Embed Size (px)

Citation preview

2 0 0 5

The Connection between Risk Management and Internal Control in Organizations

Mag. Norbert Wagner

Budapest, 11.4.2008

Budapest, 11.4.2008

2

Internal Auditing

Risk Management

Internal Control

Connections

Budapest, 11.4.2008

3

Internal Auditing

Risk Management

Internal Control

Connections

Budapest, 11.4.2008

4

Internal Auditing

Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organization‘s operations. It helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control and governance processes.

(The IIA, Definition of Internal Auditing, 2004)

Budapest, 11.4.2008

5

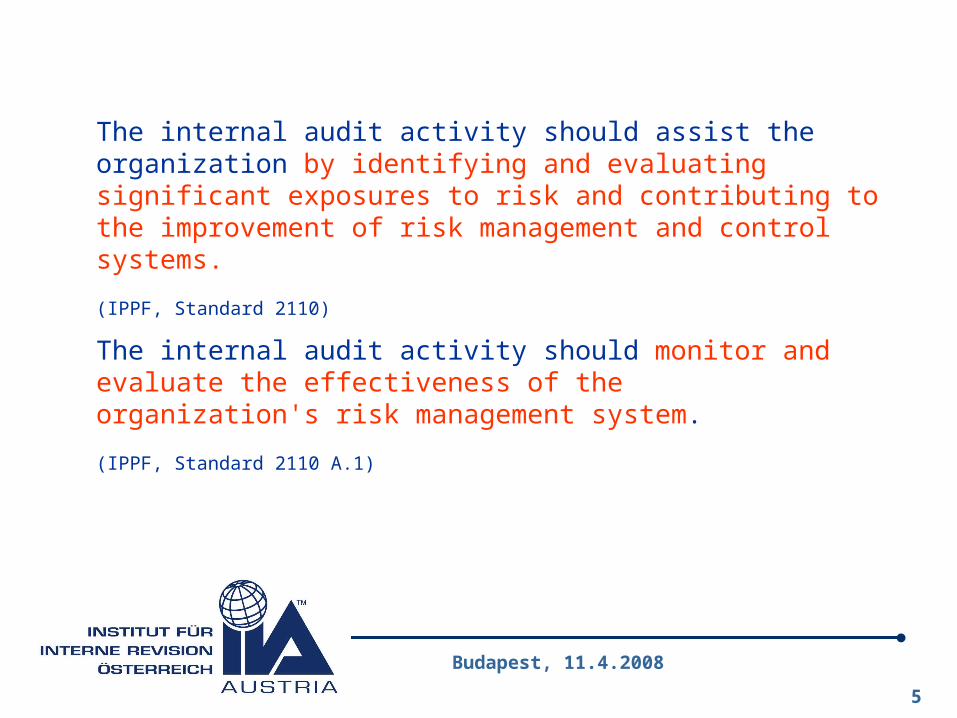

The internal audit activity should assist the organization by identifying and evaluating significant exposures to risk and contributing to the improvement of risk management and control systems.

(IPPF, Standard 2110)

The internal audit activity should monitor and evaluate the effectiveness of the organization's risk management system.

(IPPF, Standard 2110 A.1)

Budapest, 11.4.2008

6

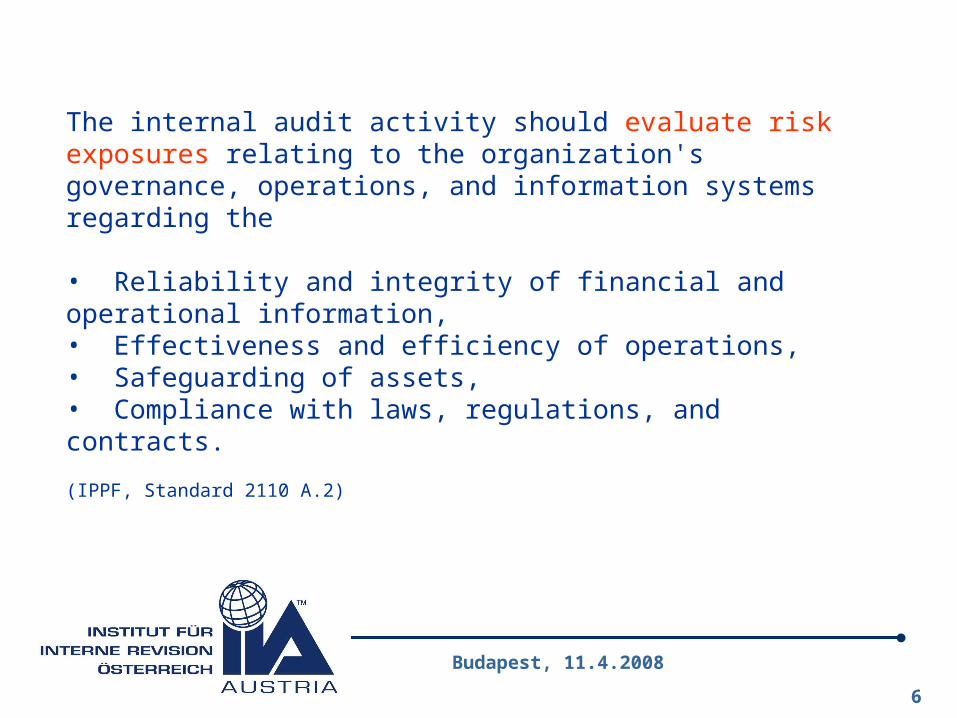

The internal audit activity should evaluate risk exposures relating to the organization's governance, operations, and information systems regarding the

• Reliability and integrity of financial and operational information, • Effectiveness and efficiency of operations,• Safeguarding of assets,• Compliance with laws, regulations, and contracts.

(IPPF, Standard 2110 A.2)

Budapest, 11.4.2008

7

Internal Auditing

Risk Management

Internal Control

Connections

Budapest, 11.4.2008

8

Risk Management

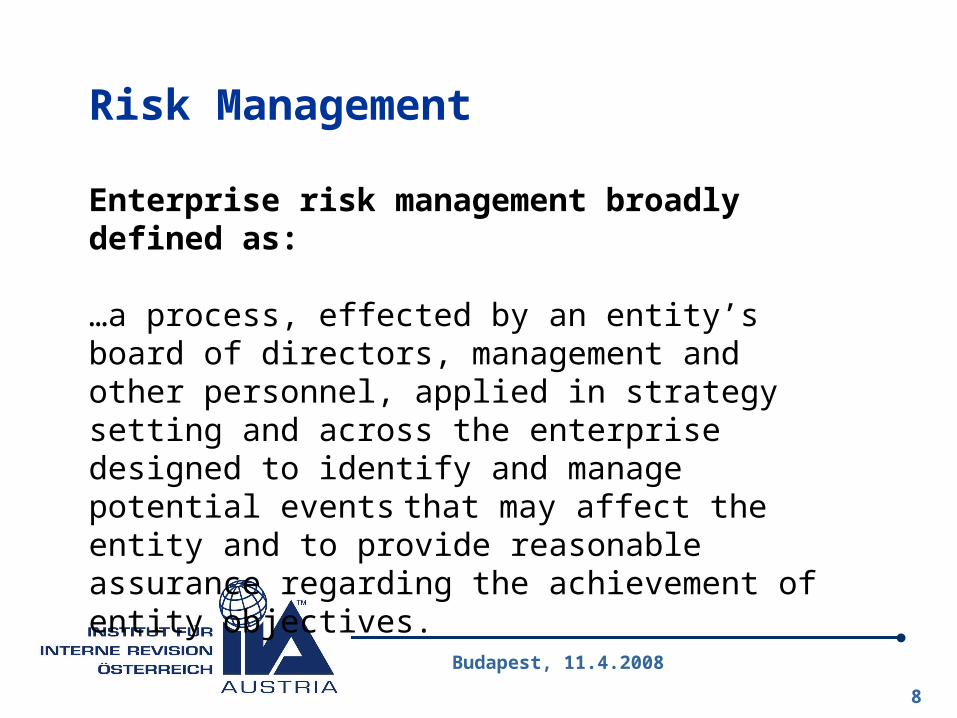

Enterprise risk management broadly defined as:

…a process, effected by an entity’s board of directors, management and other personnel, applied in strategy setting and across the enterprise designed to identify and manage potential events that may affect the entity and to provide reasonable assurance regarding the achievement of entity objectives.

Budapest, 11.4.2008

9

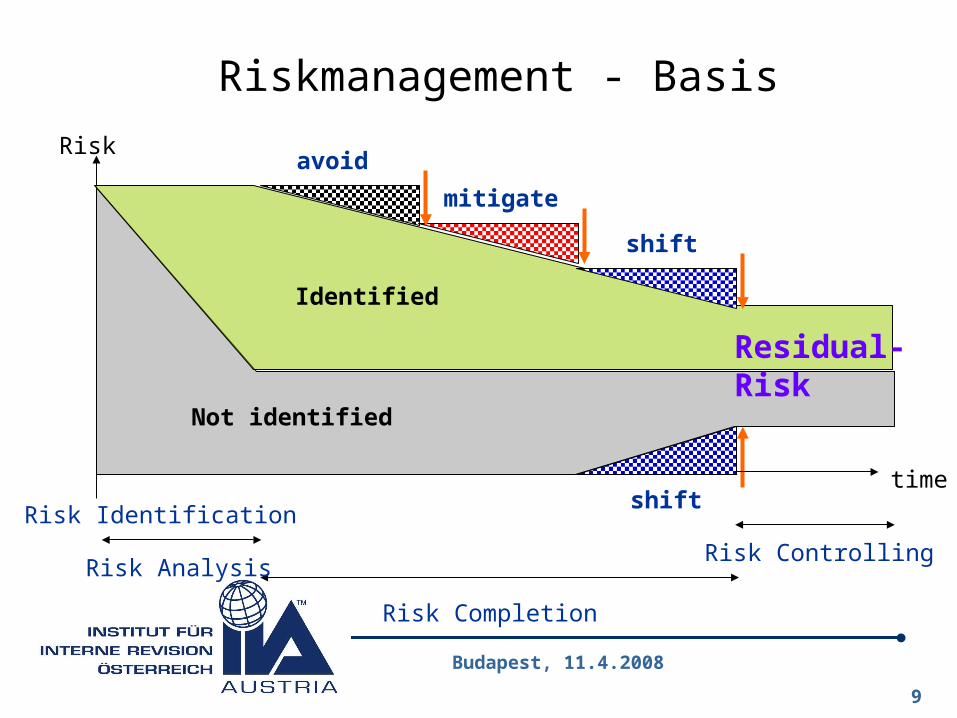

Risk

time

Riskmanagement - Basis

Not identified

Identified

avoid

mitigate

shift

shift

Residual-Risk

Risk Identification

Risk Analysis

Risk Completion

Risk Controlling

Budapest, 11.4.2008

10

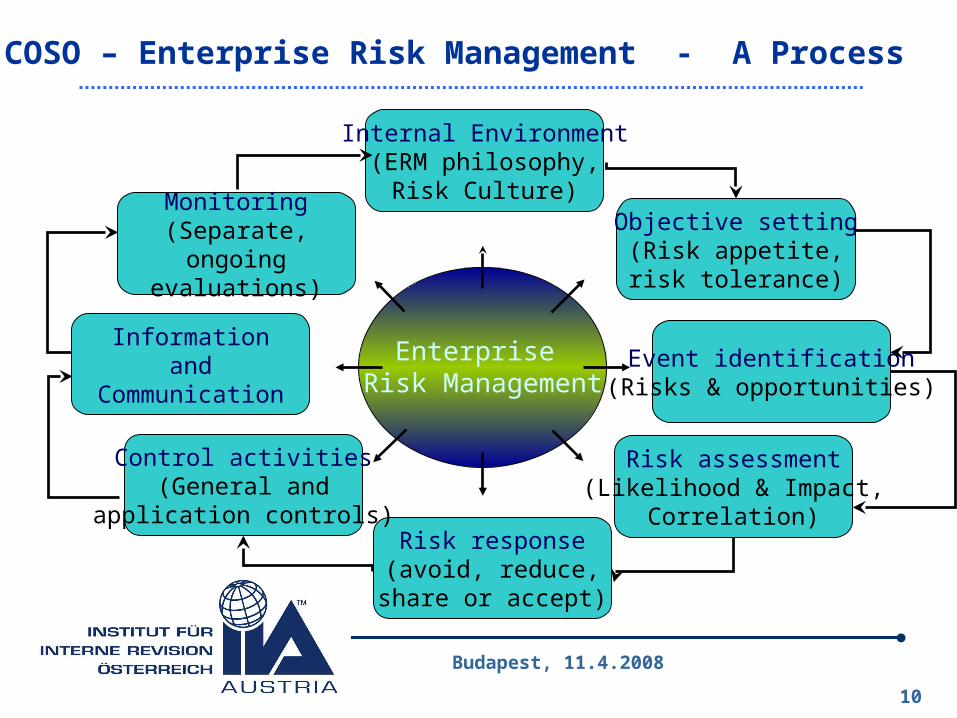

Enterprise Risk Management

Internal Environment(ERM philosophy,

Risk Culture)Objective setting(Risk appetite,risk tolerance)

Risk assessment(Likelihood & Impact,

Correlation)Risk response(avoid, reduce,

share or accept)

Event identification(Risks & opportunities)

Control activities(General and

application controls)

Information and Communication

Monitoring(Separate, ongoing

evaluations)

COSO – Enterprise Risk Management - A Process

Budapest, 11.4.2008

11

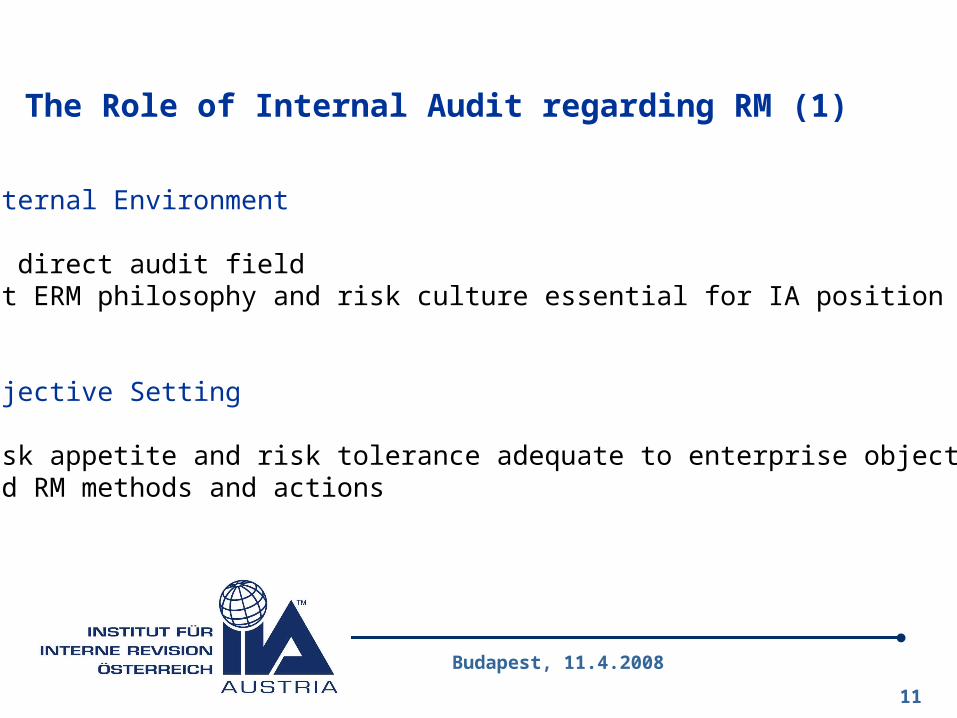

The Role of Internal Audit regarding RM (1)

Internal Environment

No direct audit fieldBut ERM philosophy and risk culture essential for IA position

Objective Setting

Risk appetite and risk tolerance adequate to enterprise objectivesand RM methods and actions

Budapest, 11.4.2008

12

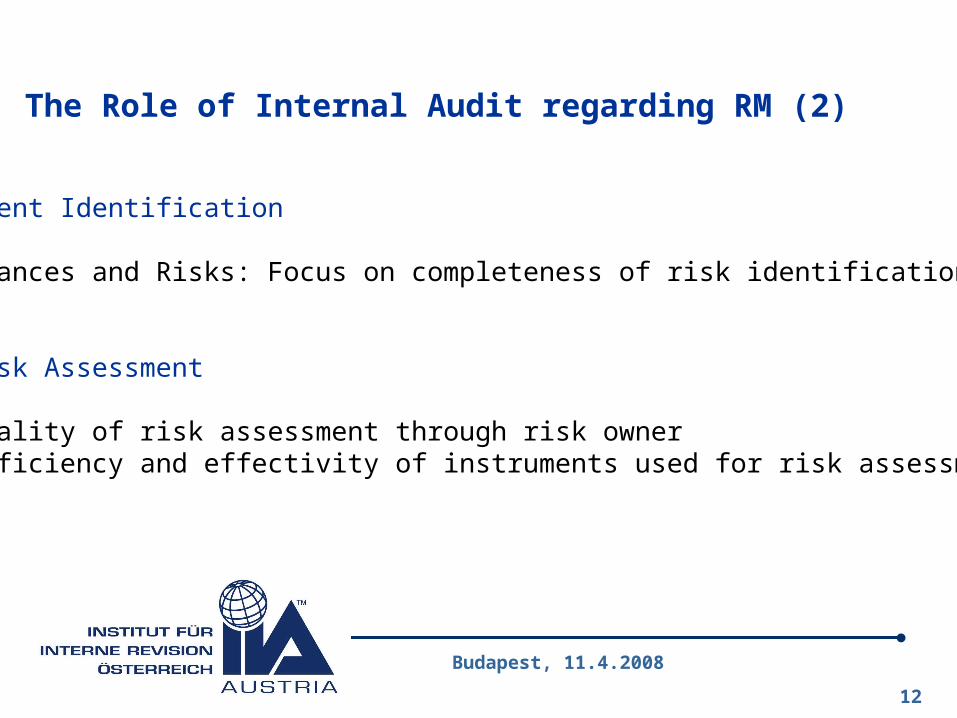

The Role of Internal Audit regarding RM (2)

Event Identification

Chances and Risks: Focus on completeness of risk identification

Risk Assessment

Quality of risk assessment through risk ownerEfficiency and effectivity of instruments used for risk assessment

Budapest, 11.4.2008

13

The Role of Internal Audit regarding RM (3)

Risk Response

Regularity and completeness of analysis and assessment of applied risk control activities

Control Activities

Quality of risk assessment through risk ownerEfficiency and effectivity of instruments used for risk assessment

Budapest, 11.4.2008

14

The Role of Internal Audit regarding RM (4)

Information and Communication

Regularity and effectivity of information process Completeness, accountability and understandability of directives

Monitoring

Regularity, usefulness and efficiency of each monitoring processEfficiency and effectivity of instruments used for risk assessment

Budapest, 11.4.2008

15

Internal Auditing

Risk Management

Internal Control

Connections

Budapest, 11.4.2008

16

Internal Control

Internal control is broadly defined as a process, effected by an entity's board of directors, management and other personnel, designed to provide reasonable assurance regarding the achievement of objectives in the following categories:

• Effectiveness and efficiency of operations,• Reliability of financial reporting,• Compliance with applicable laws and regulations.

Budapest, 11.4.2008

17

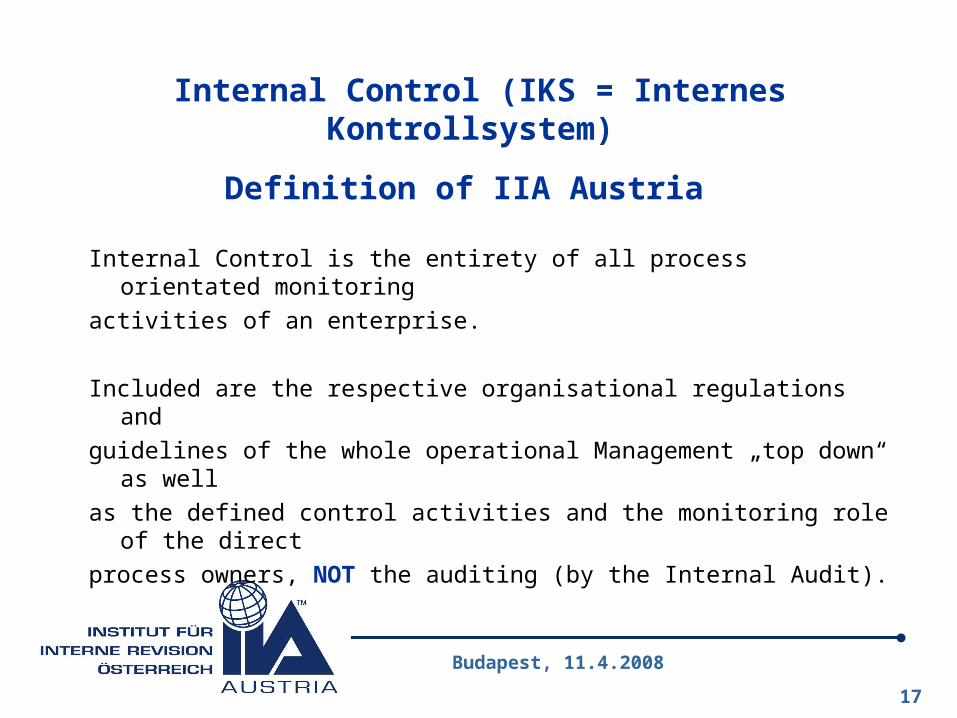

Internal Control (IKS = Internes Kontrollsystem)

Definition of IIA Austria

Internal Control is the entirety of all process orientated monitoring

activities of an enterprise.

Included are the respective organisational regulations and

guidelines of the whole operational Management „top down“ as well

as the defined control activities and the monitoring role of the direct

process owners, NOT the auditing (by the Internal Audit).

Budapest, 11.4.2008

18

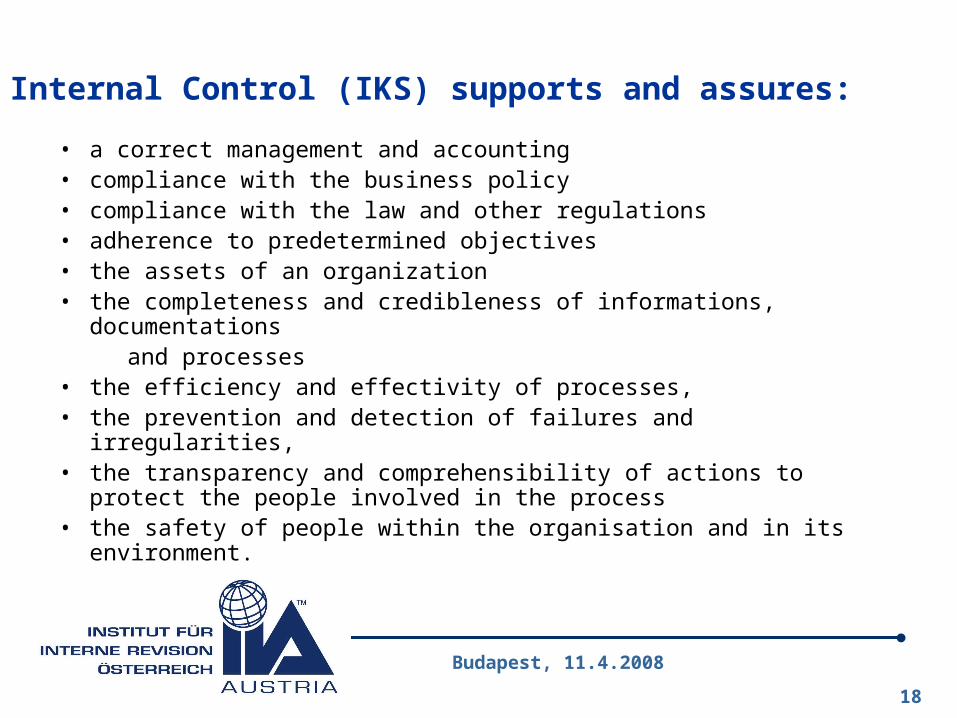

Internal Control (IKS) supports and assures:

• a correct management and accounting• compliance with the business policy• compliance with the law and other regulations• adherence to predetermined objectives• the assets of an organization• the completeness and credibleness of informations, documentations and processes• the efficiency and effectivity of processes,• the prevention and detection of failures and irregularities,• the transparency and comprehensibility of actions to protect the

people involved in the process • the safety of people within the organisation and in its environment.

Budapest, 11.4.2008

19

Internal Auditing

Risk Management

Internal Control

Connections

Budapest, 11.4.2008

20

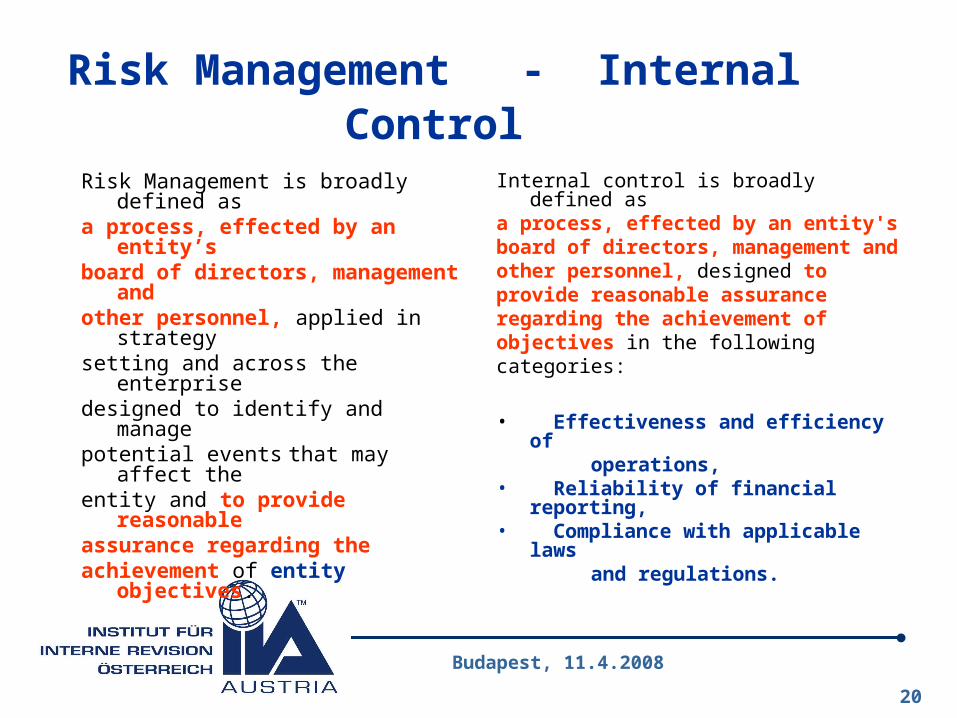

Risk Management - Internal Control

Risk Management is broadly defined as a process, effected by an entity’s board of directors, management and other personnel, applied in strategysetting and across the enterprisedesigned to identify and managepotential events that may affect theentity and to provide reasonableassurance regarding theachievement of entity objectives.

Internal control is broadly defined asa process, effected by an entity'sboard of directors, management andother personnel, designed toprovide reasonable assuranceregarding the achievement ofobjectives in the followingcategories:

• Effectiveness and efficiency of operations,• Reliability of financial reporting,• Compliance with applicable laws and regulations.

Budapest, 11.4.2008

21

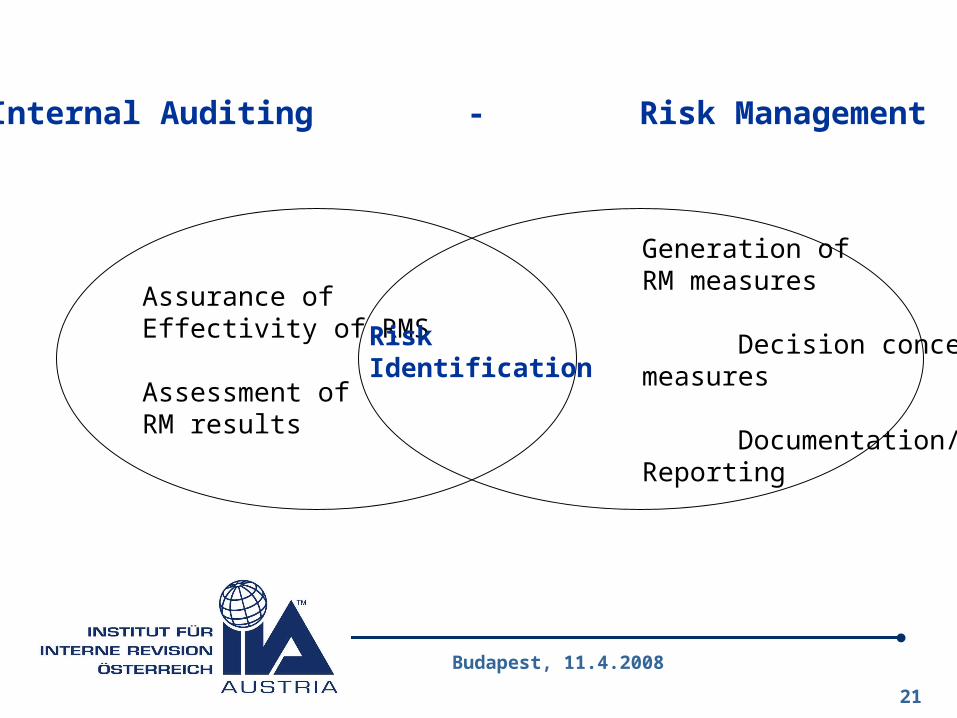

Assurance ofEffectivity of RMS

Assessment of RM results

Generation of RM measures

Decision concerning measures

Documentation/Reporting

Internal Auditing - Risk Management

RiskIdentification

Budapest, 11.4.2008

22

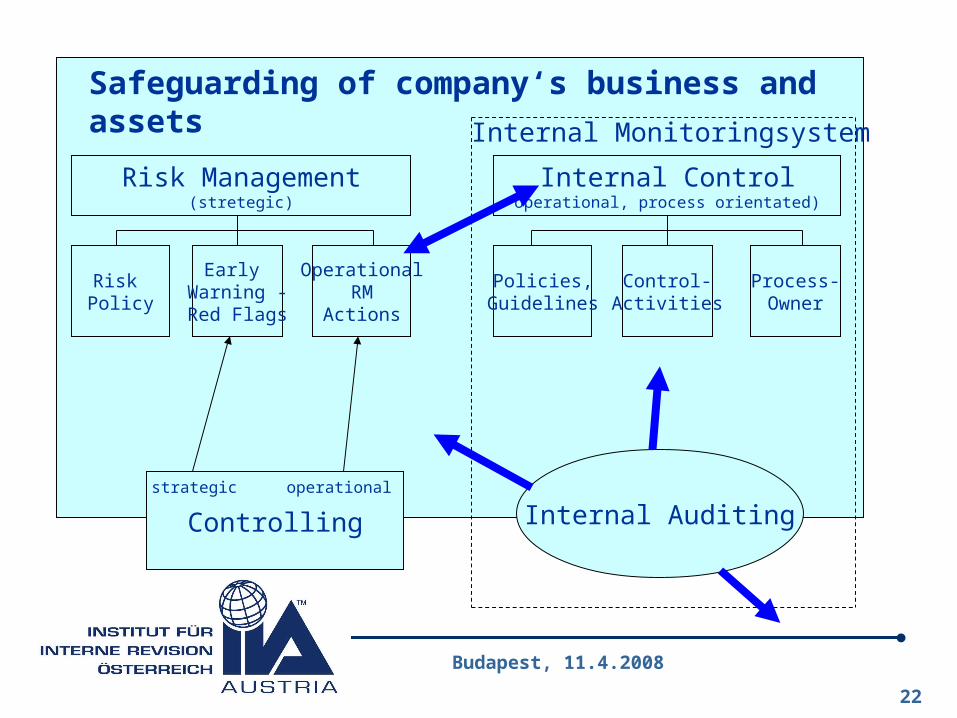

Safeguarding of company‘s business and assets

Risk Management(stretegic)

Internal Controloperational, process orientated)

Risk Policy

Early Warning -Red Flags

OperationalRM

Actions

Process-Owner

Control-Activities

Policies,Guidelines

Internal Monitoringsystem

Internal AuditingControlling

strategic operational

Budapest, 11.4.2008

23

Thank you