Embed Size (px)

Citation preview

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 4

2005 Annual Results

Helen WeirGroup Finance Director

24 February 2006

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 5

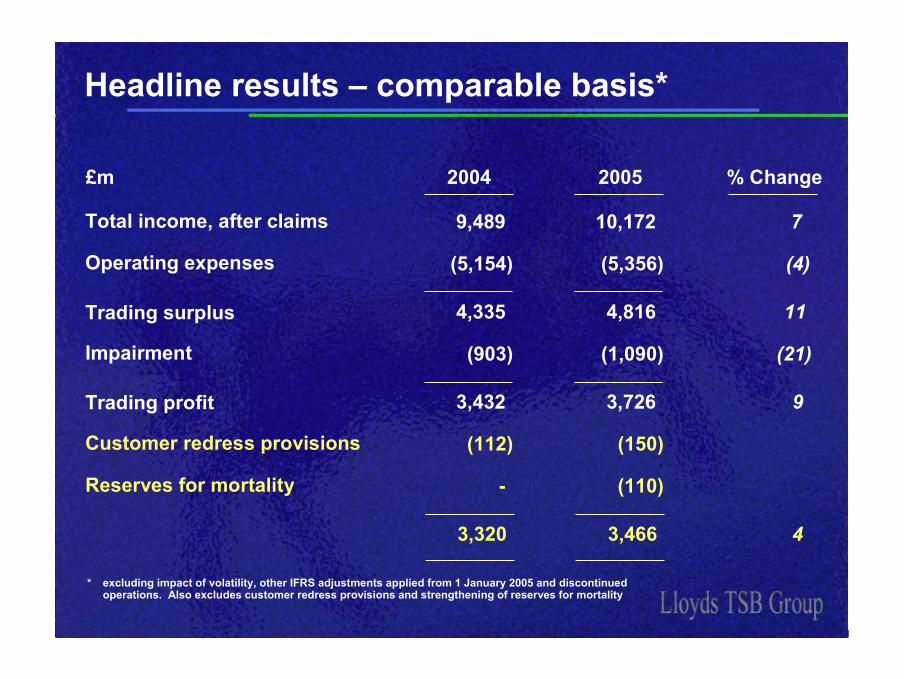

Headline results – comparable basis*

Earnings per share 47.2p42.6p 11

Economic profit £1,620m£1,417m 14

Dividend per share 34.2p34.2p

* excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations in 2004. Also excludes customer redress provisions and strengthening of reserves for mortality

Profit before tax £3,726m£3,432m 9

Post-tax return on equity 23.3%22.2%

20052004 % Change

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 6

Overview – results highlights*

• Continued earnings momentum

• Accelerating revenue growth

• Positive jaws: cost income ratio improved again

• Satisfactory asset quality

• Robust capital ratios

• Post-tax return on equity remains strong

* comparable basis – excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations. Also excludes customer redress provisions and strengthening of reserves for mortality

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 7

Headline results – comparable basis*

Total income, after claims 10,1729,489 7

Operating expenses (5,356)(5,154) (4)

3,4663,320 4

£m 20052004 % Change

Trading surplus 4,8164,335 11

Impairment (1,090)(903) (21)

Trading profit 3,7263,432 9

Reserves for mortality (110)-

Customer redress provisions (150)(112)

* excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations. Also excludes customer redress provisions and strengthening of reserves for mortality

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 8

Impact of IFRS adjustments applied from 1/1/05

(321)

UK Retail Banking (213) • Effective interest rates• Impairment

£m Key Drivers

Insurance & Investments (73) • FRS 27, including £45 million reserves for mortality

Wholesale & International Banking 20 • Financial Instruments and Development Capital mark-to-market

Central group items (55) • Minority interests reclassification from equity to debt

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 9

Earnings momentum*

* comparable basis – excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations. Also excludes customer redress provisions and strengthening of reserves for mortality

£mUKRB

£m % varW&IB

£m % varGroup

£m % varI&I

£m % var

Income 5,118 4 3,875 10 10,172 71,547 11

Costs (2,532) (1) (2,186) (7) (5,356) (4)(639) (5)

Impairment (905) (34) (185) 20 (1,090) (21)-

Trading surplus 2,586 7 1,689 14 4,816 11908 15

Profit before tax 1,681 (3) 1,504 20 3,726 9908 15

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 10

Income growth improving*

Net interest income 5,2034,901 6

£m 20052004 % Change

Other income, net of claims 4,9194,537 8

10,1729,489 7

Policyholder grossingadjustments 5051

Total income, net of claims 10,1229,438 7

Other income 5,1164,751

Insurance claims (197)(214)

* comparable basis – excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations. Also excludes customer redress provisions and strengthening of reserves for mortality

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 11

Good asset and deposit growth*

UK Retail Banking Wholesale & International Banking

* comparable basis – excluding impact of volatility, other IFRS adjustments applied from 1 January 2005and discontinued operations

+10%

+7%

+7%

Average interest earning assets

2004 2005

£89.9bn£98.5bn

Average customer deposits

2004 2005

£62.2bn £66.6bn

Average interest earning assets

2004 2005

£77.6bn£83.0bn

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 12

Net interest margin – stable*

* relating to the Group’s banking businesses, excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations

2.75%

2.89%

2.80%

2.80%

2004H1 2004H2 2005H1 2005H2

2004: 2.84%

2005: 2.78%

Product margin 8Funding effect (3)

5bp

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 13

Net interest income*

UK Retail Banking 3,3073,228 2

Insurance & Investments† 10194 7

Wholesale & InternationalBanking 2,1651,986 9

Central group items (370)(407)

5,5135,090 8

* comparable basis – excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations

† excluding policyholder grossing adjustments

£m 20052004 % Change

5,2034,901 6

Policyholder grossing adjustments 310189

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 14

Other income, net of insurance claims*

UK Retail Banking 1,8111,696 7

Insurance & Investments† 1,3961,252 12

Wholesale & InternationalBanking 1,7101,544 11

Central group items 245

4,6594,399 6

* comparable basis – excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations. Also excludes strengthening of reserves for mortality

† excluding policyholder grossing adjustments

£m 20052004 % Change

4,9194,537 8

Policyholder grossing adjustments (260)(138)

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 15

Strong cost control maintained*

UK Retail Banking 2,5322,509 (1)

Insurance & Investments† 607573 (6)

Wholesale & InternationalBanking 2,1862,047 (7)

Central group items (1)(12)

5,3565,154 (4)

* comparable basis – excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations. Also excludes customer redress provisions

† excluding policyholder grossing adjustments

£m 20052004 % Change

5,3245,117 (4)

Policyholder grossing adjustments 3237

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 16

Focus on costs

Operational principles

• Simplify

• Improve efficiency

• Leverage common systems/processes cross-group

– Transforming group wide procurement

– Consolidation of back office processes

– Organisational delayering/ simplification

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 17

Focus on costs

Financial principles

• Self funding

• Payback c. 2 years

• Reinvest c. 50% of benefits

• c. £40 million investment in 2005

• c. £20-30 million net benefit in 2006

• c. £100-150 million net benefit in 2007

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 18

4%

7%

5%

1%

7%

10%

11%

4%

Group

Wholesale &International

Banking

Insurance &Investments

UK RetailBanking

Income growth ahead of costs in all divisions*

* comparable basis – excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations. Also excludes customer redress provisions and strengthening of reserves for mortality

Group Cost:Income Ratio

Income Costs

54.3%52.7%

2004 2005

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 19

Impairment losses on loans and advances*

% of Average Lending2005

£mVariance

% 200520042004£m

Wholesale & International Banking 185 20 0.310.43230

UK Retail Banking 905 (34) 0.920.75676

Total 1,090 0.660.61903 (21)

* comparable basis – excluding other IFRS adjustments applied from 1 January 2005 and discontinued operations

- Credit cards 307 (27) 4.013.42242

- Personal loans/overdrafts 585 (24) 4.764.20473

- Mortgages 13 0.02(0.05)(39) -

Insurance & Investments - --(3) -

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 20

Impairment losses on loans and advances*

% of Average Lending2005

£mVariance

% 200520042004£m

Wholesale & International Banking 185 20 0.310.43230

UK Retail Banking 905 (34) 0.920.75676

Total 1,090 0.660.61903 (21)

* comparable basis – excluding other IFRS adjustments applied from 1 January 2005 and discontinued operations

- Credit cards 307 (27) 4.013.42242

- Personal loans/overdrafts 585 (24) 4.764.20473

- Mortgages 13 0.02(0.05)(39) -

Insurance & Investments - --(3) -

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 21

Impairment losses – UK Retail Banking*

* comparable basis – excluding other IFRS adjustments applied from 1 January 2005 and discontinued operations

Mortgageprovisionrelease

Volumegrowth

Assetquality

2004 2005

£905m£126m

£676m

£64m£715m£39m

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 22

New business – probability of default

Credit Cards

Personal Loans

100

Index

Jan-04

Feb-04

Mar-04

Apr-04

May-04

Jun-04Ju

l-04

Aug-04Sep

-04Oct-

04Nov-0

4Dec

-04Ja

n-05Feb

-05Mar-

05Apr-0

5May

-05Ju

n-05Ju

l-05

Aug-05Sep

-05Oct-

05Nov-0

5Dec

-05

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 23

Asset quality – impaired assets

Impaired Assets Impaired Assets as a Percentage of Total Lending

2.1%2.3% 2.3%

1 January2005

30 June2005

31 December2005

£3,515m£3,894m £4,122m

1 January2005

30 June2005

31 December2005

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 24

+14%

£1,417m

£1,620m

2004 2005

Economic Profit

Maintaining high returns*

* comparable basis – excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations. Also excludes customer redress provisions and strengthening of reserves for mortality

Post-tax Returnon Equity

22.2%23.3%

2004 2005

Post-tax Return on Risk-weighted Assets

1.98% 1.92%

2004 2005

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 25

Capital ratios remain robust

• £1 billion in dividends received from Scottish Widows

• Sufficient retained earnings to support expected risk-weighted asset growth

Total capitalratio

10.1% 10.9%

Risk-weightedassets

£131.8bn £144.9bn

1 January2005

31 December2005

Tier 1 ratio 7.9%8.2%

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 26

Scottish Widows – strong capital management

Available assets, including support account 22.0 23.2

Net surplus 4.2 4.1

Realistic value of liabilities (17.8) (19.1)

Long-Term Fund (£bn)31 December

2004

31 December2005

estimated

Working capital ratio 19.0% 17.8%

Risk capital margin cover 9.3x 11.5x

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 27

Improving our balance sheet management

• Moving from ‘buy and hold’ to ‘origination and distribution’

• During 2006, rolling mortgage securitisation programme

• Over time, programme expanded to include other asset classes

• Exploring ways to repatriate further capital from Scottish Widows

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 28

Reducing the pension schemes’ deficit

• During 2005, additional voluntary contributions of £220 million

• Triennial valuation currently being finalised

• Discussions underway with Trustees with objective of reducing the schemes’ deficit

IAS 19 pension deficit 2,9103,075

Deferred tax (873)(923)

£m 20052004

IAS 19 pension deficit, net of tax 2,0372,152

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 29

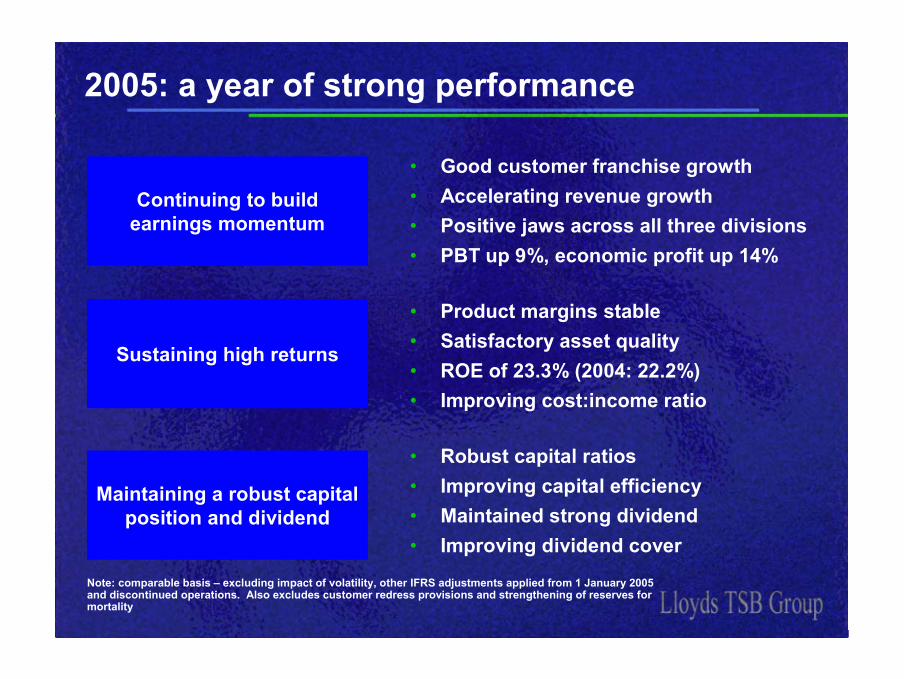

2005: a year of strong performance

Continuing to build earnings momentum

• Good customer franchise growth• Accelerating revenue growth• Positive jaws across all three divisions• PBT up 9%, economic profit up 14%

Sustaining high returns

• Product margins stable• Satisfactory asset quality• ROE of 23.3% (2004: 22.2%)• Improving cost:income ratio

Maintaining a robust capital position and dividend

• Robust capital ratios• Improving capital efficiency• Maintained strong dividend• Improving dividend cover

Note: comparable basis – excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations. Also excludes customer redress provisions and strengthening of reserves for mortality

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 32

2005 Annual Results

Eric DanielsGroup Chief Executive

24 February 2006

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 33

Four key messages

• We have significant potential in our franchises

• We can structurally improve our productivity

• We can manage capital to fund growth

• We are building the skills and financial strength to accelerate growth – in core businesses and from new markets

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 34

Reminder: our strategy

• Enhance earnings quality• Maintain profitability• Start growth

• Deepen relationships• Improve productivity• Build capabilities• Accelerate growth

• Leverage capabilities in new markets

Economic profit

Phase One

Phase Two

Phase Three

Focus on core markets

Build customer franchises

Expand from strength

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 35

Our financial progress

* 2002-4 figures on a UK GAAP basis excluding discontinued operations. 2004-5 figures are on an IFRS comparable basis excluding major one-offs

Income, £bn*

IFRS comparable

8.99.29.0

10.29.5

'02 '03 '04 '05

PBT, £bn*

3.2

3.4

3.1

3.7

3.4

'02 '03 '04 '05

ROE, %*

23.5%23.1%

25.2%

22.2%23.3%

'02 '03 '04 '05

Cost:income ratio, %*

53.5%

55.1%

51.9%

54.3%

52.7%

'02 '03 '04 '05

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 36

Our priorities for Phase 2

• Strong revenue growth

• A step change in operational efficiency

• Enhanced capital efficiency and dividend capacity

• Double digit economic profit growth

Build our franchise reach and depth

Enhance our product capabilities

Improve our productivity

Work our capital harder

Financial goals for Phase 2Strategic priorities

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 37

UK Retail Banking: driving growth

What we are doing in 2005-6Our objectives

• Growing sales volumes

• Changing product sales mix

• Increasing direct channel sales

• Increasing branch sales capacity and effectiveness

• Reducing overheads and back office costs

Grow income from existing customer base

Grow income from new customers

Improve productivity

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 38

UK Retail Banking: sales volumes

2005 sales volume growth, %

Indexed sales volumes as a % of prior year period

Indexed net recruitment, target

customers

… and driving target customer recruitment

… increasing direct channel sales …

Improving branch sales performance …

150

100

2004 2005

39

28

Internet TelephonyStart ‘05 Start Feb ‘06

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 39

UK Retail Banking: sales productivity

2004-2005 % change

• New strategic sales platform

• Improved customer leads

Indexed sales

… to increase sales productivity

… and improving sales effectiveness …

Increasing sales capacity …

145

100

LTSBtoday

Our goal

Tasks sent to branches

Faxes handled by branches

Time to process a loan sale

(15%)

(50%)

(30%)

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 40

UK Retail Banking: sales mix

H2 04-05 growth per customer,target customers

Total retail product sales volumes

… to drive higher non-lending income per customer

Changing the overall product sales mix …

* includes secured and unsecured lending and related protection products

Non-lending

Lending*59% 53%

41% 47%

2004 2005 (1.2%)

1.4%

Non-lending revenue

Total revenue

Lending revenue

6.1%

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 41

UK Retail Banking: the demographic opportunity

<0 0-10% >10%

<30 yrs 30 - 44 45 - 54 55 - 64 65+ yrs

10% (7%) 40% 23% 34%

Current accounts

Unsecured lending

Mortgages

Savings and investments

Market risk-adjusted revenue growth to 2010: share by age and product

Source: internal analysis

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 42

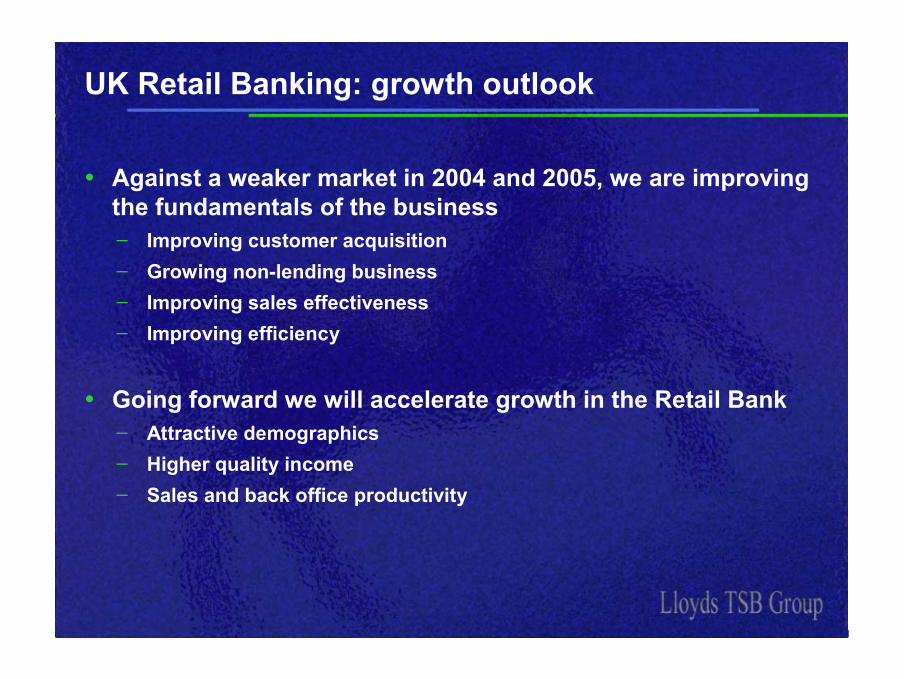

UK Retail Banking: growth outlook

• Against a weaker market in 2004 and 2005, we are improving the fundamentals of the business Improving customer acquisition Growing non-lending business Improving sales effectiveness Improving efficiency

• Going forward we will accelerate growth in the Retail Bank Attractive demographics Higher quality income Sales and back office productivity

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 43

W&IB: break-out growth

What we are doing in 2005-6Our objectives

• Growing product capabilities• Driving cross sell• Capturing relationship

headroom• Building asset distribution

Grow the Corporate Markets business

Build on the growth momentum in Business

Banking

• Winning higher value customers

• Improving productivity and service

• Simplifying our offer and our operations

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 44

W&IB: 2005 performance

Business unit performance

* comparable basis – excluding impact of volatility, other IFRS adjustments applied from 1 January 2005 and discontinued operations

Corporate Markets 958732 31

Profit before tax* (£m) 20052004 % Change

Business Banking 206153 35

Asset Finance 219240 (9)

International Banking 133120 11

Wholesale & InternationalBanking

+20%

CARE - CONTAINS PRICE SENSITIVE INFORMATION

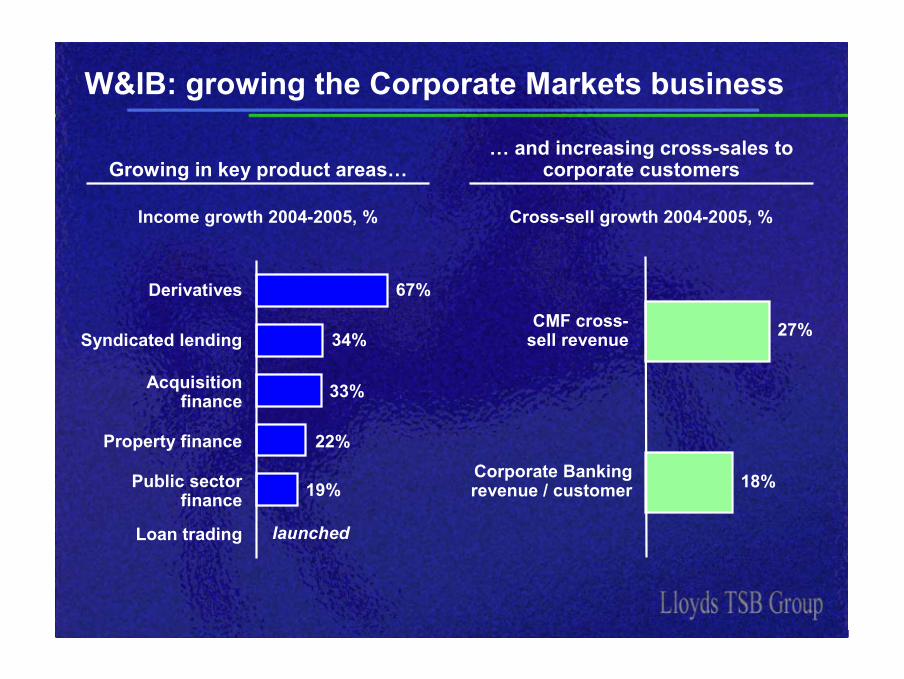

Investor Relations, Group Finance Division HAW - page 45

W&IB: growing the Corporate Markets business

Cross-sell growth 2004-2005, %Income growth 2004-2005, %

… and increasing cross-sales to corporate customersGrowing in key product areas…

CMF cross-sell revenue 27%

18%Corporate Banking revenue / customer

67%

19%

34%

22%

launched

33%

Derivatives

Syndicated lending

Acquisition finance

Property finance

Public sector finance

Loan trading

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 46

W&IB: growing the Corporate Markets business

• Excellent service• Creativity• Follow-up

Relationship quality

Relationship depth

Customer satisfaction

Recent surveys show improving customer perception of our capabilities*

• Syndications• Interest rate derivatives• Foreign exchange

• Overall satisfaction

+ 100%+ 30%+ 25%

+ 66%+ 50%+ 24%

+ 137%

* improvement in number of customers responding positively. Selected comparisons taken from major independent market surveys with our ‘larger corporate’ customer segment

% improvement 2004-5

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 47

W&IB: moving Business Banking to growth

• Relationship managers back in branches• Income generating contacts up• Improved customer satisfaction by 9% pts

Improving sales and service

• Growing market share• Gaining in switchers and start-ups

Growing the franchise

• Improved cost:income ratio by 4% ptsSimplifying operations

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 48

W&IB: 2005 cost growth

Around half of W&IB’s cost growth 2004-5 will deliver future profit growth – mainly in CMF and Business Banking

3.0% ‘jaws’

6.4% ‘jaws’

W&IB revenue growth

9.8%

6.8%

Total W&IB cost

growth

1.3%

Frontline staff

growth

1.4%

Investment in processing

improvements

Investment in growth initiatives

0.7%3.4%

Underlying W&IB cost

growth

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 49

W&IB: growth outlook

• We can continue our performance momentum

– Step up our share of ‘lead’ relationships

– Grow mid-market share in key regions

– Build our product range

– Accelerate revenue growth in Business Banking

– Increase back office productivity

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 50

Insurance & Investments: accelerating growth

What we are doing in 2005-6Our objectives

• Focusing on the most valuable IFA relationships and improving service

• Improving our bancassurance product range and sales effectiveness

• Improving investment performance

• Raising individual product IRRs

• Repatriating excess capital

Maximise distribution reach

Develop better products

Improve capital management

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 51

I&I: Scottish Widows IFA performance

Service improvements and more competitive products, will continue to drive sales and market share growth

Market share*Weighted sales, £m

5.9%6.8%

5.7%

2003 2004 2005* total LP&I market estimate

432

562

392

2003 2004 2005

+30%+10%

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 52

I&I: bancassurance performance

Revised offers and salesforce development have delivered overall sales growth of 13%, with particular success in OEICs

OEIC sales, £mOverall weighted sales, £m

+77%242

274

2004 2005

+13%

67

119

2004 2005

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 53

Insurance & Investments: growth outlook

• Strong LP&I performance – growing market share in a growing market

• We can continue to grow and improve profitability

IFA - improved investment performance and product mix

Bancassurance - simplified products, better salesforce productivity, attractive customer base

Capital efficiency

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 54

Achieving a step change in productivity

# 2002-4 figures on a UK GAAP basis excluding discontinued operations. 2004-5 figures are on an IFRS comparable basis excluding major one-offs

* 2002-3 underlying – excluding acquisitions and disposals† 2002-4 uses UK GAAP; 2004-5 uses comparable IFRS, excluding customer redress provisions and

strengthening of reserves for mortality

(1.6) (1.6)

UK GAAP IFRS

Our ‘jaws’ discipline has delivered results

Change in staff numbers (y/e FTE)Group cost:income ratio#

(1,624)(3,188)

200520042003*

(1,209)

Change in income per FTE†

+6%

+12%

200520042003*

+14%

200520042003

55.1%53.5%

54.3%52.7%

2004

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 55

Achieving a step change in productivity

What we are doingStrategic priorities

• Consolidating processes

• Applying ‘lean manufacturing’

• Transforming procurement

• Simplifying management structure

• Extending Sigma programme

Leverage our scale

Exploit our cost management skills

Match best in class efficiency standards

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 56

Working our capital harder

What we are doingStrategic priorities

• Focusing on economic profitability at a customer and product level

• Further improving capital efficiency in Scottish Widows

• Developing distribution capabilities in Corporate Markets

• Implementing asset securitisation

Maximise capital efficiency in each business

Shift lower yield risk off our balance sheet

Focus on our strength in origination

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 57

Phase 3: leveraging capabilities in new markets

• We are building the right capabilities– Customer and sales skills

– Manufacturing skills

– Cost management skills

– Capital management skills

• In a consolidating global FS market, value creation will be driven by the transfer of advantaged capabilities– Not through scale alone

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division HAW - page 58

Four key messages

• We have significant potential in our franchises

• We are structurally improving our productivity

• We are managing capital to fund growth

• We are building the skills and financial strength to accelerate growth – in core businesses and from new markets

CARE - CONTAINS PRICE SENSITIVE INFORMATION

Investor Relations, Group Finance Division PRH 1

Forward looking statements

This document is a summary only of certain information contained in the announcement dated 24 February 2006 and should be read in conjunction with the full text of the announcement.

This document contains forward looking statements with respect to the business, strategy and plans of the Lloyds TSB Group and its current goals and expectations relating to its future financial condition and performance. Statements that are not historical facts, including statements about Lloyds TSB Group’s or management’s beliefs and expectations, are forward looking statements. By their nature, forward looking statements involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. Lloyds TSB Group’s actual future results may differ materially from the results expressed or implied in these forward looking statements as a result of a variety of factors, including UK domestic and global economic and business conditions, risks concerning borrower credit quality, market related risks such as interest rate risk and exchange rate risk in its banking businesses and equity risk in its insurance businesses, inherent risks regarding changing demographic developments, catastrophic weather and similar contingencies outside Lloyds TSB Group’s control, any adverse experience in inherent operational risks, any unexpected developments in regulation or regulatory actions, changes in customer preferences, competition, industry consolidation, acquisitions and other factors. For more information on these and other factors, please refer to Lloyds TSB Group’s Registration Statement on Form 20-F filed with the US Securities and Exchange Commission and to any subsequent reports furnished by Lloyds TSB Group to the US Securities and Exchange Commission or to the London Stock Exchange. The forward looking statements contained in this document are made as of the date hereof, and Lloyds TSB Group undertakes no obligation to update any of its forward looking statements.