First Dollar Form 38%– Hybrid 2%– None 4%

Mean basket as percentage of purchase price was 0.69% and median 0.60%

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

0704-0823629_MCL

8

Indemnification—Basket Carveouts

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

Taxes (Rep) 26%

Intentional Misrepresentation 18%

Fraud 41%

Due Authority (Rep) 11%

Capitalization (Rep) 21%

Broker’s/Finder’s Fees (Rep) 14%

0704-0823629_MCL

9

Indemnification—Caps

Yes – Less Than Purchase Price 74%

Yes, But Amount Not Determinable 14%

Silent 8%

Yes – Equal or Greater Than Purchase Price 3%

Express “No Cap” 1%

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

0704-0823629_MCL

10

Indemnification—Cap Carveouts

Taxes (Rep) 27%

Intentional Misrepresentation 28%

Fraud 77%

Due Authority (Rep) 14%

Capitalization (Rep) 26%

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

0704-0823629_MCL

11

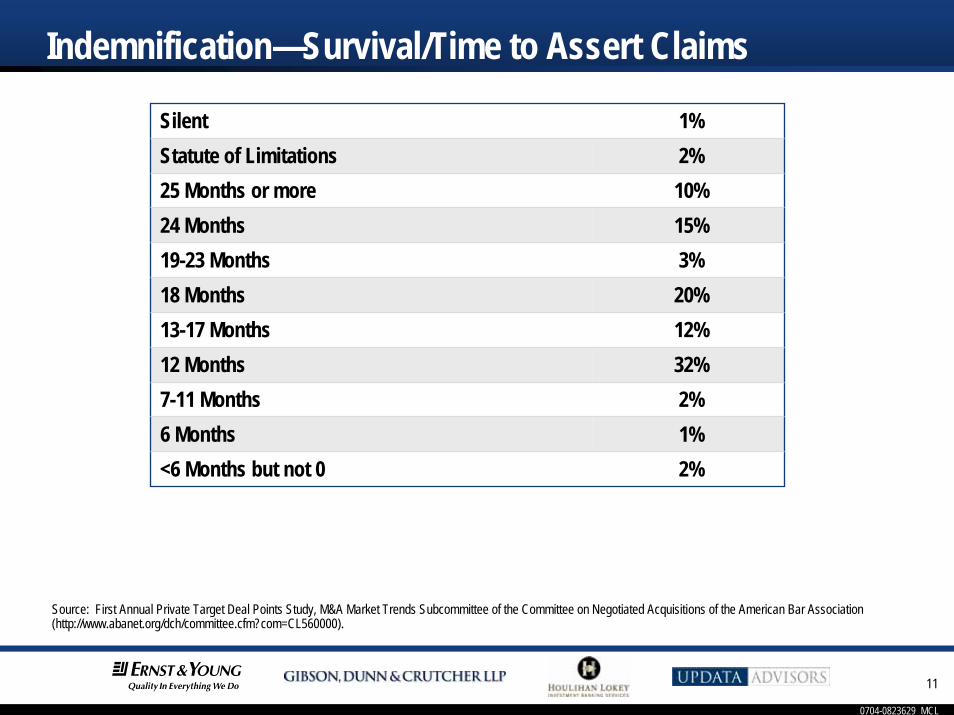

Indemnification—Survival/Time to Assert Claims

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

Silent 1%Statute of Limitations 2%25 Months or more 10%24 Months 15%19-23 Months 3%18 Months 20%13-17 Months 12%12 Months 32%7-11 Months 2%6 Months 1%<6 Months but not 0 2%

0704-0823629_MCL

12

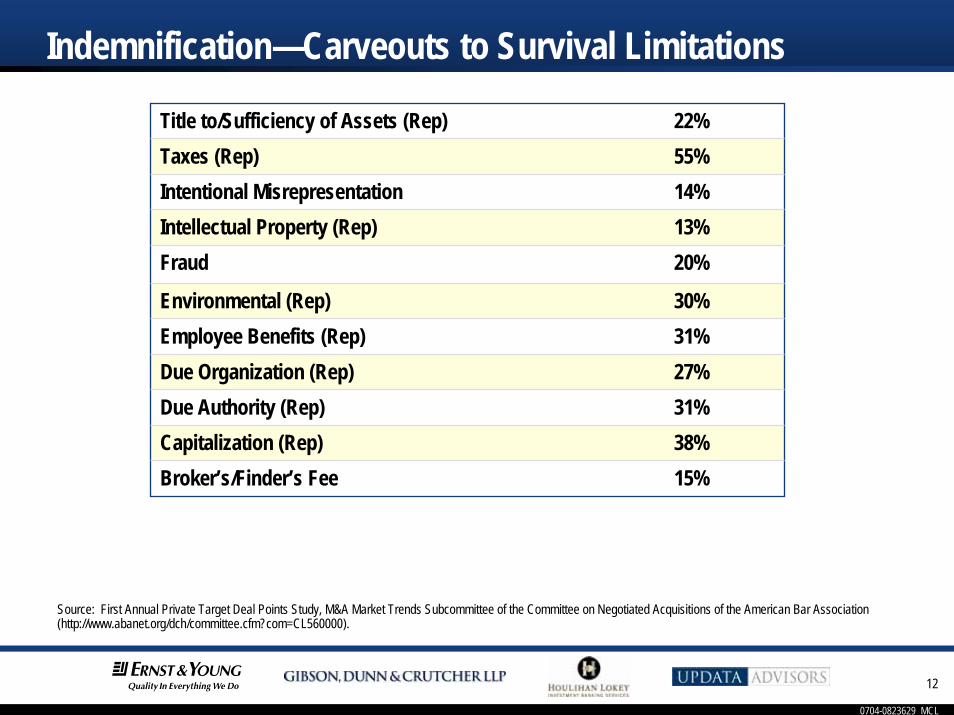

Indemnification—Carveouts to Survival Limitations

Title to/Sufficiency of Assets (Rep) 22%Taxes (Rep) 55%Intentional Misrepresentation 14%Intellectual Property (Rep) 13%Fraud 20%

Environmental (Rep) 30%Employee Benefits (Rep) 31%Due Organization (Rep) 27%Due Authority (Rep) 31%Capitalization (Rep) 38%Broker’s/Finder’s Fee 15%

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

0704-0823629_MCL

13

Indemnification—Exclusive Remedy and EscrowsHoulihan Lokey Study

74% of deals with representations and warranties surviving closing had escrowsMedian percentage of purchase price equaled 6.8%Median length of escrow agreement equaled 18 months

ABA StudyIndemnification exclusive remedy in 76% of deals (with 14% silent, 8% expressly non-exclusive and 2% redacted)

Source: [Houlihan Lokey slides;] First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

0704-0823629_MCL

14

Indemnification as Exclusive Remedy—Carveouts

Intentional Misrepresentation 29%

Fraud 85%

Equitable Remedies 27%

Capitalization (Rep) 3%

Breach of Covenant 19%

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

0704-0823629_MCL

15

Closing Conditions—Right to Walk from Deal if There Has Been a Material Adverse Change

Stand alone vs. Back-doorQuantified MACsProspectsMAC Carveouts

0704-0823629_MCL

16

Material Adverse Change (MAC) ConditionStand-Alone:

“No Material Adverse Change” (Since the Date of This Agreement, there has not been any Target Material Adverse Change)

“Back-Door”:“Absence of Changes” representation (Since the Balance Sheet Date, there has not been any Target Material Adverse Change)

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

0704-0823629_MCL

17

Frequency of Buyer’s MAC Condition

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

Stand-Alone MAC Condition 75%

“Back-Door MAC” Without Stand-Alone MAC Condition 20%

No MAC Condition 5%

0704-0823629_MCL

18

Example of MAC That Includes Quantitative Standard“Material Adverse Effect” means any change or effect that is or would reasonably be expected to be materially adverse to the assets, properties, Business, operations, liabilities, results of operation or financial condition of [Target] and its Subsidiaries, taken as a whole; including, without limitation, the occurrence prior to Closing of any single event, or any series of related events, or set of related circumstances, which could reasonably be expected to cause an actual, direct net decrease in EBITDA for either the 12 month period ending January 31, 2004 or EBITDA for any 12 month periods ending after the Closing Date but prior to the first anniversary of the Closing Date, in excess of [****] (after giving effect to any other offsetting increases or decreases affecting EBITDA); [****]

(Language from Global Imaging Systems acquisition of Imagine Technology Group)

0704-0823629_MCL

19

Example of MAC that Includes Reference to Change in Target’s Prospects

“[Target] Material Adverse Effect” shall mean any change, event, occurrence or condition which has had, or could reasonably be expected to have, individually or in the aggregate, a material adverse effect on the business, assets, liabilities, financial condition, results of operations or prospects of the [Target], taken as a whole…

(Language from CNET Networks Inc. Inc acquisition of Twofolds Photos Inc.)

0704-0823629_MCL

20

Frequency of Quantified and Prospects MAC Conditions

MAC Defined to Include Specified Dollar Amount or Other Metric (“Quantified MAC”) 8%

Includes MAC on Target’s Prospects 23%

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

0704-0823629_MCL

21

Examples of MAC Carveouts"MATERIAL ADVERSE CHANGE" means, when used in connection with a Person, any change, event, violation, inaccuracy, circumstance or effect that is materially adverse to the business, assets, liabilities, financial condition, results of operations or prospects of such Person taken as a whole, other than as a result of (i) changes generally adversely affecting the United States economy (so long as such Target is not disproportionately affected thereby) (ii) performance by such Person of its obligations under this Agreement or, with respect to [Target] only, the failure of Target to consent to actions reasonably requested by [Target] pursuant to Section 4.1 of this Agreement, (iii) the announcement or pendency of the transactions contemplated by this Agreement, or (iv) war or the outbreak of hostilities…

No MAC Carveouts 20%Includes MAC Carveouts 80%

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

0704-0823629_MCL

22

Data on Use of MAC CarveoutsNo General Economic Conditions Carveout 35%Includes General Economic Conditions Carveout 65%

Of those that include the General Economic Conditions Carveout:Disregards Disproportionate Effect 39%Does Not Disregard Disproportionate Effect 61%

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

0704-0823629_MCL

23

More Data on MAC CarveoutsNo “Industry Conditions Carveout” 41%Includes “Industry Conditions Carveout” 59%

Of those that include the “Industry Conditions Carveout”:Disregards Disproportionate Effect 45%Does Not Disregard Disproportionate Effect 54%

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000).

0704-0823629_MCL

24

Other Common MAC Carveouts

Source: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000); First Annual Public Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/buslaw/committees/CL560000).

Private Targets:Acts of war or terrorismChange in law or accounting principleDownturn in financial marketsTaking of action contemplated or required by the agreementAnnouncement of pendency of deal

17%28%30%32%44%

Public Targets:Failure to meet projectionsActs of war or terrorismChange in accountingChange in lawAnnouncement or Pendency

15%24%42%43%69%

0704-0823629_MCL

25

SOX Impact on Reps and Warranties

Sources: First Annual Private Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/dch/committee.cfm?com=CL560000); First Annual Public Target Deal Points Study, M&A Market Trends Subcommittee of the Committee on Negotiated Acquisitions of the American Bar Association (http://www.abanet.org/buslaw/committees/CL560000).

Financial Statements of Target Private PublicFair presentation of the financial position of the Company

Qualified by GAAPNot qualified by GAAPNo representation

17%84%2%

33%67%–%

Non-Audit Services 3%

Auditor Independence 4%

Off-Balance Sheet Transactions 9%

Internal Controls 32%

0704-0823629_MCL

26

Case StudiesCase Studies

0704-0823629_MCL

27

BiographiesBiographies

0704-0823629_MCL

28

BiographiesWalter A. Maull, Jr., Moderator, Director, Ernst & Young– Tony has over 20 years of finance experience with the world’s largest financial institutions. Prior to

joining E&Y, Tony was the VP of Marketing for Experian-Scorex Americas. Experian-Scorex, the technology and risk analytics arm of Experian, is a worldwide provider of software and professional services to over 2,000 financial services companies across 63 countries. Tony was responsible for the identification and integration of acquisitions and the comprehensive go to market strategy of the combined organizations. Prior to Experian-Scorex, Tony was with CIBC World Markets in their Technology Investment Banking Group where he led CIBC’s expansion into the Southeast. He focused on mid to late stage enterprise software and outsourced business services equity financing and mergers and acquisitions. Tony earned his BS in Accounting from George Mason University.

Greg Ager, Partner, Updata Advisors– Greg has 17 years of investment banking experience, having completed approximately 60 transactions

aggregating over $7 billion in value for emerging and middle market technology companies. Prior to joining Updata Advisors, Greg was the senior East Coast Technology Investment Banker at Wachovia Securities, Managing Director and Head of East Coast Software, where he completed transactions for clients such as Computer Associates, INFOR Global Solutions, Aspen Technology, Safeguard, Unica, Blackbaud and Vocus. Previously, Greg spent ten years in Silicon Valley where he completed transactions for many industry leaders including Oracle, Novell, Silicon Graphics and AnswerThink. Prior to joining TWP, Greg held various roles with the Business Services Investment Banking Group at Montgomery Securities, and with the technology investment banking groups at Smith Barney and Morgan Stanley. Greg received an M.B.A. from the J.L. Kellogg Graduate School of Management at Northwestern University and a B.A. in economics and political science from Yale University.

0704-0823629_MCL

29

BiographiesAnita M. Antenucci, Managing Director Washington, D.C. office, Houlihan Lokey– Anita is co-head of the Aerospace•Defense•Government (ADG) industry group and head of its

Aerospace and Defense segment. Over the past thirteen years, a period of significant consolidation in the aerospace and defense industries, she has grown a leading middle-market practice in aerospace and defense mergers and acquisitions. Her transactional experience has spanned the industry’s diverse makeup, with multiple transactions in such segments as defense electronics, aircraft systems, combat vehicles, satellite manufacturing, and engineering services. Her client base has included the industry’s leading prime contractors, as well as dozens of small and mid-sized companies in the industry’s second and third tiers. Prior to joining Houlihan Lokey, Anita served as co-President and Managing Director of Quarterdeck Investment Partners, LLC. Anita holds degrees from the School of Advanced International Studies (SAIS) of The Johns Hopkins University and from Northwestern University in the United States and studied at the Institut d’Etudes Politiques in France.

Paul Feeko, Partner & TAS Leader for the Mid-Atlantic– Paul is a CPA with over 20 years experience. E&Y’s TAS group includes over 70 full-time transaction

professionals in disciplines such as due diligence, transaction tax and valuation. He has also led Ernst & Young’s TAS services to The Carlyle Group since joining the firm in 2002. Prior to joining Ernst & Young, Paul led local transaction support practices at Arthur Andersen and PwC. He has been a full-time transaction support professional since 1995. Prior to that he was with the audit practice of Coopers & Lybrand, where he specialized in public company filings and registrations. Paul has significant experience in transactions across a wide range of industries including services, manufacturing and distribution industries, real estate and hospitality, telecommunications and technology, media and publishing, engineering and communications, and aerospace/defense. He has assisted in all phases of the transaction process, including strategy and development, identifying acquisition candidates or potential buyers, conducting business reviews, evaluating proposed structures and financing alternatives, pricing, negotiating and documenting transactions. Paul received a B.A. in Accounting from Penn State.

0704-0823629_MCL

30

BiographiesStephen I. Glover, Partner, Gibson, Dunn & Crutcher LLP– Steve has an extensive practice representing public and private companies in complex mergers

and acquisitions, joint ventures and other corporate transactions. His clients include large, nationally recognized public companies; locally based companies that are active participants in the mergers and acquisitions market; and private equity groups. The transactions involve many different industries and include both domestic and cross-border deals. Steve was named by the 2006 International Financial Law Review as a Leading Lawyer in US Mergers & Acquisitions. He was also identified among "Ten of the D.C. Area's Top Deal-Making Attorneys" by Legal Times in 2006, was selected as the top Commercial/Corporate Transactions attorney in Washington, D.C. by The Washington Business Journal in 2004, and was ranked one of the top three corporate/commercial transactions attorneys in the District of Columbia by Chambers USA America’s Leading Business Lawyers in both 2006 and 2005. Steve served as a law clerk to Justice Thurgood Marshall in the United States Supreme Court and to J. Skelly Wright, Chief Judge of the U.S. Court of Appeals for the District of Columbia Circuit. He earned his law degree cum laude from Harvard Law School, and received his undergraduate degree summa cum laude from Amherst College.