Embed Size (px)

Citation preview

2004 Indiana Energy 2004 Indiana Energy ConferenceConference

““Perspectives on the Perspectives on the Energy Puzzle” Energy Puzzle”

September 16, 2004September 16, 2004

HOWARD WEIL INC.

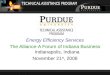

Oil Prices – Hitting all-time highs, but easing Oil Prices – Hitting all-time highs, but easing

$0

$10

$20

$30

$40

$50

$60

Spot Prices Futures

WT

I ($

/BB

l)

HOWARD WEIL INC.

14-yr. avg. $22.94

Avg. 1990 – 2000 $20.68

Avg. ‘00 – ‘04 $29.86

Source: Bloomberg

What is driving high crude oil prices?What is driving high crude oil prices?

Demand pull – particularly China

Less spare production capacity

Weak U.S. dollar

Political uncertainty

- Iraq

- Russia – Yukos and recent terrorist attacks

- Up until Aug. 15, referendum in Venezuela

Speculators in market

HOWARD WEIL INC.

Energy expenditures as a % of GDP are decliningEnergy expenditures as a % of GDP are declining

HOWARD WEIL INC.

0%

2%

4%

6%

8%

10%

12%

14%

16%

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

Source: EIA/DOE

HOWARD WEIL INC.

Inflation adjusted, crude is below highs of early 1980’sInflation adjusted, crude is below highs of early 1980’s

$0

$10

$20

$30

$40

$50

$60

$70

Ave

rage

An

nu

al p

rice

($/

Bb

l)

Crude Oil Prices in 2003 Dollars1970-1983 Arabian Light/1984 – Current Brent Spot

Average = $31.35/bbl

Source: Bloomberg and Howard Weil

Coal prices at record highsCoal prices at record highs

$20

$25

$30

$35

$40

$45

$50

$55

$60

$65

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Eas

tern

Coa

l ($/

Sh

ort-

ton

)

HOWARD WEIL INC.

Source: Bloomberg

Coal Demand FundamentalsCoal Demand Fundamentals

Tremendous consumption in China pulling worldwide prices

– China disincentivized coal exports in 2003

– U.S. exports up 57% year-to-date

Change in ownership of domestic electric coal-fired generation – capacity utilization up to 72% from 67% six years ago

Cost advantage of coal fleet relative to natural gas

Stronger U.S. economy translates into higher steam and metallurgical coal demand

HOWARD WEIL INC.

Coal Supply FundamentalsCoal Supply Fundamentals

Lack of capital deployed to develop new mines– 3-5 year lag before “greenfield” mines can add substantial

productionPermitting constraints delay future production growthRailroad constraints impeding deliverability, predominantly from Powder River Basin (western US)– Only region with excess production capacity

More reserves in hands of publicly traded companies– Companies maintaining capital discipline– Private equity buying companies out of bankruptcy

HOWARD WEIL INC.

Absence of surety bond market squeezing out smaller producers

Rising mining costs

– Low hanging fruit has been picked

Inventories now 20% below 3-year average

Coal Supply Fundamentals (cont.)Coal Supply Fundamentals (cont.)

HOWARD WEIL INC.

Coal stockpiles heading toward 30-year lowsCoal stockpiles heading toward 30-year lows

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

E

Coa

l Sto

ckp

iles

(000

sh

ort

ton

s)

HOWARD WEIL INC.Source: EIA, Bloomberg, Howard Weil

As coal demand has risen, inventories continue to declineAs coal demand has risen, inventories continue to decline

0

20

40

60

80

100

120

140

Co

al

Inv

ento

ries

(D

ay

s)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Co

al

Dem

an

d (

00

0 T

on

s)

Inventories - Days of Forward Demand U.S. Coal Demand

HOWARD WEIL INC.Source: EIA, Bloomberg, Howard Weil

Declining Inventories = Rising PricesDeclining Inventories = Rising Prices

90,000

100,000

110,000

120,000

130,000

140,000

150,000

160,000

Co

al

Sto

cks

(00

0 s

ho

rt t

on

s)

$0

$10

$20

$30

$40

$50

$60

$70

Ea

ster

n C

oa

l P

rice

($

/sh

ort

to

n)

Coal Stockpiles Coal Prices

HOWARD WEIL INC.Source: EIA, Bloomberg, Howard Weil

Coal still trading at 50% discount to natural gasCoal still trading at 50% discount to natural gas

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan-0

0

Apr-0

0

Jul-0

0

Oct

-00

Jan-0

1

Apr-0

1

Jul-0

1

Oct

-01

Jan-0

2

Apr-0

2

Jul-0

2

Oct

-02

Jan-0

3

Apr-0

3

Jul-0

3

Oct

-03

Jan-0

4

Apr-0

4

Jul-0

4

HistoricalAverage 34%

HOWARD WEIL INC.Source: EIA, Bloomberg, Howard Weil

Natural gas prices… more than a spikeNatural gas prices… more than a spike

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Nat

ura

l Gas

Pri

ce (

$/M

MB

tu)

Spot Gas Futures

Futures

HOWARD WEIL INC.Source: Bloomberg

Gas storage near full…not the problemGas storage near full…not the problem

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Wk

1

Wk

9

Wk

17

Wk

25

Wk

33

Wk

41

Wk

49

Wk

5

Wk

13

Wk

21

Wk

29

Wk

37

Wk

45

Wk

1

Wk

9

Wk

17

Wk

25

Wk

33

Wk

41

Wk

49

Wk

5

Wk

13

Wk

21

Wk

29

Wk

37

Gas

Sto

rage

Lev

els

(Tcf

)

Historical Low 7-yr Historical High 7-yr 01 - 04 Actual

2001 2002 2003 2004

HOWARD WEIL INC.

Source: EIA/DOE

Natural gas rig count is at all time highsNatural gas rig count is at all time highs

HOWARD WEIL INC.

0

200

400

600

800

1000

1200

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Oil GasSource: Baker Hughes

Despite increased drilling, production not respondingDespite increased drilling, production not responding

Annual Production ChangeAvg. Gas Rig Count

2000 2001 2002 2003 2004E

-7%

-5%

-3%

-1%

1%

3%

U.S

. P

rod

uc

tio

n C

ha

ng

e

500

600

700

800

900

1,000

1,100

Ga

s R

ig C

ou

nt

Production Change Rig Count

-1.2% 0.6% -4.7% -4.8% -2.5% 720 939 691 872 1,031

HOWARD WEIL INC.Source: Baker Hughes and Howard Weil

17% 17% 16% 18% 19% 19% 20% 21% 23% 23% 25% 24% 27% 28% 29% 30%

0

10

20

30

40

50

60

Production Decline Rate of Base:

Bcf

/d

1990

2005E2004E2003E2002E2001E20001999199819971996199519941993199219911990Pre-1990

Drilling Year:

U.S. Natural Gas Production HistoryIndicates 30% 2005 Decline Rate

Utilizes Data Supplied by IHS Energy; Copyright 1990-2004 IHS EnergyChart Prepared by and Property of EOG Resources, Inc.; Copyright 2002-2004

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001E 2002E 2003E 2004E 2005E

HOWARD WEIL INC.

Trend toward declining Canadian exportsTrend toward declining Canadian exports

0

2

4

6

8

10

12

1955

1958

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

2000

2003

Net

Im

por

ts (

Bcf

/d)

HOWARD WEIL INC.

Canadian gas deregulated

Source: EIA/DOE

Rising exports to Mexico a negativeRising exports to Mexico a negative

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

E

Exp

orts

(B

cf/d

)

HOWARD WEIL INC.

Source: EIA/DOE and Howard Weil

LNG imports are helping with the problem…LNG imports are helping with the problem…

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

LN

G I

mp

orts

(M

Mcf

/d)

HOWARD WEIL INC.Source: EIA/DOE and Howard Weil

……but the impact is longer term and there are ramificationsbut the impact is longer term and there are ramifications

HOWARD WEIL INC.

0

5,000

10,000

15,000

20,000

25,000

2004 2005 2006 2007 2008 2009

LN

G C

apac

ity

(MM

cf/d

)

Existing Proposed Onshore Proposed Offshore

Source: EIA/DOE, FERC and Howard Weil

Fundamentals point to continued strength in gas pricesFundamentals point to continued strength in gas prices

Natural Gas Supply/Demand Balance

HOWARD WEIL INC.

Supply 2002 2003 2004E Canada 9.8 8.8 8.6 Mexico (0.7) (0.9) (1.2) LNG 0.6 1.4 1.8 Sub 9.7 9.2 9.2 Production 52.1 51.4 51.0 Storage 1.3 (0.5) 0.0 Total Supply 63.1 60.1 60.2Demand Electric 15.5 13.5 14.1 Industrial 20.1 19.2 19.5 Res/Comm 21.9 22.6 22.0 Other 5.5 4.8 4.8 Total Demand 63.1 60.1 60.4

Balance 0.0 (0.0) (0.2)

Bcf/d

Source: EIA/DOE and Howard Weil

A step-change to higher gas pricesA step-change to higher gas prices

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$/M

MB

tu

$2.00 Gas

$2.75 Gas

$4.00 - $5.00 Gas

HOWARD WEIL INC.Source: Bloomberg and Howard Weil

Sampling of Regional Electricity prices ($/MWhr)Sampling of Regional Electricity prices ($/MWhr)

HOWARD WEIL INC.

1Q'04 1Q'03 ChangeCalifornia $44.31 $50.69 -12.6%Cinergy $42.05 $50.96 -17.5%Texas $40.46 $53.65 -24.6%New England $69.41 $76.05 -8.7%

2Q'04 2Q'03 ChangeCalifornia $48.77 $38.75 25.9%Cinergy $45.09 $32.88 37.1%Texas $49.24 $51.09 -3.6%New England $61.40 $54.96 11.7%

3Q'04TD 3Q'03TD ChangeCalifornia $53.50 $48.42 10.5%Cinergy $45.16 $43.32 4.2%Texas $51.93 $45.85 13.3%New England $57.21 $54.16 5.6%

Source: Megawatt Daily

New York

-$10

$0

$10

$20

$30

Q1 Q2 Q3TD

$/M

wh

2003 2004

COB

-$10

$0

$10

$20

$30

Q1 Q2 Q3TD

$/M

wh

2003 2004

ERCOT

-$10

$0

$10

$20

$30

Q1 Q2 Q3TD

$/M

wh

2003 2004

SERC

-$10

$0

$10

$20

$30

Q1 Q2 Q3TD

$/M

wh

2003 2004

Sampling of regional spark spreads ($/MWhr)Sampling of regional spark spreads ($/MWhr)

Source: Megawatt Daily

Solutions to the Energy DilemmaSolutions to the Energy Dilemma

Conservation

Fuel diversity

Spending on electric transmission grid

Alternative energy

Alaskan Pipeline

Energy bill

HOWARD WEIL INC.

HOWARD WEIL INC..

HOWARD WEIL INC..