Embed Size (px)

Citation preview

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 1/45

1

Lehman ShockAn Insider’s Perspective

Jean-Paul LEBOUTET

SLIDES FOR FURTHER REFERENCE

GLOBIS UNIVERSITY SEMINARS, 16 December 2011

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 2/45

2 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 2

DEVELOPMENT AND BURST OF THE BUBBLE

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 3/45

3 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 3

Subprime mortgage financing has been only a limited part of the whole market,but it jeopardized investors’ confidence

45%

50%

5%

Value of all housing in the USA at end of June 2008 (Fed):19,300 billion $

Equity Prime Mortgage Subprime

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 4/45

4 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 4

Ascension and decline of the Case-Schiller Index (Real Estate prices, USA)

50.00

70.00

90.00

110.00

130.00

150.00

170.00

190.00

210.00

M a r - 8 7

O c t - 8 7

M a y - 8 8

D e c - 8 8

J u l - 8 9

F e b - 9 0

S e p - 9 0

A p r - 9 1

N o v - 9 1

J u n - 9 2

J a n - 9 3

A u g - 9 3

M a r - 9 4

O c t - 9 4

M a y - 9 5

D e c - 9 5

J u l - 9 6

F e b - 9 7

S e p - 9 7

A p r - 9 8

N o v - 9 8

J u n - 9 9

J a n - 0 0

A u g - 0 0

M a r - 0 1

O c t - 0 1

M a y - 0 2

D e c - 0 2

J u l - 0 3

F e b - 0 4

S e p - 0 4

A p r - 0 5

N o v - 0 5

J u n - 0 6

J a n - 0 7

A u g - 0 7

M a r - 0 8

O c t - 0 8

M a y - 0 9

D e c - 0 9

J u l - 1 0

F e b - 1 1

Case-Shiller Index

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 5/45

5 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Equity, Real Estate and GPD growth in the USA – 2003 to 2006

95

105

115

125

135

145

155

Census House Purchase Price S&P 500 current $ US GDP

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 6/45

6 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 7/457 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Major Stock Indices through 2 bubbles

600700

800

900

1000

1100

1200

1300

1400

1500

1600

S&P 500 Index

300035004000450050005500600065007000

FTSE 100 Index

500070009000

1100013000150001700019000

2100023000

NIKKEI 225

2000

3000

4000

50006000

7000

9 6 . 0

1 . 0

1

9 6 . 0

8 . 0

1

9 7 . 0

3 . 0

1

9 7 . 1

0 . 0

1

9 8 . 0

5 . 0

1

9 8 . 1

2 . 0

1

9 9 . 0

7 . 0

1

0 0 . 0

2 . 0

1

0 0 . 0

9 . 0

1

0 1 . 0

4 . 0

1

0 1 . 1

1 . 0

1

0 2 . 0

6 . 0

1

0 3 . 0

1 . 0

1

0 3 . 0

8 . 0

1

0 4 . 0

3 . 0

1

0 4 . 1

0 . 0

1

0 5 . 0

5 . 0

1

0 5 . 1

2 . 0

1

CAC 40 Index

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 8/458 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

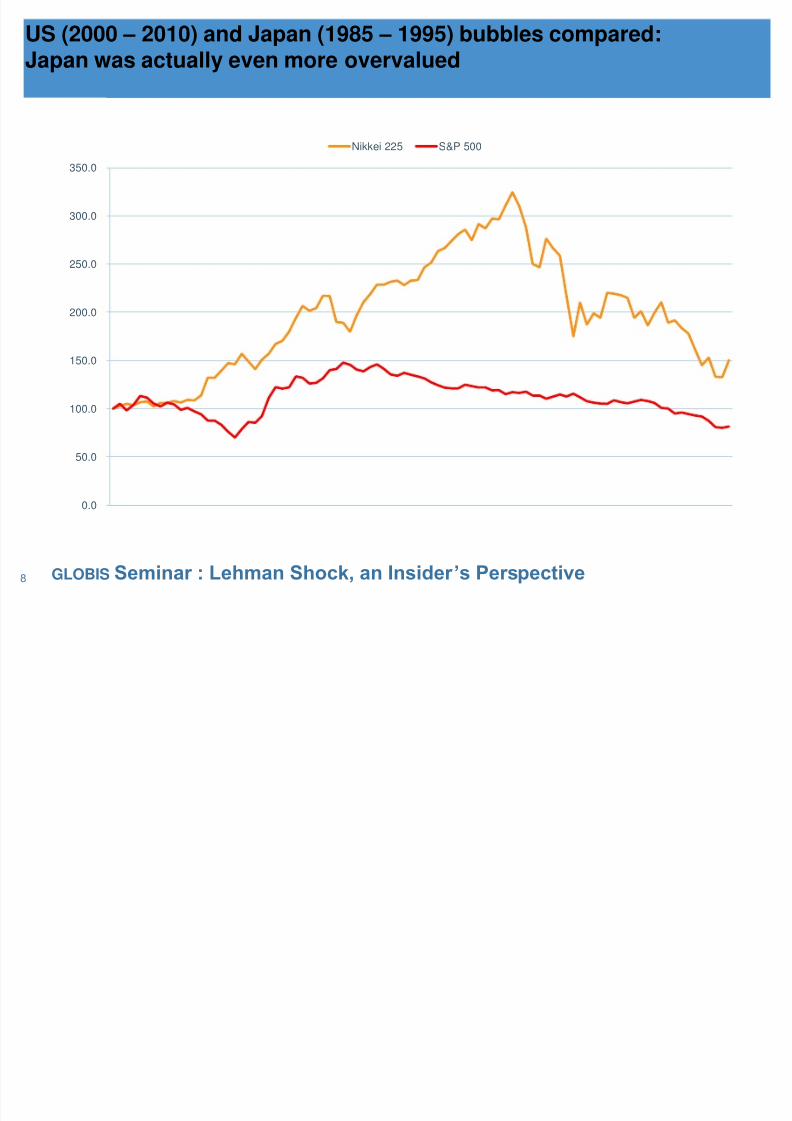

US (2000 – 2010) and Japan (1985 – 1995) bubbles compared:Japan was actually even more overvalued

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Nikkei 225 S&P 500

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 9/459 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 9

ECONOMIC BACKGROUND OF THE BUBBLE

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 10/4510 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Current Payments Balance USA, EU, Japan, BRICS(World Bank Data Base)

-850

-650

-450

-250

-50

150

350

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

United States European Union Japan China India Russian Federation Brazil

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 11/4511 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Foreign Exchange Reserves USA, EU, Japan, China, Korea (BUSD)(World Bank Data Base)

0

500

1000

1500

2000

2500

3000

3500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

China Japan United States European Union

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 12/4512 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Less and less savings… (computed from World Bank Data Base)

10

15

20

25

30

35

40

45

1 9 7 0

1 9 7 1

1 9 7 2

1 9 7 3

1 9 7 4

1 9 7 5

1 9 7 6

1 9 7 7

1 9 7 8

1 9 7 9

1 9 8 0

1 9 8 1

1 9 8 2

1 9 8 3

1 9 8 4

1 9 8 5

1 9 8 6

1 9 8 7

1 9 8 8

1 9 8 9

1 9 9 0

1 9 9 1

1 9 9 2

1 9 9 3

1 9 9 4

1 9 9 5

1 9 9 6

1 9 9 7

1 9 9 8

1 9 9 9

2 0 0 0

2 0 0 1

2 0 0 2

2 0 0 3

2 0 0 4

2 0 0 5

2 0 0 6

2 0 0 7

2 0 0 8

2 0 0 9

Gross Domestic Savings as a % of GDPUnited States Japan Euro area

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 13/4513 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

…More and more Debt (Central Government Debt as a % of GDP)

(Computed from World Bank Data Base)

25

30

35

40

45

50

55

60

65

70

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

USA

90

100

110

120

130

140

150160

170

180

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

JAPAN

40

45

50

55

60

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

EU

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 14/4514 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 14

FINANCIAL SERVICES BEHIND THE BUBBLE

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 15/4515 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 15

Traditional Mortgage Loan

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 16/4516 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 16

Basic Securitization scheme for Mortgage

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 17/4517 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 17

Packaged Mortgage Securitization (non synthetic)

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 18/4518 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 18

Everything should be fine unless default rates explode(Scheme published by the IMF)

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 19/4519 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Credit Default Swap principle

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 20/4520 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Growth of Credit Default Swaps

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 21/45

21 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 21

Buyers and sellers of protection, March 2007: roles are no longerseparated, any type of institution is insurer as well as insured(BIS & Milken Institute)

Banks'

trading;33%

LoanPortfolios ofbanks, etc,

7%

Insurers;18%

HedgeFunds; 31%

Mutual andPension

funds, 8%

Corporations and other,

3%

CDS buyers of protection

Banks'trading39%

LoanPortfolios ofbanks, etc

20%

Insurers6%

Hedge Funds28%

Mutual andPension

funds4%

Corporationsand other

3%

CDS sellers of protection

Source: Bank for International Settlements – Milken Institute

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 22/45

22 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

How assets are not always reported

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 23/45

23 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 23

Treatment of various financing and evaluation tools until 2009~2010

Repo at money market rate:A financial transaction. Hence, assets stay on balance sheet.

Repo at high cost (more than 1% of the value):Equivalent to an asset sale; further true sale supposed. Hence, assets

disappear from BS and are not recorded in the Off BS.

Securitized assets in a SPV: If Arranger doesn’t provide recourse or is insured, with a CDS for

instance, any residual commitment is merged in the derivatives positionoff BS, and no consolidation of the SPV.

Total return swap:Wipes out credit and market risks. Hence, assets protected disappear

from BS. Counterparty risk of the swap is merged in the off BSderivatives positions, valued according to the purchaser’s risk model.

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 24/45

24 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 24

What a technical “manual” said

“In order to avoid adverse impact on regular internal and external capital and credit exposurereporting a bank may use Total Return Swap toreduce the amount of lower-quality assets on the

balance sheet. This can be done by entering intoa short-term TRS with, say, a two-week term thatstraddles the reporting date.”

Moorad Choudhry, Head of Treasury at KBC, inStructured Credit Products, 2004, Wiley Financepublishing, page 106

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 25/45

25 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 25

LEHMAN BROTHERS COMPETITIVE SITUATION

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 26/45

26 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

SWOT Analysis of Lehman Brothers(JP Leboutet)

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 27/45

27 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Relative size and performance of major investment banks in 2007(computed from the 10K filings)

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

Lehman Brothers Goldman Sachs Merrill Lynch JPM Chase Morgan Stanley

Net revenues / Assets Capital / Assets

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 28/45

28 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Concentration in Investment Banking since 1995(Jean-Paul Leboutet)

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 29/45

29 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Concentration in Investment Banking since 1995 (

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 30/45

30 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Concentration in Investment Banking since 1995

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 31/45

31 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 31

SHOCK & CRISIS DEVELOPMENTS

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 32/45

32 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Stock volatility (anticipation of change in price to come) surges all of a sudden(S&P 500 volatility index – “VIX”)

0

10

20

30

40

50

60

70

80

90

02-Jan-96 02-Jan-97 02-Jan-98 02-Jan-99 02-Jan-00 02-Jan-01 02-Jan-02 02-Jan-03 02-Jan-04 02-Jan-05

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 33/45

33 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Market reaction to Lehman Brothers Bankruptcy:Stock indices from September, 10 to October, 31 - 2008

2300

2800

3300

3800

4300

4800

S&P 500 Index

7000

8000

9000

10000

11000

12000

13000

NIKKEI 225

3800400042004400460048005000

520054005600

FTSE 100

12000130001400015000160001700018000190002000021000

HANG SENG

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 34/45

34 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Market reaction to Lehman Brothers Bankruptcy:Selected Banks Stock price from September, 10 to October, 31 - 2008

8090

100

110

120

130

140

150

160Goldman Sachs

10

15

20

25

30

35

Barclays PLC

3032343638404244464850

JP Morgan - Chase

17

22

27

32

37

42

Bank of America

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 35/45

35 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Interbank lending stops

Since the LIBOR (London Inter-Bank Offered Rate) is not set, but rather is a

reported average of what large banks have been charging and paying each otherin recent transactions, no government or central bank has any direct control.During the credit freeze of September 2008, banks were reporting their opinions since there was little interbank lending to go on.

00.5

1

1.5

2

2.5

3

3.5

4

LIBOR 1 Month June to December 2008

0

12

3

4

5

6

7

8

LIBOR 1-Month from 2000 to 2011

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 36/45

36 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Time Line of the Great Financial Crisis (1/2)

Shock announcement begins the pre-panic phase

2007 04 02 New Century Financial in Chapter 11 move 2007 06 23 $3.2 Billion Move By Bear Stearns To Rescue Fund 2007 08 06 American Home files for bankruptcy

Panic of 2007 2007 08 17 Fed Cuts Discount Rate to 5.75% to Ease Credit Crunch 2007 08 22 Lehman, Accredited, HSBC Shut Offices; Crisis spreads 2007 09 17 UK Government guarantees Northern Rock deposits

Losses show in earnest after Q3

2007 10 24 Merrill Lynch Reports Loss on $8.4 Billion Write-down 2007 11 08 Morgan Stanley takes $3.7bn hit 2007 11 27 Citigroup to Sell $7.5 Billion Stake to Abu Dhabi 2007 12 18 The ECB lends over $500 billion for Christmas

Losses after Q4 rising

2008 01 15 Citi Writes Down $18 Billion 2008 02 14 UBS confirms sub-prime $18.4 billion loss 2008 03 03 HSBC in $17bn credit crisis loss

Bear Stearns collapses

2008 03 11 Central Banks inject $200 billion of liquidity into markets 2008 03 14 JPMorgan and Fed Move to Bail Out Bear Stearns

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 37/45

37 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

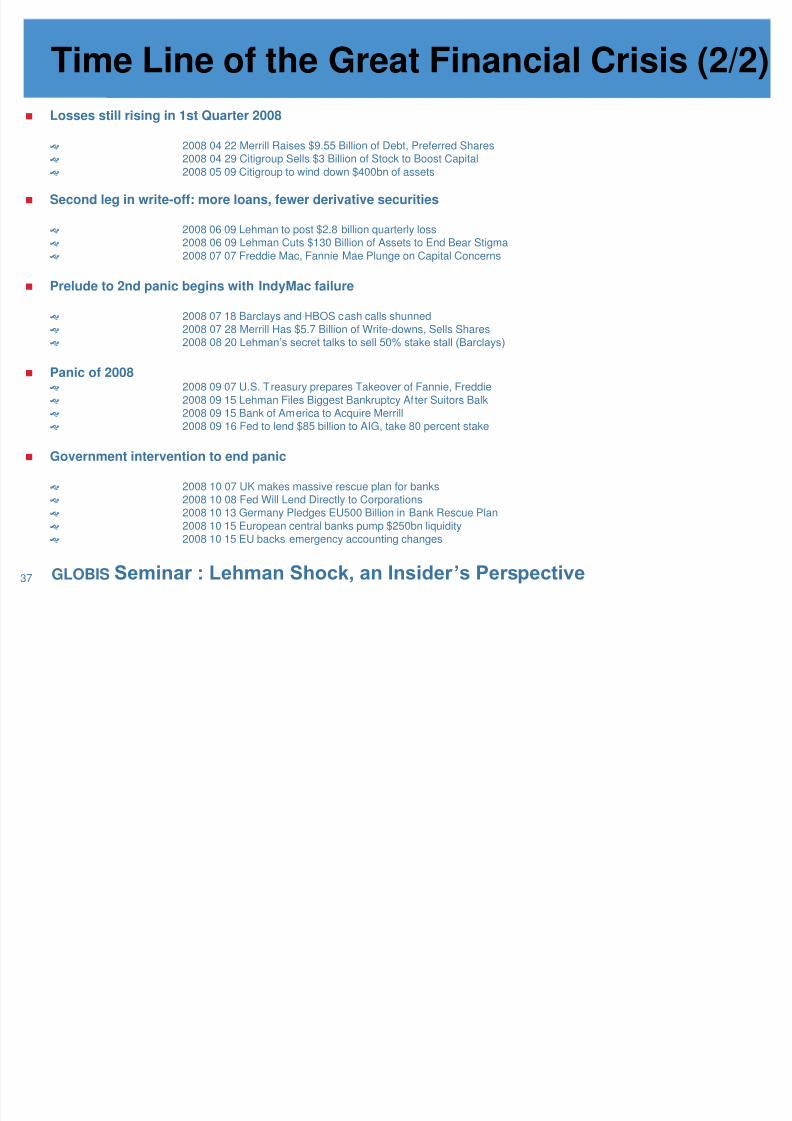

Time Line of the Great Financial Crisis (2/2)

Losses still rising in 1st Quarter 2008

2008 04 22 Merrill Raises $9.55 Billion of Debt, Preferred Shares 2008 04 29 Citigroup Sells $3 Billion of Stock to Boost Capital 2008 05 09 Citigroup to wind down $400bn of assets

Second leg in write-off: more loans, fewer derivative securities

2008 06 09 Lehman to post $2.8 billion quarterly loss 2008 06 09 Lehman Cuts $130 Billion of Assets to End Bear Stigma 2008 07 07 Freddie Mac, Fannie Mae Plunge on Capital Concerns

Prelude to 2nd panic begins with IndyMac failure

2008 07 18 Barclays and HBOS cash calls shunned 2008 07 28 Merrill Has $5.7 Billion of Write-downs, Sells Shares 2008 08 20 Lehman’s secret talks to sell 50% stake stall (Barclays)

Panic of 2008 2008 09 07 U.S. Treasury prepares Takeover of Fannie, Freddie 2008 09 15 Lehman Files Biggest Bankruptcy After Suitors Balk 2008 09 15 Bank of America to Acquire Merrill 2008 09 16 Fed to lend $85 billion to AIG, take 80 percent stake

Government intervention to end panic

2008 10 07 UK makes massive rescue plan for banks 2008 10 08 Fed Will Lend Directly to Corporations 2008 10 13 Germany Pledges EU500 Billion in Bank Rescue Plan 2008 10 15 European central banks pump $250bn liquidity 2008 10 15 EU backs emergency accounting changes

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 38/45

38 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 38

REGULATORS, CREDIT AGENCIES, GOVERNANCE

R l i i l i l

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 39/45

39 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Regulatory supervision: tools were in placebut not anticipating abnormal market behavior…

(BIS 2000 working paper)

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 40/45

40 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Credit rating agencies reacted largely after the fact

Sept. 9 (Bloomberg) – Lehman Brothers Holdings Inc., the fourth-biggest U.S.

securities firm, was put on watch for a possible downgrade to its credit rating byStandard & Poor's as the shares plunged 45 percent today.

Lehman's long-term `A' and short-term `A-1' counterparty credit ratings were put oncredit watch with ``negative'' implications, S&P said today.

``We continue to view Lehman's near-term liquidity assatisfactory,'' Sprinzen said. ``Overall, and despite nervous market sentiment in

recent month Lehman has maintained a very stable funding profile. We consider itsexcess liquidity position and contingent funding plan to be sound.'’

Lehman could meet its secured funding needs by drawing on credit facilitiesextended by the U.S. Federal Reserve since Bear Stearns Cos. ``near collapse'' inmid-March, he said.

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 41/45

41 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Employees, regulators, the public felt fine as long as the stock price was still around 40$in a tough environment.

0

10

20

30

40

50

60

70

80

90

LEHMAN BROTHERS Stock Price since floatation in May 1994

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 42/45

42 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Could the federal government have saved Lehman Brothers and prevented the biggestfinancial blowup since the Great Depression?

September 2, 2010

BERNANKE CHANGES STORY ON LEHMAN COLLAPSE - Posted by John Cassidy

Bernanke repeated an argument he has used many times before: the Fed lacked the legal authority torescue Lehman. Under an obscure provision of the Federal Reserve Act of 1934, the Fed could lend largesums of money to stricken Wall Street firms—or any other type of firm—but only if the firm could provideadequate collateral.

But for the first time Bernanke also offered a second argument: even if the Fed had gone beyond its legal

remit and tried to save Lehman, it wouldn’t have worked, because the panic enveloping the firm wasalready too advanced. All along, Bernanke insisted, he was determined to try to prevent Lehman’s demise.

He said he was perfectly aware that if Lehman were allowed to fail, or did fail, the consequences would be―absolutely catastrophic…. I never wavered in my view that we should do absolutely everything we could do

to prevent a collapse.

Barclays was ready to take over and stabilize Lehman in the same way that, six months earlier, J. P.Morgan had taken over and stabilized Bear Stearns. The official story is that this option fell throughbecause Barclays needed to obtain shareholder approval, which would have taken at least days, and theBritish government refused to waive this requirement.

But what if the Fed and the Treasury had made a public announcement that they had approved a takeoverby Barclays and were willing to provide Lehman with bridging finance until the deal could be completed?Wouldn’t that have been enough to reassure the firm’s creditors and counterparties? It isn’t immediately

obvious that the answer is no.

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 43/45

43 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective

Excessive Compensation can be considered an issue in financial services and inmanagement in general but it is not obvious to make it a Lehman specific problem.(from Forbes Magazine internet site data base)

Company CEO Pay over 5 Years

2003-2007 (million $)

Fate post 2008

Lehman Brothers Richard Fuld 354 Bankruptcy

Countrywide Financial Angelo Mozilo 392 Bankruptcy

Goldman Sachs Llyod Blankfein NA (73 in 2007) On going

Morgan Stanley John Mack 56 On going

Bank of America Kenneth Lewis 165 On going

Washington Mutual Kerry Killinger 65 Bankruptcy

JP Morgan Chase James Dimon 89 On going

Aflac Daniel Amos 140 On going

General Dynamics Nicholas Chabraja 141 On going

Forest Labs Howard Solomon 196 On going

Comcast Brian Roberts 135 On going

Oracle Lawrence Ellison 428 On going

Occiedental Petroleum Ray Irani 551 On going

Inter Active Corp Barry Diller 462 On going

Coach Lew Frankfort 254 On going

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 44/45

44 GLOBIS Seminar : Lehman Shock, an Insider’s Perspective 44

2011 CHINA BUBBLE BURST

8/3/2019 2 - 16 Dec 2011 GLOBIS - Further Reference SLIDES

http://slidepdf.com/reader/full/2-16-dec-2011-globis-further-reference-slides 45/45

China scraps national property price index17 February 2011 – Channelnewasia.com

SHANGHAI :

China has said it will stop publishing its much-watched national property price index -- a