Embed Size (px)

Citation preview

11/16/2018

©Packaging Strategies 2018

Flexible Packaging

Key Growth Opportunities in North America and Beyond

11/16/2018

©Packaging Strategies 2018

About Smithers Pira

11/16/2018

©Packaging Strategies 2018

Session ObjectivesProvide an overview of the flexible packaging market

Outline where the growth is happening

• End use segments

• Geographically• Materials/technologies

3

11/16/2018

©Packaging Strategies 2018

Flexible Packaging Definition

Flexible plastic packaging which can come in

• Bags and flat pouches• Stand‐up pouches• Other consumer flexible plastic

packaging products

Flexible paper packaging

Flexible foil packaging

4

Polymers

Paper Foil

2018 Global Flexible Packaging Demand($US millions)

11/16/2018

©Packaging Strategies 2018

Global Demand

5

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

2017 2022

Global Demand($US millions)

Category 2017‐2022CAGR

Consumer 4.7%

Industrial 3.9%

Total volume projected to grow by 4.1%

Total value projected to grow by 4.3%

Global GDP projected to grow by 3.6%

Sources: IMF

11/16/2018

©Packaging Strategies 2018

Growth Driver:Shipping Friendly

Lightweight

More units per case/pallet

Durable – less damage

Less protective packaging

6

11/16/2018

©Packaging Strategies 2018

Growth Driver:Product Protection

Readily adaptable to new market opportunities marijuana packaging

7

Versatile

High‐barrier and retort formats – no need for chill chain

Suitable for developing markets

11/16/2018

©Packaging Strategies 2018

Growth Driver:Supply Chain Efficiency

Form‐fill‐seal (FFS) film materialis shipped empty

Greater inventory control/less warehouse space for the converter

Vertical FFS machine speeds improving ~250 pouches/minute

8

11/16/2018

©Packaging Strategies 2018

Growth Challenge: Sustainability

9

A new focus on plastics – tough EU recycling targets, but a global issue

Brands and retailers making tough commitments

• Nestlé• Unilever• Danone• Tesco• Walmart

11/16/2018

©Packaging Strategies 2018

Growth Challenge : Sustainability Enablers

• Monopolymer packs • Fewer layers in multilayer designs • Help commercialize biopolymers• Better barrier materials • Market opportunity for new lines

incorporating post‐consumer resins• Education

10

11/16/2018

©Packaging Strategies 2018

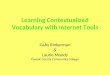

Asia‐Pacific

North America

Western Europe

Eastern Europe

Middle East & Africa

South America

2017 Global Flexible Packaging Demand($US millions)

Asia‐Pacific dominates and is growing fastest

North America second largest market

South America now returning to growth

Regional Demand

11/16/2018

©Packaging Strategies 2018

End Use Segment: United States

12

‐ 50

100 150

200

250 300

350 400

450

500

2017 United States Flexible Packaging Demand(000s tonnes)

Food Non‐Food

11/16/2018

©Packaging Strategies 2018

Packaging Format Demand: North America

13

‐ 40,000 80,000 120,000 160,000

Bags, flat pouches, and sachets

Stand‐up pouches

Rigid plastic bottles

Rigid plastic tubs, pots, and jiggers

Metal cans

2017 North America Packaging Format Demand(Packs millions)

11/16/2018

©Packaging Strategies 2018

PE

BOPP

BOPET

CPP

PVC

BOPA EVOH

2018 Global Flexible Plastic Packaging Demand(000s tonnes)

Polyethylene is the utilitarian material

BOPP is the fastest growing: 5.7% CAGR (2017‐2022)

PVC is the only material declining in usage

Substrate Demand: Flexible Plastic

11/16/2018

©Packaging Strategies 2018

Growth Opportunity:Digital printDigital (toner and inkjet) print advantages

• Economical short‐runs• Fast turnaround on print orders

Premium cost, but delivers extra consumer engagement

• Customized packaging • Short‐term promotional

packaging

15

11/16/2018

©Packaging Strategies 2018

Growth Opportunity:Digital print

Enablers• Technology and market

proposition has been pioneered on label presses

• Print equipment manufacturers developing higher throughput presses

• Graphic quality also improving

16

11/16/2018

©Packaging Strategies 2018

Growth Opportunity:E‐commerceE‐commerce booming $1.9 trillion (2016)

Direct‐to‐consumer packaging value is $32.9 billion (2018)

• 80% is corrugated/paperboard• 15 % is flexibles ($4.94 billion)

Fashion is the key segment for flexibles

17

11/16/2018

©Packaging Strategies 2018

Growth Opportunity:E‐commerce

Unique ecommerce packaging requirements• Frustration free packaging• Easily returnable• Dim weight reduction• Environmental protection

18

11/16/2018

©Packaging Strategies 2018

ConclusionsFlexible packaging is growing faster than many other forms

• Shipping friendly• Product protection• Supply chain efficiency

It includes trends that can be used to drive market growth

• Digital printing• Ecommerce• Sustainability

19

11/16/2018

©Packaging Strategies 2018

How do I learn more? Our exclusive content:

• Quantitative value and volume forecasts for all flexible packaging materials across key packaging applications and geographic markets

• In‐depth analysis of the evolution of the plastic, foil and paper supply and value chains

• Over 150 tables and figures providing data and strategic insight in a concise, easy‐to‐use format

What will you discover?

• Extensive analysis on future demand for flexible packaging, across all key world markets, contextualized within the evolution of the wider global packaging market

• Expert qualitative analysis of the state‐of‐the‐art technologies that are fuelling the ongoing growth of flexible packaging formats.www.smitherspira.com

20

11/16/2018

©Packaging Strategies 2018

More Smithers Pira Reports

21

• The Future Lifecycles of Packaging Recycling to 2023

• The Future of Recycled Packaging to 2023

• The Future of Printing for Food Packaging to 2023

• The Future of E‐commerce Packaging to 2022 (updating in 2019)

• The Future of Bioplastics for Packaging to 2022

11/16/2018

©Packaging Strategies 2018

Questions

www.smitherspira.com

Duane Neidert

Head of Consultancy, Americas

Phone: 330.762.7441

Email: [email protected]

22

![Designing Contextualized Learning · Designing Contextualized Learning Marcus Specht [marcus.specht@ou.nl], Educational Technology Expertise Centre, Open Universiteit Nederlands,](https://img.pdfslide.us/doc/110x75/600a6e9f96d1e569916acb11/designing-contextualized-learning-designing-contextualized-learning-marcus-specht.jpg)