Embed Size (px)

Citation preview

Warsaw, 8 May 2003

1Q2003 Financial Results 1Q2003 Financial Results --

a good beginning...a good beginning...

2The latest IR news on the internet: www.bphpbk.pl

Merger close to the end

Financial results for 1Q2003 (PAS)

Appendix:

up-date on credit risk management

developments in business divisions

3The latest IR news on the internet: www.bphpbk.pl

costs costs

net provisionsnet provisions

NPLsNPLs

profitprofit

result on banking result on banking

activityactivity

loansloans

Improvement Visible (1Q03 versus 1Q02)

4The latest IR news on the internet: www.bphpbk.pl

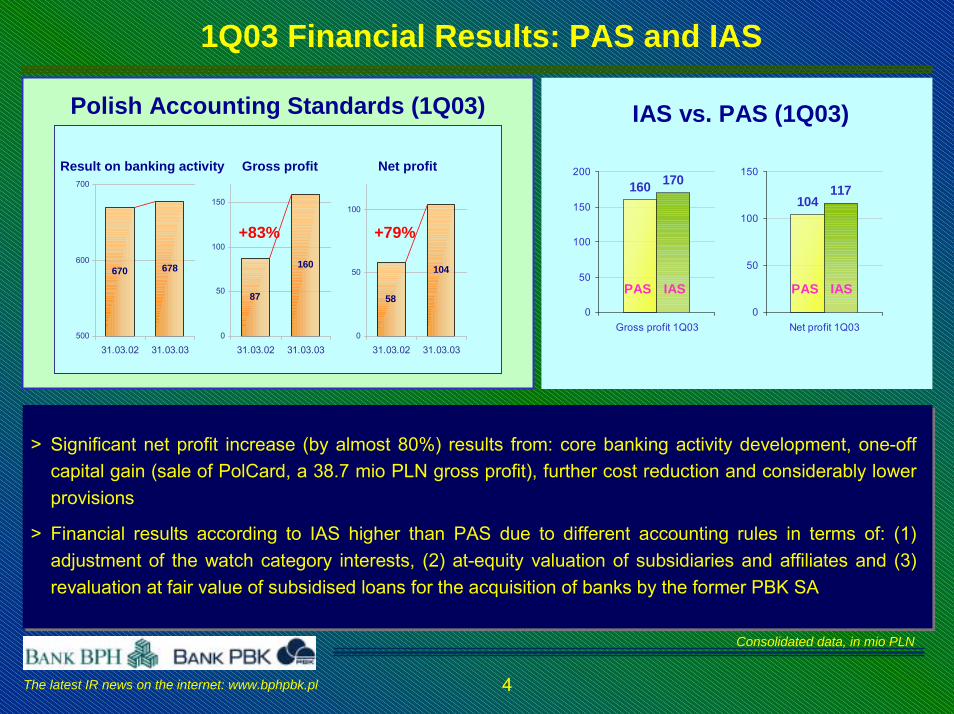

1Q03 Financial Results: PAS and IAS

Polish Accounting Standards (1Q03)

670 678

500

600

700

31.03.02 31.03.03

Result on banking activity Net profit

58

104

0

50

100

31.03.02 31.03.03

+79%

87

160

0

50

100

150

31.03.02 31.03.03

Gross profit

+83%

IAS vs. PAS (1Q03)

160 170

0

50

100

150

200

Gross profit 1Q03

104117

0

50

100

150

Net profit 1Q03

PAS IAS PAS IAS

> Significant net profit increase (by almost 80%) results from: core banking activity development, one-off capital gain (sale of PolCard, a 38.7 mio PLN gross profit), further cost reduction and considerably lower provisions

> Financial results according to IAS higher than PAS due to different accounting rules in terms of: (1) adjustment of the watch category interests, (2) at-equity valuation of subsidiaries and affiliates and (3) revaluation at fair value of subsidised loans for the acquisition of banks by the former PBK SA

Consolidated data, in mio PLN

5The latest IR news on the internet: www.bphpbk.pl

1Q03 versus 1Q02 - Improvement Visible

Lower costs & provisions

430 417

0

200

400

31.03.02 31.03.03

General costs with depreciation

-3.1% -38.7%

Net provisions and adjustments

Further drop in costs lowers C/I ratio (decline from 64.3% in 1Q02 to 61.5% in 1Q03)

Net fees and commissions cover 45% of total operating costs or ca. 82% of remuneration costs

Regardless of a general provision of 47 mio PLN created in 1Q03, net provisions and adjustments were lower by 54.1 mio PLN (by 38.7%) in comparison to 1Q02

1747

39123

0

50

100

150

31.03.02 31.03.03

Specificprovisions andadjustmentsGeneral provision

140

86

Consolidated data according to PAS, in mio PLN

6The latest IR news on the internet: www.bphpbk.pl

Completed:

> MIS income management & centralisation of accounts controls

> retail network restructuring

> SAP implementation within HR area

Ongoing:

> HQ restructuring; MbO enhancement to sales management

> development of electronic banking for Retail, Corporate and INM Clients – a joint Internet

platform

> B/O system for treasury transactions & MIS profit center management

> Basel II rules within Credit Risk Management

> IT system supporting Monitoring and Collection within CRM Area

> reorganisation of credit risk management for Retail

2003 Main Projects

7The latest IR news on the internet: www.bphpbk.pl

Cumulative SynergiesRealisation of Synergies Synergies Execution (2001 - 1Q03)

Synergies Plan (2001 - 2003)

personnel synergies58%

IT22%

promotion /communication

2%

administration / office supplies

13%

others6%

personnel synergies

43%

IT32%

promotion / communication

2%

administration /office supplies

13%

others9%

Declared merger related annual synergies of EUR 50m (operational) plus EUR 20m (IT related), to be fully realised

from 2004 onwards

� Synergies realised from 2001 – 1Q03 are 5% higher than planned

� Cumulative synergies execution as at 31.03.03 amount to 65 % of the overall plan (2001 - 2003)

2001 - 1Q03 2001 - 2003

100 105

0

50

100100

65

0

50

100

Plan

(%)

Plan

(%)

Exec

utio

n (%

)

Exec

. (%

)

� Execution of synergies mainly comes fromemployment reduction

� The second biggest synergies component are IT synergies

8The latest IR news on the internet: www.bphpbk.pl

Employment and Branch Network Restructuring

571

511487

200

300

400

500

600

31.12.200131.12.200231.03.2003

BPH PBK only

Outlets

4 2003 652

500

1500

2500

3500

4500

plan 2001-2003

execution2001-I Q 2003

Staff Reduction vs. Plan (FTEs)

Retail network restructuring finished:

Decrease in number of outlets by 24 in 1Q03 and 84 since the end of 2001, but

Alternative distribution channels development well received by clients.

Total execution of staff reduction constitutes 87% of the plan for 2001-2003. 185 FTEs were released in 1Q03, 548 FTEs are to be executed till year end (includes HQ restructuring).

9The latest IR news on the internet: www.bphpbk.pl

Merger close to the end

Financial results for 1Q2003 (PAS)

Appendix:

up-date on credit risk management

developments in business divisions

10The latest IR news on the internet: www.bphpbk.pl

Economy Continues to Fly on One Engine in Q1’03 ...

• GDP growth in Q1’03 at or below Q4’02

• Sharp employment losses, falling wage bill may jeopardise 3% consumption growth

• No investment recovery, unexpectedly strong cold weather impact on construction

• Exports continue to perform well despite European economic stagnation

N/A-4.1-6.3Investment

1.52.22.8Net inflation

4.53.63.7Ind. output

6.77.15.2Exports (EUR)

-21.3-9.3-6.0Construction

2.95.06.1Retail sales

N/A3.53.1Consumption

-2.1-1.5-0.8Wage bill

-4.0-3.0-4.0Employment

<=2.12.11.6GDP

Q1’03Q4’02Q3’02%y/y

11The latest IR news on the internet: www.bphpbk.pl

... Monetary Aggregates Show Some Improvement• M3 growth turns positive

• Corporate credit apart from base effect shows no major improvement

• Household credit slows down despite exchange rate depreciation

• PLN mortgage lending accelerates

• Deposits still in red, some improvement to be expected as suggested by Pengab

• Bad loans stabilized at near 20% level (6.8%q/q rise)

* Correcting for EUR-PLN depreciation

48.845.746.7NPLs (PLNbn)

-5.8-3.9-4.8Household deposits

19.719.119.3NPLs(% total)

11.41.410.1Corporate deposits

29/4220/6810/89Mortgage credit (PLN, EUR*)

7.28.68.4Household credit

8.41.01.6Corporate credit

0.5-2.1-1.5M3

Q1’03Q4’02Q3’02%y/y

12The latest IR news on the internet: www.bphpbk.pl

1Q03 versus 1Q02 - Improvement Visible

Strong loan increase (12%), above sector average due to further development in mortgage and corporate real estate lending

Shrinkage of retail deposits base caused mainly by lower wage bill and interest rate cuts. The Bank is about to launch new saving products

Assets increase results from higher loans and debt securities

Higher loans & stable deposits

21 89920 425

19 549

10000

20000

31.03.02 31.12.02 31.03.03

Consolidated loans

+12.0%

Consolidated deposits 29 50929 89330 662

10000

20000

30000

31.03.02 31.12.02 31.03.03

-3.7%

Receivables due to / due from non-financial and budget sector

Assets and equity

45 38645 09544 405

20000

35000

50000

31.03.02 31.12.02 31.03.03

Assets

+2.2%

Equity5 1345 0195 065

2000

4000

6000

31.03.02 31.12.02 31.03.03

+1.4%

Consolidated data according to PAS, in mio PLN

13The latest IR news on the internet: www.bphpbk.pl

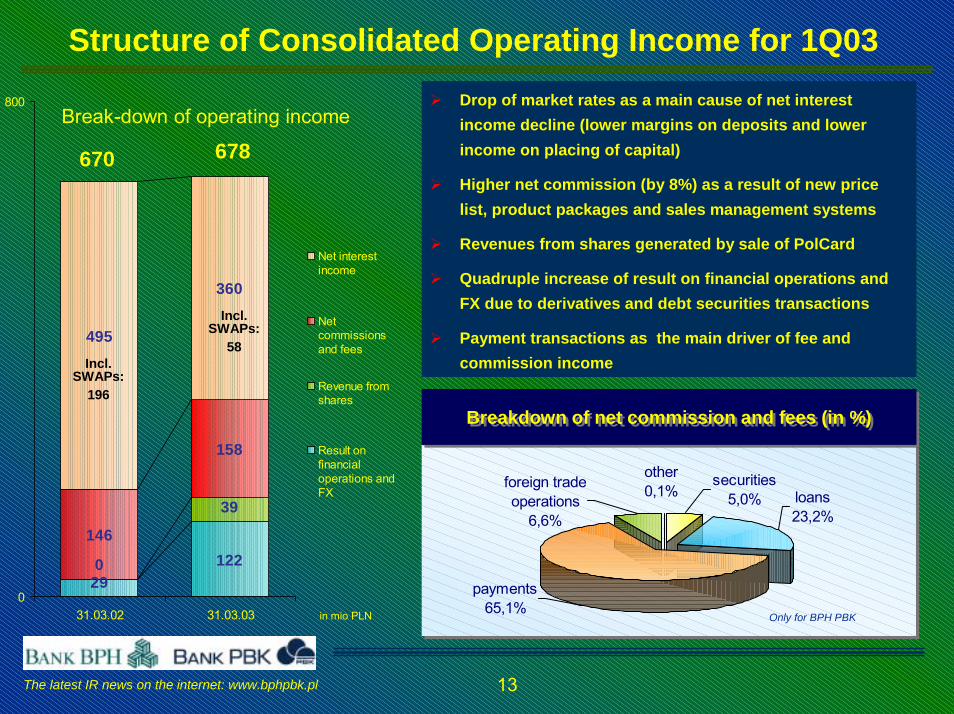

Structure of Consolidated Operating Income for 1Q03

Break-down of operating income

291220

39

146

158

495

360

0

800

31.03.02 31.03.03

Net interestincome

Netcommissionsand fees

Revenue fromshares

Result onfinancialoperations andFX

Incl. SWAPs:

196

Incl. SWAPs:

58

678670

other0,1%

securities5,0%

payments65,1%

loans23,2%

foreign trade operations

6,6%

� Drop of market rates as a main cause of net interest income decline (lower margins on deposits and lower income on placing of capital)

� Higher net commission (by 8%) as a result of new price list, product packages and sales management systems

� Revenues from shares generated by sale of PolCard

� Quadruple increase of result on financial operations and FX due to derivatives and debt securities transactions

� Payment transactions as the main driver of fee and commission income

Only for BPH PBKin mio PLN

Breakdown of net commission and fees (in %)Breakdown of net commission and fees (in %)

14The latest IR news on the internet: www.bphpbk.pl

67,0 70,9 71,8

10,86,9

6,1 3,6 3,44,9

5,4 5,3

11,2 13,1 12,6

7,0

0

10

20

30

40

50

60

70

80

90

100

31.03.02 31.12.02 31.03.03

Normal Watch Sub-standard Doubtful Lost

In %

21.321.322.122.1

Consolidated loan portfolio Unconsolidated loan portfolio by business segments as at 31.03.03 (in m PLN)

22.122.1

� Better loan portfolio quality (loan portfolio volume growth higher than irregular loans increase)

� A 7% increase in retail portfolio in line with Bank’s expectations

� Strong growth in Commercial Real Estate financing

5 205

14 018 3 500

Private individuals

Small Business

Corporate &Commercial RealEstate

Loans only (i.e. excluding guarantees and other off balance sheet exposures)

Improvement in Loan Book Quality

All data according to PAS

15The latest IR news on the internet: www.bphpbk.pl

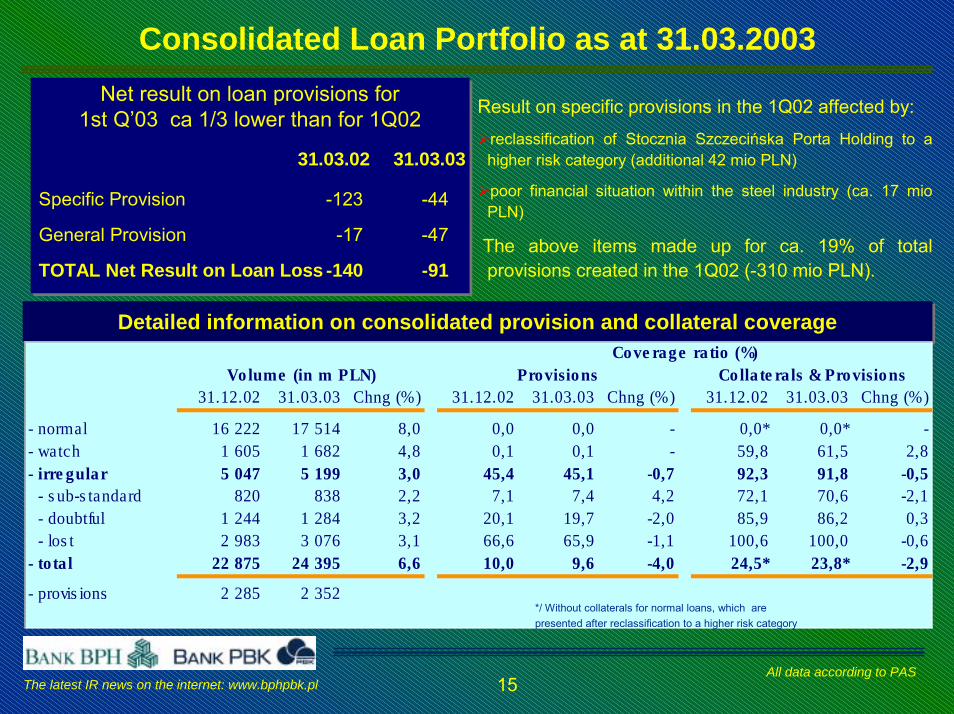

Consolidated Loan Portfolio as at 31.03.2003 Net result on loan provisions for

1st Q�03 ca 1/3 lower than for 1Q02

Specific Provision -123 -44

General Provision -17 -47

TOTAL Net Result on Loan Loss -140 -91

31.03.02 31.03.03

Result on specific provisions in the 1Q02 affected by: �reclassification of Stocznia Szczecińska Porta Holding to a

higher risk category (additional 42 mio PLN)

�poor financial situation within the steel industry (ca. 17 mioPLN)

The above items made up for ca. 19% of total provisions created in the 1Q02 (-310 mio PLN).

Detailed information on consolidated provision and collateral coverageDetailed information on consolidated provision and collateral coverage

31.12.02 31.03.03 Chng (%) 31.12.02 31.03.03 Chng (%) 31.12.02 31.03.03 Chng (%)

- normal 16 222 17 514 8,0 0,0 0,0 - 0,0* 0,0* -- watch 1 605 1 682 4,8 0,1 0,1 - 59,8 61,5 2,8- irre gular 5 047 5 199 3,0 45,4 45,1 -0,7 92,3 91,8 -0,5 - s ub-s tandard 820 838 2,2 7,1 7,4 4,2 72,1 70,6 -2,1 - doubtful 1 244 1 284 3,2 20,1 19,7 -2,0 85,9 86,2 0,3 - los t 2 983 3 076 3,1 66,6 65,9 -1,1 100,6 100,0 -0,6- tota l 22 875 24 395 6,6 10,0 9,6 -4,0 24,5* 23,8* -2,9

- provis ions 2 285 2 352

Volume (in m PLN) Provisions Colla te rals & ProvisionsCove rage ra tio (%)

*/ Without collaterals for normal loans, which are presented after reclassification to a higher risk category

All data according to PAS

16The latest IR news on the internet: www.bphpbk.pl

Selected Consolidated Financial Data for 1Q 2003 - Efficiency Ratios:

� Basic efficiency ratios

4,6

8,2

0

5

10

ROAE*

63,874,2

0

50

100

Loans/Deposits

0,5

0,9

0

0,5

1

1,5

ROAA***

64,3 61,5

0

50

100

C/I****

44,0 48,3

0

50

100

Loans/Assets

� Analysis of loan and deposit portfolio

4,53,2

0

5

10

Margin incl. SWAPs

31.03.02 31.03.03

31.03.02 31.03.03

17,314,5

0

10

20

CAR

6,9

12,5

0

5

10

15

GROAE**

*/ net profit to average equity; **/ gross profit to average equity***/ net profit to average assets; ****/ C/I = (overhead costs + depreciation) / result on banking operations

All data according to PAS

17The latest IR news on the internet: www.bphpbk.pl

Merger close to the end

Financial results for 1Q2003 (PAS)

Appendix:

up-date on credit risk management

developments in business divisions

18The latest IR news on the internet: www.bphpbk.pl

Further Risk Management Improvement.BLANA for Corporate in 2002. CACS for Retail in 2003.

Why CACS for BPH PBK?� Automated online system that supports the collection, restructuring and recovery processes of the Bank.

� Identifies delinquent cases

� Enables to implement priorities based on customers� risk

� Increases amount collected and cash flow / decreases write-off amounts.

� Increases productivity of collectors

� Reduces unnecessary collection expenses (i.e. manually sending letters).

� Automatically assigns work lists and schedules to users and provides collection activity statistics to managers for reporting and evaluation purposes.

� Accommodates increasing volumes as BPH PBK grows its customer base.

CACS capabilities� Management and Operational Reports

� Workflow Management

� Collector-Friendly Design

� Scalable, Flexible Architecture

� Robust Segmentation Capability

� Supervisor and Manager Support

� Interfaces to Current Systems

19The latest IR news on the internet: www.bphpbk.pl

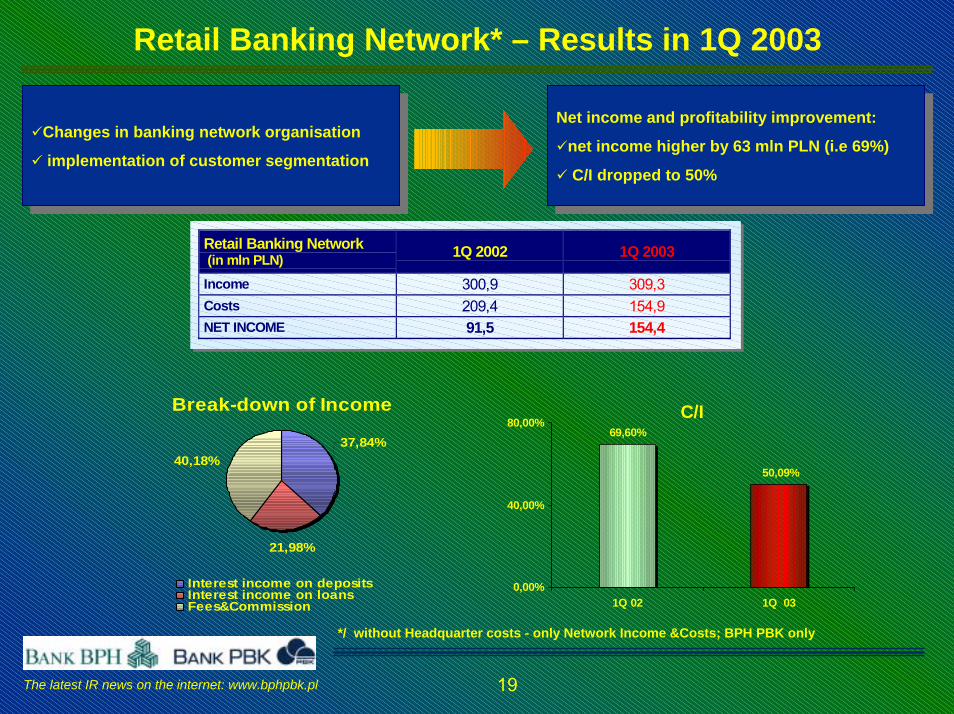

Retail Banking Network* – Results in 1Q 2003

Break-down of Income

37,84%40,18%

21,98%

Interest income on depositsInterest income on loansFees&Commission

C/I

50,09%

69,60%

0,00%

40,00%

80,00%

1Q 02 1Q 03

Retail Banking Network (in mln PLN) 1Q 2002 1Q 2003

Income 300,9 309,3Costs 209,4 154,9NET INCOME 91,5 154,4

*/ without Headquarter costs - only Network Income &Costs; BPH PBK only

�Changes in banking network organisation

� implementation of customer segmentation

�Changes in banking network organisation Net income and profitability improvement:

�net income higher by 63 mln PLN (i.e 69%)

� C/I dropped to 50%

Net income and profitability improvement:

�net income higher by 63 mln PLN (i.e 69%)

� C/I dropped to 50%� implementation of customer segmentation

20The latest IR news on the internet: www.bphpbk.pl

Retail Banking – Interest Margin on Loans & Deposits*

2,9%3,2% 3,3% 3,3% 3,3%

0,0%

1,0%

2,0%

3,0%

4,0%

1Q 2002 2Q 2002 3Q 2002 4Q 2002 1Q 2003

LOANS DEPOSITS

2,5%2,8%2,8%2,8%2,7%

0,0%

1,0%

2,0%

3,0%

4,0%

1Q 2002 2Q 2002 3Q 2002 4Q 2002 1Q 2003

Still a very stable level of interest margin on loans despite a difficult macroeconomic situation Deposit margin falls as a result of Monetary Policy Council decisions on interest rate (three cuts in

a row in January-March’03 period by 0,75 p.p.)

Still a very stable level of interest margin on loans despite a difficult macroeconomic situation Deposit margin falls as a result of Monetary Policy Council decisions on interest rate (three cuts in

a row in January-March’03 period by 0,75 p.p.)

*/ BPH PBK only

21The latest IR news on the internet: www.bphpbk.pl

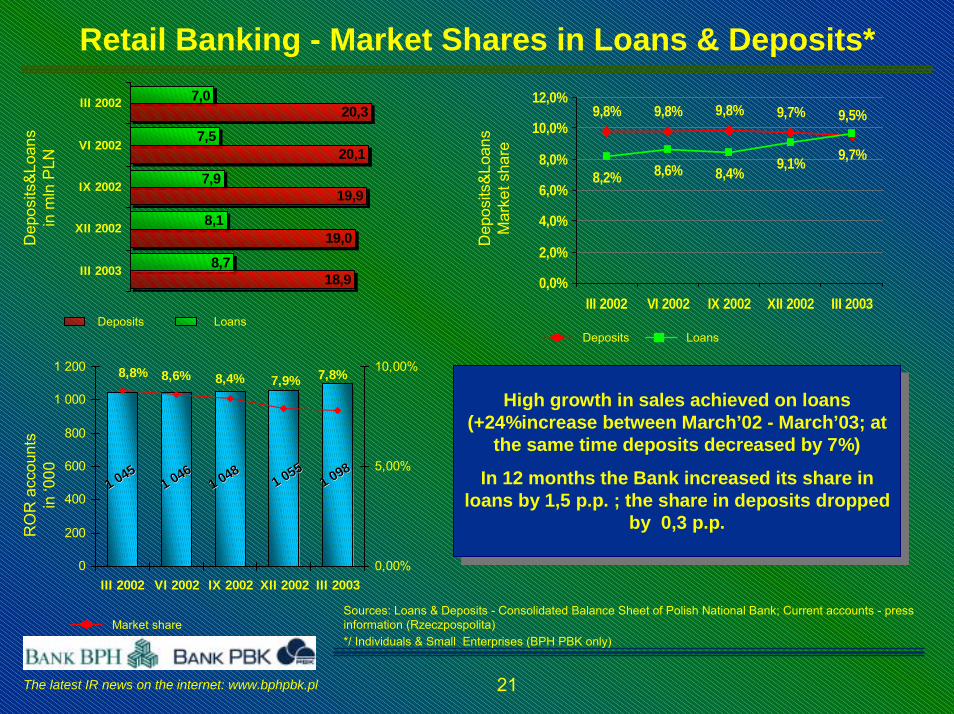

Retail Banking - Market Shares in Loans & Deposits*

18,9

19,0

19,9

20,1

20,3

8,7

8,1

7,9

7,5

7,0

III 2003

XII 2002

IX 2002

VI 2002

III 2002

Deposits Loans

High growth in sales achieved on loans (+24%increase between March’02 - March’03; at

the same time deposits decreased by 7%)

In 12 months the Bank increased its share in loans by 1,5 p.p. ; the share in deposits dropped

by 0,3 p.p.

High growth in sales achieved on loans (+24%increase between March’02 - March’03; at

the same time deposits decreased by 7%)

In 12 months the Bank increased its share in loans by 1,5 p.p. ; the share in deposits dropped

by 0,3 p.p.

Sources: Loans & Deposits - Consolidated Balance Sheet of Polish National Bank; Current accounts - press information (Rzeczpospolita)*/ Individuals & Small Enterprises (BPH PBK only)

9,8% 9,8% 9,8% 9,7% 9,5%

8,2% 8,6% 8,4% 9,1% 9,7%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

III 2002 VI 2002 IX 2002 XII 2002 III 2003

Market share

Deposits Loans

Dep

osits

&Loa

nsin

mln

PLN

Dep

osits

&Loa

nsM

arke

t sha

re

RO

R a

ccou

nts

in �0

00

7,8%7,9%8,4%8,6%8,8%

0

200

400

600

800

1 000

1 200

III 2002 VI 2002 IX 2002 XII 2002 III 20030,00%

5,00%

10,00%

1 0451 045

1 0461 046

1 0481 048

1 0981 098

1 0551 055

22The latest IR news on the internet: www.bphpbk.pl

Retail Banking Offer Development*

� Bank strengthened the second position on the mortgage market) with 72,5% portfolio increase in March’02-March’03 (2/3 of mortgage portfolio in CHF

� Stabilisation of mortgage interest margin: 3,0% in 1Q2003 co

� Very good achievement in sales of credit cards - +58%

� Significant increase in payment cards total; their number increased in January-March’03 by 35,5 thds and reached 1

(2/3 of mortgage portfolio in CHF, the rest in EURO and PLN),

� Stabilisation of mortgage interest margin: 3,0% in 1Q2003 compared to 2,9% in 1Q2002

� Very good achievement in sales of credit cards - +58% increase in January-March’03 period,

� Significant increase in payment cards total; their number increased in January-March’03 by 35,5 thds and reached 1 307,7 thds (4 th position on the market).

, the rest in EURO and PLN),

mpared to 2,9% in 1Q2002

increase in January-March’03 period,

307,7 thds (4 th position on the market).

Num

ber o

fBPH

PB

K C

redi

t Car

dsin

�000

.

0,1 2,6

28,4

44,8

0,0

25,0

50,0

VI 2002 IX 2002 XII 2002 III 2003

market market shareshare::

Mor

tga g

e lo

ans

volu

me

in m

ln P

LN

1 917

2 208

2 550

2 870

3 306

0

500

1 000

1 500

2 000

2 500

3 000

3 500

III 2002 VI 2002 IX 2002 XII 2002 III 2003

+72,5%

1 173

1 215

1 2501 272

1 307

1 000

1 400

IQ 2002 IIQ2002

IIIQ2002

IVQ2002

IQ 2003

Num

ber o

fBan

king

Car

ds**

in�0

00

� Bank strengthened the second position on the mortgage market) with 72,5% portfolio increase in March’02-March’03

13,0% 12,7% 13,5% 14,4% 14,7%***

***/ status at the end of February 2003 **/ Individuals&Small Enterprises together*/ BPH PBK only

23The latest IR news on the internet: www.bphpbk.pl

Retail Banking - Alternative Distribution Channels*

Call Centernumber of customers

e-Banking**number of customers

154 871

65 609

0

80 000

160 000

III 2002 VI 2002 IX 2002 XII 2002 III 2003

X 2,4

83 474

36 176

0

45 000

90 000

III 2002 VI 2002 IX 2002 XII 2002 III 2003

X 2,3

BPH PBK strengthened its position among leaders of alternative distribution channels

+16% increase in number of Call Center customers and +27% in e-Banking customers between January - March’03

Up-grade of Internet system for all (retail & corporate) Bank’s clients underway

BPH PBK strengthened its position among leaders of alternative distribution channels

+16% increase in number of Call Center customers and +27% in e-Banking customers between January - March’03

Up-grade of Internet system for all (retail & corporate) Bank’s clients underway

* / BPH PBK only **/ Internet accounts, SMS, WAP

24The latest IR news on the internet: www.bphpbk.pl

Corporate Banking - Market Share

17%

11%9% 8% 7% 7% 6% 6% 6%

3% 2% 2% 2%

12%

9%9%

10%

7%5%

6% 6% 5%

5% 7%4% 1%

0%

5%

10%

15%

20%

25%

30%Ba

nk P

ekao

S.A

.

Bank

Prze

mysło

wo-

Hand

lowy P

BK

PKO

BP

Citib

ank H

andlo

wy

Bank

Zach

odni

WBK

BRE

Bank

(+ M

ultiba

nk)

ING

Bank

Śląs

ki

Kred

yt Ba

nk

BIG

Bank

Gda

ński

Bank

Gos

poda

rki

Żywn

ościo

wej

Raiffe

isen B

ank P

olska

Bank

Och

rony

Środ

owisk

a

BISE

main bank auxiliary bank

Main banks and auxiliary banks for medium and large companies

Source: Gfk Polonia �Financial Monitor� survey, N=1000 companies with >10 mio PLN turnover, December 2002.

25The latest IR news on the internet: www.bphpbk.pl

Corporate Banking - Basic Business Development

8 000

8 100

8 200

8 300

8 400

January February March

11 500

12 000

12 500

13 000

13 500

14 000

January February March

AVERAGE LOAN VOLUME INCREASE

OF 8,6% (inc. NORMAL RISK LOANS

INCREASE OF 11,8%)

In comparison with only 2,1 % of increase in the sector

AVERAGE DEPOSIT VOLUME INCREASE OF

1,8%despite falling interest rates and 2,1% decrease in the

sector

+8.6%

+1.8%

Average loan volumes (PLN millions)

Average deposit volumes (PLN millions)

26The latest IR news on the internet: www.bphpbk.pl

Corporate Banking - Electronic Banking and Cash Management Development

MultiCash numbers of new instalations

337

115

0

50

100

150

200

250

300

350

400

1Q02 1Q03

Triple increase of MultiCash sales:

72% of payments by Corporate Clients

are done electronically

Electronic signature on chip cards

Newest program MultiCash PRO via

Internet

Professional implementation, trainings,

service & Hot Line

TRANS-Collect

the best corporate

service rankedby the

Business Centre Club

23 new large Clients for Cash Management products in IQ 2003

27The latest IR news on the internet: www.bphpbk.pl

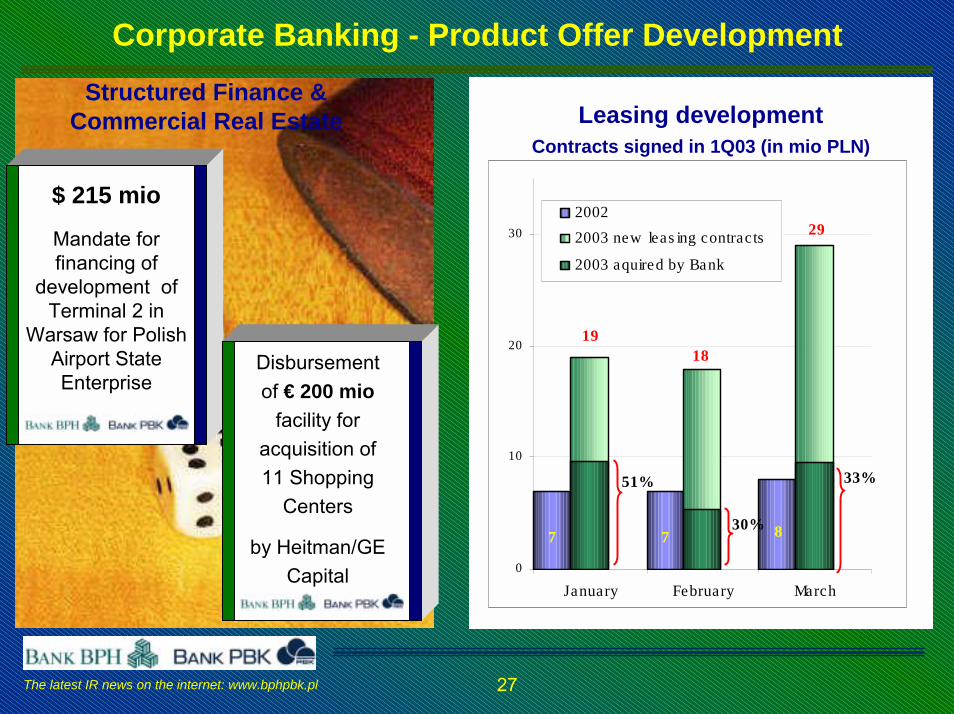

Corporate Banking - Product Offer DevelopmentStructured Finance &

Commercial Real Estate

Mandate for financing of

development of Terminal 2 in

Warsaw for Polish Airport State Enterprise

$ 215 mio

Disbursement of € 200 mio

facility for acquisition of 11 Shopping

Centers

by Heitman/GE Capital

Leasing developmentContracts signed in 1Q03 (in mio PLN)

877

29

1819

51%

30%

33%

0

10

20

30

January February March

20022003 new leas ing contracts

2003 aquired by Bank

28The latest IR news on the internet: www.bphpbk.pl

INM Division - Achievements in 1Q03 (1)

ALM Department Trading Department

Average monthly turnover in money market products increased by 18% versus 2002Second place in NBP Ranking for Money

Market Dealers in 1Q of 2003 Market maker in all PLN money market

products for both domestic and foreign banks

Growing share in PLN clearing volumes

Average monthly turnover in derivatives & fixed income increased by 127% versus 2002The Leader in t-bond and interest rate

derivatives trading (1st place in Primary Dealers Ranking of Ministry of Finance) Market maker in foreign exchange market

and liquidity provider in OTC options

100118

0

50

100

150

2002 1Q03

100

227

0

100

200

2002 1Q03

+18%

+127

%

29The latest IR news on the internet: www.bphpbk.pl

INM Division - Achievements in 1Q03 (2)

Sales & Origination Departments

Growing share in Polish debt origination market (5th position in the league tables in terms of bonds placed in March 2003 versus 13th in 1Q 2002)

Dynamic management of collaterals related to derivatives transactions with non banking Counterparts

Average monthly turnover in derivatives products & fixed income increased by 285% versus 2002

position

position

Custody Department

Average monthly volume of assets under custody increased by 33% versus 2002Growing share in custody services for

investment funds 30% as of end of March 2003Developing services for domestic and

foreign customers allowing for increase of automation of processes

100

133

0

50

100

150

2002 1Q03

+33%