Embed Size (px)

Citation preview

2020THTH ANNUAL SMALL ANNUAL SMALL SCHOOLS SCHOOLS CONFERENCECONFERENCE

DPI School Finance IssuesDPI School Finance IssuesJerry Landmark, Karen Jerry Landmark, Karen

KucharzKucharzMarch 10, 2005March 10, 2005

Finance Issues - Finance Issues - Agenda Agenda

What the Finance Team is up to.What the Finance Team is up to. Budgeting – From Estimates to Budgeting – From Estimates to

Levy CertificationLevy Certification

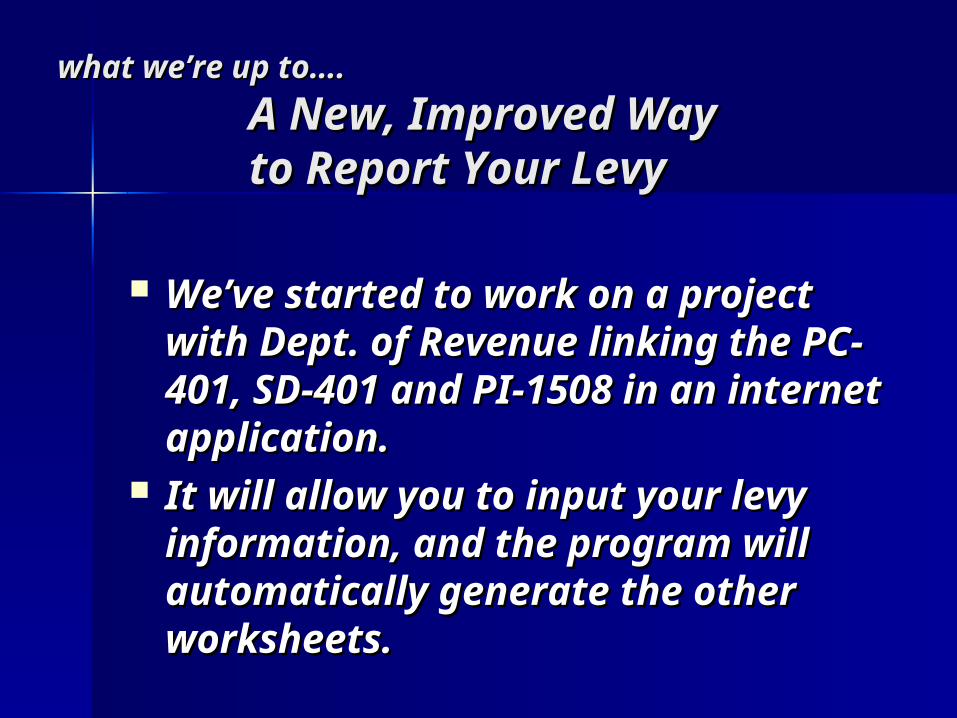

what we’re up to….what we’re up to….

A New, Improved Way A New, Improved Way to Report Your Levyto Report Your Levy

We’ve started to work on a We’ve started to work on a project with Dept. of Revenue project with Dept. of Revenue linking the PC-401, SD-401 and linking the PC-401, SD-401 and PI-1508 in an internet PI-1508 in an internet application.application.

It will allow you to input your It will allow you to input your levy information, and the levy information, and the program will automatically program will automatically generate the other worksheets.generate the other worksheets.

A district will input its total levy A district will input its total levy (one number) into the PC-401. (one number) into the PC-401. Everything else is pre-populated Everything else is pre-populated by DOR, and the pro-rations will by DOR, and the pro-rations will be automatically calculated.be automatically calculated.

what we’re up to….what we’re up to….

A New, Improved Way A New, Improved Way to Report Your Levyto Report Your Levy

The total levy will be transferred to The total levy will be transferred to the SD-401, where the district will the SD-401, where the district will break down its levy into fund, break down its levy into fund, including funds 10, 38, 41, etc.including funds 10, 38, 41, etc.

Edits will be built in, so if a district Edits will be built in, so if a district doesn’t have a Fund 41, it won’t be doesn’t have a Fund 41, it won’t be allowed to enter a number.allowed to enter a number.

what we’re up to….what we’re up to….

A New, Improved Way A New, Improved Way

to Report Your Levyto Report Your Levy

The info from the SD-401 and Pc-The info from the SD-401 and Pc-401 will automatically generate 401 will automatically generate the tax levy certification form (PI-the tax levy certification form (PI-1508) that districts send to each 1508) that districts send to each municipality in the school district.municipality in the school district.

what we’re up to….what we’re up to….

A New, Improved Way A New, Improved Way

to Report Your Levyto Report Your Levy

Benefits to districts: easier input Benefits to districts: easier input via the internet, accurate levy via the internet, accurate levy information; less chance for information; less chance for error.error.

Benefits to DPI and DOR: Benefits to DPI and DOR: accurate, up-to-date information.accurate, up-to-date information.

We anticipate it will be available We anticipate it will be available this fall.this fall.

what we’re up to….what we’re up to….

A New, Improved Way A New, Improved Way

to Report Your Levyto Report Your Levy

…….what else we’re up .what else we’re up to….to….

Debt Tables – on-line input via Debt Tables – on-line input via the Reporting Portal, it then the Reporting Portal, it then interacts with Budget and interacts with Budget and Annual Reports.Annual Reports.

Equalization Aid Calculation – Equalization Aid Calculation – automatic calculation after automatic calculation after completing annual and budget completing annual and budget reports.reports.

Budgeting Budgeting

Organize Your Budget Organize Your Budget Development Around Development Around a Calendar of a Calendar of ActivitiesActivities

BudgetingBudgeting

December: Update Enrollment December: Update Enrollment ProjectionsProjections

Use Cast Forward MethodUse Cast Forward Method Contact Your County Office for InfoContact Your County Office for Info ““Kindergarten Round-Up” in SpringKindergarten Round-Up” in Spring Be Aware of Changes in Housing Be Aware of Changes in Housing

PatternsPatterns

Early January: Early January:

Develop a Preliminary Revenue Limit Develop a Preliminary Revenue Limit Estimate using Enrollment Projections Estimate using Enrollment Projections and Prior-Year Levies/October 15 Aidand Prior-Year Levies/October 15 Aid

Determine Staffing Levels Based on Kid Determine Staffing Levels Based on Kid Count/Grade Levels/Required Class SizesCount/Grade Levels/Required Class Sizes

Make Initial Staff AssignmentsMake Initial Staff Assignments Estimate Salary Cost for Staff Based on Estimate Salary Cost for Staff Based on

Actual Salary Schedule or Schedule Actual Salary Schedule or Schedule from Negotiation Proposal (Any Grant-from Negotiation Proposal (Any Grant-Funded?)Funded?)

BudgetingBudgeting

It is not a spending limit.It is not a spending limit.

The revenue limit is “a The revenue limit is “a limit limit on the on the revenue a school district is revenue a school district is entitled to receive from entitled to receive from general general state aid* and local levies.”state aid* and local levies.”

*General state aid includes *General state aid includes equalization aid, special equalization aid, special adjustment aid and integration aidadjustment aid and integration aid

Budgeting: Preliminary Budgeting: Preliminary Revenue Limit – The BasicsRevenue Limit – The Basics

The limit includes revenue The limit includes revenue from levies for Funds 10, 38 from levies for Funds 10, 38 and 41.and 41.

Other sources of revenue are Other sources of revenue are not included in the revenue not included in the revenue limit - referendum debt service limit - referendum debt service levy (Fund 39), categorical aid, levy (Fund 39), categorical aid, grants, fees, community grants, fees, community service levy (Fund 80), etc.service levy (Fund 80), etc.

Budgeting: Preliminary Budgeting: Preliminary Revenue Limit – The BasicsRevenue Limit – The Basics

When you calculate your 2005-06 When you calculate your 2005-06 revenue limit, it’s important to revenue limit, it’s important to have your have your 2004-05 worksheet2004-05 worksheet available as well as the available as well as the October 15, October 15, 2004 aid certification.2004 aid certification.

Membership is very important to Membership is very important to the revenue limit calculation - have the revenue limit calculation - have an accurate an accurate estimateestimate of your Sept. of your Sept. 2005 FTE.2005 FTE.

Budgeting: Preliminary Budgeting: Preliminary Revenue Limit – The BasicsRevenue Limit – The Basics

Step 1:Step 1: Calculate the base (2004-05) Calculate the base (2004-05) revenue per member. revenue per member. (Worksheet lines 1 - 3)(Worksheet lines 1 - 3)

Step 2:Step 2: Calculate a new (2005-06) Calculate a new (2005-06) revenue per member amount prior to revenue per member amount prior to exemptions. exemptions. (Worksheet lines 4 - 7)(Worksheet lines 4 - 7)

Step 3:Step 3: Determine exemptions and Determine exemptions and add to New Revenue Limit per add to New Revenue Limit per Member. Member. (Worksheet lines 8 - 11)(Worksheet lines 8 - 11)

Budgeting: Preliminary Budgeting: Preliminary Revenue Limit – The BasicsRevenue Limit – The Basics

Step 4:Step 4: Determine portions of the Determine portions of the maximum limited revenue that are maximum limited revenue that are derived from:derived from:

– General AidGeneral Aid– Funds 10, 38, and 41Funds 10, 38, and 41– DOR Computer AidDOR Computer Aid

(Worksheet lines 12 - 18)(Worksheet lines 12 - 18)

Budgeting: Preliminary Budgeting: Preliminary Revenue Limit – The BasicsRevenue Limit – The Basics

What are the changes to the 2005-06 What are the changes to the 2005-06 revenue limit?revenue limit?

– Per member increasePer member increase

– Low spendingLow spending districts may districts may increase their per member increase their per member spending to spending to $8,100$8,100 in 05-06 if they in 05-06 if they want. want. (Governor’s Proposed Budget)(Governor’s Proposed Budget)

Budgeting: Preliminary Budgeting: Preliminary Revenue Limit – The BasicsRevenue Limit – The Basics

Budgeting: Preliminary Budgeting: Preliminary Revenue Limit – The BasicsRevenue Limit – The Basics

The 04-05 Final Revenue Limit provides information for the 05-06 base computation.

Budgeting: Preliminary Budgeting: Preliminary Revenue Limit – The BasicsRevenue Limit – The Basics

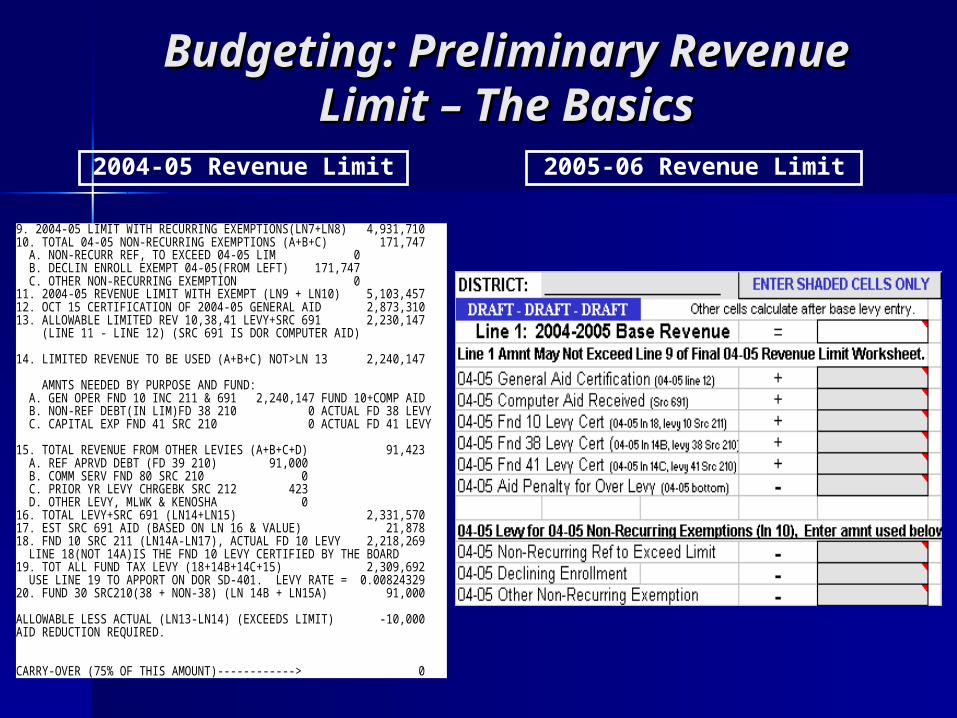

2004-05 Revenue Limit

2005-06 Revenue Limit

9. 2004-05 LIMIT WITH RECURRING EXEMPTIONS(LN7+LN8) 4,931,710 10. TOTAL 04-05 NON-RECURRING EXEMPTIONS (A+B+C) 171,747 A. NON-RECURR REF, TO EXCEED 04-05 LIM 0 B. DECLIN ENROLL EXEMPT 04-05(FROM LEFT) 171,747 C. OTHER NON-RECURRING EXEMPTION 0 11. 2004-05 REVENUE LIMIT WITH EXEMPT (LN9 + LN10) 5,103,457 12. OCT 15 CERTIFICATION OF 2004-05 GENERAL AID 2,873,310 13. ALLOWABLE LIMITED REV 10,38,41 LEVY+SRC 691 2,230,147 (LINE 11 - LINE 12) (SRC 691 IS DOR COMPUTER AID) 14. LIMITED REVENUE TO BE USED (A+B+C) NOT>LN 13 2,240,147 AMNTS NEEDED BY PURPOSE AND FUND: A. GEN OPER FND 10 INC 211 & 691 2,240,147 FUND 10+COMP AID B. NON-REF DEBT(IN LIM)FD 38 210 0 ACTUAL FD 38 LEVY C. CAPITAL EXP FND 41 SRC 210 0 ACTUAL FD 41 LEVY 15. TOTAL REVENUE FROM OTHER LEVIES (A+B+C+D) 91,423 A. REF APRVD DEBT (FD 39 210) 91,000 B. COMM SERV FND 80 SRC 210 0 C. PRIOR YR LEVY CHRGEBK SRC 212 423 D. OTHER LEVY, MLWK & KENOSHA 0 16. TOTAL LEVY+SRC 691 (LN14+LN15) 2,331,570 17. EST SRC 691 AID (BASED ON LN 16 & VALUE) 21,878 18. FND 10 SRC 211 (LN14A-LN17), ACTUAL FD 10 LEVY 2,218,269 LINE 18(NOT 14A)IS THE FND 10 LEVY CERTIFIED BY THE BOARD 19. TOT ALL FUND TAX LEVY (18+14B+14C+15) 2,309,692 USE LINE 19 TO APPORT ON DOR SD-401. LEVY RATE = 0.00824329 20. FUND 30 SRC210(38 + NON-38) (LN 14B + LN15A) 91,000 ALLOWABLE LESS ACTUAL (LN13-LN14) (EXCEEDS LIMIT) -10,000 AID REDUCTION REQUIRED. CARRY-OVER (75% OF THIS AMOUNT)------------> 0

2005-2006 Revenue Limit2005-2006 Revenue Limit

Go to Revenue Cap Go to Revenue Cap WorksheetsWorksheets

05-06 Revenue Limit Worksheet

2005-2006 Revenue Limit2005-2006 Revenue Limit

So, what does this So, what does this meanmean

for my district, and for my district, and how do I use this how do I use this information for information for

budgeting?budgeting?

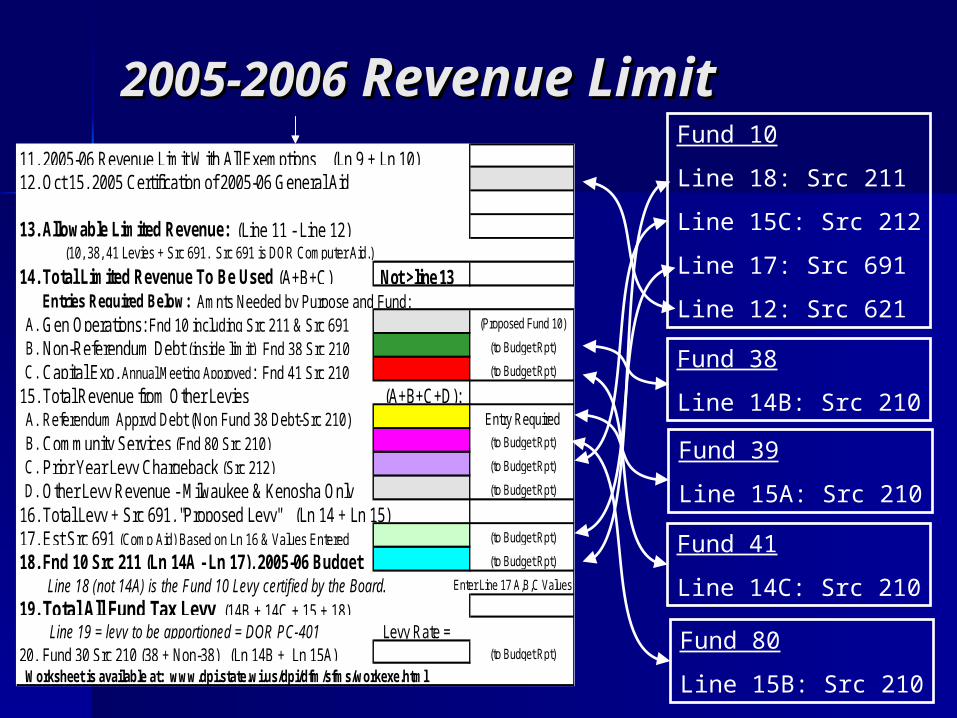

2005-20062005-2006 Revenue Limit Revenue LimitFund 10

Line 18: Src 211

Line 15C: Src 212

Line 17: Src 691

Line 12: Src 621

Fund 38

Line 14B: Src 210

Fund 39

Line 15A: Src 210

Fund 41

Line 14C: Src 210

Fund 80

Line 15B: Src 210

11. 2005-06 Revenue Limit With All Exemptions (Ln 9 + Ln 10)12. Oct 15, 2005 Certification of 2005-06 General Aid

13. Allowable Limited Revenue: (Line 11 - Line 12) (10, 38, 41 Levies + Src 691. Src 691 is DOR Computer Aid.)

14. Total Limited Revenue To Be Used (A+B+C) Not >line 13 Entries Required Below: Amnts Needed by Purpose and Fund:

A. Gen Operations: Fnd 10 including Src 211 & Src 691 (Proposed Fund 10)

B. Non-Referendum Debt (inside limit) Fnd 38 Src 210 (to Budget Rpt)

C. Capital Exp, Annual Meeting Approved: Fnd 41 Src 210 (to Budget Rpt)

15. Total Revenue from Other Levies (A+B+C+D):A. Referendum Apprvd Debt (Non Fund 38 Debt-Src 210) Entry Required

B. Community Services (Fnd 80 Src 210) (to Budget Rpt)

C. Prior Year Levy Chargeback (Src 212) (to Budget Rpt)

D. Other Levy Revenue - Milwaukee & Kenosha Only (to Budget Rpt)

16. Total Levy + Src 691, "Proposed Levy" (Ln 14 + Ln 15)17. Est Src 691 (Comp Aid) Based on Ln 16 & Values Entered (to Budget Rpt)

18. Fnd 10 Src 211 (Ln 14A - Ln 17), 2005-06 Budget (to Budget Rpt)

Line 18 (not 14A) is the Fund 10 Levy certified by the Board. Enter Line 17 A,B,C Values

19. Total All Fund Tax Levy (14B + 14C + 15 + 18) Line 19 = levy to be apportioned = DOR PC-401 Levy Rate =

20. Fund 30 Src 210 (38 + Non-38) (Ln 14B + Ln 15A) (to Budget Rpt)

Worksheet is available at: www.dpi.state.wi.us/dpi/dfm/sfms/workexe.html

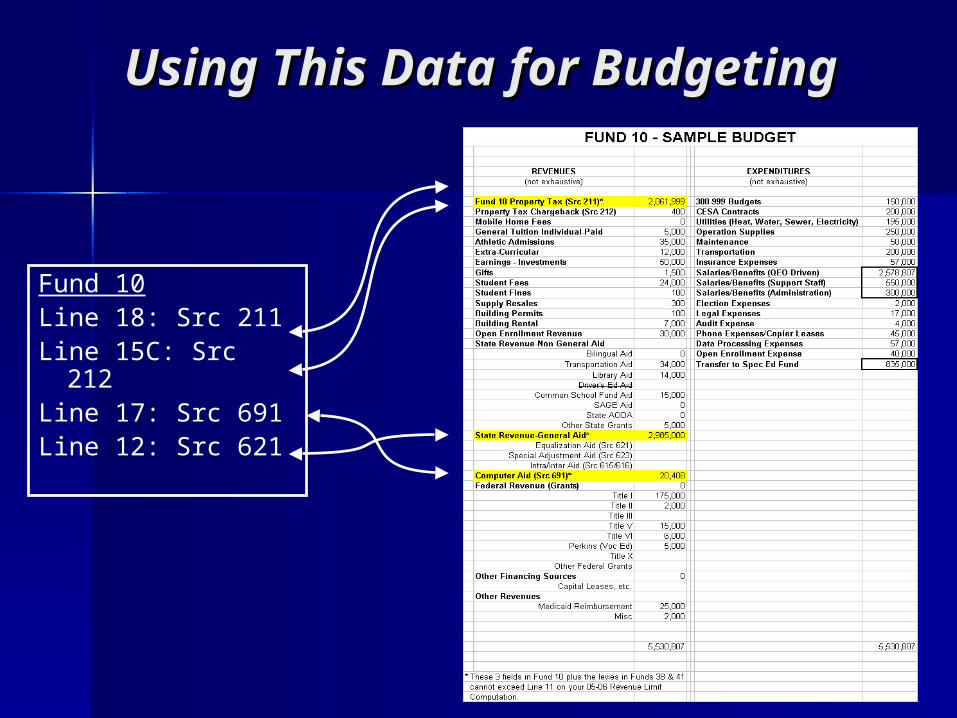

Using This Data for Using This Data for BudgetingBudgeting

Fund 10Line 18: Src 211Line 15C: Src

212Line 17: Src 691Line 12: Src 621

A bird’s eye view of your 2005-06 A bird’s eye view of your 2005-06 budget:budget:

Salary/Benefits vs. Revenue Limit

BudgetingBudgeting

Mid January: Mid January:

Determine Class-Level Budget AmountsDetermine Class-Level Budget Amounts Estimate District-Level Expenditures for Estimate District-Level Expenditures for

Utilities, Fuel, Operating Supplies, Utilities, Fuel, Operating Supplies, Maintenance Requirements, Transportation, Maintenance Requirements, Transportation, Insurance, Legal, Audit, Phone/Copier Insurance, Legal, Audit, Phone/Copier Leases, CESA Contracts, etc.Leases, CESA Contracts, etc.

Estimate all Revenues Outside of Revenue Estimate all Revenues Outside of Revenue Limit (Athletic Admissions, Earning on Limit (Athletic Admissions, Earning on Investments, Gifts, Fees, Fines, Categorical Investments, Gifts, Fees, Fines, Categorical Aid, Entitlement Grant Revenues, etc.)Aid, Entitlement Grant Revenues, etc.)

BudgetingBudgeting

February: February:

Develop Complete Picture, Identifying Develop Complete Picture, Identifying Structural Deficit and Level of CutsStructural Deficit and Level of Cuts

Develop Strategy to Absorb Deficit (BOE Develop Strategy to Absorb Deficit (BOE Finance Committee Involved)Finance Committee Involved)

Distribute Budget Parameters to Distribute Budget Parameters to Departments for Individual Budget Departments for Individual Budget DevelopmentDevelopment

BudgetingBudgeting

April: April:

By April 1, All Budgets Due in Budget By April 1, All Budgets Due in Budget Office (submitted via paper or software)Office (submitted via paper or software)

Start Final Compilation/Formulation of Start Final Compilation/Formulation of BudgetBudget

All cAll current-yearurrent-year purchase orders should be purchase orders should be submitted to business office by mid-April. submitted to business office by mid-April. This allows time to get materials for This allows time to get materials for current-year programs and for clearing out current-year programs and for clearing out purchase orders/encumbrances in purchase orders/encumbrances in preparation for year-end activities.preparation for year-end activities.

BudgetingBudgeting

Mid-April: Mid-April:

DPI Provides Early 05-06 General Aid DPI Provides Early 05-06 General Aid EstimatesEstimates

May:May:

Finalize 05-06 Budget. Approve for Finalize 05-06 Budget. Approve for Presentation at Annual Meeting.Presentation at Annual Meeting.

Before Checking Out for Summer, Staff Before Checking Out for Summer, Staff Fills Out Requisition/Purchase Orders for Fills Out Requisition/Purchase Orders for Items Wanted at the Beginning of 05-06Items Wanted at the Beginning of 05-06

BudgetingBudgeting

September: September:

33rdrd Friday Count Taken Friday Count Taken

October 15: October 15:

Update Revenue Limit Computation with Update Revenue Limit Computation with 33rdrd Friday Count and Aid Certification Friday Count and Aid Certification

November:November:

BOE Approves Levy. Tax Invoices Sent.BOE Approves Levy. Tax Invoices Sent.

BudgetingBudgeting

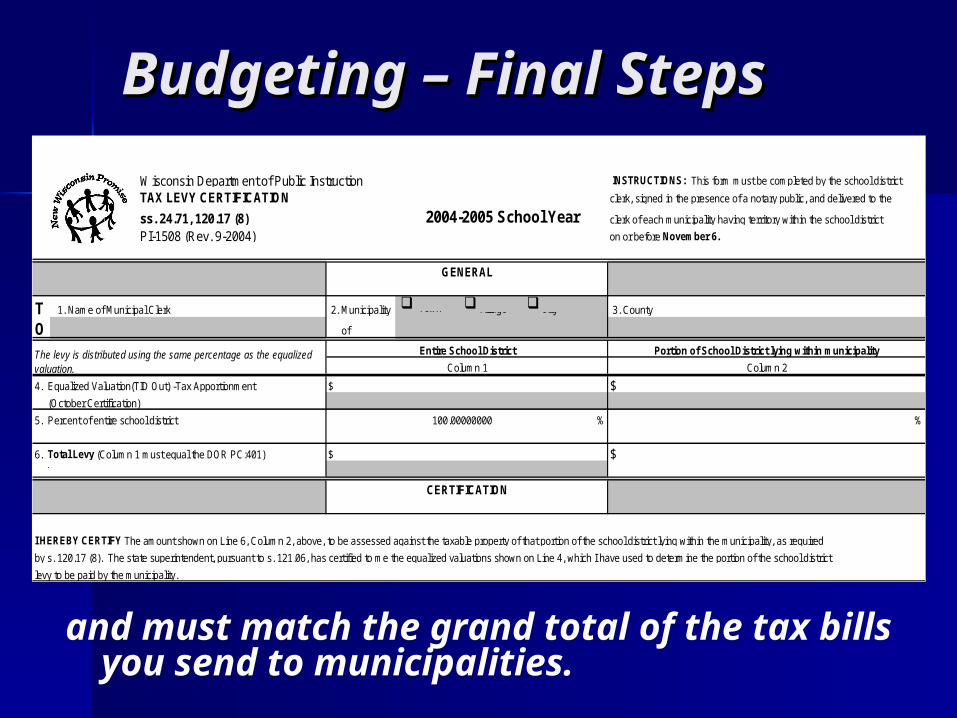

Budgeting – Final Budgeting – Final StepsSteps

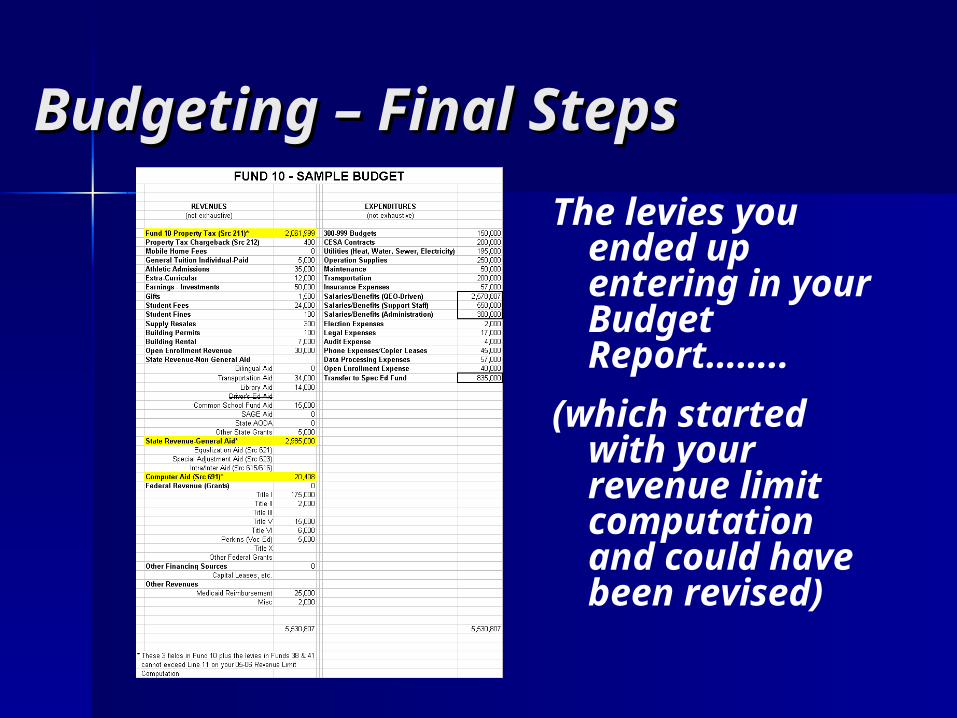

The levies you ended up entering in your Budget Report……..

(which started with your revenue limit computation and could have been revised)

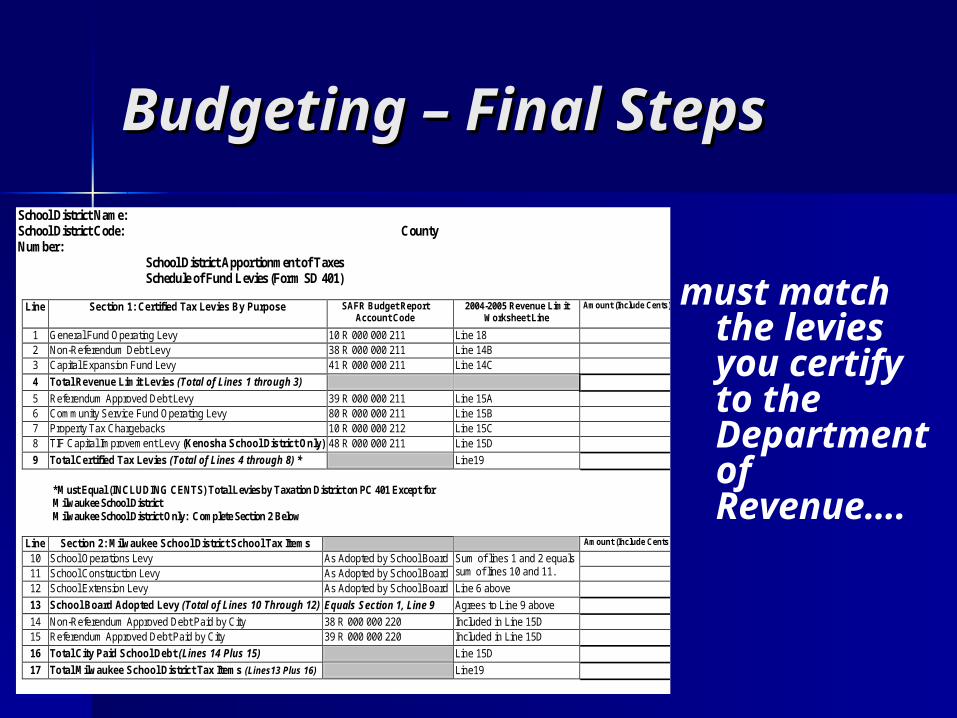

School District Name: School District Code: County Number:

School District Apportionment of Taxes Schedule of Fund Levies (Form SD 401)

Line Section 1: Certified Tax Levies By Purpose SAFR Budget Report

Account Code 2004-2005 Revenue Limit

Worksheet Line Amount (Include Cents)

1 General Fund Operating Levy 10 R 000 000 211 Line 18 2 Non-Referendum Debt Levy 38 R 000 000 211 Line 14B 3 Capital Expansion Fund Levy 41 R 000 000 211 Line 14C

4 Total Revenue Limit Levies (Total of Lines 1 through 3)

5 Referendum Approved Debt Levy 39 R 000 000 211 Line 15A 6 Community Service Fund Operating Levy 80 R 000 000 211 Line 15B 7 Property Tax Chargebacks 10 R 000 000 212 Line 15C 8 TIF Capital Improvement Levy (Kenosha School District Only) 48 R 000 000 211 Line 15D

9 Total Certified Tax Levies (Total of Lines 4 through 8) * Line19

*Must Equal (INCLUDING CENTS) Total Levies by Taxation District on PC 401 Except for Milwaukee School District Milwaukee School District Only: Complete Section 2 Below

Line Section 2: Milwaukee School District School Tax Items Amount (Include Cents)

10 School Operations Levy As Adopted by School Board 11 School Construction Levy As Adopted by School Board

Sum of lines 1 and 2 equals sum of lines 10 and 11.

12 School Extension Levy As Adopted by School Board Line 6 above

13 School Board Adopted Levy (Total of Lines 10 Through 12) Equals Section 1, Line 9 Agrees to Line 9 above

14 Non-Referendum Approved Debt Paid by City 38 R 000 000 220 Included in Line 15D 15 Referendum Approved Debt Paid by City 39 R 000 000 220 Included in Line 15D

16 Total City Paid School Debt (Lines 14 Plus 15) Line 15D

17 Total Milwaukee School District Tax Items (Lines13 Plus 16) Line19

Budgeting – Final Budgeting – Final StepsSteps

must match the levies you certify to the Department of Revenue….

Budgeting – Final Budgeting – Final StepsSteps

INSTRUCTIONS: This form must be completed by the school district

T 2. Municipality q q qO of

% %

Total Levy in Column 5.)

levy to be paid by the municipality.

I HEREBY CERTIFY The amount shown on Line 6, Column 2, above, to be assessed against the taxable property of that portion of the school district lying within the municipality, as required

by s. 120.17 (8). The state superintendent, pursuant to s. 121.06, has certified to me the equalized valuations shown on Line 4, which I have used to determine the portion of the school district

3. County

Portion of School District lying within municipality

Column 2

$

$

CERTIFICATION

$

(October Certification)

5. Percent of entire school district

6. Total Levy (Column 1 must equal the DOR PC:401)

1. Name of Municipal Clerk

4. Equalized Valuation(TID Out) -Tax Apportionment

clerk, signed in the presence of a notary public, and delivered to the

clerk of each municipality having territory within the school district

on or before November 6.

Entire School District

Wisconsin Department of Public InstructionTAX LEVY CERTIFICATION

ss. 24.71, 120.17 (8)PI-1508 (Rev. 9-2004)

2004-2005 School Year

GENERAL

100.00000000

$

Column 1The levy is distributed using the same percentage as the equalized valuation.

Town Village City

and must match the grand total of the tax bills you send to municipalities.

Budgeting & Revenue LimitBudgeting & Revenue Limit- Problem Areas -- Problem Areas -

Don’t forget to budget Open Enrollment Don’t forget to budget Open Enrollment Revenues and Expenditures.Revenues and Expenditures.

Be careful to not overlevy by your computer Be careful to not overlevy by your computer aid. The Fund 10 levy is aid. The Fund 10 levy is line 18line 18 from your from your revenue limit computation.revenue limit computation.

After October 15, remember to update your After October 15, remember to update your revenue limit with the October 15revenue limit with the October 15thth Aid Aid Certification.Certification.

Questions?Questions?

Visit our web site: Visit our web site: www.dpi.state.wi.us/dpi/dfm/sfmswww.dpi.state.wi.us/dpi/dfm/sfms

Or call:Or call:

Brad Adams, Consultant, 267-3752Brad Adams, Consultant, 267-3752 Karen Kucharz, Consultant, 267-9707Karen Kucharz, Consultant, 267-9707 Jerry Landmark, Assistant Dir., 264-Jerry Landmark, Assistant Dir., 264-

34643464 Gene Fornecker, Auditor, 267-7882Gene Fornecker, Auditor, 267-7882 Natalie Rew, Auditor, 267-9212 Natalie Rew, Auditor, 267-9212 Kathryn Guralski, Auditor, 266-3862Kathryn Guralski, Auditor, 266-3862 David Carlson, Director, 266-6968David Carlson, Director, 266-6968