Embed Size (px)

Citation preview

A N N U A L R E P O R T

2 0 1 1

2 Audited annual report 2011

CONTENTS

01 I N T R O D U C T I O N 4

1.1 FOREWORD BY THE MANAGING DIRECTOR 5

1.2 REPORT OF THE SUPERVISORY BOARD 6

1.3 OPERATING HIGHLIGHTS IN 2011 8

1.4 OVERVIEW OF SIGNIFICANT DEVELOPMENTS IN 2011 11

02 B U S I N E S S R E P O R T 16

2.1 PRESENTATION OF THE COMPANY 17 COMPANY PROFILE 17

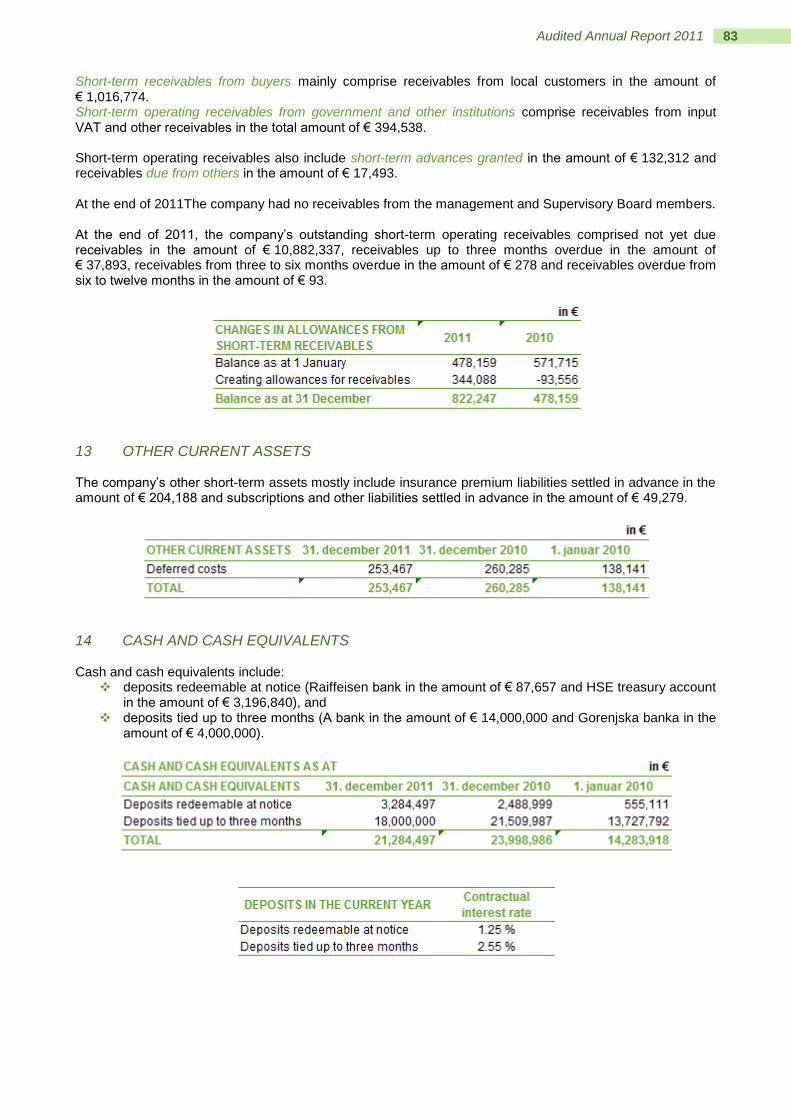

OWNERSHIP STRUCTURE OF THE COMPANY 18

COMPANY BODIES AND REPRESENTATIVES 18

CORPORATE GOVERNANCE STATEMENT 19

TRADE UNION AND WORKERS’ COUNCIL 20

ORGANISATIONAL STRUCTURE OF THE COMPANY WITH THE ORGANISATIONAL CHART 20

COMPANY’S BUSINESS ACTIVITIES 21

OWNERSHIP LINKS WITH OTHER COMPANIES 22

A BRIEF HISTORY ON THE CONSTRUCTION OF THE DRAVA RIVER POWER PLANTS 23

2.2 COMPANY’S BUSINESS POLICY 24 MISSION 24

VISION 25

STRATEGIC GOALS 25

2.3 ECONOMIC CLIMATE IN 2011 26

2.4 PURCHASING AND SUPPLIERS 27

2.5 SALES AND CUSTOMERS 28

2.6 PRODUCTION AND OPERATION 28 BASIC INFORMATION ON PP FACILITIES 28

PRODUCTION IN 2011 29

PRODUCTION SHARES OF INDIVIDUAL HPPs 30

WATER FLOW AND HIGH WATER LEVELS 31

FAILURES AND MAJOR OUTAGES 32

PRODUCTION LOSSES IN 2011 33

2.7 MAINTENANCE 34

2.8 INVESTMENTS 35 DESCRIPTION OF INDIVIDUAL MAJOR INVESTMENTS 36

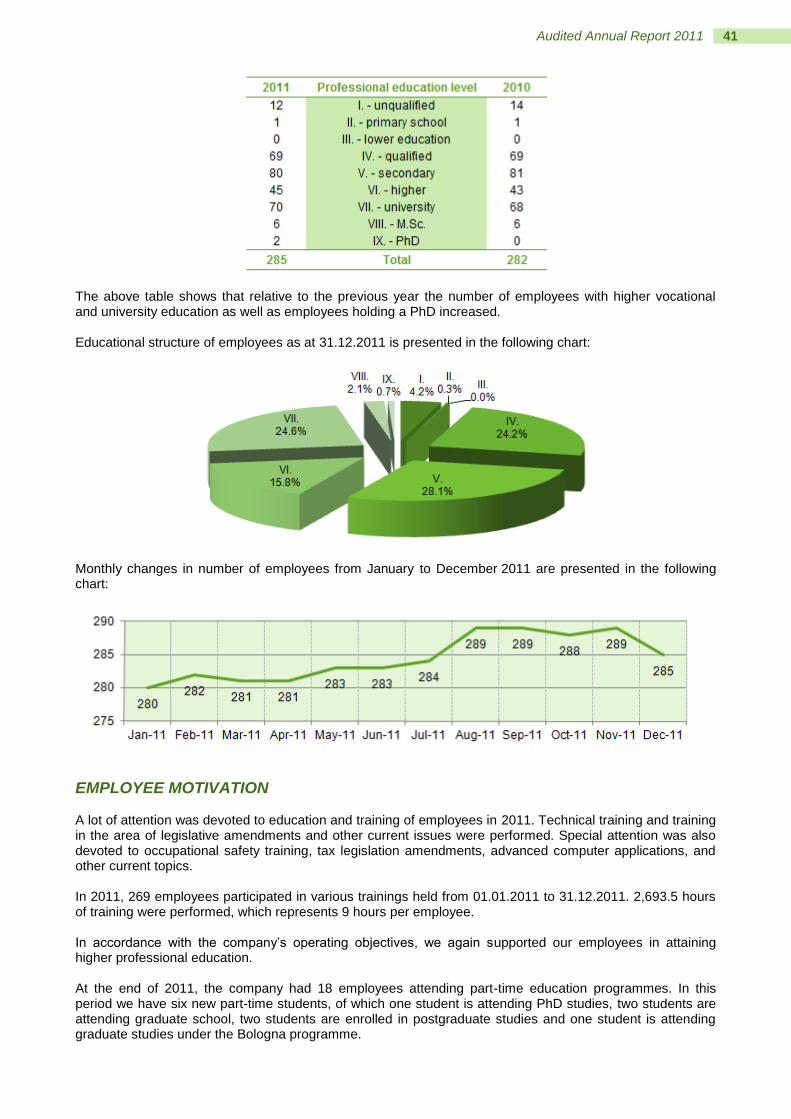

2.9 RECRUITMENT AND STAFF 40 EMPLOYEES 40

EDUCATIONAL STRUCTURE OF EMPLOYEES 40

EMPLOYEE MOTIVATION 41

SCHOLARSHIPS 42

OCCUPATIONAL HEALTH AND SAFETY AND FIRE SAFETY 42

2.10 ENVIRONMENT AND ECOLOGY 43 ENVIRONMENTAL RESPONSIBILITY 43

SUSTAINABLE DEVELOPMENT 44

ENVIRONMENTAL PROJECTS 44

2.11 ANALYSIS OF BUSINESS PERFORMANCE 47 FINANCIAL OPERATIONS 47 SELECTED FINANCIAL DATA OF THE COMPANY 48

2.12 RISK MANAGEMENT 50

3 Audited Annual Report 2011

2.13 COMMUNICATION AND PUBLIC RELATIONS 52

2.14 RESEARCH AND DEVELOPMENT 53

2.15 PLANS FOR THE FUTURE 53

2.16 IMPORTANT EVENTS AFTER THE END OF THE PERIOD 54

03 F I N A N C I A L R E P O R T 55

3.1 AUDITOR'S REPORT 56

3.2 INTRODUCTORY NOTES TO FINANCIAL STATEMENTS 58

3.3 STATEMENT BY THE MANAGING DIRECTOR 59

3.4 FINANCIAL STATEMENTS 60 STATEMENT OF FINANCIAL POSITION 60

INCOME STATEMENT 61

STATEMENT OF OTHER COMPREHENSIVE INCOME 61

STATEMENT OF CHANGES IN EQUITY 62

CASH FLOW STATEMENT 63

3.5 NOTES TO THE FINANCIAL STATEMENTS 64 REPORTING COMPANY 64

BASIS FOR PREPARATION 64

BASIS OF MEASUREMENT 65

CURRENCY REPORTINGS 66

USE OF ESTIMATES AND JUDGEMENTS 66

BRANCH AND REPRESENTATION OFFICES 66

SIGNIFICANT ACCOUNTING POLICIES 66

FAIR VALUE DETERMINATION 74

FINANCIAL RISK MANAGEMENT 74

NOTES TO THE FINANCIAL STATEMENTS 75

04 A P P E N D I C E S 94

4.1 CONTACT INFORMATION 95

4.2 LIST OF ABBREVIATIONS 96

01 I N T R O D U C T I O N

FOREWORD BY THE MANAGING DIRECTOR

REPORT OF THE SUPERVISORY BOARD

OPERATING HIGHLIGHTS IN 2011

OVERVIEW OF SIGNIFICANT DEVELOPMENTS IN 2011

5 Audited Annual Report 2011

1.1 FOREWORD BY THE MANAGING DIRECTOR

6 Audited Annual Report 2011

1.2 REPORT OF THE SUPERVISORY BOARD

7 Audited Annual Report 2011

8 Audited Annual Report 2011

1.3 OPERATING HIGHLIGHTS IN 2011 In 2011, the company Dravske elektrarne Maribor d.o.o. (hereinafter: “DEM”) operated in accordance with

the 2011 Business Plan, which was approved by the Supervisory Board on 18 March 2011.

The table below presenting the essential data of the company shows that our operations in 2011 were again successful. DEM continued its outlined course of action and achieved most of its planned objectives, some of which were even exceeded.

Compared to 2010, DEM achieved:

a 19.12 % lower net profit;

6.01 % lower total revenues, amounting to € 72,088,287;

2.57 % lower expenses, totalling € 58,963,168;

a 19.31 % lower EBIT;

1.66 % lower labour costs;

14.54 % lower electricity production;

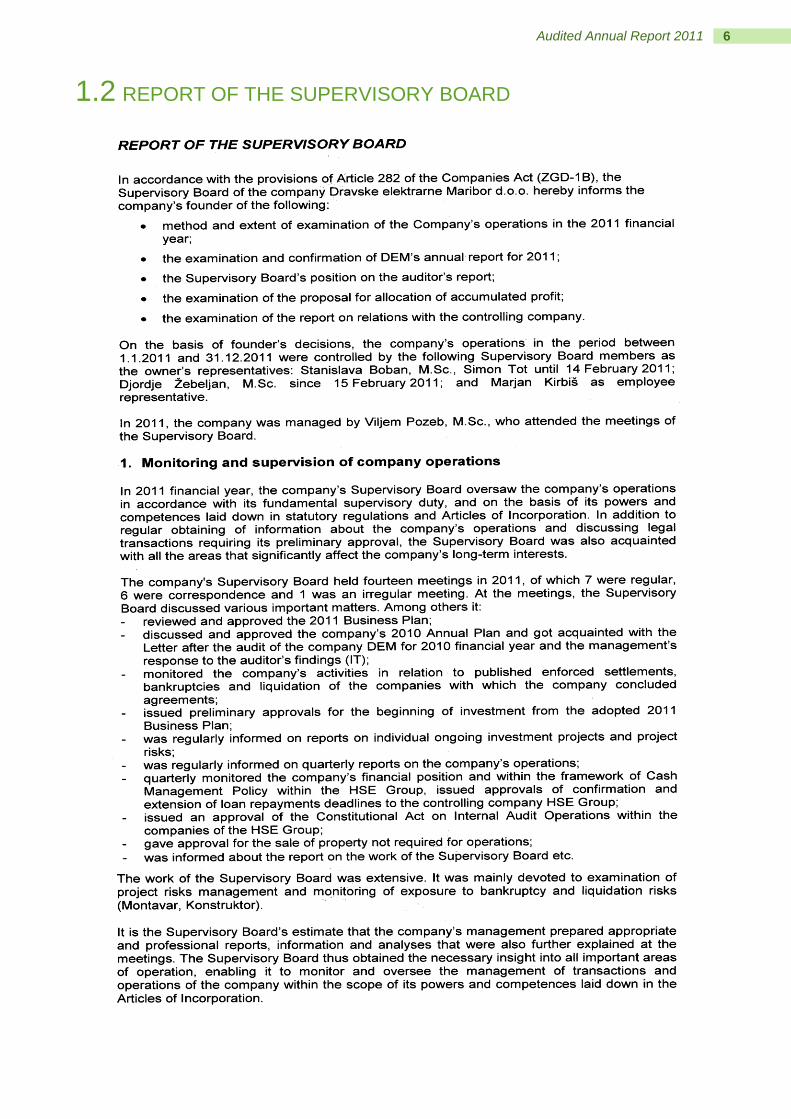

a 2.34 % increase in assets which totalled € 555,414,448 as at 31.12.2011 and

a 1.99 % increase in equity which totalled € 538,912,014 as at 31.12.2011. NET SALES REVENUE IN €

9 Audited Annual Report 2011

NET PROFIT IN €

TOTAL REVENUE IN €

EXPENSES IN €

LABOUR COSTS IN €

EBIT IN €

10 Audited Annual Report 2011

ASSETS IN €

EQUITY IN €

ELECTRICITY PRODUCTION IN GWh

NUMBER OF EMPLOYEES AT THE END OF THE PERIOD

11 Audited Annual Report 2011

1.4 OVERVIEW OF SIGNIFICANT DEVELOPMENTS IN 2011

JANUARY

Visit by the Government of the Republic of Slovenia

On 26 January 2011, Borut Pahor, the Prime Minister of the

Republic of Slovenia, and Darja Radič, M.Sc., the Minister of

the Economy, visited the company together with their

delegations. They were received by the HSE Managing

Director Matjaž Janežič, M.Sc., and the Managing Director of

DEM Viljem Pozeb, M.Sc. They were introduced to key

development projects of DEM: pumped-storage power plant Kozjak and the planned construction of

hydropower plants on the Mura River.

FEBRUARY

Issue of NSP Decree for PSP Kozjak

On 17 February 2011, the government of the Republic of Slovenia adopted a Decree on National Spatial

Plan (NSP) for pumped-storage power plant on the Drava River (PSP Kozjak) and power transmission line

between PSP and DTS Maribor. Thus, it spatially planned the facility and issued the permission for the

beginning of investment as the Decree enables the acquisition of necessary permits and approvals.

Finished overhauls and inspections of generating units on the Drava River

In the context of regular maintenance, annual overhauls and audits were concluded at the operating

generating units on the Drava River. They included control over power plant operations, planning necessary

improvements by replacing equipment and performing modification, purchase of material and timely

agreements with external contractors. Fifteen regular audits and six regular overhauls were performed as

well as all preventive maintenances of plants and some improvements, replacements and upgrades of

mechanical and electrical equipment.

MARCH

Approval of the SB to the company's 2011 Business Plan

On 18 March 2011, the company’s Supervisory Board approved the DEM’s Business Plan for 2011.

Elections to DEM’s Workers’ Council

At the end of March, elections to the Workers’ Council were held at DEM. Twenty candidates ran for nine

positions. They were nominated at the Workers’ Council or in the group of employees.

APRIL

The company's 2011 Business Plan was also approved by the General Meeting

On 22 April 2011, the company’s General Meeting approved DEM’s Business Plan for 2011.

12 Audited Annual Report 2011

PDI gets a place in the Project Council for the Preparation of Mura River Global Strategy

At the beginning of April, a special body called the Project Council was established to prepare a

comprehensive solution and global strategy of the Mura River.

This Council is coordinated by the major of Gornja Radgona Anton Kampuš and it comprises majors of

municipalities located on the bank of the Mura River and representatives of the Ministry of the Environment

and Spatial Planning of the Republic of Slovenia, Environmental Agency of the Republic of Slovenia, Ministry

for Agriculture, Forestry and Food of the Republic of Slovenia and Pomurje Development Institute Murska

Sobota (PDI).

MAY

Finished reconstruction of the switchyard at HPP Dravograd

In May, DEM successfully concluded the

reconstruction of a 110 kV switchyard at HPP

Dravograd. After final construction work and last

measurements performed, the technical inspection of

reconstructed switchyard was conducted, thereby

having concluded a € 2.1 million investment. With the

switchyard reconstruction one of key conditions is fulfilled in order to enable reliable operations of power

plant and electricity power supply to the users in Koroška region.

Establishment of the company MHE Lobnica

In the last week of May, DEM established a joint company

MHE Lobnica d.o.o. pursuant to the approval by the

Supervisory Board and the company Hmezad Jeklo d.o.o.,

Ruše. In the new company DEM holds a 65 % stake, while

the company Hmezad Jeklo d.o.o. hold a 35 % stake. MHE

Lobnica will produce approximately 600 MWh of electricity

per year.

JUNE

Sports event of the HSE Group

On 4 June 2011, a sports event of the HSE Group took place at Kodeljevo in Ljubljana. The event was

organised by the sports association of the HSE Group. Eight companies of the HSE Group competed in ten

sports disciplines. DEM’s athletes were successful as they took the third place in the group.

DEM day

On 10 June 2011, the traditional annual meeting of the company’s employees, the so-called “DEM Day”,

was held at the Limbuško nabrežje boathouse. At the gathering, jubilee awards were distributed for the time

of service in the company.

One day before (on 9 June), a gathering was organised for the now retired workers of the company.

13 Audited Annual Report 2011

Successful performance of management systems recertification

The integrated management systems assessment, which was performed in DEM for the first time last year,

was also organised this year. This year’s recertification took place from 22 to 24 June 2011. It was

organised by four external auditors from the company Bureau Veritas in Ljubljana. No inconsistency was

identified during the assessment, while the committee of DEM’s directors was responsible for the

performance of all proposed measures. The committee will monitor and control the measures on regular

basis.

JULY

Beginning of generating unit 1 renovation at HPP Zlatoličje

The renovation of the second HPP Zlatoličje generating unit started in July. Only work directly related to the

generating unit 1 will be performed on it since all the remaining work was already performed during the

renovation of generating unit 2. The work on this generating unit shall be concluded at the end of May 2012,

while at the end of June 2012 the generating unit should be included in the energy system. The renovation

will increase the operational reliability of another power plant in the DEM chain.

Establishment of Risk Management Committee of the company DEM d.o.o.

On 15 July 2011, a founding meeting of DEM’s Risk Management Committee took place (hereinafter: the

“Committee”). The Committee was appointed pursuant to the decision of the company’s Managing Director

as at 16 June 2011, while its main task was to establish a comprehensive system of risk controlling and

management within the company. The basic purpose of the Committee is to assure central determination

and risk management in the company in a structured, consistent and coordinated manner and thus provide

to the management and owner quality bases for management and governing of the company with the aim to

achieve goals planned.

AUGUST

Beginning of construction of a new part of office building

After prior reconciliation with the DEM’s Supervisory Board and numerous preparation procedures, all the

conditions for the beginning of construction of the new part of office building were met on 2 August 2011.

The selected contractor is the company Pomgrad, which, in accordance with the time schedule, predicts the

end of all work in May 2012. The construction of the new business office is necessary particularly due to the

envisaged central management of DEM and related spatial requirements as well as additional HR integration

of the companies HSE and HSE Invest.

MHE Markovci

At the beginning of August, the construction of MHE Markovci began. Soon after, the business partner

Konstruktor terminated its work due to business issues. At the end of August, the construction was continued

by the company Granit Slovenska Bistrica. The work is progressing after the constructor was replaced.

However, it will not be possible to make-up for the delay of approximately three months. The end of work or

beginning of MHE Markovci operations, which will produce 5412 MWh of electricity on the annual level, is

planned in August 2012.

14 Audited Annual Report 2011

SEPTEMBER

Launch of the solar power plant in Zlatoličje

In September, a new power plant that exploits solar energy was built

in addition to ten hydropower plants in Zlatoličje. The power plant

was named “Sončni park Zlatoličje”. The plant is placed on the

rooftop of the powerhouse. Its installed capacity amounts to

68.4 kWp by which it will annually produce approximately 75 MWh of

electricity. The project is worth 320,000. In the future, the company

plans to further upgrade the solar system in Zlatoličje. With additional solar modules, the company wants to

increase the annual production of electricity to 890 mWh using the solar power.

OCTOBER

Beginning of MHE Ruše construction

At the end of May, the companies DEM and Hmezad Jeklo Ruše established a joint company MHE Lobnica.

In October, the company acquired the working permission and as early as at 3 September 2011 officially

began constructing the new energy facility on the Lobnica River called small HPP Ruše. The work and

equipment supply are performed in accordance with the time schedule. It is envisaged that the work will be

finished by the middle of February 2012.

NOVEMBER

Solar power plant Formin

At the end of November, the construction of the second solar power plant DEM began at HPP Formin, which

was named Solar power plant Formin (SPP Formin). Its total output amounts to 112 kWp and it will be placed

on the rooftop of the powerhouse and jutting roof. The total projected annual production of electricity

amounts to 119,390 kWh.

Celebrating the 60th anniversary

In November, DEM celebrated its 60th anniversary of the

company’s establishment. For this purpose, a ceremony took place

at SNG Maribor, at which the extensive company’s history was

presented in an extraordinary manner under the guidance of the

artist Jure Ivanušič. The cultural programme was followed by

informal meeting with a banquet. The anniversary was

commemorated by DEM’s pensioners at its special meeting at the Limburško nabrežje boathouse. On this

occasion, the pensioners also presented a new film and a book about inhabitants of the Drava riverbank.

DECEMBER

DEM acquired the “Family Friendly Company” certificate

After DEM's management, Ekvilib Institute and their Audit Committee had approved that DEM would obtain a

“Family Friendly Company” certificate on 25 November 2011.

15 Audited Annual Report 2011

The company officially obtained the certificate at the ceremony held on 8 December 2011. Thus, the

company confirmed special measures, which it had adopted in

relation to working hours, informing and communication policy,

management skills, structure of payment and bonuses for

achievements and services provided to families. Measures

prescribed by the certificate are thoroughly presented to DEM’s

employees in a special booklet.

Traditional donation to Pomurje Educational Foundation (PEF)

In December, Pomurje Development Institute (PDI) left a mark on its fourth year of operations with a

traditional humanitarian gesture. Even this time, Pomurje Development Institute (PDI) and its founder DEM

granted a donation in the amount of EUR 1.500 to Pomurje Educational Foundation (PEF). The

organisations supported students of Pomurje region with the donation and enabled them “New Year’s

scholarships” programme, as referred to by PEF.

02 B U S I N E S S R E P O R T

PRESENTATION OF THE COMPANY

PURCHASING, SALES AND PRODUCTION

MAINTENANCE, INVESTMENTS, HUMAN RESOURCES AND THE ENVIRONMENT

ANALYSIS OF BUSINESS PERFORMANCE AND FUTURE PLANS

17 Audited Annual Report 2011

2.1 PRESENTATION OF THE COMPANY DEM is a limited liability company entered into the Companies register of the Maribor District Court under the entry no. 1/00278-00. The company has no subsidiaries.

COMPANY PROFILE

DEM GENERATES ELECTRICITY BY HARVESTING THE ENERGY OF WATER, OR HYDRO ENERGY.

WATER IS ONE OF THE OLDEST ENERGY RESOURCES MAN HAS LEARNED TO EXPLOIT.

IT IS ALSO THE MOST IMPORTANT RENEWABLE ENERGY SOURCE. AS MUCH AS 21.6 % OF ELECTRICITY

PRODUCED AROUND THE WORLD IS PRODUCED BY HARVESTING THE ENERGY OF WATER. THE CONVERSION OF

HYDROPOWER TO ELECTRICITY TAKES PLACE IN HYDROPOWER PLANTS. WITH THE EXCEPTION OF OLD MILLS

THAT ARE POWERED BY THE WEIGHT OF WATER,

MODERN HYDROPOWER PLANTS TAKE ADVANTAGE OF THE KINETIC ENERGY OF HEAD OF WATER.

Full company name: DRAVSKE ELEKTRARNE MARIBOR d.o.o. Abbreviated name: DEM d.o.o. Legal form: Limited liability company Address: Obrežna ulica 170, 2000 Maribor Telephone: 02 300 50 00 Fax: 02 300 56 55 Companies Register entry no.: 1/278/000 Nominal capital: € 395,011,180 Size: large company Year of establishment: 1918 Bank account: 04515-0000337195 with NKBM Tax number: 96254459 VAT ID: SI96254459 Registration number: 5044286 Website: www.dem.si E – mail: [email protected] Activity code: D35.111 Managing Director: VILJEM POZEB, M.Sc.

18 Audited Annual Report 2011

With the average annual output accounting for 25 % of total electricity produced in Slovenia and by meeting

37 % of electricity demands during the summer and 20 % in the winter, the power plants on the Drava River

are extremely important for the Slovene electricity system.

The exploitation of the Drava River’s energy potential began in 1918 when the Fala power plant was built.

This was followed by the construction and opening of the Dravograd power plant in 1943, Mariborski otok

power plant in 1948, Vuzenica power plant in 1953, Ožbalt power plant in 1960, Zlatoličje power plant in

1968 and Formin power plant in 1978.

The power plant chain on the Slovene section of the Drava River is made up of eight power plants with the

total rated generating unit power of 585 MW. If the Melje and Ceršak small power plants are taken into

account, the total rated turbine power amounts to 587 MW. Together, the power plant reservoirs hold 78

million m3 of water, of which 12.4 million can be used for electricity production.

With 8 hydropower plants on the Drava River and 2 small hydropower plants, DEM produces as much as

80 % of Slovenia's electricity which conforms with the criteria of renewable energy sources and the

internationally recognised RECS certificate (Renewable Energy Certificates System). High-quality

hydropower is provided in an environment friendly way and in line with the principles of sustainable

development.

Pursuant to its development plans, the company – which is owned by HSE – is also one of the most

important investors in the construction of power plants on the lower Sava River, the biggest development

project in the Slovene electricity sector.

OWNERSHIP STRUCTURE OF THE COMPANY Pursuant to the resolution of the Government of Slovenia on the transfer of the Government’s share to HSE, HSE became DEM’s sole owner on 21 August 2007. As at 31.12.2011, HSE’s share in DEM’s equity was € 395,011,180.

COMPANY BODIES AND REPRESENTATIVES The Articles of Incorporation of a limited liability company Dravske elektrarne Maribor d.o.o. of 22.04.2011, which have been adopted by HSE, the company’s sole member (founder), provide for the following company bodies:

SUPERVISORY BOARD

MANAGING DIRECTOR In accordance with DEM's Articles of Incorporation and applicable legislation, the founder has the function and powers of a General Meeting provided that the legal form of a limited liability company with a single member is observed. SUPERVISORY BOARD

Stanislava Boban – president (appointed: 17.06.2009 – end of term: 30.11.2012);

Djordje Ţebeljan, M.Sc. – member (appointed: 15.02.2011 – end of term: 30.11.2012);

19 Audited Annual Report 2011

Marjan Kirbiš – member, employee representative (appointed: 18.03.2008 – end of term: until recalled or until the next election in the Workers’ Council).

MANAGING DIRECTOR

The company has a single-member management. The company is represented by the director, subject to limitations. The Managing Director of the company is Viljem Pozeb, M.Sc., who started his term on 30 September 2009. The Managing Director is appointed for a term of 4 years.

CORPORATE GOVERNANCE STATEMENT The company is managed in accordance with applicable legal standards and Articles of Incorporation of the limited liability company Dravske elektrarne Maribor d.o.o. adopted by HSE as the sole member of the company DEM on 22 April 2011.

Under the Articles of Incorporation, the company is managed directly through the founder and the company bodies, i.e. the Supervisory Board and the Managing Director.

The founder independently decides on the following matters: amendments to the Articles of Incorporation; change of registered office following the proposal of the Managing Director; adoption of the company’s development strategy proposed by the Managing Director after an opinion

is received from the Supervisory Board; the business plan of the company; adoption of the annual report if the Supervisory Board does not approve it or if the Managing Director and

the Supervisory Board assign the responsibility of adopting the annual report to the founder; distribution of accumulated profit and offsetting of losses; discharge from liability to the Managing Director and Supervisory Board; purchase, allocation and termination of business interests; measures for increasing or decreasing the capital; changes to the company's nominal capital; changes to the Articles of Association and dissolution of the company; appointment of the company’s auditor; appointment and dismissal of Supervisory Board members; appointment of the company’s procurator and other authorised persons; amount of attendance fees paid to the members of the Supervisory Board and its commissions; adoption of measures for improvement of company’s operations and elimination of identified

shortcomings and irregularities; and other matters in accordance with regulations and Articles of Incorporation.

The founder cannot decide on questions related to the handling of transactions unless the managing director requires so in the event the Supervisory Board disagrees with a certain type of transaction. The founder records its decisions in the register of decisions.

The Supervisory Board is comprised of three members, of which two represent the interests of the founder that appoints and discharges them, while one represents the interests of employees and is appointed and discharged in accordance with the Workers Participation in Management Act. Supervisory Board members are appointed for a term of four years and can be re-appointed when their term of office expires. The Supervisory Board is responsible for the following matters: it monitors the management of the company’s business operations; it reviews the contents of the annual report, examines the proposal for allocation of accumulated profit

and reports, in written form, about the findings of the review to the founder; it approves the annual report or raises objections to it; it gives an opinion on the foundations of the business policy and the development plan of the

company; it approves company business plans; it approves business transactions entered into by the Managing Director in accordance with the

Articles of Incorporation; it proposes to the founder the decisions falling within its area of competence or gives opinions on the

proposals made by the Managing Director in connection with the decisions to be accepted by the founder; it appoints and dismisses the Managing Director;

20 Audited Annual Report 2011

it concludes a contract of employment with the Managing Director; it adopts the Supervisory Board Rules of Procedure; it may request reports on other issues.

The Supervisory Board can also perform other tasks stipulated by the company’s regulations, internal documents and the founder’s decisions.

The Managing Director manages the company’s activities and operations on his own responsibility and represents the company independently. The Managing Director is appointed and discharged by the company’s Supervisory Board. His/her term of office is 4 (four) years with the possibility of reappointment. Without the Supervisory Board’s consent the Managing Director may not enter into transactions or adopt decisions concerning: legal transactions and borrowing in excess of € 333,834.08 for the same item in a financial year; disposal and mortgaging of property; equity investments made by the company in other legal entities; the beginning of individual investment where the envisaged value exceeds € 100,000.00 (due to the

needs for coordinated strategic plan of the HSE Group); and the beginning of individual investment related to IT, where the envisaged value exceeds € 50,000.00 (due

to the needs for coordinated development of IT within the HSE Group) after having acquired the opinion by the head of IT department at the company’s member.

I, Viljem Pozeb, the Managing Director of the company Dravske elektrarne Maribor d.o.o., hereby declare that I have been acquainted with the Corporate Governance Code for Companies with State Capital Investments (hereinafter: the ―Code‖) in 2011. It is my estimate that in 2011 the governance of the company Dravske elektrarne Maribor d.o.o. was in line with the recommendations laid down by the Code adopted by The Capital Assets Management Agency of the Republic of Slovenia (hereinafter: AUKN) and published on 18 November 2011 on AUKN’s website (www.auknrs.si). As the managing director of Dravske elektrarne Maribor d.o.o., I declare, pursuant to point 73 of the Code that the company Dravske elektrarne Maribor d.o.o. has opted to apply the AUKN Code on a voluntary basis.

TRADE UNION AND WORKERS’ COUNCIL

ORGANISATIONAL STRUCTURE OF THE COMPANY WITH THE ORGANISATIONAL CHART The company has the following organisational units:

Managing Director;

21 Audited Annual Report 2011

assistant to the Managing Director;

advisory to the Managing Director;

departments managed by the Managing Director;

technical area with the following organisational levels: business units, departments, divisions;

sector for development and construction and general business division with the following organisational levels: departments, divisions;

temporary organisational units – projects. Their activities and tasks are performed within distinct areas of expertise, with responsibilities being delegated hierarchically. All activities within the company are well coordinated thanks to proper management. The company’s organisational chart as at 31.12.2011:

COMPANY’S BUSINESS ACTIVITIES The company’s core business activity is production of electricity in HPPs. Other activities include:

intercity and other road passengers transport; freight transport by road; wired telecommunications services; hardware and software consultancy; other information technology and computer related services; rental and operation of own or leased real estate property; accounting, bookkeeping and auditing services; tax consulting services – other than auditing; other management and business advisory services; other engineering activities and technical consulting; sports facilities operation.

22 Audited Annual Report 2011

In addition to the above activities, the company provides other registered activities in accordance with the Articles of Incorporation.

OWNERSHIP LINKS WITH OTHER COMPANIES RELATION TO THE CONTROLLING COMPANY HSE

DEM is a part of Holding Slovenske elektrarne Group. On 26 July 2001, the Government of the Republic of Slovenia founded HSE with the objective of establishing a joint presence of electricity suppliers in the market, improving their competitiveness and constructing a HPP chain on the lower Sava River. Six companies were incorporated into the new company. HSE is thus the holding company, while the other companies are its subsidiaries. Both HSE and subsidiaries are legally independent entities. As at 31.12.2011, the company HSE, based in Ljubljana at Koprska 92, is the company's controlling (holding) company which prepared the 2011 consolidated annual report for the group of companies under its control. Pursuant to Article 545 of the Companies Act (ZGD-1), DEM’s management prepared a Report on relations with related companies for 2011. The report was submitted to the certified auditor, as provided by Article 546 of the Companies Act. The report shows that, in view of the circumstances known at the time legal transactions were carried out, DEM estimates that it was not disadvantaged in any such transaction with the controlling company and its related parties, and that in 2011 no legal transaction, act or omission that could be potentially damaging to the company took place as a result of influence exercised by HSE. RELATION TO SUBSIDIARIES AND ASSOCIATES

DEM holds an equity interest in five companies:

HSE Invest 25.0 % stake

ELDOM 50.0 % stake

HESS 30.8 % stake

PDI 100.0 % stake

MHE Lobnica 65.0 % stake The abovementioned stakes are disclosed under long-term assets as long-term investments. In the following table, the stakes in HSE Invest, ELDOM and HESS are disclosed in section ―Associates‖ – taking into account the fact that an associate is a company in which the controlling company has a higher than 20 % but lower than 50 % interest. Pomurje Development Institute and small HPP Lobnica are presented in the section "Subsidiaries" – taking into account the fact that subsidiaries are companies in which the controlling company has a higher than 50 % interest. HSE INVEST HSE Invest d.o.o., a company for engineering and construction of energy plants, was established on 25 April 2002 with the adoption of the Articles of Incorporation of a Limited Liability Company. HSE Invest is thus a subsidiary, whose founders and members are HSE, DEM, SENG and SEL, all with an equal stake. In the company HSE Invest d.o.o., based at Obreţna ulica 170a in Maribor, DEM holds a 25 % stake which represents an investment in the amount of € 80,000. ELDOM ELDOM d.o.o., a company for maintenance of buildings and restaurant services, was established on 1 July 1991. Its founders are Slovenian power companies:

Dravske elektrarne Maribor; Elektro Maribor; Elektro Slovenija.

In 2004, four companies had a stake in ELDOM, namely, the three abovementioned founders and the company Elektroinštitut Milan Vidmar. Each company had a 25 % stake in ELDOM. In January 2005, we bought a 25 % stake in ELDOM which was owned by the company Elektroinštitut Milan Vidmar. Thus, we now hold a 50 % stake in the company ELDOM, based at Vetrinjska ulica 2 in Maribor.

23 Audited Annual Report 2011

| ||

HESS - Hidroelektrarne na spodnji Savi HESS d.o.o. was founded on 12 February 2008 by the companies HSE, DEM, SENG, Termoelektrarna Brestanica and Gen Energija. The company HESS was established with the transformation of the previous project coordinator, the so-called Joint venture, into a legal entity for the purposes of securing transparent investments and compliance with the concession agreement as well as the Concessions Act. HESS’s priority will be the construction of remaining hydropower plants on the lower Sava River with the possibility of further construction of the HPP chain on the middle Sava River. DEM has a 30.8 % stake in HESS. PRI - Pomurski razvojni inštitut (PDI - The Pomurje Development Institute) In June 2008, DEM established PDI with the purpose of bringing the project for the construction of HPPs on the Mura River closer to the interested public. The institute was founded with the desire to attract experts from various professional backgrounds and different areas of expertise. The institute is based in Murska Sobota. The main responsibility of the institute is mostly informing the stakeholders about the expert studies on exploitation of the Mura River water potential (environmental topics, studies of flora and fauna, as well as agricultural, economic and tourism studies) and their presentation to the general public. MHE Lobnica In May 2011, DEM and the company Hmezad Jeklo d.o.o. established a joint company ―Mala hidroelektrarna Lobnica, druţba za proizvodnjo električne energije d.o.o.‖ We hold a 65 % stake in the company small hydropower plant Lobnica d.o.o. with its registered office at Obreţna ulica 170 in Maribor. The remaining stake in the amount of 35 % belongs to another company member Hmezad Jeklo d.o.o. The company’s core business activity is hydroelectricity generation. Other activities include: other electricity production, transfer of electricity, electricity trading, construction of water facilities. On the basis of contract of members with the limited liability company small HPP Lobnica, the following company's bodies are appointed: General Meeting and Managing Director. The Managing Director of the company is Ladislav Tomšič, M.Sc. The company also has a procurator.

A BRIEF HISTORY ON THE CONSTRUCTION OF THE DRAVA RIVER POWER PLANTS 1918 1942 – 1958 1960 - 1978

HPP Fala HPP Dravograd, HPP M. otok, HPP Vuzenica, HPP Vuhred HPP Ožbalt, HPP Zlatoličje, HPP Formin

The chain of 8 HPPs on the Drava River was constructed between 1918 and 1978, and the already finished and planned renovation projects will preserve their capabilities for many decades to come. At the time of its construction, after WWI, the first Drava River hydropower plant in Slovenia, HPP Fala, was the most technologically advanced and powerful hydropower plant in the eastern Alpine region and Central Europe and a driver of industrial development and electricity network in central and northeast Slovenia.

ENERGY TIME FLOW OF CAPACITY FROM FALA TO FORMIN

24 Audited Annual Report 2011

Due to a changed economic and political situation arising from the dissolution of Austria-Hungary and the emergence of pre-WWII Yugoslavia, the construction of hydropower plants on the Drava River came to a halt.

During World War II, pier-type power plants HPP Dravograd and HPP Mariborski otok were constructed. At HPP Dravograd, which was already operational during the war, extensive renovation and completion works were carried out with which the damages from airstrikes were repaired and operation of the first two turbines restored. At HPP Mariborski otok, which was nothing more than an abandoned construction site after the war, the first turbine started operating in 1948 and was joined by another two by 1960. Construction of HPP Mariborski otok

After the end of the war, pier-type power plants HPP Vuzenica and HPP Vuhred were constructed. The first generating unit of HPP VUZENICA began operating in 1953, while the last (third) was put into operation in 1956. During the construction of HPP Vuzenica, designs were prepared for the next downstream section, HPP Vuhred. The first generating unit of HPP Vuhred was put into operation in 1955. All three generating units became operational in 1958. During the construction of HPP Vuhred, the final section of the upper Drava River power plants, i.e. a pier-type power plant HPP Ožbalt, was designed. The first generating unit at HPP Ožbalt began operating in 1960. The plant began operating at full capacity in 1962. The basic project for the so called “lower” Drava River was prepared in 1956. HPP Zlatoličje, constructed between 1964 and 1969, was the first channel-type power plant on the river. The power plant, which receives water through a 17.2 km inlet channel from the Melje dam, while the water returns to the riverbed through a 6.2 km outlet channel, is the most powerful HPP in Slovenia. With a few years’ intermission, the construction of HPP Formin, a channel-type power plant, began which started operating in 1978. Its large reservoir allows for greater flexibility of operation and ensures larger production at peak hours. This was the final stage in the process of construction of Slovenia’s power plants on the Drava River. MODERNISATION AND REFURBISHMENTS

In 1977 the capacity of the oldest power plant on the Drava River, HPP Fala, was increased through installation of an eighth generating unit. In 1991, two more generating units were installed to replace the oldest seven, which were decommissioned. Over the past two decades, the other five upper Drava River power plants were refurbished, thus increasing their capacity and peak output. The overall increase in capacity is comparable to the capacity of an additional power plant. Between 1918, when the first kilowatt hours of electricity were produced, and the end of 2010, the power plants on the Drava River generated more than 125 billion kWh of electricity. DEM’s total output, which stood at 20 MW in 1918, now totals 584 MW.

2.2 COMPANY’S BUSINESS POLICY

ENERGY FROM NATURE - FOR MANKIND AND NATURE

MISSION

DEM is the leading company in the area of efficient use of renewable energy resources in Slovenia. Due to

its focus on development it provides for quality and environment-friendly energy supply with the objective of

achieving economic success and ensuring sustainable development of the environment and markets in

which it operates.

25 Audited Annual Report 2011

VISION

To maintain its position as the leading hydroelectric power system in Slovenia through effective use of

renewable resources and optimal allocation of resources, and to expand, by means of strategic partnerships

and sensible diversification, to other interesting market areas.

STRATEGIC GOALS The company’s main strategic goals are derived from the company’s Strategic development plan for the period until 2018 and the development plan of the HSE Group for the period 2006 to 2015, looking ahead to 2025. DEM’s Supervisory Board discussed and adopted the long-term plan of renovation and development for the period 2003 to 2018 at its 13

th regular meeting on 6 May 2003.

DEM’s main strategic goals for the period until 2018 are as follows: Goals pertaining to safe and reliable production and construction of additional production capacities:

To pursue an optimal and joint maintenance policy:

maintenance on the majority of HPP facilities of the HSE Group,

ensuring safe operation of HPPs,

monitoring of facilities and equipment.

To carry out planned investments in additional production capacities:

construction of PSP Kozjak until 2019,

construction of a HPP chain on the Mura River,

renovation of existing facilities and increased output (overhaul of HPP Zlatoličje completed by the end of 2013).

To promote sustainable development;

To maximise utilisation of the natural potential of the Drava River and its tributaries;

To achieve rational utilisation of the hydroelectric potential through the use of small HPPs;

To become the core hydroelectric pillar in the HSE Group;

To fully provide (staff, organisation, financing) for the execution of strategic projects. Goals pertaining to streamlining of operations:

To ensure competitiveness through the lowering of operating costs Goals pertaining to human resources management:

To provide for educated, competent, satisfied and motivated employees;

To maintain optimal staff numbers;

To maintain optimal staff structure;

To provide for continuous training;

To care for the quality of working life. Goals pertaining to financial management:

To ensure short-term and long-term solvency;

To manage financial risks;

To secure optimal financing sources;

To pursue an optimal financial policy;

To optimise the structure of financing sources and equity structure.

26 Audited Annual Report 2011

2.3 ECONOMIC CLIMATE IN 20111 During the last months of 2011, the economic activity in Euro-zone additionally decelerated, while the

continuation of bad conditions is indicated by economic indicators. The conditions in national bond markets

and interbank market remain deteriorated.

The changes in short-term ratios in October and November indicate deceleration of economic activity in

Slovenia during the last quarter of the previous year. According to IMAD estimate, the real export of goods in

October and November in average remained below the level of the third quarter. The real volume of

manufacturing activity production, which had already decreased in the middle of 2011, remained on the

achieved level during the autumn months. The activity in the construction sector remained on an extremely

low level from July to November. After a weak growth during the summer months, the real revenue in retail

store has somewhat decreased in November, while the fall was mitigated by the increase in revenue in

engine fuel store.

Deteriorated circumstances in the labour market continued at the end of the year, while the November

changes in salaries were characterised by the payments of thirteenth salaries and Christmas bonuses, which

were the lowest during the last six years. According to deseasonalized data, the number of employed

excluding self-employed farmers also decreased in November. According to IMAD estimate, this was mainly

the consequence of decrease in construction sector. The number of registered unemployed further increased

in December. At the end of the year, it amounted to 112,754, which is 2.5 % more than at the end of 2010.

According to deseasonalized data, the average gross salary in the public sector slightly decreased in

November, while the average gross salary in private sector remained on the previous month's level. The

share of revenue and average amount of payment were lower than in 2010. Even in the previous year, the

amount of employees receiving irregular payments remained the highest in the activities with the highest

average salaries and at the same time a large stake of state ownership (supply wit electricity and gas,

mining, water supply as well as financial and insurance activities).

In 2011, the increase of consume prices in Euro-zone was higher than in 2010 and it was more extensive

than in Slovenia. The key reason for increased inflation was the growth of energy product prices as a result

of the impact of increased oil prices at the beginning of 2011 and food prices at the end of 2010 in the world

markets. Last year the inflation in Slovenia amounted to 2.1 % and it was on the similar level as in the

previous three years. The key inflation factors were the same as in Euro-zone, but we estimate that last year

the inflation in Slovenia was lower particularly due to the impact of weaker domestic economic activity.

During the nine months of the previous year, the cost competitiveness improved on mid-annual level.

However, Slovenia was still in the group of Euro-zone members with a relatively larger decrease in cost

competitiveness during the time of crisis. The last year’s improvement of cost competitiveness was mostly

the consequence of lower growth of costs per employee in comparison to productivity growth.

In December, the net repayments of loans by domestic non-banking sectors were so far the highest. The

same applies to creation of provisions and impairments.

1 Source: IMAD

27 Audited Annual Report 2011

The deficit in consolidated balance sheet of public financing amounted to € 1,377 million during the ten

months of the previous year, which is almost € 500 million less than in the same period of the previous year.

QUANTITY BALANCE SHEET OF ELECTRICITY

In 2011, the electricity production in Slovenia decreased mostly as a result of deteriorated river stage, while the consumption increased almost exclusively due to reinforced aluminium production. The production decreased by 5.5 %, while the consumption increased by 3.6 %. The hydropower plants production decreased by more than one fifth compared to high levels of the previous two years, while on the other hand the nuclear power plant production increased by one tenth and the thermal power plant production remained approximately the same. As a result of higher aluminium prices, the domestic production of this metal and thus electricity consumption were significantly reinforced and almost in total contributed to the growth of electricity consumption in Slovenia. International exchange of electricity was substantially reinforced also in 2011. The export of electricity (taking into account solely the Slovenian production of the nuclear power plant) increased by 17.5 %, while the import of electricity increased by 30.5 %. Thus, we imported over 1,700 GWh or 13 % of electricity that we use in Slovenia. Approximately one half (around 45 %) of increase in export was the result of increased domestic demand for electricity, while the other portion of increase resulted from increased electricity trade. The latter partly resulted from the increase in transfer capacities on the Slovene-Italian border. At the beginning of the year, the trade on this border was additionally facilitated by introduction of implicit auctions when concluding transactions.

2.4 PURCHASING AND SUPPLIERS Suppliers play an increasingly important role in implementation of development and strategic goals. DEM’s purchasing procedures are governed by rules on purchasing procedures and rules on placement of suppliers on approved suppliers list. As laid down in both sets of rules, an increasing amount of purchases are made from approved suppliers that meet the requirements of applicable standards and have recognised credentials. At DEM we aim to further centralise the purchasing function to the greatest extent possible, but due to the nature of our work this cannot be always fully achieved. With the aim to streamline our operations and negotiate better purchasing conditions, we are gravitating towards reducing the number of suppliers. One of the most important purchasing-related tasks is finding the best sources of high-quality goods and services that are provided by renowned domestic and foreign suppliers. The largest suppliers are normally the suppliers of capital equipment and contractors engaged to carry out large-scale maintenance work. The quality of materials and services provided by suppliers directly affects the faultless functioning of our plants, which is vital for uninterrupted electricity production. Because ensuring uninterrupted electricity production is paramount, selecting high-quality suppliers is all the more important. In accordance with quality assurance requirements under the ISO 9001 and ISO 14001 standards, DEM has been carrying out a systematic assessment of suppliers for ten years running, classifying them into groups A, B, C or D on the list of the approved suppliers. When assessing and placing approved suppliers on the list, DEM considers the suppliers of important strategic products and services that are important for the process of production and maintenance of electricity plants and equipment. In 2010, all suppliers of strategic relevance were placed in group B, which is the result of changed supplier assessment criteria. The largest foreign supplier in 2011 was the company Lahmeyer International GmbH from Germany. The biggest domestic suppliers, which supplied the capital equipment, carried out major repairs and performed maintenance services in 2011, include:

Esotech, d.d.

HSE Invest d.o.o.

28 Audited Annual Report 2011

SGP Pomgrad d.d.;

Metalna SRM d.o.o.;

Fira d.o.o.;

Iskra sistemi d.d.;

Litostroj Power d.o.o.;

VGP Drava Ptuj d.d;

CM Celje d.d.;

Montavar Metalna Nova d.o.o.

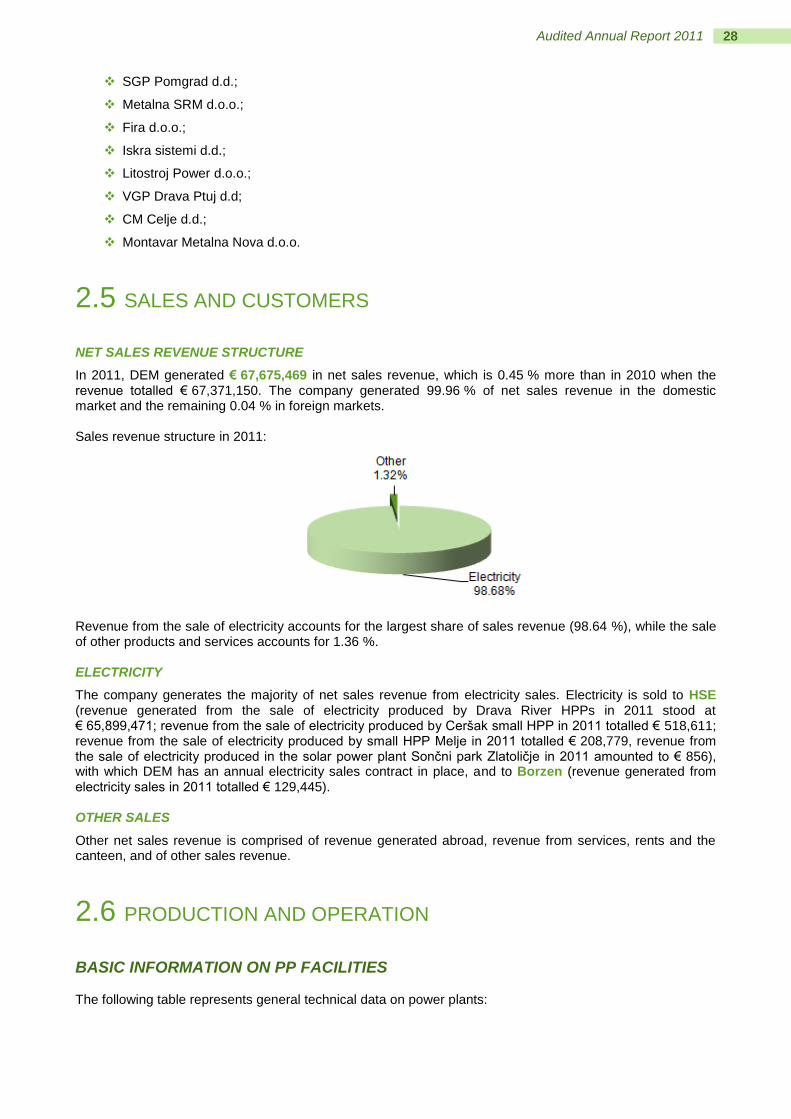

2.5 SALES AND CUSTOMERS NET SALES REVENUE STRUCTURE

In 2011, DEM generated € 67,675,469 in net sales revenue, which is 0.45 % more than in 2010 when the revenue totalled € 67,371,150. The company generated 99.96 % of net sales revenue in the domestic market and the remaining 0.04 % in foreign markets. Sales revenue structure in 2011:

Revenue from the sale of electricity accounts for the largest share of sales revenue (98.64 %), while the sale of other products and services accounts for 1.36 %. ELECTRICITY

The company generates the majority of net sales revenue from electricity sales. Electricity is sold to HSE (revenue generated from the sale of electricity produced by Drava River HPPs in 2011 stood at € 65,899,471; revenue from the sale of electricity produced by Ceršak small HPP in 2011 totalled € 518,611; revenue from the sale of electricity produced by small HPP Melje in 2011 totalled € 208,779, revenue from the sale of electricity produced in the solar power plant Sončni park Zlatoličje in 2011 amounted to € 856), with which DEM has an annual electricity sales contract in place, and to Borzen (revenue generated from electricity sales in 2011 totalled € 129,445). OTHER SALES

Other net sales revenue is comprised of revenue generated abroad, revenue from services, rents and the canteen, and of other sales revenue.

2.6 PRODUCTION AND OPERATION

BASIC INFORMATION ON PP FACILITIES The following table represents general technical data on power plants:

29 Audited Annual Report 2011

* The new generating units taken into account; generating unit 1 will be operating until the middle of 2012.

PRODUCTION IN 2011 The planned power plant production which is included in the power balance is the production that can be generated by power plants when they maintain constant operational capacity and when the monthly inflow is equivalent to an inflow corresponding to a 57 % probability that median monthly flows will be reached. The overall production or supply of electricity to the grid by all the generating units combined in 2011 – including the small HPPs – totalled 2,427,807,057 kWh of electricity, which is 102.76 % of planned production. The large generating units produced and supplied 2,412,946,668 kWh or 102.72 % of planned production, the generating units at small HPP Ceršak 4,260,789 kWh or 85.22 % of planned production and the generating units at small HPP Melje 10,583,895 kWh or 121.79 % of planned production. The solar power plants that were included into operations in 2011 produced 24.046 kWh of electricity in Zlatoličje and 1.269 kWh of electricity in Formin and altogether supplied 15,705 kWh of electricity to the grid. The entire production was supplied to HSE. Monthly production in 2011:

The planned production was not achieved in April, May, July, August and December, while during the other months it was achieved and exceeded, mostly in January when we exceeded the planned production by 77.4 %.

30 Audited Annual Report 2011

Monthly production in 2011:

The annual production chart for 2011:

PRODUCTION SHARES OF INDIVIDUAL HPPs The production share of a power plant in the chain depends on the plant's installed capacity, flow and head. The power plants built in the river bed (Dravograd, Vuzenica, Vuhred, Oţbalt, Fala and Mariborski otok) produced 58.7 %, while the channel-type power plants (Zlatoličje and Formin) produced 40.7 % of total electricity supplied to the grid. The remaining 0.6 % of electricity supplied to the grid was produced by small HPPs Ceršak and Melje as well as solar power plants Zlatoličje and Formin that were included into operations in 2011. Production of individual HPPs in 2011:

0

2000

4000

6000

8000

10000

12000

14000

16000

1 31 61 91 121 151 181 211 241 271 301 331 361

Pro

du

cti

on

(M

Wh

)

Day

Plan

Production

31 Audited Annual Report 2011

Production shares of individual HPPs in 2011:

During HPPs operation since 1918 until the end of 2011, DEM supplied 127,741,452,346 kWh of energy to the grid. In view of current consumption, Slovenia could be supplied for more than 10 years with this energy. The following table presents total production of individual power plants from the beginning of power plant's operation until (including) 2011 and its share in total production. Here, it is necessary to state that this is the share of electricity supplied to the grid.

WATER FLOW AND HIGH WATER LEVELS The average annual flow in power plants on the Drava River in 2011 was 242 m

3/s or 89.3 %, while at

Mariborski otok it totalled 245 m3/s or 90.4 % of the flow balance, which in both cases amounts to 271 m

3/s.

In 2011, the flows in January, February and October were higher, while during all the other months they were lower than planned.

The water flow of over 800 m3/s, at which measures foreseen for the event of high water levels had to be

adopted was recorded on two occasions in 2011, namely:

on 19 and 20 June 2011, when the highest water flow from Austria stood at 1,300 m3/s and in

Slovenia at 1,442 m3/s at HPP Vuhred;

on 19 and 20 September 2011, when the highest water flow from Austria stood at 1,200 m3/s and in

Slovenia at 1,365 m3/s at HPP Zlatoličje.

32 Audited Annual Report 2011

We also record several days when the flow was higher than the highest mutual flow of generating units in the individual power plant. However, it was still not necessary to adopt measures envisaged in case of high water levels. These days were, as follows:

on 28 May 2011, when the highest water flow from Austria stood at 687 m3/s and the highest water

flow in Slovenia stood at 783 m3/s at HPP Vuzenica;

on 26 and 28 October 2011, when the highest water flow from Austria stood at 680 m3/s and the

highest water flow in Slovenia stood at 789 m3/s at HPP Fala.

Water flow chart for 2011:

FAILURES AND MAJOR OUTAGES Minor maintenance work on generating units and other plants and elimination of failures were carried out by power plant maintenance crews in accordance with the programme of operations and during night time. Most frequent failures were as follows:

failures on turbine regulators (Vuzenica, Oţbalt, Fala, Mariborski otok, HPP Melje); failures of excitation systems (Dravograd, Vuzenica, Vuhred); issues with cooling water for turbine shaft seals and bearings (Vuzenica, Oţbalt, Zlatoličje,

HPP Ceršak); issues with pressure and levels in the turbine pressure unit (Fala); failure of water level measurement on the turbine cover (Zlatoličje); functioning of electricity safeties (Dravograd, Vuzenica, Vuhred, Fala, Mariborski otok, small HPP

Melje); issues with supply of electricity for own consumption (Zlatoličje); foreign object between guide vanes (Dravograd).

After having performed the activities to increase the rigidity of the turbine cover on the generating unit 2 of HPP Zlatoličje in December 2010, the generating unit was operating without interruptions. Between 11.07.2011 and 14.07.2011, secondary oil was replaced at the generating unit 2. However, the work had to be finished quickly since a disruptive discharge in the stator winding of generating unit 1 occurred on 12.07.2011 and from that time the generating unit 1 is in renovation. Thus, in the period from 12.07.2011 to 15.07.2011, HPP Zlatoličje had no generating unit without taking into account the generating units of small HPP Melje. The overall amount of water spilled as a result of failures (excluding small HPPs) in 2011 was equivalent to 353 MWh of electricity or 0.015 % of electricity supplied to the grid. The amount of water spilled due to overhauls and inspections was equivalent to 4,765 MWh of electricity or 0.2 % of planned production and due to the renovation of generating unit 1 at HPP Zlatoličje, the water was spilled for 26,396 MWh or 1.09 % of electricity supplied to the grid.

0

100

200

300

400

500

600

700

800

900

1000

01 02 03 04 05 06 07 08 09 10 11 12

Flo

w (

m3/s

)

Month

Plan

5 1 2 3 4 6 7 8 9 10 11 12

Flow M. otok

33 Audited Annual Report 2011

The water spilled as a result of surpluses was equivalent to 1,325 MWh or 0.05 % of electricity, while the water spilled due to cleaning of generating unit inlets amounted to 315 MWh of electricity or 0.0013 % of electricity supplied to the grid. Total losses in 2011 thus amounted to 33,154 MWh of electricity or 1.37 % of electricity supplied to the grid. Considering the above data, it is evident that the generating units operated at high availability, using most of the water for electricity production. This is further supported by the fact that most losses (80.2 %) arose as a result of the overhaul on generating unit 1 at HPP Zlatoličje. Operation during the year was in line with the programme of operation. The turbines of Dravske elektrarne

Maribor that have the control power of 30 MW ( 45 MW) are included in the provision of the system service concerning the secondary power and frequency control, subject to the level of water in power plant reservoirs.

PRODUCTION LOSSES IN 2011 Production losses refer to lost energy that could have been produced, but instead water was spilled over the locks for various reasons. Total losses since 1988 until (including) 2011 are presented in the following table:

In 2011, losses occurred in all power plants. Total losses amount to 1.37 % of electricity supplied to the grid. Most losses are a result of renovation of the generating unit 1 at HPP Zlatoličje (26,396 MWh), which accounts for the majority of losses in 2011. Total losses (MWh) in 2011 by month and by power plant:

34 Audited Annual Report 2011

Losses occur due to defects, overhauls, refurbishments, cleaning of turbine inlets and grid surpluses. Shares of individual losses (by cause) in 2011:

DEFECT RELATED LOSSES

Defect related losses occur when available water cannot be utilised for electricity production due to a generating unit failure, which results in spilling of water over the locks. In 2011, such losses occurred at all power plants, except for HPPs Dravograd, Vuhred and Formin. Overall, 353 MWh of electricity were lost due to defects. OVERHAUL RELATED LOSSES

Overhaul-related losses occur when water flows during overhauls and inspections are greater than the intake capacity of operational turbines. As a rule, works are carried out in the first two months of the year, when the water flows are statistically at their lowest. In 2011, overhaul-related losses were recorded at HPPs Mariborski otok, Zlatoličje and Formin. Losses at HPP Zlatoličje were the result of works carried out on generating unit 2 due to changing turbine oil. LOSSES RELATED TO THE CLEANING OF TURBINE INLETS

In 2011, we also started to record losses as a result of cleaning of turbine inlets which occur when turbine inlets need to be cleaned due to jammed grates, while the water cannot be accumulated in the power plant pools. In 2011, losses due to cleaning occurred at power plants Mariborski otok and Zlatoličje. GRID SURPLUS RELATED LOSSES

Grid surplus related losses occur when power plant reservoirs are full and there is an excess of energy that cannot be sold in the market. In such cases, the grid is controlled by spilling water over the locks. DEM has no control over such losses. Overall, 1,325 MWh of electricity were lost due to grid surpluses. REFURBISHMENT RELATED LOSSES

In 2011, 26,396 MWh of electricity were lost due to refurbishment.

2.7 MAINTENANCE All planned overhauls and inspections of generating units, switchyards and locks were carried out to the extent planned. In addition to the abovementioned works, professional services and maintenance crews also carried out planned large-scale maintenance works. Moreover, various maintenance works were carried out on joint facilities and systems of HPPs in accordance with the maintenance plan. Maintenance costs in 2011 totalled € 3,377,532 (2010: € 2,334,013), of which:

costs of spare parts and maintenance materials of fixed assets account for € 360,323,

costs of maintenance services account for € 3,017,209.

35 Audited Annual Report 2011

The total actual maintenance costs represent 102.32 % of the plan for 2011. Costs of spare parts and maintenance materials reached 75.97 %, while the costs of maintenance services reached 106.74 % of planned costs. Overview of realised maintenance costs in 2011:

The majority of maintenance costs are represented by construction maintenance costs, the largest part of which is comprised of costs arising from obligations under the concession agreement (monitoring of barriers, canals, maintenance works on the water infrastructure), which have been increasing due to growing environmental requirements. Realised maintenance costs in the period 2007 to 2011:

Through high-quality maintenance we want to ensure that, over the long-term, production facilities and buildings will be in proper condition to operate throughout their useful lives in the manner for which they were designed. The growing complexity of installed equipment that is being deployed in renovated power plants requires expert and more and more specialised maintenance services, which require higher qualification structure of contractors and additional training. The company’s long-term goal is the greatest possible self-sufficiency in the area of maintenance, because due to long useful lives of facilities all specialised expertise that is not available on the market must be preserved.

2.8 INVESTMENTS The value of capital investments in 2011 is € 15,748,830 (2010: € 9,860,500), of which:

€ 9,020,905 was financed from depreciation assets,

€ 6,727,925 was financed from other own sources.

36 Audited Annual Report 2011

Overview of capital investments realised in 2011:

Total capital investments represent 32.71 % of the plan for 2011. Investments in new buildings reached 21.54 % of the plan, investments in reliable production 39.95 %, investments in control centres 83.42 %, investments in security systems 109.31 %, investments in reconstructions 31.69 %, investments in studies, investment and project documentation 31.43 %, investments in seismic monitoring 48.98 %, investments in counter systems 116.78 %, minor capital investments 92.38 %, and investments in business information system 110.35 % while other investments reached 77.20 % of the plan.

Realised capital investments in the period 2007 to 2011:

DESCRIPTION OF INDIVIDUAL MAJOR INVESTMENTS CONSTRUCTION OF PSP KOZJAK

Within the framework of PSP project on the Drava River and the OPL to DTS Maribor, the stage of spatial planning of the facility was concluded - National Spatial Plan (NSP). On 25 February 2011, the government of the Republic of Slovenia published a Decree on National Spatial Plan for pumped-storage power plant on the Drava River and power transmission line between the PSP and DTS Maribor in the Official Gazette no. 12. The decree represents the basis of continuation of legal procedures to acquire approvals by individuals responsible for spatial development, acquisition of land and preparation of projects to obtain the building permit in accordance with regulations governing facility construction, on the basis of which the building permit is issued. The Environmental Impact Report is in preparation as well as expert bases for the Environmental Impact Report in the field of EMS, noise, vibrations and archaeology.

37 Audited Annual Report 2011

The most important approval is represented by the Environmental Impact Report as the end of the Comprehensive Environmental Impact Assessment (CEIA) of this project. In the previous year, the activities for preparation and expert bases of the Environmental Impact Report and land acquisition were not performed due to the agreement on the adapted speed of the project with regard to HSE recommendations. PCD was reviewed in the time of preparation and amendment. The audit of revised PCD was performed by Lahmeyer Internacional. Audit conclusions approve the PSP Kozjak project, both from the technical as well as constructive point of view. The audit also envisaged the review of powerhouse construction in the cavern being constructed. The cavern version of powerhouse will be constructed on the level of PCD with the purpose to confirm the most favourable technical-economic performance on the discussed location. Since the Conceptual design represents a technical basis for preparation of the Investment programme, special attention was devoted to investment cost estimate during the preparation of amendments to PCD. The basic investment programme was performed in 2008 and audited by the Audit Committee. The committee adopted a decision approving the investment programme together with its components of value and financial structure. PCD was approved by the DEM Supervisory Board and discussed by the HSE Supervisory Board in 2008. After the amendment and PCD audit in 2011 as well as the performed investment programme Studies of electricity market and PSP Kozjak products, the revised investment programme was prepared and presented to HSE in November 2011. CONSTRUCTION OF HPPs ON THE MURA RIVER

Based on concessionaire’s appointment, DEM, as investor, intend to exploit the energy of Mura River by constructing hydro power plants. In 2006, the programme ―Possibilities for the utilisation of the Mura River for energy production‖ was prepared. The programme determined the role of examination of the region’s sustainable development taking into account the construction of HPP on the Mura River. The study of the sustainable development of the area will explain the condition of environment and impacts on environment and nature. The necessary expert bases will be performed indicating possible locations of energy exploitation and HPP project-technical solutions where it is possible to construct HPP under the existing conditions. After the sustainable examination of energy exploitation of the area, the attention was devoted to expert bases, namely to the ―Examination of Locations from the Perspective of Environmental Protection‖ where the Conceptual Technical Solutions of HPP in relation to severe restrictions of environment and nature are discussed. The latter proved to be one of the most important factors. The exploitation of entire Mura River potential needs to be discussed in detail in currently prepared expert bases and Conceptual Technical Solutions in numerous versions. On the basis of the latter, the proposition of NSP proposal was prepared for HPP on the location between the inflow of the Kučnica River and highway passage over the Mura River – HPP Hrastje Mota. The proposition of the proposal was submitted to the MoE supplier and coordinator of NSP preparation at the Ministry of the Environment and Spatial Planning. This is the first stage of spatial planning procedure in accordance with applicable legislation. DEM expects that the initiative will be coordinated, thereby the working procedure will begin with the initiative and the first activity represented by the preparation of materials to obtain guidelines, which will represent the starting point for the beginning of NSP procedure. Based on findings of sustainable development study, which includes the examination of HPP construction impact on sustainability, and expert bases for consideration of HPP on the Mura River with the guidelines to investor for further decisions, the documentation for the following locations is discussed and prepared:

on the segment between Ceršak and Sladki vrh (replacement facility for small HPP Ceršak); and in the wider area of Gornja Radgona in connection with the intended construction of flood protection

of the area – construction of high water level embankments. RENOVATION OF THE MARKOVCI DAM AND CONSTRUCTION OF A SMALL HPP

The project comprises three areas:

restoration and stabilisation of the Drava riverbed; renovation of the dam; and construction of the small HPP and MV switchyard.

38 Audited Annual Report 2011

Project performance in 2011 Project work is performed in accordance with the audited time schedule taking into account the actual condition of work performance. Construction work on the intake segment of facility is concluded and the installation of mechanical and hydro-mechanical equipment is in progress. The construction work on powerhouse and outtake canals is completed up to the height of 210.00 m. In this segment of powerhouse the first elements of mechanical generator equipment are built as well as hydro-mechanical equipment of outtake gates. SONČNI PARK ZLATOLIČJE

As regards the investor, the construction of solar power plant ―Sončni park Zlatoličje‖ represents a possibility of additional exploitation of natural potentials in the area of renewable sources, while in the development and technical area they represent a possibility of planning, projecting, construction, maintenance and solar power plant management. The project comprises the construction of solar power plant in the area of Zlatoličje hydropower plant. The following activities were carried out in 2011:

preparation of tender documentation in relation to construction of SPP ―Sončni park Zlatoličje‖ – first phase,

preparation of tender documentation in relation to construction of SPP ―Sončni park Zlatoličje‖ – second phase,

preparation of tender documentation in relation to equipment supply of connection to 20kV distribution network,

preparation of tender documentation for installation of equipment of connection to 20kV distribution network,

preparation of PZI project documentation, end of SPP ―Sončni park Zlatoličje‖ construction – first phase, end of construction work, end of call for tender in relation to installation of equipment for connection to distribution network, take-over of equipment for connection to distribution network, dismantlement of on-site equipment in the project of HPP Zlatoličje renovation, construction of cable line for 20kV transmission line, performance of installation work related to connection of solar power plant equipment to distribution

network, performance of procedures of launching the equipment for connection to distribution network, solar power plant was connected to distribution network on 29 July 2011, A partial internal technical inspection of the facility ―Sončni park Zlatoličje‖ was performed – the solar

power plant was connected to distribution network on 4 August 2011, technical inspection of the facility ―Sončni park Zlatoličje‖ for the purposes of beginning of operations

as at 18 August 2011, beginning of solar power plant operations on 18 August 2011, inspection review on 6 September 2011.

On 8 October 2011, a trail run was successfully completed and the solar power plant is in operation. SOLAR POWER PLANT FORMIN

In April 2011, the project group for construction of solar power plant Formin was appointed with the task of constructing a solar power plant on the rooftop of powerhouse and garages. We obtained information on location and concluded a contract with the company HSE Invest in order to prepare project and tender documentation and participate in construction of the solar power plant at HPP Formin. On 8 November 2011, a contract for construction of SPP Formin was concluded with the company HTZ IP d.o.o. On 20 November 2011, we started the construction, while on 16 December 2011 the technical inspection of the facility SPP Formin was successfully performed for the purposes of beginning the operation of facility. On 22 December 2011, the solar power plant was connected to the network and the contractual trial run began. ANNEX TO OFFICE BUILDING – MAIN CONTROL CENTRE III CONSTRUCTION

Investment value is calculated on the basis of project value estimate (project documentation for acquisition of working permit – DOBP, which was prepared by the company Arhitekt Maribor d.o.o. in May 2007. Project number: 92/06).This value is converted to the level of fixed prices in the time when investment documentation was prepared.

39 Audited Annual Report 2011

Total investment value of constructing business facility – Control centre III including the equipment of business premises at fixed prices in June 2010 amounted to € 5,920,232 excluding VAT. Until now the following documentation was prepared and approved for the facility:

project documentation for building permit (DOBP) acquisition, which was prepared by the company

Arhitekt Maribor d.o.o. in May 2007 (Project number: 92/06),

Investment Project Identification Document (DIIP), which was prepared by the company HSE Invest

d.o.o. in June 2010,

Investment programme (IP) no. HIPM-12/2010, which was performed by the company HSE Invest

d.o.o. in July 2010,

preparatory work project is completed,

IP project is completed.

The works began on 1 August 2011 pursuant to the contract and they are performed in accordance with the approved time schedule. Currently there are no delays. The supply of all mechanical elements and installation are performed in accordance with the plan. RENOVATION OF HPP ZLATOLIČJE, MELJE DAM AND SMALL HPP MELJE

Melje Dam In November, the contractor was selected for the reconstruction of Melje dam and crane rails. Final Pasarič was selected as the most favourable contractor among three suppliers. At the beginning of December, the contract on construction work was submitted to him. Since the selected contractor had not returned the signed contract by the end of 2012, the requestor again asked him to sign it. Pursuant to a new appeal to sign the contract, the contractor sent a memo that he withdrew from the contract. Due to withdrawal from the contract, the requestor was obligated to call upon the other least expensive supplier, namely the company MAP Trade. Since MAP Trade also responded that the prices offered were not relevant anymore and that it increased the price for the abovementioned volume of work, the requestor decided to perform a new call for tender for work envisaged. Small HPP Melje Since the company Montavar is in liquidation process, while certain deficiencies remained opened and were not abolished despite several appeals by the requestor, the requestor started to realise the banking guarantee. The banking guarantee was realised by the bank on 01.12.2011 in the total amount of € 148,240.30. On the basis of realised banking guarantee, the requestor will thus settle all the opened issues alone or it will conclude appropriate orders with other contractors. HPP Zlatoličje With the beginning of generating unit 1 renovation in July, the contractor ESOTECH faced minor problems since it seemed that it would remain without the contractor due to Konstruktor's liquidity problems. Since the probability of Konstructor’s bankruptcy was increasing, Esotech informed us that it decided to replace the subcontractor pursuant to the contract LOT DM, namely the new subcontractor for the abovementioned construction work became the company MAT Trade. As a result of contractual partner's bankruptcy in accordance with the contract LOT PGO - Konstruktor VGR, the requestor started the realisation of banking guarantee concluded at Banka Koper and termination of the contract due to failure to fulfil contractual obligations. For the abovementioned work, which remained unrealised in accordance with the contract LOT PGO, a new contractor will be selected through collection of offers. Dismantlement of old generating unit 1 was slightly delayed (approximately 10 days) due to bad organisation of the contractor. With the beginning of traverse ring restoration, the installation of generating unit 1 officially began. Work on traverse ring restoration was actually performed in a larger extent than envisaged in the time schedule since during the review it had been established that it was in worse condition than traverse ring of generating unit 2, on the basis of which the volume was envisaged according to time schedule. With regard to the fact that more work is needed, the delay additionally increased with regard to the currently applicable time schedule R08. Due to the abovementioned delay, it will be necessary to perform the audit of time schedule. Equipment for T1 renovation is at the facility, while the part of equipment is in the factory waiting to be transported. All equipment in the factory was successfully taken over or final take-overs are being performed for some positions of supply. The construction of factory equipment is not critical. Litostroj preforms constant control with its installation supervisor and performs all necessary activities for undisturbed course of installation work.

40 Audited Annual Report 2011

All the equipment for generating unit G1 is supplied and adequately protected or preserved and it is waiting for installation to begin. Coordination and management are coordinated each Friday at regular coordination meetings where work is regularly controlled and possible problems during work performance are being solved. Additional work of replacing the fence around the facility and switchyard is completed as well as setting grounding strip around the facility. The replacement of external facility lightning is also in progress. The external lightning was not included in the context of renovation project, but it needs to be replaced in accordance with decree on decrease in light pollution. MINOR CAPITAL INVESTMENTS

In order to provide conditions for uninterrupted production, maintenance and operating processes, the company must also invest in minor capital investments. In 2011, minor capital investments comprised purchases of various equipment for providing uninterrupted operation and functioning. We also purchased various tools and devices, machines, vehicles and instruments.

2.9 RECRUITMENT AND STAFF

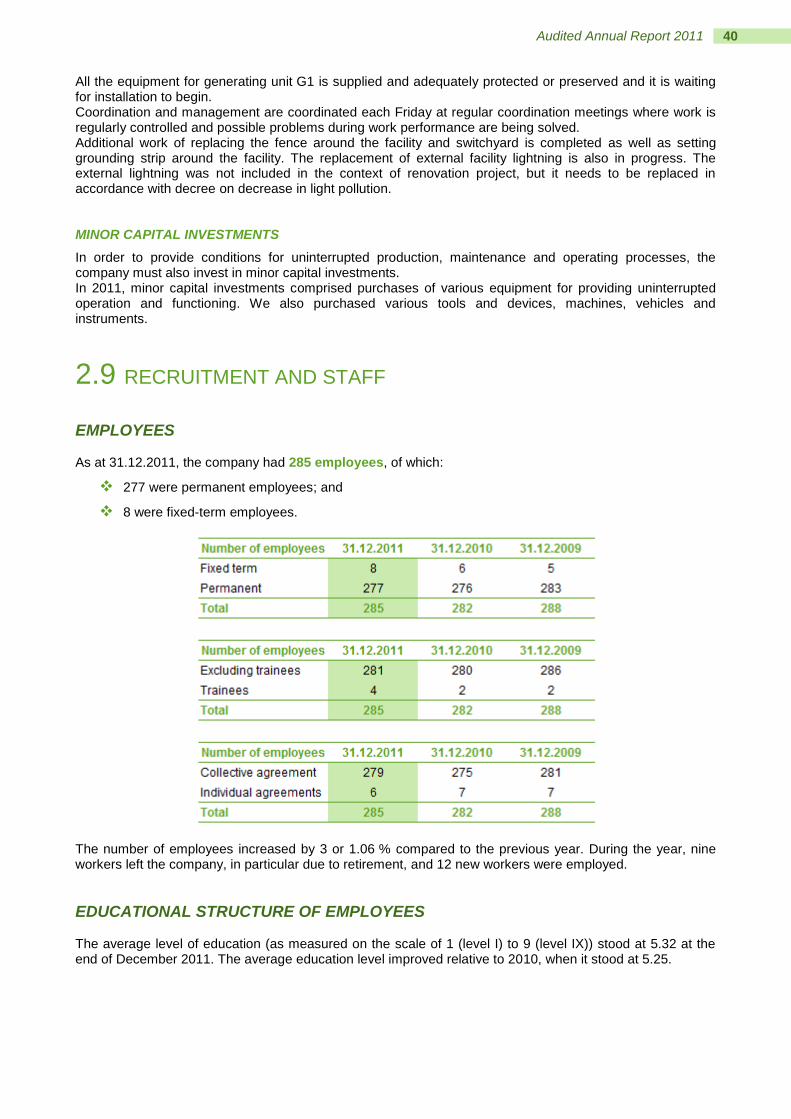

EMPLOYEES As at 31.12.2011, the company had 285 employees, of which:

277 were permanent employees; and

8 were fixed-term employees.