Embed Size (px)

Citation preview

2006 Deloitte Tax Case Study Competition National Case

From the moment they met in 1990, Pablo Garcia and Linda Smith made a great team. Pablo had the skill set to refurbish anything. He was a licensed electrician with the mindset of an inventor. Show him something that was broken, and he would come up with a way to fix it. Linda had an undergraduate degree in engineering and a Masters degree in Business Administration. She worked as a project manager for the Kitchen Electronics division of Maypoint Industries, Inc., an international, appliance manufacturing firm. She also owned a 5% limited interest in the Smith Family Limited Partnership, which is an operating cattle ranch in Texas. In 1993, the couple married. They decided the best use of their combined talents was to own and operate a residential rental real estate property. On the advice of their accountant, Joe Blackstone, the Garcia’s formed Garcia Commons, GP, with a $500,000 capital contribution. The partnership used this cash to help purchase “Garcia Estates” – a 100-unit garden apartment complex near the waterfront in Sacramento, California. Pablo and Linda are equal owners of the general partnership. (The Garcia’s home state of California adopted its Limited Liability Company statute in 1994. In today’s world, this entity would probably have converted to LLC status by now. However, as the Code and Regulations do not directly address all LLC issues, this entity remains a general partnership for the purposes of this case study.) Pablo spent most of his time working at the property – it seemed he was always fixing something, helping a tenant, or overseeing a work crew on the premises. Linda continued to work at Maypoint, and in the evenings she handled the finances and marketing for the property. By 2004, some of the Garcia Commons buildings needed renovation. There was substantial equity in the property – values in the Sacramento area had experienced several growth spurts during the 1990s and early 2000s. In August 2004, the partnership borrowed $6,000,000 on a non-recourse basis from Southwestern Savings Bank. The partnership used $2,000,000 of the loan proceeds to pay off existing qualified and nonqualified non-recourse financing. Garcia Commons used $2,000,000 of the new debt to fund the renovation of the property. And the partnership distributed the last $2,000,000 of the loan proceeds to Pablo and Linda who used the cash to purchase a 10-acre country estate, complete with a small organic fruit orchard, olive trees, and two acres of Chardonnay grape vines. On Christmas Day in 2004, a tenant in Garcia Estates caused a kitchen fire while heating oil to deep fry a turkey. The fire completely destroyed the building, displacing eight families. While the fire fighters were still cleaning up, Pablo helped those people affected

Copyright 2006© Deloitte Development LLC All Rights Reserved.

2

by the fire move into temporary quarters in a newly renovated building on the premises. Linda found bedding, clothing, and other essentials for the displaced tenants – not to mention toys for the children who had lost their Christmas presents in the blaze. Linda’s fellow employees at Maypoint donated a substantial portion of the contributed items. One Friday afternoon in March 2005, Pablo and Linda were driving to look at an apartment complex they wanted to acquire. Jeremy Jones, CEO of one of the town’s largest companies, had just returned from an exhausting overseas business trip. Jeremy fell asleep at the wheel, crossed the median, and hit the Garcia car head-on. Pablo was killed instantly and Linda was seriously injured. After enduring several surgeries, Linda survived and after several months was able to return to work at Maypoint. Linda received life insurance proceeds of $250,000 from an insurance policy on Pablo’s life. In April 2005, Linda’s attorney notified her that the insurance company for Mr. Jones had made a settlement offer for Linda’s injuries, suffering, and the loss of Pablo. Based on the attorney’s advice, Linda accepted the $2,500,000 offer. Once the pain from her injuries and the shock of losing Pablo subsided, Linda realized she needed to decide what she wanted to do in her new life. She enjoyed her work at Maypoint. However, Pablo had been the caretaker of the properties, and Linda knew she didn’t have the skill, expertise, or desire to devote all her time to the real estate. She decided to hire a management company to take care of the day-to-day activities at the apartment complexes. She started thinking about owning a business interest that would occupy her mind and that would make use of her engineering talents. In a grief counseling seminar, Linda met a business operations consultant, Marcus Green, who had recently lost his wife after a long battle with cancer. Marcus helped Linda decide that she wanted to own and operate a business in the kitchen appliance industry. Marcus had operated a number of businesses in the past, and had a knack for finding troubled companies and turning them into successful ventures. Linda decided she liked the challenge of buying a “turnaround” company with an existing customer base and product line, rather than trying to start a business “from scratch.” With the lawsuit settlement money and the life insurance proceeds from Pablo’s death, she knew she would have enough cash in hand to interest a potential seller, although not necessarily enough to buy a business outright. Marcus located a subchapter C Corporation called Kitchen Gizmos. The company made various machines for use in the kitchen--from mixers and bread makers to espresso machines. The previous owners were ready to retire and had not pursued development of new and innovative products for the past several years. Linda saw potential for expanding Gizmos’ product line to include new high tech appliances, such as computerized refrigerators and diffusion stoves.

Copyright 2006© Deloitte Development LLC All Rights Reserved. .

3

Negotiations hit a snag at an early stage. After adding up all the costs of buying the business, it became apparent that Linda would have to finance a large part of the purchase. “Or you have to find another investor to join you,” Marcus commented. Linda looked up from the counteroffer she was reading and said, “Yes, you have the skill, the interest, and enough money.” She smiled and pleaded, “You aren’t managing a business now. We should do this together.” At first Marcus protested, but together they realized there were advantages from both a business and personal perspective. The two had become good friends and wanted to continue to work together. They decided to each buy 50% interests in Kitchen Gizmos, Inc. Marcus would manage the financial operations. Linda would continue to work at Maypoint, but would gradually phase out of that company, so she could focus on product development for the new company. The New Kitchen Gizmos, Inc. took off like a rocket. By early 2006, Marcus and Linda were keeping the plant operating around the clock to meet demand. In some stores, there were waiting lists for the new appliances, as the number of customers exceeded the supply. In early fall 2007, Linda and Marcus agreed to reward the employees for their hard work by holding a company retreat. They decided to hold the event at Linda’s country estate. The caterers would use the kitchen for food preparation and the vineyard and pool area to host the various activities. Linda planned an event that was sure to leave the “Gizmo” employees inspired and motivated to make the company even more successful the next year. A few days before the event, Marcus asked Linda if they could make an announcement at the awards ceremony that would be held during the retreat. They were working late to fix a piece of equipment that had malfunctioned. Linda and Marcus were both covered in oil and dust, when Marcus laughed and said, “We really should make plans to stay together. Who else would have us?” Linda just grinned, smiled shyly, and didn’t say, “No.”

Copyright 2006© Deloitte Development LLC All Rights Reserved

4

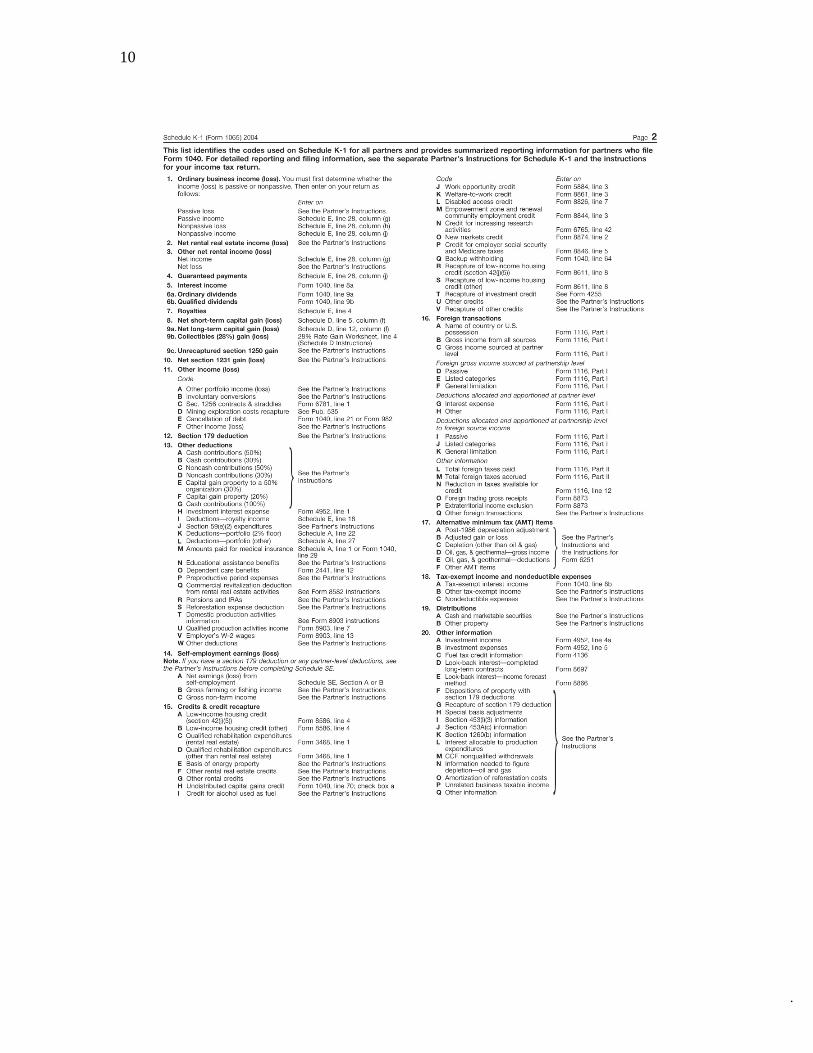

Requirements NOTE: Unless otherwise indicated, assume that tax law currently in effect applies during the time indicated in the requirement. Also assume each requirement is independent of the other requirements, and the events occur chronologically in the order in which the requirements are presented. Requirement 1. Describe the general limitations (without making any calculations), under §§465, 469 and 704(d) as they relate to deduction of losses from a partnership or limited liability company. Indicate the order in which those limitations are applied. For this requirement (only), ignore any exceptions to the rules and DO NOT address Pablo and Linda’s personal situation. Specify whether each limitation applies to a specific activity or overall to the taxpayer’s combined activities. Requirement 2. Calculate Pablo’s basis and amount at risk in Garcia Commons as of December 31, 2003 and 2004. Show your calculations and explain your rationale. Are any losses suspended at the end of each year? If so, under what provisions are they suspended? When can they be utilized? Assume all income, deductions, liabilities, and distributions are allocated equally between Pablo and Linda and that all contributions were made equally by the partners. Requirement 3. Garcia Commons, GP, distributed $1,000,000 each to Pablo and Linda during the current year. How is this distribution taxed to the partners? What is the effect on the partnership? Requirement 4. On a joint tax return, how is Pablo’s share of income and losses from Garcia Commons treated under §469? Describe, in detail, the rules that apply. Calculate the amount of allowed losses from the property for 2004. Requirement 5. On a joint tax return, how is Linda’s share of income and losses from Garcia Commons treated under the rules of §469? How are the items from the Smith Family Limited Partnership treated?

Copyright 2006© Deloitte Development LLC All Rights Reserved. .

5

Requirement 6. In today’s business world, it is typical for real estate to be owned by a limited liability company rather than by a Subchapter S corporation or a Subchapter C corporation. Describe the advantages and disadvantages of LLC status vs. Subchapter C or Subchapter S status. Why might an LLC be preferred for real estate ownership? Requirement 7. Draft a letter from Joe Blackstone to the Garcias describing the tax treatment of the Garcia Estates fire loss, receipt of insurance proceeds, and construction of the new building on the same site as the old building. Discuss the calculation of the basis in the new property. The Garcia’s are knowledgeable clients, so be sure to provide citations for your response. Requirement 8, Graduate students only. Answer these additional questions related to the replacement of the building destroyed in the fire. How would your calculation in the last question have changed if the destroyed building had been a (separate), passive activity with a $30,000 suspended passive activity loss carryover? Assume there are no other passive income or loss items that year. What would be the basis in the new building? In general, how is depreciation calculated for the new building? Requirement 9. What are the tax consequences to the individuals displaced by the fire? What tax deductions are available to the employees at Maypoint for donating clothing and other items to the victims? How do the fire victims treat the property they received from the Maypoint employees? Requirement 10. Describe, in general, how the estate tax is calculated. How are Pablo’s assets valued in an estate tax return? What additional information might be needed? What is the basis of the property in the hands of the beneficiary of the estate? Provide citations for your answers. Requirement 11, Graduate students only. How would Pablo’s estate tax calculation and Linda’s basis in assets change if Pablo died in 2010?

Copyright 2006© Deloitte Development LLC All Rights Reserved

6

Requirement 12. Discuss the tax consequences to Linda of the insurance settlement she receives as a result of Pablo’s death. Also discuss taxation of the $250,000 of life insurance proceeds. Requirement 13, Graduate students only. Assume Pablo’s will (and the partnership agreement) provided that Pablo’s partnership interest would be transferred to Linda at his death. What effect does the transfer to Linda have on the continuation of the partnership? What if the will transfers the interest to Pablo’s estate and then the Estate (several months later) sells the interest to a third party? Only address whether or not the partnership continues in existence and ignore collateral issues. Answer for three time periods and situations: 1) a transfer directly from Pablo to Linda, 2) a transfer from Pablo to his Estate, and 3) a sale from the Estate to a third party. Requirement 14. Linda and Marcus could offer to purchase either the stock or the assets of Kitchen Gizmos. Discuss the tax and business consequences of each option. Requirement 15. For the Kitchen Gizmos, Inc. fiscal year that ends June 30, 2007, calculate the following amounts related to the domestic production activities deduction using the simplified deduction method of Reg. §1.199-4:

• Qualified Production Activities Income • Wage limitation amounts used in calculating the manufacturing deduction • The allowable domestic production activities deduction under §199

Use the information provided in the July 6, 2007 letter from Linda Garcia to Joe Blackstone, CPA. Assume Kitchen Gizmos will have taxable income of $1,000,000 before this deduction. Requirement 16. Discuss the filing options that Linda asked about in her letter of November 15, 2007, and respond to her questions. The IRS issues inflation-adjusted tax tables in a Revenue Procedure each year. Refer to the 2006 Individual tax rate schedule for more information (at this writing, 2007 rates are not available).

Copyright 2006© Deloitte Development LLC All Rights Reserved. .

7

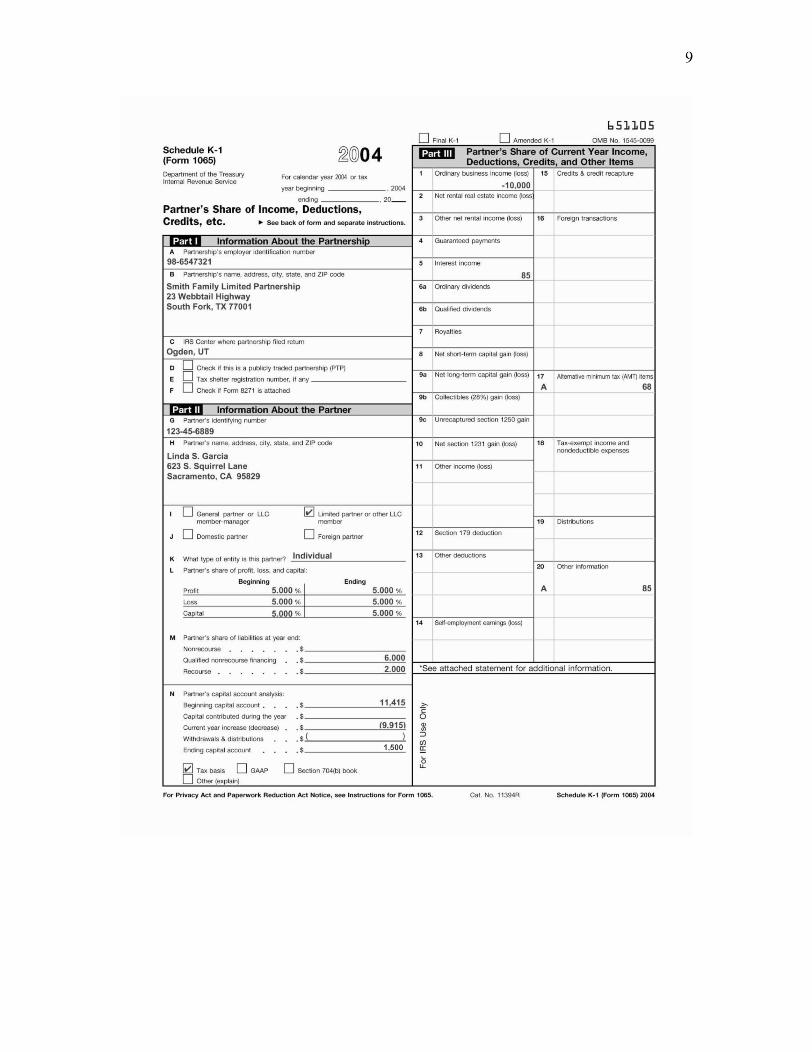

Pablo & Linda Garcia ♦ 623 S. Elk Grove Road ♦ Vineyard, CA 95829 December 20, 2004 Mr. Joe Blackstone, CPA 123 N. Western Drive Sacramento, CA 95814 Dear Joe: Linda gave me your message about needing to know how many hours we spend working for Garcia Commons. I kept a mileage log, as you have suggested in the past, but I didn’t record my hours. I spend most of my day at one building or another, handling repairs and maintenance requests, cleaning up after storms, and doing normal management work.. I would guess that I work at least seven hours each day, plus some time on the weekend. This is a full time job, so I’m sure I spent well over 2,000 hours during 2004 working at the property. If I need to track my time better, let me know. As for Linda, we estimate that she spends less than 10 hours a month working on the books and other related tasks for the partnership. We rarely have turnover these days, so she doesn’t have to advertise to find new tenants, and we have an on-site property manager who handles rent receipts and pays day-to-day expenses. Linda basically oversees the property manager. She compares rent deposits to the rent rolls, reviews and approves expenses, approves new tenants, and prepares monthly financial statements. You, of course, prepare all payroll and other tax returns. Linda’s tasks are very important to our success, but they don’t require a lot of time. And with her full time job at Maypoint, she wouldn’t have a lot of extra time anyway. My guess is that she probably works less than 100 hours a year on managing the property. We hope this information helps – let us know if there’s anything else you need. We appreciate your help in figuring out our taxes, and, as always, thank you for your efforts in keeping them as low as possible! Sincerely, PABLO Pablo Garcia

Copyright 2006© Deloitte Development LLC All Rights Reserved

8

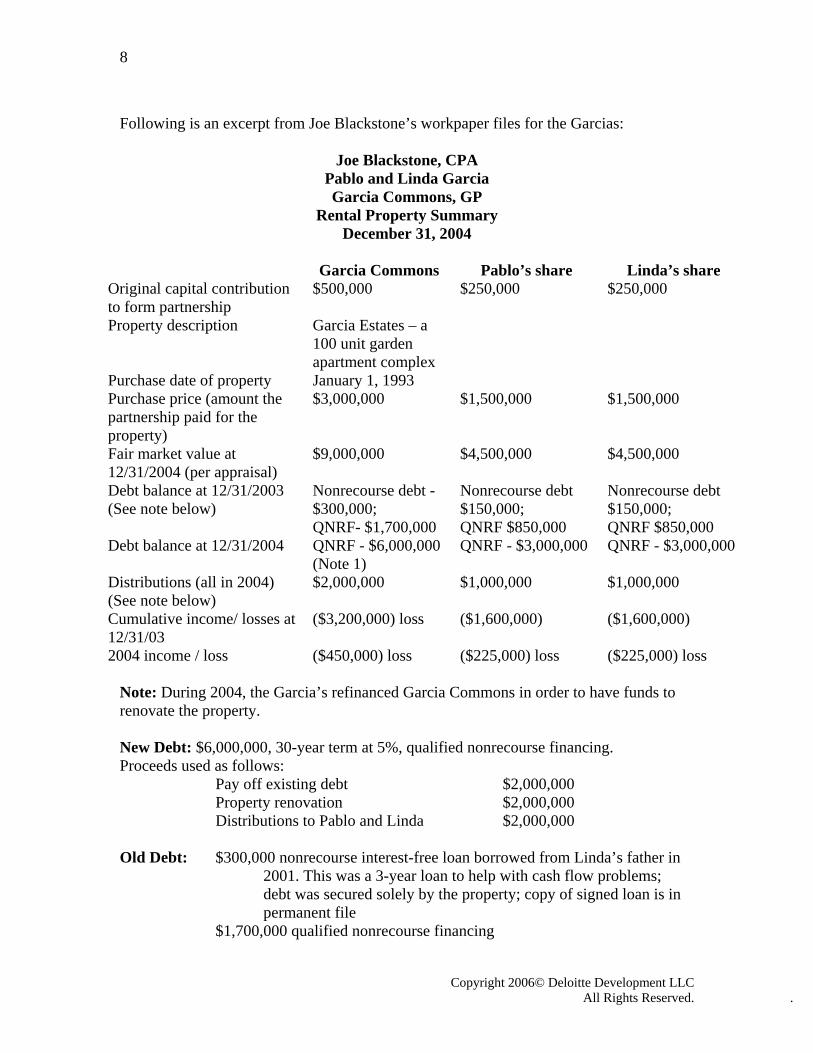

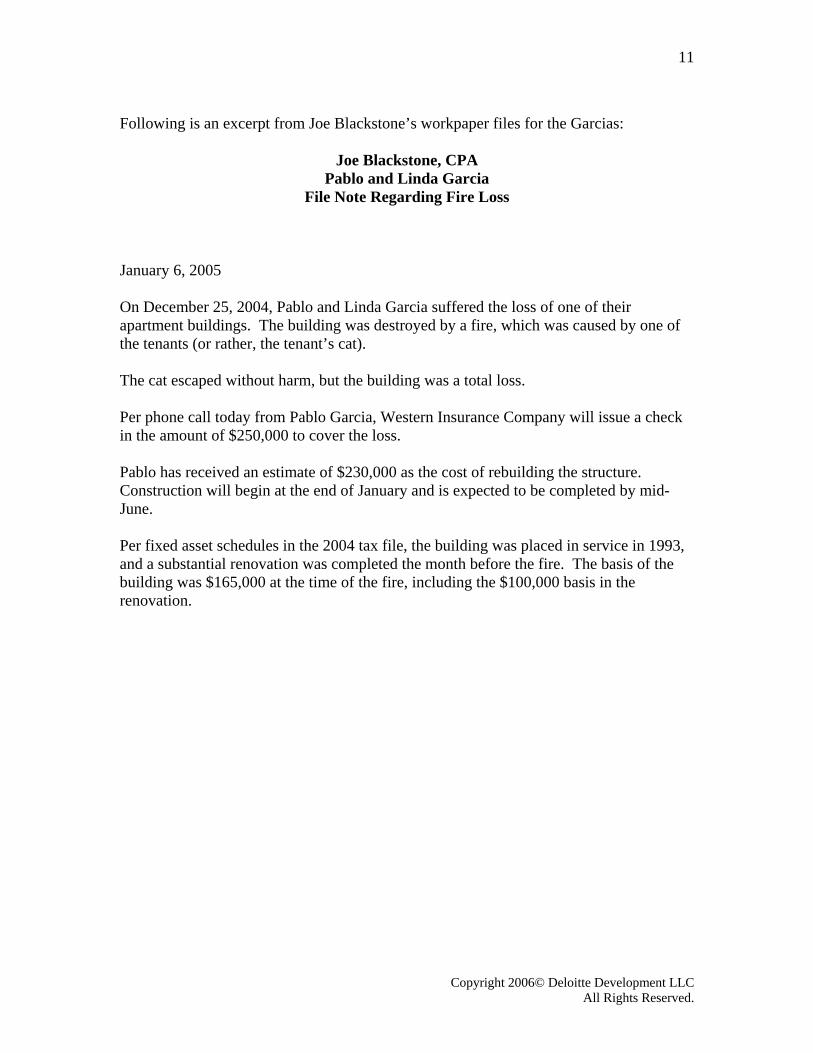

Following is an excerpt from Joe Blackstone’s workpaper files for the Garcias:

Joe Blackstone, CPA Pablo and Linda Garcia Garcia Commons, GP

Rental Property Summary December 31, 2004

Garcia Commons Pablo’s share Linda’s share Original capital contribution to form partnership

$500,000 $250,000 $250,000

Property description Garcia Estates – a 100 unit garden apartment complex

Purchase date of property January 1, 1993 Purchase price (amount the partnership paid for the property)

$3,000,000 $1,500,000 $1,500,000

Fair market value at 12/31/2004 (per appraisal)

$9,000,000 $4,500,000 $4,500,000

Debt balance at 12/31/2003 (See note below)

Nonrecourse debt - $300,000; QNRF- $1,700,000

Nonrecourse debt $150,000; QNRF $850,000

Nonrecourse debt $150,000; QNRF $850,000

Debt balance at 12/31/2004 QNRF - $6,000,000 (Note 1)

QNRF - $3,000,000 QNRF - $3,000,000

Distributions (all in 2004) (See note below)

$2,000,000 $1,000,000 $1,000,000

Cumulative income/ losses at 12/31/03

($3,200,000) loss ($1,600,000) ($1,600,000)

2004 income / loss ($450,000) loss ($225,000) loss ($225,000) loss Note: During 2004, the Garcia’s refinanced Garcia Commons in order to have funds to renovate the property. New Debt: $6,000,000, 30-year term at 5%, qualified nonrecourse financing. Proceeds used as follows: Pay off existing debt $2,000,000 Property renovation $2,000,000 Distributions to Pablo and Linda $2,000,000 Old Debt: $300,000 nonrecourse interest-free loan borrowed from Linda’s father in 2001. This was a 3-year loan to help with cash flow problems; debt was secured solely by the property; copy of signed loan is in permanent file $1,700,000 qualified nonrecourse financing

Copyright 2006© Deloitte Development LLC All Rights Reserved. .

10

.

11

Following is an excerpt from Joe Blackstone’s workpaper files for the Garcias:

Joe Blackstone, CPA Pablo and Linda Garcia

File Note Regarding Fire Loss January 6, 2005 On December 25, 2004, Pablo and Linda Garcia suffered the loss of one of their apartment buildings. The building was destroyed by a fire, which was caused by one of the tenants (or rather, the tenant’s cat). The cat escaped without harm, but the building was a total loss. Per phone call today from Pablo Garcia, Western Insurance Company will issue a check in the amount of $250,000 to cover the loss. Pablo has received an estimate of $230,000 as the cost of rebuilding the structure. Construction will begin at the end of January and is expected to be completed by mid-June. Per fixed asset schedules in the 2004 tax file, the building was placed in service in 1993, and a substantial renovation was completed the month before the fire. The basis of the building was $165,000 at the time of the fire, including the $100,000 basis in the renovation.

Copyright 2006© Deloitte Development LLC All Rights Reserved.

12

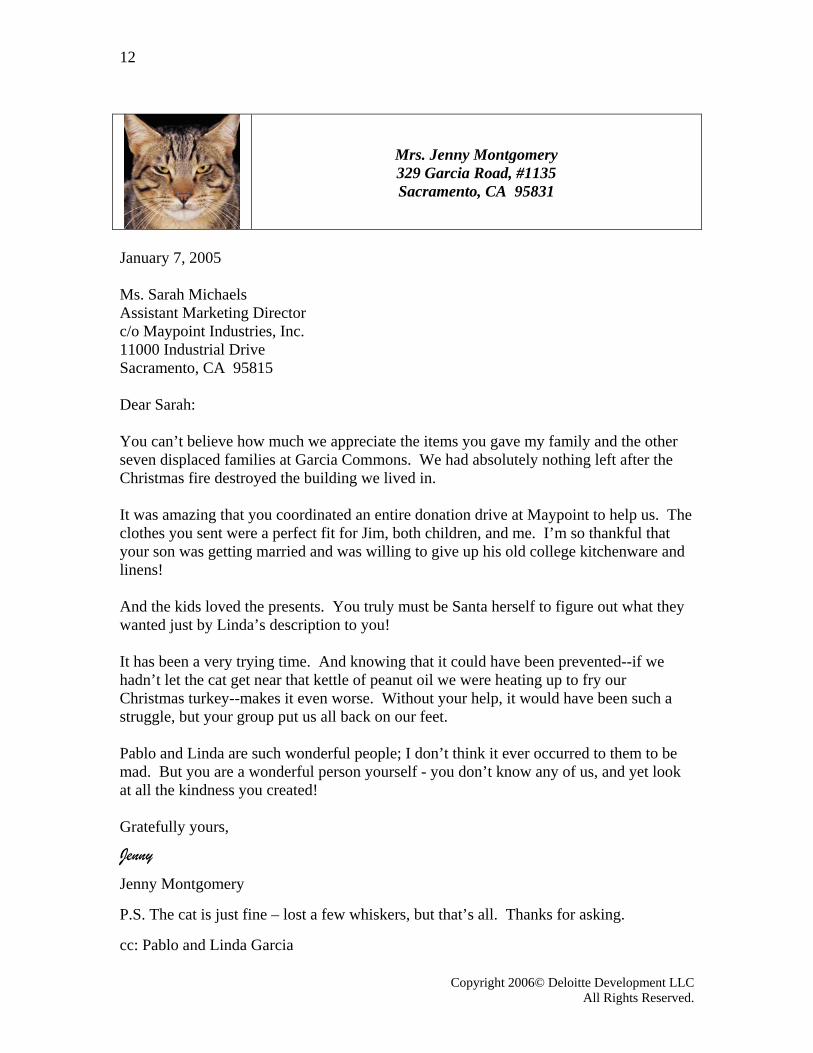

Mrs. Jenny Montgomery 329 Garcia Road, #1135 Sacramento, CA 95831

January 7, 2005 Ms. Sarah Michaels Assistant Marketing Director c/o Maypoint Industries, Inc. 11000 Industrial Drive Sacramento, CA 95815 Dear Sarah: You can’t believe how much we appreciate the items you gave my family and the other seven displaced families at Garcia Commons. We had absolutely nothing left after the Christmas fire destroyed the building we lived in. It was amazing that you coordinated an entire donation drive at Maypoint to help us. The clothes you sent were a perfect fit for Jim, both children, and me. I’m so thankful that your son was getting married and was willing to give up his old college kitchenware and linens! And the kids loved the presents. You truly must be Santa herself to figure out what they wanted just by Linda’s description to you! It has been a very trying time. And knowing that it could have been prevented--if we hadn’t let the cat get near that kettle of peanut oil we were heating up to fry our Christmas turkey--makes it even worse. Without your help, it would have been such a struggle, but your group put us all back on our feet. Pablo and Linda are such wonderful people; I don’t think it ever occurred to them to be mad. But you are a wonderful person yourself - you don’t know any of us, and yet look at all the kindness you created! Gratefully yours,

Jenny

Jenny Montgomery P.S. The cat is just fine – lost a few whiskers, but that’s all. Thanks for asking. cc: Pablo and Linda Garcia

Copyright 2006© Deloitte Development LLC All Rights Reserved.

13

Mr. Mathew Dillon, Esq.

10045 N. 74th Street Sacramento, CA 95819

April 20, 2005 Mr. Joe Blackstone, CPA 123 N. Western Drive Sacramento, CA 95814 Dear Mr. Blackstone: Linda Garcia said you requested an accounting of the assets in her late husband’s estate. Following is a list of the assets along with the value at the date of Pablo’s death. Separately owned property:

• Cash and money market accounts $650,000 • IRA and other retirement accounts ($0 basis) 350,000 • 2002 Chevy Silverado pickup truck 35,000 • Various personal effects and jewelry 15,000 • Life insurance policy 250,000

Jointly owned property:

• Garcia Commons, GP, net of outstanding mortgages $3,000,000 • Personal residence, including orchards and vineyard 2,100,000

Under Pablo’s will, his entire estate was transferred to Linda, except for a donation to his alma mater university in the amount of $50,000. Linda is the designated beneficiary of Pablo’s retirement accounts and life insurance policy. In addition, Linda asked me to inform you that she has agreed to settle the case from the accident. I expect to receive the check from the insurance company later this week, and once it clears I will be issuing the net proceeds to Linda. I am attaching a copy of my letter setting forth the terms of the settlement offer for your files. Please contact me if I can be of further assistance in this matter. Very truly yours,

Matt Mathew Dillon, Esq.

Copyright 2006© Deloitte Development LLC All Rights Reserved.

14

Mr. Mathew Dillon, Esq.

10045 N. 74th Street Sacramento, CA 95819

April 12, 2005 Mr. Mitchell S. Smyth, Esq. Goldwater and Oswald 1 S. New Haven Ave. Sacramento, CA 95819 Dear Mitch: This letter outlines the terms of the Garcia settlement we discussed last week. Under our proposal, Global Universal Insurance will pay to the Mathew Dillon, Esq. Trust Account the sum of $2,500,000. This amount will represent the following items.

• $800,000 payment to Linda for her physical injuries as a result of the accident

• $150,000 payment to reimburse Linda for her treatment for emotional distress resulting from the accident and Pablo’s death. $50,000 of this is to reimburse Linda for medical care related to her emotional distress.

• $50,000 payment to compensate Linda for her lost wages while she recuperates from the

accident • $1,500,000 as punitive damages for loss of Pablo. The parties agree that this amount is

not a wrongful death award. Both parties agree that acceptance of this proposal constitutes settlement in full of any and all claims. If you concur with the terms as stated, I will present them to my client for her approval. Thank you for your professionalism and cooperation in resolving this unfortunate matter. Very truly yours, Matt Mathew Dillon, Esq.

Copyright 2006© Deloitte Development LLC All Rights Reserved.

15

Global Universal Insurance P.O. Box 42397

Bedford Park, IL 60501

May 6, 2005 Mr. Mathew Dillon, Esq. 10045 N. 74th Street Sacramento, CA 95819 Dear Mr. Dillon: Per the settlement agreement between your client, Linda Garcia, and our insured, Mr. Jeremy Jones, we are enclosing check number B123987 in the amount of $2,500,000, made payable to the Mathew Dillon, Esq. Trust Account, for the benefit of Linda Garcia. Please sign and return the attached acknowledgement for our records. If I can be of further assistance, please let me know. Sincerely, George Lincoln George Lincoln, Senior Claim Adjustor Global Universal Insurance

Copyright 2006© Deloitte Development LLC All Rights Reserved.

16

Ms. Linda Garcia

623 S. Elk Grove Road Vineyard, CA 95829

May 31, 2005 Mr. Marcus Green 1053 Lopez Court Vineyard, CA 95829 Dear Marcus: Thank you for dinner last week and for your insights into my business affairs. As I mentioned, with the passing of Pablo, I feel like I need to start a whole new life. The apartments were Pablo’s: he loved the whole “fix up” thing and dealing with the tenants. I love the tenants, too, but with my other commitments – and frankly, my other interests – I can’t do it. So I am in the market for a good property management company, and eventually I will probably sell the complex. I have been an engineer with Maypoint for almost 20 years. I love the company and the other employees, but the corporate red tape does tend to stifle my creative energies. I like your idea of leveraging my background, experience, contacts, and interests to start my own business or buy a “turnaround” company. I have quite a bit of money from the lawsuit settlement and Pablo’s life insurance policy, so I think I can interest a seller. I would appreciate your help in finding a good situation. I would really like to find a company that makes kitchen appliances and has a good reputation for quality. The company should also have an existing distribution system and client base – and a loyal sales force – so I don’t have to spend all my time with marketing. I really like the concept of adding computer chips and other technology to make the appliances work more efficiently. In my Internet research, I didn’t find any existing companies with such high tech specialization and that definitely is value I can bring to the company. Can you help me find such an opportunity? This is a business proposition: I am not asking for a favor from a friend, and I absolutely expect to pay your normal billing rate for this service. But I am also looking forward to seeing you again. Sincerely,

Linda

Linda Garcia

Copyright 2006© Deloitte Development LLC All Rights Reserved.

17

By email: From: Marcus Green To: Linda Garcia Date: August 17, 2005 Subject: Kitchen Gizmos purchase opportunity Linda - Great news!! After all of our discussions and dinners, I think I am really getting to know you and the type of business you are interested in. I believe I have found exactly what you are looking for. Have you ever heard of Kitchen Gizmos? They make very high-end kitchen gadgets and appliances, such as espresso machines, bread makers, and all kinds of other cool gadgets. Their products are sold in high-end kitchen stores and large, independent appliance stores. John and Maggie Poindexter own the company. Ironically, John was an engineer for Maypoint about 25 years ago. Now, John and Maggie are retiring and moving to the Bahamas. Maggie mentioned that they plan to go into business with a man named Jack Starling, but that’s another story. Kitchen Gizmos has survived over the past five years based on the Poindexters’ reputation and the existing sales force. The Poindexters haven’t focused on product development, however, in quite a long time. They are eager to sell the business to you – you are a Maypoint “fellow,” and they are tired of the “rat race.” I have reviewed their books and they appear to be in order, but you probably want Joe Blackstone to look everything over. John tells me that this is a Subchapter C corporation with a June 30 year-end. I really see an opportunity for you to expand the business with your new ideas. The Poindexters are asking $5 million for the stock of the corporation. They are willing to “seller finance” a portion of the debt if necessary, but they really want to take their money and leave. Based on their current contracts and market visibility, I think the business is really worth almost twice that amount. The primary tangible asset of the corporation is its existing manufacturing equipment. The tax basis of the equipment is $1.6 million, and it has a fair market value of $2.4 million. The rest of the purchase price is the customer list, the existing sales force, workforce-in-place (valued at about $1.7 million), and a couple of patents worth $400,000. I wanted you to have a chance to read this letter before I talk to you. Once you have read it, please call me and I will come right over to discuss the next steps and answer your questions. Meeting with you is the highlight of my job. See you soon, Marcus

Copyright 2006© Deloitte Development LLC All Rights Reserved.

18

Ms. Linda Garcia, President

Kitchen Gizmos, Inc. 2590 E Stockton Blvd. Sacramento, CA 95829

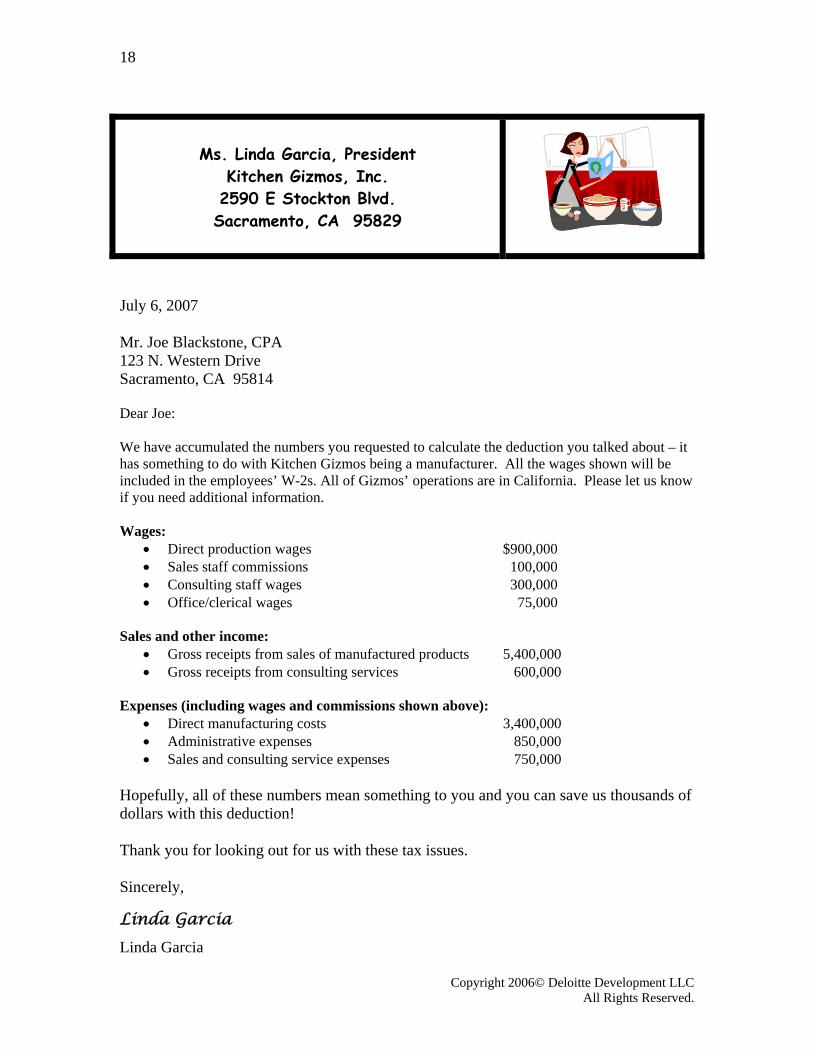

July 6, 2007 Mr. Joe Blackstone, CPA 123 N. Western Drive Sacramento, CA 95814 Dear Joe: We have accumulated the numbers you requested to calculate the deduction you talked about – it has something to do with Kitchen Gizmos being a manufacturer. All the wages shown will be included in the employees’ W-2s. All of Gizmos’ operations are in California. Please let us know if you need additional information. Wages:

• Direct production wages $900,000 • Sales staff commissions 100,000 • Consulting staff wages 300,000 • Office/clerical wages 75,000

Sales and other income:

• Gross receipts from sales of manufactured products 5,400,000 • Gross receipts from consulting services 600,000

Expenses (including wages and commissions shown above): • Direct manufacturing costs 3,400,000 • Administrative expenses 850,000 • Sales and consulting service expenses 750,000

Hopefully, all of these numbers mean something to you and you can save us thousands of dollars with this deduction! Thank you for looking out for us with these tax issues. Sincerely,

Linda Garcia

Linda Garcia

Copyright 2006© Deloitte Development LLC All Rights Reserved.

19

Ms. Linda Garcia

623 S. Elk Grove Road Vineyard, CA 95829

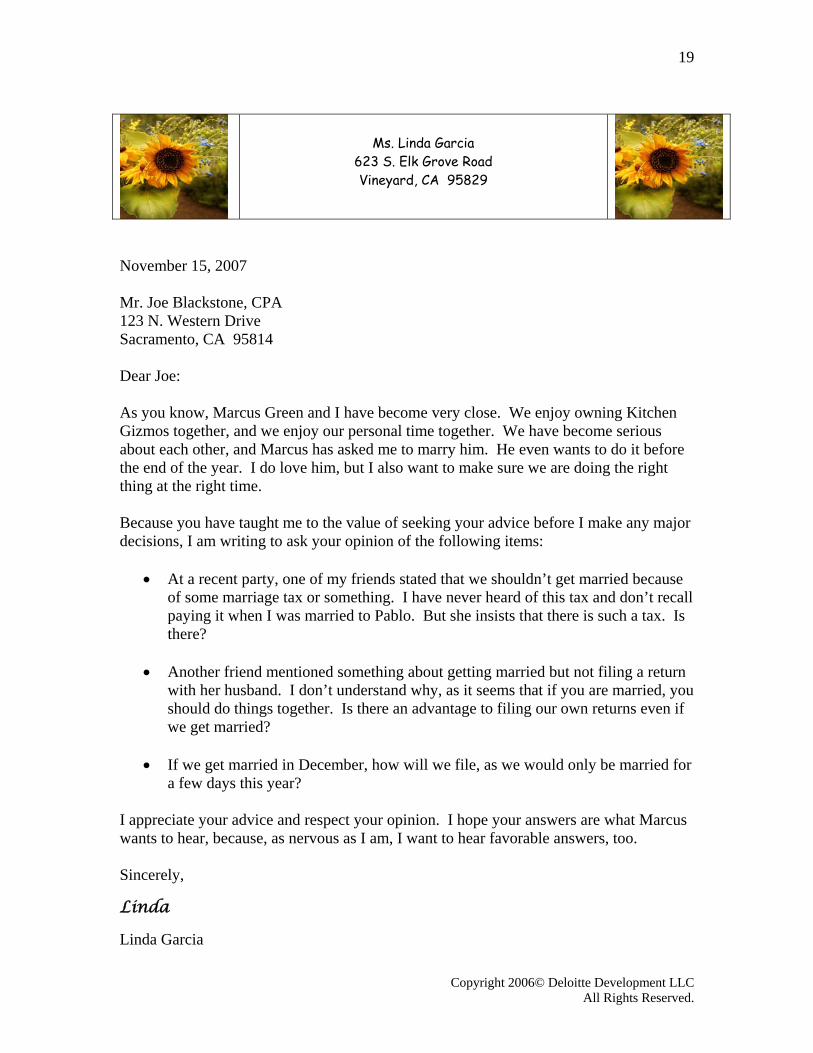

November 15, 2007 Mr. Joe Blackstone, CPA 123 N. Western Drive Sacramento, CA 95814 Dear Joe: As you know, Marcus Green and I have become very close. We enjoy owning Kitchen Gizmos together, and we enjoy our personal time together. We have become serious about each other, and Marcus has asked me to marry him. He even wants to do it before the end of the year. I do love him, but I also want to make sure we are doing the right thing at the right time. Because you have taught me to the value of seeking your advice before I make any major decisions, I am writing to ask your opinion of the following items:

• At a recent party, one of my friends stated that we shouldn’t get married because of some marriage tax or something. I have never heard of this tax and don’t recall paying it when I was married to Pablo. But she insists that there is such a tax. Is there?

• Another friend mentioned something about getting married but not filing a return

with her husband. I don’t understand why, as it seems that if you are married, you should do things together. Is there an advantage to filing our own returns even if we get married?

• If we get married in December, how will we file, as we would only be married for

a few days this year? I appreciate your advice and respect your opinion. I hope your answers are what Marcus wants to hear, because, as nervous as I am, I want to hear favorable answers, too. Sincerely,

Linda Linda Garcia

Copyright 2006© Deloitte Development LLC All Rights Reserved.

20

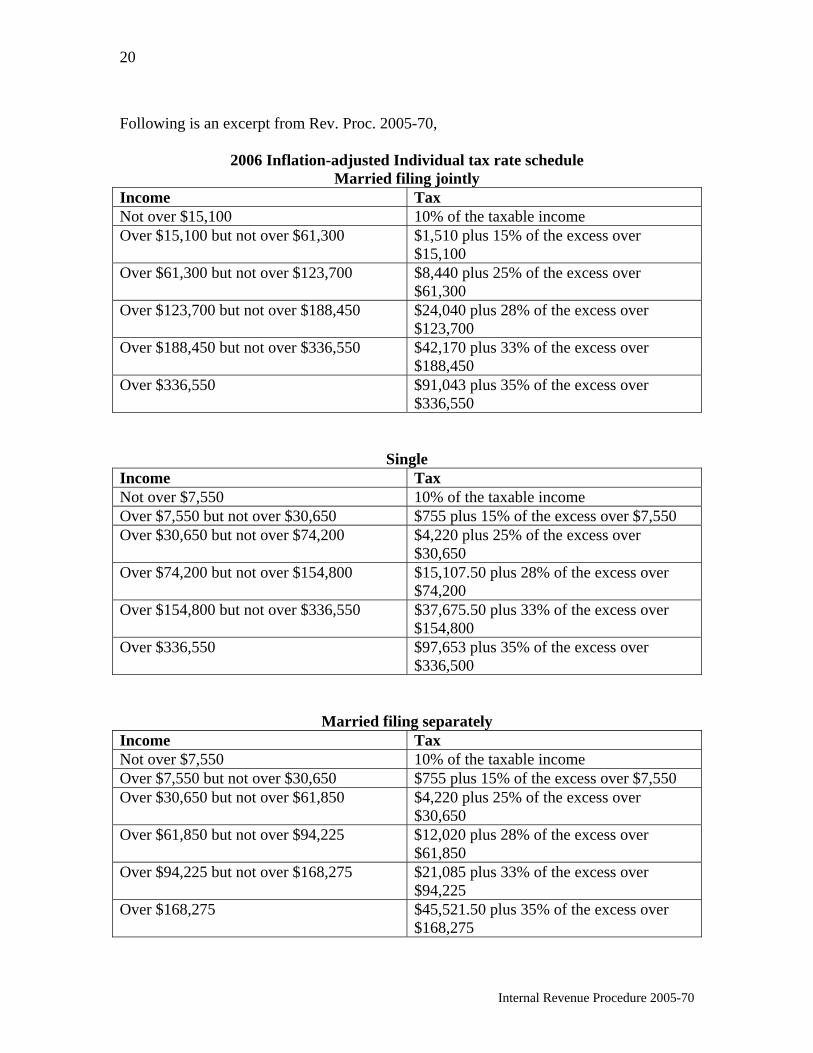

Following is an excerpt from Rev. Proc. 2005-70,

2006 Inflation-adjusted Individual tax rate schedule Married filing jointly

Income Tax Not over $15,100 10% of the taxable income Over $15,100 but not over $61,300 $1,510 plus 15% of the excess over

$15,100 Over $61,300 but not over $123,700 $8,440 plus 25% of the excess over

$61,300 Over $123,700 but not over $188,450 $24,040 plus 28% of the excess over

$123,700 Over $188,450 but not over $336,550 $42,170 plus 33% of the excess over

$188,450 Over $336,550 $91,043 plus 35% of the excess over

$336,550

Single Income Tax Not over $7,550 10% of the taxable income Over $7,550 but not over $30,650 $755 plus 15% of the excess over $7,550 Over $30,650 but not over $74,200 $4,220 plus 25% of the excess over

$30,650 Over $74,200 but not over $154,800 $15,107.50 plus 28% of the excess over

$74,200 Over $154,800 but not over $336,550 $37,675.50 plus 33% of the excess over

$154,800 Over $336,550 $97,653 plus 35% of the excess over

$336,500

Married filing separately Income Tax Not over $7,550 10% of the taxable income Over $7,550 but not over $30,650 $755 plus 15% of the excess over $7,550 Over $30,650 but not over $61,850 $4,220 plus 25% of the excess over

$30,650 Over $61,850 but not over $94,225 $12,020 plus 28% of the excess over

$61,850 Over $94,225 but not over $168,275 $21,085 plus 33% of the excess over

$94,225 Over $168,275 $45,521.50 plus 35% of the excess over

$168,275

Internal Revenue Procedure 2005-70