Embed Size (px)

Citation preview

VERITASL A N D D E V E L O P E R S

AGROTM

2 0 r e a s o n s t o i n v e s t i n b r a z i l

D e s c l i n i n g s u p p ly o f a r a b l e l a n d f r o m t o p 3 a g r i c u lt u r a l p r o d u c e r s

United Sates

200.000.000,00

180.000.000,00

160.000.000,00

140.000.000,00

120.000.000,00

100.000.000,00

80.000.000,00

60.000.000,00

40.000.000,00

20.000.000,00

0,00

Ha

India China

veritasagro.com

Source: World Bank & UN

1989

1999

2009

VERITASL A N D D E V E L O P E R S

AGROTM

The foof & Agriculture Organisation (FAO) of the United Nations has calculated that the global foodproduction will have to increase bt 70% in order to continue meeting de growing demand.

veritasagro.com

50

45

40

35

30

25

20

15

10

5

0

Glo

bal f

ood

dem

and

(pet

acal

/ day

)

1500 1550 1600 1650 1700 1750 1800 1850 1900 1950 2000 2050

The challenge to produce enough food will be greater over the next 50 years than in all human history.

VERITASL A N D D E V E L O P E R S

AGROTM

Brazil exports more soybeans than USA

LEADERSHIP

veritasagro.com

2011 2012 2013 Soy in the paranaguá port

40,9

Brazil

33,837,0

30,528,7

37,5

Annual volumes, calculated in million tonnes.

USA

VERITASL A N D D E V E L O P E R S

AGROTM

Investing in farmland means investing in rural land along whit specific crop livestock assets:

FARMLAND

veritasagro.com

Soybeans

Cotton

Paper

Meat

Dair y products

Lumber

Global populat ionis expected toincrease

50%by some

Food demandis set to grow by over

60%as the word becomes wealthier

2014

2014

2055

2055

VERITASL A N D D E V E L O P E R S

AGROTM

WORLD POPULATION GROWTH

veritasagro.com

10

9

8

7

6

5

4

3

2

1

01 9 5 0 1 9 6 0 1 9 7 0 1 9 8 0 1 9 9 0 2 0 0 0 2 0 1 0 2 0 2 0 2 0 3 0 2 0 4 0 2 0 5 0

Wor

ld P

opul

atio

n in

bill

ions

Year

Europe Sub-Saharan Africa Asia ( excl. W-Asia ) & Oceania Latin-America & Caribbean N-Africa/W-Asia

VERITASL A N D D E V E L O P E R S

AGROTM

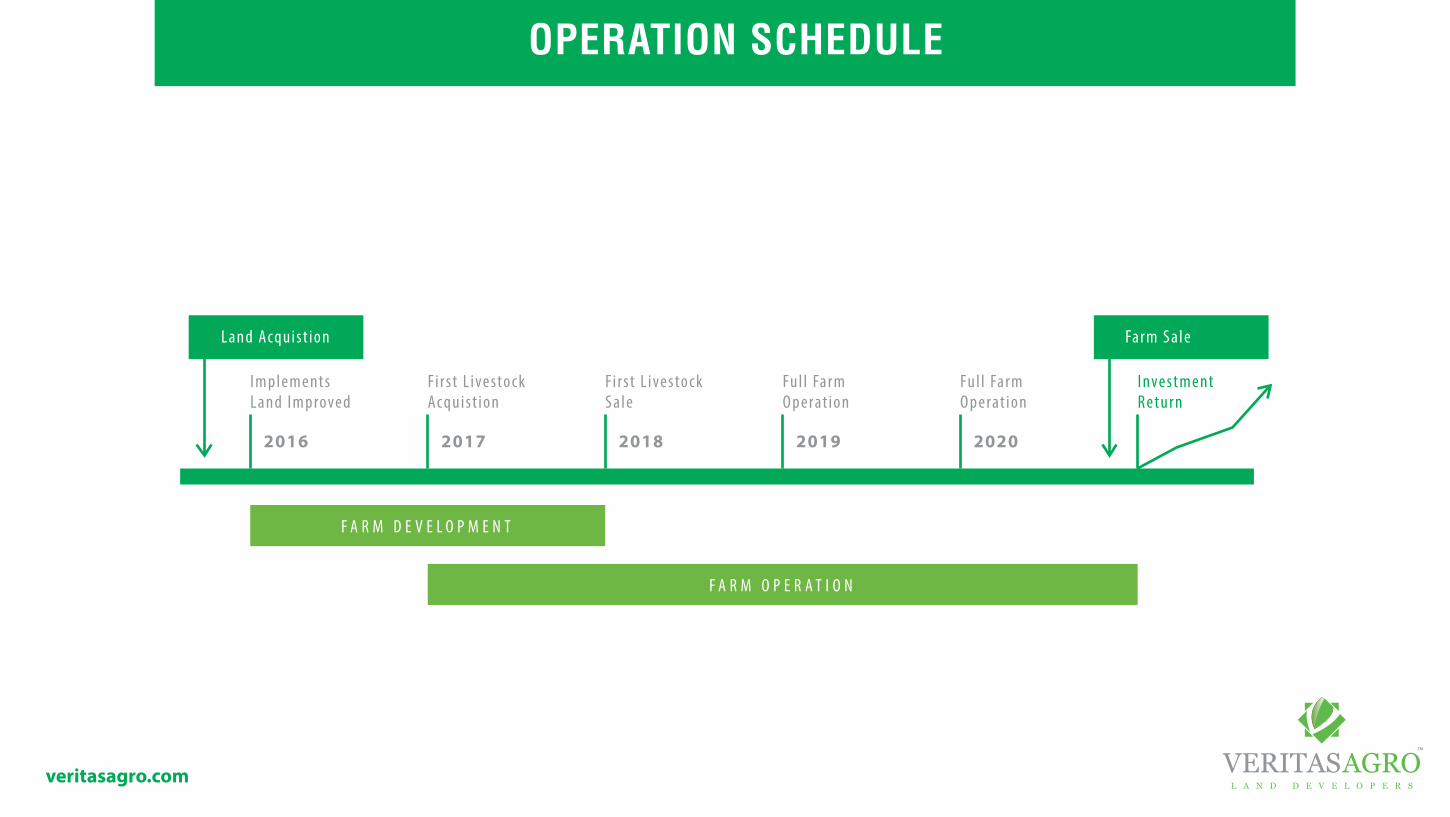

OPERATION SCHEDULE

veritasagro.com

I m p l e m e nt sLa n d I m p rove d

Fi r s t L i ve s to c kAcq u i s t i o n

F A R M D E V E L O P M E N T

F A R M O P E R A T I O N

Fi r s t L i ve s to c kS a l e

Fu l l Fa r mO p e rat i o n

Fu l l Fa r mO p e rat i o n

I nve s t m e ntR e t u r n

2016 2017 2018 2019 2020

La n d Acq u i s t i o n Fa r m S a l e

VERITASL A N D D E V E L O P E R S

AGROTM

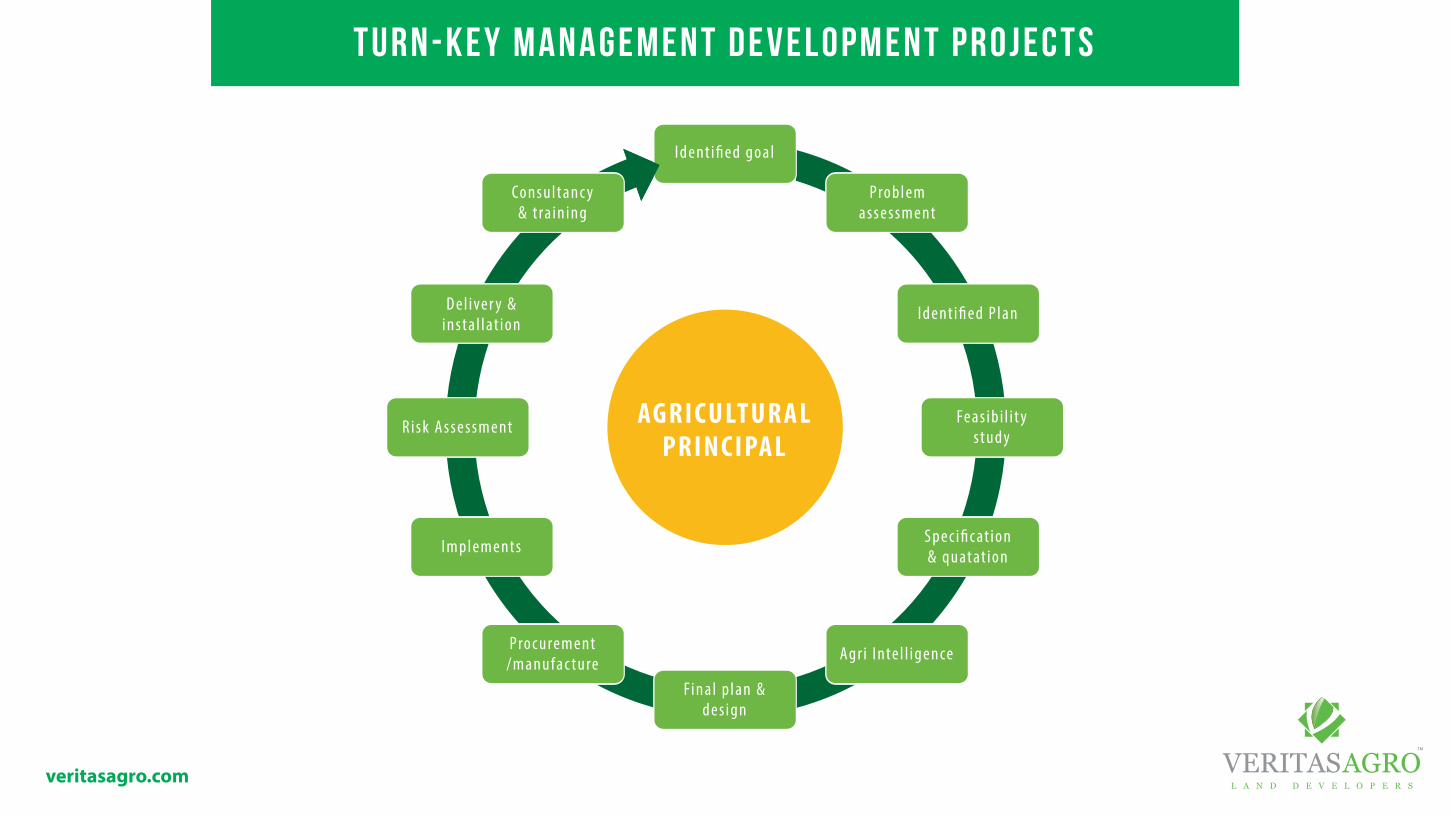

t u r n - k e y m a n a g e m e n t d e v e l o p m e n t p r o j e c t s

veritasagro.com

Id e nt i � e d g o a l

Co n s u l t a n c y& t ra i n i n g

D e l i ve r y &i n s t a l l at i o n

Fe a s i b i l i t ys t u d y

AG R I C U LT U R A LP R I N C I PA L

S p e c i � c at i o n& q u at at i o n

R i s k A s s e s s m e nt

Id e nt i � e d P l a n

Ag r i I nte l l i g e n ce

I m p l e m e nt s

Pro c u re m e nt/ m a n u f a c t u re

Fi n a l p l a n &d e s i g n

Pro b l e ma s s e s s m e nt

VERITASL A N D D E V E L O P E R S

AGROTM

veritasagro.com

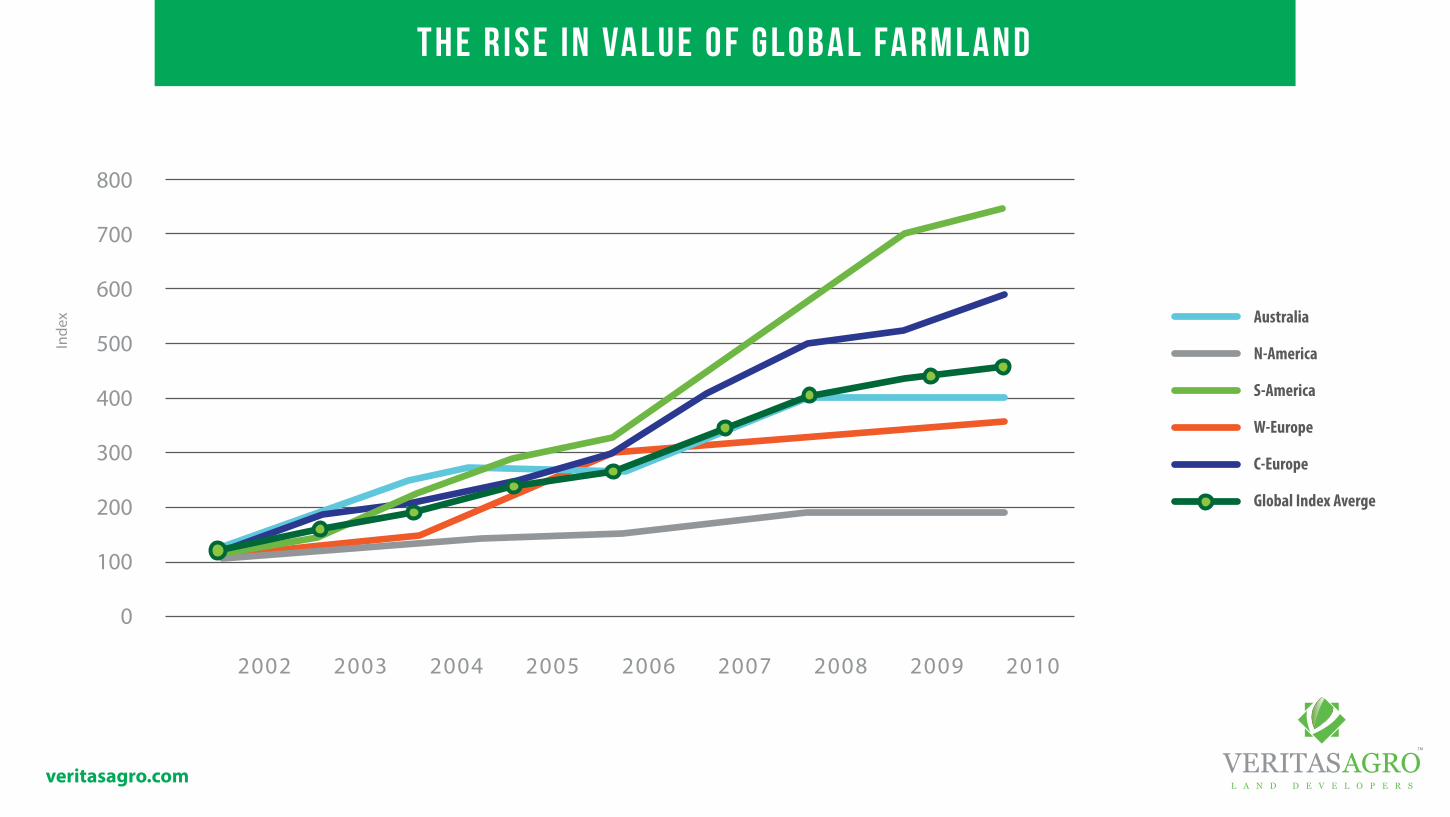

800

700

600

500

400

300

200

100

0

Australia

N-America

S-America

W-Europe

C-Europe

Global Index Averge

Inde

x

2002 2003 2004 2005 2006 2007 2008 2009 2010

t h e r i s e i n va l u e o f g l o b a l fa r m l a n d

VERITASL A N D D E V E L O P E R S

AGROTM

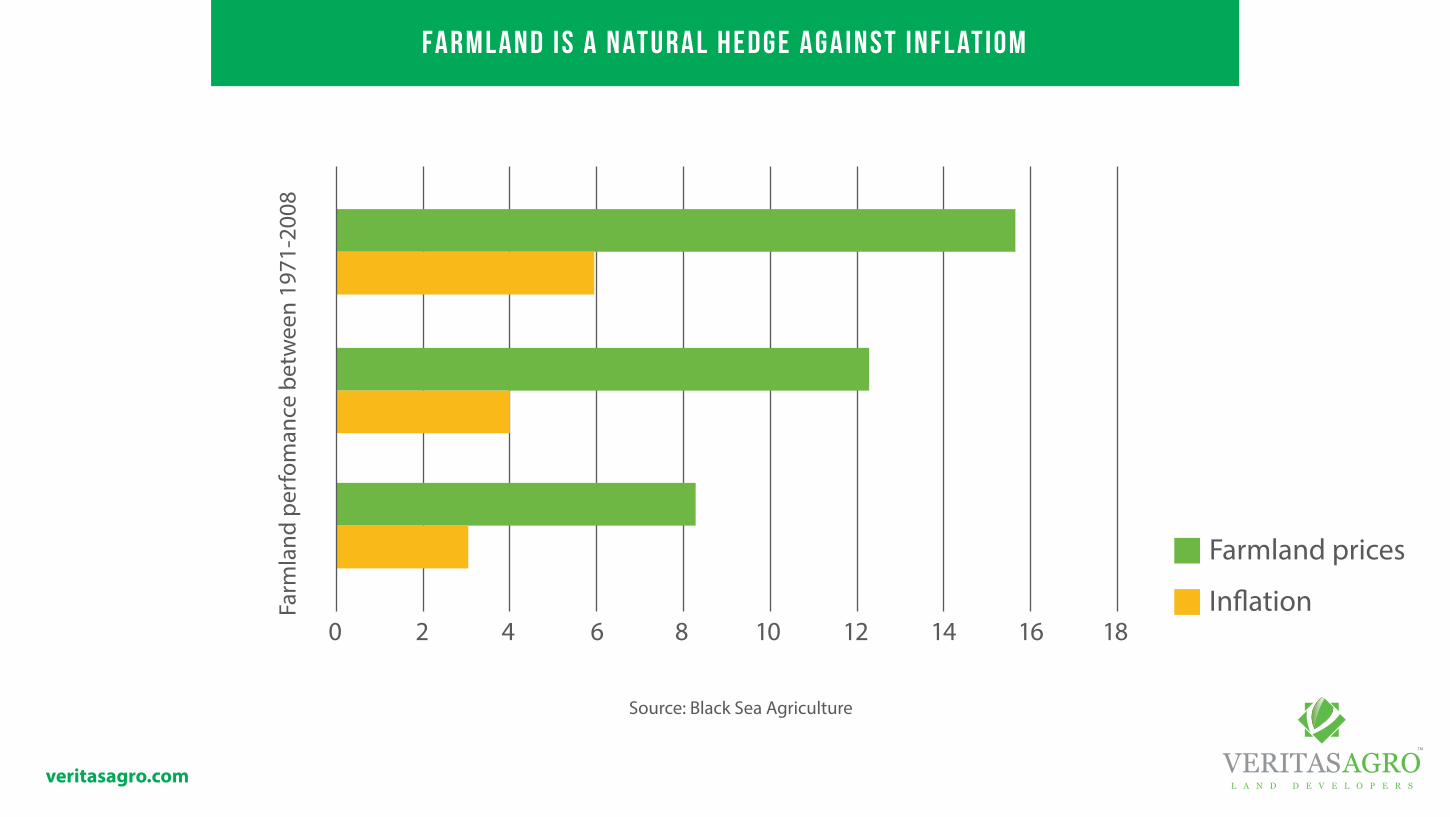

fa r m l a n d i s a n at u r a l h e d g e a g a i n s t i n f l at i o m

veritasagro.com

Source: Black Sea Agriculture

Farmland prices

In�ation

VERITASL A N D D E V E L O P E R S

AGROTM

Farm

land

per

fom

ance

bet

wee

n 19

71-2

008

0 2 4 6 8 10 12 14 16 18

g l o b a l d e m a n d i s g r o w i n g fa s t e r t h a n s u p p ly

veritasagro.com

Global Demand Components Global Supply Components

Estimated Annual World CropDemand Growth 3.1% - 3.9% Estimated Annual World Crop

Supply Growth 1.3% - 1.9%

VERITASL A N D D E V E L O P E R S

AGROTM

Food2.2% - 2.8%

Energy0.9% - 1.1%

Farmland0.2% - 0.2%

Productivity1.1% - 1.7%

Source: Food and Agricultural Organization of the United Nation; U.S. Census buerau; and IFC Analysis

WORLD POPULATION AND FARMLAND 1960-2020

veritasagro.com VERITASL A N D D E V E L O P E R S

AGROTM

Bill

iom

€

ha/

per

son

9

8

7

6

5

4

3

2

1

0

0,5

0,45

0,4

0,35

0,3

0,25

0,2

0,15

0,1

0,05

01960 1970 1980 1990 2000 2010 2020 2030

World population Farmland

farmland vs “top 3 big investments”

veritasagro.com VERITASL A N D D E V E L O P E R S

AGROTM

800

700

600

500

400

300

200

100

0

-100

Ind

ex

Shiller House Price Index

S&P Composite Index

Gold

NCRIEF Investment Farmland index

19911992

19931994

19951996

19971998

19992000

20012002

20032004

20052006

20072008

20092010

2011

2008 2009 2010

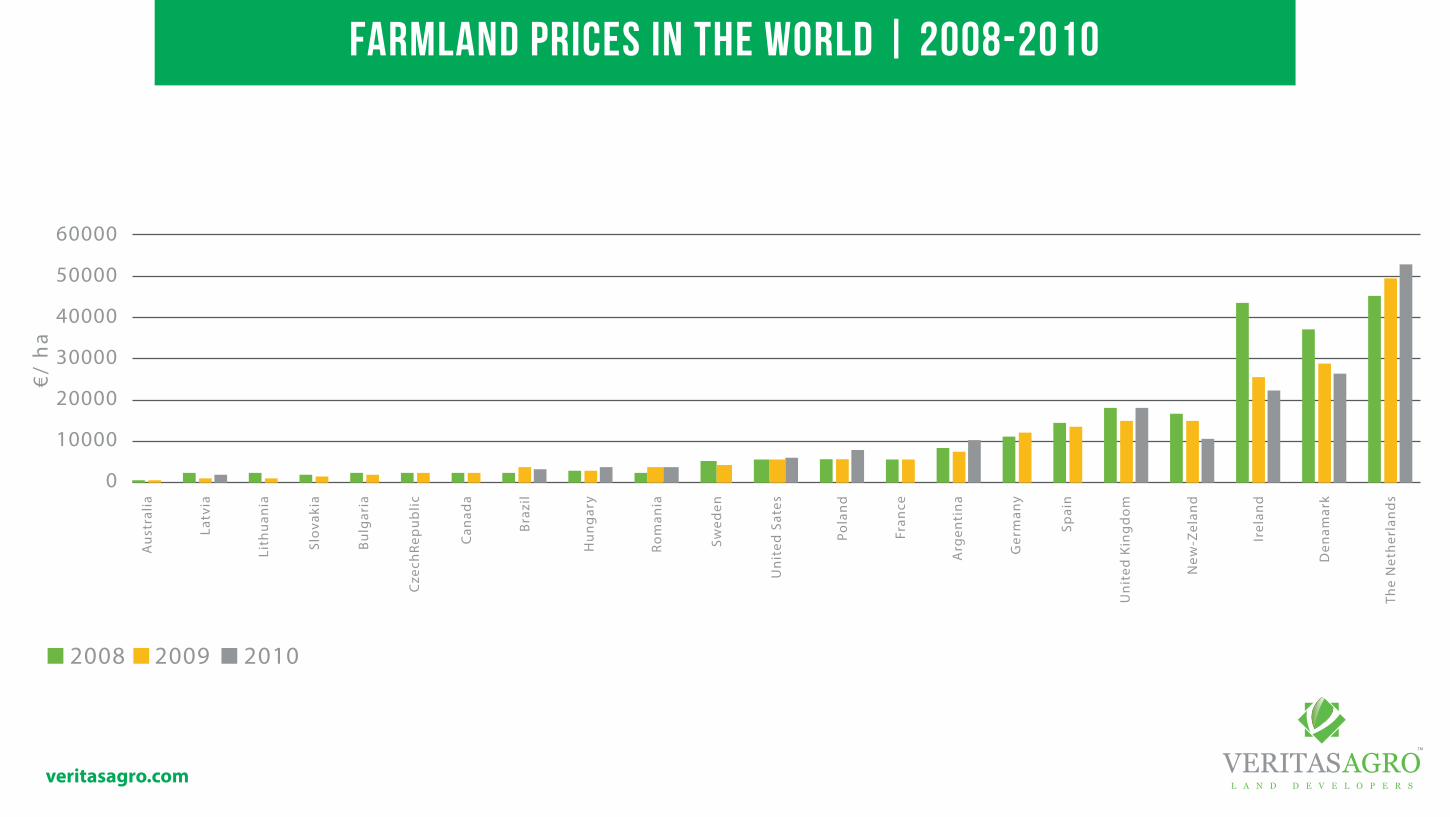

farmland prices in the world | 2008-2010

veritasagro.com VERITASL A N D D E V E L O P E R S

AGROTM

€/

ha

60000

50000

40000

30000

20000

10000

0

INVESTMENT AT GLANCE

veritasagro.com VERITASL A N D D E V E L O P E R S

AGROTM

SPECIALIZED CONSULTANCY

Veritas Agro o�ers a complete consultancy service to you, from the choice of a suitable land for agricultural activities to the selection of the commodity with the best pro�tability.

THE BEST LAND PRICES

Brazilian farmlands have the highest value an the best market price because of its abundance of natural and technological resources for agricultural production.

REFORESTRY

We are your partners in reforestation, which is the most pro�table long-term investment.

LEGAL SECURITY

We o�er legal and environmental consultancy for your safety in the buying process.

THE BEST FARMLANDS

We sell, exclusively, brazilian lands, which are the most bene�cial, valued and pro�table in the buy-to-lease model in the world.

THE LARGEST ROI

Brazil is one of the nations prepared to supply the food shortages, gaining pro�ts and a great return on investment (ROI) for the farmers in the process.

expansion of production capacity in brazil and in the world

veritasagro.com VERITASL A N D D E V E L O P E R S

AGROTM

brasil world

cerealskg/ha

fruitskg/ha

vegetable oilskg/ha

legumeskg/ha

201219901951

178,

222

6,7

293,

340

7,3

492,

6 6

32,9

201219901951

3,7

k

9,

3 k

14 k

14

,6 k

23,1

k19

,3 k

201219901951

191,

716

1,7

182,

9 2

06,5

231,

521

3,6

201219901951

10 k

1

1,4

k

13,

4 k

13 k

2

1,9

k15

,5 k

201219901951

12,

3 k

7,1

k

12,9

k8,

5 k

1

6,4

k11

,2 k

201219901951

1,3

k1,

3 k

4,

5 k

3,6

k

1,7

k

2

,7 k

beefkg/animal

chicken meatkg/animal

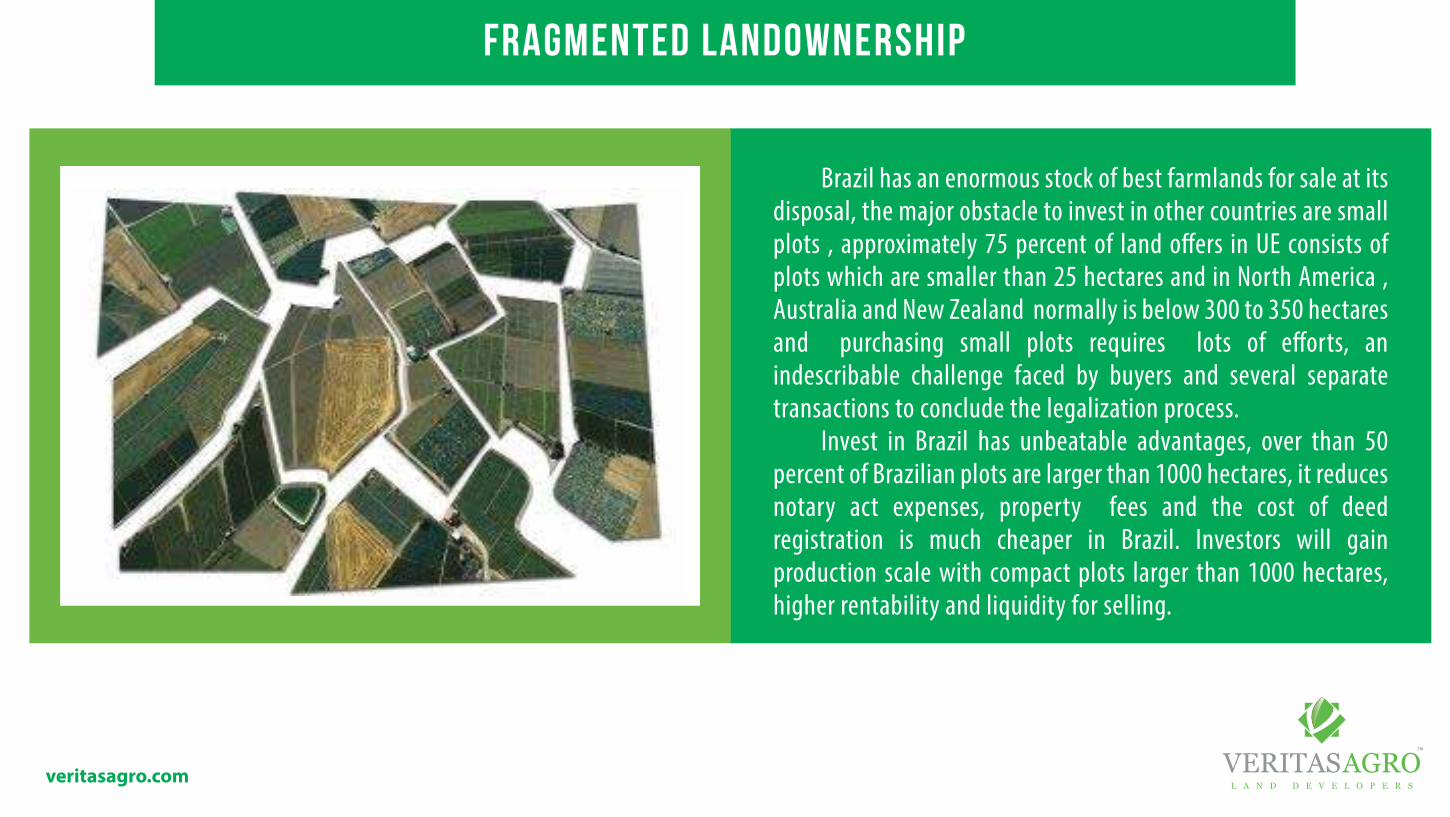

FRAGMENTED LANDOWNERSHIP

veritasagro.com VERITASL A N D D E V E L O P E R S

AGROTM

Brazil has an enormous stock of best farmlands for sale at its disposal, the major obstacle to invest in other countries are small plots , approximately 75 percent of land o�ers in UE consists of plots which are smaller than 25 hectares and in North America , Australia and New Zealand normally is below 300 to 350 hectares and purchasing small plots requires lots of e�orts, an indescribable challenge faced by buyers and several separate transactions to conclude the legalization process. Invest in Brazil has unbeatable advantages, over than 50 percent of Brazilian plots are larger than 1000 hectares, it reduces notary act expenses, property fees and the cost of deed registration is much cheaper in Brazil. Investors will gain production scale with compact plots larger than 1000 hectares, higher rentability and liquidity for selling.

i n v e s t m e n t p r o c e s s

veritasagro.com VERITASL A N D D E V E L O P E R S

AGROTM

region selectionindexing

investmentopportunities

performingpurchase

operationalimplementation

porfoliomanagement exit

• Soil quality

• Weather conditions

• Water

• Infrastructure storage and distribution

• Availability lands to be consolidated

• Selection Contrast farmers

• Contract exit planning

• Supervision sales process

• Appoint land agents if required

• Negotiations

• Supervision juridical route

• Manage exit process

• Supervision of portfolio

• Strategic advice

• Financial reporting

• Independent valuations

• Quartely reportowner/investor

• Proposal �nal/ optional operational scenario

• Cheice farm operator/farm manage/track record

• formalize contract with farm operator

• Agrinvestment strategy

• Due diligence

• Feasibility study

• Negotiations

• Supervision juridical reute

• Purchase

• Notery act

• Local network

• Local purchasing & consolidating land agent tearms

• Collecting and analysing appreciation & aggregation possibilities

• environmental consultancy

I N V E S T M E N T D I L L I G E N C E H I G H L I G H T S

veritasagro.com VERITASL A N D D E V E L O P E R S

AGROTM

Our investors receive the Brazilian Permanent Visa through investment plan.

With our real estate guidance, you will invest in the right place.

Investing in agribusiness sector generates your highest ROI and uncomparable pro�tability.

Our consultancy guides you to choose the best commodity.

We o�er advice to your land be in accordance with the environmental laws.

We gie you a customized project of the land following your pro�le.

permanent resident visa

liquidity

return on investment

choice of commodity

environmental legislation

right direction

Reasons to invest in brazilian farmlands

veritasagro.com VERITASL A N D D E V E L O P E R S

AGROTM

Many investor have doubts about which investment brings a higher liquidity. In the real estate business, there is a big dilemma on the most advantageous for the investor and in the upcomming decades the demand for arable land will increase metereocally.

In Brazil, the average price of one hectare of rural land has more than tripled in ten years, driven by the increase in the quotes of soybean/corn on the international market, and far exceeded in�ation. Moreover, in �ve years between 2008 and 2012, the land was valued at a faster pace than the dollar, investments in �xed income, equities and even gold.

H i g h e r p r o � t a b i l i t y

T h e b e s t r e t u r n o n i n v e s t m e n t

l o w l e v e l o f r i s k

S h i e l d a g a i n s t e c o n o m i c c r i s e s

S t a b i l i t y w i t h m o r e r e n t a b i l i t y

H i g h f o o d p r i c e s

comparison of rural and urban assets

veritasagro.com VERITASL A N D D E V E L O P E R S

AGROTM

Brazil has a vast amount of fresh water, wich represents about 12% of the word’s surface water resources. Besides that, about 90% of the Brazilian territory receives abundant rainfall during the year, wich favors the formation of an extensive and dense network of rivers and increases agricultural production.

From this, is possible to realize that Brazilian farmlands are the best investment in agribusiness. You can be sure that Brazil has the most productive and pro�table ground on the planet.

A p p r o p r i a t e c l i m a t e

H i g h t e c h n o l o g y

P l a n t o p o g r a p h y

T h e m o s t p r o d u c t i v e l a n d s

U n d e r v a l u e d p r i c e s

Tw o c r o p s p e r y e a r

w e l c o m e t o b r a z i l

VERITASL A N D D E V E L O P E R S

AGROTM